UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07959

Advisors Series Trust

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Jeffrey T. Rauman, President/Chief Executive Officer

Advisors Series Trust

c/o U.S. Bancorp Fund Services, LLC

777 East Wisconsin Avenue, 5th Floor

Milwaukee, WI 53202

(Name and address of agent for service)

(Name and address of agent for service)

(626) 914-7363

Registrant's telephone number, including area code

Date of fiscal year end: November 30, 2022

Date of reporting period: November 30, 2022

Item 1. Reports to Stockholders.

(a)

Semper MBS Total Return Fund

Class A – SEMOX

Investor Class – SEMPX

Institutional Class – SEMMX

Semper Short Duration Fund

Investor Class – SEMRX

Institutional Class – SEMIX

Annual Report

November 30, 2022

SEMPER FUNDS

Table of Contents

Shareholder Letter | 1 | ||

Allocation of Portfolio Assets | 11 | ||

Expense Example | 13 | ||

Investment Highlights | 15 | ||

Schedules of Investments | 17 | ||

Statements of Assets and Liabilities | 36 | ||

Statements of Operations | 39 | ||

Statements of Changes in Net Assets | 40 | ||

Financial Highlights | 44 | ||

Notes to Financial Statements | 49 | ||

Report of Independent Registered Public Accounting Firm | 64 | ||

Notice to Shareholders | 65 | ||

Statement Regarding Liquidity Risk Management Program | 66 | ||

Information about Trustees and Officers | 67 | ||

Householding | 71 | ||

Privacy Notice | 72 |

SEMPER FUNDS

January 8, 2023

Dear Shareholder,

2022 will go down on record as one of the most tumultuous and challenged performance years on record for the U.S. fixed income market, including the structured credit portion of the bond market that comprises the Semper MBS Total Return Fund (the “Total Return Fund”) and the Semper Short Duration Fund (the “Short Duration Fund”). As we described in last summer’s semi-annual report, the domestic bond market was buffeted by the uncertainty surrounding the Fed’s fight to tame sharply higher inflation, largely caused by a combination of the Fed’s 2020-2021 dovish monetary policy, unprecedented fiscal stimulus, supply chain problems, and a labor shortage, which in turn were all fallout from the COVID pandemic. The war in Ukraine and its impact on energy and food prices has also resulted in upward pressure on inflation.

With yields now having risen to levels unseen for over a decade, we believe that the income provided by debt securities has once again become an enticing and important component of investors’ allocation decisions. Yields are now high enough so that break evens for additional price declines are substantially shorter, and attractive enough to restore the diversification element that bonds historically offered during times of equity market weakness. There is now room for yields to fall, lifting bond prices higher, during these flight to safety/quality/liquidity events.

After pivoting from an accommodative policy in 2021 towards a view that rapidly increasing inflation was going to be transitory, the Fed early in 2022 shifted to an aggressively hawkish posture with the aim of combating levels of inflation that were last seen in the 1980s. As the Fed tightened policy, shorter maturity yields experienced a greater increase than longer maturities and the curve tilted to an inverted slope with the 2-year Treasury yield rising from 0.6% as of November 30th, 2021 to 4.5% as of November 30th, 2022 while the 10-year Treasury yield rose from 1.45% a year ago to 3.6% on November 30th, 2022, the end of the Funds’ current fiscal year.

Investors in fixed income markets bore the effects of the Fed’s rate hikes as the markets posted some of the worst returns on record. For the full 2022 fiscal year, the Bloomberg U.S. Aggregate Bond Index, a broad measure of the overall U.S. investment grade bond market, had a total return of -12.84%, the Bloomberg U.S. MBS Index, the benchmark index for the Total Return Fund returned -11.50%, and the Bloomberg 1-3 Year Government Index and the Bloomberg U.S. Treasury 1-3 Year Index, the benchmark indices for the Short Duration Fund returned -4.18% and -4.19%, respectively. These returns are lower than the worst calendar year returns in the history of these indices, which date back nearly 50 years. According to a report from Vanguard that references data back to 1926, the second worst year for U.S. fixed income investors, next to 2022, was 1969, during which the overall bond market suffered an 8% decline. In addition to rapidly rising interest rates, these rates have moved with extreme levels of volatility throughout the year, keeping risk premiums high and investor sentiment low.

1

SEMPER FUNDS

As investors grappled with NAV declines across virtually all fixed income funds, bond fund outflows increased sharply, with the outflows being more severe for funds focused on non-Agency mortgage-backed securities (RMBS) and structured products generally due to the uncertainty created in mortgage prepayments and home prices. The RMBS sector was already on its “back foot” from the technical created by the supply wave during the surge in refinancing and home purchase activity during 2020 and 2021. This combination of interest rate increases and RMBS market technicals pushed yields and spreads in the sector higher, to levels unseen since 2009 at the height of the housing induced Great Recession.

Portfolio Updates

The Total Return Fund and the Short Duration Fund have been negatively impacted by this extreme weakness in the fixed income market. Although both Funds have relatively low interest rate sensitivity, the spread widening in all credit sectors had a negative impact on bond prices in the Funds, despite continuing strengthening of the credit quality of these bonds from a strong housing market and good consumer credit performance.

Both Funds’ primary strategies during the fiscal year remained unchanged. The Total Return Fund, under normal market conditions, invests at least 80% of its net assets in mortgage-backed securities (“MBS”), and seeks to provide a high level of risk-adjusted current income and capital appreciation. Throughout the fiscal year, the Fund’s largest allocation was to the non-Agency RMBS sector as it has been since inception of the Fund in 2013. The November 30, 2022 allocation to RMBS totaled 87%. Approximately 33% of this allocation consisted of bonds supported by collateral with 1 – 3 years of seasoning; 30% with 3 – 10 years of seasoning; and 35% with 10-years or more seasoning. This significant seasoning is important because the more seasoned loans have generally built up substantial levels of home equity, an important source of borrower’s credit quality and overall bond credit support. The RMBS held in the Fund included a 13% allocation to Legacy bonds – bonds issued before 2008; a 16% allocation to Prime Jumbo 2.0 and Non-Qualified Mortgage bonds (Non-QM), generally issued in the last few years; a 28% allocation to Agency Credit Risk Transfer (CRT) bonds issued by Fannie Mae and Freddie Mac, which are not government guaranteed but are supported by pools of high quality Agency quality loans; and a 9% allocation to Single Family Rental bonds (SFR), bonds issued by single family home rental management companies. The Total Return Fund also had an 8% allocation to commercial MBS (CMBS), primarily multi-family housing securities. The Total Return Fund did not have an allocation to government agency guaranteed MBS given our continued relative value view on this sector characterized by greater interest rate sensitivity, lower yield, and risk of relative underperformance its longer duration and uncertainty surrounding the Fed 30% ownership position of the Agency sector.

The rapid rise in interest rates had a significant impact on Total Return Fund characteristics. Duration extended from about 1 year to 2.3 years, largely because of

2

SEMPER FUNDS

the projected extension of cash flows as mortgage refinancings slowed and the virtual elimination of expectations for early calls of deals, especially in the Non-QM and Prime Jumbo 2.0 sectors. The significant allocation to floating rate mortgage securities served to keep duration lower. Early in the fiscal year we increased the floating rate exposure from 60% to 73%. As short interest rates rose during the year, the average coupon of the Fund’s bonds increased from 4.1% to 6.5%, contributing to much higher interest income and dividend distributions. The Fund’s yield to maturity rose from 4.3% to 8.8%, in part from the higher coupons and in part from higher yield as spreads widened, further pressuring bond price declines. The average bond price in the Fund declined from $99.5 a year earlier to $82.3 as of November 30th, 2022.

Similar to the Total Return Fund, the Short Duration Fund is invested in securitized debt credit sectors including MBS, CMBS, Asset-Backed Securities (ABS), and senior tranches of collateralized loan obligations (CLO) rated AAA. Unlike the Total Return Fund which is highly concentrated in RMBS with an emphasis on mezzanine and subordinated bonds offering significant total return potential, the Short Duration Fund’s investments are more diversified and focused on senior bonds across the listed securitized debt subsectors. Additionally, the Fund is well positioned for a rising interest rate environment. The Fund maintains significant diversification with no more than 25% allocated to any of its sectors. We are maintaining a low duration to minimize interest rate sensitivity, through the purchase of securities generally with average lives under three years and many with floating rate coupons. Duration was 0.3 years as of November 30th, 2022, down from 0.4 years one year earlier. A primary reason for the continued low duration is the Fund’s 90% allocation to securities with floating rate coupons, including Agency CRT bonds and AAA-rated CLO tranches, an increase from 76% a year earlier. At fiscal year-end, approximately 24% of the portfolio was invested in non-Agency RMBS, 24% in Agency MBS, consisting of Fannie Mae and Freddie Mac issued Credit Risk Transfer securities (Agency CRT), 24% in CMBS – primarily floating rate Commercial Real Estate CLOs and Single Asset Single Borrower bonds with a significant residential real estate component along with multi-family securitizations, 2% in ABS, and 23% in AAA-rated CLO securities. The primary changes occurred very early in the fiscal year when we sold most of the Fund’s ABS which were in fixed rate subprime auto loan bonds and added to the allocation of CLO, which benefit from their floating rate coupon structures. As a result of general rate increases, increasing floating rate coupon resets, and higher yield from spread widening/price declines, the portfolio’s yield to maturity increased from 2.6% to 7.8%. While the Fund’s average bond price declined about 6% from $101.1 to $95.2, the exaggerated yield increase is in part the result of short average lives/maturities of the bonds. The average bond coupon increased from 2.65% to 5.93% during the course of the fiscal year. Over 78% of the fund assets were rated investment grade, with positive credit trends continuing.

The Total Return Fund net performance for the one year ended November 30, 2022 for the Institutional Class was -13.87%, for the Investor Class net performance was -14.16%, and for the Class A net performance was -14.15% without the maximum

3

SEMPER FUNDS

2.00% front-end sales load and -15.89% including the front-end sales load. The performance of the Bloomberg U.S. Mortgage-Backed Securities Index (the “Index”), the Fund’s benchmark index, during the fiscal year was -11.50%. Performance of the Bloomberg U.S. Aggregate Index, which represents the overall U.S. investment grade bond market was -12.84%.

The primary sources of negative performance for the Total Return Fund during the fiscal year was price depreciation from rising interest rates and from spread widening. Unrealized price declines reduced performance by about -17%. Interest income was about +5% during the fiscal year. Portfolio performance during the month of December, 2022, following the fiscal year end, was positive, and this strength has carried into the early part of January.

The Short Duration Fund net performance for the one-year ending November 30, 2022 for the Institutional Class was -2.66%, and for the Investor Class was -2.80%. The performance of the Bloomberg 1-3 Year U.S. Government Index during this same period was -4.18%. The performance of the Bloomberg 1-3 Year U.S. Treasury Index was -4.19%. The Short Duration Fund’s primary positive contributor to performance was interest income, totaling about 3%. Unrealized price declines were about -4%.

We expect to maintain a similar overall Total Return Fund composition throughout 2023, with the largest allocation to floating rate non-Agencies, and a modest allocation to CMBS, while continuing to maintain a duration lower than the overall mortgage market.

We expect that the Short Duration Fund’s overall composition will remain similar as well, with a significant allocation to RMBS, CMBS, and AAA-rated CLOs to achieve the required diversification, with very low interest rate sensitivity. When we get closer to the Fed reversing monetary policy to a more accommodative stance, potentially in response to much lower inflation and either a recession or very slow economic growth, we would expect to add to the fixed rate ABS allocation and reduce some of the Fund’s floating rate exposure.

Both the Total Return Fund and the Short Duration Fund continue to have significant capacity and appropriate liquidity.

Market Outlook

We expect RMBS and other profiles with exposure to mortgage credit to perform well in the coming several quarters, although we believe that volatility will persist until the markets become reassured that the Fed is approaching its peak level of interest rates as it continues its battle to slow inflation.

Our base case view is that home prices will decline by 10 to 15% to reach sustainable levels of affordability. Home price appreciation (HPA) surged with values increasing by approximately 40% nationally over the 2-year period from March 2020 to March 2022. Over the course of the spring and summer, the housing market transitioned from having some markets such as Los Angeles, San Francisco, and Seattle,

4

SEMPER FUNDS

exhibiting signs of becoming overheated, to a national affordability shock as mortgage rates rose sharply due to the Fed’s aggressive tightening policy. Initially, this led to concerns among some investors that a housing crisis would ensue and that markets would repeat the 2008 experience. However, the data paints a different backdrop today and we believe that after affordability normalizes in 2023, home prices will remain above pre-COVID levels.

A key driver of this view is that unlike in 2008 when there was an excess supply of housing, supply remains extremely tight today after more than a decade of lackluster volumes of housing construction. Shifting from oversupply to undersupply has a meaningful effect on the potential decline in prices. Our view is predicated on the following:

| • | Undersupply is supportive of home prices in the long run |

| ∘ | The U.S. housing shortage is estimated to be near 4 million units | |

| ∘ | In a normal year household formation runs about 1.4 to 1.5 million units | |

| ∘ | Housing completions have averaged less than 1 million per year since 2009 and have only recently begin to trend towards a rate that meets household formation | |

| ∘ | If we surged to 2 million units of completions per year, it would still take 6 to 8 years to fill the shortage |

A demand wave exists amongst Millennials

| ➣ | Millennials are now the largest age group in the U.S and as a group they serve as a potential increase to the buyer base | |

| ➣ | Data shows an increasing homeownership rate for the 25 to 34 age cohort. This metric has been increasing since 2016 after a decline during the Great Financial Crisis | |

| ➣ | Additionally, the 15 to 25 age cohort is similar in size to the Millennial demographic – foreshadowing that housing demand will persist (if not grow) in the years to come |

Affordability improvements will be met with demand

| ➣ | 30-year fixed rate mortgages rose from mid-3% to over 7% in October, before receding to mid-6% in December | |

| ➣ | Debt-to-income (DTI) ratios on home purchases have risen from historical lows of near 25% to roughly 40% | |

| ➣ | We expect DTI to retrace to 1990s and early 2000s levels of slightly below 30% and our view is that the 30 year mortgage rate is likely to remain between 6% and 7% as the Fed reaches their terminal rate and the long end of the Treasury yield curve stabilizes |

Mortgage credit has fundamentally and structurally improved versus where it stood prior to the Great Financial Crisis (GFC). Underwriting standards have been

5

SEMPER FUNDS

conservative in the post-GFC era with credit scores, loan to value ratios, and debt to income metrics all improving significantly versus where they stood in 2008. On top of the conservative underwriting, a prolonged period of strong home price growth and low interest rates has further enhanced the quality of existing mortgages and the market is comprised of borrowers with significant equity and fixed-rate mortgages.

As a result of these factors, the mortgage market is largely comprised of high-quality borrowers, with significant equity, and low, fixed-rate mortgages. Fundamental credit risk is low since these borrowers are well positioned to weather a housing contraction and continue servicing their debt, and structurally, due to a lack of adjustable rate mortgages there is very little risk of systemic payment shocks. The following data points are noteworthy contrasts:

| ➣ | The median FICO of a newly originated loan has averaged near 750 since 2008, versus a pre-GFC level of near 720. The lowest 10th percentile is near 650 versus 600 pre-GFC. | |

| ➣ | According to CoreLogic data through Q3 2022, the average LTV of 43.6% is significantly lower than the above 70% level that existed going in to the GFC. | |

| ➣ | The adjustable rate share of mortgages approached 40% in the years prior to the GFC. Today Adjustable Rate Mortgages (ARMs) make up only about 10% of outstanding mortgages. | |

| ➣ | Nationally, mortgage delinquencies are below 3% versus an average level above 4% during the late-1990s and early-2000s. Conservative underwriting has led to a lower level of stressed mortgages. |

Lastly, in addition to fundamentally stronger mortgages, homeowners are in a better fiscal position to service mortgage debt after having reduced their debt levels and cost of funds. Household debt as a percent of income is significantly lower than in 2007 and 2008.

Given the views on housing and mortgage credit, we believe that non-Agency RMBS offers compelling value at current market levels. When factoring in the fact that conservative standards following 2008 have led to these bonds being much stronger in terms of bond level credit enhancement, loan performance, and borrower credit quality, RMBS presents a substantially different return/risk opportunity than the last time we saw yields at these levels during the Great Financial Crisis.

Loss adjusted yields in the sector are attractive on an absolute and relative basis. With investment grade bonds yielding 6% to 8% and below investment grade rated RMBS yielding 9% to above 15%, the sector is poised to produce some of the strongest returns across credit markets in 2023. Yield spreads in RMBS widened more than other portions of credit markets in 2022 due to the technical of heavy volume of securitization supply during Q1 and Q2 that faced a stark reduction in demand throughout the year as funds faced elevated outflows and bank deposits declined. The consensus expectation across investment banks is that supply will shrink by 40 to 50% in 2023.

6

SEMPER FUNDS

| Investment Grade | Current | 12/31/2021 | 2022 Spread |

| Senior and Mezz | Spreads | Spread | Change |

| AGENCY CRT LCF (BBB) | 350 | 165 | 185 |

| SASB Multifamily (BBB) | 425 | 175 | 250 |

| Non-QM (BBB) | 550 | 205 | 345 |

| SFR (BBB) | 450 | 170 | 280 |

| Corp BBB | 159 | 113 | 46 |

| Below Investment Grade | Current | 12/31/2021 | 2022 Spread |

| Mezz and Sub | Spreads | Spread | Change |

| STACR CRT B1 (BB/NR) | 550 | 335 | 215 |

| STACR CRT B2 (B/NR) | 1200 | 660 | 540 |

| Non-QM Mezz (B) | 1000 | 390 | 610 |

| SFR Mezz (B/NR) | 575 | 325 | 250 |

| Corp B | 468 | 312 | 156 |

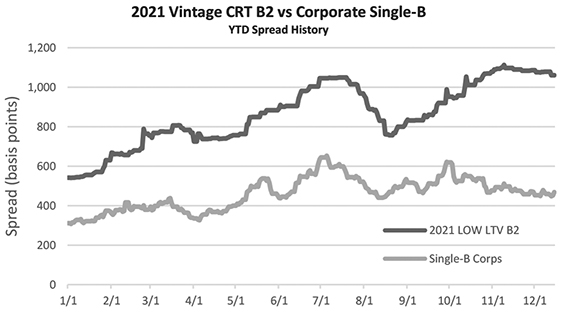

With shifting market technicals serving as a catalyst, we believe that the spread widening in non-Agency RMBS has the potential to reverse to normalized levels. Another key catalyst is the expected decline in interest rate volatility that is anticipated to occur as the Fed nears the end of the current tightening cycle. Current market consensus has the Fed reaching their terminal rate between late Q1 to early Q2. The risk premium priced into mortgage spreads moves directionally with interest rate volatility and we believe that spreads are poised to compress as volatility recedes from crisis-era levels. As an example, over the course of this year, 2021 vintage GSE CRT securities with low Loan-To-Values (LTV) at issuance have widened by almost 300 basis points relative to single-B corporates.

7

SEMPER FUNDS

We view this as a pricing dislocation that is not warranted by the fundamental profiles. Given the significant degree of structural deleveraging and asset coverage increases from home price appreciation, the credit profile of the CRT security has improved while corporate credit fundamentals have deteriorated over the timeline. This type of pricing dislocation exists across the universe of Non-Agency RMBS creating the potential for the sector to outperform as spread relationships normalize.

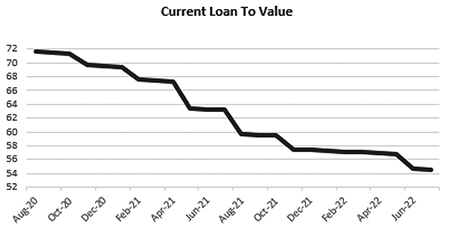

Our view is that seasoned mortgages offer one of the best opportunities for absolute and relative performance as we enter the new year. The seasoned profiles have benefited the most from fundamental improvement, yet due to market dynamics, they have yet to distinguish themselves from other credit profiles. Below is an example of a mid-2020 vintage CRT security currently valued at loss adjusted yield near 13%. The charts show LTVs that have declined significantly as well as the degree of structural improvement in credit enhancement and loss coverage ratios.

After interest rates surged higher during 2022, fixed income investments are poised to offer the benefits that investors have historically sought from their allocation. While the ultimate path and timing of the Federal Reserve’s tightening policy is still to be determined, the historical level of hikes enacted this year has created a line of sight to the future as the target rate begins to approach projections for the terminal value. Reductions in interest rate volatility is expected to lead to improved investor sentiment and demand for yields that have retraced to levels last seen nearly 15 years ago. In the midst of this backdrop, we believe that Non-Agency RMBS are poised to outperform after having experienced inordinate spread widening in 2022. Additionally, we believe that seasoned profiles, who’s pricing largely did not benefit from superior credit fundamentals in 2022, can perform even more strongly in 2023.

8

SEMPER FUNDS

Fundamental views on housing and mortgage credit combine with the favorable shift in market technicals due to a sharp supply reduction will present a supportive tone and potential tailwind, which we believe will benefit both Funds.

Sincerely,

Semper Capital Management, L.P.

Past performance is not a guarantee of future results.

Opinions expressed are those of Semper Capital Management, L.P., the Semper MBS Total Return Fund’s and the Semper Short Duration Fund’s investment adviser, and are subject to change, are not guaranteed and should not be considered investment advice.

Mutual fund investing involves risk. Principal loss is possible.

The Funds invest in debt securities: As interest rates rise, the value of debt securities decrease; whereas prepayment risk tends to occur during periods of declining interest rates. This risk is usually greater for longer-term debt securities. Recent turbulence in the financial markets and reduced liquidity in credit and fixed-income market may have an adverse effect on the Funds. Investments in mortgage-backed and asset- backed securities include additional risks that investors should be aware of such as credit risk, interest rate risk, prepayment risk, real estate market risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. Many of the risks of investing in commercial mortgage-backed securities reflect the risks of investing in the real estate securing the underlying mortgage loans. Accordingly, the Funds may not be suitable for all investors.

In addition, the MBS Total Return Fund invests in lower-rated and non-rated securities that present a greater risk of loss to principal and interest than higher-rated securities. The Fund may make short sales of securities, which involves the risk that losses to those securities may exceed the original amount invested by the Fund. The Fund may invest in securities that are less liquid which can be difficult to sell. The Fund may use certain types of investment derivatives such as futures, forwards, and swaps. Derivatives involve risks different from, and in certain cases, greater than the risks presented by more traditional investments. The Fund may use leverage which may exaggerate the effect of any increase or decrease in the value of portfolio securities. The Fund may invest in To Be Announced (“TBA”) securities which involve interest rate and investment exposure risks. The Fund may invest in when-issued securities which may involve less favorable prices for securities, when delivered, and failure to deliver securities could cause a loss to the Fund.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete listing of Fund holdings, please refer to the schedule of investments in this report.

Diversification does not assure a profit nor protect against loss in a declining market.

The Bloomberg U.S. MBS Index covers agency mortgage-backed pass-through securities – both fixed-rate and hybrid ARM – issued by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). Pool aggregates must have at least $250 million outstanding with a weighted average maturity of at least one year.

The Bloomberg 1-3 Year U.S. Government Index covers U.S. Treasury and agency securities issued by the U.S. Government with a maturity from 1 up to but not including 3 years. This unmanaged index contains only dollar-denominated issues with at least $250 million par outstanding.

The Bloomberg 1-3 Year U.S. Treasury Index covers U.S. Treasury securities issued by the U.S. Government with a maturity from 1 up to but not including 3 years. This unmanaged index contains only dollar-denominated issues with at least $250 million par outstanding.

9

SEMPER FUNDS

The Bloomberg U.S. Aggregate Index is a market capitalization-weighted index, meaning the securities in the index are weighted according to the market size of each bond type. Most U.S. traded investment grade bonds are represented. Municipal bonds, and Treasury Inflation-Protected Securities are excluded, due to tax treatment issues. The index includes Treasury securities, Government agency bonds, mortgage-backed bonds, corporate bonds, and a small amount of foreign bonds traded in the U.S.

One cannot invest directly in an index.

Effective Duration: Calculation for bonds with cash flow variability. It takes into account that expected cash flows will fluctuate as interest rates change.

Yield: Interest income divided by price for a bond or portfolio of bonds.

Yield to Maturity: Anticipated rate of return on a bond or portfolio of bonds if held until the maturity date.

Par is the face value or nominal value of a bond.

Basis point equals 1/100th of 1%.

This report must be preceded or accompanied by a prospectus.

The Semper Funds are distributed by Quasar Distributors, LLC.

10

SEMPER MBS TOTAL RETURN FUND

ALLOCATION OF PORTFOLIO ASSETS at November 30, 2022 (Unaudited)

| * | Includes Agency Credit Risk Transfer bonds, which are issued by but not guaranteed by Fannie Mae and Freddie Mac. |

Percentages represent market value as a percentage of total investments.

11

SEMPER SHORT DURATION FUND

ALLOCATION OF PORTFOLIO ASSETS at November 30, 2022 (Unaudited)

| * | Includes Agency Credit Risk Transfer bonds, which are issued by but not guaranteed by Fannie Mae and Freddie Mac. |

Percentages represent market value as a percentage of total investments.

12

SEMPER FUNDS

EXPENSE EXAMPLE at November 30, 2022 (Unaudited)

As a shareholder of a mutual fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees, and exchange fees, and (2) ongoing costs, including management fees, distribution and/or service fees, and other fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (6/1/22 – 11/30/22).

Actual Expenses

The first line of the tables below provides information about actual account values and actual expenses. You will be assessed fees for outgoing wire transfers, returned checks, and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Funds’ transfer agent. The Example below includes, but is not limited to, management fees, 12b-1 fees, fund accounting, custody and transfer agent fees. You may use this information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the tables below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

13

SEMPER FUNDS

EXPENSE EXAMPLE at November 30, 2022 (Unaudited), Continued

Total Return Fund

| Beginning | Ending | Expenses Paid | Annualized | |

| Account Value | Account Value | During Period | Expense | |

6/1/22 | 11/30/22 | 6/1/22 – 11/30/22 | Ratio(1) | |

| Class A | ||||

Actual(2) | $1,000.00 | $ 915.20 | $5.76 | 1.20% |

Hypothetical (5% return | ||||

before expenses)(3) | $1,000.00 | $1,019.05 | $6.07 | 1.20% |

| Investor Class | ||||

Actual(2) | $1,000.00 | $ 915.10 | $5.76 | 1.20% |

Hypothetical (5% return | ||||

before expenses)(3) | $1,000.00 | $1,019.05 | $6.07 | 1.20% |

| Institutional Class | ||||

Actual(2) | $1,000.00 | $ 917.20 | $4.57 | 0.95% |

Hypothetical (5% return | ||||

before expenses)(3) | $1,000.00 | $1,020.31 | $4.81 | 0.95% |

| (1) | Expenses are equal to the annualized expense ratio of each class, multiplied by the average account value over the period, multiplied by 183 (days in most recent fiscal half-year) / 365 days to reflect the one-half year expense. |

| (2) | Excluding interest expense, the actual expenses would be $5.04, $5.04, and $3.84 for Class A, Investor Class, and Institutional Class, respectively. |

| (3) | Excluding interest expense, the hypothetical expenses would be $5.32, $5.32, and $4.05 for Class A, Investor Class, and Institutional Class, respectively. |

Short Duration Fund

| Beginning | Ending | Expenses Paid | Annualized | |

| Account Value | Account Value | During Period | Expense | |

6/1/22 | 11/30/22 | 6/1/22 – 11/30/22 | Ratio(1) | |

| Investor Class | ||||

Actual(2) | $1,000.00 | $ 998.80 | $4.36 | 0.87% |

Hypothetical (5% return | ||||

before expenses)(3) | $1,000.00 | $1,020.71 | $4.41 | 0.87% |

| Institutional Class | ||||

Actual(2) | $1,000.00 | $ 999.00 | $3.11 | 0.62% |

Hypothetical (5% return | ||||

before expenses)(3) | $1,000.00 | $1,021.96 | $3.14 | 0.62% |

| (1) | Expenses are equal to the annualized expense ratio of each class, multiplied by the average account value over the period, multiplied by 183 (days in most recent fiscal half-year) / 365 days to reflect the one-half year expense. |

| (2) | Excluding interest expense, the actual expenses would be $4.26 and $3.01 for Investor Class and Institutional Class, respectively. |

| (3) | Excluding interest expense, the hypothetical expenses would be $4.31 and $3.04 for Investor Class and Institutional Class, respectively. |

14

SEMPER MBS TOTAL RETURN FUND

Comparison of the change in value of a $1,000,000 investment in the

Semper MBS Total Return Fund – Institutional Class vs

the Bloomberg U.S. MBS Index

| Since | Since | ||||

| One | Three | Five | Inception | Inception | |

Average Annual Total Return | Year | Years | Years | (7/22/13) | (12/18/15) |

| Semper MBS Total Return Fund – | |||||

| Investor Class | -14.16% | -5.17% | -1.58% | 2.31% | — |

| Semper MBS Total Return Fund – | |||||

| Institutional Class | -13.87% | -4.99% | -1.37% | 2.55% | — |

| Semper MBS Total Return Fund – | |||||

| Class A (with sales load) | -15.89% | -5.76% | -1.96% | — | -0.16% |

| Semper MBS Total Return Fund – | |||||

| Class A (without sales load) | -14.15% | -5.13% | -1.56% | — | 0.13% |

| Bloomberg U.S. MBS Index | -11.50% | -2.99% | -0.38% | 1.05% | 0.26% |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. The most recent month-end performance may be obtained by calling 1-855-736-7799 (855-SEM-PRXX).

Returns reflect reinvestment of dividends and capital gains distributions. Fee waivers were in effect prior to November 30, 2014. In the absence of fee waivers, returns would be reduced. For the years ended November 30, 2015, November 30, 2016, and November 30, 2017, the adviser recouped previously waived fees. In the absence of the recoupment, returns would be higher. Class A shares may be subject to a 2.00% front-end sales load. The performance data and graph do not reflect the deduction of taxes that a shareholder may pay on dividends, capital gains distributions, or redemption of Fund shares. This chart does not imply any future performance. Indices do not incur expenses and are not available for investment.

The Bloomberg U.S. MBS Index covers agency mortgage-backed pass-through securities – both fixed-rate and hybrid adjustable rate mortgages – issued by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). Pool aggregates must have at least $250 million par outstanding with a weighted average maturity of at least one year.

15

SEMPER SHORT DURATION FUND

Comparison of the change in value of a $1,000,000 investment in the

Semper Short Duration Fund – Institutional Class vs the Bloomberg 1-3 Year

Government Index and the Bloomberg 1-3 Year U.S. Treasury Index

| Since | |||||

| One | Three | Five | Ten | Inception | |

| Average Annual Total Return | Year | Years | Years | Years | (12/23/10) |

Semper Short Duration Fund – | |||||

| Investor Class | -2.80% | -0.68% | 0.65% | 1.12% | 1.58% |

| Semper Short Duration Fund – | |||||

| Institutional Class | -2.66% | -0.47% | 0.87% | 1.35% | 1.82% |

| Bloomberg 1-3 Year | |||||

| Government Index | -4.18% | -0.45% | 0.71% | 0.65% | 0.73% |

| Bloomberg 1-3 Year | |||||

| U.S. Treasury Index | -4.19% | -0.45% | 0.71% | 0.64% | 0.72% |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. The most recent month-end performance may be obtained by calling 1-855-736-7799 (855-SEM-PRXX).

Returns reflect reinvestment of dividends and capital gains distributions. Fee waivers are in effect. In the absence of fee waivers, returns would be reduced. The performance data and graph do not reflect the deduction of taxes that a shareholder may pay on dividends, capital gains distributions, or redemption of Fund shares. This chart does not imply any future performance. Indices do not incur expenses and are not available for investment.

The Bloomberg 1-3 Year Government Index (the “Index”) includes Treasury and agency securities issued by the U.S. Government with a maturity from one up to (but not including) three years. The Index contains only dollar denominated, investment grade issues with at least $250 million par outstanding. Total return includes the reinvestment of income.

The Bloomberg 1-3 Year U.S. Treasury Index covers U.S. Treasury securities issued by the U.S. Government with a maturity from one up to but not including three years. This unmanaged index contains only dollar-denominated issues with at least $250 million par outstanding. Total return includes the reinvestment of income.

16

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022

| Principal | ||||||||

| Amount | Value | |||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES – AGENCY – 0.0% | ||||||||

Fannie Mae-Aces | ||||||||

Series 2006-M1, Class IO, 0.209%, 3/25/36 (a)(g) | $ | 1,084,440 | $ | 6 | ||||

GNMA REMIC Trust | ||||||||

Series 2012-25, Class IO, 0.398%, 8/16/52 (a)(g) | 37,109 | 30 | ||||||

Government National Mortgage Association | ||||||||

Series 2002-28, Class IO, 0.822%, 1/16/42 (a)(g) | 9,200 | — | ||||||

Series 2005-23, Class IO, 0.004%, 6/17/45 (a)(g) | 116,624 | — | ||||||

Series 2006-68, Class IO, 0.473%, 5/16/46 (a)(g) | 114,009 | 412 | ||||||

| Total Commercial Mortgage-Backed Securities – Agency | ||||||||

| (cost $35,491) | 448 | |||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES – NON-AGENCY – 11.5% | ||||||||

Bayview Commercial Asset Trust | ||||||||

Series 2004-3, Class B2, 9.069% | ||||||||

(1 Month LIBOR USD + 5.025%), 1/25/35 (c)(h) | 33,415 | 33,500 | ||||||

Series 2006-2A, Class M1, 4.509% | ||||||||

(1 Month LIBOR USD + 0.465%), 7/25/36 (c)(h) | 648,174 | 587,908 | ||||||

Series 2006-2A, Class M3, 4.569% | ||||||||

(1 Month LIBOR USD + 0.525%), 7/25/36 (c)(h) | 936,959 | 863,663 | ||||||

Series 2006-3A, Class M1, 4.554% | ||||||||

(1 Month LIBOR USD + 0.510%), 10/25/36 (c)(h) | 819,152 | 761,834 | ||||||

Series 2007-2A, Class A1, 4.314% | ||||||||

(1 Month LIBOR USD + 0.270%), 7/25/37 (c)(h) | 1,305,632 | 1,146,796 | ||||||

Freddie Mac Multi-Family Structured Credit Risk | ||||||||

Series 2021-MN1, Class M2, 7.297% | ||||||||

(SOFR30A + 3.750%), 1/25/51 (c)(h) | 3,537,000 | 3,011,059 | ||||||

Series 2021-MN1, Class B1, 11.297% | ||||||||

(SOFR30A + 7.750%), 1/25/51 (c)(h) | 6,603,000 | 6,116,886 | ||||||

Series 2021-MN3, Class B1, 10.371% | ||||||||

(SOFR30A + 6.850%), 11/25/51 (c)(h) | 6,413,000 | 5,607,011 | ||||||

GMAC Commercial Mortgage Asset Corp. | ||||||||

Series 2005-DRUM, Class AIO, 0.171%, 5/10/50 (a)(c)(g) | 138,635,777 | 2,257,496 | ||||||

Series 2012-BLIS, Class IO, 0.576%, 7/10/50 (c)(g) | 27,557,339 | 1,520,197 | ||||||

Lehman Brothers Small Balance Commercial Mortgage Trust | ||||||||

Series 2006-3A, Class M2, 4.434% | ||||||||

(1 Month LIBOR USD + 0.390%), 12/25/36 (c)(h) | 2,705,322 | 2,592,197 | ||||||

Series 2007-1A, Class M1, 4.544% | ||||||||

(1 Month LIBOR USD + 0.500%), 3/25/37 (c)(h) | 5,881,000 | 5,586,910 | ||||||

Multi-Family Connecticut Avenue Securities Trust | ||||||||

Series 2019-01, Class M10, 7.294% | ||||||||

(1 Month LIBOR USD + 3.250%), 10/25/49 (c)(h) | 5,099,476 | 4,721,613 | ||||||

The accompanying notes are an integral part of these financial statements.

17

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Multi-Family Connecticut Avenue Securities Trust (Continued) | ||||||||

Series 2019-01, Class B10, 9.544% | ||||||||

(1 Month LIBOR USD + 5.500%), 10/25/49 (c)(h) | $ | 2,384,000 | $ | 2,114,929 | ||||

Series 2020-01, Class M10, 7.794% | ||||||||

(1 Month LIBOR USD + 3.750%), 3/25/50 (c)(h) | 1,000,000 | 917,408 | ||||||

Velocity Commercial Capital Loan Trust | ||||||||

Series 2017-2, Class M4, 5.000%, 11/25/47 (a)(c) | 333,437 | 274,102 | ||||||

Series 2018-1, Class M5, 6.260%, 4/25/48 (c) | 225,878 | 214,363 | ||||||

Series 2018-2, Class M3, 4.720%, 10/26/48 (a)(c) | 252,925 | 230,225 | ||||||

Series 2019-1, Class M5, 5.700%, 3/25/49 (a)(c) | 553,944 | 449,232 | ||||||

| Total Commercial Mortgage-Backed | ||||||||

| Securities – Non-Agency (cost $41,992,219) | 39,007,329 | |||||||

| RESIDENTIAL MORTGAGE-BACKED SECURITIES – AGENCY – 25.0% | ||||||||

Fannie Mae Connecticut Avenue Securities | ||||||||

Series 2020-R01, Class 1B1, 7.266% | ||||||||

(1 Month LIBOR USD + 3.250%), 1/25/40 (c)(h) | 1,000,000 | 942,513 | ||||||

Series 2020-SBT1, Class 2B1, 10.616% | ||||||||

(1 Month LIBOR USD + 6.600%), 2/25/40 (c)(h) | 11,475,000 | 10,291,117 | ||||||

Series 2020-SBT1, Class 1B1, 10.766% | ||||||||

(1 Month LIBOR USD + 6.750%), 2/25/40 (c)(h) | 14,106,000 | 12,653,960 | ||||||

FNMA Grantor Trust | ||||||||

Series 2003-T2, Class A1, 3.741% | ||||||||

(1 Month LIBOR USD + 0.280%), 3/25/33 (h) | 29,195 | 28,886 | ||||||

Series 2004-T3, Class 2A, 3.791%, 8/25/43 (a) | 31,429 | 30,819 | ||||||

FNMA Pool | ||||||||

Class #888534, 5.000%, 8/1/37 | 6,167 | 6,133 | ||||||

FNMA REMIC Trust | ||||||||

Series 2007-30, Class ZM, 4.250%, 4/25/37 | 60,258 | 57,617 | ||||||

Series 2007-W8, Class 1A5, 6.424%, 9/25/37 (a) | 7,333 | 7,392 | ||||||

Freddie Mac Structured Agency Credit Risk | ||||||||

Series 2021-DNA2, Class B1, 6.921% | ||||||||

(SOFR30A + 3.400%), 8/25/33 (c)(h) | 2,393,000 | 2,152,840 | ||||||

Series 2021-DNA2, Class B2, 9.521% | ||||||||

(SOFR30A + 6.000%), 8/25/33 (c)(h) | 1,000,000 | 814,104 | ||||||

Series 2019-FTR3, Class B2, 8.386% | ||||||||

(1 Month LIBOR USD + 4.800%), 9/25/47 (c)(h) | 6,233,500 | 4,883,628 | ||||||

Series 2019-FTR4, Class B2, 9.016% | ||||||||

(1 Month LIBOR USD + 5.000%), 11/25/47 (c)(h) | 10,050,000 | 8,041,081 | ||||||

Series 2019-DNA4, Class B2, 10.266% | ||||||||

(1 Month LIBOR USD + 6.250%), 10/25/49 (c)(h) | 987,000 | 884,920 | ||||||

The accompanying notes are an integral part of these financial statements.

18

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Freddie Mac Structured Agency Credit Risk (Continued) | ||||||||

Series 2020-HQA5, Class B2, 10.921% | ||||||||

(SOFR30A + 7.400%), 11/25/50 (c)(h) | $ | 4,460,000 | $ | 4,188,617 | ||||

Freddie Mac Structured Agency Credit Risk REMIC Trust | ||||||||

Series 2021-HQA1, Class B2, 8.521% | ||||||||

(SOFR30A + 5.000%), 8/25/33 (c)(h) | 1,486,000 | 1,130,788 | ||||||

Series 2021-DNA3, Class B1, 7.021% | ||||||||

(SOFR30A + 3.500%), 10/25/33 (c)(h) | 2,506,400 | 2,230,605 | ||||||

Series 2021-DNA3, Class B2, 9.771% | ||||||||

(SOFR30A + 6.250%), 10/25/33 (c)(h) | 1,000,000 | 822,153 | ||||||

Series 2021-DNA6, Class B2, 11.047% | ||||||||

(SOFR30A + 7.500%), 10/25/41 (c)(h) | 1,000,000 | 850,339 | ||||||

Series 2020-HQA1, Class B2, 9.116% | ||||||||

(1 Month LIBOR USD + 5.100%), 1/25/50 (c)(h) | 8,679,000 | 7,391,697 | ||||||

Series 2020-DNA2, Class B2, 8.816% | ||||||||

(1 Month LIBOR USD + 4.800%), 2/25/50 (c)(h) | 6,990,000 | 5,658,153 | ||||||

Series 2020-HQA2, Class B2, 11.616% | ||||||||

(1 Month LIBOR USD + 7.600%), 3/25/50 (c)(h) | 10,250,000 | 9,571,152 | ||||||

Series 2020-DNA4, Class B2, 14.016% | ||||||||

(1 Month LIBOR USD + 10.000%), 8/25/50 (c)(h) | 1,888,000 | 2,044,230 | ||||||

Series 2020-HQA4, Class B2, 13.416% | ||||||||

(1 Month LIBOR USD + 9.400%), 9/25/50 (c)(h) | 1,780,000 | 1,882,431 | ||||||

Series 2020-DNA5, Class B2, 15.021% | ||||||||

(SOFR30A + 11.500%), 10/25/50 (c)(h) | 1,810,000 | 2,030,722 | ||||||

Series 2020-DNA6, Class B2, 9.171% | ||||||||

(SOFR30A + 5.650%), 12/25/50 (c)(h) | 5,750,000 | 4,773,345 | ||||||

Freddie Mac Whole Loan Securities Trust | ||||||||

Series 2017-SC01, Class M2, 3.648%, 12/25/46 (a)(c) | 595,000 | 522,698 | ||||||

Series 2017-SC02, Class M2, 3.858%, 5/25/47 (a)(c) | 1,411,000 | 1,272,762 | ||||||

| Total Residential Mortgage-Backed | ||||||||

| Securities – Agency (cost $98,092,293) | 85,164,702 | |||||||

| RESIDENTIAL MORTGAGE-BACKED SECURITIES – NON-AGENCY – 63.0% | ||||||||

AFC Home Equity Loan Trust | ||||||||

Series 1997-3, Class 1A4, 7.470%, 9/27/27 (j) | 53,334 | 52,088 | ||||||

AMSR Trust | ||||||||

Series 2020-SFR4, Class G1, 4.002%, 11/17/37 (c) | 750,000 | 665,298 | ||||||

Series 2021-SFR3, Class H, 4.896%, 10/17/38 (c) | 1,750,000 | 1,466,244 | ||||||

Asset Backed Securities Corp. Home Equity Loan Trust | ||||||||

Series 1999-LB1, Class A1F, 7.110%, 6/21/29 | 359,644 | 355,608 | ||||||

The accompanying notes are an integral part of these financial statements.

19

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Asset Backed Securities Corp. | ||||||||

Long Beach Home Equity Loan Trust | ||||||||

Series 2000-LB1, Class AF5, 6.998%, 9/21/30 (j) | $ | 508,920 | $ | 471,819 | ||||

Banc of America Funding Corp. | ||||||||

Series 2006-D, Class 5A2, 3.009%, 5/20/36 (a) | 6,669 | 5,728 | ||||||

Series 2008-R4, Class 1A4, 4.036% | ||||||||

(1 Month LIBOR USD + 0.450%), 7/25/37 (c)(h) | 1,315,727 | 781,001 | ||||||

Bear Stearns Asset Backed Securities I Trust | ||||||||

Series 2006-IM1, Class A3, 4.604% | ||||||||

(1 Month LIBOR USD + 0.560%), 4/25/36 (h) | 4,924,148 | 6,833,345 | ||||||

Series 2006-IM1, Class A6, 4.684% | ||||||||

(1 Month LIBOR USD + 0.640%), 4/25/36 (h) | 2,924,277 | 3,926,524 | ||||||

Bellemeade Re Ltd. | ||||||||

Series 2021-2A, Class B1, 7.697% | ||||||||

(SOFR30A + 4.150%), 6/25/31 (c)(h) | 2,281,000 | 1,837,774 | ||||||

Chase Home Lending Mortgage Trust | ||||||||

Series 2019-ATR2, Class B4, 4.010%, 7/25/49 (a)(c) | 1,870,117 | 1,221,649 | ||||||

Chase Mortgage Finance Corp. | ||||||||

Series 2020-CL1, Class M4, 8.394% | ||||||||

(1 Month LIBOR USD + 4.350%), 10/25/57 (c)(h) | 318,066 | 308,170 | ||||||

Citigroup Mortgage Loan Trust | ||||||||

Series 2004-HYB4, Class WA, 3.569%, 12/25/34 (a) | 7,343 | 6,933 | ||||||

CitiMortgage Alternative Loan Trust | ||||||||

Series 2007-A7, Class 2A1, 4.444% | ||||||||

(1 Month LIBOR USD + 0.400%), 7/25/37 (h) | 154,886 | 123,348 | ||||||

COLT Mortgage Loan Trust | ||||||||

Series 2021-3, Class B2, 4.120%, 9/27/66 (a)(c) | 1,578,000 | 895,732 | ||||||

Series 2021-4, Class B2, 4.140%, 10/25/66 (a)(c) | 2,625,000 | 1,937,691 | ||||||

Conseco Finance Home Loan Trust | ||||||||

Series 2000-E, Class B1, 10.260%, 8/15/31 (a) | 121,359 | 15,798 | ||||||

CoreVest American Finance Trust | ||||||||

Series 2019-1, Class E, 5.795%, 3/15/52 (a)(c) | 242,500 | 218,097 | ||||||

Countrywide Alternative Loan Trust | ||||||||

Series 2004-15, Class 2A2, 3.757%, 9/25/34 (a) | 296,152 | 264,486 | ||||||

Series 2006-4CB, Class 2A3, 5.500%, 4/25/36 | 3,608 | 2,885 | ||||||

Series 2006-OA3, Class 1A1, 4.444% | ||||||||

(1 Month LIBOR USD + 0.400%), 5/25/36 (h) | 7,801 | 6,835 | ||||||

Series 2006-OA9, Class 1A1, 4.139% | ||||||||

(1 Month LIBOR USD + 0.200%), 7/20/46 (h) | 23,980 | 18,661 | ||||||

Countrywide Asset-Backed Certificates | ||||||||

Series 2006-24, Class 2A3, 4.194% | ||||||||

(1 Month LIBOR USD + 0.150%), 6/25/47 (h) | 928 | 926 | ||||||

The accompanying notes are an integral part of these financial statements.

20

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Credit Suisse Mortgage Trust | ||||||||

Series 2020-AFC1, Class B1, 3.445%, 2/25/50 (a)(c) | $ | 4,228,000 | $ | 3,504,524 | ||||

Series 2020-AFC1, Class B2, 4.416%, 2/25/50 (a)(c) | 5,459,650 | 4,548,422 | ||||||

Deephaven Residential Mortgage Trust | ||||||||

Series 2021-1, Class B2, 3.955%, 5/25/65 (a)(c)(e) | 3,200,000 | 2,557,694 | ||||||

Series 2021-4, Class B2, 4.472%, 11/25/66 (a)(c) | 4,000,000 | 2,703,620 | ||||||

Flagstar Mortgage Trust | ||||||||

Series 2018-1, Class B5, 3.953%, 3/25/48 (a)(c) | 1,206,000 | 649,220 | ||||||

Fort KL | ||||||||

Series 2021-SFR1, Class G, 4.105%, 9/17/38 (c) | 6,811,000 | 5,702,823 | ||||||

GreenPoint Mortgage Funding Trust | ||||||||

Series 2005-AR4, Class 4A1A, 4.664% | ||||||||

(1 Month LIBOR USD + 0.620%), 10/25/45 (h) | 16,168,121 | 14,231,850 | ||||||

GSAA Home Equity Trust | ||||||||

Series 2006-5, Class 2A1, 4.184% | ||||||||

(1 Month LIBOR USD + 0.140%), 3/25/36 (h) | 26,245 | 9,762 | ||||||

JP Morgan Mortgage Trust | ||||||||

Series 2014-IVR6, Class B4, 4.392%, 7/25/44 (a)(c) | 500,500 | 415,569 | ||||||

Series 2017-1, Class B5, 3.449%, 1/25/47 (a)(c) | 1,766,160 | 1,404,715 | ||||||

Series 2019-HYB1, Class B4, 4.052%, 10/25/49 (a)(c) | 4,979,610 | 4,437,797 | ||||||

Series 2019-5, Class B6, 4.332%, 11/25/49 (a)(c)(e) | 3,601,237 | 1,868,978 | ||||||

Series 2019-5, Class B5, 4.486%, 11/25/49 (a)(c) | 1,232,439 | 801,874 | ||||||

Series 2020-2, Class B5, 3.822%, 7/25/50 (a)(c) | 2,226,107 | 1,608,538 | ||||||

Series 2020-2, Class B6Z, 6.562%, 7/25/50 (a)(c) | 3,632,673 | 2,385,893 | ||||||

Series 2021-3, Class A3X, 0.500%, 7/25/51 (a)(c)(g) | 62,471,291 | 1,633,890 | ||||||

Series 2021-6, Class AX4, 0.200%, 10/25/51 (a)(c)(g) | 78,146,084 | 768,234 | ||||||

JP Morgan Wealth Management | ||||||||

Series 2021-CL1, Class M4, 6.297% | ||||||||

(SOFR30A + 2.750%), 3/25/51 (c)(h) | 1,036,681 | 866,669 | ||||||

Series 2021-CL1, Class M5, 7.197% | ||||||||

(SOFR30A + 3.650%), 3/25/51 (c)(h) | 705,612 | 611,725 | ||||||

Lehman Mortgage Trust | ||||||||

Series 2008-4, Class A1, 4.396% | ||||||||

(1 Month LIBOR USD + 0.380%), 1/25/37 (h) | 22,389,308 | 6,979,968 | ||||||

LSTAR Securities Investment Ltd. | ||||||||

Series 2019-3, Class A2, 8.268% | ||||||||

(1 Month LIBOR USD + 4.500%), 4/1/24 (c)(d)(h) | 3,250,159 | 3,273,958 | ||||||

Series 2019-4, Class A2, 8.268% | ||||||||

(1 Month LIBOR USD + 4.500%), 5/1/24 (c)(d)(h) | 10,441,908 | 10,516,644 | ||||||

Series 2021-1, Class A, 5.568% | ||||||||

(1 Month LIBOR USD + 1.800%), 2/1/26 (c)(d)(h) | 926,614 | 839,102 | ||||||

Series 2021-2, Class A2, 6.518% | ||||||||

(1 Month LIBOR USD + 2.750%), 3/2/26 (c)(d)(h) | 9,730,449 | 9,800,028 | ||||||

The accompanying notes are an integral part of these financial statements.

21

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Merrill Lynch Mortgage Investors Trust | ||||||||

Series 2005-AR1, Class M2, 5.049% | ||||||||

(1 Month LIBOR USD + 1.005%), 6/25/36 (h) | $ | 2,285,675 | $ | 1,925,275 | ||||

Mill City Mortgage Loan Trust | ||||||||

Series 2019-1, Class B1, 3.500%, 10/25/69 (a)(c) | 2,245,863 | 1,755,532 | ||||||

Morgan Stanley Residential Mortgage Loan Trust | ||||||||

Series 2021-5, Class A9IO, 0.250%, 8/25/51 (a)(c)(g) | 37,254,224 | 504,515 | ||||||

New Residential Mortgage Loan Trust | ||||||||

Series 2021-NQ2R, Class B1, 3.008%, 10/25/58 (a)(c)(e) | 2,034,000 | 1,677,818 | ||||||

Series 2021-NQ2R, Class B2, 3.963%, 10/25/58 (a)(c)(e) | 1,813,000 | 1,428,718 | ||||||

NMLT Trust | ||||||||

Series 2021-INV1, Class B1, 3.613%, 5/25/56 (a)(c) | 7,326,000 | 4,615,282 | ||||||

Series 2021-INV2, Class B2, 4.072%, 8/25/56 (a)(c) | 4,000,000 | 2,589,869 | ||||||

Oaktown Re VI Ltd. | ||||||||

Series 2021-1A, Class M2, 7.497% | ||||||||

(SOFR30A + 3.950%), 10/25/33 (c)(h) | 1,226,000 | 1,108,991 | ||||||

Pretium Mortgage Credit Partners LLC | ||||||||

Series 2021-NPL6, Class A2, 5.071%, 7/25/51 (c)(j) | 2,503,000 | 2,207,696 | ||||||

Progress Residential Trust | ||||||||

Series 2020-SFR3, Class H, 6.234%, 10/17/27 (c) | 1,000,000 | 926,143 | ||||||

RAAC Series Trust | ||||||||

Series 2004-SP1, Class AI3, 6.118%, 3/25/34 (d) | 2,064 | 1,995 | ||||||

Radnor RE Ltd. | ||||||||

Series 2021-2, Class M2, 8.547% | ||||||||

(SOFR30A + 5.000%), 11/25/31 (c)(h) | 1,234,000 | 1,153,937 | ||||||

RALI Series Trust | ||||||||

Series 2006-QS6, Class 1AV, 0.771%, 6/25/36 (a)(g) | 5,241,331 | 114,125 | ||||||

Series 2006-QS6, Class 1A11, 4.744% | ||||||||

(1 Month LIBOR USD + 0.700%), 6/25/36 (h) | 2,315,143 | 1,841,359 | ||||||

RAMP Series Trust | ||||||||

Series 2007-RS1, Class A3, 4.384% | ||||||||

(1 Month LIBOR USD + 0.340%), 2/25/37 (h) | 9,723,687 | 2,915,906 | ||||||

Series 2007-RS1, Class A4, 4.604% | ||||||||

(1 Month LIBOR USD + 0.560%), 2/25/37 (h) | 10,547,597 | 2,801,870 | ||||||

Reperforming Loan REMIC Trust | ||||||||

Series 2005-R1, Class 1AF1, 4.404% | ||||||||

(1 Month LIBOR USD + 0.360%), 3/25/35 (c)(h) | 1,601,648 | 1,516,673 | ||||||

Series 2006-R1, Class AF1, 4.384% | ||||||||

(1 Month LIBOR USD + 0.340%), 1/25/36 (c)(h) | 2,069,027 | 1,966,230 | ||||||

Residential Accredit Loans, Inc. Series Trust | ||||||||

Series 2005-QS13, Class 2A1, 4.716% | ||||||||

(1 Month LIBOR USD + 0.700%), 9/25/35 (h) | 3,016,480 | 2,377,008 | ||||||

The accompanying notes are an integral part of these financial statements.

22

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Residential Accredit Loans, Inc. Series Trust (Continued) | ||||||||

Series 2006-QS6, Class 1A9, 4.644% | ||||||||

(1 Month LIBOR USD + 0.600%), 6/25/36 (h) | $ | 2,832,407 | $ | 2,238,011 | ||||

Series 2008-QR1, Class 2A1, 4.544% | ||||||||

(1 Month LIBOR USD + 0.500%), 9/25/36 (h) | 1,548,223 | 1,109,417 | ||||||

Series 2006-QS18, Class 1A1, 4.644% | ||||||||

(1 Month LIBOR USD + 0.600%), 12/25/36 (h) | 2,718,634 | 2,162,352 | ||||||

Residential Funding Securities Corp. | ||||||||

Series 2002-RP1, Class A1, 4.904% | ||||||||

(1 Month LIBOR USD + 0.860%), 3/25/33 (c)(h) | 498,345 | 486,393 | ||||||

Seasoned Credit Risk Transfer Trust | ||||||||

Series 2018-2, Class XSIO, 0.065%, 11/25/57 (a) | 431,309,126 | 1,175,576 | ||||||

Series 2018-2, Class BX, 3.164%, 11/25/57 (a) | 8,004,612 | 2,632,426 | ||||||

Star Trust | ||||||||

Series 2021-SFR2, Class G, 7.304% | ||||||||

(1 Month LIBOR USD + 3.400%), 1/17/24 (c)(h) | 2,800,000 | 2,697,003 | ||||||

Series 2021-SFR2, Class H, 8.054% | ||||||||

(1 Month LIBOR USD + 4.150%), 1/17/24 (c)(h) | 2,421,000 | 2,320,062 | ||||||

Series 2021-SFR1, Class H, 8.354% | ||||||||

(1 Month LIBOR USD + 4.450%), 4/17/38 (c)(h) | 1,000,000 | 937,400 | ||||||

Starwood Mortgage Residential Trust | ||||||||

Series 2020-INV1, Class B1, 3.257%, 11/25/55 (c) | 2,750,000 | 2,084,218 | ||||||

Series 2020-INV1, Class B2, 4.261%, 11/25/55 (c) | 1,000,000 | 792,107 | ||||||

Structured Adjustable Rate Mortgage Loan Trust | ||||||||

Series 2005-21, Class 3A1, 3.530%, 11/25/35 (a) | 27,286 | 24,149 | ||||||

Terwin Mortgage Trust | ||||||||

Series 2004-4SL, Class B3, 8.000%, 3/25/34 (a)(c) | 21,259 | 15,990 | ||||||

Towd Point Mortgage Trust | ||||||||

Series 2019-HY1, Class B2, 6.194% | ||||||||

(1 Month LIBOR USD + 2.150%), 10/25/48 (c)(h) | 11,739,000 | 10,881,381 | ||||||

Series 2019-HY1, Class B3, 6.194% | ||||||||

(1 Month LIBOR USD + 2.150%), 10/25/48 (c)(h) | 6,170,000 | 4,556,840 | ||||||

Series 2019-HY1, Class B4, 6.194% | ||||||||

(1 Month LIBOR USD + 2.150%), 10/25/48 (c)(h) | 6,170,000 | 4,253,067 | ||||||

Series 2019-1, Class B2, 3.704%, 3/25/58 (a)(c) | 4,000,000 | 2,722,655 | ||||||

Series 2018-6, Class B2, 3.837%, 3/25/58 (a)(c) | 2,750,000 | 1,975,010 | ||||||

Series 2018-3, Class B2, 3.672%, 5/25/58 (a)(c) | 1,750,000 | 1,223,496 | ||||||

Series 2019-HY2, Class B2, 6.294% | ||||||||

(1 Month LIBOR USD + 2.250%), 5/25/58 (c)(h) | 8,639,000 | 7,387,853 | ||||||

Series 2019-HY2, Class B3, 6.294% | ||||||||

(1 Month LIBOR USD + 2.250%), 5/25/58 (c)(h) | 2,294,000 | 1,732,485 | ||||||

Series 2019-HY2, Class B4, 6.294% | ||||||||

(1 Month LIBOR USD + 2.250%), 5/25/58 (c)(h) | 1,836,000 | 1,316,752 | ||||||

The accompanying notes are an integral part of these financial statements.

23

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Towd Point Mortgage Trust (Continued) | ||||||||

Series 2019-HY3, Class B1, 6.044% | ||||||||

(1 Month LIBOR USD + 2.000%), 10/25/59 (c)(h) | $ | 5,514,000 | $ | 4,842,845 | ||||

Series 2019-HY3, Class B2, 6.044% | ||||||||

(1 Month LIBOR USD + 2.000%), 10/25/59 (c)(h) | 4,130,000 | 3,526,222 | ||||||

Series 2019-HY3, Class B3, 6.044% | ||||||||

(1 Month LIBOR USD + 2.000%), 10/25/59 (c)(h) | 1,106,000 | 798,400 | ||||||

Series 2019-HY3, Class B4, 6.044% | ||||||||

(1 Month LIBOR USD + 2.000%), 10/25/59 (c)(h) | 1,105,000 | 750,123 | ||||||

TRK Trust | ||||||||

Series 2021-INV2, Class B1, 4.104%, 11/25/56 (a)(c) | 4,000,000 | 2,613,849 | ||||||

Verus Securitization Trust | ||||||||

Series 2019-INV3, Class B2, 4.791%, 11/25/59 (a)(c) | 650,000 | 511,094 | ||||||

Series 2021-R3, Class B2, 4.070%, 4/25/64 (a)(c)(e) | 3,081,000 | 2,126,848 | ||||||

Series 2021-5, Class B2, 3.941%, 9/25/66 (a)(c)(e) | 1,750,000 | 1,235,313 | ||||||

Series 2021-6, Class B2, 4.526%, 10/25/66 (a)(c) | 4,369,000 | 2,632,447 | ||||||

Series 2021-8, Class B2, 4.334%, 11/25/66 (a)(c)(j) | 288,000 | 180,063 | ||||||

VOLT LLC | ||||||||

Series 2021-NPL4, Class A2, 4.949%, 3/27/51 (c)(j) | 1,500,000 | 1,284,852 | ||||||

Washington Mutual Mortgage Pass-Through | ||||||||

Certificates Series Trust | ||||||||

Series 2007-4, Class 1A5, 7.000%, 6/25/37 | 5,106,767 | 2,379,388 | ||||||

| Total Residential Mortgage-Backed | ||||||||

| Securities – Non-Agency (cost $277,048,806) | 214,573,166 | |||||||

| PRIVATE PLACEMENT PARTICIPATION AGREEMENT – 0.0% | ||||||||

CCTC Acquisition Partners LLC, | ||||||||

Convertible Promissory Note | ||||||||

12.000%, 2/8/23 (e)(f)(i) | 749,058 | 0 | ||||||

| Total Private Placement Participation Agreement | ||||||||

| (cost $749,058) | 0 | |||||||

The accompanying notes are an integral part of these financial statements.

24

SEMPER MBS TOTAL RETURN FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Shares | Value | |||||||

| MONEY MARKET FUND – 2.3% | ||||||||

First American Government | ||||||||

Obligations Fund – Class Z, 3.632% (b) | 7,992,460 | $ | 7,992,460 | |||||

| Total Money Market Fund (cost $7,992,460) | 7,992,460 | |||||||

| Total Investments (cost $425,910,327) – 101.8% | 346,738,105 | |||||||

| Liabilities less Other Assets – (1.8)% | (6,248,704 | ) | ||||||

| TOTAL NET ASSETS – 100.0% | $ | 340,489,401 | ||||||

| (a) | Variable rate security. The coupon is based on an underlying pool of loans and represents the rate in effect as of November 30, 2022. |

| (b) | Rate shown is the 7-day annualized yield as of November 30, 2022. |

| (c) | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in the program or other “qualified institutional buyers.” As of November 30, 2022, the value of these investments was $281,608,929 or 82.7% of total net assets. |

| (d) | Step-up bond. The interest rate may step up conditioned upon the aggregate remaining principal balance of the underlying mortgage loans being reduced below a targeted percentage of the aggregate original principal balance of the mortgage loans. The interest rate shown is the rate in effect as of November 30, 2022. |

| (e) | Security valued at fair value using procedures adopted by Semper Capital Management, L.P., the Fund’s valuation designee. Value determined using significant unobservable inputs. As of November 30, 2022, the total value of fair valued securities was $10,895,369 or 3.2% of total net assets. |

| (f) | Non-income producing. |

| (g) | Interest only security. |

| (h) | Variable or floating rate security based on a reference index and spread. The rate reported is the rate in effect as of November 30, 2022. |

| (i) | Security is restricted. The Fund cannot sell or otherwise transfer this agreement without prior written approval of CCTC Acquisition Partners LLC. As of November 30, 2022, the value of this investment was $0 or 0.0% of total net assets. The security was acquired in February 2018 at a cost of $749,058. |

| (j) | Step-up bond. The interest rate will step up if the issuer does not redeem the bond by an expected redemption date. The interest rate shown is the rate in effect as of November 30, 2022. |

FNMA – Federal National Mortgage Association

GNMA – Government National Mortgage Association

LIBOR – London Interbank Offered Rate

REMIC – Real Estate Mortgage Investment Conduit

SOFR – Secured Overnight Financing Rate

The accompanying notes are an integral part of these financial statements.

25

SEMPER SHORT DURATION FUND

SCHEDULE OF INVESTMENTS at November 30, 2022

| Principal | ||||||||

| Amount | Value | |||||||

| ASSET-BACKED SECURITIES – NON-AGENCY – 1.7% | ||||||||

Exeter Automobile Receivables Trust | ||||||||

Series 2021-2A, Class D, 1.400%, 4/15/27 | $ | 950,000 | $ | 866,613 | ||||

Series 2021-4A, Class D, 1.960%, 1/17/28 | 560,000 | 506,937 | ||||||

GLS Auto Receivables Trust | ||||||||

Series 2020-4A, Class D, 1.640%, 10/15/26 (c) | 1,750,000 | 1,662,606 | ||||||

SLM Private Credit Student Loan Trust | ||||||||

Series 2003-C, Class A5, 4.953% | ||||||||

(28 Day Auction Rate + 0.000%), 9/15/32 (f) | 200,000 | 194,236 | ||||||

SoFi Professional Loan Program, LLC | ||||||||

Series 2016-B, Class A1, 5.216% | ||||||||

(1 Month LIBOR USD + 1.200%), 6/25/33 (c)(f) | 57,716 | 57,689 | ||||||

Series 2016-C, Class A1, 5.116% | ||||||||

(1 Month LIBOR USD + 1.100%), 10/27/36 (c)(f) | 60,382 | 60,371 | ||||||

South Carolina Student Loan Corp. | ||||||||

Series 2013-1, Class A, 4.544% | ||||||||

(1 Month LIBOR USD + 0.500%), 1/25/41 (f) | 86,033 | 85,431 | ||||||

| Total Asset-Backed Securities – Non-Agency | ||||||||

| (cost $3,652,283) | 3,433,883 | |||||||

| COLLATERALIZED LOAN OBLIGATIONS – 22.8% | ||||||||

Anchorage Capital CLO Ltd. | ||||||||

Series 2014-4RA, Class A, 5.424% | ||||||||

(3 Month LIBOR USD + 1.050%), 1/28/31 (c)(f) | 2,448,796 | 2,416,795 | ||||||

Apidos CLO XV | ||||||||

Series 2013-15A, Class A1RR, 5.253% | ||||||||

(3 Month LIBOR USD + 1.010%), 4/20/31 (c)(f) | 1,000,000 | 984,373 | ||||||

Apidos CLO XXIV | ||||||||

Series 2016-24A, Class A1AL, 5.193% | ||||||||

(3 Month LIBOR USD + 0.950%), 10/20/30 (c)(f) | 2,500,000 | 2,455,747 | ||||||

Atlas Senior Loan Fund IX Ltd. | ||||||||

Series 2018-9A, Class A, 5.113% | ||||||||

(3 Month LIBOR USD + 0.870%), 4/20/28 (c)(f) | 919,502 | 912,606 | ||||||

Benefit Street Partners CLO V-B Ltd. | ||||||||

Series 2018-5BA, Class A1A, 5.333% | ||||||||

(3 Month LIBOR USD + 1.090%), 4/20/31 (c)(f) | 1,680,000 | 1,649,163 | ||||||

Carlyle Global Market Strategies CLO Ltd. | ||||||||

Series 2014-5A, Class A1RR, 5.219% | ||||||||

(3 Month LIBOR USD + 1.140%), 7/15/31 (c)(f) | 2,243,454 | 2,201,305 | ||||||

Series 2015-AR3, Class 1A, 5.223% | ||||||||

(3 Month LIBOR USD + 0.980%), 7/20/31 (c)(f) | 1,761,799 | 1,720,190 | ||||||

The accompanying notes are an integral part of these financial statements.

26

SEMPER SHORT DURATION FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Crestline Denali CLO XVII Ltd. | ||||||||

Series 2018-1A, Class AR, 5.139% | ||||||||

(3 Month LIBOR USD + 1.060%), 10/15/31 (c)(f) | $ | 2,500,000 | $ | 2,459,638 | ||||

Crown Point CLO IV Ltd. | ||||||||

Series 2018-4A, Class A, 5.343% | ||||||||

(3 Month LIBOR USD + 1.100%), 4/20/31 (c)(f) | 2,177,000 | 2,139,503 | ||||||

Ellington CLO IV Ltd. | ||||||||

Series 2019-4A, Class AR, 5.659% | ||||||||

(3 Month LIBOR USD + 1.580%), 4/15/29 (c)(f) | 613,986 | 609,703 | ||||||

ICG US CLO Ltd. | ||||||||

Series 2015-1A, Class A1R, 5.367% | ||||||||

(3 Month LIBOR USD + 1.140%), 10/19/28 (c)(f) | 1,284,807 | 1,268,747 | ||||||

KKR CLO 9 Ltd. | ||||||||

Series 2017-9, Class AR2, 5.029% | ||||||||

(3 Month LIBOR USD + 0.950%), 7/15/30 (c)(f) | 742,535 | 728,225 | ||||||

KKR Financial CLO Ltd. | ||||||||

Series 2013-1A, Class A1R, 5.369% | ||||||||

(3 Month LIBOR USD + 1.290%), 4/15/29 (c)(f) | 1,645,525 | 1,628,861 | ||||||

Mountain View CLO X Ltd. | ||||||||

Series 2015-10A, Class AR, 4.761% | ||||||||

(3 Month LIBOR USD + 0.820%), 10/13/27 (c)(f) | 1,013,327 | 1,008,207 | ||||||

Nassau II Ltd. | ||||||||

Series 2017-IIA, Class AL, 5.329% | ||||||||

(3 Month LIBOR USD + 1.250%), 1/15/30 (c)(f) | 732,791 | 724,922 | ||||||

Neuberger Berman Loan Advisers CLO 25 Ltd. | ||||||||

Series 2017-25A, Class AR, 5.124% | ||||||||

(3 Month LIBOR USD + 0.930%), 10/18/29 (c)(f) | 2,955,000 | 2,906,777 | ||||||

Newfleet CLO Ltd. | ||||||||

Series 2016-1A, Class A1R, 5.193% | ||||||||

(3 Month LIBOR USD + 0.950%), 4/20/28 (c)(f) | 61,564 | 61,219 | ||||||

OHA Credit Partners VII Ltd. | ||||||||

Series 2012-7A, Class AR3, 5.745% | ||||||||

(3 Month LIBOR USD + 1.070%), 2/20/34 (c)(f) | 726,000 | 700,037 | ||||||

OZLM VI Ltd. | ||||||||

Series 2014-6A, Class A1S, 5.159% | ||||||||

(3 Month LIBOR USD + 1.080%), 4/17/31 (c)(f) | 2,955,609 | 2,889,261 | ||||||

OZLM VIII Ltd. | ||||||||

Series 2014-8A, Class A1R3, 5.059% | ||||||||

(3 Month LIBOR USD + 0.980%), 10/17/29 (c)(f) | 2,241,405 | 2,203,729 | ||||||

Regatta XIV Funding Ltd. | ||||||||

Series 2018-3A, Class A, 5.548% | ||||||||

(3 Month LIBOR USD + 1.190%), 10/25/31 (c)(f) | 1,000,000 | 979,360 | ||||||

The accompanying notes are an integral part of these financial statements.

27

SEMPER SHORT DURATION FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Saranac CLO III Ltd. | ||||||||

Series 2014-3A, Class ALR, 5.202% | ||||||||

(3 Month LIBOR USD + 1.600%), 6/22/30 (c)(f) | $ | 1,734,104 | $ | 1,713,859 | ||||

Saranac CLO VII Ltd. | ||||||||

Series 2014-2A, Class A1AR, 5.905% | ||||||||

(3 Month LIBOR USD + 1.230%), 11/20/29 (c)(f) | 1,994,458 | 1,971,117 | ||||||

Sound Point CLO V-R Ltd. | ||||||||

Series 2014-IRA, Class A, 5.344% | ||||||||

(3 Month LIBOR USD + 1.150%), 7/18/31 (c)(f) | 1,550,000 | 1,508,895 | ||||||

Sound Point CLO XXI Ltd. | ||||||||

Series 2018-3A, Class A1A, 5.507% | ||||||||

(3 Month LIBOR USD + 1.180%), 10/26/31 (c)(f) | 1,000,000 | 971,773 | ||||||

Telos CLO Ltd. | ||||||||

Series 2013-4A, Class AR, 5.319% | ||||||||

(3 Month LIBOR USD + 1.240%), 1/17/30 (c)(f) | 1,063,083 | 1,047,003 | ||||||

Venture XVII CLO Ltd. | ||||||||

Series 2014-17A, Class ARR, 4.959% | ||||||||

(3 Month LIBOR USD + 0.880%), 4/15/27 (c)(f) | 1,342,935 | 1,321,130 | ||||||

Wellfleet CLO Ltd. | ||||||||

Series 2017-2A, Class A1R, 5.303% | ||||||||

(3 Month LIBOR USD + 1.060%), 10/20/29 (c)(f) | 2,925,980 | 2,881,684 | ||||||

Zais CLO 8 Ltd. | ||||||||

Series 2018-1A, Class A, 5.029% | ||||||||

(3 Month LIBOR USD + 0.950%), 4/15/29 (c)(f) | 1,010,779 | 998,197 | ||||||

| Total Collateralized Loan Obligations (cost $45,763,509) | 45,062,026 | |||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES – AGENCY – 0.0% | ||||||||

GNMA | ||||||||

Series 2009-4, Class IO, 0.390%, 1/16/49 (a)(d) | 302,690 | 740 | ||||||

| Total Commercial Mortgage-Backed Securities – Agency | ||||||||

| (cost $1,655) | 740 | |||||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES – NON-AGENCY – 24.1% | ||||||||

Arbor Realty Collateralized Loan Obligation Ltd. | ||||||||

Series 2021-FL2, Class C, 5.825% | ||||||||

(1 Month LIBOR USD + 1.950%), 5/15/36 (c)(f) | 1,113,000 | 1,042,584 | ||||||

Series 2021-FL2, Class D, 6.375% | ||||||||

(1 Month LIBOR USD + 2.500%), 5/15/36 (c)(f) | 3,000,000 | 2,777,621 | ||||||

Bayview Commercial Asset Trust | ||||||||

Series 2007-2A, Class A1, 4.314% | ||||||||

(1 Month LIBOR USD + 0.270%), 7/25/37 (c)(f) | 205,583 | 180,573 | ||||||

The accompanying notes are an integral part of these financial statements.

28

SEMPER SHORT DURATION FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

BDS Ltd. | ||||||||

Series 2021-FL7, Class D, 6.289% | ||||||||

(1 Month LIBOR USD + 2.350%), 6/16/36 (c)(f) | $ | 3,250,000 | $ | 3,027,101 | ||||

Series 2021-FL7, Class E, 6.739% | ||||||||

(1 Month LIBOR USD + 2.800%), 6/16/36 (c)(f) | 2,500,000 | 2,299,987 | ||||||

BX Commercial Mortgage Trust | ||||||||

Series 2021-VOLT, Class F, 6.275% | ||||||||

(1 Month LIBOR USD + 2.400%), 9/15/36 (c)(f) | 2,500,000 | 2,311,559 | ||||||

Series 2021-VOLT, Class G, 6.725% | ||||||||

(1 Month LIBOR USD + 2.850%), 9/15/36 (c)(f) | 1,500,000 | 1,375,101 | ||||||

Series 2019-XL, Class F, 5.909% | ||||||||

(1 Month LIBOR USD + 2.114%), 10/15/36 (c)(f) | 850,000 | 817,102 | ||||||

Series 2019-XL, Class G, 6.209% | ||||||||

(1 Month LIBOR USD + 2.414%), 10/15/36 (c)(f) | 1,717,000 | 1,642,523 | ||||||

Series 2021-SOAR, Class E, 5.676% | ||||||||

(1 Month LIBOR USD + 1.800%), 6/15/38 (c)(f) | 3,473,686 | 3,252,264 | ||||||

BXMT Ltd. | ||||||||

Series 2020-FL3, Class A, 4.881% | ||||||||

(1 Month LIBOR USD + 1.514%), 11/15/37 (c)(f)(g) | 1,250,000 | 1,232,099 | ||||||

Series 2020-FL2, Class C, 5.639% | ||||||||

(1 Month LIBOR USD + 1.764%), 2/15/38 (c)(f)(g) | 2,950,000 | 2,781,095 | ||||||

Series 2020-FL2, Class D, 5.939% | ||||||||

(1 Month LIBOR USD + 2.064%), 2/15/38 (c)(f)(g) | 2,000,000 | 1,906,323 | ||||||

Series 2021-FL4, Class C, 5.625% | ||||||||

(1 Month LIBOR USD + 1.750%), 5/15/38 (c)(f)(g) | 3,000,000 | 2,762,514 | ||||||

Series 2021-FL4, Class D, 6.125% | ||||||||

(1 Month LIBOR USD + 2.250%), 5/15/38 (c)(f)(g) | 3,500,000 | 3,200,351 | ||||||

DBCG Mortgage Trust | ||||||||

Series 2017-BBG, Class C, 4.876% | ||||||||

(1 Month LIBOR USD + 1.000%), 6/15/34 (c)(f) | 350,000 | 337,760 | ||||||

HGI CRE CLO Ltd. | ||||||||

Series 2021-FL1, Class C, 5.587% | ||||||||

(1 Month LIBOR USD + 1.700%), 6/16/36 (c)(f) | 2,500,000 | 2,370,810 | ||||||

Series 2021-FL1, Class D, 6.237% | ||||||||

(1 Month LIBOR USD + 2.350%), 6/16/36 (c)(f) | 2,000,000 | 1,850,823 | ||||||

Series 2021-FL1, Class E, 6.837% | ||||||||

(1 Month LIBOR USD + 2.950%), 6/16/36 (c)(f) | 750,000 | 691,800 | ||||||

Series 2021-FL2, Class D, 6.037% | ||||||||

(1 Month LIBOR USD + 2.150%), 9/17/36 (c)(f)(g) | 1,500,000 | 1,376,642 | ||||||

Series 2021-FL2, Class E, 6.337% | ||||||||

(1 Month LIBOR USD + 2.450%), 9/17/36 (c)(f)(g) | 2,038,000 | 1,863,479 | ||||||

The accompanying notes are an integral part of these financial statements.

29

SEMPER SHORT DURATION FUND

SCHEDULE OF INVESTMENTS at November 30, 2022, Continued

| Principal | ||||||||

| Amount | Value | |||||||

Multi-Family Housing Mortgage Loan Trust | ||||||||

Series 2021-FL5, Class D, 6.478% | ||||||||

(1 Month LIBOR USD + 2.614%), 7/15/36 (c)(f) | $ | 1,500,000 | $ | 1,403,982 | ||||

Series 2021-FL6, Class C, 5.761% | ||||||||

(1 Month LIBOR USD + 1.850%), 7/16/36 (c)(f) | 3,300,000 | 3,089,781 | ||||||

Series 2021-FL7, Class E, 6.739% | ||||||||

(1 Month LIBOR USD + 2.800%), 10/16/36 (c)(f) | 1,700,000 | 1,568,447 | ||||||

STWD Ltd. | ||||||||

Series 2021-FL2, Class D, 6.711% | ||||||||

(1 Month LIBOR USD + 2.800%), 4/18/38 (c)(f) | 2,000,000 | 1,838,158 | ||||||

Velocity Commercial Capital Loan Trust | ||||||||

Series 2017-2, Class AFL, 4.944% | ||||||||

(1 Month LIBOR USD + 0.900%), 11/25/47 (c)(f) | 106,052 | 105,459 | ||||||

Series 2019-2, Class M3, 3.480%, 7/25/49 (a)(c) | 389,580 | 345,921 | ||||||

| Total Commercial Mortgage-Backed Securities – | ||||||||

| Non-Agency (cost $50,847,086) | 47,451,859 | |||||||

| CORPORATE BOND – 1.0% | ||||||||

Korth Direct Mortgage, Inc. | ||||||||

10.000%, 3/25/25 (c)(h) | 2,000,000 | 1,891,250 | ||||||

| Total Corporate Bond (cost $1,896,473) | 1,891,250 | |||||||

| RESIDENTIAL MORTGAGE-BACKED SECURITIES – AGENCY – 24.2% | ||||||||

Fannie Mae Connecticut Avenue Securities | ||||||||

Series 2014-C04, Class 2M2, 9.016% | ||||||||

(1 Month LIBOR USD + 5.000%), 11/25/24 (f) | 93,337 | 94,270 | ||||||

Series 2017-C01, Class 1ED1, 5.266% | ||||||||

(1 Month LIBOR USD + 1.250%), 7/25/29 (f) | 191,468 | 191,255 | ||||||

Series 2017-C01, Class 1B1, 9.766% | ||||||||

(1 Month LIBOR USD + 5.750%), 7/25/29 (f) | 2,960,000 | 3,184,007 | ||||||

Series 2017-C03, Class 1M2C, 7.016% | ||||||||

(1 Month LIBOR USD + 3.000%), 10/25/29 (f) | 1,000,000 | 978,657 | ||||||

Series 2017-C04, Class 2M2, 6.866% | ||||||||

(1 Month LIBOR USD + 2.850%), 11/25/29 (f) | 917,253 | 931,467 | ||||||

Series 2019-R06, Class 2B1, 7.794% | ||||||||

(1 Month LIBOR USD + 3.750%), 9/25/39 (c)(f) | 2,000,000 | 1,935,810 | ||||||

Series 2020-SBT1, Class 1M2, 7.666% | ||||||||

(1 Month LIBOR USD + 3.650%), 2/25/40 (c)(f) | 1,983,000 | 1,941,724 | ||||||

Series 2021-R01, Class 1M2, 5.071% | ||||||||

(SOFR30A + 1.550%), 10/25/41 (c)(f) | 3,350,000 | 3,220,020 | ||||||

The accompanying notes are an integral part of these financial statements.

30

SEMPER SHORT DURATION FUND