Exhibit 99.(a)(5)(AAA)

January 1 - September 30, 2006 |

Interim Report III/2006 |

| 2006 | l | Adjusted EBIT up 10 percent |

| JAN | l | Spain's Industry Ministry amends CNE conditions |

| FEB | l | Russian natural gas secured for long term |

| MAR | l | Increase in adjusted EBIT continues to be expected for full year 2006 |

| APR | ||

| MAY | ||

| JUN | ||

| JUL | ||

| AUG | ||

| SEP | ||

| OCT | ||

| NOV | ||

| DEC |

| Interim Report III/2006 | ||

| 2 | E.ON Group Financial Highlights |

E.ON Group Key Figures at a Glance | |||||||

| January 1 – September 30 | |||||||

€ in millions | 2006 | 20051 | +/- % |

Power sales (in billion kWh)2 | 259.6 | 298.5 | -1 | ||||

Gas sales (in billion kWh)2 | 695.9 | 642 | +8 | ||||

| Sales | 49,451 | 39,520 | +25 | ||||

Adjusted EBITDA3 | 8,441 | 7,629 | +11 | ||||

Adjusted EBIT4 | 6,064 | 5,504 | +10 | ||||

Income/Loss (-) from continuing operations before income taxes and minority interests | 3,497 | 5,133 | -32 | ||||

| Income/Loss (-) from continuing operations | 2,497 | 3,138 | -20 | ||||

| Income/Loss (-) from discontinued operations, net | 132 | 3,261 | -96 | ||||

| Net income | 2,629 | 6,399 | -59 | ||||

Adjusted net income5 | 3,386 | 2,688 | +26 | ||||

| Investments | 3,891 | 3,039 | +28 | ||||

| Cash provided by operating activities | 4,492 | 4,742 | -5 | ||||

Free cash flow6 | 1,934 | 2,878 | -33 | ||||

Net financial position7 (at September 30 and December 31) | 1,039 | 3,863 | -73 | ||||

| Employees (at September 30 and December 31) | 80,296 | 79,570 | +1 |

Earnings per share (in €) | 3,99 | 9,71 | -59 |

1 | Adjusted for discontinued operations. | ||||||

2 | Unconsolidated figures. | ||||||

3 | Non-GAAP financial measure; see reconciliation to net income on page 9. | ||||||

4 | Non-GAAP financial measure; see reconciliation to net income on page 9 and commentary on pages 38-39. | ||||||

5 | Non-GAAP financial measure; see reconciliation to net income on page 10. | ||||||

6 | Non-GAAP financial measure; see reconciliation to cash provided by operating activities on page 11. | ||||||

7 | Non-GAAP financial measure; see reconciliation on page 12. | ||||||

Non-GAAP financial measures: This report contains certain non-GAAP financial measures. Management believes that the non-GAAP financial measures used by E.ON, when considered in conjunction with (but not in lieu of) other measures that are computed in U.S. GAAP, enhance an understanding of E.ON's results of operations. A number of these non-GAAP financial measures are also commonly used by securities analysts, credit rating agencies, and investors to evaluate and compare the periodic and future operating performance and value of E.ON and other companies with which E.ON competes. Additional information with respect to each of the non-GAAP financial measures used in this report is included together with the reconciliations described below.

E.ON prepares its financial statements in accordance with generally accepted accounting principles in the United States (U.S. GAAP). As noted above, this report contains certain consolidated financial measures (adjusted EBIT, adjusted EBITDA, adjusted net income, net financial position, net interest expense, and free cash flow) that are not calculated in accordance with U.S. GAAP and are therefore considered "non-GAAP financial measures" within the meaning of the U.S. federal securities laws. In accordance with applicable rules and regulations, EON has presented in this report a reconciliation of each non-GAAP financial measure to the most directly comparable U.S. GAAP measure for historical measures and an equivalent U.S. GAAP target for forward-looking measures.The footnotes presented with the relevant historical non-GAAP financial measures indicate the page of this report on which the relevant reconciliation appears.The non-GAAP financial measures used in this report should not be considered in isolation as a measure of E.ON's profitability or liquidity and should be considered in addition to, rather than as a substitute for, net income, cash provided by operating activities, and the other income or cash flow data prepared in accordance with U.S. GAAP presented in this report and the relevant reconciliations.The non-GAAP financial measures used by E.ON may differ from, and not be comparable to, similarly titled measures used by other companies.

| Interim Report III/2006 | ||

| Contents | 3 |

| 4 | Letter to Shareholders | ||

| 5 | E.ON Stock | ||

| 6 | Results of Operations | ||

| - | Energy Price Developments | ||

| - | Regulation of Network Charges in Germany | ||

| - | Sales Volume, Sales, Earnings Performance | ||

| - | Investments | ||

| - | Financial Condition | ||

| - | Employees | ||

| - | Risk Situation | ||

| - | Outlook | ||

| 16 | Market Units | ||

| 16 | - | Central Europe | |

| 18 | - | Pan-European Gas | |

| - | U.K. | ||

| 22 | - | Nordic | |

| 24 | - | U.S. Midwest | |

| 26 | Interim Financial Statements (Unaudited) | ||

| 38 | Business Segment | ||

| 40 | Financial Calendar | ||

| Interim Report III/2006 | ||

| 4 |

The E.ON Group's positive performance continued into the third quarter of 2006. For the first nine months of the year, we increased sales by 25 percent from €39.5 billion to €49.5 billion and adjusted EBIT by 10 percent from €5.5 billion to €6.1 billion. A key contributing factor was the solid earnings performance of our Central Europe and Pan-European Gas market units. Net income (after taxes and minority interests) of €2.6 billion was 59 percent below the exceptionally high prior-year figure. We continue to expect full-year adjusted EBIT to surpass the high prior-year level. As anticipated, we will not repeat the extraordinarily high net income figure posted in 2005.

Our most important strategic initiative is currently our planned acquisition of Endesa, a Spanish energy utility. In late September, we underscored our continued interest by announcing that we were raising our original offer to €35 per share. Our increased offer also meets our stringent investment criteria. Spain's Industry Ministry recently amended several critical aspects of the conditions set by the National Energy Commission (CNE) relating to our proposed acquisition of Endesa. Most importantly, the revised conditions no longer contain any requirement to dispose of any assets. On this basis, we have accepted the Industry Ministry's decision and now expect the Spanish stock-market regulator (CNMV) to proceed with the final approval of our offer. We remain confident that we will bring the transaction to a successful conclusion.

The new regulatory regime for Germany's power and natural gas networks has had far-reaching consequences for the country's energy industry. We have now received rulings from the Federal Network Agency (known by its German abbreviation, BNetzA) for our electricity network operators and for nearly all of our natural gas distribution network operators. On average, our electricity network charges were cut by more than 13 percent and, so far, our gas network charges by 10 to 12 percent compared with the costs we had filed. We will pass these reductions on to our customers and accept the rulings, although the reductions are based on an interpretation of the Network Charges Ordinances that is unfavorable to us. Despite the considerable reductions in our network charges, we will stand by our investment commitments, including our network investments.

In Germany's current energy policy debate, there are calls for additional, in some cases nonsensical regulatory intervention, for example in the power generation business. Instead of more regulation, Germany needs an energy policy that is systematically European in scope and for its energy markets and companies to be even more competition oriented. For this reason, we have launched an initiative to introduce more competition in power and gas markets and have put together a comprehensive package of measures to help achieve this goal. We are also setting standards in energy technology R&D. Our plans include the construction of the world's most modern coal-fired power plant, a pilot clean-coal generating unit, and further development of renewable energy technologies.

To help secure Europe's long-term natural gas supply, in late August we concluded agreements with Gazprom for the supply of a total of approximately 400 billion cubic meters of natural gas through 2036. The annual supply volume of roughly 24 billion cubic meters is equal to one third of E.ON Ruhrgas's current procurement. In an environment of keen global competition for natural gas supplies, these agreements enable us to procure Russian natural gas for the European energy market for the long term at competitive prices. In the wake of our participation in the NEGP project, these contracts represent another important contribution towards strengthening our position on the European gas market for the long term.

In summary, we will continue to push for energy market competition in Germany and Europe, foster advances in energy technology, and work hard to achieve our strategic objectives. In addition, the new structure of our Board of Management, which takes effect on April 1, 2007, will lay the groundwork for your company to be even more market oriented and to achieve further growth.

Sincerely yours,

Dr. Wulf H. Bernotat

Interim Report III/2006

5

E.ON Stock | ||

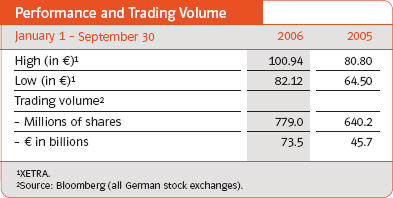

Including the dividend and special dividend, E.ON stock finished the first nine months of 2006 up 14 percent. E.ON stock thus outperformed other European blue chips as measured by the EURO STOXX 50, which advanced by 11 percent over the same period, and performed more weakly than its peer index, the STOXX Utilities, which rose by 27 percent. The trading volume of E.ON stock climbed by more than 60 percent year on year to €73.5 billion, making E.ON the fifth most-traded stock in the DAX index of Germany's top 30 blue chips. As of September 30, 2006, E.ON was the largest DAX stock in terms of market capitalization. E.ON stock is listed on the New York Stock Exchange as American Depositary Receipts (ADRs). Effective March 29, 2005, the conversion ratio between E.ON ADRs and E.ON stock is three to one. The value of three E.ON ADRs is effectively that of one share of E.ON stock. Visit eon.com for the latest information about E.ON stock. |   | |

E.ON Stock Sept.30, Dec. 31, 2006 2005 Shares outstanding (in millions)1 659 659 Closing price (in €) 93.48 87.39 Market capitalization (€ in billions)2 64.7 60.5 1Excludes treasury stock. 2Based on E.ON's entire capital stock (692,000,000 shares). Performance and Trading Volume January 1 - September 30 2006 2005 High (in €)1 100.94 80.80 Low (in €)1 82.12 64.50 Trading volume2 - Millions of shares 779.0 640.2 - € in billions 73.5 45.7 1XETRA. 2Source: Bloomberg (all German stock exchanges). E.ON Stock Performance versus European Stock Indices Percentages E.ON EURO STOXX STOXX Utilities 12/30/05 1/30/06 2/28/06 3/30/06 4/30/06 5/30/06 6/30/06 7/30/06 8/30/06 9/30/06

Interim Report III/2006

6

Results of Operations | ||

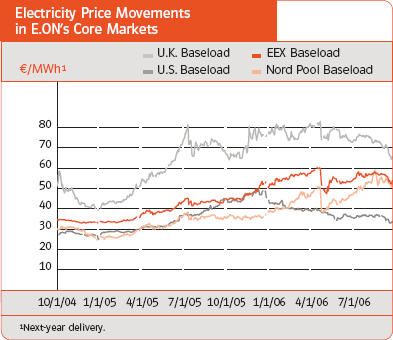

Energy Price Developments Throughout the first nine months of 2006, European power and natural gas markets were mainly governed by international oil, coal, and CO2 prices, the natural gas supply and storage situation in the United Kingdom, and hydrological levels in the Nordic region. After a long period of high and volatile prices, U.K. natural gas prices and, subsequently, power prices started to decrease in mid-August 2006. Compared with historical levels, however, prices remain high. The price of Brent crude oil reached a new high of over $78 per barrel at the beginning of August. It then fell by 20 percent, finishing the third quarter at $62 per barrel, about the same price as at the beginning of 2006. Market analysts cite concerns about U.S. economic growth and reduced tensions in the Near and Middle East as the main reasons for the decline. Coal prices also declined in late August and September 2006, falling as a result of an improved supply situation and less demand in Europe. Prices recovered at the end of the quarter due to new supply concerns in Russia and remained 15 percent above the level at the beginning of the year. The market appears to be well supported by substantial buying interest in coal derivatives and the overall supply situation. Germany's natural gas import prices are contractually indexed to oil prices, which they track with a time lag. Because oil prices have risen continually, the average price of Germany's natural gas imports was 40 percent higher in the first nine months of 2006 compared with the first nine months of 2005. The recent fall in oil prices is not yet reflected in the average price of Germany's natural gas imports due to lags in indexation. Natural gas prices in the United Kingdom have declined since mid-August reflecting more optimistic expectations regarding the commissioning of the new U.K. import infrastructure and decreasing oil prices. In early October, a short-term oversupply sent U.K. prompt gas prices as low as -5 pence per therm. However, as this dramatic price decline was mainly a result of testing new infrastructure, it has not lead to a collapse of U.K. gas contracts for annual forward delivery. At the end of September 2006, natural gas prices in the United Kingdom were about 16 percent lower than at the beginning of the year. CO2 prices have been very volatile throughout 2006. Following increases at the beginning of the year, CO2 prices dropped by 27 percent in a single day on the publication of EU member states' emissions data for 2005. Prices stabilized at about €16 per metric ton during the summer, but fell back to about €13 per metric ton in late September 2006. | Wholesale power prices across Europe are heavily influenced by fuel and CO2 prices. As a result of the drop in CO2 prices in late April 2006, U.K., Nordic, and German power prices decreased significantly. Since then, German wholesale power prices have been mainly driven by oil, coal, and CO2 price developments. U.K. wholesale power prices have declined due to lower natural gas prices. In the Nordic market, reduced hydropower availability and uncertainty on Swedish nuclear power plant outages following the incident at Forsmark pushed wholesale power prices higher in summer. With the expected restart of several Swedish nuclear power units and lower fuel and CO2 prices, Nordic power prices have recently started to decline. Natural gas prices in the United States have decreased significantly since the beginning of 2006 due to mild weather and record natural gas storage levels. Electricity prices have followed the lower natural gas prices. SO2 prices have also decreased by over 50 percent since the beginning of 2006.   | |

Electricity Price Movements in E.ON's Core Markets U.K. Baseload EEX Baseload €/MWh1 U.S. Baseload Nord Pool Baseload 10/1/04 1/1/05 4/1/05 7/1/05 10/1/05 1/1/06 4/1/06 7/1/06 1Next-year delivery. CO2 Certificate (2005-2007) Price Movements in Europe €/metric ton 10/1/04 1/1/05 4/1/05 7/1/05 10/1/05 1/1/06 4/1/06 7/1/06

Interim Report III/2006

7

Regulation of Network Charges in Germany This year, Germany's electricity and natural gas network operators were for the first time required to submit their network charges for approval.The Federal Network Agency (BNetzA) was supposed to have been ruled on network charges within six months of submission: by May 1, 2006, for electricity network charges and by August 1, 2006, for gas network charges. However, the BNetzA has not yet completed the review process in the majority of cases. E.ON Energie is an exception. The BNetzA has issued rulings on most of E.ON Energie's gas distribution network operators and all of its electricity network operators (including its transmission system operator E.ON Netz as well as its electric distribution system operators). The agency reduced the charges filed by E.ON Netz by about 16 percent, the charges filed by E.ON Energie's electricity distributors by between 11 and 15 percent (just over 13 percent on average), and the charges filed by its gas distributors by between 9 and 14 percent (preliminarily 10 to 12 percent on average). These reductions are roughly similar to the reductions thus far announced for our competitors. On the whole, the reductions are in line with our expectations which were adjusted in the course of the year. | Although the reductions were often based on a one-sided interpretation of the Network Charges Ordinances in a manner prejudicial to network operators, E.ON Energie has decided not to take legal action but to respond by taking commercial action. The BNetzA also announced that it will require network operators to refund to network customers the difference between operators' actual network charges and their approved charges for the period between November 1, 2005 (for electricity), and February 1, 2006 (for natural gas), and the date operators' charges are approved. No network charges will be refunded until the legality of the refunds is decided in the suit filed by Vattenfall Europe Transmission, a transmission system operator, against the ruling on its network charges. We recorded a provision in our Consolidated Financial Statements for the period ended September 30, 2006, to reflect the risk associated with the retroactive application of lower network charges. |

Crude Oil and Natural Gas Price Movements in E.ON's Core Markets Monthly Brent crude oil front month $/bbl German natural gas import price €/MWh U.S. front month natural gas €/MWh average prices U.K. front month natural gas €/MWh Bunde front month natural gas €/MWh 10/1/02 1/1/03 4/1/03 7/1/03 10/1/03 1/1/04 4/1/04 7/1/04 10/1/04 1/1/05 4/1/05 7/1/05 10/1/05 1/1/06 4/1/06 7/1/06

Interim Report III/2006

8

Results of Operations | ||

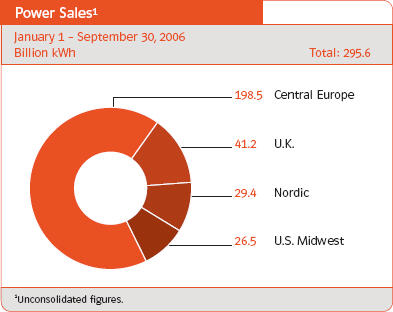

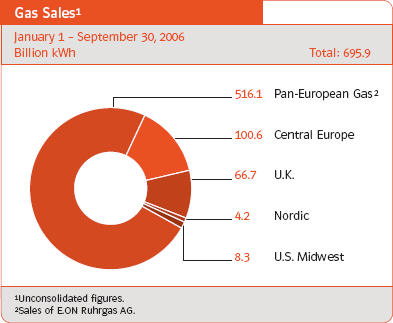

Power and Gas Sales Overall, the E.ON Group sold nearly the same amount of electricity in the first nine months of 2006 as in the prior-year period. The Central Europe market unit sold 3 percent more electricity, mainly due to the inclusion of newly consolidated regional electricity distributors in Bulgaria, Romania, and the Netherlands. By contrast, our U.K., Nordic, and U.S. Midwest market units sold less electricity than last year. We sold 8 percent more natural gas thanks primarily to colder first-quarter weather, Pan-European Gas's continuing volume growth outside Germany, and Central Europe's inclusion of newly consolidated subsidiaries in Hungary, the Czech Republic, the Netherlands, and Germany. Sales up Significantly With the exception of Nordic, all market units contributed to the significant increase in sales, which was mainly due to the following factors: the global increase in raw-material and energy prices which led to higher average power and gas prices, the inclusion of newly consolidated regional utili- | ties particularly in Bulgaria, Hungary, Romania, and the United Kingdom, and weather-driven volume increases, particularly of natural gas. Nordic's sales were slightly below the prior-year figure due to lower hydropower generation.  Adjusted EBIT up 10 Percent The improvement in adjusted EBIT at Central Europe and Pan-European Gas is also attributable to power and gas price developments, the inclusion of newly consolidated companies in Central Europe East, and higher power and gas sales volumes. However, Central Europe's adjusted EBIT was negatively impacted by provisions created to address the expected consequences of the government regulation of network charges in Germany. Thanks to the U.K. market unit's positive performance in the second and third quarters, its adjusted EBIT was nearly at the prior-year level despite the sharp decline in adjusted EBIT U.K. recorded in the first quarter. By contrast, Nordic's adjusted EBIT fell due to lower hydropower generation and to increased taxes on nuclear and hydro assets.  | |

Power Sales1 January 1 - September 30, 2006 Billion kWh Total: 295.6 198.5 Central Europe 41.2 U.K. 29.4 Nordic 26.5 U.S. Midwest 1Unconsolidated figures.

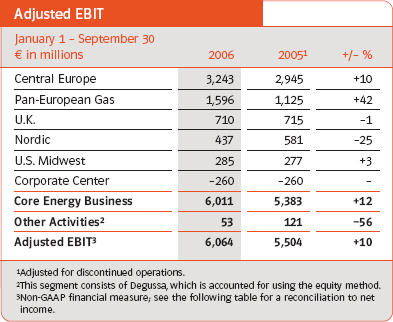

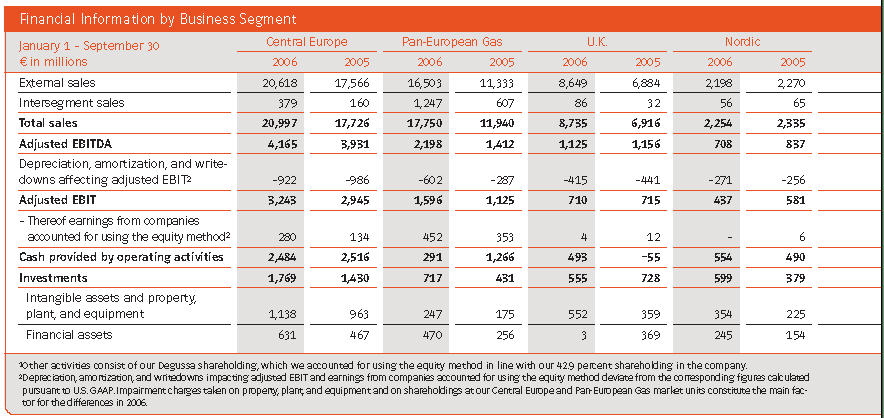

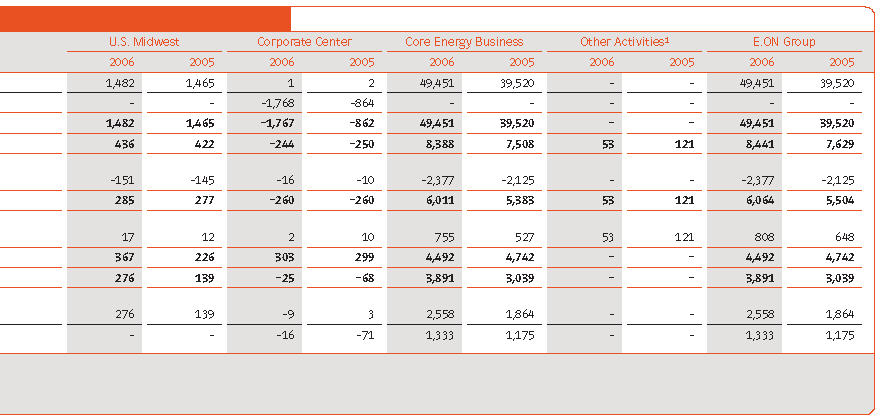

Gas Sales1 January 1 - September 30, 2006 Billion kWh Total: 695.9 516.1 Pan-European Gas2 100.6 Central Europe 66.7 U.K. 4.2 Nordic 83 U.S. Midwest 1Unconsolidated figures. 2Sales of E.ON Ruhrgas AG. Sales January 1 - September 30 € in millions 2006 20051 +/- % Central Europe 20,997 17,726 +18 Pan-European Gas 17,750 11,940 +49 U.K. 8,735 6,916 +26 Nordic 2,254 2,335 -3 U.S. Midwest 1,482 1,465 +1 Corporate Center -1,767 -862 - Sales 49,451 39,520 +25 1Adjusted for discontinued operations. Adjusted EBIT January 1 - September 30 € in millions 2006 20051 +/- % Central Europe 3,243 2,945 +10 Pan-European Gas 1,596 1,125 +42 U.K. 710 715 -1 Nordic 437 581 -25 U.S. Midwest 285 277 +3 Corporate Center -260 -260 - Core Energy Business 6,011 5,383 +12 Other Activities2 53 121 -56 Adjusted EBIT3 6,064 5,504 +10 1Adjusted for discontinued operations. 2This segment consists of Degussa, which is accounted for using the equity method. 3Non-GAAP financial measure; see the following table for a reconciliation to net income.

Interim Report III/2006

9

Net Income 59 Percent below High Prior-Year Level Net income (after income taxes and minority interests) of €2.6 billion and earnings per share of €3.99 were both 59 percent below the high prior-year level.  Adjusted interest income (net) was €57 million below the prior-year figure. The negative effect of provisions for nuclear waste management was the key factor. Net book gains in the first nine months of 2006 were significantly above the prior-year figure and resulted from the sale of securities (€351 million) and the Degussa transaction (€376 million; see commentary on page 32). In the prior-year period, net book gains resulted mainly from the sale of securities (€260 million) and from the merger of Gasversorgung Thüringen and TEAG (€112 million). We did not record restructuring expenses in the first nine months of 2006. Other nonoperating earnings primarily reflect the fulfillment of derivative gas procurement contracts and the marking to market of derivatives (-€1,954 million), particularly at the U.K. market unit. For the period ended September 30, 2005, the marking to market of derivatives resulted in a positive | effect of €582 million. In addition, we recorded impairment charges totaling €359 million due to the regulation of networks in Germany. In the previous year, the positive effect of the marking to market of derivatives was nearly offset by costs relating to the severe storm in Sweden in early 2005 and the impairment charges taken at Degussa's Fine Chemicals division. Despite our positive operating performance, income/loss (-) from continuing operations before income taxes and minority interests is considerably below the prior-year figure. The main factors were the effects of the marking to market of derivatives and impairment charges totaling €547 million at our natural gas distribution network operations resulting from the new regulation of network charges in Germany. In addition, we recorded provisions of €533 million to address the expected consequences of the retroactive application of lower network charges. Our continuing operations recorded a tax expense of €730 million in the first nine months of 2006. The decline in our tax expense primarily reflects a higher share of tax-free income. Minority interests' share of net income declined due to lower earnings contributions at the companies in question. Income/Loss (-) from discontinued operations, net, mainly includes the results of E.ON Finland, which was sold in June 2006, and Western Kentucky Energy, which is held for sale. Pursuant to U.S. GAAP, their results are reported separately in the Consolidated Statements of Income (see commentary on page 32). In the prior-year period, this item also contained the results of Viterra and Ruhrgas Industries, which were sold in 2005. Despite our positive operating performance, net income for the third quarter of 2006 of -€198 million was considerably below the high prior-year figure of €3.4 billion, primarily due to the high book gains recorded in the third quarter of 2005 on the Viterra and Ruhrgas Industries disposals. Negative factors include the marking to market of derivatives (-€674 million) relative to the prior-year quarter, impairment charges at our gas distribution network operations (-€547 million), and the increase in provisions to address anticipated regulation risks associated with the retroactive application of lower network charges (-€208 million). | |

Net Income January 1 - September 30 € in millions 2006 20051 +/- % Adjusted EBITDA2 8,441 7,629 +11 Depreciation, amortization, and impairments affecting adjusted EBIT3 -2,377 -2,125 - Adjusted EBIT2 6,064 5,504 +10 Adjusted interest income (net)4 -848 -791 - Net book gains 819 403 - Restructuring expenses - -14 - Other nonoperating earnings -2,538 31 - Income/Loss (-) from continuing operations before income taxes and minority interests 3,497 5,133 -32 Income taxes -730 -1,625 - Minority interests -270 -370 - Income/Loss (-) from continuing operations 2,497 3,138 -20 Income/Loss (-) from discontinued operations, net 132 3,261 -96 Net income 2,629 6,399 -59 1Adjusted for discontinued operations. 2Non-GAAP financial measure. 3For commentary see footnote 2 in the table on page 38. 4See reconciliation on page 39.

Interim Report III/2006

10

Results of Operations | ||

Adjusted Net Income 26 Percent above Prior-Year Figure In addition to reflecting our operating performance, net income also reflects special items such as the marking to market of derivatives. Adjusted net income is an earnings figure after interest income, income taxes, and minority interests that has been adjusted to exclude certain special items.The adjustments include book gains and losses on disposals, restructuring expenses, and other nonoperating income and expenses of a nonrecurring or rare nature (after taxes and minority interests). Adjusted net income also excludes income/loss (-) from discontinued operations, net.  Investments Significantly Higher In the period under review, the E.ON Group invested €3.9 billion, a 28 percent increase year on year. We invested €2.6 billion in intangible assets and property, plant, and equipment compared with €1.9 billion in the prior year. Investments in financial assets totaled €1.3 billion versus €1.2 billion in the prior year.  |  In the first nine months of 2006, Central Europe invested about €340 million, or 24 percent, more than in the same period last year. Investments in intangible assets and property, plant, and equipment totaled €1,138 million (prior year: €963 million) and were aimed predominantly at generation and distribution assets. Investments in financial assets increased significantly to €631 million (prior year: €467 million), primarily due to the acquisition of shareholdings in the Czech Republic and small municipal utilities in Germany and to capital increases at subsidiaries and investments in new solid-waste incineration plants. Pan-European Gas invested €717 million, of which €247 million (prior year: €175 million) went towards intangible assets and property, plant, and equipment. Investments in financial assets of €470 million (prior year: €256 million) mainly reflect the acquisition of the gas trading and storage business of Hungary's MOL (now E.ON Foldgaz Trade and E.ON Foldgaz Storage). This transaction closed in late March 2006. The U.K. market unit invested €555 million in 2006, primarily on capital expenditure for additions to property, plant, and equipment. The decrease compared to the prior year is due to higher capital expenditure in 2005 on the acquisition of the Enfield CCGT asset, Holford Gas Storage, and Economy Power's retail small and medium sized enterprise customers. This is partially offset by additional capital expenditure in 2006 (allowances under the five-year regulation review) in the regulated business and by higher expenditure on the generation portfolio, particularly to develop new renewables capacity at Lockerbie. |

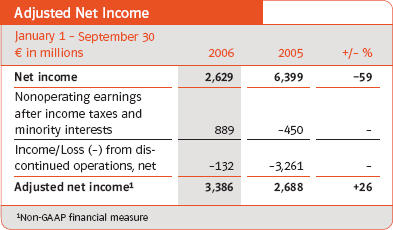

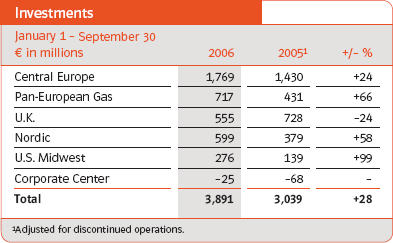

Adjusted Net Income January 1 - September 30 € in millions 2006 2005 +/- % Net income 2,629 6,399 -59 Nonoperating earnings after income taxes and minority interests 889 -450 - Income/Loss (-) from discontinued operations, net -132 -3,261 - Adjusted net income1 3,386 2,688 +26 1Non-GAAP financial measure Investments January 1- September 30 € in millions 2006 20051 +/- % Central Europe 1,769 1,430 +24 Pan-European Gas 717 431 +66 U.K. 555 728 -24 Nordic 599 379 +58 U.S. Midwest 276 139 +99 Corporate Center -25 -68 - Total 3,891 3,039 +28 1Adjusted for discontinued operations. Investments January 1 - September 30, 2006 Percentages Total: €3,891 million 46 Central Europe 18 Pan-European Gas 14 U.K. 15 Nordic 7 U.S. Midwest

Interim Report III/2006

11

Nordic invested €354 million (prior year: €225 million) in intangible assets and property, plant, and equipment to maintain existing production plants and to upgrade and extend its distribution network. The increase was mainly related to efficiency-enhancing investments in Nordic's nuclear power plants, as well as investments in its distribution network being realized earlier as a result of the severe storm in January 2005. Investments in financial assets totaled €245 million compared with €154 million in 2005. U.S. Midwest's investments of €276 million were 99 percent above the prior-year figure, primarily due to increased spending for SO2 emissions equipment and the new 750 MW base-load unit at the Trimble County 2 plant. Financial Condition Management's analysis of E.ON's financial condition uses, among other financial measures, cash provided by operating activities, free cash flow, and net financial position. Free cash flow is defined as cash provided by operating activities less investments in intangible assets and property, plant, and equipment. We use free cash flow primarily to make acquisitions, pay out cash dividends, repay debts, and make short-term financial investments. Net financial position equals the difference between our total financial assets and total financial liabilities. Management believes that these financial measures enhance the understanding of the E.ON Group's financial condition and, in particular, its liquidity.  | The E.ON Group's cash provided by operating activities in the first nine months of 2006 was 5 percent below the prior-year level. The decline in Central Europe's cash provided by operating activities is mainly attributable to an increase in working capital and in contributions to VKE, a German energy industry pension fund. A positive factor was the increase in gross profit on sales in the electricity business. Furthermore, cash provided by operating activities had been adversely affected in the prior year by nonrecurring payments relating to nuclear energy operations. The significant negative impact of the new regulation of network charges in Germany will be reflected in cash provided by operations in future periods. Pan-European Gas's positive business performance in the first nine months of 2006 is not yet reflected in its cash provided by operating activities. The main reasons are the buildup of working gas in storage at E.ON Foldgaz Trade, which became a consolidated E.ON company on March 31, 2006, and price-driven increases in expenditures for natural gas in storage at E.ON Ruhrgas AG. Other negative factors include the later payment of supplier invoices from the prior year, lower payments from customers due to higher advance payments at the end of the prior year, and price-driven increases in payments for gas procurements. The U.K. market unit's cash provided by operating activities was significantly higher year on year. The improvement was mainly due to one-off pension fund payments made in 2005. Higher gas procurement costs were recovered through higher sales prices and efficiency-enhancing initiatives. |

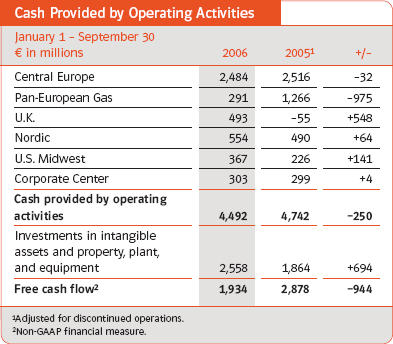

Cash Provided by Operating Activities January 1 - September 30 € in millions 2006 20051 +/- Central Europe 2,484 2,516 -32 Pan-European Gas 291 1,266 -975 U.K. 493 -55 +548 Nordic 554 490 +64 U.S. Midwest 367 226 +141 Corporate Center 303 299 +4 Cash provided by operating activities 4,492 4,742 -250 Investments in intangible assets and property, plant, and equipment 2,558 1,864 +694 Free cash flow2 1,934 2,878 -944 1Adjusted for discontinued operations. Non-GAAP financial measure.

Interim Report III/2006

12

Results of Operations | ||

Nordic's cash provided by operating activities increased because the prior-year figure had been negatively affected by a number of nonrecurring items including high cash out-flows relating to the severe storm in January 2005 and higher tax payments compared with the current year. This was, however, partially counteracted by the lower adjusted EBIT performance, primarily due to lower hydropower generation. Cash provided by operating activities at U.S. Midwest was higher mainly due to increased collections of accounts receivable in the first quarter of 2006 which resulted from higher natural gas prices in the fourth quarter of 2005. Cash increases were partly offset by pension contributions in 2006. The Corporate Center's cash provided by operating activities was at the prior-year level. Positive tax effects in the current year made up for the absence of income recorded in the prior year on the unwinding of currency swaps. In general, surplus cash provided by operating activities at Central Europe, U.K., and U.S. Midwest is lower in the first quarter of the year (despite the high sales volume typical of this season) due to the nature of their billing cycles, which in the first quarter are characterized by an increase in receivables combined with cash outflows for goods and services. During the remainder of the year, there is typically a corresponding reduction in working capital, resulting in surplus cash provided by operating activities, although sales volumes in these quarters (with the exception of U.S. Midwest) are actually lower. The fourth quarter is characterized by an increase in working capital. At Pan-European Gas, by contrast, cash provided by operating activities is recorded principally in the first quarter, whereas there are cash outflows for intake at gas storage facilities in the second and third quarters and for gas tax prepayments in the fourth quarter. A major portion of the market units' capital expenditures for intangible assets and property, plant, and equipment is paid in the fourth quarter. Due to the increase in investments in property, plant, and equipment and in intangible assets, free cash flow was 33 percent below the prior-year number. |  Net financial position, a non-GAAP financial measure, is derived from a number of figures which are reconciled to the most directly comparable U.S. GAAP measure in the next table.  |

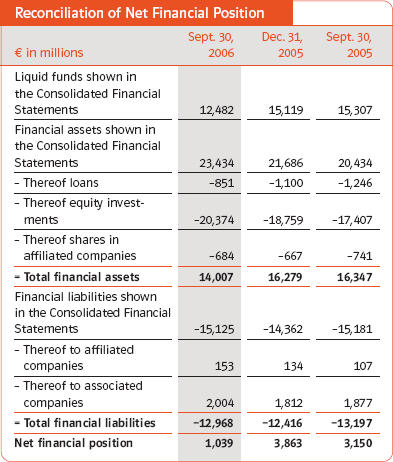

Net Financial Position Sept. 30, Dec. 31, Sept. 30, € in millions 2006 2005 2005 Bank deposits 2,869 5,859 6,126 Securities and funds (current assets) 9,613 9,260 9,181 Total liquid funds 12,482 15,119 15,307 Securities and funds (fixed assets) 1,525 1,160 1,040 Total financial assets 14,007 16,279 16,347 Financial liabilities to banks -1,570 -1,572 -2,002 Bonds (including MTN) -8,961 -9,538 -9,498

Commercial paper -1,214 - -1,061 Other financial liabilities -1,223 -1,306 -636 Total financial liabilities -12,968 -12,416 -13,197 Net financial position1 1,039 3,863 3,150 1Non-GAAP financial measure; see reconciliation in the next table.

Reconciliation of Net Financial Position Sept. 30, Dec. 31, Sept. 30, € in millions 2006 2005 2005 Liquid funds shown in the Consolidated Financial Statements 12,482 15,119 15,307 Financial assets shown in the Consolidated Financial Statements 23,434 21,686 20,434 - Thereof loans -851 -1,100 -1,246 - Thereof equity investments -20,374 -18,759 -17,407 - Thereof shares in affiliated companies -684 -667 -741 = Total financial assets 14,007 16,279 16,347 Financial liabilities shown in the Consolidated Financial Statements -15,125 -14,362 -15,181 - Thereof to affiliated companies 153 134 107 - Thereof to associated companies 2,004 1,812 1,877 = Total financial liabilities -12,968 -12,416 -13,197 Net financial position 1,039 3,863 3,150

Interim Report III/2006

13

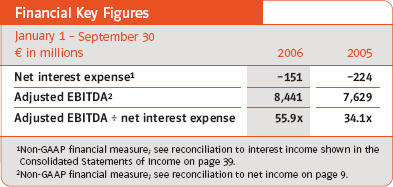

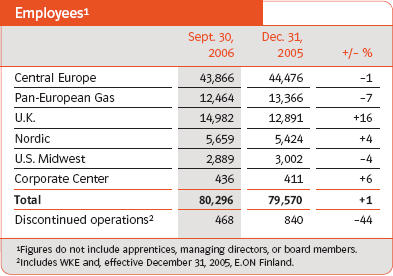

Our net financial position of €1,039 million was €2,824 million below the figure reported as of December 31, 2005 (€3,863 million). This is mainly attributable to financial outlays for investments in property, plant, and equipment, the acquisition of the natural gas business of Hungary's MOL, and the €2.6 billion payment under our contractual trust arrangement. In addition, the dividend payout (including the special dividend) and the related tax payment resulted in substantial cash outflows. Our net financial position was positively affected by proceeds from the disposal of Degussa and E.ON Finland and, in particular, by our strong cash provided by operating activities.  Net interest expense declined by €73 million from the year-earlier figure, mainly due to our, on average, better net financial position compared with the first nine months of 2005. Net interest expense only includes the interest income of those items that are also part of net financial position. On February 21, 2006, Standard & Poor's (S&P) put its AA-long-term rating for E.ON bonds and its A-1+ short-term rating on credit watch with negative implications following E.ON's announcement that E.ON had made an offer to acquire 100 percent of Endesa's stock. On February 22, 2006, Moody's announced that it was reviewing its Aa3 long-term rating for E.ON bonds for a possible downgrade, as well. Following E.ON's announcement that it was increasing its offer for Endesa, Moody's announced on September 28, 2006, that it was also reviewing its P-1 short-term rating for a possible downgrade. On September 27, 2006, S&P confirmed that E.ON's long-term and short-term ratings remained on credit watch with negative implications. Following the closing of the Endesa transaction, E.ON aims to have a single-A rating (A/A2). | On February 21, 2006, E.ON made an offer of €29.1 billion for 100 percent of Endesa's stock. Pursuant to the terms of this offer, E.ON adjusted the offer to €26.9 billion following Endesa's dividend payout in July 2006. On September 26, 2006, E.ON announced that it was increasing the existing offer to €37.1 billion. In this context, E.ON agreed to a new credit facility to finance the higher offer. Employees On September 30, 2006, the E.ON Group had 80,296 employees worldwide, as well as 2,577 apprentices and 233 board members and managing directors. Our workforce was essentially unchanged from year end 2005. At the end of the third quarter, 46,168employees, or 57.5 percent of all staff, were working outside Germany, also essentially unchanged from year end 2005.  The number of employees at Pan-European Gas declined by about 7 percent to 12,464 relative to year end 2005, mainly due to efficiency-enhancement measures at E.ON Gaz Romania. |

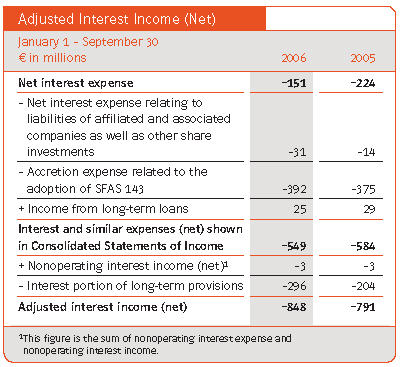

Financial Key Figures January 1 - September 30 € in millions 2006 2005 Net interest expense1 -151 -224 Adjusted EBITDA2 8,441 7,629 Adjusted EBITDA + net interest expense 55.9x 34.1x 1Non-GAAP financial measure; see reconciliation to interest income shown in the Consolidated Statements of Income on page 39. 2Non-GAAP financial measure; see reconciliation to net income on page 9. Employees1 Sept. 30, Dec. 31, 2006 2005 +/- % Central Europe 43,866 44,476 -1 Pan-European Gas 12,464 13,366 -7 U.K. 14,982 12,891 +16 Nordic 5,659 5,424 +4 U.S. Midwest 2,889 3,002 -4 Corporate Center 436 411 +6 Total 80,296 79,570 +1 Discontinued operations2 468 840 -44 1Figures do not include apprentices, managing directors, or board members. 2lncludes WKE and, effective December 31, 2005, EON Finland.

Interim Report III/2006

14

Results of Operations | ||

At the end of the third quarter of 2006, U.K. had 14,982 employees, roughly 16 percent more than at year end 2005.The increase is mainly attributable to the further additions in customer service staff and increased hiring of technical personnel at the electric distribution and metering businesses. At the end of the first nine months of 2006, Nordic had 5,659 employees, about 4 percent more than at year end 2005. The increase is mainly due to additions in retail sales staff and personnel at the network business. The 4 percent decline in U.S. Midwest's workforce compared with year end 2005 is due mainly to the sale of operating contracts of a service company in the non-regulated business. During the reporting period, wages and salaries including social security contributions and retirement payments totaled €3.5 billion, compared with €3.3 billion a year ago. Risk Situation In the normal course of business, we are subject to a number of risks that are inseparably linked to the operation of our businesses. Technologically complex facilities are involved in the production and distribution of energy. Operational failures or extended production stoppages of facilities or components of facilities could adversely impact our earnings situation. We seek to minimize these risks through ongoing employee training and qualification programs and regular maintenance and enhancement of our facilities. In the normal course of business, E.ON is exposed to interest rate, currency, commodity price, and counterparty risks which we address through the use of instruments suited to this purpose. Our market units operate in an international market environment characterized by general risks related to the business cycle and by increasingly intense competition. We use a comprehensive sales | management system and derivative financial instruments to limit the price and sales risks faced by our power and gas business on liberalized markets. The political, legal, and regulatory environment in which the E.ON Group does business is a source of additional external risks. Changes to this environment can make planning uncertain. Our goal is to play an active and informed role in shaping our business environment. We pursue this goal by engaging in a systematic and constructive dialogue with political leaders and representatives of government agencies. Currently, the following issues are of particular relevance: l The German Federal Ministry of Economics intends to intensify its antitrust oversight of the country's electricity, natural gas, and heating markets. It has been discussed that companies that individually or jointly have a dominant position on these markets should, in the future, no longer be able to charge fees or portions of fees or demand other terms of business that are less favorable than those charged or demanded by companies on comparable markets (even if the deviation is slight) or to charge fees that unfairly exceed their costs. We believe that, if implemented, these proposals would substantially impede competition on Germany's energy market. At this time, however, we are unable to quantify the effects the implementation of these proposals would have on E.ON. l Germany's Federal Cartel Office (FCO) issued an order prohibiting E.ON Ruhrgas from implementing existing long-term gas supply contracts. E.ON Ruhrgas appealed the order by filing an emergency appeal with the State Superior Court in Dusseldorf to prevent the order from taking immediate effect. The emergency appeal was not successful. We are now concentrating our efforts on the main case before the State Superior Court whose decision can be appealed to the German Federal Appeals Court. We expect that the main case will provide our customers and us with a thorough legal clarification and therefore the necessary legal assurance, in particular about the permissibility of the competitive injunction issued against us by the FCO. In accordance with the terms of the FCO's order, we have concluded new gas supply contracts (for the period after October 1, 2006) with our reseller customers affected by the order. l The FCO is carrying out an investigation into the use of CO2 certificates to calculate electricity prices. A fundamental principle of emissions trading is that factoring the cost of certificates into the price of electricity will serve to reduce CO2 emissions. The FCO is currently investigating whether the factoring in of CO2 certificates, which were allocated at no cost, is an abusive market practice. | |

Interim Report III/2006

15

The operational and strategic management of the E.ON Group relies heavily on highly complex information technology. Our IT systems are maintained and optimized by qualified E.ON Group experts, outside experts, and a wide range of technical security measures. In the period under review, the E.ON Group's risk situation did not change substantially from year end 2005. Outlook The E.ON Group's positive operating performance continued in the third quarter. We continue to expect our adjusted EBIT for 2006 to surpass the high prior-year level. However, we will not repeat the extraordinarily high net income figure posted in 2005, which resulted in particular from the book gains on our successful Viterra and Ruhrgas Industries disposals. The earnings forecast by market unit is as follows: For 2006, we expect Central Europe's adjusted EBIT to be above the prior-year level. We continue to expect to offset the adverse effects of regulatory measures affecting the operations of our network business through operating improvements in other areas and through nonrecurring effects relating to earnings from shareholdings already recorded in the course of the year. | We expect Pan-European Gas's full-year adjusted EBIT to markedly exceed the figure for 2005, mainly due to positive earnings effects from the first half of this year. On balance, the up/midstream business will benefit from temperature-driven volume increases recorded in the first quarter. Moreover, oil price developments were a significant negative factor in the prior year. We expect the downstream business to deliver a lower adjusted EBIT due to the new regulatory regime in Germany. The expected improvement in the U.K. market unit's figures following the first quarter materialized during the second and third quarters. This improvement supports our expectation that full-year 2006 adjusted EBIT will be significantly above the 2005 figure. Important factors include the impact of retail price increases, increased value from U.K.'s generation fleet, and profit and cost initiatives partially counteracted by future commodity cost increases. We anticipate that Nordic's adjusted EBIT for 2006 will be significantly below the strong figure posted in 2005. Earnings development is affected by significantly higher nuclear and hydro taxes and by the absence of earnings streams from divested hydropower assets. In addition, Nordic's electricity generation was negatively affected by the hydrological situation during the third quarter and by the unplanned outages in several Swedish nuclear units after the Forsmark incident. These effects will be partially counteracted by higher average achieved electricity prices. We expect U.S. Midwest's 2006 adjusted EBIT to slightly exceed the prior-year level due to lower costs following the exit from the organized MISO market in September. |

Interim Report III/2006

16

Market Units

Central Europe  Market Development German baseload electricity prices for 2007 delivery closed the quarter more than 5 percent higher than at the start of the year. However, the Federal Network Agency's first rulings on network charges will serve to reduce electricity and natural gas prices for end-customers. Power and Gas Sales The Central Europe market unit increased its power sales by 6.2 billion kWh to 198.5 billion kWh. The increase is nearly entirely attributable to the inclusion of newly consolidated regional electricity distributors, particularly in Bulgaria, Romania, and the Netherlands. Central Europe's regional distribution companies sold about 20 billion kWh more natural gas than in the prior-year period. More than three quarters of the increase resulted from consolidation effects. In the prior-year period, our Hungarian gas utilities contributed only six months of results, Gasver-sorgung Thuringen (GVT) three months, and NRE of the Netherlands two months. Also included in the current year is JCP of the Czech Republic, which became a consolidated E.ON company in September 2006. The remainder of the increase is primarily weather driven. Power Generation and Procurement Central Europe utilized its flexible mix of generation assets to meet about 47 percent of its electricity requirements, compared with 48 percent in the prior year. It procured around 4.5 billion kWh more electricity from outside sources than in the year-earlier period. This increase results mainly from the inclusion of newly consolidated subsidiaries in Bulgariaand Romania. |    |

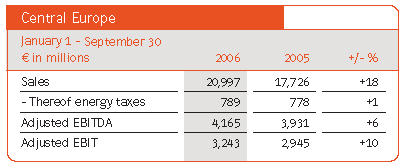

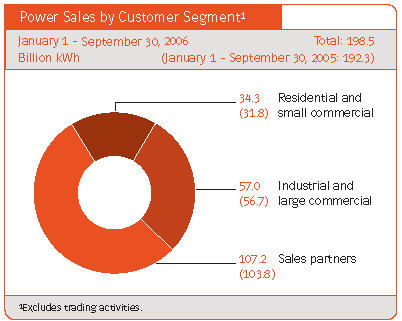

Central Europe Central Europe January 1 - September 30 € in millions 2006 2005 +/- % Sales 20,997 17,726 +18 - Thereof energy taxes 789 778 +1 Adjusted EBITDA 4,165 3,931 +6 Adjusted EBIT 3,243 2,945 +10 Power Sales by Customer Segment1 January 1 - September 30, 2006 Total: 198.5 Billion kWh (January 1- September 30, 2005: 192.3) 343 Residential and (31.8) small commercial 57.0 Industrial and (56.7) large commercial 107.2 Sales partners (103.8) 1Excludes trading activities. Gas Sales by Customer Segment1 January 1 - September 30, 2006 Total: 100.6 Billion kWh (January 1 - September 30, 2005: 80.7) 36.0 Residential and (24.7) small commercial 393 Industrial and (33.1) large commercial 253 Sales partners (223) 1Excludes trading activities. Power Generation and Procurement1 January 1 - September 30 Billion kWh 2006 2005 +/- % Owned generation 98.3 96.4 +2 Purchases 109.8 105.2 +4 Jointly owned power plants 9.2 9.1 +1 Outside sources 100.6 96.1 +5 Power procured 208.1 201.6 +3 Station use, line loss, pumped-storage hydro -9.6 -9.3 +3 Power sales 198.5 192.3 +3 1Excludes trading activities.

Interim Report III/2006

17

Sales and Adjusted EBIT Central Europe grew sales by €3.3 billion relative to the prior-year period. The expansion of our operations, particularly in Central Europe East, is responsible for about one third of the increase.The increase is mainly also attributable to adjustments to our power and gas prices resulting from the global rise in raw-material and energy prices and to weather-driven volume increases, particularly of natural gas. Adjusted EBIT rose by €298 million year on year, with Central Europe's business units developing as follows: With an increase of €75 million, Central Europe West Power's adjusted EBIT was only slightly above the prior-year figure. At the end of the second quarter, adjusted EBIT was €136 million below the prior-year figure. This modest development is mainly attributable to negative effects totaling €473 million relating to the new regulation of network charges in Germany | (see commentary on page 7).These effects could not be fully offset by further operating improvements in other areas. The passthrough of higher wholesale electricity prices to end-customers was offset by higher conventional fuel costs and higher power procurement costs. Adjusted EBIT was also negatively affected by increased charges stemming from earlier reporting periods. Positive effects included significant nonrecurring earnings from shareholdings and the absence of provisions for nuclear operations taken in the prior year. Adjusted EBIT at Central Europe West Gas was €39 million above the prior-year figure, particularly due to the fact that GVT was not a consolidated E.ON company in the prior-year period and to volume increases resulting from cold weather in the first half of the year. The regulation of network charges in Germany reduced adjusted EBIT by €46 million. Central Europe East's adjusted EBIT rose by €71 million com-pared with the same period last year. This largely reflects the inclusion, for the entire period under review, of earnings from regional distributors in Bulgaria, Hungary, and Romania acquired in 2005.The increase also results from price-driven effects at our operations in Bulgaria and the Czech Republic. Adjusted EBIT recorded under Other/Consolidation increased by €113 million, mainly due to higher income from realized hedging transactions and high earnings from shareholdings. |

Sources of Owned Generation January 1 - September 30, 2006 Percentages 46.8 Nuclear 30.9 Hard coal 6.6 Lignite 7.4 Oil and natural gas 5.8 Hydro 2.5 Other Financial Highlights by Business Unit Central Europe West Central Europe Other/ January 1 - September 30 Power Gas East Consolidation Central Europe € in millions 2006 2005 2006 2005 2006 2005 2006 2005 2006 2005 Sales1 13,836 12,457 3,573 2,548 2,480 1,772 319 171 20,208 16,948 Adjusted EBITDA 3,173 3,189 424 376 393 306 175 60 4,165 3,931 Adjusted EBIT 2,643 2,568 257 218 243 172 100 -13 3,243 2,945 1Excludes energy taxes; trading activities am recognized net.

Interim Report III/2006

18

Market Units

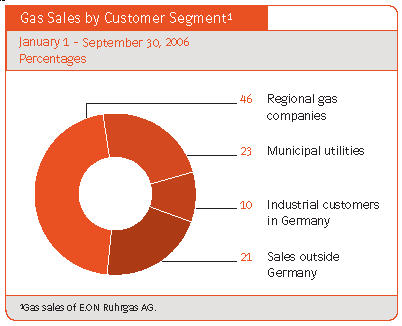

Pan-European Gas  Market Development Germany consumed about 5.5 percent more natural gas in the first nine months of 2006 than in the prior-year period, mainly due to cooler weather in the first four months of the year and increased use of natural gas for electric generation. Between July and September, natural gas consumption declined by 3 percent due to temperatures that averaged about 0.5 degrees Centigrade higher than in the previous year. Gas Sales Through September 30, Pan-European Gas sold slightly more than 8 percent more natural gas than in the prior-year period. It sold 111.2 billion kWh of natural gas in the third quarter, 2 percent less than last year.  Sales outside Germany, which rose by 29 percent to 110 billion kWh, were a significant factor in the increase and accounted for more than one fifth of total sales volume. In Denmark, France, Italy, and the Netherlands we concluded new supply contracts and contract extensions with a term of one year or more and a total volume of approximately 10 billion kWh. In the first nine months of 2006, sales volume in Germany rose by 4 percent year on year to 406 billion kWh.Third-quarter sales volume of 83 billion kWh was 10 percent below the prior-year figure. Sales by segment reflect the higher share of sales outside Germany, which increased from 18 to 21 percent of total sales volume. Regional gas companies accounted | for 46 percent of total sales volume, municipal utilities for 23 percent, and industrial customers for 10 percent compared with 48 percent, 23 percent, and 11 percent, respectively, in the prior-year period.  Supply Agreements Concluded with Gazprom In August, we concluded agreements with Gazprom for contractual commitments to new volume and contract extensions for additional volume totaling about 400 billion cubic meters of natural gas. The agreements extend existing contracts by 15 years through 2035, and, from 2010/2011 through 2036, involve the supply of additional natural gas to be transported via the Nord Stream pipeline to Germany's Baltic Sea coast. Nord Stream, a joint project of Gazprom, E.ON Ruhrgas, and Wintershall, is important for Europe's natural gas supply. E.ON Ruhrgas is also participating in the construction of two new pipelines linking Nord Stream to Germany's natural gas network. The annual supply amount of roughly 24 billion cubic meters is one third of E.ON Ruhrgas's current procurement. Gas Production Higher Pan-European Gas produced about 80 percent more natural gas and just over 20 percent more oil and condensates than in the previous year.The sharp increase results from the expansion of the upstream business and in particular from the inclusion of E.ON Ruhrgas UK North Sea for the first time. |

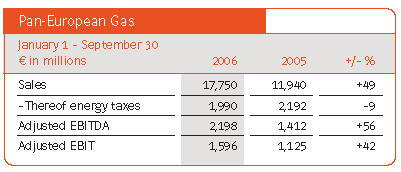

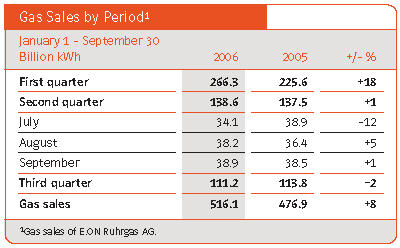

Pan-European Gas Pan-European Gas January 1 - September 30 € in millions 2006 2005 +/- % Sales 17,750 11,940 +49 - Thereof energy taxes 1,990 2,192 -9 Adjusted EBITDA 2,198 1,412 +56 Adjusted EBIT 1,596 1,125 +42 Gas Sales by Period1 January 1 - September 30 Billion kWh 2006 2005 +/- % First quarter 266.3 225.6 +18 Second quarter 138.6 137.5 +1 July 34.1 38.9 -12 August 38.2 36.4 +5 September 38.9 38.5 +1 Third quarter 111.2 113.8 -2 1Gas sales 516.1 476.9 +8 1Gas sales of EON Ruhrgas AG. Gas Sales by Customer Segment1 January 1 - September 30, 2006 Percentages 46 Regional gas companies 23 Municipal utilities 10 Industrial customers in Germany 21 Sales outside Germany 1Gas sales of EON Ruhrgas AG.

Interim Report III/2006

19

| In September, E.ON Ruhrgas UK North Sea successfully completed test-drilling in Babbage gas field, in which the company owns a 47 percent share. In order to further expand the upstream business in Norway as well, E.ON Ruhrgas Norge has applied for an operator's permit in Norway and will bid for licenses in the upcoming round of license allocations. Sales and Adjusted EBIT In the first nine months of 2006, Pan-European Gas increased sales (excluding energy taxes) by 62 percent year on year to €15.8 billion. Sales growth in the midstream business resulted primarily from higher sales volumes in conjunction with higher average sales prices. Sales rose at the upstream business due in particular to the inclusion of E.ON Ruhrgas UK North Sea along with higher sales prices driven by oil prices. This company was acquired in 2005 and only contributed to consolidated sales in November and December of the prior year. In September 2005, Pan-European Gas increased its stake in Njord Field from 15 percent to 30 percent, which also had a positive effect on sales in the current-year period. Consolidation effects were also responsible for a significant increase in sales at Downstream Shareholdings. First, E.ON Földgaz Trade and E.ON Földgaz Storage became consolidated E.ON subsidiaries on March 31, 2006. Second, the sales of E.ON Gaz Romania are included from the beginning of 2006, whereas in 2005 they were not consolidated until the third quarter. | Pan-European Gas's adjusted EBIT for the first three quarters of 2006 increased significantly year on year, from €1,125 million to €1,596 million. Continued high oil and natural gas price levels constituted the key factor in the upstream business's adjusted EBIT performance. Temperature-driven volume increases in the first quarter and sales growth outside Germany resulted in a significant increase in adjusted EBIT at the midstream business. In addition, the continual rise in oil prices had had a considerable negative impact on adjusted EBIT in the prior-year period. Furthermore, nonrecurring income from the final clearing of trading transactions contributed to the increase in adjusted EBIT; the negative effects of these transactions had had a negative impact on the prior-year figure. In the third quarter, the new regulation of network charges in Germany had a significant negative impact on adjusted EBIT at Downstream Shareholdings. In some cases, the new regulation of network charges led to significant impairment charges on our shareholdings in municipal utilities. By contrast, higher equity earnings from associated companies constituted a key positive effect on adjusted EBIT. Another was the inclusion of E.ON Gaz Romania for the entire period under review, whereas E.ON Földgaz Trade, which operates in Hungary's regulated gas market, recorded a negative adjusted EBIT due to the delay in passing through higher procurement costs. |

Financial Highlights by Business Unit Downstream- Other/ January 1 - September 30 Up-/Midstream Shareholdings Consolidation Pan-European Gas € in millions 2006 2005 2006 2005 2006 2005 2006 2005 Sales1 13,209 8,767 3,041 1,261 -490 -280 15,760 9,748 Adjusted EBITDA 1,530 936 660 468 8 8 2,198 1,412 Adjusted EBIT 1,222 712 367 405 7 8 1,596 1,125 1Excludes energy taxes.

Interim Report III/2006

20

Market Units

U.K.  Market Development U.K. market electricity and natural gas consumption at 258 billion kWh and 751 billion kWh, respectively, for the first nine months of 2006 was broadly in line with 2005. On August 17, E.ON UK announced a consumer price rise of 9.7 percent for electricity and 18.4 percent for gas effective from August 21. E.ON UK provides practical solutions to improve the energy efficiency and income of households in, or at risk of, fuel poverty through its CaringEnergy scheme. E.ON UK has committed €100 million to CaringEnergy over the next three years. E.ON UK's retail business has moved from sixth position to second position in the Energywatch league table reflecting the focus on customer service. Power and Gas Sales The decrease in Industrial and Commercial (I&C) power and gas volumes reflected E.ON UK's focus on margin rather than volume. Residential and SME power sales volumes increased despite a 2 percent reduction in the number of customer accounts; the volume increase is primarily due to colder weather in the first quarter.  | Power Generation and Procurement The slight year-on-year decrease in owned generation is due to lower gas generation (lower spark spreads) which is almost offset by increased coal generation (higher dark spreads). Coal generation was higher despite a long outage at Ratcliffe in the third quarter of 2006. Purchases from outside sources declined due to lower retail I&C sales volumes.  U.K.'s attributable generation capacity is 10,547 MW, an increase of 640 MW from September 2005. This was mainly due to the return of an oil-fired unit at Grain.  |

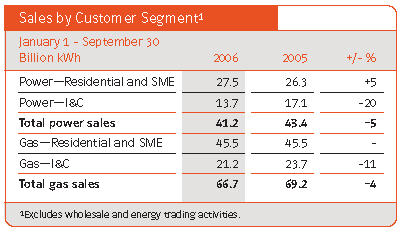

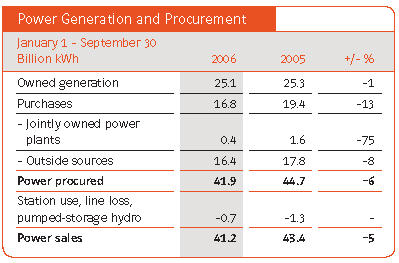

U.K. January 1 - September 30 € in millions 2006 2005 +/- % Sales 8,735 6,916 +26 Adjusted EBITDA 1,125 1,156 -3 Adjusted EBIT 710 715 -1 Sales by Customer Segment1 January 1 - September 30 Billion kWh 2006 2005 +/- % Power-Residential and SME 27.5 26.3 +5 Power-I&C 13.7 17.1 -20 Total power sales 41.2 43.4 -5 Gas-Residential and SME 45.5 45.5 - Gas-I&C 21.2 23.7 -11 Total gas sales 66.7 69.2 -4 1Excludes wholesale and energy trading activities. Power Generation and Procurement January 1 - September 30 Billion kWh 2006 2005 +/- % Owned generation 25.1 25.3 -1 Purchases 16.8 19.4 -13 - Jointly owned power plants 0.4 1.6 -75 - Outside sources 16.4 17.8 -8 Power procured 41.9 44.7 -6 Station use, line loss, pumped-storage hydro -0.7 -1.3 - Power sales 41.2 43.4 -5 Sources of Owned Generation January 1 - September 30, 2006 Percentages 61 Hard coal 36 Natural gas and merchant CHP 3 Hydro, wind, oil, other

Interim Report III/2006

21

| In response to the Renewable Obligation, E.ON UK continues to grow a balanced portfolio of renewable power purchase agreements and physical assets. In the first nine months of 2006, E.ON UK co-fired biomass materials at Kingsnorth and Ironbridge, generating a total of 205 million kWh. Work has also commenced on the construction of a 44 MW wood-burning plant in Lockerbie in southwest Scotland, which when built will be the United Kingdom's largest dedicated biomass plant. In addition, construction of an 18 MW onshore wind project at Stags Holt has started in October 2006 and will be operational in the fourth quarter of 2007. Sales and Adjusted EBIT The U.K. market unit increased its sales in the first nine months of 2006 compared with the prior year primarily due to price increases in the retail business. This was driven by higher natural gas and power prices in the wholesale market. U.K. delivered an adjusted EBIT of €710 million in the first nine months of 2006, of which €347 million was in the regulated business and €443 million in the non-regulated business. Adjusted EBIT at the non-regulated business increased by €50 million.The increase is primarily due to retail price rises, and cost and profit initiatives offset by the impact of higher natural gas costs in the first quarter 2006 and the one-off prior year benefit relating to the integration of previously outsourced customer service activities. Despite adjusted | EBIT being slightly below prior year, the performance in the second and third quarter of €263 million versus the prior year has almost reversed the underperformance in the first quarter of -€213 million versus the prior year.This improvement is in line with our expectation that the increase in retail prices along with cost and profit initiatives would restore business margins. The regulated business shows steady year-on-year growth with the €20 million adjusted EBIT increase being mainly due to a tariff change allowed by the regulator following a distribution price control review. Other/Consolidation is €75 million below the prior year due to higher service costs from a growing business, higher pension costs, and foreign-exchange costs. |

Financial Highlights by Business Unit Regulated Non-regulated Other/ January 1 - September 30 business business1 Consolidation U.K. € in millions 2006 2005 2006 2005 2006 2005 2006 2005 Sales 621 604 8,171 6,449 -57 -137 8,735 6,916 Adjusted EBITDA 457 441 747 709 -79 6 1,125 1,156 Adjusted EBIT 347 327 443 393 -80 -5 710 715 1The non-regulated business now includes the new Energy Services business, a material part of which was previously reported at the regulated business. The non-regulated business also includes a recharge from Business Services (facilities, IT, and other shared services); 2005 has been rebased to ensure that comparisons are valid. The regulated business already included the recharge due to regulatory reasons.

Interim Report III/2006

22

Market Units

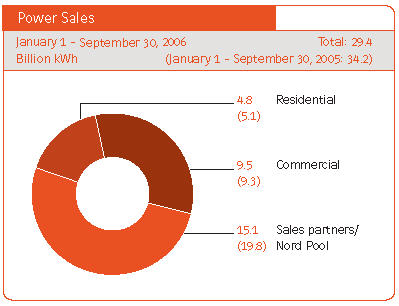

Nordic  Market Development The Nordic region consumed 22 percent more electricity than in the prior-year period, mainly due to higher consumption resulting from considerably colder weather at the beginning of the year. Autumn has been warmer than normal. Imports to Nordic from surrounding countries increased to over 9 billion kWh during the first nine months of 2006 compared with a net export of 1 billion kWh in the prior-year period. Net exports to Germany were less than 1 billion kWh compared with 9 billion kWh during the same period last year and are decreasing. Power Sales  E.ON Nordic sold 4.8 billion kWh less electricity than in the corresponding period of 2005 due to lower sales at the Nord Pool, Northern Europe's energy exchange. This was a consequence of both the sale of hydropower assets to Statkraft in late 2005, which reduced Nordic's owned generation capacity, and lower hydropower production due to the prevailing | hydropower situation. Sales to residential customers decreased compared with the previous year, while sales to commercial customers increased slightly. Power Generation and Procurement E.ON Nordic covered 69 percent of its electricity sales with power from its own generation assets. E.ON Nordic's owned generation decreased by 4.5 billion kWh relative to the prior-year period. Hydropower production decreased due to the sale of hydropower assets to Statkraft in October 2005, but primarily due to significantly lower reservoir inflow. In addition, several Swedish nuclear units were taken offline as a consequence of an incident at Vattenfall's Forsmark nuclear power station in late July. The overall decrease in hydro and nuclear production in the third quarter was somewhat counteracted by increased CHP production and higher availability of nuclear assets in the first half of the year.   |

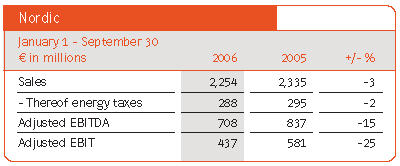

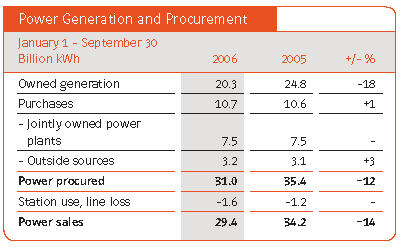

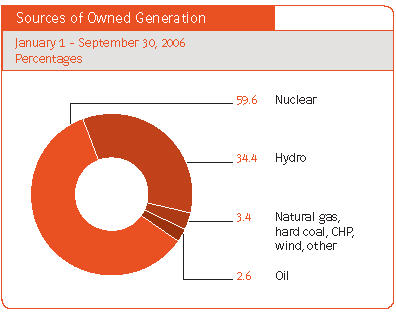

Nordic Nordic January 1 - September 30 € in millions 2006 2005 +/- % Sales 2,254 2,335 -3 - Thereof energy taxes 288 295 -2 Adjusted EBITDA 708 837 -15 Adjusted EBIT 437 581 -25 Power Sales Power Sales January 1 - September 30, 2006 Total: 29.4 Billion kWh (January 1 - September 30, 2005: 34.2) 4.8 (5.1) Residential 9.5 (9.3) Commercial 15.1 (19.8) Sales partners/ Nord Pool Power Generation and Procurement January 1 - September 30 Billion kWh 2006 2005 +/- % Owned generation 20.3 24.8 -18 Purchases 10.7 10.6 +1 - Jointly owned power plants 7.5 7.5 - Outside sources 3.2 3.1 +3 Power procured 31.0 35.4 -12 Station use, line loss -1.6 -1.2 - Power sales 29.4 34.2 -14 Sources of Owned Generation January 1 - September 30, 2006 Percentages 59.6 Nuclear 34.4 Hydro 3.4 Natural gas, hard coal, CHP, wind, other 2.6 Oil

Interim Report III/2006

23

Gas and Heat Sales Heat sales increased as a consequence of colder weather at the beginning of the year and the acquisition of heat operations in Denmark. Natural gas sales declined despite the colder weather, primarily due to lower sales to distributors and increased competition.  Sales and Adjusted EBIT E.ON Nordic's sales, excluding energy taxes, decreased by 4 percent compared with the first nine months of 2005. The decrease was primarily due to lower hydropower generation, which was partially offset by higher average sales prices. | E.ON Nordic's adjusted EBIT decreased by €144 million year on year to €437 million. Compared with the prior year, adjusted EBIT for the first nine months was negatively impacted by increased taxes on hydro and nuclear assets. Significantly lower reservoir inflow resulted in lower hydropower generation. In addition, the hydropower assets sold to Statkraft contributed to prior-year adjusted EBIT. Adjusted EBIT was positively impacted by rising spot electricity prices and successful hedging activities, which enabled Nordic to secure higher average sales prices for its production portfolio. |

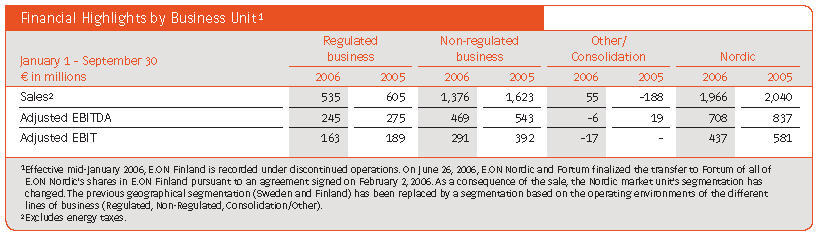

Gas and Heat Sales January 1 - September 30 Billion kWh 2006 2005 +/- % Gas sales 4.2 5.1 -18 Heat sales 5.7 5.2 +10 Financial Highlights by Business Unit1 Regulated Non-regulated Other/ January 1 - September 30 business business Consolidation Nordic € in millions 2006 2005 2006 2005 2006 2005 2006 2005 Sales2 535 605 1,376 1,623 55 -188 1,966 2,040 Adjusted EBITDA 245 275 469 543 -6 19 708 837 Adjusted EBIT 163 189 291 392 -17 - 437 581 1Effective mid-January 2006, E.ON Finland is recorded under discontinued operations. On June 26, 2006, E.ON Nordic and Fortum finalized the transfer to Fortum of all of E.ON Nordic's shares in E.ON Finland pursuant to an agreement signed on February 2, 2006. As a consequence of the sale, the Nordic market unit's segmentation has changed. The previous geographical segmentation (Sweden and Finland) has been replaced by a segmentation based on the operating environments of the different lines of business (Regulated, Non-Regulated, Consolidation/Other). 2Excludes energy taxes.

Interim Report III/2006

24

Market Units

U.S. Midwest  MISO Exit Effective September E.ON U.S. has completed the exit from the Midwest Independent System Operator (MISO) and entered into alternative arrangements with the Tennessee Valley Authority and Southwest Power Pool effective early September 2006. Power and Gas Sales  Regulated utility retail power sales volumes decreased slightly in 2006 compared with 2005, primarily due to milder weather in 2006. Off-system sales volumes were lower compared with 2005 as a result of an increased use of E.ON U.S.'s generation for native load to replace the lost volumes from a purchase contract with Electric Energy Inc. (EEI). EEI is a 1,000 MW power station in which E.ON U.S. has a 20 percent stake. In the past, E.ON U.S. could buy its share of the output at cost and utilize this to meet native load. Since January 1, 2006, EEI sells its power at market prices. E.ON U.S. can no longer utilize this | power to meet native load and now supplies this power from its own generation. Retail natural gas sales volumes declined due largely to milder winter weather compared with 2005 and reduced consumption due to higher prices. Off-system sales of natural gas decreased due to high market prices in the first quarter and correspondingly lower availability of excess gas for sale. Power Generation and Procurement Coal-fired power plants accounted for 96 percent of U.S. Midwest's electric generation in 2006, while gas-fired and hydro generating assets accounted for the remaining 4 percent.   |

U.S. Midwest U.S. Midwest January 1- September 30 € in millions 2006 2005 +/- % Sales 1,482 1,465 +1 Adjusted EBITDA 436 422 +3 Adjusted EBIT 285 277 +3

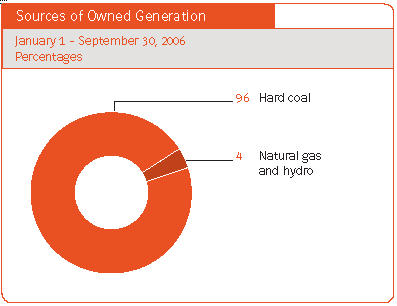

Sales by Customer Segment January 1- September 30 Billion kWh 2006 2005 +/- % Regulated utility business - Retail customers 24.8 25.4 -2 - Off-system sales 1.7 3.2 -47 Power sales 26.5 28.6 -7 Retail customers 8.3 9.3 -11 Off-system sales - 0.8 -100 Gas sales 8.3 10.1 -18 Power Generation and Procurement January 1 - September 30 Billion kWh 2006 2005 +/- % Proprietary generation - Owned power stations 26.3 26.9 -2 Purchases 2.6 3.9 -33 Power procured 28.9 30.8 -6 Station use, line loss -2.4 -2.2 - Power sales 26.5 28.6 -7 Sources of Owned Generation January 1 - September 30, 2006 Percentages 96 Hard coal 4 Natural gas and hydro

Interim Report III/2006

25

Sales and Adjusted EBIT U.S. Midwest's sales were in line with last year. Lower volumes due to milder weather were offset by higher gas prices recoverable from retail customers. U.S. Midwest's adjusted EBIT increased by 3 percent, mainly due to favorable exchange-rate variances. Lower retail volumes in the regulated business, mainly due to significantly milder weather in 2006, were offset by cost savings due to the exit from MISO in the third quarter of 2006 and lower operating expenses as a result of the completion of the amortization of prior restructuring costs. In addition, the regulated business benefited from higher earnings on environmental capital spending. | In the non-regulated business, lower earnings as a result of the sale of an interest in a coal-fired facility in North Carolina in mid-2006 were partly offset by better performance in the Argentine business. |

Financial Highlights by Business Unit Regulated Non-regulated January 1 - September 30 business business/other U.S. Midwest € in millions 2006 2005 2006 2005 2006 2005 Sales 1,432 1,405 50 60 1,482 1,465 Adjusted EBITDA 426 411 10 11 436 422 Adjusted EBIT 283 269 2 8 285 277

Interim Report III/2006

26

Interim Financial Statements (Unaudited)

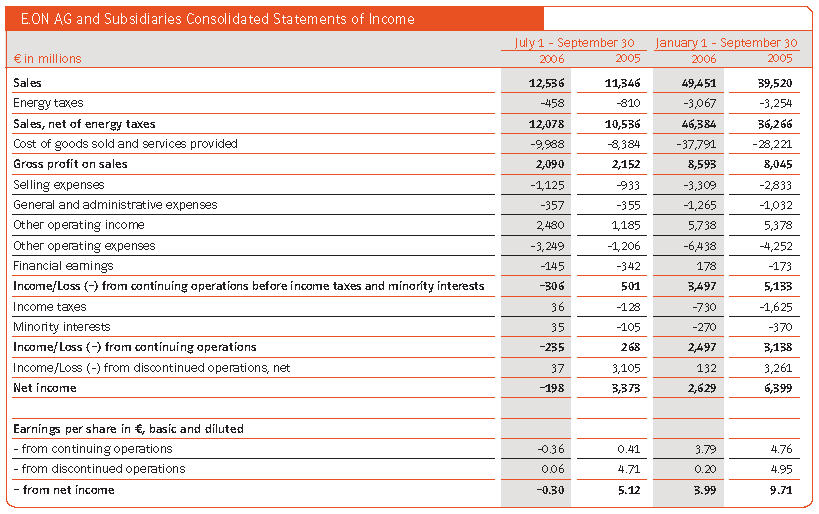

E.ON AG and Subsidiaries Consolidated Statements of Income July 1- September 30 January 1 - September 30 € in millions 2006 2005 2006 2005 Sales 12,536 11,346 49,451 39,520 Energy taxes -458 -810 -3,067 -3,254 Sales, net of energy taxes 12,078 10,536 46,384 36,266 Cost of goods sold and services provided -9,988 -8,384 -37,791 -28,221 Gross profit on sales 2,090 2,152 8,593 8,045 Selling expenses -1,125 -933 -3,309 -2,833 General and administrative expenses -357 -355 -1,265 -1,032 Other operating income 2,480 1,185 5,738 5,378 Other operating expenses -3,249 -1,206 -6,438 -4,252 Financial earnings -145 -342 178 -173 Income/Loss (-) from continuing operations before income taxes and minority interests -306 501 3,497 5,133 Income taxes 36 -128 -730 -1,625 Minority interests 35 -105 -270 -370 Income/Loss (-) from continuing operations -235 268 2,497 3,138 Income/Loss (-) from discontinued operations, net 37 3,105 132 3,261 Net income -198 3,373 2,629 6,399 Earnings per share in €, basic and diluted - from continuing operations -0.36 0.41 3.79 4.76 - from discontinued operations 0.06 4.71 0.20 4.95 - from net income -0.30 5.12 3.99 9.71

Interim Report III/2006

27

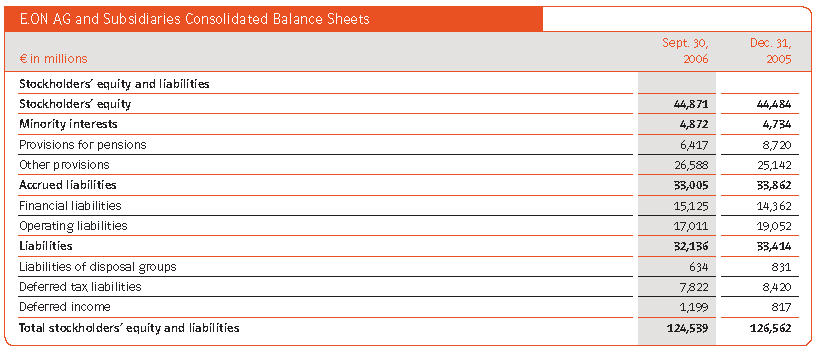

E.ON AG and Subsidiaries Consolidated Balance Sheets Sept. 30, Dec.31, € in millions 2006 2005 Assets Goodwill 15,295 15,363 Intangible assets 3,821 4,125 Property, plant, and equipment 41,655 41,323 Financial assets 23,434 21,686 Fixed assets 84,205 82,497 Inventories 3,850 2,457 Financial receivables and other financial assets 2,066 2,019 Operating receivables and other operating assets 19,309 21,354 Liquid funds (thereof cash and cash equivalents < 3 months 2006: 2,627; 2005: 4,413) 12,482 15,119 Nonfixed assets 37,707 40,949 Deferred taxes 1,505 2,079 Prepaid expenses 475 356 Assets of disposal groups 647 681 Total assets 124,539 126,562 E.ON AG and Subsidiaries Consolidated Balance Sheets Sept. 30, Dec.31, € in millions 2006 2005 Stockholders' equity and liabilities Stockholders' equity 44,871 44,484 Minority interests 4,872 4,734 Provisions for pensions 6,417 8,720 Other provisions 26,588 25,142 Accrued liabilities 33,005 33,862 Financial liabilities 15,125 14,362 Operating liabilities 17,011 19,052 Liabilities 32,136 33,414 Liabilities of disposal groups 634 831 Deferred tax liabilities 7,822 8,420 Deferred income 1,199 817 Total stockholders' equity and liabilities 124,539 126,562

Interim Report III/2006

28

Interim Financial Statements (Unaudited)

Interim Report 111/2006, 28 Interim Financial Statements (Unaudited), E.ON AG and Subsidiaries Consolidated Statements of Cash Flow, January 1 - September 30, € in millions, 2006 2005, Net income 2,629 6,399, Income applicable to minority interests 270 370, Adjustments to reconcile net income to net cash provided by operating activities, Income from discontinued operations, net -132 -3,261, Depreciation, amortization, impairment 2,875 2,125, Changes in provisions 1136 68, Changes in deferred taxes -413 -57, Other noncash income and expenses -566 -107, Gain/Loss on disposal of fixed assets -574 -196, Changes in nonfixed assets and other operating liabilities -733 -599, Cash provided by operating activities 4,492 4,742, Proceeds from disposal of, equity investments and other financial assets 3,853 5,762, intangible assets and property, plant, and equipment 125 130, Purchase of, equity investments and other financial assets -1,333 -1,175, intangible assets and property, plant, and equipment - -2,558 -1,864, Changes in other liquid funds -2,262 -388, Cash provided by (used for) investing activities of continuing operations -2,175 2,465, Payments received/made from changes in capital, including minority interests -,Payments for treasury stock, net - -44, Payment of cash dividends to stockholders of E.ON AG -4,614 -1,549, minority stockholders -232 -233, Changes in financial liabilities 796 -3,192, Cash provided by (used for) financing activities of continuing operations -4,049 -5,018, Net increase (decrease) in cash and cash equivalents maturing (< 3 months) from continuing operations -1,732 2,189, Cash provided by operating activities of discontinued operations 65 134, Cash provided by (used for) investing activities of discontinued operations -105 -347, Cash provided by (used for) financing activities of discontinued operations 2 -172, Net increase (decrease) in cash and cash equivalents maturing (<3 months) from discontinued operations -38 -385, Effect of foreign exchange rates on cash and cash equivalents (< 3 months) -16 80, Cash and cash equivalents (< 3 months) at the beginning of the period 4,413 4,176, Cash and cash equivalents (< 3 months) from discontinued operations at the end of the period _,Cash and cash equivalents (< 3 months) as shown on the balance sheet 2,627 6,060, Available-for-sale securities (> 3 months) from continuing operations at the end of the period 9,855 9,247, Liquid funds as shown on the balance sheet 12,482 15,307

Interim Report III/2006

29