UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8061

Diamond Hill Funds

(Exact name of registrant as specified in charter)

| | |

| 325 John H. McConnell Boulevard, Suite 200, Columbus, Ohio 43215 |

| (Address of principal executive offices) | | (Zip code) |

James F. Laird, Jr., 325 John H. McConnell Boulevard, Suite 200, Columbus, Ohio 43215

(Name and address of agent for service)

Registrant’s telephone number, including area code: 614-255-3333

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

Item 1. Reports to Stockholders.

This material must be preceded or accompanied by a current prospectus.

Annual Report

SMALL CAP FUND

SMALL-MID CAP FUND

LARGE CAP FUND

SELECT FUND

LONG-SHORT FUND

RESEARCH OPPORTUNITIES FUND

FINANCIAL LONG-SHORT FUND

STRATEGIC INCOME FUND

| | | | |

| Not FDIC Insured | | | May Lose Value | | | No Bank Guarantee |

Table of Contents

CAUTIONARY STATEMENT

At Diamond Hill, we pledge that, “we will communicate with our clients about our investment performance in a manner that will allow them to properly assess whether we are deserving of their trust.” Our views and opinions regarding the investment prospects of our portfolio holdings and Funds are “forward looking statements” which may or may not be accurate over the long term. While we believe we have a reasonable basis for our opinions, actual results may differ materially from those we anticipate. Information provided in this report should not be considered a recommendation to purchase or sell any particular security.

You can identify forward looking statements by words like “believe,” “expect,” “anticipate,” or similar expressions when discussing prospects for particular portfolio holdings and/or one of the Funds. We cannot assure future results. You should not place undue reliance on forward-looking statements, which speak only as of the date of this report. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. This material is not authorized for distribution to prospective investors unless preceded or accompanied by a Prospectus. Please read the Prospectus carefully for a discussion of fees, expenses, and risks. Current performance may be lower or higher than that quoted herein. You may obtain a current copy of the Prospectus or more current performance information by calling 1-888-226-5595 or visit Diamond Hill’s website www.diamond-hill.com.

2012 Annual Report

Letter to Shareholders

Dear Fellow Shareholders:

We are pleased to provide you with this year-end update for the Diamond Hill Funds. Despite strong absolute equity market returns, the past three year period has been a difficult one for most active money managers. Our equity Fund returns trailed benchmark returns over the same period; however, we remain focused on five-year periods to evaluate our results. We believe that five years is the shortest time period for statistical significance and the longest time period for the typical investor’s patience. In fact, we believe that taking a long-term view is perhaps our greatest competitive advantage. While the perception of near-term profit opportunities often attracts significant amounts of capital and erodes excess returns, there are far fewer investors willing to deploy capital based on an investment horizon of five years or more. At many institutions, the career risk associated with being wrong in the short term is simply too great for analysts to consider investment opportunities that may play out over years instead of quarters.

We believe that the next five years will be advantageous for equity investors and for our intrinsic value focused investment philosophy and process. Periods of high market correlation typically call into question the ability of active managers to outperform. Our strategies do not aim to achieve a specific result in the near term or utilize hedging strategies to nullify the effects of market volatility and macro uncertainty. We take a long-term view of performance and focus our research efforts on understanding and valuing businesses. Our fundamental intrinsic value investment philosophy remains unchanged, as it has since inception, and we believe it will remain relevant and successful regardless of how the investment landscape changes in the future.

2012 Financial Markets

The S&P 500 Index finished 2012 with a 16.0% total return as U.S. corporate profit margins remained near record levels fueling stock price gains. Globally, Europe’s debt crisis was unresolved, China’s economy showed signs of slowing, and conflict threatened the Middle East two years after the Arab Spring uprising. However, investors continued to be reluctant to fully commit to stocks as evidenced by continued net flows from equity mutual funds and into bond mutual funds.

| | Ÿ | | During the first quarter of 2012, investors left the safety of high-quality, low-yielding government debt and moved toward lower-quality, high-yield corporate bonds and equity securities. U.S. Treasuries underperformed as yields rose, reflecting an improved outlook for the U.S. economy and a near-term easing of pressures from the European debt crisis. In contrast, the S&P 500 Index posted its best first quarter return in 14 years, increasing 12.6% including dividends. Small cap equity securities, generally considered to be riskier than large cap equity securities, enjoyed their best quarterly return since 2006. |

| | Ÿ | | U.S. markets reversed course in the second quarter of 2012 and investors fled back to the perceived safety of government bonds. In contrast to the first quarter, macro news dominated the market including worries about the European debt crisis and slowing economic growth. China’s economy, a significant contributor to global economic activity, showed signs of slowing as its prime export markets struggled to grow. The result was a decline in the U.S. Treasury yield to 1.66%, as Treasury prices rose, and a 2.8% decline in the S&P 500 Index including dividends. |

| | Ÿ | | During the third quarter, U.S. equity markets reversed course again, shaking off macro-economic concerns and uncertainty around the outcome of the November election. The S&P 500 Index returned 6.4% including dividends. Despite a general feeling of anxiety and gloom among equity investors, broad U.S. equity markets were up approximately 30% over the preceding twelve months, and most market indexes were near all-time highs at the end of the quarter. Continued government stimulus played a meaningful role in boosting third quarter returns as the European Central Bank took action to reduce some nations’ borrowing cost and the U.S. Federal Reserve announced a new round of monetary stimulus measures in September 2012. |

| | Ÿ | | Despite the uncertainty leading up to the November elections and the looming “fiscal cliff”, the U.S. markets were viewed as a safe haven amid global worries. The S&P 500 Index was essentially flat in the fourth quarter of 2012 with a -0.4% total return including dividends. Financial sector stocks were the best performers during the quarter as U.S. banks continued to rebuild their capital levels and demonstrated improving credit quality and profitability. |

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 1 |

Market Outlook

The U.S. economy continues to show modest signs of recovery including a steady recovery in housing. Consumer discretionary spending continues to benefit from various government initiatives largely mitigating the effects of sluggish unemployment and continued household deleveraging. Consumer debt service levels are very low which is a positive; however, current debt service levels are largely linked to low interest/mortgage rates which may present a longer-term risk if rates rise. Household debt as a percent of disposable income has declined meaningfully but remains well above long-term averages. We continue to believe that the U.S. economy will be challenged for many years by financial deleveraging and the ultimate withdrawal of fiscal and monetary stimulus. While the U.S. faces fiscal and monetary headwinds, we believe the U.S. is still well positioned relative to other countries.

From current levels, we believe equity market returns will be positive but modestly below historical average returns over the next five years. It is our expectation that we can achieve better than market returns over the next five years through active portfolio management and stock selection.

Diamond Hill Capital Management, Inc.

| | |

| |

| |

|

| |

Christopher M. Bingaman, CFA | | Christopher A. Welch, CFA |

| Co-Chief Investment Officer | | Co-Chief Investment Officer |

The views expressed are those of the portfolio managers as of December 31, 2012, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. All data referenced are from sources deemed to be reliable but cannot be guaranteed. Securities and sectors referenced should not be construed as a solicitation or recommendation or be used as the sole basis for any investment decision.

The S&P 500 Index is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard and Poor’s selects the companies for the index to widely represent the stock market based on market size, liquidity, and industry group representation. Indexes are unmanaged, do not incur fees, and cannot be invested in directly.

Investors should consider the investment objectives, risks, and charges and expenses of the Diamond Hill Funds carefully before investing. This and other information about the Funds is in the prospectus, which can be obtained at www.diamond-hill.com. Read the prospectus carefully before you invest. Diamond Hill Capital Management, Inc., a registered investment adviser, serves as Investment Adviser to the Diamond Hill Funds and is paid a fee for its services. The Diamond Hill Funds are distributed by BHIL Distributors, Inc. (Member FINRA), an affiliated company. Investors may obtain a copy of the current prospectus at 888-226-5595 or www.diamond-hill.com. Like all mutual funds, Diamond Hill Funds are not FDIC insured, may lose value, and have no bank guarantee.

| | |

| Page 2 | | Diamond Hill Funds Annual Report December 31, 2012 |

Mission Statement, Pledge and Fundamental Principles

Mission | The mission of Diamond Hill is to serve our clients through a disciplined intrinsic value-based approach to investing, while maintaining a long-term perspective, and aligning our interests with those of our clients. |

| | To successfully pursue our mission, we are: |

COMMITTED to the Graham-Buffett investment philosophy, with goals to outperform benchmarks and our peers over 5-year rolling periods and achieve absolute returns sufficient for the risk of the asset class.

DRIVEN by our conviction to create lasting value for clients and shareholders.

MOTIVATED through our ownership of Diamond Hill funds and company stock.

Investment Philosophy | At Diamond Hill, the investment philosophy, which is rooted in the teachings of Benjamin Graham and the methods of Warren Buffett, drives the investment process — not the opposite. |

| | Most simply, we invest in a company when its market price is at a discount to our appraisal of the intrinsic value of the business (or at a premium for short positions). |

There are four guiding principles to our investment philosophy:

| | ¿ | | Treat every investment as a partial ownership interest in that company |

| | ¿ | | Always invest with a margin of safety to ensure the protection of capital, as well as return on capital |

| | ¿ | | Possess a long-term investment temperament |

| | ¿ | | Recognize that market price and intrinsic value tend to converge over a reasonable period of time |

“Investment is most intelligent when it is most businesslike.”

— BENJAMIN GRAHAM

Pledge | Consistent with our mission & investment philosophy, we pledge the following to all of our clients: |

| | Our investment discipline is to assess the economics of the underlying business, its management, and the price that must be paid to own a piece of it. We seek to concentrate our investments in businesses that are available at prices below intrinsic value (above intrinsic value for short positions) and are managed or controlled by trustworthy and capable people. Benjamin Graham pioneered this discipline during the 1930s and many others have practiced it with great success ever since, most notably Warren Buffett. |

| | We will communicate with our clients about our investment performance in a manner that will allow them to properly assess whether we are deserving of their trust. |

| | Our investment team will be comprised of people with integrity, sound experience and education, in combination with a strong work ethic and independence of thought. Especially important is that each possesses the highest level of character, business ethics and professionalism. |

| | Our employees will enjoy a working environment that supports professional and personal growth, thereby enhancing employee satisfaction, the productivity of the firm and the experience of our clients. |

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 3 |

| | “Invest With Us” means we will invest the capital you entrust to us with the same care that we invest our own capital. To this end, Diamond Hill employees and affiliates are significant investors in the same portfolios in which our clients invest and are collectively one of the largest shareholders in the Diamond Hill Funds. In addition, all Diamond Hill employees are subject to a Code of Ethics, which prohibits the purchase of any individual security that is eligible for purchase in one of Diamond Hill’s portfolios. The Code of Ethics also prohibits the purchase of third-party mutual funds that primarily invest in U.S. equity securities. Investment in the Diamond Hill mutual funds is encouraged, and third-party mutual funds can only be purchased in strategies not managed by Diamond Hill. |

Our fundamental equity principles | Valuation |

| | Every share of stock has an intrinsic value that is independent of its current stock market price. |

| | At any point in time, the stock market price may be higher or lower than intrinsic value. |

| | Over short periods of time, the stock market price is heavily influenced by the emotions of market participants, which are far more difficult to predict than intrinsic value. While stock market prices may experience extreme fluctuations on a particular day, we believe intrinsic value is far less volatile. |

| | Over sufficiently long periods of time, five years or longer, the stock market price tends to converge with intrinsic value. |

| | We believe that we can determine a reasonable approximation of intrinsic value in some cases. |

| | Intrinsic value can be determined if we have a reasonable basis for projecting the future cash flows of a business and use an appropriate discount rate. |

| | A five-year discounted cash flow analysis is the primary methodology used to determine whether there is a discrepancy between the current market price and our estimate of intrinsic value. |

| | In order to forecast the amount and timing of cash flows, we concentrate on the fundamental economic drivers of the business and the management. This might encompass the level of industry competition, regulatory factors, the threat of technological obsolescence, and a variety of other factors. |

| | The Diamond Hill investment process continually compares market price to our estimate of intrinsic value, which is updated over time as new information is available. |

| | We only invest in a business when the stock market price is lower than our conservative assessment of per share intrinsic value (or at a premium for short positions). |

| | We concentrate our investments in businesses whose per share intrinsic value is likely to increase. We seek to invest in businesses that possess a competitive advantage and significant growth prospects as well as outstanding managers and employees. |

| | We intend to achieve our return from both the closing of the gap between our purchase price and intrinsic value and the increase in per share intrinsic value. For short positions, an increasing intrinsic value may shorten the holding period. |

| | We define risk as the permanent loss of capital rather than price volatility. We manage risk by investing in companies selling at a discount (premium for short positions) to our estimate of intrinsic value, with a full understanding of the fundamental drivers of intrinsic value. In addition, we carefully consider business risks that could impact our estimate of intrinsic value. |

| | |

| Page 4 | | Diamond Hill Funds Annual Report December 31, 2012 |

Our fundamental fixed income principles | Business Analysis |

| | We leverage the industry analysis conducted by our research team to identify attractive corporate bonds and other senior corporate securities. Our business analysis focuses on the fundamental economic drivers of the business. |

| | We evaluate the quality of a firm’s management and their treatment of bondholders and stockholders. Managements that focus on growth without regard to return on invested capital or long-term cost of capital are more likely to destroy value for bondholders and stockholders. In contrast, managements that understand the competitive dynamics of their business and prudent capital allocation often produce value for both bondholders and stockholders. |

| | We seek to invest in corporate bonds of companies with improving competitive positions and return on invested capital. |

| | We focus on the intrinsic value of the business in relation to the amount of debt in the capital structure. We also evaluate the sources and uses of cash for the business including capital expenditures, working capital, interest charges and the maturity schedule of loans and bonds. |

| | The liquidity and expected volatility of a corporate bond are also important factors in valuation. Because of our long-term time horizon, we will invest in less liquid or more volatile securities; however, we require a higher yield as compensation. |

| | Our core competency is the evaluation of credit risk. As a result, we typically favor lower duration, shorter maturity corporate bonds. We focus almost entirely on the secondary market for corporate bonds rather than the primary (new issue) market. |

| | We primarily invest in investment grade and below-investment grade (high yield) corporate bonds, including a significant allocation to defensive high yield corporate bonds (due to low duration and higher credit quality). |

| | Our objectives are to generate an attractive cash distribution in excess of the current rate of inflation and an attractive total return while minimizing the risk of a permanent loss of capital over a five-year time horizon. |

| | We expect to achieve our return objective by investing in corporate bonds when we believe the market price discounts a greater risk of default or a greater loss upon default than is warranted. An additional source of return exists when the market price provides attractive compensation for short-term illiquidity or volatility, both of which are of less concern to a long-term investor. |

| | Our definition of risk is a permanent loss of capital. We seek to avoid a permanent loss of capital and to earn a sufficient return on capital to grow our purchasing power. |

| | We focus on credit risk, interest rate risk, liquidity risk, call risk, reinvestment risk and other risks when evaluating corporate bonds. |

“You simply have to behave according to what is rational than according to what is fashionable.”

— WARREN BUFFETT

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 5 |

Diamond Hill Small Cap Fund

Performance Update

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Average Annual Total Returns as of December 31, 2012 | | Inception

Date | | | One Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Expense

Ratio* | |

PERFORMANCE AT NAV without sales charges | | | | | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | 12/29/2000 | | | | 12.88% | | | | 8.82% | | | | 4.22% | | | | 10.75% | | | | 1.30% | |

Class C Shares | | | 2/20/2001 | | | | 12.04% | | | | 8.01% | | | | 3.44% | | | | 9.93% | | | | 2.05% | |

Class I Shares | | | 4/29/2005 | | | | 13.17% | | | | 9.14% | | | | 4.57% | | | | 11.05% | | | | 1.05% | |

Class Y Shares | | | 12/30/2011 | | | | 13.34% | | | | 8.97% | | | | 4.31% | | | | 10.79% | | | | 0.90% | |

BENCHMARK | | | | | | | | | | | | | | | | | | | | | | | | |

Russell 2000 Index | | | | | | | 16.35% | | | | 12.25% | | | | 3.56% | | | | 9.72% | | | | — | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | 12/29/2000 | | | | 7.24% | | | | 6.98% | | | | 3.15% | | | | 10.18% | | | | 1.30% | |

Class C Shares | | | 2/20/2001 | | | | 11.04% | | | | 8.01% | | | | 3.44% | | | | 9.93% | | | | 2.05% | |

Historical performance for Class I and Class Y shares prior to their inception is based on the performance of Class A shares. Class I and Class Y performance has been adjusted to reflect differences in sales charges.

| * | Reflects the expense ratio as reported in the Prospectus dated February 29, 2012. |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Portfolio Commentary

| | | | |

| |  | |  |

Tom Schindler, CFA

Manager | | Chris Welch, CFA

Assistant Manager | | Chris Bingaman, CFA

Assistant Manager |

The Diamond Hill Small Cap Fund returned 12.88% (Class A, without sales charge) in 2012 compared to a 16.35% return in the benchmark Russell 2000 Index. The Fund has been defensively positioned, including a double-digit average cash balance and a larger than Index weight in consumer staples, which partly explains the relative underperformance of the Fund during the year. In addition, the Fund has maintained a heavier than Index exposure to the energy sector for the better part of the past decade. While this was a contributing factor to the Fund’s outperformance from late 2003 through mid-2008, and then again in the early stages of recovery from the spring of 2009 through 2010, the energy sector was a negative factor in the Fund’s relative performance in 2011 and 2012.

The U.S. economy continued to show recovery from the late 2008 through 2009 downturn, albeit at a slower pace than is typically seen. Importantly, the Federal Reserve has continued to hold short-term rates near zero and greatly expanded its balance sheet in an attempt to ease the path of deleveraging for households

and financial institutions. When investor attention turned to the impending “fiscal cliff” following President Obama’s re-election in November, stocks declined briefly. A deal was reached to raise tax rates on high earners beginning in 2013, but the mandated across-the-board spending cuts were deferred to be debated further in 2013. Thus, while no “grand-bargain” to address the deficit issue in the U.S. has been reached and risks will continue to build as a result of this unsustainable fiscal policy, investors have quickly embraced risk again and bid stocks higher.

Turning to the energy industry, the first thing to note was the divergence of the world’s two leading light sweet crude benchmark oil prices. Brent crude, sourced in the North Sea and used throughout much of Europe, was actually up about 3.5% for the year. However, West Texas Intermediate (WTI) declined 7% for the year. Also, some areas of U.S. production faced widening differentials from the benchmark WTI price as production growth outstripped the takeaway capacity in existing pipeline infrastructure. This was generally negative for our holdings in Whiting Petroleum Corp. and Denbury Resources Inc. Natural gas prices in the U.S. generally bounced off the decade-low price reached in early 2012 as the low price for natural gas displaced some of the demand for coal during the summer. As a result, Southwestern Energy Co. was up for the year. Forest Oil

| | |

| Page 6 | | Diamond Hill Funds Annual Report December 31, 2012 |

Corp. has been a major disappointment as its acreage in the Eagle Ford project has not been nearly as productive as some others in the play, contributing to a 50% stock price decline and a management change. Finally, Berry Petroleum Co. experienced production delays in one of its major heavy oil projects. While we believe the play will still be successful, the delays do negatively impact the economic returns that had been expected. We still believe there is opportunity for these companies to generate good returns on invested capital with the current oil price environment, and we believe there is a favorable chance to have stock price gains as a result.

In industrials, we had significant positive contributions from airlines Allegiant Travel Co. and Alaska Air Group, Inc., trucking company Saia, Inc., and turf management equipment producer Toro Co. In addition, Corrections Corp. of America applied for conversion to a real estate investment trust (REIT) and is likely to receive clearance, a situation investors viewed favorably as this will allow the company to avoid federal income taxes and pass through profits to shareholders.

Our consumer discretionary holdings were all positive. Nacco Industries, Inc., Hanesbrands, Inc., Carter’s, Inc., Global Sources Ltd., and a small position in Liquidity Services, Inc. were all outperformers. A notable absence of homebuilders and housing related stocks also hurt the relative performance of the Fund. These stocks did phenomenally well in 2012 as housing showed early signs of recovery, albeit from a much lower base than pre-recessionary levels.

In financials, insurance companies continue to be the most heavily emphasized industry. Horace Mann Educators Corp. and HCC Insurance Holdings, Inc. were strong performers. Assurant, Inc. detracted from performance, down 13% for the year. Assurant continues to generate very good earnings and buy back large amounts of stock relative to its current market capitalization. However, regulators have looked for the company to reduce premium rates in its very profitable creditor placed homeowner’s insurance business. We believe earnings will be lower in the future for this business and thus Assurant’s current earnings are above a normalized level, but we still believe Assurant is worth considerably more than the six time price-to-earnings multiple investors are currently assigning. While Assured Guaranty Ltd. finished the year up about 11%, this result appeared weighed down by Moody’s announcement in March of a potential downgrade of Assured Guaranty’s underwriting subsidiary. Moody’s allowed the rest of the year to pass without making a decision. We would expect the company to aggressively buy back stock in the event of a ratings downgrade.

Thomas P. Schindler, CFA

Portfolio Manager

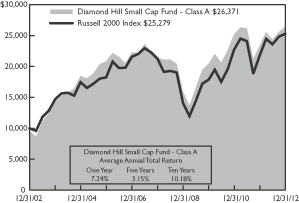

Growth of $10,000

Comparison of the change in value of a $10,000 Investment in the Diamond Hill Small Cap Fund Class A(A) and the Russell 2000 Index.

| (A) | The growth of $10,000 and total return charts represent the performance of Class A shares only, adjusted for the maximum applicable sales charge of 5.00%, which will vary from the performance of Class C, Class I and Class Y shares based on the difference in loads and fees paid by shareholders in the different classes. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 2000 Index (“Index”). The Index is a market capitalization-weighted index measuring performance of the smallest 2,000 companies, on a market capitalization basis, in the Russell 3000 Index. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 7 |

Diamond Hill Small-Mid Cap Fund

Performance Update

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Average Annual Total Returns as of December 31, 2012 | | Inception

Date | | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception

(12/30/05) | | | Expense

Ratio* | |

PERFORMANCE AT NAV without sales charges | |

Class A Shares | | | 12/30/2005 | | | | 15.43% | | | | 10.81% | | | | 6.04% | | | | 5.54% | | | | 1.25% | |

Class C Shares | | | 12/30/2005 | | | | 14.57% | | | | 10.00% | | | | 5.27% | | | | 4.79% | | | | 2.00% | |

Class I Shares | | | 12/30/2005 | | | | 15.74% | | | | 11.16% | | | | 6.40% | | | | 5.92% | | | | 1.00% | |

Class Y Shares | | | 12/30/2011 | | | | 15.84% | | | | 10.94% | | | | 6.11% | | | | 5.60% | | | | 0.85% | |

BENCHMARK | | | | | | | | | | | | | | | | | | | | | | | | |

Russell 2500 Index | | | | | | | 17.88% | | | | 13.34% | | | | 4.34% | | | | 5.52% | | | | — | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | 12/30/2005 | | | | 9.63% | | | | 8.93% | | | | 4.96% | | | | 4.77% | | | | 1.25% | |

Class C Shares | | | 12/30/2005 | | | | 13.57% | | | | 10.00% | | | | 5.27% | | | | 4.79% | | | | 2.00% | |

Historical performance for Class Y shares prior to its inception is based on the performance of Class A shares. Class Y performance has been adjusted to reflect differences in sales charges.

| * | Reflects the expense ratio as reported in the Prospectus dated February 29, 2012. |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Portfolio Commentary

| | | | |

| | | | |

Chris Welch, CFA

Manager | | Tom Schindler, CFA

Assistant Manager | | Chris Bingaman, CFA

Assistant Manager |

The Diamond Hill Small-Mid Cap Fund gained 15.43% (Class A, without sales charge) in 2012 compared to a 17.88% increase in the benchmark Russell 2500 Index. For the five-year period ending December 31, 2012, the Fund’s return was 6.04% annually while the Russell 2500 Index returned 4.34% annually over the same period. The 2012 performance trailed the benchmark largely due to poor sector allocation in energy, poor stock selection in financials, and our cash position, partially offset by favorable stock selection in some market sectors. We are pleased, however, to have outperformed the Index over the longer five-year time period.

The small-mid cap segment of the stock market continued to be a favorable place to invest not only from an absolute but also a relative basis in 2012. The Russell 2500 Index, which is widely used to measure the performance of small to mid-cap domestic stocks, outgained both the Russell 2000 Index (small cap domestic stocks) and the Russell 1000 Index (large cap domestic stocks) by more than a full percentage point this year. Over the past five years, the Russell 2500 Index has returned 4.34% annually,

compared to 3.56% annually for the Russell 2000 Index and 1.92% annually for the Russell 1000 Index.

Our returns this year benefited from favorable stock selection overall, but that was more than offset by poor sector allocation. Our positive stock selection was led by the information technology sector, where CoreLogic, Inc. was a big winner. CoreLogic more than doubled before we completely exited the position in the third quarter as it benefited from falling mortgage rates which spurred further home refinancing activity. Corrections Corp. of America was a strong performer in the industrials sector as the private prison operator rose in anticipation of tax benefits from a potential restructuring of part of its business to a real estate investment trust. A diverse array of financials sector holdings provided strong contributions to return. iStar Financial, Inc. and Popular, Inc. benefited from improved credit positions, and Hartford Financial Services Group, Inc. rose as the company announced the sale of some of its non-core lines of business.

The biggest negative from a sector allocation standpoint was our overweight position in energy stocks as energy was the worst performing sector in the market. Continued domestic oil and gas supply increases from hydraulic fracturing technology and weaker global demand for oil driven by slowdowns in Europe and China created headwinds for energy stocks. Our stockpicking within the sector partially offset the poor sector allocation, as Exterran Holdings, Inc. saw a large

| | |

| Page 8 | | Diamond Hill Funds Annual Report December 31, 2012 |

jump in value after receiving a favorable settlement for assets that had been locked in a dispute with the Venezuelan government. Our cash position also detracted from relative returns in the strong market, though we found enough opportunities to keep cash as a percent of net results in the single digit range the entire year. Our stock selection in the consumer discretionary and health care sectors trailed the benchmark. Despite owning stocks that delivered, on average, low-teens positive returns in both sectors, we trailed the 20% plus average returns of benchmark stocks in both areas.

We are very fortunate to have a strong, stable investment team serving you. We now have 15 research analysts and six research associates (“analysts-in-training”). We added three new research associates since last year’s letter, while one of our research associates left the organization for another opportunity. We have had no turnover in our equity portfolio manager or our research analyst ranks in more than a decade. Our talented and experienced research team is focused on identifying companies we can purchase for your portfolio at an attractive discount to our estimate of what the companies are worth, while always employing a long-term time horizon in our analysis.

Our 2013 outlook is similar to that of the past few years. We are still finding the best opportunities at the higher end of our market cap range. Our largest sector weights are financials (23%) and industrials (16%), and insurance stocks remain our largest focus within the financials sector due to our favorable view of the industry pricing cycle. We have reduced our energy weight to its lowest level (11%) since the inception of the Fund seven years ago, though we retain an overweight position relative to the benchmark. The steady tailwinds that supported the energy sector have weakened, but we continue to find some attractive opportunities within the sector. After the strong stock market returns of 2012, we expect positive but below-average equity returns over the next five years. In the current persistent low interest rate environment, mid-to-high single digit returns look quite attractive relative to Treasury and High Yield bonds.

We appreciate your ongoing support and look forward to continuing to work with you in the coming years.

Christopher A. Welch, CFA

Portfolio Manager

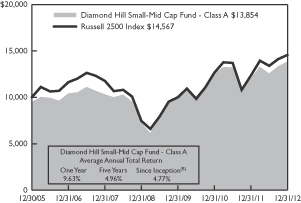

Growth of $10,000

Comparison of the change in value of a $10,000 Investment in the Diamond Hill Small-Mid Cap Fund Class A(A) and the Russell 2500 Index.

| (A) | The growth of $10,000 and total return charts represent the performance of Class A shares only, adjusted for the maximum applicable sales charge of 5.00%, which will vary from the performance of Class C, Class I and Class Y shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | Class A shares commenced operations on December 30, 2005. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 2500 Index (“Index”). The Index is a market capitalization-weighted index measuring performance of the smallest 2,500 companies, on a market capitalization basis, in the Russell 3000 Index. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 9 |

Diamond Hill Large Cap Fund

Performance Update

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Average Annual Total Returns

as of December 31, 2012 | | Inception

Date | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Expense

Ratio* | |

PERFORMANCE AT NAV without sales charges | |

Class A Shares | �� | | 6/29/2001 | | | | 12.29% | | | | 7.90% | | | | 1.52% | | | | 9.28% | | | | 1.06% | |

Class C Shares | | | 9/25/2001 | | | | 11.49% | | | | 7.08% | | | | 0.75% | | | | 8.47% | | | | 1.81% | |

Class I Shares | | | 1/31/2005 | | | | 12.62% | | | | 8.23% | | | | 1.86% | | | | 9.59% | | | | 0.81% | |

Class Y Shares | | | 12/30/2011 | | | | 12.79% | | | | 8.06% | | | | 1.61% | | | | 9.33% | | | | 0.66% | |

BENCHMARK | | | | | | | | | | | | | | | | | | | | | | | | |

Russell 1000 Index | | | | | | | 16.42% | | | | 11.12% | | | | 1.92% | | | | 7.52% | | | | — | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | 6/29/2001 | | | | 6.66% | | | | 6.06% | | | | 0.48% | | | | 8.73% | | | | 1.06% | |

Class C Shares | | | 9/25/2001 | | | | 10.49% | | | | 7.08% | | | | 0.75% | | | | 8.47% | | | | 1.81% | |

Historical performance for Class I and Class Y shares prior to their inception is based on the performance of Class A shares. Class I and Class Y performance has been adjusted to reflect differences in sales charges.

| * | Reflects the expense ratio as reported in the Prospectus dated February 29, 2012. |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Portfolio Commentary

| | | | |

| |  | | |

Chuck Bath, CFA

Manager | | Bill Dierker, CFA

Assistant Manager | | Chris Welch, CFA

Assistant Manager |

The Diamond Hill Large Cap Fund returned 12.29% (Class A, without sales charges) in 2012 compared to 16.42% for the Russell 1000 Index. The market’s returns followed a frequent pattern in recent years. Returns were strong early in the year but were mostly erased by a mid-year market sell-off as investors became concerned about a worldwide economic slowdown. The economic problems which led to these concerns were mostly attributable to the European debt crisis; however, as the problems remained primarily contained in Europe, the U.S. stock market rallied meaningfully in the second half of the year resulting in strong equity market returns in 2012.

The Fund’s relative performance was disappointing in 2012. The Fund lagged in the first quarter due to its relatively conservative positioning with a large weight in the consumer staples sector. In the second quarter, there were several stock specific issues primarily related to earnings disappointments which led to poor first six-month results. The relative performance of the Fund in the second half of the year was much improved; but it was not enough to compensate for the disappointing start to the year.

The source of the largest disappointment for the portfolio was the energy sector. Concerns regarding falling energy prices due to an economic slowdown and an unusually warm winter led to the sector performing very poorly. The exploration and production companies suffered more than most since they did not have strong refining earnings to offset disappointments surrounding rising costs and low natural gas prices. Devon Energy Corp. and Apache Corp. were two large holdings that declined more than 10% during the year as a result of these concerns. Anadarko Petroleum was another energy holding that performed poorly due primarily to concerns over environmental liabilities at a former subsidiary. The position in Anadarko was sold, in part, as a result of these concerns. Occidental Petroleum Corp. was the largest holding in the portfolio so the stock’s disappointing performance had a larger impact on the Fund. Occidental’s stock declined due to rising costs and disappointing production growth in its California properties. The management of Occidental Petroleum is addressing these issues, and we believe the company’s performance should improve.

Other than energy, all other sectors provided positive returns for 2012. The relative performance in the technology sector was disappointing as the Fund was underweight the sector, and our holdings lagged the Index. Juniper Networks, Inc. was a small holding that declined during the year due to slowing end demand from its corporate customers and a loss of market share. Microsoft Corp. increased but lagged the market due to concerns about a slowdown in its retail markets.

| | |

| Page 10 | | Diamond Hill Funds Annual Report December 31, 2012 |

One other disappointing holding was McDonald’s Corp. While the consumer discretionary sector holdings were mostly strong performers during the year, McDonald’s lagged due to a slowdown in revenue growth, particularly in Europe. We have held the shares of McDonald’s for several years, and for the most part, they have performed well. However, the shares were down just under 10% in 2012.

A couple of relatively new holdings in the consumer discretionary sector were strong contributors in 2012. Our position in Comcast Corp. and Walt Disney Co. were both up over 35% for the year as strong operating performance led to an improving earnings outlook for both companies. Mattel, Inc. was a strong performer in the first part of the year. As a result, the stock appreciated to our estimate of intrinsic value, and the shares were eliminated from the portfolio.

Our best performing sectors in 2012 were the health care and financials sectors. Amgen, Inc. and Baxter International, Inc. were both up over 38% for the year. While our Amgen position was sold as it reached intrinsic value, Baxter remained a large holding in the portfolio at year’s end. JPMorgan Chase & Co. appreciated significantly during the year despite the controversy surrounding a large trading loss in their London operation. Citigroup, Inc. was added to the portfolio late in the year, yet it was still one of the big gainers in 2012 appreciating almost 40%.

During the fourth quarter of 2012, several large financial services companies were identified as attractive investments. As a result, at year-end the financials sector was the largest weighting in the portfolio. Health care remains a large weighting, but it is under 20% of the portfolio. Energy is still a large weighting, but it was meaningfully reduced throughout the year as attractive opportunities were identified elsewhere in the market.

While I was pleased with the performance of the Diamond Hill Large Cap Fund in the second half of the year, it was unable to compensate for the poor start to the year. The Fund’s performance was disappointing as it trailed the benchmark for 2012. However, as I look back over the decade since I joined Diamond Hill, I am proud of the performance of the Fund. As I look forward to 2013, I am grateful for the opportunity to manage the Diamond Hill Large Cap Fund, and I look forward to the challenge.

Charles S. Bath, CFA

Portfolio Manager

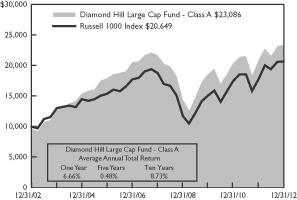

Growth of $10,000

Comparison of the change in value of a $10,000 Investment in the Diamond Hill Large Cap Fund Class A(A) and the Russell 1000 Index.

| (A) | The growth of $10,000 and total return charts represent the performance of Class A shares only, adjusted for the maximum applicable sales charge of 5.00%, which will vary from the performance of Class C, Class I and Class Y shares based on the difference in loads and fees paid by shareholders in the different classes. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 1000 Index (“Index”). The Index is a market capitalization-weighted index measuring performance of the largest 1,000 companies, on a market capitalization basis, in the Russell 3000 Index. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 11 |

Diamond Hill Select Fund

Performance Update

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Average Annual Total Returns as of December 31, 2012 | | Inception

Date | | | One Year | | | Three

Years | | | Five

Years | | | Since

Inception

(12/30/05) | | | Expense

Ratio* | |

PERFORMANCE AT NAV without sales charges | |

Class A Shares | | | 12/30/2005 | | | | 11.27% | | | | 6.33% | | | | 1.37% | | | | 3.65% | | | | 1.21% | |

Class C Shares | | | 12/30/2005 | | | | 10.44% | | | | 5.52% | | | | 0.60% | | | | 2.90% | | | | 1.96% | |

Class I Shares | | | 12/30/2005 | | | | 11.54% | | | | 6.63% | | | | 1.70% | | | | 4.00% | | | | 0.96% | |

Class Y Shares | | | 12/30/2011 | | | | 11.69% | | | | 6.46% | | | | 1.44% | | | | 3.70% | | | | 0.81% | |

BENCHMARK | | | | | | | | | | | | | | | | | | | | | | | | |

Russell 3000 Index | | | | | | | 16.42% | | | | 11.20% | | | | 2.04% | | | | 4.34% | | | | — | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | 12/30/2005 | | | | 5.71% | | | | 4.54% | | | | 0.33% | | | | 2.89% | | | | 1.21% | |

Class C Shares | | | 12/30/2005 | | | | 9.44% | | | | 5.52% | | | | 0.60% | | | | 2.90% | | | | 1.96% | |

Historical performance for Class Y shares prior to its inception is based on the performance of Class A shares. Class Y performance has been adjusted to reflect differences in sales charges.

| * | Reflects the expense ratio as reported in the Prospectus dated February 29, 2012. |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Portfolio Commentary

| | | | |

| | | | |

Bill Dierker, CFA

Manager | | Chuck Bath, CFA

Assistant Manager | | Chris Welch, CFA

Assistant Manager |

In 2012, the Diamond Hill Select Fund increased 11.27% (Class A, without sales charge) compared to our benchmark, the Russell 3000 Index, which returned 16.42%.

Our largest sector weights were in financials, health care, industrials, and consumer staples.

Most of our holdings in the financials sector increased in value. This, in combination with an overweight position in the sector, resulted in a positive contribution to absolute return. With banking industry capital at the highest level in a generation or more, we believe banks will easily meet the revised capital requirements in advance of new regulatory guidelines. This should also allow for banks to increase their balance sheet capacity and facilitate growth, in addition to returning capital to investors in the form of dividends and/or share repurchases. Key areas within the insurance industry are also well capitalized. Commercial lines insurers, in particular, continue to benefit meaningfully from increased pricing. Despite overall favorable returns for the financials sector, our individual stock selection was

poor, resulting in negative contribution relative to our benchmark. Our top contributors were JPMorgan Chase & Co., Wells Fargo & Co., Citigroup, Inc., U.S. Bancorp, Assured Guaranty Ltd., iStar Financial, Inc. and Charles Schwab Corp. JPMorgan Chase & Co. appreciated significantly during the year despite the controversy surrounding a large trading loss in its London operation. Citigroup, Inc. was added to the portfolio late in the year, yet it was still one of the big gainers in 2012 appreciating over 40%. The financials sector represented the largest sector weight in the Fund at year-end.

In the health care sector, we were overweight the sector, and our stock selection was positive. The combination of an overweight in a strong sector and solid stock selection led to the largest contribution relative to our benchmark. Our top contributors were Baxter International, Inc., Amgen, Inc., Abbott Laboratories, Pfizer, Inc. and UnitedHealth Group, Inc. Amgen, Inc. and Baxter International, Inc. were both up over 38% for the year. We sold our Amgen position as it reached intrinsic value; however, we continued to hold a significant portfolio position in Baxter at year’s end. Baxter International, Inc. provided encouraging updates regarding its new product pipeline at its annual investor day. At the end of the year, the health care sector was our second largest sector weight.

| | |

| Page 12 | | Diamond Hill Funds Annual Report December 31, 2012 |

Lower energy prices created headwinds for energy stocks. Domestic oil and gas supplies continued to increase as a result of hydraulic fracturing technology and an unusually warm winter. Weaker global demand, driven by slowdowns in Europe and China also created pressure on oil prices. The exploration and production companies suffered more than most since they did not have strong refining earnings to offset disappointments surrounding rising costs and low natural gas prices. The energy sector was the largest detractor from our performance relative to our benchmark due to a combination of an overweight in the sector and poor stock selection. Please note that “poor stock selection” does not mean that we have lost confidence in our holdings.

Other holdings that contributed to our performance included Southwest Airlines Co. and ConAgra Foods, Inc. Southwest Airlines Co. has benefited from strong domestic air travel demand and lower jet fuel prices. In addition, a strong balance sheet and free cash flow has allowed the company to aggressively repurchase its own shares. ConAgra has been able to improve its growth rate through acquisitions, with the largest being the pending purchase of Ralcorp Holdings, Inc. The company has also been successful in passing along rising commodity costs to consumers.

I appreciate your ongoing support and look forward to 2013.

William C. Dierker, CFA

Portfolio Manager

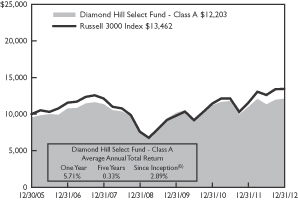

Growth of $10,000

Comparison of the change in value of a $10,000 Investment in the Diamond Hill Select Fund Class A(A) and the Russell 3000 Index.

| (A) | The growth of $10,000 and total return charts represent the performance of Class A shares only, adjusted for the maximum applicable sales charge of 5.00%, which will vary from the performance of Class C, Class I and Class Y shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | Class A shares commenced operations on December 30, 2005. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 3000 Index (“Index”). The Index is a widely recognized market capitalization-weighted index measuring the performance of the 3,000 largest U.S. companies based on total market capitalization. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 13 |

Diamond Hill Long-Short Fund

Performance Update

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Average Annual Total Returns as of December 31, 2012 | | Inception

Date | | | One Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Expense

Ratio* | |

PERFORMANCE AT NAV without sales charges | |

Class A Shares | | | 6/30/2000 | | | | 8.46% | | | | 3.66% | | | | 0.06% | | | | 7.75% | | | | 1.64% | |

Class C Shares | | | 2/13/2001 | | | | 7.70% | | | | 2.90% | | | | -0.70% | | | | 6.94% | | | | 2.39% | |

Class I Shares | | | 1/31/2005 | | | | 8.77% | | | | 3.97% | | | | 0.39% | | | | 8.06% | | | | 1.39% | |

Class Y Shares | | | 12/30/2011 | | | | 8.95% | | | | 3.82% | | | | 0.15% | | | | 7.80% | | | | 1.24% | |

BENCHMARK | | | | | | | | | | | | | | | | | | | | | | | | |

Russell 1000 Index | | | | | | | 16.42% | | | | 11.12% | | | | 1.92% | | | | 7.52% | | | | — | |

50% Russell 1000 Index/50% BofA ML US T-Bill 0-3 Mo. Index | | | | | | | 8.11% | | | | 5.78% | | | | 1.66% | | | | 4.87% | | | | — | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | 6/30/2000 | | | | 3.04% | | | | 1.90% | | | | -0.96% | | | | 7.20% | | | | 1.64% | |

Class C Shares | | | 2/13/2001 | | | | 6.70% | | | | 2.90% | | | | -0.70% | | | | 6.94% | | | | 2.39% | |

Historical performance for Class I and Class Y shares prior to their inception is based on the performance of Class A shares. Class I and Class Y performance has been adjusted to reflect differences in sales charges.

| * | Reflects the expense ratio as reported in the Prospectus dated February 29, 2012. |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Portfolio Commentary

| | | | |

| |  | | |

Chuck Bath, CFA

Co-Manager | | Ric Dillon, CFA

Co-Manager | | Chris Bingaman, CFA

Assistant Manager |

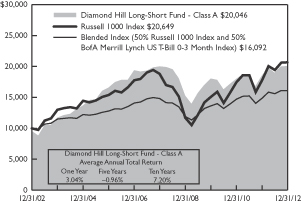

The Diamond Hill Long-Short Fund returned 8.46% (Class A, without sales charge) in 2012 compared to a 16.42% return for the long-only Russell 1000 Index and an 8.11% return for the blended benchmark (50% Russell 1000 Index/50% BofA Merrill Lynch U.S. T-Bill 0-3 Month Index).

While it was difficult for the Long-Short Fund to keep up with the long-only benchmark in a year of strong equity market returns, we were pleased to outperform the blended benchmark for the year. This was mostly due to good asset allocation. While the performance of our long portfolio was disappointing, we were helped by the larger than normal allocation to the long portfolio in a strong market year. While we target a 50% net long exposure as normal for the Fund, we have maintained a much larger net long exposure due to the attractive valuations we were able to find in the market. This was beneficial to the portfolio as it caused us to add to attractively valued long positions while trimming the short portfolio.

The source of the largest disappointment in the long portfolio was in the energy sector. Concerns regarding falling energy prices due to an economic slowdown and an unusually warm winter led to the sector performing very poorly. The exploration and production companies suffered more than most since they did not have strong refining earnings to offset disappointments surrounding rising costs and low natural gas prices. Devon Energy Corp. and Apache Corp. were two large holdings that declined more than 10% during the year as a result of these concerns. Anadarko Petroleum was another energy holding that performed poorly due primarily to concerns over environmental liabilities at a former subsidiary. The position in Anadarko was sold, in part, as a result of these concerns. Occidental Petroleum Corp. was the largest energy holding in the portfolio so the stock’s disappointing performance had a larger impact on the Fund. Occidental’s stock declined due to rising costs and disappointing production growth in its California properties. The management of Occidental Petroleum is addressing these issues, and we believe the company’s performance should improve.

One other disappointing holding in the long portfolio was McDonald’s Corp. While the consumer discretionary sector holdings were mostly strong performers during the year, McDonald’s lagged due to a slowdown in revenue growth, particularly in Europe. We

| | |

| Page 14 | | Diamond Hill Funds Annual Report December 31, 2012 |

have held the shares of McDonald’s for several years, and for the most part, they have performed well. However, the shares are down just under 10% in 2012.

A couple of new long holdings in the consumer discretionary sector were strong contributors in 2012. Our position in Comcast Corp. and Walt Disney Co. were both up over 35% for the year as strong operating performance led to an improving earnings outlook for both companies. Mattel Inc. was a strong performer in the first part of the year. As a result, the stock appreciated to our estimate of intrinsic value, and the shares were eliminated from the portfolio.

The short portfolio detracted from the total Fund return in 2012. This is typical of strong equity market years as our shorts appreciated with the market. Fortunately, our short positions were up less than the broader market. The biggest positive contributor to the short portfolio was Apollo Group, Inc. as the shares declined just under 20%. A similar decline by J.C. Penney Co., Inc. allowed that security to be a positive contributor to the performance as well. However, some large gainers in the short portfolio hurt the Fund’s returns. Brunswick Corp. was up over 60% in 2012. This has been a successful short holding in past years in the portfolio; but unfortunately, it hurt us in 2012. Short positions in retailers such as Macy’s, Inc, and Tractor Supply Co. were also negative contributors to the portfolio returns. As of year-end, Macy’s, Brunswick, and Tractor Supply Co. remained short positions in the Fund.

While the portfolio trailed the long-only Russell 1000 Index in 2012, we were pleased to exceed the blended benchmark, which is more aligned with the 50% net long bias of the portfolio.

The year 2012 marked an anniversary for the Diamond Hill Long-Short Fund. It was 10 years ago in June, 2002 that the shorting strategy was added to the Fund. Many of our shareholders have been with us for several of those years, and we wish to express our gratitude for your support and look forward to continuing to earn your trust in 2013.

| | |

| |

|

Charles S. Bath, CFA Co-Portfolio Manager | | R.H. Dillon, CFA Co-Portfolio Manager |

Growth of $10,000

Comparison of the change in value of a $10,000 Investment in the Diamond Hill Long-Short Fund Class A(A), the Russell 1000 Index and the Blended Index (50% Russell 1000 Index and 50% BofA Merrill Lynch US T-Bill 0-3 Month Index)

| (A) | The growth of $10,000 and total return charts represent the performance of Class A shares only, adjusted for the maximum applicable sales charge of 5.00%, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 1000 Index and the blended index. The Russell 1000 Index is a market capitalization-weighted index measuring performance of the largest 1,000 companies on a market capitalization basis, in the Russell 3000 Index. The blended index represents a 50% weighting of the Russell 1000 Index as described above and a 50% weighting of the BofA Merrill Lynch US T-Bill 0-3 Month Index. The BofA Merrill Lynch US T-Bill 0-3 Month Index tracks the performance of US dollar denominated US Treasury Bills publicly issued in the US domestic market with a remaining term to final maturity of less than 3 months. Both indices are unmanaged, and do not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 15 |

Diamond Hill Research Opportunities Fund

Performance Update

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Average Annual Total Returns

as of December 31, 2012 | | Inception

Date* | | | One

Year | | | Three

Years | | | Since

Inception

(3/31/09)* | | | Expense

Ratio** | |

PERFORMANCE AT NAV without sales charges | |

Class A Shares | | | 12/30/2011 | | | | 11.73% | | | | 8.09% | | | | 16.59% | | | | 1.52% | |

Class C Shares | | | 12/30/2011 | | | | 10.91% | | | | 7.29% | | | | 15.72% | | | | 2.27% | |

Class I Shares | | | 12/30/2011 | | | | 12.03% | | | | 8.38% | | | | 16.90% | | | | 1.27% | |

Class Y Shares | | | 12/30/2011 | | | | 12.17% | | | | 8.53% | | | | 17.06% | | | | 1.12% | |

BENCHMARK | | | | | | | | | | | | | | | | | | | | |

Russell 3000 Index | | | | | | | 16.42% | | | | 11.20% | | | | 19.96% | | | | — | |

PERFORMANCE AT POP includes sales charges | |

Class A Shares | | | 12/30/2011 | | | | 6.16% | | | | 6.26% | | | | 14.99% | | | | 1.52% | |

Class C Shares | | | 12/30/2011 | | | | 9.91% | | | | 7.29% | | | | 15.72% | | | | 2.27% | |

| * | The quoted performance for the Fund reflects the past performance of Diamond Hill Research Partners, L.P., a private fund managed with full investment authority by the Fund’s Adviser. The Fund is managed in all material respects in a manner equivalent to the management of the predecessor unregistered fund. The Fund’s objectives, policies, guidelines and restrictions are in all material respects equivalent to the predecessor, and the Fund was created for reasons entirely unrelated to the establishment of a performance record. The assets of the Research Partnership were converted into assets of the Fund prior to commencement of operation of the Fund. The Fund’s inception date is December 30, 2011. The performance of the Research Partnership has been restated to reflect the net expenses and maximum applicable sales charge of the Fund for its initial years of investment operations. The Research Partnership was not registered under the Investment Company Act of 1940 and therefore was not subject to certain investment restrictions imposed by the 1940 Act. If the Research Partnership had been registered under the 1940 Act, its performance may have been adversely affected. Performance is measured from March 31, 2009, the inception of the Research Partnership and is not the performance of the Fund. The Research Partnership’s past performance is not necessarily an indication of how the Fund will perform in the future either before or after taxes. |

| ** | Reflects the expense ratio as reported in the Prospectus dated February 29, 2012. |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Portfolio Commentary

The Diamond Hill Research Opportunities Fund increased 11.73% (Class A, without sales charge) in 2012 compared to a 16.42% increase in the benchmark Russell 3000 Index. We were pleased with the absolute performance of the Fund in 2012, but disappointed with the relative performance. It is not necessarily surprising that a long-short fund would underperform in such a strong market, but the magnitude was disappointing. The primary sources of the relative underperformance were our large cash position and the underperformance of the long portfolio. On a positive note, our short portfolio only modestly impacted performance as our short exposure was low relative to the portfolio’s history and our short positions increased in price less than the Russell 3000 Index.

Net exposure averaged 76.5% during the year, which created an average cash balance of 23.5%. We do not target a net exposure; rather it is the result of the opportunities analysts are finding on the long and short

side. One of the key features of the Fund is its flexibility, which allows net exposure to vary from 0% to 100%. This flexibility allows analysts to be opportunistic within their industries. Though it has been a drag on performance to date, our cash position enables us to take advantage of opportunities as they present themselves and should positively contribute to performance over time. We define risk as a permanent impairment of capital, and we will only deploy capital, long or short, when we view the expected return as attractive with a low probability of a permanent impairment. Until then, we remain content to be patient and wait for the fat pitch.

The other drag on relative performance was the long portfolio, which trailed the Russell 3000 Index. In prior years, our stock selection has been strong enough for long positions to meaningfully outperform the Index and largely offset the negative contribution from cash. Unfortunately, that was not the case during 2012. Strong absolute and relative returns in the financials and industrials sectors were offset by poor relative returns from the consumer discretionary and health care sectors.

| | |

| Page 16 | | Diamond Hill Funds Annual Report December 31, 2012 |

The largest positive contributors to performance were long positions in iStar Financial, Inc. and Saia, Inc. iStar materially repositioned its liability structure, which lowered funding costs and alleviated concerns regarding the company’s ability to meet near-term debt maturities. The company is also beginning to reap the benefits of capital allocation decisions made by management throughout the credit crisis. These decisions included buying back significant amounts of stock at large discounts to book value and repurchasing debt at material discounts to par. Saia benefited from strong pricing in the less-than-truckload industry as well as company-specific yield and cost initiatives. Management’s focus on yield rather than tonnage paid off as strong margin improvement led to a dramatic increase in earnings during the year. Other strong positive contributors in the long portfolio included Popular, Inc., Hartford Financial Services Group, Inc., Apple, Inc., Corrections Corp. of America, and Southwest Airlines Co.

There were a few major detractors to performance during the year. Alere, Inc. suffered from margin pressure due to lower production yields as the result of an FDA recall of its toxicology products. However, there were positive developments supporting our thesis as management indicated that merger and acquisition activity is behind them, which should allow management to focus on improving returns through internal measures such as cost optimization and portfolio pruning. Within the consumer discretionary sector, the largest detractors were Groupon, Inc. and Tempur-Pedic International, Inc. Competitive pressures and fundamental performance called our original theses into question, and we lowered our estimates of intrinsic value and exited both positions.

The largest positive contributors from the short side of the portfolio were Apollo Group, Inc. and Nokia Corp. Apollo’s results early in the year exhibited our anticipated decline in student enrollments and revenue per student, which created margin pressure for the company. Nokia reported weak results and market share losses during the year, which supported our thesis of a long-term secular decline in the company’s fundamentals. Share prices converged with our estimates of intrinsic value, and we covered both positions. The largest detractor in the short portfolio was Akamai Technologies, Inc., our largest short position. The company reported solid revenue growth and moderate margin recovery throughout the year. In addition, shares responded favorably to the announcement that AT&T will begin reselling Akamai’s CDN services to enterprise customers. Despite these developments, we believe our thesis of slower growth and increased competition remains intact.

Our goal remains to generate strong absolute and relative returns over rolling five-year periods. To accomplish this goal, we remain disciplined with our deployment of capital, which may result in underperformance during periods of time when the market rallies and valuations become stretched. We want to thank shareholders for their support and look forward to working with you in the years ahead.

Diamond Hill Research Analysts

Growth of $10,000

Comparison of the change in value of a $10,000 Investment in the Diamond Hill Research Opportunities Fund Class A(A) and the Russell 3000 Index.

| (A) | The growth of $10,000 and total return charts represent the performance of Class A shares only, adjusted for the maximum applicable sales charge of 5.00%, which will vary from the performance of Class C, Class I and Class Y shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | Class A shares commenced operations on January 3, 2012. The quoted performance for the Fund reflects the past performance of Diamond Hill Research Partners, L.P., a private fund managed with full investment authority by the Fund’s Adviser. The Fund is managed in all material respects in a manner equivalent to the management of the predecessor unregistered fund. The Fund’s objectives, policies, guidelines and restrictions are in all material respects equivalent to the predecessor, and the Fund was created for reasons entirely unrelated to the establishment of a performance record. The assets of the Research Partnership were converted into assets of the Fund prior to commencement of operation of the Fund. The performance of the Research Partnership has been restated to reflect the net expenses and maximum applicable sales charge of the Fund for its initial years of investment operations. The Research Partnership was not registered under the Investment Company Act of 1940 and therefore was not subject to certain investment restrictions imposed by the 1940 Act. If the Research Partnership had been registered under the 1940 Act, its performance may have been adversely affected. Performance is measured from March 31, 2009, the inception of the Research Partnership and is not the performance of the Fund. The Research Partnership’s past performance is not necessarily and indication of how the Fund will perform in the future either before or after taxes. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 3000 Index (“Index”). The Index is a widely recognized market capitalization-weighted index measuring the performance of the 3,000 largest U.S. companies based on total market capitalization. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

| | |

| Diamond Hill Funds Annual Report December 31, 2012 | | Page 17 |

Diamond Hill Financial Long-Short Fund

Performance Update

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

Average Annual Total Returns as of December 31, 2012 | | Inception

Date | | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Expense

Ratio* | |

PERFORMANCE AT NAV without sales charges | | | | | | | | | | | | | | | | | | | | | | | | |

Class A Shares | | | 8/1/1997 | | | | 26.62% | | | | 8.59% | | | | -2.55% | | | | 3.48% | | | | 1.64% | |

Class C Shares | | | 6/3/1999 | | | | 25.60% | | | | 7.79% | | | | -3.31% | | | | 2.69% | | | | 2.39% | |

Class I Shares | | | 12/31/2006 | | | | 26.94% | | | | 8.92% | | | | -2.21% | | | | 3.71% | | | | 1.39% | |