Seacoast Financial Services (SCFS) Inactive

Filed: 9 Mar 04, 12:00am

| Filed by Sovereign Bancorp, Inc. (Commission File No. 001-16581) Pursuant to Rule 425 under the Securities Act of 1933 Subject Company: Seacoast Financial Services Corporation Commission File No. 000-25077 |

| Acquisition of Waypoint Financial Corp. March 9, 2004 |

| Forward-Looking Statements This presentation contains statements of Sovereign's strategies, plans and objectives, estimates of future operating results for Sovereign Bancorp, Inc. as well as estimates of financial condition, operating efficiencies, revenue creation and shareholder value These statements and estimates constitute forward-looking statements (within the meaning of the Private Securities Litigation Reform Act of 1995) which involve significant risks and uncertainties. Actual results may differ materially from the results discussed in these forward- looking statements Factors that might cause such a difference include, but are not limited to: general economic conditions, changes in interest rates, deposit flows, loan demand, real estate values, and competition; changes in accounting principles, policies, or guidelines; changes in legislation or regulation; and other economic, competitive, governmental, regulatory, and other technological factors affecting the Company's operations, pricing, products and services 3 |

| Forward-Looking Statements 5 In addition, this presentation and filing contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, with respect to the financial condition, results of operations and business of Sovereign Bancorp, Inc. pending consummation of the merger of Seacoast Financial Services Corporation with and into Sovereign and the merger of Waypoint Financial Corp. with and into Sovereign that are subject to various factors which could cause actual results to differ materially from such projections or estimates. Such factors include, but are not limited to, the following: (1) the respective businesses of Seacoast and Waypoint may not be combined successfully with Sovereign's businesses, or such combinations may take longer to accomplish than expected; (2) expected cost savings from each of the mergers cannot be fully realized or realized within the expected timeframes; (3) operating costs, customer loss and business disruption following the mergers, including adverse effects on relationships with employees, may be greater than expected; (4) governmental approvals of each of the mergers may not be obtained, or adverse regulatory conditions may be imposed in connection with government approvals of the mergers, (5) the stockholders of Seacoast may fail to approve the merger of Seacoast with and into Sovereign and the shareholders of Waypoint may fail to approve the merger of Waypoint with and into Sovereign; (6) adverse governmental or regulatory policies may be enacted; (7) the interest rate environment may adversely impact the expected financial benefits of the mergers, and compress margins and adversely affect net interest income; (8) the risks associated with continued diversification of assets and adverse changes to credit quality; (9) competitive pressures from other financial service companies in Seacoast's, Waypoint's and Sovereign's markets may increase significantly; and (10) the risk of an economic slowdown that would adversely affect credit quality and loan originations. Other factors that may cause actual results to differ from forward-looking statements are described in Sovereign's filings with the Securities and Exchange Commission. |

| Operating and Cash Earnings Per Share This presentation contains financial information determined by methods other than in accordance with U.S. Generally Accepted Accounting Principles ("GAAP") Sovereign's management uses the non-GAAP measures of Operation Earnings and Cash Earnings in their analysis of the company's performance. These measures typically adjust net income determined in accordance with GAAP to exclude the effects of special items, including significant gains or losses that are unusual in nature or are associated with acquiring and integrating businesses, and certain non-cash charges. Operating Earnings in 2004 represents net income adjusted for the after-tax effects of merger-related charges of $0.05 to $0.06 for the First Essex Bancorp Inc. and $.07 for the Seacoast Financial Services acquisitions Cash earnings in 2004 represents operating earnings adjusted to remove the after-tax effect of amortization of intangible assets and stock-based compensation expense associated with stock options, restricted stock, bonus deferral plans and ESOP awards of $.10 to $.15 Since certain of these items and their impact on Sovereign's performance are difficult to predict, management believes presentations of financial measures excluding the impact of these items provide useful supplemental information in evaluating the operating results of Sovereign's core businesses These disclosures should not be viewed as a substitute for net income determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures, which may be presented by other companies 7 |

| Additional Information About the Merger 9 Sovereign and Waypoint will be filing documents concerning the merger with the Securities and Exchange Commission, including a registration statement on Form S-4 containing a prospectus/proxy statement which will be distributed to shareholders of Waypoint. Investors are urged to read the registration statement and the proxy statement/prospectus regarding the proposed transaction when it becomes available and any other relevant documents filed with the SEC, as well as any amendments or supplements to those documents, because they will contain important information. Investors will be able to obtain a free copy of the proxy statement/prospectus, as well as other filings containing information about Sovereign and Waypoint, free of charge on the SEC's Internet site (http://www.sec.gov). In addition, documents filed by Sovereign with the SEC, including filings that will be incorporated by reference in the prospectus/proxy statement, can be obtained, without charge, by directing a request to Sovereign Bancorp, Inc., Investor Relations, 1130 Berkshire Boulevard, Wyomissing, Pennsylvania 19610 (Tel: 610-988-0300). In addition, documents filed by Waypoint with the SEC, including filings that will be incorporated by reference in the prospectus/proxy statement, can be obtained, without charge, by directing a request to Waypoint Financial Corp., 235 North Second Street, Harrisburg, Pennsylvania 17101, Attn: Richard C. Ruben, Executive Vice President and Corporate Secretary (Tel: 717-236-4041). Directors and executive officers of Waypoint may be deemed to be participants in the solicitation of proxies from the shareholders of Waypoint in connection with the merger. Information about the directors and executive officers of Waypoint and their ownership of Waypoint common stock is set forth in Waypoint's proxy statement for its 2003 annual meeting of shareholders, as filed with the SEC on April 21, 2003. Additional information regarding the interests of those participants may be obtained by reading the prospectus/proxy statement regarding the proposed merger transaction when it becomes available. INVESTORS SHOULD READ THE PROSPECTUS/PROXY STATEMENT AND OTHER DOCUMENTS TO BE FILED WITH THE SEC CAREFULLY BEFORE MAKING A DECISION CONCERNING THE MERGER. |

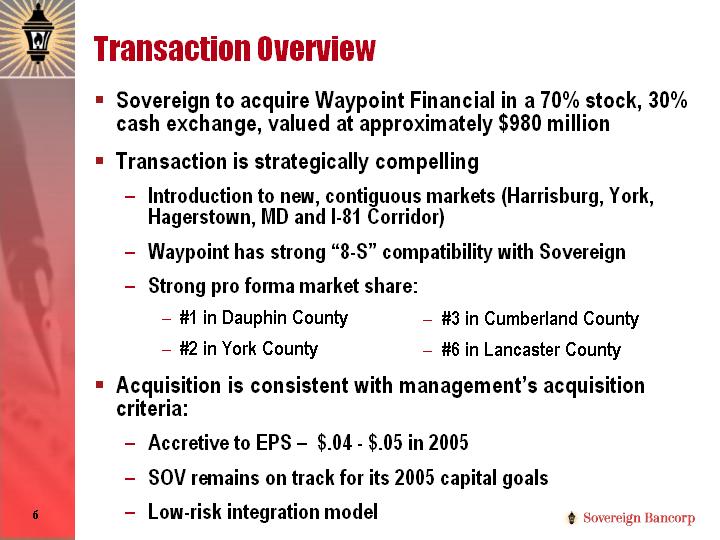

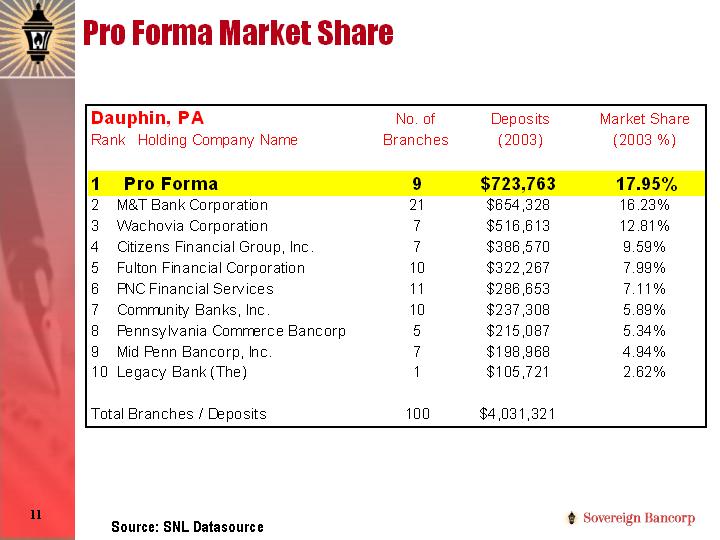

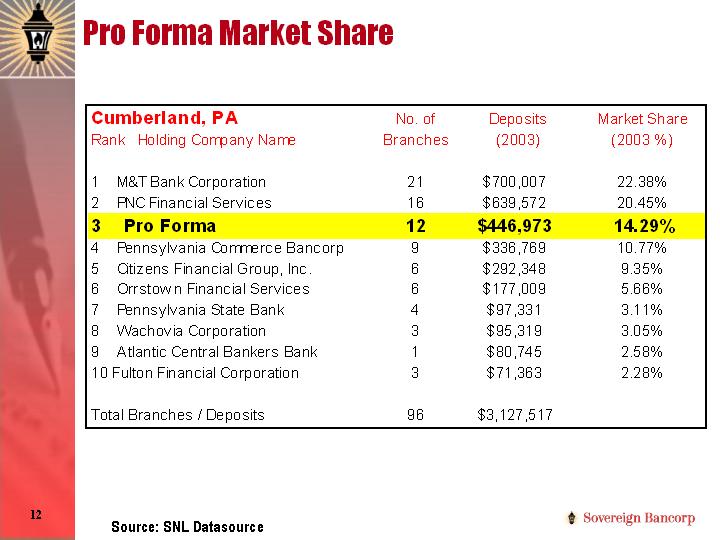

| Transaction Overview Sovereign to acquire Waypoint Financial in a 70% stock, 30% cash exchange, valued at approximately $980 million Transaction is strategically compelling Introduction to new, contiguous markets (Harrisburg, York, Hagerstown, MD and I-81 Corridor) Waypoint has strong "8-S" compatibility with Sovereign Strong pro forma market share: #1 in Dauphin County #2 in York County Acquisition is consistent with management's acquisition criteria: Accretive to EPS - $.04 - $.05 in 2005 SOV remains on track for its 2005 capital goals Low-risk integration model #3 in Cumberland County #6 in Lancaster County |

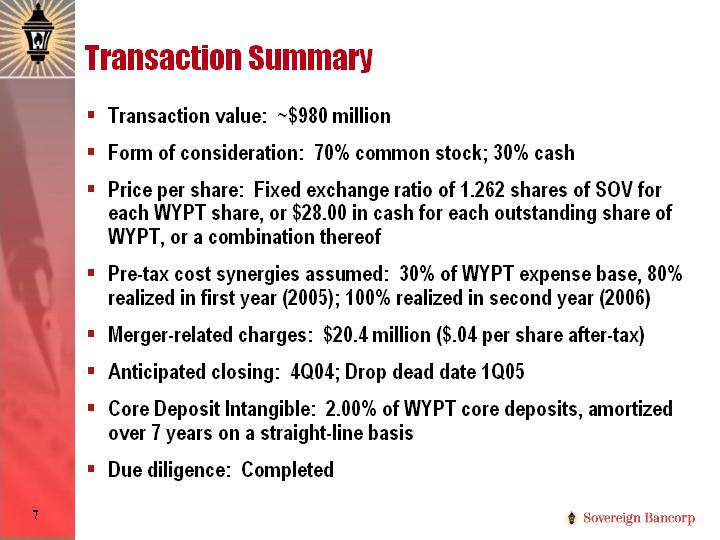

| Transaction Summary Transaction value: ~$980 million Form of consideration: 70% common stock; 30% cash Price per share: Fixed exchange ratio of 1.262 shares of SOV for each WYPT share, or $28.00 in cash for each outstanding share of WYPT, or a combination thereof Pre-tax cost synergies assumed: 30% of WYPT expense base, 80% realized in first year (2005); 100% realized in second year (2006) Merger-related charges: $20.4 million ($.04 per share after-tax) Anticipated closing: 4Q04; Drop dead date 1Q05 Core Deposit Intangible: 2.00% of WYPT core deposits, amortized over 7 years on a straight-line basis Due diligence: Completed |

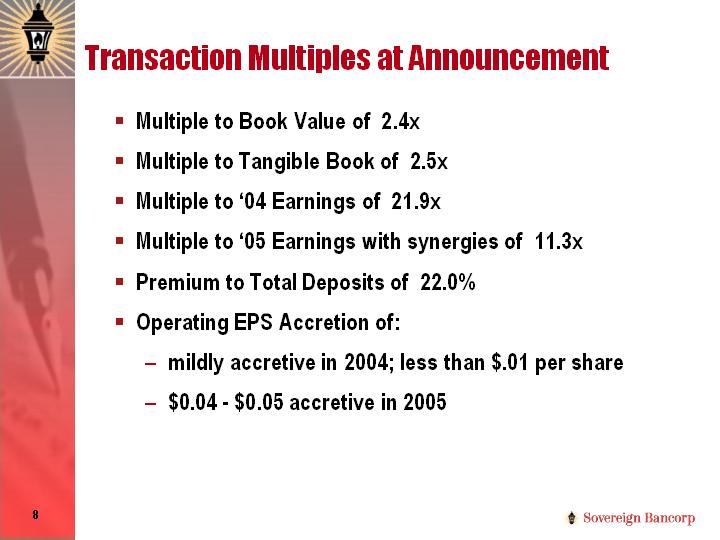

| Transaction Multiples at Announcement Multiple to Book Value of 2.4x Multiple to Tangible Book of 2.5x Multiple to '04 Earnings of 21.9x Multiple to '05 Earnings with synergies of 11.3x Premium to Total Deposits of 22.0% Operating EPS Accretion of: mildly accretive in 2004; less than $.01 per share $0.04 - $0.05 accretive in 2005 |

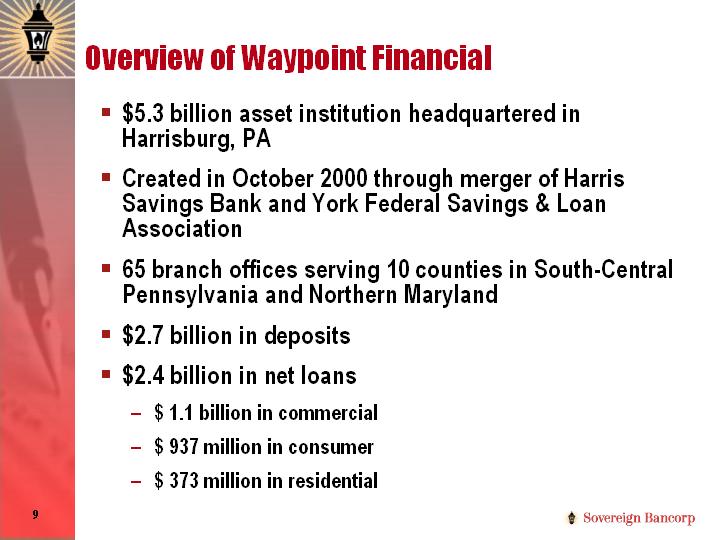

| Overview of Waypoint Financial $5.3 billion asset institution headquartered in Harrisburg, PA Created in October 2000 through merger of Harris Savings Bank and York Federal Savings & Loan Association 65 branch offices serving 10 counties in South-Central Pennsylvania and Northern Maryland $2.7 billion in deposits $2.4 billion in net loans $ 1.1 billion in commercial $ 937 million in consumer $ 373 million in residential |

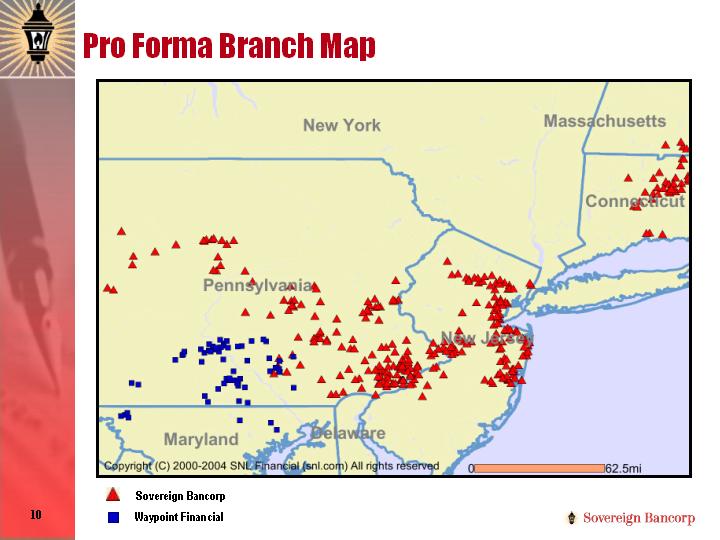

| Pro Forma Branch Map Quaker2\coral maps\sovereign & seacoast map for ppt.cdr (Recolored in powerpoint for fill effect) Sovereign Bancorp Waypoint Financial |

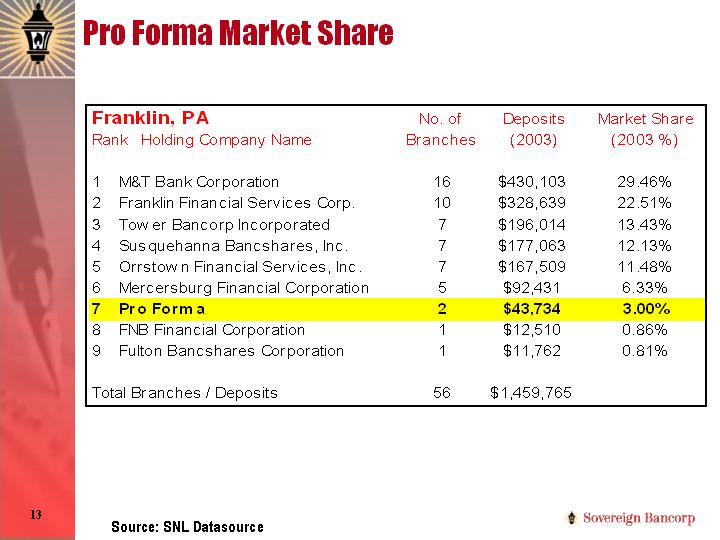

| Pro Forma Market Share Source: SNL Datasource |

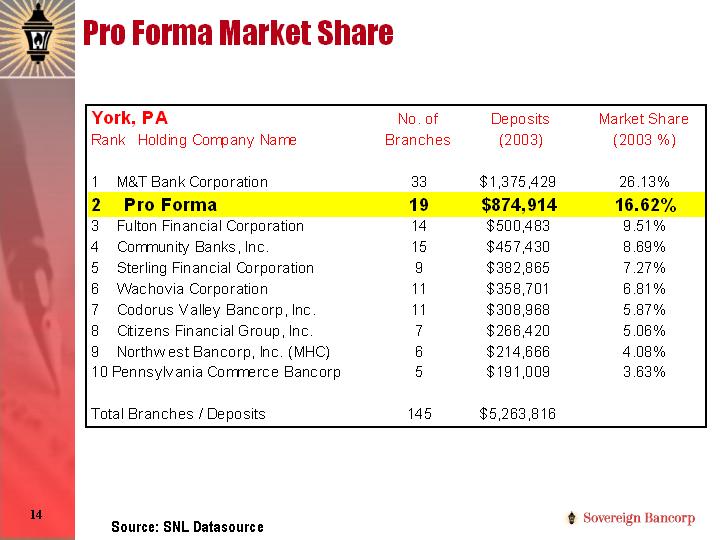

| Source: SNL Datasource Pro Forma Market Share |

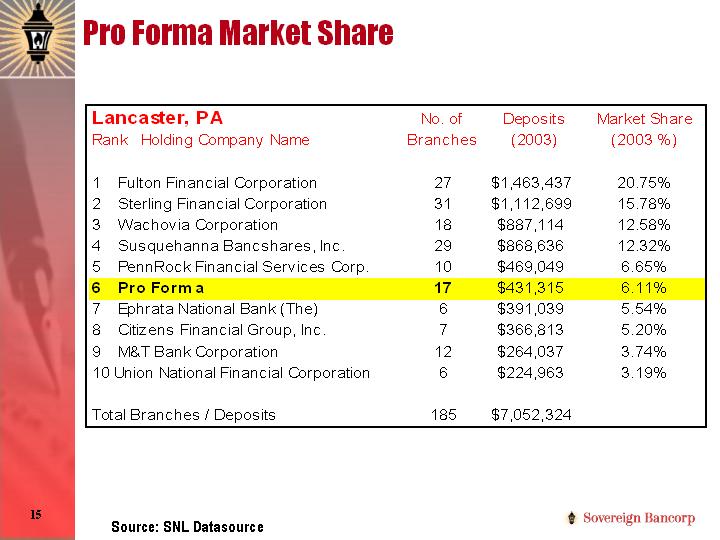

| Pro Forma Market Share Source: SNL Datasource |

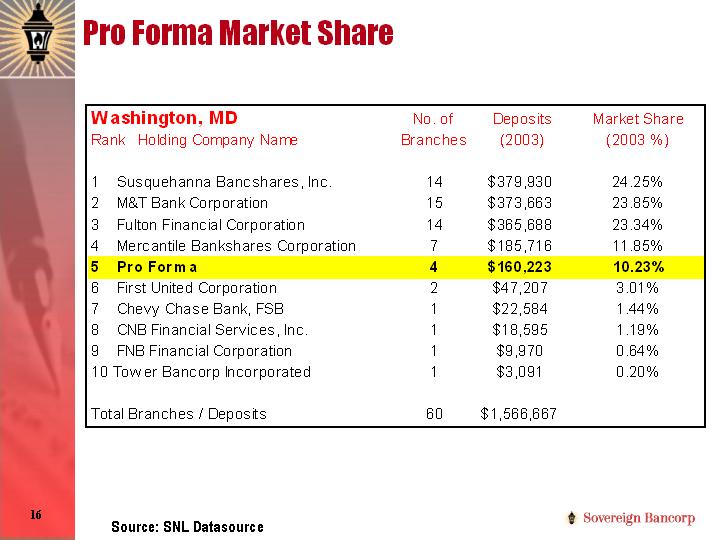

| Pro Forma Market Share Source: SNL Datasource |

| Pro Forma Market Share Source: SNL Datasource |

| Pro Forma Market Share Source: SNL Datasource |

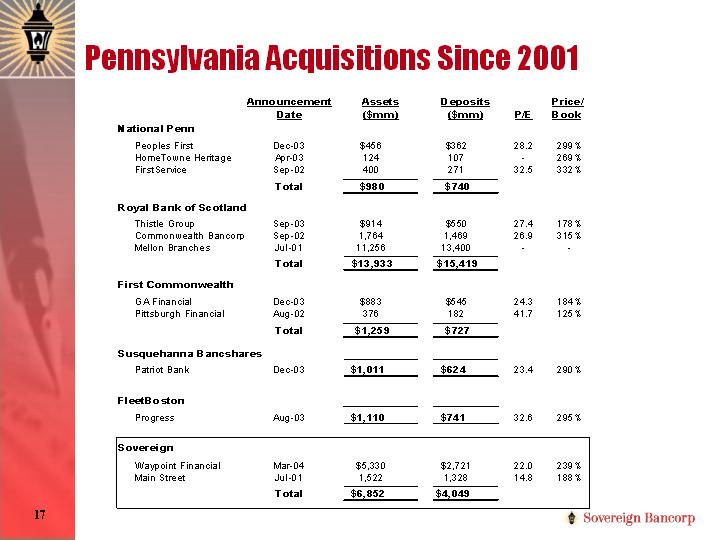

| Pennsylvania Acquisitions Since 2001 33 |

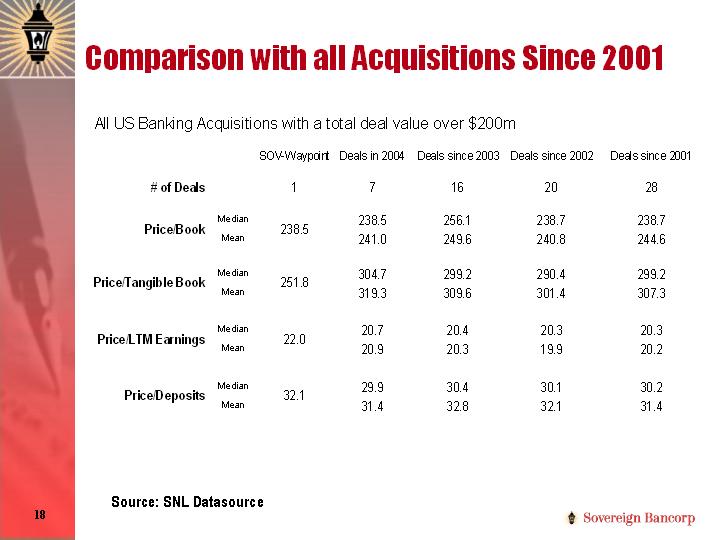

| Comparison with all Acquisitions Since 2001 35 Source: SNL Datasource |

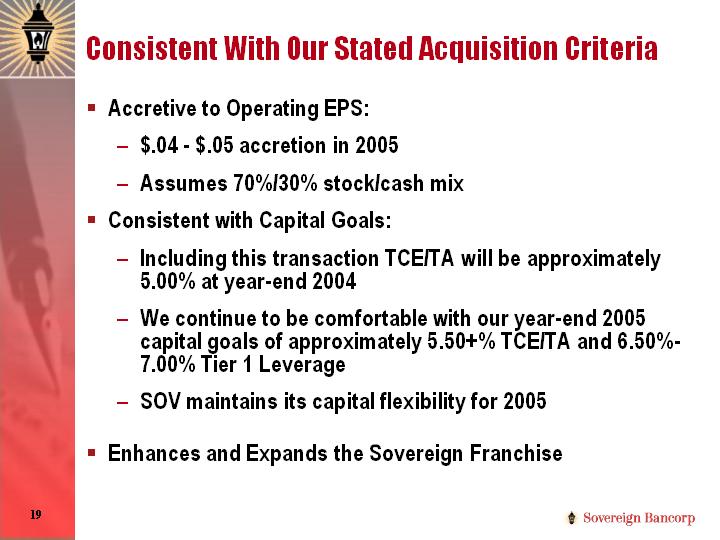

| Consistent With Our Stated Acquisition Criteria Accretive to Operating EPS: $.04 - $.05 accretion in 2005 Assumes 70%/30% stock/cash mix Consistent with Capital Goals: Including this transaction TCE/TA will be approximately 5.00% at year-end 2004 We continue to be comfortable with our year-end 2005 capital goals of approximately 5.50+% TCE/TA and 6.50%- 7.00% Tier 1 Leverage SOV maintains its capital flexibility for 2005 Enhances and Expands the Sovereign Franchise |

| Consistent With Our Vision and Mission Waypoint has a low-risk business model emphasizing retail and commercial banking Transaction opens up new markets to deliver Sovereign's broader array of products and services (e.g. cash management, capital markets, commercial lending and government banking) Fill-in acquisition of a manageable size to facilitate integration Creates leading market share positions in many desired micro-markets Sovereign has substantial experience in integrating acquisitions |

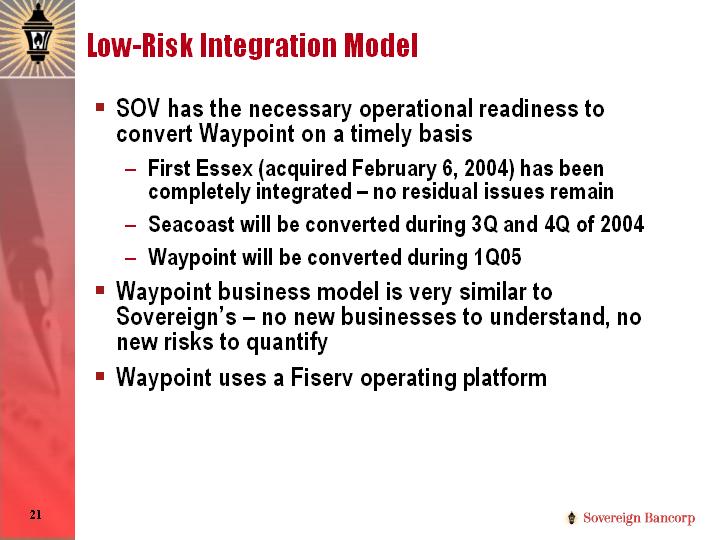

| Low-Risk Integration Model SOV has the necessary operational readiness to convert Waypoint on a timely basis First Essex (acquired February 6, 2004) has been completely integrated - no residual issues remain Seacoast will be converted during 3Q and 4Q of 2004 Waypoint will be converted during 1Q05 Waypoint business model is very similar to Sovereign's - no new businesses to understand, no new risks to quantify Waypoint uses a Fiserv operating platform |

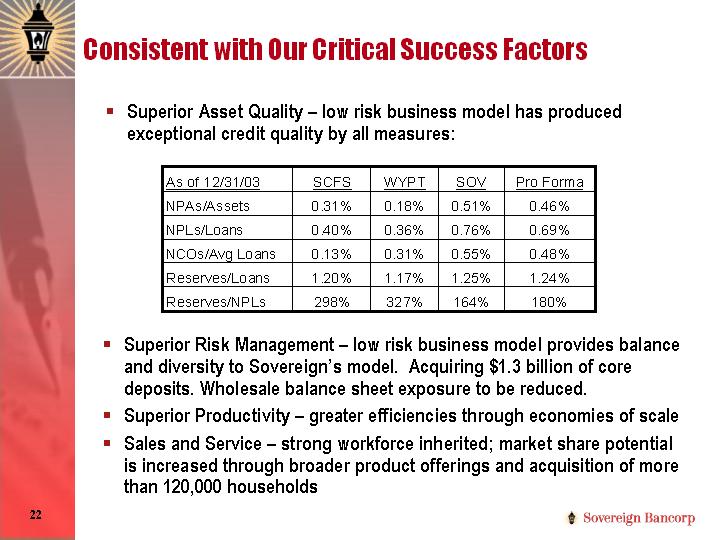

| Consistent with Our Critical Success Factors Superior Asset Quality - low risk business model has produced exceptional credit quality by all measures: Superior Risk Management - low risk business model provides balance and diversity to Sovereign's model. Acquiring $1.3 billion of core deposits. Wholesale balance sheet exposure to be reduced. Superior Productivity - greater efficiencies through economies of scale Sales and Service - strong workforce inherited; market share potential is increased through broader product offerings and acquisition of more than 120,000 households |

| Summary This acquisition is very strategically compelling, and creates exciting opportunities within Sovereign's franchise This acquisition continues to differentiate Sovereign as a leading financial institution in the Northeast We remain comfortable with the mean street estimate of $1.63 in Operating Earnings for 2004 We remain committed to striving for operating earnings of $1.65 to $1.70 per share in 2004, and cash earnings per share of $1.80 to $1.85 We remain committed to our 2004 and 2005 capital goals |

| Appendix |

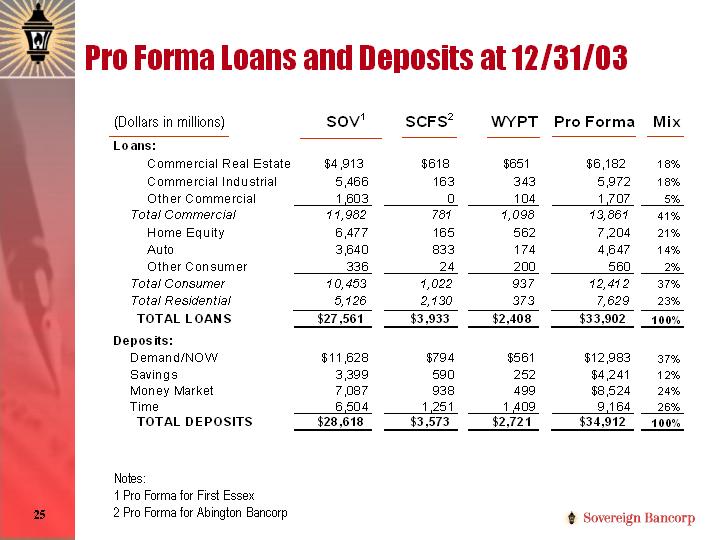

| Pro Forma Loans and Deposits at 12/31/03 49 (Dollars in millions) Notes: 1 Pro Forma for First Essex 2 Pro Forma for Abington Bancorp |

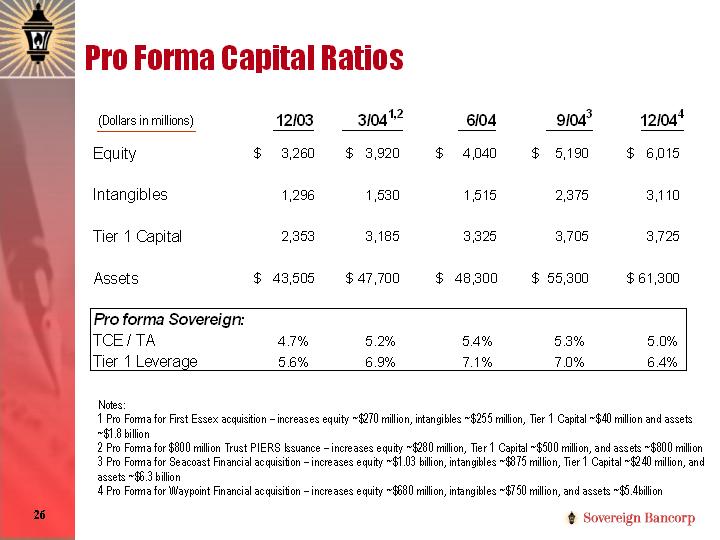

| Pro Forma Capital Ratios 51 (Dollars in millions) Notes: 1 Pro Forma for First Essex acquisition - increases equity ~$270 million, intangibles ~$255 million, Tier 1 Capital ~$40 million and assets ~$1.8 billion 2 Pro Forma for $800 million Trust PIERS Issuance - increases equity ~$280 million, Tier 1 Capital ~$500 million, and assets ~$800 million 3 Pro Forma for Seacoast Financial acquisition - increases equity ~$1.03 billion, intangibles ~$875 million, Tier 1 Capital ~$240 million, and assets ~$6.3 billion 4 Pro Forma for Waypoint Financial acquisition - increases equity ~$680 million, intangibles ~$750 million, and assets ~$5.4billion |

| Additional Transaction Details Implied exchange ratio: Stock - 1.262x (based on SOV 10-day average prior to announcement); Cash - $28.00 fixed Price protection: fixed exchange ratio; no collars Walk-away provision: Double-trigger, SOV declines 15% relative to an index and 15% absolute, with SOV ability to fill up hole Deal lock-up termination fee: 4% plus 19.9% lock up option (Sovereign can elect one but not both) Necessary Approvals: WYPT - OTS, PA, and shareholders; SOV - OTS Due Diligence: Completed Transaction Timeline: Closing anticipated to be 4Q04; transaction may be terminated if not completed by January 31, 2005 Advisors: WYPT: Ryan Beck & Co. (Investment Banking); Rhoads & Sinon LLP (Legal) SOV: Citigroup (Investment Banking); Stevens & Lee (Legal) |