We cannot assure that we will be successful in responding to the above technological and industry challenges in a timely and cost-effective manner. If we are unable to integrate new technologies and industry standards effectively, our business could be harmed.

Our business depends on the increased acceptance and use of the Internet as a medium for accessing public information and completing government filings. Rapid growth in the use of the Internet is a relatively recent phenomenon. As a result, acceptance and use may not continue to develop at historical rates and a sufficiently broad base of individual and business customers may not adopt or continue to use the Internet as a medium for accessing government portals and other online services. Demand and market acceptance for recently introduced services over the Internet are subject to a high level of uncertainty, and there exist few proven services.

The Internet has experienced, and is expected to continue to experience, significant growth in the number of users and amount of traffic. If the Web continues to experience increased numbers of users, frequency of use or increased bandwidth requirements, the Internet infrastructure may not be able to support these increased demands or perform reliably. The Internet has experienced a variety of outages and other delays as a result of damage to portions of its infrastructure, and could face such outages and delays in the future. These outages and delays could reduce the level of Internet usage and traffic on our government portals. Such outages and delays would also hinder our customers’ ability to complete eGovernment transactions. In addition, the Internet could lose its viability due to delays in the development or adoption of new standards and protocols to handle increased levels of activity or due to increased governmental regulation. If the Internet infrastructure is not adequately developed or maintained, use of our government portals and our government-to-citizen and government-to-business services may be reduced.

Our success depends on the increase in Internet usage generally and in particular as a means to access public information electronically. This in part requires the development and maintenance of the Internet infrastructure. If this infrastructure fails to develop or be adequately maintained, our business would be harmed because users may not be able to access our government portals. Among other things, this development and maintenance will require a reliable network backbone with the necessary speed, data capacity, security and timely development of complementary products for providing reliable Internet access and services.

Because we aggregate and distribute sometimes private and sensitive public information over the Internet, we may face potential liability for defamation, libel, negligence, invasion of privacy, copyright or trademark infringement, and other claims based on the nature and content of the material that is published on our outsourced government portals. Most of the agreements through which we obtain consent to disseminate this information do not contain indemnity provisions in our favor. These types of claims have been brought, sometimes successfully, against online services and Web sites in the past. We cannot assure that our general liability or errors and omissions insurance will be adequate to indemnify us for all liability that may be imposed. Any liability that is not covered by our insurance or is in excess of our insurance coverage could severely harm our business operations and financial condition.

Security breaches or system failures may harm our reputation and adversely affect future earnings.

A significant challenge to electronic commerce is the secure transmission of sensitive and/or personal information (“information”) over public networks. In addition to complying with requirements established for protecting information contained in federal and state laws, we are also required to comply with the Payment Card Industry’s Data Security Standards, or PCI DSS, because we provide online payment processing services. Since we provide the electronic transmission of information released from various government entities and we perform online payment processing services, we represent an attractive target for criminal hackers.

Despite the various security measures we have in place to protect information from unauthorized disclosure, a compromise or breach may still occur. Hackers have become increasingly sophisticated and serious, and therefore, cyber security is an ever moving target. A party who is able to circumvent our security measures could misappropriate information, including, but not limited to customer credit card information, or cause interruptions or direct damage to our government portals.

Any breach in our security resulting in the compromise of information, could expose us to fines imposed by the Payment Card Industry and jeopardize our ability to continue processing transactions with specific payment card brands. Also, should hackers compromise information, or create bugs or viruses in an attempt to sabotage the functionality of our applications and services, we may receive negative publicity, incur liability to our portal users and our partners or lose the confidence of the governments with whom we contract, any of which may cause the termination or modification of our government contracts.

Furthermore, the PCI DSS is an evolving standard that has already been modified twice since it was first issued in 2005. As it changes and new requirements are issued, we may be required to expend significant capital and other resources to comply with the PCI DSS.

Our systems may fail or limit user traffic.

Most of our communications hardware and computer hardware operations for delivering our eGovernment services are located individually in each state or city where we provide those services. We cannot assure that during the occurrence of fire, floods, earthquakes, power loss, telecommunications failures, break-ins and similar events that the modem banks and direct dial-up connections we have to serve as back-up systems will not prevent damage to our systems or cause interruptions to our services. Computer viruses, electronic break-ins or other similar disruptive problems could cause users to stop visiting our government portals and could cause our partners to terminate agreements with us. If any of these circumstances occurred, our business could be harmed. Our insurance policies may not adequately compensate us for any losses that may occur due to any failures of or interruptions in our systems.

Our government portals must accommodate a high volume of traffic and deliver frequently updated information. These government portals may experience interruptions due to any failure or delay by government agencies in the transmission or receipt of this information. Due to holidays and technical problems with state computer systems, our Web sites have experienced slower response times or decreased traffic in the past and may experience the same incidents in the future. In addition, our users depend on Internet service providers, online service providers and other Web site operators for access to our government portals and other online government-to-citizen and government-to-business services. Many of these providers and operators have experienced significant outages in the past due to system failures unrelated to our systems, holidays and heavy user traffic, and could experience the same outages, delays and other difficulties in the future. Any of these system failures could harm our business, results of operations and financial condition.

We may become subject to liability under NACHA rules and standards for processing electronic direct debit payments from bank accounts.

Our electronic check processing for online payments made by direct debit to a bank account is governed by rules and standards promulgated by the National Automated Clearing House Association, or NACHA, an industry trade association of banking institutions and regional automated clearing house associations. Under those rules, we may become liable for failing to handle transactions in accordance with those rules, or for failing to return funds within the prescribed time frame to the bank account of the person or entity disputing our authorization to debit those funds, before the dispute regarding our authorization is resolved. Our agreements with governmental

22

agencies at the state, federal, and local level transfer this obligation for rapid funds return during dispute resolution to the government agencies affected, but in the event that such return does not happen, we may be liable notwithstanding the government’s failure, and we may not be able to obtain reimbursement from the government involved or from the individual user or entity that initiated the debit without authorization. If this were to happen, our business, results of operations and financial condition may be adversely affected.

We may become liable for violations of the Driver Privacy Protection Act as adopted federally or in each state.

We act as an outsourced manager on behalf of states, for electronic access to records pertaining to motor vehicles and motor vehicle operators (driver history records) by users and certain permitted resellers. These records are the largest group of records for which we process electronic access for any state agency, and are processed in each of our portal states. These records contain “personal information” and “sensitive personal information” as defined by the federal Driver Privacy Protection Act, and state versions of that Act adopted in every state (collectively, the “DPPA”). The DPPA regulates categories and circumstances under which “personal information” and “sensitive personal information” may be disclosed to requestors. Each state has procedures for complying with the DPPA, and such procedures may vary from state to state. We closely follow the state’s existing compliance procedures for general access, with our electronic access. If we fail to follow such procedures, or we grant access to users not in compliance with such procedures, or if such procedures are deemed inadequate in some way, our business, results of operations and financial condition may be adversely affected. The DPPA permits statutory damages to be awarded to the subjects of such records, even without proof of actual damage, for certain infringements or violations of the DPPA. We may be liable for such damages in such instances, and we may have no recourse against the state, or the state may not be jointly and severally liable with us.

Compliance with changing regulation of corporate governance and public disclosure may result in additional expenses.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act of 2002, new SEC regulations and NASDAQ Global Select Market rules, are creating uncertainty for companies such as ours. These new or changed laws, regulations and standards are subject to varying interpretations in many cases due to their lack of specificity, and as a result, their application in practice may evolve over time as new guidance is provided by regulatory and governing bodies, which could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure and governance practices. We are committed to maintaining high standards of corporate governance and public disclosure. As a result, our efforts to comply with evolving laws, regulations and standards have resulted in, and are likely to continue to result in, increased general and administrative expenses and a diversion of management time and attention from revenue-generating activities to compliance activities. In particular, our efforts to comply with Section 404 of the Sarbanes-Oxley Act of 2002 and the related regulations regarding our required assessment of our internal control over financial reporting has required the commitment of significant financial and managerial resources. Further, our board members, chief executive officer and chief financial officer could face an increased risk of personal liability in connection with the performance of their duties. As a result, we may have difficulty attracting and retaining qualified board members and executive officers, which could harm our business. If our efforts to comply with new or changed laws, regulations and standards differ from the activities intended by regulatory or governing bodies due to ambiguities related to practice, our reputation may be harmed.

An informal SEC inquiry involving us has resulted in significant costs to us, may result in future costs to us, and could adversely affect us.

As disclosed in a Form 8-K and press release issued on February 6, 2008, we are currently the subject of an informal SEC inquiry of expense reporting by certain officers of the Company and certain potentially related matters. In connection with that inquiry, a review was undertaken by the Audit Committee of our Board of Directors, with the assistance of outside, independent counsel, which focused on such expense reporting. The review covered the period from January 1, 2004 through June 30, 2007 and was conducted with full cooperation by us and Jeffery S. Fraser, who was then our Chief Executive Officer. Mr. Fraser has reimbursed the Company approximately $97,000 in expenses as a result of the review, which followed reimbursement by him of approximately $186,000 in expenses made prior to the review. The reimbursement was made to correct expense reporting during the period from January 2004 through October 2006 that was inconsistent with our expense

23

reimbursement policies. The review also revealed that these expense reimbursement deficiencies were isolated to Mr. Fraser. We do not believe the amounts involved in the review are material to our financial condition or results of operations. However, in view of his recognition of the importance of the proper tone at the top for effective corporate governance, Mr. Fraser decided to retire as our Chief Executive Officer, effective February 4, 2008, but remained as a director and our Chairman of the Board.

Both we and our Audit Committee intend to continue to fully cooperate with the informal SEC inquiry described above. However, there can be no assurance that the SEC will not take any action that could adversely affect us as a result of the matters it is reviewing. We have incurred significant legal fees and other expenses in connection with the informal SEC inquiry and the Audit Committee review and could incur significant legal fees and other expenses in connection with the ongoing, informal SEC inquiry. In addition, members of our management have devoted in the past, and may need to devote in the future, a significant amount of time to these matters, which would reduce the amount of time they can devote to our business and therefore have an adverse effect on our business.

Increases in credit card association fees may result in the loss of customers or a reduction in our earnings.

From time to time, Visa, MasterCard, American Express and Discover increase the fees (interchange and assessment fees) that they charge processors such as us. We could attempt to pass these increases along to our government client customers, but this might result in the loss of those customers. If we elect not to pass along such increased fees to our government client customers in the future, we may have to absorb all or a portion of such increases thereby increasing our operating costs and reducing our earnings

Our UCC and corporate filings software development business has incurred losses under its fixed-fee contracts in the past, and our results of operations could be harmed if the costs that this business incurs to meet contractual commitments exceed our current estimates.

Our UCC and corporate filings software development business, NIC Conquest, develops and delivers applications, typically for a fixed development fee, that improve the back-office administration of government records and better enable electronic filing and distribution of business entity and UCC records for secretaries of state. This business recognizes revenues on the percentage-of-completion method of accounting utilizing costs incurred to date as compared to the estimated total costs for each contract. This method is used because management considers expended costs to be the best available measure of progress on our fixed-price contracts and results in our recognizing contract revenues over the contract term in proportion to our incurrence of contract costs. The earnings or losses recognized on individual contracts are based on estimates of contract revenues and costs. Contract losses are recognized in full when determined, and contract profit estimates are adjusted based on ongoing reviews of contract profitability. Actual results could differ from estimated amounts and could result in a reduction or elimination of previously recognized earnings. In certain circumstances, such adjustments could be significant.

In the fourth quarter of 1998, we determined that the balance of revenues remaining to be recognized under our existing contractual obligations was not expected to cover anticipated costs of developing and implementing the related applications. Estimated costs in excess of fixed contract prices of $1.3 million for completing these applications were expensed under the percentage-of-completion method of accounting in the fourth quarter of 1998. We accrued additional anticipated losses of $1.1 million in 1999, $1.4 million in 2000, and $6.0 million in 2001 based on revised estimates relating to our then-existing contracts. In 2002, we accrued approximately $3.5 million in anticipated losses due to cost overruns on contracts in Arkansas, Minnesota and Oklahoma. We have fulfilled all obligations under our contracts with the states of Minnesota and Oklahoma, and the Arkansas system is currently in the maintenance phase. As recently as the first quarter of 2005, we recorded a $5.0 million charge due to anticipated cost overruns on our contract with the California Secretary of State, as further discussed in Note 2 in the Notes to Consolidated Financial Statements included in this Form 10-K. In June 2006, the California Secretary of State officially accepted the UCC system, which also commenced the maintenance and operations phase of the contract. However, it is possible that our costs will similarly exceed revenues in the future, as a result of unforeseen difficulties in the creation of an application called for in the contract, unforeseen challenges in ensuring compatibility with existing systems, rising development, subcontractor and personnel costs, delays in completing the contract, or other reasons. If this occurs, our results of operations, financial condition and cash flows could be seriously harmed.

24

We depend on other contractors and subcontractors in connection with our performance under our UCC and corporate filings software development engagement with the California Secretary of State. If these parties fail to satisfy their obligations to us or the California Secretary of State, or if we are unable to maintain these relationships, our operating results and business prospects could be adversely affected.

A significant portion of the work we are obligated to deliver to the California Secretary of State is performed by subcontractors. There is a risk that the California Secretary of State or we may have disputes with our subcontractors arising from, among other things, the quality and timeliness of work performed by the subcontractors and customer concerns about the subcontractors. Disputes with subcontractors or the California Secretary of State could lead to legal disputes and litigation. Adverse judgments or settlements in legal disputes may result in significant monetary damages or injunctive relief against us. In addition, if any of our subcontractors fails to deliver on a timely basis the agreed-upon supplies and/or perform the agreed-upon services, our ability to fulfill our obligations as a prime contractor may be jeopardized. Subcontractor performance deficiencies could result in the termination of our contract for default. A termination for default could expose us to liability and have an adverse effect on our business prospects, financial condition, and on our ability to compete for future contracts and orders.

We have incurred significant net losses in the past, and may do so again in the future.

We expanded rapidly following our initial public offering in July 1999 and incurred substantial net losses through mid-2002 primarily as a result of our acquired software & services businesses. However, as part of a broad strategic refocusing of the Company on our profitable core outsourced portal business during 2002, we exited our eProcurement business, NIC Commerce, decided to wind down our transportation business, IDT, and restructured the other software & services businesses in an effort to accelerate our path to profitability. As a result, the Company became profitable in the second half of 2002 and has been profitable since that time with the exception of the first quarter of 2005, as a result of the $5.0 million charge we recorded on our UCC and corporate filings software development engagement with the California Secretary of State, our only remaining legacy contract from this business. Further, even though we were profitable in 2007, we may not be able to sustain or increase profitability on a quarterly or annual basis thereafter. We will need to generate significantly higher revenues while containing costs and operating expenses if we are to achieve growing profitability. We cannot be certain that our revenues will continue to grow or that we will ever achieve sufficient revenues to remain profitable on a long-term, sustained basis.

We may be unable to generate sufficient taxable income from future operations to fully utilize our significant tax net operating loss carryforwards.

We have a history of unprofitable operations primarily due to operating losses incurred in the software & services companies we have acquired since September 1999, as further discussed above. These losses have generated significant federal tax net operating losses, or NOLs. We had available at December 31, 2007, total NOL carryforwards for federal tax purposes of approximately $25.1 million that will expire in the years 2021 ($14.8 million) and 2022 ($10.3 million), respectively. For the year ended December 31, 2007 total net deferred tax assets, including NOL carryforwards, comprised approximately 16% of our total assets. We became profitable in the second half of 2002 and have been profitable since that time with the exception of the first quarter of 2005, as further discussed above. Further, even though we expect to be profitable and generate taxable income in 2008 and beyond, we may not be able to sustain the necessary levels of taxable income to fully utilize our significant NOL carryforwards prior to expiration. There is considerable management judgment necessary to determine future taxable income, and accordingly, actual results could vary significantly from such estimates. Accordingly, the recorded amount of the deferred tax assets considered realizable could be reduced in the near term if estimates of future taxable income during the carryforward periods are reduced. If this occurs, our results of operations, financial condition and cash flows could be seriously harmed.

The National Information Consortium Voting Trust owns a significant amount of our common stock, which may impede attempts to replace or remove our board or management.

As of December 31, 2007, The National Information Consortium Voting Trust owned approximately 34% of our outstanding common stock. This concentration of ownership may have the effect of delaying or preventing a change in control or changes in management, or limiting the ability of other shareholders to approve or disapprove transactions that they may deem in their best interest.

25

The resale of shares owned by the National Information Consortium Voting Trust might adversely affect our stock price.

The National Information Consortium Voting Trust may sell shares in the open market from time to time without advance notice to us or to the market. Sales of substantial amounts of shares of our common stock in the public market, or the perception that those sales may occur, could cause the market price of our common stock to decline or make it more difficult for us to sell equity securities in the future at a time and a price that we consider appropriate.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Our principal administrative office occupies a total of approximately 20,000 square feet of leased space at 25501 West Valley Parkway, Suite 300, Olathe, Kansas 66061. All of our subsidiaries also lease their facilities. We do not own any real property and do not currently anticipate acquiring real property or buildings in the foreseeable future.

ITEM 3. LEGAL PROCEEDINGS

As disclosed in a Form 8-K and in a press release issued on February 6, 2008, as well as under Item 1A of this Form 10-K, we are currently the subject of an informal SEC inquiry of expense reporting by certain officers of the Company and certain potentially related matters. In connection with that inquiry, a review was undertaken by the Audit Committee of our Board of Directors, with the assistance of outside, independent counsel, which focused on such expense reporting. The review revealed that expense reimbursement deficiencies occurred during the period from January 2004 through October 2006 related to Jeffery S. Fraser, who was then our Chief Executive Officer, and that the amount of such deficiencies was not material to our financial condition or results of operations.

In addition, the Company is involved from time to time in legal proceedings and litigation arising in the ordinary course of business. However, the Company is not currently involved with any other legal proceedings.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

No matters were submitted to a vote of the shareholders during the fourth quarter of fiscal 2007.

26

PART II

| ITEM 5. | | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock trades on the NASDAQ Global Select Market under the symbol “EGOV.” The following table shows the range of high and low sales prices reported on the NASDAQ Global Select Market for the periods indicated. On February 29, 2008, the closing price of our common stock was $6.02.

| Fiscal Year Ended December 31, 2006 | | High | | Low |

| First Quarter | | $6.60 | | $5.57 |

| Second Quarter | | $7.52 | | $5.88 |

| Third Quarter | | $7.09 | | $4.96 |

| Fourth Quarter | | $5.76 | | $4.44 |

| |

| Fiscal Year Ended December 31, 2007 | | High | | Low |

| First Quarter | | $5.82 | | $4.96 |

| Second Quarter | | $6.94 | | $5.23 |

| Third Quarter | | $7.70 | | $6.23 |

| Fourth Quarter | | $8.90 | | $6.70 |

As of February 29, 2008, there were approximately 285 holders of record of shares of our common stock.

Dividend Policy

On February 4, 2008, the NIC Board of Directors declared a special cash dividend of $0.25 per share, payable to shareholders of record as of February 18, 2008. The dividend, totaling approximately $15.7 million, was paid on February 28, 2008, out of the Company’s available cash and marketable securities.

On January 29, 2007, our Board of Directors declared a special cash dividend of $0.75 per share, payable to shareholders of record as of February 12, 2007. The dividend, totaling approximately $46.7 million, was paid on February 20, 2007 out of the Company’s available cash and marketable securities. Any future determination as to the payment of dividends will be made at the discretion of our Board of Directors and will depend on our operating results, financial condition, capital requirements, general business conditions and such other factors as the Board of Directors deems relevant.

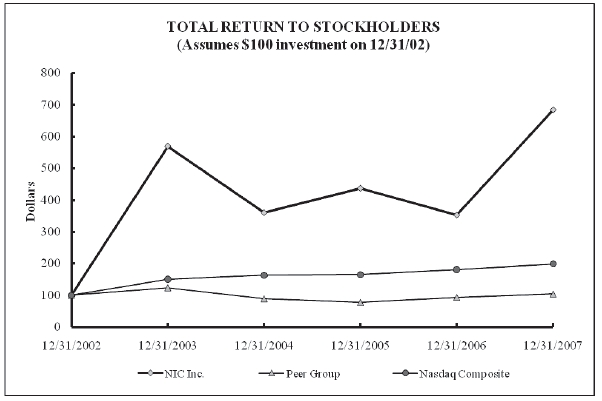

Performance Graph

The following performance graph below compares the annual change in our cumulative total shareholder return on our common stock during a period commencing on December 31, 2002, and ending on December 31, 2007 (as measured by dividing (i) the sum of (A) the cumulative amount of dividends for the measurement period, assuming dividend reinvestment and (B) the difference between our share price at the end and the beginning of the measurement period; by (ii) the share price at the beginning of the measurement period) with the cumulative total return of each of: (a) the NASDAQ Composite (U.S.) Index and (b) a Peer Group, assuming a $100 investment on December 31, 2002. It should be noted that on February 20, 2007 we paid a special cash dividend of $0.75 per share, which is included in the presentation of our performance. We did not pay any other dividends on our common stock during the period commencing on December 31, 2002, and ending on December 31, 2007. The stock price performance on the graph below is not necessarily indicative of our future price performance.

27

Comparison of Cumulative Total Return Among

NIC Inc., NASDAQ Composite (U.S.) Index and a Peer Group

| Total Return Analysis | | 12/31/2002 | | 12/31/2003 | | 12/31/2004 | | 12/31/2005 | | 12/31/2006 | | 12/31/2007 |

| NIC Inc. | | $100.00 | | $569.50 | | $360.28 | | $436.88 | | $352.48 | | $683.45 |

| Peer Group | | $100.00 | | $123.24 | | $ 88.13 | | $ 76.94 | | $ 92.73 | | $103.19 |

| Nasdaq Composite | | $100.00 | | $150.01 | | $162.89 | | $165.13 | | $180.85 | | $198.60 |

The Peer Group consists of seven companies, each of whose business focus is similar to that of NIC. While not all of the companies provide services exclusively to governments, the services provided are similar to those we provide. The members of the Peer Group are as follows: PEC Solutions, Inc. (PECS), Bearing Point, Inc. (BE) (formerly known as KPMG Consulting, Inc. (KCIN)), Accenture, Ltd. (ACN), International Business Machines Corp. (IBM), Maximus, Inc. (MMS), American Management Systems, Inc. (AMSY) and Official Payments Corporation (OPAY). Bearing Point, Inc. began trading publicly on February 8, 2001, and Accenture, Ltd. began trading publicly on July 18, 2001. American Management Systems, Inc. was included until May 3, 2004, when, as a result of the merger with CGI Group, Inc., it was no longer a member of the Peer Group. PEC Solutions, Inc. was included until April 26, 2005, when, as a result of its merger with a subsidiary of Nortel Networks, Inc., it was no longer a member of the Peer Group.

The performance graph and related text are being furnished to and not filed with the SEC, and will not be deemed to be “soliciting material” or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to the liabilities of Section 18 of the Securities Exchange Act of 1934, and will not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate such information by reference into such a filing.

28

(c) During 2007, the Company acquired shares of common stock surrendered by employees to pay income taxes due upon the vesting of restricted stock and to pay the exercise price for stock options, as follows:

| | | | | | | Total Number of | | Maximum Number (or |

| | | Total | | | | Shares Purchased | | Approximate Dollar Value) |

| | | Number of | | Average | | as Part of Publicly | | of Shares that May Yet Be |

| | | Shares | | Price Paid | | Announced Plans or | | Purchased Under the Plans or |

| Period | | Purchased | | per Share | | Programs | | Programs |

| June 1, 2007 | | | 1,182 | | | $5.70 | | N/A | | N/A |

| July 24, 2007 | | | 1,223 | | | $7.03 | | N/A | | N/A |

| July 28, 2007 | | | 36,192 | | | $6.74 | | N/A | | N/A |

| August 15, 2007 | | | 20,500 | | | $7.21 | | N/A | | N/A |

| August 17, 2007 | | | 11,254 | | | $7.52 | | N/A | | N/A |

| September 24, 2007 | | | 7,254 | | | $7.08 | | N/A | | N/A |

| October 19, 2007 | | | 6,045 | | | $7.10 | | N/A | | N/A |

ITEM 6. SELECTED CONSOLIDATED FINANCIAL DATA

The selected consolidated financial data set forth below should be read in conjunction with the consolidated financial statements and related notes, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” included in this Form 10-K.

| | | Year Ended December 31, |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 |

| Consolidated Statement of Income Data: | | (in thousands, except per share data) |

| Total revenues | | $50,831 | | $55,762 | | $59,243 | | $71,376 | | $85,755 |

| Operating income | | 7,338 | | 11,800 | | 10,191 | | 16,148 | | 16,127 |

| Income from continuing operations | | 6,328 | | 7,105 | | 6,363 | | 10,739 | | 11,955 |

| Net income | | 6,328 | | 7,105 | | 6,363 | | 10,739 | | 11,955 |

| Income per share from continuing operations – basic | | 0.11 | | 0.12 | | 0.11 | | 0.17 | | 0.19 |

| Income per share from continuing operations – diluted | | 0.11 | | 0.12 | | 0.10 | | 0.17 | | 0.19 |

| Net income per share – basic | | 0.11 | | 0.12 | | 0.11 | | 0.17 | | 0.19 |

| Net income per share – diluted | | 0.11 | | 0.12 | | 0.10 | | 0.17 | | 0.19 |

As further discussed in Note 2 in the Notes to Consolidated Financial Statements included in this Form 10-K, we recorded a $5.0 million charge for the anticipated contract loss under our contract with the California Secretary of State in the first quarter of 2005.

| | | December 31, |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 |

| Consolidated Balance Sheet Data: | | (in thousands, except for dividends declared) |

| Total assets | | $85,740 | | $93,071 | | $117,845 | | $140,134 | | $ | 111,376 |

| Long-term debt (includes current portion of notes payable/ | | | | | | | | | | | |

| capital lease obligations) | | 363 | | — | | — | | — | | | — |

| Dividends declared per share outstanding on | | | | | | | | | | | |

| February 12, 2007 | | — | | — | | — | | — | | $ | 0.75 |

| Total shareholders’ equity | | 63,164 | | 72,260 | | 85,168 | | 99,254 | | | 66,865 |

As further discussed in Note 9 in the Notes to Consolidated Financial Statements included in this Form 10-K, we paid a special dividend totaling approximately $46.7 million out of our available cash and marketable securities in February 2007.

29

| ITEM 7. | | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Caution about Forward-Looking Statements

“Safe Harbor” statement under the Private Securities Litigation Reform Act of 1995: Statements in this Annual Report on Form 10-K regarding NIC and its business, which are not current or historical facts, are “ forward-looking statements” that involve risks and uncertainties. Certain matters discussed in this report may constitute forward-looking statements within the meaning of the federal securities laws that inherently include certain risks and uncertainties. Forward-looking statements include, but are not limited to, statements of plans and objectives, statements of future economic performance or financial projections, statements of assumptions underlying such statements, and statements of the Company’s or management’s intentions, hopes, beliefs, expectations or predictions of the future. For example, statements like we “expect,” we “believe,” we “plan,” we “intend” or we “anticipate” are forward-looking statements. Investors should be aware that our actual operating results and financial performance may differ materially from our expressed expectations because of risks and uncertainties about the future including those risks discussed in this 2007 Annual Report on Form 10-K. In addition, we will not necessarily update the information in this Form 10-K if any forward-looking statement later turns out to be inaccurate. Investors are cautioned not to put undue reliance on any forward-looking statement.

There are a number of important factors that could cause actual results to differ materially from those suggested or indicated by such forward-looking statements. These include, among others, the success of the Company in signing contracts with new states and government agencies, including continued favorable government legislation; NIC’s ability to develop new services; existing states and agencies adopting those new services; acceptance of eGovernment services by businesses and citizens; competition; and general economic conditions and the other factors discussed under “CAUTIONS ABOUT FORWARD LOOKING STATEMENTS” in Part I and “RISK FACTORS” in Part I, Item 1A of this 2007 Annual Report on Form 10-K. Investors should read all of these discussions of risks carefully.

What We Do – An Executive Summary

We are a leading provider of eGovernment services that help governments use the Internet to reduce costs and provide a higher level of service to businesses and citizens. We accomplish this currently through two divisions: our core portal outsourcing businesses and our software & services businesses.

In our core business, portal outsourcing, we enter into contracts primarily with state governments and design, build and operate Web-based portals on their behalf. We enter into long-term contracts, typically three to five years, and manage operations for each government partner through separate subsidiaries that operate as decentralized businesses with a high degree of autonomy. Our portals consist of Web sites and applications that we build, which allow businesses and citizens to access government information online and complete transactions, including applying for a permit, retrieving driver’s license records or filing a form or report. We help increase our government partners’ revenues by expanding the distribution of their information assets and increasing the number of financial transactions conducted with governments. We do this by marketing portal services and soliciting users to complete government-based transactions and to enter into subscriber contracts that permit users to access the portal and the government information contained therein in exchange for transactional and/or subscription user fees. We are typically responsible for funding up-front investment and ongoing operational costs of the government portals. Our unique self-funding business model allows us to reduce our government partners’ financial and technology risks and obtain revenues by sharing in the fees generated from eGovernment services. Our partners benefit because they gain a centralized, customer-focused presence on the Internet. Businesses and citizens gain a faster, more convenient and more cost-effective means to interact with governments.

On behalf of our government partners, we enter into separate agreements with various agencies and divisions of the government to provide specific services and to conduct specific transactions. These agreements preliminarily establish the pricing of the transaction and data access services we provide and the division of revenues between the Company and the government agency. The government must approve prices and revenue sharing agreements. We generally own all the applications developed under these contracts. After completion of a defined contract term, the government agency typically receives a perpetual, royalty-free license to the applications

30

for use only. If our contract were not renewed after a defined term, the government agency would be entitled to take over the portal in place with no future obligation of the Company. In some cases, we enter into contracts to provide consulting, development and portal management services to governments in exchange for an agreed-upon fee.

Currently, we have contracts to provide portal outsourcing services for 21 states. Our closest competitor operates one state portal. We also provide portal outsourcing services to three local governments.

Our objective is to strengthen our position as the leading provider of Internet-based eGovernment services. Key strategies to achieve this objective include:

- Renew all current outsourced government portal contracts –First and foremost, we will strive to obtain renewal of all currently profitable outsourced government portal contracts. In the history of our company, we have not lost a contract renewal opportunity or re-bid process and are very proud of our highly reference-able list of government partners.

- Win new portal contracts –A key objective of the Company in 2007 was to accelerate new state portal contract wins by making incremental expenditures in the areas of business development and marketing, through a combination of additional sales personnel, strategic advertising and public relations initiatives. In 2008, we will continue with similar levels of investment in business development and portal operations to drive long-term growth. Our goal is to continue expanding our number of government partners by leveraging our strong relationships with current government partners and our reputation for providing proven eGovernment services. We intend to continue marketing our services to new governments. Our expansion efforts include developing relationships and sponsors throughout an individual government entity, pursuing strategic technology alliances, making presentations at conferences of government executives with responsibility for information technology policy, and developing contacts with organizations that act as forums for discussions between these executives.

- Increase transactional revenues from our existing government portals –Part of our strategy is to increase transactional revenues from our existing government portals by building new applications and services, taking successful applications and services and implementing them in our other government portal states, and increasing the adoption of existing portal applications and services.

We intend to accomplish this with new service offerings, increased operational focus and expanded marketing initiatives. In addition, we will work closely with the governance entities in our partner portals to evaluate the pricing of new and existing services to encourage higher usage and increased revenue streams. We plan to continue our development of new online transactional services that enable government agencies to interact more effectively and efficiently with businesses, citizens and other government agencies. We will continue to work with government agencies, professional associations and other organizations to better understand the current and future needs of our customers. We will continue to work with our government partners to create awareness of the online alternatives to traditional government interaction through initiatives such as informational brochures, government voicemail recordings and inclusion of Web site information on government communication materials. In addition, we will continue to update our portals to highlight new government service information provided on the portals. We plan to work with professional associations to directly and indirectly communicate to their members the potential convenience, ease of use and other benefits of the services our portals offer.

In addition to overall portal revenue growth, which includes both organic revenue growth and growth from new portal contract wins, an important financial metric that we use to gauge our success in increasing transactional revenues in our existing portal businesses is same state revenue growth. Prior to July 1, 2006, we defined same state revenues as those from states in operation and generating DMV revenues for two full years. DMV revenues are transaction fees that we earn from the sale of driver history records through the portals we operate. Our Indiana portal subsidiary signed a new long-term contract with the state of Indiana that commenced on July 1, 2006. This contract is based on a funding model that includes recurring fixed monthly fees for baseline services and primarily time and materials pricing for variable services. Historically, the majority of revenues under this contract were DMV and non-DMV transaction-based. Under the new contract, the majority of revenues will be classified

31

as portal management. Because the majority of revenues from the new Indiana contract are generally recurring, we will continue to include Indiana portal revenues in the calculation of same state revenue growth even though we no longer earn DMV transaction-based revenues under the contract. In June 2007, we signed a similar long-term contract with the state of Arizona that is based on a funding model that includes recurring fixed monthly fees for baseline services and primarily time and materials pricing for variable services. Under this contract, the majority of revenues will be classified as portal management.

Our long-term goal is to grow same state revenues 10-15% per year, absent online DMV price increases. Same state portal revenues grew 15% in 2007, 10% in 2006 and 17% in 2005. Our same state revenue growth in 2007 was higher than our growth in prior years primarily due to increases in same state DMV and non-DMV transaction based revenue growth. In 2007, same state DMV revenues grew by 10% (excluding Indiana from the calculation) primarily due to DMV price increases in three of our portal states in late 2006 and in one portal state in the third quarter of 2007. In 2006, same state DMV revenues grew by 3% (excluding Indiana from the calculation) and were not impacted by DMV price increases. In 2005, same state DMV revenues grew by 9% primarily due to DMV price increases in two of our portal states in late 2004. Historically, DMV price increases have been relatively infrequent, and our ability to grow same state DMV revenues has been limited, as such revenues have been driven by broader economic factors outside of our control. Absent DMV price increases, same state DMV revenues have historically grown at a rate of 1% to 3% per year.

An important component of same state revenue growth is the growth in non-DMV transaction revenues, which are transaction fees generated by other means than from the sale of DMV records, for transactions conducted primarily by business users and, to a lesser extent, consumer users through our portals. In 2007, same state non-DMV revenues grew 31% (excluding Indiana from the calculation), up from 27% in 2006 and down from 41% in 2005. We are able to grow non-DMV revenues by continually deploying new revenue generating applications and by driving adoption of existing applications within our existing portal businesses. We believe a key factor in organically growing our revenues is to continually focus on driving adoption, and on implementation of new non-DMV revenue generating applications.

- Continue to grow profitability –In addition to driving same state revenue growth, part of our strategy is to increase profitability by driving cost containment efforts throughout the Company and maintaining a lean organizational structure that fosters entrepreneurial decision-making and innovation and accentuates the strong financial leverage of our business model.

An important financial metric that we use to gauge our portal profitability is portal gross profit percentage, or gross profit rate, which is calculated by dividing portal gross profit (portal revenues minus cost of portal revenues, excluding depreciation and amortization) by portal revenues. Our long-term outlook is for our portal gross profit rate to be in the 45-50% range. Our portal gross profit rate was 47% in 2007 and 2006, down from 49% in 2005. The decrease in 2006 was partially attributable to additional personnel in several of our portals due to our continued growth and reinvestment in our core business, coupled with mid-year 2006 non-executive salary increases across all portals that were in addition to normal annual increases, in an effort to better align our employee compensation structure with the general market. Also contributing to this decrease was an increase in bank fees. A growing percentage of our non-DMV transaction-based revenues are generated from online applications whereby users pay for information or transactions via credit cards. We typically earn a percentage of the credit card transaction amount, but also must pay an associated fee to the bank that processes the credit card transaction. We earn a lower gross profit percentage on these transactions as compared to our other non-DMV applications. However, we plan to continue to implement these services as they contribute favorably to our operating income growth. We carefully monitor our portal gross profit percentage to strike the balance between generating a solid return for our shareholders and delivering value to our government partners through reinvestment in our portal operations. We currently expect our portal gross profit percentage to range from 45% to 47% in 2008.

32

We also view selling & administrative costs, expressed as a percentage of portal revenue, to be an important indicator of the relative year-over-year growth in our corporate level expenses. Selling & administrative costs as a percentage of portal revenue were 26% in 2007, 22% in 2006 and 22% in 2005. In 2007, the increase in selling & administrative costs as a percentage of portal revenue resulted primarily from our incremental investment in business development and portal operations to drive long-term growth, as further discussed above. In 2008, we expect selling & administrative costs as a percentage of portal revenue to range from 24% to 25%, which reflects a return to historical levels of modest expense growth. We also expect depreciation and amortization expense as a percentage of portal revenue to range from 3% to 4%, as we will continue to make key IT infrastructure and security investments to support our long-term expansion and enhance corporate-wide information technology security and portal operations.

Finally, our consolidated operating margin (operating income or loss divided by portal revenues) is an important measure of our overall profitability. This metric decreased to 20% in 2007, down from 23% in 2006 and up from 18% in 2005. The decrease in 2007 resulted from our incremental investment in business development and portal operations to drive long-term growth, as further discussed above. The decrease in 2005 was mainly due to the effect of the adjustment under percentage of completion accounting recorded in the first quarter of 2005 relating to our contract with the California Secretary of State, which resulted in a $3.5 million reduction in software & services revenues in 2005 as further discussed below.

Overview of Business Models and Revenue Recognition

We classify our revenues and cost of revenues into two categories: (1) portal and (2) software & services. The portal category includes revenues and cost of revenues primarily from our subsidiaries operating government portals on an outsourced basis. The software & services category includes revenues and cost of revenues primarily from our UCC and corporate filings and ethics & elections businesses. We currently derive revenue from two main sources: transaction-based fees and fees for application development. Each of these revenue types and the corresponding business models are further described below.

Our portal outsourcing businesses

We categorize our portal revenues according to the underlying source of revenue. A brief description of each category follows:

- DMV transaction-based: these are transaction fees from the sale of electronic access to driver history records, referred to as DMV records, from our state portals to data resellers, insurance companies and other pre-authorized customers on behalf of our state partners, and are generally recurring.

- Non-DMV transaction-based: these are transaction fees from sources other than the sale of DMV records, for transactions conducted by business users and consumer users through our portals, and are generally recurring. For a representative listing of non-DMV services we currently offer through our portals, refer to Part I, Item 1 in this Form 10-K.

- Software development & portal management: these are fees from the performance of software development projects and other time and materials or fixed fee services for our government partners. While we actively market portal software development services, they do not have the same degree of predictability as our transaction-based or portal management revenues.

The highest volume, most commercially valuable service we offer is electronic access to DMV records through our insurance industry records exchange network. This service accounted for approximately 54% of our portal revenues in 2007, 59% in 2006 and 62% in 2005. We believe that while this application will continue to be an important source of revenue, its contribution as a percentage of total revenues on an individual portal basis will decline modestly as other sources grow. ChoicePoint, which resells these records to the auto insurance industry, accounted for approximately 40% of portal revenues in 2007, 47% in 2006 and 46% in 2005.

33

In our outsourced portal businesses for 2007, DMV transaction-based revenues represented approximately 54% of portal revenues, non-DMV transaction-based revenues represented approximately 34%, and software development & portal management revenues represented 12%. Software development & portal management revenues as a percentage of total portal revenues increased modestly in 2007 due to our new Arizona portal contract and the Indiana portal contract, as further discussed above. Approximately 85% of our transaction-based revenues related to business-to-government transactions, while the remaining 15% related to citizen-to-government transactions.

Transaction-based revenues from our outsourced state portal business units are highly correlated to population, but are also affected by pricing policies established by government entities for public records, the number and growth of commercial enterprises and the government entity’s development of policy and information technology infrastructure supporting electronic government.

ChoicePoint and other data resellers and companies who access DMV records electronically through our insurance industry records exchange network have entered into contracts with the portals our subsidiaries operate to request these records from the various states with which we have contracts. Under the terms of these contracts, we provide data resellers with driver’s license and traffic records that vary by contract, for fees that currently range from $2.00 to $20.00 per record requested. The fees charged to all entities that access DMV records are the same for records of a particular state. We typically collect the entire fee, of which a certain portion is remitted to the state by statute. These contracts are generally self-renewing until canceled by one side or the other, and generally may be terminated at any time after 60-days notice. These contracts may be terminated immediately at the option of any party upon a material breach of the contract by the other party. Furthermore, these contracts are immediately terminable if the state statute allowing for the public release of these records is repealed.

We charge for electronic access to records on a per-record basis and, depending upon government policies, also on a fixed or sliding scale bulk basis. Our fees are set by negotiation with the government agencies that control the records and are typically approved by a government sanctioned oversight body. We recognize revenues from transactions (primarily transaction-based information access fees and filing fees) on an accrual basis net of the transaction fee due to the government, and we bill end-user customers primarily on a monthly basis. We typically receive a majority of payments via electronic funds transfer and credit card within 25 days of billing and remit payment to governments within 30 to 45 days of the transaction. The costs that we pay state agencies for data access are accrued as accounts receivable and accounts payable at the time revenue from the access of public information is recognized. We must remit a certain amount or percentage of these fees to government agencies regardless of whether we ultimately collect the fees. The pricing of transactions varies by the type of transaction and by state.

We expense as incurred all employee costs to start up, operate and maintain outsourced government portals as costs of performance under the contracts because, after the completion of a defined contract term, the government entities with which we contract typically receive a perpetual, royalty-free license to the applications we developed. Such costs are included in cost of portal revenues in the consolidated statements of income.

Our software & services businesses

UCC and corporate filings

Our UCC and corporate filings software development business derives the majority of its revenues from fixed-price application development contracts and recognizes revenues on the percentage of completion method. At December 31, 2007, this business was primarily engaged in servicing its contract with the California Secretary of State, as further discussed below, and no longer markets its applications and services in respect of new engagements.

Ethics & elections

Our ethics & elections business derives the majority of its revenues from time and materials application development and maintenance outsourcing contracts and recognizes revenues as services are provided. At December 31, 2007, our ethics & elections business was primarily engaged in servicing its contracts with the Federal Election Commission and the state of Michigan.

34

Critical Accounting Policies

Many estimates and assumptions involved in the application of generally accepted accounting principles have a material impact on reported financial condition and operating performance and on the comparability of such reported information over different reporting periods. A critical accounting policy is one which is both important to the portrayal of the Company’s financial condition and results of operations and requires management’s most difficult, subjective or complex judgments, often as a result of the need to make estimates and assumptions about the effect of matters that are inherently uncertain. Our significant accounting policies are described in Note 2 to the Notes to Consolidated Financial Statements included in this Form 10-K. We have identified the policies below as critical to our business operations and the understanding of our results of operations. Note that the preparation of our consolidated financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. There can be no assurance that actual results will not differ from those estimates.

Management has discussed the development and selection of the critical accounting policies described below with the Audit Committee of the Board of Directors, and the Audit Committee has reviewed the Company’s disclosure relating to it in this Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Uncertain Tax Positions

We account for uncertain tax positions in accordance with FASB Interpretation No. (“FIN”) 48, “Accounting for Uncertainty in Income Taxes – an interpretation of FASB Statement No. 109.” The application of income tax law is inherently complex. Laws and regulations in this area are voluminous and are often ambiguous. As such, we are required to make many subjective assumptions and judgments regarding our income tax exposures. Interpretations of and guidance surrounding income tax laws and regulations change over time. As such, changes in our subjective assumptions and judgments can materially affect amounts recognized in the consolidated balance sheets and statements of income. See Notes 2 and 10 in the Notes to the Consolidated Financial Statements included in this Form 10-K for additional detail on our adoption of FIN 48 in the first quarter of 2007 and our uncertain tax positions.

Deferred income taxes

We recognize deferred income taxes for the tax consequences in future years of differences between the tax basis of assets and liabilities and their financial reporting amounts at each year-end based on enacted laws and statutory tax rates applicable to the periods in which the differences are expected to affect taxable income. Valuation allowances are established, when necessary, to reduce deferred tax assets to the amount expected to be realized.

We have a history of unprofitable operations prior to 2003 primarily due to operating losses incurred in our software & services businesses. These losses generated significant federal tax net operating losses, or NOLs. We had available at December 31, 2007, total NOL carryforwards for federal tax purposes of approximately $25.1 million that will expire in the years 2021 ($14.8 million) and 2022 ($10.3 million), respectively. We became profitable in the second half of 2002. We currently expect the Company to continue to be profitable and generate taxable income, and have focused the business on operations that have demonstrable ability to produce positive taxable income and sustainable cash flow in the future. We believe it is more likely than not that we will generate sufficient taxable income from future operations to fully utilize the NOL carryforwards prior to expiration. Based on our current projections, we currently expect to fully utilize the NOL carryforwards by the end of 2009. The recorded amount of the deferred tax assets considered realizable could be reduced in the near term if estimates of future taxable income during the carryforward periods are reduced. There is considerable management judgment necessary to determine future taxable income, and accordingly, actual results could vary significantly from such estimates. For additional discussion of deferred income taxes, see Note 10 in the Notes to Consolidated Financial Statements included in this Form 10-K. For the years ended December 31, 2007 and 2006, total net deferred tax assets, including NOL carryforwards, comprised approximately 16% of our total assets.

35

Valuation of Marketable Securities

Our short-term investments at December 31, 2007, consist entirely of marketable auction-rate debt securities. The fair values for marketable debt securities are determined by independent pricing sources that value the securities based on market prices or broker quotes and pricing models. Considerable judgment is required in determining the assumptions used in valuation models for our auction-rate debt securities, including interest rate, credit risk and liquidity risk assumptions. Significant changes in these assumptions can have a significant effect on carrying value.

We assess other-than-temporary impairment of marketable debt securities in accordance with FASB Staff Position No. FAS 115-1, “The Meaning of Other-Than-Temporary Impairment and its Application to Certain Investments.” This assessment requires significant judgment. In making this determination, we employ a systematic methodology that considers available quantitative and qualitative evidence in evaluating potential impairment of our investments. If the cost of an investment exceeds its fair value, we evaluate general market conditions, earnings performance, credit rating, asset quality, and other key measures for our investments. We also consider the duration and extent to which the fair value has been less than cost, and our ability and intent to hold the investment. Once a decline in fair value is determined to be other-than-temporary, an impairment charge is recorded and a new costs basis in the investment is established. We have not recorded any other-than-temporary impairments for marketable debt securities. However, if market, industry and/or investee conditions deteriorate, we may record impairments in the future, which could be material.

Application development contracts

Our UCC and corporate filings software development business, NIC Conquest, derives the majority of its revenues from fixed-price application development contracts and recognizes revenues on the percentage of completion method, utilizing costs incurred to date as compared to the estimated total costs for each contract. This method is used because management considers expended costs to be the best available measure of progress on our fixed-price contracts and results in our recognizing contract revenues over the contract term in proportion to our incurrence of contract costs. The earnings or losses recognized on individual contracts are based on management’s estimates of contract revenues and costs. Contract losses are recognized in full when determined, and contract profit estimates are adjusted based on ongoing reviews of contract profitability. Use of the percentage of completion method requires that management be able to reasonably estimate total contract costs and costs to complete at each reporting date. We continuously review and reassess our estimates of contract profitability.

Our UCC and corporate filings software development business has incurred substantial losses under its fixed-price contracts primarily due to cost overruns. As recently as the first quarter of 2005, we recorded a $5.0 million charge due to anticipated cost overruns on our contract with the California Secretary of State (as further discussed below and in Note 2 to the Notes to Consolidated Financial Statements included in this Form 10-K). In June 2006, the California Secretary of State officially accepted the UCC system, which also commenced the maintenance and operations phase of the contract. However, it is possible that our costs will similarly exceed revenues in the future, as a result of unforeseen difficulties such as rising development, subcontractor and personnel costs or other reasons. If this occurs, the Company’s results of operations, financial condition and cash flows could be adversely affected. Because of the inherent uncertainties in estimating the costs of completion, it is at least reasonably possible that our estimates will change in the near term.

Financial Analysis of Years Ended December 31, 2007, 2006 and 2005

In this section, we are providing more detailed information about our operating results and changes in financial position over the past three years. This section should be read in conjunction with the consolidated financial statements and related notes included in this Form 10-K.

California Secretary of State Contract

Results of operations for the year ended December 31, 2005 include a $5.0 million charge we recorded on our software & services engagement with the California Secretary of State (the “California SOS”) in the first quarter of 2005, as further discussed in Note 2 in the Notes to Consolidated Financial Statements included in this Form 10-K. Prior to the first quarter of 2005, key elements of our obligations under the California SOS contract were

36

subcontracted to various third parties under fixed price contracts. At the end of the first quarter of 2005, as a result of system delivery issues and the concern over the ability of one of the two remaining subcontractors to meet the criteria set forth by the California SOS, we determined we would assume the lead project manager role on the contract, which was previously performed by this subcontractor. As a result of this change, we further evaluated the status of the project and concluded that a further modification to the management and oversight structure of the project was necessary to improve performance under the contract and that additional internal project management and technical personnel would be required on the engagement. We also reevaluated the expected completion date of the project, which was previously estimated to be in the first quarter of 2006, and determined to revise the estimated completion date to the end of 2006. As a result of our decision to commit these additional resources and the extension of the expected project completion date, we recorded a $5.0 million adjustment under percentage of completion accounting in the first quarter of 2005, as we expected to incur a loss of approximately $4.2 million on this project, instead of a previously projected profit of approximately $1.0 million.

The adjustment in our consolidated statement of income for the year ended December 31, 2005 resulted in a reduction of software & services revenues of approximately $3.5 million and an increase in cost of software & services revenues of approximately $1.5 million.The adjustment in our consolidated balance sheet was a reduction in unbilled revenues of approximately $3.5 million and an increase in application development contracts (a current liability) of approximately $1.5 million.

In March 2006, we entered into an amendment to our contract with the California SOS. Among other changes, the amendment reduced the aggregate contract value from approximately $25 million to approximately $19 million, and released us from the obligation to deliver the business filings, or BE, portion of the project, except for maintenance of hardware and delivery of BE images as expressly set forth in the amendment. The amendment also set forth the final criteria in order for the California SOS to accept the Uniform Commercial Code, or UCC, portion of the project and move it into the maintenance and operations phase.

As a result of the amendment, we recorded an adjustment under percentage of completion accounting in the first quarter of 2006. The adjustment in our consolidated statement of income for the year ended December 31, 2006 resulted in a reduction of software & services revenues of approximately $2.1 million and a reduction of cost of software & services revenues of approximately $2.1 million. The adjustment in our consolidated balance sheet was a reduction in unbilled revenues of approximately $2.1 million, a reduction of accrued liabilities of approximately $1.6 million, and a reduction of application development contracts of approximately $0.5 million. This adjustment did not affect operating income, net income or earnings per share.

In June 2006, the California SOS officially accepted the UCC portion of the project, which also commenced the 42-month maintenance and operations phase.

We regularly review our cost estimates to complete and do not currently believe our estimated contract loss will exceed the $4.2 million estimate established in the first quarter of 2005. However, it is at least reasonably possible that our estimate will change in the near term. Further, it is possible that we will similarly incur cost overruns in the future as we have in the past as a result of unforeseen difficulties such as rising development, subcontractor and personnel costs or other reasons. If this occurs, our results of operations, financial condition and cash flows could be adversely affected.

At December 31, 2007, our corporate filings software & services business was primarily engaged in servicing the maintenance and operations obligation under its contract with the California SOS. This business is not marketing its applications and services for new engagements.

Stock-Based Compensation

In December 2004, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting Standards (“SFAS”) No. 123R (revised 2004), “Share–Based Payment,” that requires companies to expense the grant-date fair value of stock options and other equity-based compensation issued to employees. SFAS No. 123R eliminates the use of the intrinsic value method prescribed in Accounting Principles Board Opinion (“APB”) No. 25, “Accounting for Stock Issued to Employees,” that we used to account for our stock-based compensation plans prior to January 1, 2006.

37

Effective January 1, 2006, we adopted the provisions of SFAS No. 123R using the modified prospective application transition method, which did not require us to restate our financial statements prior to the effective date of SFAS No. 123R. For vested stock option awards that were outstanding on January 1, 2006, the modified prospective application transition method did not require us to record any additional compensation expense. For unvested stock option awards that were outstanding on January 1, 2006, awards that were previously included as part of the pro forma net income and earnings per share calculations of SFAS No. 123 have been charged to expense over the remaining vesting period, without any changes in measurement. For all new equity-based awards that have been granted or modified after January 1, 2006, we have used SFAS No. 123R’s measurement model, expense recognition, and settlement provisions.

Prior to the adoption of SFAS No. 123R, we did not recognize stock-based compensation expense if the exercise price of stock options granted to employees or nonemployee directors was greater than or equal to the price of our common stock on the grant date. In addition, we did not recognize stock-based compensation expense for shares issued under our employee stock purchase plan. Beginning January 1, 2006 with the adoption of SFAS No. 123R, we began recognizing stock-based compensation expense for the cost of stock options, restricted stock awards and shares issued under our employee stock purchase plan. The following table presents stock-based compensation expense included in our consolidated statements of income for the years ended December 31, 2006 and 2007 (in thousands):

| | Year Ended December 31, |

| | 2007 | | 2006 |

| Cost of portal revenues, exclusive of depreciation & amortization | $ | 411 | | | $ | 346 | |

| Cost of software & services revenues, exclusive of depreciation | | | | | | | |

| and amortization | | 18 | | | | 19 | |

| Selling & administrative | | 1,248 | | | | 966 | |

| Stock-based compensation expense before income taxes | | 1,677 | | | | 1,331 | |

| Income tax benefit | | (655 | ) | | | (520 | ) |

| Net stock-based compensation expense | $ | 1,022 | | | $ | 811 | |

As of December 31, 2007, there was approximately $0.3 million of total unrecognized compensation cost, net of estimated forfeitures, related to nonvested stock options and approximately $2.1 million of total unrecognized compensation cost, net of estimated forfeitures, related to nonvested restricted stock awards. We expect to recognize the cost related to stock options over a weighted-average period of 1.2 years and the cost related to restricted stock awards over the next 3.0 years. We did not grant any stock options during the year-ended December 31, 2007 and 2006, and do not currently anticipate granting stock options in the future. Instead, the Company expects to grant only restricted stock awards.

On October 26, 2005, our Board of Directors approved the acceleration of vesting of all unvested options to purchase common stock of the Company that had an exercise price that was greater than the market price on that date. The closing price of our common stock on the NASDAQ Global Select Market on October 26, 2005 was $5.63 per share. As a condition of the acceleration and to prevent unintended personal benefit, the Company’s directors, executive officers and employees must refrain from selling common stock acquired upon the exercise of accelerated options until the original vesting date or, if earlier, termination of employment with or service to the Company. All other terms and conditions applicable to such options, including exercise prices, remained unchanged. This action resulted in the accelerated vesting of options to purchase 163,873 shares of common stock of the Company, or approximately six percent of the total of all then-outstanding Company options.

We accelerated the vesting of these options because we believed it was in the best interest of our shareholders to reduce future compensation expense that we would otherwise have been required to report in our statement of income upon adoption of SFAS No. 123R in the first quarter of 2006. Further, because the options had exercise prices in excess of the then-current market price, they were viewed to have limited economic value and were not achieving their objective of incentive compensation and retention. As a result of the vesting acceleration, approximately $0.5 million in aggregate future expense was eliminated.

38

We believe that equity-based compensation, particularly restricted stock awards, will continue to play an important role in supporting employee retention and providing individuals with long-term incentives to meet Company goals. For additional information regarding our adoption of SFAS No. 123R, see Note 11 in the Notes to Consolidated Financial Statements included in this Form 10-K.

Results of Operations

| Key Financial Metrics | | 2007 | | 2006 | | 2005 |

| Revenue growth – outsourced portals | | 18 | % | | 21 | % | | 19 | % |

| Same state revenue growth – outsourced portals | | 15 | % | | 10 | % | | 17 | % |

| Recurring portal revenue % | | 93 | % | | 95 | % | | 96 | % |

| Gross profit % - outsourced portals | | 47 | % | | 47 | % | | 49 | % |

| Selling & administrative expenses as % of portal revenues | | 26 | % | | 22 | % | | 22 | % |

| Operating income margin % (operating income as a | | | | | | | | | |

| % of portal revenues) | | 20 | % | | 23 | % | | 18 | % |

PORTAL REVENUES. In the analysis below, we have categorized our portal revenues according to the underlying source of revenue (in thousands), with the corresponding percentage increase or decrease from the prior year period.

| | | | | Increase | | | | | Increase | | | |

| Portal Revenue Analysis | | 2007 | | from 2006 | | 2006 | | from 2005 | | 2005 |

| DMV transaction-based | | $ | 44,387 | | 8 | % | | $ | 41,247 | | 16 | % | | $ | 35,630 |

| Non-DMV transaction-based | | | 27,981 | | 21 | % | | | 23,165 | | 15 | % | | | 20,145 |