UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07959

Advisors Series Trust

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Jeffrey T. Rauman, President/Chief Executive Officer

Advisors Series Trust

c/o U.S. Bancorp Fund Services, LLC

777 East Wisconsin Avenue, 5th Floor

Milwaukee, WI 53202

(Name and address of agent for service)

(Name and address of agent for service)

(626) 914-7363

Registrant's telephone number, including area code

Date of fiscal year end: September 30, 2023

Date of reporting period: September 30, 2023

Item 1. Reports to Stockholders.

(a)

| Annual Report | |

| September 30, 2023 |

Poplar Forest Funds

Poplar Forest Partners Fund

Class A (PFPFX)

Class I (IPFPX)

Poplar Forest Cornerstone Fund

Investor Class (IPFCX)

POPLAR FOREST FUNDS

TABLE OF CONTENTS

| Performance | 1 |

| Letter to Partner | 2 |

| Sector Allocation of Portfolio Assets | 14 |

| Expense Example | 16 |

| Investment Highlights | 18 |

| Schedules of Investments | 21 |

| Statements of Assets and Liabilities | 28 |

| Statements of Operations | 30 |

| Statements of Changes in Net Assets | 31 |

| Financial Highlights | 33 |

| Notes to Financial Statements | 36 |

| Report of Independent Registered Public Accounting Firm | 47 |

| Notice to Shareholders | 49 |

| Information about Trustees and Officers | 50 |

| Householding | 54 |

| Privacy Notice | 55 |

POPLAR FOREST FUNDS

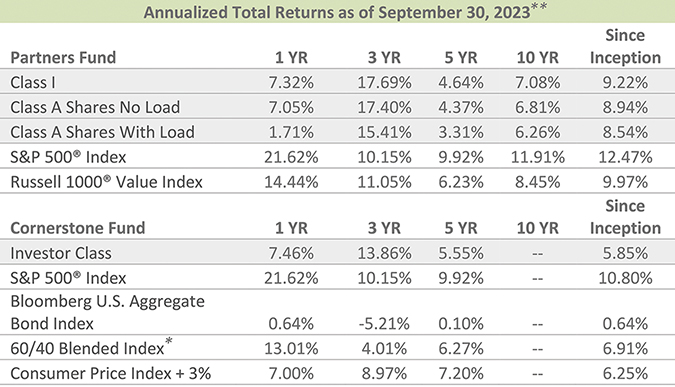

Performance of each Fund class for the 1-, 3-, 5-, 10-year and since inception periods as of September 30, 2023 is as follows:

| * | The 60/40 blended index comprises 60% S&P 500® Index and 40% Bloomberg U.S. Aggregate Bond Index. | |

| ** | Returns for periods greater than 1 year have been annualized. |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 1-877-522-8860. Performance for Class A shares with load reflects a maximum 5.00% sales charge. Class A shares without load do not take into account any sales charges which would reduce performance.

As of the Funds’ most recently filed registration statement, the Partners Fund Class A shares gross expense ratio is 1.29%; net expense ratio is 1.20% and is applicable to investors. The Partners Fund Institutional Class shares gross expense ratio is 1.04%; net expense ratio is 0.95% and is applicable to investors. The Cornerstone Fund gross expense ratio is 1.44%; net expense ratio is 0.90% and is applicable to investors. The Adviser has contractually agreed to the fee waiver through at least January 27, 2024.

| Poplar Forest Funds Annual Report, September 2023 | |

1

POPLAR FOREST FUNDS

Portfolio Manager Commentary

Dear Partner,

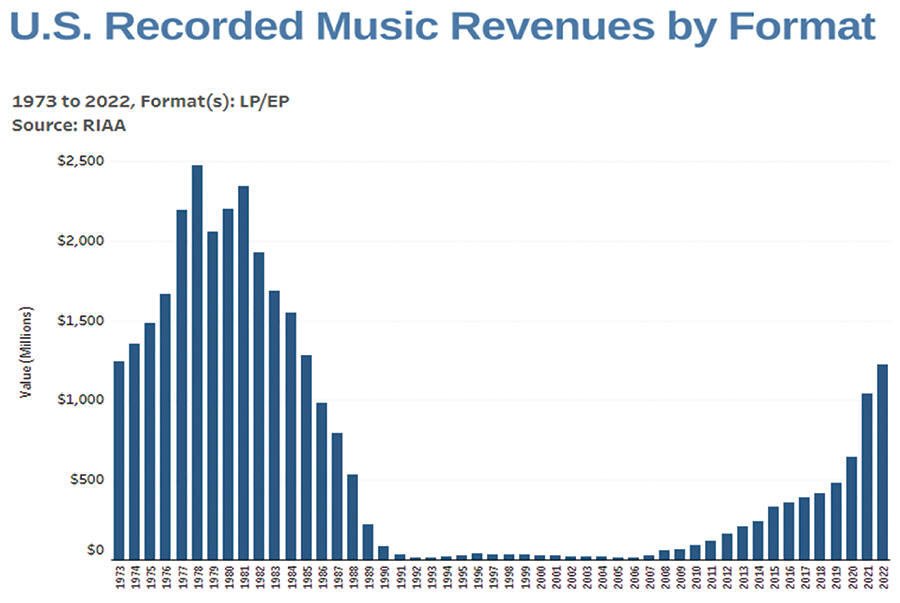

I’ve been a music nut since I was in middle school. As soon as my savings allowed, I bought a stereo system that provided hours of listening pleasure all through high school and college. By graduation, LPs were giving way to compact discs. Then came MP3s and streaming. I’ve been a Spotify devotee for more than a decade and I find it is simply amazing that my phone can access over 100 million songs virtually anywhere, anytime.

As mind-boggling as Spotify is, I found myself missing the sound quality and physical interaction with my carefully curated album collection. I still had more than a hundred of my beloved LPs – from The Clash, to B.B. King, Tom Petty, Stevie Ray Vaughn, and so many more – in a crate in the closet, but nothing to play them on. So I sprung for a new turntable and speakers, and started buying vinyl again. I’m not alone. As you can see below, after almost disappearing in the 1990s, album sales are on the rise again. What to make of this resurgence of old, analog technology in our increasingly digital world? I think it is more than sound quality and appreciating the cover art and liner notes. Listening to an album also reveals its “deep cuts” – tracks you might not discover on a hit-driven streaming service.

One album for which I’ve recently gained a new appreciation is Brothers and Sisters, which was released in 1973 by The Allman Brothers Band. As a teen, I didn’t have enough life experience to appreciate the lyrics, keyboard solos, and blues riffs the band laid down, but today, at 58, I find that the music speaks to me. While this record includes one of the band’s biggest hits, “Ramblin’ Man,” I’m particularly drawn to three lesser-known tunes: “Pony Boy,” “Jelly Jelly,” and “Southbound.” These songs have existed for fifty years, but I suspect few people know them well – like I didn’t until I looked past the hits and dug a little deeper.

| Poplar Forest Funds Annual Report, September 2023 | |

2

POPLAR FOREST FUNDS

When picking stocks for Poplar Forest’s portfolio, my colleagues and I do much the same thing. While we pursue Value stocks of all sizes, of course, we often find particularly compelling opportunities in the investment world’s equivalent of the music industry’s deep cuts: out-of-favor, unappreciated, or undiscovered medium-sized companies, or “Midcaps.” My thinking about Midcaps is that because fewer people are paying attention to them, there may be more opportunity to uncover values that others don’t see. In addition, Midcap companies may have scale advantages over their smaller competitors and more growth potential than their largest competitors.

In recent years, investors overall have been enthralled by the performance of the biggest companies while they’ve increasingly ignored just about everything else. It hasn’t always been this way; historically, the stocks that you may not have heard about are often the ones that may get your portfolio grooving.

“Band is jumping and so am I

I’m just groovin’, can’t stop moving…

When morning comes and it’s time to go

Pony Boy, carry me home.”

From “Pony Boy”

I have long believed that having the flexibility to invest in Midcaps was critical to long-term investment success. In my Capital Group days, when I was managing portfolios with $20 billion of assets, I realized that I had lost that flexibility and that realization was part of the reason I started Poplar Forest in 2007. Early in my career, before the market was sliced and diced the way it is now, the importance of Midcaps was harder to prove, but now, more than 25 years later, we have the data.

Well-known index provider FTSE Russell splits the U.S market into two groups: the largest thousand companies (the “Large Cap” Index) and the next 2,000 (the “Small Cap” Index). The largest thousand are further segregated into the Top 200 (generally at least $40 billion market cap) and Midcaps (the next 800). As you can see below, from June 30, 1996, when I first became a diversified portfolio manager, through Sept. 30, 2023, Midcap Value stocks have beaten their larger peers by almost 2% a year and Small Cap Value stocks by more than 1% per year. While 1-2% a year may not sound like much, over 25 years, it makes a huge difference. History suggests that Midcaps make more money in the long-term, and Poplar Forest was specifically designed to take advantage of this potential for outperformance.

| Annualized | Value of $10,000 | Excess Return | |

Total Return | invested on | Relative to | |

| 6/30/96-9/30/23 | 6/30/96(1) | Top 200 | |

| Russell Top 200 Value Index | 7.85% | $ 78,406 | |

| Russell Midcap Value Index | 9.73% | $125,564 | +60% |

Russell 1000 Value Index | 8.38% | $ 89,612 | +14% |

| Russell 2000 Value Index | 8.55% | $ 93,522 | +19% |

(1) Through September 30, 2023. | |||

| Source: FTSE Russell and Poplar Forest calculations. Past performance does not guarantee future results. | |||

Poplar Forest owns stock in plenty of big companies, like Merck, Intel, Chevron and Wells Fargo, but the size of our portfolios doesn’t limit us to investing in only the

| Poplar Forest Funds Annual Report, September 2023 | |

3

POPLAR FOREST FUNDS

biggest. When you compare the market cap distribution of our portfolio to the stocks owned by other Value managers, you can see that we offer a differentiated Value strategy with above average exposure to what has historically been a sweet spot in markets. In market environments in which investors favor the biggest companies, our exposure to Midcap companies may be a hindrance, but over time, we believe that our investment flexibility will prove to be advantageous. Much like Allman Brothers guitarist Dickey Betts sings in the chorus to “Pony Boy,” the final song on the Brothers and Sisters album, I believe that Midcaps will help carry us home.

| % of Fund Assets by Market Capitalization | |||

| Poplar Forest | Morningstar Large | Large Value | |

| Company size | Partners Fund | Value Index | Fund Average |

| Giant (>$222.8B) | 8.1% | 30.8% | 40.4% |

| Large ($43.6B – $222.8B) | 33.4% | 45.8% | 24.5% |

| Mid ($7.9B – $43.6B) | 41.1% | 22.9% | 28.2% |

| Small ($2.1B – $7.9B) | 11.2% | 0.6% | 4.0% |

| Source: Morningstar Data as of 08/31/23 | |||

Since the start of 2023, we’ve made five new investments – almost all Midcaps: Tyson Foods ($20 billion market cap) in the first quarter, Oshkosh ($6 billion) in the second, and three new investments in the most recent quarter. Of the three newest stocks, two are economically-sensitive companies ($5-7 billion each) that we believe are under-earning and whose P/E multiples are depressed because of investors’ fear of recession. Both businesses consistently generate free cash flow and offer, in our assessment, above average earnings growth potential over the next few years, yet they are both valued at just 9x Wall Street’s best guess for 2024 earnings. The third new investment is a nearly $40 billion market cap, historically recession-resistant business with an above average dividend yield, a strong balance sheet and a valuation of slightly more than 13x expected 2024 earnings. In short, we have invested in: two cyclical stocks that we believe offer attractive upside potential with limited downside in a recession given their valuations; and one defensive business with limited earnings risk in a recession and a well-covered dividend that produces a substantial yield premium relative to the company’s peers.

Having the market cap flexibility to pursue bargains in any of the thousand largest companies in the U.S. has allowed us to build a portfolio that we believe offers very compelling value on both an absolute basis and relative to other Large Value funds. As you can see below, based on Morningstar’s assessment, our portfolio companies offer comparable long-term earnings growth at a close to 25% P/E discount as compared to other Large Value portfolios.

| Portfolio Comparison | |||

| Poplar Forest | Morningstar Large | Large Value | |

| Partners Fund | Value Index | Fund Average | |

| Long-term Earnings Growth | 10.0% | 10.7% | 9.4% |

| Price/Earnings | 11.4x | 14.9x | 14.2x |

| Price/Book | 1.6x | 2.4x | 2.2x |

| Price/Sales | 0.7x | 1.5x | 1.7x |

| Price/Cash Flow | 6.2x | 9.7x | 9.6x |

| Source: Morningstar Data as of 08/31/23 | |||

Poplar Forest Funds Annual Report, September 2023 |

4

POPLAR FOREST FUNDS

“You’re my blue sky, you’re my sunny day

Lord you know it makes me high

When you turn your love my way.”

From “Blue Sky” on the Allman’s 1972 Album Eat a Peach

For the last 18 months, investors have understandably been living with fears of recession as the Fed set about normalizing monetary policy after COVID. Short-term interest rates have increased from near zero to more than 5.25% and the yield on 10-year Treasury bonds almost tripled from around 1.5% to more than 4.6%. History suggests that such a dramatic tightening of monetary policy will cause a recession, but so far, investors mostly see blue skies. Monthly payments for new home and auto loans have soared due to higher prices and higher interest rates and historically, that leads to a weakening economy. Yet employment is still strong and consumer spending has remained resilient while inflation has moderated.

The emerging opinion is that inflation has been defeated without a recession, and as a result, the Fed can soon stop raising interest rates. Economic resilience has allowed companies to maintain margins and corporate earnings estimates have been trending higher in recent months. Stocks, as measured by the S&P 500 Index (“S&P 500”), have been quite strong this year, though that strength has been concentrated in the biggest growth companies.

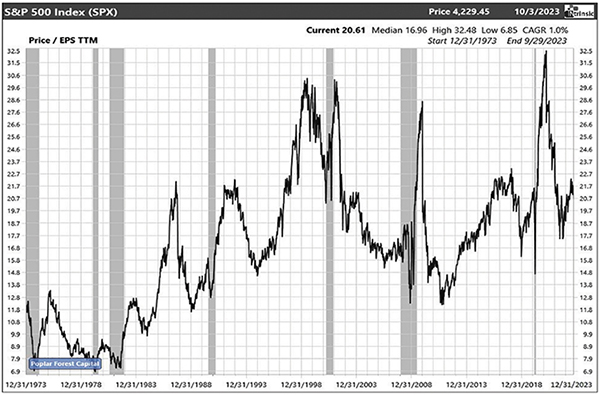

P/E ratios can be a helpful tool for judging investors’ attitudes. When the outlook is optimistic, buyers are willing to assign a high multiple for stocks, while pessimism is reflected in low multiples. As you can see in the chart below, outside of recessionary periods when earnings are depressed, the price/earnings ratio of the S&P 500 has rarely exceeded 21-22x trailing earnings – the S&P 500 is currently near this lofty level.

Source: Intrinsic Research. TTM = trailing 12 months

Poplar Forest Funds Annual Report, September 2023 |

5

POPLAR FOREST FUNDS

In the half-century since the release of Brothers and Sisters, the only non-recessionary period in which investors were more optimistic, as reflected in P/E ratios, was during the late-1990s Tech Bubble – and we know how badly that ended. High valuations, in and of themselves, don’t mean that stocks can’t keep moving higher if earnings grow, but they may help gauge downside potential. With current valuations – and implied investor expectations – about as high as they get, the S&P 500 would appear to offer a mediocre tradeoff between risk and reward. In contrast, the low valuation of Poplar Forest Partners portfolio suggests a much more attractive risk/reward ratio.

The companies in our portfolio are currently being valued at roughly 10x Wall Street’s best guess for earnings in 2024 – a valuation that offers very attractive upside should a recession be avoided. Our risk-adjusted fair value analysis for the companies we own suggests they deserve to be valued at 14.5-15.0x 2024 earnings – a 45-50% premium to their current valuation. With the S&P 500 currently valued at roughly 19x expected 2024 earnings, our companies look like particularly good value.

“Oh, it’s stormin’, stormin’ rain and I’m as lonesome as a man can be…

it’s a down-right rotten, low down dirty shame, the way that you treated me.”

From “Jelly Jelly”

At a time when other investors are focused on blue economic skies, we think it is prudent to plan more conservatively. To help us avoid the “Jelly Jelly” blues at Poplar Forest, our financial forecasts continue to assume a recession will hit sometime in the next 12 months. I sincerely hope that assumption is too conservative, but given restrictive monetary policy and exuberant investor attitudes, it seems especially prudent right now to emphasize risk management in our portfolio management decisions. Monetary policy is purported to work with long and variable lags, and history suggests that it could start storming soon.

In a recession, we believe that our companies’ earnings may get hit by about 20%. If that is correct, then our portfolio would be valued at just 12.5x – still a very low multiple in an absolute sense, and even more so considering those would be depressed earnings. The upside potential weighted against what appears to be limited recessionary downside is one of the best risk/reward ratios I can remember.

“I got that old lonesome feelin’ that’s sometimes called the blues

Well I been workin’ every night, travelin’ every day…

You can tell your other man, sweet daddy’s on his way…

Well I’m going to make it on up to you

For all the things you should have had before.”

from Southbound

When I first started Poplar Forest, album sales were just starting to emerge from a 16-year drought in sales. I realize that collecting, storing, and listening to records isn’t as easy as streaming digital music, but I find it to be more than worth the trouble. As I’ve said, the sound is richer and there is something viscerally satisfying about pulling a treasured album out of its sleeve, placing it on the platter and dropping the needle. In a way, it’s almost like I can “touch” the music when playing an LP – something that doesn’t happen when I stream a digital recording.

In the same way that an album can be a physical manifestation of music, “free cash flow” – the amount of money left over after a company has paid its bills and invested

Poplar Forest Funds Annual Report, September 2023 |

6

POPLAR FOREST FUNDS

for future growth – may be a similar expression of business success. When the free cash flow that our companies produce is divided by the value of those companies, the result is what we call the “free cash yield.” Based on results over the last 12 months, our portfolio is valued at a 7% free cash yield (a substantial premium to the S&P 500’s 4.0% free cash yield) and we see prospects for double-digit annual growth in those cash flows in the next three to five years. While the short-term may be volatile as bulls and bears debate the likelihood of recession, our portfolio’s combination of free cash yield and growth point to substantial long-term appreciation potential.

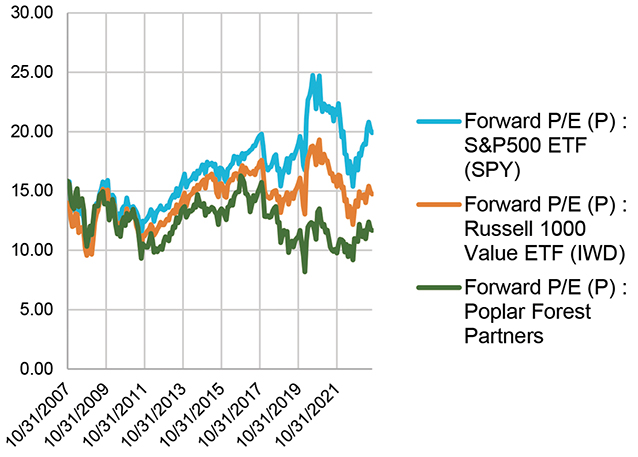

As you can see below, in late 2007 when we started Poplar Forest, and after a multi-year run starting in 2000 that saw the Russell 1000 Value Index beat the S&P by a cumulative 50%, there was not much value left in Value stocks, at least as compared to the S&P 500. Today, the tables have turned and our opportunity set is about as robust as I can remember it. Interest rates are roughly back to where they were in 2007 while the P/E ratio for the S&P 500 is roughly 25% higher; yet, we’ve been able to assemble a portfolio that has a 25% lower valuation as compared to the companies we owned back then.

Source: CapitalIQ

I started Poplar Forest with the goal of providing like-minded clients with market beating long-term investment results through a high conviction, disciplined, absolute value investment strategy. Then, as now, I was focused on finding out-of-favor and underappreciated stocks with idiosyncratic return characteristics and I believe we’ve done a good job of that. However, the decade-long compression in Value stocks’ relative valuations has certainly been an unexpected headwind to our results. That said, those headwinds have created an environment that in our view positions Value investing for a renaissance similar to that experienced by album sales over the last decade.

Poplar Forest Funds Annual Report, September 2023 |

7

POPLAR FOREST FUNDS

We remain committed to an investment process that seeks to uncover what we believe are bargains with above average long-term potential and below average risk. In a market environment in which investors are enamored with the leading Growth stocks, it might be easy for us to get those old lonesome blues were it not for the support of a fantastic group of client partners on whose behalf we work each day. I don’t know when the current Growth stock infatuation will end, but when it does, I believe that our portfolio has the potential to produce chart-topping results – to quote Gregg Allman in “Southbound”: “Sweet Daddy’s on his way!”

Sincerely,

J. Dale Harvey

September 30, 2023

Poplar Forest Funds Annual Report, September 2023 |

8

POPLAR FOREST FUNDS

Partners Fund Portfolio Review

The Partners Fund Institutional Class shares produced a return of 7.32% while Class A shares (no load) produced an 7.05% return for the twelve months ending September 30, 2023. This compared to a return of 21.62% for the S&P 500 Index (“S&P 500”) and 14.44% for the Russell 1000 Value Index.

Relative to the S&P 500, the portfolio’s top contributing sectors to performance over this fiscal period were Industrials, Real Estate (from an underweight in a poorly performing sector) and Energy. The bottom contributing sectors were Financials, Consumer Discretionary and Communication Services.

At the security level, the top contributors were Intel Corporation, Cencora (formerly AmerisourceBergen), FedEx, Chevron and AIG. The Fund’s top detractors from overall performance were Advance Auto, CVS Health Corporation, Dollar Tree, Tyson Foods and Fidelity National Information Services.

Portfolio Changes and Positioning

Poplar Forest Capital’s process is designed to find attractive investment opportunities in all parts of the economic cycle. By focusing on normalized earnings power, we try to avoid capitalizing above-trend and below-trend results. Additionally, we incorporate a recession assumption and evaluate the balance sheet of each of our investments to understand whether the financial strength exists to manage through more difficult than forecast periods. Within this framework, our goal is to find companies whose prospects are underappreciated by investors. Over the last year, we have become more cautious on the U.S. economy given the Fed’s battle to tame inflation and unwinding of quantitative easing. This has led us to exit positions with lower credit ratings and greater cyclicality. Our new investments have more defensive business models – greater recurring revenues – and idiosyncratic opportunities to improve profitability. The imbedded credit quality of our portfolio is arguably higher than at any time since we opened our doors in late 2007. At the same time, our concentrated value portfolio trades at one of the widest discounts to the S&P 500 since inception. We expect this discount to buffer the portfolio if a recession ensues and provide additional return potential as turnaround metrics are achieved.

Cornerstone Fund Portfolio Review

The Cornerstone Fund produced a 7.46% return. This compares to a 13.01% return for a 60/40 blend of the S&P 500® Index and the Bloomberg U.S. Aggregate Bond Index for the twelve months ending September 30, 2023.

At the security level, the Fund benefitted from top contributing equity investments Las Vegas Sands, FedEx, Cencora (formerly AmerisourceBergen), Intel and Apollo Global. Top detracting equity investments were Advance Auto, CVS Health, Dollar Tree, Tyson Foods and Fidelity National Information Services.

While the overlap between the equities owned in the Cornerstone and Partners Funds is high, the Cornerstone Fund remains far more defensive with roughly 38% in cash and equivalents and fixed income investments. Our equity exposure remains at ~61% which is where it has been for the last year but down from where it was historically. As interest rates have climbed, we have shifted our investments within fixed income to a higher ratio of treasuries to corporates. At September 30, 2023 our fixed investments in AAA bonds were 57% versus 50.6% a year ago.

Poplar Forest Funds Annual Report, September 2023 |

9

POPLAR FOREST FUNDS

We remain focused on trying to manage downside risk while also striving to protect our investors’ long-term purchasing power. Our equities currently account for approximately 61% of the Fund, in line with where the portfolio was at September 30, 2022. The draw-down this year was less than that of the Partners Fund.

As we look ahead, we believe our portfolio is well positioned to generate solid inflation-adjusted returns. The Fund remains focused on high quality companies that are trading at what we believe are discounted valuations, while our bond selections continue to emphasize our goal of capital preservation.

Disclosures

Must be preceded or accompanied by a prospectus.

Mutual fund investing involves risk. Principal loss is possible. The Funds may invest in debt securities which typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. The Funds may invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater in emerging markets. Investing in small and medium sized companies may involve greater risk than investing in larger, more established companies because small and medium capitalization companies can be subject to greater share price volatility. The Funds may invest in options, which may be subject to greater fluctuations in value than an investment in the underlying securities. When the Funds invest in other funds and ETFs an investor will indirectly bear the principal risks and its share of the fees and expenses of the underlying funds. Investments in asset-backed and mortgage-backed securities involve additional risks such as credit risk, prepayment risk, possible illiquidity and default, and increased susceptibility to adverse economic developments. Diversification does not assure a profit, nor does it protect against a loss in a declining market.

Value stocks typically are less volatile than growth stocks; however, value stocks have a lower expected growth rate in earnings and sales.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. Fund holdings and sector allocations are subject to change and should not be considered recommendations to buy or sell any security.

Poplar Forest Funds are distributed by Quasar Distributors, LLC.

Partners Fund Top Ten Holdings and Percentage Weights as of 9/30/23:

| Equitable Holdings | 4.80% | |

| Intel Corp. | 4.78% | |

| Cencora Inc. | 4.65% | |

| IBM | 4.64% | |

| Chevron Corp. | 4.42% | |

| United Therapeutics | 4.40% | |

| Allstate Corp. | 4.30% | |

| CVS Health Corp. | 4.17% | |

| National Fuel Gas | 4.16% | |

| Dow Inc. | 4.13% |

Poplar Forest Funds Annual Report, September 2023 |

10

POPLAR FOREST FUNDS

Cornerstone Fund Top Ten Equity Holdings and Percentage Weights as of 9/30/23:

| United Therapeutics | 2.94% | |

| IBM | 2.88% | |

| Intel Corp. | 2.77% | |

| Equitable Holdings | 2.74% | |

| Cencora Inc. | 2.69% | |

| Allstate Corp. | 2.61% | |

| Philip Morris | 2.59% | |

| CVS Health Corp. | 2.59% | |

| National Fuel Gas | 2.57% | |

| Dow Inc. | 2.53% |

S&P 500 Index: Is a market value weighted index consisting of 500 stocks chosen for market size, liquidity and industry group representation. The Index is unmanaged.

Russell 1000® Index: An index of approximately 1,000 of the largest companies in the U.S. equity market. The Index is a subset of the Russell 3000 Index, representing the top companies by market capitalization.

Russell 1000® Growth Index: Measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

Russell 1000® Value index: measures the performance of the Russell 1000’s value segment, which is defined to include firms whose share prices have lower price/book ratios and lower expected long-term mean earnings growth rates.

Russell 2000 Index: The Russell 2000 Index refers to a stock market index that measures the performance of the 2,000 smaller companies included in the Russell 3000 Index. The Russell 2000 is managed by FTSE Russell and is widely regarded as a bellwether of the U.S. economy because of its focus on smaller companies that focus on the U.S. market.

Russell Top 200 Value Index: Measures the performance of the 200 largest companies (63% of total market capitalization) in the Russell 1000 Index, with a weighted average market capitalization of $186 billion. The Russell Top 200 Index is tracked by an exchange-traded fund, iShares Russell Top 200 Index (NYSE Arca: IWL).

Russell Midcap Value Index: Measures the performance of the midcap value segment of the U.S. equity universe. It includes those Russell Midcap Index companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years).

The Bloomberg U.S. Aggregate Bond Index: is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

Blended index: (also known as a blended benchmark) is a combination of two or more indices in varying percentages. To take a simple example, if an investor’s assets are allocated to 60% stocks and 40% bonds, the portfolio’s performance might be best measured against a blended benchmark consisting of 60% in a stock index (e.g. S&P 500® index) and 40% in a bond index (e.g. Bloomberg U.S. Aggregate Bond Index).

Poplar Forest Funds Annual Report, September 2023 |

11

POPLAR FOREST FUNDS

The Consumer Price Index (CPI): is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. The annual percentage change in a CPI is used as a measure of inflation.

Morningstar Large Value Index: Average of all Value funds in Morningstar’s mutual fund database. The index is designed to provide consistent representation of the large-cap value segment of the U.S. equity market, with no overlapping constituents across styles.

Morningstar Large Value Fund Average: Large-value funds invest in stocks of big U.S. companies that are less expensive or growing more slowly than other large-cap stocks. Stocks in the top 70% of the capitalization of the U.S. equity market are defined as large-cap. Value is defined based on low valuations (low price ratios and high dividend yields) and slow growth (low growth rates for earnings, sales, book value, and cash flow).

It is not possible to invest directly in an index.

Index performance is not indicative of a Fund’s performance. Past performance does not guarantee future results.

Earnings growth is not a measure of a Fund’s future performance.

Absolute Value: Refers to valuing businesses using discounted cash flow analysis to determine a company’s financial worth.

Compound Annual Growth Rate (CAGR): The year-over-year growth rate of an investment over a specified period of time. The compound annual growth rate is calculated by taking the nth root of the total percentage growth rate, where n is the number of years in the period being considered.

Earnings Growth: The annual rate of growth of earnings typically measured as Earnings Per Share Growth.

Earnings Per Share (EPS): The net income of a company divided by the total number of shares it has outstanding.

Free Cash Flow: Is equal to the after-tax net income of a company plus depreciation and amortization less capital expenditures.

Free Cash Yield: A financial solvency ratio that compares the free cash flow per share a company is expected to earn against its market value per share.

Inflation: Is a quantitative measure of the rate at which the average price level of a basket of selected goods and services in an economy increases over a period of time. Often expressed as a percentage, inflation indicates a decrease in the purchasing power of a nation’s currency.

Price/Book Ratio (P/B): The price/book ratio of a fund is the weighted average of the price/book ratios of all the stocks in a fund’s portfolio.

Price/Cash Flow Ratio (P/CF): A stock valuation measure calculated by dividing a firm’s cash flow per share into the current stock price. Financial analysts often prefer to value stocks using cash flow rather than earnings because the latter is more easily manipulated.

Price/Earnings (P/E) Ratio: Is a common tool for comparing the prices of different common stocks and is calculated by dividing the earnings per share into the current market price of a stock.

Poplar Forest Funds Annual Report, September 2023 |

12

POPLAR FOREST FUNDS

Price/Sales Ratio: This ratio represents the amount an investor is willing to pay for a dollar generated from a particular company’s operations.

Risk-adjusted Returns: The return on an investment such as a stock or corporate bond when compared to cash or equivalents.

Trailing 12 Months (TTM): A term used to describe the past 12 consecutive months of a company’s performance data, that’s used for reporting financial figures.

Poplar Forest Funds Annual Report, September 2023 |

13

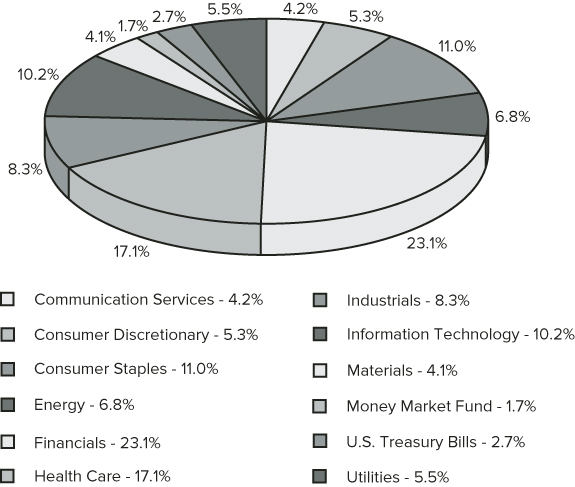

POPLAR FOREST PARTNERS FUND

SECTOR ALLOCATION OF PORTFOLIO ASSETS at September 30, 2023 (Unaudited)

Percentages represent market value as a percentage of total investments.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

Poplar Forest Funds Annual Report, September 2023 |

14

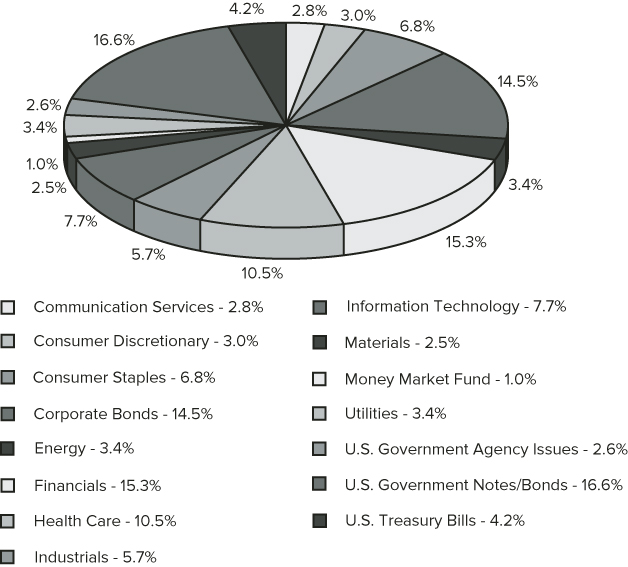

POPLAR FOREST CORNERSTONE FUND

SECTOR ALLOCATION OF PORTFOLIO ASSETS at September 30, 2023 (Unaudited)

Percentages represent market value as a percentage of total investments.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

Poplar Forest Funds Annual Report, September 2023 |

15

POPLAR FOREST FUNDS

EXPENSE EXAMPLE at September 30, 2023 (Unaudited)

As a shareholder of a mutual fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees, and exchange fees, and (2) ongoing costs, including management fees, distribution and/or service fees, and other fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (4/1/23 – 9/30/23).

Actual Expenses

For each class of each Fund, two lines are presented in the tables below, with the first line providing information about actual account values and actual expenses. You will be assessed fees for outgoing wire transfers, returned checks, and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Funds’ transfer agent. The Example below includes, but is not limited to, management fees, 12b-1 fees, fund accounting, custody and transfer agent fees. You may use this information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period’’ to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class of each Fund, the second line provides information about hypothetical account values and hypothetical expenses based on the respective Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the tables for each class of each Fund is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Poplar Forest Funds Annual Report, September 2023 |

16

POPLAR FOREST FUNDS

EXPENSE EXAMPLE at September 30, 2023 (Unaudited), Continued

| Beginning | Ending | Expenses Paid | Annualized | |

| Account Value | Account Value | During Period | Expense | |

4/1/23 | 9/30/23 | 4/1/23 – 9/30/23 | Ratio* | |

| Poplar Forest Partners Fund | ||||

| Class A Shares | ||||

| Actual | $1,000.00 | $963.80 | $5.91 | 1.20% |

| Hypothetical (5% return | ||||

| before expenses) | $1,000.00 | $1,019.05 | $6.07 | 1.20% |

| Institutional Class Shares | ||||

| Actual | $1,000.00 | $965.30 | $4.68 | 0.95% |

| Hypothetical (5% return | ||||

| before expenses) | $1,000.00 | $1,020.31 | $4.81 | 0.95% |

| Beginning | Ending | Expenses Paid | Annualized | |

| Account Value | Account Value | During Period | Expense | |

4/1/23 | 9/30/23 | 4/1/23 – 9/30/23 | Ratio* | |

| Poplar Forest Cornerstone Fund | ||||

| Investor Class Shares | ||||

| Actual | $1,000.00 | $977.80 | $4.46 | 0.90% |

| Hypothetical (5% return | ||||

| before expenses) | $1,000.00 | $1,020.56 | $4.56 | 0.90% |

| * | Expenses are equal to the annualized expense ratio of each class, multiplied by the average account value over the period, multiplied by 183 (days in most recent fiscal half-year) / 365 days to reflect the one-half year expense. |

Poplar Forest Funds Annual Report, September 2023 |

17

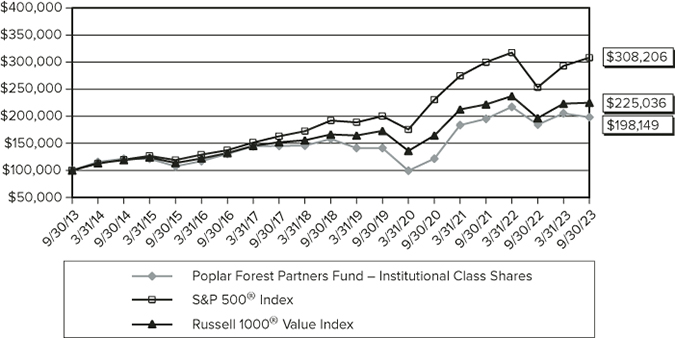

POPLAR FOREST PARTNERS FUND

Comparison of the change in value of a $100,000 investment in the

Poplar Forest Partners Fund – Institutional Class Shares vs

the S&P 500® Index and the Russell 1000® Value Index

Average Annual Total Return: | 1 Year | 5 Year | 10 Year |

| Poplar Forest Partners Fund – | |||

| Institutional Class Shares | 7.32% | 4.64% | 7.08% |

| Poplar Forest Partners Fund – | |||

| Class A Shares (with sales load) | 1.71% | 3.31% | 6.26% |

| Poplar Forest Partners Fund – | |||

| Class A Shares (without sales load) | 7.05% | 4.37% | 6.81% |

S&P 500® Index | 21.62% | 9.92% | 11.91% |

Russell 1000® Value Index | 14.44% | 6.23% | 8.45% |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-877-522-8860.

Returns reflect the reinvestment of dividends and capital gain distributions. Fee waivers are in effect. In the absence of fee waivers, returns would be reduced. Class A shares may be subject to a 5.00% front-end sales load. The performance data and graph do not reflect the deduction of taxes that a shareholder may pay on dividends, capital gain distributions, or redemption of Fund shares. This chart does not imply any future performance. Indices do not incur expenses and are not available for investment.

The S&P 500® Index is a market-value weighted index consisting of 500 stocks chosen for market size, liquidity, and industry group representation.

The Russell 1000® Value Index is an index of approximately 1,000 of the largest companies in the U.S. equity markets, and is a subset of the Russell 3000® Index.

Poplar Forest Funds Annual Report, September 2023 |

18

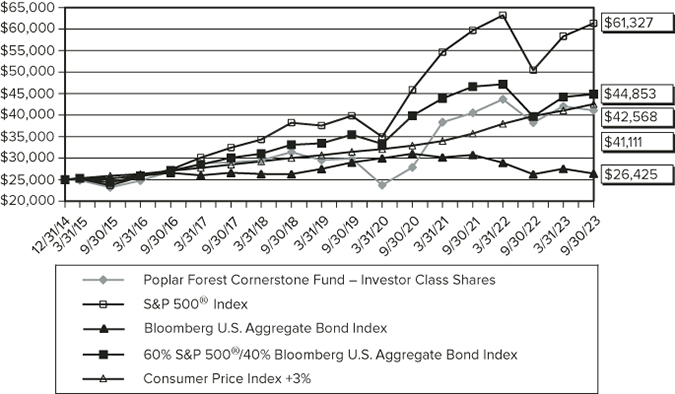

POPLAR FOREST CORNERSTONE FUND

Comparison of the change in value of a $25,000 investment in the

Poplar Forest Cornerstone Fund – Investor Class Shares vs.

the S&P 500® Index, the Bloomberg U.S. Aggregate Bond Index,

the Blended Index and the Consumer Price Index +3%

| Since | |||

Average Annual Total Return: | 1 Year | 5 Year | Inception1 |

| Poplar Forest Cornerstone Fund – | |||

| Investor Class Shares | 7.46% | 5.55% | 5.85% |

S&P 500® Index | 21.62% | 9.92% | 10.80% |

| Bloomberg U.S. Aggregate Bond Index | 0.64% | 0.10% | 0.64% |

60% S&P 500®/ 40% U.S. Aggregate Bond Index | 13.01% | 6.27% | 6.91% |

| Consumer Price Index +3% | 7.00% | 7.20% | 6.25% |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-877-522-8860.

Returns reflect the reinvestment of dividends and capital gain distributions. Fee waivers are in effect. In the absence of fee waivers, returns would be reduced. The performance data and graph do not reflect the deduction of taxes that a shareholder may pay on dividends, capital gain distributions, or redemption of Fund shares. This chart does not imply any future performance. Indices do not incur expenses and are not available for investment.

The S&P 500® Index is a market-value weighted index consisting of 500 stocks chosen for market size, liquidity, and industry group representation.

The Bloomberg U.S. Aggregate Bond Index is a broad based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable market, including Treasuries, government related and corporate securities.

Poplar Forest Funds Annual Report, September 2023 |

19

POPLAR FOREST CORNERSTONE FUND

The blended index is a 60% S&P 500® Index and 40% Bloomberg U.S. Aggregate Bond Index blend.

Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. The annual percentage change in the CPI is used as a measure of inflation. The CPI +3% is a measure defined as an objective in the Fund’s prospectus.

1 | The Fund commenced operations on December 31, 2014. |

Poplar Forest Funds Annual Report, September 2023 |

20

POPLAR FOREST PARTNERS FUND

SCHEDULE OF INVESTMENTS at September 30, 2023

| Shares | COMMON STOCKS – 95.6% | Value | |||||

| Air Freight & Logistics – 3.6% | |||||||

| 39,500 | FedEx Corp. | $ | 10,464,340 | ||||

| Banks – 5.8% | |||||||

| 135,000 | Citigroup, Inc. | 5,552,550 | |||||

| 274,000 | Wells Fargo & Co. | 11,195,640 | |||||

| 16,748,190 | |||||||

| Biotechnology – 4.4% | |||||||

| 56,500 | United Therapeutics Corp. (a) | 12,761,655 | |||||

| Capital Markets – 0.9% | |||||||

| 45,000 | Stifel Financial Corp. | 2,764,800 | |||||

| Chemicals – 4.1% | |||||||

| 232,500 | Dow, Inc. | 11,987,700 | |||||

| Consumer Finance – 2.2% | |||||||

| 241,000 | Ally Financial, Inc. | 6,429,880 | |||||

| Consumer Staples Distribution – 3.0% | |||||||

| 82,500 | Dollar Tree, Inc. (a) | 8,782,125 | |||||

| Diversified Telecommunication Services – 2.6% | |||||||

| 503,000 | AT&T, Inc. | 7,555,060 | |||||

| Electrical Equipment – 2.1% | |||||||

| 158,500 | Sensata Technologies Holding plc | 5,994,470 | |||||

| Entertainment – 1.6% | |||||||

| 432,000 | Warner Bros. Discovery, Inc. (a) | 4,691,520 | |||||

| Financial Services – 7.9% | |||||||

| 490,000 | Equitable Holdings, Inc. | 13,911,100 | |||||

| 164,000 | Fidelity National Information Services, Inc. | 9,064,280 | |||||

| 22,975,380 | |||||||

| Food Products – 4.0% | |||||||

| 227,000 | Tyson Foods, Inc. – Class A | 11,461,230 | |||||

| Gas Utilities – 4.2% | |||||||

| 232,500 | National Fuel Gas Co. | 12,069,075 | |||||

| Health Care Providers & Services – 8.8% | |||||||

| 75,000 | Cencora, Inc. | 13,497,750 | |||||

| 173,000 | CVS Health Corp. | 12,078,860 | |||||

| 25,576,610 | |||||||

| Hotels, Restaurants & Leisure – 2.7% | |||||||

| 168,000 | Las Vegas Sands Corp. | 7,701,120 | |||||

| Insurance – 6.2% | |||||||

| 112,000 | Allstate Corp. | 12,477,920 | |||||

| 90,000 | American International Group, Inc. | 5,454,000 | |||||

| 17,931,920 | |||||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

21

POPLAR FOREST PARTNERS FUND

SCHEDULE OF INVESTMENTS at September 30, 2023, Continued

| Shares | Value | ||||||

| IT Services – 5.4% | |||||||

| 102,000 | DXC Technology Co. (a) | $ | 2,124,660 | ||||

| 96,000 | International Business Machines Corp. | 13,468,800 | |||||

| 15,593,460 | |||||||

| Machinery – 2.6% | |||||||

| 79,000 | Oshkosh Corp. | 7,538,970 | |||||

| Multi-Utilities – 1.3% | |||||||

| 85,500 | Dominion Energy, Inc. | 3,819,285 | |||||

| Oil, Gas & Consumable Fuels – 6.8% | |||||||

| 76,000 | Chevron Corp. | 12,815,120 | |||||

| 152,500 | Murphy Oil Corp. | 6,915,875 | |||||

| 19,730,995 | |||||||

| Pharmaceuticals – 3.9% | |||||||

| 110,000 | Merck & Co., Inc. | 11,324,500 | |||||

| Semiconductors & Semiconductor Equipment – 4.8% | |||||||

| 390,000 | Intel Corp. | 13,864,500 | |||||

| Textiles, Apparel & Luxury Goods – 2.7% | |||||||

| 270,000 | Tapestry, Inc. | 7,762,500 | |||||

| Tobacco – 4.0% | |||||||

| 126,000 | Philip Morris International, Inc. | 11,665,080 | |||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $228,543,236) | 277,194,365 | ||||||

| SHORT-TERM INVESTMENTS – 4.4% | |||||||

| Money Market Fund – 1.7% | |||||||

| 5,000,193 | Morgan Stanley Institutional Liquidity Funds – | ||||||

| Treasury Portfolio, Institutional Class, 5.203% (b) | 5,000,193 | ||||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

22

POPLAR FOREST PARTNERS FUND

SCHEDULE OF INVESTMENTS at September 30, 2023, Continued

| Principal | |||||||

| Amount | Value | ||||||

| U.S. Treasury Bills – 2.7% | |||||||

| $ | 4,900,000 | 5.341%, 10/26/2023 (c) | $ | 4,882,796 | |||

| 3,000,000 | 5.387%, 12/7/2023 (c) | 2,970,808 | |||||

| 7,853,604 | |||||||

| TOTAL SHORT-TERM INVESTMENTS | |||||||

| (Cost $12,852,585) | 12,853,797 | ||||||

| Total Investments | |||||||

| (Cost $241,395,821) – 100.0% | 290,048,162 | ||||||

| Liabilities in Excess of Other Assets – (0.0)% | (58,061 | ) | |||||

| TOTAL NET ASSETS – 100.00% | $ | 289,990,101 | |||||

| (a) | Non-income producing security. |

| (b) | Rate shown represents the 7-day annualized yield as of September 30, 2023. |

| (c) | Rate shown is the discount rate at September 30, 2023. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

23

POPLAR FOREST CORNERSTONE FUND

SCHEDULE OF INVESTMENTS at September 30, 2023

| Shares | COMMON STOCKS – 61.0% | Value | |||||

| Air Freight & Logistics – 2.5% | |||||||

| 2,900 | FedEx Corp. | $ | 768,268 | ||||

| Banks – 4.1% | |||||||

| 16,300 | Citigroup, Inc. | 670,419 | |||||

| 14,200 | Wells Fargo & Co. | 580,212 | |||||

| 1,250,631 | |||||||

| Biotechnology – 2.9% | |||||||

| 4,000 | United Therapeutics Corp. (a) | 903,480 | |||||

| Chemicals – 2.5% | |||||||

| 15,100 | Dow, Inc. | 778,556 | |||||

| Consumer Finance – 1.3% | |||||||

| 15,200 | Ally Financial, Inc. | 405,536 | |||||

| Consumer Staples Distribution – 1.7% | |||||||

| 4,900 | Dollar Tree, Inc. (a) | 521,605 | |||||

| Diversified Telecommunication Services – 1.7% | |||||||

| 35,500 | AT&T, Inc. | 533,210 | |||||

| Electrical Equipment – 1.4% | |||||||

| 11,700 | Sensata Technologies Holding plc | 442,494 | |||||

| Entertainment – 1.1% | |||||||

| 29,600 | Warner Bros. Discovery, Inc. (a) | 321,456 | |||||

| Financial Services – 6.2% | |||||||

| 4,021 | Apollo Global Management, Inc. | 360,925 | |||||

| 29,700 | Equitable Holdings, Inc. | 843,183 | |||||

| 12,400 | Fidelity National Information Services, Inc. | 685,348 | |||||

| 1,889,456 | |||||||

| Food Products – 2.5% | |||||||

| 15,000 | Tyson Foods, Inc. – Class A | 757,350 | |||||

| Gas Utilities – 2.6% | |||||||

| 15,200 | National Fuel Gas Co. | 789,032 | |||||

| Health Care Providers & Services – 5.3% | |||||||

| 4,600 | Cencora, Inc. | 827,862 | |||||

| 11,400 | CVS Health Corp. | 795,948 | |||||

| 1,623,810 | |||||||

| Hotels, Restaurants & Leisure – 1.6% | |||||||

| 10,800 | Las Vegas Sands Corp. | 495,072 | |||||

| Insurance – 3.7% | |||||||

| 7,200 | Allstate Corp. | 802,152 | |||||

| 5,700 | American International Group, Inc. | 345,420 | |||||

| 1,147,572 | |||||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

24

POPLAR FOREST CORNERSTONE FUND

SCHEDULE OF INVESTMENTS at September 30, 2023, Continued

| Shares | Value | ||||||

| IT Services – 3.6% | |||||||

| 10,500 | DXC Technology Co. (a) | $ | 218,715 | ||||

| 6,300 | International Business Machines Corp. | 883,890 | |||||

| 1,102,605 | |||||||

| Machinery – 1.8% | |||||||

| 5,800 | Oshkosh Corp. | 553,494 | |||||

| Multi-Utilities – 0.8% | |||||||

| 5,600 | Dominion Energy, Inc. | 250,152 | |||||

| Oil, Gas & Consumable Fuels – 3.4% | |||||||

| 4,000 | Chevron Corp. | 674,480 | |||||

| 8,400 | Murphy Oil Corp. | 380,940 | |||||

| 1,055,420 | |||||||

| Pharmaceuticals – 2.2% | |||||||

| 6,600 | Merck & Co., Inc. | 679,470 | |||||

| Semiconductors & Semiconductor Equipment – 2.8% | |||||||

| 23,900 | Intel Corp. | 849,645 | |||||

| Software – 1.3% | |||||||

| 2,500 | VMware, Inc. (a) | 416,200 | |||||

| Textiles, Apparel & Luxury Goods – 1.4% | |||||||

| 14,400 | Tapestry, Inc. | 414,000 | |||||

| Tobacco – 2.6% | |||||||

| 8,600 | Philip Morris International, Inc. | 796,188 | |||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $15,902,362) | 18,744,702 | ||||||

| Principal | |||||||

| Amount | CORPORATE BONDS – 12.9% | ||||||

| Banks – 2.2% | |||||||

| Citizens Financial Group, Inc. | |||||||

| $ | 700,000 | 3.750%, 07/01/2024 | 674,322 | ||||

| Electric Utilities – 3.4% | |||||||

| Dominion Energy South Carolina, Inc. | |||||||

| 300,000 | 4.250%, 08/15/2028 | 280,359 | |||||

| DTE Electric Co. | |||||||

| 925,000 | 3.000%, 03/01/2032 | 766,372 | |||||

| 1,046,731 | |||||||

| Gas Utilities – 2.4% | |||||||

| National Fuel Gas Co. | |||||||

| 800,000 | 3.950%, 09/15/2027 | 733,932 | |||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

25

POPLAR FOREST CORNERSTONE FUND

SCHEDULE OF INVESTMENTS at September 30, 2023, Continued

| Principal | |||||||

| Amount | Value | ||||||

| Pharmaceuticals – 2.4% | |||||||

| Bristol-Myers Squibb Co. | |||||||

| $ | 725,000 | 6.125%, 05/01/2038 | $ | 725,586 | |||

| Specialty Retail – 2.5% | |||||||

| Dick’s Sporting Goods, Inc. | |||||||

| 1,000,000 | 3.150%, 01/15/2032 | 769,879 | |||||

| TOTAL CORPORATE BONDS | |||||||

| (Cost $4,151,255) | 3,950,450 | ||||||

| U.S. GOVERNMENT AGENCY ISSUES – 2.6% | |||||||

| Federal Home Loan Banks | |||||||

| 800,000 | 4.500%, 09/30/2027 (c) | 791,102 | |||||

| TOTAL U.S. GOVERNMENT AGENCY ISSUES | |||||||

| (Cost $800,000) | 791,102 | ||||||

| PREFERRED STOCKS – 1.5% | |||||||

| Consumer Finance – 1.5% | |||||||

| Ally Financial, Inc. | |||||||

| 700,000 | Series B, 4.700% (5 Year CMT Rate + | ||||||

| 3.868%), 8/15/2072 (b) | 481,896 | ||||||

| TOTAL PREFERRED STOCKS | |||||||

| (Cost $713,346) | 481,896 | ||||||

| U.S. GOVERNMENT NOTES/BONDS – 16.6% | |||||||

| U.S. Treasury Notes | |||||||

| 310,000 | 0.500%, 11/30/2023 | 307,548 | |||||

| 145,000 | 0.750%, 12/31/2023 | 143,348 | |||||

| 165,000 | 0.875%, 01/31/2024 | 162,547 | |||||

| 165,000 | 1.500%, 02/29/2024 | 162,348 | |||||

| 145,000 | 2.250%, 03/31/2024 | 142,726 | |||||

| 800,000 | 4.125%, 01/31/2025 | 787,844 | |||||

| 300,000 | 2.625%, 04/15/2025 | 288,586 | |||||

| 770,000 | 3.875%, 02/15/2043 | 669,659 | |||||

| 815,000 | 4.125%, 08/15/2053 | 739,103 | |||||

| U.S. Treasury Notes TIPS | |||||||

| 901,187 | 0.125%, 07/15/2024 | 880,415 | |||||

| 896,303 | 0.250%, 07/15/2029 | 799,292 | |||||

| TOTAL U.S. GOVERNMENT NOTES/BONDS | |||||||

| (Cost $5,378,154) | 5,083,416 | ||||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

26

POPLAR FOREST CORNERSTONE FUND

SCHEDULE OF INVESTMENTS at September 30, 2023, Continued

| Shares/ | |||||||

| Principal | |||||||

| Amount | SHORT-TERM INVESTMENTS – 5.2% | Value | |||||

| Money Market Fund – 1.0% | |||||||

| 310,698 | Morgan Stanley Institutional Liquidity Funds – | ||||||

| Treasury Portfolio, Institutional Class, 5.203% (d) | $ | 310,698 | |||||

| U.S. Treasury Bills – 4.2% | |||||||

| $ | 325,000 | 5.148%, 10/26/2023 (e) | 323,859 | ||||

| 500,000 | 5.310%, 11/24/2023 (e) | 496,104 | |||||

| 168,000 | 4.747%, 4/18/2024 (e) | 163,127 | |||||

| 165,000 | 5.189%, 6/13/2024 (e) | 158,899 | |||||

| 165,000 | 5.400%, 9/5/2024 (e) | 156,957 | |||||

| 1,298,946 | |||||||

| TOTAL SHORT-TERM INVESTMENTS | |||||||

| (Cost $1,610,689) | 1,609,644 | ||||||

| Total Investments | |||||||

| (Cost $28,555,806) – 99.8% | 30,661,210 | ||||||

| Other Assets in Excess of Liabilities – 0.2% | 59,474 | ||||||

| TOTAL NET ASSETS – 100.00% | $ | 30,720,684 | |||||

CMT – Constant Maturity Treasury

TIPS – Treasury Inflation Protected Securities

| (a) | Non-income producing security. |

| (b) | Variable or floating rate security based on a reference index and spread. The rate reported is the rate in effect as of September 30, 2023. |

| (c) | Step-up bond; pays one interest rate for a certain period and a higher rate thereafter. The interest rate shown is the rate in effect as of September 30, 2023, and steps up every six months with a terminal rate of 10% as of March 30, 2027. |

| (d) | Rate shown represents the 7-day annualized yield as of September 30, 2023. |

| (e) | Rate shown is the discount rate at September 30, 2023. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

27

POPLAR FOREST FUNDS

STATEMENTS OF ASSETS AND LIABILITIES at September 30, 2023

| Poplar Forest | Poplar Forest | |||||||

| Partners Fund | Cornerstone Fund | |||||||

| ASSETS | ||||||||

| Investments in securities, at value (identified cost | ||||||||

| $241,395,821 and $28,555,806, respectively) | $ | 290,048,162 | $ | 30,661,210 | ||||

| Receivables | ||||||||

| Fund shares issued | 51,726 | — | ||||||

| Dividends and interest | 522,212 | 117,978 | ||||||

| Prepaid expenses | 27,887 | 4,750 | ||||||

| Total assets | 290,649,987 | 30,783,938 | ||||||

| LIABILITIES | ||||||||

| Payables | ||||||||

| Fund shares redeemed | 347,246 | 8,000 | ||||||

| Due to Adviser | 176,565 | 6,130 | ||||||

| 12b-1 fees | 13,849 | — | ||||||

| Custody fees | 3,315 | 555 | ||||||

| Administration and fund accounting fees | 45,508 | 16,352 | ||||||

| Transfer agent fees and expenses | 34,372 | 4,003 | ||||||

| Audit fees | 22,500 | 21,000 | ||||||

| Chief Compliance Officer fee | 2,083 | 2,083 | ||||||

| Trustee fees and expenses | 550 | 551 | ||||||

| Accrued expenses | 13,898 | 4,580 | ||||||

| Total liabilities | 659,886 | 63,254 | ||||||

| NET ASSETS | $ | 289,990,101 | $ | 30,720,684 | ||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

28

POPLAR FOREST FUNDS

STATEMENTS OF ASSETS AND LIABILITIES at September 30, 2023, Continued

| Poplar Forest | Poplar Forest | |||||||

| Partners Fund | Cornerstone Fund | |||||||

| CALCULATION OF NET ASSET VALUE PER SHARE | ||||||||

| Class A Shares | ||||||||

| Net assets applicable to shares outstanding | $ | 22,717,011 | $ | — | ||||

| Shares issued and outstanding [unlimited number | ||||||||

| of shares (par value $0.01) authorized] | 487,790 | — | ||||||

| Net asset value and redemption price per share | $ | 46.57 | $ | — | ||||

| Maximum offering price per share (Net asset value | ||||||||

| per share divided by 95.00%) | $ | 49.02 | $ | — | ||||

| Investor Class Shares | ||||||||

| Net assets applicable to shares outstanding | $ | — | $ | 30,720,684 | ||||

| Shares issued and outstanding [unlimited number | ||||||||

| of shares (par value $0.01) authorized] | — | 1,145,504 | ||||||

| Net asset value, offering and redemption price per share | $ | — | $ | 26.82 | ||||

| Institutional Class Shares | ||||||||

| Net assets applicable to shares outstanding | $ | 267,273,090 | $ | — | ||||

| Shares issued and outstanding [unlimited number | ||||||||

| of shares (par value $0.01) authorized] | 5,726,254 | — | ||||||

| Net asset value, offering and redemption price per share | $ | 46.68 | $ | — | ||||

| COMPONENTS OF NET ASSETS | ||||||||

| Paid-in capital | $ | 230,557,771 | $ | 27,314,737 | ||||

| Total distributable earnings | 59,432,330 | 3,405,947 | ||||||

| Net assets | $ | 289,990,101 | $ | 30,720,684 | ||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

29

POPLAR FOREST FUNDS

STATEMENTS OF OPERATIONS For the Year Ended September 30, 2023

| Poplar Forest | Poplar Forest | |||||||

| Partners Fund | Cornerstone Fund | |||||||

| INVESTMENT INCOME | ||||||||

| Income | ||||||||

| Dividends | $ | 9,341,777 | $ | 572,505 | ||||

| Interest | 658,424 | 455,316 | ||||||

| Total Income | 10,000,201 | 1,027,821 | ||||||

| Expenses | ||||||||

| Advisory fees (Note 4) | 2,744,179 | 250,300 | ||||||

| Administration and fund accounting fees (Note 4) | 292,115 | 97,719 | ||||||

| Transfer agent fees and expenses (Note 4) | 145,454 | 22,936 | ||||||

| Sub-transfer agent fees (Note 4) | 80,985 | 843 | ||||||

| 12b-1 fees – Class A shares (Note 5) | 62,391 | — | ||||||

| Registration fees | 38,994 | 4,722 | ||||||

| Custody fees (Note 4) | 37,405 | 5,404 | ||||||

| Audit fees | 22,500 | 21,003 | ||||||

| Printing and mailing expense | 18,634 | 4,219 | ||||||

| Trustees fees and expenses | 17,121 | 16,893 | ||||||

| Chief Compliance Officer fee (Note 4) | 12,500 | 12,501 | ||||||

| Legal fees | 7,323 | 7,324 | ||||||

| Insurance expense | 5,832 | 2,374 | ||||||

| Interest expense (Note 7) | 2,381 | — | ||||||

| Miscellaneous | 30,956 | 7,918 | ||||||

| Total expenses | 3,518,770 | 454,156 | ||||||

| Less: Advisory fees waived (Note 4) | (322,385 | ) | (172,569 | ) | ||||

| Net expenses | 3,196,385 | 281,587 | ||||||

| Net investment income | 6,803,816 | 746,234 | ||||||

| REALIZED AND UNREALIZED GAIN ON INVESTMENTS | ||||||||

| Net realized gain from investments | 7,661,715 | 503,400 | ||||||

| Net change in unrealized appreciation on investments | 8,554,026 | 799,623 | ||||||

| Net realized and unrealized gain on investments | 16,215,741 | 1,303,023 | ||||||

| Net Increase in Net Assets Resulting from Operations | $ | 23,019,557 | $ | 2,049,257 | ||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

30

POPLAR FOREST PARTNERS FUND

STATEMENTS OF CHANGES IN NET ASSETS

| Year Ended | Year Ended | |||||||

| September 30, 2023 | September 30, 2022 | |||||||

| NET INCREASE/(DECREASE) IN NET ASSETS FROM: | ||||||||

| OPERATIONS | ||||||||

| Net investment income | $ | 6,803,816 | $ | 5,151,136 | ||||

| Net realized gain from investments | 7,661,715 | 21,976,629 | ||||||

| Net change in unrealized appreciation/ | ||||||||

| (depreciation) on investments | 8,554,026 | (45,477,946 | ) | |||||

| Net increase/(decrease) in net assets | ||||||||

| resulting from operations | 23,019,557 | (18,350,181 | ) | |||||

| DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| Net dividends and distributions to shareholders — | ||||||||

| Class A Shares | (1,490,955 | ) | (3,177,349 | ) | ||||

| Net dividends and distributions to shareholders — | ||||||||

| Institutional Class Shares | (18,740,307 | ) | (38,843,292 | ) | ||||

| Total dividends and distributions to shareholders | (20,231,262 | ) | (42,020,641 | ) | ||||

| CAPITAL SHARE TRANSACTIONS | ||||||||

| Net increase/(decrease) in net assets derived | ||||||||

| from net change in outstanding shares (a) | (12,650,817 | ) | 46,622,960 | |||||

| Total decrease in net assets | (9,862,522 | ) | (13,747,862 | ) | ||||

| NET ASSETS | ||||||||

| Beginning of year | 299,852,623 | 313,600,485 | ||||||

| End of year | $ | 289,990,101 | $ | 299,852,623 | ||||

| (a) | A summary of share transactions is as follows: |

Year Ended September 30, 2023 | Year Ended September 30, 2022 | ||||||||||||||||

| Class A Shares | Shares | Paid-in Capital | Shares | Paid-in Capital | |||||||||||||

| Shares sold | 39,588 | $ | 1,959,738 | 123,157 | $ | 6,537,843 | |||||||||||

| Shares issued on | |||||||||||||||||

| reinvestments of distributions | 24,537 | 1,225,624 | 53,592 | 2,723,003 | |||||||||||||

| Shares redeemed | (83,934 | ) | (4,111,423 | ) | (99,674 | ) | (5,070,147 | ) | |||||||||

| Net increase/(decrease) | (19,809 | ) | $ | (926,061 | ) | 77,075 | $ | 4,190,699 | |||||||||

Year Ended September 30, 2023 | Year Ended September 30, 2022 | ||||||||||||||||

| Institutional Class Shares | Shares | Paid-in Capital | Shares | Paid-in Capital | |||||||||||||

| Shares sold | 996,167 | $ | 49,799,303 | 1,418,632 | $ | 75,102,907 | |||||||||||

| Shares issued on | |||||||||||||||||

| reinvestments of distributions | 267,033 | 13,340,977 | 561,705 | 28,529,000 | |||||||||||||

| Shares redeemed | (1,526,866 | ) | (74,865,036 | ) | (1,153,787 | ) | (61,199,646 | ) | |||||||||

| Net increase/(decrease) | (263,666 | ) | $ | (11,724,756 | ) | 826,550 | $ | 42,432,261 | |||||||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

31

POPLAR FOREST CORNERSTONE FUND

STATEMENTS OF CHANGES IN NET ASSETS

| Year Ended | Year Ended | |||||||

| September 30, 2023 | September 30, 2022 | |||||||

| NET INCREASE/(DECREASE) IN NET ASSETS FROM: | ||||||||

| OPERATIONS | ||||||||

| Net investment income | $ | 746,234 | $ | 549,728 | ||||

| Net realized gain from investments | 503,400 | 2,183,894 | ||||||

| Net change in unrealized appreciation/ | ||||||||

| (depreciation) on investments | 799,623 | (4,474,030 | ) | |||||

| Net increase/(decrease) in net assets | ||||||||

| resulting from operations | 2,049,257 | (1,740,408 | ) | |||||

| DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| Net dividends and distributions to shareholders — | ||||||||

| Investor Class Shares | (2,422,156 | ) | (3,563,788 | ) | ||||

| Total dividends and distributions to shareholders | (2,422,156 | ) | (3,563,788 | ) | ||||

| CAPITAL SHARE TRANSACTIONS | ||||||||

| Net increase in net assets derived from | ||||||||

| net change in outstanding shares (a) | 2,987,055 | 3,967,318 | ||||||

| Total increase/(decrease) in net assets | 2,614,156 | (1,336,878 | ) | |||||

| NET ASSETS | ||||||||

| Beginning of year | 28,106,528 | 29,443,406 | ||||||

| End of year | $ | 30,720,684 | $ | 28,106,528 | ||||

| (a) | A summary of share transactions is as follows: |

Year Ended September 30, 2023 | Year Ended September 30, 2022 | ||||||||||||||||

| Investor Class Shares | Shares | Paid-in Capital | Shares | Paid-in Capital | |||||||||||||

| Shares sold | 70,046 | $ | 1,974,059 | 62,751 | $ | 1,948,560 | |||||||||||

| Shares issued on | |||||||||||||||||

| reinvestments of distributions | 85,138 | 2,355,782 | 114,029 | 3,375,255 | |||||||||||||

| Shares redeemed | (47,594 | ) | (1,342,786 | ) | (45,031 | ) | (1,356,497 | ) | |||||||||

| Net increase | 107,590 | $ | 2,987,055 | 131,749 | $ | 3,967,318 | |||||||||||

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

32

POPLAR FOREST PARTNERS FUND

FINANCIAL HIGHLIGHTS For a share outstanding throughout each year

| Class A Shares | ||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Net asset value, beginning of year | $ | 46.07 | $ | 55.97 | $ | 35.69 | $ | 42.22 | $ | 52.65 | ||||||||||

| Income from investment operations: | ||||||||||||||||||||

| Net investment income^ | 0.90 | 0.69 | 0.74 | 0.74 | 0.58 | |||||||||||||||

| Net realized and unrealized | ||||||||||||||||||||

| gain/(loss) on investments | 2.54 | (3.18 | ) | 20.48 | (6.65 | ) | (6.50 | ) | ||||||||||||

| Total from investment operations | 3.44 | (2.49 | ) | 21.22 | (5.91 | ) | (5.92 | ) | ||||||||||||

| Less distributions: | ||||||||||||||||||||

| From net investment income | (0.50 | ) | (0.94 | ) | (0.94 | ) | (0.62 | ) | (0.50 | ) | ||||||||||

| From net realized | ||||||||||||||||||||

| gain on investments | (2.44 | ) | (6.47 | ) | — | — | (4.01 | ) | ||||||||||||

| Total distributions | (2.94 | ) | (7.41 | ) | (0.94 | ) | (0.62 | ) | (4.51 | ) | ||||||||||

| Net asset value, end of year | $ | 46.57 | $ | 46.07 | $ | 55.97 | $ | 35.69 | $ | 42.22 | ||||||||||

| Total return | 7.05 | % | -5.68 | % | 60.26 | % | -14.27 | % | -10.71 | % | ||||||||||

| Ratios/supplemental data: | ||||||||||||||||||||

| Net assets, end of year (thousands) | $ | 22,717 | $ | 23,387 | $ | 24,098 | $ | 16,840 | $ | 29,359 | ||||||||||

| Ratio of expenses | ||||||||||||||||||||

| to average net assets: | ||||||||||||||||||||

| Before fee waiver | 1.30 | % | 1.29 | % | 1.34 | % | 1.43 | % | 1.36 | % | ||||||||||

| After fee waiver | 1.20 | % | 1.20 | % | 1.21 | % | 1.25 | % | 1.25 | % | ||||||||||

| Ratio of net investment income | ||||||||||||||||||||

| to average net assets: | ||||||||||||||||||||

| Before fee waiver | 1.73 | % | 1.21 | % | 1.35 | % | 1.75 | % | 1.25 | % | ||||||||||

| After fee waiver | 1.83 | % | 1.30 | % | 1.48 | % | 1.93 | % | 1.36 | % | ||||||||||

| Portfolio turnover rate | 35.12 | % | 30.29 | % | 40.94 | % | 40.35 | % | 30.72 | % | ||||||||||

| ^ | Based on average shares outstanding. |

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

33

POPLAR FOREST PARTNERS FUND

FINANCIAL HIGHLIGHTS For a share outstanding throughout each year

| Institutional Class | ||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Net asset value, beginning of year | $ | 46.16 | $ | 56.07 | $ | 35.75 | $ | 42.29 | $ | 52.79 | ||||||||||

| Income from investment operations: | ||||||||||||||||||||

| Net investment income^ | 1.03 | 0.83 | 0.86 | 0.84 | 0.69 | |||||||||||||||

| Net realized and unrealized | ||||||||||||||||||||

| gain/(loss) on investments | 2.55 | (3.19 | ) | 20.50 | (6.65 | ) | (6.53 | ) | ||||||||||||

| Total from investment operations | 3.58 | (2.36 | ) | 21.36 | (5.81 | ) | (5.84 | ) | ||||||||||||

| Less distributions: | ||||||||||||||||||||

| From net investment income | (0.62 | ) | (1.08 | ) | (1.04 | ) | (0.73 | ) | (0.65 | ) | ||||||||||

| From net realized | ||||||||||||||||||||

| gain on investments | (2.44 | ) | (6.47 | ) | — | — | (4.01 | ) | ||||||||||||

| Total distributions | (3.06 | ) | (7.55 | ) | (1.04 | ) | (0.73 | ) | (4.66 | ) | ||||||||||

| Net asset value, end of year | $ | 46.68 | $ | 46.16 | $ | 56.07 | $ | 35.75 | $ | 42.29 | ||||||||||

| Total return | 7.32 | % | -5.43 | % | 60.63 | % | -14.03 | % | -10.49 | % | ||||||||||

| Ratios/supplemental data: | ||||||||||||||||||||

| Net assets, end of year (thousands) | $ | 267,273 | $ | 276,465 | $ | 289,502 | $ | 192,576 | $ | 362,369 | ||||||||||

| Ratio of expenses | ||||||||||||||||||||

| to average net assets: | ||||||||||||||||||||

| Before fee waiver | 1.05 | % | 1.04 | % | 1.09 | % | 1.18 | % | 1.11 | % | ||||||||||

| After fee waiver | 0.95 | % | 0.95 | % | 0.96 | % | 1.00 | % | 1.00 | % | ||||||||||

| Ratio of net investment income | ||||||||||||||||||||

| to average net assets: | ||||||||||||||||||||

| Before fee waiver | 1.98 | % | 1.46 | % | 1.59 | % | 2.00 | % | 1.50 | % | ||||||||||

| After fee waiver | 2.08 | % | 1.55 | % | 1.72 | % | 2.18 | % | 1.61 | % | ||||||||||

| Portfolio turnover rate | 35.12 | % | 30.29 | % | 40.94 | % | 40.35 | % | 30.72 | % | ||||||||||

| ^ | Based on average shares outstanding. |

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

34

POPLAR FOREST CORNERSTONE FUND

FINANCIAL HIGHLIGHTS For a share outstanding throughout each year

| Investor Shares | ||||||||||||||||||||

| Year Ended September 30, | ||||||||||||||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | ||||||||||||||||

| Net asset value, beginning of year | $ | 27.08 | $ | 32.49 | $ | 22.76 | $ | 25.58 | $ | 28.20 | ||||||||||

| Income from investment operations: | ||||||||||||||||||||

| Net investment income^ | 0.66 | 0.54 | 0.60 | 0.45 | 0.42 | |||||||||||||||

| Net realized and unrealized | ||||||||||||||||||||

| gain/(loss) on investments | 1.43 | (2.03 | ) | 9.64 | (2.11 | ) | (1.83 | ) | ||||||||||||

| Total from investment operations | 2.09 | (1.49 | ) | 10.24 | (1.66 | ) | (1.41 | ) | ||||||||||||

| Less distributions: | ||||||||||||||||||||

| From net investment income | (0.45 | ) | (0.72 | ) | (0.51 | ) | (0.34 | ) | (0.42 | ) | ||||||||||

| From net realized | ||||||||||||||||||||

| gain on investments | (1.90 | ) | (3.20 | ) | — | (0.82 | ) | (0.79 | ) | |||||||||||

| Total distributions | (2.35 | ) | (3.92 | ) | (0.51 | ) | (1.16 | ) | (1.21 | ) | ||||||||||

| Net asset value, end of year | $ | 26.82 | $ | 27.08 | $ | 32.49 | $ | 22.76 | $ | 25.58 | ||||||||||

| Total return | 7.46 | % | -5.60 | % | 45.53 | % | -6.89 | % | -4.71 | % | ||||||||||

| Ratios/supplemental data: | ||||||||||||||||||||

| Net assets, end of year (thousands) | $ | 30,721 | $ | 28,107 | $ | 29,443 | $ | 22,084 | $ | 26,739 | ||||||||||

| Ratio of expenses | ||||||||||||||||||||

| to average net assets: | ||||||||||||||||||||

| Before fee waiver | 1.45 | % | 1.44 | % | 1.53 | %# | 1.76 | % | 1.64 | % | ||||||||||

| After fee waiver | 0.90 | % | 0.90 | % | 0.90 | %# | 0.90 | % | 0.90 | % | ||||||||||

| Ratio of net investment income | ||||||||||||||||||||

| to average net assets: | ||||||||||||||||||||

| Before fee waiver | 1.83 | % | 1.22 | % | 1.38 | % | 1.05 | % | 0.92 | % | ||||||||||

| After fee waiver | 2.38 | % | 1.76 | % | 2.01 | % | 1.91 | % | 1.66 | % | ||||||||||

| Portfolio turnover rate | 36.43 | % | 29.73 | % | 36.13 | % | 39.97 | % | 38.12 | % | ||||||||||

| ^ | Based on average shares outstanding. |

| # | Includes expenses of Class A Shares which converted to Investor Class Shares on October 30, 2020. |

The accompanying notes are an integral part of these financial statements.

Poplar Forest Funds Annual Report, September 2023 |

35

POPLAR FOREST FUNDS

NOTES TO FINANCIAL STATEMENTS at September 30, 2023

NOTE 1 – ORGANIZATION

The Poplar Forest Partners Fund (the “Partners Fund”) and the Poplar Forest Cornerstone Fund (“Cornerstone Fund”), (each, a “Fund” and collectively, the “Funds”) are diversified series of Advisors Series Trust (the “Trust”), which is registered under the Investment Company Act of 1940, as amended, (the “1940 Act”) as an open-end management investment company. Each Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies.”

The investment objective of the Partners Fund is to seek long-term growth of capital. The investment objective of the Cornerstone Fund is to seek to achieve current income and long-term growth of capital. The Partners Fund currently offers Class A shares and Institutional Class shares. The Cornerstone Fund currently offers Investor Class shares. Class A shares are subject to a maximum front-end sales load of 5.00%, which decreases depending on the amount invested. The Partner Fund’s Class A shares and Institutional Class shares commenced operations on December 31, 2009.

The Cornerstone Fund’s Class A shares and Institutional Class shares commenced operations on December 31, 2014. At the close of business on October 30, 2020, the Cornerstone Fund’s Class A shares converted to the Institutional Class shares. On January 28, 2021, the class name changed from Institutional Class to Investor Class.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Funds. These policies are in conformity with accounting principles generally accepted in the United States of America.

| A. | Security Valuation: All investments in securities are recorded at their estimated fair value, as described in Note 3. | |

| B. | Federal Income Taxes: It is the Funds’ policy to comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all of its taxable income to its shareholders. Therefore, no Federal income or excise tax provision is required. | |

| The Funds recognize the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. The tax returns of the Funds’ prior three fiscal years are open for examination. Management has reviewed all open tax years in major jurisdictions and concluded that there is no impact on the Funds’ net assets and no tax liability resulting from unrecognized tax events relating to uncertain income tax positions taken or expected to be taken on a tax return. The Funds identify their major tax jurisdictions as U.S. Federal and the state of Wisconsin. The Funds are not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months. |

Poplar Forest Funds Annual Report, September 2023 |

36

POPLAR FOREST FUNDS

NOTES TO FINANCIAL STATEMENTS at September 30, 2023, Continued