UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SOLICITATION/RECOMMENDATION STATEMENT UNDER

SECTION 14(d)(4) OF THE SECURITIES EXCHANGE ACT OF 1934

ENDESA, S.A.

(Name of Subject Company)

ENDESA, S.A.

(Name of Person Filing Statement) |

Ordinary shares, nominal value €1.20 each

American Depositary Shares, each representing the right to receive one ordinary share

(Title of Class of Securities)

00029274F1

(CUSIP Number of Class of Securities) |

Álvaro Pérez de Lema

Authorized Representative of Endesa, S.A.

410 Park Avenue, Suite 410

New York, NY 10022

(212) 750-7200

(Name, address and telephone number of person

authorized to receive notices and communications on

behalf of the person filing statement) |

With a Copy to:

Joseph B. Frumkin

Sergio J. Galvis

Richard A. Pollack

Angel L. Saad

Sullivan & Cromwell LLP

125 Broad Street

New York, NY 10004

(212) 558-4000 |

S Check the box if the filing relates solely to preliminary communications made before the commencement of a tender offer.

| IMPORTANT LEGAL INFORMATION |

This document has been made available to shareholders of Endesa, S.A. (the "Company" or "Endesa"). Investors are urged to read Endesa’s Solicitation/Recommendation Statement on Schedule 14D-9, which will be filed by the Company with the U.S. Securities and Exchange Commission (the "SEC”), as it contains important information. The Solicitation/Recommendation Statement and other public filings made from time to time by the Company with the SEC will be available without charge from the SEC's website at www.sec.gov and at the Company’s principal executive offices in Madrid, Spain.

Statements in this document other than factual or historical information are “forward-looking statements”. Forward-looking statements regarding Endesa’s anticipated financial and operating results and statistics are not guarantees of future performance and are subject to material risks, uncertainties, changes and other factors which may be beyond Endesa’s control or may be difficult to predict. No assurances can be given that the forward-looking statements in this document will be realized.

Forward-looking statements may include, but are not limited to, statements regarding: (1) estimated future earnings; (2) anticipated increases in wind and CCGTs generation and market share; (3) expected increases in demand for gas and gas sourcing; (4) management strategy and goals; (5) estimated cost reductions and increased efficiency; (6) anticipated developments affecting tariffs, pricing structures and other regulatory matters; (7) anticipated growth in Italy, France and elsewhere in Europe; (8) estimated capital expenditures and other investments; (9) expected asset disposals; (10) estimated increases in capacity and output and changes in capacity mix; (11) repowering of capacity; and (12) macroeconomic conditions.

The following important factors, in addition to those discussed elsewhere in this document, could cause actual financial and operating results and statistics to differ materially from those expressed in our forward-looking statements:

- Economic and Industry Conditions: Materially adverse changes in economic or industry conditions generally or in our markets; the effect of existing regulations and regulatory changes; tariff reductions; the impact of any fluctuations in interest rates; the impact of fluctuations in exchange rates; natural disasters; the impact of more stringent environmental regulations and the inherent environmental risks relating to our business operations; and the potential liabilities relating to our nuclear facilities.

- Transaction or Commercial Factors: Any delays in or failure to obtain necessary regulatory, antitrust and other approvals for our proposed acquisitions or asset disposals, or any conditions imposed in connection with such approvals; our ability to integrate acquired businesses successfully; the challenges inherent in diverting management's focus and resources from other strategic opportunities and from operational matters during the process of integrating acquired businesses; the outcome of any negotiations with partners and governments; any delays in or failure to obtain necessary regulatory approvals (including environmental) to construct new facilities or repower or enhance our existing facilities; shortages or changes in the price of equipment, materials or labor; opposition of political and ethnic groups; adverse changes in the political and regulatory environment in the countries where we and our related companies operate; adverse weather conditions, which may delay the completion of power plants or substations, or natural disasters, accidents or other unforeseen events; and the inability to obtain financing at rates that are satisfactory to us.

- Political/Governmental Factors: Political conditions in Latin America and changes in Spanish, European and foreign laws, regulations and taxes.

- Operating Factors: Technical difficulties; changes in operating conditions and costs; the ability to

| | | implement cost reduction plans; the ability to maintain a stable supply of coal, fuel and gas and the impact of fluctuations on fuel and gas prices; acquisitions or restructurings; and the ability to implement an international and diversification strategy successfully. |

| | Ÿ | Competitive Factors: the actions of competitors; changes in competition and pricing environments; and the entry of new competitors in our markets. |

Further information about the reasons why actual results and developments may differ materially from the expectations disclosed or implied by our forward-looking statements can be found under “Risk Factors” in our annual report on Form 20-F for the year ended December 31, 2005.

Except as may be required by applicable law, Endesa disclaims any obligation to revise or update any forward-looking statements in this document.

SPAIN AND PORTUGAL Accomplishing Commitments Valencia , 25 June 2007

Spain and Portugal. Accomplishing Commitments Results Business Drivers Deregulated activities Regulated activities Efficiency improvement Regulation 1

Spain and Portugal. Accomplishing Commitments Results 2006 Results 1Q 07 Results Track record and forecast results Business Drivers Deregulated activities Regulated activities Efficiency improvement Regulation 2

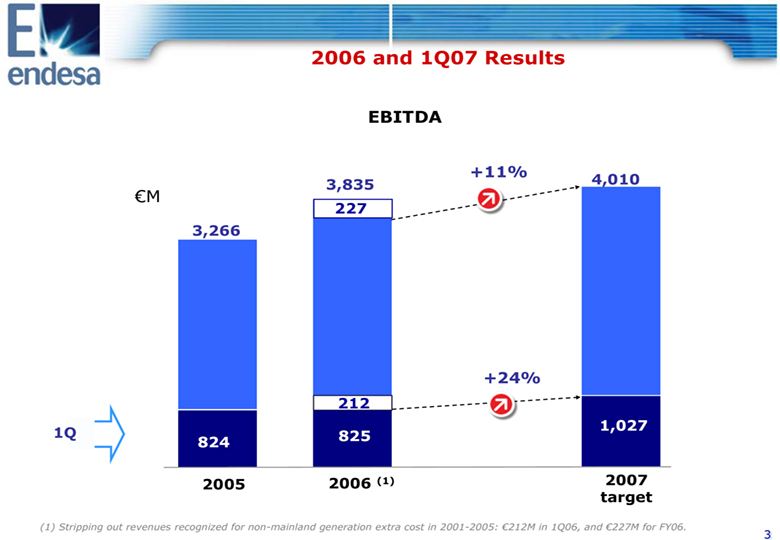

2006 and 1Q07 Results EBITDA +11% 4,010 3,835 (euro)M 227 3,266 +24% 212 1,027 1Q 825 824 2005 2006 (1) 2007 target (1) Stripping out revenues recognized for non-mainland generation extra cost in 2001-2005: (euro)212M in 1Q06, and (euro)227M for FY06. 3

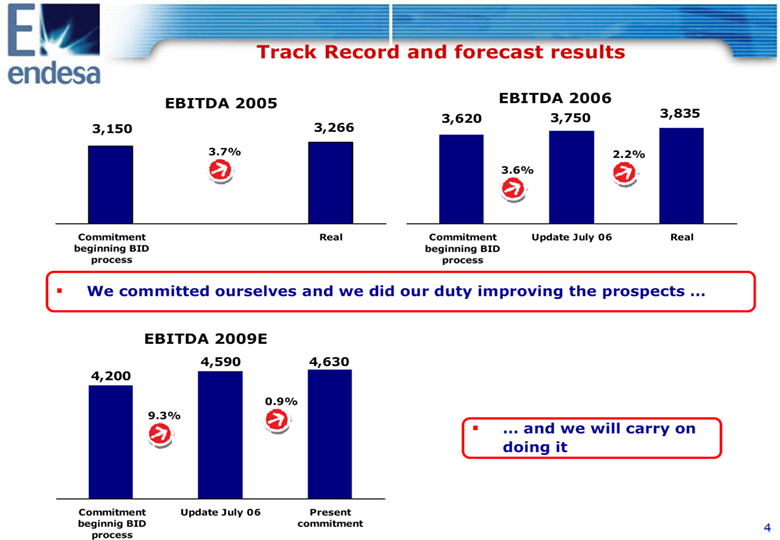

Track Record and forecast results EBITDA 2005 EBITDA 2006 3,620 3,750 3,835 3,150 3,266 3.7% 2.2% 3.6% Commitment Real Commitment Update July 06 Real beginning BID beginning BID process process We committed ourselves and we did our duty improving the prospects ... EBITDA 2009E 4,590 4,630 4,200 0.9% 9.3% .... and we will carry on doing it Commitment Update July 06 Present beginnig BID commitment process 4

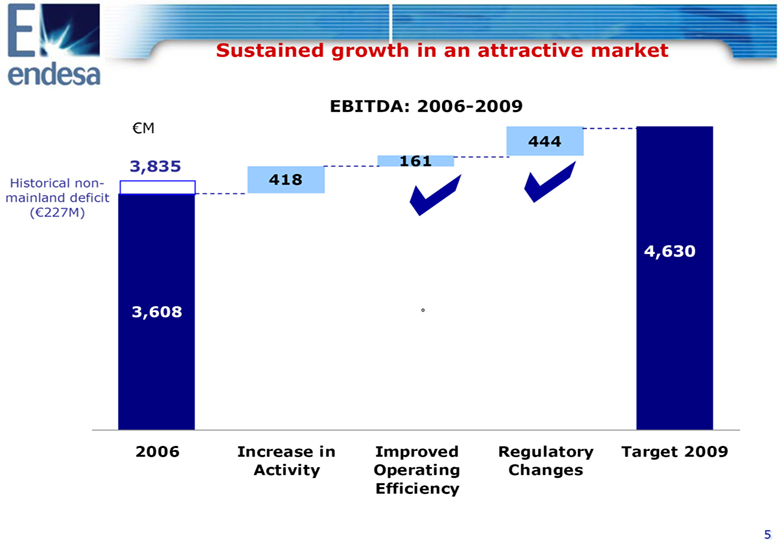

Sustained growth in an attractive market EBITDA: 2006-2009 (euro)M 444 3,835 161 Historical non- 418 mainland deficit ((euro)227M) 4,630 3,608 (0) 2006 Increase in Improved Regulatory Target 2009 Activity Operating Changes Efficiency 5

Spain and Portugal. Accomplishing Commitments Results Business Drivers Business View Deregulated activities Regulated activities Efficiency improvement Regulation 6

Business View of the Strategic Plan Competition Asset portfolio Risk management (balance) Fuel supply Operating efficiency The Customer Versus the regulatory risk Consolidated improvement in supply quality Added-value products and services Regulation Deregulated business subject to market forces Regulated business with sufficient profitability for efficient management Environment More environmentally efficient production and consumption CO2 Under this strategy, Spain and Portugal has successfully met and exceeded demanding targets 7

Spain and Portugal. Accomplishing commitments Results Business Drivers Deregulated activities Business chain management Revenues enhancement Customers portfolio Selective and profitable commercial policy Mainland fuel cost CDM management Regulated activities Efficiency improvement Regulation 8

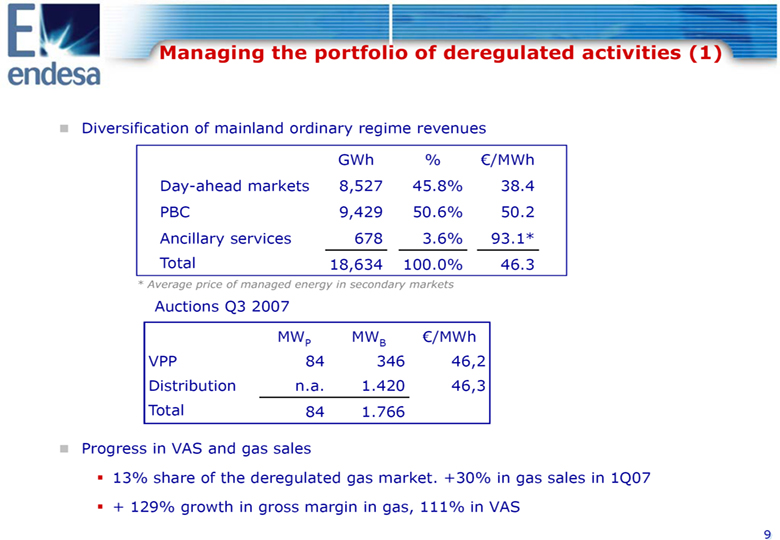

Managing the portfolio of deregulated activities (1) Diversification of mainland ordinary regime revenues GWh % (euro)/MWh Day-ahead markets 8,527 45.8% 38.4 PBC9,429 50.6% 50.2 Ancillary services 678 3.6% 93.1* Total 18,634 100.0% 46.3 * Average price of managed energy in secondary markets Auctions Q3 2007 (euro)/MWh MWP MWB VPP 84346 46,2 Distribution n.a. 1.420 46,3 Total 84 1.766 Progress in VAS and gas sales 13% share of the deregulated gas market. +30% in gas sales in 1Q07 + 129% growth in gross margin in gas, 111% in VAS 9

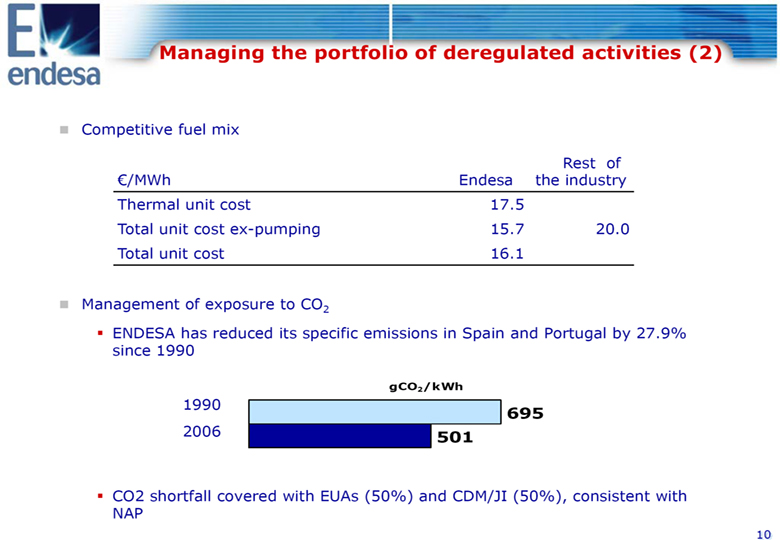

Managing the portfolio of deregulated activities (2) Competitive fuel mix Rest of (euro)/MWh Endesa the industry Thermal unit cost17.5 Total unit cost ex-pumping 15.7 20.0 Total unit cost 16.1 Management of exposure to CO2 ENDESA has reduced its specific emissions in Spain and Portugal by 27.9% since 1990 gCO2/kWh 1990 695 2006 501 CO2 shortfall covered with EUAs (50%) and CDM/JI (50%), consistent with NAP 10

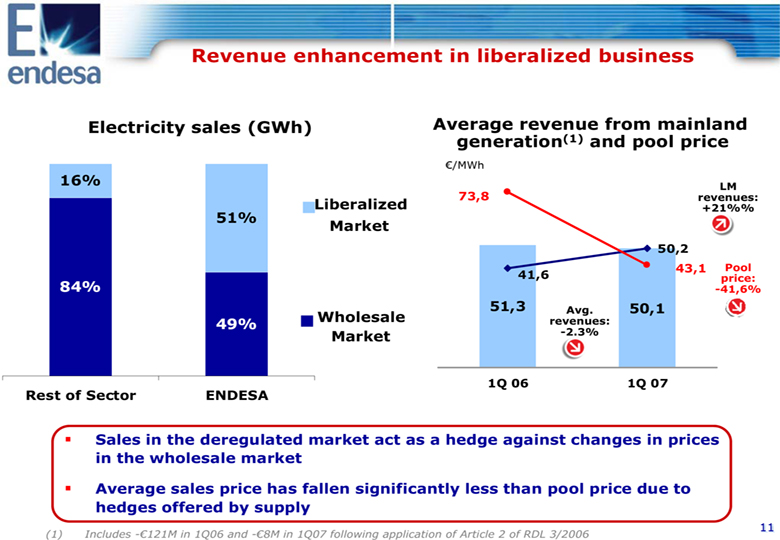

Revenue enhancement in liberalized business Electricity sales (GWh) Average revenue from mainland generation(1) and pool price (euro)/MWh 16% LM 73,8 revenues: Liberalized +21%% 51% Market 50,2 43,1 Pool 41,6 price: 84% -41,6% 51,3 Avg. 50,1 49% Wholesale revenues: Market -2.3% 1Q 06 1Q 07 Rest of Sector ENDESA Sales in the deregulated market act as a hedge against changes in prices in the wholesale market Average sales price has fallen significantly less than pool price due to hedges offered by supply (1) Includes -(euro)121M in 1Q06 and - -(euro)8M in 1Q07 following application of Article 2 of RDL 3/2006 11

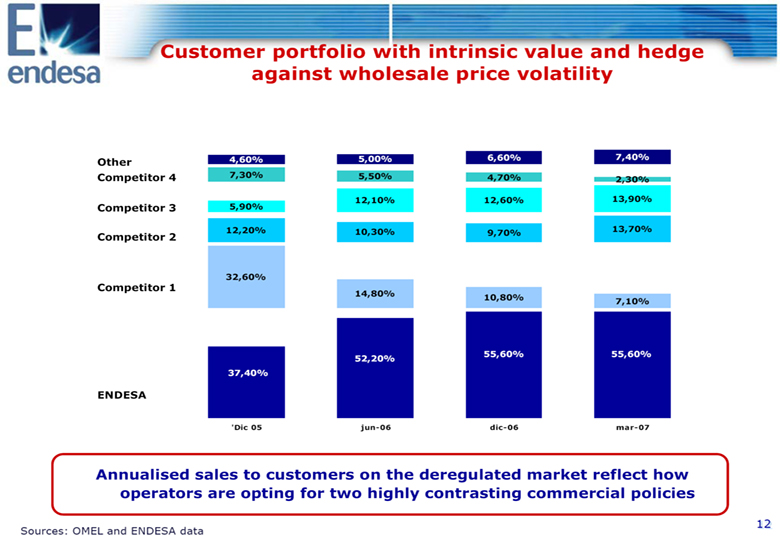

Customer portfolio with intrinsic value and hedge against wholesale price volatility 4,60% 5,00% 6,60% 7,40% Other Competitor 4 7,30% 5,50% 4,70% 2,30% 12,10% 12,60% 13,90% Competitor 3 5,90% 12,20% 10,30% 9,70% 13,70% Competitor 2 32,60% Competitor 1 14,80% 10,80% 7,10% 55,60% 55,60% 52,20% 37,40% ENDESA 'Dic 05 jun-06 dic-06 mar-07 Annualised sales to customers on the deregulated market reflect how operators are opting for two highly contrasting commercial policies Sources: OMEL and ENDESA data 12

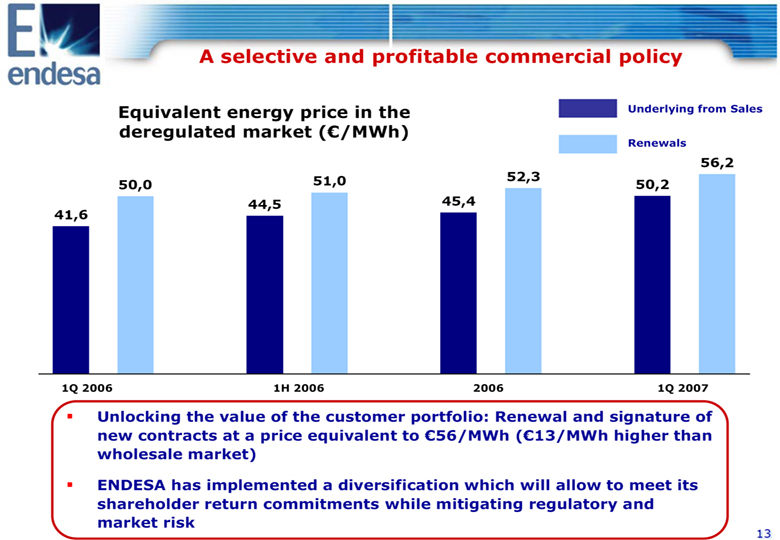

A selective and profitable commercial policy Equivalent energy price in the Underlying from Sales deregulated market ((euro)/MWh) Renewals 56,2 51,0 52,3 50,0 50,2 44,5 45,4 41,6 1Q 2006 1H 2006 2006 1Q 2007 Unlocking the value of the customer portfolio: Renewal and signature of new contracts at a price equivalent to (euro)56/MWh ((euro)13/MWh higher than wholesale market) ENDESA has implemented a diversification which will allow to meet its shareholder return commitments while mitigating regulatory and market risk 13

Competitive mainland fuel costs thanks to efficient use of generation portfolio Cost of mainland fuel Load factor of thermal in O.R. plants(1) vs. rest of the sector (euro)/MWh -3.1% 65.8% 16.2 49.5% 15.7 ENDESA 1Q06 ENDESA 1Q07 ENDESA Rest of the sector Even in a scenario with high rainfall, ENDESA still boasts the most competitive and efficient generation business in the sector Fuel prices have decreased on account of higher hydro and nuclear output (1) Conventional thermal facilities excluding fuel-oil 14

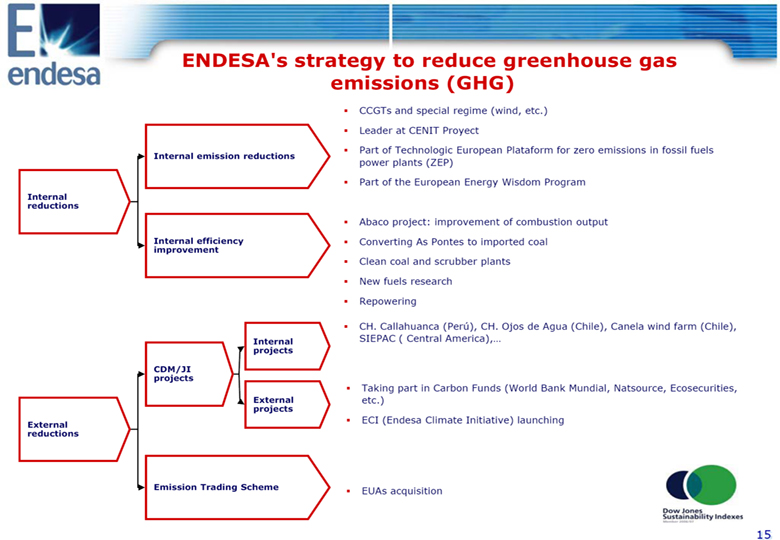

ENDESA's strategy to reduce greenhouse gas emissions (GHG) CCGTs and special regime (wind, etc.) Leader at CENIT Proyect Part of Technologic European Plataform for zero emissions in fossil fuels Internal emission reductions power plants (ZEP) Part of the European Energy Wisdom Program Internal reductions Abaco project: improvement of combustion output Internal efficiency Converting As Pontes to imported coal improvement Clean coal and scrubber plants New fuels research Repowering CH. Callahuanca (Peru), CH. Ojos de Agua (Chile), Canela wind farm (Chile), Internal SIEPAC ( Central America),... projects CDM/JI projects Taking part in Carbon Funds (World Bank Mundial, Natsource, Ecosecurities, External etc.) projects External ECI (Endesa Climate Initiative) launching reductions Emission Trading Scheme EUAs acquisition 15

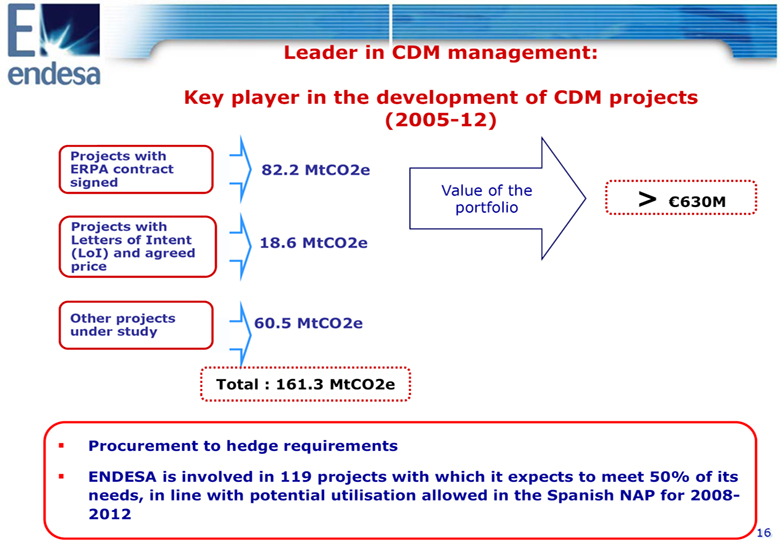

Leader in CDM management: Key player in the development of CDM projects (2005-12) Projects with ERPA contract 82.2 MtCO2e signed Value of the > portfolio (euro)630M Projects with Letters of Intent 18.6 MtCO2e (LoI) and agreed price Other projects 60.5 MtCO2e under study Total : 161.3 MtCO2e Procurement to hedge requirements ENDESA is involved in 119 projects with which it expects to meet 50% of its needs, in line with potential utilisation allowed in the Spanish NAP for 2008-2012 16

Spain and Portugal. Accomplishing Commitments Results Business Drivers Deregulated activities Regulated activities Efficient management of regulated services and profitability Distribution: EBITDA's strong growth and ... ... quality of supply Non-mainland: retribution adaptation Renewables/CHP Efficiency improvement Regulation 17

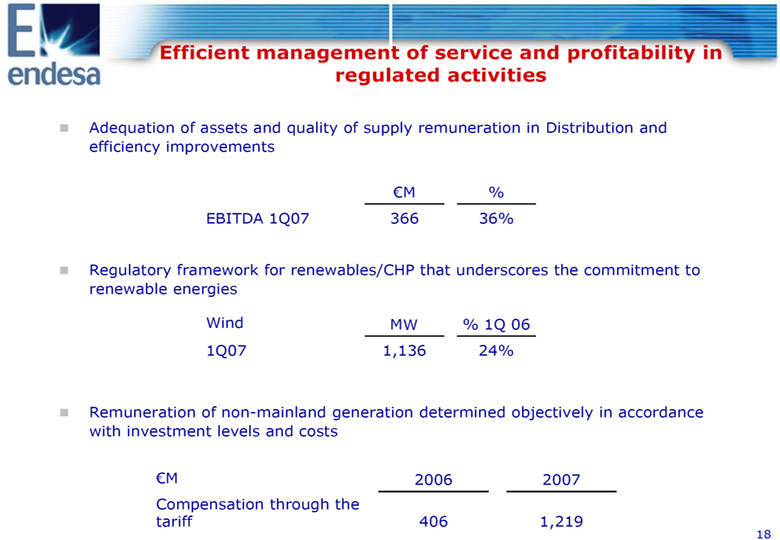

Efficient management of service and profitability in regulated activities Adequation of assets and quality of supply remuneration in Distribution and efficiency improvements (euro)M % EBITDA 1Q07 366 36% Regulatory framework for renewables/CHP that underscores the commitment to renewable energies Wind (euro)M % 1Q 06 1Q07 1,136 24% Remuneration of non-mainland generation determined objectively in accordance with investment levels and costs (euro)M 2006 2007 Compensation through the tariff 406 1,219 18

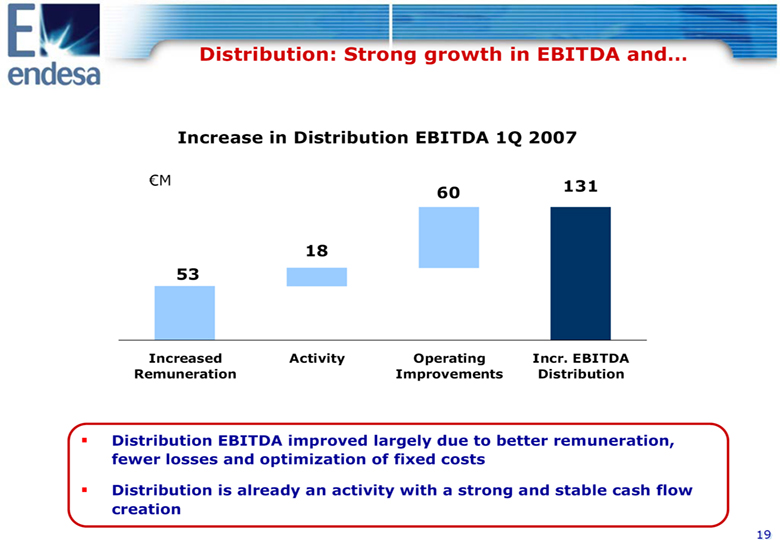

Distribution: Strong growth in EBITDA and... Increase in Distribution EBITDA 1Q 2007 (euro)M 131 60 18 53 Increased Activity Operating Incr. EBITDA Remuneration Improvements Distribution Distribution EBITDA improved largely due to better remuneration, fewer losses and optimization of fixed costs Distribution is already an activity with a strong and stable cash flow creation 19

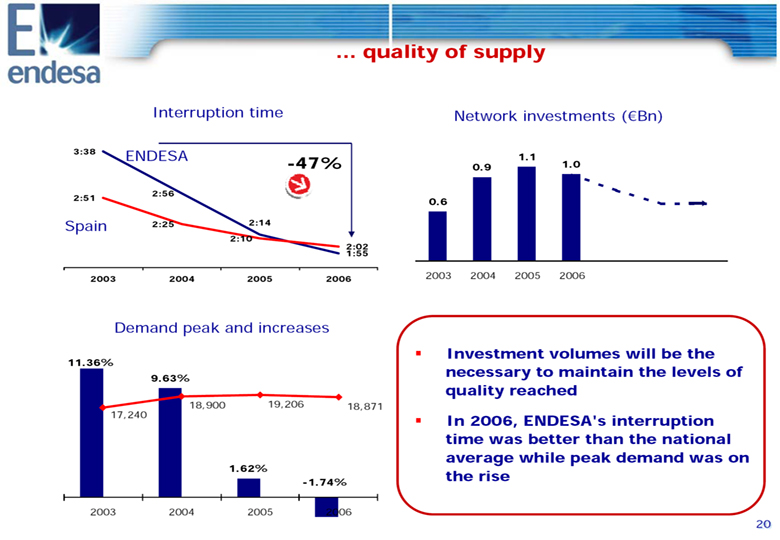

.... quality of supply Interruption time Network investments ((euro)Bn) 3:38 ENDESA 1.1 -47% 0.9 1.0 2:56 2:51 0.6 Spain 2:25 2:14 2:10 2:02 1:55 2003 2004 2005 2006 2003 2004 2005 2006 Demand peak and increases Investment volumes will be the 11.36% 9.63% necessary to maintain the levels of quality reached 18,900 19,206 18,871 17,240 In 2006, ENDESA's interruption time was better than the national average while peak demand was 1.62% -1.74% on the rise 2003 2004 2005 2006 20

Regulatory framework and stable remuneration for non-mainland electricity systems since 2006 Remuneration of investment, operating & maintenance and fuel costs Ministerial Orders developing rules for Recognition of right to review costs for non-mainland systems 2001-2005: published in - Shortfall recorded (*): (euro)887Mn March 2006 2006: (euro)562Mn of pending shortfall This provides these Since 2007 methodology included in Ministerial systems with a stable Orders is applied and adequate to their - 1st year including costs derived from the MO in characteristics the electricity tariff. (euro) 1,219 Mn compensation in tariff regulatory framework Shortfall = 0 - Rules for the settlement and payment guarantees system pending approval oPreliminary estimates up to 2006 in accordance with the second transitory provision of Regulation ITC/914/2006 of 30 March, which establishes the method for calculating the remuneration for guarantee of capacity of generation facilities in the mainland and non-mainland ordinary regimes. Includes financial updating. 21

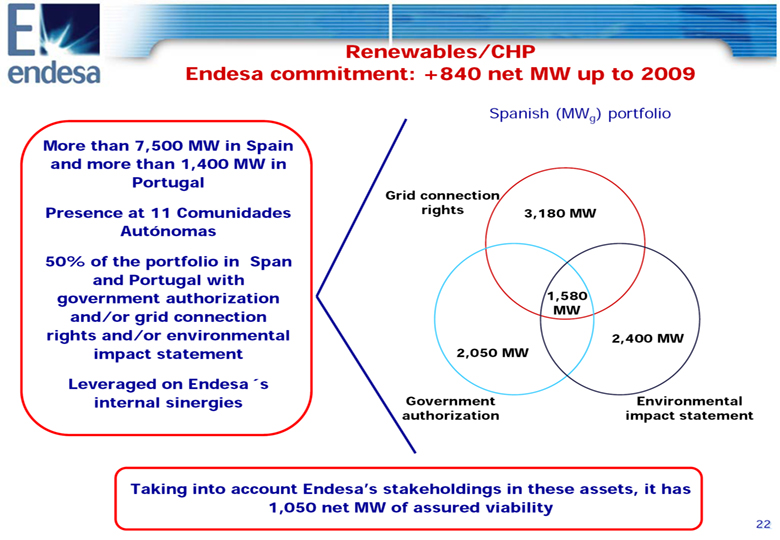

Renewables/CHP Endesa commitment: +840 net MW up to 2009 Spanish (MWg) portfolio More than 7,500 MW in Spain and more than 1,400 MW in Portugal Grid connection Presence at 11 Comunidades rights 3,180 MW Autonomas 50% of the portfolio in Span and Portugal with government authorization 1,580 MW and/or grid connection rights and/or environmental 2,400 MW impact statement 2,050 MW Leveraged on Endesa's internal sinergies Government Environmental authorization impact statement Taking into account Endesa's stakeholdings in these assets, it has 1,050 net MW of assured viability 22

Spain and Portugal. Accomplishing Commitments Results Business Drivers Deregulated activities Regulated activities Efficiency improvement Regulation 23

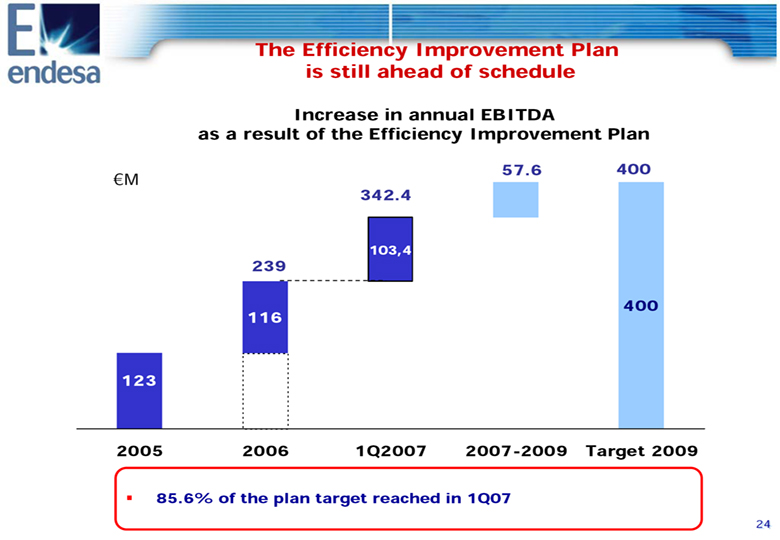

The Efficiency Improvement Plan is still ahead of schedule Increase in annual EBITDA as a result of the Efficiency Improvement Plan 57.6 400 (euro)M 342.4 103,4 239 400 116 123 2005 2006 1Q2007 2007-2009 Target 2009 85.6% of the plan target reached in 1Q07 24

Spain and Portugal. Accomplishing Commitments Results Business Drivers Deregulated activities Regulated activities Efficiency improvement Regulation 25

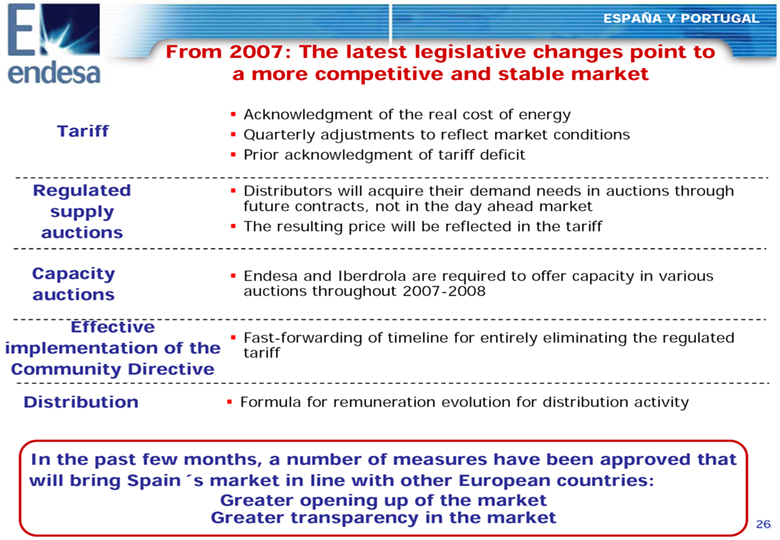

ESPANA Y PORTUGAL From 2007: The latest legislative changes point to a more competitive and stable market Acknowledgment of the real cost of energy Tariff Quarterly adjustments to reflect market conditions Prior acknowledgment of tariff deficit Regulated Distributors will acquire their demand needs in auctions through supply future contracts, not in the day ahead market auctions The resulting price will be reflected in the tariff Capacity Endesa and Iberdrola are required to offer capacity in various auctions auctions throughout 2007-2008 Effective Fast-forwarding of timeline for entirely eliminating the regulated implementation of the tariff Community Directive Distribution Formula for remuneration evolution for distribution activity In the past few months, a number of measures have been approved that will bring Spain's market in line with other European countries: Greater opening up of the market Greater transparency in the market 26

Conclusion We have a commitment 4.630 (euro)M EBITDA in 2009 Business View of the Strategic Plan Spain and Competition Asset portfolio Risk management (balance) Fuel supply Portugal Operating efficiency The Customer We know what Regulatory risks Consolidated improvement in supply quality we have to do Value-added products and services Regulation Liberalized activities placed on the market Regulated activities with sufficient revenues for efficient management Accomplishing Environment More efficient production and consumption from an environmental standpoint CO2 Commitments Under this strategy, ENDESA's Business in Spain and Portugal has successfully met and exceeded several demanding targets 7 3.835 4.010 3.266 17% We are doing it 24% 1.027 2005 2006 2007 27

Legal Information This document was made available to shareholders of Endesa, S.A.. In relation with the announced joint offer by ENEL SpA and Acciona, S.A., Endesa shareholders are urged to read the report of Endesa's board of directors when it is filed by the Company with the Comision Nacional del Mercado de Valores (the "CNMV"), as well as Endesa's Solicitation/Recommendation Statement on Schedule 14D-9 when it is filed by the Company with the U.S. Securities and Exchange Commission (the "SEC"), as it will contain important information. Such documents and other public filings made from time to time by Endesa with the CNMV or the SEC are available without charge from the Endesa's website at www.endesa.es, from the the CNMV's website at www.cnmv.es and from the SEC's website at www.sec.gov and at Endesa's principal executive offices in Madrid, Spain. This presentation contains certain "forward-looking" statements regarding anticipated financial and operating results and statistics and other future events. These statements are not guarantees of future performance and they are subject to material risks, uncertainties, changes and other factors that may be beyond ENDESA's control or may be difficult to predict. Forward-looking statements include, but are not limited to, information regarding: estimated future earnings; anticipated increases in wind and CCGTs generation and market share; expected increases in demand for gas and gas sourcing; management strategy and goals; estimated cost reductions; tariffs and pricing structure; estimated capital expenditures and other investments; estimated asset disposals; estimated increases in capacity and output and changes in capacity mix; repowering of capacity and macroeconomic conditions. For example, the investment plan for 2007-2009 included in this presentation are forward-looking statements and are based on certain assumptions which may or may not prove correct. The main assumptions on which these expectations and targets are based are related to the regulatory setting, exchange rates, divestments, increases in production and installed capacity in markets where ENDESA operates, increases in demand in these markets, assigning of production amongst different technologies, increases in costs associated with higher activity that do not exceed certain limits, electricity prices not below certain levels, the cost of CCGT plants, and the availability and cost of the gas, coal, fuel oil and emission rights necessary to run our business at the desired levels. In these statements we avail ourselves of the protection provided by the Private Securities Litigation Reform Act of 1995 of the United States of America with respect to forward-looking statements. The following important factors, in addition to those discussed elsewhere in this presentation, could cause actual financial and operating results and statistics to differ materially from those expressed in our forward-looking statements: Economic and industry conditions: significant adverse changes in the conditions of the industry, the general economy or our markets; the effect of the prevailing regulations or changes in them; tariff reductions; the impact of interest rate fluctuations; the impact of exchange rate fluctuations; natural disasters; the impact of more restrictive environmental regulations and the environmental risks inherent to our activity; potential liabilities relating to our nuclear facilities. Transaction or commercial factors: any delays in or failure to obtain necessary regulatory, antitrust and other approvals for our proposed acquisitions or asset disposals, or any conditions imposed in connection with such approvals; our ability to integrate acquired businesses successfully; the challenges inherent in diverting management's focus and resources from other strategic opportunities and from operational matters during the process of integrating acquired businesses; the outcome of any negotiations with partners and governments. Delays in or impossibility of obtaining the pertinent permits and rezoning orders in relation to real estate assets. Delays in or impossibility of obtaining regulatory authorisation, including that related to the environment, for the construction of new facilities, repowering or improvement of existing facilities; shortage of or changes in the price of equipment, material or labour; opposition of political or ethnic groups; adverse changes of a political or regulatory nature in the countries where we or our companies operate; adverse weather conditions, natural disasters, accidents or other unforeseen events, and the impossibility of obtaining financing at what we consider satisfactory interest rates. Political/governmental factors: political conditions in Latin America; changes in Spanish, European and foreign laws, regulations and taxes. Operating factors: technical problems; changes in operating conditions and costs; capacity to execute cost-reduction plans; capacity to maintain a stable supply of coal, fuel and gas and the impact of the price fluctuations of coal, fuel and gas; acquisitions or restructuring; capacity to successfully execute a strategy of internationalisation and diversification. Competitive factors: the actions of competitors; changes in competition and pricing environments; the entry of new competitors in our markets. Further details on the factors that may cause actual results and other developments to differ significantly from the expectations implied or explicitly contained in the presentation are given in the Risk Factors section of Form 20-F filed with the SEC and in the ENDESA Share Registration Statement filed with the Comision Nacional del Mercado de Valores (the Spanish securities regulator or the "CNMV" for its initials in Spanish).No assurance can be given that the forward-looking statements in this document will be realised. Except as may be required by applicable law, neither Endesa nor any of its affiliates intends to update these forward-looking statements. 28

SPAIN AND PORTUGAL Accomplishing Commitments Valencia , 25 June 2007