UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 30, 2007

COMMISSION FILE NUMBER: 000-26125

RUBIO’S RESTAURANTS, INC.

(Exact Name of Registrant as Specified in Its Charter)

| DELAWARE | 33-0100303 |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification Number) |

| | |

1902 WRIGHT PLACE, SUITE 300, CARLSBAD, CALIFORNIA 92008

(Address of Principal Executive Offices)

(760) 929-8226

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | | Name of Each Exchange on Which Registered |

| Common Stock, par value $0.001 per share | | The NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes o No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer, as defined in Rule 12b-2 of the Act.

Large accelerated filer o | | Accelerated filer o |

Non-accelerated filer o | | Smaller reporting company þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

The aggregate market value of the voting stock held by non-affiliates of the registrant based upon the closing sale price of the registrant’s common stock on June 29, 2007 as reported on the NASDAQ Global Market was approximately $74.6 million. This amount excludes 2,519,228 shares of the registrant’s common stock held by the executive officers, directors and each person who beneficially owned 10% or more of the registrant’s outstanding common stock. Exclusion of such shares should not be construed to indicate that any such person possesses the power, direct or indirect, to direct or cause the direction of the management or policies of the registrant or that such person is controlled by or under common control with the registrant.

As of March 25, 2008, there were 9,950,477 shares of the registrant’s common stock, par value $0.001 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of our definitive proxy statement for the 2008 annual meeting of stockholders are incorporated by reference into PART III of this annual report on Form 10-K. Our 2008 annual meeting of stockholders is scheduled to be held on July 24, 2008. We intend to file our definitive proxy statement with the Securities and Exchange Commission not later than 120 days after the conclusion of our fiscal year ended December 30, 2007.

RUBIO’S RESTAURANTS, INC.

| | | |

| | | Page |

| PART I | | |

| Item 1. | Business | 4 |

| Item 1A. | Risk Factors | 12 |

| Item 1B. | Unresolved Staff Comments | 18 |

| Item 2. | Properties | 18 |

| Item 3. | Legal Proceedings | 18 |

| Item 4. | Submission of Matters to a Vote of Security Holders | 18 |

| | | |

| PART II | | |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 19 |

| Item 6. | Selected Consolidated Financial Data | 21 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 22 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 28 |

| Item 8. | Consolidated Financial Statements and Supplementary Data | 28 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 28 |

| Item 9A. | Controls and Procedures | 28 |

| Item 9B. | Other Information | 29 |

| | | |

| PART III | | |

| Item 10. | Directors and Executive Officers and Corporate Governance | 29 |

| Item 11. | Executive Compensation | 29 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 29 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 29 |

| Item 14. | Principal Accountant Fees and Services | 29 |

| | | |

| PART IV | | |

| Item 15. | Exhibits and Consolidated Financial Statement Schedules | 30 |

| | | |

| | Signatures | 32 |

| | Index to Consolidated Financial Statements | F-1 |

FORWARD-LOOKING STATEMENTS

This report includes statements of our expectations, intentions, plans and beliefs that constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 and are intended to come within the safe harbor protection provided by those sections. These forward-looking statements are principally contained in the section captioned “Business” under Item 1 below and the section captioned “Management’s Discussion and Analysis of Financial Condition and Results of Operations” under Item 7 below. In some cases, you can identify forward-looking statements by terms such as may, will, should, expect, plan, intend, forecast, anticipate, believe, estimate, predict, potential, continue or the negative of these terms or other comparable terminology. These forward-looking statements involve a number of risks and uncertainties, including but not limited to, those factors discussed under “Risk Factors” under Item 1A below and those discussed in other documents we file with the Securities and Exchange Commission. As a result of these risks and uncertainties, our actual results or performance may differ materially from any future results or performance expressed or implied by the forward-looking statements. These forward-looking statements represent beliefs and assumptions only as of the date of this annual report. Except as required by applicable law, we undertake no obligation to release publicly the results of any revisions or updates to these forward-looking statements to reflect events or circumstances arising after the date of this annual report.

As of March 25, 2008, we owned and operated 174 fast-casual Mexican restaurants, three licensed locations, and two franchised restaurants that offer high-quality, fresh and distinctive Mexican cuisine, at attractive prices; including chargrilled chicken, steak and fresh seafood items such as burritos, tacos and quesadillas inspired by the Baja, California region of Mexico. We were incorporated in California in 1985 and re-incorporated in Delaware in October 1997. We have two wholly owned subsidiaries, Rubio’s Restaurants of Nevada, Inc., which was incorporated in Nevada in 1997, and Rubio’s Promotions, Inc., which was incorporated in Arizona in 2007. Our restaurants are located in California, Arizona, Nevada, Colorado and Utah. As of March 25, 2008, we had approximately 3,400 employees.

RUBIO’S FRESH MEXICAN GRILL® CONCEPT

The Rubio’s Fresh Mexican Grill® concept evolved from the original “Rubio’s, Home of the Fish Taco®” concept, which our co-founder Ralph Rubio first developed following his college spring break trips to the Baja peninsula of Mexico in the mid-1970s. Ralph and his father, Raphael, opened the first Rubio’s® restaurant 25 years ago in the Mission Bay area of San Diego, California and introduced fish tacos to America. Building on the initial success of the concept, we expanded our menu and upgraded our restaurant layout over the years to appeal to a broader customer base, including a concept name change to Rubio’s Baja Grill® in 1997 to reflect these improvements. In 2002, Rubio’s further evolved, completing a transformation from Rubio’s original fish taco concept to Rubio’s Fresh Mexican Grill. The Rubio’s concept now features grilled chicken, steak and seafood items as well as our original, Baja-style World Famous Fish TacosSM. In 2005, we began a multi-year re-imaging program for our existing restaurants so that our interiors and exteriors display distinctive designs that match our high-quality, fresh food. In 2007, we rolled out Rubio’s A-Go-Go, which features major enhancements in our to-go, delivery and catering program that include improved packaging, product offerings, order processing and order fulfillment that we believe will make our program more convenient and attractive for our guests. Since the end of fiscal 2002 through March 2008, the number of company-owned restaurants has increased from 135 to 174. We believe Rubio’s Fresh Mexican Grill is well positioned as an innovator in the fast-casual Mexican cuisine segment. The critical elements of our market positioning are as follows:

| | • | FRESHLY PREPARED HIGH-QUALITY FOOD WITH BOLD, DISTINCTIVE TASTES AND FLAVORS. We differentiate ourselves from competitive restaurants by offering high-quality, flavorful, and made-to-order products using Baja-inspired recipes at attractive prices. Our menu strategy is predicated on developing unique, distinctive and flavorful products that generate strong guest loyalty. Rubio’s excels with seafood, and our signature items include our World Famous Fish Tacos, Baja Grill® Burritos with chargrilled chicken or steak and our authentic Street Tacos. Rubio’s also offers a number of burritos, tacos and quesadillas prepared in a variety of ways featuring grilled, marinated chicken, steak, pork, shrimp and mahi mahi. In addition, we serve freshly prepared salads and bowls. Our menu also includes HealthMex® offerings that are lower in fat and calories, and Kid’s Meals designed especially for children. Our guacamole, chips, beans and rice are prepared fresh daily in our restaurants. Guests may enhance and customize their meals at our complimentary salsa bar that features a variety of freshly prepared salsas. Our menu is served at lunch and dinner, as well as breakfast in a limited number of our restaurants. |

| | • | CASUAL, FUN DINING EXPERIENCE. Our restaurants are designed to create a fun and casual ambiance by capturing the relaxed, comfortable and colorful atmosphere inspired by the Baja, California region of Mexico. Our design elements include colorful Mexican tiles, saltwater aquariums with tropical fish, Baja beach photos and tropical prints, surfboards on the walls and authentic palm-thatched patio umbrellas, or palapas, in most locations. We believe our restaurants have broad appeal to a wide range of guests. |

| | • | EXCELLENT DINING VALUE. Our restaurants offer high-quality food typically associated with sit-down, casual dining restaurants, but generally at prices substantially lower than those found at casual dining restaurants. In addition to attractive prices, we offer the convenience and service platform of a traditional fast-casual or quick-service format. We provide guests a clean and comfortable environment in which to enjoy their meals on site. We also offer guests the convenience of take-out service for both individual meals and large party orders. We believe the strong value we deliver to our guests is critical to generating guest satisfaction, repeat business, and continued loyalty. |

OUR BUSINESS STRATEGIES

Our business objective is to become a leading fast-casual Mexican restaurant brand. To achieve this objective, we are pursuing the following strategies:

| | • | CREATE A DISTINCTIVE CONCEPT AND BRAND. Our restaurants provide guests with a fun and casual dining experience that we believe helps to promote frequent visits and strong guest loyalty. Our key initiatives are designed to deliver a great guest experience, enhance the performance of our existing restaurants, and strengthen our brand identity. These initiatives include developing proprietary menu offerings with bold, intense flavors, upgrading the ambiance of our restaurants, and delivering best-in-class service standards. We strive to promote awareness and generate trial through regional and local media campaigns and neighborhood brand-building efforts. |

| | • | ACHIEVE FAVORABLE RESTAURANT-LEVEL ECONOMICS. We believe we are able to achieve favorable operating results in our core markets due to the appeal of our concept, careful site selection, cost-effective development, consistent application of our management and training programs, and a focus on continuously improving our economic model. We utilize centralized and local restaurant information and accounting systems, which allow our management to monitor and control labor, food and other direct operating expenses on a real-time basis and provide them with timely access to financial and operating data. We believe we achieve a lower-than-average product cost compared with our competitors, due to our lower cost and high product mix seafood items versus a less diverse menu made up of higher cost items such as chicken and steak. As we expand and optimize our menu, we continue to focus on creating highly desirable, high-margin items. We also believe that our culture and emphasis on training leads to lower employee turnover rates, and higher productivity, compared with industry averages. |

| | • | FOCUS ON BUILDING SALES AT EXISTING RESTAURANTS. We regularly conduct and evaluate marketing research to analyze our markets, customer base, product mix and competition in order to remain relevant in the eyes of our consumers. Rubio’s marketing mix includes a combination of regional radio, in-store merchandising, public relations, neighborhood marketing, e-marketing and print media tactics. We periodically implement new products and promotions to increase traffic in our restaurants. |

| | • | ENSURE A HIGH-QUALITY GUEST EXPERIENCE. We strive to provide a consistent, high-quality guest experience in order to generate frequent visits and customer loyalty. We focus on creating a fun, team-like culture for our restaurant employees which we believe fosters a friendly and inviting atmosphere for our guests. Through extensive training, experienced restaurant-level management, and rigorous operational controls, we seek to ensure prompt, friendly and efficient service for our guests. We utilize an interactive voice response, or IVR, and Web-based guest feedback program to continually monitor our performance against guest expectations. We also seek out and respond to direct comments and questions from guests who utilize our toll-free guest comment line and “contact us” page on our Web-site. |

| | • | EXECUTE FOCUSED REGIONAL EXPANSION STRATEGY. We believe that our restaurant concept has significant opportunities for expansion in both our existing and neighboring markets. An expansion strategy focused primarily on company-owned unit growth will allow us to grow our brand and maintain the quality of food and service expected by our customers. We generally target high-traffic, high-visibility end-cap locations in urban and suburban markets with medium to high family income levels. Our three- to five-year expansion plan begins with an annual unit growth rate of approximately 10% in 2008 and increases to 20% by 2011. We currently plan to open 18 to 22 company-owned restaurants in fiscal 2008 in our existing geographic markets. The current slow down in housing, combined with general economic climate, has caused us to focus almost exclusively on sites located in mature trade areas. This narrower focus could limit our growth potential in 2008 and 2009. In addition, we will be required to secure a credit facility or line of credit in 2008 to support our planned restaurant growth. We cannot assure you that we can secure a credit facility or line of credit on acceptable terms, or at all. |

UNIT ECONOMICS

For purposes of analyzing our store operating results, and to eliminate the effects of start-up, training, and other costs associated with new store openings, we measure comparable store results on only those units that have been open for at least 15 months. During fiscal 2007, we had 153 units that were open for over 15 months. These units generated average sales of $1,037,000 per unit, average operating income of $123,000, or 11.9% of sales, and average operating cash flows of $173,000, or 16.7% of sales. Comparable store sales increased 6.2% in fiscal 2007 following an increase of 2.0% in fiscal 2006 and an increase of 1.2% in fiscal 2005.

These results are not necessarily indicative of our future results or the results we may obtain in other units currently open, or those we may open in the future.

EXISTING LOCATIONS

The following table sets forth information about our existing restaurants as of March 25, 2008. We own and operate 174 restaurants. We also have two franchised locations in Las Vegas, Nevada and have licensed our concept to other restaurant operators for three non-traditional locations in the San Diego and Los Angeles areas of California at Petco Park Stadium in San Diego, the San Diego International Airport food court and the Honda Center in Anaheim. The majority of our restaurants are in high-traffic retail centers and are not stand-alone units.

Company-Owned and Operated Locations | | Opened |

| Los Angeles Area | | | 72 |

| San Diego Area | | | 44 |

| Phoenix/Tucson Area | | | 29 |

| Denver Area | | | 3 |

| San Francisco Area | | | 11 |

| Sacramento Area | | | 9 |

| Las Vegas Area | | | 4 |

| Salt Lake City Area | | | 2 |

| Total Company-Owned Locations | | | 174 |

| | | | |

Franchise and Licensed Locations | | | |

| Los Angeles Area | | | 1 |

| San Diego Area | | | 2 |

| Las Vegas Area | | | 2 |

| Total Franchised and Licensed Locations | | | 5 |

We currently lease all of our restaurant locations with the exception of one owned building. We plan to continue to lease substantially all of our future restaurant locations in order to minimize the cash investment associated with each unit.

Historically, our restaurants have ranged from 1,800 to 3,300 square feet, excluding our smaller, food court locations. We expect the size of our future sites to range from 2,000 to 2,800 square feet. We intend to continue to develop restaurants that will require, on average, a total cash investment of approximately $575,000 to $625,000, excluding estimated pre-opening expenses of approximately $50,000 to $60,000 per unit, which includes approximately $20,000 to $30,000 of non-cash rent expense during the build-out period.

EXPANSION AND SITE SELECTION

Our expansion strategy targets major metropolitan areas that have attractive demographic characteristics. Once a metropolitan area is selected, we identify viable trade areas that have high-traffic patterns, strong demographics, such as medium to high family incomes, high education levels and high density of both daytime employment and residential developments, limited competition and strong retail and entertainment developments. Within a desirable trade area, we select sites that provide specific levels of visibility, accessibility, parking, co-tenancy and exposure to a large number of potential guests.

We believe that the quality of our site selection criteria is critical to our continuing success. Therefore, our senior management team is actively involved in the selection of new sites and markets, personally visiting all new markets and all sites prior to final approval. Each new market and site must be approved by our Real Estate Site Approval Committee, which consists of members of senior management. This process allows us to analyze each potential location, taking into account its effect on all aspects of our business, such as marketing, personnel, food service and supply chain dynamics.

Our three- to five-year expansion plan begins with an annual unit growth rate of approximately 10% in 2008, and increases to 20% by 2011. We currently plan to open 18 to 22 company-owned restaurants in fiscal 2008 in our existing geographic markets. The current slow down in housing, combined with the general economic climate, has caused us to focus almost exclusively on sites located in mature trade areas. This narrower focus could limit our growth potential in 2008 and 2009. In addition, we will be required to secure a credit facility or line of credit in 2008 to support our planned restaurant growth. We cannot assure you that we can secure a credit facility or line of credit on acceptable terms, or at all.

In connection with our strategy to expand into selected markets, we have and will continue to consider franchising our restaurant concept. We currently have a limited franchising program. As of March 25, 2008, we have one signed franchise development agreement. This agreement represents a commitment to open five restaurants in five years. The franchisee under this agreement opened its first restaurant in April 2006 and its second restaurant in August 2007. We are currently evaluating our options with respect to the franchising program, and the management and financial resources that will be required to build the operational infrastructure needed to support the franchising of our restaurants.

MENU

Our made-to-order menu - including our signature World Famous Fish Tacos - features burritos, soft-shell tacos, enchiladas, quesadillas, nachos and salads. All our products are made with high-quality ingredients including marinated, chargrilled chicken breast and carne asada steak as well as seafood, representative of the Baja, California region of Mexico, such as chargrilled mahi mahi, sautéed shrimp and Alaskan Pollock. The menu features most of Rubio’s favorite tacos bundled as meal combinations, where two tacos are served on plates with beans and chips. The goal of our menu is to maintain our heritage of offering distinctive fish and seafood items, while also including offerings of chicken, pork and beef items. Side items including our guacamole, chips, beans and rice and are all made fresh daily in our restaurants. Each of our restaurants also provide self-serve salsa bars where guests may choose from four different salsas made fresh every day in every restaurant. Our prices - targeted at the consumer who wants to spend $6.00 to $10.00 for a meal - range from about $1.49 for our snack-size Street Tacos to $6.99 for Grilled Shrimp Quesadillas. Most of our restaurants, other than those located in Nevada, also offer a selection of imported Mexican and domestic beers.

Our HealthMex menu items, designed to have less than 30% calories from fat and offered in most of our restaurants, include tacos, burritos served on whole-wheat tortillas, and salads, all made with chargrilled chicken or mahi mahi.

Our Kid’s Meals combine a choice of chicken taquitos, chicken bites, a World Famous Fish Taco, a cheese quesadilla or a bean and cheese burrito, along with a side dish of beans, rice or chips, and a small drink, churro and a toy surprise.

From time to time, we introduce limited-time-only products and promotions to provide added variety and encourage guest frequency. These products and promotions include, but are not limited to, Langostino lobster tacos and burritos, grilled Chilean salmon tacos, burritos and salads, and crispy shrimp tacos and burritos.

DECOR AND ATMOSPHERE

We believe that the decor and atmosphere of our restaurants are critical factors in our guests’ overall dining experience. In 2005, we began a multi-year re-image program for our existing restaurants so that our interiors and exteriors display distinctive designs that match our high-quality, fresh food. During 2007, we re-imaged six of our restaurants, which completed our re-imaging program. The Company re-imaged 27 restaurants in 2005 and 75 restaurants in 2006.

MARKETING

Our marketing mix includes a combination of regional radio advertising, in-store merchandising, public relations, neighborhood marketing, e-marketing and print media tactics. We use radio advertising as a marketing tool to increase brand awareness, attract new guests, and encourage existing guests to visit more frequently. Our advertising is designed to increase sales and transactions by conveying our brand positioning and creating awareness of new or limited-time products or promotions.

Local store marketing, public relations, and e-marketing are used to increase community awareness and generate traffic on a local level. A variety of programs are available for our restaurant general managers to target various business-building opportunities within the local community and trade area surrounding each restaurant. We believe word-of-mouth advertising is also a key component in attracting and retaining guests.

As part of our expansion strategy, we select markets that we believe will support multiple units and the efficient use of advertising. We sometimes utilize local public relations initiatives to help establish brand awareness for new restaurants as we build toward media efficiency. We expect our marketing expenditures to increase as we add new restaurants and focus on building awareness to drive new guests to our units and increase repeat visits by existing customers.

OPERATIONS

UNIT MANAGEMENT AND EMPLOYEES

We currently have approximately 3,400 employees. Our typical restaurant employs one general manager, one to two assistant managers and 18 to 25 hourly employees, approximately 40% of which are full-time employees and approximately 60% of which are part-time employees. The general manager is responsible for the day-to-day operations of the restaurant, including food quality, service, staffing and product ordering. We seek to train and develop from within, or hire experienced general managers and staff and to motivate and retain them by providing opportunities for increased responsibilities and advancement, as well as performance-based cash incentives. These performance incentives are tied to sales and profitability. All hourly employees in our restaurants are eligible for self-funded health benefits 60 days after they are hired. All full-time restaurant management employees are eligible for health benefits the first day of the month following their hire date. Full-time corporate employees are eligible for health benefits on their hire date. Employees over 21 years of age who have worked for us for more than one year are eligible to participate in our 401(k) plan. Because the members of our executive leadership team are typically not eligible to participate in our 401(k) plan, the Company adopted a non-qualified, unfunded retirement savings plan effective December 1, 2007.

We currently employ 2 district general managers and 18 district managers, each of whom reports to 1 of 3 regional directors. These three regional directors in turn report to a Senior Vice President of Operations. These district managers oversee restaurant management in all phases of operation, as well as assist in opening new restaurants. These district managers are eligible to participate in our cash bonus plan, and the three regional directors are eligible to participate in our cash bonus and stock incentive plans.

TRAINING

We strive to maintain quality and consistency in each of our restaurants through the careful training and supervision of personnel and the establishment of, and adherence to, high standards of personnel performance, food and beverage preparation, guest service, and maintenance of facilities. We have implemented a training program that is designed to teach new managers the technical and supervisory skills necessary to direct the operations of our restaurants in a professional and profitable manner. Each manager must successfully complete a five-week training course, which includes hands-on experience in both the kitchen and dining areas of our restaurants. They are also required to study our operations manuals and to view videotapes relating to food and beverage handling (particularly food safety and sanitation), preparation and service. In addition, we maintain a continuing education program to provide our restaurant managers with ongoing training and support. We strive to maintain a team-oriented atmosphere and attempt to instill enthusiasm and dedication in our employees. We regularly solicit employee suggestions concerning how we can improve our operations in order to be responsive to both them and our guests.

QUALITY CONTROLS

Our emphasis on superior guest service is complemented by our quality control programs. We utilize an interactive voice response, or IVR, and Web-based guest feedback program to continually monitor our performance against guest expectations. We also seek out and respond to direct comments and questions from guests who utilize our toll-free guest comment line and the “contact us” page on our Web-site. District managers are directly responsible for ensuring that guest comments are addressed appropriately to achieve a high level of guest satisfaction. Our director of quality assurance and food safety is responsible for ensuring product consistency, quality and safety among our restaurants.

HOURS OF OPERATION

Our restaurants are generally open Sunday through Thursday from 10:30 a.m. until 10:00 p.m., and on Friday and Saturday from 10:30 a.m. to 11:00 p.m.

MANAGEMENT INFORMATION SYSTEMS

All of our restaurants use computerized point-of-sale systems, which are designed to improve operating efficiency, provide corporate management timely access to financial and marketing data and reduce restaurant and corporate administrative time and expense. These systems record each order and display the food requests on monitors in the kitchen for the cooks to prepare. The data captured for use by operations and corporate management includes gross and net sales amounts, cash and credit card receipts and quantities of each menu item sold. Sales and receipt information is transmitted to the corporate office daily, where it is reviewed and reconciled by the accounting department before being recorded in the accounting system. The daily sales information is transmitted nightly to the corporate office and distributed to management via an intranet Web page each morning. A Windows-based back office system is used in all restaurants to manage food cost, labor cost and sales reporting. On a weekly basis, a report of actual food cost compared with ideal food cost is also generated.

Our corporate systems provide management with operating reports that show restaurant performance comparisons with budget and prior-year results both for the current accounting period and year-to-date, as well as trend formats by both dollars and percentage of sales. These systems allow us to closely monitor restaurant sales, cost of sales, labor expense and other restaurant trends on a daily, weekly and monthly basis. We believe these systems enable both restaurant and corporate management to supervise the operational and financial performance of our restaurants on a real-time basis, and will accommodate future expansion.

PURCHASING

We strive to obtain consistent high-quality ingredients at competitive prices from reliable sources. To attain operating efficiencies and to provide fresh ingredients for our food products while obtaining the lowest possible ingredient prices for the required quality, employees at the corporate office control the purchase of food items from a variety of international, national, regional and local suppliers at negotiated prices. Most food, produce and other products are shipped from a central distributor directly to the restaurants two to three times per week. We do not maintain a central food product warehouse or commissary. We do, however, maintain some products in third party warehouses for certain seafood items. Except for our contract with our central distributor, our contract with Coca-Cola North America FoodService, and several contracts ranging from 6 to 12 months for seafood, chicken and some beef, we do not have any long-term contracts with our food suppliers. In the past, we have not experienced significant delays in receiving our food and beverage inventories, restaurant supplies or equipment.

COMPETITION

The restaurant industry is intensely competitive. There are many different segments within the restaurant industry that are distinguished by types of service, food types and price/value relationships. We position our restaurants in the high-quality, fresh and distinctive, fast-casual Mexican cuisine segment of the industry. In this segment, our direct competitors include, among others, Baja Fresh, La Salsa, Chipotle and Qdoba. We also compete indirectly with full-service Mexican restaurants including Chevy’s, On The Border and El Torito as well as fast food restaurants, particularly those focused on Mexican cuisine, such as El Pollo Loco, Taco Bell and Del Taco. Competition in the fast-casual Mexican cuisine segment is based primarily upon food quality, taste, service, location, restaurant ambiance and price. Although we believe we compete favorably with respect to each of these factors, many of our direct and indirect competitors are well-established national, regional or local chains and have substantially greater financial, marketing, personnel and other resources. We also compete with many other retail establishments for site locations.

TRADEMARKS AND SERVICE MARKS

We have maintained registrations for two trademarks and nine service marks including, but not limited to, “Rubio’s,” “Rubio’s Baja Grill, Home of the Fish Taco,” “Home of the Fish Taco,” “HealthMex,” “Fish (Pesky) Caricature,” “Baja Grill,” “Best of Baja,” “Rubio’s Crispy Shrimp,” “Rubio’s Street Tacos,” “Rubio’s Fresh Mexican Grill” and “Beach Mex” with the United States Patents and Trademark Office. In addition, we have filed “Wrapsaladas,” “Cerveza Time,” “Rubio’s Street Burritos,” “Rubio’s Fish Taco Tuesdays,” “Rubio’s a-Go-Go,” “Tacos a-Go-Go,” “Burritos a-Go-Go,” “Beach Mex Buffet,” “Baja Box,” “Fiesta Kit,” “Grilled Gourmet Tacos” and “World Famous Fish Tacos.” We believe that our trademarks, service marks and other proprietary rights have significant value and are important to the marketing of our restaurant concept.

SEASONALITY

Our business is subject to seasonal fluctuations. Historically, sales in most of our restaurants have been higher during the second and third quarters of each fiscal year, during the warmer spring and summer months, particularly because most of our restaurants offer patio seating. As a result, our highest earnings generally occur in the second and third quarters of each fiscal year.

GOVERNMENT REGULATION

Our restaurants are subject to licensing and regulation by state and local health, sanitation, safety, fire and other authorities, including licensing and permit requirements for the sale of alcoholic beverages and food. To date we have not experienced an inability to obtain or maintain any necessary licenses, permits or approvals. In addition, the development and construction of additional restaurants are also subject to compliance with applicable zoning, land use and environmental regulations.

SEC FILINGS; INTERNET ADDRESS

Our Internet address is www.rubios.com. We file our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports with the SEC and make such filings available, free of charge, on www.rubios.com, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information found on our website shall not be deemed incorporated by reference by any general statement incorporating by reference this report into any filing under the Securities Act of 1933 or under the Securities Exchange Act of 1934, except to the extent we specifically incorporate the information found on our website by reference, and shall not otherwise be deemed filed under such Acts.

Our filings are also available through the SEC website, www.sec.gov, and at the SEC Public Reference Room at 100 F Street, NE Washington DC 20549. For more information about the SEC Public Reference Room, you can call the SEC at 1-800-SEC-0330.

MANAGEMENT

OUR EXECUTIVE OFFICERS

As of March 25, 2008, our executive officers are as follows:

Name | | Age | | Position with the Company |

| Dan Pittard | | 58 | | President and Chief Executive Officer |

| Frank Henigman | | 45 | | Senior Vice President and Chief Financial Officer |

| Lawrence Rusinko | | 47 | | Senior Vice President of Marketing |

| Marc Simon | | 55 | | Senior Vice President of Operations |

| Gerry Leneweaver | | 61 | | Senior Vice President of People Services |

| Ken Hull | | 52 | | Senior Vice President of Development |

DAN PITTARD has been President and Chief Executive Officer and a member of our Board of Directors since August 2006. Mr. Pittard’s diverse background brings unique qualifications for leadership at Rubio’s. He has served in key executive positions at companies including McKinsey & Company, PepsiCo, Inc. and Amoco Corp. (now part of BP p.l.c.). Mr. Pittard served a wide range of clients as a partner at McKinsey & Company from 1980 to 1992, including consumer companies for whom he helped develop profitable growth strategies and build new organizational capabilities. During his tenure at PepsiCo, Inc. from 1992 to 1995, he held several senior executive positions including Senior Vice President, Operations for PepsiCo Foods International, and Senior Vice President and General Manager, New Ventures for Frito-Lay. In this latter position, he worked with Taco Bell Corp. to create retail products and introduce them into supermarkets. At Amoco Corp. from 1995 to 1998, he served as Group Vice President. As Group Vice President, he had responsibility for several businesses with over $8 billion in revenues, including Amoco Corp.’s retail business that had 8,000 locations. During his tenure, he entered into a strategic alliance with McDonald’s Corporation to build joint locations. From 1998 to 1999, Mr. Pittard served as Senior Vice President, Strategy and Business Development for Gateway, Inc. In 1999, Mr. Pittard formed Pittard Investments LLC, and in 2004, he formed Pittard Partners LLC. Through these entities, Mr. Pittard has invested in and consulted for private companies. He served on the Board of Novatel Wireless, a publicly traded company, from 2002 to 2004. Mr. Pittard graduated from the Georgia Institute of Technology with a Bachelor of Science degree in Industrial Management and received an MBA from the Harvard Graduate School of Business Administration.

FRANK HENIGMAN has been Chief Financial Officer since June 2007, and Senior Vice President and Chief Financial Officer since November 2007. Prior to joining Rubio’s in 2006, Mr. Henigman served as Director of Accounting and Risk Control for Sumitomo Corporation of America/Pacific Summit Energy LLC located in Newport Beach, California from January 2005 to April 2006. Prior to Sumitomo, Mr. Henigman served as Director of Finance at Shell Trading Gas & Power Co. from 1998 to 2004. Mr. Henigman holds a Bachelor of Science, Business Administration and Marketing degree from California State University, Northridge and an MBA, Finance, from University of Southern California. Mr. Henigman has earned the designation of a Certified Management Accountant, a globally recognized certification for managerial accounting and finance professionals.

LAWRENCE RUSINKO has been Vice President of Marketing since October 2005, and Senior Vice President of Marketing since November 2007. Prior to joining Rubio’s in 2005, Mr. Rusinko served as Senior Vice President of Marketing at Friendly’s, a family dining and ice cream concept, from July 2003 until May 2005. Prior to that, Mr. Rusinko served for over 8 years at Panera Bread as Director of Marketing from May 1995 until March 1997 and as Vice President of Marketing from April 1997 until July 2003, and spent 6 ½ years in various marketing positions of progressive responsibility at Taco Bell. Mr. Rusinko holds a Bachelor of Science degree in Industrial Engineering from Northwestern University and an MBA from the J.L. Kellogg Graduate School of Management at Northwestern University.

MARC SIMON joined Rubio’s on November 28, 2007 as Senior Vice President of Operations and brings an extensive business and operations background to the Company. Most recently, he served as Chief Executive Officer for America’s Incredible Pizza Company in Tulsa, Oklahoma from October 2006 to August 2007. From 1994 to 1998, Mr. Simon worked for McDonald’s Corporation as Vice President for Corporate Development. He led the team that brought Chipotle Mexican Grill into McDonald’s and later served as Regional Director for Chipotle from 1998 to 2006. Mr. Simon has a master’s degree in Fine Arts and a master’s degree in Library and Informational Science from Case Western Reserve University and a Bachelor of Arts degree from Ohio University.

GERRY LENEWEAVER has been Vice President of People Services since June 2005, and Senior Vice President of People Services since November 2007. Prior to joining Rubio’s, Mr. Leneweaver led his own human resources consulting firm, AGL Associates, in Boston, from February 2004 to May 2005. Prior to that, Mr. Leneweaver served as Senior Vice President of Human Resources at American Hospitality Concepts, Inc. (The Ground Round, Inc.) from May 1999 to February 2004. He has also been in senior management roles at TGI Friday’s, Inc., The Limited, Inc., Atari, Inc., and PepsiCo, Inc. (Pizza Hut and Frito-Lay). He holds a Bachelor of Science degree in Industrial Relations from LaSalle University in Philadelphia.

KEN HULL joined Rubio’s on December 3, 2007 as Senior Vice President of Development. Most recently, Mr. Hull was Vice President of Development and Franchising for Frisch’s Restaurants, Inc. in Cincinnati, Ohio from 1999 to 2007. Frisch’s is an operator of Big Boy and Golden Corral restaurants. Prior to joining Frisch’s in 1999, Mr. Hull served as Director of International Development and Director of International Real Estate for McDonald’s Corporation. Earlier in his career, Mr. Hull worked for Hardee’s and KFC in Real Estate management positions. Mr. Hull has a Bachelor of Science degree in Landscape Architecture and Urban Planning from Iowa State University.

Any investment in our common stock involves a high degree of risk. You should consider carefully the following information about these risks, together with the other information contained in this annual report, before you decide to buy our common stock. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our operations. If any of the following risks actually occur, our business would likely suffer and our results could differ materially from those expressed in any forward-looking statements contained in this annual report including those contained in the section captioned “Business” under Item 1 above and the section captioned “Management’s Discussion and Analysis of Financial Condition and Results of Operations” under Item 7 below. In such case, the trading price of our common stock could decline, and you may lose all or part of the money you paid to buy our common stock

WE MAY NOT ACHIEVE OUR EXPECTED REVENUES, COMPARABLE STORE SALES AND OVERALL EARNINGS PER SHARE DUE TO VARIOUS RISKS THAT AFFECT THE FOOD SERVICE INDUSTRY.

We and other companies in the restaurant industry face a variety of risks that may impact our business and results of operations. Our expected sales levels and earnings rely heavily on the acceptability and quality of the products we serve. If any variances are experienced with respect to the recognition of our brand, the acceptance of our promotions in the market, the effectiveness of our advertising campaigns or the ability to manage our ongoing operations, including the ability to absorb unexpected costs, we could fall short of our revenue and earnings expectations. Factors that could have a significant impact on earnings include:

| · | | general economic conditions in our geographic markets, including the economic downturn that commenced during the end of fiscal 2007; |

| · | | labor costs for our hourly and management personnel, including increases in federal or state minimum wage requirements; |

| · | | the cost, availability and quality of foods and beverages, particularly chicken, beef, fish, cheese and produce; |

| · | | costs related to our leases; |

| · | | impact of weather and national disasters on revenues and costs of food; |

| · | | impact of increased fuel and energy costs; |

| · | | timing of new restaurant openings and related expenses; |

| · | | the cost of store closings; |

| · | | the amount of sales contributed by new and existing restaurants; |

| · | | our ability to achieve and sustain profitability on a quarterly or annual basis; |

| · | | the ability of our marketing initiatives and operating improvement initiatives to increase sales; |

| · | | negative publicity relating to food quality, illness, obesity, injury or other health concerns related to certain foods; |

| · | | changes in consumer preferences, traffic patterns and demographics; |

| · | | the type, number and location of existing or new competitors in the fast-casual restaurant industry; and |

| · | | insurance and utility costs. |

One of the most important financial measures to investors in restaurant businesses such as ours is comparable store sales. Investors use this measure to track our historic performance as well as to compare our trend results against other restaurant businesses. We expect our comparable store sales (which include company-operated restaurants only and represent the change in period-over-period sales for restaurants that have had at least 15 full months of operations) in fiscal 2008 to be adversely impacted by weaker consumer spending and the effect of comparing our sales to our record sales in fiscal 2007. If our comparable store sales are lower than expected by investors or are otherwise disappointing, our stock price may be adversely affected.

IF WE ARE NOT ABLE TO SUCCESSFULLY PURSUE OUR EXPANSION STRATEGY, OUR BUSINESS AND RESULTS OF OPERATIONS MAY BE ADVERSELY IMPACTED.

Our three to five year expansion plan begins with an annual unit growth rate of approximately 10% in 2008, and increases to 20% by 2011. We currently plan to open 18 to 22 company-owned restaurants in fiscal 2008 in our existing geographic markets. The current slow down in housing, combined with the general economic climate, has caused us to focus almost exclusively on sites located in mature trade areas. This narrower focus could limit our growth potential in 2008 and 2009. In addition, we will be required to secure a credit facility or line of credit in 2008 to support our planned restaurant growth plan. We cannot assure you that we can secure a credit facility or line of credit on acceptable terms, or at all. If we do not obtain a credit facility or line of credit, our growth will be significantly limited in 2008. In addition, the terms of any credit facility may impose restrictions on the operation of our business.

In addition, the success of our expansion strategy will depend on a variety of factors, many of which are beyond our control. These factors include, among others:

| · | | our ability to operate our restaurants profitably; |

| · | | our ability to respond effectively to the intense competition in the restaurant industry generally, and in the fast-casual restaurant industry segment; |

| · | | our ability to locate suitable high-quality restaurant sites or negotiate acceptable lease terms; |

| · | | our ability to obtain required local, state and federal governmental approvals and permits related to construction of the sites, and the sale of food and alcoholic beverages; |

| · | | our dependence on contractors to construct new restaurants in a timely manner; |

| · | | our ability to attract, train and retain qualified and experienced restaurant personnel and management; and |

| · | | our ability to control the construction and other costs associated with opening new restaurants. |

If we are not able to successfully address these factors, we may not be able to expand at the rate contemplated and may have to adjust our expansion strategy, and our business and results of operations may be adversely impacted.

WE MAY NOT PREVAIL IN OUR CURRENT LITIGATION MATTERS.

From time to time, we have been involved in litigation matters related to the operation of our restaurants. As discussed in Item 3, Legal Proceedings below, we are involved in two litigation matters arising out of California employment law. The Company has and intends to continue to vigorously defend itself in each of these actions. The outstanding claims or issues in these actions are in the early litigation stages, and we cannot assure you of the eventual outcome. In addition to these actions, we may also be subject to other employee-related claims or claims by our customers from time to time. Regardless of merit or eventual outcome, these matters may cause a diversion of our management's time and attention, significant damage awards and the expenditure of legal fees and expenses. In addition, claims asserted against us may result in adverse publicity. An unfavorable outcome in one or more of these matters or any future actions brought against the Company could have a material impact on our financial position and results of operations.

WE ARE VULNERABLE TO CHANGES IN CONSUMER PREFERENCES AND ECONOMIC AND OTHER CONDITIONS THAT COULD HARM OUR BUSINESS, FINANCIAL CONDITION, AND RESULTS OF OPERATIONS AND CASH FLOWS.

Our business, like other restaurant businesses, is affected by changes in consumer tastes, national, regional and local economic conditions, demographic trends, consumer confidence in the economy and discretionary spending priorities. Factors such as traffic patterns, weather conditions, local demographics and the type, number and location of competing restaurants may adversely affect the performance of individual locations. In addition, inflation and increased food and energy costs may harm the restaurant industry in general and our locations in particular. Adverse changes in any of these factors could reduce consumer traffic or impose practical limits on pricing, which could harm our business, financial condition, results of operations and cash flows. We cannot assure you that consumers will continue to regard our products favorably or that we will be able to develop new products that appeal to consumer preferences. Any failure to satisfy consumer preferences could have a materially adverse affect on our business. Our continued success will depend in part on our ability to anticipate, identify and respond to changing consumer preferences and economic conditions.

OUR BUSINESS MAY BE ADVERSELY AFFECTED BY FOOD-BORNE ILLNESS INCIDENTS, NEGATIVE PUBLICITY OR CLAIMS FROM OUR GUESTS.

We cannot guarantee that our internal controls and training at our restaurants will be fully effective in preventing all food-borne illnesses. Furthermore, our reliance on third party suppliers, distributors and warehouse providers makes it difficult to monitor food safety compliance and increases the risk that food-borne illness would affect multiple locations rather than a single restaurant. Third party food suppliers, distributors and warehouse providers outside of our control could cause some food-borne illness incidents. New illnesses resistant to our current precautions may develop in the future, or diseases with long incubation periods could arise, that could give rise to claims or allegations on a retroactive basis. One or more instances of food-borne illness in one of our restaurants could negatively affect our restaurant sales if highly publicized. This risk exists even if it were later determined that the illness was wrongly attributed to one of our restaurants. A number of other restaurant chains have experienced incidents related to food borne illnesses that have had a material adverse impact on their operations, and we cannot assure you that we can avoid a similar impact upon the occurrence of a similar incident at our restaurants. In addition, we may be subject to liability claims from guests alleging food-related illness, injuries suffered on our premises or other food quality, health or operational concerns. Adverse publicity resulting from such allegations may materially affect us and our restaurants, regardless of whether such allegations are true or whether we are ultimately held liable.

WE DEPEND UPON A LIMITED NUMBER OF THIRD PARTY SUPPLIERS, DISTRIBUTORS AND WAREHOUSE PROVIDERS.

Our ability to maintain consistent quality menu items depends in part upon our ability to acquire fresh food products and related items, including essential ingredients used in the Mexican restaurant business from reliable sources in accordance with our specifications. Shortages or interruptions in the supply of fresh food products caused by unanticipated demand, problems in production or distribution, contamination of food products, an outbreak of food-borne diseases, inclement weather or other conditions could materially adversely affect the availability, quality and cost of ingredients, which could adversely affect our business, financial condition, results of operations and cash flows. We have contracts with a limited number of suppliers, distributors and warehouse providers for our food, beverages and other supplies for our restaurants. If any of our suppliers, distributors or warehouse providers do not perform adequately or if any one or more of such entities seeks to terminate its agreement or fails to perform as anticipated, or if there is any disruption in any of our supply relationships or distribution operations for any reason, it could have a material adverse effect on our business, financial condition, results of operations and cash flows. Our inability to replace our distribution operations and our suppliers in a short period of time on acceptable terms could increase our costs and could cause shortages at our restaurants of food and other items that may cause our restaurants to remove certain items from a restaurant’s menu or temporarily close a restaurant. If we temporarily close a restaurant or remove popular items from a restaurant’s menu, that restaurant may experience a significant reduction in revenue during the time affected by the shortage.

IF WE ARE NOT ABLE TO ANTICIPATE AND REACT TO INCREASES IN OUR FOOD AND LABOR COSTS, OUR PROFITABILITY COULD BE ADVERSELY AFFECTED.

Our restaurant operating costs principally consist of food and labor costs. Our profitability is dependent on our ability to anticipate and react to changes in these costs. Various factors beyond our control, including increased food and energy costs, adverse weather conditions, short supply and natural disasters may affect our food costs. Changes in government regulations could also affect both our food costs and labor costs. We may be unable to anticipate and react to changing costs, whether through our purchasing practices, menu composition or menu price adjustments in the future. In the event that cost increases cause us to increase our menu prices, we face the risk that our guests will choose to patronize lower-priced restaurants. Failure to react in a timely manner to changing food and labor costs, or to retain guests if we are forced to raise menu prices, could have a material adverse effect on our business and results of operations.

OUR RESTAURANTS ARE CONCENTRATED IN THE WESTERN REGION OF THE UNITED STATES, AND THEREFORE, OUR BUSINESS IS SUBJECT TO FLUCTUATIONS IF ADVERSE CONDITIONS OCCUR IN THAT REGION.

As of March 25, 2008, all but five of our existing restaurants are located in the western region of the United States. Accordingly, we are susceptible to fluctuations in our business caused by adverse economic or other conditions in this region, including natural disasters, terrorist activities or similar events. Our significant investment in, and long-term commitment to, each of our restaurants limits our ability to respond quickly or effectively to changes in local competitive conditions or other changes that could affect our operations. In addition, some of our competitors have many more units than we do. Consequently, adverse economic or other conditions in a region, a decline in the profitability of several existing restaurants or the introduction of several unsuccessful new restaurants in a geographic area, could have a more significant effect on our results of operations than would be the case for a company with a larger number of restaurants or with more geographically dispersed restaurants.

LABOR AND EMPLOYMENT LAWS AND REGULATIONS, PARTICULARLY STATE MINIMUM WAGE LAWS, MAY IMPACT OUR BUSINESS.

A substantial number of our employees are subject to various federal and state minimum wage requirements. Many of our employees work in restaurants located in California and receive salaries equal to or slightly greater than the California minimum wage. California’s current hourly minimum wage is $8.00. Any increase in the hourly minimum wage in California or other states or jurisdictions where we do business may increase the cost of labor and reduce our profitability. Additionally, various federal and state laws govern the relationship with our employees and affect our operating costs. In addition to minimum wage laws discussed above, these laws include:

| | · | mandatory employee health insurance; |

| | · | workers’ compensation rates; and |

| | · | citizenship requirements. |

Significant additional governmental imposed increase in any of these areas could materially affect our business, financial condition and operating results.

THE RESTAURANT INDUSTRY IS INTENSELY COMPETITIVE AND WE MAY NOT HAVE THE RESOURCES TO COMPETE ADEQUATELY.

The restaurant industry is intensely competitive. There are many different segments within the restaurant industry that are distinguished by types of service, food types and price/value relationships. We position our restaurants in the high-quality, fresh and distinctive, fast casual Mexican restaurant segment of the industry. In this segment, our direct competitors include, among others, Baja Fresh, La Salsa, Chipotle and Qdoba. We also compete indirectly with full-service Mexican restaurants including Chevy’s, On The Border, Chi Chi’s and El Torito and fast food restaurants, particularly those focused on Mexican food such as El Pollo Loco, Taco Bell and Del Taco. Competition in our industry segment is based primarily upon food quality, price, restaurant ambiance, service and location. Many of our direct and indirect competitors are well-established national, regional or local chains and have substantially greater financial, marketing, personnel and other resources than we do. We also compete with many other retail establishments for site locations. If we are unable to compete effectively in our industry segment, our business and operations will be adversely affected.

OUR FAILURE OR INABILITY TO ENFORCE OUR CURRENT AND FUTURE TRADEMARKS AND TRADE NAMES COULD ADVERSELY AFFECT OUR EFFORTS TO ESTABLISH BRAND EQUITY.

Our ability to successfully expand our concept will depend on our ability to establish and maintain "brand equity" through the use of our current and future trademarks, service marks, trade dress and other proprietary intellectual property, including our name and logos. We currently hold two registered trademarks and have nine service marks relating to our brand and we have filed applications for 12 additional marks. Some or all of the rights in our intellectual property may not be enforceable, even if registered against any prior users of similar intellectual property or our competitors who seek to utilize similar intellectual property in areas where we operate or intend to conduct operations. If we fail to enforce any of our intellectual property rights, we may be unable to capitalize on our efforts to establish brand equity. It is also possible that we will encounter claims from prior users of similar intellectual property in areas where we operate or intend to conduct operations, which could result in additional expenditures and divert management’s time and attention from our operations.

WE MAY NOT BE SUCCESSFUL IN IMPLEMENTING AND EXECUTING A FRANCHISE PROGRAM.

In connection with our strategy to expand into selected markets, we have and will continue to consider franchising our restaurant concept. We currently have a limited franchising program. We started a franchise program by entering into agreements with three franchisee groups between 2001 and 2002. In April 2003, our relationship with one of the franchisee groups was terminated when the group defaulted on its franchise agreement and closed its franchised location. We re-opened this unit as a company-owned restaurant in May 2003, but subsequently closed it in December 2005. In September 2003, we agreed to acquire a franchisee’s location and then in December 2006 acquired their other restaurant and development territory. In addition, in June 2006, we acquired all four restaurants owned by the third original franchise group. Currently we have one franchisee that has a five-year, five-unit development agreement for which they opened their first restaurant in 2006 and their second restaurant in August 2007. Restaurant companies typically rely on franchise revenues as a significant source of revenues and potential for growth. The opening and success of our franchised restaurants depend on a number of factors, including availability of suitable sites, our ability to obtain acceptable lease or purchase terms for new locations, permitting and government regulatory compliance and our ability to meet construction schedules. The franchisees may not have all of the business abilities or access to financial resources necessary to open our restaurants or to successfully develop or operate our restaurants in their franchise areas in a manner consistent with our standards. Our inability to successfully execute a franchising program could adversely affect our business and results of operations.

WE MAY BE LOCKED INTO LONG-TERM AND NON-CANCELABLE LEASES AND MAY BE UNABLE TO RENEW LEASES AT THE END OF THEIR TERMS.

Many of our current leases are non-cancelable and typically have an initial term of 10 years and one or more renewal terms of three or more years that we may exercise at our option. Leases that we enter into in the future likely will also be long-term and non-cancelable and have similar renewal options. If we close a restaurant, we may remain committed to perform our obligations under the applicable lease, which would include, among other things, payment of the base rent for the balance of the lease term. Alternatively, at the end of the lease term and any renewal period for a restaurant, we may be unable to renew the lease without substantial additional cost, if at all. We may close or relocate the restaurant, which could subject us to construction and other costs and risks, and could have a material adverse effect on our business. Additionally, the revenue and profit, if any, generated at a relocated restaurant, may not equal the revenue and profit generated at the existing restaurant.

IF THE AMOUNTS THAT WE HAVE ACCRUED IN CONNECTION WITH THE CLOSURE OF SELECTED STORES ARE INADEQUATE OR WE CLOSE MORE STORES THAN ANTICIPATED, WE MAY EXPERIENCE ADVERSE EFFECTS ON OUR EARNINGS EXPECTATIONS.

Our accruals for expenses related to store closures are estimates. Estimates are inherently uncertain, and actual results may deviate, perhaps substantially, from our estimates as a result of the many risks and uncertainties affecting our business, including, but not limited to, those set forth in these risk factors. The amounts we have recorded for store closures are based on our current assessments of the conditions of these locations. The market for, and physical condition of, these locations may change in the future and materially affect our future earnings. We review these accruals on a quarterly basis and may make adjustments that have a material positive or negative impact on our future earnings.

OUR OPERATING RESULTS MAY FLUCTUATE SIGNIFICANTLY DUE TO SEASONALITY AND OTHER FACTORS, WHICH COULD HAVE A NEGATIVE EFFECT ON THE PRICE OF OUR COMMON STOCK.

Our business is subject to seasonal fluctuations. Historically, sales in most of our restaurants have been higher during the second and third quarters of each fiscal year. As a result, we generally find our highest earnings occur in the second and third quarters of each fiscal year. Accordingly, results for any one quarter or for any year are not necessarily indicative of results to be expected for any other quarter or for any other year and should not be relied upon as the sole measure of our future performance. Comparable unit sales for any particular future period may increase or decrease versus our previous performance.

THE ABILITY TO ATTRACT AND RETAIN HIGHLY QUALIFIED PERSONNEL TO OPERATE, MANAGE AND SUPPORT OUR RESTAURANTS IS EXTREMELY IMPORTANT AND OUR FAILURE TO DO SO COULD ADVERSELY AFFECT US.

Our success and the success of our individual restaurants depend upon our ability to attract and retain highly motivated, well-qualified restaurant operators and management personnel, as well as a sufficient number of qualified employees, including guest service and kitchen staff, to keep pace with our expansion schedule. Qualified individuals needed to fill these positions are in short supply in some geographic areas. Our ability to recruit and retain such individuals may delay the planned openings of new restaurants or result in higher employee turnover in existing restaurants, which could have a material adverse effect on our business or results of operations. We also face significant competition in the recruitment of qualified employees. In addition, we are heavily dependent upon the services of our officers and key management involved in restaurant operations, marketing, product development, finance, purchasing, real estate development, information technologies, human resources and administration. The loss of any of these individuals could have a material adverse effect on our business and results of operations. We generally do not have long-term employment contracts with key personnel.

VARIOUS GOVERNMENT REGULATIONS MAY IMPACT OUR BUSINESS.

The restaurant industry is subject to licensing and regulation by state and local health, sanitation, safety, fire and other authorities, including licensing requirements and regulations related to the preparation and sale of food and the sale of alcoholic beverages, as well as laws governing our relationships with employees. See “Labor and Employment Laws and Regulations, Particularly State Minimum Wage Laws May Impact our Business” above. The inability to obtain or maintain such licenses or to comply with applicable regulations could adversely affect our results of operations. We are also subject to federal regulation and certain state laws, governing the offer and sale of franchises. Many state franchise laws impose substantive requirements on franchise agreements, including limitations on non-competition provisions and on provisions concerning the termination or non-renewal of a franchise. The failure to obtain or retain licenses or approvals to sell franchises could adversely affect us and our franchisees. Changes in, and the cost of compliance with, government regulations could also have a material adverse effect on our operations.

WE ARE REQUIRED TO EVALUATE OUR INTERNAL CONTROLS UNDER SECTION 404 OF THE SARBANES-OXLEY ACT OF 2002 AND ANY ADVERSE RESULTS FROM SUCH EVALUATION COULD RESULT IN A LOSS OF INVESTOR CONFIDENCE IN OUR FINANCIAL REPORTS AND HAVE AN ADVERSE EFFECT ON OUR STOCK PRICE.

Pursuant to Section 404 of the Sarbanes-Oxley Act of 2002, beginning with this annual report on Form 10-K , we will be required to furnish a report by our management on our internal control over financial reporting. Such report must contain, among other matters, an assessment of the effectiveness of our internal control over financial reporting and audited consolidated financial statements as of the end of our fiscal year. This assessment must include disclosure of any material weaknesses in our internal control over financial reporting identified by management. This annual report on Form 10-K does not require an attestation from the Company’s audit firm. Each year we must perform the system and process documentation and evaluation needed to comply with Section 404, which is both costly and challenging. During this process, if our management identifies one or more material weaknesses in our internal control over financial reporting, we will be unable to assert such internal control is effective. If we are unable to assert that our internal control over financial reporting is effective (or if our auditors are unable to attest that our management’s report is fairly stated or they are unable to express an unqualified opinion on the effectiveness of our internal controls), investors could lose confidence in the accuracy and completeness of our financial reports, which could have an adverse effect on our stock price.

Furthermore, our independent registered public accounting firm may be required to attest to whether our assessment of the effectiveness of our internal control over financial reporting is fairly stated in all material respects, and separately report on whether it believes we maintained effective internal control over financial reporting. We have in the past discovered, and may in the future discover, areas of internal controls that need improvement. We may be required to obtain auditor attestation as early as the annual report on Form 10-K for our fiscal year ending December 28, 2008.

OUR CURRENT INSURANCE MAY NOT PROVIDE ADEQUATE LEVELS OF COVERAGE AGAINST LOSSES, CLAIMS OR THE EFFECTS OF ADVERSE PUBLICITY.

We may incur certain losses that are uninsurable or that we believe are not economically insurable, such as losses due to earthquakes, floods and other natural disasters. In view of the location of many of our existing and planned restaurants, our operations are particularly susceptible to damage and disruption caused by earthquakes. Further, although we maintain insurance coverage for employee-related litigation, the deductible per incident is high and because of the high cost, we carry only limited insurance for the effects of such claims. In addition, punitive damage awards are generally not covered by insurance. In addition, our insurance does not provide coverage for the type of claims asserted in the two employee actions discussed in Item 3. Legal Proceedings, below. Any insurance we maintain may not be sufficient to provide coverage against any asserted claims. We also may be unable to maintain our insurance or obtain insurance in the future on acceptable terms, or at all.

WE MAY INCUR SIGNIFICANT REAL ESTATE RELATED COSTS AND LIABILITIES THAT COULD ADVERSELY AFFECT OUR FINANCIAL CONDITION.

The majority of our restaurants are leased locations in multi-unit retail centers. The age and condition of the real estate we occupy varies. Some of our locations may require significant repairs due to normal deterioration or due to sudden and unanticipated incidents, such as plumbing failures. It is difficult to predict how many of our restaurant locations will require major repairs or refurbishment and it is also difficult to predict what portion of these potential costs would be covered by insurance. Also, as a lessee of real estate, we are subject to and have received claims that our operations at these locations may have caused property damage or personal injury to others. The fact that the majority of our restaurants are located in multi-unit retail buildings means that if there is a plumbing failure or other event in one of our restaurants, neighboring tenants may be affected, which can subject us to liability for property damage and personal injuries. If we were to incur increased real estate costs and liabilities, it could adversely affect our financial condition and results of operations.

SALES BY OUR EXISTING STOCKHOLDERS OF A LARGE NUMBER OF SHARES OF OUR COMMON STOCK COULD CAUSE OUR STOCK PRICE TO DECLINE.

The Company has a limited number of institutional stockholders, each of whom holds more than 5% of the Company’s outstanding stock. The market price of our common stock could decline as a result of sales by one of these stockholders of a large number of shares of our common stock in the market or the perception that such sales could occur. These sales also might make it more difficult for us to sell equity securities in the future at a time and at a price that we deem appropriate.

THE INTERESTS OF OUR CONTROLLING STOCKHOLDERS MAY CONFLICT WITH YOUR INTERESTS.

As of March 25, 2008, our executive officers, directors and entities affiliated with them, in the aggregate, beneficially own approximately 28.7% of our outstanding common stock. These stockholders may be able to influence the outcome of matters requiring stockholder approval, including the election of directors and approval of significant corporate transactions. This concentration of ownership may also have the effect of delaying or preventing a change in control of our Company and could also depress our stock price.

None.

Item 2. PROPERTIES

Our corporate headquarters, consisting of approximately 16,500 square feet, are located in Carlsbad, California. The principal executive offices of our two wholly owned subsidiaries, Rubio’s Restaurants of Nevada, Inc. and Rubio’s Promotions, Inc. are also located in Carlsbad, California. We occupy our headquarters under a lease that was extended until March 31, 2011, with options to extend the lease for an additional eight years. We lease each of our restaurant facilities with the exception of one restaurant in El Cajon, California where we own the building but lease the land. The majority of our leases are for 10-year terms and include options to extend the terms. The majority of the leases also include both fixed rate and percentage-of-sales rent provisions.

On March 24, 2005, a former employee of ours filed a California state court action alleging that we failed to provide the former employee with certain meal and rest period breaks and overtime pay. The matter was moved into arbitration, and the former employee amended the complaint to claim that the former employee represents a class of potential plaintiffs. The amended complaint alleges that current and former shift leaders who worked in our California restaurants during specified time periods worked off the clock and missed meal and rest breaks. This case is still in the pre-class certification discovery stage, and no class has been certified. The Company denies the former employee’s claims, and intends to continue to vigorously defend this action. Regardless of merit or eventual outcome, this arbitration may cause a diversion of our management's time and attention and the expenditure of legal fees and expenses. An unfavorable outcome in this matter could have a material impact on our financial position and results of operations.

In March 2007, we reached an agreement to settle a class action lawsuit filed in California state court related to how we classified certain employees under California overtime laws. The settlement agreement, which was approved by the court in June 2007, provided for an aggregate settlement payment of $7.5 million. The settlement resulted in a one-time pre-tax charge of $8.0 million in the fourth quarter of fiscal 2006, which includes the settlement amount and legal costs incurred related to this agreement. We recently learned that approximately 160 current and former employees who qualified to participate as class members in this class action settlement were not included in the settlement list approved by the court, and some number of these individuals may file claims to participate in the class action. The Company intends, during the second quarter of 2008, to file a motion requesting the court to include these individuals in the approved settlement and to provide that their claims are payable out of the aggregate settlement payment. There is no assurance that the court will grant the Company’s request.

No matter was submitted to a vote of our stockholders during the quarter ended December 30, 2007.

PART II

MARKET INFORMATION FOR COMMON STOCK

Our common stock is listed on the NASDAQ Global Market under the symbol “RUBO.” Our common stock began trading on May 21, 1999. The closing sales price of our common stock as reported on NASDAQ on March 25, 2008 was $6.48. As of March 25, 2008, there were approximately 4,069 beneficial holders of our common stock, including 298 holders of record.

The following table sets forth, for the periods indicated, the high and low closing sales prices for our common stock for each quarter of our two most recent fiscal years, as regularly reported on NASDAQ. Such quotations represent inter-dealer prices without retail markup, markdown or commission and may not necessarily represent actual transactions.

| | High | | Low | |

| 2006: | | | | | |

| First Quarter | | $ | 10.22 | | | 8.28 | |

| Second Quarter | | $ | 8.75 | | | 7.08 | |

| Third Quarter | | $ | 9.69 | | | 8.50 | |

| Fourth Quarter | | $ | 10.50 | | | 8.80 | |

| | | | | | | | |

| 2007: | | | | | | | |

| First Quarter | | $ | 11.46 | | | 9.01 | |

| Second Quarter | | $ | 12.93 | | | 10.07 | |

| Third Quarter | | $ | 11.12 | | | 9.71 | |

| Fourth Quarter | | $ | 10.99 | | | 8.33 | |

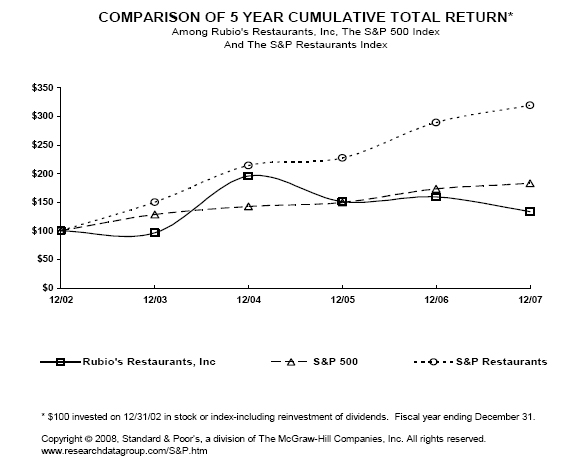

DIVIDEND POLICY