UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2005

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 1-14569

PLAINS ALL AMERICAN PIPELINE, L.P.

(Exact name of registrant as specified in its charter)

Delaware | 76-0582150 |

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification No.) |

333 Clay Street, Suite 1600, Houston, Texas 77002

(Address of principal executive offices) (Zip Code)

(713) 646-4100

(Registrant’s telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Title of each class | | Name of each exchange on which registered |

Common Units | | New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer x | Accelerated Filer o | Non-Accelerated Filer o |

Indicate by check mark if the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

The aggregate value of the Common Units held by non-affiliates of the registrant (treating all executive officers and directors of the registrant and holders of 10% or more of the Common Units outstanding, for this purpose, as if they may be affiliates of the registrant) was approximately $2.3 billion on June 30, 2005, based on $43.86 per unit, the closing price of the Common Units as reported on the New York Stock Exchange on such date.

At February 17, 2006, there were outstanding 73,768,576 Common Units.

DOCUMENTS INCORPORATED BY REFERENCE

NONE

PLAINS ALL AMERICAN PIPELINE, L.P. AND SUBSIDIARIES

FORM 10-K—2005 ANNUAL REPORT

Table of Contents

FORWARD-LOOKING STATEMENTS

All statements included in this report, other than statements of historical fact, are forward-looking statements, including but not limited to statements identified by the words “anticipate,” “believe,” “estimate,” “expect,” “plan,” “intend” and “forecast,” and similar expressions and statements regarding our business strategy, plans and objectives of our management for future operations. However, the absence of these words does not mean that the statements are not forward-looking. These statements reflect our current views with respect to future events, based on what we believe are reasonable assumptions. Certain factors could cause actual results to differ materially from results anticipated in the forward-looking statements. These factors include, but are not limited to:

· the success of our risk management activities;

· environmental liabilities or events that are not covered by an indemnity, insurance or existing reserves;

· maintenance of our credit rating and ability to receive open credit from our suppliers and trade counterparties;

· abrupt or severe declines or interruptions in outer continental shelf production located offshore California and transported on our pipeline system;

· declines in volumes shipped on the Basin Pipeline, Capline Pipeline and our other pipelines by us and third party shippers;

· the availability of adequate third party production volumes for transportation and marketing in the areas in which we operate;

· demand for natural gas or various grades of crude oil and resulting changes in pricing conditions or transmission throughput requirements;

· fluctuations in refinery capacity in areas supplied by our transmission lines;

· the availability of, and our ability to consummate, acquisition or combination opportunities;

· our access to capital to fund additional acquisitions and our ability to obtain debt or equity financing on satisfactory terms;

· successful integration and future performance of acquired assets or businesses and the risks associated with operating in lines of business that are distinct and separate from our historical operations;

· the impact of current and future laws, rulings and governmental regulations;

· the effects of competition;

· continued creditworthiness of, and performance by, our counterparties;

· interruptions in service and fluctuations in rates of third party pipelines;

· increased costs or lack of availability of insurance;

· fluctuations in the debt and equity markets, including the price of our units at the time of vesting under our Long-Term Incentive Plans;

· the currency exchange rate of the Canadian dollar;

· the impact of crude oil and natural gas price fluctuations;

· shortages or cost increases of power supplies, materials or labor;

· weather interference with business operations or project construction;

· general economic, market or business conditions; and

· other factors and uncertainties inherent in the marketing, transportation, terminalling, gathering and storage of crude oil and liquefied petroleum gas.

Other factors described elsewhere in this document, or factors that are unknown or unpredictable, could also have a material adverse effect on future results. Please read “Risks Related to Our Business” discussed in Item 1A. “Risk Factors.” Except as required by applicable securities laws, we do not intend to update these forward-looking statements and information.

PART I

Items 1 and 2. Business and Properties

General

Plains All American Pipeline, L.P. is a Delaware limited partnership formed in September 1998. Our operations are conducted directly and indirectly through our primary operating subsidiaries, Plains Marketing, L.P., Plains Pipeline, L.P. and Plains Marketing Canada, L.P. As used in this Form 10-K, the terms “we”, “us”, “our”, “ours” and similar terms refer to Plains All American Pipeline, L.P. and its subsidiaries, unless the context indicates otherwise. We are engaged in interstate and intrastate crude oil transportation and crude oil gathering, marketing, terminalling and storage, as well as the marketing and storage of liquefied petroleum gas and other natural gas related petroleum products. We refer to liquefied petroleum gas and other natural gas related petroleum products collectively as “LPG.”

We are one of the largest midstream crude oil companies in North America. We have an extensive network of pipeline transportation, terminalling, storage and gathering assets in key oil producing basins, transportation corridors and at major market hubs in the United States and Canada. Our crude oil and LPG operations can be categorized into two primary business activities:

· Crude Oil Pipeline Transportation Operations. As of December 31, 2005, we owned approximately 15,000 miles (of which approximately 13,000 miles are included in our pipeline segment) of active gathering and mainline crude oil pipelines located throughout the United States and Canada. Our activities from pipeline operations generally consist of transporting volumes of crude oil for a fee and third party leases of pipeline capacity, barrel exchanges and buy/sell arrangements.

· Gathering, Marketing, Terminalling and Storage Operations. As of December 31, 2005, we owned approximately 39 million barrels of active above-ground crude oil terminalling and storage facilities, approximately 15 million barrels of which relate to our gathering, marketing, terminalling and storage segment (the remaining approximately 24 million barrels of tankage are associated with our pipeline transportation operations within our pipeline segment). These facilities include a crude oil terminalling and storage facility at Cushing, Oklahoma. Cushing, which we refer to as the Cushing Interchange, is one of the largest crude oil market hubs in the United States and is the designated delivery point for New York Mercantile Exchange, or NYMEX, crude oil futures contracts. We utilize our storage tanks to counter-cyclically balance our gathering and marketing operations and to execute various hedging strategies to stabilize profits and reduce the negative impact of crude oil market volatility, while at the same time providing upside exposure to opportunities inherent in volatile market conditions. Our terminalling and storage operations also generate revenue at the Cushing Interchange and our other locations through a combination of storage and throughput charges to third parties. We also own approximately 1.8 million barrels of LPG storage. Our gathering and marketing activities include:

· the purchase of U.S. and Canadian crude oil at the wellhead and the bulk purchase of crude oil at pipeline and terminal facilities, as well as foreign cargoes at their load port and various other locations in transit;

· the transportation of crude oil on trucks, barges, pipelines and ocean-going vessels;

· the subsequent resale or exchange of crude oil at various points along the crude oil distribution chain; and

· the purchase of LPG from producers, refiners and other marketers, the storage of LPG at storage facilities owned by us or third parties, the transportation of LPG to our terminals and the sale of LPG to wholesalers, retailers and industrial end users.

1

In addition, through our 50% equity ownership in PAA/Vulcan Gas Storage, LLC (“PAA/Vulcan”), we are engaged in the development and operation of natural gas storage facilities.

Business Strategy

Our principal business strategy is to provide competitive and efficient crude oil transportation, gathering, marketing, terminalling and storage services to our producer and refiner customers, and to address the regional crude oil supply and demand imbalances that exist in the United States and Canada by combining the strategic location and distinctive capabilities of our transportation and terminalling assets with our extensive marketing and distribution expertise. We believe successful execution of this strategy will enable us to generate sustainable earnings and cash flow. We intend to grow our business by:

· increasing and optimizing throughput on our existing pipeline and gathering assets and realizing cost efficiencies through operational improvements;

· utilizing our Gulf Coast assets, our Cushing Terminal and leased assets to increase our presence in the importation of foreign crude oil through Gulf of Mexico receipt facilities;

· developing and implementing internal growth projects that address evolving needs in the crude oil transportation sector and that are well positioned to benefit from long-term industry trends and opportunities;

· selectively pursuing strategic and accretive acquisitions of crude oil marketing, transportation, gathering, terminalling and storage assets that complement our existing asset base and distribution capabilities; and

· using our terminalling and storage assets in conjunction with merchant and hedging activities to address physical market imbalances, mitigate inherent risks and increase margin.

To a lesser degree, we engage in a similar business strategy with respect to the wholesale marketing and storage of LPG and, through our 50% ownership in PAA/Vulcan, in the storage of natural gas. We also intend to prudently and economically leverage our asset base, knowledge base and skill sets to participate in other energy-related businesses that have characteristics and opportunities similar to our existing activities.

Financial Strategy

Targeted Credit Profile

We believe that a major factor in our continued success is our ability to maintain a competitive cost of capital and access to the capital markets. We have consistently communicated to the financial community our intention to maintain a strong credit profile that we believe is consistent with an investment grade credit rating. We have targeted a general credit profile with the following attributes:

· an average long-term debt-to-total capitalization ratio of approximately 50%;

· an average long-term debt-to-EBITDA ratio of approximately 3.5x or less (EBITDA is earnings before interest, taxes, depreciation and amortization); and

· an average EBITDA-to-interest coverage ratio of approximately 3.3x or better.

Based on our financial position at December 31, 2005 and operating and financial results for 2005, we were within our targeted credit profile. In order for us to maintain our targeted credit profile and achieve growth through internal growth projects and acquisitions, we intend to fund at least 50% of the capital requirements associated with these activities with equity and cash flow in excess of distributions. From time

2

to time, we may be outside the parameters of our targeted credit profile as, in certain cases, these capital expenditures may initially be financed using debt.

Credit Rating

As of February 2006, our senior unsecured ratings with Standard & Poor’s and Moody’s Investment Services were BBB- stable and Baa3 stable, respectively, both of which are considered “investment grade.’’ We have targeted the attainment of even stronger investment grade ratings of BBB+ and Baa1 for Standard & Poor’s and Moody’s Investment Services, respectively. We cannot give assurance that our current ratings will remain in effect for any given period of time, that we will be able to attain the higher ratings we have targeted or that one or both of these ratings will not be lowered or withdrawn entirely by the ratings agency. Note that a credit rating is not a recommendation to buy, sell or hold securities, and may be revised or withdrawn at any time.

Competitive Strengths

We believe that the following competitive strengths position us to successfully execute our principal business strategy:

· Many of our pipeline transportation and storage assets are strategically located and operationally flexible and have additional capacity or expansion capability. Our primary crude oil pipeline transportation and gathering assets are located in well-established oil producing regions and transportation corridors and are connected, directly or indirectly, with our terminalling and storage assets that are located at major trading locations and premium markets that serve as gateways to major North American refinery and distribution markets where we have strong business relationships. Specific assets with additional capacity or expansion potential include our ownership interest in the Capline System, our Cushing Terminal and our St. James Terminal, which is expected to be in service in 2007. Our Cushing Terminal is a designated delivery point for the NYMEX crude oil futures contract and is one of the most modern large-scale terminalling and storage facilities at the Cushing Interchange, incorporating operational enhancements designed to safely and efficiently terminal, store, blend and segregate large volumes and multiple varieties of crude oil. When completed, our St. James Terminal will have many similar characteristics.

· We possess specialized crude oil market knowledge. We believe our business relationships with participants in various phases of the crude oil distribution chain, from crude oil producers to refiners, as well as our own industry expertise, provide us with an extensive understanding of the North American physical crude oil markets.

· Our business activities are counter-cyclically balanced. We believe that our terminalling and storage activities and our gathering and marketing activities are counter-cyclical. We believe that this balance of activities, combined with our pipeline transportation operations, generally provides us with the flexibility to maintain a base level of margin irrespective of whether a strong or weak market exists and, in certain circumstances, to realize incremental margin during volatile market conditions.

· We have the evaluation, integration and engineering skill sets and the financial flexibility to continue to pursue acquisition and expansion opportunities. Over the past eight years, we have completed and integrated approximately 35 acquisitions with an aggregate purchase price of approximately $2.0 billion. We have also implemented internal expansion capital projects totaling over $400 million. In addition, we believe we have significant resources to finance future strategic expansion and acquisition opportunities. As of December 31, 2005, we had approximately $789 million available under our committed credit facilities, subject to covenant compliance. We believe we have one of the strongest capital structures relative to other master limited partnerships with

3

capitalizations greater than $1.0 billion. In addition, the investors in our general partner are diverse and financially strong and have demonstrated their support by providing capital to help finance previous acquisitions. We believe they are supportive long-term sponsors of the partnership.

· We have an experienced management team whose interests are aligned with those of our unitholders. Our executive management team has an average of more than 20 years industry experience, with an average of more than 15 years with us or our predecessors and affiliates. Members of our senior management team own an approximate 5% interest in our general partner and collectively own approximately 900,000 common units, including fully vested options. In addition, through grants of phantom units, the senior management team also owns significant contingent equity incentives that generally vest upon achievement of performance objectives, continued service or both.

We believe many of these competitive strengths have similar application to our efforts to expand our presence in the natural gas storage sector. See “—Natural Gas Storage Market Overview” and

“—Description of PAA/Vulcan Natural Gas Storage Assets.”

Organizational History

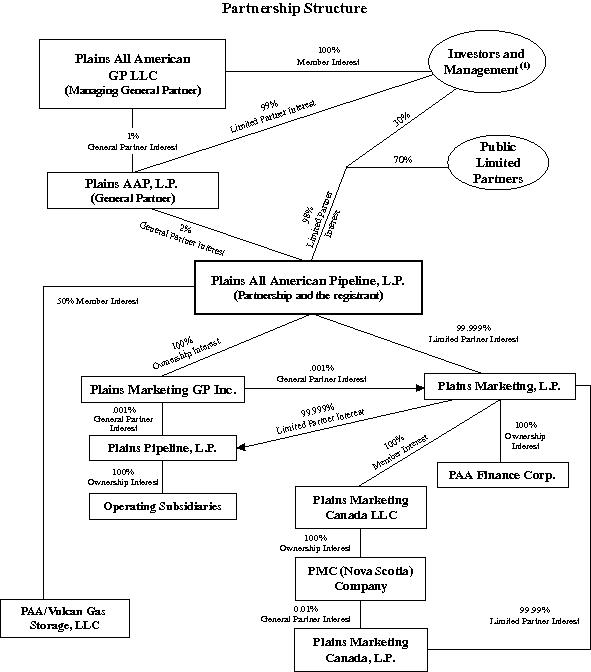

We were formed as a master limited partnership in September 1998 to acquire and operate the midstream crude oil businesses and assets of a predecessor entity. We completed our initial public offering in November 1998. Since June 2001, our 2% general partner interest has been held by Plains AAP, L.P., a Delaware limited partnership. Plains All American GP LLC, a Delaware limited liability company, is Plains AAP, L.P.’s general partner. Unless the context otherwise requires, we use the term “general partner” to refer to both Plains AAP, L.P. and Plains All American GP LLC. Plains AAP, L.P. and Plains All American GP LLC are essentially held by seven owners. See Item 12. “Security Ownership of Certain Beneficial Owners and Management and Related Unitholder Matters—Beneficial Ownership of General Partner Interest.”

Partnership Structure and Management

Our operations are conducted through, and our operating assets are owned by, our subsidiaries. We own our interests in our subsidiaries through two operating partnerships, Plains Marketing, L.P. and Plains Pipeline, L.P. Our Canadian and LPG operations are conducted through Plains Marketing Canada, L.P.

Our general partner, Plains AAP, L.P., is managed by its general partner, Plains All American GP LLC, which has ultimate responsibility for conducting our business and managing our operations. See Item 10. “Directors and Executive Officers of our General Partner.” Our general partner does not receive a management fee or other compensation in connection with its management of our business, but it is reimbursed for substantially all direct and indirect expenses incurred on our behalf.

The chart on the next page depicts the current structure and ownership of Plains All American Pipeline, L.P. and certain subsidiaries.

4

(1) Based on Form 4 filings for officers and directors, 13D filings for Paul G. Allen and Richard Kayne and other information believed to be reliable for the remaining investors, this group, or affiliates of such investors, beneficially owns approximately 21.6 million limited partner units, representing approximately 30% of all outstanding units.

5

Acquisitions

The acquisition of assets and operations that are strategic and complementary to our existing operations constitutes an integral component of our business strategy and growth objective. Such assets and operations include crude oil related assets and LPG assets, as well as energy related assets that have characteristics and opportunities similar to these business lines, and enable us to leverage our asset base, knowledge base and skill sets. We have established a target to complete, on average, $200 million to $300 million in acquisitions per year, subject to availability of attractive assets on acceptable terms. Since 1998, and through December 31, 2005, we have completed numerous acquisitions for a cumulative purchase price of approximately $2.0 billion. In addition, from time to time, we have sold assets that are no longer considered essential to our operations.

The following table summarizes selected acquisitions that we have completed over the past five years:

Acquisition | | Date | | Description | | Approximate

Purchase Price

(in millions) | |

Investment in Natural Gas Storage Facilities | | September 2005 | | Joint venture with Vulcan Gas Storage LLC to develop and operate natural gas storage facilities. | | | $ 125 | (1) | |

Schaefferstown Propane Storage Facility | | August 2004 | | Storage capacity of approximately 0.5 million barrels of refrigerated propane | | | $ 32 | | |

Cal Ven Pipeline System | | May 2004 | | 195 miles of gathering and mainline crude oil pipelines in northern Alberta | | | $ 19 | | |

Link Energy LLC | | April 2004 | | The North American crude oil and pipeline operations of Link Energy, LLC (“Link”) | | | $ 332 | | |

Capline and Capwood Pipeline Systems | | March 2004 | | An approximate 22% undivided joint interest in the Capline Pipeline System and an approximate 76% undivided joint interest in the Capwood Pipeline System | | | $ 158 | | |

South Saskatchewan Pipeline System | | November 2003 | | A 158-mile mainline crude oil pipeline and 203 miles of gathering lines in Saskatchewan | | | $ 48 | | |

ArkLaTex Pipeline System | | October 2003 | | 240 miles of crude oil gathering and mainline pipelines and 470,000 barrels of crude oil storage capacity | | | $ 21 | | |

Iraan to Midland Pipeline System | | June 2003 | | 98-mile mainline crude oil pipeline | | | $ 18 | | |

South Louisiana Assets | | June 2003 and December 2003 | | Various terminalling and gathering assets in South Louisiana, including a 100% interest in Atchafalaya Pipeline, L.L.C. | | | $ 18 | | |

Iatan Gathering System | | March 2003 | | West Texas crude oil gathering system | | | $ 24 | | |

Red River Pipeline System | | February 2003 | | 334-mile crude oil pipeline along with 645,000 barrels of crude oil storage capacity | | | $ 19 | | |

6

Shell West Texas Assets | | August 2002 | | Basin Pipeline System, Permian Basin Pipeline System and the Rancho Pipeline System | | | $ 324 | | |

Canadian Operations | | May/July 2001 | | The assets of CANPET Energy Group (crude oil and LPG marketing) and substantially all of the Canadian crude oil pipeline, gathering, storage and terminalling assets of Murphy Oil Company Ltd. (560 miles of crude oil and condensate mainlines along with 1.1 million barrels of crude oil storage and terminalling capacity) | | | $ 232 | | |

(1) Represents 50% of the purchase price for the acquisition made by our joint venture. The joint venture completed an acquisition for approximately $250 million during 2005. See “—Investment in Natural Gas Storage Facilities” below.

Ongoing Acquisition Activities

Consistent with our business strategy, we are continuously engaged in discussions with potential sellers regarding the possible purchase by us of assets and operations that are strategic and complementary to our existing operations. Such assets and operations include crude oil related assets, LPG assets and, through our interest in PAA/Vulcan, natural gas storage assets. In addition, we have in the past and intend in the future to evaluate and pursue other energy related assets that have characteristics and opportunities similar to these business lines, and enable us to leverage our asset base, knowledge base and skill sets. Such acquisition efforts may involve participation by us in processes that have been made public and involve a number of potential buyers, commonly referred to as “auction” processes, as well as situations in which we believe we are the only party or one of a limited number of potential buyers in negotiations with the potential seller. These acquisition efforts often involve assets which, if acquired, could have a material effect on our financial condition and results of operations.

Investment in Natural Gas Storage Facilities

PAA/Vulcan, a limited liability company, was formed in the third quarter of 2005. We own 50% of PAA/Vulcan and the remaining 50% is owned by Vulcan Gas Storage LLC, a subsidiary of Vulcan Capital, the investment arm of Paul G. Allen. The Board of Directors of PAA/Vulcan consists of an equal number of our representatives and representatives of Vulcan Gas Storage, and is responsible for providing strategic direction and policy-making. We, as the managing member, are responsible for the day-to-day operations. PAA/Vulcan is not a variable interest entity, and we do not have the ability to control the entity; therefore, we account for the investment under the equity method in accordance with Accounting Principles Board Opinion No. 18, “The Equity Method of Accounting for Investments in Common Stock.” This investment is reflected on a separate line in our consolidated balance sheet.

In September 2005, PAA/Vulcan acquired Energy Center Investments LLC (“ECI”), an indirect subsidiary of Sempra Energy, for approximately $250 million. ECI develops and operates underground natural gas storage facilities. We and Vulcan Gas Storage LLC each made an initial cash investment of approximately $112.5 million, and a subsidiary of PAA/Vulcan entered into a $90 million credit facility contemporaneously with closing. Approximately $255 million of the total funding of $315 million was used to finance the acquisition and closing costs. It is anticipated that the remaining balance will be combined

7

with funds obtained from future financing activities related to the construction of an underground natural gas storage facility in South Louisiana.

Crude Oil Market Overview

Our assets and our business strategy are designed to service our producer and refiner customers by addressing regional crude oil supply and demand imbalances that exist in the United States and Canada. According to the Energy Information Administration (“EIA”), the United States consumes approximately 15.3 million barrels of crude oil per day, while only producing 5.2 million barrels per day. Accordingly, the United States relies on foreign imports for nearly 66% of the crude oil used by U.S. domestic refineries. This imbalance represents a continuing trend. Foreign imports of crude oil into the U.S. have tripled over the last 21 years, increasing from 3.2 million barrels per day in 1984 to 10.1 million barrels per day for the 12 months ended November 2005, as U.S. refinery demand has increased and domestic crude oil production has declined due to natural depletion.

The Department of Energy segregates the United States into five Petroleum Administration Defense Districts (“PADDs”) which are used by the energy industry for reporting statistics regarding crude oil supply and demand. The table below sets forth supply, demand and shortfall information for each PADD for the twelve months ended November 2005 and is derived from information published by the EIA (see EIA website at www.eia.doe.gov).

Petroleum Administration Defense District | | | | Regional

Supply | | Refinery Demand | | Supply

Shortfall | |

| | (Millions of barrels per day) | |

PADD I (East Coast) | | | 0.0 | | | | 1.6 | | | | (1.6 | ) | |

PADD II (Midwest) | | | 0.5 | | | | 3.3 | | | | (2.8 | ) | |

PADD III (South) | | | 2.8 | | | | 7.1 | | | | (4.3 | ) | |

PADD IV (Rockies) | | | 0.3 | | | | 0.6 | | | | (0.3 | ) | |

PADD V (West Coast) | | | 1.6 | | | | 2.7 | | | | (1.1 | ) | |

Total U.S. | | | 5.2 | | | | 15.3 | | | | (10.1 | ) | |

Although PADD III has the largest supply shortfall, PADD II is believed to be the most critical region with respect to supply and transportation logistics because it is the largest, most highly populated area of the U.S. that does not have direct access to oceanborne cargoes.

Over the last 21 years, crude oil production in PADD II has declined from approximately 1.0 million barrels per day to approximately 500,000 barrels per day. Over this same time period, refinery demand has increased from approximately 2.7 million barrels per day in 1984 to 3.3 million barrels per day for the twelve months ended November 2005. As a result, the volume of crude oil transported into PADD II has increased 65%, from 1.7 million barrels per day to 2.8 million barrels per day. This aggregate shortfall is principally supplied from the north by direct imports from Canada and from the Gulf Coast area and the Cushing Interchange to the south.

The logistical transportation, terminalling and storage challenges associated with regional volumetric supply and demand imbalances are further complicated by the fact that crude oil from different sources is not fungible. The crude slate available to U.S. refineries consists of over 50 different grades and varieties of crude oil. Each crude grade has distinguishing physical properties, such as specific gravity (generally referred to as light or heavy), sulfur content (generally referred to as sweet or sour) and metals content as well as varying economic attributes. In many cases, these factors result in the need for such grades to be batched or segregated in the transportation and storage processes, blended to precise specifications or adjusted in value. In addition, from time to time, natural disasters and geopolitical factors, such as hurricanes, earthquakes, tsunamis, inclement weather, labor strikes, refinery disruptions, embargoes and armed conflicts, may impact supply, demand and transportation and storage logistics.

8

Description of Segments and Associated Assets

Our crude oil and LPG business activities are conducted through two primary segments, Pipeline Operations and Gathering, Marketing, Terminalling and Storage Operations (“GMT&S”). We have an extensive network of pipeline transportation, terminalling, storage and gathering assets in key oil producing basins, transportation corridors and at major market hubs in the United States and Canada.

Following is a description of the activities and assets for each of our business segments.

Pipeline Operations

As of December 31, 2005, we owned approximately 15,000 miles of active gathering and mainline crude oil pipelines located throughout the United States and Canada. Approximately 13,000 miles of these pipelines are used in our pipeline operations segment with the remainder used in our GMT&S segment. Our activities from pipeline operations generally consist of transporting crude oil for a fee and third party leases of pipeline capacity, as well as barrel exchanges and buy/sell arrangements.

Substantially all of our pipeline systems are controlled or monitored from one of two central control rooms with computer systems designed to continuously monitor real-time operational data, such as measurement of crude oil quantities injected into and delivered through the pipelines, product flow rates, and pressure and temperature variations. The systems are designed to enhance leak detection capabilities, sound automatic alarms in the event of operational conditions outside of pre-established parameters and provide for remote controlled shut-down of the majority of our pump stations on the pipeline systems. Pump stations, storage facilities and meter measurement points along the pipeline systems are linked by telephone, satellite, radio or a combination thereof to provide communications for remote monitoring and in some instances control, which reduces our requirement for full-time site personnel at most of these locations.

We make repairs on and replacements of our mainline pipeline systems when necessary or appropriate. We attempt to control corrosion of the mainlines through the use of cathodic protection, corrosion inhibiting chemicals injected into the crude stream and other protection systems typically used in the industry. Maintenance facilities containing spare parts and equipment for pipe repairs, as well as trained response personnel, are strategically located along the pipelines and in concentrated operating areas. We believe that all of our pipelines have been constructed and are maintained in all material respects in accordance with applicable federal, state, provincial and local laws and regulations, standards prescribed by the American Petroleum Institute (“API”), the Canadian Standards Association and accepted industry practice. See “—Regulation—Pipeline and Storage Regulation.”

Major Pipeline Assets

All American Pipeline System

The All American Pipeline is a common carrier crude oil pipeline system that transports crude oil produced from certain outer continental shelf, or OCS, fields offshore California via connecting pipelines to refinery markets in California. The system extends approximately 10 miles along the California coast from Las Flores to Gaviota (24-inch diameter pipe) and continues from Gaviota approximately 126 miles to our station in Emidio, California (30-inch diameter pipe). Between Gaviota and our Emidio Station, the All American Pipeline interconnects with our San Joaquin Valley, or SJV, Gathering System as well as various third party intrastate pipelines. The system is subject to tariff rates regulated by the Federal Energy Regulatory Commission (“FERC”).

The All American Pipeline currently transports OCS crude oil received at the onshore facilities of the Santa Ynez field at Las Flores and the onshore facilities of the Point Arguello field located at Gaviota. ExxonMobil, which owns all of the Santa Ynez production, and Plains Exploration and Production

9

Company (“PXP”) and other producers that together own approximately 70% of the Point Arguello production, have entered into transportation agreements committing to transport all of their production from these fields on the All American Pipeline. These agreements, which expire in August 2007, provide for a minimum tariff with annual escalations based on specific composite indices. The producers from the Point Arguello field that do not have contracts with us have no other existing means of transporting their production and, therefore, ship their volumes on the All American Pipeline at the filed tariffs. For 2005 and 2004, the tariffs averaged $1.87 per barrel and $1.81 per barrel, respectively. Effective January 1, 2006, based on the contractual escalator, the average tariff increased to $2.04 per barrel. The agreements do not require these owners to transport a minimum volume.

Approximately 10% of our revenues less purchases and field operating costs are derived from the pipeline transportation business associated with these two fields. The relative contribution to our revenues less direct field operating costs from these fields has decreased from approximately 26% in 2001 to current levels because of both (i) declines in volumes produced and transported from these fields and (ii) increases in our revenues from acquisitions and internal expansion projects. Since our acquisition of the system in 1998, the volume decline has been substantially offset by an increase in pipeline tariffs. Over the last ten years, transportation volumes received from the Santa Ynez and Point Arguello fields have declined from 92,000 and 60,000 average daily barrels, respectively, in 1995 to 41,000 and 10,000 average daily barrels, respectively, for 2005. We expect that there will continue to be natural production declines from each of these fields as the underlying reservoirs are depleted. A 5,000 barrel per day decline in volumes shipped from these fields would result in a decrease in annual pipeline segment profit of approximately $3.5 million, based on a tariff of $2.04 per barrel.

The table below sets forth the historical volumes received from both of these fields for the past five years:

| | Year Ended December 31, | |

| | 2005 | | 2004 | | 2003 | | 2002 | | 2001 | |

| | (barrels in thousands) | |

Average daily volumes received from: | | | | | | | | | | | | | | | | | | | | | |

Point Arguello (at Gaviota) | | | 10 | | | | 10 | | | | 13 | | | | 16 | | | | 18 | | |

Santa Ynez (at Las Flores) | | | 41 | | | | 44 | | | | 46 | | | | 50 | | | | 51 | | |

Total | | | 51 | | | | 54 | | | | 59 | | | | 66 | | | | 69 | | |

Basin Pipeline System

The Basin Pipeline System, in which we own an approximate 87% undivided joint interest, is a primary route for transporting Permian Basin crude oil to Cushing, Oklahoma, for further delivery to Mid-Continent and Midwest refining centers. We acquired our interest in the Basin Pipeline System in August 2002. Since acquisition, we have been the operator of the system. The Basin system is a 515-mile mainline, telescoping crude oil system with a capacity ranging from approximately 144,000 barrels per day to 400,000 barrels per day depending on the segment. System throughput (as measured by system deliveries) was approximately 290,000 barrels per day (net to our interest) during 2005. Within the current operating range, a 20,000 barrel per day decline in volumes shipped on the Basin system would result in a decrease in annual pipeline segment profit of approximately $1.4 million.

The Basin system consists of three primary movements of crude oil: (i) barrels that are shipped from Jal, New Mexico to the West Texas markets of Wink and Midland, where they are exchanged and/or further shipped to refining centers; (ii) barrels that are shipped to the Mid-Continent region on the Midland to Wichita Falls segment and the Wichita Falls to Cushing segment; and (iii) foreign and Gulf of Mexico barrels that are delivered into Basin at Wichita Falls and delivered to a connecting carrier or shipped to Cushing for further distribution to Mid-Continent or Midwest refineries. The system also

10

includes approximately 5.5 million barrels (4.8 million barrels, net to our interest) of crude oil storage capacity located along the system.

In 2004, we expanded an approximate 425-mile section of the system from Midland to Cushing. With the completion of this expansion, the capacity of this section has increased approximately 15%, from 350,000 barrels per day to approximately 400,000 barrels per day. The Basin system is subject to tariff rates regulated by the FERC.

Capline/Capwood Pipeline Systems

The Capline Pipeline System, in which we own a 22% undivided joint interest, is a 633-mile, 40-inch mainline crude oil pipeline originating in St. James, Louisiana, and terminating in Patoka, Illinois. The Capline Pipeline System is one of the primary transportation routes for crude oil shipped into the Midwestern U.S., accessing over 2.7 million barrels of refining capacity in PADD II. Shell is the operator of this system. Capline has direct connections to a significant amount of crude production in the Gulf of Mexico. In addition, with its two active docks capable of handling 600,000-barrel tankers as well as access to the Louisiana Offshore Oil Port (“LOOP”), it is a key transporter of sweet and light sour foreign crude to PADD II. With a total system operating capacity of 1.14 million barrels per day of crude oil, approximately 248,000 barrels per day are subject to our interest. During 2005, throughput on our interest has averaged approximately 132,000 barrels per day. A 10,000 barrel per day decline in volumes shipped on the Capline system would result in a decrease in our annual pipeline segment profit of approximately $1.3 million.

The Capwood Pipeline System, in which we own a 76% undivided joint interest, is a 58-mile, 20-inch mainline crude oil pipeline originating in Patoka, Illinois, and terminating in Wood River, Illinois. The Capwood Pipeline System has an operating capacity of 277,000 barrels per day of crude oil. Of that capacity, approximately 211,000 barrels per day are subject to our interest. The system has the ability to deliver crude oil at Wood River to several other PADD II refineries and pipelines. Movements on the Capwood system are driven by the volumes shipped on Capline as well as by volumes of Canadian crude that can be delivered to Patoka via the Mustang Pipeline. PAA assumed the operatorship of the Capwood system from Shell Pipeline Company LP at the time of purchase. During 2005 throughput net to our interest averaged approximately 107,000 barrels per day.

11

Our significant pipeline systems are discussed on the previous pages. Following is a tabular presentation of all of our active pipeline assets in the United States and Canada, including those previously mentioned, grouped by geographic location:

Region | | Pipeline | | Ownership

Percentage | | Pipeline

Mileage | | 2005

Average Net

Barrels

per day(1) | |

Southwest US | | Basin | | | 87.0 | % | | | 515 | | | | 290,000 | | |

| | West Texas Gathering | | | 100.0 | % | | | 800 | | | | 81,000 | | |

| | Permian Basin Gathering | | | 100.0 | % | | | 819 | | | | 56,000 | | |

| | Dollarhide | | | 100.0 | % | | | 24 | | | | 5,000 | | |

| | Mesa | | | 53.5 | % | | | 79 | | | | 32,000 | | |

| | Iraan | | | 100.0 | % | | | 98 | | | | 30,000 | | |

| | Iatan | | | 100.0 | % | | | 360 | | | | 21,000 | | |

| | New Mexico | | | 100.0 | % | | | 1,185 | | | | 77,000 | | |

| | Texas | | | 100.0 | % | | | 1,276 | | | | 93,000 | | |

| | Lefors | | | 100.0 | % | | | 68 | | | | 2,000 | | |

| | Merkel | | | 100.0 | % | | | 128 | | | | 3,000 | | |

| | Hardemann | | | 100.0 | % | | | 65 | | | | 5,000 | | |

| | Garden City | | | 100.0 | % | | | 5 | | | | 7,000 | | |

| | Spraberry Gathering | | | 100.0 | % | | | 412 | | | | 33,000 | | |

Western US | | All American | | | 100.0 | % | | | 140 | | | | 51,000 | | |

| | San Joaquin Valley | | | 100.0 | % | | | 77 | | | | 74,000 | | |

US Rocky Mountains | | Butte | | | 22.0 | % | | | 370 | | | | 17,000 | | |

| | North Dakota | | | 100.0 | % | | | 620 | | | | 77,000 | | |

US Gulf Coast | | Sabine Pass | | | 100.0 | % | | | 33 | | | | 11,000 | | |

| | Ferriday | | | 100.0 | % | | | 290 | | | | 8,000 | | |

| | La Gloria | | | 100.0 | % | | | 119 | | | | 24,000 | | |

| | Red River | | | 100.0 | % | | | 359 | | | | 17,000 | | |

| | ArkLaTex | | | 100.0 | % | | | 107 | | | | 15,000 | | |

| | Red Rock | | | 100.0 | % | | | 55 | | | | 3,000 | | |

| | Atchafalaya | | | 100.0 | % | | | 35 | | | | 13,000 | | |

| | Eugene Island | | | 100.0 | % | | | 66 | | | | 10,000 | | |

| | Bridger Lakes | | | 100.0 | % | | | 17 | | | | 2,000 | | |

| | Capline | | | 22.0 | % | | | 633 | | | | 132,000 | | |

| | Capwood/Patoka | | | 76.0 | % | | | 58 | | | | 116,000 | | |

| | Pearsall | | | 100.0 | % | | | 62 | | | | 2,000 | | |

| | Mississippi/Alabama | | | 100.0 | % | | | 601 | | | | 57,000 | | |

| | Southwest Louisiana | | | 100.0 | % | | | 217 | | | | 4,000 | | |

| | Cocodrie | | | 100.0 | % | | | 27 | | | | 6,000 | | |

| | Golden Meadows | | | 100.0 | % | | | 33 | | | | 4,000 | | |

| | Turtle Bayou | | | 100.0 | % | | | 14 | | | | 5,000 | | |

| | Erath | | | 100.0 | % | | | 50 | | | | 6,000 | | |

| | Hiedelberg | | | 100.0 | % | | | 72 | | | | 13,000 | | |

| | East Texas | | | 100.0 | % | | | 19 | | | | 7,000 | | |

Central US | | Oklahoma | | | 100.0 | % | | | 1,498 | | | | 62,000 | | |

| | Midcontinent | | | 100.0 | % | | | 1,197 | | | | 29,000 | | |

| | Cushing to Broome | | | 100.0 | % | | | 100 | | | | 66,000 | | |

| | United States Total | | | | | | | 12,703 | | | | 1,566,000 | | |

Canada | | Cal Ven | | | 100.0 | % | | | 92 | | | | 16,000 | | |

| | Manito | | | 100.0 | % | | | 101 | | | | 63,000 | | |

| | Milk River | | | 100.0 | % | | | 19 | | | | 102,000 | | |

| | Cactus Lake | | | 14.9 | % | | | 82 | | | | 3,000 | | |

| | Wascana | | | 100.0 | % | | | 107 | | | | 4,000 | | |

| | Wapella | | | 100.0 | % | | | 73 | | | | 16,000 | | |

| | Joarcam | | | 100.0 | % | | | 35 | | | | 3,000 | | |

| | South Sask | | | 100.0 | % | | | 158 | | | | 48,000 | | |

| | Canada Total | | | | | | | 667 | | | | 255,000 | | |

| | Total | | | | | | | 13,370 | | | | 1,821,000 | | |

| | | | | | | | | | | | | | | | | |

(1) Reflects volumes for the entire year for all pipeline systems including those reclassified to the pipeline segment during 2005.

12

Gathering, Marketing, Terminalling and Storage Operations

The combination of our gathering and marketing operations and our terminalling and storage operations provides a counter-cyclical balance that has a stabilizing effect on our operations and cash flow. The strategic use of our terminalling and storage assets in conjunction with our gathering and marketing operations generally provides us with the flexibility to maintain a base level of margin irrespective of whether a strong or weak market exists and, in certain circumstances, to realize incremental margin during volatile market conditions. Following is a description of our activities with respect to this segment.

Gathering and Marketing Operations

Crude Oil. The majority of our gathering and marketing activities are in the geographic locations previously discussed. These activities include:

· purchasing crude oil from producers at the wellhead and in bulk from aggregators at major pipeline interconnects or trading locations, as well as foreign cargoes at their load port and various other locations in transit;

· transporting crude oil on our own proprietary gathering assets and our common carrier pipelines or, when necessary or cost effective, assets owned and operated by third parties, including pipelines, trucks, barges and ocean-going vessels;

· exchanging crude oil for another grade of crude oil or at a different geographic location, as appropriate, in order to maximize margins or meet contract delivery requirements; and

· marketing crude oil to refiners or other resellers.

We purchase crude oil from multiple producers and believe that we generally have established broad-based relationships with the crude oil producers in our areas of operations. Gathering and marketing activities involve relatively large volumes of transactions, often with lower margins than pipeline and terminalling and storage operations.

The following table shows the average daily volume of our lease gathering and bulk purchases for the past five years:

| | Year Ended December 31, | | |

| | 2005 | | 2004 | | 2003 | | 2002 | | 2001 | |

| | (barrels in thousands) | | |

Lease gathering | | | 610 | | | | 589 | | | | 437 | | | | 410 | | | | 348 | | |

Bulk purchases (domestic and foreign) | | | 219 | | | | 161 | | | | 90 | | | | 68 | | | | 46 | | |

Total volumes per day | | | 829 | | | | 750 | | | | 527 | | | | 478 | | | | 394 | | |

| | | | | | | | | | | | | | | | | | | | | | | |

Crude Oil Purchases. We purchase crude oil in North America from producers under contracts, the majority of which range in term from a thirty-day evergreen to three year term. In a typical producer’s operation, crude oil flows from the wellhead to a separator where the petroleum gases are removed. After separation, the crude oil is treated to remove water, sand and other contaminants and is then moved into the producer’s on-site storage tanks. When the tank is approaching capacity, the producer contacts our field personnel to purchase and transport the crude oil to market. We utilize our truck fleet and gathering pipelines as well as third party pipelines, trucks, barges and ocean-going vessels to transport the crude oil to market. We own or lease approximately 500 trucks used for gathering crude oil. In addition, we purchase foreign crude oil. Under these contracts we may purchase crude oil upon delivery in the U.S. or we may purchase crude oil in foreign locations and transport crude oil on third party tankers.

Bulk Purchases. In addition to purchasing crude oil from producers, we purchase both domestic and foreign crude oil in bulk at major pipeline terminal locations and barge facilities. We purchase crude oil in

13

bulk when we believe additional opportunities exist to realize margins further downstream in the crude oil distribution chain. The opportunities to earn additional margins vary over time with changing market conditions.

Crude Oil Sales. The marketing of crude oil is complex and requires current detailed knowledge of crude oil sources and end markets and a familiarity with a number of factors including grades of crude oil, individual refinery demand for specific grades of crude oil, area market price structures for the different grades of crude oil, location of customers, availability of transportation facilities and timing and costs (including storage) involved in delivering crude oil to the appropriate customer. We sell our crude oil to major integrated oil companies, independent refiners and other resellers in various types of sale and exchange transactions. The majority of these contracts are at market prices and have terms ranging from one month to three years.

We establish a margin for crude oil we purchase by selling crude oil for physical delivery to third party users, such as independent refiners or major oil companies, or by entering into a future delivery obligation with respect to futures contracts on the NYMEX, International Petroleum Exchange (“IPE”) or over-the-counter. Through these transactions, we seek to maintain a position that is substantially balanced between crude oil purchases and sales and future delivery obligations. From time to time, we enter into various types of sale and exchange transactions including fixed price delivery contracts, floating price collar arrangements, financial swaps and crude oil futures contracts as hedging devices. Except for pre-defined inventory positions, our policy is generally to purchase only crude oil for which we have a market, to structure our sales contracts so that crude oil price fluctuations do not materially affect the segment profit we receive, and to not acquire and hold crude oil, futures contracts or other derivative products for the purpose of speculating on crude oil price changes as these activities could expose us to significant losses.

Crude Oil Exchanges. We pursue exchange opportunities to enhance margins throughout the gathering and marketing process. When opportunities arise to increase our margin or to acquire a grade of crude oil that more closely matches our physical delivery requirement or the preferences of our refinery customers, we exchange physical crude oil with third parties. These exchanges are effected through contracts called exchange or buy/sell agreements. Through an exchange agreement, we agree to buy crude oil that differs in terms of geographic location, grade of crude oil or physical delivery schedule from crude oil we have available for sale. Generally, we enter into exchanges to acquire crude oil at locations that are closer to our end markets, thereby reducing transportation costs and increasing our margin. We also exchange our crude oil to be physically delivered at a later date, if the exchange is expected to result in a higher margin net of storage costs, and enter into exchanges based on the grade of crude oil, which includes such factors as sulfur content and specific gravity, in order to meet the quality specifications of our physical delivery contracts. The accounting for buy/sell agreements is expected to change in 2006. See Note 2 to our Consolidated Financial Statements.

Producer Services. Crude oil purchasers who buy from producers compete on the basis of competitive prices and highly responsive services. Through our team of crude oil purchasing representatives, we maintain ongoing relationships with producers in the United States and Canada. We believe that our ability to offer high-quality field and administrative services to producers is a key factor in our ability to maintain volumes of purchased crude oil and to obtain new volumes. Field services include efficient gathering capabilities, availability of trucks, willingness to construct gathering pipelines where economically justified, timely pickup of crude oil from tank batteries at the lease or production point, accurate measurement of crude oil volumes received, and effective management of pipeline deliveries. Accounting and other administrative services include securing division orders (statements from interest owners affirming the division of ownership in crude oil purchased by us), providing statements of the crude oil purchased each month, disbursing production proceeds to interest owners, and calculating and paying ad valorem and production taxes on behalf of interest owners. In order to compete effectively, we must maintain records of title and division order interests in an accurate and timely manner for purposes of

14

making prompt and correct payment of crude oil production proceeds, together with the correct payment of all severance and production taxes associated with such proceeds.

Liquefied Petroleum Gas and Other Petroleum Products. We also market and store LPG and other petroleum products in the United States and Canada. These activities include:

· purchasing LPG (primarily propane and butane) from producers at gas plants and in bulk at major pipeline terminal points and storage locations;

· transporting the LPG via common carrier pipelines, railcars and trucks to our own terminals and third party facilities for subsequent resale to retailers and other wholesale customers; and

· exchanging product to other locations to maximize margins and /or to meet contract delivery requirements.

We purchase LPG from numerous producers and have established long-term, broad based relationships with LPG producers in our areas of operation. We purchase LPG directly from gas plants, major pipeline terminals, refineries and storage locations. Marketing activities for LPG typically consist of smaller volumes per transaction relative to crude oil.

LPG Purchases. We purchase LPG from producers, refiners, and other LPG marketing companies under contracts that range from immediate delivery to one year in term. In a typical producer’s or refiner’s operation, LPG that is produced at the gas plant or refinery is fractionated into various components including propane and butane and then purchased by us for movement via tank truck, railcar or pipeline.

In addition to purchasing LPG at gas plants or refineries, we also purchase LPG in bulk at major pipeline terminal points and storage facilities from major oil companies, large independent producers or other LPG marketing companies. We purchase LPG in bulk when we believe additional opportunities exist to realize margins further downstream in our LPG distribution chain. The opportunities to earn additional margins vary over time with changing market conditions. Accordingly, the margins associated with our bulk purchases will fluctuate from period to period.

LPG Sales. The marketing of LPG is complex and requires current detailed knowledge of LPG sources and end markets and a familiarity with a number of factors including the various modes and availability of transportation, area market prices and timing and costs of delivering LPG to customers.

We sell LPG primarily to industrial end users and retailers, and limited volumes to other marketers. Propane is sold to small independent retailers who then transport the product via bobtail truck to residential consumers for home heating and to some light industrial users such as forklift operators. Butane is used by refiners for gasoline blending and as a diluent for the movement of conventional heavy oil production. Butane demand for use as a heavy oil diluent has increased as indigenous supplies of Canadian condensate have declined.

We establish a margin for propane by transporting it in bulk, via various transportation modes, to terminals where we deliver the propane to our retailer customers for subsequent delivery to their individual heating customers. We also create margin by selling propane for future physical delivery to third party users, such as retailers and industrial users. Through these transactions, we seek to maintain a position that is substantially balanced between propane purchases and sales and future delivery obligations. From time to time, we enter into various types of sale and exchange transactions including floating price collar arrangements, financial swaps and crude oil and LPG-related futures contracts as hedging devices. Except for pre-defined inventory positions, our policy is generally to purchase only LPG for which we have a market, and to structure our sales contracts so that LPG spot price fluctuations do not materially affect the segment profit we receive. Margin is created on the butane purchased by delivering large volumes during the short refinery blending season through the use of our extensive leased railcar fleet and the use of our own storage facilities and third party storage facilities. We also create margin on

15

butane by capturing the difference in price between condensate and butane when butane is used to replace condensate as a diluent for the movement of Canadian heavy oil production. Although we seek to maintain a position that is substantially balanced within our LPG activities, as a result of production, transportation and delivery variances as well as logistical issues associated with inclement weather conditions, from time to time we experience net unbalanced positions for short periods of time. In connection with managing these positions and maintaining a constant presence in the marketplace, both necessary for our core business, our policies provide that any net imbalance may not exceed 250,000 barrels. These activities are monitored independently by our risk management function and must take place within predefined limits and authorizations.

LPG Exchanges. We pursue exchange opportunities to enhance margins throughout the marketing process. When opportunities arise to increase our margin or to acquire a volume of LPG that more closely matches our physical delivery requirement or the preferences of our customers, we exchange physical LPG with third parties. These exchanges are effected through contracts called exchange or buy/sell agreements. Through an exchange agreement, we agree to buy LPG that differs in terms of geographic location, type of LPG or physical delivery schedule from LPG we have available for sale. Generally, we enter into exchanges to acquire LPG at locations that are closer to our end markets in order to meet the delivery specifications of our physical delivery contracts.

Credit. Our merchant activities involve the purchase of crude oil and LPG for resale and require significant extensions of credit by our suppliers of crude oil and LPG. In order to assure our ability to perform our obligations under crude oil purchase agreements, various credit arrangements are negotiated with our suppliers. These arrangements include open lines of credit directly with us and, to a lesser extent, standby letters of credit issued under our senior unsecured revolving credit facility.

When we sell crude oil and LPG, we must determine the amount, if any, of the line of credit to be extended to any given customer. We manage our exposure to credit risk through credit analysis, credit approvals, credit limits and monitoring procedures. If we determine that a customer should receive a credit line, we must then decide on the amount of credit that should be extended.

Because our typical crude oil sales transactions can involve tens of thousands of barrels of crude oil, the risk of nonpayment and nonperformance by customers is a major consideration in our business. We believe our sales are made to creditworthy entities or entities with adequate credit support. Generally, sales of crude oil are settled within 30 days of the month of delivery (in the case of foreign cargoes, typically 10 days after delivery), and pipeline, transportation and terminalling services also settle within 30 days from invoice for the provision of services.

We also have credit risk with respect to our sales of LPG; however, because our sales are typically in relatively small amounts to individual customers, we do not believe that we have material concentration of credit risk. Typically, we enter into annual contracts to sell LPG on a forward basis, as well as sell LPG on a current basis to local distributors and retailers. In certain cases our customers prepay for their purchases, in amounts ranging from approximately $2 per barrel to 100% of their contracted amounts. Generally, sales of LPG are settled within 30 days of the date of invoice.

Terminalling and Storage Operations

We own approximately 39 million barrels of active above-ground crude oil terminalling and storage assets. Approximately 15 million barrels of capacity are used in our GMT&S segment, and the remaining 24 million barrels are used in our Pipeline segment. Our storage and terminalling operations increase our margins in our business of purchasing and selling crude oil and also generate revenue through a combination of storage and throughput charges to third parties. Storage fees are generated when we lease tank capacity to third parties. Terminalling fees, also referred to as throughput fees, are generated when we receive crude oil from one connecting pipeline and redeliver crude oil to another connecting carrier in

16

volumes that allow the refinery to receive its crude oil on a ratable basis throughout a delivery period. Both terminalling and storage fees are generally earned from:

· refiners and gatherers that segregate or custom blend crudes for refining feedstocks; and

· pipeline operators, refiners or traders that need segregated tankage for foreign cargoes.

The tankage that is used to support our arbitrage activities positions us to capture margins in a contango market (when the oil prices for future deliveries are higher than the current prices) or when the market switches from contango to backwardation (when the oil prices for future deliveries are lower than the current prices).

Our most significant terminalling and storage asset is our Cushing Terminal located at the Cushing Interchange. The Cushing Interchange is one of the largest wet-barrel trading hubs in the U.S. and the delivery point for crude oil futures contracts traded on the NYMEX. The Cushing Terminal has been designated by the NYMEX as an approved delivery location for crude oil delivered under the NYMEX light sweet crude oil futures contract. As the NYMEX delivery point and a cash market hub, the Cushing Interchange serves as a primary source of refinery feedstock for the Midwest refiners and plays an integral role in establishing and maintaining markets for many varieties of foreign and domestic crude oil. Our Cushing Terminal was constructed in 1993, with an initial tankage capacity of 2 million barrels, to capitalize on the crude oil supply and demand imbalance in the Midwest. The Cushing Terminal is also used to support and enhance the margins associated with our merchant activities relating to our lease gathering and bulk purchasing activities. See “—Gathering, Marketing, Terminalling and Storage Operations—Gathering and Marketing Operations—Bulk Purchases.” Since 1999, we have completed five separate expansion phases, which increased the capacity of the Cushing Terminal to a total of approximately 7.4 million barrels. The Cushing Terminal now consists of fourteen 100,000-barrel tanks, four 150,000-barrel tanks and twenty 270,000-barrel tanks, all of which are used to store and terminal crude oil. The Cushing Terminal also includes a pipeline manifold and pumping system that has an estimated throughput capacity of over 1.0 million barrels per day. The Cushing Terminal is connected to the major pipelines and other terminals in the Cushing Interchange through pipelines that range in size from 10 inches to 24 inches in diameter.

The Cushing Terminal is designed to serve the needs of refiners in the Midwest (PADD II). In order to service an increase in volumes and varieties of foreign and domestic crude oil projected to be transported through the Cushing Interchange, we incorporated certain attributes into the original design of the Cushing Terminal including:

· multiple, smaller tanks to facilitate simultaneous handling of multiple crude varieties in accordance with normal pipeline batch sizes;

· dual header systems connecting most tanks to the main manifold system to facilitate efficient switching between crude grades with minimal contamination;

· bottom drawn sumps that enable each tank to be efficiently drained down to minimal remaining volumes to minimize crude oil contamination and maintain crude oil integrity during changes of service;

· mixer(s) on each tank to facilitate blending crude oil grades to refinery specifications; and

· a manifold and pump system that allows for receipts and deliveries with connecting carriers at their maximum operating capacity.

As a result of incorporating these attributes into the design of the Cushing Terminal, we believe we are favorably positioned to serve the needs of Midwest (PADD II) refiners to handle an increase in the number of varieties of crude oil transported through the Cushing Interchange. The pipeline manifold and

17

pumping system of our Cushing Terminal is designed to support more than 10 million barrels of tank capacity. Our tankage in Cushing ranges in age from less than a year old to approximately 12 years old and the average age is approximately 5 years old. In contrast, we estimate that the average age of the remaining tanks in Cushing owned by third parties is in excess of 40 years. We believe that provides us with a long-term competitive advantage.

Our Cushing Terminal also incorporates numerous environmental and operational safeguards that distinguish it from all other facilities at the Cushing Interchange. Each tank is equipped with both primary and secondary floating roof seals, a secondary liner (the equivalent of a double bottom) with leak detection devices, dual zone overfill protection alarms and a foam dispersal system that, in the event of a fire, is fed by a fully automated fire water distribution system. Additionally, almost all terminal piping is aboveground for monitoring and inspection purposes and the facility is fully automated with real-time computer monitoring of operational data.

We also have a marine terminal in Mobile, Alabama (the “Mobile Terminal”) that consists of eighteen tanks ranging in size from 10,000 barrels to 225,000 barrels, with current useable capacity of 1.5 million barrels. Approximately 1.8 million barrels of additional storage capacity is available at our nearby Ten Mile Facility through a 36” pipeline connecting the two facilities. The Mobile Terminal is equipped with a ship/tanker dock, barge dock, truck-unloading facilities and various third party connections for crude movements to area refiners. Additionally, the Mobile Terminal serves as a source for imports of foreign crude oil to PADD II refiners through our Mississippi/Alabama pipeline system, which connects to the Capline System at our station in Liberty, Mississippi.

In 2005, we began construction of a 3.2 million barrel crude oil terminal at the St. James crude oil interchange in Louisiana, which is one of the three most liquid crude oil interchanges in the United States. We plan to build seven tanks ranging from 190,000 barrels to 625,000 barrels at the St. James Terminal, which is expected to be operational in mid-2007. The facility will also include a manifold and header system that will allow for receipts and deliveries with connecting pipelines at their maximum operating capacity.

We also own LPG storage facilities located in Alto, Michigan; Schaefferstown, Pennsylvania; Tulsa, Oklahoma and Claremont, New Hampshire. The Alto facility is approximately 20 miles southeast of Grand Rapids. The Alto facility is capable of storing over 1.2 million barrels of LPG. The Schaefferstown facility is approximately 65 miles northwest of Philadelphia and is capable of storing over 0.5 million barrels of propane. The Tulsa facility consists of a 130-mile pipeline originating in Medford, Oklahoma. The Tulsa Terminal is capable of storing 19,000 barrels of propane and has two truck loading stations. The Claremont facility is on the Vermont border and has the capacity to store approximately 17,000 barrels of propane. In addition, the Claremont facility has three truck loading stations and four rail unloading stations. We believe these facilities will further support the expansion of our LPG business in Canada and the northern tier of the U.S. as we combine the facilities’ existing fee-based storage business with our wholesale propane marketing expertise. In addition, there may be opportunities to expand these facilities as LPG markets continue to develop in the region.

Crude Oil Volatility; Counter Cyclical Balance; Risk Management

Crude oil prices have historically been very volatile and cyclical, with NYMEX benchmark prices ranging from a high of almost $71 per barrel (August 2005) to as low as $10 per barrel (March 1986) over the last 20 years. Segment profit from terminalling and storage activities is dependent on the crude oil throughput volume, capacity leased to third parties, capacity that we use for our own activities, and the level of other fees generated at our terminalling and storage facilities. Segment profit from our gathering and marketing activities is dependent on our ability to sell crude oil at a price in excess of our aggregate cost. Although margins may be affected during transitional periods, these operations are not directly

18

affected by the absolute level of crude oil prices, but are affected by overall levels of supply and demand for crude oil and relative fluctuations in market related indices.

During periods when supply exceeds the demand for crude oil, the market for crude oil is often in contango, meaning that the price of crude oil for future deliveries is higher than current prices. A contango market has a generally negative impact on marketing margins, but is favorable to the storage business, because storage owners at major trading locations (such as the Cushing Interchange) can simultaneously purchase production at current prices for storage and sell at higher prices for future delivery.

When there is a higher demand than supply of crude oil in the near term, the market is backwardated, meaning that the price of crude oil for future deliveries is lower than current prices. A backwardated market has a positive impact on marketing margins because crude oil gatherers can capture a premium for prompt deliveries. In this environment, there is little incentive to store crude oil as current prices are above future delivery prices.

The periods between a backwardated market and a contango market are referred to as transition periods. Depending on the overall duration of these transition periods, how we have allocated our assets to particular strategies and the time length of our crude oil purchase and sale contracts and storage lease agreements, these transition periods may have either an adverse or beneficial affect on our aggregate segment profit. A prolonged transition from a backwardated market to a contango market, or vice versa (essentially a market that is neither in pronounced backwardation nor contango), represents the most difficult environment for our gathering, marketing, terminalling and storage activities. When the market is in contango, we will use our tankage to improve our gathering margins by storing crude oil we have purchased for delivery in future months that are selling at a higher price. In a backwardated market, we use less storage capacity but increased marketing margins provide an offset to this reduced cash flow. We believe that the combination of our terminalling and storage activities and gathering and marketing activities provides a counter-cyclical balance that has a stabilizing effect on our operations and cash flow. In addition, we supplement the counter-cyclical balance of our asset base with derivative hedging activities in an effort to maintain a base level of margin irrespective of whether a strong or weak market exists and, in certain circumstances, to realize incremental margin during volatile market conditions. References to counter-cyclical balance elsewhere in this report are referring to this relationship between our terminalling and storage activities and our gathering and marketing activities in transitioning crude oil markets.

As use of the financial markets for crude oil has increased by producers, refiners, utilities and trading entities, risk management strategies, including those involving price hedges using NYMEX and IPE futures contracts and derivatives, have become increasingly important in creating and maintaining margins. In order to hedge margins involving our physical assets and manage risks associated with our crude oil purchase and sale obligations and, in certain circumstances, to realize incremental margin during volatile market conditions, we use derivative instruments, including regulated futures and options transactions, as well as over-the-counter instruments. In analyzing our risk management activities, we draw a distinction between enterprise level risks and trading related risks. Enterprise level risks are those that underlie our core businesses and may be managed based on whether there is value in doing so. Conversely, trading related risks (the risks involved in trading in the hopes of generating an increased return) are not inherent in the core business; rather, those risks arise as a result of engaging in the trading activity. Our risk management policies and procedures are designed to monitor NYMEX, IPE and over-the-counter positions and physical volumes, grades, locations and delivery schedules to ensure that our hedging activities are implemented in accordance with such policies. We have a risk management function that has direct responsibility and authority for our risk policies, our trading controls and procedures and certain other aspects of corporate risk management. Our risk management function also approves all new risk management strategies through a formal process. With the exception of the controlled trading program discussed below, our approved strategies are intended to mitigate enterprise level risks that are inherent in our core businesses of crude oil gathering and marketing and storage.

19

Our policy is generally to purchase only crude oil for which we have a market, and to structure our sales contracts so that crude oil price fluctuations do not materially affect the segment profit we receive. Except for the controlled trading program discussed below, we do not acquire and hold crude oil futures contracts or other derivative products for the purpose of speculating on crude oil price changes as these activities could expose us to significant losses.

Although we seek to maintain a position that is substantially balanced within our crude oil lease purchase and LPG activities, we may experience net unbalanced positions for short periods of time as a result of production, transportation and delivery variances as well as logistical issues associated with inclement weather conditions. In connection with managing these positions and maintaining a constant presence in the marketplace, both necessary for our core business, we engage in a controlled trading program for up to an aggregate of 500,000 barrels of crude oil. This controlled trading activity is monitored independently by our risk management function and must take place within predefined limits and authorizations.

Although the intent of our risk-management strategies is to hedge our margin, not all of our derivatives qualify for hedge accounting. In such instances, changes in the fair values of these derivatives will receive mark-to-market treatment in current earnings, and result in greater potential for earnings volatility.

Geographic Data; Financial Information about Segments

See Note 13 to our Consolidated Financial Statements.

Natural Gas Storage Market Overview