Table of Contents

As filed with the Securities and Exchange Commission on February 25, 2016.

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Or

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

Or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Or

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from N/A to N/A

Commission file number: 001-14930

HSBC Holdings plc

(Exact name of Registrant as specified in its charter)

| N/A | United Kingdom | |

| (Translation of Registrant’s name into English) | (Jurisdiction of incorporation or organisation) |

8 Canada Square

London E14 5HQ

United Kingdom

(Address of principal executive offices)

Russell C Picot

8 Canada Square

London E14 5HQ

United Kingdom

Tel +44 (0) 20 7991 8888

Fax +44 (0) 20 7992 4880

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

Title of each class | Name of each exchange on which registered | |

| Ordinary Shares, nominal value US$0.50 each. | London Stock Exchange | |

| Hong Kong Stock Exchange | ||

| Euronext Paris | ||

| Bermuda Stock Exchange | ||

| New York Stock Exchange* | ||

American Depository Shares, each representing 5 Ordinary Shares of nominal value US$0.50 each. | New York Stock Exchange | |

6.20% Non-Cumulative Dollar Preference Shares, Series A | New York Stock Exchange* | |

American Depositary Shares evidenced by American Depositary receipts, each representing one- fortieth of a Share of 6.20% Non-Cumulative Dollar Preference Shares, Series A | New York Stock Exchange | |

| 5.10% Senior Unsecured Notes Due 2021 | New York Stock Exchange | |

| 4.00% Senior Unsecured Notes Due 2022 | New York Stock Exchange | |

| 4.875% Senior Unsecured Notes Due 2022 | New York Stock Exchange | |

| 7.625% Subordinated Notes due 2032 | New York Stock Exchange | |

| 7.35% Subordinated Notes due 2032 | New York Stock Exchange | |

| 6.5% Subordinated Notes 2036 | New York Stock Exchange | |

| 6.5% Subordinated Notes 2037 | New York Stock Exchange | |

| 6.8% Subordinated Notes Due 2038 | New York Stock Exchange | |

| 6.100% Senior Unsecured Notes due 2042 | New York Stock Exchange | |

8.125% Perpetual Subordinated Capital Securities Exchangeable at the Issuer’s Option into Non- Cumulative Dollar Preference Shares | New York Stock Exchange | |

8.00% Perpetual Subordinated Capital Securities Exchangeable at the Issuer’s Option into Non- Cumulative Dollar Preference Shares, Series 2 | New York Stock Exchange | |

4.250% Subordinated Notes due 2024 | New York Stock Exchange | |

5.250% Subordinated Notes due 2044 | New York Stock Exchange | |

| 4.250% Subordinated Notes due 2025 | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Securities Exchange Act of 1934: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Securities Exchange Act of 1934: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Ordinary Shares, nominal value US$0.50 each 19,685,096,934

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yesþ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

¨ Yesþ No.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

þ Yes¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

¨ Yes¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filerþ | Accelerated filer¨ | Non-accelerated filer¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ | International Financial Reporting Standards as issued by the International Accounting Standards Boardþ | Other ¨ |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow.

¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

¨ Yesþ No

| * | Not for trading, but only in connection with the registration of American Depositary Shares. |

Table of Contents

Table of Contents

| ||||

Strategic Report

An overview of how we are structured, what we do and where, our strategic actions, the principal risks we face, and high-level performance information. The section is introduced by both the Group Chairman and Group Chief Executive, and also explains the role of the Board.

ThisStrategic Report was approved by the Board on 22 February 2016. Douglas Flint, Group Chairman | 01a | Cautionary statement regarding forward-looking statements | ||

| 01b | Certain defined terms | |||

| 02 | HSBC at a glance | |||

| 04 | Who we are | |||

| 06 | Group Chairman’s Statement | |||

| 10 | Group Chief Executive’s Review | |||

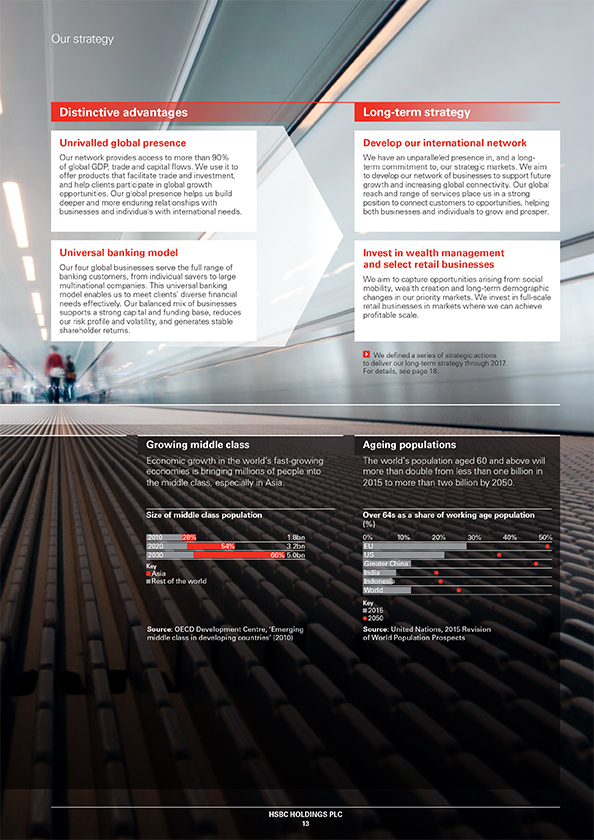

| 12 | Our strategy | |||

| 14 | Value of the network | |||

| 16 | Delivering our network to customers | |||

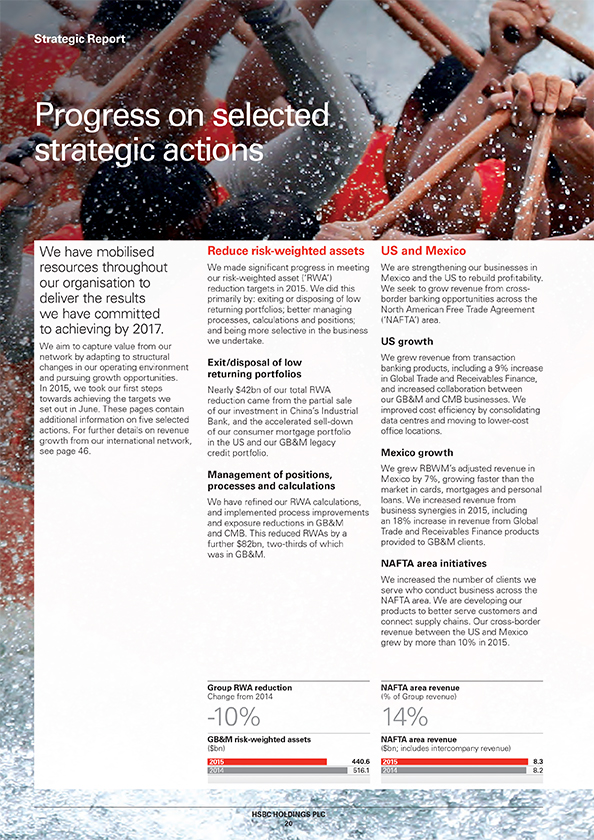

| 20 | Progress on selected strategic actions | |||

| 22 | Financial overview | |||

| 28 | Global businesses | |||

| 32 | Regions | |||

| 34 | How we do business | |||

| 39 | Our approach to tax | |||

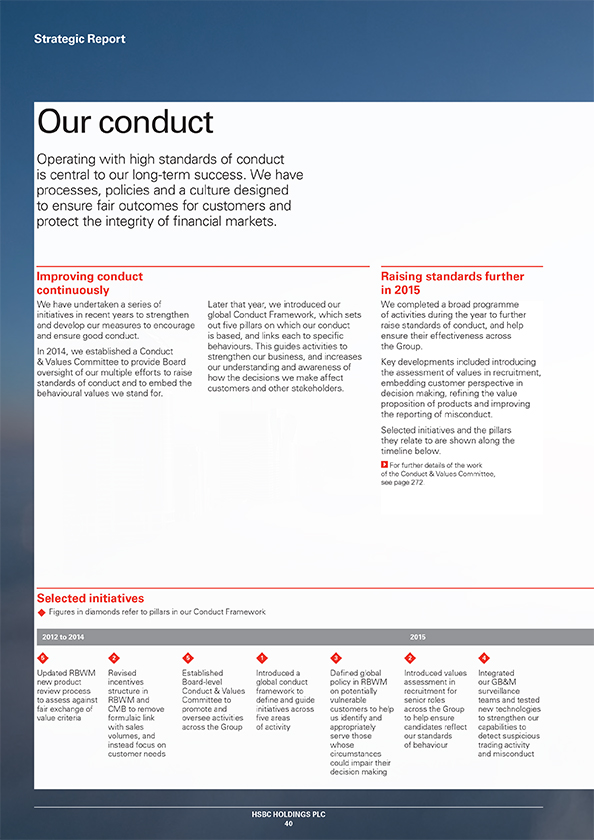

| 40 | Our conduct | |||

| 42 | Risk overview | |||

| 44

|

| |||

| ||||

Financial Review

Detailed reporting of our financial performance, at Group level as well as within our matrix structure. It also includes our full risk report and reporting on how we manage capital. | 47 | Detailed financial performance | ||

| – 48 Financial summary | ||||

| – 65 Global businesses | ||||

| ||||

| 100b | Regulation and supervision | |||

100j | Disclosures pursuant to Section 13(r) of the Securities Exchange Act | |||

101 | Risk | |||

227 |

| |||

| ||||

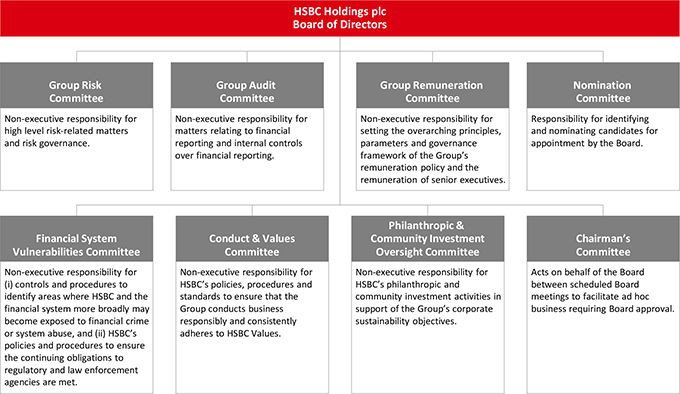

Corporate Governance

Details of our Board of Directors and senior management, and our approach to corporate governance and remuneration. | 249 | Corporate Governance Report | ||

| 249 | Biographies of Directors and senior management | |||

| 256 | Board of Directors | |||

| 262 | Board committees | |||

| 275 | Internal control | |||

| 278 | Employees | |||

| 285 | Directors’ Remuneration Report

| |||

| ||||

Financial Statements

Our financial statements and related notes and reports. | 323 | Report of Independent Registered Public Accounting Firm to the Board of Directors and Shareholders of HSBC Holdings plc only | ||

| – 323 31 December 2015 | ||||

– 335 31 December 2014

| ||||

| 336 | Financial Statements | |||

| 347 | Notes on the Financial Statements

| |||

| ||||

Other Information

Important information for our shareholders, including contact information. Like any industry and company, we have our set of abbreviations and terminology. Accordingly, we provide an explanation of the abbreviations used and a glossary of key terms.

| 470 | Shareholder information | ||

| 478g | Glossary of accounting terms and US equivalents | |||

| 479 | Abbreviations | |||

| 483 | Glossary | |||

| 491 |

| |||

HSBC HOLDINGS PLC 1 |

Table of Contents

Strategic Report

Cautionary statement regarding forward-looking statements

This Form 20-F contains certain forward-looking statements with respect to HSBC’s financial condition, results of operations, capital position and business.

Statements that are not historical facts, including statements about HSBC’s beliefs and expectations, are forward-looking statements. Words such as ‘expects’, ‘anticipates’, ‘intends’, ‘plans’, ‘believes’, ‘seeks’, ‘estimates’, ‘potential’ and ‘reasonably possible’, variations of these words and similar expressions are intended to identify forward-looking statements. These statements are based on current plans, estimates and projections, and therefore undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made. HSBC makes no commitment to revise or update any forward-looking statements to reflect events or circumstances occurring or existing after the date of any forward-looking statements.

Written and/or oral forward-looking statements may also be made in the periodic reports to the US Securities and Exchange Commission, summary financial statements to shareholders, proxy statements, offering circulars and prospectuses, press releases and other written materials, and in oral statements made by HSBC’s Directors, officers or employees to third parties, including financial analysts.

Forward-looking statements involve inherent risks and uncertainties. Readers are cautioned that a number of factors could cause actual results to differ, in some instances materially, from those anticipated or implied in any forward-looking statement. These include, but are not limited to:

| – | changes in general economic conditions in the markets in which we operate, such as continuing or deepening recessions and fluctuations in employment beyond those factored into consensus forecasts; changes in foreign exchange rates and interest rates; volatility in equity markets; lack of liquidity in wholesale funding markets; illiquidity and downward price pressure in national real estate markets; adverse changes in central banks’ policies with respect to the provision of liquidity support to financial markets; heightened market concerns over sovereign creditworthiness in over-indebted countries; adverse changes in the funding status of public or private defined benefit pensions; and consumer perception as to the continuing availability of credit and price competition in the market segments we serve; |

| – | changes in government policy and regulation, including the monetary, interest rate and other policies of central banks and other regulatory authorities; initiatives to change the size, scope of activities and interconnectedness of financial institutions in connection with the implementation of stricter regulation of financial institutions in key markets worldwide; revised capital and liquidity benchmarks which could serve to deleverage bank balance sheets and lower returns available from the current business model and portfolio mix; imposition of levies or taxes designed to change business mix and risk appetite; the practices, pricing or responsibilities of financial institutions serving their consumer markets; expropriation, nationalisation, |

confiscation of assets and changes in legislation relating to foreign ownership; changes in bankruptcy legislation in the principal markets in which we operate and the consequences thereof; general changes in government policy that may significantly influence investor decisions; extraordinary government actions as a result of current market turmoil; other unfavourable political or diplomatic developments producing social instability or legal uncertainty which in turn may affect demand for our products and services; the costs, effects and outcomes of product regulatory reviews, actions or litigation, including any additional compliance requirements; and the effects of competition in the markets where we operate including increased competition from non bank financial services companies, including securities firms; and |

| – | factors specific to HSBC, including discretionary RWA growth and our success in adequately identifying the risks we face, such as the incidence of loan losses or delinquency, and managing those risks (through account management, hedging and other techniques). Effective risk management depends on, among other things, our ability through stress testing and other techniques to prepare for events that cannot be captured by the statistical models it uses; and our success in addressing operational, legal and regulatory, and litigation challenges, notably compliance with the DPA. |

HSBC HOLDINGS PLC

1a

Table of Contents

Certain defined terms

Unless the context requires otherwise, ‘HSBC Holdings’ means HSBC Holdings plc and ‘HSBC’, the ‘Group’, ‘we’, ‘us’ and ‘our’ refer to HSBC Holdings together with its subsidiaries. Within this document the Hong Kong Special

Administrative Region of the People’s Republic of China is referred to as ‘Hong Kong’. When used in the terms ‘shareholders’ equity’ and ‘total shareholders’ equity’, ‘shareholders’ means holders of HSBC Holdings

ordinary shares and those preference shares and capital securities issued by HSBC Holdings classified as equity. The abbreviations ‘$m’ and ‘$bn’ represent millions and billions (thousands of millions) of US dollars, respectively.

HSBC HOLDINGS PLC

1b

Table of Contents

Strategic Report

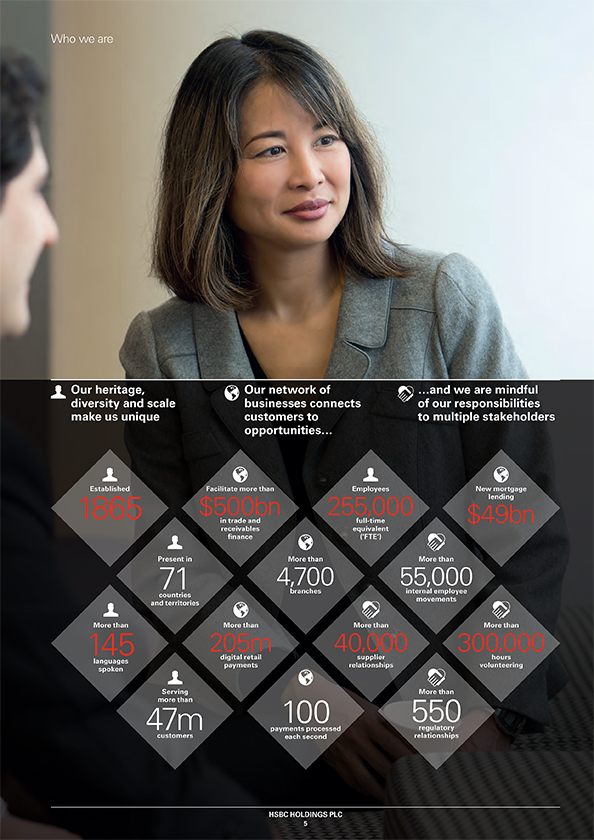

We are one of the most international banking

and financial services organisations in the world.

Group

Our operating model consists of four global businesses and five geographical regions supported by 11 global functions.

Reported profit before tax

(2014: $18.7bn)

$18.9bn

Reported revenue

(2014: $61.2bn)

$59.8bn

Key highlights

| – | We grew adjusted revenue by 1%, primarily in client-facing GB&M, CMB and Principal RBWM. |

| – | Adjusted operating expenses increased by 5% from 2014. However, costs in the second half of the year were in line with the first half as our cost saving initiatives began to take effect. |

| – | Through management initiatives, we were able to reduce risk-weighted assets (‘RWAs’) by $124bn in 2015 and therefore also the amount of capital we are required to hold. |

Adjusted profit before tax

(2014: $22.0bn)

$20.4bn

Risk-weighted assets

(2014: $1,220bn)

$1,103bn

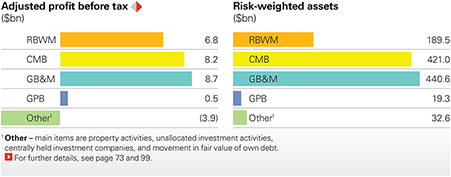

Global businesses

Our global businesses set globally consistent

business strategies and operating models.

They manage the products and business

propositions offered to our customers.

Retail Banking and Wealth Management (‘RBWM’)

|

Commercial Banking (‘CMB’)

|

Global Banking and Markets (‘GB&M’)

|

Global Private Banking (‘GPB’)

| |||

We help millions of people across the world to manage their finances, buy their homes, and save and invest for the future. Our Insurance and Asset Management businesses support all our global businesses in meeting their customers’ needs.

Further details on page 30 | We support more than two million business customers in 55 countries with banking products and services to help them operate and grow. Our customers range from small enterprises focused primarily on their domestic markets, through to large companies operating globally.

Further details on page 28 | We provide financial services and products to companies, governments and institutions. Our comprehensive range of products and solutions, across capital financing, advisory and transaction banking services, can be combined and customised to meet our clients’ specific objectives.

Further details on page 29

| We help high net worth individuals and their families to grow, manage and preserve their wealth.

Further details on page 31 | |||

Reported profit before tax |

|

|

| |||

| $5.0bn | $8.0bn | $7.9bn | $0.3bn |

HSBC HOLDINGS PLC

2

Table of Contents

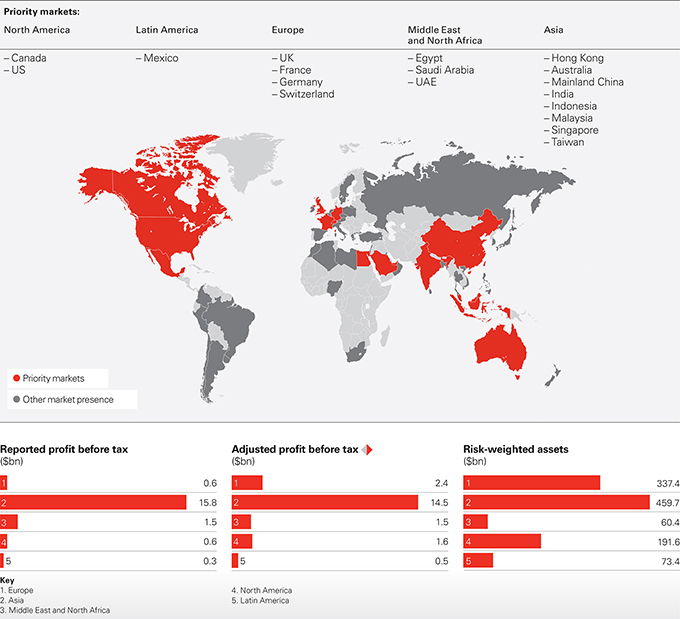

HSBC at a glance

Key metrics

Geographical regions

We operate in 71 countries and territories around the world. Our operating entities represent HSBC to customers, regulators, employees and other stakeholders. |  For further For furtherdetails on our regions, see page 32. | |

Market presence

HSBC HOLDINGS PLC

3

Table of Contents

Table of Contents

Table of Contents

Strategic Report

Statement

We enter 2016 with a clear strategy and with

a plan for its implementation already well

under way. Our diversified business model

and balance sheet strength form the foundation

for our future progress, and position HSBC

well to deal with today’s challenging economic

and financial conditions.

| 2015 was marked by some seismic shifts in global economic conditions, most notably the continuation of a sharp decline in commodity and oil prices, in part attributable to growing concerns over China’s slowing economic growth. As a consequence, monetary policy remained accommodative throughout the major developed economies and key currency interest rates remained at historically low levels. Fiscal priorities continued to focus on controlling spending, an emphasis replicated in the private sector as weak revenue growth persisted in many industries.

Against this backdrop, the Group’s financial performance in 2015 was broadly satisfactory, with reported profit before tax rising 1% to $18.9bn. On the adjusted basis used to measure management and business performance, profit before tax of $20.4bn was 7% lower than that achieved in 2014, driven by higher costs and credit charges.

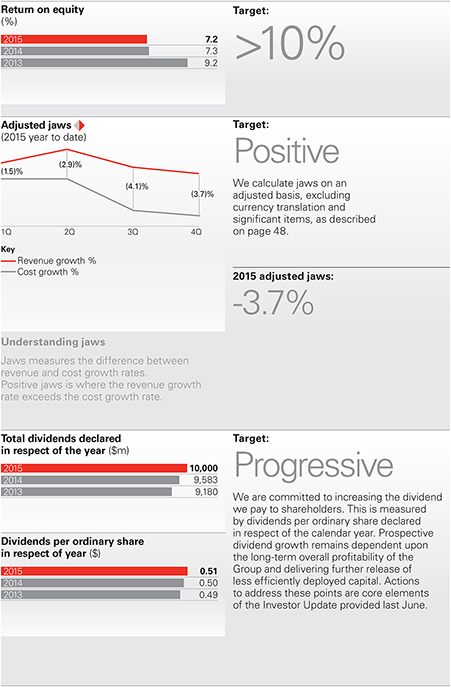

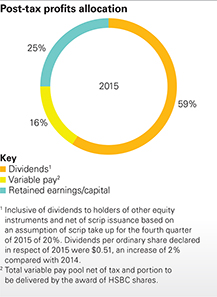

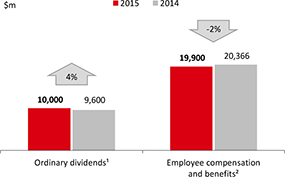

Earnings per share of $0.65 compared with $0.69 in 2014. Sound management of capital, accelerated run-off of legacy books and shrinking the balance sheet in areas that can no longer support the expanded capital requirements now in force, contributed to the common equity tier 1 ratio increasing by 0.8 percentage points to 11.9%. This capital released from managing the asset base, together with that generated from operations, allowed the Board to approve a fourth interim dividend in respect of 2015 of $0.21 per ordinary share. This took dividends per ordinary share in respect of the year to $0.51, $0.01 higher than 2014. Total dividends in respect of 2015 amounted to $10.0bn, $0.4bn higher than in respect of 2014.

In approving the dividend increase, the Board noted that prospective dividend growth remained dependent upon the long-term overall profitability of the Group and delivering further release of less efficiently deployed capital. Actions to address these points are core elements of the Investor Update provided last June. |

HSBC HOLDINGS PLC

6

Table of Contents

Group Chairman’s Statement

Sound progress on strategic initiatives

TheStrategic Report highlights delivery to date against the strategic objectives laid out in last June’s Investor Update.

When assessing management performance during 2015, outside of the financial results, the Board took particular account of the following aspects.

The successful negotiation of a majority stake in a new nationally licensed securities joint-venture in mainland China is the culmination of more than a decade of seeking out an appropriate platform through which to participate in the country’s fast-developing securities markets. Once final approvals have been received, we believe this will establish a landmark opportunity for HSBC to contribute to the development of China’s capital markets.

‘Our three major businesses generated higher revenue, notwithstanding the uncertain economic environment and the considerable reshaping necessitated by regulatory changes’

During 2015, the Group maintained, reinforced and broadened its leadership position in all aspects of the internationalisation of the renminbi. This position has been built over the past five years to establish a highly competitive platform to service China’s international trade and investment flows as it pursues the financial liberalisation and outgoing investment priorities laid out in the recent 13th five-year plan. The recent highly successful State visit to the UK, following an equally successful Economic and Financial dialogue in China, served to illustrate the huge potential for mutually beneficial cooperation between the UK and China from which HSBC is uniquely positioned to benefit in the realm of financial services.

The disposal of our Brazilian operations, which is expected to complete shortly, was both timely and well executed. This divestment was a key element of the Board’s desire to simplify the Group and redeploy capital to geographic areas where we have greater competitive strength, most particularly in Asia.

Our three major businesses generated higher revenue, notwithstanding the uncertain economic

environment and the considerable reshaping necessitated by regulatory changes. Global Banking and Markets and Retail Banking and Wealth Management, in particular, have made significant changes to their business models and are now beginning to see the benefits. Commercial Banking continued to leverage the value of the Group’s international network and product capabilities. Global Private Banking, chastened by the exposure of historical failings in Switzerland, accelerated disposal of a number of customer portfolios as it refocused its business model on core customer segments within a fully transparent operating model.

Across all businesses, the Board recognised a heightened emphasis on customer focus, which permeated recruitment, training, product design and incentives. This is essential to the restoration of trust.

Finally, and underpinning the above, we made further progress embedding the standards now expected to protect customers and the financial system from bad actors and financial crime. We are, however, not yet where we need to be. There is still more investment to make with ever greater urgency as more and more activity takes place digitally through multiple channels and via increasingly sophisticated mobile devices. HSBC’s determination to address emerging risks and identify bad actors remains resolute. The Board has made it one of its top priorities to oversee and ensure management’s delivery of the necessary enhancements to customer and transaction screening systems.

The regulatory landscape has

become clearer

The second half of 2015 saw completion of some of the most important and complex initiatives undertaken to repair the fault lines that contributed to the global financial crisis. International agreement was reached on the amount of total loss-absorbing capacity that global systemically important banks, such as HSBC, need for orderly resolution, without risks to public funds. This allowed the Financial Stability Board to report to G20 leaders that they had finalised the tools needed to end ‘too big to fail’ in the banking sector. There is still much to do to build these tools into national legislative and regulatory frameworks; however, this international agreement is an important step forward towards finally settling the capital base against which we can assess our target returns.

HSBC HOLDINGS PLC

7

Table of Contents

Strategic Report |Group Chairman’s Statement

There is now broad agreement that the implementation of the suite of regulatory reforms introduced post-crisis has made the financial system more resilient. Accordingly, public policy priorities are now focusing on harnessing this greater strength and resilience to support economic growth, which we welcome.

Concentration within the current regulatory agenda is increasingly on new and emerging risks and vulnerabilities. There is growing industry participation in dialogue around these emerging threats, most notably regarding cyber risk, the changing liquidity dynamics resulting from more market-based finance and financial exclusion stemming from excessive risk aversion.

Likewise, addressing the root causes of the misconduct issues that have bedevilled our industry in recent years has led to growing cooperation arising out of the multiplicity of joint working groups and enquiries that have examined the most serious failings. 2016 sees the introduction of the new Senior Managers’ Regime in the UK, which will reinforce individual responsibility and accountability, which we welcome.

Also in the UK, 2015 saw further clarity given to the operation of the ‘ring-fenced’ bank structure and a welcome announcement of a reduction in the scope and rate of the bank levy going forward.

It is too early to say whether this amounts to a new understanding between the industry and the public, but it is encouraging that the industry is once again gaining a voice at a time of great economic and geopolitical uncertainty. We can only fulfil our essential role if we have regained trust, a fact that is now fully understood.

Review of headquarters’ location

As we announced last week, the Board concluded its review of domicile alternatives and decided unanimously to remain headquartered in the UK. As we evaluated jurisdictions against the specified criteria, it became clear that the combination of our strategic focus on Asia and maintaining our hub in one of the world’s leading international financial centres, London, was not only compatible, but offered the best outcome for our customers and shareholders. This decision was taken after some 10 months of careful analysis and assessment of geopolitical, economic, regulatory and financial factors. Advice was taken from internationally respected experts and from leading financial advisers. After considering all the relevant factors, the Board concluded that having our headquarters in the UK and our significant business in Asia Pacific led from Hong Kong, delivers the best of both worlds to our stakeholders. The completion of this review closes out one of the 10 strategic actions set out at our Investor Update last June. | Board changes

Subsequent to the changes announced with our interim results, we have made further changes to the Board. Safra Catz stepped down from the Board at the end of 2015 and Sir Simon Robertson, our Deputy Chairman, and Rona Fairhead will retire at the forthcoming Annual General Meeting.

| |||||

‘There is now broad agreement that the implementation of the suite of regulatory reforms introduced post-crisis has made the financial system more resilient’

| ||||||

Safra served on the Board for nearly eight years while Simon and Rona are HSBC’s longest serving non-executive Directors, having served for close to 10 and 12 years, respectively. Over their respective periods of service, they have made invaluable contributions to the Group, not least during the global financial crisis, for which the Board is extremely grateful. Their combined expertise and experience in matters of governance, audit and risk, remuneration, technology, and international business affairs has been invaluable to HSBC and they will, upon their retirement, be sorely missed. On behalf of shareholders and the Board, I want to take this further opportunity to recognise their immense contributions to HSBC.

The Board was delighted to announce the appointments of Paul Walsh and Henri de Castries as independent non-executive Directors. Paul joined the Board on 1 January 2016 and Henri’s appointment takes effect from 1 March 2016.

Paul Walsh was Group CEO of Diageo plc between 2000 and 2013. Under his leadership, Diageo was refocused from a diversified food, beverage and hotels conglomerate into one of the world’s leading global alcoholic beverage businesses. In building this position, Paul took Diageo from a largely European and US business into emerging markets and to global leadership through the acquisition of many of the world’s leading brands.

Henri de Castries has more than 25 years of international experience in the finance industry. Henri has been Chairman and Chief Executive Officer of AXA, one of the world’s leading global insurance and asset management companies since April 2010 after serving as Chairman of its Management Board from May 2000.

Their international experience and track record in leading the reshaping of growing businesses, including undertaking business portfolio realignments, will be of great value to the Board as we address the opportunities and challenges ahead. | ||||||

HSBC HOLDINGS PLC

8

Table of Contents

Group Chairman’s Statement

Looking back – our 150th anniversary

In 2015, HSBC marked its 150th anniversary by recognising its staff for their essential contributions through the ages, and its customers for their shared commitment and loyalty. As we enter the next period of our history, I want to reiterate these messages of gratitude and underline our recognition that such commitment and loyalty have to be earned.

HSBC has also always recognised its responsibilities to the communities it serves and so in this special year committed $150m of additional funding to community projects around the world over three years.

We also wanted to identify a distinctive cause with global significance to mark our special anniversary.

‘We enter 2016 with a clear strategy and with much of the Group’s required reshaping completed or under way’

We were delighted, therefore, to announce a partnership with Cancer Research UK to support the scientific leaders of tomorrow through a $25m contribution towards the development and construction of the Francis Crick Institute. This state-of-the-art biomedical research facility will open in the heart of London in 2016 and support more than 1,200 scientists, collaborating to tackle the diseases that pose the greatest threat to humanity – cancer, heart disease, lung disease and infectious diseases, including HIV and malaria.

To mark HSBC’s support, 150 PhD students, selected from across the world, will have the opportunity to conduct vital research at the new institute.

Looking ahead

Current market conditions are inevitably concentrating attention on the risks that exist within the global economy. It is, however, important also to recognise again the resilience that our diversified business model and balance sheet strength provide, as well as noting the many counterbalances that should help to underpin the global economy.

China’s slower economic growth will undoubtedly contribute to a bumpier financial environment, but it is still expected to be the largest contributor to global growth as its economy transitions to higher added value manufacturing and services and becomes more consumer driven. This transition is driving our focus on the Pearl River Delta as a priority growth opportunity given its concentration of high tech, research focused and digital businesses.

There is a real possibility of meaningful stimulus for the global economy to come from further trade liberalisation initiatives such as the Trans-Pacific Partnership agreement, which was signed earlier this month.

The global focus on infrastructure development, most notably the Belt and Road initiative in China and the Juncker plan in Europe will expand public/ private financing opportunities.

Similarly, the agreements reached on climate change at the recent COP21 conference in Paris will require further significant infrastructure renewal. They will also greatly expand the market for sustainable financing options such as green bonds where HSBC is a leading participant. Reinforcing this position, the Group recently committed $1bn to a green bond portfolio to fund projects in sectors such as renewable energy, energy efficiency, clean transportation and climate change adaption as well as SME financing in sectors such as public transport, education and healthcare.

Technology advancements in financial services are broadening access, improving customer service and lowering the costs of service delivery. At the same time, the amount of data held digitally is exploding, reinforcing the need to bolster cyber security. There is an urgent public policy need to clarify how responsibility is to be shared, given the growing number of routes through which customers can authorise movement of money from their accounts or the sharing of data within these accounts.

We enter 2016 with a clear strategy and with much of the Group’s required reshaping completed or under way. Our 264,000 staff, like their predecessors, went the extra mile consistently throughout 2015 to meet the demands placed on them by our customers, regulators and the public. I want to place on the record the Board’s appreciation of that commitment and our gratitude for what they have achieved to make HSBC fit for the next 150 years.

Douglas Flint

Group Chairman

22 February 2016

HSBC HOLDINGS PLC

9

Table of Contents

Strategic Report

Group Chief Executive’s Review

HSBC is better balanced, better connected and better placed to capitalise on higher return businesses than it was 12 months ago.

Business performance

Our performance in 2015 again demonstrated the fundamental strength of our business. Targeted investment, prudent lending and our diversified, universal banking business model helped us achieve revenue growth in a difficult market environment whilst also reducing risk-weighted assets.

We also started to implement the actions that we announced at our Investor Update in June to adapt HSBC to new operating conditions. Completing these plans will refocus the business to achieve stronger, sustainable growth and we are acting on them quickly and efficiently.

On an adjusted basis, we grew revenue over the course of the year. Global Banking and Markets performed strongly and Commercial Banking grew steadily in spite of slower trade. Principal Retail Banking and Wealth Management also grew following a strong Wealth Management performance in the first half. Global Private Banking grew in Asia, but was down overall due to the impact of the continued repositioning of the business.

Our adjusted operating expenses increased as we continued to strengthen our compliance capability whilst also investing for growth. However, a combination of strict cost management and the cost reduction programmes that we started in the middle of the year helped us keep second half costs flat relative to the first half, excluding the bank levy.

Loan impairment charges remained generally low despite an increase in provisions towards the end of the year. This demonstrates again our prudent approach to lending and the benefit of our de-risking measures since 2011.

In total, we generated $11.3bn of capital in 2015, which enabled us to increase the dividend and strengthen the common equity tier 1 ratio.

HSBC HOLDINGS PLC

10

Table of Contents

Group Chief Executive’s Review

Adapting HSBC

The plans that we announced at our Investor Update are designed to grow income, reduce costs and thereby increase our return on equity. There is a lot to do to achieve our targets but we have made a good start.

Reducing our risk-weighted assets (‘RWAs’) is vital to achieving a better return for shareholders. In 2015, management action reduced RWAs by $124bn, which takes us nearly half-way towards our target to be achieved by the end of 2017. Much of this reduction came from Global Banking and Markets, although a large proportion also came from Commercial Banking, accelerated asset sales in our US Consumer and Mortgage Lending portfolio and the sale of our investment in Industrial Bank. We expect to deliver further RWA reductions in 2016, in addition to a decrease of around $33bn from the sale of our business in Brazil.

‘The plans that we announced at our Investor Update are designed to grow income, reduce costs and increase our return on equity. There is a lot to do to achieve our targets but we have made a good start’

We have received a number of offers for our business in Turkey since June, none of which were deemed to be in the best interests of shareholders. We have therefore decided to retain and restructure our Turkish operations, maintaining our wholesale banking business and refocusing our retail banking network. This will provide better value for shareholders and continue to allow our clients to capitalise on HSBC’s international footprint.

Our cost-reduction measures are already having an impact on our cost base and HSBC is now a leaner business than at the half-year. All of our initiatives to reduce costs are under way and we expect further progress in 2016.

We continued to redevelop our businesses in the US and Mexico over the course of 2015. These are important businesses in the context of the wider Group and we are committed to turning them around. An increase in cross-border business across the NAFTA area and improved collaboration between global businesses helped to generate increased revenue. They remain works in progress.

We are investing in areas of the business that extract the greatest gain from our international network and market-leading strength in Asia.

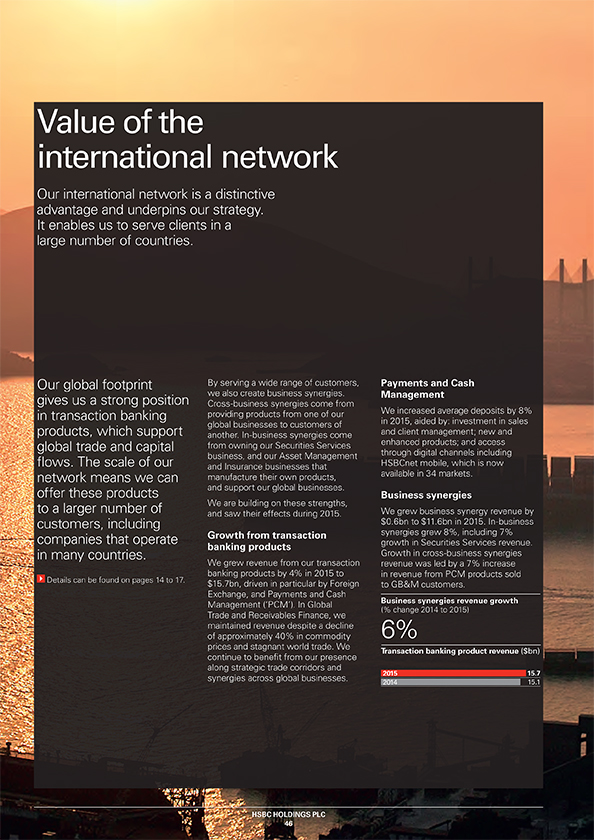

Investment in flagship transaction banking products helped to increase our market share, particularly in Payments and Cash Management, Foreign Exchange and Securities Services.

The development of our Asia businesses is gaining momentum and we achieved growth in excess of GDP in seven out of eight of our priority Asia markets.

We continue to expand our business in the Pearl River Delta and reached a number of milestones in 2015, including the signing of an agreement to form the first majority foreign-owned securities company in mainland China. When approved, this will allow us to engage in the full spectrum of securities business in the country.

We remain the world’s number one bank for offshore renminbi services and increased revenue by 3% year-on-year in this vitally important growth market.

Summary and outlook

HSBC is better balanced, better connected and better placed to capitalise on higher return businesses than it was 12 months ago. Our universal banking model is generating higher income from collaboration between businesses and our operating expenses and capital ratio are trending in the right direction. Maintaining these trends while boosting revenue will be the principal challenge in the year ahead.

The current economic environment is uncertain, but our diversified banking model, low earnings volatility and strong capital generation give us strength and resilience that will stand us in good stead.

We remain focused on delivering our nine remaining strategic actions by the end of 2017.

Stuart Gulliver

Group Chief Executive

22 February 2016

HSBC HOLDINGS PLC

11

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Strategic Report

This page is intentionally left blank

HSBC HOLDINGS PLC

18

Table of Contents

This page is intentionally left blank

HSBC HOLDINGS PLC

19

Table of Contents

Table of Contents

Table of Contents

Strategic Report

Reported results

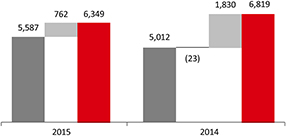

This table shows our reported results for | Reported results | 2015 | 2014 | 2013 | ||||||||||

| $m | $m | $m | ||||||||||||

| Net interest income | 32,531 | 34,705 | 35,539 | |||||||||||

| Net fee income | 14,705 | 15,957 | 16,434 | |||||||||||

| Net trading income | 8,723 | 6,760 | 8,690 | |||||||||||

| Other income | 3,841 | 3,826 | 3,982 | |||||||||||

| Net operating income before loan impairment charges and other credit risk provisions (revenue) | 59,800 | 61,248 | 64,645 | |||||||||||

Loan impairment charges and other credit risk provisions (‘LICs’) | (3,721 | ) | (3,851 | ) | (5,849 | ) | ||||||||

| Net operating income | 56,079 | 57,397 | 58,796 | |||||||||||

Total operating expenses | (39,768 | ) | (41,249 | ) | (38,556 | ) | ||||||||

| Operating profit | 16,311 | 16,148 | 20,240 | |||||||||||

Share of profit in associates and joint ventures | 2,556 | 2,532 | 2,325 | |||||||||||

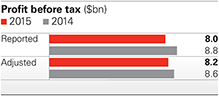

| Profit before tax | 18,867 | 18,680 | 22,565 | |||||||||||

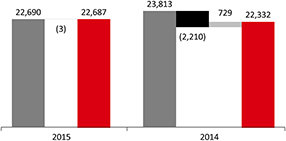

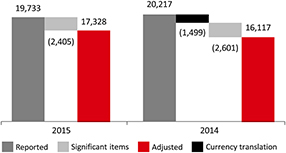

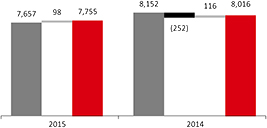

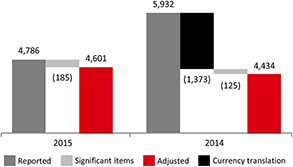

Reported profit before tax

Reported profit before tax was $18.9bn, up by $0.2bn or 1% from 2014. This was driven by a favourable movement in significant items of $2.6bn partly offset by $0.9bn of adverse effects of foreign currency translation between the years. The favourable movement in significant items included lower fines, settlements, UK customer redress and associated provisions (down by $1.3bn in total) and a gain on the partial disposal of Industrial Bank ($1.4bn).

Excluding the effects of significant items and currency translation, profit before tax was down by 7% from 2014. We describe the drivers of our performance under ‘Adjusted performance’ on page 23.

Reported revenue

Revenue of $59.8bn was $1.4bn or 2% lower than in 2014. Revenue benefited from a favourable movement in significant items but this was more than offset by the adverse effect of currency translation of $4.8bn between the years.

Significant items affecting revenue in 2015 included:

| – | a $1.4bn gain on the partial sale of our shareholding in Industrial Bank; |

| – | lower provisions and charges relating to the ongoing review of compliance with the Consumer Credit Act in the UK ($0.6bn lower than in 2014); and |

| – | an increase in favourable movements on our own debt designated at fair value from changes in credit spreads of $0.6bn. |

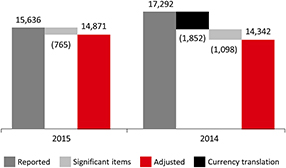

Reported LICs

Loan impairment charges and other credit risk provisions (‘LICs’) of $3.7bn were $0.1bn or 3% lower than in 2014, reflecting the favourable impact of currency translation between the years.

Reported operating expenses

Operating expenses of $39.8bn were $1.5bn or 4% lower than in 2014. This reduction primarily reflected the favourable effect of currency translation of $3.3bn between the years.

The total of significant items was broadly in line with 2014, although there were notable movements as follows:

| – | lower provisions and charges relating to UK customer redress ($0.7bn lower than in 2014); and |

| – | the non-recurrence of a charge of $0.6bn in 2014 relating to a settlement with the US Federal Housing Finance Agency; broadly offset by |

| – | settlements and provisions in connection with legal matters ($0.5bn higher than in 2014); and |

| – | costs-to-achieve relating to business transformation of $0.9bn in 2015 (for further details, see page 58). |

Reported income from associates

Income from associates of $2.6bn was in line with 2014.

HSBC HOLDINGS PLC

22

Table of Contents

Financial overview

Adjusted performance

Our reported results are prepared in accordance with IFRSs as detailed in the Financial Statements on page 347. We also present adjusted performance measures as we believe these help explain our performance and these are highlighted with the following symbol:

To arrive at adjusted performance, we adjust for:

| – | the year-on-year effects of foreign currency translation; and |

| – | the effect of significant items that distort year-on-year comparisons and are excluded in order to understand better the underlying trends in the business. |

For reconciliations of our reported results to an adjusted basis, including lists of significant items, see pages 66–67 and 77–78.

Adjusted results

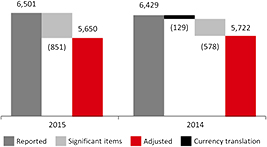

This table shows our adjusted results for 2015. | Adjusted results | 2015 | 2014 | |||||||

| $m | $m | |||||||||

| Net operating income before loan income charges and other credit risk provisions (revenue) | 57,765 | 57,227 | ||||||||

| Loan impairment charges and other credit risk provisions (‘LICs’) | (3,721 | ) | (3,168 | ) | ||||||

| Total operating expenses | (36,182 | ) | (34,576 | ) | ||||||

| Operating profit | 17,862 | 19,483 | ||||||||

| Share of profit in associates and joint ventures | 2,556 | 2,493 | ||||||||

| Profit before tax | 20,418 | 21,976 | ||||||||

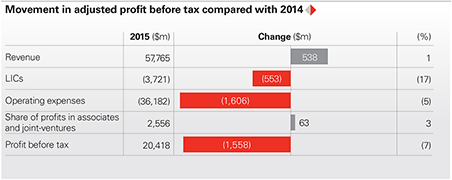

Adjusted profit before tax

| – | Our adjusted profit before tax fell by $1.6bn or 7%. |

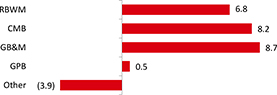

| – | We grew adjusted revenue by $0.5bn or 1%, notably in GB&M (up by $1.2bn or 7%), CMB (up by $0.4bn or 3%) and Principal RBWM, which is our RBWM business excluding the US run-off |

| portfolio (up by $0.4bn or 2%). These increases were partly offset in GPB (down by $0.1bn or 6%) and Other (down by $0.3bn). |

| – | Our LICs were $0.6bn or 17% higher than in 2014, primarily due to increases in CMB ($0.5bn) and RBWM ($0.3bn), partly offset by a reduction in GB&M ($0.3bn). |

| – | Our adjusted operating expenses increased by $1.6bn or 5%. Excluding the bank levy, operating expenses in the second half of 2015 were broadly in line with the first half of the year. This was despite investment and inflationary pressures, and partly reflects the initial effect of our cost saving initiatives as well as a strong focus on cost management. |

HSBC HOLDINGS PLC

23

Table of Contents

Strategic Report | Financial overview

| Adjusted performance (continued) | ||||

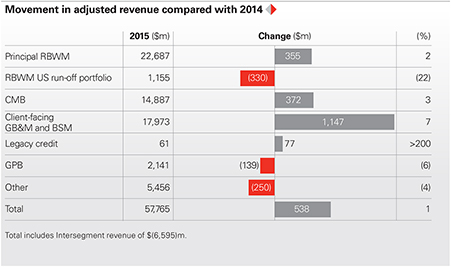

Adjusted revenue

Adjusted revenue rose by 1% in part due to growth in GB&M, CMB and Principal RBWM reflecting the following:

– GB&M: Revenue of $18.0bn was $1.2bn or 7% higher than in 2014. This was driven by higher revenue in all client-facing businesses except Principal Investments. In Equities, revenue increased by $0.5bn, reflecting higher client flows and increased market volatility. Revenue from transaction banking products rose $0.4bn as volatility drove higher client flows in Foreign Exchange, as assets under custody in Asia rose in Securities Services, and as deposits rose in Payments and Cash Management (‘PCM’). Revenue was also higher in Balance Sheet Management (‘BSM’), rising $0.1bn. |  | |||

– CMB: We grew revenue by $0.4bn or 3%, in particular in Credit and Lending (up by $0.4bn) and PCM (up by $0.1bn). This growth was mainly in Hong Kong and the UK, reflecting average balance sheet growth. In Hong Kong, lending balance growth was primarily in 2014 and the first half of 2015. Balances were broadly unchanged for the remainder of 2015 reflecting subdued demand for credit. In Global Trade and Receivables Finance, performance was resilient (revenue down $44m or 2%) despite a significant decline in commodity prices (approximately 40%) and stagnant world trade.

– RBWM: Our revenue was broadly unchanged from 2014. We continued to reduce the size of the balances in our US Consumer and Mortgage Lending (‘CML’) run-off portfolio, resulting in a fall in revenue of $0.3bn. However, in our Principal RBWM | business, revenue was higher (up by $0.4bn or 2%). This was driven by increased Wealth Management revenue in Asia (up by $0.2bn) in the first half of 2015, from growth in investment distribution, which more than offset weaker investor sentiment in the second half of 2015. There was also growth in Europe (up by $0.3bn), notably from insurance manufacturing. We also increased our current account, savings and deposit revenue by $0.1bn, notably in Hong Kong and the UK, from an increase in customer deposit balances of $32bn. This was partly offset by a decrease in Personal Lending revenue of $0.3bn, primarily from lower overdraft fees in the UK after the introduction of a text message alert service in late 2014. | – GPB: Our revenue fell by $0.1bn or 6% reflecting lower brokerage and account services fee income from a managed reduction in client assets. However, revenue increased in Asia, notably in the first half of 2015, due to higher client activity as a result of stock market performance.

– Other: Revenue was $0.3bn or 4% lower, reflecting adverse hedging ineffectiveness movements compared with favourable movements in 2014 (a net adverse movement of $0.2bn), together with the non-recurrence of a gain on the external hedging of an intra-Group financing transaction of $0.2bn. In addition, dividend income was $0.1bn lower following the partial sale of our shareholding in Industrial Bank. | ||

HSBC HOLDINGS PLC

24

Table of Contents

Financial overview

| Adjusted performance (continued) | ||||

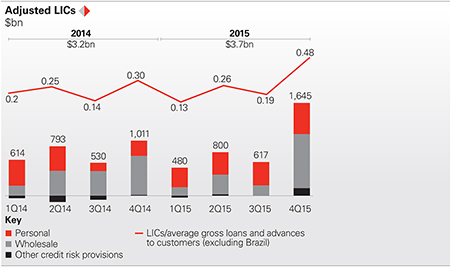

Adjusted LICs

– Our LICs were $0.6bn or 17% higher than in 2014, mainly in CMB ($0.5bn). This included a fourth quarter increase in specific LICs in a small number of countries, largely reflecting local factors, as well as LICs related to oil and gas.

– LICs increased in RBWM by $0.3bn, mainly in Brazil as delinquency rates increased; while in the UAE, impairments on mortgages rose, following a review of the quality and value of collateral.

– In GB&M, there was a reduction of $0.3bn in specific impairments as 2014 included a small number of significant charges, notably in Brazil and Hong Kong.

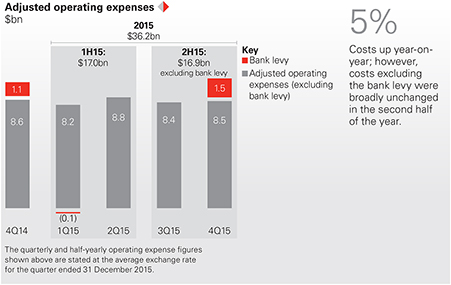

Adjusted operating expenses

– Our adjusted operating expenses in 2015 were up $1.6bn or 5% on 2014.

– Run-the-bank costs rose by $0.8bn or 2%. This was mainly due to wage inflation in Latin America and Asia. We also recruited additional staff across the Group to support business growth.

– Change-the-bank costs rose by $0.5bn or 16% on 2014. This reflected investment in regulatory programmes and compliance, including infrastructure and systems.

– The bank levy of $1.4bn was $0.4bn or 34% higher than in 2014. Excluding the bank levy, adjusted operating expenses in the second half of 2015 were broadly in line with the first half of the year. This was despite investment and inflation, and reflected the initial effect of our cost-saving initiatives and a strong focus on cost management. This included a reduction in full-time equivalent staff in the second half of the year of 4,585 and lower travel costs. |

| |||

|

Adjusted income from associates

– Our share of profit from associates and joint-ventures was broadly unchanged in 2015. The majority of this profit was from our investments in Bank of Communications Co. (‘BoCom’) and The Saudi British Bank. | |||

HSBC HOLDINGS PLC

25

Table of Contents

Strategic Report | Financial overview

Balance sheet and capital strength

| Balance sheet strength

Total reported assets were $2.4 trillion, 8.5% lower than at 31 December 2014. On a constant currency basis, total assets were $91bn or 4% lower. This reduction in part reflects the efficient use of our balance sheet to maximise shareholder returns.

We are focused on reducing our use of the balance sheet in areas that are capital intensive relative to returns. This provides capacity for growth in higher returning business areas and regions. For example, in GB&M, we have reduced trading assets by decreasing holdings of debt securities in our Rates business in Europe and North America.

Capital strength

We manage our capital in an effort to ensure we exceed current regulatory requirements and are well placed to meet those expected in the future.

We monitor our position by using capital ratios. These measure capital relative to a regulatory assessment of risks taken. We quantify how these risks relate to our businesses using risk-weighted assets. Details of these risks are included on page 227.

Our common equity tier 1 (‘CET1’) ratio at 31 December 2015 was 11.9%, up from 11.1% at 31 December 2014.

Distributable reserves

The distributable reserves of HSBC Holdings plc at 31 December 2015 were $47bn, and at 31 December 2014 were $49bn. |

HSBC HOLDINGS PLC

26

Table of Contents

Financial overview

|

Delivering on our Group financial targets

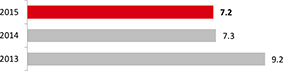

| Return on equity

Our medium-term target is to achieve a return on equity (‘RoE’) of more than 10%. This target is modelled on a CET1 ratio in the range of 12% to 13%.

In 2015, we achieved an RoE of 7.2% compared with 7.3% in 2014. The bank levy and significant items, such as fines, penalties, customer redress and associated provisions, had a significant effect on our 2015 RoE, reducing the return achieved by 190 basis points.

Adjusted jaws

Our target is to grow revenue faster than operating expenses on an adjusted basis. This is referred to as positive jaws. In 2015, we grew adjusted revenue by 0.9% whilst our adjusted operating expenses rose by 4.6%.

Jaws was therefore negative 3.7%. Jaws for 2015 was affected by the revenue performance in the second half of the year. Adjusted revenue growth in the first half of 2015 was 4.5% but fell in the second half of 2015, reflecting the economic environment, including slowing GDP growth in China. This resulted in overall revenue growth of 0.9% for 2015.

The increase in adjusted operating expenses in 2015 included a $0.4bn rise in the bank levy (to $1.4bn). Excluding this increase, jaws in 2015 would have been negative 2.8%. During the second half of 2015, we made progress on our cost saving plans set out at our Investor Update. We reduced the growth rate in adjusted operating expenses, down from 7.3% in the first half of 2015 to 4.7% for the year.

Progressive dividend

In 2015, we increased the dividends per ordinary share in respect of the year to $0.51 from $0.50 in 2014. |

HSBC HOLDINGS PLC

27

Table of Contents

Strategic Report

We manage our products and services

globally through four global businesses.

For further details on the financial performance

of our global businesses, see pages 68 to 73.

Commercial Banking (‘CMB’)

Customers

CMB serves more than two million customers in 55 countries and territories. Our customers range from small enterprises focused primarily on their domestic markets through to corporates operating globally.

We have been simplifying our product range and services to meet clients’ needs better. Since 2013, we have reduced the number of products we offer around the world from 975 to fewer than 410. We have also completed role-specific conduct training for more than 20,000 employees to help ensure that products are sold appropriately.

Products and services

We support our customers with tailored financial products and services to allow them to operate efficiently and to grow. This includes providing them with working capital, term loans, payment services and international trade facilitation, among other services. We offer expertise in mergers and acquisitions, and provide access to financial markets. | In 2015, the quality of our service was recognised by several leading awards. For the fourth consecutive year, we were recognised as the Best Global Cash Manager (for Non-Financial Institutions) in theEuromoney Cash Management survey. We were also recognised as the Best Overall Global Trade Finance Bank, among other awards, in theTrade Finance Awards for Excellence.

Business synergies

CMB is at the centre of business synergies within the Group, enabling nearly $6bn of business synergy revenue in 2015. For example, it provides trade finance, working capital and liquidity management solutions to GB&M clients. It also provides Capital Finance expertise, and Insurance and Asset Management capabilities from across the Group to benefit customers.

Areas of focus

We are focused on creating value from our network, which covers 90% of global trade and capital flows. We are therefore investing in digital and technology aspects of our core Payments and Cash Management (‘PCM’), and Global Trade and Receivables Finance propositions, as well as in the Pearl River Delta, ASEAN and NAFTA growth areas.

We achieved significant risk-weighted asset efficiencies through management initiatives in 2015 and continue to ensure our capital is deployed effectively. | Continued revenue growth in Hong Kong and the UK

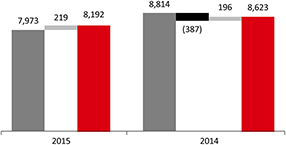

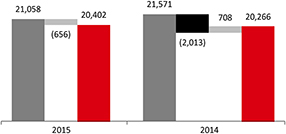

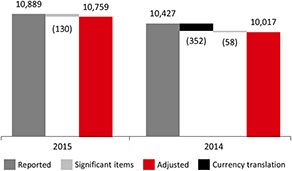

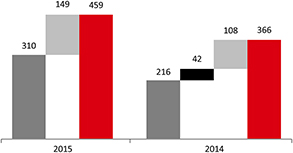

– Adjusted profit before tax of $8.2bn was $0.4bn or 5% lower than in 2014, as revenue growth was more than offset by a rise in LICs and higher costs.

– We grew revenue by $0.4bn or 3%, in particular in Credit and Lending, and PCM. This was mainly in Hong Kong and the UK, reflecting average balance sheet growth, although demand for credit in Hong Kong was subdued in the second half of 2015, with balances remaining broadly unchanged.

– LICs were $0.5bn or 36% higher, reflecting enhanced credit risk in the oil and gas sector, notably in North America, Asia, and Middle East and North Africa. In addition, we raised LICs against a small number of specific clients in Indonesia, the UAE and the UK.

– Costs increased by $0.4bn or 6%, notably in Asia and the US, due to wage inflation and investment in growth initiatives, regulatory programmes and compliance.

– Management initiatives set out in our Investor Update in June 2015 contributed a reduction in risk-weighted assets (‘RWAs’) of $23.0bn or more than 75% of our 2015–2017 target.

Adjustedprofit before tax -5% | ||

HSBC HOLDINGS PLC

28

Table of Contents

Global businesses

Global Banking and Markets (‘GB&M’)

Customers

GB&M supports major government, corporate and institutional clients worldwide in achieving their long-term strategic goals through tailored and innovative solutions. Our deep sector expertise extends across transaction banking, financing, advisory, capital markets and risk management. We serve nearly 4,000 clients in more than 50 countries and territories, helping them to realise opportunities in the markets that matter to them.

We continue to strengthen the services we provide and our relationships with clients. We regularly assess these relationships, using benchmarking and internal programmes. As a result, in 2015 we improved the on-boarding experience for clients and enabled relationship bankers to spend more time understanding clients’ needs. Customer feedback allows us to identify opportunities to further improve our business and the wider client experience.

Products and services

Our product specialists continue to deliver a comprehensive range of transaction banking, financing, advisory, capital markets and risk management services. In 2015, our product strengths were recognised by numerous | accolades, including Most Innovative Investment Bank and Best Bank for Securities Services inThe Banker awards. We were ranked number one Bank for Corporates (Global Market Share) in theEuromoney FX Survey, and for the third consecutive year we were voted Best Bond House in Asia byFinanceAsia.

In addition, we provide award-winning research to investors with an emphasis on emerging markets.

Business synergies

In 2015, GB&M enabled business synergies of $8.4bn, supporting growth in a number of areas. For example, we provide Markets products to CMB and RBWM customers, Capital Financing products to CMB customers, and also use CMB and Asset Management products to serve GB&M clients.

Areas of focus

Deepening relationships with clients in both event and transaction banking products remains a priority. We will focus on regions where we see the greatest growth opportunities such as NAFTA, ASEAN and the Pearl River Delta. We also plan to grow our business from the internationalisation of China’s renminbi currency and by investing in digital capabilities.

We made significant progress towards reducing RWAs in 2015. This will remain a focus as we continue to exit legacy credit, manage our Markets and Capital Financing businesses and employ a disciplined approach to new client business.

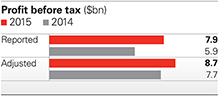

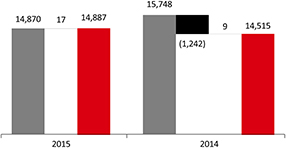

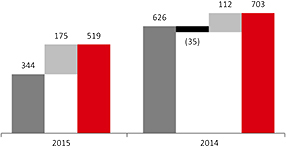

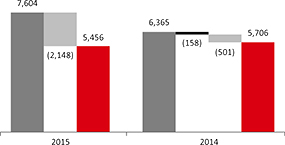

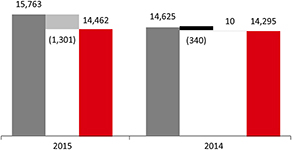

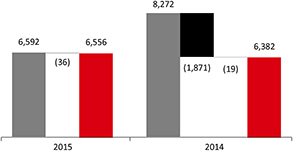

Our continued focus on cost discipline will result in further simplification of the business from streamlining of our business lines, operations and technology. | Adjusted profit growth of 14% compared with 2014

– Adjusted profit before tax was higher by $1.1bn due to higher revenue and lower LICs, partly offset by increased costs.

– Our revenue increased by $1.2bn or 7%, with higher revenue in all businesses except Principal Investments. In client-facing GB&M, revenue rose due to increased client flows and volatility in Equities (up by $0.5bn) and in transaction banking products (up by $0.4bn). Revenue was also higher in Balance Sheet Management (up $0.1bn).

– LICs were $0.3bn lower. This reflected minimal impairments in 2015 compared with a net charge in 2014 in client-facing GB&M. However, in 2015 we had lower net releases of credit risk provisions, primarily on available-for-sale asset-backed securities in legacy credit.

– Our operating expenses increased by $0.4bn or 5%, mainly from higher performance-related costs and higher staff costs reflecting wage inflation. In addition, we continued to invest in our PCM and Foreign Exchange businesses, as well as in regulatory programmes and compliance.

– Management initiatives identified in our Investor Update in June 2015 contributed to an overall reduction in RWAs of $72bn this year. This is 54% of our target of $134bn (stated at December 2015 exchange rates).

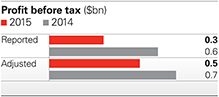

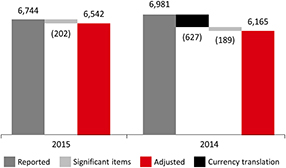

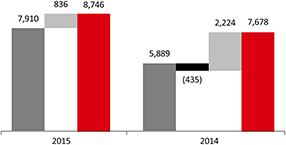

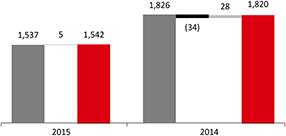

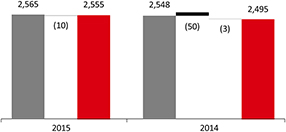

– The graph below shows reported and adjusted profit before tax. The difference between these figures primarily reflects fines, penalties and charges in relation to legal matters, which totalled $1.9bn and $0.9bn in 2014 and 2015, respectively. Significant items are detailed on page 66.

Adjustedprofit before tax +14% | ||

HSBC HOLDINGS PLC

29

Table of Contents

Strategic Report |Global businesses

Retail Banking and Wealth Management (‘RBWM’)

Customers

RBWM serves close to 45 million customers worldwide through four main business areas: Retail Banking, Wealth Management, Asset Management and Insurance.

Since 2012, we have taken numerous actions to improve the way we conduct our business. We have removed the formulaic link between product sales and remuneration, paying all staff on a discretionary basis, which includes assessment of their behaviour and the satisfaction of our customers. We have simplified our product range, reviewed the fairness of our product features and pricing, and enhanced the way we monitor the quality of our sales.

Products and services

RBWM provides services to individuals under the HSBC Premier and Advance propositions aimed at mass affluent and emerging affluent customers who value international connectivity and benefit from our global reach and scale. For customers who have simpler everyday banking needs, RBWM offers a full range of banking products and services reflecting local requirements. | Asset Management and Insurance We operate our own Asset Management and Insurance businesses. By owning these businesses directly, we can tailor their products to the needs of customers and maintain end-to-end control over their quality. We are investing for growth in these businesses, leveraging our network and strong client relationships.

Business synergies

RBWM makes a significant contribution to the overall success of the Group. In 2015, Insurance Manufacturing (within Wealth Management) and Asset Management generated revenue of $1.7bn and $1.1bn, respectively, from the provision of services to clients across all of our global businesses. In addition, the foreign exchange and wealth management needs of our RBWM clients create opportunities for GB&M.

RBWM’s strong deposit franchise supports a stable and diversified core funding base for the Group, and the branch network supports the needs of other global business clients while enhancing the visibility of the HSBC brand.

Areas of focus

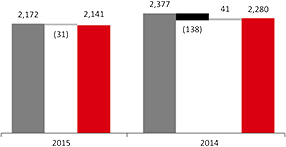

RBWM’s focus is on growing the business through relationship-led personal lending and wealth management, while transforming our customer experience and cost base through investment in digital infrastructure. | Despite a challenging second half of 2015, Wealth Management revenue grew by 8%

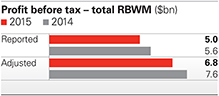

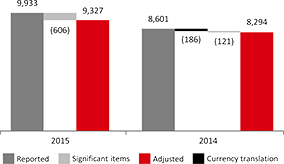

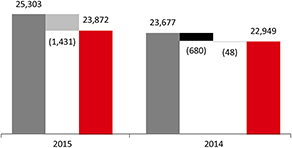

Total RBWM – Total RBWM adjusted profit before tax fell by $0.7bn or 10%, with a decrease in profit before tax in both Principal RBWM and from the continued reduction in our US run-off portfolio.

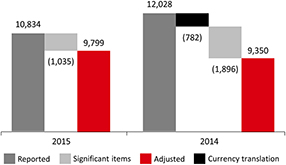

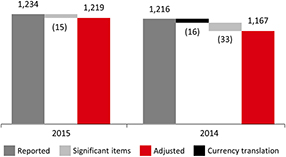

The graph below shows reported and adjusted profit before tax. The difference between them primarily reflects fines, penalties and charges in relation to legal matters, which totalled $1.6bn and $1.3bn in 2014 and 2015, respectively. Significant items are detailed on page 66.

Principal RBWM– In our Principal RBWM business, profit before tax was down by $0.5bn or 7%, reflecting higher costs and LICs. Revenue grew.

– Revenue rose $0.4bn in Wealth Management in Asia in the first half of the year from investment distribution, offsetting weaker investor sentiment in the second half of 2015. Wealth Management income in Europe also grew as insurance manufacturing increased. Deposit and savings income grew in Asia and the UK as deposits increased by $32bn. This was partly offset by lower overdraft fees in the UK.

– LICs increased by $0.3bn or 20%, mainly in Brazil from increased impairment charges following the economic slowdown, and the UAE following a review of collateral in the mortgage book.

– Costs rose by $0.5bn or 4%, driven by inflation in Asia and Latin America. Our marketing costs also increased as we relaunched our Global Advance account proposition with notable investment in the UK, and we continued to invest in regulatory programmes and compliance.

Adjustedprofit before tax – total RBWM -10% |

HSBC HOLDINGS PLC

30

Table of Contents

Global businesses

Global Private Banking (‘GPB’)

Customers

GPB serves high net worth individuals and families, including those with international banking needs, through 18 booking centres covering our priority markets.

Since 2011, GPB has taken significant steps to simplify and improve the way it conducts its business. We have reduced the number of booking centres to refocus resources on a smaller number of locations where we have the scale to support our new client service model and enhanced sales quality standards.

We have also reduced the number of offshore markets we cover to ensure appropriate focus is given to key growth areas.

GPB remains committed to implementing the most effective global standards, including customer due diligence, a tax transparency framework and financial crime compliance measures. | Products and services

We work closely with our clients to provide solutions to grow, manage and preserve wealth. Our products and services include: Investment Management, incorporating advisory, discretionary and brokerage services; Private Wealth Solutions, comprising trusts and estate planning, designed to protect wealth and preserve it for future generations; and a full range of Private Banking services.

Business synergies

GPB aims to bring the best of the Group’s research, product and service capabilities to GPB clients.

To achieve this, we have three client service groups: the Corporate Client Group, enhancing connectivity with CMB and GB&M; the Wealth Client Group, delivering a seamless transition across the RBWM and GPB wealth franchises; and the Global Solutions Group, delivering non-traditional wealth management solutions.

Wherever possible, GPB uses product capabilities within GB&M, CMB and RBWM, including asset management, research, insurance, trade finance and capital financing, to offer a unique proposition to our clients.

Areas of focus

GPB aspires to build on HSBC’s commercial banking heritage and be the leading private bank for high net worth business owners and principals. We work closely and systematically with CMB and GB&M to deliver a coordinated private and corporate coverage model for our clients. | Continued repositioning of our GPB business

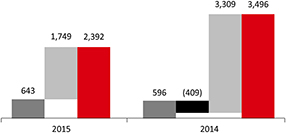

– Adjusted profit before tax fell by 26% to $0.5bn, mainly because revenue fell by 6% as we continued to reposition the GPB business.

– However, revenue increased in Asia, notably in the first half of 2015, due to higher client activity as a result of a strong stock market performance, which more than offset the weaker investor sentiment in the second half of the year.

– We attracted positive net new money of $14bn in 2015 in the parts of the business that fit our target model, mainly in Hong Kong, the UK, Singapore and the US.

Adjustedprofit before tax -26% | ||

HSBC HOLDINGS PLC

31

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Strategic Report |How we do business

Building lasting business relationships

Ensuring fair outcomes

We recognise that delivering fair outcomes for customers and upholding financial market integrity is critical to a sustainable business model.

We continue to enhance our product governance processes to further ensure products are designed to meet customers’ needs and are sold appropriately. In the UK, for example, we have started to alert customers by text message when they are about to go into overdraft. As a result, customer complaints in this area have declined by 67% and customers have saved more than $129.9m in fees.

For further details on the steps we have taken to strengthen conduct across the Group, see page 40. For further details on compliance risk and for further details on conduct-related costs included in significant items, see pages 178 and 97, respectively.

Increasing quality of service

We seek feedback from customers in order to assess how well we are doing and what we can do better. In 2015, we improved our processes for responding to customer complaints and tools for understanding their causes. For example, in India our analysis of customer complaints led us to improve customer communication regarding minimum balances and change our fee structure. Complaints in this area subsequently reduced by 62%.

Through our commercial banking research programmes, we have spoken to more than 50,000 businesses to gather feedback on our products and services from existing and potential customers. We use competitor benchmarking, brand tracking and customer surveys to evaluate our performance. In RBWM, we conducted more than 350,000 individual customer surveys.

Developing long-term opportunities

Technology and climate change are two areas that present both challenges and opportunities to us and our customers.

Investing in technology

We are investing in innovation and digital capabilities to serve customers better, and enhancing security around financial transactions and customer data.

In 2015, we enabled the Apple Pay mobile payment service for customers in the UK and the US, and launched live-chat online customer service in six markets including the UK, Hong Kong and France. We made digital secure keys available in the UK to simplify the customer login experience. In Argentina and the Philippines, we launched our new online banking platform, which will be deployed in additional countries in 2016.

Facilitating a low-carbon economy

Reducing global carbon dioxide emissions is a critical challenge for society. We see the potential for financial services to facilitate investment that can help the world transition to a low-carbon economy.

In 2015, our Global Research team was ranked number one for Integrated Climate Change for the second year running in the Extel Survey. Furthermore, our Asset Management business joined the Montreal Pledge to disclose the carbon intensity of its portfolio.

For more information about our climate business, see page 37.

HSBC Global Research

1st

for integrated climate

change research, ranked

by Extel Survey 2015.

HSBC HOLDINGS PLC

36

Table of Contents

Table of Contents

Strategic Report |How we do business

Empowering people

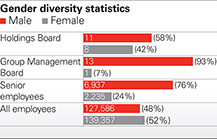

Valuing diversity

We are proud to provide an open, supportive and inclusive workplace where people can grow and achieve their potential. Our commitment to diversity and inclusion helps us attract, develop and retain employees. We are also committed to reflecting the communities we serve.

Our employees lead and organise seven global employee networks to promote diversity. They focus on gender, age, ethnicity, sexual orientation, religion, working parents and disability.

To help managers address bias in hiring, promotion and talent identification, we use education programmes and have expanded mentoring initiatives for under-represented groups.

In 2015, we won Diversity Team of the Year at the European Diversity Awards. We were also one of 10 companies recognised as a Top Global Employer in Stonewall’s Global Workplace Equality Index.

We continue to address gender representation, particularly at senior levels, with additional focus on promotions and hiring. We also continue to expand support and flexible working programmes for parents returning to work.

Our award-winning Balance employee network aims to address gender diversity across HSBC, encouraging dialogue and a better understanding of the challenges and opportunities in promoting a gender-balanced workforce throughout the Group. It is available to staff of all genders, and had active groups in more than 30 offices around the world in 2015.

Encouraging ownership

We promote individual ownership and responsibility, and have created forums to encourage dialogue. In 2015, we continued to facilitate agenda-free exchange meetings across the Group for employees to collaborate on ideas and initiatives to improve our work. We also held 14 webcasts with senior executives to promote understanding of our strategic actions and allow employees to ask questions.

Equipping employees

Our training programmes reinforce a culture grounded in our values. In 2015, we completed a three-year programme of values-led leadership training for all employees.

We are building employee training centres in Birmingham, Dubai and mainland China. These will operate alongside HSBC University, our online training service.

In 2015, we also launched HSBC Confidential, which brought together all our existing whistleblowing channels on to a global platform that allows employees to raise concerns confidentially without fear of personal repercussions. The global channel can be accessed by telephone, email, web or mail. For further details, see ‘Whistleblowing’ on page 179.

Rewarding positive behaviours

We have embedded behaviour ratings in our performance review processes, which are factored into variable pay considerations.

In 2015, we introduced an At Our Best online recognition tool for all employees. It allows them to recognise colleagues’ actions by awarding points that are redeemed for gifts and benefits.

Exchange meeting participation

(% of employees that attended a 2015 meeting)

53%

Employee retention

84.1%

HSBC HOLDINGS PLC

38

Table of Contents

|

| |||||

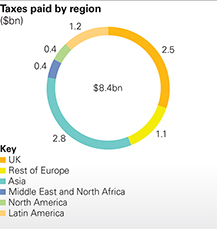

| Ensuring sustainable outcomes | Tax | |||||

Managing environmental

and social impacts

We continue to reduce the environmental impact of our operations and have robust policies and processes to manage sustainability risks in our business activities.

We are reducing the amount of energy we consume, and increasing the proportion from renewable sources. We have signed agreements to increase the percentage of our electricity from new wind and solar sources to 9%, and have a target of 25% by 2020. We report on our carbon dioxide emissions for the year in the Report of the Directors on page 98.

Our sustainability risk policies cover a number of sensitive industries and themes. After we issued new standards in our forestry and agricultural commodities policies in 2014, we took the decision to stop banking more than 160 customers as soon as possible because they did not comply. In 2015, HSBC was recognised as a leader in the Forest 500 ranking of 150 investors’ policies on the sustainability of forest commodity supply chains.

We also support a transition to certified, sustainable palm oil. Our standards require our palm oil customers to have all their operations certified as sustainable by the end of 2018, and we continue to support them in meeting this goal.

In 2015, there were more than 2,300 attendances by relationship and risk managers of training on our sustainability risk policies to help ensure their implementation is robust.

Details on our sustainability risk framework and policies are available online at www.hsbc.com/citizenship/ sustainability/finance.

Respecting human rights

We apply human rights considerations directly as they affect our employees and indirectly through our suppliers and customers, and through our action to prevent bribery and corruption. For example, our code of conduct for suppliers includes elements related to human rights, as do our project finance lending and sustainability risk policies. Our Statement on Human Rights, issued in 2015, explains how we do this and is available on our website. We will integrate the provisions of the Modern Slavery Act 2015 into our business and supply chain, and will report in line with the guidelines published by the UK government.

We are guided by the International Bill of Human Rights, and support the UN Declaration of Human Rights and the principles concerning fundamental rights set out in the International Labour Organisation’s Declaration on Fundamental Principles and Rights at Work.

Investing in our communities