July 31, 2013

United States Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549

Attention: Mr. William H. Thompson

Ms. Yolanda Goubadia

Re: Bio Matrix Scientific Group, Inc..

Amendment No 2 to Form 10-K for the Fiscal Year ended September 30, 2012

Amendment No 1 to Form 10-Q for the Fiscal Quarters ended December 31, 2012 and March 31, 2013

filed June 21, 2013

Response dated June 19, 2013

File No. 000-32201

Dear Mr. Thompson and Ms. Goubadia :

The following responses address the comments of the Staff (the “Staff”) as set forth in its letter dated July 10, 2013 (the “Comment Letter”) relating to the abovementioned Exchange Act filings made by Bio Matrix Scientific Group, Inc. (The "Company").

On behalf of the Company, we respond as set forth below. The numbers of the responses in this letter correspond to the numbers of the Staff’s comments as set forth in the Comment Letter.

1.

The date of October 6, 1998 is the actual historical date of incorporation of the Company. The date of August 2, 2005 is the actual date of inception of Bio-Matrix Scientific Group, Inc., a Nevada corporation, which was acquired by the Company on July 3, 2006 in a transaction accounted for as a reverse merger.

From Note 1 to Notes to Financial Statements(emphasis added)

“Bio-Matrix Scientific Group, Inc. (“Company”) was organized October 6, 1998, under the laws of the State of Delaware as Tasco International, Inc.

From October 6, 1998 to June 3, 2006 its activities have been limited to capital formation, organization, and development of its business plan to provide production of visual content and other digital media, including still media, 360-degree images, video, animation and audio for the Internet.

On July 3, 2006 the Company abandoned its efforts in the field of digital media production when it acquired 100% of the share capital of Bio-Matrix Scientific Group, Inc., a Nevada corporation, (“BMSG”) for consideration consisting of 10,000,000 shares of the common stock of the Company and the cancellation of 10,000,000 shares of the Company owned and held by John Lauring.

As a result of this transaction, the former stockholder of BMSG held approximately 80% of the voting capital stock of the Company immediately after the transaction. For financial accounting purposes, this acquisition was a reverse acquisition of the Company by BMSG under the purchase method of accounting, and was treated as a recapitalization with BMSG as the acquirer.Accordingly, the financial statements have been prepared to give retroactive effect to August 2, 2005 (date of inception), of the reverse acquisition completed on July 3, 2006, and represent the operations of BMSG.

Through its wholly owned subsidiary, Regen BioPharma ,Inc., the Company intends to engage primarily in the development of regenerative medical applications which we intend to license from other entities up to the point of successful completion of Phase I and or Phase II clinical trials after which we would either attempt to sell or license those developed applications or, alternatively, advance the application further to Phase III clinical trials”

2.

The Balance Sheets for the Fiscal Year ended 9/30/2012 as well as for the quarters ended 12/31/2012 as well as 3/31/2013 have been amended to include Equity in Losses of Entest (accounted for under the Equity Method) within Retained Earnings (Deficit) accumulated during the development stage

3.

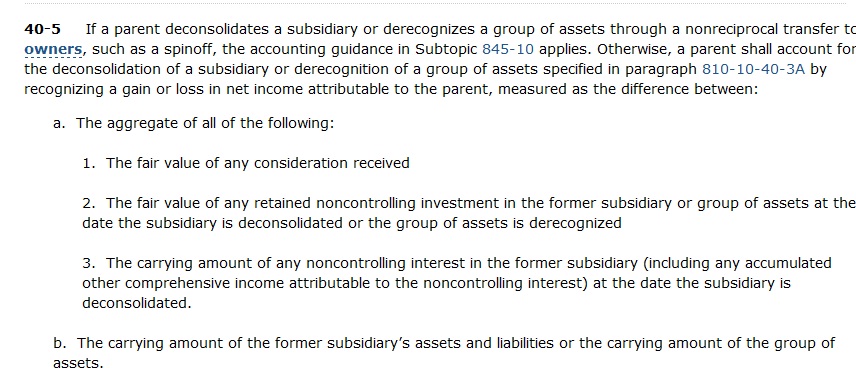

The financial statements have been amended to include the carrying value of the noncontrolling interest in the computation of gain on deconsolidation of Entest.

Gain on deconsolidation was recognized as the difference between:

(a) The aggregate of:

i. Consideration received being the excess of Entest liabilities eliminated from the consolidated Balance Sheet over Entest assets eliminated from the balance sheet as of the deconsolidation date ($182,649) plus

ii. The fair value (calculated utilizing Level 1 inputs in accordance with ASC 820) of the retained noncontrolling interest ($42,000,000 representing the stock price multiplied by the number of shares)

iii.. The carrying value of the noncontrolling interest ($536,961)

iv.. OCI. No OCI was applicable as ENTB’s results were consolidated with BMSN’s from the date of the acquisition of the 10,000,000 shares , therefore no other Comprehensive Income or Loss was generated during the period of consolidation.

And :

(b) The historical cost of the 10,000,000 shares of Entest stock owned by the Company ( representing the carrying value of the noncontrolling interest retained upon deconsolidation) was 100% of the stock of Entest CA. At the time Entest CA was transferred to JB Clothing Company , equity, book value, and sunk costs of ENTEST CA which were negligible

http://www.sec.gov/Archives/edgar/data/1449447/000139390509000266/jbc_8k.htm

http://www.sec.gov/Archives/edgar/data/1449447/000139390509000266/jbc_ex99-1.htm

http://www.sec.gov/Archives/edgar/data/1449447/000139390509000266/jbc_ex99-2.htm

ASC 810-10 40-5 provides the following guidance regarding deconsolidation of majority owned subsidiaries:

4. Other Losses reflect those losses attributable to Entest Biomedical, Inc. from the period beginning January 1, 2011 and ending February 3, 2011( Entest was deconsolidated on February 4, 2011) . Statements for Profit and Loss from inception for the Fiscal Year ended 9/30/2012 as well as for the quarters ended 12/31/2012 and 3/31/2013 have been amended to include this number in Operating Loss.

5.

Amounts for Deficit Attributable to Noncontrolling Interest have been removed from the Retained earnings column and are now reflected in a separate column in the Statement of Shareholder’s Equity.

With regards to ASC 810-10-50-1A , ASC 810-10-50-1A is applicable to disclosures regarding less than wholly owned subsidiaries. Subsidiaries are defined in the ASC Master Glossary as entities in which the Company has a controlling financial interest (ie greater than 50%). As of FYE 2012 and FYE 2011 there were no less than wholly owned subsidiaries in which the Company had a controlling financial interest. As such, the Company believes ASC 810-10-50-1A is not applicable for the FYE 2012 and 2011

In addition, with regards to the period from inception to FYE 2012 , ASC 810-10-50-1A requires presentation of transactions with owners acting in their capacity as owners ( contributions and distributions) and each component of Other Comprehensive Income. During the period of consolidation, changes in ownership percentage occurred primarily through issuances of common stock by Entest to unrelated third parties ( not sales or purchases by the Company) and Entest recognized no Other Comprehensive Income.

From the deconsolidation date until the quarter ended June 30, 2012 , the Investment in Entest was accounted for under the Equity Method as the Company’s ownership interest was over 20%. Under the Equity Method, the shareholder’s proportionate share of the investee’s net income increases the carrying value of the investment whereas the shareholder’s proportionate share of net losses decreases the carrying value of the investment.

(ASC 323-10-35.4)

By June 30, 2012 the Company’s interest in Entest fell below 20% ( as a result of additional stock issuances by Entest) and the 10,000,000 shares were reclassified as Available for Sale.

6.

The Company prepares its Statement of Cash Flow under the ‘indirect method” (ASC 230-45-28) which requires adjusting net income to reconcile it to net cash flow. Such reconciliation require recognition of noncash activities which affect Net Income (See ASC 230-45-28(b))

7. Amended to comply with the Commission’s comment

8. Amended to comply with the Commission’s comment.

The Company acknowledges that:

The Company is responsible for the adequacy and accuracy of the disclosure in the filing;

Staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and

The Company may not assert staff comments as a defense in any proceeding initiated by

Thank you for your kind assistance and the courtesies that you have extended to assist us in fulfilling our obligations under the Securities and Exchange Act of 1934. If, at any time, you have any further questions, please let us know.

Sincerely,

David R. Koos,

Chairman & CEO