UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-09223

Pioneer Series Trust XIV

(Exact name of registrant as specified in charter)

60 State Street, Boston, MA 02109

(Address of principal executive offices) (ZIP code)

Christopher J. Kelley, Amundi Asset Management, Inc.,

60 State Street, Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 742-7825

Date of fiscal year end: September 30, 2023

Date of reporting period: October 1, 2022 through September 30, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Pioneer Strategic Income Fund

Annual Report | September 30, 2023

| | | | | |

| A: PSRAX | C: PSRCX | K: STRKX | R: STIRX | Y: STRYX |

visit us: www.amundi.com/us

Pioneer Strategic Income Fund | Annual Report | 9/30/231

President’s Letter

Dear Shareholders,

On February 13, 2023, Amundi US celebrated the 95th anniversary of Pioneer Fund, the second-oldest mutual fund in the United States. We recognized the anniversary with ringing of the closing bell at the New York Stock Exchange, which seemed fitting for this special milestone.

Pioneer Fund was launched on February 13, 1928 by Phil Carret, one of the earliest proponents of value investing and a leading innovator in the asset management industry. Mr. Carret began investing in the 1920s and founded Pioneer Investments (now Amundi US) in 1928, and was one of the first investors to realize he could uncover value through rigorous, innovative, fundamental research techniques.

Consistent with Mr. Carret’s investment approach and employing many of the same techniques utilized in the 1920s, Amundi US's portfolio managers have adapted Mr. Carret’s philosophy to a new age of “active” investing.

The last few years have seen investors face some unprecedented challenges, from a global pandemic that shuttered much of the world’s economy for months, to geopolitical strife, to rising inflation that has reached levels not seen in decades. Now, more than ever, Amundi US believes active management – that is, making active investment decisions across all of our portfolios – can help mitigate risk during periods of market volatility.

At Amundi US, active management begins with our own fundamental, bottom-up research process. Our team of dedicated research analysts and portfolio managers analyzes each security under consideration, communicating frequently with the management teams of the companies and other entities issuing the securities, and working together to identify those securities that we believe best meet our investment criteria for our family of funds. Our risk management approach begins with each security under consideration, as we strive to develop a deep understanding of the potential opportunity, while considering any potential risk factors.

Today, as shareholders, we have many options. It is our view that active management can serve shareholders well, not only when markets are thriving, but also during periods of market stress. As you consider your long-term investment goals, we encourage you to work with your financial professional to develop an investment plan that paves the way for you to pursue both your short-term and long-term goals.

2Pioneer Strategic Income Fund | Annual Report | 9/30/23

We greatly appreciate the trust you have placed in us and look forward to continuing to serve you in the future.

Lisa M. Jones

Head of the Americas, President and CEO of US

Amundi Asset Management US, Inc.

November 2023

Any information in this shareowner report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

Pioneer Strategic Income Fund | Annual Report | 9/30/233

Portfolio Management Discussion | 9/30/23

In the following interview, Andrew Feltus and Jonathan Scott discuss the factors that affected the performance of Pioneer Strategic Income Fund during the 12-month period ended September 30, 2023. Mr. Feltus, CFA, Managing Director, Co-Director of High Yield, and a portfolio manager at Amundi Asset Management US, Inc. (Amundi US), and Mr. Scott, a senior vice president, Deputy Director of Multi-Sector Fixed Income, and a portfolio manager at Amundi US, are responsible for the day-to-day management of the Fund, along with Brad Komenda, Managing Director, Director of Investment Grade Corporates, and a portfolio manager at Amundi US, and Kenneth J. Taubes, Executive Vice President, Chief Investment Officer, US, and a portfolio manager at Amundi US.

| Q | How did the Fund perform during the 12-month period ended September 30, 2023? |

| A | Pioneer Strategic Income Fund’s Class A shares returned 1.91% at net asset value during the 12-month period ended September 30, 2023, while the Fund’s benchmark, the Bloomberg US Universal Index (the Bloomberg Index), returned 1.61%. During the same period, the average return of the 355 mutual funds in Morningstar’s Multisector Bond Funds category was 4.95%. |

| Q | How would you describe the market environment for fixed-income investments during the 12-month period ended September 30, 2023? |

| A | The period opened in the wake of a series of aggressive Federal Reserve (Fed) interest-rate increases as the US central bank sought to counter rising levels of inflation, which had peaked at over 9% in June of 2022. The Fed’s determined stance had brought the target for its benchmark federal funds rate from 0.00% – 0.25% in March of 2022, to 3.00% – 3.25% entering October 2022. In addition, the US Treasury yield curve, which had moved notably higher in response to the Fed’s actions, became inverted as the market anticipated a recession. (A yield curve is a line that plots the interest rates, at a set point in time, of bonds having equal credit quality but differing maturity dates. An inverted yield curve means that longer-term rates are lower than shorter-term rates.) |

| | With inflation showing signs of modest easing at the start of the period at the end of September 2022, investors began to |

4Pioneer Strategic Income Fund | Annual Report | 9/30/23

| | anticipate a pivot by the Fed to a more dovish policy stance on monetary policy after several months of interest-rate increases. That optimism led to strong returns for bonds in both October and November 2022, despite the Fed’s increase to the federal funds rate target range of another 75 basis points (bps) in November. (A basis point is equal to 1/100th of a percentage point.) In December, however, after a solid start to the fourth quarter, the market soon turned its attention to the potential recessionary effects of the higher interest-rate regime put in place by the Fed, which led riskier assets, including corporate bonds, to give back some of their gains from earlier in the quarter as the month progressed. In addition, the Fed implemented a more modest 50 bps increase to the federal funds rate target range at its December meeting, leaving the target range at 4.25% – 4.50% at the end of 2022, its highest level since the fall of 2007. |

| | Entering 2023, riskier assets rallied again, amid renewed investor optimism that the Fed and other leading central banks were poised to stop raising interest rates. January 2023 saw Treasury yields pull back from their more recent highs on the outlook for a potential easing of monetary policy. That, in turn, boosted performance for bonds in general. In addition, the reopening of China’s economy as the Chinese government unwound its “Zero-COVID” policy eased concerns about slowing global economic growth. Against that backdrop, areas of the market that had lagged during the 2022 sell-off (such as growth stocks and corporate bonds) outperformed. On February 1, the Fed increased the federal funds rate target again, but this time by a comparatively moderate 25 bps, bringing the target range to 4.50% – 4.75%. |

| | In March, however, the failure of some regional US banks and the collapse of European lender Credit Suisse raised fears of a financial crisis. In response, the Fed implemented a new lending program to support bank liquidity, while market participants began to anticipate decreases in the federal funds rate target range by the Fed before the end of the calendar year. At its March 23 meeting, the Fed went forward with another modest 25 bps increase to the federal funds target, bringing the range to 4.75% ‒ 5.00%. The financial markets viewed that increase as an |

Pioneer Strategic Income Fund | Annual Report | 9/30/235

| | indication that the Fed believed the financial system, overall, remained on solid footing. |

| | With the unemployment rate hovering around record lows, in April the markets welcomed news of 2% first quarter gross domestic product (GDP) growth, driven by continued consumer strength. While high inflation and the strong labor market resulted in the Fed's signaling a higher terminal (ending) federal funds rate of 5.6%, markets were encouraged that the central bank was possibly nearing the end of its rate-hiking cycle. Corporate profits posted declines for both the first and second quarters of 2023, but investors embraced the very high percentage of earnings reports that came in above expectations. |

| | The Fed increased the federal funds target range by 25 bps in early May, bringing the range to 5.00% ‒ 5.25%, before taking a pause at its June meeting. On July 26, 2023, the Fed once again raised the federal funds target range by 25 bps, then the Fed took another pause at its September meeting, leaving the range at 5.25% ‒ 5.50% as of period-end. |

| | Most asset classes sold off in the third quarter of 2023, most notably in September, as US bond yields rose dramatically, driven by the Fed’s “higher for longer” monetary policy, coupled with the negative impact of higher Treasury issuance and increasing concerns about the US government’s budget deficit. In addition, weaker economic growth in China and Europe weighed on market sentiment. The yield on the 10-year Treasury ended September of 2023 at 4.58%, versus 3.83% 12 months earlier. |

| | Given the rise in Treasury yields and softening in investor sentiment towards credit-sensitive securities seen late in the 12-month period, performance for the broad fixed-income markets was muted for the 12 months ended September 30, 2023, as reflected in the Bloomberg Index’s modest return of 1.61%. Interest-rate-sensitive Treasuries were the biggest laggards within the Fund’s benchmark, while high-yield corporate bonds led performance. |

6Pioneer Strategic Income Fund | Annual Report | 9/30/23

| Q | What factors affected the Fund’s performance relative to the benchmark Bloomberg Index during the 12-month period ended September 30, 2023? |

| A | As a multisector fixed-income strategy, the Fund seeks to deliver competitive returns while delivering volatility similar to its benchmark by investing across a diversified range of investment-grade and non-investment-grade global fixed-income asset classes. The investment strategy seeks to add value through both sector allocation and security selection, focusing on “spread” sectors that trade at a yield advantage relative to US Treasuries. These include sectors such as corporate bonds, agency mortgage-backed securities (MBS), securitized credit assets, and emerging markets debt that typically have offered higher risk-adjusted returns than Treasuries as well as greater security selection opportunities. Taking a dynamic approach to sector allocation, we may consider increasing the Fund’s risk profile when we feel markets are offering significant compensation for risk, and reduce risk when markets are offering less attractive value. |

| | The Fund’s overall security selection results contributed positively to benchmark-relative returns for the 12-month period, while positioning with respect to interest rates detracted from relative performance. |

| | Within the Fund’s allocation to investment-grade corporates, exposure to issuers within both the industrials and financials sectors benefited relative performance. Within industrials, a position in an airline manufacturer highlighted positive contributions, along with exposure to energy-related credits as oil prices rose over the course of the period. Holdings of a gold producer also performed well. The Fund’s positioning within financials benefited from a rally in European banks during the first quarter of 2023, as well as from holdings of an aircraft leasing firm. More broadly, a portfolio bias toward higher-quality securities within the Fund’s corporate exposures helped benchmark-relative performance. |

| | Sector allocation results also contributed modestly to the Fund’s relative performance for the 12-month period. Specifically, a significant underweight to Treasuries and an overweight to non-agency MBS aided the Fund’s benchmark-relative results. In |

Pioneer Strategic Income Fund | Annual Report | 9/30/237

| | addition, an approximately 4% portfolio exposure to insurance-linked securities (ILS) benefited the Fund’s relative returns, as did the portfolio’s non-US dollar (USD) exposures, most notably the portfolio’s allocations to the Polish zloty and the Korean won. |

| | During a period in which the Fund outperformed its benchmark, the one key detractor from relative performance was the portfolio's positioning with respect to interest rates. Specifically, the Fund had an above-benchmark stance with respect to duration and corresponding interest-rate sensitivity. That positioning detracted from relative performance as Treasury yields rose. (Duration is a measure of the sensitivity of the price, or the value of principal, of a fixed-income investment to a change in interest rates, expressed as a number of years.) |

| Q | Did the Fund have any investments in derivative securities during the 12-month period ended September 30, 2023? |

| A | Yes, the Fund did have investments in three types of derivatives: Treasury futures, index-based credit-default-swap contracts (CDX), and forward foreign currency contracts (“currency forwards”). We used Treasury futures to help manage portfolio duration. The use of futures had a negative impact on the Fund’s relative results. We used the CDX positions in an effort to manage the Fund’s exposure to credit-sensitive sectors; the CDX used for hedging purposes (short exposure) detracted from the Fund’s relative returns, while longer-exposure CDX helped the Fund’s relative performance. The Fund’s exposure to currency forwards was a technique used as part of our efforts to manage the risks associated with investing the portfolio in non-USD currencies. The tactic had a mixed impact on the Fund's benchmark-relative results, as long exposures helped performance while shorter exposures (hedges) detracted. |

| Q | Did the Fund’s distributions* (or yield) to shareholders change during the 12-month period ended September 30, 2023? |

| A | The Fund’s monthly distribution rate experienced a slight uptick over the 12-month period as interest rates continued to move higher. |

| * | Distributions are not guaranteed. |

8Pioneer Strategic Income Fund | Annual Report | 9/30/23

| Q | What is your investment outlook? |

| A | While recent economic data may show signs consistent with a domestic “soft landing,” in which growth slows but remains positive while inflation is brought under control, we are wary of extrapolating the current growth signals too far into the future. Consumer spending has been waning after a summer boost, business sentiment has been softening, and the still-tight US labor market has been cooling. In addition, higher interest rates and tighter lending conditions are just starting to take their toll on businesses. In a “higher for longer” interest-rate environment, businesses may encounter increasing difficulty with regard to carrying higher interest expenses and eventually rolling over maturing loans. We expect economic growth will slow in the coming quarters, and while it may take into early 2024 to know if the economy has a soft or hard landing, we continue to view the odds of a soft landing as relatively low. |

| | The recent rise in yields has been rapid and significant. Since the Fed’s last rate increase on July 26, 10-year Treasury yields have moved from 3.86% to 4.58%. The rise in long-term Treasury rates is likely not due to higher expected inflation, in our view. Rather, it appears the bond market is currently discounting a “higher for forever” scenario, in which the Fed’s “neutral” rate has increased substantially. |

| | We view longer-term interest rates as fundamentally attractive and well above fair value, but recognize that rates could move higher in the short term as investors reposition in response to recent volatility. In terms of sector exposures, agency MBS appear increasingly attractive to us, following recent spread widening (Credit spreads are commonly defined as the differences in yield between Treasuries and other types of fixed-income securities with similar maturities.) We remain relatively cautious with regard to the portfolio’s exposures to both corporate credit and securitized credit, with a higher-quality bias, given narrower-than-average spreads and elevated prospects for a slowing economy on the horizon. |

Pioneer Strategic Income Fund | Annual Report | 9/30/239

Please refer to the Schedule of Investments on pages 21 - 95 for a full listing of Fund securities.

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict including Russia's military invasion of Ukraine, sanctions against Russia, other nations or individuals or companies and possible countermeasures, market disruptions caused by tariffs, trade disputes or other government actions, or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

Until recently, a commonly used reference rate for floating rate securities was LIBOR (London Interbank Offered Rate). Publication of most LIBOR settings has ceased on a representative basis. The impact of the transition from LIBOR on the Fund's transactions and financial markets generally cannot yet be determined.

Investments in high-yield or lower rated securities are subject to greater-than average price volatility, illiquidity and possibility of default.

The market price of securities may fluctuate when interest rates change.When interest rates rise, the prices of fixed-income securities in the Fund will generally fall. Conversely, when interest rates fall, the prices of fixed-income securities in the Fund will generally rise.

Investments in the Fund are subject to possible loss due to the financial failure of issuers of underlying securities and their inability to meet their debt obligations.

Prepayment risk is the chance that an issuer may exercise its right to prepay its security, if falling interest rates prompt the issuer to do so. Forced to reinvest the unanticipated proceeds at lower interest rates, the Fund would experience a decline in income and lose the opportunity for additional price appreciation.

The securities issued by U.S. Government-sponsored entities (e.g., FNMA, Freddie Mac) are neither guaranteed nor issued by the U.S. Government.

The portfolio may invest in mortgage-backed securities, which during times of fluctuating interest rates may increase or decrease more than other fixed income securities. Mortgage-backed securities are also subject to prepayments.

10Pioneer Strategic Income Fund | Annual Report | 9/30/23

Investing in foreign and/or emerging markets securities involves risks relating to interest rates, currency exchange rates, economic, and political conditions.

For more information on this or any Pioneer fund, please visit amundi.com/usinvestors or call 1-800-622-9876. This material must be preceded or accompanied by the Fund's current prospectus or summary prospectus.

Any information in this shareholder report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

Pioneer Strategic Income Fund | Annual Report | 9/30/2311

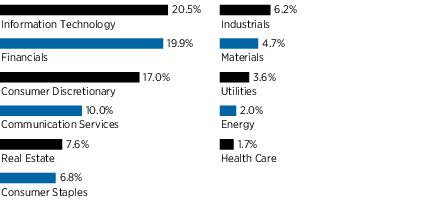

Portfolio Summary | 9/30/23

Portfolio Diversification

(As a percentage of total investments)*

+ Amount rounds to less than 0.1%.

10 Largest Holdings

| (As a percentage of total investments)* |

| 1. | U.S. Treasury Notes, 4.50%, 9/30/30 | 5.80% |

| 2. | U.S. Treasury Bonds, 4.375%, 8/15/43 | 2.22 |

| 3. | U.S. Treasury Bills, 10/24/23 | 2.12 |

| 4. | U.S. Treasury Notes, 3.50%, 2/15/33 | 1.93 |

| 5. | U.S. Treasury Bonds, 2.25%, 2/15/52 | 1.20 |

| 6. | Wells Fargo & Co., 7.50% | 1.06 |

| 7. | Federal National Mortgage Association, 6.00%, 10/1/53 | 0.81 |

| 8. | U.S. Treasury Inflation Indexed Bonds, 1.50%, 2/15/53 | 0.77 |

| 9. | Federal National Mortgage Association, 1.50%, 11/1/41 | 0.74 |

| 10. | Federal National Mortgage Association, 2.50%, 10/1/53 (TBA) | 0.70 |

| | |

| * | Excludes short-term investments, TBA Sale Commitments and all derivative contracts except for options purchased. The Fund is actively managed, and current holdings may be different. The holdings listed should not be considered recommendations to buy or sell any securities. |

12Pioneer Strategic Income Fund | Annual Report | 9/30/23

Prices and Distributions | 9/30/23

Net Asset Value per Share

| Class | 9/30/23 | 9/30/22 |

| A | $8.91 | $9.05 |

| C | $8.71 | $8.85 |

| K | $8.92 | $9.07 |

| R | $9.07 | $9.21 |

| Y | $8.91 | $9.05 |

| | | |

Distributions per Share: 10/1/22 - 9/30/23

| Class | Net

Investment

Income | Short-Term

Capital Gains | Long-Term

Capital Gains |

| A | $0.3169 | $— | $— |

| C | $0.2515 | $— | $— |

| K | $0.3609 | $— | $— |

| R | $0.2914 | $— | $— |

| Y | $0.3509 | $— | $— |

Index Definitions

The Bloomberg U.S. Universal Index is an unmanaged index that represents the union of the U.S. Aggregate Index, the U.S. High Yield Corporate Index, the 144A Index, the Eurodollar Index, the Emerging Markets Index, the non-ERISA portion of the CMBS Index, and the CMBS High Yield Index. Municipal debt, private placements and non-dollar-denominated issues are excluded. Indices are unmanaged and their returns assume reinvestment of dividends and do not reflect any fees or expenses. It is not possible to invest directly in an index.

The index defined here pertains to the “Value of $10,000 Investment” and “Value of $5 Million Investment” charts on pages 14 - 18.

Pioneer Strategic Income Fund | Annual Report | 9/30/2313

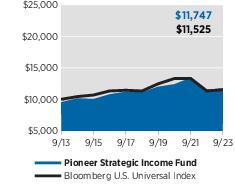

| Performance Update | 9/30/23 | Class A Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class A shares of Pioneer Strategic Income Fund at public offering price during the periods shown, compared to that of the Bloomberg U.S. Universal Index.

Average Annual Total Returns

(As of September 30, 2023) |

| Period | Net

Asset

Value

(NAV) | Public

Offering

Price

(POP) | Bloomberg

U.S.

Universal

Index |

| 10 Years | 2.09% | 1.62% | 1.43% |

| 5 Years | 1.03 | 0.11 | 0.34 |

| 1 Year | 1.91 | -2.71 | 1.61 |

Expense Ratio

(Per prospectus dated February 1, 2023) |

| Gross |

| 1.03% |

Value of $10,000 Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

NAV results represent the percent change in net asset value per share. NAV returns would have been lower had sales charges been reflected. POP returns reflect deduction of maximum 4.50% sales charge. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

14Pioneer Strategic Income Fund | Annual Report | 9/30/23

| Performance Update | 9/30/23 | Class C Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class C shares of Pioneer Strategic Income Fund during the periods shown, compared to that of the Bloomberg U.S. Universal Index.

Average Annual Total Returns

(As of September 30, 2023) |

| Period | If

Held | If

Redeemed | Bloomberg

U.S.

Universal

Index |

| 10 Years | 1.41% | 1.41% | 1.43% |

| 5 Years | 0.36 | 0.36 | 0.34 |

| 1 Year | 1.21 | 0.23 | 1.61 |

Expense Ratio

(Per prospectus dated February 1, 2023) |

| Gross |

| 1.68% |

Value of $10,000 Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

Class C shares held for less than one year are also subject to a 1% contingent deferred sales charge (CDSC). “If Held” results represent the percent change in net asset value per share. “If Redeemed” returns reflect deduction of the CDSC for the one-year period, assuming a complete redemption of shares at the last price calculated on the last business day of the period, and no CDSC for the five- and 10-year periods. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

Pioneer Strategic Income Fund | Annual Report | 9/30/2315

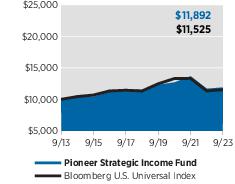

| Performance Update | 9/30/23 | Class K Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $5 million investment made in Class K shares of Pioneer Strategic Income Fund during the periods shown, compared to that of the Bloomberg U.S. Universal Index.

Average Annual Total Returns

(As of September 30, 2023) |

| Period | Net

Asset

Value

(NAV) | Bloomberg

U.S.

Universal

Index |

| 10 Years | 2.52% | 1.43% |

| 5 Years | 1.46 | 0.34 |

| 1 Year | 2.28 | 1.61 |

Expense Ratio

(Per prospectus dated February 1, 2023) |

| Gross | Net |

| 0.61% | 0.59% |

Value of $5 Million Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

Class K shares are not subject to sales charges and are available for limited groups of eligible investors, including institutional investors. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

The net expense ratio reflects the contractual expense limitation currently in effect through February 1, 2025 for Class K shares. There can be no assurance that Amundi US will extend the expense limitation beyond such time. Please see the prospectus and financial statements for more information.

Performance results shown reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for more current expense ratios.

16Pioneer Strategic Income Fund | Annual Report | 9/30/23

| Performance Update | 9/30/23 | Class R Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class R shares of Pioneer Strategic Income Fund during the periods shown, compared to that of the Bloomberg U.S. Universal Index.

Average Annual Total Returns

(As of September 30, 2023) |

| Period | Net

Asset

Value

(NAV) | Bloomberg

U.S.

Universal

Index |

| 10 Years | 1.75% | 1.43% |

| 5 Years | 0.70 | 0.34 |

| 1 Year | 1.60 | 1.61 |

Expense Ratio

(Per prospectus dated February 1, 2023) |

| Gross |

| 1.36% |

Value of $10,000 Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

Class R shares are not subject to sales charges and are available for limited groups of eligible investors, including institutional investors. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

Pioneer Strategic Income Fund | Annual Report | 9/30/2317

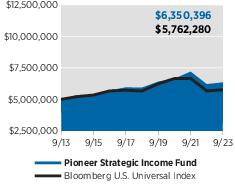

| Performance Update | 9/30/23 | Class Y Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $5 million investment made in Class Y shares of Pioneer Strategic Income Fund during the periods shown, compared to that of the Bloomberg U.S. Universal Index.

Average Annual Total Returns

(As of September 30, 2023) |

| Period | Net

Asset

Value

(NAV) | Bloomberg

U.S.

Universal

Index |

| 10 Years | 2.42% | 1.43% |

| 5 Years | 1.37 | 0.34 |

| 1 Year | 2.28 | 1.61 |

Expense Ratio

(Per prospectus dated February 1, 2023) |

| Gross | Net |

| 0.71% | 0.69% |

Value of $5 Million Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

Class Y shares are not subject to sales charges and are available for limited groups of eligible investors, including institutional investors. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The net expense ratio reflects the contractual expense limitation in effect through February 1, 2025 for Class Y shares. There can be no assurance that Amundi US will extend the expense limitation beyond such time. Please see the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for more current expense ratios.

18Pioneer Strategic Income Fund | Annual Report | 9/30/23

Comparing Ongoing Fund Expenses

As a shareowner in the Fund, you incur two types of costs:

| (1) | ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses; and |

| (2) | transaction costs, including sales charges (loads) on purchase payments. |

This example is intended to help you understand your ongoing expenses (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 at the beginning of the Fund’s latest six-month period and held throughout the six months.

Using the Tables

Actual Expenses

The first table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period as follows:

| (1) | Divide your account value by $1,000

Example: an $8,600 account value ÷ $1,000 = 8.6 |

| (2) | Multiply the result in (1) above by the corresponding share class’s number in the third row under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. |

Expenses Paid on a $1,000 Investment in Pioneer Strategic Income Fund

Based on actual returns from April 1, 2023 through September 30, 2023.

| Share Class | A | C | K | R | Y |

Beginning Account

Value on 4/1/23 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 |

Ending Account Value

(after expenses) on 9/30/23 | $974.40 | $971.30 | $976.70 | $972.60 | $977.30 |

Expenses Paid

During Period* | $5.25 | $8.40 | $2.92 | $6.68 | $3.42 |

| | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.06%, 1.70%, 0.59%, 1.35%, and 0.69% for Class A, Class C, Class K, Class R, and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

Pioneer Strategic Income Fund | Annual Report | 9/30/2319

Comparing Ongoing Fund Expenses (continued)

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) that are charged at the time of the transaction. Therefore, the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Expenses Paid on a $1,000 Investment in Pioneer Strategic Income Fund

Based on a hypothetical 5% return per year before expenses, reflecting the period from April 1, 2023 through September 30, 2023.

| Share Class | A | C | K | R | Y |

Beginning Account

Value on 4/1/23 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 |

Ending Account Value

(after expenses) on 9/30/23 | $1,019.75 | $1,016.55 | $1,022.11 | $1,018.30 | $1,021.61 |

Expenses Paid

During Period* | $5.37 | $8.59 | $2.99 | $6.83 | $3.50 |

| | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.06%, 1.70%, 0.59%, 1.35%, and 0.69% for Class A, Class C, Class K, Class R, and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

20Pioneer Strategic Income Fund | Annual Report | 9/30/23

Schedule of Investments | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | UNAFFILIATED ISSUERS — 103.2% | |

| | Senior Secured Floating Rate

Loan Interests — 0.6% of Net Assets*(a) | |

| | Chemicals-Diversified — 0.1% | |

| 1,891,200 | LSF11 A5 HoldCo LLC, Term Loan, 8.931% (Term SOFR + 350 bps), 10/15/28 | $ 1,846,284 |

| | Total Chemicals-Diversified | $1,846,284 |

|

|

| | Electric-Generation — 0.1% | |

| 2,545,000 | Generation Bridge Northeast LLC, Term Loan B, 9.566% (Term SOFR + 425 bps), 8/22/29 | $ 2,548,181 |

| | Total Electric-Generation | $2,548,181 |

|

|

| | Electronic Composition — 0.0%† | |

| 1,347,994 | Energy Acquisition LP, First Lien Initial Term Loan, 9.772% (Term SOFR + 425 bps), 6/26/25 | $ 1,337,674 |

| | Total Electronic Composition | $1,337,674 |

|

|

| | Finance-Special Purpose Banks — 0.0%† | |

| 1,258,784 | Bank of Industry, Ltd., Facility, 11.67% (Term SOFR + 600 bps), 12/11/23 | $ 1,261,459 |

| | Total Finance-Special Purpose Banks | $1,261,459 |

|

|

| | Medical-Wholesale Drug Distribution —

0.1% | |

| 3,150,225 | Owens & Minor, Inc., Term B-1 Loan, 9.166% (Term SOFR + 375 bps), 3/29/29 | $ 3,150,225 |

| | Total Medical-Wholesale Drug Distribution | $3,150,225 |

|

|

| | Metal Processors & Fabrication — 0.2% | |

| 5,710,434 | Grinding Media, Inc. (Molycop, Ltd.), First Lien Initial Term Loan, 9.53% (Term SOFR + 400 bps), 10/12/28 | $ 5,674,744 |

| 1,012,883 | WireCo WorldGroup, Inc., Initial Term Loan, 9.695% (Term SOFR + 425 bps), 11/13/28 | 1,013,516 |

| | Total Metal Processors & Fabrication | $6,688,260 |

|

|

| | Oil-Field Services — 0.0%† | |

| 299,535 | ProFrac Holdings II LLC, Term Loan, 12.78% (Term SOFR + 725 bps), 3/4/25 | $ 300,658 |

| | Total Oil-Field Services | $300,658 |

|

|

The accompanying notes are an integral part of these financial statements.

Pioneer Strategic Income Fund | Annual Report | 9/30/2321

Schedule of Investments | 9/30/23 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Recreational Centers — 0.1% | |

| 2,711,800 | Fitness International LLC, Term B Loan, 8.769% (Term SOFR + 325 bps), 4/18/25 | $ 2,700,785 |

| | Total Recreational Centers | $2,700,785 |

|

|

| | Total Senior Secured Floating Rate Loan Interests

(Cost $19,728,306) | $19,833,526 |

|

|

| Shares | | | | | | |

| | Common Stocks — 0.1% of Net Assets | |

| | Automobile Components — 0.0%† | |

| 9,565,478(b) | Ascent CNR Corp., Class A | $ 956,548 |

| | Total Automobile Components | $956,548 |

|

|

| | Household Durables — 0.0%† | |

| 1,018,282(b) | Desarrolladora Homex SAB de CV | $ 701 |

| | Total Household Durables | $701 |

|

|

| | Oil, Gas & Consumable Fuels — 0.0%† | |

| 336(b) | Frontera Energy Corp. | $ 2,673 |

| | Total Oil, Gas & Consumable Fuels | $2,673 |

|

|

| | Paper & Forest Products — 0.0%† | |

| 162,828 | Emerald Plantation Holdings, Ltd. | $ — |

| | Total Paper & Forest Products | $— |

|

|

| | Passenger Airlines — 0.1% | |

| 128,171(b) + | Grupo Aeromexico SAB de CV | $ 1,654,768 |

| | Total Passenger Airlines | $1,654,768 |

|

|

| | Total Common Stocks

(Cost $2,712,800) | $2,614,690 |

|

|

Principal

Amount

USD ($) | | | | | | |

| | Asset Backed Securities — 8.6% of

Net Assets | |

| 500,000 | 321 Henderson Receivables III LLC, Series 2008-1A, Class C, 9.36%, 1/15/48 (144A) | $ 487,720 |

| 500,000 | 321 Henderson Receivables III LLC, Series 2008-1A, Class D, 10.81%, 1/15/50 (144A) | 494,477 |

The accompanying notes are an integral part of these financial statements.

22Pioneer Strategic Income Fund | Annual Report | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | Asset Backed Securities — (continued) | |

| 4,000,000(a) | 522 Funding CLO, Ltd., Series 2019-4A, Class E, 12.588% (3 Month Term SOFR + 726 bps), 4/20/30 (144A) | $ 3,608,132 |

| 4,750,000(a) | 522 Funding CLO, Ltd., Series 2019-5A, Class ER, 12.068% (3 Month Term SOFR + 676 bps), 4/15/35 (144A) | 4,239,907 |

| 3,500,000 | A10 Bridge Asset Financing LLC, Series 2019-B, Class D, 4.523%, 8/15/40 (144A) | 3,292,674 |

| 532,440 | Accelerated Assets LLC, Series 2018-1, Class B, 4.51%, 12/2/33 (144A) | 514,049 |

| 752,677 | Accelerated Assets LLC, Series 2018-1, Class C, 6.65%, 12/2/33 (144A) | 731,158 |

| 1,000,000 | Amur Equipment Finance Receivables X LLC, Series 2022-1A, Class E, 5.02%, 12/20/28 (144A) | 889,437 |

| 1,413,000 | Amur Equipment Finance Receivables XI LLC, Series 2022-2A, Class E, 9.32%, 10/22/29 (144A) | 1,350,830 |

| 5,250,000 | Amur Equipment Finance Receivables XII LLC, Series 2023-1A, Class D, 7.48%, 7/22/30 (144A) | 5,165,877 |

| 3,975,000(a) | Arbor Realty Commercial Real Estate Notes, Ltd., Series 2021-FL3, Class D, 7.647% (1 Month Term SOFR + 231 bps), 8/15/34 (144A) | 3,713,624 |

| 5,400,000(a) | Arbor Realty Commercial Real Estate Notes, Ltd., Series 2021-FL4, Class E, 8.847% (1 Month Term SOFR + 351 bps), 11/15/36 (144A) | 4,947,761 |

| 2,000,000 | Arivo Acceptance Auto Loan Receivables Trust, Series 2022-1A, Class D, 7.38%, 9/17/29 (144A) | 1,835,869 |

| 1,054,000(c) | B2R Mortgage Trust, Series 2015-1, Class D, 4.831%, 5/15/48 (144A) | 1,028,692 |

| 3,295,000(a) | Battalion CLO IX, Ltd., Series 2015-9A, Class ER, 11.82% (3 Month Term SOFR + 651 bps), 7/15/31 (144A) | 2,686,357 |

| 1,600,000(a) | Benefit Street Partners CLO XIX, Ltd., Series 2019-19A, Class D, 9.37% (3 Month Term SOFR + 406 bps), 1/15/33 (144A) | 1,582,141 |

| 3,755,393 | Blackbird Capital Aircraft, Series 2021-1A, Class B, 3.446%, 7/15/46 (144A) | 3,135,753 |

| 3,000,000(a) | Carlyle US CLO, Ltd., Series 2019-4A, Class CR, 8.508% (3 Month Term SOFR + 320 bps), 4/15/35 (144A) | 2,839,596 |

The accompanying notes are an integral part of these financial statements.

Pioneer Strategic Income Fund | Annual Report | 9/30/2323

Schedule of Investments | 9/30/23 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Asset Backed Securities — (continued) | |

| 2,150,000 | Cascade MH Asset Trust, Series 2021-MH1, Class B1, 4.573%, 2/25/46 (144A) | $ 1,618,814 |

| 4,000,000(c) | Cascade MH Asset Trust, Series 2021-MH1, Class B3, 7.711%, 2/25/46 (144A) | 2,941,452 |

| 4,250,000(a) | Catskill Park CLO, Ltd., Series 2017-1A, Class D, 11.588% (3 Month Term SOFR + 626 bps), 4/20/29 (144A) | 3,877,564 |

| 1,250,000(c) | CFMT LLC, Series 2021-HB5, Class M4, 5.683%, 2/25/31 (144A) | 1,153,278 |

| 12,000,000(c) | CFMT LLC, Series 2021-HB7, Class M4, 5.072%, 10/27/31 (144A) | 10,804,297 |

| 7,465,000 | Cologix Canadian Issuer LP, Series 2022-1CAN, Class A2, 4.94%, 1/25/52 (144A) | 4,939,129 |

| 2,500,000 | Commercial Equipment Finance LLC, Series 2021-A, Class D, 6.49%, 12/17/29 (144A) | 2,347,813 |

| 70,511 | Commonbond Student Loan Trust, Series 2017-BGS, Class C, 4.44%, 9/25/42 (144A) | 56,920 |

| 4,155,000 | Continental Credit Card ABS LLC, Series 2019-1A, Class C, 6.16%, 8/15/26 (144A) | 4,004,615 |

| 6,550,000 | Continental Finance Credit Card ABS Master Trust, Series 2022-A, Class C, 9.33%, 10/15/30 (144A) | 6,176,348 |

| 3,000,000 | Continental Finance Credit Card ABS Master Trust, Series 2022-A, Class D, 12.42%, 10/15/30 (144A) | 2,784,984 |

| 1,000,000 | Crossroads Asset Trust, Series 2021-A, Class E, 5.48%, 1/20/28 (144A) | 970,269 |

| 2,300,000 | DataBank Issuer, Series 2021-1A, Class C, 4.43%, 2/27/51 (144A) | 1,821,836 |

| 854,906 | Diamond Resorts Owner Trust, Series 2019-1A, Class C, 4.02%, 2/20/32 (144A) | 854,443 |

| 6,000,000 | ExteNet LLC, Series 2019-1A, Class C, 5.219%, 7/25/49 (144A) | 5,690,677 |

| 9,460,000(c) | Finance of America HECM Buyout, Series 2022-HB1, Class M6, 9.317%, 2/25/32 (144A) | 7,362,677 |

| 7,657,186(d) | Finance of America Structured Securities Trust, Series 2021-S2, Class A2, 1.75%, 9/25/71 (144A) | 7,235,349 |

| 14,078,742(d) | Finance of America Structured Securities Trust, Series 2021-S3, Class A2, 2.25%, 12/28/26 (144A) | 12,513,976 |

The accompanying notes are an integral part of these financial statements.

24Pioneer Strategic Income Fund | Annual Report | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | Asset Backed Securities — (continued) | |

| 1,000,000(a) | First Eagle BSL CLO, Ltd., Series 2019-1A, Class C, 9.938% (3 Month Term SOFR + 461 bps), 1/20/33 (144A) | $ 948,673 |

| 3,000,000(a) | First Eagle BSL CLO, Ltd., Series 2019-1A, Class D, 13.288% (3 Month Term SOFR + 796 bps), 1/20/33 (144A) | 2,617,443 |

| 5,500,000 | Four Seas LP, Series 2017-1A, Class A2, 5.927%, 8/28/27 (144A) | 5,024,868 |

| 7,543(c) | Gold Key Resorts LLC, Series 2014-A, Class C, 5.87%, 3/17/31 (144A) | 7,496 |

| 5,022,000(a) | Goldentree Loan Management US CLO 2, Ltd., Series 2017-2A, Class E, 10.288% (3 Month Term SOFR + 496 bps), 11/28/30 (144A) | 4,706,653 |

| 4,250,000(a) | Goldentree Loan Management US CLO 6, Ltd., Series 2019-6A, Class DR, 8.426% (3 Month Term SOFR + 310 bps), 4/20/35 (144A) | 4,029,705 |

| 1,250,000(a) | Gulf Stream Meridian 3, Ltd., Series 2021-IIIA, Class D, 12.32% (3 Month Term SOFR + 701 bps), 4/15/34 (144A) | 1,167,575 |

| 10,000,000 | Hertz Vehicle Financing III LP, Series 2021-2A, Class D, 4.34%, 12/27/27 (144A) | 8,720,462 |

| 9,996,000 | HOA Funding LLC - HOA, Series 2021-1A, Class A2, 4.723%, 8/20/51 (144A) | 8,185,824 |

| 591,860 | Home Partners of America Trust, Series 2019-1, Class F, 4.101%, 9/17/39 (144A) | 513,723 |

| 2,220,000 | HPEFS Equipment Trust, Series 2023-2A, Class D, 6.97%, 7/21/31 (144A) | 2,223,406 |

| 3,175,000(a) | ICG US CLO, Ltd., Series 2016-1A, Class DRR, 13.071% (3 Month Term SOFR + 770 bps), 4/29/34 (144A) | 2,472,017 |

| 2,250,000(a) | ICG US CLO, Ltd., Series 2021-1A, Class E, 11.90% (3 Month Term SOFR + 659 bps), 4/17/34 (144A) | 1,929,951 |

| 352,320 | JG Wentworth XXII LLC, Series 2010-3A, Class A, 3.82%, 12/15/48 (144A) | 348,115 |

| 3,070,000 | JPMorgan Chase Bank N.A. - CACLN, Series 2021-2, Class F, 4.393%, 12/26/28 (144A) | 2,865,892 |

| 4,025,000(a) | MF1, Ltd., Series 2021-FL7, Class D, 7.995% (1 Month Term SOFR + 266 bps), 10/16/36 (144A) | 3,861,601 |

The accompanying notes are an integral part of these financial statements.

Pioneer Strategic Income Fund | Annual Report | 9/30/2325

Schedule of Investments | 9/30/23 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Asset Backed Securities — (continued) | |

| 7,500,000(a) | MF1, Ltd., Series 2021-FL7, Class E, 8.245% (1 Month Term SOFR + 291 bps), 10/16/36 (144A) | $ 7,078,980 |

| 2,063,157 | Mosaic Solar Loan Trust, Series 2019-2A, Class D, 6.18%, 9/20/40 (144A) | 1,977,049 |

| 3,189,976 | Mosaic Solar Loan Trust, Series 2021-1A, Class D, 3.71%, 12/20/46 (144A) | 2,679,546 |

| 5,000,000(a) | Neuberger Berman CLO XVII, Ltd., Series 2014-17A, Class ER2, 12.807% (3 Month Term SOFR + 746 bps), 4/22/29 (144A) | 4,623,570 |

| 4,500,000(a) | Newark BSL CLO 1, Ltd., Series 2016-1A, Class DR, 11.869% (3 Month Term SOFR + 651 bps), 12/21/29 (144A) | 3,978,243 |

| 5,950,000 | NMEF Funding LLC, Series 2022-B, Class C, 8.54%, 6/15/29 (144A) | 5,919,307 |

| 1,119,000 | Octane Receivables Trust, Series 2020-1A, Class D, 5.45%, 3/20/28 (144A) | 1,097,176 |

| 1,456,780 | Orange Lake Timeshare Trust, Series 2019-A, Class D, 4.93%, 4/9/38 (144A) | 1,366,105 |

| 1,900,000(a) | Palmer Square Loan Funding, Ltd., Series 2022-1A, Class C, 7.908% (3 Month Term SOFR + 260 bps), 4/15/30 (144A) | 1,825,338 |

| 6,400,000 | PEAR LLC, Series 2021-1, Class B, 0.000%, 1/15/34 (144A) | 4,482,816 |

| 4,300,000 | PG Receivables Finance, Series 2020-1, Class C, 5.44%, 7/20/25 (144A) | 4,294,625 |

| 745,000 | Post Road Equipment Finance, Series 2021-1A, Class E, 4.36%, 3/15/29 (144A) | 735,796 |

| 5,000,000(a) | Race Point VIII CLO, Ltd., Series 2013-8A, Class DR2, 9.141% (3 Month Term SOFR + 376 bps), 2/20/30 (144A) | 4,847,620 |

| 9,600,000 | Republic Finance Issuance Trust, Series 2021-A, Class D, 5.23%, 12/22/31 (144A) | 7,965,501 |

| 3,000,000(c) | RMF Buyout Issuance Trust, Series 2021-HB1, Class M4, 4.704%, 11/25/31 (144A) | 2,510,101 |

| 6,000,000(c) | RMF Buyout Issuance Trust, Series 2021-HB1, Class M5, 6.00%, 11/25/31 (144A) | 4,841,101 |

| 3,750,000(c) | RMF Buyout Issuance Trust, Series 2022-HB1, Class M5, 4.50%, 4/25/32 (144A) | 417,187 |

| 1,500,000 | Rosy Blue Carat SCS, Series 2018-1, Class A1R, 8.481%, 3/15/30 (144A) | 1,509,000 |

The accompanying notes are an integral part of these financial statements.

26Pioneer Strategic Income Fund | Annual Report | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | Asset Backed Securities — (continued) | |

| 9,550,000 | Santander Bank Auto Credit-Linked Notes, Series 2022-B, Class F, 11.91%, 8/16/32 (144A) | $ 9,606,838 |

| 937,798 | Sierra Timeshare Receivables Funding LLC, Series 2019-1A, Class D, 4.75%, 1/20/36 (144A) | 905,687 |

| 846,357 | Sierra Timeshare Receivables Funding LLC, Series 2020-2A, Class D, 6.59%, 7/20/37 (144A) | 810,019 |

| 3,500,000(a) | Signal Peak CLO 2 LLC, Series 2015-1A, Class DR2, 8.438% (3 Month Term SOFR + 311 bps), 4/20/29 (144A) | 3,379,379 |

| 4,750,000(a) | Sound Point CLO XXI, Ltd., Series 2018-3A, Class C, 8.912% (3 Month Term SOFR + 356 bps), 10/26/31 (144A) | 4,268,521 |

| 3,000,000(a) | Sound Point CLO XXVIII, Ltd., Series 2020-3A, Class E, 12.513% (3 Month Term SOFR + 716 bps), 1/25/32 (144A) | 2,661,690 |

| 5,000,000(c) | Towd Point HE Trust, Series 2021-HE1, Class M2, 2.50%, 2/25/63 (144A) | 4,347,983 |

| 2,750,000 | Tricolor Auto Securitization Trust, Series 2021-1A, Class F, 5.08%, 5/15/28 (144A) | 2,663,025 |

| 4,250,000 | Tricon American Homes Trust, Series 2020-SFR2, Class E1, 2.73%, 11/17/39 (144A) | 3,589,461 |

| 1,000,000 | Upstart Securitization Trust, Series 2021-1, Class C, 4.06%, 3/20/31 (144A) | 971,210 |

| 1,294,000 | VFI ABS LLC, Series 2022-1A, Class D, 6.68%, 11/26/29 (144A) | 1,216,611 |

| 736,375 | Westgate Resorts LLC, Series 2020-1A, Class C, 6.213%, 3/20/34 (144A) | 727,384 |

| 2,650,249 | Westgate Resorts LLC, Series 2022-1A, Class C, 2.488%, 8/20/36 (144A) | 2,489,389 |

| 1,673,841 | Westgate Resorts LLC, Series 2022-1A, Class D, 3.838%, 8/20/36 (144A) | 1,555,652 |

| 4,000,000(a) | Whitebox CLO II, Ltd., Series 2020-2A, Class ER, 12.707% (3 Month Term SOFR + 736 bps), 10/24/34 (144A) | 3,833,204 |

| | Total Asset Backed Securities

(Cost $305,374,886) | $274,497,013 |

|

|

| | Collateralized Mortgage

Obligations—11.9% of Net Assets | |

| 5,970,020(c) | Bayview MSR Opportunity Master Fund Trust, Series 2021-2, Class A8, 2.50%, 6/25/51 (144A) | $ 3,566,605 |

The accompanying notes are an integral part of these financial statements.

Pioneer Strategic Income Fund | Annual Report | 9/30/2327

Schedule of Investments | 9/30/23 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 2,120,000(a) | Bellemeade Re, Ltd., Series 2019-1A, Class B1, 9.434% (1 Month USD LIBOR + 400 bps), 3/25/29 (144A) | $ 2,144,604 |

| 2,610,806(a) | Bellemeade Re, Ltd., Series 2019-1A, Class M2, 8.134% (1 Month USD LIBOR + 270 bps), 3/25/29 (144A) | 2,628,649 |

| 840,000(a) | Bellemeade Re, Ltd., Series 2020-3A, Class B1, 11.784% (SOFR30A + 646 bps), 10/25/30 (144A) | 881,404 |

| 1,450,000(a) | Bellemeade Re, Ltd., Series 2020-4A, Class B1, 10.434% (1 Month USD LIBOR + 500 bps), 6/25/30 (144A) | 1,479,697 |

| 8,062,000(c) | BINOM Securitization Trust, Series 2022-RPL1, Class M3, 3.00%, 2/25/61 (144A) | 4,940,533 |

| 3,133,312(c) | Brean Asset Backed Securities Trust, Series 2021-RM1, Class A, 1.40%, 10/25/63 (144A) | 2,608,984 |

| 2,588,481 | Brean Asset Backed Securities Trust, Series 2021-RM2, Class M1, 1.75%, 10/25/61 (144A) | 2,066,533 |

| 3,376,042(c) | Cascade Funding Mortgage Trust, Series 2019-RM3, Class C, 4.00%, 6/25/69 (144A) | 2,933,148 |

| 2,577,810(c) | CIM Trust, Series 2021-J2, Class B2, 2.671%, 4/25/51 (144A) | 1,841,000 |

| 3,060,002(c) | CIM Trust, Series 2021-J2, Class B3, 2.671%, 4/25/51 (144A) | 2,066,153 |

| 5,264,850(c) | Citigroup Mortgage Loan Trust, Series 2018-RP3, Class B2, 3.25%, 3/25/61 (144A) | 3,381,546 |

| 8,629,509(c) | Citigroup Mortgage Loan Trust, Series 2021-INV2, Class B1W, 2.989%, 5/25/51 (144A) | 6,433,569 |

| 2,029,190(c) | Citigroup Mortgage Loan Trust, Inc., Series 2018-RP1, Class B2, 3.188%, 9/25/64 (144A) | 1,346,356 |

| 2,670,000(a) | Connecticut Avenue Securities Trust, Series 2020-SBT1, Class 1M2, 9.079% (SOFR30A + 376 bps), 2/25/40 (144A) | 2,779,896 |

| 4,940,000(a) | Connecticut Avenue Securities Trust, Series 2020-SBT1, Class 2M2, 9.079% (SOFR30A + 376 bps), 2/25/40 (144A) | 5,148,359 |

| 16,450,000(a) | Connecticut Avenue Securities Trust, Series 2022-R02, Class 2B1, 9.815% (SOFR30A + 450 bps), 1/25/42 (144A) | 16,820,125 |

The accompanying notes are an integral part of these financial statements.

28Pioneer Strategic Income Fund | Annual Report | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 503,617(c) | CSFB Mortgage-Backed Pass-Through Certificates, Series 2003-17, Class B1, 5.50%, 6/25/33 | $ 5 |

| 2,638,958(c) | CSMC, Series 2021-RPL2, Class M3, 3.591%, 1/25/60 (144A) | 1,642,269 |

| 8,240,000(a)(e) | Eagle Re, Ltd., Series 2023-1, Class M1B, 9.265% (SOFR30A + 395 bps), 9/26/33 (144A) | 8,240,000 |

| 8,469,085(a)(f) | Federal Home Loan Mortgage Corp. REMICs, Series 4087, Class SB, 0.602% (SOFR30A + 592 bps), 7/15/42 | 611,169 |

| 4,623,860(a)(f) | Federal Home Loan Mortgage Corp. REMICs, Series 4091, Class SH, 1.122% (SOFR30A + 644 bps), 8/15/42 | 445,178 |

| 2,194,433(f) | Federal Home Loan Mortgage Corp. REMICs, Series 4999, Class QI, 4.00%, 5/25/50 | 413,552 |

| 2,684,059(f) | Federal Home Loan Mortgage Corp. REMICs, Series 5067, Class GI, 4.00%, 12/25/50 | 520,366 |

| 115,996 | Federal National Mortgage Association REMICs, Series 2009-36, Class HX, 4.50%, 6/25/29 | 113,939 |

| 2,404,043(a)(f) | Federal National Mortgage Association REMICs, Series 2012-14, Class SP, 1.121% (SOFR30A + 644 bps), 8/25/41 | 147,151 |

| 1,837,230(a)(f) | Federal National Mortgage Association REMICs, Series 2018-43, Class SM, 0.771% (SOFR30A + 609 bps), 6/25/48 | 142,277 |

| 2,121,369(a)(f) | Federal National Mortgage Association REMICs, Series 2019-33, Class S, 0.621% (SOFR30A + 594 bps), 7/25/49 | 106,519 |

| 1,743,647(a)(f) | Federal National Mortgage Association REMICs, Series 2019-41, Class PS, 0.621% (SOFR30A + 594 bps), 8/25/49 | 152,902 |

| 1,684,963(a)(f) | Federal National Mortgage Association REMICs, Series 2019-41, Class SM, 0.621% (SOFR30A + 594 bps), 8/25/49 | 147,987 |

| 1,915,387(f) | Federal National Mortgage Association REMICs, Series 2020-83, Class EI, 4.00%, 11/25/50 | 389,760 |

| 217,117,325(c)(f) | Flagstar Mortgage Trust, Series 2021-4, Class AX1, 0.205%, 6/1/51 (144A) | 2,207,758 |

| 5,655,111(c) | Flagstar Mortgage Trust, Series 2021-7, Class B3, 2.929%, 8/25/51 (144A) | 3,615,483 |

The accompanying notes are an integral part of these financial statements.

Pioneer Strategic Income Fund | Annual Report | 9/30/2329

Schedule of Investments | 9/30/23 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 3,585,000(a) | Freddie Mac STACR REMIC Trust, Series 2020-DNA5, Class B1, 10.115% (SOFR30A + 480 bps), 10/25/50 (144A) | $ 3,898,493 |

| 2,910,000(a) | Freddie Mac STACR REMIC Trust, Series 2020-DNA6, Class B1, 8.315% (SOFR30A + 300 bps), 12/25/50 (144A) | 2,860,908 |

| 2,630,000(a) | Freddie Mac STACR REMIC Trust, Series 2020-DNA6, Class B2, 10.965% (SOFR30A + 565 bps), 12/25/50 (144A) | 2,712,187 |

| 1,060,842(a) | Freddie Mac STACR REMIC Trust, Series 2020-HQA2, Class M2, 8.529% (SOFR30A + 321 bps), 3/25/50 (144A) | 1,094,059 |

| 2,670,000(a) | Freddie Mac STACR REMIC Trust, Series 2020-HQA3, Class B2, 15.429% (SOFR30A + 1,011 bps), 7/25/50 (144A) | 3,330,147 |

| 2,869,170(a) | Freddie Mac STACR REMIC Trust, Series 2020-HQA4, Class B1, 10.679% (SOFR30A + 536 bps), 9/25/50 (144A) | 3,096,528 |

| 2,340,000(a) | Freddie Mac STACR REMIC Trust, Series 2021-HQA4, Class B1, 9.065% (SOFR30A + 375 bps), 12/25/41 (144A) | 2,323,930 |

| 9,485,000(a) | Freddie Mac STACR REMIC Trust, Series 2022-DNA2, Class B1, 10.065% (SOFR30A + 475 bps), 2/25/42 (144A) | 9,591,706 |

| 5,510,000(a) | Freddie Mac STACR Trust, Series 2019-HRP1, Class B1, 9.479% (SOFR30A + 416 bps), 2/25/49 (144A) | 5,647,727 |

| 4,110,000(a) | Freddie Mac Structured Agency Credit Risk Debt Notes, Series 2020-HQA5, Class B1, 9.315% (SOFR30A + 400 bps), 11/25/50 (144A) | 4,349,009 |

| 6,250,000(a) | Freddie Mac Structured Agency Credit Risk Debt Notes, Series 2020-HQA5, Class B2, 12.715% (SOFR30A + 740 bps), 11/25/50 (144A) | 6,861,025 |

| 171,915 | Global Mortgage Securitization, Ltd., Series 2004-A, Class B2, 5.25%, 11/25/32 (144A) | 2 |

| 1,090,569 | Government National Mortgage Association, Series 2009-83, Class EB, 4.50%, 9/20/39 | 1,051,912 |

| 35,181 | Government National Mortgage Association, Series 2012-130, Class PA, 3.00%, 4/20/41 | 34,982 |

| 1,957,466(a)(f) | Government National Mortgage Association, Series 2019-103, Class SB, 0.611% (1 Month Term SOFR + 594 bps), 8/20/49 | 139,035 |

The accompanying notes are an integral part of these financial statements.

30Pioneer Strategic Income Fund | Annual Report | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 9,815,138(f) | Government National Mortgage Association, Series 2019-110, Class PI, 3.50%, 9/20/49 | $ 1,677,675 |

| 16,291,209(a)(f) | Government National Mortgage Association, Series 2019-117, Class SB, 0.000% (1 Month Term SOFR + 331 bps), 9/20/49 | 104,852 |

| 23,424,396(f) | Government National Mortgage Association, Series 2019-128, Class IB, 3.50%, 10/20/49 | 3,720,628 |

| 23,415,442(f) | Government National Mortgage Association, Series 2019-128, Class ID, 3.50%, 10/20/49 | 2,961,360 |

| 10,755,248(f) | Government National Mortgage Association, Series 2019-159, Class CI, 3.50%, 12/20/49 | 1,886,955 |

| 1,896,162(f) | Government National Mortgage Association, Series 2020-15, Class IM, 3.50%, 2/20/50 | 309,359 |

| 4,599,475(f) | Government National Mortgage Association, Series 2020-7, Class CI, 3.50%, 1/20/50 | 1,004,377 |

| 13,609,573(a)(f) | Government National Mortgage Association, Series 2020-9, Class SA, 3.35% (1 Month Term SOFR + 324 bps), 1/20/50 | 131,411 |

| 2,454,122(c) | GS Mortgage-Backed Securities Corp. Trust, Series 2019-PJ3, Class B4, 3.961%, 3/25/50 (144A) | 1,911,235 |

| 1,490,000(c) | GS Mortgage-Backed Securities Corp. Trust, Series 2019-PJ3, Class B5, 3.961%, 3/25/50 (144A) | 773,508 |

| 4,900,000(c) | GS Mortgage-Backed Securities Corp. Trust, Series 2021-RPL1, Class B1, 2.75%, 12/25/60 (144A) | 3,464,402 |

| 9,640,000(c) | GS Mortgage-Backed Securities Corp. Trust, Series 2022-PJ4, Class A33, 3.00%, 9/25/52 (144A) | 6,205,584 |

| 2,516,806(c) | GS Mortgage-Backed Securities Trust, Series 2021-PJ9, Class B3, 2.934%, 2/26/52 (144A) | 1,724,004 |

| 2,865,150(c) | GS Mortgage-Backed Securities Trust, Series 2022-MM1, Class B3, 2.819%, 7/25/52 (144A) | 1,985,522 |

| 4,595,055(c) | GS Mortgage-Backed Securities Trust, Series 2022-PJ1, Class B3, 2.834%, 5/28/52 (144A) | 3,031,270 |

| 1,220,000(a) | Home Re, Ltd., Series 2020-1, Class B1, 12.434% (1 Month USD LIBOR + 700 bps), 10/25/30 (144A) | 1,242,523 |

| 1,477,634(a) | Home Re, Ltd., Series 2020-1, Class M2, 10.684% (1 Month USD LIBOR + 525 bps), 10/25/30 (144A) | 1,492,291 |

The accompanying notes are an integral part of these financial statements.

Pioneer Strategic Income Fund | Annual Report | 9/30/2331

Schedule of Investments | 9/30/23 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 75,550,279(c)(f) | Hundred Acre Wood Trust, Series 2021-INV1, Class AX1, 0.226%, 7/25/51 (144A) | $ 815,595 |

| 2,562,912(c) | Hundred Acre Wood Trust, Series 2021-INV1, Class B2, 3.226%, 7/25/51 (144A) | 1,962,418 |

| 4,350,000(c) | Imperial Fund Mortgage Trust, Series 2021-NQM2, Class B2, 4.304%, 9/25/56 (144A) | 2,652,235 |

| 931,000(c) | JP Morgan Mortgage Trust, Series 2018-7FRB, Class B5, 6.644%, 4/25/46 (144A) | 715,480 |

| 138,283,280(c)(f) | JP Morgan Mortgage Trust, Series 2021-10, Class AX1, 0.121%, 12/25/51 (144A) | 808,197 |

| 2,000,000(c) | JP Morgan Mortgage Trust, Series 2021-3, Class A5, 2.50%, 7/25/51 (144A) | 1,237,611 |

| 6,414,101(c) | JP Morgan Mortgage Trust, Series 2021-7, Class B3, 2.803%, 11/25/51 (144A) | 4,184,153 |

| 122,556,932(c)(f) | JP Morgan Mortgage Trust, Series 2021-8, Class AX1, 0.121%, 12/25/51 (144A) | 669,847 |

| 8,227,822(c) | JP Morgan Mortgage Trust, Series 2021-8, Class B3, 2.846%, 12/25/51 (144A) | 5,378,773 |

| 1,977,893(c) | JP Morgan Mortgage Trust, Series 2021-INV1, Class B3, 2.98%, 10/25/51 (144A) | 1,296,109 |

| 1,682,530(c) | JP Morgan Mortgage Trust, Series 2021-INV1, Class B4, 2.98%, 10/25/51 (144A) | 898,225 |

| 3,999,452(c) | JP Morgan Mortgage Trust, Series 2021-INV4, Class B2, 3.214%, 1/25/52 (144A) | 2,896,685 |

| 4,213,708(c) | JP Morgan Mortgage Trust, Series 2021-INV4, Class B3, 3.214%, 1/25/52 (144A) | 2,841,328 |

| 4,592,765(c) | JP Morgan Mortgage Trust, Series 2022-3, Class B3, 3.113%, 8/25/52 (144A) | 3,189,428 |

| 5,650,000(c) | JP Morgan Mortgage Trust, Series 2022-4, Class A5, 3.00%, 10/25/52 (144A) | 3,629,231 |

| 5,468,285(c) | JP Morgan Mortgage Trust, Series 2022-4, Class B3, 3.259%, 10/25/52 (144A) | 3,630,235 |

| 5,846,524(c) | JP Morgan Mortgage Trust, Series 2022-5, Class B3, 2.958%, 9/25/52 (144A) | 3,745,080 |

| 8,483,294(c) | JP Morgan Mortgage Trust, Series 2022-INV1, Class B3, 3.295%, 3/25/52 (144A) | 5,684,822 |

| 5,375,197(a) | JPMorgan Chase Bank N.A. - CHASE, Series 2020-CL1, Class M3, 8.784% (1 Month Term SOFR + 346 bps), 10/25/57 (144A) | 5,399,997 |

| 2,213,437(a) | JPMorgan Chase Bank N.A. - JPMWM, Series 2021-CL1, Class M3, 7.115% (SOFR30A + 180 bps), 3/25/51 (144A) | 2,041,659 |

The accompanying notes are an integral part of these financial statements.

32Pioneer Strategic Income Fund | Annual Report | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 1,964,036(a) | JPMorgan Chase Bank N.A. - JPMWM, Series 2021-CL1, Class M4, 8.065% (SOFR30A + 275 bps), 3/25/51 (144A) | $ 1,771,370 |

| 1,023,657 | La Hipotecaria El Salvadorian Mortgage Trust, Series 2016-1A, Class A, 3.358%, 1/15/46 (144A) | 921,291 |

| 1,936,994 | La Hipotecaria Mortgage Trust, Series 2019-2A, Class BBB, 4.75%, 9/29/46 (144A) | 1,762,664 |

| 267,520(a) | La Hipotecaria Panamanian Mortgage Trust, Series 2010-1GA, Class A, 2.75% (Panamanian Mortgage Reference Rate - 300 bps), 9/8/39 (144A) | 254,144 |

| 6,302,403 | La Hipotecaria Panamanian Mortgage Trust, Series 2021-1, Class GA, 4.35%, 7/13/52 (144A) | 5,648,529 |

| 3,051,718(c) | Mello Mortgage Capital Acceptance, Series 2021-MTG1, Class B2, 2.646%, 4/25/51 (144A) | 2,078,778 |

| 3,955,678(c) | Mello Mortgage Capital Acceptance, Series 2021-MTG2, Class B2, 2.669%, 6/25/51 (144A) | 2,700,312 |

| 7,999,051(c) | Mello Mortgage Capital Acceptance, Series 2022-INV2, Class B3, 3.53%, 4/25/52 (144A) | 5,480,922 |

| 4,256,642(c) | MFA Trust, Series 2021-AEI2, Class B3, 3.285%, 10/25/51 (144A) | 2,970,296 |

| 7,172,000(c) | MFA Trust, Series 2021-RPL1, Class M2, 2.855%, 7/25/60 (144A) | 5,262,000 |

| 2,942,107(c) | Mill City Mortgage Loan Trust, Series 2017-3, Class B2, 3.25%, 1/25/61 (144A) | 2,172,796 |

| 6,145,000(c) | Mill City Mortgage Loan Trust, Series 2019-GS1, Class M3, 3.25%, 7/25/59 (144A) | 4,669,300 |

| 1,324,090(c) | Morgan Stanley Residential Mortgage Loan Trust, Series 2021-1, Class B3, 2.949%, 3/25/51 (144A) | 914,334 |

| 6,134,321(c) | Morgan Stanley Residential Mortgage Loan Trust, Series 2021-2, Class B2, 2.898%, 5/25/51 (144A) | 4,316,125 |

| 8,152,672(a) | New Residential Mortgage Loan Trust, Series 2020-2A, Class B4A, 6.43% (1 Month USD LIBOR + 250 bps), 10/25/46 (144A) | 7,757,121 |

| 13,903,950(c) | New Residential Mortgage Loan Trust, Series 2020-RPL1, Class B1, 3.881%, 11/25/59 (144A) | 10,151,716 |

The accompanying notes are an integral part of these financial statements.

Pioneer Strategic Income Fund | Annual Report | 9/30/2333

Schedule of Investments | 9/30/23 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 3,500,000 | NYMT Loan Trust, Series 2022-CP1, Class M2, 3.514%, 7/25/61 (144A) | $ 2,643,124 |

| 1,748,758(a) | Oaktown Re V, Ltd., Series 2020-2A, Class M2, 10.679% (SOFR30A + 536 bps), 10/25/30 (144A) | 1,780,871 |

| 2,680,710(c) | Oceanview Mortgage Trust, Series 2021-1, Class B2, 2.721%, 5/25/51 (144A) | 1,918,156 |

| 3,069,432(c) | Oceanview Mortgage Trust, Series 2021-1, Class B3A, 3.242%, 6/25/51 (144A) | 2,162,879 |

| 2,477,974(c) | Oceanview Mortgage Trust, Series 2021-3, Class B3, 2.713%, 6/25/51 (144A) | 1,178,095 |

| 1,875,279(c) | PRMI Securitization Trust, Series 2021-1, Class B2, 2.479%, 4/25/51 (144A) | 1,263,634 |

| 3,576,156(c) | PRMI Securitization Trust, Series 2021-1, Class B3, 2.479%, 4/25/51 (144A) | 2,263,887 |

| 2,799,960(c) | Provident Funding Mortgage Trust, Series 2021-1, Class B1, 2.384%, 4/25/51 (144A) | 2,050,412 |

| 2,717,328(c) | Provident Funding Mortgage Trust, Series 2021-2, Class B2, 2.352%, 4/25/51 (144A) | 1,861,242 |

| 2,776,757(c) | Provident Funding Mortgage Trust, Series 2021-INV1, Class B3, 2.782%, 8/25/51 (144A) | 1,934,430 |

| 2,303,829(c) | Provident Funding Mortgage Trust, Series 2021-J1, Class B2, 2.637%, 10/25/51 (144A) | 1,667,775 |

| 3,378,636(c) | Provident Funding Mortgage Trust, Series 2021-J1, Class B3, 2.637%, 10/25/51 (144A) | 2,315,397 |

| 1,460,000(a) | Radnor Re, Ltd., Series 2021-2, Class M2, 10.315% (SOFR30A + 500 bps), 11/25/31 (144A) | 1,510,691 |

| 3,345,892(c) | Rate Mortgage Trust, Series 2021-HB1, Class B2, 2.703%, 12/25/51 (144A) | 2,296,210 |

| 1,829,725(c) | Rate Mortgage Trust, Series 2021-HB1, Class B3, 2.703%, 12/25/51 (144A) | 1,167,078 |

| 4,236,099(c) | Rate Mortgage Trust, Series 2021-J1, Class B2, 2.707%, 7/25/51 (144A) | 3,047,738 |

| 1,732,010(c) | Rate Mortgage Trust, Series 2021-J1, Class B3, 2.707%, 7/25/51 (144A) | 1,049,713 |

| 2,231,134(c) | Rate Mortgage Trust, Series 2021-J3, Class B3, 2.713%, 10/25/51 (144A) | 1,503,324 |

| 1,723,000(c) | Rate Mortgage Trust, Series 2021-J4, Class B4, 2.634%, 11/25/51 (144A) | 585,291 |

The accompanying notes are an integral part of these financial statements.

34Pioneer Strategic Income Fund | Annual Report | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 3,937,372(c) | Rate Mortgage Trust, Series 2022-J1, Class B3, 2.751%, 1/25/52 (144A) | $ 2,656,275 |

| 1,971,279(c) | RCKT Mortgage Trust, Series 2021-2, Class B3, 2.563%, 6/25/51 (144A) | 1,372,336 |

| 10,150,000(c) | RCKT Mortgage Trust, Series 2022-3, Class A17, 3.00%, 5/25/52 (144A) | 6,392,630 |

| 2,436,205(c) | RCKT Mortgage Trust, Series 2022-3, Class B3, 3.188%, 5/25/52 (144A) | 1,663,490 |

| 3,038,892(c) | Sequoia Mortgage Trust, Series 2021-1, Class B3, 2.66%, 3/25/51 (144A) | 2,098,385 |

| 1,141,883(c) | Sequoia Mortgage Trust, Series 2021-2, Class B4, 2.552%, 4/25/51 (144A) | 511,214 |

| 1,171,204(c) | Sequoia Mortgage Trust, Series 2021-3, Class B4, 2.65%, 5/25/51 (144A) | 533,593 |

| 2,381,575(c) | Sequoia Mortgage Trust, Series 2021-4, Class B4, 2.666%, 6/25/51 (144A) | 1,088,622 |

| 1,494,270(c) | Sequoia Mortgage Trust, Series 2021-5, Class B4, 3.05%, 7/25/51 (144A) | 728,236 |

| 1,783,000(c) | Sequoia Mortgage Trust, Series 2021-9, Class B4, 2.86%, 1/25/52 (144A) | 652,117 |

| 4,100,000(c) | Sequoia Mortgage Trust, Series 2022-1, Class A7, 2.50%, 2/25/52 (144A) | 2,419,126 |

| 2,743,712(c) | Sequoia Mortgage Trust, Series 2022-1, Class B4, 2.946%, 2/25/52 (144A) | 1,051,868 |

| 4,550,000(a) | STACR Trust, Series 2018-HRP2, Class B1, 9.629% (SOFR30A + 431 bps), 2/25/47 (144A) | 4,834,303 |

| 5,000,000(c) | Towd Point Mortgage Trust, Series 2017-1, Class B3, 3.84%, 10/25/56 (144A) | 3,671,449 |

| 6,374,998(c) | Towd Point Mortgage Trust, Series 2017-3, Class B3, 3.897%, 7/25/57 (144A) | 4,869,800 |

| 5,639,000(a) | Towd Point Mortgage Trust, Series 2019-HY1, Class B2, 7.584% (1 Month Term SOFR + 226 bps), 10/25/48 (144A) | 5,307,916 |

| 9,185,805(c) | Towd Point Mortgage Trust, Series 2021-R1, Class A1, 2.918%, 11/30/60 (144A) | 7,470,696 |

| 1,830,000(a) | Triangle Re, Ltd., Series 2021-1, Class B1, 9.934% (1 Month USD LIBOR + 450 bps), 8/25/33 (144A) | 1,846,847 |

| 5,605,651(a) | Triangle Re, Ltd., Series 2021-1, Class M2, 9.334% (1 Month USD LIBOR + 390 bps), 8/25/33 (144A) | 5,632,862 |

| 3,440,510(c) | UWM Mortgage Trust, Series 2021-INV4, Class B2, 3.227%, 12/25/51 (144A) | 2,536,215 |

The accompanying notes are an integral part of these financial statements.

Pioneer Strategic Income Fund | Annual Report | 9/30/2335

Schedule of Investments | 9/30/23 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Collateralized Mortgage

Obligations—(continued) | |

| 800,000(c) | Visio Trust, Series 2019-2, Class B1, 3.91%, 11/25/54 (144A) | $ 541,482 |

| 2,250,000(c) | Wells Fargo Mortgage Backed Securities Trust, Series 2022-2, Class A5, 3.00%, 12/25/51 (144A) | 1,442,482 |

| 8,970,000(c) | Wells Fargo Mortgage Backed Securities Trust, Series 2022-2, Class A6, 2.50%, 12/25/51 (144A) | 5,271,168 |

| 8,364,523(c) | Wells Fargo Mortgage Backed Securities Trust, Series 2022-INV1, Class B3, 3.437%, 3/25/52 (144A) | 5,691,606 |

| | Total Collateralized Mortgage Obligations

(Cost $495,444,444) | $379,575,553 |

|

|

| | Commercial Mortgage-Backed

Securities—6.0% of Net Assets | |

| 5,800,000(a) | Alen Mortgage Trust, Series 2021-ACEN, Class E, 9.447% (1 Month Term SOFR + 411 bps), 4/15/34 (144A) | $ 2,991,512 |

| 3,600,000(a) | AREIT Trust, Series 2022-CRE6, Class D, 8.163% (SOFR30A + 285 bps), 1/20/37 (144A) | 3,379,563 |

| 5,158,815(d)(f) | Bayview Commercial Asset Trust, Series 2007-2A, Class IO, 0.000%, 7/25/37 (144A) | — |

| 1,500,000(a) | BDS, Ltd., Series 2020-FL5, Class C, 7.495% (1 Month Term SOFR + 216 bps), 2/16/37 (144A) | 1,456,377 |

| 2,025,000(c) | Benchmark Mortgage Trust, Series 2020-IG3, Class B, 3.391%, 9/15/48 (144A) | 1,096,917 |

| 1,895,412(a) | BSREP Commercial Mortgage Trust, Series 2021-DC, Class G, 9.297% (1 Month Term SOFR + 396 bps), 8/15/38 (144A) | 1,262,435 |

| 9,000,000(a) | BX Trust, Series 2021-ARIA, Class E, 7.691% (1 Month Term SOFR + 236 bps), 10/15/36 (144A) | 8,542,479 |

| 781,417(a) | Capital Funding Mortgage Trust, Series 2020-9, Class A, 8.58% (1 Month Term SOFR + 325 bps), 11/15/23 (144A) | 738,147 |

| 4,425,000(a) | Capital Funding Mortgage Trust, Series 2021-19, Class B, 20.54% (1 Month Term SOFR + 1,521 bps), 11/6/23 (144A) | 4,320,048 |

The accompanying notes are an integral part of these financial statements.

36Pioneer Strategic Income Fund | Annual Report | 9/30/23

Principal

Amount

USD ($) | | | | | | Value |

| | Commercial Mortgage-Backed

Securities—(continued) | |

| 1,500,000(a) | CGDB Commercial Mortgage Trust, Series 2019-MOB, Class F, 7.997% (1 Month Term SOFR + 266 bps), 11/15/36 (144A) | $ 1,385,040 |

| 2,470,000(a) | CLNY Trust, Series 2019-IKPR, Class E, 8.164% (1 Month Term SOFR + 284 bps), 11/15/38 (144A) | 2,218,100 |

| 148,421,147(c)(f) | COMM Mortgage Trust, Series 2014-CR19, Class XA, 1.08%, 8/10/47 | 813,289 |

| 2,485,000(c) | COMM Mortgage Trust, Series 2015-DC1, Class B, 4.035%, 2/10/48 | 2,128,041 |

| 7,650,000(c) | COMM Mortgage Trust, Series 2020-CBM, Class E, 3.754%, 2/10/37 (144A) | 6,977,648 |

| 3,912,000(c) | COMM Mortgage Trust, Series 2020-CBM, Class F, 3.754%, 2/10/37 (144A) | 3,494,859 |

| 3,750,000 | COMM Mortgage Trust, Series 2020-CX, Class A, 2.173%, 11/10/46 (144A) | 2,856,222 |

| 4,083,017(c) | CSAIL Commercial Mortgage Trust, Series 2015-C1, Class C, 4.392%, 4/15/50 | 3,002,808 |

| 2,680,000(c) | CSAIL Commercial Mortgage Trust, Series 2015-C4, Class D, 3.708%, 11/15/48 | 2,159,055 |