Table of Contents

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

Filed by the registrant x

Filed by a party other than the registrant ¨

Check the appropriate box:

¨ | Preliminary proxy statement | ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14-a6(e)(2)) | |||

x | Definitive proxy statement | |||||

¨ | Definitive additional materials | |||||

¨ | Soliciting material under Rule 14a-12 |

Global Crossing Limited

(Name of Registrant as specified in its Charter)

Payment of filing fee (Check the appropriate box):

x | No fee required. | |||

¨ | Fee computed on table below per Exchange Act Rule 14a-6(i)(4), and 0-11. | |||

(1) | Title of each class of securities to which transaction applies: | |||

(2) | Aggregate number of securities to which transactions applies: | |||

(3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): | |||

(4) | Proposed maximum aggregate value of transaction: | |||

(5) | Total fee paid: | |||

¨ | Fee paid previously with preliminary materials. | |||

¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | |||

(1) | Amount previously paid: | |||

(2) | Form, schedule or registration statement no.: | |||

(3) | Filing party: | |||

(4) | Date filed: | |||

Table of Contents

2005 PROXY STATEMENT AND 2004 ANNUAL REPORT

TABLE OF CONTENTS

I. CEO LETTER | I-1 | |||||

II. MEETING NOTICES | II-1 | |||||

III. 2005 PROXY STATEMENT | ||||||

| III-1 | ||||||

| III-4 | ||||||

| III-13 | ||||||

| III-17 | ||||||

| III-18 | ||||||

| III-19 | ||||||

Proposal No. 1—Amendment of 2003 Global Crossing Limited Stock Incentive Plan | III-20 | |||||

| III-28 | ||||||

| III-30 | ||||||

| III-41 | ||||||

| III-42 | ||||||

| Delivery of Documents to Shareholders Sharing an Address | III-42 | |||||

| Incorporation by Reference | III-42 | |||||

| III-43 | ||||||

IV. 2004 ANNUAL REPORT | ||||||

| IV-1 | ||||||

| IV-1 | ||||||

| IV-2 | ||||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | IV-4 | |||||

| IV-45 | ||||||

| IV-46 | ||||||

| IV-47 | ||||||

| IV-49 | ||||||

| IV-111 | ||||||

| IV-112 | ||||||

Table of Contents

A Letter From John Legere

To Our Shareholders,

2004 was a year in which Global Crossing took decisive actions to adapt to a rapidly changing marketplace, and provided solid proof that we are building the value of your investment through steady execution of our strategy to provide enterprises with global Internet Protocol (IP) solutions.

In the past year, management successfully attained several critical goals that provided a solid foundation for our business. Our current business plan became fully funded as a result of the recapitalization plan we completed on December 23, 2004, and we ended the year with $365 million in unrestricted cash. This recapitalization plan included the issuance of high-yield bonds by our Global Crossing United Kingdom (GCUK) business, as well as the refinancing of debt held by Singapore Technologies Telemedia (ST Telemedia), our majority investor, into a new security that will convert into common equity within four years. ST Telemedia’s strategic and financial support in 2004 was invaluable in helping our company achieve its improved financial position.

From all indications, enterprise demand for IP services will continue to grow—and we believe the value of our seamless global network will grow in parallel as we continue our strategic focus.

Our go-to-market strategy is now focused more sharply on providing enterprises with global IP services, and includes three categories of business. First is the “Invest and Grow” category, on which our strategy is focused and where we believe we have differentiated capabilities. Second is the “Manage for Margin” category, including the wholesale voice business, which we have restructured and will continue to manage to increase its profitability. Finally, the “Harvest or Exit” category is comprised of areas of the business that are not core to our strategy going forward.

The “Invest and Grow” category includes the channels servicing global enterprises, conferencing and carrier data customers, and new indirect channels focused on providing IP services to enterprise and government end users. These core businesses grew in 2004, with the greatest improvements coming from IP-based services such as IP VPN, IP video, conferencing and managed services. This growth occurred despite significant challenges during the year, including the restatement of our 2003 financials and perceived uncertainties regarding the company’s liquidity. We expect these “Invest and Grow” businesses to continue growing at a healthy pace in 2005.

Throughout the year, we secured a number of new contracts with customers including BorgWarner, DHL, and Varig Airlines. All these customers are global enterprises that require globally available services such as converged IP solutions, managed services and conferencing. This trend of customer wins has continued into the first quarter of 2005 with such notable sales as our $100 million, seven-year contract to provide the British Council with a managed IP VPN connecting 7,000 users at 260 sites in 110 countries—exactly the kind of customer need our capabilities were built to serve. Additionally, in 2004 we signed master services agreements with partners such as Telmex, Allstream, New World Telecom, and Sify—agreements that are key to our indirect distribution strategy. By taking advantage of our Fast-TrackTM Services offering to provide converged IP solutions to their end-users, these new partners have reduced their time to market, expanded their reach beyond their home geographies, and broadened their product offerings to their enterprise customers.

The “Manage for Margin” or global wholesale voice business is one that historically has contributed significantly to Global Crossing’s top-line revenue. The telecommunications industry continued to experience significant price erosion in 2004, and as a result, last year we took decisive actions to successfully restructure our legacy wholesale voice business and improve its financial contribution. We did this by initiating more than 700 pricing actions in the fourth quarter with both our international and also our domestic long distance wholesale customers, and these pricing actions accounted for the majority of our revenue declines in 2004. As we continue

I-1

Table of Contents

to manage this business very tightly, we expect to see improved gross margins and cash flow, even as our strategic customer focus and related product and pricing actions result in a reduction in revenues.

Our “Harvest or Exit” business category includes the Small Business Group (SBG), Trader Voice (TV) and consumer businesses. On March 21, 2005, we announced a definitive agreement to sell SBG to Matrix Telecom, a Platinum Equity company, for $35 million in anticipated net cash proceeds. We expect to close the transaction in the third quarter of 2005. On March 25, 2005, we announced the sale of Trader Voice to WestCom Corporation, a One Equity Partners company, for $22 million in anticipated net cash proceeds. That transaction is expected to close in the second quarter of 2005. The sale of these businesses is key to the execution of Global Crossing’s business plan and will offer the customers associated with these businesses the opportunity to receive support from companies that specialize in their niche markets.

We have created a smaller, more focused company that is driving its results toward cash-flow break even in the second half of 2006. As part of this effort we resized our workforce, resulting in the elimination of approximately 450 positions in the fourth quarter of 2004 and annual operating expense savings of approximately $38 million.

Revenue for 2004 totaled approximately $2.5 billion, a decline of 10 percent from 2003, but accompanied by an improvement of more than 200 basis points in gross margin percentages year over year, to 30 percent for all of 2004. This planned revenue decline reflects the company’s focus on its core enterprise business and on improving margins. During the fourth quarter, when we began executing our wholesale voice pricing actions, we improved gross margins to 36 percent. We have shifted the mix of our customer base and the trajectory is in line with our enterprise strategy, with 38 percent of fourth quarter revenues in the enterprise sector, 55 percent in carrier, and 7 percent in the non-core businesses. For comparison purposes, our customer revenue for enterprise, carrier and non-core businesses in 2003 was 30 percent, 62 percent and 8 percent, respectively. Additionally, we shifted our product mix toward higher margins and “sticky” revenues, with 46 percent of 2004 revenues associated with data, IP, conferencing and managed services, 47 percent with wholesale voice and 7 percent with non-core products. This was a strong improvement from 2003, when we ended the year with revenues of 38 percent, 54 percent and 8 percent in those categories, respectively.

IP services are the core of Global Crossing’s strategy, and in 2004 we increased IP traffic by more than 30 percent. We transported more than 29 billion minutes of traffic over our Voice over IP (VoIP) backbone, constituting nearly 50 percent of our total voice traffic, and we continued to operate our network at industry leading levels of better than “five nines” (99.999 percent) reliability.

From our regular satisfaction surveys and other contacts with customers, we know that the enterprises in our target markets put increasing levels of value on flawless execution, responsive performance and problem solving, timely and accurate billing, and competent, knowledgeable support teams that are attentive to their needs. This is precisely the type of service our employees around the world provide, and they continue to be a major factor in customers’ decisions to do business with us.

Telecommunications is one of the most dynamic industries in the world, subject to rapid technological change and shifts in market structure, with the recent announcements regarding the proposed acquisitions of AT&T by SBC and MCI by Verizon or Qwest being the latest examples. The process of integrating such large companies often has a negative impact on the customer experience, so Global Crossing will focus on meeting the needs of customers affected by these acquisitions in a superior manner.

In conclusion, Global Crossing ended 2004 with a fully funded business. We have a unique set of global network assets, and we have focused our business on areas where we have differentiated capabilities in providing converged IP solutions, on a global basis, to enterprises and the carriers that serve them. In the fourth quarter of 2004, we delivered the first evidence that we are successfully executing our more focused strategy, resulting in

I-2

Table of Contents

improved financial performance. We appreciate your support as we continue to deliver on the promise of a company whose vision appears more prescient with each new turn our industry takes. And we look forward to the opportunity to discuss with you at our Annual General Meeting of Shareholders in New York City on June 14, 2005 our results, and our future plans to maximize the value of your investment.

John Legere

CEO

Global Crossing

I-3

Table of Contents

April 26, 2005

Dear Shareholder:

The Board of Directors cordially invites you to attend the 2005 Annual General Meeting of Shareholders, which we will hold at 10:00 a.m., Eastern Daylight Time, on June 14, 2005 at the Swissôtel The Drake, 440 Park Avenue, New York, New York.

The Notice of 2005 Annual General Meeting and Proxy Statement accompanying this letter describe the business to be acted upon at the meeting. The annual report for the year ended December 31, 2004 is also enclosed.

It is important that your shares be represented at the Annual General Meeting, whether or not you plan to attend the meeting in person. Please complete, sign and date the enclosed proxy card and return it in the accompanying prepaid envelope to ensure that your shares will be represented at the meeting.

Thank you for your continued support.

LODEWIJK CHRISTIAAN VAN WACHEM

Chairman of the Board of Directors

II-1

Table of Contents

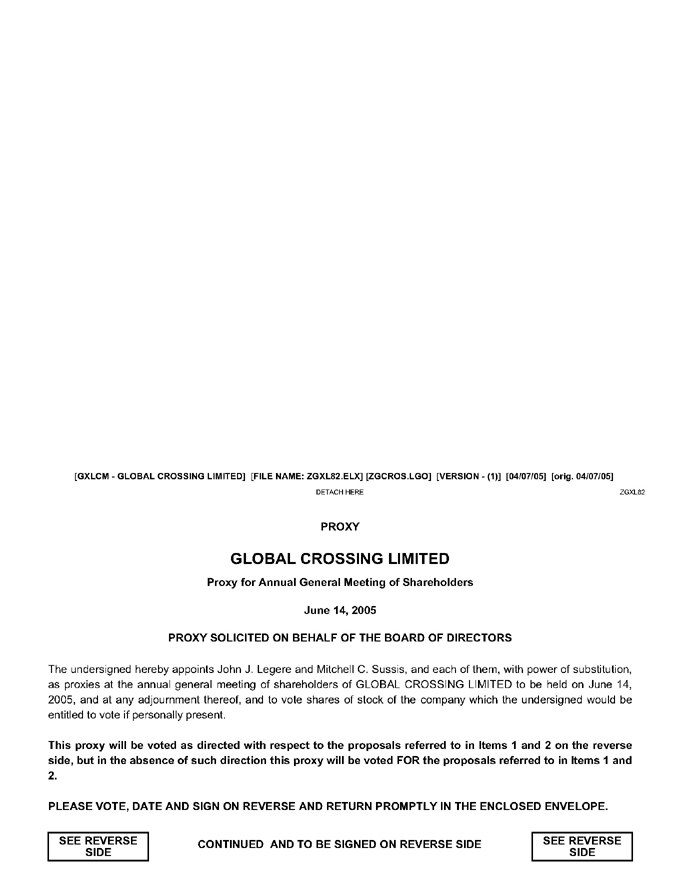

Notice of 2005 Annual General Meeting of Shareholders

We will hold the 2005 Annual General Meeting of Shareholders (the “annual meeting”) of Global Crossing Limited (“Global Crossing”) at the Swissôtel The Drake, 440 Park Avenue, New York, New York, on June 14, 2005, at 10:00 a.m., Eastern Daylight Time, for the following purposes:

To receive the report of the independent registered public accounting firm of Global Crossing and the financial statements for the year ended December 31, 2004 and to take the following actions:

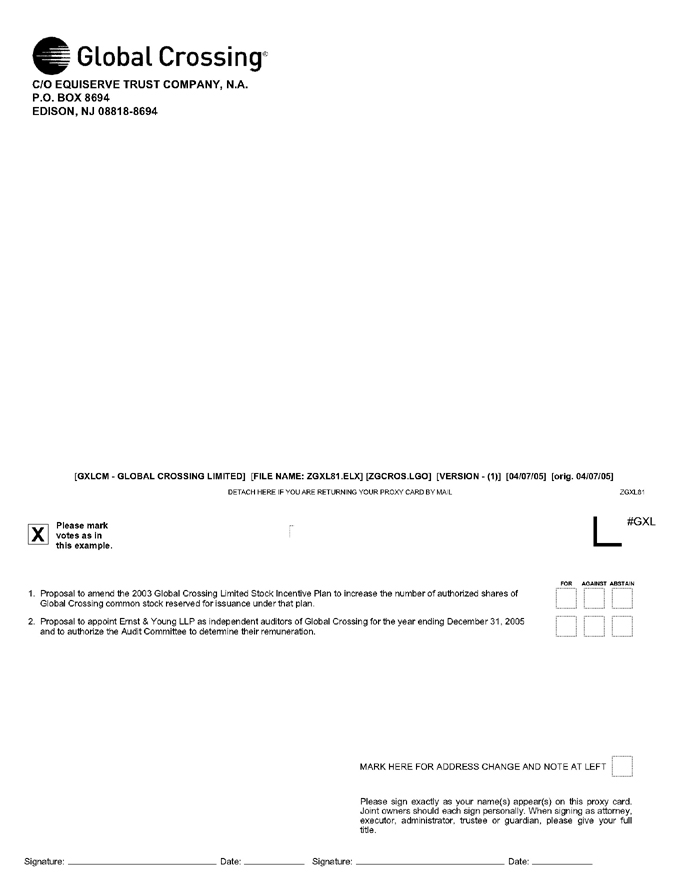

| 1. | To consider and act upon a proposal to amend the 2003 Global Crossing Limited Stock Incentive Plan, to increase the number of authorized shares of Global Crossing common stock reserved for issuance under that plan; |

| 2. | To appoint Ernst & Young LLP as the independent registered public accounting firm of Global Crossing for the year ending December 31, 2005 and to authorize the Audit Committee to determine their remuneration; and |

| 3. | To transact any other business that may properly come before the annual meeting and any adjournment or postponement of the meeting. |

Only common and preferred shareholders of record at the close of business on April 18, 2005, which has been fixed as the record date for notice of the annual meeting, are entitled to receive this notice and to vote at the meeting.

It is important that your shares be represented at the annual meeting. Whether or not you expect to attend the meeting, please vote by completing, signing and dating the enclosed proxy card and returning it promptly in the reply envelope provided.

By order of the Board of Directors,

MITCHELL C. SUSSIS

Secretary, Vice President & Deputy General Counsel

April 26, 2005

II-2

Table of Contents

2005 PROXY STATEMENT

The Board of Directors of Global Crossing Limited is soliciting your proxy for use at the Annual General Meeting of Shareholders to be held on June 14, 2005 (the “annual meeting”). These proxy materials are being mailed to shareholders beginning on or about April 26, 2005.

Global Crossing Limited, or “New GCL,” was formed under the laws of Bermuda in 2002. On January 28, 2002, Global Crossing Ltd., a company formed under the laws of Bermuda in 1997 (“Old GCL”), and a number of its subsidiaries commenced cases under chapter 11 of title 11 of the United States Code in the United States Bankruptcy Court for the Southern District of New York. December 9, 2003 was the effective date for the joint plan of reorganization of Old GCL and such subsidiaries (the “Effective Date”). On that date, Old GCL transferred substantially all of its assets to New GCL. New GCL thereby became the parent company of the Global Crossing consolidated group of companies and succeeded to Old GCL’s reporting obligations under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Except as otherwise noted herein, references in this proxy statement to “Global Crossing,” “the Company,” “we,” “our” and “us” in respect of time periods on or prior to December 9, 2003 are references to Old GCL and its subsidiaries, while such references in respect of time periods after December 9, 2003 are references to New GCL and its subsidiaries. Pursuant to our plan of reorganization, on the Effective Date a subsidiary of Singapore Technologies Telemedia Pte Ltd (“ST Telemedia”, together with its subsidiaries, the “STT Shareholder Group”) invested $250 million in cash in exchange for a 61.5% equity interest in New GCL consisting of 6,600,000 common shares and 18,000,000 preferred shares.

Our principal executive offices are located at Wessex House, 45 Reid Street, Hamilton HM12, Bermuda. Our telephone number is 441-296-8600. You may visit us at our website located atwww.globalcrossing.com.

Date, Time and Place

We will hold the Annual General Meeting at the Swissôtel The Drake, 440 Park Avenue, New York, New York, on June 14, 2005 at 10:00 a.m., Eastern Daylight Time, subject to any adjournments or postponements.

Who Can Vote; Votes Per Share

Common and preferred shareholders of record at the close of business on April 18, 2005 are eligible to vote at the annual meeting. As of the close of business on that date, we had outstanding 22,494,783 shares of common stock par value U.S. $.01 per share, and 18,000,000 shares of 2.0% Cumulative Senior Convertible Preferred Shares (the “Senior Preferred Shares”) par value U.S. $.10 per share. All of the Senior Preferred Shares and 6,600,000 common shares are currently held by a subsidiary of ST Telemedia. The Senior Preferred Shares are convertible into common shares on a one-for-one basis, subject to adjustment in certain circumstances.

Under our bye-laws and the certificate of designations for the Senior Preferred Shares, each common share and each Senior Preferred Share currently entitles the holder to one vote on all matters entitled to be voted on by holders of our common shares, with the Senior Preferred Shares and the common shares voting together as a single class. Each common share and each Senior Preferred Share will therefore be entitled to one vote on each proposal described in this proxy statement. Although the holders of the common and Senior Preferred Shares also have certain separate class voting rights under Bermuda law, no separate class vote will take place at the 2005 annual meeting.

III-1

Table of Contents

Quorum and Voting Requirements

The presence in person or by proxy of at least two shareholders entitled to vote and holding shares representing more than 50 percent of the votes of all outstanding common shares and Senior Preferred Shares will constitute a quorum at the annual meeting. Abstentions and broker “non-votes” are counted for purposes of establishing a quorum. A broker “non-vote” occurs when a nominee (such as a broker) holding shares for a beneficial owner does not vote on a particular proposal because the nominee does not have discretionary voting power for that particular matter and has not received instructions from the beneficial owner.

Approval of each of the proposals set out below requires the affirmative vote of at least a simple majority of the votes cast. Abstentions and broker “non-votes” will not affect the voting results, although they will have the practical effect of reducing the number of affirmative votes required to achieve a majority by reducing the total number of shares from which the majority is calculated. Approval of Proposal No. 1 (regarding the 2003 Global Crossing Limited Stock Incentive Plan) additionally requires that a majority of the outstanding shares on April 18, 2005 actually cast votes on the matter. Abstentions and broker “non-votes”, if any, will have the practical effect of reducing the likelihood that this requirement will be satisfied.

How to Vote

If your shares are held in the name of a bank, broker or other holder of record, you will receive instructions from the holder of record that you must follow in order for your shares to be voted. If you are the shareholder of record, you may either vote in person at the meeting or by proxy. All common shares represented by a proxy that is properly executed by the shareholder of record and received by our transfer agent, EquiServe Trust Company N.A. (“Equiserve”), by 9:00 a.m., Eastern Daylight Time, on June 14, 2005, will be voted as specified in the proxy, unless validly revoked as described below. To vote by mail, please sign, date and mail your proxy card in the envelope provided. If you return a proxy by mail and do not specify your vote, your shares will be voted as recommended by the Board of Directors.

As an alternative to appointing a proxy, a shareholder that is a corporation may appoint any person to act as its representative by delivering written evidence of that appointment, which must be received at our principal executive offices not later than one hour before the time fixed for the beginning of the meeting. A representative so appointed may exercise the same powers, including voting rights, as the appointing corporation could exercise if it were an individual shareholder.

The Board of Directors is not currently aware of any business that will be brought before the annual meeting other than the proposals described in this proxy statement. If, however, other matters are properly brought before the annual meeting or any adjournment or postponement of the meeting, the persons appointed as proxies will have discretionary authority to vote the shares represented by duly executed proxies in accordance with their discretion and judgment.

Revocation of Proxies

You may revoke your proxy or, in the case of a corporation, its authorization of a representative, at any time before it is voted (1) by so notifying the Secretary of the Company in writing at the address of our principal executive offices not less than one hour before the time fixed for the beginning of the meeting, (2) by signing and dating a new and different proxy card or (3) by voting your shares in person or by an appointed agent or representative at the meeting. You cannot revoke your proxy merely by attending the annual meeting.

Proxy Solicitation

We will bear the costs of soliciting proxies from the holders of our common shares. Proxies will initially be solicited by us by mail, but directors, officers and selected other employees of the Company may also solicit

III-2

Table of Contents

proxies by personal interview, telephone, facsimile or e-mail. Directors, executive officers and any other employees who solicit proxies will not be specially compensated for those services, but may be reimbursed for out-of-pocket expenses incurred in connection with the solicitation. Brokerage houses, nominees, fiduciaries and other custodians will be requested to forward soliciting materials to beneficial owners and will be reimbursed for their reasonable out-of-pocket expenses incurred in sending proxy materials to beneficial owners. We have engaged Georgeson Shareholder Communications, Inc. to assist us in coordinating the mailing of proxy materials at an estimated fee of $5,000 plus disbursements. Equiserve has agreed to assist us in connection with the tabulation of proxies.

2004 Audited Financial Statements

Under our bye-laws and Bermuda law, audited financial statements must be presented to shareholders at an annual general meeting of shareholders. To fulfill this requirement, we will present at the annual meeting consolidated financial statements for the fiscal year 2004, which have been audited by Ernst & Young LLP. Copies of those financial statements are included in our 2004 Annual Report to Shareholders (the “Annual Report”), which is attached to this proxy statement. Representatives of Ernst & Young LLP have been invited to attend the annual meeting and to respond to appropriate questions and will have the opportunity to make a statement should they so desire.

III-3

Table of Contents

DIRECTORS AND EXECUTIVE OFFICERS

As New GCL emerged from bankruptcy on December 9, 2003, the terms of office of our current directors do not expire until, at the earliest, December 9, 2005 (unless certain circumstances occur as hereinafter described). Therefore, the agenda for the annual meeting does not include the election of directors. However, for informational purposes, we are including in this Proxy Statement the following important information regarding our directors and executive officers.

Our board of directors consists of ten members, all of whom assumed their positions as directors and committee members upon our emergence from bankruptcy. Eight members were appointed by STT Crossing Ltd., our majority shareholder (“STT Crossing”), which is a subsidiary of ST Telemedia. In this Proxy Statement, references to the “STT Shareholder Group” mean ST Telemedia and any of its subsidiaries that are shareholders of the Company from time to time. The remaining two members of the board were appointed by the Creditors Committee (the “Creditors Committee”) in our bankruptcy proceedings. Each director appointed by the STT Shareholder Group has a term of three years unless earlier removed by the STT Shareholder Group. The directors appointed by the Creditors Committee will serve as directors until the second anniversary of our emergence from bankruptcy, December 9, 2005.

Our bye-laws provide that the STT Shareholder Group will be able to appoint up to eight (8) directors to our board based upon the STT Shareholder Group’s percentage ownership of our shares at any given time. This right of the STT Shareholder Group to designate directors is summarized as follows:

| a. | For so long as the STT Shareholder Group owns both Global Crossing common stock and Global Crossing Senior Preferred Shares representing in the aggregate not less than 50 percent of our outstanding common stock calculated on a fully diluted basis, the STT Shareholder Group will be entitled to appoint eight directors to our board, holding office at any one time, each for a term of three years (which can be renewed). |

| b. | If the STT Shareholder Group owns both Global Crossing common shares and Global Crossing Senior Preferred Shares representing in the aggregate less than 50 percent, but not less than 35 percent, of our outstanding common shares calculated on a fully diluted basis, the STT Shareholder Group will be entitled to appoint six directors to our board, holding office at any one time, each for a term of three years (which can be renewed). |

| c. | If the STT Shareholder Group owns both Global Crossing common shares and Global Crossing Senior Preferred Shares representing in the aggregate less than 35 percent, but not less than 20 percent, of our outstanding common shares calculated on a fully diluted basis, the members of the STT Shareholder Group will be entitled to appoint four directors to our board, holding office at any one time, each for a term of three years (which can be renewed). |

| d. | If the STT Shareholder Group owns both Global Crossing common shares and Global Crossing Senior Preferred Shares representing in the aggregate less than 20 percent of our outstanding common shares calculated on a fully diluted basis, but not less than the lesser of (x) 5 percent of our outstanding common shares calculated on a fully diluted basis and (y) 50 percent of the number of our common shares (calculated on an as-converted basis) acquired by the members of the STT Shareholder Group in the aggregate, the members of the STT Shareholder Group shall be entitled to appoint two directors to our board, holding office at any one time, each for a term of three years (which can be renewed). |

| e. | For so long as the STT Shareholder Group is entitled to appoint at least two directors, a director designated by the STT Shareholder Group shall serve as (i) Chairman of the Board, (ii) Chairman of the Audit Committee (to the extent permitted by applicable stock exchange rules), (iii) Chairman of the Compensation Committee, (iv) Chairman of the Executive Committee and (v) Chairman of the Nominating and Corporate Governance Committee. |

If the share ownership percentage of the STT Shareholder Group at any time falls below one of the thresholds specified above, then the term of office of the number of directors that the STT Shareholder Group is no longer entitled to appoint shall terminate at the following meeting of Shareholders (whether annual or special).

III-4

Table of Contents

Our bye-laws also provide that if a Creditors Committee director resigns (or is otherwise unable to serve) during the initial two year term, the other Creditors Committee director appoints his replacement for the balance of the two year term. If both Creditors Committee directors resign (or are otherwise unable to serve) during the initial two year term, the “alternate director” (if any) previously designated by either such Creditors Committee director will serve out the rest of that director’s two year term. If both Creditors Committee directors resign (or are otherwise unable to serve) during the initial two year term and an alternate had not been appointed, then the estate representative (which is handling the remaining affairs of Old GCL) has the right to designate their replacement(s) for the balance of the two year term. After the initial two year terms, the estate representative’s (successor-in-interest to the Creditors’ Committee) rights to appoint and replace these two directors ends and they are subject to election by majority shareholder vote.

The following table sets forth the names, ages and positions of our directors, Executive Committee members and executive officers. Additional biographical information concerning these individuals is provided in the text following the table. The directors’ committee assignments are also set forth below, with the committees further discussed below under “Board Meetings and Committees.”

Name | Age | Position | ||

Lodewijk Christiaan van Wachem | 73 | Chairman of the Board of Directors5 | ||

Peter Seah Lim Huat | 58 | Vice Chairman of the Board of Directors4 | ||

E.C. “Pete” Aldridge, Jr. | 66 | Director1, 2, 3 | ||

Archie Clemins | 61 | Director2, 5 | ||

Donald L. Cromer | 69 | Director2, 4 | ||

Richard R. Erkeneff | 69 | Director2, 3 | ||

Lee Theng Kiat | 52 | Director1, 4, 5 | ||

Charles Macaluso | 61 | Director1 | ||

Michael Rescoe | 52 | Director3 | ||

Robert J. Sachs | 56 | Director4, 5 | ||

Steven T. Clontz | 54 | Member of Executive Committee | ||

Jeremiah D. Lambert | 70 | Member of Executive Committee | ||

John J. Legere | 46 | Chief Executive Officer1 | ||

David Carey | 51 | Executive Vice President, Strategy and Corporate Development | ||

Anthony D. Christie | 44 | Executive Vice President and Chief Marketing Officer | ||

Daniel J. Enright | 45 | Executive Vice President, Global Operations | ||

Paul A. O’Brien | 52 | Executive Vice President, Global Enterprise and Collaboration Services | ||

Edward T. Higase | 38 | Executive Vice President, Worldwide Carrier Services | ||

William I. Lees, Jr. | 46 | Senior Vice President, Accounting and Financial Operations | ||

Jean F.H.P. Mandeville | 45 | Executive Vice President and Chief Financial Officer | ||

John B. McShane | 43 | Executive Vice President and General Counsel | ||

Philip Metcalf | 46 | Managing Director, Global Crossing UK | ||

John R. Mulhearn, Jr. | 54 | Senior Vice President, Global Wholesale Voice and Access Management | ||

José Antonio Ríos | 59 | Chief Administrative Officer, President of Global Crossing International and Chairman of the Board of Global Crossing UK | ||

Gerald B. Santos | 61 | Senior Vice President, Corporate Communications | ||

Daniel J. Wagner | 40 | Chief Information Officer and Executive Vice President, Business Infrastructure |

| 1 | Member, Executive Committee |

| 2 | Member, Government Security Committee |

| 3 | Member, Audit Committee |

| 4 | Member, Compensation Committee |

| 5 | Member, Nominating and Corporate Governance Committee |

III-5

Table of Contents

Directors of the Company

Lodewijk Christiaan van Wachem—Mr. Van Wachem has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2006. He is currently a member of the board of directors of ATCO (Canada) Ltd. (energy, logistics) and of the executive board of Rand Europe (policy think tank). He was chairman of the board of directors of Zurich Financial Services from 1993 through April 2005 and was chairman of the supervisory board of Royal Philips Electronics N.V. from 1993 through March 2005. He became a director of Royal Dutch Shell Group in 1977, president in 1982 and chairman of the committee of managing directors in 1985. He served in that capacity until 1992, when he was appointed chairman of the supervisory board of the Royal Dutch Petroleum Company, a position he held through July 2002. Until 2002 he also served on the supervisory boards of Akzo Nobel, BMW and Bayer as well as on the board of directors of International Business Machines Corp.

Peter Seah Lim Huat—Mr. Seah has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2006. Since January 2005 he has been a member of the Temasek Advisory Panel of Temasek Holdings (Pte) Ltd (investment company) and Deputy Chairman on ST Telemedia’s Board of Directors. From December 2001 until December 2004 he was president and chief executive officer of Singapore Technologies Pte Ltd (former Temasek holding company for technology and communications investments) (“ST”) and also a member of its board of directors. Before joining ST in December 2001, he was a banker for the prior 33 years, retiring as vice chairman & chief executive officer of Overseas Union Bank in September 2001. Mr. Seah is chairman and, since February 2005, interim chief executive officer of SembCorp Industries (engineering) and Singapore Technologies Engineering. Presently, he also sits on the boards of CapitaLand Limited, Chartered Semiconductor Manufacturing Ltd, StarHub Pte. Ltd. and ST Assembly Test Services in the ST Group. Mr. Seah also serves on the boards of the Government of Singapore Investment Corporation, EDB Investments Pte Ltd, PT Indonesian Satellite Corporation Tbk and Siam Commercial Bank Public Company Limited. His other appointments include being a member of the Economic Review Committee’s Sub-committee on Policies Related to Taxation, the CPF System, Wages and Land. He is also the vice president of the Singapore Chinese Chamber of Commerce & Industry and the honorary treasurer of Singapore Business Federation Council.

E.C. “Pete” Aldridge, Jr.—Mr. Aldridge has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2006. He currently serves on the boards of Lockheed Martin Corporation (systems integrator, information technology) and Alion Science and Technology Corporation (technology). From May 2001 until May 2003, Mr. Aldridge served as Under Secretary of Defense for Acquisition, Technology, and Logistics. In this position, he was responsible for all matters relating to U.S. Department of Defense acquisition, research and development, advanced technology, international programs, and the industrial base. Prior to this appointment, Mr. Aldridge served as chief executive officer of Aerospace Corporation from March 1992 through May 2001; president of McDonnell Douglas Electronic Systems from December 1988 through March 1992; and Secretary of the Air Force from June 1986 through December 1998. Mr. Aldridge has also held numerous other senior positions within the Department of Defense.

Archie Clemins—Mr. Clemins has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2006. He has been, since January 2000, the owner and president of Caribou Technologies, Inc., and, since November 2001, co-owner of TableRock International LLC, both international consulting firms, and concentrates on the transition of commercial technology to the government sectors, both in the United States and Asia. In addition to serving on the boards of other technology and venture capital concerns, including Extended Systems, Mr. Clemins is the vice chairman of Advanced Electron Beams, Inc., which focuses on low energy electron beam technology, and vice chairman of Positron Systems, Inc., a company whose intellectual property determines the fatigue levels of metals. As an officer of the United States Navy from 1966 through December 1999, Mr. Clemins’ active duty service included tours on several attack submarines and command of the USS Pogy. Promoted to Flag (General Officer) rank in 1991, he had five follow-on assignments, including Commander, Pacific Fleet Training Command in San Diego, California and Commander, Seventh Fleet, headquartered in Yokosuka, Japan. Mr. Clemins concluded his military career in Hawaii as an Admiral and the 28th Commander of the U. S. Pacific Fleet.

III-6

Table of Contents

Donald L. Cromer—Mr. Cromer has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2006. He currently acts as a consultant to the U.S. Department of Defense, the United States Air Force and the following companies: The Boeing Company, Booz Allen Hamilton Inc. (a strategy and technology consulting firm) and the Institute for Defense Analysis. He has been a trustee of Aerospace Corporation since January 2002 and a board member of Draper Laboratory, Inc. (a not-for-profit laboratory for applied research, engineering development, education, and technology transfer). He also serves on the boards of the following private companies: Universal Space Network, Vadium, Inc., and Innovative Intelcom Industries. He is also affiliated with the California Space Authority and serves as a member of Aeronautics and Space Engineering Board of the National Research Council. General Cromer’s military career in the Air Force spanned 32 years. He retired in 1991 as the Commander of Space Division, Los Angeles, CA (the satellite, missile and launch vehicle acquisition center for the Air Force). Subsequent to his retirement, he joined Hughes Space and Communications Company and served as president from 1993 to 1998.

Richard R. Erkeneff—Mr. Erkeneff has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2006. He was, from October 1995 until August 2003, president and chief executive officer of United Industrial Corporation (“UIC”), a company focused on the design and production of defense, training, transportation and energy systems. Mr. Erkeneff has also served as a director of UIC since October 1995. In addition, Mr. Erkeneff was chief executive officer of AAI Corporation (“AAI”), a wholly-owned subsidiary of UIC responsible for the design, manufacture, testing and support of advanced Tactical Unmanned Aerial Vehicles, from November 1993 until August 2003, and president of AAI from November 1993 to January 2003. Prior to joining AAI, Mr. Erkeneff held positions as senior vice president of the Aerospace Group at McDonnell Douglas Corporation, and president and executive vice president of McDonnell Douglas Electronics Systems Company. Mr. Erkeneff’s directorship at UIC will expire on May 24, 2005, after which he is expected to become a consultant to UIC’s board of directors.

Lee Theng Kiat—Mr. Lee has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2006. He has been president and chief executive officer of ST Telemedia since 1994. He joined ST in 1985 and has held various senior ST positions including directorships in Legal and Strategic Business Development. In 1993, following ST’s decision to enter the telecommunications sector, Mr. Lee spearheaded the creation of ST Telemedia as a new business area for ST. Mr. Lee, a lawyer by training, began his career as an officer of the Singapore Legal Service, remaining with that entity for more than eight years. Mr. Lee also serves on the boards of the PT Indonesian Satellite Corporation Tbk and Equinix, Inc.

Charles Macaluso—Mr. Macaluso has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2005. He is a founding principal and the chief executive officer of Dorchester Capital Advisors (formerly East Ridge Consulting, Inc.), a management consulting and corporate advisory firm founded in 1996. From March 1996 to June 1998, Mr. Macaluso was a partner at Miller Associates, Inc., a company principally involved in corporate workouts. From 1989 to 1996, Mr. Macaluso was a partner at The Airlie Group, LLP, a fund specializing in leveraged buyout, mezzanine and equity investments. Mr. Macaluso currently serves as chairman of the board of Lazy Days, RV, is the lead director of Darling International and Geo Specialty Chemical and a member of the audit committee of O’Sullivan Industries. He also serves on the board of directors of RBX Industries.

Michael Rescoe—Mr. Rescoe has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2005. He is executive vice president and chief financial officer of the Tennessee Valley Authority (the “TVA”), a federal corporation that is the nation’s largest public power provider, a position he has held since July 2003. Mr. Rescoe was a senior officer and the chief financial officer of 3Com Corporation, a global technology manufacturing company specializing in Internet connection technology for both voice and data applications, from April 2000 until November 2002. During 1999 and 2000, Mr. Rescoe was associated with Forstman Little, a leveraged buyout firm. Prior thereto, Mr. Rescoe was chief financial officer of PG&E Corporation, a power and natural gas energy holding company, since 1997. For over a dozen years prior to that Mr. Rescoe was a senior investment banker with Kidder, Peabody and a senior managing director of Bear Stearns specializing in strategy and structured financing.

III-7

Table of Contents

Robert J. Sachs—Mr. Sachs has served as a director of Global Crossing since December 2003 with his term set to expire on December 9, 2006. He has been a principal of Continental Consulting Group, LLC, a Boston, Massachusetts based consulting firm serving the cable television industry, since February 2005, having previously held that same position from January 1998 through July 1999. From August 1999 through February 2005, Mr. Sachs was president and chief executive officer of the National Cable & Telecommunications Association (NCTA), the principal trade association of the cable industry in the United States, representing cable television operators, program services, and equipment and service providers. Prior to co-founding Continental Consulting Group in 1998, Mr. Sachs served in various legal and executive capacities for Continental Cablevision, Inc. and its successor, MediaOne, for 18 years. Mr. Sachs serves as a trustee of the Dana-Farber Cancer Institute and the Wang Center for the Performing Arts and is vice-chair of the national Coalition for Cancer Survivorship.

Executive Committee Members

Steven T. Clontz—Mr. Clontz has served as a member of the Executive Committee of Global Crossing since December 2003 and is president, chief executive officer of Starhub Pte. Ltd. (“Starhub”) (communications), having joined Starhub in that capacity in January 1999. Mr. Clontz has also served as a director of Starhub since 1999. From December 1995 through December 1998, Mr. Clontz served as chief executive officer, president and a director of IPC Information Systems, based in New York City. Prior to that, Mr. Clontz worked at BellSouth International, joining in 1987 and holding senior executive positions of increasing responsibility, serving the last three years as president Asia-Pacific. Mr. Clontz currently serves as a director of Interdigital Communications Corporation. Mr. Clontz began his career as an engineer with Southern Bell in 1973.

Jeremiah D. Lambert—Mr. Lambert has served as a member of the Executive Committee of Global Crossing since December 2003 and served Old GCL as co-chairman of the Board, chaired its audit committee and special committee on accounting matters, and also served as a member of Old GCL’s compensation committee until December 2003. A Global Crossing director since April 2002, Mr. Lambert served as chairman of the board of directors of Old GCL’s former subsidiary, Asia Global Crossing, Ltd. (“Asia Global Crossing”), from September 2002 through March 2003. Mr. Lambert is a nationally known lawyer whose practice has focused on corporate clients in regulated industries, including those in the electricity, natural gas and telecom sectors. Mr. Lambert served as a senior partner in Shook, Hardy & Bacon L.L.P. from December 1997 until April 2002, when he withdrew to join Old GCL’s board of directors. Prior to that date, Mr. Lambert was the co-founder and chair of Peabody, Lambert & Meyers, P.C., a law firm in Washington, D.C. Mr. Lambert began his legal practice at Cravath, Swaine & Moore in New York City and is a frequent lecturer and author on legal topics.

John J. Legere—Mr. Legere has been chief executive officer of Global Crossing since October 2001 and has served as a member of the Executive Committee of the board since December 2003. He also served as a director of Old GCL from October 2001 through December 2003. He served as president and chief executive officer of Asia Global Crossing from February 2000 until January 2002. Mr. Legere has two decades of experience in the telecommunications industry. Prior to joining Asia Global Crossing, he was senior vice president of Dell Computer Corporation and president for Dell’s operations in Europe, the Middle East and Africa from July 1999 until February 2000, and president, Asia-Pacific for Dell from June 1998 until June 1999. From April 1994 to November 1997, Mr. Legere was president and chief executive officer of AT&T Asia/Pacific and spent time also as head of AT&T Global Strategy and Business Development. From 1997 to 1998, he was president of worldwide outsourcing at AT&T Solutions.

Other Executive Officers of the Company

David R. Carey—Mr. Carey was named executive vice president, strategy and corporate development of Global Crossing in November 2003. From March 2002 through November 2003, Mr. Carey served as executive vice president, enterprise sales, where he was responsible for overseeing all sales and marketing activities relating to our enterprise customers. From September 1999 through March 2002, Mr. Carey served in numerous capacities at Global Crossing, including senior vice president-operations planning from January 2002 through

III-8

Table of Contents

March 2002; senior vice president-network planning and development, from December 2000 through January 2002; senior vice president-business and network development from January 2000 through December 2000; and senior vice president-business development from September 1999 through January 2000. Before joining Global Crossing, Mr. Carey served as senior vice president, marketing and chief marketing officer for Frontier Corporation’s business lines from October 1997 through September 1999. Prior to that, Mr. Carey spent seven years in the energy industry, serving as president & chief executive officer of LG&E Natural Inc., a subsidiary of LG&E Energy Corp. based in Louisville, Kentucky. Mr. Carey began his career with AT&T. During his 15 years there, he held a wide range of executive positions in marketing, sales, operations and personnel.

Anthony D. Christie—Mr. Christie was named executive vice president and chief marketing officer of Global Crossing in November 2003. From February 2002 through November 2003, Mr. Christie served as senior vice president, global product management, having previously served as senior vice president, business integration and strategic planning from November 2001. Mr. Christie is accountable for global product strategy development, deployment, marketing, and profit and loss for all wholesale and retail products for the Company. Prior to joining Global Crossing, Mr. Christie was vice president, business development and strategic planning for Asia Global Crossing from March 2000 through October 2001. In this position, Mr. Christie was accountable for all business and corporate development, joint venture and mergers and acquisitions activities, as well as overall strategic planning for the company. Prior to joining Asia Global Crossing, Mr. Christie was general manager and network vice president at AT&T Solutions in New York City from November 1999 through March 2000, having also held the position of Global Sales and Operations vice president in AT&T’s outsourcing division from June 1998 through November 1999. From June 1997 through June 1998, Mr. Christie was a Sloan Fellow at MIT. Prior thereto, Mr. Christie held positions in AT&T’s International Operations Division that included an assignment as the regional managing director for the Consumer Markets Division in Asia.

Daniel J. Enright—Mr. Enright was named executive vice president, operations in June 2003. In this role, Mr. Enright is responsible for our network architecture, planning and engineering, customer operations, network operations and field operations. Mr. Enright is also responsible for managing our network capital, operating expenses and third party maintenance expenses. Mr. Enright has held other positions at Global Crossing, including senior vice president—global network engineering and operations from March 2002 through June 2003; vice president—global service operations from June 2001 through March 2002; vice president North America engineering and field operations from July 2000 through June 2001; and vice president—North America network and field operations from April 1999 through July 2000. Mr. Enright joined Global Crossing in 1999 from Frontier Communications Services, where he had served since October 1996 as vice president for network operations and service provisioning. In that role, he led the network operations and service provisioning team during the construction of Frontier’s nationwide fiber-optic network. Prior to Frontier, Mr. Enright held various engineering and operations positions at Highland Telephone and Rochester Telephone.

Edward T. Higase—Mr. Higase has been executive vice president, worldwide carrier services of Global Crossing since September 2004, having previously served as executive vice president, carrier sales and marketing of Global Crossing since January 2002. Since October 2004, Mr. Higase has been responsible for overseeing sales activities for data services related to our carrier, ISP, and ASP customers worldwide. Mr. Higase previously served as president, carrier services for Asia Global Crossing, from August 2000 to December 2001. Prior to Asia Global Crossing, Mr. Higase was corporate director and general manager from November 1999 to August 2000 of the medium-size business Corporate Accounts Division for Dell Computer Corporation in Japan. Prior to this assignment, he served as corporate director, Dell Online for Asia Pacific from August 1998 to November 1999, where he led the growth of Internet-based transactions in the Asia Pacific Region. Mr. Higase began his career with AT&T in Japan. During his nine years with the company, he held a wide range of senior and executive positions in marketing, sales, and business management across AT&T’s business markets division, consumer markets division, outsourcing unit, and the international business unit.

William I. Lees, Jr.—Mr. Lees was named senior vice president, accounting and financial operations of Global Crossing in March 2005. Mr. Lees acts as our principal accounting officer in this position. Previously, he

III-9

Table of Contents

served as senior vice president, corporate controller of Mediacom Communications Corporation (“Mediacom”), a cable television company, from October 2001 through February 2005. Prior thereto, Mr. Lees served as executive vice president and chief financial officer for Regus Business Centre Corp., a multinational real estate services company, from July 1999 to September 2001. Prior thereto, he served as corporate controller and director for Formica Corporation from September 1998 to July 1999, and as chief financial officer for Imperial Schrade Corporation from September 1993 to September 1998. He was previously employed for 13 years by Ernst & Young.

Jean F.H.P. Mandeville—Mr. Mandeville was named executive vice president and chief financial officer of Global Crossing in February 2005. Mr. Mandeville served as a member of our Executive Committee from December 2003 to January 2005. Mr. Mandeville was chief financial officer of ST Telemedia from July 2002 through January 2005. From 1992 to June 2002, Mr. Mandeville served in various capacities at British Telecom PLC, including president of Asia Pacific from July 2000 to June 2002, director of international development Asia Pacific from June 1999 to July 2000 and general manager, special projects from January 1998 to July 1999. Mr. Mandeville also previously served on the board of directors of SmarTone HK and LGT Korea, both public companies.

John B. McShane—Mr. McShane was named executive vice president and general counsel of Global Crossing in March 2002. Mr. McShane oversees and manages all of our legal matters. Mr. McShane joined Global Crossing in February 1999 as our European assistant general counsel where he oversaw and managed legal affairs for the European region, including the buildout of our PEC network. As assistant general counsel he also had responsibility for the oversight of worldwide sales and telecommunications network outsourcing transactions for Global Crossing’s Solutions business unit and major vendor supply agreements. Prior to joining Global Crossing, Mr. McShane spent twelve years at several international law firms, including positions as an associate at Simpson Thacher & Bartlett from 1987 through 1996 and as senior counsel at Shearman and Sterling, Cadwalader, Wickersham & Taft, and Brown & Wood, where his main focus was on representing major commercial banks, financial institutions and corporations in connection with a broad range of their corporate, commercial and financing activities.

Philip Metcalf—Mr. Metcalf became Managing Director of GCUK in October 2004. Previously, he held senior posts with Global Crossing affiliates in the UK and the US, including Global Construction from June 2001 to March 2002, Global Service Delivery and Assurance from April 2002 to August 2002, and Managing Director for Europe from April 2002 to August 2004. Additionally, from September 2002 to August 2004, he was CEO of our former Global Marine subsidiary, which he successfully re-structured and sold to new ownership. Prior to joining Global Crossing, Mr. Metcalf was employed by Stone and Webster Engineering (now part of the Shaw Group), where he worked for eight years in various capacities, including Head of Engineering, Head of IT, Project Manager, and ultimately Operations Director. Mr. Metcalf sits on the Boards of substantially all the Global Crossing legal entities in Europe, including the GCUK Board, and is Head of Security in the UK and Head of Safety in the UK (including chairing the Rail Safety Management Group).

John R. Mulhearn, Jr.—Mr. Mulhearn has served as senior vice president, global wholesale voice and access management for Global Crossing since October 2004. He has global responsibility for the sale and support of wholesale voice products, and in addition, is accountable for securing agreements and managing the cost structure for all global long haul and local access (switched and special) capabilities in support of Global Crossing’s carrier and enterprise customer segments, as well as for network infrastructure requirements. Previously he served as senior vice president of global access management from May 2002 until September 2004, vice president, global access management from March 2002 until May 2002, vice president North America carrier relations from June 2001 through March 2002 and vice president operations from March 2000 through June 2001. Prior to joining Global Crossing, Mr. Mulhearn previously worked for 28 years at AT&T. During his tenure at AT&T, he held positions in sales, marketing, operations, regulatory, outsourcing and human resources. In 1993, he took an assignment in Canada to work for Unitel Communications Inc. (partially owned by AT&T) as senior vice president of sales and marketing. In that role, Mr. Mulhearn was responsible for government, national and regional commercial accounts.

III-10

Table of Contents

Paul A. O’Brien—Mr. O’Brien has been executive vice president, global enterprise and collaboration services since September 2004, having previously served as senior vice president of enterprise sales from November 2003. Mr. O’Brien is responsible for overseeing all sales and support activities related to our enterprise customers worldwide. He also oversees the conferencing services sales force. Mr. O’Brien has more than 20 years of experience in the telecommunications and IT fields. Prior to joining Global Crossing, he founded the Arden Group in October of 2002, an organization that specializes in providing operations expertise to the global technology/IT industry. From April 1998 through October 1999 he served as the vice president and general manager of GTE Internetworking’s IPTelecom startup. He went on to serve as president of GTE Telecom and senior vice president of sales and marketing for GTE-Internetworking from October 1999 to July 2000, where he was a member of the company’s management committee. From July 2000 to April 2002 he was the head of sales for Genuity and President of Genuity Telecom, GTE’s Internetworking spin-off. He has also held executive positions at NCR from January 1995 through April 1998, where he was vice president and general manager of the communications industry business unit; Cincinnati Bell Telephone, where he was vice president of marketing from August 1990 through January 1995; and beforehand at AT&T, where he was the New England area manager. He currently serves as the director of EnvoyWorldWide, which provides real-time interaction management services to deliver time-sensitive notifications, enabling customers to streamline supply chains and ensure business continuity. He has attended Dartmouth College’s Amos Tuck Executive Development Program as well as AT&T’s Executive Development Program.

José Antonio Ríos—Mr. Ríos was named chairman of the board of directors of Global Crossing UK in September 2004 and has been chief administrative officer of Global Crossing since November 2002. Mr. Ríos has also served as president of Global Crossing International since May 2001 and was chairman of the board of Global Crossing’s former Global Marine Systems subsidiary (“Global Marine”) from September 2002 through its divestment in August 2004. Mr. Ríos has more than 20 years of experience managing a wide range of companies in the technology and media sectors. Prior to joining Global Crossing in February 2001 as president Latin America and corporate senior vice president, Mr. Ríos served as president and chief executive officer of Telefónica Media from June 1999 through August 2000 and president of Atento Worldwide from July 2000 through June 2002. Earlier in his career, Mr. Ríos was the founding president and chief executive officer of Galaxy Latin America (subsequently named DIRECTV™ Latin America), where he was responsible for the planning, development, and launch of DIRECTV™, a division of Hughes Electronics. During his four-year tenure, he was a vice president of Hughes Electronics and a member of its management committee. Mr. Ríos previously served as the first chief operating officer and corporate vice president of the Cisneros Group of Companies. He was also a founding member of its worldwide executive committee. During his 13-year tenure with the Cisneros Group, Mr. Ríos held a succession of increasingly responsible positions, including tenure as a board member or president in over 60 Cisneros companies worldwide. From 2000 to 2002, Mr. Ríos served as chairman of the supervisory board of Endemol Entertainment, Europe’s premier independent TV production company based in Holland and with operations in 28 countries around the world. He also serves on the board of directors of Claxson Interactive Group Inc. and is an active national board member of Operation Smile, a philanthropic organization that provides global medical assistance to children born with facial deformities. In addition, Mr. Ríos serves as a board member of the Inter-American Dialogue’s Latin America Advisor.

Gerald B. Santos—Mr. Santos was named senior vice president, corporate communications of Global Crossing in October 2001. He manages all aspects of external and internal communications efforts including public relations, marketing communications, employee communications, advertising and branding. Prior to joining Global Crossing, Mr. Santos was vice president of worldwide public relations and communications with Concert Communications from July 1999 through June 2001. Prior to his role at Concert, Mr. Santos held several senior leadership positions in the communications organization within AT&T, most recently as vice president, global communications for AT&T Asia/Pacific from September 1996 through July 1999.

Daniel J. Wagner—Mr. Wagner was named chief information officer and executive vice president—business infrastructure of Global Crossing in January 2004. Mr. Wagner oversees our global information technology function, including operations, telecommunications, development, security, and

III-11

Table of Contents

technology integration. Mr. Wagner served as chief information officer and senior vice president—business information from August 2002 through December 2003. From March 2002 through August 2002 Mr. Wagner served as senior vice president of information technology, real estate, procurement and vendor management. In addition to his corporate responsibilities, Mr. Wagner served on the board of directors of Global Marine from February 2002 through its divestment in August 2004. Mr. Wagner also served as president of Global Crossing Europe from October 2001 through March 2002 and managing director of Global Crossing UK from January 2001 through October 2001. Mr. Wagner served Global Crossing as vice president of business integration for North America following its acquisition of Frontier Communications. While at Frontier, between June 1999 and July 2000, he held several other key management positions, including senior director of finance and integration, and vice president of service delivery. Before joining Frontier in 1994, Mr. Wagner was a management consultant for Andersen Consulting and his own independent firm for several years.

III-12

Table of Contents

The Board of Directors and various Committees met numerous times during 2004. The Board of Directors held twelve meetings, six of which were telephonic and six of which were “in-person”. The Audit Committee met 25 times, with 21 telephonic and four “in-person” meetings. The Compensation Committee met seven times, with three telephonic and four “in-person” meetings. The Nominating and Corporate Governance Committee met one time at an “in-person” meeting. The Executive Committee met three times, with two telephonic and one “in-person” meeting. The Government Security Committee met five times, with one telephonic and four “in-person” meetings.

We have adopted an ethics policy that applies to all of our directors, officers (including chief executive officer, chief financial officer and any other person performing similar functions) and employees. The policy, together with the charters of our audit committee, compensation committee, nominating and corporate governance committee, executive committee and government security committee, can be found on our website atwww.globalcrossing.com, or can be mailed to shareholders upon written request to our Secretary at Wessex House, 45 Reid Street, Hamilton HM12, Bermuda. If a waiver of our ethics policy is granted to any of our directors or executive officers, such waiver will be posted on our website within five days of that waiver being granted.

We expect and require all of our directors to attend our annual meeting of shareholders. All of our directors attended our previous annual shareholder meeting held on December 15, 2004.

As a “controlled company” (as defined in NASDAQ rules), we are not required to comply with NASDAQ rules that require listed companies to have a majority of independent directors or nominating and corporate governance and compensation committees composed entirely of independent directors or to have written charters for certain committees addressing specified matters. At such time as we are no longer a “controlled company,” if ever, we will amend our committee charters, if necessary, and change the composition of our committees to ensure compliance with these NASDAQ requirements.

The five standing committees of the Board of the Company are the Audit Committee, the Compensation Committee, the Nominating and Corporate Governance Committee, the Executive Committee and the Government Security Committee. These committees are described in the following paragraphs.

Audit Committee

The Audit Committee consists of Messrs. Rescoe (chairman), Aldridge and Erkeneff, all of whom satisfy the independence and other requirements of NASDAQ rules. The Board has determined that Mr. Rescoe, the committee’s chairman, is an “audit committee financial expert” as defined in applicable Securities and Exchange Commission rules. The primary purpose of the Audit Committee is to assist the Board of Directors of the Company in fulfilling its responsibility for the integrity of the Company’s financial reports. To carry out this purpose, the Audit Committee oversees: (A) management’s conduct of the Company’s financial reporting process, including the integrity of the financial statements and other financial information provided by the Company to governmental and regulatory bodies, to shareholders and other security holders, or to other users of such information, (B) the Company’s compliance with legal and regulatory requirements that may have a material impact on the Company’s financial statements, (C) the appointment, qualifications (including independence), compensation and performance of the Company’s independent registered public accounting firm and the quality of the annual independent audit of the Company’s financial statements, (D) the performance of the Company’s internal audit function and management’s establishment and application of the Company’s systems of internal accounting and financial controls and disclosure controls, and (E) the adequacy of and adherence to (including any waivers granted to executive officers from adherence to) the Company’s code of business conduct and ethics, and such other matters as are incidental thereto. The Audit Committee also carries out other functions from time to time as assigned to it by the Board.

III-13

Table of Contents

In carrying out its purpose, the goal of the Audit Committee is to serve as an independent and objective monitor of the Company’s financial reporting process and internal control systems, including the activities of the Company’s independent registered public accounting firm and internal audit function, and to provide an open avenue of communication with the Board for, and among, the independent registered public accounting firm, internal audit operations and financial and executive management.

Report of the Audit Committee

Management is responsible for the preparation of the Company’s financial statements and the independent registered public accounting firm is responsible for examining those statements. In connection with the preparation of the December 31, 2004 financial statements, the Audit Committee (1) reviewed and discussed the audited restated financial statements with management; (2) discussed with the independent registered public accounting firm the matters required to be discussed under generally accepted auditing standards, including Statement on Auditing Standards No. 61 (as amended); and (3) received the written disclosures and the letter from the independent accountants required by Independence Standards Board Standard No. 1 (Independence Discussions with Audit Committees), as the same may be modified or supplemented, and has discussed with the independent registered public accounting firm the firm’s independence.

Based upon these reviews and discussions, the Audit Committee recommended, and the Board of Directors approved, that the Company’s audited financial statements be included in the annual report on Form 10-K for the fiscal year ended December 31, 2004, for filing with the Securities and Exchange Commission. The Audit Committee also selected Ernst & Young LLP as the independent registered public accounting firm for fiscal year ending December 31, 2005, subject to the rights of the shareholders under Bermuda law to appoint the auditors at the annual meeting.

THE AUDIT COMMITTEE

Michael Rescoe, Chairman

E.C. “Pete” Aldridge, Jr.

Richard R. Erkeneff

Principal Accounting Firm Fees

The following table sets forth the fees billed to the Company for the fiscal year ended December 31, 2004 by our present principal independent registered public accounting firm, Ernst & Young LLP, and for the fiscal year ended December 31, 2003 by our principal independent registered public accounting firm for that year, Grant Thornton LLP:

| 2004 | 2003 | |||||||

Audit Fees | $ | 10,186,000 | (1) | $ | 4,491,000 | (3) | ||

Audit Related Fees | — | — | ||||||

Tax Fees | 278,000 | (2) | — | |||||

All Other Fees | — | — | ||||||

Total | $ | 10,464,000 | $ | 4,491,000 | ||||

| (1) | Includes $1,359,000 of fees and expenses related to the financial statements published in the offering memorandum for the private placement of approximately $404 million principal amount of senior notes by our United Kingdom subsidiary and $3,200,000 of fees and expenses related to the audit of our internal control over financial reporting pursuant to section 404 of the Sarbanes-Oxley Act of 2002. |

| (2) | Includes fees and expenses relating to tax return preparation and consulting services in Europe and Latin America. |

| (3) | Includes $1,623,000 of fees and expenses relating to required audit of emergence date (December 9, 2003) balance sheet. Excludes fees of approximately $411,000 related to the restatement that is the subject of our amended 2003 annual report on Form 10-K/A filed on October 8, 2004. |

III-14

Table of Contents

Pursuant to paragraph (c)(7)(i)(B) of Rule 2-01 of Securities and Exchange Commission Regulation S-X, the Audit Committee has adopted a pre-approval policy pursuant to which the committee delegated to its chairman the authority to approve in advance audit or non-audit services to be performed by the Company’s independent accountants, provided that the Chairman and management are required to report any such pre-approval decision to the Audit Committee at its next scheduled meeting. This pre-approval policy is intended to be utilized only when it would be impracticable to call a meeting of the full committee.

Compensation Committee

The Compensation Committee consists of Messrs. Seah (chairman), Cromer, Lee and Sachs. The primary purpose of the Compensation Committee is to discharge certain responsibilities of the Board related to the compensation of the Company’s “key employees” (as defined by the committee) and related matters. In fulfilling this purpose, the Compensation Committee performs the following functions:

| • | Establishes the overall compensation philosophy and policies of the Company, subject to concurrence by the Board. |

| • | Annually reviews peer company market data to assess the Company’s competitive position for each significant component of key employee compensation. |

| • | Approves corporate goals and objectives relevant to compensation for all key employees other than the CEO and the executive vice presidents (“EVPs”), and recommends those goals and objectives for approval by the Board with respect to the CEO and the EVPs; provided that the Compensation Committee itself approves goals and objectives for awards intended to qualify for an exemption under Section 162(m) of the Internal Revenue Code of 1986, as amended (“Performance-Based Executive Compensation”). |

| • | Based on an evaluation of the key employees’ performance against those corporate goals and objectives, (i) approves the compensation level for each key employee other than the CEO and the EVPs and (ii) recommends to the Board the compensation level for the CEO and the EVPs; provided that the Compensation Committee itself determines all Performance-Based Executive Compensation. |

| • | Administers awards and compensation programs and plans intended to qualify as Performance-Based Executive Compensation, including determining performance measures and goals; setting thresholds, targets, and maximum awards; reviewing performance compared to goals; and certifying goal attainment and approving incentive payments. |

| • | Reviews the key employee compensation programs and equity-based compensation plans to determine whether they are properly coordinated and achieving their intended purposes and makes or recommends any appropriate modifications, including the establishment of new such programs. |

| • | Grants awards of shares or share options pursuant to the Company’s equity-based plans. |

Nominating and Corporate Governance Committee

The Nominating and Corporate Governance Committee consists of Messrs. van Wachem (chairman), Clemins, Lee and Sachs. The Nominating and Corporate Governance Committee assists the Board of Directors of the Company in fulfilling its responsibility to the shareholders by (i) identifying individuals qualified to serve as directors and recommending that the Board support the selection of the nominees for all directorships, whether such directorships are filled by the Board or the shareholders, (ii) developing and recommending to the Board a set of corporate governance guidelines and principles and (iii) reviewing, on a periodic basis, the overall corporate governance of the Company and recommending improvements when necessary. The Company’s corporate governance guidelines, as recommended by the Nominating and Corporate Governance Committee and approved by the Board of Directors, can be found on our website atwww.globalcrossing.com, or can be mailed to shareholders upon written request to our Secretary at Wessex House, 45 Reid Street, Hamilton HM12, Bermuda.

III-15

Table of Contents

At this time, as described above, the right to appoint individuals for board membership is currently held by both our majority shareholder, the STT Shareholder Group, and the Creditors Committee directors. These designation rights will in general control the nomination process until either (a) the STT Shareholder Group’s share ownership percentage in the Company changes or (b) the Creditor’s Committee directors’ terms are completed. However, should events occur so as to permit new directors to be nominated for appointment to our Board, although the Nominating Committee has not adopted formal procedures for the submission of shareholders’ recommendations for nominees for Board membership, such recommendations may be made in the manner specified below under “Submission of Future Shareholder Proposals.”

Executive Committee

The Executive Committee consists of Messrs. Lee (chairman), Aldridge (with Mr. Erkeneff serving as Mr. Aldridge’s alternate member of the Committee consistent with the Alternate Director provisions of the Company’s bye-laws), Clontz, Lambert, Legere, and Macaluso. The Executive Committee has the power to exercise all the powers of the Board when exigencies or practical considerations prevent the convening of the full Board in a timely manner, subject to such limitations as the Board and/or applicable law may from time to time impose. In addition, the Committee may meet to review and discuss the strategic direction of and major developments at the Company, and may advise and make recommendations to management and the Board relating to such matters.

Government Security Committee

The Government Security Committee (the “Security Committee”) consists of Messrs. Aldridge (chairman), Cromer, Clemins and Erkeneff. The Security Committee discharges those responsibilities related to the security of the Company’s domestic United States operations as are required of the Security Committee or its individual members pursuant to the terms of the Network Security Agreement (“NSA”) dated as of September 24, 2003 among the Company, Old GCL, ST Telemedia, the Federal Bureau of Investigation, the United States Department of Justice, the Department of Defense, and the Department of Homeland Security. The NSA, a copy of which is included as an exhibit to our 2002 annual report on Form 10-K, establishes processes and procedures to ensure the security of our U.S. network assets, which include transmission and routing equipment, switches and associated operational support systems and personnel (referred to in the NSA as the “Domestic Communications Infrastructure”). The Committee is comprised solely of directors who are U.S. citizens who, if not already in possession of U.S. security clearances, must apply for U.S. security clearances pursuant to Executive Order 12968 immediately upon their appointment to the Security Committee.

III-16

Table of Contents

SECURITY OWNERSHIP OF MANAGEMENT AND OTHERS