Filed by Provident Bancorp, Inc.

Subject Company: Provident Bancorp, Inc.

Pursuant to Rule 425 under the Securities Act of 1933

And Deemed Filed Pursuant to Rule 14a-12

Under the Securities Exchange Act of 1934

Commission File No. 0-25233

Provident Bancorp, Inc.

Expanding Market Footprint Through a Strategic Merger

Provident Bancorp, Inc., Montebello, NY

Acquisition of

Warwick Community Bancorp, Inc., Warwick, NY

Disclaimer

Statements contained in this news release that are not historical facts are forward-looking statements as that term is defined in the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to risks and uncertainties which could cause actual results to differ materially from those currently anticipated due to a number of factors.

Words such as “expect”, “feel”, “believe”, “will”, “may”, “anticipate”, “plan”, “estimate”, “intend”, “should”, and similar expressions are intended to identify forward-looking statements. These statements include, but are not limited to, financial projections and estimates and their underlying assumptions; statements regarding plans, objectives and expectations with respect to future operations, products and services; and statements regarding future performance. These statements are subject to certain risks and uncertainties, many of which are difficult to predict and generally beyond the control of Provident Bancorp, Inc. (PBCP) and Warwick Community Bancorp, Inc. (WSBI). The following factors, among others, could cause actual results to differ materially from the anticipated results or other expectations expressed in the forward-looking statements: (1) the businesses of PBCP and WSBI may not be combined successfully, or the combination may take longer to accomplish than expected; (2) the growth opportunities and cost savings from the merger may not be fully realized or may take longer to realize than expected; (3) operating costs and business disruption following the merger, including adverse effects on relationships with employees, may be greater than expected; (4) governmental approvals of the merger may not be obtained, or adverse regulatory conditions may be imposed in connection with governmental approvals of the merger; (5) the stockholders of either PBCP or WSBI may fail to approve the merger; (6) competitive factors which could affect net interest income and non-interest income, general economic conditions which could affect the volume of loan originations, deposit flows and real estate values; (7) the levels of non-interest income and the amount of loan losses as well as other factors discussed in the documents filed by PBCP and WSBI with the Securities and Exchange Commission from time to time. Neither PBCP nor WSBI undertakes any obligation to update these forward-looking statements to reflect events or circumstances that occur after the date on which such statements were made. This document may be deemed to be solicitation material in respect of the proposed merger of PBCP and WSBI. In connection with the proposed transaction, a registration statement on Form S-4 will be filed with the SEC. STOCKHOLDERS OF PBCP AND

STOCKHOLDERS OF WSBI ARE ENCOURAGED TO READ THE REGISTRATION STATEMENT AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE JOINT PROXY STATEMENT/PROSPECTUS THAT WILL BE PART OF THE REGISTRATION STATEMENT, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED MERGER. The final joint proxy statement/prospectus will be mailed to stockholders of PBCP and stockholders of WSBI. Investors and security holders will be able to obtain the documents free of charge at the SEC’s website, www.sec.gov, from Provident Bancorp, Inc., 400 Rella Boulevard, Montebello, New York 10901, Attention: Investor Relations, or from Warwick Community Bancorp, Inc., 18 Oakland Avenue, Warwick, New York 10990, Attention: Investor Relations.

PBCP, WSBI and their respective directors and executive officers and other members of management and employees may be deemed to participate in the solicitation of proxies in respect of the proposed transactions. Information regarding PBCP’s directors and executive officers is available in PBCP’s Form 10-KA, which was filed with the SEC on January 28, 2004, and information regarding WSBI’s directors and executive officers is available in WSBI’s proxy statement for its 2003 annual meeting of stockholders, which was filed on April 4, 2003. Additional information regarding the interests of such potential participants will be included in the joint proxy statement/prospectus and the other relevant documents filed with the SEC when they become available.

1

Transaction Overview

Complementary franchises in terms of markets, customers

and asset/liability mix

Accretive to earnings per share

Relatively low transaction risk

Enhances value for both PBCP and WSBI shareholders

Culturally similar

Pro forma ownership of WSBI shareholders approximates

13.6%

Requires WSBI shareholder approval

2

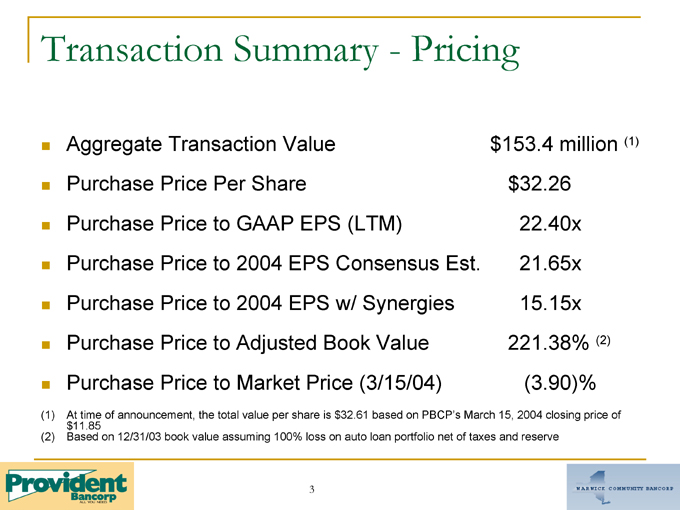

Transaction Summary—Pricing

Aggregate Transaction Value $153.4 million (1)

Purchase Price Per Share $ 32.26

Purchase Price to GAAP EPS (LTM) 22.40x

Purchase Price to 2004 EPS Consensus Est. 21.65x

Purchase Price to 2004 EPS w/ Synergies 15.15x

Purchase Price to Adjusted Book Value 221.38% (2)

Purchase Price to Market Price (3/15/04) (3.90)%

(1) At time of announcement, the total value per share is $32.61 based on PBCP’s March 15, 2004 closing price of $11.85 (2) Based on 12/31/03 book value assuming 100% loss on auto loan portfolio net of taxes and reserve

3

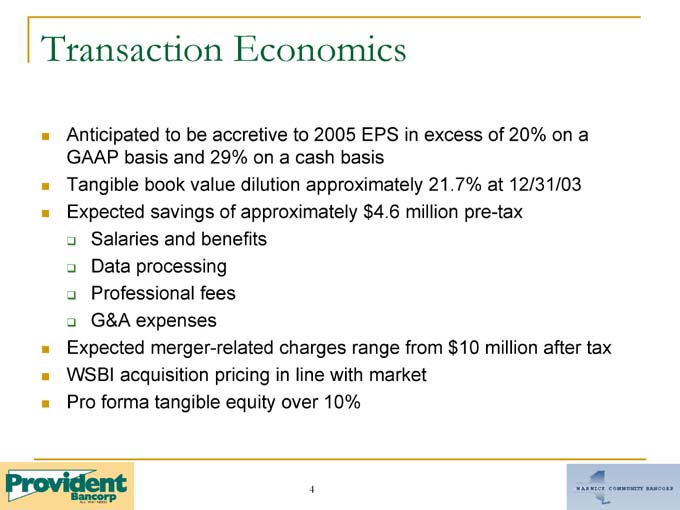

Transaction Economics

Anticipated to be accretive to 2005 EPS in excess of 20% on a GAAP basis and 29% on a cash basis

? Tangible book value dilution approximately 21.7% at 12/31/03

? Expected savings of approximately $4.6 million pre-tax

? Salaries and benefits

? Data processing

? Professional fees

? G&A expenses

? Expected merger-related charges range from $10 million after tax

? WSBI acquisition pricing in line with market

? Pro forma tangible equity over 10%

4

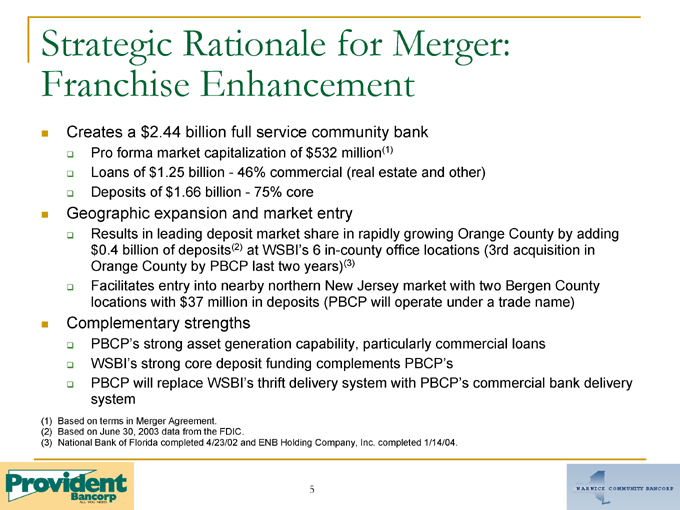

Strategic Rationale for Merger: Franchise Enhancement

Creates a $2.44 billion full service community bank

Pro forma market capitalization of $532 million(1)

Loans of $1.25 billion—46% commercial (real estate and other)

Deposits of $1.66 billion—75% core

Geographic expansion and market entry

Results in leading deposit market share in rapidly growing Orange County by adding $0.4 billion of deposits(2) at WSBI’s 6 in-county office locations (3rd acquisition in Orange County by PBCP last two years)(3)

Facilitates entry into nearby northern New Jersey market with two Bergen County locations with $37 million in deposits (PBCP will operate under a trade name)

Complementary strengths

PBCP’s strong asset generation capability, particularly commercial loans

WSBI’s strong core deposit funding complements PBCP’s

PBCP will replace WSBI’s thrift delivery system with PBCP’s commercial bank delivery system

(1) Based on terms in Merger Agreement.

(2) Based on June 30, 2003 data from the FDIC.

(3) National Bank of Florida completed 4/23/02 and ENB Holding Company, Inc. completed 1/14/04.

5

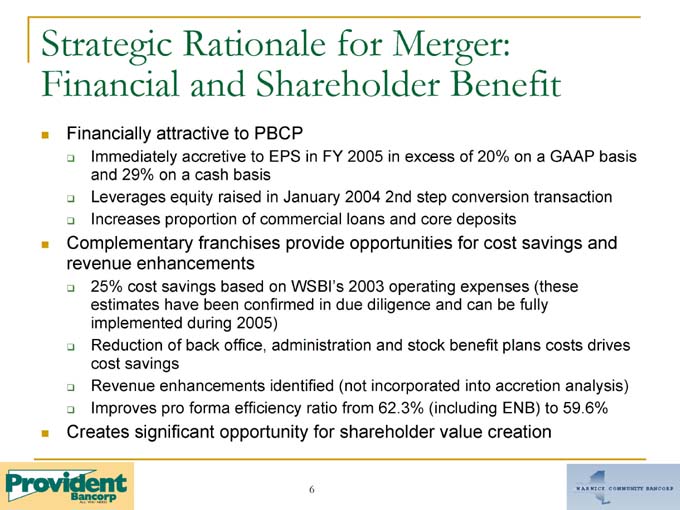

Strategic Rationale for Merger: Financial and Shareholder Benefit

? Financially attractive to PBCP

? Immediately accretive to EPS in FY 2005 in excess of 20% on a GAAP basis and 29% on a cash basis

? Leverages equity raised in January 2004 2nd step conversion transaction

? Increases proportion of commercial loans and core deposits

? Complementary franchises provide opportunities for cost savings and revenue enhancements

? 25% cost savings based on WSBI’s 2003 operating expenses (these estimates have been confirmed in due diligence and can be fully implemented during 2005)

? Reduction of back office, administration and stock benefit plans costs drives cost savings

? Revenue enhancements identified (not incorporated into accretion analysis)

? Improves pro forma efficiency ratio from 62.3% (including ENB) to 59.6%

? Creates significant opportunity for shareholder value creation

6

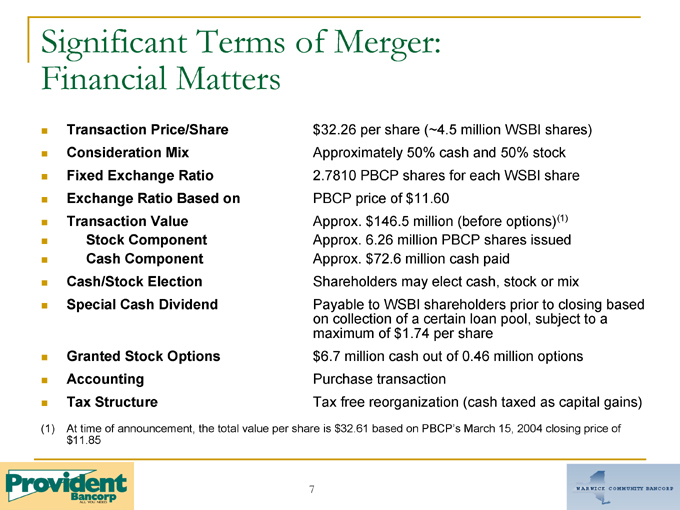

Significant Terms of Merger: Financial Matters

Transaction Price/Share $32.26 per share (4.5 million WSBI shares)

Consideration Mix Approximately 50% cash and 50% stock

Fixed Exchange Ratio 2.7810 PBCP shares for each WSBI share

Exchange Ratio Based on PBCP price of $11.60

Transaction Value Approx. $146.5 million (before options)(1)

Stock Component Approx. 6.26 million PBCP shares issued

Cash Component Approx. $72.6 million cash paid

Cash/Stock Election Shareholders may elect cash, stock or mix

Special Cash Dividend Payable to WSBI shareholders prior to closing based

on collection of a certain loan pool, subject to a

maximum of $1.74 per share

Granted Stock Options $6.7 million cash out of 0.46 million options

Accounting Purchase transaction

Tax Structure Tax free reorganization (cash taxed as capital gains)

(1) At time of announcement, the total value per share is $32.61 based on PBCP’s March 15, 2004 closing price of $11.85

7

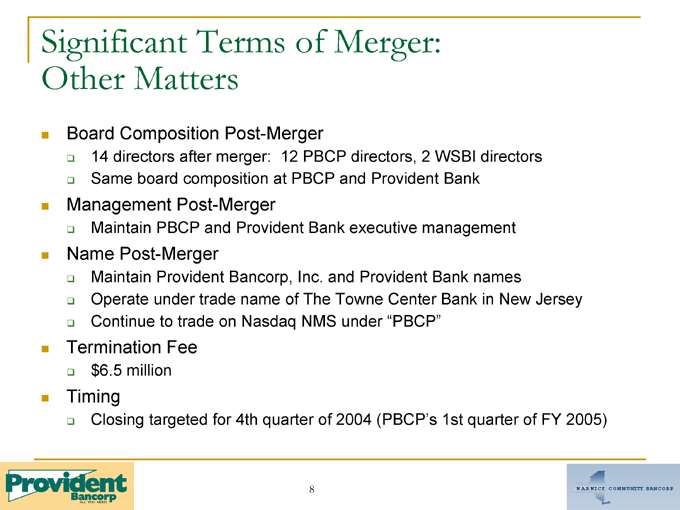

Significant Terms of Merger: Other Matters

Board Composition Post-Merger

14 directors after merger: 12 PBCP directors, 2 WSBI directors

Same board composition at PBCP and Provident Bank

Management Post-Merger

Maintain PBCP and Provident Bank executive management

Name Post-Merger

Maintain Provident Bancorp, Inc. and Provident Bank names

Operate under trade name of The Towne Center Bank in New Jersey

Continue to trade on Nasdaq NMS under “PBCP”

Termination Fee

$ 6.5 million

Timing

Closing targeted for 4th quarter of 2004 (PBCP’s 1st quarter of FY 2005)

8

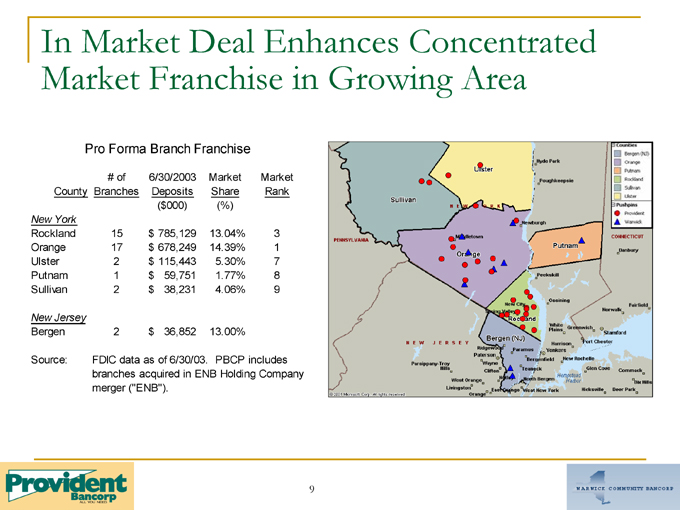

In Market Deal Enhances Concentrated Market Franchise in Growing Area

Pro Forma Branch Franchise

# of 6/30/2003 Market Market

County Branches Deposits Share Rank

($000) (%)

New York

Rockland 15 $ 785,129 13.04% 3

Orange 17 $ 678,249 14.39% 1

Ulster 2 $ 115,443 5.30% 7

Putnam 1 $ 59,751 1.77% 8

Sullivan 2 $ 38,231 4.06% 9

New Jersey

Bergen 2 $ 36,852 13.00%

Source: FDIC data as of 6/30/03. PBCP includes branches acquired in ENB Holding Company merger (“ENB”).

9

Combines PBCP’s Strong Asset Generation with WSBI’s Strong Core Deposits Growth

PBCP’s Expanding Loan Portfolio: Led By Growth in Commercial Loans

FY03 Pro

FY01 FY02 FY03 Forma

w/ENB

1-4 & Other $ 435.1 $ 449.5 $ 461.4 $ 584.2

Commercial $ 180.2 $ 221.7 $ 252.9 $ 351.5

WSBI’s Deposit Growth: Led by Core Deposits

FY01 FY02 FY03

CDs $ 122.9 $117.3 $98.2

Core Deposits $ 299.3 $349.4 $389.4

Note: Commercial includes commercial real estate loans and commercial and industrial loans. Source: PBCP 10Q at 12/31/03, ENB internal reports at 12/31/03 and WSBI 10K at 12/31/03.

10

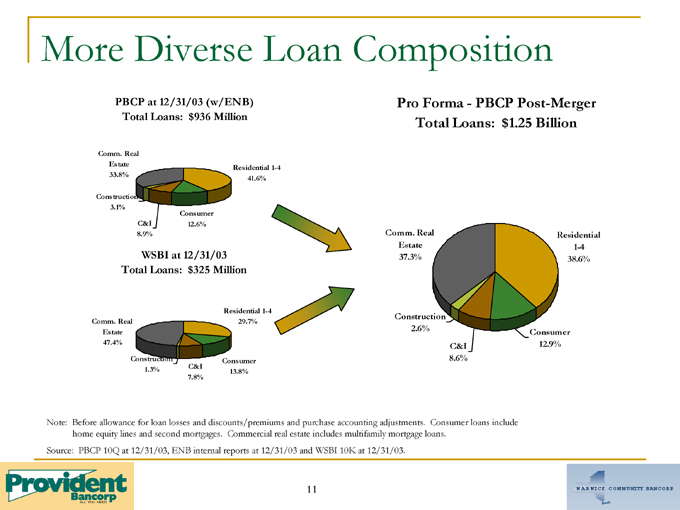

More Diverse Loan Composition

PBCP at 12/31/03 (w/ENB) Total Loans: $936 Million

Comm. Real Estate 33.8%

Construction 3.1%

C&I 8.9%

Consumer 12.6%

Residential 1-4 41.6%

WSBI at 12/31/03 Total Loans: $325 Million

Comm. Real Estate 47.4%

Construction 1.3%

C&I 7.8%

Consumer 13.8%

Residential 1-4 29.7%

Pro Forma—PBCP Post-Merger Total Loans: $1.25 Billion

Comm. Real Estate 37.3%

Construction 2.6%

C&I 8.6%

Consumer 12.9%

Residential 1-4 38.6%

Note: Before allowance for loan losses and discounts/premiums and purchase accounting adjustments. Consumer loans include home equity lines and second mortgages. Commercial real estate includes multifamily mortgage loans.

Source: PBCP 10Q at 12/31/03, ENB internal reports at 12/31/03 and WSBI 10K at 12/31/03.

11

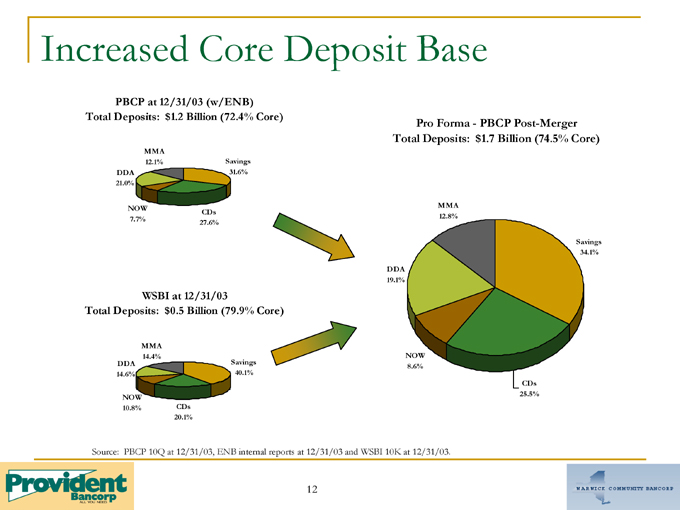

Increased Core Deposit Base

PBCP at 12/31/03 (w/ENB) Total Deposits: $1.2 Billion (72.4% Core)

MMA 12.1%

DDA 21.0%

NOW 7.7%

CDs 27.6%

Savings 31.6%

WSBI at 12/31/03

Total Deposits: $0.5 Billion (79.9% Core)

MMA 14.4%

DDA 14.6%

NOW 10.8%

CDs 20.1%

Savings 40.1%

Pro Forma—PBCP Post-Merger Total Deposits: $1.7 Billion (74.5% Core)

MMA 12.8%

DDA 19.1%

NOW 8.6%

CDs 25.5%

Savings 34.1%

Source: PBCP 10Q at 12/31/03, ENB internal reports at 12/31/03 and WSBI 10K at 12/31/03.

12

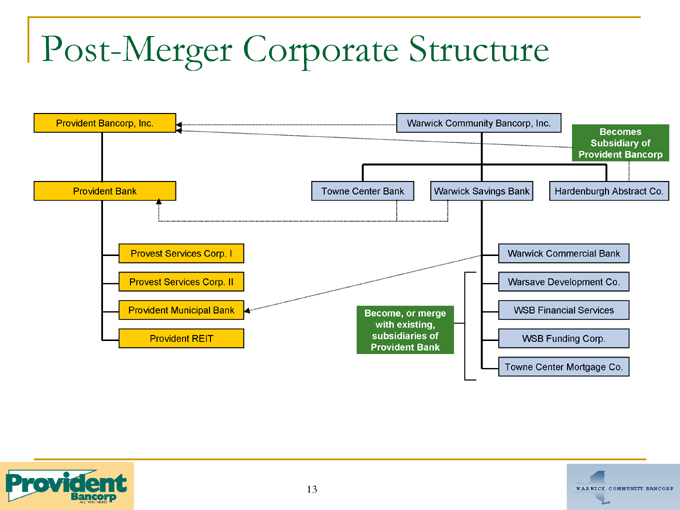

Post-Merger Corporate Structure

Provident Bancorp, Inc.

Provident Bank

Provest Services Corp. I

Provest Services Corp. II

Provident Municipal Bank

Provident REIT

Warwick Community Bancorp, Inc.

Becomes Subsidiary of

Provident Bancorp

Towne Center Bank Warwick Savings Bank Hardenburgh Abstract Co.

Become, or merge with existing, subsidiaries of Provident Bank

Warwick Commercial Bank

Warsave Development Co.

WSB Financial Services

WSB Funding Corp.

Towne Center Mortgage Co.

13

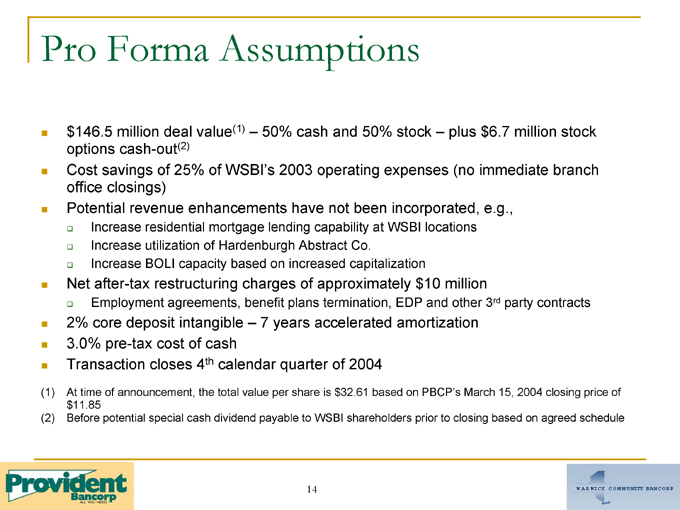

Pro Forma Assumptions

$ 146.5 million deal value(1) – 50% cash and 50% stock – plus $6.7 million stock options cash-out(2)

Cost savings of 25% of WSBI’s 2003 operating expenses (no immediate branch office closings)

Potential revenue enhancements have not been incorporated, e.g.,

Increase residential mortgage lending capability at WSBI locations

Increase utilization of Hardenburgh Abstract Co.

Increase BOLI capacity based on increased capitalization

Net after-tax restructuring charges of approximately $10 million

Employment agreements, benefit plans termination, EDP and other 3rd party contracts

2% core deposit intangible – 7 years accelerated amortization

3.0% pre-tax cost of cash

Transaction closes 4th calendar quarter of 2004

(1) At time of announcement, the total value per share is $32.61 based on PBCP’s March 15, 2004 closing price of $11.85 (2) Before potential special cash dividend payable to WSBI shareholders prior to closing based on agreed schedule

14

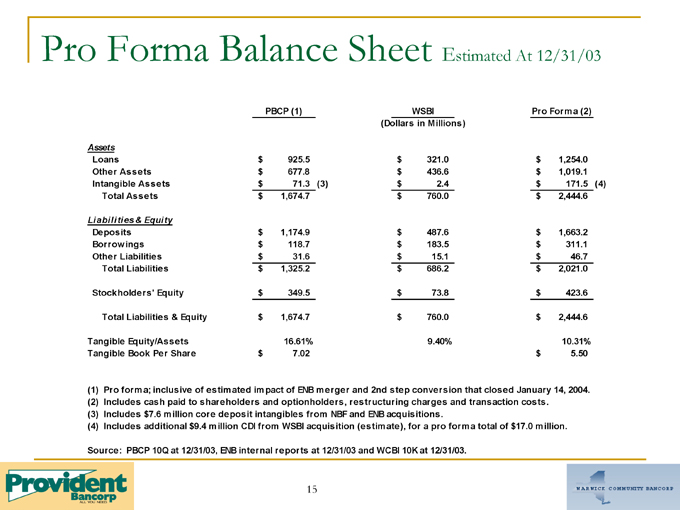

Pro Forma Balance Sheet Estimated At 12/31/03

PBCP (1) WSBI Pro Forma (2)

(Dollars in Millions)

Assets

Loans $ 925.5 $ 321.0 $ 1,254.0

Other Assets $ 677.8 $ 436.6 $ 1,019.1

Intangible Assets $ 71.3 (3) $ 2.4 $ 171.5 (4)

Total Assets $ 1,674.7 $ 760.0 $ 2,444.6

Liabilities & Equity

Deposits $ 1,174.9 $ 487.6 $ 1,663.2

Borrowings $ 118.7 $ 183.5 $ 311.1

Other Liabilities $ 31.6 $ 15.1 $ 46.7

Total Liabilities $ 1,325.2 $ 686.2 $ 2,021.0

Stockholders’ Equity $ 349.5 $ 73.8 $ 423.6

Total Liabilities & Equity $ 1,674.7 $ 760.0 $ 2,444.6

Tangible Equity/Assets 16.61% 9.40% 10.31%

Tangible Book Per Share $ 7.02 $ 5.50

(1) Pro forma; inclusive of estimated impact of ENB merger and 2nd step conversion that closed January 14, 2004. (2) Includes cash paid to shareholders and optionholders, restructuring charges and transaction costs.

(3) Includes $7.6 million core deposit intangibles from NBF and ENB acquisitions.

(4) Includes additional $9.4 million CDI from WSBI acquisition (estimate), for a pro forma total of $17.0 million.

Source: PBCP 10Q at 12/31/03, ENB internal reports at 12/31/03 and WCBI 10K at 12/31/03.

15

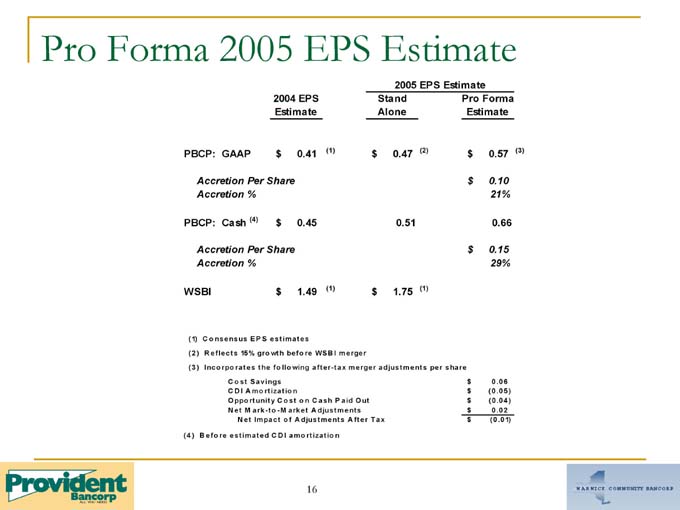

Pro Forma 2005 EPS Estimate

2005 EPS Estimate

2004 EPS Stand Pro Forma

Estimate Alone Estimate

PBCP: GAAP $ 0.41 (1) $ 0.47 (2) $ 0.57 (3)

Accretion Per Share $ 0.10

Accretion % 21%

PBCP: Cash (4) $ 0.45 0.51 0.66

Accretion Per Share $ 0.15

Accretion % 29%

WSBI $ 1.49 (1) $ 1.75 (1)

(1) C o nsensus EP S estimates

(2) R eflects 15% growth befo re WSBI merger

(3) Incorporates the fo llowing after-tax merger adjustments per share

Cost Savings $ 0.06

C D I Amortization $ (0.05)

Opportunity Cost on Cash Paid Out $ (0.04)

Net M ark-to -M arket Adjustments $ 0.02

Net Impact o f Adjustments After Tax $ (0.01)

(4) Before estimated C D I amortization

16

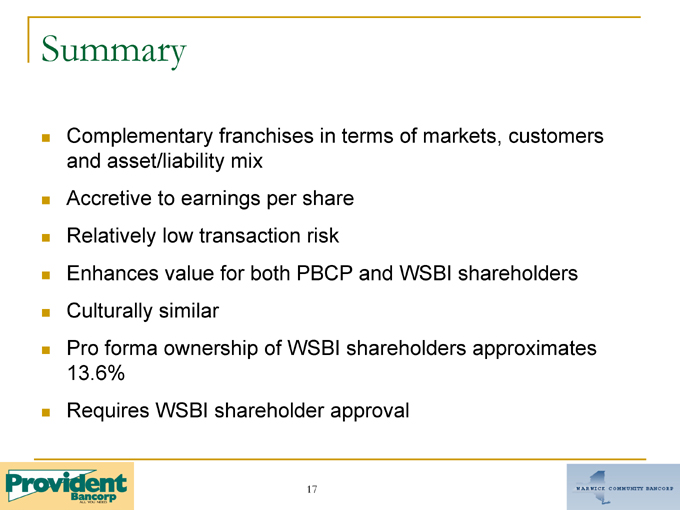

Summary

Complementary franchises in terms of markets, customers and asset/liability mix

Accretive to earnings per share

Relatively low transaction risk

Enhances value for both PBCP and WSBI shareholders

Culturally similar

Pro forma ownership of WSBI shareholders approximates 13.6%

Requires WSBI shareholder approval

17

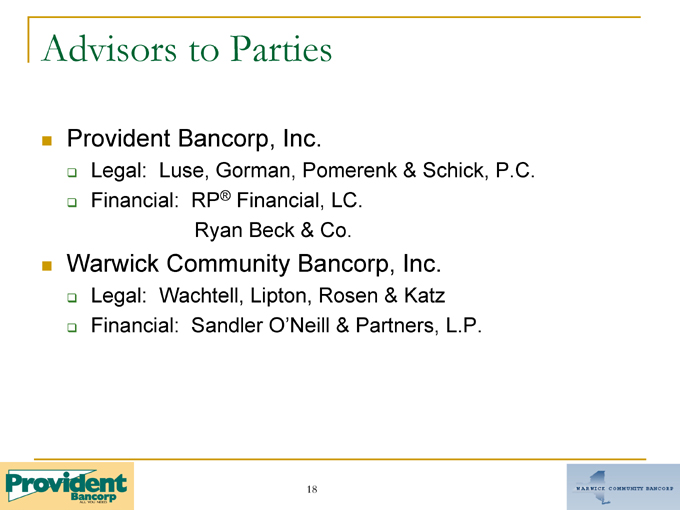

Advisors to Parties

Provident Bancorp, Inc.

Legal: Luse, Gorman, Pomerenk & Schick, P.C.

Financial: RP® Financial, LC.

Ryan Beck & Co.

Warwick Community Bancorp, Inc.

Legal: Wachtell, Lipton, Rosen & Katz

Financial: Sandler O’Neill & Partners, L.P.

18