QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS PURSUANT TO SECTIONS 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

(Mark One)

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2004

OR

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 1-15371

iSTAR FINANCIAL INC.

(Exact name of registrant as specified in its charter)

| Maryland | | 95-6881527 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification Number) |

1114 Avenue of the Americas, 27th Floor

New York, NY |

|

10036 |

| (Address of principal executive offices) | | (Zip code) |

Registrant's telephone number, including area code:(212) 930-9400

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: Name of Exchange on which registered: | | Name of Exchange on which registered: |

| Common Stock, $0.001 par value | | New York Stock Exchange |

| 8.000% Series D Cumulative Redeemable | | New York Stock Exchange |

| Preferred Stock, $0.001 par value | | |

| 7.875% Series E Cumulative Redeemable | | New York Stock Exchange |

| Preferred Stock, $0.001 par value | | |

7.800% Series F Cumulative Redeemable

Preferred Stock, $0.001 par value | | New York Stock Exchange |

7.650% Series G Cumulative Redeemable

Preferred Stock, $0.001 par value | | New York Stock Exchange |

7.500% Series I Cumulative Redeemable

Preferred Stock, $0.001 par value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant: (i) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (ii) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is an accelerated filer (as defined in Exchange Act Rule 12-b-2). Yes ý No o

As of June 30, 2004 the aggregate market value of the common stock, $0.001 par value per share of iStar Financial Inc. ("Common Stock"), held by non-affiliates(1) of the registrant was approximately $4.3 billion, based upon the closing price of $40.00 on the New York Stock Exchange composite tape on such date.

As of March 1, 2005, there were 111,487,900 shares of Common Stock outstanding.

- (1)

- For purposes of this Annual Report only, includes all outstanding Common Stock other than Common Stock held directly by the registrant's directors and executive officers.

DOCUMENTS INCORPORATED BY REFERENCE

- 1.

- Portions of the registrant's definitive proxy statement for the registrant's 2005 Annual Meeting, to be filed within 120 days after the close of the registrant's fiscal year, are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

| | Page

|

|---|

| PART I | | |

| Item 1. Business | | 2 |

| Item 2. Properties | | 19 |

| Item 3. Legal Proceedings | | 19 |

| Item 4. Submission of Matters to a Vote of Security Holders | | 19 |

PART II |

|

|

| Item 5. Market for Registrant's Equity and Related Share Matters | | 20 |

| Item 6. Selected Financial Data | | 23 |

Item 7. Management's Discussion and Analysis of Financial Condition

and Results of Operations | | 26 |

| Item 7a. Quantitative and Qualitative Disclosures about Market Risk | | 48 |

| Item 8. Financial Statements and Supplemental Data | | 51 |

Item 9. Changes in and Disagreements with Registered Public Accounting Firm

on Accounting and Financial Disclosure | | 113 |

| Item 9A. Controls and Procedures | | 113 |

PART III |

|

|

| Item 10. Directors and Executive Officers of the Registrant | | 114 |

| Item 11. Executive Compensation | | 114 |

| Item 12. Security Ownership of Certain Beneficial Owners and Management | | 114 |

| Item 13. Certain Relationships and Related Transactions | | 114 |

| Item 14. Principal Registered Public Accounting Firm Fees and Services | | 114 |

PART IV |

|

|

| Item 15. Exhibits, Financial Statement Schedules and Reports on Form 8-K | | 115 |

SIGNATURES |

|

119 |

PART I

Item 1. Business

Explanatory Note for Purposes of the "Safe Harbor Provisions" of Section 21E of the Securities Exchange Act of 1934, as amended

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, which involve certain risks and uncertainties. Forward-looking statements are included with respect to, among other things, iStar Financial Inc.'s (the "Company's") current business plan, business strategy and portfolio management. The Company's actual results or outcomes may differ materially from those anticipated. Important factors that the Company believes might cause such differences are discussed in the cautionary statements presented under the caption "Factors That May Affect the Company's Business Strategy" in Item 1 of this Form 10-K or otherwise accompany the forward-looking statements contained in this Form 10-K. In assessing all forward-looking statements, readers are urged to read carefully all cautionary statements contained in this Form 10-K.

Overview

The Company is the leading publicly-traded finance company focused on the commercial real estate industry. The Company provides custom-tailored financing to high-end private and corporate owners of real estate, including senior and junior mortgage debt, senior and mezzanine corporate capital, and corporate net lease financing. The Company, which is taxed as a real estate investment trust ("REIT"), seeks to deliver strong dividends and superior risk-adjusted returns on equity to shareholders by providing innovative and value added financing solutions to its customers.

The Company's primary product lines include:

- •

- Structured Finance. The Company provides senior and subordinated loans that typically range in size from $20 million to $100 million. These loans may be either fixed or variable rate and are structured to meet the specific financing needs of the borrowers. The Company offers borrowers a wide range of structured finance options, including first mortgages, second mortgages, partnership loans, participating debt and interim facilities. The Company's structured finance transactions have maturities generally ranging from three to ten years. As of December 31, 2004, based on gross carrying values, the Company's structured finance assets represented 25% of its assets.

- •

- Portfolio Finance. The Company provides funding to regional and national borrowers who own multiple facilities in geographically diverse portfolios. Loans are cross-collateralized to give the Company the benefit of all available collateral and underwritten to recognize inherent portfolio diversification. Property types include multifamily, suburban office, hotels and other property types where individual property values are less than $20 million on average. Loan terms are structured to meet the specific requirements of the borrower and typically range in size from $25 million to $150 million. The Company's portfolio finance transactions have maturities generally ranging from three to ten years. As of December 31, 2004, based on gross carrying values, the Company's portfolio finance assets represented 15% of its assets.

- •

- Corporate Finance. The Company provides senior and subordinated capital to corporations engaged in real estate or real estate-related businesses. Financings may be either secured or unsecured and typically range in size from $20 million to $150 million. The Company's corporate finance transactions have maturities generally ranging from five to ten years. As of December 31, 2004, based on gross carrying values, the Company's corporate finance assets represented 10% of its assets.

2

- •

- Loan Acquisition. The Company acquires whole loans and loan participations which present attractive risk-reward opportunities. Loans are generally acquired at a small discount to the principal balance outstanding. Loan acquisitions typically range in size from $5 million to $100 million and are collateralized by all major property types. The Company's loan acquisition transactions have maturities generally ranging from three to ten years. As of December 31, 2004, based on gross carrying values, the Company's loan acquisition assets represented 6% of its assets.

- •

- Corporate Tenant Leasing. The Company provides capital to corporations and borrowers who control facilities leased to single creditworthy customers. The Company's net leased assets are generally mission-critical headquarters or distribution facilities that are subject to long-term leases with public companies, many of which are rated corporate credits, and which provide for all expenses at the facility to be paid by the corporate customer on a triple net lease basis. Corporate tenant lease, or CTL, transactions have terms generally ranging from ten to 20 years and typically range in size from $20 million to $150 million. As of December 31, 2004, based on gross carrying values, the Company's CTL assets (including investments in and advances to joint ventures and unconsolidated subsidiaries and assets held for sale) represented 44% of its assets.

As more fully discussed in Note 1 to the Company's Consolidated Financial Statements, the Company began its business in 1993 through private investment funds formed to capitalize on inefficiencies in the real estate finance market. In March 1998, these funds contributed their approximately $1.1 billion of assets to the Company's predecessor in exchange for a controlling interest in that company. Since that time, the Company has grown by originating new lending and leasing transactions, as well as through corporate acquisitions.

Specifically, in September 1998, the Company acquired the loan origination and servicing business of a major insurance company, and in December 1998, the Company acquired the mortgage and mezzanine loan portfolio of its largest private competitor. Additionally, in November 1999, the Company acquired TriNet Corporate Realty Trust, Inc., then the largest publicly-traded company specializing in corporate sale/leaseback transactions for office and industrial facilities. The acquisition of TriNet was structured as a stock-for-stock merger of TriNet with a subsidiary of the Company. Throughout this Report, the Company refers to TriNet as TriNet or the Leasing Subsidiary and refers to the acquisition of TriNet as the TriNet Acquisition.

Concurrent with the TriNet Acquisition, the Company also acquired its former external advisor in exchange for shares of the Company's Common Stock and converted its organizational form to a Maryland corporation. As part of the conversion to a Maryland corporation, the Company replaced its former dual class common share structure with a single class of Common Stock. The Company's Common Stock began trading on the New York Stock Exchange on November 4, 1999. Prior to this date, the Company's common shares were traded on the American Stock Exchange.

Investment Strategy

The Company's investment strategy targets specific sectors of the real estate and corporate credit markets in which it believes it can deliver innovative, custom-tailored and flexible financial solutions to its customers, thereby differentiating its financial products from those offered by other capital providers.

The Company has implemented its investment strategy by:

- •

- Focusing on the origination of large, structured mortgage, corporate and lease financings where customers require flexible financial solutions and "one-call" responsiveness post-closing.

- •

- Avoiding commodity businesses in which there is significant direct competition from other providers of capital such as conduit lending and investment in commercial or residential mortgage-backed securities.

3

- •

- Developing direct relationships with borrowers and corporate customers as opposed to sourcing transactions solely through intermediaries.

- •

- Adding value beyond simply providing capital by offering borrowers and corporate customers specific lending expertise, flexibility, certainty of closing and a continuing relationship beyond the closing of a particular financing transaction.

- •

- Taking advantage of market anomalies in the real estate financing markets when the Company believes credit is mispriced by other providers of capital, such as the spread between lease yields and the yields on corporate customers' underlying credit obligations.

The Company seeks to invest in a mix of portfolio financing transactions to create asset diversification and single-asset financings for properties with strong, long-term competitive market positions. The Company's credit process focuses on:

- •

- Building diversification by asset type, property type, obligor, loan/lease maturity and geography.

- •

- Financing commercial real estate assets in major metropolitan markets.

- •

- Underwriting assets using conservative assumptions regarding collateral value and future property performance.

- •

- Requiring adequate cash flow coverage on its investments.

- •

- Stress testing potential investments for adverse economic and real estate market conditions.

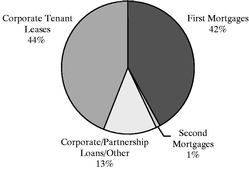

As of December 31, 2004, based on current gross carrying values, the Company's business consists of the following product lines:

Product Line

4

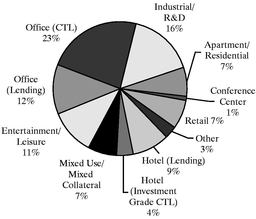

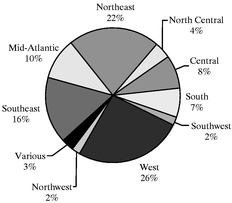

The Company seeks to maintain an investment portfolio which is diversified by asset type, underlying property type and geography. As of December 31, 2004, based on current gross carrying values, the Company's total investment portfolio has the following characteristics:

Asset Type

Property Type

Geography

5

The Company's Underwriting Process

The Company discusses and analyzes investment opportunities during regular weekly meetings which are attended by all of its investment professionals, as well as representatives from its legal, risk management and capital markets areas. The Company has developed a process for screening potential investments called the Six Point Methodologysm. Through this process the Company evaluates an investment opportunity prior to beginning its formal commitment process by: (1) evaluating the source of the opportunity; (2) evaluating the quality of the collateral or corporate credit, as well as its market or industry dynamics; (3) evaluating the equity or corporate sponsor; (4) determining whether it can implement an appropriate legal and financial structure for the transaction given its risk profile; (5) performing an alternative investment test; and (6) evaluating the liquidity of the investment and its ability to match fund the asset.

The Company has an intensive underwriting process in place for all potential investments. This process provides for comprehensive feedback and review by all disciplines within the Company, including investments, credit, risk management, legal/structuring and capital markets. Participation is encouraged from all professionals throughout the entire origination process, from the initial consideration of the opportunity, through the Six Point Methodologysm and into the preparation and distribution of a comprehensive memorandum for the Company's internal and Board of Directors investment committees.

Effective January 20, 2005, commitments of less than $75.0 million require the unanimous consent of the Company's internal investment committee, consisting of senior management representatives from each of the Company's key disciplines. For commitments between $75.0 million and $150.0 million, the further approval of the investment committee of the Company's board of directors' (the "Board of Directors") is also required. All commitments of $150.0 million or more must be approved by the Company's full Board of Directors. In addition, strategic investments such as a corporate merger or acquisition of another business entity (other than a corporate net lease financing) or any other material transaction in an amount over $75.0 million involving the Company's entry into a new line of business, must be approved by the Company's full Board of Directors.

Financing Strategy

The Company has access to a wide range of debt and equity capital resources to finance its investment and growth strategies. At December 31, 2004, the Company had over $2.4 billion of tangible book equity capital and a total market capitalization of approximately $10.1 billion. The Company believes that its size, diversification, investor sponsorship and track record are competitive advantages in obtaining attractive financing for its businesses.

The Company seeks to maximize risk-adjusted returns on equity and financial flexibility by accessing a variety of public and private debt and equity capital sources. While the Company believes that it is important to maintain diverse sources of funding, it began to emphasize unsecured funding sources of debt, such as long-term unsecured corporate debt, approximately 18 months ago. The Company believes that unsecured debt is more cost-effective, flexible and efficient than secured debt. The Company's current sources of debt capital include:

- •

- Long-term, unsecured corporate debt.

- •

- iStar Asset Receivables ("STARs"), the Company's proprietary match-funded, securitized debt program.

- •

- A combined $3.0 billion of capacity under its unsecured and secured revolving credit facilities at year end.

- •

- Individual mortgages secured by certain of the Company's assets.

6

The Company's business model is premised on significantly lower leverage than many other commercial finance companies. In this regard, the Company seeks to:

- •

- Maintain a prudent corporate leverage level based upon the Company's mix of business and appropriate leverage levels for each of its primary business lines.

- •

- Maintain a large tangible equity base and conservative credit statistics.

- •

- Match fund assets and liabilities.

The Company has not historically utilized, and does not currently plan to utilize, "off-balance sheet" financing vehicles other than normal corporate tenant leasing joint ventures with unrelated third parties, which may be accounted for under the equity method due to the existence of provisions providing for a sharing of control with the venture partners. Detailed information on the Company's one remaining joint venture in which the Company currently has investments/operations, which totaled approximately $5.7 million at December 31, 2004, including information on the Company's share of the joint venture's non-recourse debt, is provided in Item 7—"Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources," and in Note 6 to the Company's Consolidated Financial Statements.

A more detailed discussion of the Company's current capital resources is provided in Item 7—"Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources."

Hedging Strategy

The Company has variable-rate lending assets and variable-rate debt obligations. These assets and liabilities create a natural hedge against changes in variable interest rates. This means that as interest rates increase, the Company earns more on its variable-rate lending assets and pays more on its variable-rate debt obligations and, conversely, as interest rates decrease, the Company earns less on its variable-rate lending assets and pays less on its variable-rate debt obligations. When the Company's variable-rate debt obligations exceed its variable-rate lending assets, the Company utilizes derivative instruments to limit the impact of changing interest rates on its net income. The Company does not use derivative instruments to hedge assets or for speculative purposes. The derivative instruments the Company uses are typically in the form of interest rate swaps and interest rate caps. Interest rate swaps effectively change variable-rate debt obligations to fixed-rate debt obligations. Interest rate caps effectively limit the maximum interest rate on variable-rate debt obligations.

In addition, when appropriate the Company enters into interest rate swaps that convert fixed-rate debt to variable rate in order to mitigate the risk of changes in fair value of the fixed-rate debt obligations.

The primary risks from the Company's use of derivative instruments is the risk that a counterparty to a hedging arrangement could default on its obligation and the risk that the Company may have to pay certain costs, such as transaction fees or breakage costs, if a hedging arrangement is terminated by it. As a matter of policy, the Company enters into hedging arrangements with counterparties that are large, creditworthy financial institutions typically rated at least "A/A2" by Standard & Poor's and Moody's Investors Service, respectively. The Company's hedging strategy is monitored by its Audit Committee on behalf of its Board of Directors and may be changed by the Board of Directors without shareholder approval.

Developing an effective strategy for dealing with movements in interest rates is complex and no strategy can completely insulate the Company from risks associated with such fluctuations. There can be no assurance that the Company's hedging activities will have the desired beneficial impact on its results of operations or financial condition.

A more detailed discussion of the Company's hedging policy is provided in Item 7—"Managements Discussion and Analysis of Financial Conditions and Results of Operations—Liquidity and Capital Resources."

7

Business

Real Estate Lending

The Company provides structured financing to high-end private and corporate owners of real estate, including senior and junior mortgage debt and senior and mezzanine corporate capital.

Set forth below is information regarding the Company's primary real estate lending product lines as of December 31, 2004:

| | Current

Carrying

Value

| | %

of Total

| |

|---|

| | (In thousands)

| |

| |

|---|

| Structured finance | | $ | 1,784,746 | | 44.74 | % |

| Portfolio finance | | | 1,058,018 | | 26.53 | % |

| Corporate finance | | | 691,731 | | 17.34 | % |

| Loan acquisition | | | 454,130 | | 11.39 | % |

| | |

| |

| |

| | Gross carrying value | | $ | 3,988,625 | | 100.00 | % |

| | | | | |

| |

| | Provision for loan losses | | | (42,436 | ) | | |

| | |

| | | |

| | Total carrying value, net | | $ | 3,946,189 | | | |

| | |

| | | |

As more fully discussed in Note 3 to the Company's Consolidated Financial Statements, the Company continually monitors borrower performance and completes a detailed, loan-by-loan formal credit review on a quarterly basis. After having originated or acquired over $12.2 billion of investment transactions over its ten-year history, the Company and its private investment fund predecessors have experienced minimal actual losses on their lending investments.

Despite the Company's historical track record of having minimal credit losses and loans on non-accrual status, the Company considers it prudent to reflect provisions for loan losses on a portfolio basis based upon the Company's assessment of general market conditions, the Company's internal risk management policies and credit risk rating system, industry loss experience, the Company's assessment of the likelihood of delinquencies or defaults, and the value of the collateral underlying its investments. Accordingly, since its first full quarter operating its current business as a public company (the quarter ended June 30, 1998), management has reflected quarterly provisions for loan losses in its operating results.

Summary of Interest Characteristics

As more fully discussed in Item 7—"Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources" as well as in Item 7a—"Quantitative and Qualitative Disclosures about Market Risk," the Company utilizes certain interest rate risk management techniques, including both asset/liability matching and certain other hedging techniques, in order to mitigate the Company's exposure to interest rate risks.

As of December 31, 2004, the Company's Lending Business portfolio has the following interest rate characteristics:

| | Current

Carrying

Value

| | %

of Total

| |

|---|

| | (In thousands)

| |

| |

|---|

| Fixed-rate loans | | $ | 1,246,560 | | 31.25 | % |

| Variable-rate loans | | | 2,742,065 | | 68.75 | % |

| | |

| |

| |

| Gross carrying value | | $ | 3,988,625 | | 100.00 | % |

| | |

| |

| |

Summary of Prepayment Terms

The Company is exposed to risks of prepayment on its loan assets, and generally seeks to protect itself from such risks by structuring its loans with prepayment restrictions and/or penalties.

8

As of December 31, 2004, the Company's Lending Business portfolio has the following call protection characteristics:

| | Current

Carrying

Value

| | %

of Total

| |

|---|

| | (In thousands)

| |

| |

|---|

| Fixed prepayment penalties | | $ | 1,804,069 | | 45.24 | % |

| Currently open to prepayment with no penalty | | | 986,407 | | 24.73 | % |

| Substantial lock-out for original term(1) | | | 726,084 | | 18.20 | % |

| Yield maintenance | | | 377,104 | | 9.45 | % |

| Other | | | 94,961 | | 2.38 | % |

| | |

| |

| |

| Gross carrying value | | $ | 3,988,625 | | 100.00 | % |

| | |

| |

| |

Explanatory Note:

- (1)

- For the purpose of this table, the Company has assumed a substantial lock-out to mean at least three years.

Summary of Lending Business Maturities

As of December 31, 2004, the Company's Lending Business portfolio has the following maturity characteristics:

Year of Maturity

| | Number of

Transactions

Maturing

| | Current

Carrying

Value

| | %

of Total

| |

|---|

| |

| | (In thousands)

| |

| |

|---|

| 2005 | | 23 | | $ | 813,660 | | 20.40 | % |

| 2006 | | 29 | | | 1,163,926 | | 29.18 | % |

| 2007 | | 21 | | | 657,997 | | 16.50 | % |

| 2008 | | 14 | | | 309,309 | | 7.75 | % |

| 2009 | | 18 | | | 601,982 | | 15.09 | % |

| 2010 | | 2 | | | 37,561 | | 0.94 | % |

| 2011 | | 6 | | | 89,687 | | 2.25 | % |

| 2012 | | 2 | | | 41,409 | | 1.04 | % |

| 2013 | | 6 | | | 83,358 | | 2.09 | % |

| 2014 | | 2 | | | 95,257 | | 2.39 | % |

| 2015 and thereafter | | 4 | | | 94,479 | | 2.37 | % |

| | |

| |

| |

| |

| Total | | 127 | | $ | 3,988,625 | | 100.00 | % |

| | |

| |

| |

| |

| Weighted average maturity | | | | | 2.92 years | | | |

| | | | |

| | | |

Structured Finance

The Company provides senior and subordinated loans that typically range in size from $20 million to $100 million. These loans may be either fixed or variable rate and are structured to meet the specific financing needs of the borrowers, including the acquisition or financing of large, quality real estate. The Company offers borrowers a wide range of structured finance options, including first mortgages, second mortgages, partnership loans, participating debt and interim facilities. The Company's structured finance transactions have maturities generally ranging from three to ten years.

9

As of December 31, 2004, the Company's structured finance investments have the following characteristics:

Investment Class

| | Collateral Types

| | # of

Loans

In Class

| | Current

Carrying

Value(1)

| | Current

Principal

Balance

Outstanding

| | Weighted

Average

Stated

Pay Rate(2)

| | Weighted

Average First

Dollar

Current

Loan-to-

Value(3)

| | Weighted

Average Last

Dollar

Current

Loan-to-

Value(4)

| |

|---|

| |

| |

| | (In thousands)

| |

| |

| |

| |

|---|

| First Mortgages | | Office/Residential/Retail/

Industrial, R&D/Conference

Center/Mixed Use/

Hotel/Entertainment,

Leisure | | 36 | | $ | 1,341,310 | | $ | 1,352,089 | | 6.92 | % | 0 | % | 67 | % |

| Junior First Mortgages(5) | | Office/Residential/Mixed

Use/Hotel | | 10 | | | 268,517 | | | 271,223 | | 9.74 | % | 50 | % | 74 | % |

| Second Mortgages | | Mixed Use | | 4 | | | 61,482 | | | 58,228 | | 7.20 | % | 52 | % | 74 | % |

| Corporate Loans/Other | | Office/Industrial, R&D/Mixed Use/Hotel | | 11 | | | 113,437 | | | 112,609 | | 11.35 | % | 57 | % | 72 | % |

| | | | |

| |

| |

| | | | | | | |

| Total | | | | 61 | | $ | 1,784,746 | | $ | 1,794,149 | | | | | | | |

| | | | |

| |

| |

| | | | | | | |

Explanatory Notes:

- (1)

- Where Current Carrying Value differs from Current Principal Balance Outstanding, the difference represents unamortized amount of acquired premiums, discounts or deferred loan fees.

- (2)

- All variable-rate loans assume a one-month LIBOR rate of 2.40% (the actual one-month LIBOR rate at December 31, 2004). As of December 31, 2004, three loans with a combined carrying value of $73.2 million have a stated accrual rate that exceeds the stated pay rate.

- (3)

- Weighted average ratio of first dollar current loan carrying value to underlying collateral value using third-party appraisal or the Company's internal valuation.

- (4)

- Weighted average ratio of last dollar current loan carrying value to underlying collateral value using third-party appraisal or the Company's internal valuation.

- (5)

- Junior first mortgages represent promissory notes secured by first mortgages which are junior to other promissory notes secured by the same first mortgage.

Portfolio Finance

The Company provides funding to regional and national borrowers who own multiple facilities in geographically diverse portfolios. Loans are cross-collateralized to give the Company the benefit of all available collateral and underwritten to recognize inherent portfolio diversification. Property types include multifamily, suburban office, hotels and other property types where individual property values are less than $20 million on average. Loan terms are structured to meet the specific requirements of the borrower and typically range in size from $25 million to $150 million. The Company's portfolio finance transactions have maturities generally ranging from three to ten years.

As of December 31, 2004, the Company's portfolio finance investments have the following characteristics:

Investment Class

| | Collateral Types

| | # of

Loans

In Class

| | Current

Carrying

Value(1)

| | Current

Principal

Balance

Outstanding

| | Weighted

Average

Stated

Pay Rate(2)

| | Weighted

Average First

Dollar

Current

Loan-to-

Value(3)

| | Weighted

Average Last

Dollar

Current

Loan-to-

Value(4)

| |

|---|

| |

| |

| | (In thousands)

| |

| |

| |

| |

|---|

| First Mortgages | | Office/Residential/Mixed

Use/Hotel/

Entertainment, Leisure | | 6 | | $ | 346,831 | | $ | 349,774 | | 6.30 | % | 0 | % | 65 | % |

| Junior First Mortgages(5) | | Office/Hotel/

Entertainment, Leisure | | 5 | | | 194,285 | | | 194,400 | | 7.49 | % | 52 | % | 61 | % |

| Second Mortgages | | Hotel | | 1 | | | 27,406 | | | 26,988 | | 12.60 | % | 68 | % | 86 | % |

| Corporate Loans/Other | | Office/Residential/Mixed

Use/Hotel/

Entertainment, Leisure/Other | | 14 | | | 489,496 | | | 494,750 | | 9.51 | % | 49 | % | 70 | % |

| | | | |

| |

| |

| | | | | | | |

| Total | | | | 26 | | $ | 1,058,018 | | $ | 1,065,912 | | | | | | | |

| | | | |

| |

| |

| | | | | | | |

Explanatory Notes:

- (1)

- Where Current Carrying Value differs from Current Principal Balance Outstanding, the difference represents unamortized amount of acquired premiums, discounts or deferred loan fees.

10

- (2)

- All variable-rate loans assume a one-month LIBOR rate of 2.40% (the actual one-month LIBOR rate at December 31, 2004).

- (3)

- Weighted average ratio of first dollar current loan carrying value to underlying collateral value using third-party appraisal or the Company's internal valuation.

- (4)

- Weighted average ratio of last dollar current loan carrying value to underlying collateral value using third-party appraisal or the Company's internal valuation.

- (5)

- Junior first mortgages represent promissory notes secured by first mortgages which are junior to other promissory notes secured by the same first mortgage.

Corporate Finance

The Company provides senior and subordinated capital to corporations engaged in real estate or real estate-related businesses. Financings may be either secured or unsecured and typically range in size from $20 million to $150 million. The Company's corporate finance transactions have maturities generally ranging from five to ten years.

As of December 31, 2004, the Company's corporate finance investments have the following characteristics:

Investment Class

| | Collateral Types

| | # of

Loans

In Class

| | Current

Carrying

Value(1)

| | Current

Principal

Balance

Outstanding

| | Weighted

Average

Stated

Pay Rate(2)

| | Weighted

Average First

Dollar

Current

Loan-to-

Value(3)

| | Weighted

Average Last

Dollar

Current

Loan-to-

Value(4)

| |

|---|

| |

| |

| | (In thousands)

| |

| |

| |

| |

|---|

| First Mortgages | | Industrial, R&D/Hotel/

Entertainment, Leisure/ Retail/Other | | 11 | | $ | 411,245 | | $ | 425,381 | | 6.58 | % | 4 | % | 57 | % |

| Junior First Mortgages(5) | | Retail/Entertainment, Leisure/Other | | 4 | | | 51,805 | | | 52,391 | | 6.55 | % | 52 | % | 60 | % |

| Corporate Loans/Other | | Office/Residential/Retail/ Industrial, R&D/Mixed Use/Other | | 13 | | | 228,681 | | | 235,053 | | 7.41 | % | 51 | % | 63 | % |

| | | | |

| |

| |

| | | | | | | |

| Total | | | | 28 | | $ | 691,731 | | $ | 712,825 | | | | | | | |

| | | | |

| |

| |

| | | | | | | |

Explanatory Notes:

- (1)

- Where Current Carrying Value differs from Current Principal Balance Outstanding, the difference represents unamortized amount of acquired premiums, discounts or deferred loan fees.

- (2)

- All variable-rate loans assume a one-month LIBOR rate of 2.40% (the actual one-month LIBOR rate at December 31, 2004). As of December 31, 2004, one loan with a carrying value of ($154,000) has a stated accrual rate that exceeds the stated pay rate.

- (3)

- Weighted average ratio of first dollar current loan carrying value to underlying collateral value using third-party appraisal or the Company's internal valuation.

- (4)

- Weighted average ratio of last dollar current loan carrying value to underlying collateral value using third-party appraisal or the Company's internal valuation.

- (5)

- Junior first mortgages represent promissory notes secured by first mortgages which are junior to other promissory notes secured by the same first mortgage.

Loan Acquisition

The Company acquires whole loans and loan participations which represent attractive risk-reward opportunities. Loans are generally acquired at a small discount to the principal balance outstanding. Loan acquisitions typically range in size from $5 million to $100 million and are collateralized by all major property types. The Company's loan acquisition transactions have maturities generally ranging from three to ten years.

For accounting purposes, these loans are initially reflected at the Company's acquisition cost which represents the outstanding balance net of the acquisition discount or premium. The Company amortizes such discounts or premiums as an adjustment to increase or decrease the yield, respectively, realized on these loans using the effective interest method. As such, differences between carrying value and principal balances outstanding do not represent embedded losses or gains as the Company generally plans to hold such loans to maturity.

11

As of December 31, 2004, the Company's loan acquisition investments have the following characteristics:

Investment Class

| | Collateral Types

| | # of

Loans

In Class

| | Current

Carrying

Value(1)

| | Current

Principal

Balance

Outstanding

| | Weighted

Average

Stated

Pay Rate(2)

| | Weighted

Average First

Dollar

Current

Loan-to-

Value(3)

| | Weighted

Average Last

Dollar

Current

Loan-to-

Value(4)

| |

|---|

| |

| |

| | (In thousands)

| |

| |

| |

| |

|---|

| First Mortgages | | Office/Retail/Hotel/Other | | 6 | | $ | 350,922 | | $ | 362,232 | | 7.99 | % | 6 | % | 78 | % |

| Second Mortgages | | Hotel | | 1 | | | 15,000 | | | 15,000 | | 7.24 | % | 45 | % | 58 | % |

| Corporate Loans/Other | | Hotel | | 5 | | | 88,208 | | | 108,757 | | 7.64 | % | 44 | % | 54 | % |

| | | | |

| |

| |

| | | | | | | |

| Total | | | | 12 | | $ | 454,130 | | $ | 485,989 | | | | | | | |

| | | | |

| |

| |

| | | | | | | |

Explanatory Notes:

- (1)

- Where Current Carrying Value differs from Current Principal Balance Outstanding, the difference represents unamortized amount of acquired premiums, discounts or deferred loan fees.

- (2)

- All variable-rate loans assume a one-month LIBOR rate of 2.40% (the actual one-month LIBOR rate at December 31, 2004).

- (3)

- Weighted average ratio of first dollar current loan carrying value to underlying collateral value using third-party appraisal or the Company's internal valuation.

- (4)

- Weighted average ratio of last dollar current loan carrying value to underlying collateral value using third-party appraisal or the Company's internal valuation.

Corporate Tenant Leasing

The Company, directly and through its Leasing Subsidiary, provides capital to corporations and borrowers who control facilities leased to single creditworthy customers. The Company's net leased assets are generally mission-critical headquarters or distribution facilities that are subject to long-term leases with rated public companies, many of which are corporate credits, and which provide for all expenses at the facility to be paid by the corporate customer on a triple net lease basis. CTL transactions have terms generally ranging from ten to 20 years and typically range in size from $20 million to $150 million.

The Company pursues the origination of CTL transactions by structuring purchase/leasebacks and by acquiring facilities subject to existing long-term net leases. In a typical purchase/leaseback transaction, the Company purchases a corporation's facility and leases it back to that corporation subject to a long-term net lease. This structure allows the corporate customer to reinvest the proceeds from the sale of its facilities into its core business, while the Company capitalizes on its structured financing expertise.

The Company generally intends to hold its CTL assets for long-term investment. However, subject to certain tax restrictions, the Company may dispose of an asset if it deems the disposition to be in the Company's best interests and may either reinvest the disposition proceeds, use the proceeds to reduce debt, or distribute the proceeds to shareholders.

The Company's CTL investments primarily represent a diversified portfolio of mission-critical headquarters or distribution facilities subject to net lease agreements with creditworthy corporate customers. The Company generally seeks general-purpose real estate with residual values that represent a discount to current market values and replacement costs. Under a typical net lease agreement, the corporate customer agrees to pay a base monthly operating lease payment and all facility operating expenses (including taxes, maintenance and insurance).

The Company generally seeks corporate customers with the following characteristics:

- •

- Established companies with stable core businesses or market leaders in growing industries.

- •

- Investment-grade credit strength or appropriate credit enhancements if corporate credit strength is not sufficient on a stand-alone basis.

- •

- Commitment to the facility as a mission-critical asset to their on-going businesses.

12

As of December 31, 2004, the Company had 128 corporate customers operating in more than 21 major industry sectors, including automotive, energy, finance, healthcare, recreation, technology and telecommunications. The majority of these customers represent well-recognized national and international companies, such as Federal Express, IBM, Nike, Nokia, the U.S. Government and Verizon.

As of December 31, 2004, the Company's CTL portfolio has the following tenant credit characteristics:

| | Annualized In-Place

Operating

Lease Income(3)

| | % of In-Place

Operating

Lease Income

|

|---|

| | (In thousands)

| |

|

|---|

| Investment grade(1) | | $ | 103,949 | | 35.01% |

| Implied investment grade(2) | | | 43,920 | | 14.79% |

| Non-investment grade | | | 81,943 | | 27.59% |

| Unrated | | | 67,138 | | 22.61% |

| | |

| |

|

| | | $ | 296,950 | | 100.00% |

| | |

| |

|

Explanatory Notes:

- (1)

- A customer's credit rating is considered "Investment Grade" if the tenants' or its guarantor has a published senior unsecured credit rating of Baa3/BBB- or above by one or more of the three national rating agencies. Where a customer's credit is rated investment grade by one agency and non-investment grade by another, the Company only classifies the credit "Investment Grade" if the agency rating the credit investment grade is Standard & Poor's or Moody's Investors Service.

- (2)

- A customer's credit rating is considered "Implied Investment Grade" if it is 100.00% owned by an investment-grade parent or it has no published ratings, but has credit characteristics that the Company believes warrant an investment grade senior unsecured credit rating. Examples at December 31, 2004 include Hewlett-Packard Co., Northrop Grumman Information and Volkswagen of America, Inc.

- (3)

- Reflects annualized GAAP operating lease income for the quarter ended December 31, 2004 for leases in place at December 31, 2004. The operating lease income includes the Company's pro rata share from facilities owned by the Company's joint ventures.

Risk Management Strategies. The Company believes that diligent risk management of its CTL assets is an essential component of its long-term strategy. There are several ways to optimize the performance and maximize the value of CTL assets. The Company monitors its portfolio for changes that could affect the performance of the markets, credits and industries in which it has invested. As part of this monitoring, the Company's risk management group reviews market, customer and industry data and frequently inspects its facilities. In addition, the Company attempts to develop strong relationships with its large corporate customers, which provide a source of information concerning the customers' facilities needs. These relationships allow the Company to be proactive in obtaining early lease renewals and in conducting early marketing of assets where the customer has decided not to renew.

As of December 31, 2004, the Company owned 349 office and industrial, entertainment and retail facilities principally subject to net leases to 127 customers, comprising 32.8 million square feet in 38 states.

13

The Company also has a portfolio of 17 hotels under a long-term master lease with a single customer. Information regarding the Company's CTL assets as of December 31, 2004 is set forth below:

SIC Code

| | # of

Leases

| | % of In-Place

Operating

Lease Income(1)

| | % of Total

Revenue(2)

|

|---|

| 73 | | Business Services | | 15 | | 12.09 | % | 4.81% |

| 79 | | Amusement and Recreation Services | | 4 | | 11.27 | % | 4.49% |

| 70 | | Hotels, Rooming, Housing & Lodging | | 3 | | 8.64 | % | 3.44% |

| 35 | | Industrial/Commercial Machinery, incl. Computers | | 16 | | 8.33 | % | 3.32% |

| 62 | | Security and Commodity Brokers | | 1 | | 7.07 | % | 2.82% |

| 37 | | Transportation Equipment | | 7 | | 6.97 | % | 2.77% |

| 36 | | Electronic & Other Elec. Equipment | | 13 | | 6.39 | % | 2.55% |

| 48 | | Communications | | 7 | | 5.95 | % | 2.37% |

| 30 | | Rubber and Misc. Plastics Products | | 2 | | 5.77 | % | 2.30% |

| 55 | | Automotive Dealers and Gasoline Service Stations | | 25 | | 4.21 | % | 1.68% |

| 50 | | Wholesale Trade—Durable Goods | | 8 | | 2.75 | % | 1.10% |

| 42 | | Motor Freight Transp. & Warehousing | | 3 | | 2.36 | % | 0.94% |

| 64 | | Insurance Agents, Brokers & Service | | 3 | | 2.35 | % | 0.93% |

| 58 | | Eating and Drinking Places | | 13 | | 2.00 | % | 0.80% |

| 91 | | Executive, Legislative and General Gov't. | | 3 | | 1.83 | % | 0.73% |

| 63 | | Insurance Carriers | | 3 | | 1.78 | % | 0.71% |

| 45 | | Airports, Flying Fields & Terminal Services | | 1 | | 1.21 | % | 0.48% |

| 87 | | Engineering, Accounting & Research Services | | 4 | | 1.12 | % | 0.45% |

| 54 | | Food Stores | | 2 | | 1.08 | % | 0.43% |

| 51 | | Wholesale Trade—Non-Durable Goods | | 3 | | 1.02 | % | 0.41% |

| 93 | | Public Finance, Taxation, and Monetary Policy | | 1 | | 1.02 | % | 0.40% |

| | | Various | | 14 | | 4.79 | % | 1.91% |

| | | | |

| |

| | |

| | | Total | | 151 | | 100.00 | % | |

| | | | |

| |

| | |

Explanatory Notes:

- (1)

- Reflects annualized GAAP operating lease income for the quarter ended December 31, 2004 for leases in place at December 31, 2004. The operating lease income includes the Company's pro rata share from facilities owned by the Company's joint ventures.

- (2)

- Reflects annualized GAAP operating lease income for the quarter ended December 31, 2004 for leases in place at December 31, 2004 as a percentage of annualized total revenue for the quarter ended December 31, 2004.

14

As of December 31, 2004, lease expirations on the Company's CTL assets, including facilities owned by the Company's joint ventures, are as follows:

Year of Lease Expiration

| | Number of Leases Expiring

| | Annualized In-Place Operating Lease Income(1)

| | % of In-Place Operating Lease

Income

| | % of Total

Revenue(2)

|

|---|

| |

| | (In thousands)

| |

| |

|

|---|

| 2005 | | 5 | | $ | 2,843 | | 0.96% | | 0.38% |

| 2006 | | 15 | | | 23,874 | | 8.04% | | 3.20% |

| 2007 | | 14 | | | 13,637 | | 4.59% | | 1.83% |

| 2008 | | 5 | | | 9,644 | | 3.25% | | 1.29% |

| 2009 | | 6 | | | 8,096 | | 2.73% | | 1.09% |

| 2010 | | 11 | | | 14,832 | | 4.99% | | 1.99% |

| 2011 | | 4 | | | 2,747 | | 0.93% | | 0.37% |

| 2012 | | 12 | | | 19,532 | | 6.58% | | 2.62% |

| 2013 | | 5 | | | 5,391 | | 1.82% | | 0.72% |

| 2014 | | 28 | | | 21,719 | | 7.31% | | 2.91% |

| 2015 and thereafter | | 46 | | | 174,635 | | 58.80% | | 23.42% |

| | |

| |

| |

| | |

| Total | | 151 | | $ | 296,950 | | 100.00% | | |

| | |

| |

| |

| | |

Weighted average

remaining lease term | | | | | 11.20 years | | | | |

| | | | |

| | | | |

Explanatory Notes:

- (1)

- Reflects annualized GAAP operating lease income for the quarter ended December 31, 2004 for leases in place at December 31, 2004. The operating lease income includes the Company's pro rata share from facilities owned by the Company's joint ventures.

- (2)

- Reflects annualized GAAP operating lease income for the quarter ended December 31, 2004 for leases in place at December 31, 2004 as a percentage of annualized total revenue for the quarter ended December 31, 2004.

Policies with Respect to Other Activities

The Company's investment, financing and conflicts of interests policies are managed under the ultimate supervision of the Company's Board of Directors. The Board of Directors can amend, revise or eliminate these policies at any time without a vote of shareholders. At all times, the Company intends to make investments in a manner consistent with the requirements of the Code for the Company to qualify as a REIT.

Investment Restrictions or Limitations

The Company does not have any prescribed allocation among investments or product lines. Instead, the Company focuses on corporate and real estate credit underwriting to develop an in-depth analysis of the risk/reward ratios in determining the pricing and advisability of each particular transaction.

The Company believes that it is not, and intends to conduct its operations so as not to become, regulated as an investment company under the Investment Company Act. The Investment Company Act generally exempts entities that are "primarily engaged in purchasing or otherwise acquiring mortgages and other liens on and interests in real estate" (collectively, "Qualifying Interests"). The Company intends to rely on current interpretations of the Securities and Exchange Commission in an effort to qualify for this exemption. Based on these interpretations, the Company, among other things, must maintain at least 55.00% of its assets in Qualifying Interests and at least 25.00% of its assets in real estate-related assets (subject to reduction to the extent the Company invests more than 55.00% of its assets in Qualifying Interests). Generally, the Company's senior mortgages, CTL assets and certain of its subordinated mortgages constitute Qualifying Interests.

15

Subject to the limitations on ownership of certain types of assets and the gross income tests imposed by the Code, the Company also may invest in the securities of other REITs, other entities engaged in real estate activities or other issuers, including for the purpose of exercising control over such entities.

Competition

The Company is engaged in a competitive business. In originating and acquiring assets, the Company competes with public and private companies, including finance companies, mortgage banks, pension funds, savings and loan associations, insurance companies, institutional investors, investment banking firms and other lenders and industry participants, as well as individual investors. Existing industry participants and potential new entrants compete with the Company for the available supply of investments suitable for origination or acquisition, as well as for debt and equity capital. Certain of the Company's competitors are larger than the Company, have longer operating histories, may have access to greater capital and other resources, may have management personnel with more experience than the officers of the Company, and may have other advantages over the Company in conducting certain businesses and providing certain services.

Regulation

The operations of the Company are subject, in certain instances, to supervision and regulation by state and federal governmental authorities and may be subject to various laws and judicial and administrative decisions imposing various requirements and restrictions, which, among other things: (1) regulate credit granting activities; (2) establish maximum interest rates, finance charges and other charges; (3) require disclosures to customers; (4) govern secured transactions; and (5) set collection, foreclosure, repossession and claims-handling procedures and other trade practices. Although most states do not regulate commercial finance, certain states impose limitations on interest rates and other charges and on certain collection practices and creditor remedies and require licensing of lenders and financiers and adequate disclosure of certain contract terms. The Company is also required to comply with certain provisions of the Equal Credit Opportunity Act that are applicable to commercial loans.

In the judgment of management, existing statutes and regulations have not had a material adverse effect on the business conducted by the Company. However, it is not possible to forecast the nature of future legislation, regulations, judicial decisions, orders or interpretations, nor their impact upon the future business, financial condition or results of operations or prospects of the Company.

The Company has elected and expects to continue to make an election to be taxed as a REIT under Section 856 through 860 of the Code. As a REIT, the Company must currently distribute, at a minimum, an amount equal to 90.00% of its taxable income and must distribute 100.00% of its taxable income to avoid paying corporate federal income taxes. REITs are also subject to a number of organizational and operational requirements in order to elect and maintain REIT status. These requirements include specific share ownership tests and assets and gross income composition tests. If the Company fails to qualify as a REIT in any taxable year, the Company will be subject to federal income tax (including any applicable alternative minimum tax) on its taxable income at regular corporate tax rates. Even if the Company qualifies for taxation as a REIT, the Company may be subject to state and local income taxes and to federal income tax and excise tax on its undistributed income.

The American Jobs Creation Act

The American Jobs Creation Act of 2004 (the "Act") was enacted on October 22, 2004. The Act modifies the manner in which the Company applys the gross income and asset test requirements under the Code. With respect to the asset tests, the Act expands the types of securities that qualify as "straight debt" for purposes of the 10.00% value limitation. The Act also clarifies that certain types of debt instruments, including loans to individuals or estates and securities of a REIT, are not "securities" for purposes of the

16

10.00% value limitation. With respect to the gross income tests, the Act provides that for the Company's taxable years beginning on or after January 1, 2005, except to the extent provided by Treasury regulations, its income from certain hedging transactions that are clearly identified as hedges under Section 1221 of the Code, including gain from the sale or disposition of such a transaction, will be excluded from gross income for purposes of the 95.00% gross income test, to the extent the transaction hedges any indebtedness incurred or to be incurred by the trust to acquire or carry real estate.

The Act also sets forth rules that permit a REIT to avoid disqualification forde minimis failures (as defined in the Act) to satisfy the 5.00% and 10.00% value limitations under the asset tests if the REIT either disposes of the assets within six months after the last day of the quarter in which the REIT identifies the failure (or such other time period prescribed by the Treasury), or otherwise meets the requirements of such asset tests by the end of such time period. In addition, if a REIT fails to meet any of the asset test requirements for a particular quarter, and thede minimis exception described above does not apply, the REIT may cure such failure if the failure was due to reasonable cause and not to willful neglect, the REIT identifies such failure to the IRS and disposes of the assets that caused the failure within six months after the last day of the quarter in which the identification occurred, and the REIT pays a tax with respect to the failure equal to the greater of: (i) $50,000; or (ii) an amount determined (pursuant to Treasury regulations) by multiplying the highest rate of tax for corporations under Section 11 of the Code, by the net income generated by the assets for the period beginning on the first date of the failure and ending on the date the REIT has disposed of the assets (or otherwise satisfies the requirements). In addition to the foregoing, the Act also provides that if a REIT fails to satisfy one or more requirements for REIT qualification, other than by reason of a failure to comply with the provisions of the reasonable cause exception to the gross income tests and the provisions described above with respect to failure to comply with the asset tests, the REIT may retain its REIT qualification if the failures are due to reasonable cause and not willful neglect, and if the REIT pays a penalty of $50,000 for each such failure. The provisions described in this paragraph will only apply to the Company's taxable years beginning on or after January 1, 2005.

Factors That May Affect the Company's Business Strategy

The implementation of the Company's business strategy and investment policies are subject to certain risks, including the effect of economic and other conditions in the United States generally and in markets where the Companys' customers, collateral and corporate facilities are located. In addition, the following factors may affect the Company's financial condition and results of operations:

- •

- The Company has experienced significant competition in its core lending and corporate tenant leasing businesses in recent years as capital inflows into these businesses have been plentiful. In order to continue growing its asset base, the Company has announced new strategic initiatives such as the acquisition of Falcon Financial Investment Trust which represents an expansion of the Company's efforts to penetrate the market for providing real estate-based financing to auto dealers. The Company will seek additional strategic initiatives to grow its asset base. There can be no assurance that any of these initiatives will be successful in achieving growth for the Company.

- •

- The Company may not be able to redeploy capital from loans that have been repaid or assets that are sold on terms as attractive as the loans being repaid or the assets that are sold, which may adversely impact its earnings.

- •

- The Company may suffer a loss if a borrower defaults on a non-recourse loan or an unsecured loan.

- •

- The Company may suffer a loss in the event of a bankruptcy of a borrower, particularly if the borrower has incurred debt that is senior to the Company's loan.

- •

- The Company is subject to the risk that provisions of its loan agreements may be unenforceable or that it may experience delays in enforcing remedies.

17

- •

- Some of the Company's assets are participating interests in loans in which the Company shares the rights, obligations and benefits of the loan with other participating lenders. The Company is subject to the risks associated with these loan participations, such as less than full control rights.

- •

- Lease expirations, defaults and terminations will adversely affect its revenue if the Company cannot replace the leases on advantageous terms.

- •

- The Company's ownership interests in corporate facilities may be illiquid, hindering its ability to mitigate a loss.

- •

- The Company may need to make significant capital improvements to its corporate facilities in order to remain competitive which could adversely affect its financial performance.

- •

- The Company needs continued access to significant capital, including debt, in order to grow. Increased leverage magnifies changes in its net worth and creates the risk that it might not be able to service its debt obligations.

- •

- The Company may utilize interest rate hedging arrangements which may adversely affect the Company's borrowing cost. These arrangements may also expose the Company to other risks like the risk of paying additional costs or fees if the hedging arrangement is terminated by the Company or the risk that the counterparty to the hedging arrangement might default on its obligations.

- •

- As an owner of real estate, the Company faces risks of liability under environmental laws.

- •

- The Company will suffer adverse consequences if it fails to qualify as a REIT.

Environmental Matters

Under various federal, state and local environmental laws, ordinances and regulations, a current or previous owner of real estate (including, in certain circumstances, a secured lender that succeeds to ownership or control of a property) may become liable for the costs of removal or remediation of certain hazardous or toxic substances at, on, under or in its property. Those laws typically impose cleanup responsibility and liability without regard to whether the owner or control party knew of or was responsible for the release or presence of such hazardous or toxic substances. The costs of investigation, remediation or removal of those substances may be substantial. The owner or control party of a site may be subject to common law claims by third parties based on damages and costs resulting from environmental contamination emanating from a site. Certain environmental laws also impose liability in connection with the handling of or exposure to asbestos-containing materials, pursuant to which third parties may seek recovery from owners of real properties for personal injuries associated with asbestos-containing materials. Absent succeeding to ownership or control of real property, a secured lender is not likely to be subject to any of these forms of environmental liability. The Company is not currently aware of any environmental issues which could materially affect the Company.

Code of Conduct

The Company has adopted a code of business conduct for all of its employees and directors, including the Company's chief executive officer, chief financial officer, other executive officers and personnel. A copy of the Company's code of conduct is attached to this Annual Report on Form 10-K as Exhibit 14.0 and is also available on the Company's website atwww.istarfinancial.com. The Company intends to post on its website material changes to, or waivers from, its code of conduct, if any, within two days of any such event. As of December 31, 2004, there were no such changes or waivers since its adoption in February 2000.

18

Employees

As of March 1, 2005, the Company had 167 employees and believes its relationships with its employees to be good. The Company's employees are not represented by a collective bargaining agreement.

Other

In addition to this Annual Report, the Company files quarterly and special reports, proxy statements and other information with the SEC. All documents are filed with the SEC and are available free of charge on the Company's corporate website, which iswww.istarfinancial.com. Effective as of January 1, 2003, through the Company's website, the Company makes available free of charge its annual proxy statement, Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those Reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after the Company electronically files such material with, or furnishes it to, the SEC. You may also read and copy any document filed at the public reference facilities at 450 Fifth Street, N.W., Washington, D.C. 25049. Please call the SEC at (800) SEC-0330 for further information about the public reference facilities. These documents also may be accessed through the SEC's electronic data gathering, analysis and retrieval system ("EDGAR") via electronic means, including the SEC's homepage on the internet atwww.sec.gov.

Item 2. Properties

The Company's principal executive and administrative offices are located at 1114 Avenue of the Americas, New York, NY 10036. Its telephone number, general facsimile number and web address are (212) 930-9400, (212) 930-9494 andwww.istarfinancial.com, respectively. The lease for the Company's primary corporate office space expires in February 2010. The Company believes that this office space is suitable for its operations for the foreseeable future. The Company also maintains super-regional offices in Atlanta, Georgia; Hartford, Connecticut; and San Francisco, California, as well as regional offices in Boston, Massachusetts and Dallas, Texas.

See Item 1—"Corporate Tenant Leasing" for a discussion of CTL facilities held by the Company and its Leasing Subsidiary for investment purposes and Item 8—"Schedule III—Corporate Tenant Lease Assets and Accumulated Depreciation" for a detailed listing of such facilities.

Item 3. Legal Proceedings

The Company is not a party to any material litigation or legal proceedings, or to the best of its knowledge, any threatened litigation or legal proceedings which, in the opinion of management, individually or in the aggregate, would have a material adverse effect on its results of operations or financial condition.

Item 4. Submission of Matters to a Vote of Security Holders

There were no matters submitted to a vote of security holders during the fourth quarter of 2004.

19

PART II

Item 5. Market for Registrant's Equity and Related Share Matters

The Company's Common Stock trades on the New York Stock Exchange ("NYSE") under the symbol "SFI."

The high and low sales prices per share of Common Stock are set forth below for the periods indicated.

Quarter Ended

| | High

| | Low

|

|---|

| 2003 | | | | | | |

| March 31, 2003 | | $ | 29.90 | | $ | 27.05 |

| June 30, 2003 | | $ | 36.60 | | $ | 29.68 |

| September 30, 2003 | | $ | 38.95 | | $ | 35.00 |

| December 31, 2003 | | $ | 40.00 | | $ | 37.25 |

2004 |

|

|

|

|

|

|

| March 31, 2004 | | $ | 42.95 | | $ | 38.60 |

| June 30, 2004 | | $ | 42.75 | | $ | 34.50 |

| September 30, 2004 | | $ | 41.23 | | $ | 37.03 |

| December 31, 2004 | | $ | 45.57 | | $ | 41.32 |

On March 1, 2005, the closing sale price of the Common Stock as reported by the NYSE was $42.75. The Company had 3,236 holders of record of Common Stock as of March 1, 2005.

At December 31, 2004, the Company had five series of preferred stock outstanding: 8.000% Series D Preferred Stock, 7.875% Series E Preferred Stock, 7.800% Series F Preferred Stock, 7.650% Series G Preferred Stock and 7.500% Series I Preferred Stock. Each of the Series D, E, F, G and I preferred stock is publicly traded.

Dividends

The Company's management expects that any taxable income remaining after the distribution of preferred dividends and the regular quarterly or other dividends on its Common Stock will be distributed annually to the holders of the Common Stock on or prior to the date of the first regular quarterly dividend payment date of the following taxable year. The dividend policy with respect to the Common Stock is subject to revision by the Board of Directors. All distributions in excess of dividends on preferred stock or those required for the Company to maintain its REIT status will be made by the Company at the sole discretion of the Board of Directors and will depend on the taxable earnings of the Company, the financial condition of the Company, and such other factors as the Board of Directors deems relevant. The Board of Directors has not established any minimum distribution level. In order to maintain its qualifications as a REIT, the Company intends to pay regular quarterly dividends to its shareholders that, on an annual basis, will represent at least 90.00% of its taxable income (which may not necessarily equal net income as calculated in accordance with GAAP), determined without regard to the deduction for dividends paid and excluding any net capital gains.

Holders of Common Stock will be entitled to receive distributions if, as and when the Board of Directors authorizes and declares distributions. However, rights to distributions may be subordinated to the rights of holders of preferred stock, when preferred stock is issued and outstanding. In addition, most of the Company's borrowings contain covenants that limit the Company's ability to pay distributions on its capital stock based upon the Company's adjusted earnings provided however, that these borrowings generally permit the Company to pay the minimum amount of distributions necessary to maintain the Company's REIT status. In any liquidation, dissolution or winding up of the Company, each outstanding share of Common Stock will entitle its holder to a proportionate share of the assets that remain after the Company pays its liabilities and any preferential distributions owed to preferred shareholders.

20

The following table sets forth the dividends paid or declared by the Company on its Common Stock:

Quarter Ended

| | Shareholder

Record Date

| | Dividend/

Share

|

|---|

| 2003(1) | | | | | |

| March 31, 2003 | | April 15, 2003 | | $ | 0.6625 |

| June 30, 2003 | | July 15, 2003 | | $ | 0.6625 |

| September 30, 2003 | | October 15, 2003 | | $ | 0.6625 |

| December 31, 2003 | | December 15, 2003 | | $ | 0.6625 |

2004(2) |

|

|

|

|

|

| March 31, 2004 | | April 15, 2004 | | $ | 0.6975 |

| June 30, 2004 | | July 15, 2004 | | $ | 0.6975 |

| September 30, 2004 | | October 15, 2004 | | $ | 0.6975 |

| December 31, 2004 | | December 15, 2004 | | $ | 0.6975 |

Explanatory Notes:

- (1)

- For tax reporting purposes, the 2003 dividends were classified as 68.90% ($1.8258) ordinary income, 2.46% ($0.0651) 20.00% capital gain, 1.90% ($0.0503) 15.00% capital gain (post May 5, 2003), 2.67% ($0.0709) 25.00% Section 1250 capital gain and 24.08% ($0.6380) return of capital for those shareholders who held shares of the Company for the entire year.

- (2)

- For tax reporting purposes, the 2004 dividends were classified as 49.15% ($1.3713) ordinary income, 2.20% ($0.0613) 15.00% capital gain, 7.45% ($0.0278) 25.00% Section 1250 capital gain and 41.20% ($1.1496) return of capital for those shareholders who held shares of the Company for the entire year.

The Company declared dividends aggregating $920,000, $585,000, $8.0 million, $11.0 million, $7.8 million, $6.1 million, $87,656 and $7.4 million, respectively, on its Series B, C, D, E, F, G, H and I preferred stock, respectively, for the year ended December 31, 2004. There are no dividend arrearages on any of the preferred shares currently outstanding.

Distributions to shareholders will generally be taxable as ordinary income, although a portion of such dividends may be designated by the Company as capital gain or may constitute a tax-free return of capital. The Company annually furnishes to each of its shareholders a statement setting forth the distributions paid during the preceding year and their characterization as ordinary income, capital gain or return of capital.

The Company intends to continue to declare quarterly distributions on its Common Stock. No assurance, however, can be given as to the amounts or timing of future distributions, as such distributions are subject to the Company's earnings, financial condition, capital requirements, debt covenants and such other factors as the Company's Board of Directors deems relevant. On February 15, 2005, the Company announced that, effective April 1, 2005, its Board of Directors approved an increase in the regular quarterly dividend on its Common Stock for 2005 to $0.7325 per share, representing $2.93 per share on an annualized basis.

21

Disclosure of Equity Compensation Plan Information

Plan category

| | (a)

Number of securities

to be issued upon

exercise of

outstanding options,

warrants and rights

| | (b)

Weighted-average

exercise price of

outstanding options,

warrants and rights

| | (c)

Number of securities

remaining available for

future issuance under

equity compensation

plans (excluding securities

reflected in column (a))

|

|---|

| Equity compensation plans approved by security holders-stock options(1) | | 1,320,611 | | $ | 17.99 | | 913,675 |

| Equity compensation plans approved by security holders-restricted stock awards(2) | | 411,061 | | | N/A | | N/A |

| Equity compensation plans approved by security holders-high performance units(3) | | — | | | N/A | | N/A |

| Equity compensation plans not approved by security holders | | — | | | — | | — |

| | |

| |

| |

|

| Total | | 1,731,672 | | $ | 17.99 | | 913,675 |

| | |

| |

| |

|

Explanatory Notes:

- (1)

- Stock Options—As more fully discussed in Note 10 to the Company's Consolidated Financial Statements, there were approximately 1.3 million stock options outstanding as of December 31, 2004. These 1.3 million options, together with their weighted-average exercise price, have been included in columns (a) and (b), above. The 913,675 figure in column (c) represents the aggregate amount of stock options or restricted stock awards that could be granted under compensation plans approved by the Company's security holders after giving effect to previously issued awards of stock options, shares of restricted stock and other performance awards (see Note 10 to the Company's Consolidated Financial Statements for a more detailed description of the Company's Long-Term Incentive Plan).

- (2)

- Restricted Stock—As of December 31, 2004, the Company has issued 1,206,397 shares of restricted stock. The restrictions on 411,061 of such shares primarily relate to the passage of time for vesting periods which have not lapsed, and are thus not included in the Company's outstanding share balance. These shares have been included in column (a), above.

- (3)

- High Performance Unit Program—In May 2002, the Company's shareholders approved the iStar Financial High Performance Unit Program. The Program is more fully described in the Company's proxy statement dated April 8, 2002 and in Note 10 to the Company's Consolidated Financial Statements. The program entitles the employee participants to receive distributions in the nature of common stock dividends if the total rate of return on the Company's Common Stock exceeds certain performance levels. The first, second and third tranches of the program were completed on December 31, 2002, 2003 and 2004, respectively. As a result of the Company's superior performance during the valuation period for all three tranches, the program participants are entitled to share in distributions equivalent to dividends payable on 819,254 shares, 987,149 shares and 1,031,875 shares of the Company's Common Stock, in the aggregate, as and when such dividends are paid by the Company for the 2002, 2003 and 2004 plan, respectively. Such dividend payments for the first tranche began with the first quarter 2003 dividend, for the second tranche began with the first quarter dividend 2004 and those for the third tranche will begin with the first quarter 2005 dividend and will reduce net income allocable to common stockholders when paid. No shares of the Company's Common Stock will be issued in connection with this program and thus no effect has been reflected in the above table.

22

Item 6. Selected Financial Data

The following table sets forth selected financial data on a consolidated historical basis for the Company. This information should be read in conjunction with the discussions set forth in Item 7—"Management's Discussion and Analysis of Financial Condition and Results of Operations." Certain prior year amounts have been reclassified to conform to the 2004 presentation.

| | For the Years Ended December 31,

| |

|---|

| | 2004

| | 2003

| | 2002

| | 2001

| | 2000

| |

|---|

| | (In thousands, except per share data and ratios)

| |

|---|

| OPERATING DATA: | | | | | | | | | | | | | | | | |

| Interest income | | $ | 353,799 | | $ | 304,391 | | $ | 255,631 | | $ | 254,119 | | $ | 268,011 | |

| Operating lease income | | | 286,389 | | | 232,043 | | | 210,033 | | | 155,980 | | | 148,144 | |

| Other income | | | 54,236 | | | 36,677 | | | 27,993 | | | 30,921 | | | 17,902 | |

| | |

| |

| |

| |

| |

| |

| | Total revenue | | | 694,424 | | | 573,111 | | | 493,657 | | | 441,020 | | | 434,057 | |

| | |

| |

| |

| |

| |