EXHIBIT 99.2

Future operating results

Global economic conditions

Subscriber growth, retention and usage levels

Fax and voice service growth

New products, services and features

Corporate spending

Liquidity

Network capacity, coverage and security

Regulatory developments

Taxes

Certain statements in this presentation constitute “forward-looking statements” within the meaning of the Private

Securities Litigation Reform Act of 1995, particularly those contained in the slide “2009 Assumptions/Guidance.” These

forward-looking statements are based on management’s current expectations or beliefs as of February 19, 2009 and

are subject to numerous assumptions, risks and uncertainties that could cause actual results to differ materially from

those described in the forward-looking statements. We undertake no obligation to revise or publicly release the results

of any revision to these forward-looking statements. Readers should carefully review the risk factors described in this

presentation. Such statements address the following subjects:

Safe Harbor for Forward-Looking Statements

All information in this presentation speaks as of February 19, 2009 and any

distribution of this presentation after that date is not intended and will not be

construed as updating or confirming such information.

Risk Factors

Inability to sustain growth in our customer base, revenue or profitability, particularly in light of the uncertain U.S. or

worldwide economy and the related impact on customer acquisitions, cancelations and credit card payment declines

Competition in price, quality, features and geographic coverage

Higher than expected tax rates or exposure to additional tax liability

Inability to obtain telephone numbers in sufficient quantities on acceptable terms in desired locations

Enactment of burdensome telecommunications or Internet regulations including increased taxes or fees

Reduced use of fax services due to increased use of email, scanning or widespread adoption of digital signatures

Inadequate intellectual property protection or violations of third party intellectual property rights

System failures or breach of system or network security and resulting harm to our reputation

Inability to adapt to technological change, or third party development of new technologies superior to ours

Loss of services of executive officers and other key employees

Inability to maintain existing or enter into new supplier and marketing relationships on acceptable terms

Other factors set forth in our Annual Report on Form 10-K filed on 02/25/2008 and the other reports filed by us from time to

time with the Securities and Exchange Commission

The following factors, among others, could cause our business, prospects, financial condition, operating results and cash flows to

be materially adversely affected:

All brand names and logos are trademarks of j2 Global Communications, Inc. or its affiliates in the U.S. and/or internationally.

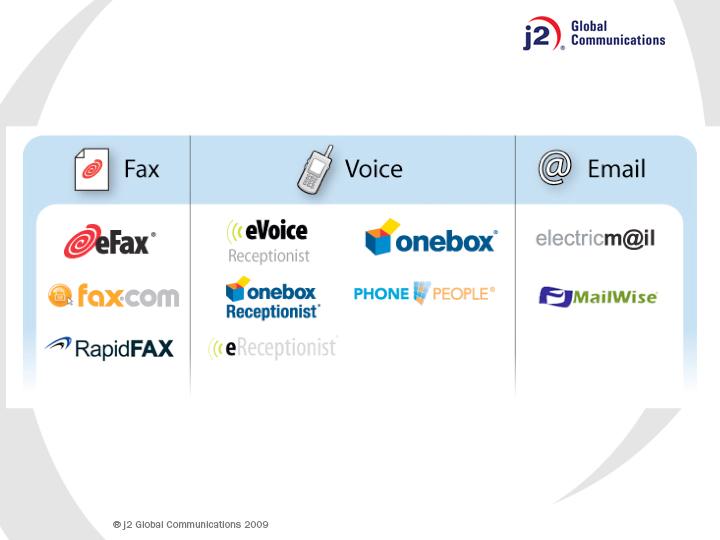

Messaging/Communications as a Service

Core j2 Global Assets

11.6+ M Subscribed Telephone Numbers (DIDs)

1.2+ M Paid DIDs

Global Advanced Messaging Network

3,100+ cities in 46 countries on 6 continents

19.8M+ unique DIDs worldwide in inventory

Intellectual Property

57 issued patents and licensing programs designed to monetize the portfolio

Protection of brands and marks

Programs designed to effectively collect evidence to prosecute junk faxers

Expertise

Effective customer acquisition strategies and Web marketing

Breadth, depth and management of a complex network & architecture

Successful acquisition and integration of 21 businesses in 7 countries

Strong Financial Position

13 consecutive years of Revenue growth

7 consecutive years of positive and growing Operating Earnings

$88M of Free Cash Flow (FY 2008)

$162M of cash & investments to fund growth/ Nominal debt related to holdback

( as of 12/31/08)

Individuals

Targeted marketing (search, online media and radio)

Sold through: eFax.com, eVoice.com, Onebox.com, PhonePeople.com, Fax.com, j2.com and

other brand Websites

Use of proprietary Life Cycle Management

Advertising, Up-selling, and Calling-Party-Pays revenue supports the Free base

Small to Mid-Sized Businesses (SMBs)

Sold through: eFax Corporate, Onebox Receptionist and eVoice Receptionist Websites

Supported by Chat and Telesales groups in U.S. and Europe (in multiple languages)

Self-service Web-based broadcast fax engine at jblast.com

Outsourced email, spam & virus protection and archiving

Use of proprietary Life Cycle Management (i.e. feature up-sell)

Enterprise (SMEs)/Large Enterprise/Government

Direct sales force in U.S. and Europe

Marketed through Web and traditional direct selling methods

Designed for > 150 DID accounts

Subscriber Acquisition

Eight Drivers for Paid DID Additions

Subscribers coming directly to the Company’s Websites/Telesales

Brand awareness driven by demand-generation programs and “word of mouth”

Search engine discovery

Accounts for over 40% of monthly paid DID signups

Free-to-Paid subscriber upgrades

Life Cycle Management

eFax Corporate SMB sales

Hybrid Website and human interaction (i.e. Telesales)

Direct SME/Enterprise/Government

Through the outside Corporate Sales team

Direct domestic marketing spend for paid subscribers

Targeted marketing program across various media

International marketing programs

Cross-sell

Offer additional services to existing customers

Acquisitions

Paid Subscription Drivers

(1) Includes SFAS 123(R) non-cash compensation expense.

(2) Includes SFAS 123(R) non-cash compensation expense, net of tax benefit. Tax rates for Q4 and full year are 24.6% and 29.0% respectively.

(3) See slide 19 for computation of free cash flow.

GAAP Results

GAAP Revenues

$60.6M

$241.5M

Gross Profit/Margin (1)

$49.4M 81.5%

$195.3M 80.9%

Operating Profit/Margin (1)

$26.2M 43.2%

$97.9M 40.6%

GAAP EPS (2)

$0.45 Per Share

$1.58 Per Share

Free Cash Flow (3)

$25.4M

$88.2M

Cash and Investments

$162M

$162M

$

Margin

Q4 2008

$

Margin

FY 2008

Fax Services

2008 Review

Fax DIDs increased to ~1,050,000

Multiple pricing programs working well

Expanded network to 46 countries and 3,100+ cities

Acquired Mijanda brands and customer base

Strong Corporate Sales 24 wins in 2008 of large customers

Aggressive ROI based management of advertising campaigns

Headwind on usage revenue and retention rates as economy weakened

Strength of USD hurt international revenues in Q3 and Q4

2009 Outlook

Leverage j2’s corporate advantages

Purchasers seeking established, profitable, trusted and well capitalized providers

Increased focus on Canada and top European countries

Continuing multiple pricing programs serving multiple segments

Leveraging analytics and experience to further optimize advertising spend

Fax indexing/other service enhancements to be fully rolled out

Continuing lighter than average usage and retention in a weak economy

Continuing focus on M&A

Voice Services

2008 Review

Voice DIDs grew 127% from ~80,000 to ~190,000; grew to ~10% of j2

revenue

Began international marketing efforts; introduced eReceptionist brand in

Europe

Speech-to-text deployed in the US

Increased Telesales staff and expanded CS support

Continued cross-selling to Fax customer base

Acquired Phone People (j2’s largest voice acquisition)

2009 Outlook

Extend market leadership position with organic and M&A growth

Continue to refine user experience and value proposition

One-click cross-sells between fax and voice customers

Testing additional enhanced features

Refine brand strategy to expand market size

Localize to support additional European languages and markets

Customer service efficiency and enhancements

Other Businesses

Successfully completed acquisition of Mailwise (hygiene provider)

Cross-sell of Electric Mail services to Mailwise customers

Integration of Mailwise nearing completion

Currently evaluating additional M&A opportunities

Patent Licensing

Patents out of reexamination in late 2008/early 2009

Opportunity to create new licensing programs and proceed with stayed

litigation

Advertising/Broadcast Fax

Impact of weakening economy

Expect softness to continue

Only 2% of j2’s revenue

j2 Operations

2008

Achieved revenues and above range EPS targets

Successfully managed cost structure for all departments

Revenues grew 9.4% while employee headcount was kept flat with 12/31/07

Increased operational efficiencies steadily throughout the year

Margins at an all time high in Q4

Improved gross margins by 1.9% from 79.6% to 81.5%

Improved operating margins by 5.9% from 37.3% to 43.2%

Effective deployment of cash through acquisitions and stock buyback

Acquired 4 companies across multiple services

2009

Continue to enhance and expand on 2008 operational excellence

Active pipeline of M&A opportunities – leverage j2’s acquisition and

integration expertise

Continue to leverage j2’s talent pool

Effective advertising programs with increased ROI focus

Prudent management of capital expenditures

Economy

2009 worse than 2008; 4 Quarters of GDP contraction; global recession; increasing

unemployment; bottom not yet reached

Stronger USD relative to GBP and Euro

Operational View

Continuing focus on optimizing margins and free cash flow

Decrease in usage revenue and retention rates

Shifting Mix to lower MARPU DIDs (Corporate, Voice and secondary Fax brands)

Increased Investment in IP

M&A/higher yielding investments for our cash

Other Items

Lower Other Income due to falling interest rates

Modestly higher share count/higher SFAS 123(R) expense

Tax rate assumed to be ~ 30.5%

2009 Assumptions/Guidance

Modest Increase in Revenues and Non-GAAP EPS

Metrics

18

Q1

Q2

Q3

Q4

Total

Q1

Q2

Q3

Q4

Total

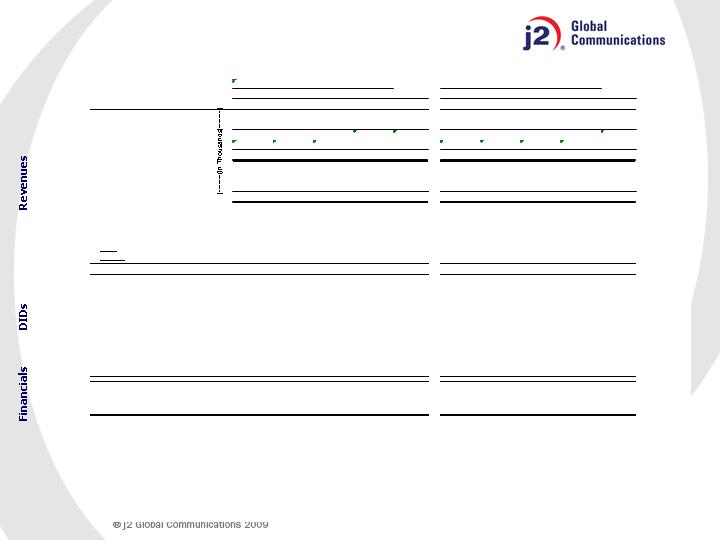

Fixed Subscriber Revenues

$37,757

$39,643

$41,362

$43,336

$162,098

$44,260

$46,593

$47,481

$48,125

$186,459

Variable Subscriber Revenues

12,536

12,970

12,667

12,057

50,231

12,956

12,943

12,985

11,497

50,382

Subscriber Revenues

$50,293

$52,613

$54,029

$55,393

212,329

$57,216

$59,536

$60,466

$59,622

236,841

Other Revenues

3,848

1,367

1,717

1,437

8,368

1,433

1,140

1,086

1,014

4,673

Total Revenues

$54,141

$53,980

$55,746

$56,830

220,697

$58,649

$60,676

$61,552

$60,636

241,513

DID - Based Revenues

$48,684

$50,929

$52,204

$53,473

$205,290

$55,301

$57,551

$58,440

$57,691

$228,983

Non-DID Based Revenues

5,457

3,051

3,542

3,357

15,407

3,348

3,125

3,112

2,944

12,529

Total Revenues

$54,141

$53,980

$55,746

$56,830

220,697

$58,649

$60,676

$61,552

$60,636

241,512

Subscriber Revenues/Total Revenues

92.9%

97.5%

96.9%

97.5%

96.2%

97.6%

98.1%

98.2%

98.3%

98.1%

DID - Based/Total Revenues

89.9%

94.3%

93.6%

94.1%

93.0%

94.3%

94.8%

94.9%

95.1%

94.8%

%

Fixed

Subscriber Revenues

75.1%

75.3%

76.6%

78.2%

76.3%

77.4%

78.3%

78.5%

80.7%

78.7%

%

Variable

Subscriber Revenues

24.9%

24.7%

23.4%

21.8%

23.7%

22.6%

21.7%

21.5%

19.3%

21.3%

Paid DIDs

(1) (2)

930,273

972,599

1,017,985

1,063,698

1,098,650

1,162,872

1,198,950

1,236,079

Average Monthly Revenue/DID

$17.16

$17.26

$16.80

$16.44

$16.30

$16.29

$15.87

$15.05

Cancel Rate

(3)

3.0%

2.8%

3.0%

2.7%

2.8%

2.9%

3.0%

3.1%

Free DIDs

10,355,815

10,671,519

10,706,503

10,874,104

10,098,143

10,233,875

10,357,506

10,362,771

Average Monthly Revenue/DID

$0.05

$0.05

$0.06

$0.07

$0.08

$0.07

$0.07

$0.06

Total DID Inventory (MM)

16.9

17.0

17.1

17.2

17.4

17.5

17.3

19.8

Cities Covered

2,884

2,933

2,950

3,024

3,084

3,126

3,137

3,135

Countries Covered

40

42

42

42

44

45

46

46

Cash & Investment

(millions)

$210.3

$233.1

$239.8

$229.8

$181.3

$149.9

$151.8

$161.9

Free Cash Flow

(4)

(millions)

$26.1

$20.6

$15.7

$21.4

$83.9

$26.9

$23.0

$12.8

$25.4

$88.2

(1)

Paid DIDs reflect a reserve for the net impact of price increase, database upgrades and database clean up.

(2)

DIDs also reflect reserves taken in conjunction with asset acquisitions for anticipated product migration and/or price increase.

(3)

Cancel Rate is defined as individual customer DIDs with greater than 4 months of continuous service (continuous service includes customer DIDs which are administratively cancelled

and reactivated within the same calendar month), and DIDs related to enterprise customers beginning with their first day of service. Cancel rate is calculated monthly and expressed here as an average

over the three months of the quarter.

(4)

Free Cash Flow is net cash provided by operating activities, less purchases of property and equipment. See slide 19 for computation of free cash flow.

Quarterly revenues for 2007 and Q1 2008 have been reclassified between fixed, variable and other revenue and between DID based and non-DID based revenue.

This reclassification is related to revised revenue classification for a j2 subsidiary, it does not impact total revenues for the quarter.

2008

2007

(1) Net cash provided by operating activities, less purchases of property & equipment. Free Cash Flow amounts are not meant as a substitute

for GAAP, but are solely for informational purposes.

Computation of Free Cash Flow

($ in millions)

Q1 '07

Q2 '07

Q3 '07

Q4 '07

Q1 '08

Q2 '08

Q3 '08

Q4 '08

Net cash from operating activities

$26.659

$23.113

$18.656

$25.779

$27.411

$23.840

$13.738

$25.727

Purch. of property & equipment

(0.529)

(2.506)

(2.940)

(4.340)

(0.469)

(0.796)

(0.937)

(0.305)

Free Cash Flow

(1)

$26.130

$20.607

$15.716

$21.439

$26.942

$23.044

$12.801

$25.422