UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08361

Goldman Sachs Variable Insurance Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606-6303

(Address of principal executive offices) (Zip code)

| Copies to: | ||

| Geoffrey R.T. Kenyon, Esq. | ||

Caroline Kraus | Dechert LLP | |

| Goldman, Sachs & Co. | 100 Oliver Street | |

| 200 West Street | 40th Floor | |

| New York, NY 10282 | Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: December 31

Date of reporting period: June 30, 2013

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| The Semi-Annual Reports to Stockholders are filed herewith. |

Goldman

Sachs Variable Insurance Trust

Goldman Sachs

Global Markets

Navigator Fund

Semi-Annual Report

June 30, 2013

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Principal Investment Strategies and Risks

This is not a complete list of the risks that may affect the Fund. For additional information concerning the risks applicable to the Fund, please see the Fund’s Prospectus.

Shares of the Goldman Sachs Variable Insurance Trust — Goldman Sachs Global Markets Navigator Fund are offered to separate accounts of participating life insurance companies for the purpose of funding variable annuity contracts and variable life insurance policies. Shares of the Fund are not offered directly to the general public. The variable annuity contracts and variable life insurance policies are described in the separate prospectuses issued by participating insurance companies. You should refer to those prospectuses for information about surrender charges, mortality and expense risk fees and other charges that may be assessed by participating insurance companies under the variable annuity contracts or variable life insurance policies. Such fees or charges, if any, may affect the return you realize with respect to your investments. Ask your representative for more complete information. Please consider the Fund’s objective, risks and charges and expenses, and read the Prospectus carefully before investing. The Prospectus contains this and other information about the Fund.

The Goldman Sachs Global Markets Navigator Fund seeks to achieve investment results that approximate the performance of the Goldman Sachs Global Markets Navigator Index (the “Index”). The Index is comprised of, and allocates exposure to, a set of underlying indices representing various global asset classes including, but not limited to, global equity, fixed income and commodity assets. The Index is constructed using a proprietary methodology developed by the index provider, and is rebalanced at least monthly. The Fund’s performance may not match, and may vary substantially from, that of the Index. There can be no assurance that the methodology used by the index provider in constructing the Index will correctly forecast certain risks or make effective tactical decisions, and the Fund’s attempt to track this Index may cause it to underperform general securities markets and/or other asset classes. Derivative instruments (including swaps) may involve a high degree of financial risk. These risks include the risk that a small movement in the price of the underlying security or benchmark may result in a disproportionately large movement, unfavorable or favorable, in the price of the derivative instrument; risk of default by a counterparty; and liquidity risk. The Fund’s use of derivatives may result in leverage, which can make the Fund more volatile. Over-the-counter transactions are subject to less government regulation and supervision. The Fund’s equity investments are subject to market risk, which means that the value of its investments may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. The Fund’s fixed income investments are subject to the risks associated with debt securities generally, including credit, liquidity and interest rate risk. The Fund is also subject to the risk that the issuers of sovereign debt or the government authorities that control the payment of debt may be unable or unwilling to repay principal or interest when due. High yield, lower rated investments involve greater price volatility and present greater risks than higher rated fixed income securities. The value of the Fund’s treasury inflation protected securities (TIPS) generally fluctuates in response to inflationary concerns, and as inflationary concerns decrease, TIPS become less valuable. Any guarantee on U.S. government securities applies only to the underlying securities of the Fund if held to maturity and not to the value of the Fund’s shares. The Fund is subject to the risk that exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. At times, the Fund may be unable to sell certain of its portfolio securities without a substantial drop in price, if at all. The Fund’s investments in other investment companies (including ETFs) subject it to additional expenses. Because the Fund may concentrate its investments in an industry (only in the event that an industry represents 20% or more of

1

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

the Fund’s index), the Fund may be subject to greater risk of loss as a result of adverse economic, business or other developments affecting that industry. The Fund is “non-diversified” and may invest more of its assets in fewer issuers than “diversified” funds. Accordingly, the Fund may be more susceptible to adverse developments affecting any single issuer held in its portfolio and to greater losses resulting from these developments.

The “GS Global Markets Navigator Index” is a trademark or service mark of Goldman, Sachs & Co. and has been licensed for use by the Investment Adviser in connection with the Fund. As the licensor of this trademark or service mark, Goldman, Sachs & Co. does not make any representation regarding the advisability of investing in the Fund.

2

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

INVESTMENT OBJECTIVE

The Fund seeks to achieve investment results that approximate the performance of the GS Global Markets Navigator Index.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Investment Strategies Team discusses the Goldman Sachs Variable Insurance Trust — Goldman Sachs Global Markets Navigator Fund’s (the “Fund”) performance and positioning for the six-month period ended June 30, 2013 (the “Reporting Period”).

How did the Fund perform during the Reporting Period?

During the Reporting Period, the Fund’s Service Shares generated a cumulative total return of 6.37%. This return compares to the 8.30% cumulative total return of the Fund’s benchmark, the GS Global Markets Navigator Index (the “Index”), during the same time period. A blended index comprised 60% of the Standard & Poor’s® 500 Indexa (with dividends reinvested) and 40% of the Barclays U.S. Aggregate Bond Indexb (with dividends reinvested) generated a cumulative total return of 7.10% during the same time period.

The S&P 500® Index and the Barclays U.S. Aggregate Bond Index generated cumulative total returns of 13.82% and -2.44%, respectively, during the same time period.

Importantly, during the Reporting Period, the Fund’s overall annualized volatility was 10.50%, less than the S&P® 500 Index’s annualized volatility of 12.10% during the same time period.

What economic and market factors most influenced the Fund during the Reporting Period?

U.S. equity markets rallied during the first quarter of 2013 despite the overhang of automatic spending cuts, or sequestration, that went into effect in March 2013. U.S. equity performance reflected a variety of improving U.S. economic indicators — strong momentum in the housing market continued and the employment picture improved. However, in the second quarter of 2013, bullish sentiment began to fade, and the U.S. equity rally halted in mid-May 2013 when Federal Reserve (“Fed”) Chair Bernanke announced the potential “tapering” of the pace of quantitative easing asset purchases. U.S. equity markets reacted negatively again in June 2013 to news the slowing of the asset purchase program could begin later in the year, with the program ending by the middle of 2014 if the economy grows as expected. U.S. equity markets calmed toward the end of the month as a downward revision of first quarter Gross Domestic Product (“GDP”) from 2.4% to 1.8% supported reassurance from the Fed that it would only begin reducing asset purchases if the economy was clearly on track.

In the international equity markets, European equities managed gains during the Reporting Period overall, despite a banking crisis in Cyprus and further economic contraction in the Eurozone. Strong performance by the Japanese equity market dominated returns for the Reporting Period but was partially offset by weaker returns for the Asia ex-Japan region, where such returns were exaggerated by depreciating currencies. The yen weakened to its lowest level against the U.S. dollar since mid-2009 on expectations the new head of the Bank of Japan will aggressively pursue a 2% inflation target. Japanese equities hit a five-year high during May 2013 before taking a sharp turn down with a number of other global equity markets. However, after Fed Chair Bernanke’s comments about the potential “tapering” of the pace of quantitative easing asset purchases, the rally in international equities virtually halted. In June, international equity markets also reacted negatively to news the Fed could begin slowing its asset purchase program later in 2013.

The global fixed income markets, which had begun the Reporting Period in January 2013 with a rally, reversed course during February 2013, primarily on worries about U.S. fiscal policy gridlock and Italy’s elections. In March 2013, Cyprus’ bailout by Euro-area finance ministers raised the prospect of a tax on bank deposits, prompting fears of a more widespread run on European banks. Investors grew more defensive, and government bond yields declined. In contrast, spread, or non-U.S. Treasury, sectors

| a | The S&P 500 Index is the Standard & Poor’s 500 Composite Stock Prices Index of 500 stocks, an unmanaged index of common stock prices. The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. |

| b | The Barclays U.S. Aggregate Bond Index represents an unmanaged diversified portfolio of fixed income securities, including U.S. Treasuries, investment-grade corporate bonds, and mortgage-backed and asset-backed securities. The Index figures do not reflect any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. |

3

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

remained relatively firm. In early April 2013, government bond yields declined on disappointing economic data before stabilizing later in the month. Spread sectors performed well, as investors looked past sluggish economic data for higher yielding assets in the exceptionally low interest rate environment. After Fed Chair Bernanke said the U.S. central bank could begin reducing asset purchases, government bond yields rose substantially. At the same time, spread sectors grew more volatile, reflecting widespread uncertainty over how markets may function as the Fed withdraws support. In June 2013, bond investors focused on the U.S. economy and stronger than expected payrolls data, which reinforced expectations the Fed would start reducing its quantitative easing during 2013. Government bond yields continued to increase, as the Fed meeting and press conference were more hawkish than expected. Spread sectors remained volatile. Meanwhile, European economic data improved, with modest increases in the Eurozone Purchasing Managers Indices and accelerating expansion in the U.K. Japan’s economy continued to respond positively to its government and central bank policies. In contrast, China’s economic data raised concerns about the extent of that nation’s slowdown.

What key factors were responsible for the Fund’s performance during the Reporting Period?

The Fund seeks to achieve its objective by investing in financial instruments that provide exposure to the various underlying global equity and fixed income indices that comprise the Index. Using a momentum-based methodology, the Fund strives to manage risk and hedge this with “potential” in changing market environments.

Momentum investing seeks growth of capital by gaining exposure to asset classes that have exhibited trends in price performance over selected time periods. In managing the Fund, we use a methodology that evaluates historical three-, six- and nine-month returns, volatilities and correlations across a range of nine global asset classes. Represented by indices, these asset classes include, within the equities category, U.S. large-cap, Europe, Asia, emerging markets, U.K. and small-cap stocks. Within the fixed income category, the Fund may allocate assets to U.S., European and Japanese fixed income securities. The analysis of these asset classes drives the aggregate allocations of the Fund over time. We believe market price momentum — either positive or negative — has significant predictive power.

During the Reporting Period, the Fund’s fixed income allocations detracted from its relative performance. The Fund’s allocation to German government bonds hurt returns most, especially during May and June 2013. Its exposure to U.S. Treasury securities also detracted from relative returns during the Reporting Period.

On the positive side, the Fund’s positioning in equities added to its relative performance. In particular, the Fund benefited from its allocation to Japanese equities and its exposure to U.S. large-cap and small-cap stocks.

How did volatility affect the Fund during the Reporting Period?

As part of our investment approach, we seek to mitigate the Fund’s volatility. As mentioned earlier, during the Reporting Period, the Fund’s actual volatility (annualized, using daily returns) was 10.50% versus the S&P 500® Index’s annualized volatility of 12.10%.

How was the Fund positioned during the Reporting Period?

During the Reporting Period, we tactically managed the Fund’s allocations across equity and fixed income markets based on the momentum and volatility of these asset classes. When the Reporting Period began, the Fund’s allocations were split rather evenly between equities and fixed income. By the end of March 2013, the Fund’s allocation to equities had risen to approximately 80% of its total assets, as the Fund benefited from the strong first calendar quarter rally in the global equity markets. During the first quarter of 2013, we concentrated the Fund’s equity investments in U.S. and Japanese equities and eliminated its position in emerging markets equities.

Within its fixed income allocation at the beginning of the Reporting Period, the Fund had a weighting of approximately 40% of its total assets in U.S. Treasury securities. By the end of March 2013, the Fund’s weighting in U.S. Treasury securities had dipped to less than 5% of its total assets, and we held it near zero throughout the second quarter of 2013.

In addition, toward the end of June 2013, the Fund’s daily volatility control was triggered (that is, the Fund’s 90-day realized volatility exceeded our predetermined 10% threshold) and in keeping with our momentum-based methodology, we proportionally reduced portfolio risk by 20% and added an allocation to cash.

4

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

How did the Fund use derivatives and similar instruments during the Reporting Period?

During the Reporting Period, the Fund used exchange-traded index futures contracts to gain exposure to U.S. small-cap equities and to non-U.S. developed market equities, including those in Europe and Japan, as well as to gain exposure to U.S. and non-U.S. fixed income.

Were there any changes to the Fund’s portfolio management team during the Reporting Period?

After 33 years of distinguished service, Don Mulvihill, CIO of Customized Beta Strategies within the Quantitative Investment Strategies (“QIS”) team, decided to retire from the firm. As of June 2013, Gary Chropuvka assumed Mr. Mulvihill’s role as Head of the Customized Beta Strategies business, overseeing the team’s tax-efficient, rules-based and customized beta investment strategies. Mr. Chropuvka brings extensive experience having joined QIS in 1999 with Mr. Mulvihill to manage the team’s tax-efficient investment strategies. All of Mr. Mulvihill’s direct investment responsibilities were performed within a co-lead or team leadership structure and follow processes that provide continuity in day-to-day investment decision-making in each portfolio.

What is the Fund’s tactical asset allocation view and strategy for the months ahead?

By the end of the Reporting Period, we had reduced the Fund’s allocation to equities and fixed income. We had added a significant allocation to cash, as we sought to reduce risk, largely in response to heightened volatility and poor momentum across the financial markets during June 2013. In fixed income, at the end of the Reporting Period, the Fund had exposure to German and Japanese government bonds. Within equities, it had exposure to U.S. large-cap and small-cap equities. At the end of the Reporting Period, the Fund had a reduced allocation to Japanese equities because of the increased volatility in the Japanese equity market. The Fund, like the Index, had neutral exposure to emerging markets equities.

Going forward, we intend to position the Fund to provide exposure to price momentum from among nine underlying asset classes, while dynamically seeking to manage the volatility, or risk, of the overall portfolio. When volatility increases, our goal is to preserve capital by moving the Fund into less volatile assets such as fixed income. When we believe the financial markets have become more stable, we expect to allocate a greater portion of the Fund’s assets to equities. There is no guarantee the Fund’s dynamic management strategy will cause it to achieve its investment objective.

5

FUND BASICS

Global Markets Navigator Fund

as of June 30, 2013

STANDARDIZED TOTAL RETURNS1

| For the period ended 6/30/13 | One Year | Since Inception | Inception Date | |||||||

| Service | 11.81 | % | 8.50 | % | 4/16/12 | |||||

| 1 | Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at net asset value (“NAV”). Because Service Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

Total return figures in the above chart represent past performance and do not indicate future results, which will vary. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the total return figures in the above chart. Please visit www.goldmansachsfunds.com/vit to obtain the most recent month-end returns. Performance reflects fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced.

EXPENSE RATIOS2

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||

| Service | 1.08 | % | 3.78 | % | ||||

| 2 | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations), are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least April 30, 2014, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

6

FUND BASICS

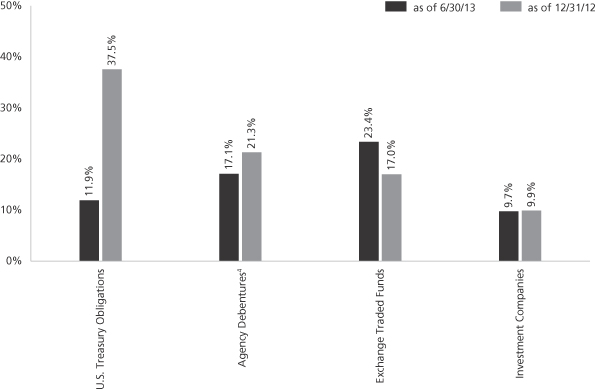

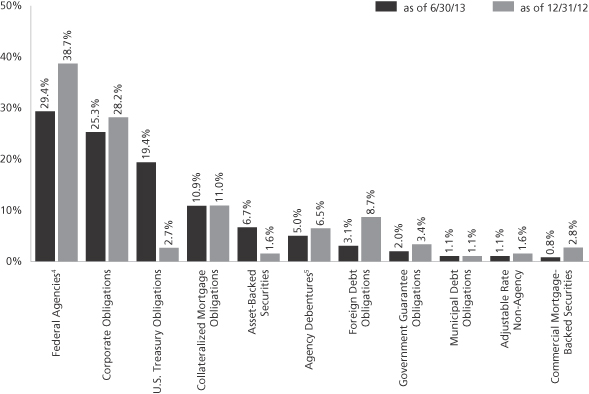

FUND COMPOSITION3

| 3 | The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. Figures in the above graph may not sum to 100% due to the exclusion of other assets and liabilities. Underlying sector allocations of exchange traded funds (“ETFs”) held by the Fund are not reflected in the graph above. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

| 4 | “Agency Debentures” include agency securities offered by companies such as Federal Home Loan Bank and Federal Home Loan Mortgage Corporation, which operate under a government charter. While they are required to report to a government regulator, their assets are not explicitly guaranteed by the government and they otherwise operate like any other publicly traded company. |

7

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Schedule of Investments

June 30, 2013 (Unaudited)

| Principal Amount | Interest Rate | Maturity Date | Value | |||||||||||

| Agency Debentures(a) – 17.1% | ||||||||||||||

| FHLB | ||||||||||||||

| $ | 4,724,000 | 0.000 | % | 09/20/13 | $ | 4,723,575 | ||||||||

| FNMA | ||||||||||||||

| 4,724,000 | 0.000 | 09/18/13 | 4,723,584 | |||||||||||

|

| |||||||||||||

| TOTAL AGENCY DEBENTURES | ||||||||||||||

| (Cost $9,445,376) | $ | 9,447,159 | ||||||||||||

|

| |||||||||||||

| Shares | Description | Values | ||||||||||||

| Exchange Traded Fund – 23.4% | ||||||||||||||

| 175,974 | Vanguard S&P 500 | $ | 12,916,492 | |||||||||||

| (Cost $12,537,769) | ||||||||||||||

|

| |||||||||||||

| Shares | Rate | Value | ||||||||||||

| Investment Company(b) – 9.7% | ||||||||||||||

| Goldman Sachs Financial Square Government Fund — | | ||||||||||||

| 5,372,192 | 0.006% | $ | 5,372,192 | |||||||||||

| (Cost $5,372,192) | ||||||||||||||

|

| |||||||||||||

| Principal Amount | Interest Rate | Maturity Date | Value | |||||||||||

| U.S. Treasury Obligations – 11.9% | ||||||||||||||

| United States Treasury Bill(a) |

| ||||||||||||

| $ | 6,028,000 | 0.000 | % | 08/01/13 | $ | 6,027,974 | ||||||||

| United States Treasury Note |

| ||||||||||||

| 535,000 | 3.125 | 05/15/21 | 574,435 | |||||||||||

|

| |||||||||||||

| TOTAL U.S. TREASURY OBLIGATIONS | ||||||||||||||

| (Cost $6,632,355) | $ | 6,602,409 | ||||||||||||

|

| |||||||||||||

| TOTAL INVESTMENTS – 62.1% | ||||||||||||||

| (Cost $33,987,692) | $ | 34,338,252 | ||||||||||||

|

| |||||||||||||

| OTHER ASSETS IN EXCESS OF | | 20,986,466 | |||||||||||

|

| |||||||||||||

| NET ASSETS – 100.0% | $ | 55,324,718 | ||||||||||||

|

| |||||||||||||

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. | ||

| (a) | Issued with a zero coupon. Income is recognized through the accretion of discount. | |

| (b) | Represents an affiliated issuer. | |

| Investment Abbreviations: | ||||

FHLB | — | Federal Home Loan Bank | ||

| FNMA | — | Federal National Mortgage Association | ||

| ADDITIONAL INVESTMENT INFORMATION |

FUTURES CONTRACTS — At June 30, 2013, the Fund had the following futures contracts:

| ||||||||||||||

| Type | Number of Contracts Long (Short) | Expiration Date | Current Value | Unrealized Gain (Loss) | ||||||||||

| EURO STOXX 50 Index | 47 | September 2013 | $ | 1,589,393 | $ | (53,076 | ) | |||||||

| Euro-Bund | 53 | September 2013 | 9,763,104 | (112,234 | ) | |||||||||

| FTSE 100 Index | 29 | September 2013 | 2,717,687 | (50,452 | ) | |||||||||

| Russell 2000 Mini Index | 14 | September 2013 | 1,364,580 | 12,120 | ||||||||||

TSE TOPIX Index | 106 | September 2013 | 12,087,719 | 191,613 | ||||||||||

| TOTAL | $ | (12,029 | ) | |||||||||||

| 8 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Statement of Assets and Liabilities

June 30, 2013 (Unaudited)

| Assets: | ||||

Investments of unaffiliated issuers, at value (cost $28,615,500) | $ | 28,966,060 | ||

Investments of affiliated issuer, at value (cost $5,372,192) | 5,372,192 | |||

Cash | 15,725,356 | |||

Receivables: | ||||

Investments sold | 2,924,705 | |||

Fund shares sold | 1,264,174 | |||

Collateral on certain derivative contracts(a) | 1,077,516 | |||

Futures variation margin | 223,908 | |||

Reimbursement from investment adviser | 16,595 | |||

Dividends and interest | 2,145 | |||

Other assets | 702 | |||

| Total assets | 55,573,353 | |||

| Liabilities: | ||||

Payables: | ||||

Investments purchased | 121,048 | |||

Amounts owed to affiliates | 40,249 | |||

Fund shares redeemed | 27,483 | |||

Accrued expenses | 59,855 | |||

| Total liabilities | 248,635 | |||

| Net Assets: | ||||

Paid-in capital | 52,491,158 | |||

Undistributed net investment loss | (22,055 | ) | ||

Accumulated net realized gain | 2,513,156 | |||

Net unrealized gain | 342,459 | |||

| NET ASSETS | $ | 55,324,718 | ||

Total Service Shares of beneficial interest outstanding $0.001 par value (unlimited shares authorized): | 5,018,547 | |||

Net asset value, offering and redemption price per share: | $11.02 | |||

(a) Represents cash on deposit with counterparty relating to initial margin requirements on future transactions of $1,077,516.

| The accompanying notes are an integral part of these financial statements. | 9 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Statement of Operations

For the Six Months Ended June 30, 2013 (Unaudited)

| Investment income: | ||||

Dividends — unaffiliated issuers | $ | 102,685 | ||

Interest | 19,612 | |||

Dividends — affiliated issuer | 285 | |||

| Total investment income | 122,582 | |||

| Expenses: | ||||

Management fees | 156,686 | |||

Amortization of offering costs | 65,817 | |||

Distribution and Service fees — Service Class | 49,584 | |||

Professional fees | 38,344 | |||

Custody, accounting and administrative services | 29,076 | |||

Printing and mailing costs | 27,715 | |||

Trustee fees | 8,787 | |||

Transfer Agent fees | 3,966 | |||

Other | 4,763 | |||

| Total expenses | 384,738 | |||

Less — expense reductions | (182,946 | ) | ||

| Net expenses | 201,792 | |||

| NET INVESTMENT LOSS | (79,210 | ) | ||

| Realized and unrealized gain (loss): | ||||

Net realized gain (loss) from: | ||||

Investments | (146,845 | ) | ||

Futures contracts | 2,364,084 | |||

Foreign currency transactions | �� | (65,358 | ) | |

Net change in unrealized gain (loss) on: | ||||

Investments | 149,419 | |||

Futures contracts | (161,664 | ) | ||

Foreign currency translation | 9,432 | |||

| Net realized and unrealized gain | 2,149,068 | |||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 2,069,858 | ||

| 10 | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Statements of Changes in Net Assets

| For the Six Months Ended June 30, 2013 (Unaudited) | For the Period Ended December 31, 2012(a) | |||||||

| From operations: | ||||||||

Net investment income (loss) | $ | (79,210 | ) | $ | 20,384 | |||

Net realized gain | 2,151,881 | 430,993 | ||||||

Net change in unrealized gain (loss) | (2,813 | ) | 345,272 | |||||

| Net increase in net assets resulting from operations | 2,069,858 | 796,649 | ||||||

| Distributions to shareholders: | ||||||||

| From net realized gains | — | (33,093 | ) | |||||

| From share transactions: | ||||||||

Proceeds from sales of shares | 31,011,557 | 29,921,805 | ||||||

Reinvestment of distributions | — | 33,093 | ||||||

Cost of shares redeemed | (3,746,273 | ) | (4,728,878 | ) | ||||

| Net increase in net assets resulting from share transactions | 27,265,284 | 25,226,020 | ||||||

| TOTAL INCREASE | 29,335,142 | 25,989,576 | ||||||

| Net assets: | ||||||||

Beginning of period | 25,989,576 | — | ||||||

End of period | $ | 55,324,718 | $ | 25,989,576 | ||||

| Undistributed net investment income (loss) | $ | (22,055 | ) | $ | 57,155 | |||

| Summary of share transactions: | ||||||||

Shares sold | 2,848,414 | 2,978,079 | ||||||

Shares issued on reinvestment of distributions | — | 3,229 | ||||||

Shares redeemed | (339,529 | ) | (471,646 | ) | ||||

| NET INCREASE | 2,508,885 | 2,509,662 | ||||||

(a) Commenced operations on April 16, 2012.

| The accompanying notes are an integral part of these financial statements. | 11 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Financial Highlights

Selected Data for a Share Outstanding Throughout Each Period

| Income (loss) from investment operations | ||||||||||||||||||||||||||||||||||||||||||||||||

| Year | Net asset value, beginning of period | Net investment income (loss)(a) | Net realized and unrealized gain | Total from investment operations | Distributions from net realized gains | Net asset value, end of period | Total return(b) | Net assets, end of period (in 000s) | Ratio of net expenses to average net assets(c) | Ratio of total expenses to average net assets(c) | Ratio of net investment income (loss) to average net assets | Portfolio turnover rate(d) | ||||||||||||||||||||||||||||||||||||

FOR THE SIX MONTHS ENDED JUNE 30, (UNAUDITED) | ||||||||||||||||||||||||||||||||||||||||||||||||

2013 | $ | 10.36 | $ | (0.02 | ) | $ | 0.68 | $ | 0.66 | $ | — | $ | 11.02 | 6.37 | % | $ | 55,325 | 1.77 | %(e) | 1.94 | %(e) | (0.40 | )%(e) | 177 | % | |||||||||||||||||||||||

FOR THE PERIOD ENDED DECEMBER 31, | ||||||||||||||||||||||||||||||||||||||||||||||||

2012 (Commenced April 16, 2012) | 10.00 | 0.02 | 0.35 | 0.37 | (0.01 | ) | 10.36 | 3.74 | 25,990 | 1.04 | (e) | 4.21 | (e) | 0.27 | (e) | 300 | ||||||||||||||||||||||||||||||||

| (a) | Calculated based on the average shares outstanding methodology. |

| (b) | Assumes investment at the net asset value at the beginning of the period, reinvestment of all distributions, and a complete redemption of the investment at the net asset value at the end of the period. Total returns for periods less than one full year are not annualized. |

| (c) | Expense ratios exclude expenses of the Underlying Funds in which the Fund invests. |

| (d) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| (e) | Annualized. |

| The accompanying notes are an integral part of these financial statements. | 12 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Notes to Financial Statements

June 30, 2013 (Unaudited)

1. ORGANIZATION

Goldman Sachs Variable Insurance Trust (the “Trust” or “VIT”) is a Delaware statutory trust registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company. The Trust includes the Goldman Sachs Global Markets Navigator Fund (the “Fund”). The Fund is a non-diversified portfolio under the Act offering one class of shares — Service Shares. Shares of the Trust are offered to separate accounts of participating life insurance companies for the purpose of funding variable annuity contracts and variable life insurance policies.

Goldman Sachs Asset Management, L.P. (“GSAM”), an affiliate of Goldman, Sachs & Co. (“Goldman Sachs”), serves as investment adviser to the Fund pursuant to a management agreement (the “Agreement”) with the Trust.

2. SIGNIFICANT ACCOUNTING POLICIES

The financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) and require management to make estimates and assumptions that may affect the reported amounts and disclosures. Actual results may differ from those estimates and assumptions.

A. Investment Valuation — The Fund’s valuation policy is to value investments at fair value.

B. Investment Income and Investments — Investment income includes interest income and dividend income, net of any foreign withholding taxes, less any amounts reclaimable. Interest income is accrued daily and adjusted for amortization of premiums and accretion of discounts. Dividend income is recognized on ex-dividend date or, for certain foreign securities, as soon as such information is obtained subsequent to the ex-dividend date. Investment transactions are reflected on trade date. Realized gains and losses are calculated using identified cost. Investment transactions are recorded on the following business day for daily net asset value (“NAV”) calculations. Any foreign capital gains tax is accrued daily based upon net unrealized gains, and is payable upon sale of such investments.

For derivative contracts, realized gains and losses are recorded upon settlement of the contract.

C. Expenses — Expenses incurred directly by the Fund are charged to the Fund, and certain expenses incurred by the Trust that may not solely relate to the Fund are allocated to the Fund and the other funds of the Trust on a straight-line and/or pro-rata basis depending upon the nature of the expenses and are accrued daily.

D. Offering Costs — Offering costs paid in connection with the offering of shares of the Fund have been amortized on a straight-line basis over 12 months from the date of commencement of operations.

E. Federal Taxes and Distributions to Shareholders — It is the Fund’s policy to comply with the requirements of the Internal Revenue Code of 1986, as amended (the “Code”), applicable to regulated investment companies (mutual funds) and to distribute each year substantially all of its investment company taxable income and capital gains to its shareholders. Accordingly, the Fund is not required to make any provisions for the payment of federal income tax. Distributions to shareholders are recorded on the ex-dividend date. Income and capital gains distributions, if any, are declared and paid annually.

Net capital losses are carried forward to future fiscal years and may be used to the extent allowed by the Code to offset any future capital gains. Losses that are carried forward will retain their character as either short-term or long-term capital losses. Utilization of capital loss carryforwards will reduce the requirement of future capital gains distributions.

13

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Notes to Financial Statements (continued)

June 30, 2013 (Unaudited)

2. SIGNIFICANT ACCOUNTING POLICIES (continued)

The characterization of distributions to shareholders for financial reporting purposes is determined in accordance with federal income tax rules, which may differ from GAAP. The source of the Fund’s distributions may be shown in the accompanying financial statements as either from net investment income, net realized gain or capital. Certain components of the Fund’s net assets on the Statement of Assets and Liabilities reflect permanent GAAP/tax differences based on the appropriate tax character.

F. Foreign Currency Translation — The accounting records and reporting currency of the Fund are maintained in United States (“U.S.”) dollars. Assets and liabilities denominated in foreign currencies are translated into U.S. dollars using the current exchange rates at the close of each business day. The effect of changes in foreign currency exchange rates on investments is included within net realized and unrealized gain (loss) on investments. Changes in the value of other assets and liabilities as a result of fluctuations in foreign exchange rates are included in the Statement of Operations within net change in unrealized gain (loss) on foreign currency transactions. Transactions denominated in foreign currencies are translated into U.S. dollars on the date the transaction occurred, the effects of which are included within net realized gain (loss) on foreign currency transactions.

3. INVESTMENTS AND FAIR VALUE MEASUREMENTS

The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The levels used for classifying investments are not necessarily an indication of the risk associated with investing in these investments. The three levels of the fair value hierarchy are described below:

Level 1 — Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities;

Level 2 — Quoted prices in markets that are not active or financial instruments for which significant inputs are observable (including, but not limited to, quoted prices for similar investments, interest rates, foreign exchange rates, volatility and credit spreads), either directly or indirectly;

Level 3 — Prices or valuations that require significant unobservable inputs (including GSAM’s assumptions in determining fair value measurement).

The Trustees have adopted Valuation Procedures that govern the valuation of the portfolio investments held by the Fund, including investments for which market quotations are not readily available. The Trustees have delegated to GSAM day-to-day responsibility for implementing and maintaining internal controls and procedures related to the valuation of the Fund’s portfolio investments. To assess the continuing appropriateness of pricing sources and methodologies, GSAM regularly performs price verification procedures and issues challenges as necessary to third party pricing vendors or brokers, and any differences are reviewed in accordance with the Valuation Procedures.

14

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

3. INVESTMENTS AND FAIR VALUE MEASUREMENTS (continued)

A. Level 1 and Level 2 Fair Value Investments — The valuation techniques and significant inputs used in determining the fair values for investments classified as Level 1 and Level 2 are as follows:

Equity Securities — Equity securities and investment companies traded on a U.S. securities exchange or the NASDAQ system, or those located on certain foreign exchanges, including but not limited to the Americas, are valued daily at their last sale price or official closing price on the principal exchange or system on which they are traded. If no sale occurs, equity securities and exchange traded investment companies are valued at the last bid price for long positions and at the last ask price for short positions. Investments in investment companies (other than those that are exchange traded) are valued at the NAV on the valuation date. To the extent these investments are actively traded, they are classified as Level 1 of the fair value hierarchy.

Unlisted equity securities for which market quotations are available are valued at the last sale price on the valuation date, or if no sale occurs, at the last bid price. Securities traded on certain foreign securities exchanges are valued daily at fair value determined by an independent fair value service (if available) under Valuation Procedures approved by the Trustees and consistent with applicable regulatory guidance. The independent fair value service takes into account multiple factors including, but not limited to, movements in the securities markets, certain depositary receipts, futures contracts and foreign currency exchange rates that have occurred subsequent to the close of the foreign securities exchange. These investments are generally classified as Level 2 of the fair value hierarchy.

Debt Securities — Debt securities for which market quotations are readily available are valued daily on the basis of quotations supplied by dealers or an independent pricing service approved by the Trustees. The pricing services may use valuation models or matrix pricing, which consider: (i) yield or price with respect to bonds that are considered comparable in characteristics such as rating, interest rate and maturity date or (ii) quotations from securities dealers to determine current value. Short-term debt obligations that mature in sixty days or less and that do not exhibit signs of credit deterioration are valued at amortized cost, which approximates fair value. With the exception of treasury securities, which are generally classified as Level 1, these investments are generally classified as Level 2 of the fair value hierarchy.

Derivative Contracts — A derivative is an instrument whose value is derived from underlying assets, indices, reference rates or a combination of these factors.

Exchange-traded derivatives, including futures contracts, typically fall within Level 1 of the fair value hierarchy. Over-the-counter (“OTC”) derivatives are valued using market transactions and other market evidence, including market-based inputs to models, calibration to market-clearing transactions, broker or dealer quotations, or other alternative pricing sources. Where models are used, the selection of a particular model to value an OTC derivative depends upon the contractual terms of, and specific risks inherent in, the instrument, as well as the availability of pricing information in the market. Valuation models require a variety of inputs, including contractual terms, market prices, yield curves, credit curves, measures of volatility, voluntary and involuntary prepayment rates, loss severity rates and correlations of such inputs. For OTC derivatives that trade in liquid markets, model inputs can generally be verified and model selection does not involve significant management judgment. OTC derivatives are classified within Level 2 of the fair value hierarchy when significant inputs are corroborated by market evidence.

i. Futures Contracts — Futures contracts are contracts to buy or sell a standardized quantity of a specified commodity or security and are valued based on exchanged settlement prices or independent market quotes. Futures contracts are valued at the last settlement price, or in the absence of a sale, the last bid price for long positions and at the last ask price for short positions, at the end of each day on the board of trade or exchange upon which they are traded. Upon entering into a futures contract, a Fund deposits cash or securities in an account on behalf of the broker in an amount sufficient to meet the initial margin requirement. Subsequent payments are made or received by the Fund equal to the daily change in the contract value and are recorded as variation margin receivable or payable with a corresponding offset to unrealized gains or losses.

15

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Notes to Financial Statements (continued)

June 30, 2013 (Unaudited)

3. INVESTMENTS AND FAIR VALUE MEASUREMENTS (continued)

B. Level 3 Fair Value Investments — To the extent that the aforementioned significant inputs are unobservable, or if quotations are not readily available, or if GSAM believes that such quotations do not accurately reflect fair value, the fair value of the Fund’s investments may be determined under Valuation Procedures approved by the Trustees. GSAM, consistent with its procedures and applicable regulatory guidance, may make an adjustment to the most recent valuation prices of either domestic or foreign securities in light of significant events to reflect what it believes to be the fair value of the securities at the time of determining a Fund’s NAV. Significant events which could affect a large number of securities in a particular market may include, but are not limited to: significant fluctuations in U.S. or foreign markets; market dislocations; market disruptions; or unscheduled market closings. Significant events which could also affect a single issuer may include, but are not limited to: corporate actions such as reorganizations, mergers and buy-outs; ratings downgrades; and bankruptcies.

C. Fair Value Hierarchy — The following is a summary of the Fund’s investments and derivatives classified in the fair value hierarchy as of June 30, 2013:

| Investment Type | Level 1 | Level 2 | Level 3 | |||||||||

| Assets | ||||||||||||

| Fixed Income | ||||||||||||

Agency Debentures | $ | — | $ | 9,447,159 | $ | — | ||||||

U.S. Treasury Obligations and/or Other U.S. Government Agencies | 6,602,409 | — | — | |||||||||

Exchange Traded Fund | 12,916,492 | — | — | |||||||||

Investment Company | 5,372,192 | — | — | |||||||||

| Total | $ | 24,891,093 | $ | 9,447,159 | $ | — | ||||||

| Derivative Type | ||||||||||||

| Assets(a) | ||||||||||||

| Futures Contracts | $ | 203,733 | $ | — | $ | — | ||||||

| Liabilities(a) | ||||||||||||

| Futures Contracts | $ | (215,762 | ) | $ | — | $ | — | |||||

| (a) | Amount shown represents unrealized gain (loss) at period end. |

For further information regarding security characteristics, see the Schedule of Investments.

16

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

4. INVESTMENTS IN DERIVATIVES

The following table sets forth, by certain risk types, the gross value of derivative contracts as of June 30, 2013. These instruments were used to meet the Fund’s investment objectives and to obtain and/or manage exposure related to the risks below. The values in the table below exclude the effects of cash collateral received or posted pursuant to these derivative contracts, and therefore are not representative of the Fund’s net exposure.

| Risk | Statement of Assets and Liabilities | Assets(a) | Statement of Assets and Liabilities | Liabilities(a) | ||||||||

| Equity | Receivable for unrealized gain on futures variation margin | $ | 203,733 | Payable for unrealized loss on futures variation margin | $ | (103,528 | ) | |||||

| Interest Rate | — | — | Payable for unrealized loss on futures variation margin | (112,234 | ) | |||||||

| Total | $ | 203,733 | $ | (215,762 | ) | |||||||

| (a) | Includes unrealized gain (loss) on futures contracts described in the Additional Investment Information section of the Schedule of Investments. Only current day’s variation margin is reported within the Statement of Assets and Liabilities. |

The following table sets forth, by certain risk types, the Fund’s gains (losses) related to these derivatives and their indicative volumes for the six months ended June 30, 2013. These gains (losses) should be considered in the context that these derivative contracts may have been executed to economically hedge certain investments, and accordingly, certain gains (losses) on such derivative contracts may offset certain (losses) gains attributable to investments. These gains (losses) are included in “Net realized gain (loss)” or “Net change in unrealized gain (loss)” on the Statement of Operations:

| Risk | Statement of Operations | Net Realized Gain (Loss) | Net Change in Unrealized Gain (Loss) | Average Number of Contracts(a) | ||||||||||

| Equity | Net realized gain (loss) from futures contracts/Net change in unrealized gain (loss) on futures contracts | $ | 2,417,261 | $ | (38,542 | ) | 248 | |||||||

| Interest Rate | Net realized gain (loss) from futures contracts/Net change in unrealized gain (loss) on futures contracts | (53,177 | ) | (123,122 | ) | 41 | ||||||||

| (a) | Average number of contracts is based on the average of month end balances for the period ended June 30, 2013. |

In December 2011, the Financial Accounting Standards Board (“FASB”) issued an Accounting Standards Update (“ASU”) No. 2011-11: Disclosures about Offsetting Assets and Liabilities (“netting”) on the Statement of Assets and Liabilities that are subject to master netting arrangements or similar agreements. ASU 2011-11 was amended by ASU No. 2013-01, clarifying which investments and transactions are subject to the netting disclosure. The scope of the disclosure requirements is limited to derivative instruments, repurchase agreements and reverse repurchase agreements, and securities borrowing and securities lending transactions. This information is intended to enable users of the Fund’s financial statements to evaluate the effect or potential effect of netting arrangements on the Fund’s financial position. The ASU is effective for financial statements with fiscal years beginning on or after January 1, 2013, and interim periods within those fiscal years. The Fund adopted the disclosure requirement on netting for the current reporting period. Since these amended principles require additional disclosures concerning offsetting and related arrangements, adoption did not affect the Fund’s financial condition or result of operations.

17

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Notes to Financial Statements (continued)

June 30, 2013 (Unaudited)

4. INVESTMENTS IN DERIVATIVES (continued)

For financial reporting purposes, the Fund does not offset financial assets and financial liabilities that are subject to master netting arrangements or similar agreements on the Statement of Assets and Liabilities.

In order to better define its contractual rights and to secure rights that will help a Fund mitigate its counterparty risk, a Fund may enter into an International Swaps and Derivatives Association, Inc. Master Agreement (“ISDA Master Agreement”) or similar agreement with its derivatives counterparties. An ISDA Master Agreement is a bilateral agreement between a Fund and a counterparty that governs OTC derivatives, including foreign exchange contracts, and typically contains, among other things, collateral posting terms and netting provisions in the event of a default and/or termination event. The provisions of the ISDA Master Agreement typically permit a single net payment in the event of a default (close-out netting) or similar event, including the bankruptcy or insolvency of the counterparty.

Collateral and margin requirements differ between exchange traded derivatives and OTC derivatives. Margin requirements are established by the broker or clearing house for exchange-traded and centrally cleared derivatives (financial futures contracts, options and centrally cleared swaps) pursuant to governing agreements for those instrument types. Brokers can ask for margin in excess of the minimum in certain circumstances. Collateral terms are contract-specific for OTC derivatives (foreign currency exchange contracts, options and certain swaps). For derivatives traded under an ISDA Master Agreement, the collateral requirements are typically calculated by netting the mark to market amount for each transaction under such agreement and comparing that amount to the value of any collateral currently pledged by a Fund and the counterparty. Additionally, a Fund may be required to post additional collateral to the counterparty in the form of initial margin, the terms of which would be outlined in the confirmation of the OTC transaction.

For financial reporting purposes, cash collateral that has been pledged to cover obligations of a Fund and cash collateral received from the counterparty, if any, is reported separately on the Statement of Assets and Liabilities as receivables/payables for collateral on certain derivative contracts. Non-cash collateral pledged by a Fund, if any, is noted in the Schedule of Investments. Generally, the amount of collateral due from or to a counterparty must exceed a minimum transfer amount threshold (e.g., $250,000) before a transfer is required to be made. To the extent amounts due to a Fund from its counterparties are not fully collateralized, contractually or otherwise, the Fund bears the risk of loss from counterparty nonperformance. A Fund attempts to mitigate counterparty risk by only entering into agreements with counterparties that it believes to be of good standing and by monitoring the financial stability of those counterparties.

Additionally, the netting of assets and liabilities and the offsetting of collateral pledged or received are based on contractual netting/set-off provisions in the ISDA Master Agreement or similar agreements, however, in the event of a default or insolvency of a counterparty, a court could determine that such rights are not enforceable due the restrictions or prohibitions against the right of setoff that may be imposed due to a particular jurisdiction’s bankruptcy or insolvency laws.

18

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

4. INVESTMENTS IN DERIVATIVES (continued)

The following table sets forth the Fund’s net exposure for derivative instruments that are subject to enforceable master netting arrangements or similar agreements as of June 30, 2013:

| Offsetting of Derivatives Assets: | Gross Amounts Available for Offset But Not Netted in the Statement of Assets and Liabilities | |||||||||||||||||||||||

| Derivatives | Gross Amounts of Recognized Assets | Gross Amounts offset in the Statement of Assets and Liabilities | Net Amounts of Assets Presented in the Statement of Assets and Liabilities | Financial Instruments | Cash Collateral Received | Net Amount(1) | ||||||||||||||||||

| Futures Contracts* | $ | 223,908 | $ | — | $ | 223,908 | $ | — | $ | — | $ | 223,908 | ||||||||||||

| * | Exchange Traded Futures — Credit Suisse Securities LLC as Futures Commission Merchant |

| (1) | Net amount represents the net amount due from the counterparty in the event of a default based on the contractual set-off rights under the agreement. |

5. AGREEMENTS AND AFFILIATED TRANSACTIONS

A. Management Agreement — Under the Agreement, GSAM manages the Fund, subject to the general supervision of the Trustees.

As compensation for the services rendered pursuant to the Agreement, the assumption of the expenses related thereto and administration of the Fund’s business affairs, including providing facilities, GSAM is entitled to a management fee, accrued daily and paid monthly, equal to an annual percentage rate of the Fund’s average daily net assets.

For the six months ended June 30, 2013, contractual and effective net management fees with GSAM were at the following rates:

| Contractual Management Fee Rate | ||||||||||||||||||||||||||

| First $1 billion | Next $1 billion | Next $3 billion | Next $3 billion | Over $8 billion | Effective Rate | Effective Net Management Fee Rate | ||||||||||||||||||||

| 0.79% | 0.71 | % | 0.68 | % | 0.66 | % | 0.65 | % | 0.79 | % | 0.77 | %* | ||||||||||||||

| * | GSAM has agreed to waive a portion of its management fee payable by the Fund in an amount equal to any management fees it earns as an investment adviser to any of the affiliated funds in which the Fund invests through at least April 30, 2014. Prior to such date GSAM may not terminate the arrangement without the approval of the Trustees. |

B. Distribution and Service Plan — The Trust, on behalf of the Service Shares of the Fund, has adopted a Distribution and Service Plan (the “Plan”). Under the Plan, Goldman Sachs, which serves as distributor (the “Distributor”), is entitled to a fee accrued daily and paid monthly for distribution services and personal and account maintenance services, which may then be paid by Goldman Sachs to authorized dealers, equal to, on an annual basis, 0.25% of the Fund’s average daily net assets.

C. Transfer Agency Agreement — Goldman Sachs also serves as the transfer agent of the Fund for a fee pursuant to Transfer Agency Agreement. The fees charged for such transfer agency services are accrued daily and paid monthly at an annual rate of 0.02% of the average daily net assets of the Fund.

19

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Notes to Financial Statements (continued)

June 30, 2013 (Unaudited)

5. AGREEMENTS AND AFFILIATED TRANSACTIONS (continued)

D. Line of Credit Facility — As of June 30, 2013, the Fund participated in a $780,000,000 committed, unsecured revolving line of credit facility (the “facility”) together with other funds of the Trust and registered investment companies having management agreements with GSAM or its affiliates (“Other Borrowers”). Pursuant to the terms of the facility, the Fund and Other Borrowers could increase the credit amount by an additional $220,000,000, for a total of up to $1,000,000,000. This facility is to be used solely for temporary or emergency purposes, which may include the funding of redemptions. The interest rate on borrowings is based on the federal funds rate. The facility also requires a fee to be paid by the Fund based on the amount of the commitment that has not been utilized. For the six months ended June 30, 2013, the Fund did not have any borrowings under the facility. Prior to May 8, 2013, the committed amount available through the facility was $630,000,000.

E. Other Expense Agreements and Affiliated Transactions — GSAM has agreed to limit certain “Other Expense” of the Fund (excluding transfer agent fees and expenses, taxes, interest, brokerage fees, litigation, indemnification, shareholder meeting and other extraordinary expenses) to the extent such expenses exceed, on an annual basis, a percentage rate of the average daily net assets of the Fund. Such Other Expense reimbursements, if any, are accrued daily and paid monthly. In addition, the Fund is not obligated to reimburse GSAM for prior fiscal year expense reimbursements, if any. The Other Expense limitation as an annual percentage rate of average daily net assets for the Fund is 0.004%. This Other Expense limitation will remain in place through at least April 30, 2014, and prior to such date GSAM may not terminate the arrangement without the approval of the Trustees. For the six months ended June 30, 2013, GSAM reimbursed $173,706 to the Fund. In addition, the Fund has entered into certain offset arrangements with the custodian and the transfer agent, which may result in a reduction of the Fund’s expenses and are received irrespective of the application of the “Other Expense” limitation described above. For the six months ended June 30, 2013, custody fee credits were $5,069.

As of June 30, 2013, the amounts owed to affiliates of the Fund were $28,935, $10,476, and $838 for management, distribution and service, and transfer agent fees, respectively.

F. Other Transactions with Affiliates — The following table provides information about the investment in shares of a fund of which the Fund is an affiliate for the period ended June 30, 2013:

| Name of Affiliated Fund | Number of Shares Held Beginning of Period | Shares Bought | Shares Sold | Number of Shares Held End of Period | Value at End of Period | Dividend Income | ||||||||||||||||||

| Goldman Sachs Financial Square Government Fund | 2,562,496 | 3,380,892 | (571,196 | ) | 5,372,192 | $ | 5,372,192 | $ | 285 | |||||||||||||||

20

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

6. PORTFOLIO SECURITIES TRANSACTIONS

The cost of purchases and proceeds from sales and maturities of long-term securities for the six months ended June 30, 2013, were as follows:

Purchases of U.S. Government | Purchases (Excluding U.S. Government and Agency Obligations | Sales and Maturities of | Sales and Maturities (Excluding | |||||||||||

| $2,972,361 | $ | 17,168,145 | $ | 11,936,898 | $ | 8,859,514 | ||||||||

7. TAX INFORMATION

As of June 30, 2013, the Fund’s aggregate security unrealized gains and losses based on cost for U.S. federal income tax purposes were as follows:

| Tax cost | $ | 34,001,779 | ||

| Gross unrealized gain | 381,015 | |||

| Gross unrealized loss | (44,542 | ) | ||

| Net unrealized security gain | $ | 336,473 |

The difference between GAAP-basis and tax-basis unrealized gains (losses) is attributable primarily to wash sales and net mark to market gains (losses) on regulated futures contracts.

GSAM has reviewed the Fund’s tax positions for all open tax years (the current and prior three years, as applicable) and has concluded that no provision for income tax is required in the Fund’s financial statements. Such open tax years remain subject to examination and adjustment by tax authorities.

8. OTHER RISKS

The Fund’s risks include, but are not limited to, the following:

Foreign Custody Risk — A Fund that invests in foreign securities may hold such securities and foreign currency with foreign banks, agents, and securities depositories appointed by the Fund’s custodian (each a “Foreign Custodian”). In some countries, Foreign Custodians may be subject to little or no regulatory oversight or independent evaluation of their operations. Further, the laws of certain countries may place limitations on a Fund’s ability to recover its assets if a Foreign Custodian enters into bankruptcy. Investments in emerging markets may be subject to greater custody risks than investments in more developed markets. Custody services in emerging market countries are often undeveloped and may be less regulated than in more developed countries, and thus may not afford the same level of investor protection as would apply in developed countries.

Shareholder Concentration Risk — Certain funds, accounts, individuals, or Goldman Sachs affiliates may from time to time own (beneficially or of record) or control a significant percentage of the Fund’s shares. Redemptions by these entities of their holdings in the Fund may impact the Fund’s liquidity and NAV. These redemptions may also force the Fund to sell securities.

| The accompanying notes are an integral part of these financial statements. | 21 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Notes to Financial Statements (continued)

June 30, 2013 (Unaudited)

8. OTHER RISKS (continued)

Investments in Other Investment Companies — As a shareholder of another investment company, including an exchange traded fund (“ETF”), a Fund will directly bear its proportionate share of any management fees and other expenses paid by such other investment companies, in addition to the fees and expenses regularly borne by the Fund. ETFs are subject to risks that do not apply to conventional mutual funds, including but not limited to the following: (i) the market price of the ETF’s shares may trade at a premium or a discount to their NAV; and (ii) an active trading market for an ETF’s shares may not develop or be maintained.

Liquidity Risk — The Fund may make investments that are illiquid or that may become less liquid in response to market developments or adverse investor perceptions. Illiquid investments may be more difficult to value. Liquidity risk may also refer to the risk that a Fund will not be able to pay redemption proceeds within the allowable time period because of unusual market conditions, an unusually high volume of redemption requests, or other reasons. To meet redemption requests, the Fund may be forced to sell investments at an unfavorable time and/or under unfavorable conditions.

Market and Credit Risks — In the normal course of business, the Fund trades financial instruments and enters into financial transactions where risk of potential loss exists due to changes in the market (market risk). Additionally, the Fund may also be exposed to credit risk in the event that an issuer fails to perform or that an institution or entity with which the Fund has unsettled or open transactions defaults.

Investing in foreign markets may involve special risks and considerations not typically associated with investing in the U.S. These risks include revaluation of currencies, high rates of inflation, repatriation restrictions on income and capital, and adverse political and economic developments. Moreover, securities issued in these markets may be less liquid, be subject to government ownership controls, have delayed settlements and their prices may be more volatile than those of comparable securities in the U.S.

Non-Diversification Risk — The Fund is non-diversified, meaning that is permitted to invest a larger percentage of its assets in fewer issuers than diversified mutual funds. Thus, the Fund may be more susceptible to adverse developments affecting any single issuer held in its portfolio, and may be more susceptible to greater losses because of these developments.

Industry Concentration Risk — The Fund will not invest more than 25% of the value of its total assets in the securities of one or more issuers conducting their principal business activities in the same industry, except that, to the extent that an industry represents 20% or more of the Fund’s index at the time of investment, the Fund may invest up to 35% of its assets in that industry. Concentrating Fund investments in issuers conducting business in the same industry will subject the Fund to a greater risk of loss as a result of adverse economic, business or other developments affecting that industry than if its investments were not so concentrated.

22

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

9. INDEMNIFICATIONS

Under the Trust’s organizational documents, its Trustees, officers, employees and agents are indemnified, to the extent permitted by the Act and state law, against certain liabilities that may arise out of performance of their duties to the Fund. Additionally, in the course of business, the Fund enters into contracts that contain a variety of indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, GSAM believes the risk of loss under these arrangements to be remote.

10. OTHER MATTERS

Other — On February 8, 2012, the Commodity Futures Trading Commission (CFTC) adopted amendments to several of its rules relating to commodity pool operators, including Rule 4.5. The Fund currently relies on Rule 4.5’s exclusion from CFTC regulation for regulated investment companies. GSAM is currently evaluating the amendments and their impact, if any, on the Fund’s financial statements.

11. SUBSEQUENT EVENTS

Subsequent events after the Statement of Assets and Liabilities date have been evaluated through the date the financial statements were issued. GSAM has concluded that there is no impact requiring adjustment or disclosure in the financial statements.

23

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

| Fund Expenses — Period Ended June 30, 2013 (Unaudited) |

As a shareholder of the Service Shares of the Fund, you incur ongoing costs, including management fees, distribution and service (12b-1) fees and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2013 through June 30, 2013.

Actual Expenses — The first line in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000=8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes — The second line in the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual net expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only. As a shareholder of the Fund, you do not incur any transaction costs, such as sales charges, redemption fees, or exchange fees, but shareholders of other funds may incur such costs. The second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds whose shareholders may incur transaction costs.

| Beginning Account Value 1/01/13 | Ending Account Value 6/30/13 | Expenses Paid for the 6 Months Ended 6/30/13* | ||||||||||

| Actual | $ | 1,000 | $ | 1,063.70 | $ | 5.22 | ||||||

| Hypothetical 5% return | 1,000 | 1,019.74 | + | 5.11 | ||||||||

| * | Expenses are calculated using the Fund’s annualized net expense ratio, which represents the ongoing expenses as a percentage of net assets for the six months ended June 30, 2013. Expenses are calculated by multiplying the annualized net expense ratio by the average account value for the period; then multiplying the result by the number of days in the most recent fiscal half year; and then dividing that result by the number of days in the fiscal year. The annualized net expense ratio for the period was 1.02%. |

| + | Hypothetical expenses are based on the Fund’s actual annualized net expense ratio and an assumed rate of return of 5% per year before expenses. |

24

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Statement Regarding Basis for Approval of Management Agreement (Unaudited)

Background

The Goldman Sachs Global Markets Navigator Fund (the “Fund”) is an investment portfolio of Goldman Sachs Variable Insurance Trust (the “Trust”). The Board of Trustees oversees the management of the Trust and reviews the investment performance and expenses of the Fund at regularly scheduled meetings held during the year. In addition, the Board of Trustees determines annually whether to approve the continuance of the Trust’s investment management agreement (the “Management Agreement”) with Goldman Sachs Asset Management, L.P. (the “Investment Adviser”) on behalf of the Fund.

The Management Agreement was most recently approved for continuation until June 30, 2014 by the Board of Trustees, including those Trustees who are not parties to the Management Agreement or “interested persons” (as defined in the Investment Company Act of 1940, as amended) of any party thereto (the “Independent Trustees”), at a meeting held on June 12-13, 2013 (the “Annual Meeting”).

The review process undertaken by the Trustees spans the course of the year and culminates with the Annual Meeting. To assist the Trustees in their deliberations, the Trustees have established a Contract Review Committee (the “Committee”), comprised of the Independent Trustees. The Committee held four meetings over the course of the year since the Management Agreement was last approved. At those Committee meetings, regularly scheduled Board or other committee meetings and/or the Annual Meeting, the Board, or the Independent Trustees, as applicable, considered matters relating to the Management Agreement, including:

| (a) | the nature and quality of the advisory, administrative and other services provided to the Fund by the Investment Adviser and its affiliates, including information about: |

| (i) | the structure, staff and capabilities of the Investment Adviser and its portfolio management teams; |

| (ii) | the groups within the Investment Adviser and its affiliates that support the portfolio management teams or provide other types of necessary services, including fund services groups (e.g., accounting and financial reporting, tax, shareholder services and operations), controls and risk management groups (e.g., legal, compliance, valuation oversight, credit risk management, internal audit, compliance testing, market risk analysis, finance and strategy and central funding), sales and distribution support groups and others (e.g., information technology and training); |

| (iii) | trends in headcount; |

| (iv) | the Investment Adviser’s financial resources and ability to hire and retain talented personnel and strengthen its operations; and |

| (v) | the parent company’s support of the Investment Adviser and its mutual fund business, as expressed by the firm’s senior management; |

| (b) | information on the investment performance of the Fund, including comparisons to the performance of a group of similar mutual funds, as provided by the Investment Adviser, using the peer group identified by a third party mutual fund data provider engaged as part of the contract review process (the “Outside Data Provider”), and a benchmark performance index, and general investment outlooks in the markets in which the Fund invests; |

| (c) | the terms of the Management Agreement and agreements with affiliated service providers entered into by the Trust on behalf of the Fund; |

| (d) | expense information for the Fund, including the relative management fee and expense levels of the Fund as compared to those of comparable funds managed by other advisers, as provided by the Outside Data Provider; |

| (e) | with respect to the extensive expense comparison data provided by the Outside Data Provider, its processes in producing that data for the Fund; |

| (f) | the undertaking of the Investment Adviser to limit certain expenses of the Fund that exceed a specified level; |

| (g) | information relating to the profitability of the Management Agreement and the transfer agency and distribution and service arrangements of the Fund and the Trust as a whole to the Investment Adviser and its affiliates; |

| (h) | whether the Fund’s existing management fee schedule adequately addressed any economies of scale; |

25

GOLDMAN SACHS VARIABLE INSURANCE TRUST GLOBAL MARKETS NAVIGATOR FUND

Statement Regarding Basis for Approval of Management Agreement (Unaudited) (continued)

| (i) | a summary of the “fall-out” benefits derived by the Investment Adviser and its affiliates from their relationships with the Fund, including the fees received by the Investment Adviser’s affiliates from the Fund for transfer agency, portfolio trading, distribution and other services; |

| (j) | a summary of potential benefits derived by the Fund as a result of its relationship with the Investment Adviser; |

| (k) | information regarding commissions paid by the Fund and broker oversight, other information regarding portfolio trading and how the Investment Adviser carries out its duty to seek best execution; |

| (l) | the manner in which portfolio manager compensation is determined, and the number and types of accounts managed by the portfolio managers; |

| (m) | the nature and quality of the services provided to the Fund by its unaffiliated service providers, and the Investment Adviser’s general oversight and evaluation (including reports on due diligence) of those service providers as part of the administration services provided under the Management Agreement; and |

| (n) | the Investment Adviser’s processes and policies addressing various types of potential conflicts of interest; its approach to risk management; the annual review of the effectiveness of the Fund’s compliance program; and periodic compliance reports. |

The Trustees also received an overview of the Fund’s distribution arrangements. They received information regarding the Fund’s assets, share purchase and redemption activity and the payment of Rule 12b-1 distribution and service fees paid by the Fund’s Service Shares. Information was also provided to the Trustees relating to revenue sharing payments made by and services provided by the Investment Adviser and its affiliates to intermediaries that promote the sale, distribution and/or servicing of Fund shares.