FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of July, 2020

Brazilian Distribution Company

(Translation of Registrant’s Name Into English)

Av. Brigadeiro Luiz Antonio,

3142 São Paulo, SP 01402-901

Brazil

(Address of Principal Executive Offices)

(Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F)

Form 20-F X Form 40-F

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule

101 (b) (1)):

Yes ___ No X

(Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule

101 (b) (7)):

Yes ___ No X

(Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.)

Yes ___ No X

|

São Paulo, July 29, 2020 - GPA [B3: PCAR3; NYSE: CBD] announces its results for the 2nd quarter of 2020. All comparisons are with the same period in 2019, except where stated otherwise. In addition, as from 2019, the results include the effects of IFRS 16/CPC 06 (R2) – Leases, which eliminates the distinction between operating and financial leases and requires the recognition of a financial asset and liability related to future leases discounted to present value for virtually all lease agreements of our stores.

2Q20 RESULTS

The following comments refer to numbers after the application of IFRS 16, unless indicated otherwise. The operations of Grupo Éxito related to 2Q20 are included in GPA’s consolidated results and the variations in relation to 2Q19 (pro forma) are for comparison purposes only.

| Operating and Financial Performance | Consolidated Gross Revenue of R$ 22.9 billion in 2Q20, +61.1% in total sales and +19.3% in pro forma1, highlighting the strong increase of GPA operations in Brazil (+20.1%), superior than the market performance in the period. The successful expansion of Assaí (21 stores opened in the last 12 months), optimization of the Multivarejo store portfolio and the expressive acceleration of digital ecosystem explain this performance. Grupo Éxito continues to report consistent growth, despite the scenario of important restrictions on the movement of people, especially in Colombia. The multi-channel, multi-format and multi-region strategy once again proves successful, with rapid adaptability and strong adherence to client demands and new consumption conditions, which is also reflected on the growth in online sales. ▪ GPA Brazil (Food)2: R$ 17.1 billion, significant growth of 20.0% in total sales, 12.8% in ‘same-store’ sales and 14.8% in ‘same-store’ sales excluding gas stations and drugstores. ✔ Assaí: R$ 9.0 billion (+R$ 1.9 billion vs. the prior year – the biggest historical increase registered in a quarter), with growth of 26.4% in total sales and 10.0% in ‘same-store’ sales. The highlight was the accelerated expansion of new stores and the higher sales to individual consumers – more than offsetting the challenges of the food service segment in Brazil. ✔ Multivarejo: R$ 8.0 billion, significant growth of 13.6% in total sales and 15.8% in ‘same-store’ sales. Excluding the negative effect from the gas station (-37.0%) and drugstore (-15.4%) operations, ‘same-store’ sales grew 20.3%. There was strong sales performance in all banners, with an increase of 3.7x in online sales being the highlight, already representing 5.6% of food sales in Multivarejo and 15.3% of sales in the Pão de Açucar banner. ▪ Grupo Éxito: R$ 5.8 billion, which represents solid growth of 17.0% in pro forma sales and 6.0% in ‘same-store’ sales in a constant currency, despite the challenging scenario in Colombia. The highlight was the growth of innovative formats: Éxito Wow (+15.3%) and Carulla FreshMarket (+27.6%), which confirm the effectiveness of the strategy adopted by the Company. Uruguay registered a strong ‘same-store’ sales in a constant currency (+13.1%), driven by well-executed commercial campaigns. The online platform accelerated in all countries and remains an important growth lever, already representing 11.9%3 of total sales.

Consolidated Adjusted EBITDA came to R$ 1.6 billion (+83.2% vs. 2Q19), +32.6% in pro forma and margin of 7.6%, confirming the positive trend in the Brazilian and international operations in all formats and channels. ▪ GPA Brazil (Food)3: R$ 1.2 billion, +29.7% vs. 2Q19 with margin of 7.5% (+70 bps vs. 2Q19). Assaí’s adjusted margin expanded 30 bps to 7.3% (despite the strong comparison base of 7.0%), and Multivarejo had robust growth in both annual (+110 bps) and sequential (+50 bps vs. 1Q20 and +150 bps vs. 4Q19) comparisons, with adjusted margin of 7.7%. The strong sales contributed to the significant dilution of SG&A expenses in both formats, and consequently to margin expansion. ▪ Grupo Éxito: R$ 424 million, +29.2% vs. 2Q19, with margin of 8.1% (+70 bps vs. 2Q19), representing a strong contribution to the consolidated result despite the important challenges related to the restriction of movement of people, which put a higher pressure on the Group’s complementary businesses (Tuya credit cards, Puntos Colombia and Malls).

Net income from continuing operations came to R$ 274 million, +322.0% vs. 2Q19, with margin of 1.3%, reflecting the group’s operational improvement in all formats and the successful strategies adopted since the beginning of the year. Multivarejo’s important recovery, combined with Assaí’s solid performance and the consolidation of strong results of Grupo Éxito more than offset the increase in depreciation and higher cost of debt. | |

| Leverage | ▪ The quarter was marked by strong operating cash inflow and the conclusion of another important step in the process of monetization of mature and non-core assets, which contributed to a reduction of R$ 1.5 billion in net debt vs 1Q20. Thus, net debt went from R$ 10.8 billion to R$ 9.2 billion and Net Debt/EBITDA4 was reduced from 2.5x in 1Q20 to 2.2x in 2Q20. ▪ The Company ended 2Q20 with a strong financial position of R$ 7.7 billion in cash, equivalent to approximately 2x the short-term debt (vs. 120% in 1Q20 and 156% in 2Q19). | |

| |

| Capex | ▪ Gross investments of consolidated GPA came to R$ 536 million. Two (2) Assaí stores were opened and another 16 are under construction (13 organic and 3 conversions), in line with the Company’ strategy. It is important to mention that in the last 12 months, 21 Assaí’ new stores were opened. ▪ The Company reaffirms its expansion and optimization plan; however, due to the pandemic scenario, a few changes in deadlines or postponements may occur. We should end 2020 with the opening of 19 Assaí stores, conversions of 38 Extra Super into Mercado Extra, refurbishment of 8 Pão de Açúcar stores in the latest generation model. In Grupo Éxito we expect between 5 to 7 stores (from openings, conversions and remodeling), focused on innovative models Éxito WOW, Carulla FreshMarket and Surtimayorista by the end of the year. |

1 Pro forma: results of Grupo Éxito in 2Q19 included in the consolidated result for comparability purposes only;

2 GPA Brazil: GPA Food Brazil does not include result of “Others” (Cheftime, Stix Fidelidade and James);

3 Grupo Éxito’s online sales include Marketplace GMV

4 Pre-IFRS16 adjusted, accumulated in the last 12 months.

2Q20 RESULTS

Consolidated GPA:

2Q20

(1) Other: Includes the operations with most recent initiatives, such as James Delivery, Cheftime and Stix Fidelidade.

(2) Pro forma variation includes the results of Grupo Éxito in 2Q19 as if it were part of the group in the past and is presented for comparison purposes only.

(3) To reflect the calendar effect, the following reductions were made in 2Q20: 10 bps in GPA Food (10 bps in Assaí and 20 bps in Multivarejo) as well as 00 bps in Grupo Éxito.

(4) Includes increases in constant exchange rate for the international operations.

(5) Excludes the gas station and drugstore operations.

Significant growth in pro forma sales (+19.3%), driven by: i) accelerated expansion of Assaí’ banner (+26.4%), which opened 3 stores in 2020, despite a scenario marked by uncertainties due to the pandemic, and ii) strong growth in the retail operations at Multivarejo (+13.6%). There was an important recovery in Hypermarket (+19.3%) and 3.7x growth in online sales, which remain an important growth platform for the group, already accounting for 5.6% of food sales.

The international operations, demonstrated by Grupo Éxito, continued to post solid growth in pro forma basis (+17.0%) and in ‘same-store’ sales at constant exchange rate (+6.0%). Colombia’s operation, which represents 76% of Grupo Éxito’s total sales, grew 3.4% in ‘same-store’ sales in 2Q20, despite the scenario of strong restrictions on movement of people during the pandemic. The growth in food sales remains strong, especially in innovative and online formats (which represents 14.7%6 of sales in Colombia and 11.9%6 of the group total sales). Uruguay, the second largest market, continued to post strong growth (+25.6% in total sales and +13.1% in ‘same-store’ sales), driven by highly successful campaigns and strong expansion of the omnichannel format.

(6)Online sales of Grupo Éxito include marketplace GMV.

| |

(1) GPA Brazil results does not include results of “other businesses” (Stix, James and Cheftime); (2) Operating income before interest, tax, depreciation and amortization; (3) Adjusted for Other Operating Income and Expenses; Note: Tax credits were not materially different from previous quarters.

“The second quarter results reflect the success of our multi-channel, multi-format and multi-region strategy and of our digital ecosystem. We overcame important operational challenges posed by the new economic and consumption scenario, and reported strong and positive sales performance in all the retail formats we operate. In addition to the important growth in the food segment and the strong recovery in the non-food segment, we registered an accelerated growth in food e-commerce, which proved highly profitable and remains a major growth platform, both in Brazil and the international operations. The strong level of sales promoted significantly dilution of fixed expenses, which enabled us to attain important operating results, with EBITDA growth in all businesses and extremely healthy margins.

Assaí proved to be very resilient, attracted new individual clients and more than offset the challenges faced by the food service segment in the period. Multivarejo showed that its portfolio is highly aligned with consumers’ needs and new consumption models, with an important recovery at hypermarket and ensuring its leadership in the e-commerce segment in Brazil. Grupo Éxito reported growth with strong margins, despite facing significant restrictions on the movement of people in Colombia, its largest market, thereby contributing to the Company’s strong results.

We closed the quarter with net income from continuing operations of R$ 274 million and a robust financial position of R$ 7.7 billion in cash (approximately 2x higher than the short-term debt) which gives us the confidence to affirm that we are increasingly prepared for the huge challenges ahead.”

Peter Estermann – CEO of GPA

| |

I. OPERATING PERFORMANCE BY BUSINESS

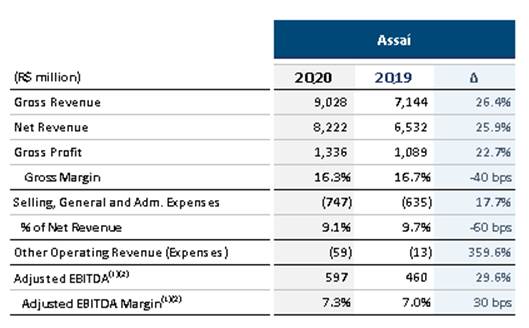

Assaí:

2Q20 and 1H20

(1) To reflect the calendar effect, 10 bps was reduced in Assaí in 2Q20.

Another quarter of strong total sales growth (+26.4%), driven by the successful expansion of the banner, effective commercial activities and higher consumption at home during quarantine, given that sales to individual consumers more than offset the challenges faced by the food service segment in Brazil.

Gross revenue was R$ 9.0 billion in the quarter (+26.4%), up R$ 1.9 billion from the same period of the previous year, due to the strong performance of the 39 stores opened in the last 24 months, which are still in maturation period, but already account for around 24.0% of the banner's total sales.

‘Same-store’ sales posted significant growth of 10.0%, despite the strong comparison base (+8.1% in 2Q19), showing the format’s capacity to adapt and its resilience. The growth in sales to individual consumers and resellers since the start of the pandemic more than offset the lower demand from food service. The successful commercial campaigns, such as “Mothers’ Week,” “Groceries Festival” and “Cleaning and Personal Care Festival,” combined with the forging of partnerships with governments and NGOs for sale of food staple baskets, contributed to this strong growth.

In line with the banner’s plan to expand rapidly to other regions of Brazil, two stores were opened in the quarter, one in Mato Grosso do Sul and another in Maranhão. Sixteen (16) stores are under construction and should be inaugurated in the next semester, with three Extra Hiper stores in the process of conversion and 13 organic stores, in line with the initial expectation of opening stores for 2020, despite the pandemic scenario and the restrictions for construction of the sites.

Passaí cards amount to approximately 1.1 million since their launch, with over 740,000 active cards. Card penetration currently stands at 5.3%, reinforcing the value proposition for customers.

The rollout of credit and debit card POS machines under the Passaí brand was concluded in July 2020 and reached all of the banner's stores with great customer receptivity.

Gross profit was R$1.3 billion, with gross margin of 16.3%. This margin level is mainly due to the large portfolio of stores that still in the maturation curve, which means they have not yet captured the full potential of the banner's stores. A highly competitive price policy was maintained, despite the scenario of higher food inflation.

Selling, general and administrative expenses came to R$ 747 million, corresponding to 9.1% of net sales, lower than revenue growth (-60 bps vs. 2Q19). The strategy to maintain its price policy during the quarter (which resulted in strong sales growth), contributed significantly to the dilution of fixed expenses and supported the consequent improvement in EBITDA margin.

| |

Adjusted EBITDA continued presenting solid growth, to R$ 597 million in 2Q20 (+29.6%), with margin expansion of 30 bps when compared to the same period last year, reaching 7.3%.

(1) Operating income before interest, tax, depreciation and amortization. (2) Adjusted for Other Operating Income and Expenses.

Multivarejo:

2Q20

(1) Includes sales by Delivery and rental revenue from commercial centers.

(1) To reflect the calendar effect, 20 bps was reduced in Multivarejo in 2Q19.

Significant growth in ‘same-store’ sales excluding gas stations and drugstores (+20.3%), with all retail operations presenting a strong performance. The result in the quarter was driven mainly by: i) continuous improvements due to optimization of the store portfolio - which is increasingly adapted to the different demands of consumers and new consumption models; ii) strong recovery in Hypermarket - with the new value proposition of the non-food segment being the highlight; and iii) strong growth in e-commerce - a platform of strategic importance that offers profitable growth to the Company.

| |

Gross revenue grew 13.6% in the quarter while ‘same-store’ sales excluding gas stations and drugstores reached +20.3%, with strong performance in all retail formats and important growth of 11.6% in total food sales (+13.3% ‘same-store’ food sales). The highlights were: i) significant recovery in hypermarkets, with positive impact of the new value proposition of the non-food segment (+42.7 vs. 2Q19 and +51.5% ‘same-store’), ii) the accelerated growth in online food sales (+272%) and iii) the significant growth in the renovated stores. All operations, except gas stations and drugstores, benefitted from the stronger demand due to pandemic scenario, with market share gains in all months of the quarter. It is worth mentioning that the dynamic of lower customer traffic at stores with more complete baskets, continued during the observed period.

Highlights by banner:

| ● | Extra Hyper: Significant growth in ‘same-store’ sales of 22.4%, driven by the model’s strong alignment with consumers’ needs, that during the pandemic started to consume based on the one-stop-shop model (lower traffic in stores, but more complete baskets). The non-food segment registered solid growth, benefitted by its new value proposition (new agreements with suppliers, assortment more adherent to consumer demands and more optimized inventories). The sale of products related to remote work (chairs, desks, IT items), gifts during Mothers’ Day campaign (smartphones and other electronic devices) and items related to spending more time at home (home appliances, toys and games) were the highlights. | |

| ● | Pão de Açúcar: Strong ‘same-store’ sales growth of 15.1% in 2Q20, driven by the excellent performance of 46 stores renovated for the next generation concept (+18.3% in the period). Renovated stores already represent 41% of banner’s total sales, and there is an intention to convert more ~10 stores in the following months. 2Q20 was also marked by successful and well-executed commercial initiatives, such as the wine campaign held in May that sold 230,000 bottles in a single day, as well as the “Off Price” and “My Discount” campaigns, which already represent around 30% of store sales. | |

| ● | Mercado Extra: Consistent sales performance, with strong expansion of 17.4% in ‘same-store’ sales in 2Q20. The format’s growth outpaced the performance of stores not converted yet, despite the strong comparison base from last year. The neighborhood format proved successful and aligned with consumers who search for stores near their homes during the period of social isolation. |

| ● | Compre Bem: Strong ‘same-store’ sales, with significant growth of 53.1%. The stores converted during 2018 (which already had a strong comparison base) and converted in 2019 were the highlight. In addition to the continuous gain of new clients and increase in volumes, the banner continues to develop and in May 2020 started its food e-commerce operations in the interior of the São Paulo State, with delivery service performed by its brick-and-mortar stores. |

| ● | Proximity: Important ‘same-store’ sales growth of 25.6%, maintaining the strong double-digit growth already observed in recent quarters, despite the impacts caused by the new consumer standard during the pandemic. The Mini Extra and Minuto Pão de Açúcar formats reported a good performance and the convenience stores faced challenges related to the reduction in traffic (-37.8%). Highlight for campaigns related to private-label products and the “Pão de Açúcar Mais” and “Clube Extra” apps. The “Aliados” program expanded significantly its base and contributed positively to the format’s performance in the quarter. |

Private-Label Brands: In 2Q20, there were important campaigns for Private-Label Brands, which continued to be one of the Company’s growth pillars, reaching penetration of 19.1%[1] in Multivarejo’s food sales(+160 bps vs. 2Q19 considering the new criteria).

Gross profit was R$ 1.9 billion in 2Q20, with margin of 25.7%. This is the second sequential quarter with significant improvement in gross margin (+60bps vs. 1Q20 and +170 bps vs. 4Q19), supported by successful commercial activities and strong reduction in shrinkage (+90 bps vs. 4Q19).

1 Penetration of private-label brands considers the change in perimeter, with integration of all the product categories made by the Company directly in the stores (bakery, butchery, pizzas, etc). Based on the old perimeter, penetration would have reached 14.5%, a 220 bps increase compared to 2Q19.

| |

The gross margin comparison reported in 2Q20 vs 2Q19 reflects the impact of lower income from commercial centers during the pandemic and the higher participation of non-food products in sales (46% of Hypermarket sales in 2Q20 vs. 36% in 2Q19). Excluding these impacts, gross margin of food category would have increased 110 bps, benefitted by the reduction in food promoshare.

Selling, general and administrative expenses totaled R$ 1.4 billion, increasing only 2.0% when compared to 2Q19 and corresponding to 18.8% of net sales (-170 bps vs. 2Q19), due to the rigorous control of expenses without affecting service quality. The strong sales growth contributed to additional dilution of SG&A expenses. In the quarter, the main savings were in marketing (less investments in advertising and leaflet distribution), maintenance, utilities, Telecom/IT and administrative expenses.

Adjusted EBITDA grew 29.9%, reaching R$ 563 million, with margin of 7.7% (+110 bps from 2Q19 and +50 bps from 1Q20), supported by strong sales, operating efficiency gains and the strong dilution of expenses in the quarter.

This result shows the excellent management and great capacity to adapt of the various formats in a scenario of high uncertainties, which required rapid changes and resulted in benefits arising from the reduction of social activities and a higher consumption at home, but also important challenges for the gas station, drugstore and commercial center operations.

(1) Multivarejo does not include the result of other complementary businesses. (2) Earnings before interest, tax, depreciation and amortization. (3) Adjusted for Other Operating Income and Expenses.

Digital Ecosystem

Pioneer in e-commerce and loyalty programs, Multivarejo has consistently structured its physical and digital assets over the past few years. These assets, combined with a team-oriented culture, enabled fast adaptation to consumer evolutions, such as the personalization and complete dematerialization of promotions through apps or new e-commerce formats, facilitating the rollout of Express e-commerce and James Delivery in record time. The more than 20 million clients from our loyalty program make our database one of the most advanced regarding consumer knowledge in the country.

The unexpected scenario of the pandemic further accelerated the evolution of clients’ behavior and consumption, giving us more confident of the pertinence of the decisions taken and allowing us to build solid and resilient bases.

| |

The strong performance of food e-commerce consolidated Multivarejo’s leadership position in the online food sales segment in Brazil. We have unique assets in the market, which combined with the group’s operating excellence, establish important competitive advantages and make the digital ecosystem an important growth lever.

| ● | Food e-commerce registered strong growth, and in the first half of 2020 already exceeded total sales for the year 2019 by 25%. In 2Q20, sales grew 272% vs the same period last year, driven by: i) higher number of clients; ii) expansion of Express model (which increased from 94 stores in 2Q19 to 291 stores in 2Q20); iii) inauguration of 2 new small distribution centers; and iv) expansion of James presence to 323 stores (vs. 18 in 2Q19). Currently, online sales account for 5.6% of Multivarejo food sales and 15.3% of Pão de Açúcar banner. E-commerce proved to be profitable and, in the quarter, presented EBITDA margin at higher levels than the average of food retail segment, mainly due to various operating improvement initiatives that resulted in higher productivity and greater business scalability. |

| ● | Loyalty Apps registered over 13 million active downloads, up 42% from the same period last year - representing around 30% of Multivarejo sales and 40% of online sales. Thus, sales from loyal clients already represent 71% of Multivarejo’s total sales, reaching 90% of Pão de Açúcar sales and 62% of Extra sales. |

| ● | James Delivery registered strong sales growth of 1,200% in GMV, 962% in number of orders and 21% in average ticket when compared to 2Q19. In the Retail vertical, the increase was even stronger, reaching over 3,000% in GMV, 1,800% in number of orders, 66% in average ticket, with average spending per client increasing 166%. This growth was supported by customers’ increasing adherence to the platform, which was reinforced by structural initiatives, such as the successful launch of the new subscription platform “James Prime.” Other factors were the higher maturation and penetration in the cities already served, as well as the rollout of operations to new places, expanding the operation from 50 stores prior to the pandemic to 320 stores in over 20 cities. |

| ● | The foodtech Cheftime grew 856% vs 2Q19, driven by the acceleration of in-store presence through a greater number of items from the production center and the beginning of the incorporation of items produced in -store (rotisserie and cafeteria). The period was marked by the launch of the “Cheftime Restaurant,” a delivery service of ready-to-eat meals produced at Pão de Açúcar stores, combining Cheftime’s food expertise with the dark kitchens model and the James app. Cheftime Restaurant already can be found in São Paulo and Rio de Janeiro and has been reporting growth of 19% per week. Finally, the higher demand for convenience during the pandemic also contributed to a strong evolution of digital sales, which more than doubled its size. |

Three new small exclusive distribution centers should be opened in the following months, reinforcing our presence in strategic regions and enabling the group's expansion to unexplored regions. We also expect to expand our non-food product mix and launch a robust marketplace in the second semester of 2020. We continue to invest in technologies that improve customer experience and increase productivity and profitability. Therefore, the Company expects the online channel to reach R$ 1 billion2 in sales in 2020 (almost 3x higher than 2019) through expansion of its operating capacity.

2 It is a mere estimate and should not be understood or treated as guidance.

| |

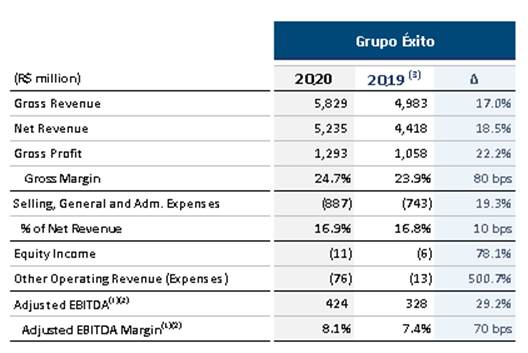

Grupo Éxito:

2Q20

GPA acquired 96.57% of the capital stock of Grupo Éxito on November 27, 2019. Therefore, Grupo Éxito’s results are being considered in Consolidated GPA only in 2Q20. Growth and variations in relation to 2Q19 are merely for comparison purposes.

(1) To reflect the calendar effect, the following reductions were made in 2Q20: 0 bps in Grupo Éxito, with 0 bps in Colombia, 30 bps in Uruguay and -10 bps in Argentina.

(2) Includes the formats Surtimayorista, Malls, Aliados and Other Businesses. (3) Same store presented a growth with a constant currency

Gross revenue achieved R$ 5.8 billion in 2Q20, with growth of 17.0% in total sales, positively influenced by: i) growth of food sales in Colombia and Uruguay, ii) strong growth of online sales in all countries where the group operates and; on the other hand, pressured by: i) challenges related to the strong restrictions of movement of people, especially in Colombia and Argentina, and ii) the reduction of customer traffic in stores located at shopping malls in Uruguay.

The ‘same-store’ sales increased 6.0% in the quarter, mainly due to the strong performance of innovative formats. The 9 Éxito Wow stores grew +15.3%, and already account for 19.2% of Éxito’s banner total sales, and the 13 Carulla FreshMarket stores grew +27.6%, already representing 27.9% of Carulla’s banner total sales.

The highlights by country follow:

| ● | Colombia: ‘same-store’ sales grew 3.4% in constant currency, reflecting the reduced movement of people given the strong restrictions imposed by the government, as well as the postponement of a relevant commercial campaign (“Megaprima”) – that usually was conducted in brick-and-mortar stores but was “transferred” to the online format. There was an accelerated development of the omnichannel platform, whose traffic grew 4x when compared to the same quarter of last year. Currently, 90 stores support the delivery model in Colombia and 360 stores offer sales via WhatsApp and Click & Collect. Online sales already represent 14.7% of total sales in Colombia. |

| ● | Uruguay: consistent and strong growth of 13.1% in ‘same-store’ sales, driven by the very successful commercial activities (mainly in food segment sales) and the robust growth of the omnichannel platform. All banners reported positive performance, especially Devoto (+16.2%) and Disco (+12.9%) and there was significant growth of 58.3% in e-commerce. The development of omnichannel platform remains one of the strategic pillars of the operation in Uruguay, and the pick-up service at Devoto stores was launched in May. |

| ● | Argentina: ‘same-store’ sales of 24.4% in 2Q20 amid a challenging economic scenario in the country. Sales were pressured by: i) strong restrictions on movement of people; ii) reduction in operating hours at stores imposed by the government and iii) prohibition on sales of non-food products in some regions. The positive highlight was the proximity format (+49.6%), benefited from the preference given to convenience formats during the pandemic. The online operations also continue to expand, and a Click & Collect service was launched in 2Q20. |

| |

Gross profit was R$ 1.3 billion, up 22.2% compared to 2Q19, with margin of 24.7%, which is an extremely healthy margin for the group’s retail operations. Gross margin improved by 80 bps based on the pro forma results of the previous year, mostly explained by accounting reclassifications made in 2Q19 between the Selling, General and Administrative Expenses lines and costs. Excluding this effect, margin would be slightly under pressure given the performance of complementary businesses during the pandemic period.

Selling, general and administrative expenses were R$ 887 million, +1.6% vs. 2Q19, equivalent to 16.9% of net sales (vs. 19.8% in 2Q19) with the same impact of the accounting reclassifications made in 2Q19 that were already mentioned. Excluding this effect, there would still be a significant reduction of expenses as a percentage of net revenue due to the continuous focus on controlling expenses adopted by the Group.

Adjusted EBITDA was R$ 424 million (+29.2% vs. 2Q19), with margin of 8.1% (+70 bps vs. 2Q19). There was strong margin expansion despite the big challenges faced by complementary operations such as Malls, Tuya Credit Card and Puntos Colombia, some of which are consolidated by Equity Income (Tuya Credit Card/Puntos Colombia). Note that most of the provisioning for projected delinquency in the financial portfolio was already made in the first semester and the majority of commercial centers and shopping malls are going through a process of gradual reopening since the beginning of June.

Despite the scenario of uncertainties that endures and the recent increase in Covid-19 cases in Colombia, we maintain optimistic on the operations of Grupo Éxito and are working on various fronts to minimize the possible impacts from this scenario. Grupo Éxito should continue to contribute positively to GPA’s consolidated results in 2020, given the strong EBITDA growth already registered during the first semester (12.3%).

(1) Earnings before interest, tax, depreciation and amortization. (2) Adjusted for Other Operating Income and Expenses. (3) Pro forma, for comparison purposes only.

| |

II. EQUITY INCOME

Consolidated equity income amounted to R$ 30 million in 2Q20, an improvement of R$ 39 million from the same period last year. The line is composed of:

i) inflow of R$ 12 million related to the interest held in financial operations in Brazil (36% of FIC) and Colombia (50% of Tuya/Puntos Colombia)

ii) inflow of R$ 18 million related to the 34% stake in CDiscount (one of world’s largest e-commerce businesses), which reported significant growth in its marketplace and better performance of direct sales, as well as a more favorable product mix and operating improvements, contributing positively for 2Q20 results.

III. OTHER INCOME AND EXPENSES

Other Income and Expenses came to an expense of R$ 35 million in 2Q20, explained by expenses related to: i) the integration of Latin America assets and the restructuring of the Brazil operations (sale of 3 Pão de Açúcar stores, closure of 1 Drugstore and opening of 2 Assaí stores in the quarter) and ii) non-recurring impacts related to COVID-19, such as the need for more security at stores, purchasing of COVID-19 tests, financial aid for employees with children and higher expenses with hygiene and cleaning.

Lastly, note that the asset monetization process will continue to produce positive effects in the coming quarters, and by the end of 2020 this line should become stable compared to the previous year in the Brazil perimeter, totaling around R$ 250 million.

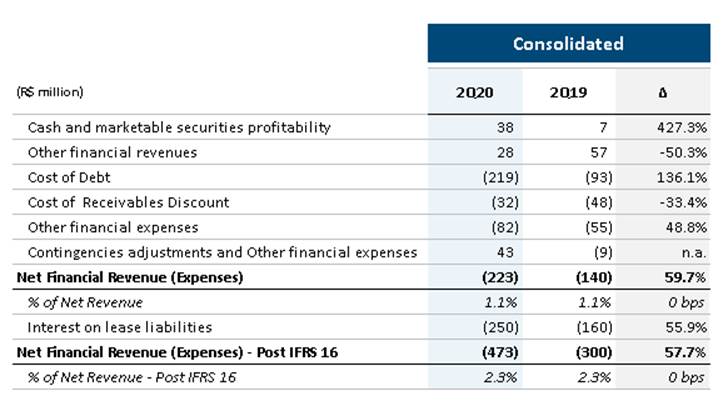

IV. FINANCIAL RESULT

The net financial result of GPA Consolidated totaled and expense of R$ 473 million, representing 2.3% of net sales, stable when compared to same period last year.

Due to the adoption of IFRS 16, the financial result now includes Interest on lease liability, which came to an expense of R$ 250 million in the quarter.

| |

Considering the net financial result (R$ 223 million), excluding the effect from Interest on lease liability, the main variations were:

| ● | Financial income: increase of R$ 31 million vs 2Q19 in cash and marketable securities profitability, reflecting the higher cash balance invested in the period. In Other financial revenues, there was a R$ 29 million lower contribution mainly explained by monetary restatement; |

| ● | Financial expenses (including the cost of selling receivables): increase of R$ 137 million from 2Q19, due to higher interest expenses caused by the increase of gross debt; |

| ● | Net effect from exchange variation: increase of R$ 52 million from 2Q19, resulting in an income of R$ 43 million, mainly due to the gain of R$ 24 million related to the effects from exchange variation on the dividends received from Grupo Éxito. |

V. NET INCOME

Consolidated GPA ended 2Q20 with consolidated net income from controlling shareholders of R$ 333 million, and the net income of continuing operations stood at 4.2x higher than the previous year, adding up to R$ 274 million (strong growth of 322.0%)

The 2Q20 result showed the group’s operating improvement and the success of the strategies adopted, with important recovery at Multivarejo, solid performance at Assaí and consolidation of Grupo Éxito’s strong results, which more than offset the increase in depreciation and cost of debt.

| |

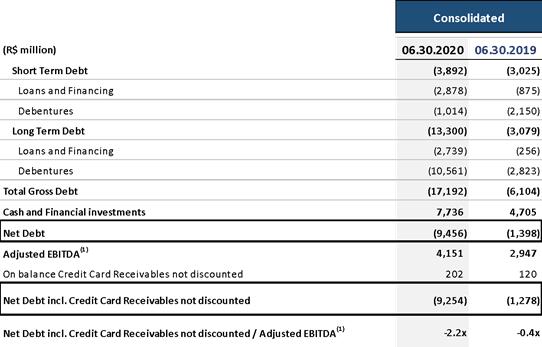

VI. NET DEBT

The calculation of the indicators in the following table excludes the lease liabilities related to IFRS 16.

(1) Adjusted EBITDA before IFRS 16 in the last 12 months.

Net debt adjusted by the balance of unsold receivables was R$ 9.2 billion for GPA Consolidated vs R$ 1.3 billion in 2Q19, which mainly reflects the funding operation for the acquisition of Grupo Éxito. The Company reduced its leverage in R$ 1.5 billion compared to 1Q20, due to the strong operating cash flow and the monetization of some non-core assets.

The net debt/adjusted EBITDA(1) ratio was 2.2x by the end of 2Q20, compared to 2.5x in 1Q20 and 0.4x in 2Q19, a level that is aligned with the Company’s expectations.

The Company ended 2Q20 with a solid financial position, with a cash balance of R$ 7.7 billion, equivalent to approximately 2x its short-term debt (vs. 120% in 1Q20 and 156% in 2Q19). Moreover, the balance of unsold receivables totaled R$ 202 million.

| |

VII. INVESTMENTS

Gross investments totaled R$ 536 million, of which: i) R$ 464 million in the Brazilian perimeter – supporting the opening of two Assaí stores in the quarter and the construction of another 16 stores that will open in the next quarters (13 organic and 3 conversions from Hiper) and ii) R$ 71 million in Grupo Éxito.

The Company's expansion, conversion and remodeling plan was maintained, but some delays or postponements may occur given the pandemic scenario. We expect to conclude 2020 with the opening of 19 Assaí stores (16 organic and 3 conversions), 38 renovations of Extra Super into Mercado Extra, 8 Pão de Açúcar renovations in the last generation of stores in Brazil. In Grupo Éxito we expect between 5 to 7 stores (from openings, conversions and remodeling), focused on innovative models Éxito WOW, Carulla FreshMarket and Surtimayorista by the end of the year.

| |

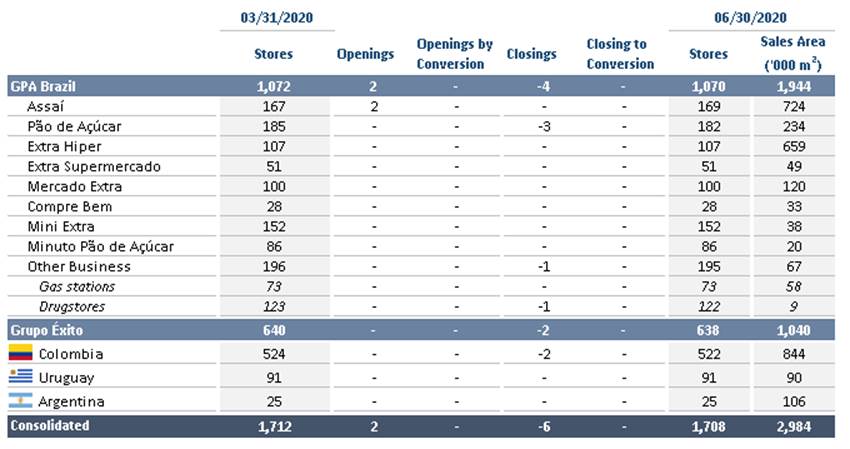

VIII. STORE PORTFOLIO CHANGES BY BANNER - BRAZIL

In the quarter, 2 Assaí stores were opened, totaling 169 stores of this banner. The Company continued to make adjustments to its portfolio by closing 3 Pão de Açúcar stores and 1 Drugstore.

| |

IX. CONSOLIDATED FINANCIAL STATEMENTS

Balance Sheet

| |

Income Statement - 2Q20

(1) Consolidated includes results of other complementary businesses; (2) Share of profit in an associate includes Cdiscount’s results in the Consolidated figures; (3) Net income after non-controlling interest; (4) Adjusted for Other Operating Income and Expenses.

| |

Cash Flow – Consolidated (*)

| |

X. BREAKDOWN OF SALES BY BUSINESS – BRAZIL

(1) Includes sales from Extra Supermercado, Mercado Extra, Extra Hiper and Compre Bem. (2) Includes sales by Mini Extra and Minuto Pão de Açúcar.

(3) Includes sales from Gas stations, Drugstores, Delivery and rental revenue from commercial centers. (4) GPA includes the result of James Delivery, Stix Fidelidade and Cheftime

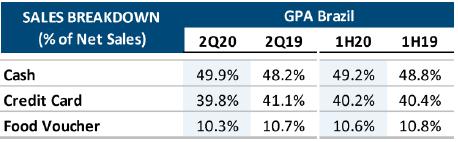

XI. BREAKDOWN OF SALES (% of Net Sales) – BRAZIL

| |

2Q20 Results Conference Call and Webcast

Thursday, July 30, 2020

10:30 a.m. (Brasília) | 9:30 a.m. (New York) | 2:30 p.m. (London)

Conference call in Portuguese (original language)

+55 (11) 4210-1803 or +55 (11) 3181-8565

Conference call in English (simultaneous translation)

+1 (412) 717-9627 or +1 (844) 204-8942

Webcast: http://www.gpari.com.br

Replay

+55 11 3193-1012

Access code for audio in Portuguese: 1932275#

Access code for audio in English: 1779586#

http://www.gpari.com.br

Investor Relations Contacts

GPA Phone: 55 (11) 3886-0421 gpa.ri@gpabr.com www.gpari.com.br

|

Disclaimer: Statements contained in this release relating to the business outlook of the Company, projections of operating/financial results, growth prospects of the Company and market and macroeconomic estimates are merely forecasts and are based on the beliefs, plans and expectations of Management in relation to the Company’s future. These expectations are highly dependent on changes in the market, Brazil’s general economic performance, the industry and international markets, and hence are subject to change.

| |

APPENDIX

Company’s Business:

Food – Brazil: Amounts reported refer to the sum of Assaí and Multivarejo operations.

Grupo Éxito: Amounts reported refer to Grupo Éxito’s operations in Colombia, Uruguay and Argentina. GPA acquired 96.57% of the capital stock of Grupo Éxito on November 27, 2019.

Consolidated: Amounts reported refer to the sum of the operations of Food – Brazil, Grupo Éxito, Cdiscount and other businesses of the Company.

Discontinued Activities: Refer to Via Varejo operations until May 2019 and other subsequent effects related to the write-off of investments.

EBITDA: EBITDA is calculated in accordance with Instruction 527 issued by the Securities and Exchange Commission of Brazil (CVM) on October 4, 2012.

Adjusted EBITDA: Measure of profitability calculated by excluding Other Operating Income and Expenses from EBITDA. Management uses this measure in its analyses as it believes it eliminates nonrecurring expenses and revenues and other nonrecurring items that could compromise comparability and analysis of results.

Earnings per Share: Diluted earnings per share are calculated as follows:

● Numerator: profit in the year adjusted by dilutive effects of stock options granted by subsidiaries.

● Denominator: number of shares of each category adjusted to include potential shares corresponding to dilutive instruments (stock options), less the number of shares that could be bought back at the market, as applicable.

Equity instruments that will or may be settled with the Company and its subsidiaries’ shares are only included in the calculation when their settlement has a dilutive impact on earnings per share.

‘same-store’ growth: ‘same-store’ growth, as mentioned in this document, is adjusted by the calendar effect in each period.

| |

Growth and Changes: The growth and changes presented in this document refer to variations from the same period last year, except where stated otherwise.

Retail vertical: Corresponds to sales of James Delivery in the Pão de Açúcar, Extra and Minuto Pão de Açúcar operations.

| |

SIGNATURES

Pursuant to the requirement of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| COMPANHIA BRASILEIRA DE DISTRIBUIÇÃO | ||

| Date: July 29, 2020 | By: /s/ Peter Estermann Name: Peter Estermann Title: Chief Executive Officer | |

| By: /s/ Christophe José Hidalgo Name: Christophe José Hidalgo Title: Investor Relations Officer | ||

FORWARD-LOOKING STATEMENTS

This press release may contain forward-looking statements. These statements are statements that are not historical facts, and are based on management's current view and estimates offuture economic circumstances, industry conditions, company performance and financial results. The words "anticipates", "believes", "estimates", "expects", "plans" and similar expressions, as they relate to the company, are intended to identify forward-looking statements. Statements regarding the declaration or payment of dividends, the implementation of principal operating and financing strategies and capital expenditure plans, the direction of future operations and the factors or trends affecting financial condition, liquidity or results of operations are examples of forward-looking statements. Such statements reflect the current views of management and are subject to a number of risks and uncertainties. There is no guarantee that the expected events, trends or results will actually occur. The statements are based on many assumptions and factors, including general economic and market conditions, industry conditions, and operating factors. Any changes in such assumptions or factors could cause actual results to differ materially from current expectations.