UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08361

Goldman Sachs Variable Insurance Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606-6303

(Address of principal executive offices) (Zip code)

Caroline Kraus

Goldman, Sachs & Co.

200 West Street

New York, NY 10282

Copies to:

Geoffrey R.T. Kenyon, Esq.

Dechert LLP

200 Clarendon Street

27th Floor Boston, MA 02116-5021

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: December 31

Date of reporting period: December 31, 2012

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| The Annual Reports to Stockholders are filed herewith. |

Goldman

Sachs Variable Insurance Trust

Goldman Sachs Core Fixed Income Fund

Goldman Sachs Equity Index Fund

Goldman Sachs Government Income Fund

Goldman Sachs Growth Opportunities Fund

Annual Report

December 31, 2012

GOLDMAN SACHS VARIABLE INSURANCE TRUST FUNDS

Principal Investment Strategies and Risks

This is not a complete list of the risks that may affect the Funds. For additional information concerning the risks applicable to the Funds, please see the Funds’ Prospectuses.

Shares of the Goldman Sachs Variable Insurance Trust Funds are offered to separate accounts of participating life insurance companies for the purpose of funding variable annuity contracts and variable life insurance policies. Shares of the Funds are not offered directly to the general public. The variable annuity contracts and variable life insurance policies are described in the separate prospectuses issued by participating insurance companies. You should refer to those prospectuses for information about surrender charges, mortality and expense risk fees and other charges that may be assessed by participating insurance companies under the variable annuity contracts or variable life insurance policies. Such fees or charges, if any, may affect the return you realize with respect to your investments. Ask your representative for more complete information. Please consider a Fund’s objective, risks and charges and expenses, and read the Prospectus carefully before investing. The Prospectus contains this and other information about a Fund.

The Goldman Sachs Core Fixed Income Fund invests primarily in fixed income securities, including U.S. government securities, corporate debt securities, privately issued mortgage-backed securities and asset-backed securities. The Fund’s investments in fixed income securities are subject to the risks associated with debt securities generally, including credit, liquidity and interest rate risk. Any guarantee on U.S. government securities applies only to the underlying securities of the Fund if held to maturity and not to the value of the Fund’s shares. The Fund’s investments in mortgage-backed securities are also subject to prepayment risk (i.e., the risk that in a declining interest rate environment, issuers may pay principal more quickly than expected, causing the Fund to reinvest proceeds at lower prevailing interest rates). The Fund may invest in foreign and emerging markets securities, which may be more volatile and less liquid than investments in U.S. securities and will be subject to the risks of currency fluctuations and adverse economic and political developments. Derivative instruments may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; risks of default by a counterparty; and liquidity risk (i.e., the risk that an investment may not be able to be sold without a substantial drop in price, if at all).

The Goldman Sachs Equity Index Fund attempts to replicate the aggregate price and yield performance of a benchmark index (i.e., the Standard & Poor’s 500 Index) that measures the investment returns of large capitalization stocks. The Fund’s equity investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. The Fund is not actively managed, and therefore the Fund will not typically dispose of a security until the security is removed from the index. The Fund’s performance may vary substantially from the performance of the benchmark it tracks as a result of share purchases and redemptions, transaction costs, expenses and other factors.

The Goldman Sachs Government Income Fund invests primarily in U.S. government securities. The Fund’s investments in fixed income securities are subject to the risks associated with debt securities generally, including credit, liquidity and interest rate risk. The Fund’s net asset value and yield are not guaranteed by the U.S. government or by its agencies, instrumentalities or sponsored enterprises. Any guarantee on U.S. government securities applies only to the underlying securities of the Fund if held to maturity and not to the value of the Fund’s shares. The Fund’s investments in mortgage-backed securities are also subject to prepayment risk (i.e., the risk that in a declining interest rate environment, issuers may pay principal more quickly than expected, causing the Fund to reinvest proceeds at lower prevailing interest rates).

1

GOLDMAN SACHS VARIABLE INSURANCE TRUST FUNDS

Derivative instruments may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; the risk of default by a counterparty; and liquidity risk.

The Goldman Sachs Growth Opportunities Fund invests primarily in U.S. equity investments with a primary focus on mid-capitalization companies. The Fund’s equity investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. The securities of mid-capitalization companies involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements. Different investment styles (e.g., “growth”) tend to shift in and out of favor, and at times the Fund may underperform other funds that invest in similar asset classes.

2

MARKET REVIEW

Goldman Sachs Variable Insurance Trust Funds

Market Review

The U.S. equity and fixed income markets generated positive returns during the 12 months ended December 31, 2012 (the “Reporting Period”).

Equity Markets

Representing the U.S. equity market, the S&P® 500 Index rose 15.96% during the Reporting Period to mark the fourth straight year of gains. The year 2012 started with the strongest first quarter since 1998 for the S&P® 500 Index. Also during the first quarter of 2012, the Dow Jones Industrial Average closed above 13,000 for the first time since May 2008, and the NASDAQ reached a new 11-year high. U.S. equities rose largely on evidence that the labor and manufacturing markets were improving. In addition, the Federal Reserve Board (the “Fed”) reaffirmed its commitment to low interest rates until at least late-2014.

U.S. equity markets slid, however, during the second quarter of 2012, when first quarter Gross Domestic Product (“GDP”) was revised down from 2.2% to 1.9%, and employment reports suggested deterioration in the labor market. Spain’s banking system bailout and increasing concerns over Europe’s financial crisis weighed on global equity markets, including the U.S. equity market, as well. At the same time, disappointing economic reports from faster growing regions of the world renewed fears of a global economic slowdown.

During the summer of 2012, U.S. equity markets rallied back on more strong statements from central banks. In September, the Fed announced another round of quantitative easing, dubbed QE3, this time with no expiration date but with the explicit goal of reducing unemployment. The Fed also extended its policy of near-zero interest rates until at least mid-2015. In Europe, European Central Bank (“ECB”) president Mario Draghi voiced strong support for the euro and the European Monetary Union, which was well received by financial markets in the U.S. Continued improvements in home prices and the Fed’s commitment to buy mortgage-backed securities increased hopes of a recovery in the housing market, which helped offset the downward pressures of lackluster economic growth and a stalled labor market.

There were increasing signs of economic recovery seen early in the fourth quarter of 2012. The U.S. reported better than expected third quarter GDP growth of 2%, the 13th consecutive quarter of economic expansion, and the unemployment rate dropped to 7.8%, the lowest rate seen since January 2009. U.S. manufacturing activity increased, and the housing market showed further signs of improvement, as construction of new homes hit a four-year high. Despite this positive data, the U.S. equity market pulled back in October on some cautious corporate earnings guidance. Also pressuring the U.S. equity market were the worst storm in decades battering the East Coast and polls showing the U.S. presidential race tightening to a dead heat.

The U.S. equity market crept higher in November 2012, as election day preserved the status quo in the White House and Congress, even as the “fiscal cliff” drew nearer. Housing starts and measures of employment improved, and manufacturing and non-manufacturing surveys showed expansion in the economy. In December 2012, further clarification from the Fed, tying its low interest rate policy to the condition that unemployment drop to 6.5% or lower helped to offset increasing worries about the then-looming fiscal cliff of tax increases and spending cuts.

For the Reporting Period as a whole, all ten sectors within the S&P® 500 Index posted gains. The consistent and persistent commitment to accommodative monetary policy from the U.S. Fed and other central banks drove market-leading returns in the financials sector. The heavily weighted financials sector was also the largest positive contributor (weight times performance) to S&P® 500 Index returns. On optimism about the economy and improved consumer confidence, the consumer discretionary sector also performed well. Conversely, the energy sector posted positive returns but was comparatively weak during the Reporting Period, as oil prices remained relatively stable, balancing continued unrest in several oil-producing regions with potential supply increases from U.S. shale production and a modest outlook for global economic growth.

All segments of the U.S. equity market advanced during the Reporting Period, with mid-cap stocks, as measured by the Russell Midcap® Index, gaining most, followed by large-cap stocks and then small-cap stocks, as measured by the Russell 1000® Index and the Russell 2000® Index, respectively, which performed similarly to each other. From a style perspective, value-oriented stocks solidly outpaced growth-oriented stocks across the capitalization spectrum. (All as measured by the Russell Investments indices.)

3

MARKET REVIEW

Fixed Income Markets

The U.S. fixed income market, as represented by the Barclays U.S. Aggregate Bond Index (“Barclays Index”), returned 4.21% during the Reporting Period. Non-government sectors led the gains.

Spread, or non-U.S. Treasury, sectors started the Reporting Period on a rally that persisted through March 2012, helped by a global trend of improving economic data. In the U.S., manufacturing activity accelerated, and the unemployment rate fell faster than anticipated to a three-year low of 8.3%. Despite this favorable economic backdrop, persistent concerns about the Eurozone’s financial crisis continued to support demand for lower-risk government bonds. Highly accommodative monetary policy by global central banks also helped curb increases in U.S., Japanese and German government bond yields.

The positive trend for spread sectors reversed during the second quarter of 2012. Global economic data weakened, and concerns mounted about heavy losses in Spain’s banking sector and the possibility of Greece exiting the Eurozone. May was the toughest month in the Reporting Period overall for riskier asset classes. Equity indices fell sharply and emerging market sovereign bonds underperformed U.S. Treasuries by more than 5%. In June, investors’ risk appetite began to recover as a second round of Greek elections reaffirmed that country’s commitment to austerity and European Union leaders reached broad consensus on a recapitalization of Spanish banks. U.S. economic data began to improve, particularly in the housing sector with the Standard & Poor’s/Case-Shiller Home Price Indices showing a clear upward trend. Labor market data beat expectations again, and by the end of the Reporting Period, the U.S. unemployment rate had dropped to 7.8%. These factors sparked renewed rallies across spread sectors that persisted for most of the remainder of the Reporting Period, fueled primarily by investors’ search for yield in an extremely low interest rate environment.

Early in the third calendar quarter, U.S. and German interest rates traded near record lows — 1.39% for the U.S. 10-year Treasury bond and 1.17% for the German 10-year bund—on mounting expectations for further monetary stimulus. Central banks delivered on these expectations. In July 2012, the ECB cut its benchmark interest rate to 0.75% and its deposit rate to zero. In September, the ECB pledged to purchase potentially unlimited amounts of distressed government bonds in secondary markets as needed. As mentioned above, the Fed announced open-ended purchases of agency mortgage-backed securities in a third round of quantitative easing, dubbed QE3, and extended the likely period of low rates from mid-2014 to mid-2015.

Volatility increased in the lead-up to the November 2012 U.S. elections, though the reelection of President Obama had little impact on the fixed income markets. After a brief pause, spread sector rallies resumed, despite mounting uncertainty about the then-looming fiscal cliff. In the final days of the Reporting Period, the fixed income markets focused on the eleventh-hour negotiations in Washington, D.C., as lawmakers strived to reach agreement on fiscal policies ahead of the year-end deadline for automatic spending cuts and the expiration of Bush-era tax cuts.

During the Reporting Period as a whole, higher-yielding fixed income sectors outperformed U.S. Treasury securities. Non-agency mortgage-backed securities performed best, with an excess return of 29.2% over similar-duration U.S. Treasuries. Agency mortgage-backed securities were the weakest performers, generating an excess return of 0.9% over U.S. Treasuries during the Reporting Period.

Looking Ahead

Equity Markets

After a strong 2012, we continue to see opportunities as we enter 2013 and remain constructive in our view ahead for U.S. equities. We recognize fiscal policy may lead to a drag on economic growth, and recent steps taken by the Fed to provide additional monetary accommodation may not fully offset the impact. The political climate in the U.S., and the lack of clarity around the outcome of fiscal negotiations, has contributed to an elevated feeling of uncertainty for both businesses and individuals. However, corporate balance sheets remain strong, which we believe provides companies with the ability to generate shareholder value, even in a slower economic growth environment. The S&P 500 Index, as a broad measure of the U.S. equity market, was trading below its historical average price-to-earnings ratio at the end of the Reporting Period, while its dividend yield was greater than the yield

4

MARKET REVIEW

on the 10-year U.S. Treasury bond. Continued strength in the U.S. housing recovery should provide, in our view, support to the economy and boost confidence among consumers.

Through these conditions, our investment decisions remain driven by our long-standing process and philosophy. We dive deep into the fundamentals of our holdings, meet with companies’ managements and have continuous discussions and debates amongst ourselves to ensure that the portfolios are reflective of our highest conviction ideas. We construct the portfolios around businesses that we believe should create long-term value for shareholders and are leveraged to secular growth trends rather than to political outcomes or macroeconomic expectations.

In our view, companies with strong business franchises become more attractive in uncertain environments. Holding competitive advantages, a strong management team and the ability to allocate capital allows the business to adapt and continuously execute on its long-term plans regardless of current sentiment. Companies are not static entities. We believe strong management teams know they must adapt to regulatory changes, expand into new markets and improve their product offerings in order to remain competitive and grow. These are the types of investments we believe will reward our shareholders over the long term. As always, deep research resources, a forward-looking investment process and truly actively managed portfolios are keys, in our view, to both preserving capital and outperforming the market over the long term.

Fixed Income Markets

Just after the close of the Reporting Period, U.S. lawmakers struck a deal to avert triggering several automatic tax increases. However, the new Congress will need to revisit fiscal issues, including spending cuts and the raising of the U.S. debt ceiling.

In our opinion, the fiscal cliff agreement is far from ideal, but we believe the underlying momentum in the U.S. economy is healthy. Indeed, our view of 2013 economic growth is more optimistic than the consensus view. We believe pent-up investment demand will be released in the wake of the fiscal cliff resolution. We also expect a continued recovery in the housing market and an environment favorable to riskier asset classes. As a result, we expect the long-term end of the U.S. Treasury yield curve to remain under pressure.

Our fixed income positioning overall reflects the “risk-on” environment, with an underweight in U.S. interest rate risk relative to fixed income portfolio benchmarks and overweighted positions in corporate credit and mortgage-backed securities. At the end of the Reporting Period, we planned to maintain our core position — an overweight to lower coupon mortgage-backed securities that are the target of Fed purchases, an underweight to coupons that are most vulnerable to refinancing at current historically low rates, and an overweight to higher coupons that have already priced in this risk.

5

GOLDMAN SACHS VARIABLE INSURANCE TRUST CORE FIXED INCOME FUND

INVESTMENT OBJECTIVE

The Fund seeks a total return consisting of capital appreciation and income that exceeds the total return of the Barclays U.S. Aggregate Bond Index.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Fixed Income Investment Management Team discusses the Goldman Sachs Variable Insurance Trust — Goldman Sachs Core Fixed Income Fund’s (the “Fund”) performance and positioning for the 12-month period ended December 31, 2012 (the “Reporting Period”).

How did the Fund perform during the Reporting Period?

During the Reporting Period, the Fund’s Service Shares generated an average annual total return of 6.70%. This return compares to the 4.21% average annual total return of the Fund’s benchmark, the Barclays U.S. Aggregate Bond Index (the “Barclays Index”), during the same time period.

What key factors were responsible for the Fund’s performance during the Reporting Period?

Our top-down cross-sector strategy contributed the most to the Fund’s relative outperformance during the Reporting Period. Our cross-sector strategy is one in which we invest Fund assets across a variety of fixed income sectors, including some that may not be included in the Barclays Index. The Fund’s duration and U.S. yield curve positioning relative to the Barclays Index also enhanced results. Duration is a measure of the Fund’s sensitivity to changes in interest rates. Yield curve indicates a spectrum of maturities. In addition, bottom-up individual issue selection was a strong driver of relative returns.

Which fixed income market sectors most affected Fund performance?

The Fund’s overweighted position in the strongly performing non-agency mortgage-backed securities sector contributed positively to relative results. An overweight to corporate credit, which also outperformed U.S. Treasuries during the Reporting Period, was advantageous as well.

Individual issue selection within the investment grade corporate bond and collateralized sectors enhanced relative performance. Among corporate bonds, investments in the financials and industrials sub-sectors boosted returns. Within the collateralized sector, the Fund benefited from its holdings in non-agency adjustable-rate mortgages (“ARMs”) and pass-through mortgage securities. (Pass-through mortgage securities consist of a pool of residential mortgage loans, where homeowners’ monthly payments of principal, interest and prepayments pass from the original bank through a government agency or investment bank to investors.) Our issue selection among asset-backed securities (“ABS”) and covered bonds also added value. Detracting slightly was issue selection among commercial mortgage-backed securities (“CMBS”).

Did the Fund’s duration and yield curve positioning strategy help or hurt its results during the Reporting Period?

Tactical management of the Fund’s duration and yield curve positioning added to its relative returns for the Reporting Period overall. At the beginning of the Reporting Period, the Fund held a short duration position relative to that of the Barclays Index because we believed that interest rates would begin to increase when the Fed’s Operation Twist concluded in June 2012. (Ultimately, the Fed extended Operation Twist to the end of December 2012.) In the second quarter, as riskier asset classes declined on further evidence of slowing global economic growth and renewed tensions in Europe, we maintained the Fund’s short duration positioning relative to the Barclays Index. We subsequently shifted the Fund to a longer duration position relative to the Barclays Index in response to the Fed’s commitment to keep short-term interest rates low and based on our outlook for subdued economic growth and deteriorating financial conditions in Europe. This positioning contributed positively as U.S. economic data weakened and concerns about Spanish and Italian debt increased. In addition, during the third quarter, the Fund benefited from its longer duration position in U.S. and German government bonds, concentrated in the intermediate segment of the yield curve, as yields declined. In the fourth quarter, as interest rates moved higher, this longer duration positioning detracted. By the end of the Reporting Period, we had shifted the Fund to a shorter duration position relative to the Barclays Index once again.

How did the Fund use derivatives and similar instruments during the Reporting Period?

As market conditions warranted during the Reporting Period, currency transactions were carried out using primarily over-the-counter (“OTC”) forward foreign exchange contracts. Currency transactions were used as we sought both to enhance

6

GOLDMAN SACHS VARIABLE INSURANCE TRUST CORE FIXED INCOME FUND

returns and to hedge the Fund’s portfolio against currency exchange rate fluctuations. Also, Treasury futures were used as warranted to facilitate specific duration, yield curve and country strategies. Overall, we employ derivatives and similar instruments for the efficient management of the Fund’s portfolio. Derivatives and similar instruments allow us to manage interest rate, credit and currency risks more effectively by allowing us both to hedge and to apply active investment views with greater versatility and to afford greater risk management precision than we would otherwise be able to implement.

Were there any notable changes in the Fund’s weightings during the Reporting Period?

As mentioned earlier, we actively adjusted the Fund’s duration as market conditions shifted. From a sector perspective, we maintained the Fund’s overweight in non-agency mortgage-backed securities. In July and August 2012, the Fund held a substantial overweight in agency mortgage-backed securities because we believed the Fed would re-enter the market and begin purchasing the securities. As the market similarly anticipated Fed action, spreads, or yield differentials to U.S. Treasuries, tightened, and we began unwinding the Fund’s position before the Fed actually announced its open-ended mortgage purchases. After the announcement, agency mortgage-backed security spreads tightened further.

During the first half of the Reporting Period, we shifted the Fund from an underweight in pass-through mortgage securities to a significant overweight. In the second half, we reduced the Fund’s allocation to pass-through mortgage securities to a more modest overweighted position. We increased the Fund’s already overweight position in corporate credit toward the end of the Reporting Period.

How was the Fund positioned relative to the Barclays Index at the end of the Reporting Period?

At the end of the Reporting Period, the Fund was underweight U.S. government securities and overweight investment grade corporate bonds relative to the Barclays Index. It was overweight quasi-government bonds, ABS, CMBS, residential mortgage-backed securities and pass-through mortgage securities. In addition, the Fund had exposure to covered bonds and emerging markets debt.

7

FUND BASICS

Core Fixed Income Fund

as of December 31, 2012

STANDARDIZED TOTAL RETURNS1

| For the period ended 12/31/12 | One Year | Five Year | Since Inception | Inception Date | ||||||||||

| Service | 6.70 | % | 5.10 | % | 5.21 | % | 1/09/06 | |||||||

| 1 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at net asset value (“NAV”). Because Service Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

Total return figures in the above chart represent past performance and do not indicate future results, which will vary. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the total return figures in the above chart. Please visit www.goldmansachsfunds.com/vit to obtain the most recent month-end returns. Performance reflects fee waivers and/or expense limitations in effect. In their absence, performance would be reduced.

EXPENSE RATIOS2

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||

| Service | 0.67 | % | 0.83 | % | ||||

| 2 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least April 27, 2013, and prior to such date the investment adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

8

FUND BASICS

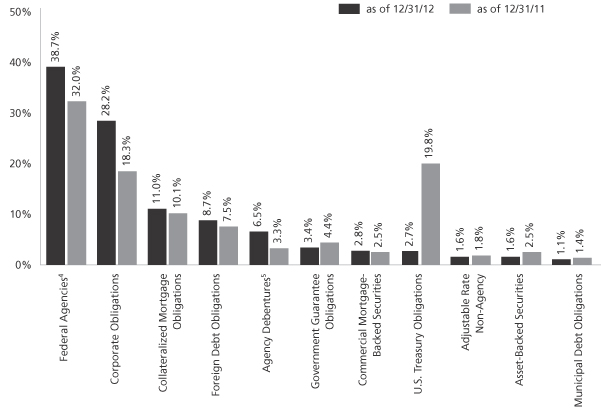

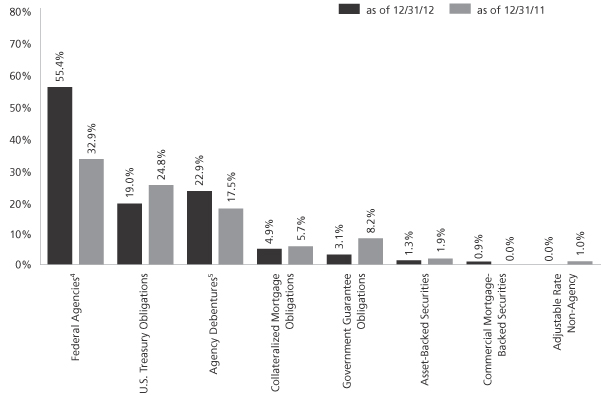

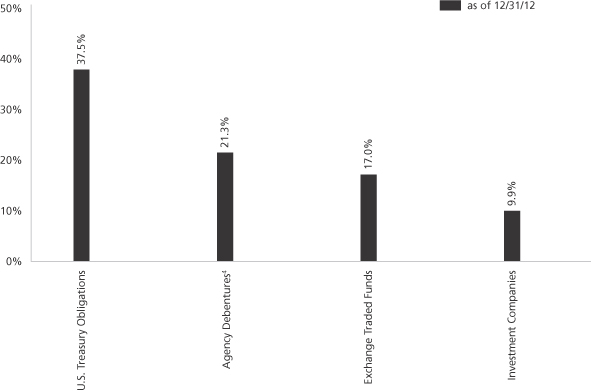

FUND COMPOSITION3

| 3 | The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. Figures in the above graph may not sum to 100% due to the exclusion of other assets and liabilities. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

| 4 | “Federal Agencies” are mortgage-backed securities guaranteed by the Government National Mortgage Association (“GNMA”), Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corp. (“FHLMC”). GNMA instruments are backed by the full faith and credit of the United States Government. |

| 5 | “Agency Debentures” include agency securities offered by companies such as FNMA and FHLMC, which operate under a government charter. While they are required to report to a government regulator, their assets are not explicitly guaranteed by the government and they otherwise operate like any other publicly traded company. |

9

GOLDMAN SACHS VARIABLE INSURANCE TRUST CORE FIXED INCOME FUND

Performance Summary

December 31, 2012

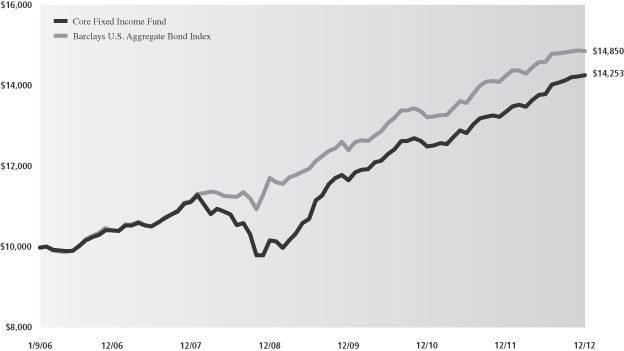

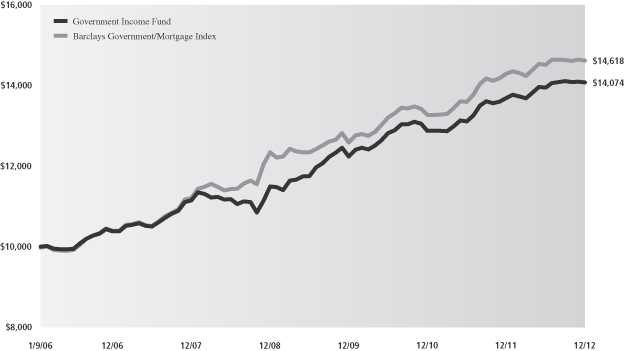

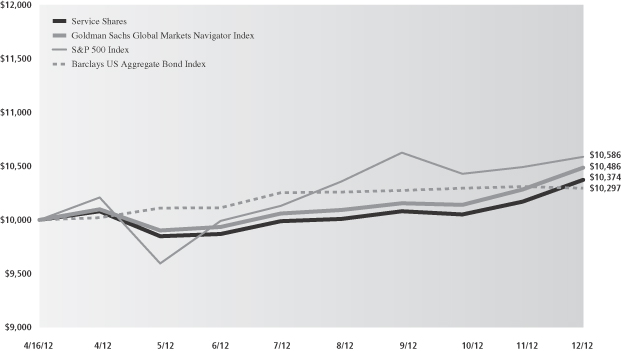

The following graph shows the value, as of December 31, 2012, of a $10,000 investment made in the Fund on January 9, 2006 (commencement of operations). For comparative purposes, the performance of the Fund’s benchmark, the Barclays U.S. Aggregate Bond Index, is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects Fund level expenses, but does not reflect fees and expenses associated with any variable annuity contract or variable life insurance policy that uses the Fund as an investment option for any contract or policy. Had performance reflected all of those fees and expenses, performance would have been reduced. Performance also would have been reduced had expense limitations not been in effect. In addition to the investment adviser’s decisions regarding issuer/industry/country investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover, and subscription and redemption cash flows affecting the Fund.

Core Fixed Income Fund’s Lifetime Performance

Performance of a $10,000 investment, with distributions reinvested, from January 9, 2006 through December 31, 2012.

| Average Annual Total Return through December 31, 2012 | One Year | Five Years | Since Inception | |||

Core Fixed Income Fund (Commenced January 9, 2006) | 6.70% | 5.10% | 5.21% |

10

GOLDMAN SACHS VARIABLE INSURANCE TRUST EQUITY INDEX FUND

INVESTMENT OBJECTIVE

The Fund seeks to achieve investment results that correspond to the aggregate price and yield performance of a benchmark index that measures the investment returns of large capitalization stocks.

Portfolio Management Discussion and Analysis

Below, SSgA Funds Management, Inc. (“SSgA”), the Fund’s Subadvisor, discusses the Goldman Sachs Variable Insurance Trust — Goldman Sachs Equity Index Fund’s (the “Fund”) performance and positioning for the 12-month period ended December 31, 2012 (the “Reporting Period”).

How did the Fund perform during the Reporting Period?

During the Reporting Period, the Fund’s Service Shares generated an average annual total return of 15.50%. This return compares to the 15.96% average annual total return of the Fund’s benchmark, the Standard & Poor’s® 500 Index (with dividends reinvested) (the “S&P 500 Index”), during the same time period.

During the Reporting Period, which sectors and which industries in the S&P 500 Index were the strongest contributors to the Fund’s performance?

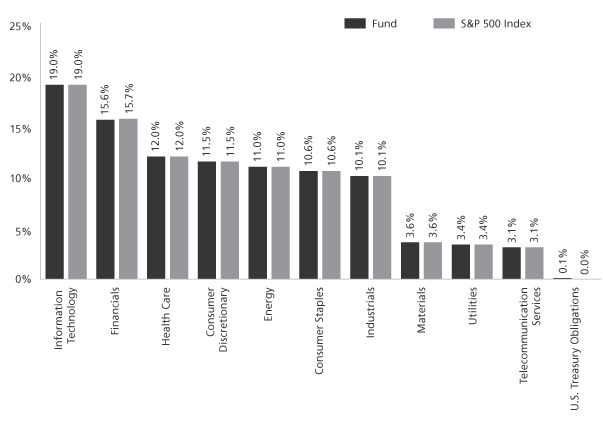

All 10 sectors in the S&P 500 Index recorded gains during the Reporting Period. In terms of total return, the sectors that made the strongest positive contributions to the S&P 500 Index and to the Fund were financials, consumer discretionary and health care. The largest sector by weighting in the S&P 500 Index at the end of the Reporting Period was information technology at a weighting of 19.03%. The industries with the strongest performance in terms of total return were diversified financials; media; retailing; banks; and customer durables and apparel.

On the basis of impact (which takes both total returns and weightings into account), the sectors that made the strongest positive contributions to the S&P 500 Index and to the Fund were financials, information technology and consumer discretionary. The industries with the strongest performance on the basis of impact were diversified financials; software and services; pharmaceuticals, biotechnology and life sciences; capital goods; and media.

Which sectors and industries in the S&P 500 Index were the weakest contributors to the Fund’s performance?

During the Reporting Period, the utilities, energy and consumer staples sectors were the weakest performing sectors in terms of total return. The weakest performing industries in terms of total return were semiconductors and semiconductor equipment; utilities; consumer services; energy; and transportation.

On the basis of impact, utilities, energy and materials were the weakest performing sectors. The weakest performing industries on the basis of impact were semiconductors and semiconductor equipment; utilities; consumer services; commercial and professional services; and transportation.

Which individual stocks were the top performers, and which were the greatest detractors?

On the basis of impact, the stocks that made the strongest positive contribution were Apple, Bank of America, JPMorgan Chase, Citigroup and Comcast. The weakest performers were Hewlett-Packard, Intel, Occidental Petroleum, McDonald’s and Exelon.

How did the Fund use derivatives and similar instruments during the Reporting Period?

During the Reporting Period, we did not use derivatives as part of an active management strategy to add value to the Fund’s results. However, we used equity index futures to equitize the Fund’s cash holdings. In other words, we put the Fund’s cash holdings to work by using them as collateral for the purchase of equity index futures. We also used these equity index futures to provide liquidity for daily cash flow requirements.

What changes were made to the makeup of the S&P 500 Index during the Reporting Period?

Eighteen stocks were removed from the S&P 500 Index during the Reporting Period. They were Compuware, Constellation Energy Group, Medco Health Solutions, Supervalu, Motorola Mobility Holdings, El Paso, Novellus Systems, Sara Lee, Progress Energy, Goodrich, Sears Holdings, Lexmark International, DeVry, Alpha Natural Resources, Sunoco, Cooper Industries, R.R. Donnelly and Sons, and Titanium Metals.

There were also 18 additions to the S&P 500 Index during the Reporting Period. They were WPX Energy, Crown Castle International, Fossil, Phillips 66, Kinder Morgan, Alexion Pharmaceuticals, Lam Research, Monster Beverage, Seagate Technology, Ensco, LyondellBasell Industries, ADT, Pentair, Kraft Foods Group, PetSmart, Dollar General, Garmin and Delphi Automotive.

11

FUND BASICS

Equity Index Fund

as of December 31, 2012

STANDARDIZED TOTAL RETURNS1

| For the period ended 12/31/12 | One Year | Five Year | Since Inception | Inception Date | ||||||||||

| Service | 15.50 | % | 1.37 | % | 3.42 | % | 1/09/06 | |||||||

| 1 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at net asset value (“NAV”). Because Service Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

Total return figures in the above chart represent past performance and do not indicate future results, which will vary. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the total return figures in the above chart. Please visit www.goldmansachsfunds.com/vit to obtain the most recent month-end returns. Performance reflects fee waivers and/or expense limitations in effect. In their absence, performance would be reduced.

EXPENSE RATIOS2

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||

| Service | 0.48 | % | 0.70 | % | ||||

| 2 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least April 27, 2013, and prior to such date the investment adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

TOP TEN HOLDINGS AS OF 12/31/123

| Holding | % of Net Assets | Line of Business | ||||

| Apple, Inc. | 3.9% | Technology Hardware & Equipment | ||||

| Exxon Mobil Corp. | 3.1 | Energy | ||||

| General Electric Co. | 1.7 | Capital Goods | ||||

| Chevron Corp. | 1.7 | Energy | ||||

| International Business Machines Corp. | 1.6 | Software & Services | ||||

| Microsoft Corp. | 1.6 | Software & Services | ||||

| Johnson & Johnson | 1.5 | Pharmaceuticals, Biotechnology & Life Sciences | ||||

| AT&T, Inc. | 1.5 | Telecommunication Services | ||||

| Google, Inc. Class A | 1.5 | Software & Services | ||||

| The Procter & Gamble Co. | 1.4 | Household & Personal Products | ||||

| 3 | The top 10 holdings may not be representative of the Fund’s future investments. |

12

FUND BASICS

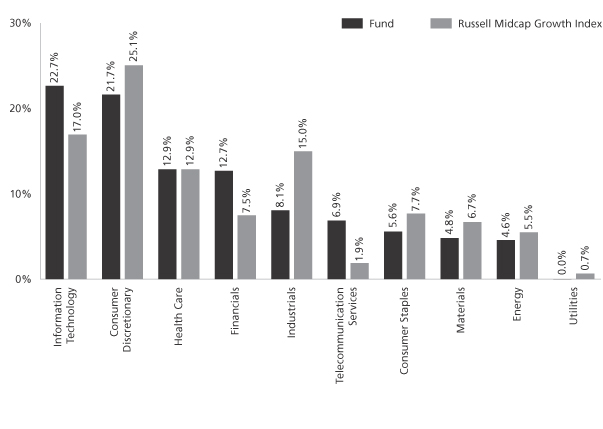

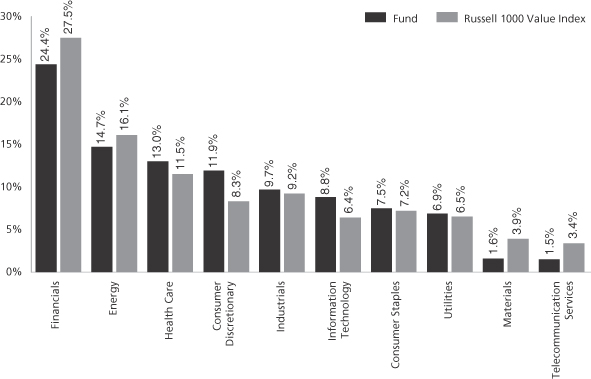

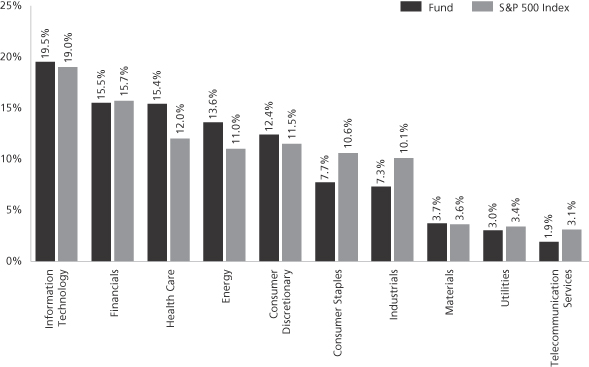

FUND VS. BENCHMARK SECTOR ALLOCATIONS4

As of December 31, 2012

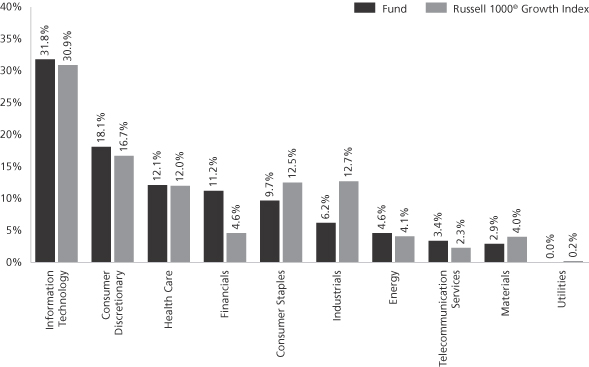

| 4 | The Fund’s composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

13

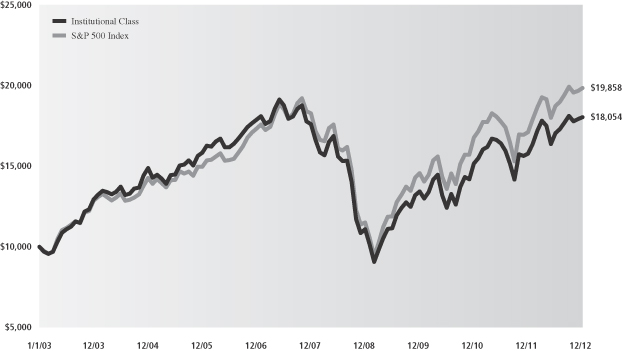

GOLDMAN SACHS VARIABLE INSURANCE TRUST EQUITY INDEX FUND

Performance Summary

December 31, 2012

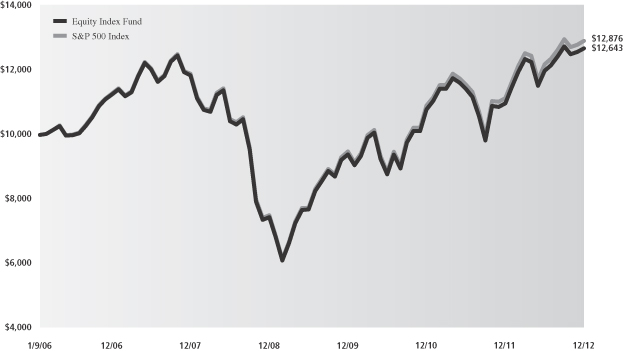

The following graph shows the value, as of December 31, 2012, of a $10,000 investment made in the Fund on January 9, 2006 (commencement of operations). For comparative purposes, the performance of the Fund’s benchmark, the S&P 500 Index (with dividends reinvested), is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects Fund level expenses, but does not reflect fees and expenses associated with any variable annuity contract or variable life insurance policy that uses the Fund as an investment option for any contract or policy. Had performance reflected all of those fees and expenses, performance would have been reduced. Performance also would have been reduced had expense limitations not been in effect. In addition to the investment adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover, and subscription and redemption cash flows affecting the Fund.

Equity Index Fund’s Lifetime Performance

Performance of a $10,000 investment, with distributions reinvested, from January 9, 2006 through December 31, 2012.

| Average Annual Total Return through December 31, 2012 | One Year | Five Years | Since Inception | |||

Equity Index Fund (Commenced January 9, 2006) | 15.50% | 1.37% | 3.42% |

14

GOLDMAN SACHS VARIABLE INSURANCE TRUST GOVERNMENT INCOME FUND

INVESTMENT OBJECTIVE

The Fund seeks a high level of current income, consistent with safety of principal.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Fixed Income Investment Management Team discusses the Goldman Sachs Variable Insurance Trust — Goldman Sachs Government Income Fund’s (the “Fund”) performance and positioning for the 12-month period ended December 31, 2012 (the “Reporting Period”).

How did the Fund perform during the Reporting Period?

During the Reporting Period, the Fund’s Service Shares generated an average annual total return of 2.78%. This return compares to the 2.26% average annual total return of the Fund’s benchmark, the Barclays Government/Mortgage Index (the “Barclays Index”) during the same time period.

What key factors were responsible for the Fund’s performance during the Reporting Period?

Bottom-up individual issue selection within the collateralized sector added the most to the Fund’s relative returns during the Reporting Period. Our top-down cross-sector strategy also enhanced relative performance. Our cross-sector strategy is one in which we invest Fund assets across a variety of fixed income sectors, including some that may not be included in the Barclays Index. In addition, the Fund’s duration and U.S. yield curve positioning relative to the Barclays Index contributed positively. Duration is a measure of the Fund’s sensitivity to changes in interest rates. Yield curve indicates a spectrum of maturities.

Which fixed income market sectors most affected Fund performance?

As riskier asset classes rallied during the Reporting Period, the Fund benefited from its exposure to agency mortgage-backed securities, non-agency mortgage-backed securities (which are not represented in the Barclays Index) and asset-backed securities (“ABS”). More specifically, from the beginning of the Reporting Period until September 2012, when the Fed announced its third round of quantitative easing, the Fund’s overweight in agency mortgage-backed securities and its “down in coupon” focus (or, its emphasis on those securities with lower interest rates) added to relative results. In the fourth calendar quarter, the Fund’s investments in premium and super-premium agency mortgage-backed securities were particularly advantageous.

The Fund also benefited from individual issue selection within the collateralized sector. More specifically, the Fund’s holdings of pass-through mortgage securities boosted relative performance. (Pass-through mortgages consist of a pool of residential mortgage loans, where homeowners’ monthly payments of principal, interest and prepayments pass from the original bank through a government agency or investment bank to investors.) Our investments among commercial mortgage-backed securities (“CMBS”) also added to Fund performance. In addition, the Fund benefited from issue selection among both U.S. Treasury securities of between two-year and six-year maturities and longer maturity Treasury Inflation Protected Securities (“TIPS”).

Detracting was our individual issue selection within the government/agency sector, specifically the Fund’s exposure to select agency bonds.

Did the Fund’s duration and yield curve positioning strategy help or hurt its results during the Reporting Period?

Tactical management of the Fund’s duration and yield curve positioning added to its relative returns. The Fund benefited from its short duration position relative to that of the Barclays Index during the first quarter of 2012, as 10-year U.S. Treasury yields increased in response to improved U.S. economic data and subdued volatility surrounding the European sovereign debt crisis. During the second calendar quarter, 10-year U.S. Treasury yields fell sharply amidst renewed worries about Europe’s financial problems. We shifted the Fund to a longer duration position relative to the Barclays Index, which enhanced relative results. In the third calendar quarter, we shortened the Fund’s duration stance again, and its duration and yield curve positioning had a minimally positive impact on relative performance. During the fourth calendar quarter, the Fund’s short duration position relative to the Barclays Index detracted from relative returns. More specifically, the Fund’s underweight in U.S. Treasuries with 10-year and 30-year maturities was a drag on performance as interest rates fell during November.

15

GOLDMAN SACHS VARIABLE INSURANCE TRUST GOVERNMENT INCOME FUND

How did the Fund use derivatives and similar instruments during the Reporting Period?

As market conditions warranted during the Reporting Period, the Fund engaged in U.S. Treasury futures to hedge interest rate exposure and facilitate specific duration and yield curve strategies.

Were there any notable changes in the Fund’s weightings during the Reporting Period?

As mentioned earlier, in implementing our active duration strategy, we shifted the Fund’s duration from a shorter position than that of the Barclays Index to a comparatively longer duration position in late April in response to the Fed’s easing bias, our outlook for a continuation of subdued economic growth and deterioration in overall financial conditions. We then shifted the Fund to a shorter duration bias during the third calendar quarter as turmoil in Europe appeared to support an increase in interest rates.

From a sector perspective, we tactically shifted the Fund’s position in agency mortgage-backed securities, such that at the end of the second calendar quarter, the Fund was overweight agency mortgage-backed securities. We maintained a substantial overweight overall to agency mortgage-backed securities through September 2012 when the Fed announced a third round of quantitative easing. Because of improving housing fundamentals, the Fund had exposure to non agency mortgage-backed securities throughout the Reporting Period.

How was the Fund positioned relative to the Barclays Index at the end of the Reporting Period?

At the end of the Reporting Period, the Fund was significantly underweight U.S. government securities relative to the Barclays Index. It was overweight quasi-government bonds, ABS, residential mortgage-backed securities, agency collateralized mortgage obligations and pass-through mortgage securities.

16

FUND BASICS

Government Income Fund

as of December 31, 2012

STANDARDIZED TOTAL RETURNS1

| For the period ended 12/31/12 | One Year | Five Year | Since Inception | Inception Date | ||||||||||

| Service | 2.78 | % | 4.77 | % | 5.02 | % | 1/09/06 | |||||||

| 1 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at net asset value (“NAV”). Because Service Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

Total return figures in the above chart represent past performance and do not indicate future results, which will vary. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the total return figures in the above chart. Please visit www.goldmansachsfunds.com/vit to obtain the most recent month-end returns. Performance reflects fee waivers and/or expense limitations in effect. In their absence, performance would be reduced.

EXPENSE RATIOS2

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||

| Service | 0.81 | % | 1.13 | % | ||||

| 2 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least April 27, 2013, and prior to such date the investment adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

17

FUND BASICS

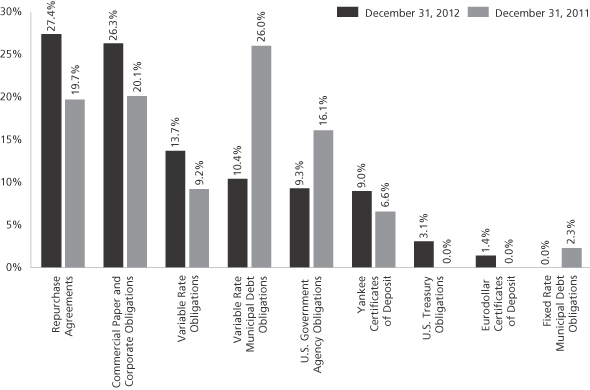

FUND COMPOSITION3

| 3 | The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. Figures in the graph may not sum to 100% due to the exclusion of other assets and liabilities. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

| 4 | “Federal Agencies” are mortgage-backed securities guaranteed by the Government National Mortgage Association (“GNMA”), Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corp. (“FHLMC”). GNMA instruments are backed by the full faith and credit of the United States Government. |

| 5 | “Agency Debentures” include agency securities offered by companies such as FNMA and FHLMC, which operate under a government charter. While they are required to report to a government regulator, their assets are not explicitly guaranteed by the government and they otherwise operate like any other publicly traded company. |

18

GOLDMAN SACHS VARIABLE INSURANCE TRUST GOVERNMENT INCOME FUND

Performance Summary

December 31, 2012

The following graph shows the value, as of December 31, 2012, of a $10,000 investment made in the Fund on January 9, 2006 (commencement of operations). For comparative purposes, the performance of the Fund’s benchmark, the Barclays Government/Mortgage Index, is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects Fund level expenses, but does not reflect fees and expenses associated with any variable annuity contract or variable life insurance policy that uses the Fund as an investment option for any contract or policy. Had performance reflected all of those fees and expenses, performance would have been reduced. Performance also would have been reduced had expense limitations not been in effect. In addition to the investment adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover, and subscription and redemption cash flows affecting the Fund.

Government Income Fund’s Lifetime Performance

Performance of a $10,000 investment, with distributions reinvested, from January 9, 2006 through December 31, 2012.

| Average Annual Total Return through December 31, 2012 | One Year | Five Years | Since Inception | |||

Government Income Fund (Commenced January 9, 2006) | 2.78% | 4.77% | 5.02% |

19

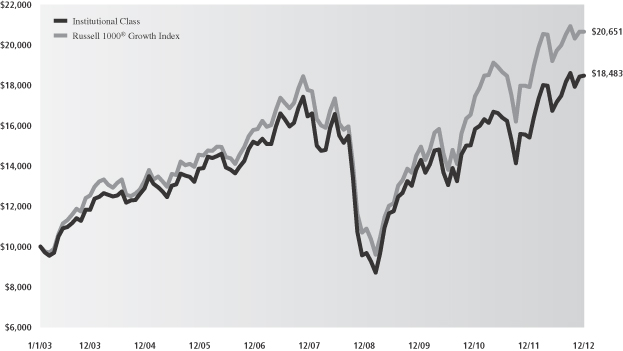

GOLDMAN SACHS VARIABLE INSURANCE TRUST GROWTH OPPORTUNITIES FUND

INVESTMENT OBJECTIVE

The Fund seeks long-term growth of capital.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Growth Equity Management Team discusses the Goldman Sachs Variable Insurance Trust — Goldman Sachs Growth Opportunities Fund’s (the “Fund”) performance and positioning for the 12-month period ended December 31, 2012 (the “Reporting Period”).

How did the Fund perform during the Reporting Period?

During the Reporting Period, the Fund’s Service Shares generated an average annual total return of 19.37%. This return compares to the 15.76% average annual total return of the Fund’s benchmark, the Russell Midcap® Growth Index (with dividends reinvested) (the “Russell Index”), during the same time period.

What key factors were responsible for the Fund’s performance during the Reporting Period?

The Fund outperformed the Russell Index largely because of effective stock selection.

Which equity market sectors contributed to Fund performance?

Our bottom-up approach focuses on security selection, and as a result, we do not make active sector-level investment decisions. That said, on a sector level, security selection in the information technology, telecommunication services and consumer discretionary sectors added to the Fund’s relative performance. Stock selection in the industrials, health care and materials sectors detracted from relative returns.

Which individual stocks added to the Fund’s relative performance during the Reporting Period?

Equinix, a leading data center solutions company, was the top contributor to the Fund’s relative returns during the Reporting Period. The company’s core business remained strong and its pricing up in the three main markets in which it operates — the U.S., Europe and Asia. Equinix also acquired data centers in Frankfurt, Hong Kong, Shanghai and Singapore to further drive growth. During the third quarter of 2012, the company announced its plans to convert to a real estate investment trust (“REIT”), which in our opinion should provide tax and valuation benefits. Meanwhile, during the Reporting Period, the market began to recognize that Equinix was trading at a discount to other data center operators that are publicly traded REITs and also to appreciate the growth and stability of Equinix’s revenue stream. At the end of the Reporting Period, we maintained conviction in the company’s ability to drive revenue growth, as it benefits from several secular growth drivers, including cloud computing, growth in Internet traffic and enterprise outsourcing, and rising demand for optimized network performance.

Another notable contributor during the Reporting Period was wireless communications infrastructure operator SBA Communications. Its shares performed well as it benefited from secular growth trends that are driving the wireless communication industry. We expect the company’s leasing revenues to continue to grow as wireless providers build out their 4G (fourth generation) networks to support increasing demand for mobile data usage. Furthermore, the company’s management is evaluating the possibility of converting SBA Communications into a REIT, which we believe could unlock further shareholder value. In our view, the secular growth trends driving the wireless communication industry remain intact as the industry continues to evolve from voice to data usage and as carriers must make additional investments in their networks to support increasing demand. We believe SBA Communications is well positioned to benefit from increased data usage, network upgrades and improved coverage as well as from regulations that govern the construction of new towers, which create high barriers to entry.

The Fund’s investment in PVH also contributed positively to relative performance. Shares of the apparel maker performed especially well during the second half of the Reporting Period on news of better than expected second quarter earnings. Earlier in 2012, PVH had faced economic headwinds in Europe as well as high cotton prices. However, cotton prices declined later in the Reporting Period. During the second calendar quarter, PVH’s Tommy Hilfiger brand was particularly strong in Europe. In November, the company share price rose to an all-time high following the announcement of its planned acquisition of Warnaco Group. Should the acquisition be completed, PVH would have full control of the Calvin Klein brand, which is widely expected to expand the company’s presence in Europe, Asia and Latin America. (The deal is expected to close in early 2013.) In our opinion, the acquisition could boost the company’s earnings and enhance its growth profile. We believe that PVH’s higher-margin brands,

20

GOLDMAN SACHS VARIABLE INSURANCE TRUST GROWTH OPPORTUNITIES FUND

such as Tommy Hilfiger and Calvin Klein, are likely to grow faster than the company’s heritage business and as a result, the company’s operating profit could accelerate meaningfully.

Which individual stocks detracted from the Fund’s performance during the Reporting Period?

A position in Deckers Outdoor detracted from the Fund’s relative returns during the Reporting Period. The company’s earnings and earnings guidance were disappointing during 2012, as the footwear and apparel designer continued to deal with the impact of an unseasonably warm 2011 winter, which had pressured its inventory position and profitability. In our view, the inventory pressure should subside over the course of 2013. We continue to believe in the strength of the company’s Ugg brand and expect Deckers Outdoor to show improved sales and profit margin expansion in 2013.

An investment in Rovi also hampered relative performance during the Reporting Period. Rovi holds patents on interactive program guides for video delivery services and devices. The Fund held the stock because we saw the growth potential of Rovi’s electronic programming guide business. However, after some management execution errors and delays in the market development of this key business, we lost confidence in the company’s ability to capitalize on the opportunity. We eliminated the Fund’s position and reallocated the capital to higher conviction names.

Another key detractor from the Fund’s results during the Reporting Period was NetApp, a developer of data storage hardware and software for enterprise clients. The company cut its revenue guidance in the second calendar quarter, citing macroeconomic weakness and softening industry trends. In addition, investors appeared concerned about a possible drop in 2012 year-end business technology spending. NetApp’s share price suffered the most during the second quarter and in October, but it began to recover toward the end of Reporting Period. We continue to believe NetApp has a strong competitive position in an industry benefiting from several secular growth trends, such as virtualization, which should increase demand for the company storage products. For example, NetApp specializes in network-attached storage that we believe should continue to take market share from direct-attached products. In our opinion, the company’s storage devices are easier to buy, install and manage than competing products, which should also drive market share gains.

Did the Fund make any significant purchases or sales during the Reporting Period?

The Fund bought shares of Family Dollar Stores during the Reporting Period. The company operates a chain of more than 7,000 general merchandise retail discount stores in 44 states, providing consumers with a diverse array of merchandise in neighborhood stores. We have confidence in the business strategy presented by the company’s new chief executive officer, which we expect to be implemented during the next few calendar quarters.

During the Reporting Period, we purchased shares of Activision Blizzard, a worldwide publisher of online, personal computer, console, handheld and mobile interactive entertainment products. Activision Blizzard owns three of the largest franchises in the electronic gaming industry — Call of Duty and Skylanders on gaming consoles and World of Warcraft on personal computers. World of Warcraft is offered through a monthly subscription model that provides a large and reliable cash flow stream, which can be used to invest in newer intellectual properties, such as Skylanders or Call of Duty. In our view, these newer intellectual properties, as well as upcoming new releases, have profit margin structures larger than the corporate average, and we believe they should drive the company’s operating margins higher over the next few years.

We initiated a position in Chipotle Mexican Grill, which develops and operates fast casual, fresh Mexican food restaurants throughout the U.S. and in select international locations. We believe that Chipotle Mexican Grill, with its unique business model and strong brand recognition, is a best-in-class franchise with attractive expansion opportunities both domestically and internationally. We are also confident in the management team’s ability to execute and in the company’s ability to maintain strong year-over-year sales growth, driven by sustained menu pricing power and continued high operating margins.

During the Reporting Period, the Fund sold its position in electronic transaction processing provider Global Payments as the ramifications of a security breach continued to unfold. While the fundamentals of the business did not materially change, we believe Global Payments’ sterling reputation has been tarnished. In the aftermath of the security breach, we saw potential for slowing growth in the company’s important sales channels within North America, which account for 70% of its total revenue.

We liquidated the Fund’s position in Western Union, which provides global money transfer services. Though Western Union’s transaction-based business model and free cash flow generation remained attractive, we were concerned about the company’s inability to increase revenue growth. In addition, Western Union issued 2012 earnings per share guidance that fell below expectations. Consequently, we eliminated the Fund’s position and reallocated the capital to higher conviction names.

21

GOLDMAN SACHS VARIABLE INSURANCE TRUST GROWTH OPPORTUNITIES FUND

We eliminated the Fund’s position in St. Jude Medical during the Reporting Period. Reports of safety and quality issues continued to be an overhang for the global medical device company, allowing competitors to grow their market share. St. Jude Medical was also experiencing pricing headwinds, with negative price pressure amid flat to marginal volume growth.

Were there any notable changes in the Fund’s weightings during the Reporting Period?

There were no notable changes in the Fund’s weightings during the Reporting Period.

How did the Fund use derivatives and similar instruments during the Reporting Period?

In keeping with its investment process, the Fund did not use derivatives during the Reporting Period.

How was the Fund positioned relative to the Russell Index at the end of the Reporting Period?

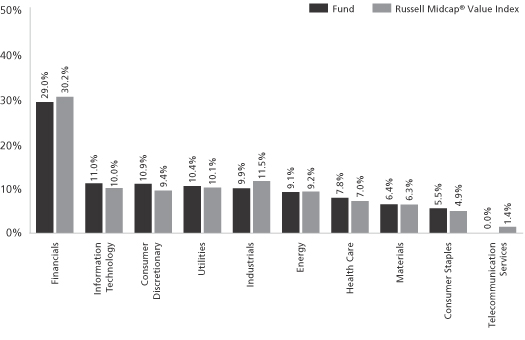

As mentioned, the Fund’s sector positioning relative to the Russell Index is the result of our stock selection, as we take a pure bottom-up, research-intensive approach to investing. From that perspective, then, at the end of the Reporting Period, the Fund’s portfolio was broadly diversified with overweighted positions compared to the Russell Index in the information technology, telecommunication services and financials. The Fund had smaller weightings than the Russell Index in the industrials sector, consumer discretionary, energy, consumer staples, utilities and materials sectors. It was relatively neutral compared to the Russell Index in the health care sector at the end of the Reporting Period.

22

FUND BASICS

Growth Opportunities Fund

as of December 31, 2012

STANDARDIZED TOTAL RETURNS1

| For the period ended 12/31/12 | One Year | Five Year | Since Inception | Inception Date | ||||||||||

| Service | 19.37 | % | 5.14 | % | 6.68 | % | 1/09/06 | |||||||

| 1 | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at net asset value (“NAV”). Because Service Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

Total return figures in the above chart represent past performance and do not indicate future results, which will vary. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the total return figures in the above chart. Please visit www.goldmansachsfunds.com/vit to obtain the most recent month-end returns. Performance reflects fee waivers and/or expense limitations in effect. In their absence, performance would be reduced.

EXPENSE RATIOS2

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||

| Service | 1.15 | % | 1.41 | % | ||||

| 2 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least April 27, 2013, and prior to such date the investment adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

TOP TEN HOLDINGS AS OF 12/31/123

| Holding | % of Net Assets | Line of Business | ||||

| SBA Communications Corp. Class A | 3.6% | Telecommunication Services | ||||

| PVH Corp. | 2.7 | Consumer Durables & Apparel | ||||

| CBRE Group, Inc. Class A | 2.3 | Real Estate | ||||

| Equinix, Inc. | 2.2 | Software & Services | ||||

| Rackspace Hosting, Inc. | 2.1 | Software & Services | ||||

| PetSmart, Inc. | 2.1 | Retailing | ||||

| Amphenol Corp. Class A | 2.0 | Technology Hardware & Equipment | ||||

| Agilent Technologies, Inc. | 2.0 | Pharmaceuticals, Biotechnology & Life Sciences | ||||

| Xilinx, Inc. | 1.9 | Semiconductors & Semiconductor Equipment | ||||

| Crown Castle International Corp. | 1.9 | Telecommunication Services | ||||

| 3 | The top 10 holdings may not be representative of the Fund’s future investments. |

23

FUND BASICS

FUND vs. BENCHMARK SECTOR ALLOCATIONS4

As of December 31, 2012

| 4 | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

24

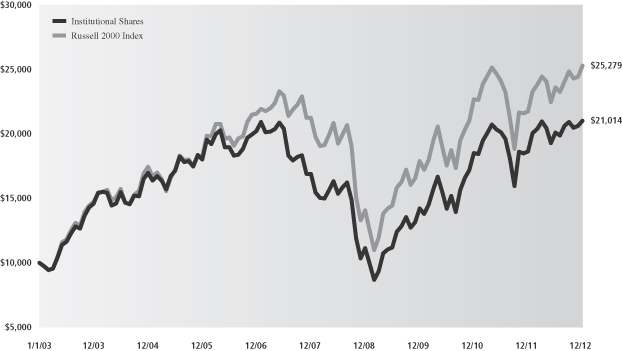

GOLDMAN SACHS VARIABLE INSURANCE TRUST GROWTH OPPORTUNITIES FUND

Performance Summary

December 31, 2012

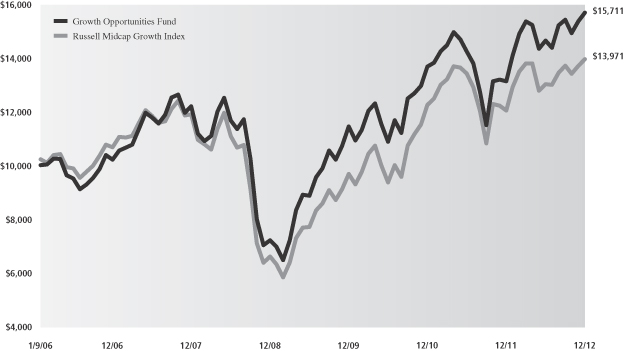

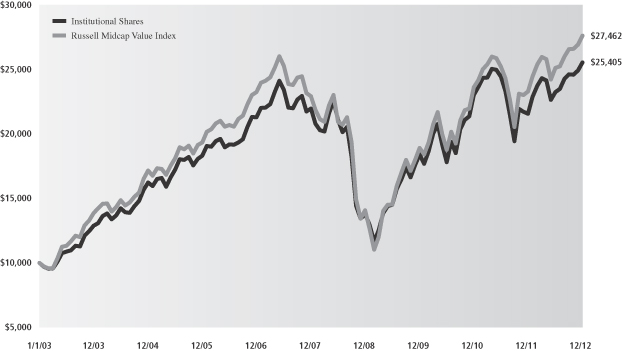

The following graph shows the value, as of December 31, 2012, of a $10,000 investment made in the Fund on January 9, 2006 (commencement of operations). For comparative purposes, the performance of the Fund’s benchmark, the Russell Midcap Growth Index (with dividends reinvested), is shown. This performance data represents past performance and should not be considered indicative of future performance which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects Fund level expenses, but does not reflect fees and expenses associated with any variable annuity contract or variable life insurance policy that uses the Fund as an investment option for any contract or policy. Had performance reflected all of those fees and expenses, performance would have been reduced. Performance also would have been reduced had expense limitations not been in effect. In addition to the investment adviser’s decisions regarding issuer/industry investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover, and subscription and redemption cash flows affecting the Fund.

Growth Opportunities Fund’s Lifetime Performance

Performance of a $10,000 investment, with distributions reinvested, from January 9, 2006 through December 31, 2012.

| Average Annual Total Return through December 31, 2012 | One Year | Five Years | Since Inception | |||

Growth Opportunities Fund (Commenced January 9, 2006) | 19.37% | 5.14% | 6.68% |

25

GOLDMAN SACHS VARIABLE INSURANCE TRUST CORE FIXED INCOME FUND

Schedule of Investments

December 31, 2012

| Principal Amount | Interest Rate | Maturity Date | Value | |||||||||

| Corporate Obligations – 28.2% | ||||||||||||

| Automobiles & Components – 0.4% |

| ||||||||||

| Ford Motor Credit Co. LLC |

| ||||||||||

| $ | 525,000 | 3.984% | 06/15/16 | $ | 553,875 | |||||||

|

| |||||||||||

| Banks – 6.9% |

| ||||||||||

| Abbey National Treasury Services PLC |

| ||||||||||

| 175,000 | 2.875 | 04/25/14 | 177,543 | |||||||||

| ANZ Capital Trust II(a)(b) |

| ||||||||||

| 425,000 | 5.360 | 12/15/53 | 433,500 | |||||||||

| Bank of America Corp. |

| ||||||||||

| 225,000 | 6.000 | 09/01/17 | 263,625 | |||||||||

| 200,000 | 5.750 | 12/01/17 | 232,744 | |||||||||

| 100,000 | 5.625 | 07/01/20 | 117,903 | |||||||||

| 350,000 | 5.700 | 01/24/22 | 420,900 | |||||||||

| Barclays Bank PLC(b) |

| ||||||||||

| 125,000 | 6.050 | 12/04/17 | 138,299 | |||||||||

| Capital One Bank NA |

| ||||||||||

| 300,000 | 8.800 | 07/15/19 | 404,797 | |||||||||

| Capital One Financial Corp. |

| ||||||||||

| 225,000 | 1.000 | 11/06/15 | 223,728 | |||||||||

| CBA Capital Trust II(a)(b)(c) |

| ||||||||||

| 325,000 | 6.024 | 12/31/49 | 331,849 | |||||||||

| Citigroup, Inc. |

| ||||||||||

| 600,000 | 5.000 | 09/15/14 | 632,064 | |||||||||

| 175,000 | 4.500 | 01/14/22 | 195,391 | |||||||||

| ING Bank N.V.(b) |

| ||||||||||

| 450,000 | 2.000 | 09/25/15 | 453,330 | |||||||||

| JPMorgan Chase & Co. |

| ||||||||||

| 100,000 | 3.250 | 09/23/22 | 102,971 | |||||||||

| Merrill Lynch & Co., Inc. |

| ||||||||||

| 325,000 | 6.400 | 08/28/17 | 382,485 | |||||||||

| Mizuho Corporate Bank Ltd.(b) |

| ||||||||||

| 200,000 | 2.550 | 03/17/17 | 209,142 | |||||||||

| 225,000 | 2.950 | 10/17/22 | 222,238 | |||||||||

| Morgan Stanley & Co. |

| ||||||||||

| 325,000 | 6.250 | 08/28/17 | 374,148 | |||||||||

| 450,000 | 5.950 | 12/28/17 | 512,984 | |||||||||

| 125,000 | 5.500 | 07/24/20 | 139,750 | |||||||||

| 125,000 | 5.500 | 07/28/21 | 141,922 | |||||||||

| 125,000 | 4.875 | 11/01/22 | 129,215 | |||||||||

| Regions Financial Corp. |

| ||||||||||

| 325,000 | 5.750 | 06/15/15 | 351,406 | |||||||||

| Resona Bank Ltd.(a)(b)(c) |

| ||||||||||

| 650,000 | 5.850 | 12/31/49 | 699,730 | |||||||||

| Royal Bank of Scotland Group PLC |

| ||||||||||

| 250,000 | 2.550 | 09/18/15 | 255,592 | |||||||||

| Santander Holdings USA, Inc. |

| ||||||||||

| 75,000 | 3.000(a) | 09/24/15 | 76,432 | |||||||||

| 165,000 | 4.625 | 04/19/16 | 174,334 | |||||||||

| Standard Chartered PLC(b) |

| ||||||||||

| 150,000 | 5.500 | 11/18/14 | 161,535 | |||||||||

| The Bear Stearns Companies LLC |

| ||||||||||

| 400,000 | 7.250 | 02/01/18 | 500,650 | |||||||||

| Union Bank NA |

| ||||||||||

| 425,000 | 2.125 | 06/16/17 | 436,106 | |||||||||

|

| |||||||||||

| Principal Amount | Interest Rate | Maturity Date | Value | |||||||||

| Corporate Obligations – (continued) | ||||||||||||

| Banks – (continued) |

| ||||||||||

| Wachovia Bank NA |

| ||||||||||

| $ | 300,000 | 6.600% | 01/15/38 | $ | 410,472 | |||||||

|

| |||||||||||

| 9,306,785 | ||||||||||||

|

| |||||||||||

| Chemicals – 1.0% |

| ||||||||||

| CF Industries, Inc. |

| ||||||||||

| 150,000 | 6.875 | 05/01/18 | 182,625 | |||||||||

| Eastman Chemical Co. |

| ||||||||||

| 150,000 | 2.400 | 06/01/17 | 155,379 | |||||||||

| 150,000 | 4.800(a) | 09/01/42 | 162,208 | |||||||||

| Ecolab, Inc. |

| ||||||||||

| 450,000 | 4.350 | 12/08/21 | 503,403 | |||||||||

| NewMarket Corp.(b) |

| ||||||||||

| 225,000 | 4.100 | 12/15/22 | 229,560 | |||||||||

| The Dow Chemical Co. |

| ||||||||||

| 137,000 | 7.600 | 05/15/14 | 149,384 | |||||||||

|

| |||||||||||

| 1,382,559 | ||||||||||||

|

| |||||||||||

| Diversified Manufacturing – 0.4% |

| ||||||||||

| General Electric Co. |

| ||||||||||

| 300,000 | 2.700 | 10/09/22 | 305,246 | |||||||||

| Xylem, Inc. |

| ||||||||||

| 250,000 | 3.550 | 09/20/16 | 266,257 | |||||||||

|

| |||||||||||

| 571,503 | ||||||||||||

|

| |||||||||||

| Electric – 0.6% |

| ||||||||||

| PPL WEM Holdings PLC(a)(b) |

| ||||||||||

| 220,000 | 5.375 | 05/01/21 | 247,871 | |||||||||

| Progress Energy, Inc. |

| ||||||||||

| 350,000 | 7.000 | 10/30/31 | 448,469 | |||||||||

| Puget Sound Energy, Inc. Series A(a)(c) |

| ||||||||||

| 75,000 | 6.974 | 06/01/67 | 79,594 | |||||||||

|

| |||||||||||

| 775,934 | ||||||||||||

|

| |||||||||||

| Energy – 4.1% |

| ||||||||||

| Anadarko Petroleum Corp. |

| ||||||||||

| 125,000 | 6.375 | 09/15/17 | 149,145 | |||||||||

| BG Energy Capital PLC(a)(c) |

| ||||||||||

| 325,000 | 6.500 | 11/30/72 | 349,102 | |||||||||

| BP Capital Markets PLC |

| ||||||||||

| 225,000 | 3.200 | 03/11/16 | 239,888 | |||||||||

| 500,000 | 4.500 | 10/01/20 | 576,627 | |||||||||

| 145,000 | 3.561 | 11/01/21 | 156,920 | |||||||||

| Dolphin Energy Ltd.(b) |

| ||||||||||

| 181,512 | 5.888 | 06/15/19 | 204,993 | |||||||||

| 200,000 | 5.500 | 12/15/21 | 233,300 | |||||||||

| Gazprom OAO Via Gaz Capital SA(d) |

| ||||||||||

| 350,000 | 9.250 | 04/23/19 | 460,687 | |||||||||

| Nexen, Inc. |

| ||||||||||

| 150,000 | 5.875 | 03/10/35 | 185,673 | |||||||||

| 305,000 | 6.400 | 05/15/37 | 396,480 | |||||||||

| Pemex Project Funding Master Trust |

| ||||||||||

| 150,000 | 6.625 | 06/15/35 | 190,125 | |||||||||

|

| |||||||||||

| 26 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST CORE FIXED INCOME FUND

| Principal Amount | Interest Rate | Maturity Date | Value | |||||||||

| Corporate Obligations – (continued) | ||||||||||||

| Energy – (continued) |

| ||||||||||

| Petrobras International Finance Co. |

| ||||||||||

| $ | 40,000 | 5.750% | 01/20/20 | $ | 45,416 | |||||||

| 190,000 | 5.375 | 01/27/21 | 213,484 | |||||||||

| PTTEP Canada International Finance Ltd.(b) |

| ||||||||||

| 240,000 | 5.692 | 04/05/21 | 277,497 | |||||||||

| Ras Laffan Liquefied Natural Gas Co. Ltd. III(b) |

| ||||||||||

| 250,000 | 5.500 | 09/30/14 | 268,887 | |||||||||

| Rosneft Oil Co. via Rosneft International Finance Ltd.(b) |

| ||||||||||

| 200,000 | 4.199 | 03/06/22 | 204,586 | |||||||||

| TNK-BP Finance SA |

| ||||||||||

| 140,000 | 7.875 | 03/13/18 | 170,100 | |||||||||

| Transocean, Inc. |

| ||||||||||

| 100,000 | 4.950 | 11/15/15 | 109,451 | |||||||||

| 625,000 | 6.500 | 11/15/20 | 755,781 | |||||||||

| 125,000 | 6.375 | 12/15/21 | 151,868 | |||||||||

| Weatherford International Ltd. |

| ||||||||||

| 175,000 | 9.625 | 03/01/19 | 228,250 | |||||||||

|

| |||||||||||

| 5,568,260 | ||||||||||||

|

| |||||||||||

| Food & Beverage – 1.4% |

| ||||||||||

| Heineken NV(b) |

| ||||||||||

| 225,000 | 3.400 | 04/01/22 | 234,690 | |||||||||

| Kraft Foods Group, Inc.(b) |

| ||||||||||

| 275,000 | 6.125 | 08/23/18 | 336,628 | |||||||||

| Mondelez International, Inc. |

| ||||||||||

| 150,000 | 5.375 | 02/10/20 | 181,663 | |||||||||

| 200,000 | 6.500 | 02/09/40 | 268,667 | |||||||||

| Pernod-Ricard SA(b) |

| ||||||||||

| 575,000 | 4.450 | 01/15/22 | 635,751 | |||||||||

| SABMiller Holdings, Inc.(b) |

| ||||||||||

| 275,000 | 2.450 | 01/15/17 | 286,659 | |||||||||

|

| |||||||||||

| 1,944,058 | ||||||||||||

|

| |||||||||||

| Food & Staples Retailing – 0.6% |

| ||||||||||

| CVS Caremark Corp.(a) |

| ||||||||||