2011 Annual Meeting April 25, 2012

2 FORWARD - LOOKING STATEMENT We may, from time to time, make written or oral “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, including statements contained in our filings with the Securities and Exchange Commission (the “SEC”), our reports to shareholders and in other communications by us. This presentation contains “forward - looking statements” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” and “potential.” Examples of forward - looking statements include, but are not limited to, estimates with respect to our financial condition, results of operation and business that are subject to various factors which could cause actual results to differ materially from these estimates. These factors include, but are not limited to : • changes to interest rates, the ability to control costs and expenses; • our ability to integrate new technology into its operations; • general economic conditions; • the success of our efforts to diversify its revenue base by developing additional sources of non - interest income while continuing to manage its existing fee based business; • the impact on us of the changing statutory and regulatory requirements; and • the risks inherent in commencing operations in new markets. Any or all of our forward - looking statements in this presentation, and in any other public statements, we make may turn out to be wrong. They can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties. Consequently, no forward - looking statements can be guaranteed. We disclaim any obligation to subsequently revise any forward - looking statements to reflect events or circumstances after the date of such statements, or to reflect the occurrence of anticipated or unanticipated events .

President’s Message Our Business Environment Our Performance Shareholder Value Looking Ahead 3 Annual Meeting 2012

Building for the Future New Brand Board of Directors Financial Overview 4 President’s Message

Building for the Future Talented management team Loan production office – Rochelle Park Added 4 seasoned and proven commercial lenders 5 President’s Message

New Brand Defines our differentiator, which is the Customer experience Understanding our Customer needs Being relationship oriented community bank Establishing an emotional connection with our Customers (Not process) In essence we get “Closer to Our Customers” 6 President’s Message

Board of Directors Chairman of the Board succession by Edward Leppert We strengthened the Board’s lending oversight and organizational capabilities with the addition of two directors to the Bank’s Board of Directors (Robert McNerney and Richard Branca) that have extensive real estate expertise . Critical to strong risk management 7 President’s Message

8 Our Business Environment Equity Markets (source: SNL Financial LC) • 11 consecutive quarters of positive growth in GDP • Economy has shown signs of stabilizing • Equity markets trading near 2006 levels (Bubble???) • Interest rates at historical lows • This recovery has lagged all other recoveries and is sluggish, however showing positive signs

9 Our Business Environment 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0 10.0 11.0 Feb-02 Sep-02 Apr-03 Nov-03 Jun-04 Jan-05 Aug-05 Mar-06 Oct-06 May-07 Dec-07 Jul-08 Feb-09 Sep-09 Apr-10 Nov-10 Jun-11 Jan-12 NJ Unemployment US and NJ Unemployment Rate • High level of unemployment; however, improving modestly • L ack of confidence from both businesses and consumers • Consumers and businesses not spending and not reinvesting back into the economy; in turn, savings and cash are growing and their financial conditions are strengthening (source: dlshort.com) (source: Department of Labor)

10 Our Business Environment • Real Estate Markets still exhibit weakness, however no longer free falling - x CRE market in Northern NJ still strained x Office space in Northern NJ is still flat x NYC markets are strengthening and building momentum x Northern NJ will benefit from progression x Multi - family is the flavor of choice (low cap rates are risk point) x Retail will continue to be strained due to many big boxes downsizing, which may create opportunities for small businesses again x Lack of market for land (difficult to value) • Markets further from NYC will recover more slowly

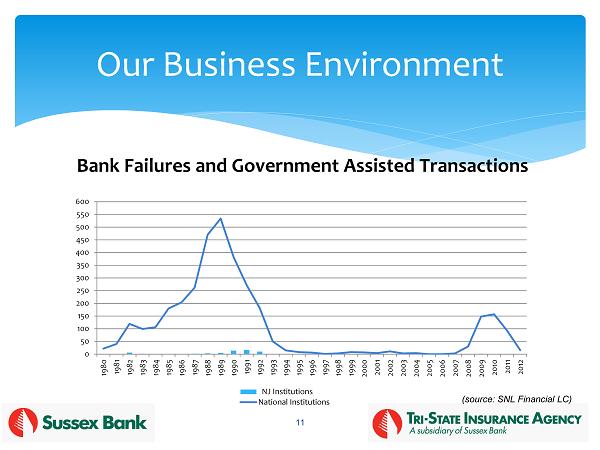

11 Our Business Environment 0 50 100 150 200 250 300 350 400 450 500 550 600 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 NJ Institutions National Institutions Bank Failures and Government Assisted Transactions (source: SNL Financial LC)

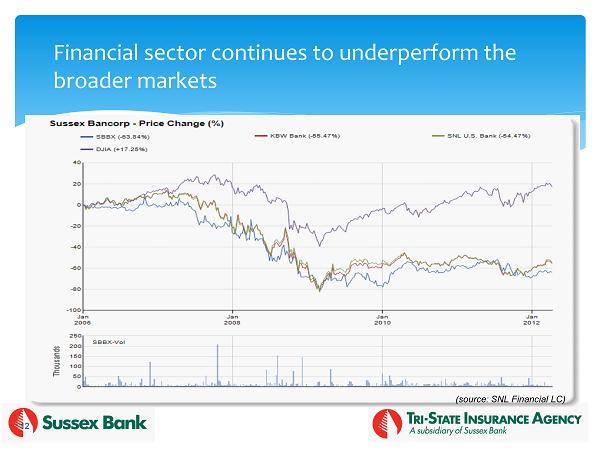

12 Financial sector continues to underperform the broader markets (source: SNL Financial LC)

Select accomplishments Lending and Credit Quality Market Extension Financial Performance 13 Our Performance

Executive and senior management Relationship banking paradigm New commercial lending team Company’s culture now emphasizes: ▪ Partnership, Teamwork, Trust and Respect ▪ Customer Experience & Sales ▪ Risk management -- especially Credit & Interest Rate Risk -- understanding the “What If ?” ▪ Governance ▪ Employee growth and development (R&R) ▪ Continuing to be good corporate citizens by giving back the communities we serve 14 Select Accomplishments

Introduced a plan to be customer centric New credit and administrative process Improved operations infra - structure that enhance our capabilities Loan production office in Rochelle Park Built capabilities in the Treasury area (ALCO and Investments) Security strategies improving IRR and credit exposure (risk / reward) Improved financial reporting and transparency (internally and externally) Modernizing our technology and delivery channels Reducing problem assets by 21% Tri - state Insurance success story (to be continued) 15 Select Accomplishments

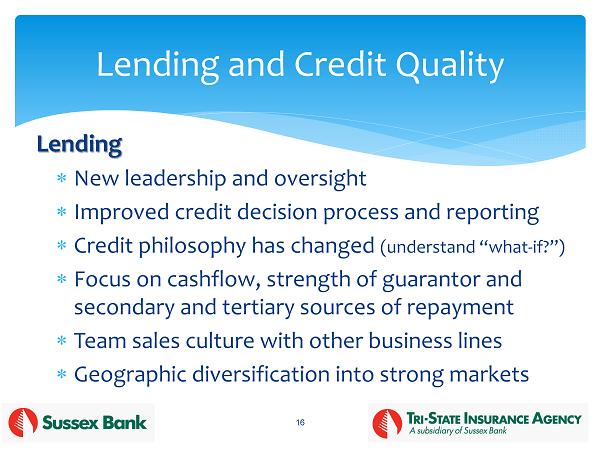

Lending New leadership and oversight Improved credit decision process and reporting Credit philosophy has changed (understand “what - if?”) Focus on cashflow , strength of guarantor and secondary and tertiary sources of repayment Team sales culture with other business lines Geographic diversification into strong markets 16 Lending and Credit Quality

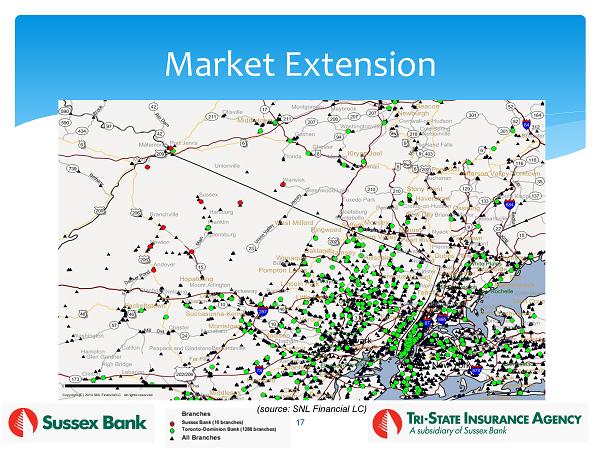

17 Market Extension (source: SNL Financial LC)

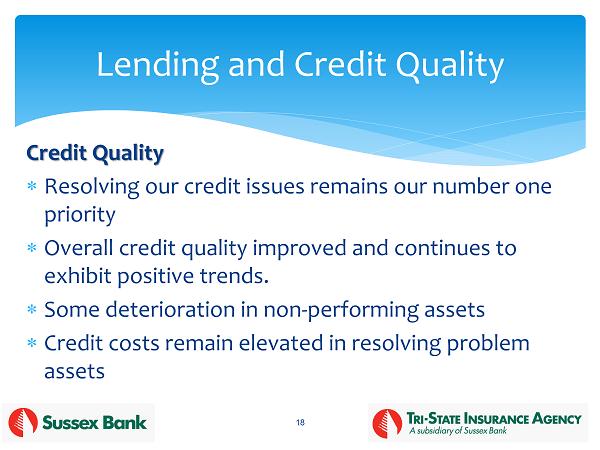

Credit Quality Resolving our credit issues remains our number one priority Overall credit quality improved and continues to exhibit positive trends . Some deterioration in non - performing assets Credit costs remain elevated in resolving problem assets 18 Lending and Credit Quality

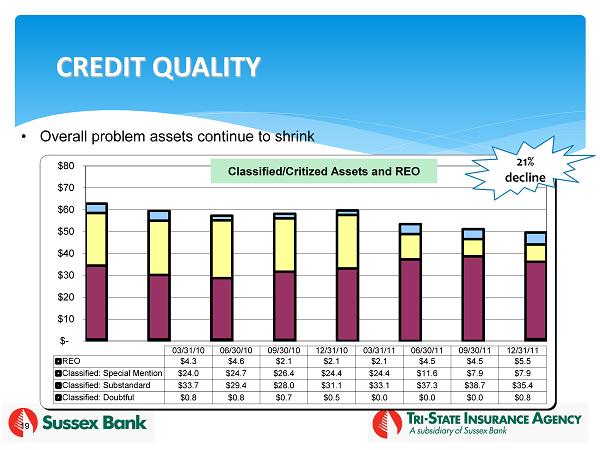

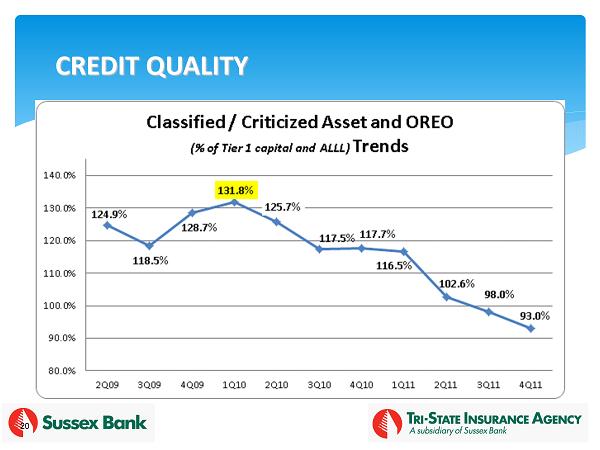

19 CREDIT QUALITY $- $10 $20 $30 $40 $50 $60 $70 $80 03/31/10 06/30/10 09/30/10 12/31/10 03/31/11 06/30/11 09/30/11 12/31/11 REO $4.3 $4.6 $2.1 $2.1 $2.1 $4.5 $4.5 $5.5 Classified: Special Mention $24.0 $24.7 $26.4 $24.4 $24.4 $11.6 $7.9 $7.9 Classified: Substandard $33.7 $29.4 $28.0 $31.1 $33.1 $37.3 $38.7 $35.4 Classified: Doubtful $0.8 $0.8 $0.7 $0.5 $0.0 $0.0 $0.0 $0.8 Classified/Critized Assets and REO • Overall problem assets continue to shrink 21% decline

20 CREDIT QUALITY

21 CREDIT QUALITY • Top 23 problem loan relationships represent approximately 72% of criticized and classified loans (by balance) • Executive management reviews the status of each of those relationships on a weekly basis ▪ Develop strategies for each of them ▪ Follow - up on the execution of those strategies ▪ Sounding board for workout group in structuring solutions • The resolution process takes long, however we are making strong headway in getting to resolution, which will improve our credit quality.

22 FINANCIAL PERFORMANCE (Peer Group source : SNL Financial LC - 10 NJ Commercial Banks with assets less than $1 billion with a similar profile as Sussex Bank )

Balance sheet - Total assets increased by 6.9% over last year - Total deposits increased 10.2% over last year (first half flat, but finished year strong) - Loans grew 0.4% over last year (portfolio began shrinking early in 1Q into year - end) Capital adequacy: all in excess of the ratios required to be deemed “well - capitalized” 23 FINANCIAL PERFORMANCE: 2011 Highlights

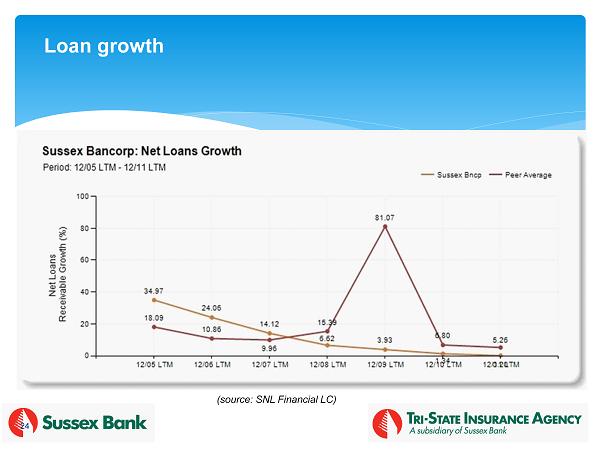

24 Loan growth (source: SNL Financial LC)

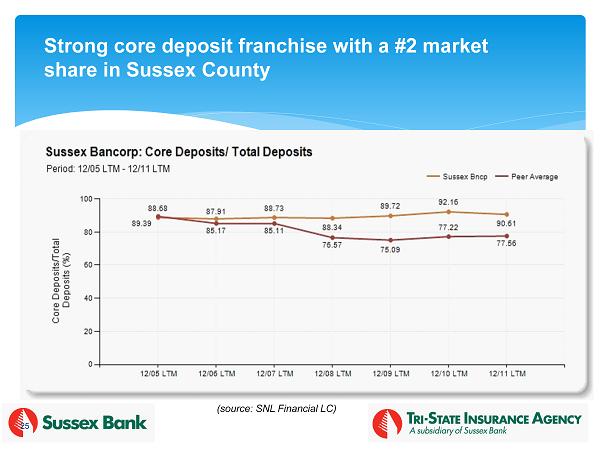

25 Strong core deposit franchise with a #2 market share in Sussex County (source: SNL Financial LC)

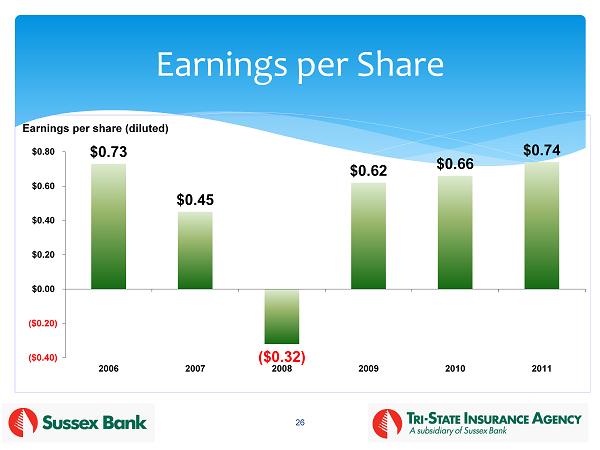

26 Earnings per Share $0.73 $0.45 ($0.32) $0.62 $0.66 $0.74 ($0.40) ($0.20) $0.00 $0.20 $0.40 $0.60 $0.80 2006 2007 2008 2009 2010 2011 Earnings per share (diluted)

Income Statement (+$294k or 13.5%) Non - interest income +$672k (security strategies +$593k and Tri - State +$199k) Net interest income ( te ) +$548k (driven by 6bp growth in the margin) Partly offset by $755k (or 5.0%) increase in non - interest expense (salaries and loan collections costs) 27 FINANCIAL PERFORMANCE: 2011 Highlights

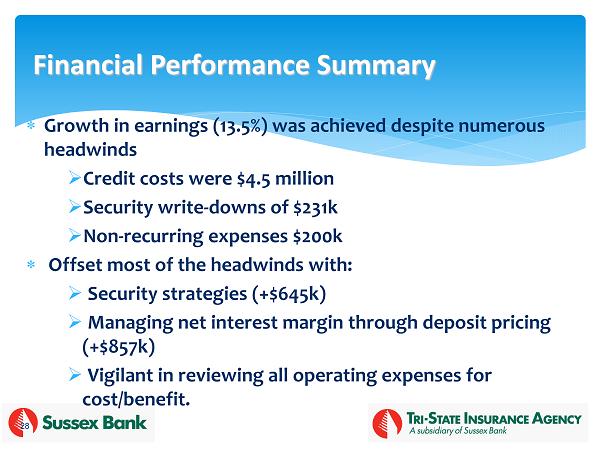

Growth in earnings (13.5%) was achieved despite numerous headwinds » Credit costs were $4.5 million » Security write - downs of $231k » Non - recurring expenses $200k Offset most of the headwinds with: » Security strategies (+$645k) » Managing net interest margin through deposit pricing (+$857k) » Vigilant in reviewing all operating expenses for cost/benefit. 28 Financial Performance Summary

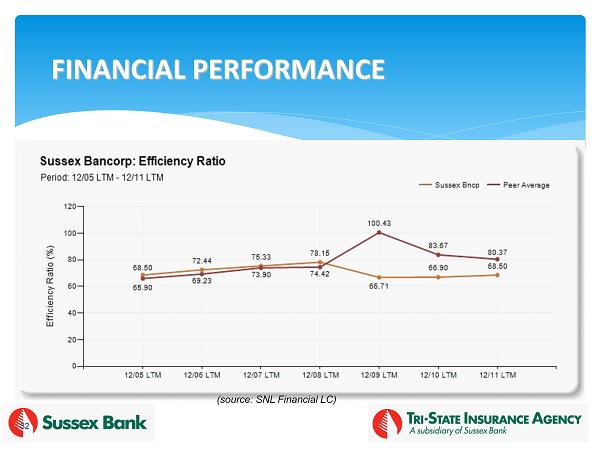

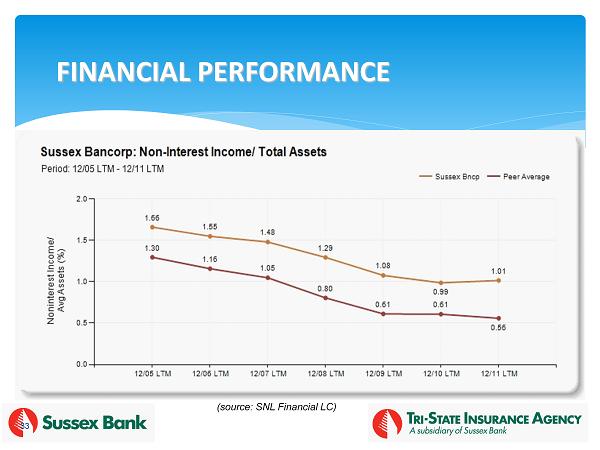

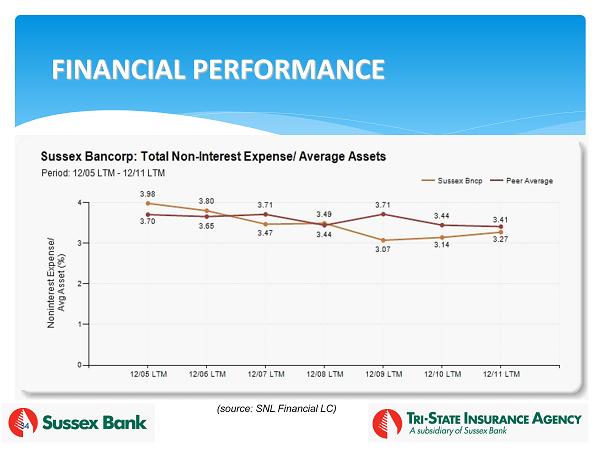

29 FINANCIAL PERFORMANCE (source: SNL Financial LC)

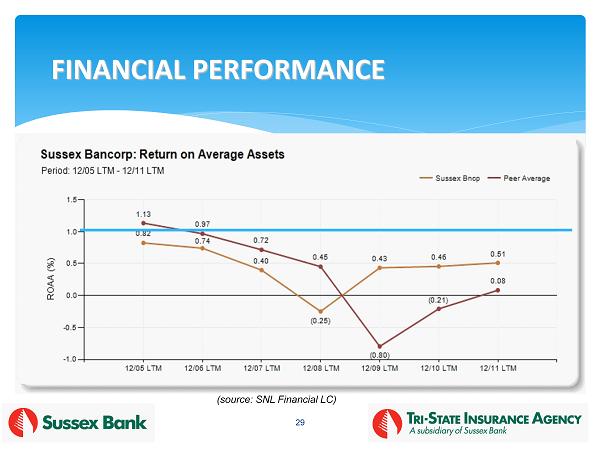

30 FINANCIAL PERFORMANCE (source: SNL Financial LC)

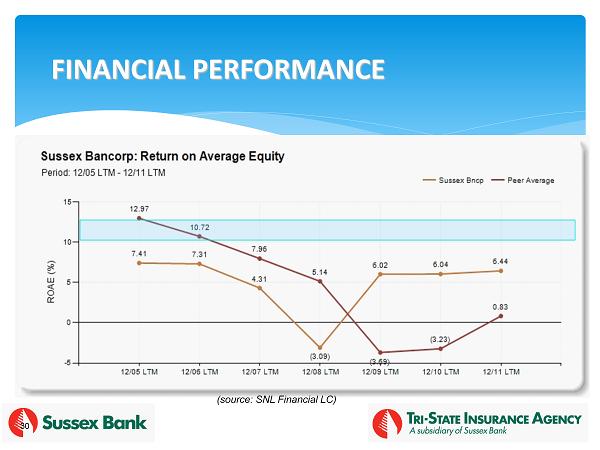

31 FINANCIAL PERFORMANCE (source: SNL Financial LC)

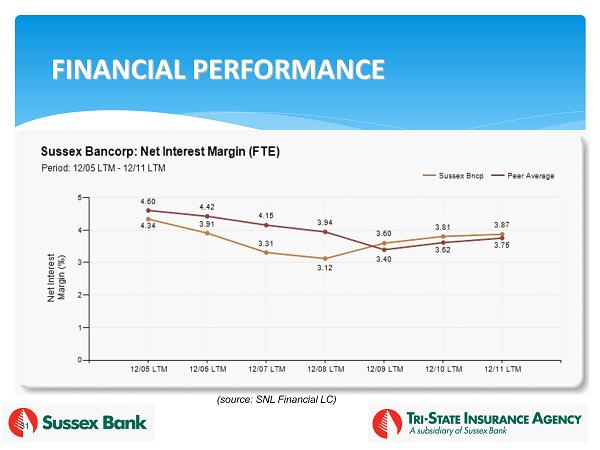

32 FINANCIAL PERFORMANCE (source: SNL Financial LC)

33 FINANCIAL PERFORMANCE (source: SNL Financial LC)

34 FINANCIAL PERFORMANCE (source: SNL Financial LC)

35 Shareholder Value Building our business through: + Leadership and management + Corporate governance + Risk management and improved credit quality + Customer experience + Employee experience will strengthen our financial performance= Long term shareholder value

36 Questions?