Filed by NSTAR Pursuant to Rule 425

Under the Securities Act of 1933

And Deemed Filed Pursuant to Rule 14a-12

Under the Securities Exchange Act of 1934

Subject Company: NSTAR

Commission File No.: 333-170754

Overview of the Announced NU/NSTAR Merger December 6, 2010 |

2 Safe Harbor Information Concerning Forward-Looking Statements In addition to historical information, this filing may contain a number of “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. Words such as anticipate, expect, project, intend, plan, believe, and words and terms of similar substance used in connection with any discussion of future plans, actions, or events identify forward-looking statements. Forward-looking statements relating to the proposed merger include, but are not limited to: statements about the benefits of the proposed merger involving NSTAR and Northeast Utilities, including future financial and operating results; NSTAR’s and Northeast Utilities' plans, objectives, expectations and intentions; the expected timing of completion of the transaction; and other statements relating to the merger that are not historical facts. Forward-looking statements involve estimates, expectations and projections and, as a result, are subject to risks and uncertainties. There can be no assurance that actual results will not materially differ from expectations. Important factors could cause actual results to differ materially from those indicated by such forward-looking statements. With respect to the proposed merger, these factors include, but are not limited to: risks and uncertainties relating to the ability to obtain the requisite NSTAR and Northeast Utilities shareholder approvals; the risk that NSTAR or Northeast Utilities may be unable to obtain governmental and regulatory approvals required for the merger, or required governmental and regulatory approvals may delay the merger or result in the imposition of conditions that could reduce the anticipated benefits from the merger or cause the parties to abandon the merger; the risk that a condition to closing of the merger may not be satisfied; the length of time necessary to consummate the proposed merger; the risk that the businesses will not be integrated successfully; the risk that the cost savings and any other synergies from the transaction may not be fully realized or may take longer to realize than expected; disruption from the transaction making it more difficult to maintain relationships with customers, employees or suppliers; the diversion of management time on merger-related issues; the effect of future regulatory or legislative actions on the companies; and the risk that the credit ratings of the combined company or its subsidiaries may be different from what the companies expect. These risks, as well as other risks associated with the merger, are more fully discussed in the joint proxy statement/prospectus that is included in the Registration Statement on Form S-4 (Registration No. 333-170754) that was filed by Northeast Utilities with the SEC in connection with the merger. Additional risks and uncertainties are identified and discussed in NSTAR’s and Northeast Utilities’ reports filed with the SEC and available at the SEC’s website at www.sec.gov. Forward-looking statements included in this release speak only as of the date of this release. Neither NSTAR nor Northeast Utilities undertakes any obligation to update its forward-looking statements to reflect events or circumstances after the date of this release. |

3 Agenda Rationale and Benefits of Merger Overview of NSTAR Impacts on CL&P and Yankee Gas |

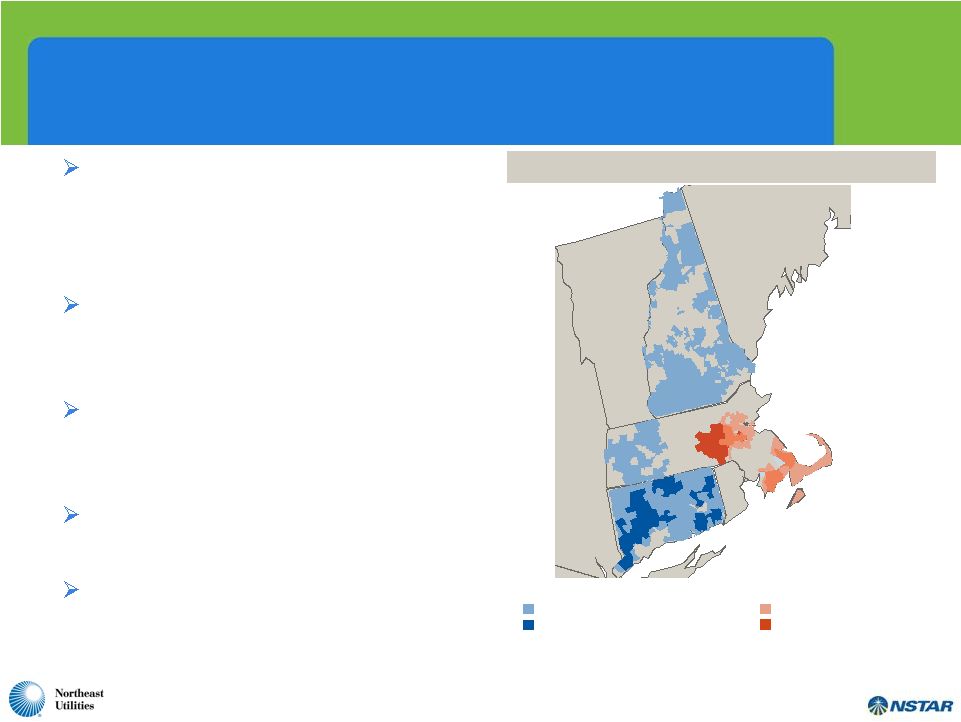

4 A Compelling Combination – Creates Largest Utility Company in New England Significant transmission investment opportunities combined with balance sheet strength provides for substantial growth potential Larger, more diverse and better positioned to support economic growth and renewables in New England Accretive to earnings in Year 1 and provides enhanced total shareholder return proposition Enhances service quality capabilities to the largest customer base in New England Highly experienced and complementary leadership team with proven track record NSTAR Electric Service Area NSTAR Gas Service Area Northeast Utilities Electric Service Area Northeast Utilities Gas Service Area ME NY VT NH M A RI Combined Service Territory |

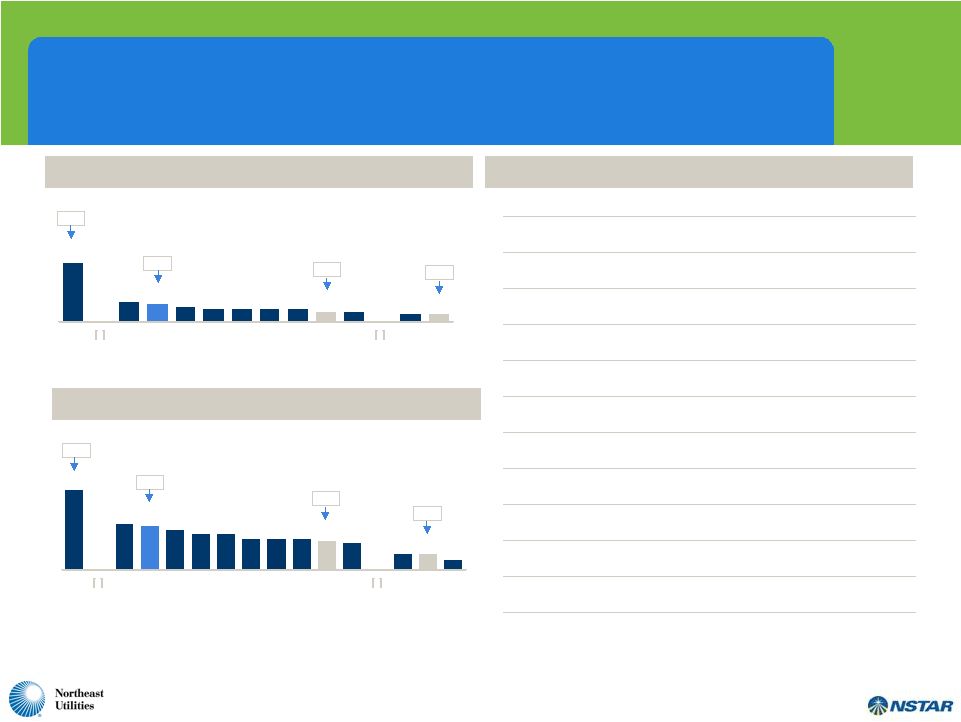

5 A New England Based Utility Holding Company Supporting the Regional Economy Combined Statistics 2009 Revenue ($bn) $8.5 Regulated Utilities 6 Regulated States 3 Electric Customers 3,000,000 Gas Customers 500,000 Electric Transmission (Miles) 4,500 Electric Distribution (Miles) 72,000 Gas Distribution (Miles) 6,300 Generation (MW) 1,200 Total Rate Base ($bn) $10.8 Employees 9,300 $10.8 $9.5 $8.0 $7.0 $6.9 $6.8 $6.6 $5.4 $5.2 $4.1 $4.1 $31.6 SO XEL Pro Forma NU DTE WEC AEE CNP CEG NU SCG TEG NST #16 #21 #1 #29 3.1 3.0 2.7 2.4 2.4 2.1 2.1 2.1 1.9 1.8 1.1 1.1 0.7 5.4 EXC PGN Pro Forma NU ETR AEE D CNP DTE PEG NU POM PNW NST SCG #13 #19 #1 #26 ___________________________ Source: FactSet, company filings. 1. US utility rankings as of 10/15/10, based on companies in the S&P 500 Utilities Index excluding IPPs and Gas LDCs. Ranking by Market Capitalization ($ in billions) Ranking by Electric Customers (in millions) (1) (1) |

6 Specific Benefits to NU A projected ~ 20% dividend increase Cash flow increase to eliminate equity issuance for foreseeable future Likely credit upgrades and reduction in debt issuance leading to lower long-term, short-term interest costs Increased market liquidity Enhanced opportunities to reduce costs over time Ability to achieve higher earnings growth rate |

7 Enhanced Credit Quality Strong balance sheet and cash flows position NU to fund rate base growth program principally through internally generated funds Combined company and operating subsidiaries will have an enhanced credit profile Highest quality business profile Highly diversified earnings and cash flow 100% stock transaction – no new debt issued for merger No long-term debt triggers |

8 Benefits to NSTAR Enhanced earnings and dividend growth outlook Ability to apply strong balance sheet and cash flow to attractive transmission investment opportunities Larger utility footprint provides access to projects and opportunities not available today More diverse and better balanced earnings profile Compelling total return opportunity |

9 Key Merger Terms Timing / Approvals: Expected to close within 9 – 12 months Shareholders, federal, and state Headquarters: Dual – Hartford and Boston Company Name: Northeast Utilities Consideration: 100% NU shares Exchange Ratio: 1.312 shares of NU per NSTAR share Pro Forma Ownership: 56% NU shareholders 44% NSTAR shareholders Pro Forma Dividend: Following close, dividend increase for NU shareholders to NSTAR level Dividend parity for NSTAR shareholders Governance: Chuck Shivery to be non-executive Chairman Tom May to be President and CEO 14 Board members 7 nominated by Northeast Utilities including Chuck Shivery 7 nominated by NSTAR including Tom May Balanced Terms and Governance |

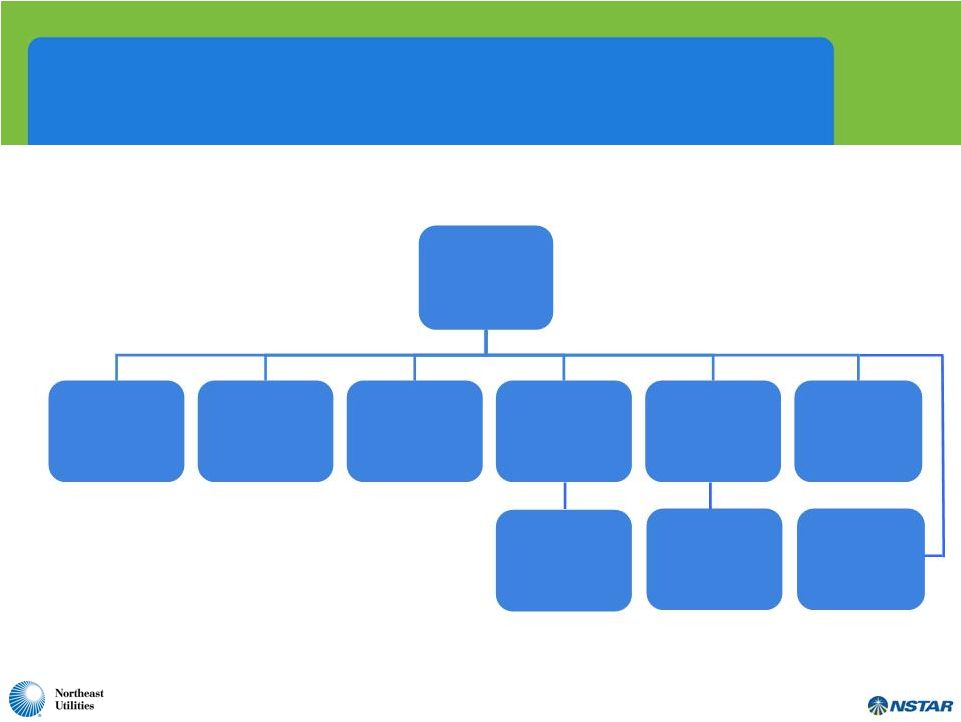

10 Post Merger High Level Company Organization Chart Northeast Utilities Connecticut Light & Power Yankee Energy Systems, Inc. (Holding Company) NU Enterprises, Inc Public Service Company of New Hampshire Western Massachusetts Electric Company NSTAR LLC (Holding Company) NSTAR Companies (NSTAR Electric, NSTAR Gas, etc.) Other NU Companies (NUSCO, Rocky River Realty, etc.) Yankee Gas Services Company |

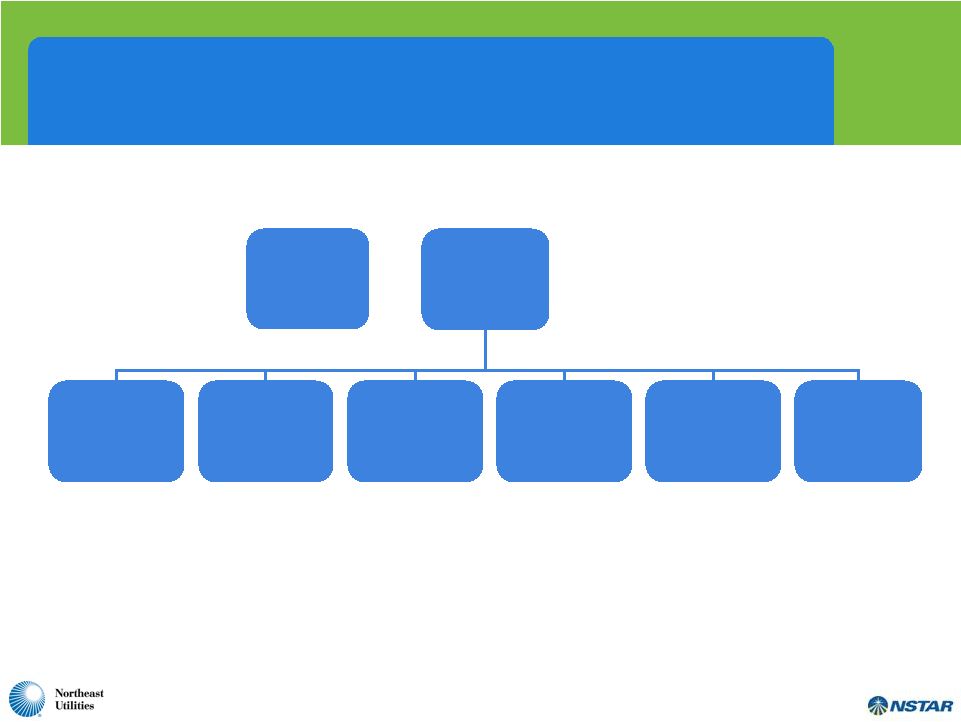

11 Executive Management Organization Tom May President & Chief Executive Officer Greg Butler General Counsel David McHale Chief Administrative Officer Lee Olivier Chief Operating Officer Christine Carmody Human Resources Jim Judge Chief Financial Officer Joe Nolan Corporate Relations Chuck Shivery Non-Executive Chairman |

12 Building A Larger, More Diverse and Better Positioned Regulated Utility Business FERC 31% CT 26% NH 11% MA 32% Rate Base By State / Federal Electric Generation 4% Electric Distribution 54% Gas Distribution 11% Electric Transmission 31% Rate Base By Business Combined 2009 Rate Base: $10.8 billion |

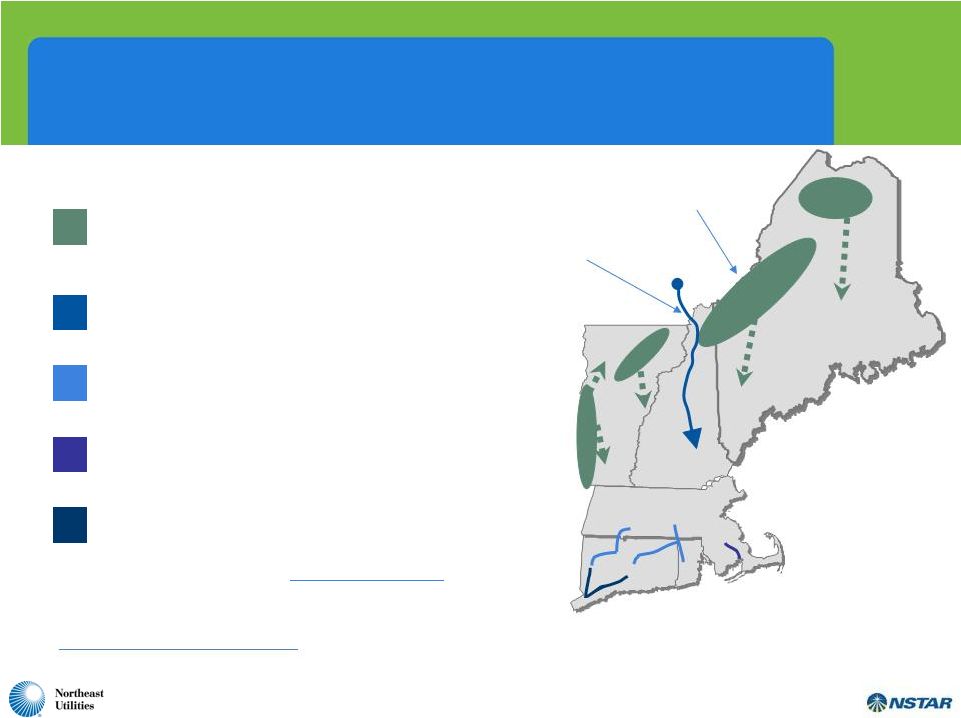

13 Southwest Connecticut Reliability: Projects Complete 1 Connecticut Borders (MA, RI): NEEWS Projects Under Way 3 5 Excellent Transmission Opportunities into Largest New England Load Centers Hydro-Québec- HVDC 4 HVDC Line between Québec and New Hampshire Potential Wind Sites Southeastern Massachusetts (MA): Cape Cod Line 2 Load Center Populations (1) Greater Boston: 4,600,000 Hartford: 1,200,000 Fairfield County: 900,000 1. .Source: IHS Global Insight Winter 2009 – 2010, US Markets: State Economies, U.S. Census Bureau 2009 estimates. 13 Renewables & Clean Energy (ME/NH/VT): Projects in Development/ High Wind potential areas |

14 Regulatory Timeline Oct 2010 Closing Expected in 9 – 12 months Q4 2010 Q1 2011 Q2 2011 Q3 2011 Merger Announced Commence Regulatory Filings File Joint Proxy Statement/Prospectus Regulatory Processes FERC, SEC, NRC, DOJ, MDPU, FCC, Maine PUC Northeast Utilities and NSTAR Shareholder Meetings Develop Transition Implementation Plans Receive Regulatory Approvals Close Merger |

15 NSTAR – A Track Record of Strong Performance • High levels of customer service and reliability • Constructive regulatory outcomes • Solid, consistent financial results • Strong credit profile and positive cash flow |

NSTAR – Key Facts and Figures NSTAR is the largest Massachusetts-based investor-owned electric and gas utility NSTAR transmits and delivers electricity and gas to 1.1 million electric customers in 81 communities and approximately 300,000 gas customers in 51 communities Residential customers comprise 87% of the total electric customers and 90% of the total gas customers For the nine months ended September 30, 2010, NSTAR derived 86% of its operating revenues from electric operations and 14% from gas operations NSTAR employs more than 3,000 people Service Territory MA NSTAR Electric Service Area NSTAR Gas Service Area 16 |

17 NSTAR Electric Provides distribution and transmission electricity service to 1.1 million customers over an area of 1,702 square miles Approximately 35,000 miles of distribution lines with 37% being under ground, and 951 miles of transmission lines Created January 1, 2007 through the merger of Commonwealth Electric Company, Cambridge Electric Light Company, and Boston Edison Company Currently operating under a 2007 – 2012 distribution rate settlement that establishes annual inflation-adjusted distribution rates that are generally offset by an equal reduction in transition rates (stranded cost charges) Distribution rate base at 12/31/09 of $2.5 billion Transmission rates set by the FERC as part of ISO-NE regional system (similar to NU) |

18 NSTAR Gas Distributes natural gas to approximately 300,000 customers over an area of 1,067 square miles Like Yankee Gas, the sales and transportation of gas are divided into two categories – firm and interruptible Supply portfolio consists of natural gas supply contracts, transportation contracts on interstate pipelines, market area storage and peaking services A portion of the gas supply storage is provided by Hopkinton, a wholly- owned subsidiary of NSTAR, with facilities consisting of LNG liquefaction and vaporization, and above-ground storage tanks Last rate proceeding was a settlement in 2005 Commercial, industrial, and residential customers can choose their supplier of natural gas Rate base at 12/31/09 of $500 million |

19 A Long History of Negotiated, Multi-Year Distribution Rate Agreements • 25 years of rate agreements – last litigated rate increase in 1986 • Fully reconciling pension & post-retirement mechanism and recovery of energy supply • Current electric seven year rate plan through December 31, 2012 • 10.5% ROE with +/- 2% neutral zone • Plan to pursue a new rate agreement effective in 2013 |

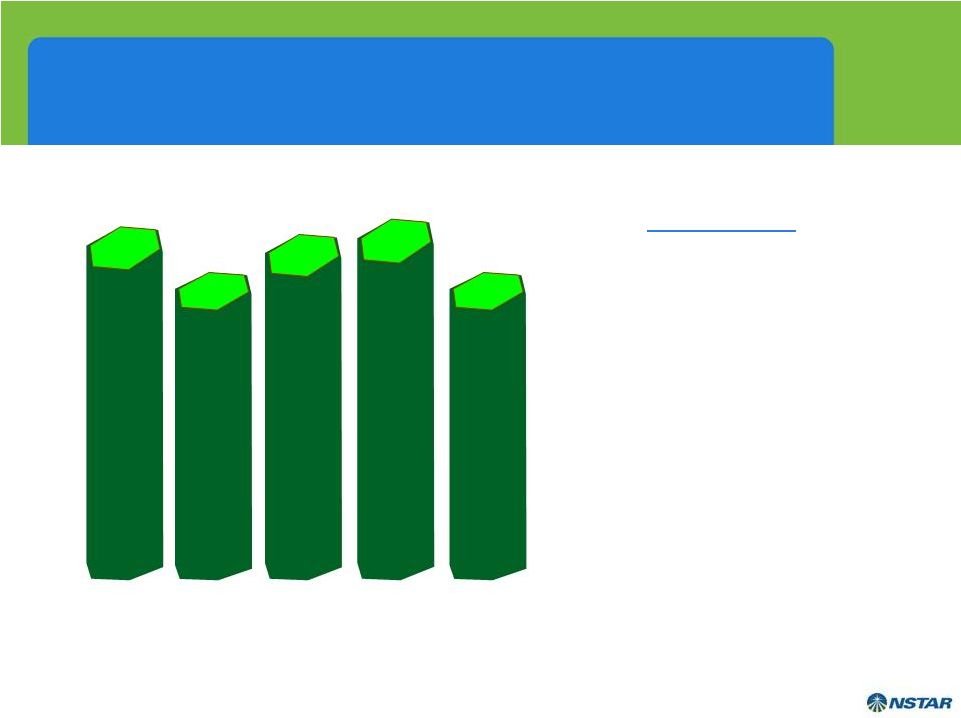

20 History of Disciplined Cost Control $453 2005 $431 2006 2007 Operations & Maintenance Expense $447 $ IN MILLIONS 2008 $454 2009 $431 • Productivity & automation • Performance driven culture • Engaged workforce and constructive union relations • Continuous improvement philosophy Key Drivers |

21 Highest Credit Rating in the Industry NSTAR A+ FPL Group, Inc. A Southern Company A Consolidated Edison, Inc. A- Dominion Resources, Inc. A- DPL Inc. A- Duke Energy Corporation A- Energy East Corporation A- KeySpan Corp. A- Niagara Mohawk Power Corporation A- Vectren Corporation A- ALLETE, Inc. BBB+ Alliant Energy Corporation BBB+ Integrys Energy Group, Inc. BBB+ Kentucky Utilities Company BBB+ Louisville Gas and Electric Company BBB+ MDU Resources Group, Inc. BBB+ MidAmerican Energy Holdings Company BBB+ OGE Energy Corp. BBB+ PG&E Corporation BBB+ Portland General Electric Company BBB+ Progress Energy, Inc. BBB+ SCANA Corporation BBB+ Sempra Energy BBB+ Wisconsin Energy Corporation BBB+ Xcel Energy Inc. BBB+ American Electric Power Company, Inc. BBB CenterPoint Energy, Inc. BBB Cleco Corporation BBB El Paso Electric Company BBB Energy Corporation BBB Exelon Corporation BBB FirstEnergy Corp. BBB Great Plains Energy Inc. BBB Green Mountain Power Corporation BBB Hawaiian Electric Industries, Inc. BBB IDACORP, Inc. BBB Northeast Utilities BBB North Western Corporation BBB Pepco Holdings, Inc. BBB PPL Corporation BBB Public Service Enterprise Group Inc. BBB TECO Energy, Inc. BBB UIL Holdings Corporation BBB Allegheny Energy, Inc. BBB- Ameren Corporation BBB- Avista Corporation BBB- Black Hills Corporation BBB- CMS Energy Corporation BBB- Constellation Energy Group, Inc. BBB- Duquesne Light Company BBB- Edison International BBB- Empire District Electric Company BBB- IPALCO Enterprises, Inc. BBB- NiSource Inc. BBB- Otter Tail Corporation BBB- Pinnacle West Capital Corporation BBB- Westar Energy, Inc. Puget Energy, Inc. BBB- Puget Energy, Inc. BB+ NV Energy, Inc. BB PNM Resources, Inc. BB- Energy Future Holdings Corp. B- #1 NSTAR A+ *As published by EEI |

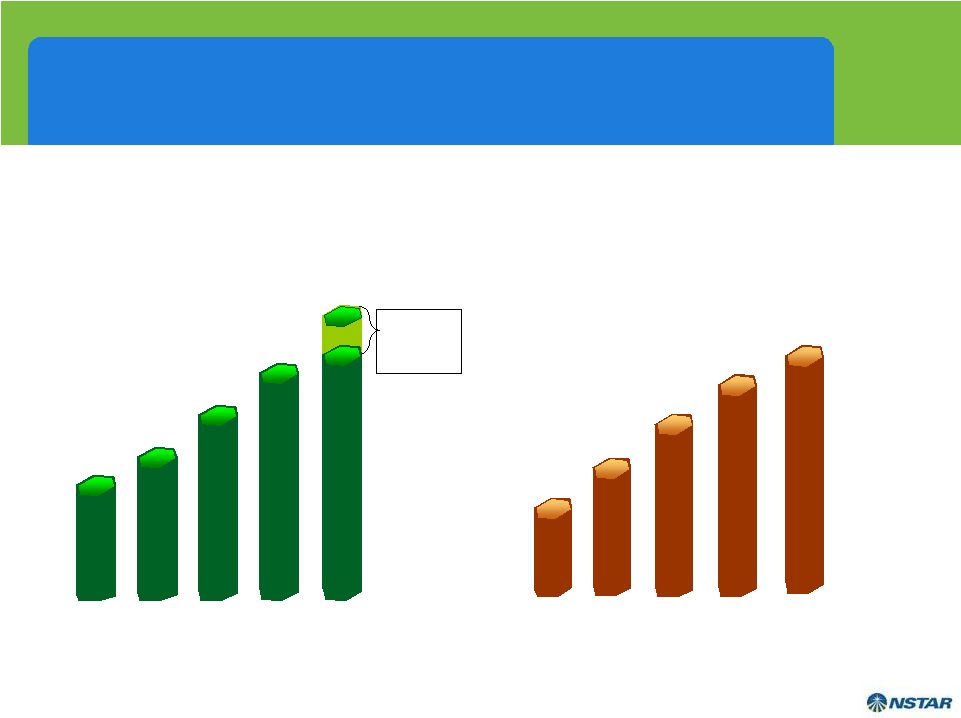

22 Earnings and Dividend Growth $2.22 $1.93 $2.07 2006 2007 2008 2009 $2.37 $2.45 - $2.60 2010 Guidance $1.21 $1.30 $1.40 2006 2007 $1.50 2008 2009 2010 $1.60 Earnings Growth of 7% Outperforms Industry…19 Consecutive Years of Operating Earnings Growth Consistent, Above Average Dividend Growth…12 Consecutive Years of Increase |

23 Impact on CL&P and Yankee Gas No changes to the tariff rates or services of CL&P or Yankee Gas (or other NU affiliates) are planned or contemplated as a condition of the merger There is no consolidation of NSTAR Electric, NSTAR Gas, CL&P, and/or Yankee Gas (or other NU affiliates) that would result from the merger The merger will not result in a change of control of CL&P or Yankee Gas (or other NU affiliates) and they will continue to be first-tier subsidiaries of NU The merger will strengthen the financial integrity and investment capability of NU; a corollary effect will be the enhancement of CL&P’s and Yankee Gas’ capability to maintain reliable and cost-effective delivery systems Over time, the integration of NSTAR and NU is anticipated to produce net savings in costs that will be passed on to customers through reduced costs of service |

24 Creates New England’s premier energy provider More diverse, stable and higher earnings growth profile than could be achieved standalone Highly experienced management teams with proven track records of success Combined company will have one of the most attractive total return profiles in the industry Summary |

25 Appendix |

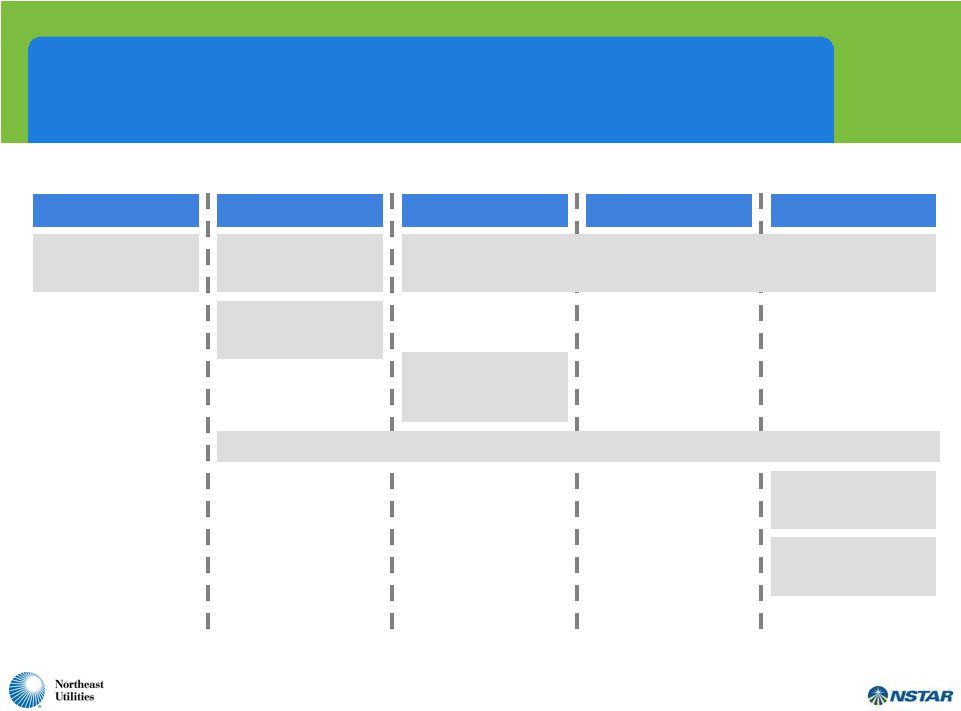

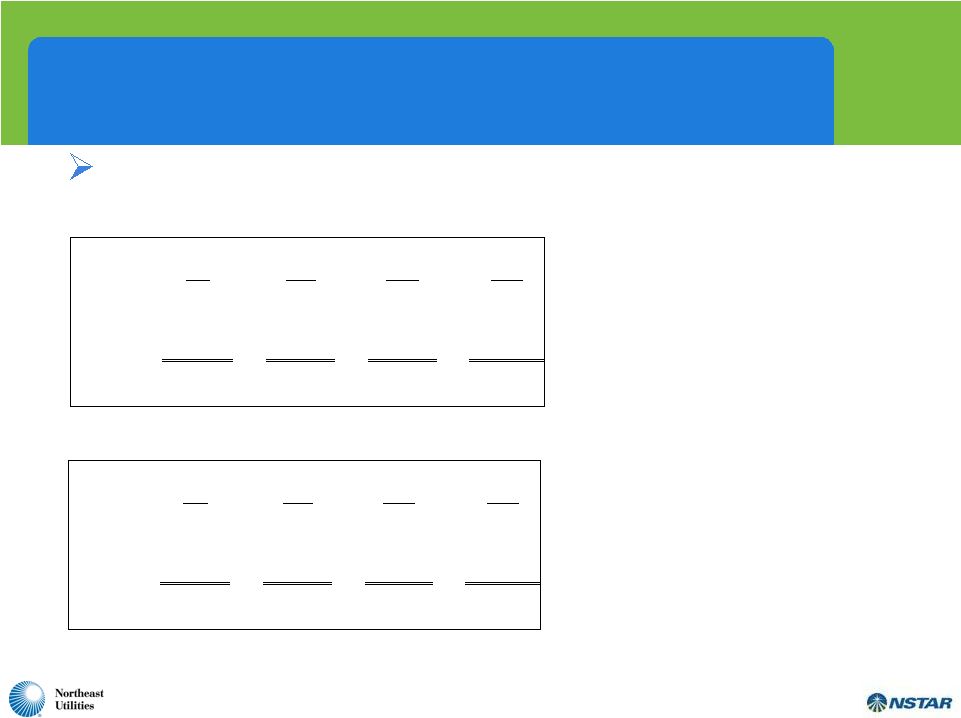

26 NSTAR Electric Comparison of typical bills* Boston Cambridge Commonwealth CL&P Edison Electric Electric Generation $82.88 $59.85 $59.85 $59.85 Transmission $13.39 $11.15 $13.70 $11.80 Delivery $38.34 $48.10 $42.26 $48.96 Other $7.98 $5.14 -$3.07 $11.90 TOTAL BILL $142.59 $124.24 $112.74 $132.51 Non-Generation $59.71 $64.39 $52.89 $72.66 Residential (Based on 750 kWh per Month) Boston Cambridge Commonwealth CL&P Edison Electric Electric Generation $1,172 $853 $853 $798 Transmission $182 $372 $204 $160 Delivery $464 $865 $436 $419 Other $142 $69 $1 $159 TOTAL BILL $1,960 $2,159 $1,494 $1,536 Non-Generation $788 $1,306 $641 $738 Commercial (Based on 10,000 kWh per Month & 40 kW (33% Load Factor)) *As published by EEI – Typical Bills, Summer 2010 |

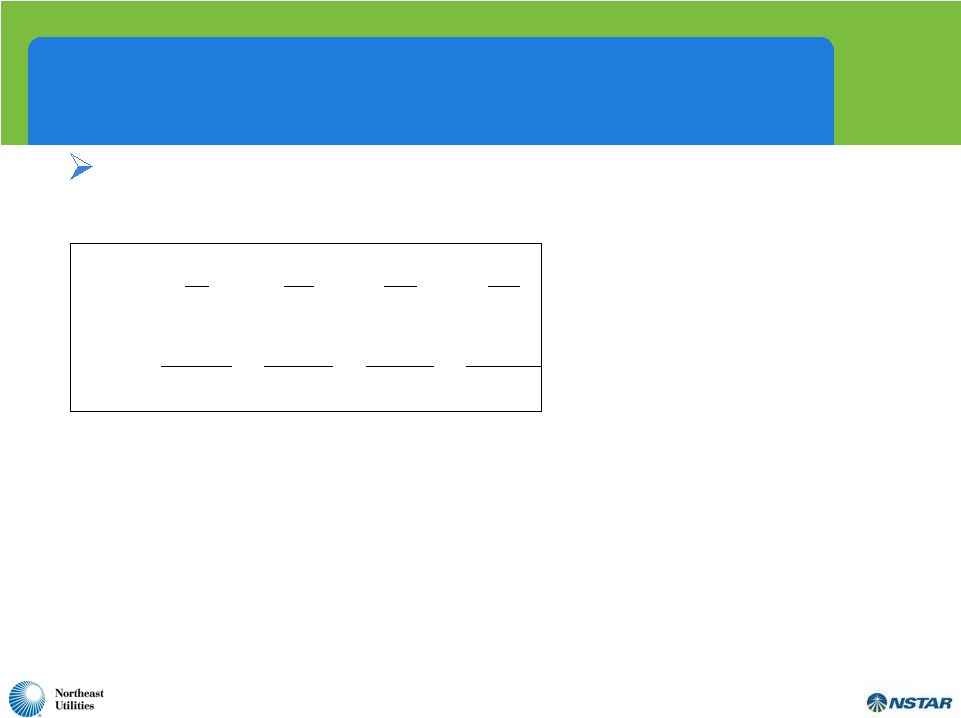

27 NSTAR Electric Comparison of typical bills* Boston Cambridge Commonwealth CL&P Edison Electric Electric Generation $25,582 $28,424 $28,424 $28,236 Transmission $5,368 $6,220 $4,987 $6,316 Delivery $7,404 $17,829 $7,285 $8,975 Other $4,208 $3,262 -$611 $6,810 TOTAL BILL $42,562 $55,735 $40,085 $50,337 Non-Generation $16,980 $27,311 $11,661 $22,101 Industrial (Based on 400,000 kWh per Month & 1,000 kW (54% Load Factor)) *As published by EEI – Typical Bills, Summer 2010 |

Additional Information and Where To Find It

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. In connection with the proposed merger between Northeast Utilities and NSTAR, on November 22, 2010, Northeast Utilities filed with the SEC a Registration Statement on Form S-4 (Registration No. 333-170754) that includes a preliminary joint proxy statement of Northeast Utilities and NSTAR that also constitutes a preliminary prospectus of Northeast Utilities. These materials are not yet final and may be amended. Northeast Utilities and NSTAR will mail the final joint proxy statement/prospectus to their respective shareholders.Northeast Utilities and NSTAR urge investors and shareholders to read the joint proxy statement/prospectus regarding the proposed merger when it becomes available, as well as other documents filed with the SEC, because they will contain important information.You may obtain copies of all documents filed with the SEC regarding this proposed transaction, free of charge, at the SEC’s website (www.sec.gov). You may also obtain these documents, free of charge, from Northeast Utilities’ website (www.nu.com) under the tab “Investors” and then under the heading “Financial/SEC Reports.” You may also obtain these documents, free of charge, from NSTAR’s website (www.nstar.com) under the tab “Investor Relations.”

Participants in the Merger Solicitation

Northeast Utilities, NSTAR and their respective trustees, executive officers and certain other members of management and employees may be soliciting proxies from Northeast Utilities and NSTAR shareholders in favor of the merger and related matters. Information regarding the persons who may, under the rules of the SEC, be deemed participants in the solicitation of Northeast Utilities and NSTAR shareholders in connection with the proposed merger will be set forth in the joint proxy statement/prospectus when it is filed with the SEC. You can find information about NSTAR’s executive officers and trustees in its definitive proxy statement filed with the SEC on March 12, 2010. You can find information about Northeast Utilities’ executive officers and trustees in its definitive proxy statement filed with the SEC on April 1, 2010. Additional information about Northeast Utilities’ executive officers and trustees and NSTAR’s executive officers and trustees can be found in the above-referenced Registration Statement on Form S-4 when it becomes available. You can obtain free copies of these documents from NSTAR and Northeast Utilities using the website information above.