UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-09067

Kirr, Marbach Partners Funds, Inc.

(Exact name of registrant as specified in charter)

621 Washington Street, Columbus, IN 47201

(Address of principal executive offices) (Zip code)

Kirr, Marbach & Company, LLC, 621 Washington Street, Columbus, IN 47201

(Name and address of agent for service)

(812) 376-9444

Registrant's telephone number, including area code

Date of fiscal year end: September 30, 2014

Date of reporting period: March 31, 2014

Item 1. Report to Stockholders.

Kirr, Marbach Partners

Value Fund

| Semi-Annual Report | |

| March 31, 2014 |

www.kmpartnersfunds.com

KIRR, MARBACH PARTNERS

VALUE FUND

“Games are won by players who focus on the playing field—not by those whose eyes are glued to the scoreboard. If you can enjoy Saturdays and Sundays without looking at stock prices, give it a try on weekdays.”

—Warren Buffett

May 5, 2014

Dear Fellow Shareholders:

The U.S. equity market, as represented by the Russell 3000 and S&P 500, continued to perform strongly in the six-month period ending March 31, 2014. Value Fund slightly underperformed its benchmarks for the same period, all of which can be traced to trailing the benchmarks slightly during the torrid last calendar quarter of 2014 (ending December 31, 2013). We think it is good news stocks were able to withstand the beginning of the Federal Reserve’s “tapering” of its emergency program of quantitative easing, some softer economic data early in 2014 and geopolitical upheaval abroad.

In addition, we made some good news of our own. For the second consecutive year, we are proud to let you know Value Fund won a prestigious Best Fund Award from Lipper—a Thomson Reuters company, an independent mutual fund research and rating service. Value Fund won the 2014 Lipper Best Multi-Cap Core Fund Award out of 581 funds for the 5-year period ended November 30, 2013 based on risk-adjusted performance. Value Fund previously won the 2013 Lipper Best Multi-Cap Core Fund Award out of 647 funds for the 3-year period ended November 30, 2012 based on risk-adjusted performance. We believe receiving a Lipper Best Fund Award for two years in a row validates we can compete on an investment performance basis with the biggest and best firms in our industry. Further, we are invested alongside you and glad our “slow and steady” approach won this “race” for our investors.

| Periods ending | Value Fund(1) | Russell 3000(2) | S&P 500(3) | |||

March 31, 2014(4) | Total Return | Index | Index | |||

| 6-months | 10.78 | % | 12.28 | % | 12.51 | % |

| One-year | 23.96 | % | 22.61 | % | 21.86 | % |

| Two-years | 21.07 | % | 18.52 | % | 17.84 | % |

| Three-years | 15.00 | % | 14.61 | % | 14.66 | % |

| Five-years | 29.22 | % | 21.93 | % | 21.16 | % |

| Ten-years | 8.37 | % | 7.86 | % | 7.42 | % |

| Since Inception (December 31, 1998) | 8.40 | % | 5.37 | % | 4.72 | % |

The Fund’s Gross Expense Ratio and Net Expense Ratio were 1.54% and 1.45% respectively, according to the Prospectus dated January 28, 2014. Until February 28, 2015, the Adviser has contractually agreed to waive its management fee and/or reimburse the Fund’s other expenses. Investment performance reflects waivers in effect. In the absence of such waivers, total return would be reduced.

Performance data quoted represents past performance; past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 1-800-870-8039. The fund imposes a 1.00% redemption fee on shares held less than 30 days. Performance data quoted does not reflect the redemption fee. If reflected, total returns would be reduced.

| (1) | The performance data quoted assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

1

KIRR, MARBACH PARTNERS

VALUE FUND

| (2) | The Russell 3000 Index is an unmanaged, capitalization-weighted index generally representative of the overall U.S. stock market. This Index cannot be invested in directly. |

| (3) | The S&P 500 Index is an unmanaged, capitalization-weighted index generally representative of the U.S. market for large capitalization stocks. This Index cannot be invested in directly. |

| (4) | One-year, Two-years, Three-years, Five-years, Ten-years and Since Inception returns are Average Annualized Returns. |

The Stock Market

U.S. stocks experienced some harrowing moments in January and early February. As mentioned above, some data on the U.S. economy was softer than investors had expected, perhaps due in part to the severe winter weather. Similarly, concerns about Federal Reserve policy resurfaced as new Chair Janet Yellen took the reins from Ben Bernanke. It seems lately there is always an overseas crisis. Indeed, just as the Eurozone crisis faded into memory, Russia reminded us the world remains a dangerous place.

Similarly, the U.S. stock market reminded investors lulled by a strong 2012 and 2013 it can still quickly turn vicious. The Dow Jones Industrial Average plunged 326 points on February 3, which left it down 7.3% for the year-to-date. U.S. stocks had not suffered a correction (10% decline) since 2011, so many investors were shaken. As shown in the Crandall, Pierce graph, since 1944 stocks have endured a bear market (20% decline) or correction every 2 years, on average. Thus, a correction is neither a rare occurrence nor something to be overly fearful of. When the talking heads on TV and headlines have you feeling down, try Warren Buffett’s suggestion!

Speaking of Buffett’s 2013 Berkshire Hathaway shareholder letter, he told the tale of two investments he was able to make decades ago, at what turned out to be ridiculously low prices, in the wake of the bursting of the bubbles in farmland and commercial real estate. He said:

“There is one major difference between my two small investments and an investment in stocks. Stocks provide you minute-to-minute valuations for your holdings whereas I have yet to see a quotation for either my farm or the New York real estate.

“It should be an enormous advantage for investors in stocks to have those wildly fluctuating valuations placed on their holdings—and for some investors, it is. After all, if a moody fellow with a farm bordering my property yelled out a price every day to me at which he would either buy my farm or sell his—and those prices varied widely over short periods of time depending on his mental state—how in the world could I be other than benefited by his erratic behavior? If his daily shout-out was ridiculously low, and I had some spare cash, I would buy his farm. If the number he yelled was absurdly high, I could either sell to him or just go on farming.

“Owners of stocks, however, too often let the capricious and often irrational behavior of their fellow owners cause them to behave irrationally, as well. Because there is so much chatter about markets, the economy, interest rates, price behavior of stocks, etc., some investors believe it is important to listen to pundits—and, worse yet, important to consider acting upon their comments.

“Those people who can sit quietly for decades when they own a farm or apartment house often become frenetic when they are exposed to a stream of stock quotations and accompanying commentators delivering an implied message of ‘Don’t just sit there, do something.’ For these investors, liquidity is transformed from the unqualified benefit it should be to a curse.

2

KIRR, MARBACH PARTNERS

VALUE FUND

“A ‘flash crash’ or some other extreme market fluctuation can’t hurt an investor any more than an erratic and mouthy neighbor can hurt my farm investment. Indeed, tumbling markets can be helpful to the true investor if he has cash available when prices get far out of line with values. A climate of fear is your friend when investing; a euphoric world is your enemy.

“During the extraordinary financial panic that occurred late in 2008, I never gave a thought to selling my farm or New York real estate, even though a severe recession was clearly brewing. And, if I had owned 100% of a solid business with good long-term prospects, it would have been foolish for me to even consider dumping it. So why would I have sold my stocks that were small participations in wonderful businesses? True, any one of them might eventually disappoint, but as a group they were certain to do well. Could anyone really believe the earth was going to swallow up the incredible productive assets and unlimited human ingenuity existing in America?”

We have stated our belief the overall recovery from the Great Recession has broadened to the point where it should be much more sustainable and less susceptible to shocks. Additionally, we concentrate on analyzing companies and finding stocks selling at a discount to intrinsic value. This type of micro-analysis is the basis of value investing. Thus, we don’t spend a lot of time trying to forecast unknowable macro-factors, such as Federal Reserve policy changes or military invasions. Speaking of Federal Reserve policy, many investors feared the eventual winding-down of its emergency program of “quantitative easing.” These same investors wrongly believed stock prices had been propelled higher primarily due to Fed policy. We thought tapering would be a positive sign for the strength of the economy and good for stocks. In other words, investors should not “fear the taper.” The Federal Reserve has begun to reduce its monthly purchases of bonds by about $10 billion/month, which the equity and fixed income markets and economy appear to have taken in stride.

Valuations are materially higher than at the once-in-a-lifetime levels of five years ago. Thus, in our opinion, the overall market can probably be characterized as “fairly valued” (but not overstretched). It is more difficult to find investment candidates with attractive risk/reward characteristics, but we continue to like what we own and remain fully invested.

Percent Change in Top Ten Holdings from Book Cost (as of 3/31/2014)

| 1. | Alliance Data Systems Corp. | +270.4 | % | 6. | NewMarket Corporation | +115.2 | % | ||||||||

| 2. | Portfolio Recovery Associates, Inc. | +207.2 | % | 7. | Cognizant Technology Solutions | +420.2 | % | ||||||||

| 3. | WABCO Holdings Inc. | +454.5 | % | 8. | Ascent Capital Group LLC. | +208.2 | % | ||||||||

| 4. | LyondellBasell Industries NV | +337.2 | % | 9. | Canadian Pacific Railway LTD | +409.7 | % | ||||||||

| 5. | NCR Corporation | +136.4 | % | 10. | Rosetta Resources, Inc. | +172.4 | % |

Performance quoted represents past performance and is no guarantee of future results.

Fund holdings and sector allocations are subject to change and are not recommendations to buy or sell any security.

3

KIRR, MARBACH PARTNERS

VALUE FUND

Summary

We’re pleased with our continuing national recognition, but at the same time truly humbled by the trust and confidence you place in us, each and every day, to allow us the privilege to manage your precious assets. Public recognition or not, we wouldn’t have a business without our fellow shareholders. We will continue to strive to earn your business.

Regards,

|  |

| Mark D. Foster, CFA | Mickey Kim, CFA |

| President | Vice-President, Treasurer and Secretary |

Value Fund invests in foreign securities, which involves greater volatility and political, economic and currency risks and differences in accounting methods. Value Fund may also invest in small- and medium-capitalization companies, which tend to have more limited liquidity and greater price volatility than large-capitalization companies.

Past performance is not a guarantee of future results.

Please refer to the Schedule of Investments for complete fund holdings information.

The information provided herein represents the opinion of Value Fund’s investment adviser and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

A Lipper Fund Award is awarded to one fund in each Lipper classification for achieving the strongest trend of consistent risk-adjusted performance against its classification peers over a three-, five- or ten-year period. Although Lipper makes reasonable efforts to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by Lipper. Users acknowledge that they have not relied upon any warranty, condition, guarantee, or representation made by Lipper. Any use of the data for analyzing, managing, or trading financial instruments is at the user’s own risk. This is not an offer to buy or sell securities. Lipper—a Thomson Reuters company is an independent mutual fund research and rating service.

This material must be preceded or accompanied by a current Prospectus.

Quasar Distributors, LLC is the Distributor for Value Fund.

For further information about Value Fund and/or an account application, please call Matt Kirr at Value Fund at (812) 376-9444 or (800) 808-9444 or write to Value Fund at 621 Washington Street, Columbus, IN 47202-1729.

4

KIRR, MARBACH PARTNERS

VALUE FUND

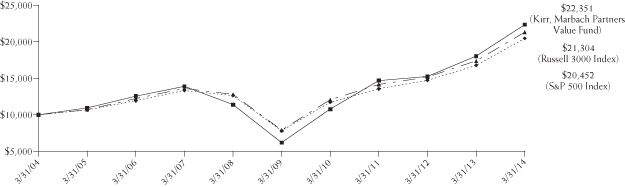

Value of $10,000 Investment (Unaudited)

This chart assumes an initial investment of $10,000. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate, so that your shares, when redeemed maybe worth more or less than their original cost. Performance assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| Average Annual Rate of Return (%) | ||||

| One Year Ended | Five Years Ended | Ten Years Ended | Since Inception* to | |

| March 31, 2014 | March 31, 2014 | March 31, 2014 | March 31, 2014 | |

| Kirr Marbach Partners Value Fund | 23.96% | 29.22% | 8.37% | 8.40% |

| Russell 3000 Index** | 22.61% | 21.93% | 7.86% | 5.37% |

| S&P 500 Index*** | 21.86% | 21.16% | 7.42% | 4.72% |

| * | December 31, 1998 |

| ** | The Russell 3000 Index is an unmanaged, capitalization-weighted index generally representative of the overall U.S. stock market. This Index cannot be invested in directly. |

| *** | The Standard & Poor’s 500 Index (S&P 500) is an unmanaged, capitalization-weighted index generally representative of the U.S. market for large capitalization stocks. This Index cannot be invested in directly. |

5

KIRR, MARBACH PARTNERS

VALUE FUND

Expense Example – March 31, 2014

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, which may include redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (October 1, 2013 – March 31, 2014).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. Although the Fund charges no sales load or transaction fees, you will be assessed fees for outgoing wire transfers, returned checks and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Fund’s transfer agent. If you request that a redemption be made by wire transfer, currently a $15.00 fee is charged by the Fund’s transfer agent. You will be charged a transaction fee equal to 1.00% of the net amount of the redemption if you redeem your shares within 30 days of purchase. IRA accounts will be charged a $15.00 annual maintenance fee. To the extent the Fund invests in shares of other investment companies as part of its investment strategy, you will indirectly bear your proportionate share of any fees and expenses charged by the underlying funds in which the Fund invests in addition to the expenses of the Fund. Actual expenses of the underlying funds are expected to vary among the various underlying funds. These expenses are not included in the example below. The example below includes, but is not limited to, management fees, shareholder servicing fees, fund accounting, custody and transfer agent fees. However, the example below does not include portfolio trading commissions and related expenses, interest expense and other extraordinary expenses as determined under generally accepted accounting principles. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning | Ending | Expenses Paid | |

| Account Value | Account Value | During Period | |

| 10/1/13 | 3/31/14 | 10/1/13 – 3/31/14(1) | |

| Actual | $1,000.00 | $1,107.80 | $7.62 |

| Hypothetical (5% return before expenses) | 1,000.00 | 1,017.70 | 7.29 |

| (1) | Expenses are equal to the Fund’s annualized expense ratio after expense reimbursement of 1.45% multiplied by the average account value over the period, multiplied by 182/365 to reflect the one-half year period. The annualized expense ratio prior to expense reimbursement was 1.46%. |

6

KIRR, MARBACH PARTNERS

VALUE FUND

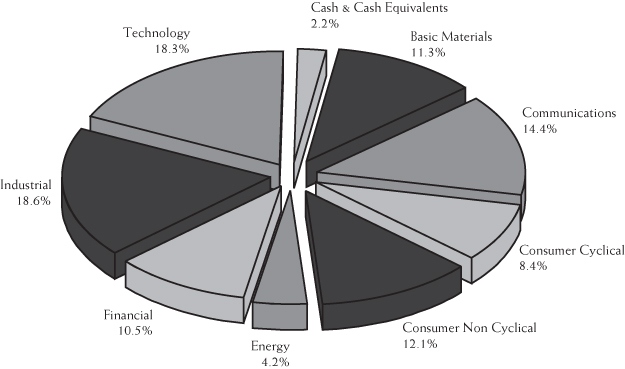

Allocation of Portfolio Net Assets

March 31, 2014 (Unaudited)

Top Ten Equity Holdings

as of March 31, 2014 (Unaudited)

(% of net assets)

| Alliance Data Systems Corp. | 4.7 | % | |||

| Portfolio Recovery Associates, Inc. | 4.1 | % | |||

| WABCO Holdings, Inc. | 3.9 | % | |||

| LyondellBasell Industries NV – Class A | 3.7 | % | |||

| NCR Corp. | 3.7 | % | |||

| NewMarket Corp. | 3.3 | % | |||

| Cognizant Technology Solutions Corp. – Class A | 3.3 | % | |||

| Ascent Capital Group, Inc. – Class A | 3.1 | % | |||

| Canadian Pacific Railway Ltd. | 3.1 | % | |||

| Rosetta Resources, Inc. | 3.1 | % |

7

KIRR, MARBACH PARTNERS

Schedule of Investments

VALUE FUND

Schedule of Investments

March 31, 2014 (Unaudited)

| Number | |||||||

| of Shares | Value | ||||||

| COMMON STOCKS – 97.8% | |||||||

| Basic Materials – 11.3% | |||||||

| 47,800 | Innospec, Inc. | $ | 2,161,994 | ||||

| 31,397 | LyondellBasell Industries | ||||||

| NV – Class A | 2,792,449 | ||||||

| 6,500 | NewMarket Corp. | 2,540,070 | |||||

| 51,050 | Taminco Corp.* | 1,072,561 | |||||

| 8,567,074 | |||||||

| Communications – 14.4% | |||||||

| 79,430 | ARRIS Group, Inc.* | 2,238,337 | |||||

| 38,085 | Knowles Corp.* | 1,202,343 | |||||

| 16,300 | Liberty Media Corp. – Class A* | 2,130,899 | |||||

| 16,625 | NeuStar, Inc. – Class A* | 540,479 | |||||

| 80,900 | News Corporation – Class A* | 1,393,098 | |||||

| 12,120 | Time Warner Cable, Inc. – Class A | 1,662,622 | |||||

| 22,820 | Tribune Co.* | 1,817,613 | |||||

| 10,985,391 | |||||||

| Consumer Cyclical – 8.4% | |||||||

| 11,735 | AMC Entertainment | ||||||

| Holdings, Inc. – Class A* | 284,574 | ||||||

| 46,225 | American Airlines Group, Inc.* | 1,691,835 | |||||

| 2,800 | AutoZone, Inc.* | 1,503,880 | |||||

| 25,695 | Dollar Tree, Inc.* | 1,340,765 | |||||

| 83,950 | Pier 1 Imports, Inc. | 1,584,976 | |||||

| 6,406,030 | |||||||

| Consumer Non Cyclical – 12.1% | |||||||

| 55,280 | Alere, Inc.* | 1,898,868 | |||||

| 13,100 | Alliance Data Systems Corp.* | 3,569,095 | |||||

| 31,500 | Ascent Capital | ||||||

| Group, Inc. – Class A* | 2,379,825 | ||||||

| 18,136 | Covidien PLC | 1,335,898 | |||||

| 9,183,686 | |||||||

| Energy – 4.2% | |||||||

| 22,565 | EPL Oil & Gas, Inc.* | 871,009 | |||||

| 50,479 | Rosetta Resources, Inc.* | 2,351,312 | |||||

| 3,222,321 | |||||||

| Financial – 10.5% | |||||||

| 38,525 | American International Group, Inc. | 1,926,635 | |||||

| 54,420 | ING U.S., Inc. | 1,973,813 | |||||

| 1,676 | Markel Corp.* | 999,064 | |||||

| 53,550 | Portfolio Recovery Associates, Inc.* | 3,098,403 | |||||

| 7,997,915 | |||||||

| Industrial – 18.6% | |||||||

| 15,763 | Canadian Pacific Railway Ltd. | 2,371,228 | |||||

| 33,060 | EMCOR Group, Inc. | 1,546,878 | |||||

| 28,386 | EnerSys | 1,966,866 | |||||

| 38,428 | KBR, Inc. | 1,025,259 | |||||

| 54,030 | MasTec, Inc.* | 2,347,063 | |||||

| 53,892 | Titan International, Inc. | 1,023,409 | |||||

| 19,891 | Tyco International Ltd. | 843,378 | |||||

| 28,353 | WABCO Holdings, Inc.* | 2,992,943 | |||||

| 14,117,024 | |||||||

| Technology – 18.3% | |||||||

| 49,000 | Cognizant Technology | ||||||

| Solutions Corp. – Class A* | 2,479,890 | ||||||

| 21,007 | eBay, Inc.* | 1,160,426 | |||||

| 28,990 | Liquidity Services, Inc.* | 755,190 | |||||

| 76,064 | NCR Corp.* | 2,780,139 | |||||

| 35,520 | Open Text Corp.* | 1,694,659 | |||||

| 31,180 | Oracle Corp. | 1,275,574 | |||||

| 67,390 | Tessera Technologies, Inc. | 1,592,426 | |||||

| 59,940 | Yahoo! Inc.* | 2,151,846 | |||||

| 13,890,150 | |||||||

| TOTAL COMMON STOCKS | |||||||

| (Cost $36,141,703) | 74,369,591 | ||||||

| SHORT-TERM INVESTMENT – 2.3% | |||||||

| 1,740,447 | Fidelity Institutional Money | ||||||

| Market Portfolio, 0.05%** | 1,740,447 | ||||||

| TOTAL SHORT-TERM | |||||||

| INVESTMENT (Cost $1,740,447) | 1,740,447 | ||||||

| Total Investments | |||||||

| (Cost $37,882,150) – 100.1% | 76,110,038 | ||||||

| Other Assets and | |||||||

| Liabilities, Net (0.1)% | (50,050 | ) | |||||

| TOTAL NET ASSETS – 100.0% | $ | 76,059,988 | |||||

| * | Non-income producing security. |

| ** | Rate in effect as of March 31, 2014. |

See Notes to the Financial Statements

8

KIRR, MARBACH PARTNERS

VALUE FUND

| Statement of Assets and Liabilities | ||||

| March 31, 2014 (Unaudited) | ||||

| ASSETS: | ||||

| Investments, at current value | ||||

| (cost $37,882,150) | $ | 76,110,038 | ||

| Receivable for Fund shares sold | 45,951 | |||

| Prepaid expenses | 18,678 | |||

| Dividends receivable | 14,736 | |||

| Interest receivable | 67 | |||

| Total Assets | 76,189,470 | |||

| LIABILITIES: | ||||

| Payable to Adviser | 66,289 | |||

| Accrued expenses | 47,863 | |||

| Payable for capital shares redeemed | 9,508 | |||

| Accrued distribution fees | 5,822 | |||

| Total liabilities | 129,482 | |||

| NET ASSETS | $ | 76,059,988 | ||

| NET ASSETS CONSIST OF: | ||||

| Capital Stock | $ | 46,493,794 | ||

| Undistributed net investment loss | (692,257 | ) | ||

| Undistributed net realized loss on investments | (7,969,477 | ) | ||

| Net unrealized appreciation on investments | 38,227,928 | |||

| Total Net Assets | $ | 76,059,988 | ||

| Shares outstanding (500,000,000 shares | ||||

| of $0.01 par value authorized) | 3,288,233 | |||

Net asset value and offering price per share(1) | $ | 23.13 | ||

| (1) | A redemption fee of 1.00% is assessed against shares redeemed within 30 days of purchase. |

Statement of Operations

Six Months Ended March 31, 2014 (Unaudited)

| INVESTMENT INCOME: | ||||

| Dividend income | ||||

| (net of withholding of $3,119) | $ | 216,799 | ||

| Interest income | 549 | |||

| Total Investment Income | 217,348 | |||

| EXPENSES: | ||||

| Investment Adviser fees | 360,272 | |||

| Distribution fees | 31,763 | |||

| Legal fees | 29,505 | |||

| Administration fees | 21,342 | |||

| Transfer agent fees | 20,108 | |||

| Federal & state registration fees | 14,424 | |||

| Fund accounting fees | 14,164 | |||

| Audit fees | 10,357 | |||

| Custody fees | 7,901 | |||

| Directors fees | 6,006 | |||

| Postage & printing fees | 4,574 | |||

| Other | 3,914 | |||

| Total expenses before reimbursement | 524,330 | |||

| Less: Reimbursement from Investment Adviser | (1,936 | ) | ||

| Net Expenses | 522,394 | |||

| NET INVESTMENT LOSS | (305,046 | ) | ||

| REALIZED AND UNREALIZED | ||||

| GAIN ON INVESTMENTS: | ||||

| Net realized gains on investments | 953,233 | |||

| Net change in unrealized appreciation | ||||

| on investments | 6,670,684 | |||

| Net realized and unrealized gain | ||||

| on investments | 7,623,917 | |||

| NET INCREASE IN NET ASSETS | ||||

| RESULTING FROM OPERATIONS | $ | 7,318,871 | ||

See Notes to the Financial Statements

9

KIRR, MARBACH PARTNERS

VALUE FUND

Statement of Changes in Net Assets

| Six Months Ended | ||||||||

| March 31, 2014 | Year Ended | |||||||

(Unaudited) | September 30, 2013 | |||||||

| OPERATIONS: | ||||||||

| Net investment loss | $ | (305,046 | ) | $ | (204,734 | ) | ||

| Net realized gain on investments | 953,233 | 3,511,813 | ||||||

| Net change in unrealized appreciation on investments | 6,670,684 | 11,635,790 | ||||||

| Net increase in net assets resulting from operations | 7,318,871 | 14,942,869 | ||||||

| CAPITAL SHARE TRANSACTIONS: | ||||||||

| Proceeds from shares sold | 7,581,994 | 11,412,117 | ||||||

| Proceeds from reinvestment of distributions | — | — | ||||||

| Payments for shares redeemed | (5,441,860 | ) | (8,191,775 | ) | ||||

| Redemption fees | 291 | 1,459 | ||||||

| Net increase in net assets resulting from capital share transactions | 2,140,425 | 3,221,801 | ||||||

| TOTAL INCREASE IN NET ASSETS | 9,459,296 | 18,164,670 | ||||||

| NET ASSETS: | ||||||||

| Beginning of period | 66,600,692 | 48,436,022 | ||||||

| End of period (including undistributed net investment loss of | ||||||||

| ($692,257) and ($387,211), respectively) | $ | 76,059,988 | $ | 66,600,692 | ||||

| CHANGES IN SHARES OUTSTANDING: | ||||||||

| Shares sold | 343,265 | 629,869 | ||||||

| Shares issued to holders in reinvestment of dividends | — | — | ||||||

| Shares redeemed | (244,082 | ) | (445,974 | ) | ||||

| Net increase | 99,183 | 183,895 | ||||||

See Notes to the Financial Statements

10

KIRR, MARBACH PARTNERS

VALUE FUND

Financial Highlights

For a Fund share outstanding throughout the period.

| March 31, 2014 | Year Ended September 30, | |||||||||||||||||||||||

(Unaudited)(1) | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||||||||||

| PER SHARE DATA: | ||||||||||||||||||||||||

| Net asset value, beginning of period | $ | 20.88 | $ | 16.12 | $ | 11.78 | $ | 11.53 | $ | 9.57 | $ | 10.54 | ||||||||||||

| Investment operations: | ||||||||||||||||||||||||

| Net investment income (loss) | (0.09 | ) | (0.06 | ) | (0.07 | ) | (0.09 | ) | (0.07 | ) | 0.11 | |||||||||||||

| Net realized and unrealized | ||||||||||||||||||||||||

| gain (loss) on investments | 2.34 | 4.82 | 4.41 | 0.34 | 2.14 | (1.08 | ) | |||||||||||||||||

| Total from investment operations | 2.25 | 4.76 | 4.34 | 0.25 | 2.07 | (0.97 | ) | |||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

| Dividends from net investment income | — | — | — | — | (0.11 | ) | — | |||||||||||||||||

| Dividends from net capital gains | — | — | — | — | — | — | ||||||||||||||||||

| Total distributions | — | — | — | — | (0.11 | ) | — | |||||||||||||||||

| Paid in capital from redemption fees | — | (2) | — | (2) | — | (2) | — | (2) | — | — | (2) | |||||||||||||

| Net asset value, end of period | $ | 23.13 | $ | 20.88 | $ | 16.12 | $ | 11.78 | $ | 11.53 | $ | 9.57 | ||||||||||||

| TOTAL RETURN | 10.78 | % | 29.53 | % | 36.84 | % | 2.17 | % | 21.79 | % | (9.20 | )% | ||||||||||||

| SUPPLEMENTAL DATA AND RATIOS: | ||||||||||||||||||||||||

| Net assets, end of period (in millions) | $ | 76.1 | $ | 66.6 | $ | 48.4 | $ | 66.3 | $ | 29.0 | $ | 25.7 | ||||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||||||

| Before expense reimbursement | 1.46 | % | 1.54 | % | 1.65 | % | 1.66 | % | 1.90 | % | 1.99 | % | ||||||||||||

| After expense reimbursement | 1.45 | % | 1.45 | % | 1.45 | % | 1.45 | % | 1.45 | % | 1.45 | % | ||||||||||||

| Ratio of net investment income (loss) | ||||||||||||||||||||||||

| to average net assets: | ||||||||||||||||||||||||

| Before expense reimbursement | (0.85 | )% | (0.45 | )% | (0.63 | )% | (1.05 | )% | (1.12 | )% | 0.71 | % | ||||||||||||

| After expense reimbursement | (0.84 | )% | (0.36 | )% | (0.42 | )% | (0.84 | )% | (0.67 | )% | 1.25 | % | ||||||||||||

| Portfolio turnover rate | 7 | % | 21 | % | 14 | % | 15 | % | 23 | % | 48 | % | ||||||||||||

| (1) | All ratios for the six month period ended March 31, 2014 have been annualized, except total return and portfolio turnover. |

| (2) | Less than $0.01 per share. |

See Notes to the Financial Statements

11

KIRR, MARBACH PARTNERS

VALUE FUND

Notes to the Financial Statements

March 31, 2014 (Unaudited)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Kirr, Marbach Partners Funds, Inc. (the “Corporation”) was organized as a Maryland corporation on September 23, 1998 and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end diversified management investment company issuing its shares in series, each series representing a distinct portfolio with its own investment objective and policies. The one series presently authorized is the Kirr, Marbach Partners Value Fund (the “Fund”). The investment objective of the Fund is to seek long-term capital growth. The Fund commenced operations on December 31, 1998.

The following is a summary of significant accounting policies consistently followed by the Fund.

| a) | Investment Valuation – Securities listed on the Nasdaq National Market are valued at the Nasdaq Official Closing Price (“NOCP”). Other securities traded on a national securities exchange (including options on indices so traded) are valued at the last sales price on the exchange where the security is primarily traded. Exchange-traded securities for which there were no transactions and Nasdaq-traded securities for which there is no NOCP are valued at the mean of the bid and asked prices. Securities for which market quotations are not readily available are valued at fair value as determined in good faith under the supervision of the Board of Directors. Foreign securities have been issued by foreign private issuers registered on United States exchanges in accordance with Section 12 of the Securities Exchange Act of 1934. Debt securities maturing in 60 days or less are valued at amortized cost, which approximates fair value. Debt securities having maturities over 60 days or for which amortized cost is not deemed to reflect fair value may be priced by independent pricing services that use prices provided by market makers or estimates of market values obtained from yield data relating to instruments or securities with similar characteristics. | |

The Fund has performed an analysis of all existing investments to determine the significance and character of all inputs to their fair value determination. Various inputs are used in determining the value of each of the Fund’s investments. These inputs are summarized in the following three broad categories: |

| Level 1 – | Unadjusted quoted prices in active markets for identical assets or liabilities that the company has the ability to access. | ||

| Level 2 – | Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability either directly or indirectly. These inputs may include quoted prices for the identical instruments on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates, and similar data. | ||

| Level 3 – | Unobservable inputs for the asset or liability to the extent that relevant observable inputs are not available, representing the company’s own assumptions about the assumptions that a market participant would use in valuing the asset or liability, and that would be based on the best information available. |

| The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3. |

12

KIRR, MARBACH PARTNERS

VALUE FUND

Notes to the Financial Statements (Continued)

March 31, 2014 (Unaudited)

| The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety. | ||

| The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities. The following is a summary of the inputs used to value the Fund’s investments as of March 31, 2014: |

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Common Stocks | $ | 74,369,591 | $ | — | $ | — | $ | 74,369,591 | ||||||||

| Short-Term Investment | 1,740,447 | — | — | 1,740,447 | ||||||||||||

| Total Investments | $ | 76,110,038 | $ | — | $ | — | $ | 76,110,038 | ||||||||

| Refer to the Schedule of Investments for industry classifications. Transfers between levels are recognized at the end of the reporting period. During the period ended March 31, 2014, the Fund recognized no transfers to/from Level 1 or Level 2. The Fund did not invest in any Level 3 investments during the period. |

| b) | Federal Income Taxes – A provision, for federal income taxes or excise taxes, has not been made since the Fund has elected to be taxed as a “regulated investment company” and intends to distribute substantially all taxable income to its shareholders and otherwise comply with the provisions of the Internal Revenue Code applicable to regulated investment companies. There is no tax liability resulting from unrecognized tax benefits relating to uncertain income tax positions taken or expected to be taken on the tax return for the fiscal year ended September 30, 2013, or for any other tax years which are open for exam. As of September 30, 2013, open tax years include the tax years ended September 30, 2010 through 2013. The Fund is also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the period, the Fund did not incur any interest or penalties. | |

| c) | Income and Expense – The Fund is charged for those expenses that are directly attributable to the Fund, such as advisory, administration and certain shareholder service fees. | |

| d) | Distributions to Shareholders – Dividends from net investment income and distributions of net realized capital gains, if any, will be declared and paid at least annually. The character of distributions made during the period from net investment income or net realized gains may differ from the characterization for federal income tax purposes due to differences in the recognition of income, expense and gain items for financial statement and tax purposes. All short term capital gains are included in ordinary income for tax purposes. | |

| e) | Use of Estimates – The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. | |

| f) | Repurchase Agreements – The Fund may enter into repurchase agreements with certain banks or non-bank dealers. The Adviser will monitor, on an ongoing basis, the value of the underlying securities to ensure that the value always equals or exceeds the repurchase price plus accrued interest. |

13

KIRR, MARBACH PARTNERS

VALUE FUND

Notes to the Financial Statements (Continued)

March 31, 2014 (Unaudited)

| g) | Other – Investment and shareholder transactions are recorded on the trade date. The Fund determines the gain or loss realized from the investment transactions by comparing the original cost of the security lot sold with the net sales proceeds. Dividend income is recognized on the ex-dividend date or as soon as information is available to the Fund and interest income is recognized on an accrual basis. Accounting principles generally accepted in the United States require that permanent financial reporting and tax differences be reclassified to capital stock. | |

| h) | Events Subsequent to Year End – Management has evaluated fund related events and transactions that occurred subsequent to March 31, 2014 through the date of issuance of the Fund’s financial statements. There were no events or transactions that occurred during this period that materially impacted the amounts or disclosures in the Fund’s financial statements. |

2. INVESTMENT TRANSACTIONS

The aggregate purchases and sales of securities, excluding short-term investments, by the Fund for the six months ended March 31, 2014, were as follows:

| Purchases | Sales | |||||||

| U.S. Government | $ | — | $ | — | ||||

| Other | $ | 5,310,806 | $ | 4,596,397 | ||||

At September 30, 2013, the components of accumulated earnings (losses) on a tax basis were as follows:

| Cost of investments | $ | 35,886,533 | ||

| Gross unrealized appreciation | $ | 32,082,677 | ||

| Gross unrealized depreciation | $ | (1,256,244 | ) | |

| Net unrealized appreciation | $ | 30,826,433 | ||

| Undistributed ordinary income | — | |||

| Undistributed long-term capital loss | — | |||

| Total distributable earnings | — | |||

| Other accumulated gains/losses | $ | (8,579,110 | ) | |

| Total accumulated earnings (losses) | $ | 22,247,323 |

As of September 30, 2013, the Fund had capital loss carryforwards of $8,191,899 as follows:

| Capital Loss Carryover | Character | Expiration | ||

| $1,627,363 | — | 09/30/2017 | ||

| $6,564,536 | — | 09/30/2018 |

As of September 30, 2013, the Fund deferred, on a tax basis, late year losses as follows:

| Net Investment Income | Short-Term | ||

| $387,211 | $— |

The Fund paid no distributions during the six months ended March 31, 2014 and the year ended September 30, 2013.

14

KIRR, MARBACH PARTNERS

VALUE FUND

Notes to the Financial Statements (Continued)

March 31, 2014 (Unaudited)

3. AGREEMENTS

The Fund has entered into an Investment Advisory Agreement with Kirr, Marbach & Company, LLC (the “Investment Adviser”). Pursuant to its advisory agreement with the Fund, the Investment Adviser is entitled to receive a fee, calculated daily and payable monthly, at the annual rate of 1.00% as applied to the Fund’s daily net assets.

The Investment Adviser has contractually agreed to waive its management fee and/or reimburse the Fund’s other expenses to the extent necessary to ensure that the Fund’s total annual operating expenses (excluding acquired fund fees and expenses, interest, taxes, brokerage commissions and extraordinary expenses) do not exceed 1.45% of its average daily net assets until February 28, 2015. Accordingly, for the six months ended March 31, 2014, the Investment Adviser waived advisory fees in the amount of $1,936. The Investment Adviser may decide to continue the agreement, or revise the total annual operating expense limitations after February 28, 2015. Any waiver or reimbursement is subject to later adjustment to allow the Investment Adviser to recoup amounts waived or reimbursed to the extent actual fees and expenses for a period are less than the expense limitation cap of 1.45%, provided, however, that the Investment Adviser shall only be entitled to recoup such amounts for a period of three years from the date such amount was waived or reimbursed. Waived/reimbursed fees and expenses subject to potential recovery by year of expiration are as follows:

| Year of expiration | Amount | ||

| 9/30/2014 | $133,379 | ||

| 9/30/2015 | $102,054 | ||

| 9/30/2016 | $ 53,758 | ||

| 9/30/2017 | $ 1,936 |

As of March 31, 2014, it was possible, but not probable, those amounts would be recovered by the Investment Adviser. At the end of each fiscal year in the future, the Fund will continue to assess the potential recovery of waived/reimbursed fees and expenses for financial reporting purposes.

Quasar Distributors, LLC, (the “Distributor”) serves as principal underwriter of the shares of the Fund pursuant to a Distribution Agreement between the Distributor and the Corporation. The Fund’s shares are sold on a no-load basis and, therefore, the Distributor receives no sales commission or sales load for providing services to the Fund. The Corporation has adopted a plan pursuant to Rule 12b-1 under the 1940 Act (the “12b-1 Plan”), which authorizes the Corporation to pay the Distributor and certain financial intermediaries who assist in distributing the Fund shares or who provided shareholder services to Fund shareholders a distribution and shareholder servicing fee of up to 0.25% of the Fund’s average daily net assets (computed on an annual basis). All or a portion of the fee may be used by the Fund or the Distributor to pay its distribution fee and costs of printing reports and prospectuses for potential investors and the costs of other distribution and shareholder servicing expenses. During the six months ended March 31, 2014, the Fund incurred expenses of $31,763 pursuant to the 12b-1 Plan.

U.S. Bancorp Fund Services, LLC serves as transfer agent, administrator and accounting services agent for the Fund. U.S. Bank, N.A. serves as custodian for the Fund.

The Fund imposes a 1% redemption fee on shares held 30 days or less. For the six months ended March 31, 2014 and the year ended September 30, 2013, the Fund collected $291 and $1,459 respectively, in redemption fees.

15

KIRR, MARBACH PARTNERS

VALUE FUND

Additional Information (Continued)

March 31, 2014 (Unaudited)

BOARD APPROVAL OF INVESTMENT ADVISORY AGREEMENT

On, November 20, 2013, at an in-person meeting of the Board of Directors of the Kirr, Marbach Partners Fund, Inc. (the “Corporation”), the Directors, including a majority of the disinterested Directors, approved the continuation of the investment advisory agreement dated June 10, 2005 (the “Advisory Agreement”) between the Corporation and Kirr, Marbach & Company, LLC (the “Adviser”). It was noted that, as described in the Adviser’s memorandum, the Adviser has significant experience providing investment advice and is qualified to provide investment advisory services to the Fund. In addition, it was noted that the Adviser promoted a culture of compliance. It was noted that the Fund has exhibited very strong performance overall and has materially outperformed its benchmarks since inception (i.e., the S&P 500 and the Russell 3000) as of September 30, 2013. The directors also noted that a significant percentage of the Fund is owned by Adviser insiders and therefore the directors feel that the Adviser’s interests are aligned with other Fund shareholders. The directors considered information relating to the Fund’s fees, costs and expense ratios and compared such fees, costs and expense ratios to competitive industry fee structures and expense ratios. Specifically, the directors reviewed charts prepared by the administrator based on data compiled by a nationally recognized third party comparative data provider. In connection with this, the directors also considered the control of the Fund’s operating expenses through the expense cap agreement, and noted that the current expense cap agreement maintains an overall reasonable total expense level as evidenced by the comparative data presented at the meeting and that while assets were increasing the Adviser was still absorbing expenses. In addition, the Board noted that the Adviser is providing substantially similar investment advisory services to the Fund and its other separate account clients and, with the current expense cap arrangement in place, providing such services to the Fund at substantially similar rates to those charged to the Adviser’s other clients. The directors considered whether the Adviser would receive any fall-out benefits through its relationship with the Fund, and it was noted that because none of the other service providers to the Fund are affiliated with the Adviser, there are no identifiable material fall-out benefits accruing to the Adviser. The directors considered the Adviser’s cost of providing services to the Fund and the profitability of its relationship to the Fund. It was noted that the Adviser’s profitability was in line with its profitability for providing investment advice to its separate account clients given the current expense cap agreement, and the directors noted that the Adviser’s profit in connection with its services to the Fund appeared reasonable. The directors considered whether economies of scale were being realized that could justify reduced expenses for the Fund. It was noted that current asset levels had increased from prior years, but the Adviser was still absorbing expenses. During the deliberations, the disinterested directors did not identify any single consideration or particular piece of information that was all important or controlling in determining whether to approve the Advisory Agreement. The disinterested directors evaluated all information presented to them and determined that the compensation paid to the Adviser under the Advisory Agreement was fair and reasonable in light of the services to be performed.

16

KIRR, MARBACH PARTNERS

VALUE FUND

Additional Information

March 31, 2014 (Unaudited)

AVAILABILITY OF FUND PORTFOLIO INFORMATION

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q, which is available on the SEC’s website at www.sec.gov. The Fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington D.C. For information on the Public Reference Room call 1-800-SEC-0330. In addition, the Fund will post its complete schedule of portfolio holdings as of the end of its last completed fiscal quarter as part of its quarterly shareholder update on the Fund’s website on or soon after the 14th day after the end of each fiscal quarter.

AVAILABILITY OF PROXY VOTING INFORMATION

Both a description of the Fund’s Proxy Voting Policies and Procedures and information about the Fund’s proxy voting record will be available (1) without charge, upon request, by calling 1-800-870-8039, and (2) on the SEC’s website at www.sec.gov.

17

(This Page Intentionally Left Blank.)

Directors

Mark D. Foster, CFA

Mickey Kim, CFA

Jeffrey N. Brown

Mark E. Chesnut

John F. Dorenbusch

Principal Officers

Mark D. Foster, CFA, President

Mickey Kim, CFA, Vice President, Treasurer and Secretary

Investment Adviser

Kirr, Marbach & Company, LLC

621 Washington Street

Columbus, IN 47201

Distributor

Quasar Distributors, LLC

615 East Michigan Street

Milwaukee, WI 53202

Custodian

U.S. Bank, N.A.

1555 North River Center Drive

Milwaukee, WI 53212

Administrator,

Transfer Agent and

Dividend – Disbursing Agent

U.S. Bancorp Fund Services, LLC

615 E. Michigan Street

Milwaukee, WI 53202

Independent Registered

Public Accounting Firm

Tait, Weller & Baker LLP

1818 Market Street, Suite 2400

Philadelphia, PA 19103

Legal Counsel

Kirkland & Ellis LLP

300 North LaSalle

Chicago, IL 60654

This report should be accompanied or preceded by a prospectus.

The Fund’s Statement of Additional Information contains additional information about the

Fund’s directors and is available without charge upon request by calling 1-800-808-9444.

The Fund’s Proxy Voting Policies and Procedures are available without charge upon request by calling 1-800-808-9444. A description of the

Fund’s proxy voting policies and procedures is available on the Fund’s website, www.kmpartnersfunds.com, or on the SEC’s website, at

www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the twelve months ended June 30,

is available without charge upon request by calling 1-800-808-9444 or on the SEC’s website, at www.sec.gov.

Semi-Annual Report

March 31, 2014

Item 2. Code of Ethics.

Not applicable for semi-annual reports.

Item 3. Audit Committee Financial Expert.

Not applicable for semi-annual reports.

Item 4. Principal Accountant Fees and Services.

Note applicable for semi-annual reports.

Item 5. Audit Committee of Listed Registrants.

Not applicable for semi-annual reports.

Item 6. Schedule of Investments.

Schedule of Investments is included as part of the report to shareholders filed under Item 1 of this Form.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable to open-end investment companies.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable to open-end investment companies.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchases.

Not applicable to open-end investment companies.

Item 10. Submission of Matters to a Vote of Security Holders.

Not Applicable.

Item 11. Controls and Procedures.

| (a) | The Registrant’s President and Treasurer have reviewed the Registrant's disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940 (the “Act”)) as of a date within 90 days of the filing of this report, as required by Rule 30a-3(b) under the Act and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934. Based on their review, such officers have concluded that the disclosure controls and procedures are effective in ensuring that information required to be disclosed in this report is appropriately recorded, processed, summarized and reported and made known to them by others within the Registrant and by the Registrant’s service provider. |

| (b) | There were no significant changes in the Registrant's internal control over financial reporting (as defined in Rule 30a-3(d) under the Act) that occurred during the second fiscal quarter of the period covered by this report that has materially affected, or is reasonably likely to materially affect, the Registrant's internal control over financial reporting. |

Item 12. Exhibits.

| (a) | (1) Any code of ethics or amendment thereto, that is subject of the disclosure required by Item 2, to the extent that the registrant intends to satisfy Item 2 requirements through filing an exhibit. Not applicable for semi-annual reports. |

(2) Certifications pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. Filed herewith.

(3) Any written solicitation to purchase securities under Rule 23c-1 under the Act sent or given during the period covered by the report by or on behalf of the registrant to 10 or more persons. Not applicable to open-end investment companies.

| (b) | Certification pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. Furnished herewith. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

(Registrant) Kirr, Marbach Partners Funds, Inc.

By (Signature and Title)* /s/ Mr. Mark Foster

Mr. Mark Foster, President

Date June 5, 2014

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

By (Signature and Title)* /s/ Mr. Mark Foster

Mr. Mark Foster, President

Date June 5, 2014

By (Signature and Title)* /s/ Mr. Mickey Kim

Mr. Mickey Kim, Treasurer

Date June 5, 2014

* Print the name and title of each signing officer under his or her signature.