United States

Securities And Exchange Commission

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-8061

(Exact name of registrant as specified in charter)

325 John H. McConnell Boulevard, Suite 200, Columbus, Ohio 43215

(Address of principal executive offices) (Zip code)

James F. Laird, 325 John H. McConnell Boulevard, Suite 200, Columbus, Ohio 43215

(Name and address of agent for service)

Registrant's telephone number, including area code: (614) 255-3333

Date of fiscal year end: 12/31

Date of reporting period: 12/31/07

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, Washington, DC 20549-0102. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Diamond Hill Funds Annual Report

This material must be preceded or

accompanied by a current prospectus.

Annual Report

December 31, | | SMALL CAP FUND |

2007 | | SMALL-MID CAP FUND |

| | | LARGE CAP FUND |

| | | SELECT FUND |

| | | LONG-SHORT FUND |

| | | FINANCIAL LONG-SHORT FUND |

| | | STRATEGIC INCOME FUND |

| | | NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

| Letter to Shareholders | 1 |

| Mission Statement, Pledge, and Fundamental Principles | 3 |

| Management Discussion of Fund Performance | |

| Diamond Hill Small Cap Fund | 6 |

| Diamond Hill Small-Mid Cap Fund | 9 |

| Diamond Hill Large Cap Fund | 11 |

| Diamond Hill Select Fund | 13 |

| Diamond Hill Long-Short Fund | 15 |

| Diamond Hill Financial Long-Short Fund | 17 |

| Diamond Hill Strategic Income Fund | 20 |

| Financial Statements | |

| Schedules of Investments | 22 |

| Statements of Assets & Liabilities | 35 |

| Statements of Operations | 37 |

| Statements of Changes in Net Assets | 38 |

| Schedule of Capital Share Transactions | 40 |

| Financial Highlights | 42 |

| Notes to Financial Statements | 52 |

| Report of Independent Registered Public Accounting Firm | 58 |

| Other Items | 59 |

| Schedule of Shareholder Expenses | 60 |

| Management of the Trust | 62 |

CAUTIONARY STATEMENT

At Diamond Hill, we pledge that, “we will communicate with our clients about our investment performance in a manner that will allow them to properly assess whether we are deserving of their trust.” Our views and opinions regarding the investment prospects of our portfolio holdings and Funds are “forward looking statements” which may or may not be accurate over the long term. While we believe we have a reasonable basis for our opinions, actual results may differ materially from those we anticipate. Information provided in this report should not be considered a recommendation to purchase or sell any particular security.

You can identify forward looking statements by words like “believe,” “expect,” “anticipate,” or similar expressions when discussing prospects for particular portfolio holdings and/or one of the Funds. We cannot assure future results. You should not place undue reliance on forward-looking statements, which speak only as of the date of this report. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. This material is not authorized for distribution to prospective investors unless preceded or accompanied by a Prospectus. Please read the Prospectus carefully for a discussion of fees, expenses, and risks. Current performance may be lower or higher than that quoted herein. You may obtain a current copy of the Prospectus or more current performance information by calling 1-888-226-5595 or at Diamond Hill’s website (www.diamond-hill.com).

Dear Fellow Shareholders:

We are pleased to provide you with this year end update for the Diamond Hill Funds. Our focus remains on seeking out investment opportunities where the price-to-intrinsic value relationship provides an opportunity to earn an attractive rate of return while also providing a margin of safety. The following table summarizes the performance of the Diamond Hill Class A shares relative to their benchmarks as of December 31, 2007.

| |

| | | | Total Return | | |

| | NAV 12/31/07 | Three Months Ended 12/31/07 | Six Months Ended 12/31/07 | One Year Ended 12/31/07 | Three Years Ended 12/31/07 | Five Years Ended 12/31/07 | Ten Years Ended 12/31/07 | Since Inception | Inception Date |

| | | | | | | | | | |

| Small Cap Fund (DHSCX) | 22.53 | -4.17% | -9.23% | -3.79% | 5.15% | 17.68% | | 14.60% | 12/29/00 |

| Russell 2000 | | -4.57% | -7.52% | -1.55% | 6.80% | 16.24% | | 8.13% | |

| Small-Mid Cap Fund (DHMAX) | 10.50 | -3.48% | -6.97% | -0.91% | | | | 4.31% | 12/31/05 |

| Russell 2500 | | -4.31% | -6.72% | 1.38% | | | | 8.51% | |

| Large Cap Fund (DHLAX) | 16.25 | -2.01% | -0.14% | 5.42% | 12.12% | 17.63% | | 9.43% | 6/29/01 |

| Russell 1000 | | -3.23% | -1.31% | 5.77% | 9.08% | 13.43% | | 4.77% | |

| Select Fund (DHTAX) | 10.61 | -2.49% | -0.77% | 5.63% | | | | 9.57% | 12/31/05 |

| Russell 3000 | | -3.35% | -1.84% | 5.13% | | | | 10.29% | |

| Long-Short Fund (DIAMX) | 18.40 | 0.86% | 3.37% | 3.14% | 13.56% | 16.03% | | 10.00% | 6/30/00 |

| Russell 1000 | | -3.23% | -1.31% | 5.77% | 9.08% | 13.43% | | 2.21% | |

| Morningstar TM Long-Short Category Average | | -0.33% | -0.32% | 4.50% | 5.69% | 7.39% | | 5.01% | |

| Financial Long-Short Fund (BANCX) | 16.20 | -14.39% | -17.83% | -17.05% | -1.09% | 9.87% | 8.13% | 10.05% | 8/1/97 |

| S&P 1500 Supercomposite Financials (A) | | -14.03% | -17.64% | -18.32% | 1.18% | 8.79% | 4.97% | 5.57% | |

| Strategic Income Fund (DSIAX) | 10.41 | -5.23% | -7.46% | -4.78% | 2.45% | 6.88% | | 7.44% | 9/30/02 |

| Merril Lynch Domestic Master Index | | 3.11% | 6.16% | 7.17% | 4.66% | 4.49% | | 4.58% | |

Source: Diamond Hill Funds, Bloomberg LP and Frank Russell Company

Returns are shown without sales charges but include all other expenses. Returns greater than one year are annualized.

| (A) | Returns for the S&P 1500 Supercomposite Financials are price change only before November 29, 2001 and total return thereafter. |

Equity Markets

The year 2007 was a difficult period for investors. During the year, we saw the buyout market heat up dramatically and then fizzle out. We saw credit spreads fall to very narrow levels, only to increase substantially by year end. For the first time in many years, concerns over inflation began to emerge, partially reflected in the high price of oil and gold, as well as the substantial devaluation of the U.S. dollar. Most disturbing for financial market participants were the mortgage meltdown and the associated fallout in the structured securities market (mortgage backed securities, CDOs, leveraged hedge funds, etc.). Look no further than the implosion in certain financial stocks (mortgage originators, large securities firms, bond insurers, and mortgage insurers) to see how deep the concerns have become. This “credit crisis” may have important consequences for the economy. For many years, investors have incorrectly predicted the “death of the U.S. consumer.” Easy credit, low savings rates and significant home equity extraction sustained consumer spending. One must now wonder if the credit crisis will impact consumers’ access to credit, which would impact the contribution of consumer spending to the U.S. economy, and the economies of our trading partners. Either way, one can have a healthy debate about whether credit driven consumption is in the long-term best interest of the U.S. economy.

The major U.S. indices had mixed results in 2007, with large cap stocks generating mediocre performance (S&P 500) up 5.5%. Mid-cap stocks (S&P 400) outperformed large cap stocks, rising 8%. Small cap stocks (S&P 600) were down fractionally. Digging a little deeper into market returns, in 2007 there was a strong style bias with “growth” stocks comfortably outperforming “value” stocks. In 2007, “factors” that were rewarded by the market included price momentum, earnings revisions, earnings growth, market cap, and the percentage of sales from foreign markets. One of the worst factors for 2007 was valuation. Diamond Hill focuses on our estimate of intrinsic value, which incorporates growth and value considerations. Nonetheless, performance in 2007 was better than what one might think given the aforementioned market context.

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 1 |

The performance of our equity funds in 2007 was mixed. Our funds with a bias towards large cap stocks (Long-Short, Large Cap and Select) had positive absolute returns. While positive for the year, Long-Short underperformed its long only benchmark, and its peers. In the Long-Short fund, we estimate that our longs outperformed our long only benchmark, while our aggregate short positions offset some of that performance. The Large Cap fund slightly underperformed its benchmark (which has growth and value stocks in it) but easily outperformed its value peers. The Select Fund outperformed its benchmark and peer group for the year. Our two funds with a bias towards mid cap and small cap stocks had negative absolute returns in 2007. The Small-Mid Cap fund trailed its index and its peer group. The Small Cap fund trailed its index, but outperformed its peer group. The performance of the Diamond Hill Financial Long-Short Fund reflected the difficulties created by the housing downturn and the associated financial debacle. The fund, while negative on a total return basis, outperformed its benchmark while trailing its peer group.

At various times during the past few years, we’ve expressed our concerns over the sustainability of earnings growth, the agency risk in the investment management business, and the shift from greed to fear in the financial markets. We’ve also talked about how investment managers are often defined by how they handle adversity. The current market environment is putting many to the test. We remain singularly focused on intrinsic value, which is driven by our estimate of normalized earnings and the 5 year estimated growth in those earnings. We continue to believe that our long term time horizon is a significant advantage vs. the market and our peers. Could the market go lower? We think that is the wrong question. The question we think makes more sense is, “For a long-term investor, do the current return opportunities compensate an investor for the risks he is taking?” We would like to close with an interesting observation. As of January 25, 2008, the date of this letter, the total return on the S&P 500 since its peak on March 24, 2000 is now negative. That is nearly eight years of negative returns (on a compound annual basis), and that is unusual. To us, this is not the time to focus on the negative. Rather, it is a time to look for opportunities in the market. In fact, we are finding more opportunities in the market than we have in some time. We are confident that our long-term focus will allow us to take advantage of the values created in a market that is currently gripped by fear.

Fixed Income Markets

Credit risk in the fixed income markets was an issue as well as problems in the sub-prime mortgage markets. These issues surfaced in spades in the second half of 2007, and the results have been more restrictive lending standards on the part of lenders, a dramatic slowdown in consumer spending, massive write-offs by the financial community and an increased skepticism of the value of risk assets. The Federal Reserve has begun a campaign to lower interest rates and provide liquidity to the financial system. While they will eventually be successful in stabilizing markets, many feel that they have been too slow to react and that they have a long way to go.

Our focus is on those factors that would indicate to us that the impending economic and credit downturn is fully discounted in the prices of the securities in which we invest. The frequency and magnitude of losses in the financial sector continue to accelerate, but we believe that we are getting closer to the point of maximum pain. Importantly, much of the losses have been offset by private equity and hybrid equity capital infusions and, to a lesser extent, dividend cuts. The Federal Reserve signaled that it is willing to more aggressively move the fed funds rate towards the two-year Treasury yield and, with increasingly weak economic data points likely in coming months, we can expect continued lower interest rates in the short end of the yield curve. There also seems to be some support building for a short-term fiscal response to the weak economy. It remains to be seen what that package might include and when it might become effective.

We are encouraged by our prospects over a long-term horizon. In the near term, we expect to face continued volatility, as the market struggles to discount a very uncertain outlook.

We thank you for your continued commitment to our investment philosophy. As fellow shareholders, we will work hard to continue to earn your trust.

Diamond Hill Capital Management, Inc.

Bill C. Dierker, CFA

Assistant Portfolio Manager

| |

| Page 2 | Diamond Hill Funds Annual Report December 31, 2007 |

| |

Mission Statement, Pledge and Fundamental Principles |

| |

Mission | The mission of Diamond Hill is to serve our clients through a disciplined intrinsic-value-based approach to investing, while maintaining a long-term perspective, and aligning our interests with those of our clients. |

| | |

| | To successfully pursue our mission, we are: |

| | |

| | COMMITTED to the Graham-Buffett investment philosophy, with goals (over 5-year rolling periods) to outperform benchmarks and our peers, and achieve absolute returns sufficient for risk of asset class. |

| | |

| | DRIVEN by our conviction to create lasting value for clients and shareholders. |

| | |

| | MOTIVATED through ownership of Diamond Hill funds and company stock. |

| | |

Investment Philosophy | At Diamond Hill, the investment philosophy, which is rooted in the teachings of Benjamin Graham and the methods of Warren Buffett, drives the investment process — not the opposite. |

| | |

| | Most simply, we invest in a company when its market price is at a discount to our appraisal of the intrinsic value of the business (or at a premium for short positions). |

| | |

| | There are four guiding principles to our investment philosophy: |

| | Treat every investment as a partial ownership interest in that company |

| | Invest with protection of capital, as well as return on capital, in mind |

| | Have a long-term investment temperament |

| | Recognize that market price and intrinsic value converge over time |

| | |

| | “Investment is most intelligent when it is most businesslike.” |

| | |

| | — BENJAMIN GRAHAM |

| | |

| | |

Pledge | Consistent with our mission & investment philosophy, we pledge the following to all of our clients: |

| | |

| | Our investment discipline is to assess the economics of the underlying business, its management, and the price that must be paid to own a piece of it. We seek to concentrate our investments in businesses that are available at prices below intrinsic value (at a premium for short positions) and are managed or controlled by trustworthy and capable people. Benjamin Graham pioneered this discipline during the 1930s and many others have practiced it with great success ever since, most notably Warren Buffett. |

| | |

| | We will communicate with our clients about our investment performance in a manner that will allow them to properly assess whether we are deserving of their trust. |

| | |

| | Our investment team will be comprised of people with integrity, sound experience and education, in combination with a strong work ethic and independence of thought. Especially important is that each possesses the highest level of character, business ethics and professionalism. |

| | |

| | Our employees will enjoy a working environment that supports professional and personal growth, thereby enhancing employee satisfaction, the productivity of the firm and the experience of our clients. |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 3 |

| | “Invest With Us” means we will invest the capital you entrust to us with the same care that we invest our own capital. To this end, Diamond Hill employees and affiliates are significant investors in the same portfolios in which our clients invest and are collectively the largest shareholders in the Diamond Hill Funds. In addition, all Diamond Hill employees are subject to a Code of Ethics, which states that all personal investments must be made in a Diamond Hill fund, unless approved by our Chief Compliance Officer. |

| | |

Our | Valuation |

fundamental | |

investment | Every share of stock has an intrinsic value that is independent of its current stock market price. |

| | |

| | At any point in time, the stock market price may be either significantly higher or lower than intrinsic value. |

| | |

| | Over short periods of time, as evidenced by extreme stock market volatility, the stock market price is heavily influenced by the emotions of market participants, which are far more difficult to predict than intrinsic value. While stock market prices may experience extreme fluctuations on a particular day, we believe intrinsic value is far less volatile. |

| | |

| | Over sufficiently long periods of time, five years and longer, the stock market price tends to converge with intrinsic value. |

| | |

| | Calculating Intrinsic Value Estimate |

| | |

| | We believe that we can determine a reasonable approximation of that intrinsic value in some cases. |

| | |

| | That value can be determined if we have a reasonable basis for projecting the future cash flows of a business and use an appropriate discount rate. |

| | |

| | In estimating intrinsic value, we use an interdisciplinary approach. Not only do we perform financial modeling including discounted cash flow, private market value, and leveraged buyout analyses, we draw from other areas we believe are relevant to our investment decision-making. These include economics, statistics and probability theory, politics, psychology, and consumer behavior. |

| | |

| | In short, we do not want to exclude from our thinking anything that can help us forecast future cash flows, our most important as well as most difficult job. |

| | |

| | The Diamond Hill investment process continually compares market price to our estimate of intrinsic value, which is updated over time as new information arises. |

| | |

| | Suitable Investments |

| | |

| | We only invest in a business when the stock market price is lower than our conservative assessment of per share intrinsic value (or at a premium for short positions). |

| | |

| | We concentrate our investments in businesses whose per share intrinsic value is likely to grow. To achieve this, we assess the underlying economics of the businesses in which we invest and the industries and markets in which they participate. We seek to invest in businesses that possess a competitive advantage and significant growth prospects as well as outstanding managers and employees. |

| | |

| | Every business in which we invest is “handicapped” by its price. While we would prefer to own only great businesses with superior managers, there are very few businesses that satisfy those criteria and additionally are available at attractive prices. As a result, we may invest in less attractive businesses at more than attractive prices. Depending on the price that we pay, our returns from less than ideal businesses may be even better than our returns from ideal businesses. |

| |

| Page 4 | Diamond Hill Funds Annual Report December 31, 2007 |

| | Risk & Return |

| | |

| | We intend to achieve our return from both the closing of the gap between our purchase price and intrinsic value and the growth in per share intrinsic value. For short positions, a growing intrinsic value may shorten the holding period. |

| | |

| | We do not define risk by price volatility. We define risk as the possibility that we are unable to obtain the return of the capital that we invest as well as a reasonable return on that capital when you need the capital for other purposes. If your time horizon is less than five years, then you should not invest that capital in the stock market. |

| | |

Our fundamental strategic income principles | Yield & Return The primary goal for our strategic income strategy is to generate a yield greater than the current rate of inflation without bearing undue credit or interest rate risk. However, we cannot guarantee any specific yield. We balance our income objective with a focus on total return. Over five-year rolling periods, our objective is to earn equity-like returns in the income markets with lower year-to-year volatility and more importantly, a much lower risk of permanent loss of capital. |

| | |

| | |

| | “You simply have to behave according to what is rational than according to what is fashionable.” |

| | |

| | — WARREN BUFFETT |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 5 |

|

Diamond Hill Small Cap Fund |

Performance Update |

Results (Class A) Since Inception*

| | Year Ended 12/31/07 | Five Years Ended 12/31/07 | Since 12/29/00 Inception |

| Diamond Hill Small Cap Fund (DHSCX) | (3.79%) | 17.68% | 14.60% |

| Russell 2000 Index | (1.55%) | 16.24% | 8.13% |

| * | The Fund return excludes any sales charges but includes all other expenses. Standardized returns are disclosed on the following page. Results longer than one year are annualized. |

|

R.H. Dillon, CFA Co-Portfolio Manager |

| |

|

Thomas P. Schindler, CFA Co-Portfolio Manager |

| |

|

Christopher A. Welch, CFA Assistant Portfolio Manager |

The Diamond Hill Small Cap Fund - Class A returned a negative 3.79% in 2007, trailing the Russell 2000 return of negative 1.55%. The trailing 3-year annualized return of 5.15% also falls below the Russell 2000 Index comparable return of 6.80% while the trailing 5-year return of 17.68% exceeds the comparable Russell 2000 return of 16.24%, reflecting both strong absolute and relative performance in calendar years 2003 and 2004 and thus for the five year period overall.

In several ways, 2007 reversed longer-term trends in the marketplace. First, larger capitalization stocks meaningfully outperformed smaller capitalization stocks. Many market commentators have called for this to occur for the past several years citing among other things the length of time of the small cap outperformance cycle, large cap valuations becoming more compelling vis-à-vis small cap, and the benefits of greater multinational exposure as the U.S. economic growth lags global economic growth and the U.S. dollar has weakened relative to most major currencies. We have not disagreed with many of these sentiments, but 2007 has been the first calendar year these macro views have translated to a successful asset allocation call. Second, stocks generally categorized as “growth” outperformed those categorized as “value.” While we do not like to become preoccupied by these labels, because of the respective weighting in various style indices, this is generally stating the obvious fact that financials and consumer discretion fared very poorly in the stock market while information technology and healthcare fared relatively well. Third, while the Federal Reserve Bank had previously been raising short-term rates in order to return to something akin to a “neutral” monetary policy stance in the past several years, events in the credit markets caused a reversal at the Fed, which has begun to aggressively ease rates in an attempt to stimulate the U.S. economy as well as calm market participants who have rediscovered risk and demanded higher spreads to compensate them for that risk.

On the positive side, our investments in the energy sector were again positive contributors to returns in 2007 after a relatively poor 2006. Oil prices once again rose substantially year-over-year, while natural gas prices were flattish. Our energy holdings as a group have been much larger than the index and individual positions including Helmerich & Payne (a 4.4% position on 12/31/2007), Cimarex (4.6%), and Encore Acquisition (4.4%) are the largest in the Fund. With the exception of Lufkin Industries (1.5%) but including the now eliminated Tidewater, our energy stocks returned in a range of 17% to 65% in 2007. In 2006, many exploration and production companies experienced cost increases, primarily labor and equipment, leading to margin pressure. In 2007, revenue growth has been strong as a result of either the higher price for oil or production increases or both, leading to positive gains in year-over-year earnings at the same time valuations on trailing basis are in most cases well below the market in general.

Financial news in the second half of 2007 was dominated by developments in the housing and credit markets. The crux of the problem has been the coincidence of poor underwriting standards and now declining home prices. In the first part of this decade, housing prices appreciated well above historic norms, and at unprecedented rates in many markets, particularly the coasts. Factors contributing to higher home prices were the expansion of credit both from low interest rates (an outgrowth of the Fed’s policy to lower rates and narrower spreads due to lower risk premiums) and looser lending standards (higher percentage loan-to-value, the increasing share of adjustable rate, interest-only, stated income, and other “products” which many previously unqualified including “subprime” borrowers into the market) and market psychology. Now as defaults and foreclosure rates have skyrocketed, credit losses and provisions for future losses have increased.

| |

| Page 6 | Diamond Hill Funds Annual Report December 31, 2007 |

While our portfolio had less in financials than the Russell 2000 Index, our holdings were impacted negatively. There were three financial holdings subject to acquisitions, First Charter, MAF Bancorp, and Eagle Hospitality that contributed positively to returns. Each of the other financial holdings declined during the year, in many cases substantially. One other holding, MoneyGram (1.0%), also experienced a substantial decline in its stock as a result of its investments in asset backed securities. This was particularly disappointing since the vast majority of the company’s value was represented by the money transfer business which is fee based and growing quite rapidly. The company also processed official checks for financial institutions which gave rise to a float-based portfolio that was the source of funds for the losing investments.

The other sector of the market which performed particularly poorly was consumer discretion. Spending has suffered in part due to the inability of consumers to utilize their homes as a source of cash. There has long been concern over the condition of household balance sheets, which while in the previous years had not led to a meaningful slowdown in consumer spending, may be finally taking its toll. In our Fund, a few retailers were notable examples. Finish Line, in addition to fundamental weakness, made a terrible offer to acquire Genesco, a company twice its market cap at very near the peak of the market in June. The offer consisted of cash to be financed nearly entirely by UBS. The merger is now tied up in the courts, but we have since sold our position at a considerable loss. Also, Charming Shoppes (0.9%), a retailer catering to plus size women, experienced lower earnings and subsequent stock price. Even auto retailer Penske Automotive (1.4%), which focuses nearly entirely on foreign nameplates including luxury automakers BMW and Mercedes, experienced a meaningful stock price decline despite continued solid earnings.

Industrial companies were a mixed lot in 2007. Lincoln Electric (1.8%), Kaydon (1.6%), and Toro (2.8%) all appreciated 17% or more. On the other hand, railcar companies Greenbrier (0.6%) and Trinity (1.1%) each declined more than 20% for the full year, mitigated by partial sales we made at higher prices during the year. Orders for most types of railcars declined this year and competition is intense, but backlogs remain reasonably healthy. Finally, AirTran (2.2%) and Frontier Airlines (0.4%) both declined during the year as higher fuel prices offset much of the improved revenues and traffic the industry experienced.

Thank you for your support, and we look forward to working with you in the coming years.

| | |

| R. H. Dillon, CFA | Thomas P. Schindler, CFA | Christopher A. Welch, CFA |

| Co-Portfolio Manager | Co-Portfolio Manager | Assistant Portfolio Manager |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 7 |

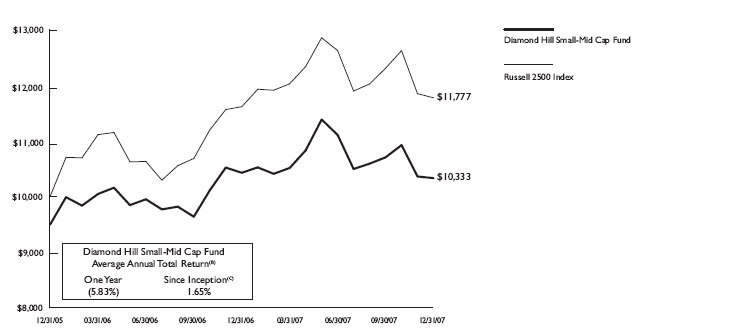

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Small Cap Fund - Class A(A) and the Russell 2000 Index

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on December 29, 2000. |

Past performance is no guarantee of future results. The principal value and investment return of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Tabular Presentation of Schedule of Investments |

| |

The table below provides the Small Cap Fund's sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund's investments.

Sector Allocation | | % of Net Assets |

| Consumer Discretionary | | | 18 | % | |

| Consumer Staples | | | 6 | % | |

| Energy | | | 24 | % | |

| Financial | | | 15 | % | |

| Health Care | | | 2 | % | |

| Industrial | | | 14 | % | |

| Information Technology | | | 2 | % | |

| Materials | | | 1 | % | |

| Utilities | | | 5 | % | |

| Cash and Cash Equivalents | | | 13 | % | |

| | | | 100 | % | |

| |

| Page 8 | Diamond Hill Funds Annual Report December 31, 2007 |

|

Diamond Hill Small-Mid Cap Fund |

Performance Update |

Results (Class A) Since Inception*

| | | Year Ended 12/31/07 | | Since 12/31/05 Inception | |

| Diamond Hill Small-Mid Cap Fund | | | (0.91 | %) | | 4.31 | % |

| Russell 2500 Index | | | 1.38 | % | | 8.51 | % |

| * | The Fund return excludes any sales charges but includes all other expenses. Standard returns are disclosed on the following page. |

| |

|

Christopher A. Welch, CFA Portfolio Manager |

| |

|

Christopher M. Bingaman, CFA Assistant Portfolio Manager |

| |

|

Thomas P. Schindler, CFA Assistant Portfolio Manager |

The Diamond Hill Small-Mid Cap Fund Class A load-waived shares returned negative 0.91% in 2007. This figure trailed the positive 1.38% return of the Russell 2500 Index. Given the 12/30/05 inception date, the fund does not yet have a performance record for 3 or 5 years.

One factor that negatively impacted the fund’s returns was the market’s emphasis on growth, and the corresponding poor returns to valuation, in 2007. The Russell 2500 Growth Index returned positive 9.7% compared to the negative 7.3% return of the Russell 2500 Value Index. While we use the style-neutral Russell 2500 Index as our benchmark, our stock selection process places a large emphasis on valuation, and that emphasis did not provide favorable results over the last 12 months. Valuation historically has proven to have little use as an indicator of short-term stock price movements, but it tends to be correlated with better performance over longer time periods such as 5 years.

Our energy holdings were strong contributors to performance during the year. We maintained a large weight in the sector throughout the period and were rewarded by our individual stock selections, led by greater than 55% returns in each of Helmerich & Payne (a 4.2% position on 12/31/2007), Noble Energy (2.2%) and Southwestern Energy (1.7%). The threat of domestic and possibly global recession is clearly a risk to energy stocks. However, we believe that the long-term fundamentals of the companies, the tight global supply-demand balance, and the increasing challenge in not only replacing declining production, but also adding new supplies of oil and natural gas to meet growing worldwide demand, support an attractive outlook over the next five years for our energy stocks. Energy continues to be our largest sector weight in the portfolio.

The strength in our energy stocks was offset by weakness in holdings in the consumer discretionary and financial sectors. Many of our retail industry investments fell significantly due to economic pressure on consumer spending as well as, in some cases such as Finish Line, company-specific issues. Financial stocks, in our case led by regional banks, were hit hard by the deteriorating credit environment. Hanmi Financial (0.5%) and Sovereign Bancorp (1.1%) both declined more than 50%.

The year-end cash position was 15%. Our relatively large cash holdings during the year added slightly to performance on both an absolute and relative basis, as we earned more on the cash than the 1.4% return for our benchmark. Our preference is to hold less cash, and we will continue to look for attractive opportunities to deploy cash into stocks trading at a discount to intrinsic value.

Thank you for your support, and we look forward to working with you in the coming years.

| | |

| Christopher A. Welch, CFA | Christopher M. Bingaman, CFA | Thomas P. Schindler, CFA Portfolio |

| Portfolio Manager | Assistant Portfolio Manager | Assistant Portfolio Manager |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 9 |

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Small-Mid Cap Fund - Class A(A) and the Russell 2500 Index

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on December 31, 2005. |

| | Past performance is no guarantee of future results. The principal value and investment return of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. |

| | The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

Tabular Presentation of Schedule of Investments |

| |

The table below provides the Small-Mid Cap Fund's sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund's investments.

Sector Allocation | | % of Net Assets |

| Consumer Discretionary | | 17 | % | |

| Consumer Staples | | | 5 | % | |

| Energy | | | 21 | % | |

| Financial | | | 16 | % | |

| Health Care | | | 1 | % | |

| Industrial | | | 14 | % | |

| Information Technology | | | 2 | % | |

| Materials | | | 4 | % | |

| Utilities | | | 5 | % | |

| Cash and Cash Equivalents | | | 15 | % | |

| | | | 100 | % | |

| |

| Page 10 | Diamond Hill Funds Annual Report December 31, 2007 |

|

Diamond Hill Large Cap Fund |

Performance Update |

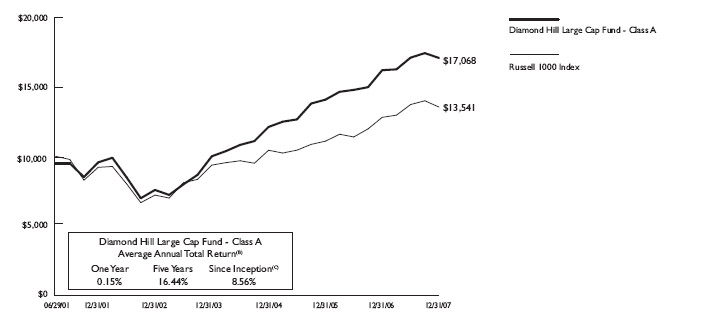

Results (Class A) Since Inception*

| | Year Ended 12/31/07 | Five Years Ended 12/31/07 | Since 6/29/01 Inception |

| Diamond Hill Large Cap Fund (DHLAX) | 5.42% | 17.63% | 9.43% |

| Russell 1000 Index | 5.77% | 13.43% | 4.77% |

| * | The Fund return excludes any sales charges but includes all other expenses. Standardized returns are disclosed on the following page. Results longer than one year are annualized. |

| |

|

Charles S. Bath, CFA Portfolio Manager |

| |

|

William C. Dierker, CFA Assistant Portfolio Manager |

The Diamond Hill Large Cap Fund Class A load-waived shares returned 5.42% in 2007 compared to 5.77% for the Russell 1000 Index. While only approximating market returns in 2007, We remain pleased with the long-term performance of the Fund in both relative and absolute terms. While the second half of 2007 was difficult for the market in general, the long-term returns for the Fund have been attractive.

Energy continued to dominate the portfolio in 2007. For most of the year the portfolio weighting in the sector approximated 20% and the strong performance of these stocks was important to the performance of the overall portfolio. Apache Corp. (a 6.8% position on 12/31/2007) our largest energy holding was up over 60% for the year. Devon Energy (5.9%), our second largest energy holding was up over 30% in 2007. We did make a significant change in our energy holdings when we sold our large position in Conoco Phillips in the 4th quarter to invest in other opportunities in the sector.

Commodity related names not directly tied to energy were also some of the biggest gainers in 2007. Fluor Corp. (1.3%), an engineering company was the biggest percentage gainer for the year. Copper company Freeport McMoran (2.1%) was another large commodity company which increased more than 50% for the year. In a broad sense, it was the commodity and energy stocks which dominated as the biggest positive contributors to the portfolio.

Most of the disappointments in the year were related to the financial services industry or were technology companies reporting disappointing results. Companies such as Lexmark and Advanced Micro Devices reported surprisingly poor results and were eliminated from the portfolio. However, their negative performance was a drag on the portfolio. Financial services companies such as American International Group (3.4%) and Wells Fargo (3.2%) were down due to the turmoil in the financial services sector as well as some disappointment surrounding their operating results. Unfortunately, Merrill Lynch (1.7%) was down over 40% due to the losses in its portfolio related to the subprime mortgage market. Although the performance of the financial services stocks was disappointing, the portfolio’s exposure to that sector was significantly less than the market weighting until we made significant additional purchases at the end of November. This underweighting helped the relative performance of the portfolio.

As of year-end I have been managing the Diamond Hill Large Cap portfolio for over 5 years. I have been pleased with the performance of the portfolio over that time and we want to thank shareholders for their continued support.

| | |

| |

| Charles S. Bath, CFA | Bill C. Dierker, CFA |

| Portfolio Manager | Assistant Portfolio Manager |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 11 |

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Large Cap Fund - Class A(A) and the Russell 1000 Index

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

(C) Class A shares commenced operations on June 29, 2001.

Past performance is no guarantee of future results. The principal value and investment return of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| |

Tabular Presentation of Schedule of Investments |

| |

The table below provides the Large Cap Fund's sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund's investments.

Sector Allocation | | % of Net Assets |

| Consumer Discretionary | | | 11 | % | |

| Consumer Staples | | | 10 | % | |

| Energy | | | 21 | % | |

| Financial | | | 21 | % | |

| Health Care | | | 11 | % | |

| Industrial | | | 9 | % | |

| Information Technology | | | 2 | % | |

| Materials | | | 10 | % | |

| Cash and Cash Equivalents | | | 5 | % | |

| | | | 100 | % | |

| |

| Page 12 | Diamond Hill Funds Annual Report December 31, 2007 |

|

Diamond Hill Select Fund |

| |

Performance Update |

| |

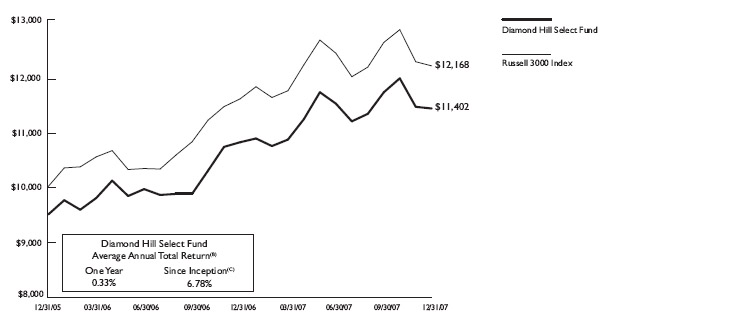

Results (Class A) Since Inception*

| | Year Ended 12/31/07 | Since 12/31/05 Inception |

| Diamond Hill Select Fund | 5.63% | 9.57% |

| Russell 3000 Index | 5.13% | 10.29% |

| * | The Fund return excludes any sales charges but includes all other expenses. Standard returns are disclosed on the following page. |

|

William C. Dierker, CFA Portfolio Manager |

| |

|

Charles S. Bath, CFA Assistant Portfolio Manager |

The year 2007 was mixed for the Diamond Hill Select Fund. The load-waived Class A shares enjoyed a total return of 5.63%. While this performance would normally represent a below average return for a long only equity strategy, it did exceed the 5.13% annual return of the Russell 3000 Index, the Fund’s benchmark, and the Fund’s value peers during a difficult time in the market. Since the inception of the Select Fund at the end of 2005, the Fund’s compounded annual return has been 9.57%. This has trailed the benchmark return of 10.29%. At the beginning of 2007, we were finding better value in large cap stocks. This orientation helped results, as large cap stocks did well, particularly late in the year as investors started to worry about the direction of the economy. The Select Fund’s flexibility allows us to focus the fund’s holdings on where we see the best values. While we are agnostic when it comes to capitalization, the Fund is still heavily weighted in investments drawn from our Large Cap Fund. We retain the ability to draw upon ideas from our Small-Mid Cap and Small Cap fund. When the market presents us with attractive values in those parts of the market, we take advantage of those opportunities.

During 2007, the fund continued to benefit from our investments in the energy and materials sector. Investments in energy companies Apache (a 6.0% position on 12/31/2007), Devon (5.3%), ConocoPhillips, Anadarko Petroleum (3.4%) and Occidental Petroleum (2.2%) generated important contributions to the return of the Fund. Investments in Fluor (0.8%), Freeport-McMoRan Copper & Gold (2.4%), Union Pacific and Weyerhaeuser also contributed to the performance of the Fund. The fund also benefited by an underweight in the financial sector. The S&P 1500 Financial Index was down over 18% for the year, and being underweighted in financials contributed to our absolute and relative performance. Our underweight in Financials also better positioned us to be able to take advantage of the values that started to emerge in the financial sector late in the year. In 2007, positions that detracted from performance were generally companies that had disappointing performance in their businesses, or were exposed to the difficulties in the mortgage market. These positions included American International Group (3.7%), Lexmark International, Citigroup, Advance Micro Devices, AirTran (1.0%). As of year end, we continued to hold American International Group (3.7%), AirTran (1.0%) and ACCO Brands (0.9%).

The equity market continues to come to grips with the economic and company specific fallout from the dramatic slowdown in the housing market and the associated impacts in the financial markets (asset write-downs, ratings downgrades, significant dilution from new equity capital, etc.). While this is a trying time for investors, we believe that our long-term investment horizon will put us in the enviable position of taking advantage of the opportunities being created by the fear that is increasingly evident in the market. We appreciate your continued support. As fellow shareholders, we will continue to act in your best interests.

| | |

| |

| William C. Dierker, CFA | Charles S. Bath, CFA |

| Portfolio Manager | Assistant Portfolio Manager |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 13 |

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Select Fund - Class A(A) and the Russell 3000 Index

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on December 31, 2005. |

| | Past performance is no guarantee of future results. The principal value and investment return of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. |

| | The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| |

Tabular Presentation of Schedule of Investments |

| |

The table below provides the Select Fund's sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund's investments.

Sector Allocation | | % of Net Assets |

| Consumer Discretionary | | | 13 | % | |

| Consumer Staples | | | 9 | % | |

| Energy | | | 20 | % | |

| Financial | | | 17 | % | |

| Health Care | | | 13 | % | |

| Industrial | | | 9 | % | |

| Information Technology | | | 5 | % | |

| Materials | | | 11 | % | |

| Cash and Cash Equivalents | | | 3 | % | |

| | | | 100 | % | |

| |

| Page 14 | Diamond Hill Funds Annual Report December 31, 2007 |

| |

Diamond Hill Long-Short Fund |

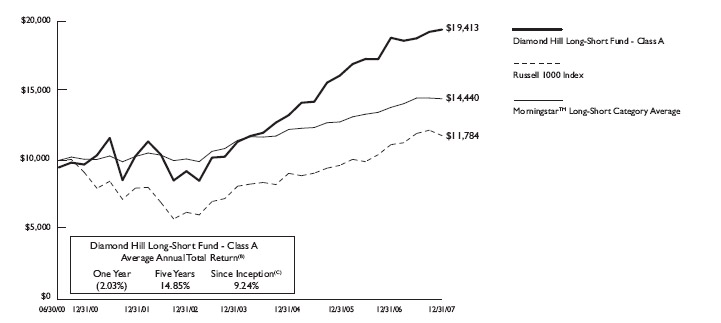

Results (Class A) Since Inception*

| | Year Ended 12/31/07 | Five Years Ended 12/31/07 | Since 6/30/00 Inception |

| Diamond Hill Long-Short Fund (DIAMX) | 3.14% | 16.03% | 10.00% |

| Russell 1000 Index | 5.77% | 13.43% | 2.21% |

| Morningstar™ Long-Short Category Average | 4.50% | 7.39% | 5.01% |

| * | The Fund return excludes any sales charges but includes all other expenses. Standardized returns are disclosed on the following page. Results longer than one year are annualized. |

|

R.H. Dillon, CFA Co-Portfolio Manager |

| |

|

Charles S. Bath, CFA Co-Portfolio Manager |

| |

|

Christopher M. Bingaman, CFA Assistant Portfolio Manager |

The Diamond Hill Long-Short Fund Class A, load-waived shares returned 3.14% in 2007 compared to 5.77% for the Russell 1000 Index and 4.50% for the Morningstar Long-Short Category Average. This year’s anemic return comes in the fifth consecutive year of positive results for the fund and the long-only benchmark. Given the fund’s long-short structure, our expectation is for the fund to perform better than the long-only benchmark in down markets; conversely the fund may do worse in up markets.

Once again in 2007, energy holdings represented our largest exposure for the long portion of the fund and they served the fund well. We have held both Apache (a 6.8% position on 12/31/2007) and Devon (5.6%) for several years, and both stocks were up significantly last year. Another important performer was McDonalds (4.4%), a stock purchased in 2006. In total, the long portion of the fund’s performance was in line with the long-only Russell 1000 Index.

The performance of the short portfolio was disappointing last year. While half of the positions provided a positive contribution to the fund, the three largest positions actually were among the worst performers (for a short position, which means the stock went up). Ironically, two of the three, Apollo (1.6%) and Apple (1.3%) were positive contributors in 2007. The third, Amazon (2.2%) went against us, as the company’s profitability levels were considerably better than our estimates. We increased our estimates of intrinsic value for all three companies, and subsequently trimmed position sizes during the year, however because the stocks appreciated above those higher estimates we ended the year short positions in all three.

During most five year periods, we would expect the stock market to provide positive returns. While we certainly understand that during shorter periods like 12 months we may trail a long-only benchmark during a strong market, over time our goal is to have the short positions provide a positive contribution to return to the portfolio.

We want to thank shareholders for their support in 2007. We look forward to working with you in the years ahead.

| | | |

| | |

| R.H. Dillon, CFA | Charles S. Bath, CFA | Christopher M. Bingaman, CFA |

| Co-Portfolio Manger | Co-Portfolio Manager | Assistant Portfolio Manager |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 15 |

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Long-Short Fund - Class A(A), the Russell 1000 Index and the Morningstar™ Long-Short Category Average

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I-hares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on June 30, 2000. |

Past performance is no guarantee of future results. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| |

Tabular Presentation of Schedule of Investments |

| |

The table below provides the Long-Short Fund's sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund's investments.

Sector Allocation | % of Long Portfolio | | % of Net Assets |

Long Portfolio | | | | | |

| Consumer Discretionary | 9% | | | 11% | |

| Consumer Staples | 7% | | | 8% | |

| Energy | 18% | | | 21% | |

| Financial | 16% | | | 18% | |

| Health Care | 9% | | | 11% | |

| Industrial | 8% | | | 9% | |

| Information Technology | 3% | | | 3% | |

| Materials | 8% | | | 10% | |

| Cash & Cash Equivalents | 22% | | | 9% | |

| | 100% | | | | |

| | | | | | |

Short Portfolio | % of Short Portfolio | | | | |

| Consumer Discretionary | 48% | | | -14% | |

| Consumer Staples | 10% | | | -3% | |

| Health Care | 8% | | | -2% | |

| Industrial | 4% | | | -1% | |

| Information Technology | 15% | | | -5% | |

| Exchange Traded Funds | 15% | | | -5% | |

| | 100% | | | | |

| | | | | | |

Other | | | | | |

| Segregated Cash with Brokers | | | | 30% | |

| | | | | 100% | |

| |

| Page 16 | Diamond Hill Funds Annual Report December 31, 2007 |

|

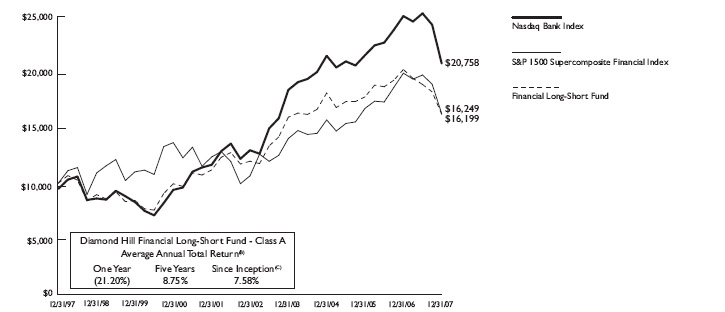

Diamond Hill Financial Long-Short Fund |

Performance Update |

| |

Results (Class A) Since Inception*

| | Year Ended 12/31/07 | Five Years Ended 12/31/07 | Since 8/1/97 Inception |

| Diamond Hill Financial Long-Short Fund (BANCX) | (17.05%) | 9.87% | 10.05% |

| S&P 1500 SuperComposite Financial Index | (18.32%) | 8.79% | 5.57% |

| * | The Fund return excludes any sales charges but includes all other expenses. Standardized returns are disclosed on the following page. Results longer than one year are annualized. |

|

Christopher M. Bingaman, CFA Portfolio Manager |

| |

|

William C. Dierker, CFA Assistant Portfolio Manager |

Thank you for your interest in the Diamond Hill Financial Long-Short Fund.

As evidenced by a negative 17.05% total return of the load-waived Class A shares, 2007 was an extremely challenging year for the Diamond Hill Financial Long-Short Fund. The Fund’s primary benchmark (the S&P 1500 SuperComposite Financials Index) posted a slightly worse total return of negative 18.32%. With the exception of a slight decline in the small cap Russell 2000 Index, U.S. equity indices were generally in positive territory for the year, albeit modestly. The disparity in performance between the financial sector and the rest of the equity market was obviously quite substantial and marked the first time since 1999 that the sector underperformed by such a wide margin. Overall, I would characterize the performance of the Fund in 2007 as disappointing given the cash levels and short positions that were maintained throughout the year. The short portfolio performed very well during the year and provided some very sizable gains. However, given our heavy long bias in the portfolio, these were more than offset by declines in most of our long positions. Especially hard hit were the diversified financials (Citigroup (a 3.7% position on 12/31/2007) and AIG (5.8%)), the investment banks (Merrill Lynch (3.9%) and Morgan Stanley (2.4%)) and most of our mid and small cap bank investments. Upside performers in the sector were few and far between during 2007. In the Fund, two insurance names (Assurant (1.6%) and PartnerRE (1.2%)) were both up nicely during the year, while small cap bank First Charter of Charlotte, NC (1.5%) was added to the portfolio and subsequently announced a merger agreement with Fifth Third at a substantial premium. Also, Bank of New York Mellon (3.1%) completed its merger during the year and continued to perform reasonably well. Finally, as we frequently communicate to both current and prospective investors, we judge ourselves based on long-term returns (rolling five year periods) and on that front remain satisfied that shareholders have received sufficient absolute returns which were also ahead of relevant benchmarks for the period ending December 31, 2007.

Looking forward we expect much better returns in the near future for the financial sector. The dramatically changing credit environment during 2007 caused tremendous unease and in some instances even panic. It now appears that the deterioration in credit and other pressures in many areas of the sector are fully, if not overly, discounted into the stocks. As is often the case with many of the credit sensitive areas (bank, thrifts, etc.), the stocks appear to be valued at near trough valuation levels on well below normalized earnings levels. In terms of fundamentals, many areas of the sector are still struggling however, in many ways the stress of the recent past will allow for substantial improvement going forward. Capacity has been removed in many areas (most notably in mortgage finance) and credit spreads have widened allowing for improved risk-adjusted margins on many credit based products. Also, the changes in the structured finance market may actually help many domestic lending institutions as they once again become the primary source of funds for many types of consumer credit. Therefore, given this outlook for the sector, we have been adding to our long positions and continuing to reduce short exposure. Two examples of recent additions to the Fund are Synovus Financial (2.4%) and Huntington Bancshares (3.6%). In both cases, the stocks are currently trading at substantial discounts to our estimate of intrinsic value and both may be excellent acquisition candidates in the next few years. Regarding merger and acquisition in general, we do not expect a pick up in deal activity in the near term however continued consolidation within the banking and thrift industries during the next couple of years is likely given the continuing secular growth challenges and opportunities for significant efficiency gains. As one might expect from looking at the portfolio, we continue to see the most attractive risk reward situations in the large cap area of the sector, however for the first time in at least three years, many small and mid cap banks are once again priced at very attractive levels.

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 17 |

As in the past, we continue to believe shareholders in the fund will benefit from a relatively concentrated portfolio. We typically hold between 30 and 40 stocks with an average position size of roughly 3%. Also, as many of you already know, we have elected to maintain the portfolio as a long-short fund for the foreseeable future. We do not intend to do this as a ‘hedge’ to mitigate our long exposure/volatility, but instead as a way to enhance our performance over time. Finally, we continually strive to maintain our disciplined process of evaluating both the fundamentals and valuations of our current and prospective investments.

We would like to thank our shareholders for their continued support of the Fund.

| | |

| |

| Christopher M. Bingaman, CFA | William C. Dierker, CFA |

| Portfolio Manager | Assistant Portfolio Manager |

| |

| Page 18 | Diamond Hill Funds Annual Report December 31, 2007 |

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Financial Long-Short Fund - Class A(A), the S&P SuperComposite 1500 Financial Index and the NASDAQ Bank Index

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The average annual total returns shown above are adjusted for maximum applicable sales charge of 5.00%. |

| (C) | Class A shares commenced operations on August 1, 1997. |

Past performance is no guarantee of future results. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| |

Tabular Presentation of Schedule of Investments |

| |

The table below provides the Financial Long-Short Fund's sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund's investments.

| | % of Long | | % of Net |

Sector Allocation | Portfolio | | Assets |

Long Portfolio | | | | | |

Common Stocks: | | | | | |

Finance - Banks & Thrifts | 44% | | | 51% | |

Finance - Broker Dealer | 5% | | | 6% | |

Finance - Diversified | 7% | | | 8% | |

Finance - Specialties | 2% | | | 2% | |

Insurance | 13% | | | 15% | |

| Cash & Cash Equivalents | 26% | | | 8% | |

| Preferred Stocks: | | | | | |

Finance | 2% | | | 2% | |

Real Estate Investment Trust | 1% | | | 2% | |

| | 100% | | | | |

| | | | | | |

Short Portfolio | % of Short | | | | |

| Common Stocks: | Portfolio | | | | |

Finance - Banks & Thrifts | 75% | | | -7% | |

Exchange Traded Fund | 25% | | | -2% | |

| | 100% | | | | |

Other | | | | | |

Segregated Cash with Brokers | | | | 15% | |

| | | | | 100% | |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 19 |

| |

Diamond Hill Strategic Income Fund |

Performance Update |

| |

Results (Class A) Since Inception*

| | | Year Ended 12/31/07 | | Five Years Ended 12/31/07 | | Since 9/30/02 Inception | |

| Diamond Hill Strategic Income Fund (DSIAX) | | | (4.78 | %) | | 6.88 | % | | 7.44 | % |

| Merrill Lynch Domestic Master Index | | | 7.17 | % | | 4.49 | % | | 4.58 | % |

| * | The Fund return excludes any sales charges but includes all other expenses. Standardized returns are disclosed on the following page. Results longer than one year are annualized. |

|

Kent Rinker Co-Portfolio Manager |

| |

|

William Zox, CFA, J.D., LL.M. Co-Portfolio Manager |

| |

|

Rick Moore, CFA Assistant Portfolio Manager |

The year, 2007, was the most difficult year in the history of the Diamond Hill Strategic Income Fund. In fact, the credit conditions that became apparent throughout the second half of the year were unlike any that we have seen in the last 30 years. The Fund's load-waived Class A shares declined 4.78% compared to a gain of 7.17% for the Merrill Lynch Domestic Master Index. The returns for the Index were heavily influenced by a dramatic decline in U. S. Treasury yields. On the other hand, the poor performance of the Fund was primarily caused by our 40-45% exposure to the preferred securities market. This market, which has consistently shown positive results, had a very poor second half of the year and an equally poor 2007. For example, the preferred market had a negative return of 9.2% in the fourth quarter and a negative return of 11.3% for the calendar year.

Since this market caused the negative returns in our portfolio, our year-end comments will focus primarily on the preferred securities area. The first thing to understand is that this market is made up primarily of issues that are backed by financial concerns and some of these issues can be relatively small in total size. Therefore, when the credit markets became frozen and illiquid, these issues were in the center of the storm. Prices dropped dramatically, on little volume.

In response to the deteriorating credit conditions in the markets, we raised our allocation to cash and callable agency securities to a range of 15-30%, and we kept the portfolio at the higher end of this range. While this helped somewhat, we did, however, maintain our large preferred allocation through the balance of the year for several reasons. First, we did not believe that Treasuries offered sufficient yield to meet our income objectives. Second, we felt that preferreds offered attractive yields, with much higher credit quality than high-yield bonds. Within our preferred allocation, we swapped out of a number of non-rated REIT preferreds for preferreds issued by much larger, highly rated financial institutions. Over the last two quarters, this position has been punished by the market. However, over the long-term, these trades should be quite rewarding. All of the preferred securities in the Strategic Income Fund are senior in priority to the common equity. Corporate managers should now realize that their highest priority is to restore the market's faith in their creditworthiness. Virtually all of the issuers in this market are raising capital and doing what they can to shore up their balance sheets.

It is our opinion that, over the next several years, the preferred issuers will focus on restoring their credit and spreads over Treasuries will revert back to a more normal level.

Our confidence in the long-term, from today's levels, is tempered by our concerns with the markets over the next several months and possibly quarters. We still have a difficult credit environment to deal with. However, we look for substantial easing in monetary policy from the Federal Reserve and we will probably see some sort of short-term fiscal policy that will attempt to provide relief to the financial markets. We will also see some dividend cuts and some corporate layoffs.

We believe that the income from our portfolio is quite secure and that the valuations of our holdings are very attractive. Therefore, we are encouraged by our investment potential over a long-term horizon.

| | | |

|  |  |

| Kent Rinker | William Zox, CFA, J.D., LL.M. | Rick Moore, CFA |

| Co-Portfolio Manager | Co-Portfolio Manager | Assistant Portfolio Manager |

| |

| Page 20 | Diamond Hill Funds Annual Report December 31, 2007 |

Comparison of the Change in Value of a $10,000 Investment in the Diamond Hill Strategic Income Fund - Class A(A) and the Merrill Lynch Domestic Master Index

| (A) | The chart above represents the performance of Class A shares only, which will vary from the performance of Class C and Class I shares based on the difference in loads and fees paid by shareholders in the different classes. |

| (B) | The total return shown above is adjusted for maximum applicable sales charge of 3.50%. |

| (C) | Class A shares commenced operations on September 30, 2002. |

Past performance is no guarantee of future results. The principal value and investment return of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| |

Tabular Presentation of Schedule of Investments |

| |

The table below provides the Strategic Income Fund's sector allocation. We hope it will be useful to shareholders as it summarizes key information about the Fund's investments.

Sector Allocation | | % of Net Assets |

| Finance Common Stock | | | 4 | % | |

| REIT Common Stock | | | 3 | % | |

| REIT Preferred Stock | | | 10 | % | |

| Trust Preferred Stock | | | 33 | % | |

| Collateralized Debt Obligations | | | 2 | % | |

| Corporate Bonds - Maturing > 2 Years | | | 22 | % | |

| Corporate Bonds - Maturing or | | | | | |

| Likely to Be Called < 2 Years | | | 4 | % | |

| U.S. Government or Agency Securities | | | 5 | % | |

| Cash and Cash Equivalents | | | 17 | % | |

| | | | 100 | % | |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 21 |

Diamond Hill Small Cap Fund

Schedule of Investments

December 31, 2007

| | | Shares | | Market Value | |

| | | | | | |

Preferred Stock — 1.2% | | | | | |

Financial — 1.2% | | | | | |

| Mid-America Apartment | | | | | |

Communities, Inc. - REIT ◊ | | | 108,854 | | $ | 4,653,509 | |

| | | | | | | | |

Common Stocks — 86.2% | | | | | | | |

Consumer Discretionary — 18.6% | | | | | | | |

Aaron Rents, Inc. ◊ | | | 370,000 | | | 7,118,800 | |

| Acco Brands Corp.* | | | 450,000 | | | 7,218,000 | |

American Greetings Corp. ◊ | | | 371,500 | | | 7,541,450 | |

Belo Corp. ◊ | | | 231,000 | | | 4,028,640 | |

Brink's Co., The ◊ | | | 145,000 | | | 8,662,300 | |

Callaway Golf Co. ◊ | | | 440,400 | | | 7,676,172 | |

Charming Shoppes, Inc.* ◊ | | | 646,200 | | | 3,495,942 | |

K-Swiss, Inc. ◊ | | | 327,100 | | | 5,920,510 | |

MoneyGram International, Inc. ◊ | | | 242,960 | | | 3,734,295 | |

Penske Automotive Group, Inc. ◊ | | | 300,000 | | | 5,238,000 | |

Steiner Leisure Ltd.* ◊ | | | 197,100 | | | 8,703,936 | |

| | | | | | | 69,338,045 | |

| | | | | | | | |

Consumer Staples — 6.2% | | | | | | | |

| Del Monte Foods Co. | | | 500,000 | | | 4,730,000 | |

Flowers Foods, Inc. ◊ | | | 326,700 | | | 7,648,047 | |

| Hanesbrands, Inc.* | | | 300,000 | | | 8,151,000 | |

Lance, Inc. ◊ | | | 120,457 | | | 2,459,732 | |

| | | | | | | 22,988,779 | |

| | | | | | | | |

Energy — 23.9% | | | | | | | |

Berry Petroleum Co. ◊ | | | 178,400 | | | 7,929,880 | |

Cimarex Energy Co. ◊ | | | 400,000 | | | 17,011,999 | |

Encore Acquisition Co.* ◊ | | | 489,298 | | | 16,327,874 | |

Helmerich & Payne, Inc. ◊ | | | 410,300 | | | 16,440,720 | |

Hornbeck Offshore Services, Inc.* ◊ | | | 174,050 | | | 7,823,548 | |

| Lufkin Industries, Inc. | | | 95,000 | | | 5,442,550 | |

| Southwestern Energy Co.* | | | 112,800 | | | 6,285,216 | |

Whiting Petroleum Corp.* ◊ | | | 200,195 | | | 11,543,244 | |

| | | | | | | 88,805,031 | |

| | | | | | | | |

Financial — 14.5% | | | | | | | |

| 1st Source Corp. | | | 263,700 | | | 4,564,647 | |

Banner Corp. ◊ | | | 178,840 | | | 5,138,073 | |

Capital Corp. of the West ◊ | | | 242,100 | | | 4,704,003 | |

Centennial Bank Holdings, Inc.* ◊ | | | 743,300 | | | 4,296,274 | |

First State Bancorp ◊ | | | 483,720 | | | 6,723,708 | |

Hanmi Financial Corp. ◊ | | | 398,000 | | | 3,430,760 | |

| Hanover Insurance Group | | | 135,000 | | | 6,183,000 | |

| Imperial Capital Bancorp, Inc. | | | 167,200 | | | 3,059,760 | |

| Taylor Capital Group, Inc. | | | 235,200 | | | 4,798,080 | |

UCBH Holdings, Inc. ◊ | | | 296,700 | | | 4,201,272 | |

United Fire & Casualty Co. ◊ | | | 236,400 | | | 6,876,876 | |

| | | | | | | 53,976,453 | |

| | | | | | | | |

Health Care — 1.7% | | | | | | | |

| Analogic Corp. | | | 95,275 | | | 6,452,023 | |

| | | | | | | | |

Industrial — 13.9% | | | | | | | |

AirTran Holdings, Inc.* ◊ | | | 1,165,000 | | | 8,341,400 | |

Apogee Enterprises, Inc. ◊ | | | 209,650 | | | 3,587,112 | |

Frontier Airlines Holdings, Inc.* ◊ | | | 310,600 | | | 1,633,756 | |

Gehl Co.* ◊ | | | 100,000 | | | 1,604,000 | |

Greenbrier Companies, Inc., The ◊ | | | 101,400 | | | 2,257,164 | |

Griffon Corp.* ◊ | | | 170,000 | | | 2,116,500 | |

Kaydon Corp. ◊ | | | 110,800 | | | 6,043,032 | |

Lincoln Electric Holdings, Inc. ◊ | | | 97,100 | | | 6,911,578 | |

Toro Co., The ◊ | | | 192,800 | | | 10,496,032 | |

Trinity Industries, Inc. ◊ | | | 144,650 | | | 4,015,484 | |

Werner Enterprises, Inc. ◊ | | | 278,390 | | | 4,740,982 | |

| | | | | | | 51,747,040 | |

| | | | | | | | |

Information Technology — 1.7% | | | | | | | |

| Verigy Ltd.* | | | 231,020 | | | 6,276,814 | |

| | | | | | | | |

Materials — 0.5% | | | | | | | |

Century Aluminum Co.* ◊ | | | 36,100 | | | 1,947,234 | |

| | | | | | | | |

Utilities — 5.2% | | | | | | | |

Integrys Energy Group, Inc. ◊ | | | 147,610 | | | 7,629,961 | |

UGI Corp. ◊ | | | 243,200 | | | 6,627,200 | |

WGL Holdings, Inc. ◊ | | | 157,500 | | | 5,159,700 | |

| | | | | | | 19,416,861 | |

| | | | | | | | |

Total Common Stocks | | | | | $ | 320,948,280 | |

| |

| Page 22 | Diamond Hill Funds Annual Report December 31, 2007 |

Diamond Hill Small Cap Fund

Schedule of Investments (Continued)

December 31, 2007

| | Shares | | Market Value | |

| | | | | | |

Registered Investment Companies — 59.8% | | | | | | | |

| First American Prime | | | | | | | |

| Obligations Fund - Class Z | | | 6,476,206 | | $ | 6,476,206 | |

| Mount Vernon Securities | | | | | | | |

Lending Prime Portfolio †† | | | 173,001,157 | | | 173,001,157 | |

| Reserve Primary Fund - Class 12 | | | 43,479,131 | | | 43,479,131 | |

| | | | | | | | |

Total Registered Investment Companies | | | | | $ | 222,956,494 | |

| | | | | | | | |

Total Investment Securities — 147.2% | | | | | | | |

| (Cost $540,693,405)** | | | | | $ | 548,558,283 | |

| | | | | | | | |

Liabilities In Excess | | | | | | | |

Of Other Assets — (47.2%) | | | | | | (175,964,549 | ) |

| | | | | | | | |

Net Assets — 100.0% | | | | | $ | 372,593,734 | |

| * | Non-income producing security. |

| ** | Represents cost for financial reporting purposes. |

◊ | All or portion of the security is on loan. The total value of the securities on loan, as of December 31, 2007, was $164,626,402. |

†† | Represents collateral for securities loaned. |

REIT - Real Estate Investment Trust

See accompanying Notes to Financial Statements.

Diamond Hill Small-Mid Cap Fund

Schedule of Investments

December 31, 2007

| | | Shares | | Market Value | |

| | | | | | |

Preferred Stock — 1.0% | | | | | | | |

Financial — 1.0% | | | | | | | |

| Mid-America Apartment | | | | | | | |

Communities, Inc. - REIT ◊ | | | 7,100 | | $ | 303,525 | |

| | | | | | | | |

Common Stocks — 83.8% | | | | | | | |

Consumer Discretionary — 17.2% | | | | | | | |

Aaron Rents, Inc. ◊ | | | 24,300 | | | 467,532 | |

| Acco Brands Corp.* | | | 39,500 | | | 633,580 | |

American Greetings Corp. ◊ | | | 15,600 | | | 316,680 | |

Belo Corp. ◊ | | | 24,900 | | | 434,256 | |

Black & Decker Corp., The ◊ | | | 7,760 | | | 540,484 | |

| Brink's Co., The | | | 9,500 | | | 567,530 | |

Callaway Golf Co. ◊ | | | 24,050 | | | 419,192 | |

Charming Shoppes, Inc.* ◊ | | | 39,500 | | | 213,695 | |

Circuit City Stores, Inc. ◊ | | | 25,000 | | | 105,000 | |

K-Swiss, Inc. ◊ | | | 27,500 | | | 497,750 | |

MoneyGram International, Inc. ◊ | | | 16,903 | | | 259,799 | |

| Office Depot, Inc.* | | | 22,900 | | | 318,539 | |

| Penske Automotive Group, Inc. | | | 16,200 | | | 282,852 | |

Steiner Leisure Ltd.* ◊ | | | 8,000 | | | 353,280 | |

| | | | | | | 5,410,169 | |

| | | | | | | | |

Consumer Staples — 4.7% | | | | | | | |

| Del Monte Foods Co. | | | 41,900 | | | 396,374 | |

Flowers Foods, Inc. ◊ | | | 15,350 | | | 359,344 | |

Hanesbrands, Inc.* ◊ | | | 19,600 | | | 532,532 | |

Lance, Inc. ◊ | | | 8,900 | | | 181,738 | |

| | | | | | | 1,469,988 | |

| | | | | | | | |

Energy — 21.3% | | | | | | | |

Berry Petroleum Co. ◊ | | | 9,200 | | | 408,940 | |

| Cimarex Energy Co. | | | 26,300 | | | 1,118,539 | |

Encore Acquisition Co.* ◊ | | | 30,495 | | | 1,017,618 | |

Helmerich & Payne, Inc. ◊ | | | 33,200 | | | 1,330,324 | |

Hornbeck Offshore Services, Inc.* ◊ | | | 11,200 | | | 503,440 | |

| Lufkin Industries, Inc. | | | 6,300 | | | 360,927 | |

| Noble Energy, Inc. | | | 8,730 | | | 694,210 | |

| Southwestern Energy Co.* | | | 9,620 | | | 536,026 | |

| Whiting Petroleum Corp.* | | | 11,790 | | | 679,811 | |

| | | | | | | 6,649,835 | |

| |

| Diamond Hill Funds Annual Report December 31, 2007 | Page 23 |

Diamond Hill Small-Mid Cap Fund

Schedule of Investments (Continued)

December 31, 2007

| | | Shares | | Market Value | |

| | | | | | |

Financial — 14.7% | | | | | |

| 1st Source Corp. | | | 21,100 | | $ | 365,241 | |

Assurant, Inc. ◊ | | | 6,400 | | | 428,160 | |

| Centennial Bank Holdings, Inc.* | | | 46,200 | | | 267,036 | |

City National Corp. ◊ | | | 6,300 | | | 375,165 | |

Comerica, Inc. ◊ | | | 8,500 | | | 370,005 | |

| Hanmi Financial Corp. | | | 19,595 | | | 168,909 | |

| Hanover Insurance Group | | | 9,700 | | | 444,260 | |

| Huntington Bancshares, Inc. | | | 39,800 | | | 587,448 | |

Sovereign Bancorp, Inc. ◊ | | | 30,300 | | | 345,420 | |

| Synovus Financial Corp. | | | 20,400 | | | 491,232 | |

UCBH Holdings, Inc. ◊ | | | 21,520 | | | 304,723 | |

| United Fire & Casualty Co. | | | 16,700 | | | 485,803 | |

| | | | | | | 4,633,402 | |

| | | | | | | | |

Health Care — 1.6% | | | | | | | |

| Analogic Corp. | | | 7,600 | | | 514,672 | |

| | | | | | | | |

Industrial — 14.3% | | | | | | | |

AirTran Holdings, Inc.* ◊ | | | 79,200 | | | 567,072 | |

| Dover Corp. | | | 18,100 | | | 834,230 | |

Fluor Corp. ◊ | | | 5,000 | | | 728,600 | |

| Lincoln Electric Holdings, Inc. | | | 4,990 | | | 355,188 | |

Pentair, Inc. ◊ | | | 4,700 | | | 163,607 | |

Toro Co., The ◊ | | | 11,200 | | | 609,728 | |

Trinity Industries, Inc. ◊ | | | 18,100 | | | 502,456 | |

| U.S. Airways Group, Inc.* | | | 24,760 | | | 364,220 | |

Werner Enterprises, Inc. ◊ | | | 20,810 | | | 354,394 | |

| | | | | | | 4,479,495 | |

| | | | | | | | |

Information Technology — 1.7% | | | | | | | |

| Verigy Ltd.* | | | 19,485 | | | 529,407 | |

| | | | | | | | |

Materials — 3.5% | | | | | | | |

| Domtar Corp.* | | | 67,060 | | | 515,691 | |

| MeadWestvaco Corp. | | | 18,500 | | | 579,050 | |

| | | | | | | 1,094,741 | |

| | | | | | | | |

Utilities — 4.9% | | | | | | | |

| Energen Corp. | | | 7,000 | | | 449,610 | |