United States

Securities And Exchange Commission

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-8061

Diamond Hill Funds

(Exact name of registrant as specified in charter)

325 John H. McConnell Boulevard, Suite 200, Columbus, Ohio 43215

(Address of principal executive offices) (Zip code)

James F. Laird, Jr., 325 John H. McConnell Boulevard, Suite 200, Columbus, Ohio 43215

(Name and address of agent for service)

Registrant's telephone number, including area code: (614) 255-3333

Date of fiscal year end: 12/31

Date of reporting period: 12/31/09

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| | | |

Table of Contents |

| Letter to Shareholders | 1 |

| Mission Statement, Pledge, and Fundamental Principles | 4 |

| Special Investment Letter | 7 |

| Management Discussion of Fund Performance | |

| | Diamond Hill Small Cap Fund | 10 |

| | Diamond Hill Small-Mid Cap Fund | 13 |

| | Diamond Hill Large Cap Fund | 16 |

| | Diamond Hill Select Fund | 19 |

| | Diamond Hill Long-Short Fund | 22 |

| | Diamond Hill Financial Long-Short Fund | 25 |

| | Diamond Hill Strategic Income Fund | 28 |

| Financial Statements | |

| | Schedules of Investments | 31 |

| | Statements of Assets & Liabilities | 42 |

| | Statements of Operations | 44 |

| | Statements of Changes in Net Assets | 45 |

| | Schedule of Capital Share Transactions | 47 |

| | Financial Highlights | 49 |

| | Notes to Financial Statements | 56 |

| Report of Independent Registered Public Accounting Firm | 63 |

| Other Items | 64 |

| Schedule of Shareholder Expenses | 65 |

| Management of the Trust | 66 |

| Notice of Privacy Policy | 67 |

CAUTIONARY STATEMENT

At Diamond Hill, we pledge that, “we will communicate with our clients about our investment performance in a manner that will allow them to properly assess whether we are deserving of their trust.” Our views and opinions regarding the investment prospects of our portfolio holdings and Funds are “forward looking statements” which may or may not be accurate over the long term. While we believe we have a reasonable basis for our opinions, actual results may differ materially from those we anticipate. Information provided in this report should not be considered a recommendation to purchase or sell any particular security.

You can identify forward looking statements by words like “believe,” “expect,” “anticipate,” or similar expressions when discussing prospects for particular portfolio holdings and/or one of the Funds. We cannot assure future results. You should not place undue reliance on forward-looking statements, which speak only as of the date of this report. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. This material is not authorized for distribution to prospective investors unless preceded or accompanied by a Prospectus. Please read the Prospectus carefully for a discussion of fees, expenses, and risks. Current performance may be lower or higher than that quoted herein. You may obtain a current copy of the Prospectus or more current performance information by calling 1-888-226-5595 or at Diamond Hill’s website (www.diamond-hill.com).

Letter to Shareholders

Dear Fellow Shareholders:

We are pleased to provide you with this year-end update for the Diamond Hill Funds. Our long-term focus has not changed. We continue to follow a proven intrinsic value methodology focused on absolute returns. We seek investment opportunities where the price-to-intrinsic value relationship provides an opportunity to earn an attractive rate of return over a five year period, while also providing a margin of safety.

Financial Markets

“Unprecedented” is the most frequently used word to describe what happened in the financial markets in 2009. After declining over 55% from the October 2007 peak, equity markets staged a remarkable recovery. The S&P 500 Index increased more than 60% from its March 2009 low, closing the year up 26.5%. The Russell 1000 and Russell 2000 Indexes increased 28.43% and 27.17%, respectively. With the possible exception of technology stocks around the turn of the century, this volatility in the broad stock market was unprecedented at least since the 1930s. The coordinated rescue effort by governments around the world to avert a global financial crisis was unprecedented, as was the level of U.S. fiscal and monetary stimulus enacted in 2009.

The year began with a brief rally in January, as investors reacted positively to new policy initiatives and support for the ailing financial sector. However, the markets soon reflected pessimism that the policy changes would be insufficient and recognition that financial sector risk remained high. In addition, corporate earnings reports were not only worse than expected, but also the quality was low and guidance for 2009 earnings fell dramatically. Consumer confidence readings were at the lowest recorded levels for the third consecutive month in February.

Initially driven by positive comments from financial giants Bank of America and JP Morgan Chase and from short covering, the market staged a second more significant rally in early March that would continue through most of the year. In April, economic data began to indicate a broad bottoming, with some significant improvement in key economic indicators, and 2009 first quarter earnings reports were better than expected, providing further fuel for the rally. Earnings continued to come in better than expected through the rest of the year, but primarily on the back of cost cutting, rather than revenue growth. Economic news was mixed in the third and fourth quarters. In October, the unemployment rate reached 10.2%, the highest level since 1983. Despite continued high levels of unemployment, the Conference Board of Consumer Confidence Index improved in December and retail sales posted their fourth consecutive monthly increase.

A key feature of the 2008/09 equity market decline was the indiscriminate selling of both high and low quality stocks. In contrast, the rally that began in March 2009 was initially driven by P/E multiple expansion in low quality stocks. Valuation dispersions were below normalized levels; implying investors could buy higher quality, stable companies with low earnings risk, strong franchises, dividend security, and a strong balance sheet at similar valuations as lower quality and more cyclical stocks. However, in November, we began to see a change in market leadership. Higher quality companies performed well, with the information technology and financial sectors losing some of their leadership. Valuation differences between high and low quality companies remain narrow, indicating the best value may still be in the higher quality companies.

We were very pleased with the absolute and relative performance of our equity funds for periods ended December 31, 2009. Not only did all equity funds post strong positive results in 2009, but they also outperformed their respective benchmarks. More importantly, Diamond Hill’s Small Cap, Large Cap, Long-Short and Financial Long-Short Funds all exceeded their respective benchmark1 returns over a five-year time period. Our Small-Mid Cap and Select Funds, which have been in existence for less than five years, have outperformed their benchmarks since inception. We remain focused on long-term performance and committed to our investment philosophy, which is rooted in the belief that market price and intrinsic value tend to converge over a reasonable period of time.

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 1 |

Portfolio Risk Management

Our job at Diamond Hill is to manage whatever set of risks the market presents, while seeking to achieve superior returns on an absolute basis over five year periods. During the 2007 – 2009 period of volatility, the market presented both risks and opportunities. We believe we successfully managed our portfolio risks by aggressively reevaluating our assumptions regarding the appropriate discount rate, or required rate of return, for each of our holdings and paying close attention to business and balance sheet risks. Importantly, our portfolio diversification limits are stated in absolute terms rather than relative to any benchmark, which is another form of risk control employed across all strategies. At the same time, we are not afraid to take advantage of especially attractive market opportunities created by investors mistaking short-term market volatility for true investment risk. The former is driven by emotion and in some cases has little relation to the underlying value of a company. For more details on this subject, see the Special Investment Letter “Managing Risk and What We Learned from the Crisis,” by Chris Welch, CFA, Portfolio Manager, on page 7 of this report.

Market Outlook

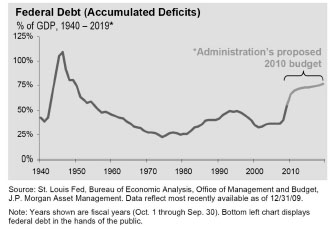

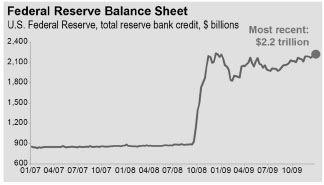

For now, the markets continue to benefit from fiscal and monetary stimulus. However, the cost associated with massive deficit spending and maintaining interest rates near zero for an extended period of time will present future challenges. We believe that over the next five years, the impact from the removal of fiscal and monetary stimulus currently supporting the economy is likely to be significant. The potential for a government pullback on spending programs, along with a rise in inflation and/or real interest rates due to the explosion in government borrowing could be problematic for the economy, as well as for the markets.

Significant Fiscal Stimulus…

… and Significant Monetary Stimulus

| | |

| Page 2 | Diamond Hill Funds Annual Report December 31, 2009 |

Given the market environment and rapid market appreciation, our expectation is for below average equity returns over the next five years. In the credit markets, the rebound in corporate profitability, higher net equity issuance and lower net debt issuance has led to an improvement in corporate credit quality. However, much of this improvement is already reflected in the prices of corporate bonds through the rapid tightening of credit spreads. On the margin, we have continued to add to more defensive sectors like consumer staples and healthcare, where we are finding attractive valuation opportunities. We continue to emphasize multi-national companies with strong brand franchises and worldwide competitive advantages. Our long-term secular thesis for energy remains intact, due to the continued tight conditions in worldwide supply and demand for oil.

As in the past, we will take advantage of opportunities that show disproportionate reward relative to the level of risk. We remain committed to our disciplined, intrinsic value investment philosophy, and we believe our approach to portfolio risk management will serve our clients well, regardless of the market environment.

| | Diamond Hill Capital Management, Inc.

R.H. Dillon, CFA Chief Investment Officer |

| | |

| | |

The views expressed are those of the portfolio manager as of December 31, 2009, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. All data referenced are from sources deemed to be reliable but cannot be guaranteed. Securities and sectors referenced should not be construed as a solicitation or recommendation or be used as the sole basis for any investment decision.

| 1 | The referenced benchmark for the Long-Short Fund is the blended index, 50% Russell 1000 Index and 50% 3month T-bill. |

The S&P 500 Index is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. Standard and Poor’s selects the companies for the index to widely represent the stock market based on market size, liquidity, and industry group representation. Indexes are unmanaged, do not incur fees, and cannot be invested in directly.

The Russell 1000 Index measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000 represents approximately 90% of the U.S. market.

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 8% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership.

Investors should consider the investment objectives, risks, and charges and expenses of the Diamond Hill Funds carefully before investing. This and other information about the Funds is in the prospectus, which can be obtained at www.diamond-hill.com. Read the prospectus carefully before you invest. Diamond Hill Capital Management, Inc., a registered investment adviser, serves as Investment Adviser to the Diamond Hill Funds and is paid a fee for its services. The Diamond Hill Funds are distributed by BHIL Distributors, Inc. (Member FINRA), an affiliated company. Investors may obtain a copy of the current prospectus at 888-226-5595 or www.diamond-hill.com. Like all mutual funds, Diamond Hill Funds are not FDIC insured, may lose value, and have no bank guarantee.

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 3 |

Mission Statement, Pledge

and Fundamental Principles

| Mission | The mission of Diamond Hill is to serve our clients through a disciplined intrinsic value-based approach to investing, while maintaining a long-term perspective, and aligning our interests with those of our clients. |

| | |

| | To successfully pursue our mission, we are: |

| | |

| | COMMITTED to the Graham-Buffett investment philosophy, with goals (over 5-year rolling periods) to outperform benchmarks and our peers, and achieve absolute returns sufficient for risk of asset class. DRIVEN by our conviction to create lasting value for clients and shareholders. MOTIVATED through ownership of Diamond Hill funds and company stock. |

| | |

Investment Philosophy | At Diamond Hill, the investment philosophy, which is rooted in the teachings of Benjamin Graham and the methods of Warren Buffett, drives the investment process — not the opposite. Most simply, we invest in a company when its market price is at a discount to our appraisal of the intrinsic value of the business (or at a premium for short positions). There are four guiding principles to our investment philosophy: ♦ Treat every investment as a partial ownership interest in that company ♦ Always invest with a margin of safety to ensure the protection of capital, as well as return on capital ♦ Possess a long-term investment temperament ♦ Recognize that market price and intrinsic value tend to converge over a reasonable period of time |

| | “Investment is most intelligent when it is most businesslike.” — BENJAMIN GRAHAM |

| Pledge | Consistent with our mission & investment philosophy, we pledge the following to all of our clients: |

| | |

| | Our investment discipline is to assess the economics of the underlying business, its management, and the price that must be paid to own a piece of it. We seek to concentrate our investments in businesses that are available at prices below intrinsic value (above intrinsic value for short positions) and are managed or controlled by trustworthy and capable people. Benjamin Graham pioneered this discipline during the 1930s and many others have practiced it with great success ever since, most notably Warren Buffett. We will communicate with our clients about our investment performance in a manner that will allow them to properly assess whether we are deserving of their trust. Our investment team will be comprised of people with integrity, sound experience and education, in combination with a strong work ethic and independence of thought. Especially important is that each possesses the highest level of character, business ethics and professionalism. |

| | |

| Page 4 | Diamond Hill Funds Annual Report December 31, 2009 |

| | Our employees will enjoy a working environment that supports professional and personal growth, thereby enhancing employee satisfaction, the productivity of the firm and the experience of our clients. “Invest With Us” means we will invest the capital you entrust to us with the same care that we invest our own capital. To this end, Diamond Hill employees and affiliates are significant investors in the same portfolios in which our clients invest and are collectively the largest shareholders in the Diamond Hill Funds. In addition, all Diamond Hill employees are subject to a Code of Ethics, which states that all personal investments must be made in a Diamond Hill fund, unless approved by our Chief Compliance Officer. |

| | |

Our

fundamental

investment

principles | Valuation Every share of stock has an intrinsic value that is independent of its current stock market price. At any point in time, the stock market price may be either higher or lower than intrinsic value. |

| | |

| | Over short periods of time, as evidenced by extreme stock market volatility, the stock market price is heavily influenced by the emotions of market participants, which are far more difficult to predict than intrinsic value. While stock market prices may experience extreme fluctuations on a particular day, we believe intrinsic value is far less volatile. Over sufficiently long periods of time, five years and longer, the stock market price tends to converge with intrinsic value. Calculating Intrinsic Value Estimate We believe that we can determine a reasonable approximation of that intrinsic value in some cases. That value can be determined if we have a reasonable basis for projecting the future cash flows of a business and use an appropriate discount rate. In estimating intrinsic value, we use an interdisciplinary approach. Not only do we perform financial modeling including discounted cash flow, private market value, and leveraged buyout analyses, we draw from other areas we believe are relevant to our investment decision-making. These include economics, statistics and probability theory, politics, psychology, and consumer behavior. In short, we do not want to exclude from our thinking anything that can help us forecast future cash flows, our most important as well as most difficult job. The Diamond Hill investment process continually compares market price to our estimate of intrinsic value, which is updated over time as new information arises. Suitable Investments We only invest in a business when the stock market price is lower than our conservative assessment of per share intrinsic value (or higher than our assessment of per share intrinsic value for short positions). We concentrate our investments in businesses whose per share intrinsic value is likely to grow. To achieve this, we assess the underlying economics of the businesses in which we invest and the industries and markets in which they participate. We seek to invest in businesses that possess a competitive advantage and significant growth prospects as well as outstanding managers and employees. |

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 5 |

| | Every business in which we invest is “handicapped” by its price. While we would prefer to own only great businesses with superior managers, there are very few businesses that satisfy those criteria and additionally are available at attractive prices. As a result, we may invest in less attractive businesses at more than attractive prices. Depending on the price that we pay, our returns from less than ideal businesses may be even better than our returns from ideal businesses. Risk & Return We intend to achieve our return from both the closing of the gap between our purchase price and intrinsic value and the growth in per share intrinsic value. For short positions, a growing intrinsic value may shorten the holding period. We define risk as the permanent loss of capital. We manage risk by investing in companies selling at a discount (premium) to our estimate of intrinsic value, with a full understanding of the fundamental drivers of intrinsic value. In addition, we carefully consider business risks that could impact our estimate of intrinsic value. We regularly monitor and update our estimate of intrinsic value, adjusting for new information. If we are successful in accurately assessing intrinsic value, we will minimize the risk of loss and increase the return potential. |

| | |

Our

fundamental

strategic

income

principles | Yield Our primary goal is to generate a yield greater than the current rate of inflation without bearing undue credit or interest rate risk. However, we cannot guarantee any specific yield. Approach A flexible approach allows us to invest in both investment grade and non-investment grade corporate bonds as well as in preferred securities, real estate investment trusts, master limited partnerships, and closed end funds. |

| | |

| | We can also invest in securities issued by the U.S. government and its agencies when conditions warrant. Total Return We balance our income objective with a focus on total return. Over the next five years, our objective is to earn equity-like returns in the income markets with lower year-to-year volatility and more importantly, a much lower risk of permanent loss of capital. |

| | |

| | “You simply have to behave according to what is rational than according to what is fashionable.” — WARREN BUFFETT |

| | |

| Page 6 | Diamond Hill Funds Annual Report December 31, 2009 |

Special Investment Letter –

Managing Risk and What We Learned from the Crisis

With the possible exception of technology stocks around the turn of the century, the volatility we have seen in the broad stock market, and particularly in financial stocks, is unprecedented since at least the 1930s. The S&P 500 Index lost over 55% of its value from the October 2007 peak to the March 2009 trough. Over the same period, the S&P 500 Financials Index lost more than 80% of its value. Both indexes have rallied sharply from the market trough, with the broad S&P 500 Index up more than 60% from the bottom and the Financials Index gaining over 130% through December 31, 2009. These recoveries leave the indexes well short of their prior peaks, however. The S&P 500 Index would need to see an additional 40%+ gain to reach its former peak, while the S&P Financials Index would need to gain more than 160% to achieve new highs.

Our job at Diamond Hill is to manage whatever set of risks the market presents, while seeking to achieve superior returns on an absolute and relative basis over five year or longer time periods. The rest of this piece will discuss two of the most significant ways in which we attempted to manage recent market risks and opportunities, as well as some of the things we observed and learned through the downturn.

Discount Rate

An important part of the valuation process for stocks is setting the proper discount rate, or required rate of return, for each individual company. The value of any company is the sum of the discounted future cash flows. Forecasting the cash flows is the activity that generally receives the greatest attention, but the use of the proper discount rate is also a key piece of the puzzle. The discount rate represents the riskiness of the forecasted cash flows – higher risk activities require higher returns to justify an investment. Thus, the discount rate applied to the cash flows of Procter & Gamble Co. (PG) or McDonalds Corp. (MCD) should be much lower than the discount rate used for an investment in a small airline or mining company.

A company’s balance sheet is also a factor in determining the appropriate discount rate for future cash flows. A firm with high levels of cash and no debt deserves a lower discount rate, all things equal, than one in the same business with roughly the same scale but having a balance sheet with high debt levels and little cash. The latter firm may be able to meet their debt payments under most economic scenarios. However, in a sharp downturn, the lack of cash flow necessary to cover debt payments may force the company to sell off assets at a low price or issue new equity at low prices to raise funds to meet debt payments. In either case, existing investors’ equity ownership is diluted. The main point is that a weaker balance sheet, all things equal, raises the riskiness of future expected cash streams.

How did this impact Diamond Hill strategies during the recent downturn? We have always recognized the importance of setting appropriate discount rates and have always differentiated between companies with stronger and weaker balance sheets. We also focus on the longer-term risks of a business model. By focusing long-term, we avoid placing an artificially low discount rate on a cyclical business that may be achieving unsustainable near-term peak operating results. However, in this downturn we discovered that for some of our holdings, what we had considered to be conservative discount rates were not conservative enough to fully reflect the risk of dilutive capital raises and other balance sheet related moves, which reduced the future expected gains to equity holders. Some of this dilutive effect was centered on banks and other financial holdings, but it also extended to industrials, technology and several other areas of the market where the sharp downturn forced value-diluting actions in order to protect companies’ viability. After experiencing such effects for a few of our holdings, we aggressively scoured the rest of our portfolios to make sure that we were fully incorporating appropriate discount rates for all our investments. In limited cases, we adjusted our discount rates. This adjustment did not necessarily lead to a change in our investment position – in some cases it simply led to a narrower, but still ample, margin of safety. We regularly review all the variables in our intrinsic value estimates and take action when warranted by any change in our estimates or market prices.

Price Volatility vs. Investment Risk

While we felt a need to reevaluate some of our discount rates, we observed many cases where we believed that other market participants were misreading the situation based on excess fear. This fear created some extremely attractive investment opportunities, as well as some short-term price volatility. However, in our opinion, the short-term price volatility did not always correspond equally with higher levels of long-term investment risk. To illustrate the difference between short-term price volatility and long-term investment risk, let’s look at our investment in Juniper Networks, Inc. (JNPR).

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 7 |

Juniper Networks has a strong number two position in the router market, behind Cisco Systems, Inc. (CSCO). JNPR has achieved double-digit operating profit margins each year since 2003, excluding a goodwill impairment charge in 2006, and management has shown a strong commitment to balancing growth with cost control. As of Fall 2008, the company had built a fortress balance sheet, with $2.5 billion in cash and investments, and no debt. In comparison, JNPR’s market capitalization fell below $10 billion in October 2008 and dipped under $7 billion in March 2009.

The demand for Juniper’s products relates to consumer and corporate Internet bandwidth usage. The growth in Internet video consumption is widely forecast to continue for many years, and that growth should further accelerate as high definition video becomes a larger portion of what is viewed online. While technological advances may lead to slower demand growth for JNPR’s products versus overall bandwidth usage, in our opinion it seems unlikely that the company will fail to achieve at least a high-single-digit sales growth rate over the next 5+ years. Given JNPR’s product position and continued innovation, our view is that the company’s competitive position is unlikely to deteriorate significantly over the next 5 years.

Despite the advantages of a strong competitive position, a rock solid balance sheet and an industry with dependable longterm growth characteristics, Juniper’s stock traded down aggressively with the rest of the market. JNPR fell from the mid-high $30s in late 2007 to the mid-$20s by September 2008, eventually declining to the low teens near the 2009 market trough. We initiated positions in multiple Diamond Hill strategies, as this quality company with favorable growth characteristics traded down to a level where we felt it was selling at a sizable discount to our estimate of intrinsic value.

When we made these purchases, we were aware that the fear of continued economic decline might further depress the price, and it did. Fortunately, realization of this risk also presented an opportunity for us to enhance our returns by adding to the position at even better prices. For example, we bought more shares in the Small-Mid Cap Fund after the price dropped 10% from our original purchase and again after the price dropped another 10%.

In this case, our views were eventually endorsed by the market. JNPR rallied strongly as the market rose, and we sold our shares in May 2009 when the price reached our intrinsic value estimate. We earned 35%-75% holding period returns on our purchases of JNPR. The stock now trades modestly above the levels at which we sold our positions, while our estimate of intrinsic value is little changed.

Managing Portfolio Risk

One lesson from the downturn is to take advantage of especially attractive opportunities on the infrequent occasions when they present themselves. In our view, these opportunities often arise due to investors mistaking short-term volatility for true investment risk. The former is driven by emotion and in some cases has little relation to the underlying value of companies, which equals the sum of discounted cash flows those companies will produce over time. At Diamond Hill, we define risk as the permanent loss of capital. Although future events could prove us wrong, we believe that Juniper Networks was one of numerous investment opportunities that the market presented during the downturn entailing significantly greater likelihood of short-term price volatility than true long-term investment risk. Unfortunately, we are finding fewer of these high-reward, low-risk opportunities in the current market environment.

A major part of our job at Diamond Hill is managing portfolio risk. We pay close attention to business and balance sheet risk to set appropriate discount rates for the companies we invest in, and we will continue to take advantage of opportunities that show disproportionate rewards relative to the level of risk. This approach has served our clients well in both up and down markets. We remain committed to our disciplined, intrinsic value investment philosophy, and we believe that our approach to portfolio risk management will serve our clients well in future market environments. We thank you for your continuing support and confidence.

| | Diamond Hill Investments Christopher A. Welch, CFA Portfolio Manager |

| | |

| | |

| | |

| Page 8 | Diamond Hill Funds Annual Report December 31, 2009 |

The views expressed are those of the portfolio manager as of December 31, 2009, are subject to change, and may differ from the views of other portfolio managers of the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. All data referenced are from sources deemed to be reliable but cannot be guaranteed. Securities and sectors referenced should not be construed as a solicitation or recommendation or be used as the sole basis for any investment decision.

Standard and Poor’s 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Standard and Poor’s 500 Financials Index is a capitalization-weighted index, with 79 members.

Mentioned Securities and Respective Weights in the Diamond Hill Funds as of 12/31/09:

| | Small Cap Fund | Small-Mid Cap Fund | Large Cap Fund | Select Fund | Long-Short Fund | Financial Long-Short Fund | Strategic Income Fund |

| CSCO | 0.0% | 0.0% | 2.0% | 2.5% | 2.3% | 0.0% | 0.0% |

| JNPR | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

| MCD | 0.0% | 0.0% | 1.9% | 2.5% | 2.0% | 0.0% | 0.0% |

| PG | 0.0% | 0.0% | 3.0% | 3.0% | 3.1% | 0.0% | 0.0% |

Investors should consider the investment objectives, risks, and charges and expenses of the Diamond Hill Funds carefully before investing. This and other information about the Funds is in the prospectus, which can be obtained at www.diamond-hill.com. Read the prospectus carefully before you invest. Diamond Hill Capital Management, Inc., a registered investment adviser, serves as Investment Adviser to the Diamond Hill Funds and is paid a fee for its services. The Diamond Hill Funds are distributed by BHIL Distributors, Inc. (Member FINRA), an affiliated company. Investors may obtain a copy of the current prospectus at 888-226-5595 or www.diamond-hill.com. Like all mutual funds, Diamond Hill Funds are not FDIC insured, may lose value, and have no bank guarantee.

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 9 |

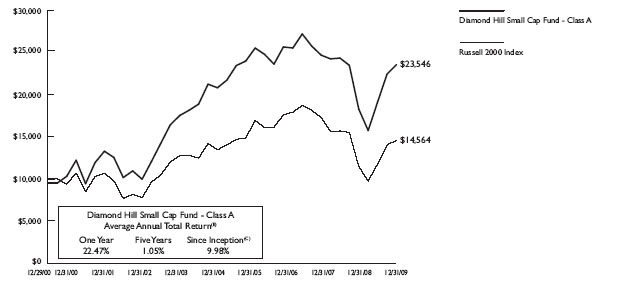

Diamond Hill Small Cap Fund

Performance Update

Average Annual Total Returns as of December 31, 2009

| | | One Year | | | Five Years | | | Since Inception (12/29/00) | | | Expense Ratio* | |

PERFORMANCE AT NAV without sales charges | |

| Class A Shares | | | 28.92 | % | | | 2.10 | % | | | 10.61 | % | | | 1.41 | % |

| Class C Shares | | | 27.99 | % | | | 1.33 | % | | | 9.78 | % | | | 2.16 | % |

| Class I Shares | | | 29.43 | % | | | 2.48 | % | | | 10.84 | % | | | 1.02 | % |

| BENCHMARK | |

| Russell 2000 Index | | | 27.17 | % | | | 0.51 | % | | | 4.26 | % | | | | |

PERFORMANCE AT POP includes sales charges | |

| Class A Shares | | | 22.47 | % | | | 1.05 | % | | | 9.98 | % | | | | |

| Class C Shares | | | 26.99 | % | | | 1.33 | % | | | 9.78 | % | | | | |

Historical performance for Class C shares and Class I shares prior to their inception is based on the performance of Class A shares. Class C and Class I performance has been adjusted to reflect differences in sales charges and expenses between classes.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

*Reflects the expense ratio as reported in the Summary Prospectus as amended October 1, 2009.

Portfolio Commentary

| The Diamond Hill Small Cap Fund (Class A, without sales charge) returned 28.92% in 2009. This figure compares to a 27.17% return for the benchmark Russell 2000 Index. For the 5-year period ended 12/31/09, the Fund’s return was 2.10%, annually, while the Russell 2000 Index returned 0.51%, annually, over the same period. Since-inception on 12/29/00, the Fund has returned 10.61%, annualized, compared to 4.26% for the Russell 2000 Index. While we are pleased with both the absolute and relative performance of the Fund since inception, we recognize that the strong performance in the first five years is responsible for attaining the satisfactory absolute result. While the past five years have been disappointing on an absolute basis, we are pleased to have outperformed on a relative basis both during the major downturn in 2008, as well as the strong recovery of 2009. During the year, holdings in the energy sector were the largest positive contributor to performance. Oil prices rebounded sharply after the steep decline that began in the middle of 2008, while natural gas ended the year slightly lower than it began, but the average price in 2009 was considerably lower than in 2008. Cimarex Energy Co. nearly doubled on the year and ended the year as the largest equity position in the Fund. Despite the natural gas price headwind, the company looks positioned for production growth from the Cana shale and has also benefitted from high natural gas liquids content, which are priced more in line with oil and currently allow more attractive well economics. Encore Acquisition Co., which has agreed to merge with Denbury Resources Inc., and Whiting Petroleum Corp. both benefitted from higher oil prices as they are in the early stages of developing their acreage in the Bakken through horizontal drilling. Berry Petroleum Co. nearly tripled on the year after being severely pressured in 2008. The company has diversified from its California heavy-oil roots, yet still remains leveraged to oil prices given its relatively high fixed cost structure. Also, because many of Berry’s cost are driven by natural gas prices, it benefits when the oil to gas spread is wide as in 2009. Southwestern Energy Co. continues to exhibit very high production growth, as it continues to focus on the Fayetteville shale. Finally, during the course of the year, we sold two oil service holdings, Helmerich & Payne, Inc. and Lufkin Industries, Inc. after large increases in their respective stock prices. |

| | |

| Page 10 | Diamond Hill Funds Annual Report December 31, 2009 |

For the year, the largest positive portfolio repositioning was the increase in the insurance holdings and the decrease in bank holdings within the financial sector. Assured Guaranty Ltd. and XL Capital Ltd. were both large successes, while the majority of our former small cap bank holdings have not recovered substantially, as have many of the larger cap banks and stocks of companies in other sectors that were under extreme distress in 2008 and early 2009. Financials are now the largest sector in the Fund. Banks were the largest detractors from performance in 2009 with First State Bancorp (New Mexico), Hanmi Financial Corp., Banner Corp., UCBH Holdings, Inc., and Imperial Capital Bancorp, Inc., all suffering losses before their sales. In addition, Huntington Bancshares, Inc., which we continue to hold, also was a large negative contributor.

While we held considerably less companies in the information technology, health care, and industrials sectors, when compared to the Russell 2000 Index, those we did own performed generally in line or better. Notable successes include BE Aerospace, Inc., KLA-Tencor Corp., Apogee Enterprises, Inc., Waters Corp., InVentiv Health, Inc., and Lifepoint Hospitals, Inc. Notable laggards included KHD Humboldt Wedag International Ltd., Res-Care, Inc., The Brink’s Company, and Lincoln Electric Holdings Inc.

The largest negative portfolio repositioning was the premature sales of several consumer cyclical and one basic materials company that have recovered substantially, as the economy has regained more solid footing. These include American Greetings Corp., Penske Auto Group, Inc., Black&Decker Corp. (which has agreed to merge with Stanley Works), and Charming Shoppes, Inc. on the consumer side and Century Aluminum Co. on the materials side. As a result, we underperformed in our stock selection in those two sectors by a wide margin.

We will continue to balance risk and reward in our appraisal of individual company values and appreciate your ongoing support and look forward to continuing to work with you in the coming years.

| | |

| Thomas P. Schindler, CFA | Christopher M. Bingaman, CFA | Christopher A. Welch, CFA |

| Portfolio Manager | Assistant Portfolio Manager | Assistant Portfolio Manager |

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 11 |

Growth of $10,000

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Small Cap Fund - Class A(A) and the Russell 2000 Index.

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on December 29, 2000. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 2000 Index (“Index”). The Index is an unmanaged capitalization weighted index which measures the performance of the 2,000 smallest companies based on total market capitalization. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Tabular Presentation of Schedule of Investments

The table below provides the Small Cap Fund’s sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund’s investments.

| Sector Allocation | | % of Net Assets | |

| Consumer Discretionary | | | 8 | % |

| Consumer Staples | | | 11 | % |

| Energy | | | 13 | % |

| Financial | | | 20 | % |

| Health Care | | | 7 | % |

| Industrial | | | 10 | % |

| Information Technology | | | 7 | % |

| Utilities | | | 5 | % |

| Cash and Cash Equivalents | | | 19 | % |

| | | | 100 | % |

The sector allocations are as of 12/31/09 and are subject to change.

| | |

| Page 12 | Diamond Hill Funds Annual Report December 31, 2009 |

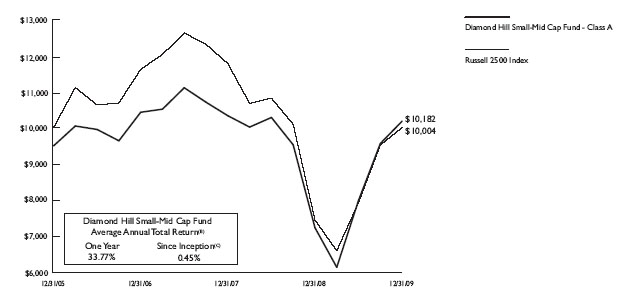

Diamond Hill Small-Mid Cap Fund

Performance Update

Average Annual Total Returns as of December 31, 2009

| | | One Year | | | Since Inception (12/31/05) | | | Expense Ratio* | |

PERFORMANCE AT NAV without sales charges | | | | | | | | | |

| Class A Shares | | | 40.77 | % | | | 1.76 | % | | | 1.36 | % |

| Class C Shares | | | 39.86 | % | | | 1.04 | % | | | 2.11 | % |

| Class I Shares | | | 41.36 | % | | | 2.15 | % | | | 0.97 | % |

| BENCHMARK | | | | | | | | | | | | |

| Russell 2500 Index | | | 34.39 | % | | | 0.01 | % | | | | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | |

| Class A Shares | | | 33.77 | % | | | 0.45 | % | | | | |

| Class C Shares | | | 38.86 | % | | | 1.04 | % | | | | |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

*Reflects the expense ratio as reported in the Summary Prospectus as amended October 1, 2009.

Portfolio Commentary

| The Diamond Hill Small-Mid Cap Fund (Class A, without sales charge) returned 40.77% in 2009. This figure compares to a 34.39% return for the benchmark Russell 2500 Index. For the four-year period since inception on 12/31/05, the Fund’s return was 1.76%, annually, while the Russell 2500 Index returned 0.01% over the same period. The since-inception performance is disappointing on an absolute basis, though we are pleased to have outperformed on a relative basis both during the major downturn in 2008, as well as the strong recovery of 2009. Entering the year, we felt there was a unique opportunity in a number of formerly large cap stocks that had fallen into the mid cap market capitalization range during the downturn. Retrospective evidence of such opportunity is offered by the significant outperformance of the Russell 2500 Index (Small-Mid Cap) over the Russell indexes covering large cap and small cap stocks, despite meaningful overlap in holdings in those indexes. Our investments from fall 2008 through early 2009 in a number of these situations, such as Juniper Networks, Inc., Prudential Financial, Inc. and Freeport McMoran Copper & Gold, Inc., contributed significant benefits to portfolio performance. From a sector perspective, all economic sectors contributed positive absolute performance during 2009. The energy sector offered the highest contribution to performance, led by Cimarex Energy Co., Noble Energy, Inc. and Encore Acquisition Co., which announced late in the year that it agreed to be acquired by Denbury Resources, Inc. That acquisition is expected to be completed in early 2010. With regard to individual securities, a group of insurance stocks including XL Capital Ltd., Prudential Financial, Inc. and Assured Guaranty Ltd. were significant gainers. SunTrust Banks, Inc. also was a leading contributor in 2009. A number of technology stocks also generated strong gains, including KLA-Tencor Corp., Alliance Data Systems Corp. and Juniper Networks, Inc. On the negative side, the three largest detractors from performance were all banks: Huntington Bancshares, Inc., Synovus Financial Corp. and UCBH Holdings, Inc. |

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 13 |

In our 2008 Portfolio Commentary, we wrote the following:

Generally speaking, the portfolio had a fairly high exposure to economically sensitive sectors and companies at year-end. This is not because we are predicting an economic “recovery” in the next 6-12 months; in fact, it is a near certainty that economic news will continue to be weak for some time. However, many stocks in these sectors appear to be discounting not only a recessionary environment, but even near depression-type of economic activity levels. This remains a possibility, but there are some early signs that the government’s efforts to stabilize the financial system are beginning to work – namely, certain key credit spreads have begun to meaningfully shrink in recent weeks. Furthermore, the continuing government commitment to avoiding an economic collapse suggests that a forecast of that level of weakness is likely not the most probable outcome. In any event, we feel that the individual companies we own in the portfolio are positioned and priced to deliver attractive returns over the next 5 years, and we will continue to carefully assess the risk levels we are incurring in pursuit of strong returns.

While the economic outlook has improved modestly over the past 12 months, the reaction of stock prices has been dramatic. Returns that we thought might take 5 years to realize occurred, in many cases, over the course of a few months. The “fear discount” that was being applied to many economically sensitive companies a year ago no longer appears to be in place. As such, we sold a number of our more cyclical holdings during the year as prices reached our intrinsic value estimates. In general, we found better margins of safety in higher quality companies as the year progressed, with an emphasis on opportunities in the health care and consumer staples sectors. The portfolio cash level also rose from 8% at year-end 2008 to 18% at year-end 2009. We will continue to balance risk and reward in our appraisal of individual company values.

We appreciate your ongoing support and look forward to continuing to work with you in the coming years.

| | |

| Christopher A. Welch, CFA | Christopher M. Bingaman, CFA | Thomas P. Schindler, CFA Portfolio |

| Portfolio Manager | Assistant Portfolio Manager | Assistant Portfolio Manager |

| | |

| Page 14 | Diamond Hill Funds Annual Report December 31, 2009 |

Growth of $10,000

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Small-Mid Cap Fund - Class A(A) and the Russell 2500 Index.

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The total return shown above is adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on December 31, 2005. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 2500 Index (“Index”). The Index is an unmanaged capitalization weighted index which measures the performance of the 2,500 smallest companies based on total market capitalization. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Tabular Presentation of Schedule of Investments

The table below provides the Small-Mid Cap Fund’s sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund’s investments.

| Sector Allocation | | % of Net Assets | |

| Consumer Discretionary | | | 8 | % |

| Consumer Staples | | | 11 | % |

| Energy | | | 17 | % |

| Financial | | | 17 | % |

| Health Care | | | 8 | % |

| Industrial | | | 11 | % |

| Information Technology | | | 5 | % |

| Utilities | | | 6 | % |

| Cash and Cash Equivalents | | | 17 | % |

| | | | 100 | % |

The sector allocations are as of 12/31/09 and are subject to change.

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 15 |

Diamond Hill Large Cap Fund

Performance Update

Average Annual Total Returns as of December 31, 2009

| | | One Year | | | Five Years | | | Since Inception (6/29/01) | | | Expense Ratio* | |

PERFORMANCE AT NAV without sales charges | | | | | | | | | | | | |

| Class A Shares | | | 30.21 | % | | | 3.89 | % | | | 5.23 | % | | | 1.20 | % |

| Class C Shares | | | 29.34 | % | | | 3.09 | % | | | 4.41 | % | | | 1.95 | % |

| Class I Shares | | | 30.71 | % | | | 4.29 | % | | | 5.47 | % | | | 0.81 | % |

| BENCHMARK | | | | | | | | | | | | | | | | |

| Russell 1000 Index | | | 28.43 | % | | | 0.79 | % | | | 1.23 | % | | | | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | | | | | |

| Class A Shares | | | 23.72 | % | | | 2.82 | % | | | 4.60 | % | | | | |

| Class C Shares | | | 28.34 | % | | | 3.09 | % | | | 4.41 | % | | | | |

Historical performance for Class C shares and Class I shares prior to their inception is based on the performance of Class A shares. Class C and Class I performance has been adjusted to reflect differences in sales charges and expenses between classes.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

* Reflects the expense ratio as reported in the Summary Prospectus as amended October 1, 2009.

Portfolio Commentary

| The Diamond Hill Large Cap Fund (Class A, without sales charge) returned 30.21% in 2009 compared to 28.43% for the Russell 1000 index. This year was certainly a relief after awful market returns in 2008, and I am glad to have outperformed in this market recovery. The Fund was down well over 20% during the market lows of March 2009, and the performance during the recovery was gratifying. The first quarter of 2009, coming as it did after a difficult 2008, was the most demanding period of my 27-year career. I am certainly glad that piece of market history is now behind us. Nevertheless, this decade is unique in providing ten years of negative returns in the broad market indexes. Much of this was a function of severely overvalued markets at the beginning of the decade. When taking a much longer-term perspective, equities have still provided a good long-term return to shareholders. It is this long-term perspective where our focus remains and where we encourage our shareholders to focus as well. Our energy holdings continued to represent the largest area of investment in the portfolio for much of the year. We focused on this area of investment over five years ago and continue to feel there are good long-term opportunities available in this sector. Our focus has been on the North American exploration and production companies, as they provide the best combination of attractive assets and good valuation. Exxon Mobil Corp. apparently agrees, as they recently bid to acquire XTO Energy, Inc., one of the holdings in the portfolio and solid contributor to portfolio performance. However, Anadarko Petroleum Corp. was an even greater contributor as it was a large holding in the Fund and appreciated over 60%. Large holdings like Apache Corporation and Occidental Petroleum Corp. were also up over 35% and contributed to the Fund’s performance. Health care is now approaching 20% of the portfolio and was an important contributor in 2009 as well. Medtronic, Inc., a depressed company with good growth prospects, appreciated nearly 40%, and at year-end, it was the largest health care holding. However, Schering-Plough Corp. was clearly the biggest contributor to performance, as it benefited from the acquisition by Merck & Co. As a result of the merger, we swapped into the shares of Merck & Co., due to the benefits of combining the two large pharmaceutical companies. Pfizer, Inc. was also a large holding, and it should benefit from the acquisition of Wyeth Pharmaceuticals, Inc. These two merged pharmaceutical companies should benefit from the opportunity to remove considerable costs from their business, while continuing to grow their revenues. Health care appears to provide an area of attractive value in the equity markets, as investors shun this controversial but relatively stable industry for companies with greater cyclical recovery opportunity. |

| | |

| Page 16 | Diamond Hill Funds Annual Report December 31, 2009 |

Some of our technology holdings provided strong performance for the portfolio, but as they appreciated to our price targets, they were eliminated. Stocks like Juniper Networks, Inc. and Texas Instruments, Inc. were up over 35% but were sold when their price reached our estimates of intrinsic value. Both these companies are strong competitors in attractive markets, and I would like to own these stocks again in the future, if they can be purchased at attractive prices.

Huntington Bancshares, Inc. and Synovus Financial Corp. were by far the worst performers, and they were eliminated from the portfolio after declines of 86% and 65%, respectively. However, the proceeds from these sales were used to purchase SunTrust Banks, Inc., which was the biggest winner in the portfolio. The swap ended up being successful, as the recovery in SunTrust Banks, Inc. exceeded the recovery in the bank stocks we sold.

Other disappointing holdings in the portfolio were our investments in the paper industry. Shares of International Paper Co. and Domtar Corp. were sold early in the year with losses of 45% and 51%. Our concerns about secular weakness in the paper industry were overwhelmed by near-term cyclical recovery opportunities. However, the pressure on the industry remains, and I do not foresee returning to these investments.

As of the end of 2009, I am concluding my seventh full year of managing the Diamond Hill Large Cap Fund. Of any period in the 27 years I have spent in the investment business, the period of 2008-2009 has been the most difficult for owners of U.S. equities. Thank you for your continued support.

| | |

| Charles S. Bath, CFA | Bill C. Dierker, CFA | Christopher A. Welch, CFA |

| Portfolio Manager | Assistant Portfolio Manager | Assistant Portfolio Manager |

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 17 |

Growth of $10,000

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Large Cap Fund - Class A(A) and the Russell 1000 Index.

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on thedifference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on June 29, 2001. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 1000 Index (“Index”). The Index is an unmanaged capitalization weighted index which measures the performance of the 1,000 largest companies based on total market capitalization. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Tabular Presentation of Schedule of Investments

The table below provides the Large Cap Fund’s sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund’s investments.

| Sector Allocation | | % of Net Assets | |

| Consumer Discretionary | | | 2 | % |

| Consumer Staples | | | 15 | % |

| Energy | | | 19 | % |

| Financial | | | 14 | % |

| Health Care | | | 19 | % |

| Industrial | | | 14 | % |

| Information Technology | | | 9 | % |

| Utilities | | | 2 | % |

| Cash and Cash Equivalents | | | 6 | % |

| | | | 100 | % |

| The sector allocations are as of 12/31/09 and are subject to change. |

| | |

| Page 18 | Diamond Hill Funds Annual Report December 31, 2009 |

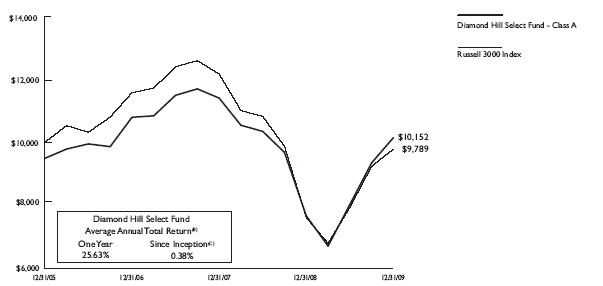

Diamond Hill Select Fund

Performance Update

Average Annual Total Returns as of December 31, 2009

| | | One Year | | | Since Inception (12/31/05) | | | Expense Ratio* | |

PERFORMANCE AT NAV without sales charges | | | | | | | | | |

| Class A Shares | | | 32.26 | % | | | 1.68 | % | | | 1.31 | % |

| Class C Shares | | | 31.86 | % | | | 0.97 | % | | | 2.06 | % |

| Class I Shares | | | 33.63 | % | | | 2.08 | % | | | 0.92 | % |

| BENCHMARK | | | | | | | | | | | | |

| Russell 3000 Index | | | 28.34 | % | | | (0.53 | %) | | | | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | |

| Class A Shares | | | 25.63 | % | | | 0.38 | % | | | | |

| Class C Shares | | | 30.86 | % | | | 0.97 | % | | | | |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

*Reflects the expense ratio as reported in the Summary Prospectus as amended October 1, 2009.

Portfolio Commentary

What a difference a year makes! This time last year, we were bemoaning the extreme risk aversion by investors. Remember when people were buying Treasury Bills at a premium, locking in negative returns as a result? “Return of Capital” was more important than “Return on Capital.” In 2008, the top five Benchmarks in terms of total return were:

| | | 2008 Return | | | 2009 Return | |

| Barclays Capital LT Treasuries | | | 25.06 | % | | | 13.10 | % |

| Barclays Capital Global LT Treasuries | | | 12.97 | % | | | 2.19 | % |

| Barclays Capital U.S. Aggregate Bonds | | | 5.24 | % | | | 5.93 | % |

| Gold Futures | | | 4.82 | % | | | 23.97 | % |

| Three-month T-Bills | | | 1.46 | % | | | 0.16 | % |

In 2009, the top five Benchmarks in terms of total return were:

| | | 2008 Return | | | 2009 Return | |

| MSCI Emerging Markets | | | (45.92 | %) | | | 62.29 | % |

| Barclays Capital High Yield Bonds | | | (26.16 | %) | | | 58.21 | % |

| S&P/GSCI Commodity Index | | | (42.80 | %) | | | 50.30 | % |

| Russell Mid-Cap Growth | | | (44.32 | %) | | | 46.31 | % |

| NASDAQ Composite | | | (40.54 | %) | | | 43.89 | % |

Many who focused on “Return of Capital” missed out on the “Return on Capital.” As of December 23, 2009, net inflows to bond mutual funds for the year totaled $335.9 billion. During the same period, net inflows to U.S. focused open end mutual funds totaled a negative $23.7 billion.

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 19 |

For most of the first quarter of 2009, this conservatism seemed to be the smart choice. For example, from the end of 2008 to March 9, 2009, the Diamond Hill Select Fund had a total return of (24.6%). Although we didn’t know it at the time, March 9th would prove to be the low point of the year. From March 9 to the end of 2009, the Select Fund had a total return of 75.5%. For the full year of 2009, the Select Fund has a total return of 32.26% (Class A, without sales charge) compared to a 28.34% return for the benchmark Russell 3000 Index. Longer-term performance vs. benchmark and peers is solid, but the absolute returns still lag behind our objectives. It is safe to say that over the past ten years, investors were not compensated for the risks that they took.

Looking at the drivers of performance for the Select Fund in 2009, it was a mixed bag of names. The top five contributors to the absolute return of the Select Fund were Hanesbrands, Inc., Freeport-McMoran Copper and Gold, Inc., Schering Plough, Corp., SunTrust Banks, Inc., and Anadarko Petroleum Corp.

On the negative side, the top five detractors from the absolute return of the Select Fund were Huntington Bancshares, Inc., Synovus Financial Corp., International Paper Co., Avery Dennison Corp., and Domtar Corp.

In terms of sectors, I would highlight four sectors and their contribution (or lack thereof) to our performance relative to the Russell 3000 Index. The energy sector was our largest source of outperformance relative to the Russell 3000. We were overweight energy throughout the year, and our stock selection added considerable value as well. Similar to energy, we were overweight the industrial sector throughout 2009, and our stock selections added value. In the health care sector, our performance benefitted from our overweight of the sector, as well as our stock selection. Finally, while all of our holdings in the technology sector were strong contributors to the return of the Select Fund, our holdings underperformed the Index holdings. The fact that we were underweight in the best performing sector in the Russell 3000 did not help our performance.

Last year, I talked about the “importance of being confident in the long-term growth of the U.S. economy and the normal functioning of the capital markets.” Our long-term oriented investment philosophy served us well, as we navigated the 2008-2009 market challenges. I expect that this philosophy will serve us well, as we confront the challenges that future markets will undoubtedly pose. As fellow shareholders in the Select Fund, we are committed to act in your best interests.

| | |

| William C. Dierker, CFA | Charles S. Bath, CFA | Christopher A. Welch, CFA |

| Portfolio Manager | Assistant Portfolio Manager | Assistant Portfolio Manager |

| | |

| Page 20 | Diamond Hill Funds Annual Report December 31, 2009 |

Growth of $10,000

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Select Fund - Class A(A) and the Russell 3000 Index.

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The total return shown above is adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on December 31, 2005. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The chart above represents a comparison of a hypothetical $10,000 investment and the reinvestment of dividends and capital gains in the indicated share class versus a similar investment in the Russell 3000 Index (“Index”). The Index is an unmanaged capitalization weighted index which measures the performance of the 3,000 largest companies based on total market capitalization. The Index is unmanaged, and does not reflect the deduction of fees associated with a mutual fund such as investment management and accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index although they can invest in the underlying securities.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

Tabular Presentation of Schedule of Investments

The table below provides the Select Fund’s sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund’s investments.

| Sector Allocation | | % of Net Assets | |

| Consumer Discretionary | | | 3 | % |

| Consumer Staples | | | 14 | % |

| Energy | | | 17 | % |

| Financial | | | 12 | % |

| Health Care | | | 21 | % |

| Industrial | | | 12 | % |

| Information Technology | | | 9 | % |

| Utilities | | | 2 | % |

| Cash and Cash Equivalents | | | 10 | % |

| | | | 100 | % |

| The sector allocations are as of 12/31/09 and are subject to change. |

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 21 |

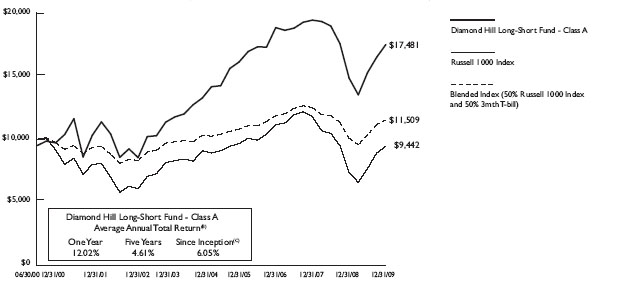

Diamond Hill Long-Short Fund

Performance Update

Average Annual Total Returns as of December 31, 2009

| | | One Year | | | Five Years | | | Since Inception (6/30/00) | | | Expense Ratio* | |

PERFORMANCE AT NAV without sales charges | | | | | | | | | | | | |

| Class A Shares | | | 17.93 | % | | | 5.69 | % | | | 6.63 | % | | | 1.68 | % |

| Class C Shares | | | 17.02 | % | | | 4.89 | % | | | 5.82 | % | | | 2.43 | % |

| Class I Shares | | | 18.39 | % | | | 6.11 | % | | | 6.86 | % | | | 1.29 | % |

| BENCHMARK | | | | | | | | | | | | | | | | |

| Russell 1000 Index | | | 28.43 | % | | | 0.79 | % | | | (0.60 | %) | | | | |

| 50% Russell 1000 Index / 50% Citi 3 Month T-Bill | | | 14.14 | % | | | 2.18 | % | | | 1.39 | % | | | | |

PERFORMANCE AT POP includes sales charges | | | | | | | | | | | | | | | | |

| Class A Shares | | | 12.02 | % | | | 4.61 | % | | | 6.05 | % | | | | |

| Class C Shares | | | 16.02 | % | | | 4.89 | % | | | 5.82 | % | | | | |

Historical performance for Class C shares and Class I shares prior to their inception is based on the performance of Class A shares. Class C and Class I performance has been adjusted to reflect differences in sales charges and expenses between classes.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.diamond-hill.com.

*Reflects the expense ratio as reported in the Summary Prospectus as amended October 1, 2009.

Portfolio Commentary

| The Diamond Hill Long-Short Fund (Class A, without sales charge) returned 17.93% in 2009 compared to 28.43% for the Russell 1000 and 10.46% for the Morningstar Long-Short category average. This year was marked by an awful first quarter decline, as the market reached its yearly low in the first quarter. The subsequent rally was gratifying, as 2009 became a strong recovery year following the disastrous market of 2008. The portfolio performed well in 2009 but clearly lagged the rapidly rising equity markets in the last three quarters of the year. This is typical of a long-short fund and should be expected in rapidly rising markets. The short positions provided a drag on performance, making it difficult for the portfolio to appreciate in line with a strong market. However, we are very happy with the long-term performance of the Fund, as it has meaningfully outperformed its benchmarks over longer time periods. The long portion of the portfolio was dominated by the energy sector in 2009. This sector was the largest weight for most of the year, and many of the biggest contributors to the performance on the long side of the portfolio were in this sector. Anadarko Petroleum Corp. was the strongest contributor, as it appreciated more than 60%. Apache Corp. was the largest long equity position for much of the year, and it was up over 35%. Many of the characteristics which made this group so attractive for the past several years, including good valuation and growth opportunities, remain. Therefore, at year-end it was one of the largest sector weights in the long portfolio. Health care was our other large sector weight at year-end. It was nearly 20% of the portfolio and along with energy, was our largest sector weight. Valuations in this sector became depressed, as investors worried about health care reform and abandoned the sector for investments with more cyclical recovery opportunity. Medtronic, Inc., a depressed company with good growth prospects, appreciated nearly 40% and was our largest health care holding at year-end. However, Schering-Plough Corp. was the biggest contributor to performance, as it appreciated more than 70% subsequent to the merger with Merck & Co. As a result of the merger, we swapped into the shares of Merck & Co., due to the benefits of combining the two large pharmaceutical companies. Pfizer, Inc. was also a large holding, and it should benefit from the merger with Wyeth Pharmaceuticals, Inc. These two merged pharmaceutical companies should benefit from the opportunity to remove costs from their business, while continuing to grow their revenues. |

| | |

| Page 22 | Diamond Hill Funds Annual Report December 31, 2009 |

Some of our technology holdings provided strong performance for the portfolio, but as they appreciated to our price targets, they were eliminated. Stocks like Juniper Networks, Inc. and Texas Instruments, Inc. were up over 35% but were sold, because their prices reached our estimates of intrinsic value. Overall, technology stocks did well for the Fund, but our underweight position in the sector hurt the long portion of the portfolio.

While the long portion of the portfolio did well, there were still some disappointments. Domtar Corp. and International Paper Co. were down 51% and 45%, respectively, when they were sold early in the year. Our concerns about secular weakness in the paper industry were overwhelmed by near-term cyclical recovery opportunities. However, the pressure on the industry remains, and we continue to monitor these names in case they become attractive short opportunities.

For the most part, the short portion of the portfolio was a drag on performance. However, a couple of meaningful successes were our positions in the for-profit education market. Apollo Group, Inc. and Corinthian Colleges, Inc. were meaningful contributors, as both declined more than 20%, before the positions were closed out. There were a few other minor successes, but most short positions were meaningful drags on the portfolio. Royal Caribbean Cruises Ltd. and Amazon, Inc. were the biggest negative contributors from the consumer portion of the portfolio. Amazon more than doubled for the year, but we have maintained the short position, as increasing levels of competition should pressure the valuation of the shares. We are also maintaining the Royal Caribbean Cruises Ltd. position, as increased capacity in the industry should bring renewed pressure to profitability. However, our worst short position for the year was Dow Chemical Co. This was a large short position, due to our skepticism regarding the Rohm & Haas Co. acquisition. We remain skeptical, but the stock has appreciated over 70% in the hope of a strong cyclical earnings recovery. The stock remained a meaningful short position at year-end.

As of the end of 2009, we have concluded a very painful decade for the equities market. Returns for most major indexes in the decade ending in 2009 were negative. However, when using a much longer time frame, equity returns are still quite attractive. During this difficult decade, we appreciate the faith shareholders have placed in Diamond Hill. We thank you for your continued support.

| | |

| R.H. Dillon, CFA | Charles S. Bath, CFA | Christopher M. Bingaman, CFA |

| Portfolio Co-Manger | Portfolio Co-Manager | Assistant Portfolio Manager |

| | |

| Diamond Hill Funds Annual Report December 31, 2009 | Page 23 |

Growth of $10,000

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Long-Short Fund - Class A(A), the Russell 1000 Index and the Blended Index (50% Russell 1000 Index and 50% 3mth T-bill).

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on June 30, 2000. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.