UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-9631 |

|

Cohen & Steers Institutional Realty Shares, Inc. |

(Exact name of registrant as specified in charter) |

|

280 Park Avenue, New York, NY | | 10017 |

(Address of principal executive offices) | | (Zip code) |

|

Adam M. Derechin

Cohen & Steers Capital Management, Inc.

280 Park Avenue

New York, New York 10017 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (212) 832-3232 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | June 30, 2007 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

August 9, 2007

To Our Shareholders:

We are pleased to submit to you our report for the six months ended June 30, 2007. The net asset value at that date was $52.07 per share. In addition, a regular dividend of $0.315 per share was declared for shareholders of record on June 28, 2007 and was paid on June 29, 2007.a

The total return, including income and change in net asset value, for Cohen & Steers Institutional Realty Shares and the comparative benchmarks were:

| | | Six Months

Ended June 30, 2007 | |

| Cohen & Steers Institutional Realty Shares | | | –6.77 | % | |

| FTSE NAREIT Equity REIT Indexb | | | –5.89 | % | |

| S&P 500 Indexb | | | 6.96 | % | |

The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return and the principal value of an investment will fluctuate and shares, if redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Total returns of the fund current to the most recent month-end can be obtained by visiting our Web site at cohenandsteers.com.

Investment Review

Following four years of strong absolute and relative performance, including a 35% total return in 2006 (as measured by the FTSE NAREIT Equity REIT Index) and seven years of positive returns, REITs had generally negative returns in the first half of 2007. REITs began the year on a positive note, buoyed by a January bidding contest between Vornado and The Blackstone Group for control of Equity Office Properties (EOP). Blackstone prevailed, purchasing EOP at a sizable premium, prompting investors at that time to raise valuation estimates for publicly traded real estate securities.

REITs struggled over the remainder of the period, however, declining nearly 20% from their February highs. This reflected concerns over rising interest rates and uncertainty about whether asset pricing would suffer. Expectations for

a Please note that distributions paid by the fund to shareholders are subject to recharacterization for tax purposes. The final tax treatment of these distributions is reported to shareholders after the close of each fiscal year.

b The FTSE NAREIT Equity REIT Index is an unmanaged, market capitalization weighted index of all publicly traded REITs that invest predominantly in the equity ownership of real estate. The index is designed to reflect the performance of all publicly traded equity REITs as a whole. The S&P 500 Index is an unmanaged index of common stocks that is frequently used as a general measure of stock market performance.

1

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

Federal Reserve monetary easing were pushed back as economic growth continued and inflation fears persisted. The possibility that the Fed might in fact raise rates entered the picture, and the yield on the 10-year Treasury bond in June climbed to 5.26%, its highest level in five years; the yield retreated to 5.03% by period end.

Growth rates for real estate companies generally stabilized, after accelerating in the past few years. This signaled an end to the stock-multiple expansion phase of the real estate cycle, and set expectations for more normalized returns for REITs. Put another way, capitalization rate compression for real estate assets is likely over (a cap rate is the inverse of the earnings multiple).

Most property sectors declined. Among the poorest performing sectors were self storage, due to concerns that a slowing economy might materially affect demand; and health care, as these companies are typically more sensitive to rising interest rates, due to the long-term nature of their leases.

Apartments stage partial recovery

Apartments initially underperformed on concerns about the weakening housing market. However, the group's performance improved late in the period when Archstone-Smith, a leading apartment REIT, agreed to be acquired by a partnership sponsored by Tishman Speyer and Lehman Brothers for $22.2 billion, a 22.7% premium to the stock price before a rumor of the deal was published on May 24, 2007. This deal underscored for the market the overall positive prospects for apartment fundamentals and the sustainability of apartment asset pricing. The sector outperformed for the period as a whole.

Merger activity stimulated the hotel sector's relative performance. Late in the quarter, Equity Inns, the third-largest hotel REIT as measured by the number of hotels owned, announced that it would be acquired by an affiliate of Whitehall Street Global Real Estate in a transaction valued at $2.2 billion. This represented a 19% premium to the stock's previous day closing price.

Relative performance hindered by self storage, aided by health care

The fund underperformed its benchmark, hindered by our overweight in the self-storage sector. Our underweight in regional malls was a detractor, as the sector outperformed despite a poor second quarter. Stock selection in the apartment, diversified and hotel sectors also hampered the fund's performance. Factors that aided the fund's relative return included our underweight in health care and stock selection in the office sector.

Investment Outlook

Before REITs can manage a sustainable performance recovery, investors may require more clarity on inflation and economic growth. In our opinion, if the economy gains momentum, it would likely benefit real estate companies; however, it might cause the Fed to raise interest rates, unsettling stock prices, including REITs. A cooling economy, on the other hand, would likely prompt the Fed to cut rates, which could lift stocks, as a rate reduction is not currently expected by the market.

2

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

We believe that a fair degree of pessimism has now been priced into REITs, including the possibility of some decline in property asset values. We believe REITs, on the whole, are attractively valued, with many trading at compelling discounts (more than 20% in some cases) to their underlying net asset values, compared with their long-term average of a 5% premium to NAV. The private equity market continues to value REITs more aggressively than the public market, as evidenced by the continued privatizations of real estate companies.

From a property sector perspective we continue to favor apartments, and believe that recent events underscore our view that a downward trend in owner-occupied housing prices, coupled with tightening credit standards, are clear positives for the sector. In our view, uncertainty in the housing market should ultimately result in lower overall home ownership rates in the next five years, which in turn should benefit apartment owners. We also like the self-storage and office sectors on a stock-specific basis, and believe that the market has taken too negative a view of these sectors.

Sincerely,

| |  | |

|

| MARTIN COHEN | | ROBERT H. STEERS | |

|

| Co-chairman | | Co-chairman | |

|

| | |  | |

|

| | | JAMES S. CORL | |

|

| | | Portfolio Manager | |

|

The views and opinions in the preceding commentary are as of the date stated and are subject to change. This material represents an assessment of the market environment at a specific point in time, should not be relied upon as investment advice and is not intended to predict or depict performance of any investment.

Visit Cohen & Steers online at cohenandsteers.com

For more information about any of our funds, visit cohenandsteers.com, where you'll find daily net asset values, fund fact sheets and portfolio highlights. You can also access newsletters, education tools and market updates covering REIT, utility and preferred securities sectors.

In addition, our Web site contains comprehensive information about our firm, including our most recent press releases, profiles of our senior investment professionals, and an overview or our investment approach.

3

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

Performance Review (Unaudited)

Average Annual Total Returns—For the Periods Ended June 30, 2007

| | | 1 Year | | 5 Years | | Since Inceptiona | |

| Fund | | | 11.64 | % | | | 20.63 | % | | | 20.60 | % | |

The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance information current to the most recent month-end can be obtained by visiting our Web site at cohenandsteers.com. The performance table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The fund's manager has contractually agreed to waive certain fees and/or reimburse the fund for expenses for the life of the fund. Absent such arrangements, returns would have been lower.

a Inception date of February 14, 2000.

4

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

Expense Example (Unaudited)

As a shareholder of the fund, you incur two types of costs: (1) transaction costs and (2) ongoing costs including management fees and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period 01/01/07 – 06/30/07.

Actual Expenses

The first line of the table below provides information about actual account values and expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing cost of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account Value

January 1, 2007 | | Ending

Account Value

June 30, 2007 | | Expenses Paid

During Period*

January 1, 2007–

June 30, 2007 | |

| Actual (–6.77% return) | | $ | 1,000.00 | | | $ | 932.30 | | | $ | 3.59 | | |

| Hypothetical (5% annual return before expenses) | | $ | 1,000.00 | | | $ | 1,021.08 | | | $ | 3.76 | | |

* Expenses are equal to the Fund's annualized expense ratio of 0.75% multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). If the fund had borne all of its expenses that were assumed by the manager, the annualized expense ratio would have been 0.76%

5

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

JUNE 30, 2007

Top Ten Holdings

(Unaudited)

| Security | | Market

Value | | % of

Net Assets | |

| Public Storage | | $ | 76,162,421 | | | | 6.0 | % | |

| Simon Property Group | | | 74,021,415 | | | | 5.9 | | |

| Boston Properties | | | 68,845,833 | | | | 5.5 | | |

| Equity Residential | | | 64,028,016 | | | | 5.1 | | |

| ProLogis | | | 61,639,144 | | | | 4.9 | | |

| Vornado Realty Trust | | | 59,416,300 | | | | 4.7 | | |

| AvalonBay Communities | | | 54,103,001 | | | | 4.3 | | |

| Host Hotels & Resorts | | | 44,497,376 | | | | 3.5 | | |

| SL Green Realty Corp. | | | 43,723,755 | | | | 3.5 | | |

| Macerich Co. | | | 41,777,874 | | | | 3.3 | | |

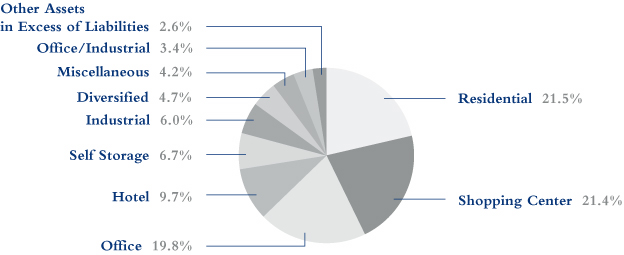

Sector Breakdown

(Based on Net Assets)

(Unaudited)

6

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

SCHEDULE OF INVESTMENTS

June 30, 2007 (Unaudited)

| | | | | Number

of Shares | | Value | |

| COMMON STOCK | | | 97.4 | % | | | | | | | | | |

| DIVERSIFIED | | | 4.7 | % | | | | | | | | | |

| Vornado Realty Trust | | | | | | | 540,935 | | | $ | 59,416,300 | | |

| HEALTH CARE | | | 2.4 | % | | | | | | | | | |

| Health Care Property Investors | | | | | | | 298,700 | | | | 8,641,391 | | |

| Nationwide Health Properties | | | | | | | 32,632 | | | | 887,590 | | |

| Ventas | | | | | | | 556,451 | | | | 20,171,349 | | |

| | | | | | | | 29,700,330 | | |

| HOTEL | | | 9.7 | % | | | | | | | | | |

| Hilton Hotels Corp. | | | | | | | 909,100 | | | | 30,427,577 | | |

| Host Hotels & Resorts | | | | | | | 1,924,627 | | | | 44,497,376 | | |

| Starwood Hotels & Resorts Worldwide | | | | | | | 422,600 | | | | 28,343,782 | | |

| Strategic Hotels & Resorts | | | | | | | 600,700 | | | | 13,509,743 | | |

| Sunstone Hotel Investors | | | | | | | 168,199 | | | | 4,775,170 | | |

| | | | | | | | 121,553,648 | | |

| INDUSTRIAL | | | 6.0 | % | | | | | | | | | |

| AMB Property Corp. | | | | | | | 269,400 | | | | 14,337,468 | | |

| ProLogis | | | | | | | 1,083,289 | | | | 61,639,144 | | |

| | | | | | | | 75,976,612 | | |

| OFFICE | | | 19.8 | % | | | | | | | | | |

| Alexandria Real Estate Equities | | | | | | | 227,673 | | | | 22,043,300 | | |

| BioMed Realty Trust | | | | | | | 764,900 | | | | 19,214,288 | | |

| Boston Properties | | | | | | | 674,100 | | | | 68,845,833 | | |

| Brookfield Properties Corp. | | | | | | | 1,600,575 | | | | 38,909,978 | | |

| Douglas Emmett | | | | | | | 318,900 | | | | 7,889,586 | | |

| Kilroy Realty Corp. | | | | | | | 312,600 | | | | 22,144,584 | | |

| Mack-Cali Realty Corp. | | | | | | | 296,900 | | | | 12,912,181 | | |

| Maguire Properties | | | | | | | 401,900 | | | | 13,797,227 | | |

| SL Green Realty Corp. | | | | | | | 352,924 | | | | 43,723,755 | | |

| | | | | | | | 249,480,732 | | |

See accompanying notes to financial statements.

7

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2007 (Unaudited)

| | | | | Number

of Shares | | Value | |

| OFFICE/INDUSTRIAL | | | 3.4 | % | | | | | | | | | |

| EastGroup Properties | | | | | | | 207,700 | | | $ | 9,101,414 | | |

| Liberty Property Trust | | | | | | | 628,900 | | | | 27,627,577 | | |

| PS Business Parks | | | | | | | 89,587 | | | | 5,677,128 | | |

| | | | | | | | 42,406,119 | | |

| RESIDENTIAL | | | 21.5 | % | | | | | | | | | |

| APARTMENT | | | 20.1 | % | | | | | | | | | |

| Apartment Investment & Management Co. | | | | | | | 576,100 | | | | 29,046,962 | | |

| Archstone-Smith Trust | | | | | | | 239,600 | | | | 14,162,756 | | |

| AvalonBay Communities | | | | | | | 455,106 | | | | 54,103,001 | | |

| BRE Properties | | | | | | | 600,100 | | | | 35,579,929 | | |

| Camden Property Trust | | | | | | | 261,400 | | | | 17,505,958 | | |

| Equity Residential | | | | | | | 1,403,200 | | | | 64,028,016 | | |

| Essex Property Trust | | | | | | | 124,560 | | | | 14,486,328 | | |

| Home Properties | | | | | | | 41,000 | | | | 2,129,130 | | |

| Post Properties | | | | | | | 27,584 | | | | 1,437,954 | | |

| UDR | | | | | | | 807,162 | | | | 21,228,361 | | |

| | | | | | | | 253,708,395 | | |

| MANUFACTURED HOME | | | 1.4 | % | | | | | | | | | |

| Equity Lifestyle Properties | | | | | | | 209,700 | | | | 10,944,243 | | |

| Sun Communities | | | | | | | 215,200 | | | | 6,406,504 | | |

| | | | | | | | 17,350,747 | | |

| TOTAL RESIDENTIAL | | | | | | | | | | | 271,059,142 | | |

| SELF STORAGE | | | 6.7 | % | | | | | | | | | |

| Extra Space Storage | | | | | | | 367,100 | | | | 6,057,150 | | |

| Public Storage | | | | | | | 991,440 | | | | 76,162,421 | | |

| U-Store-It Trust | | | | | | | 133,800 | | | | 2,192,982 | | |

| | | | | | | | 84,412,553 | | |

| SHOPPING CENTER | | | 21.4 | % | | | | | | | | | |

| COMMUNITY CENTER | | | 8.8 | % | | | | | | | | | |

| Developers Diversified Realty Corp. | | | | | | | 450,900 | | | | 23,766,939 | | |

| Equity One | | | | | | | 353,250 | | | | 9,025,537 | | |

See accompanying notes to financial statements.

8

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2007 (Unaudited)

| | | | | Number

of Shares | | Value | |

| Federal Realty Investment Trust | | | | | | | 442,633 | | | $ | 34,197,826 | | |

| Inland Real Estate Corp. | | | | | | | 160,000 | | | | 2,716,800 | | |

| Kimco Realty Corp. | | | | | | | 124,700 | | | | 4,747,329 | | |

| Regency Centers Corp. | | | | | | | 288,728 | | | | 20,355,324 | | |

| Weingarten Realty Investors | | | | | | | 390,092 | | | | 16,032,781 | | |

| | | | | | | | 110,842,536 | | |

| REGIONAL MALL | | | 12.6 | % | | | | | | | | | |

| General Growth Properties | | | | | | | 618,420 | | | | 32,745,339 | | |

| Macerich Co. | | | | | | | 506,890 | | | | 41,777,874 | | |

| Simon Property Group | | | | | | | 795,587 | | | | 74,021,415 | | |

| Taubman Centers | | | | | | | 203,012 | | | | 10,071,425 | | |

| | | | | | | | 158,616,053 | | |

| TOTAL SHOPPING CENTER | | | | | | | | | | | 269,458,589 | | |

| SPECIALTY | | | 1.8 | % | | | | | | | | | |

| Plum Creek Timber Co. | | | | | | | 445,100 | | | | 18,542,866 | | |

| Rayonier | | | | | | | 102,300 | | | | 4,617,822 | | |

| | | | | | | | 23,160,688 | | |

TOTAL COMMON STOCK

(Identified cost—$829,924,594) | | | | | | | | | | | 1,226,624,713 | | |

| | | | | Principal

Amount | | | |

| COMMERCIAL PAPER | | | 2.0 | % | | | | | | | | | |

New Center Asset Trust, 4.15%, due 07/2/07

(Identified cost—$25,522,057) | | | | | | $ | 25,525,000 | | | | 25,522,057 | | |

| TOTAL INVESTMENTS (Identified cost—$855,446,651) | | | 99.4 | % | | | | | | | 1,252,146,770 | | |

| OTHER ASSETS IN EXCESS OF LIABILITIES | | | 0.6 | % | | | | | | | 8,179,916 | | |

NET ASSETS (Equivalent to $52.07 per share based on 24,206,054

shares of capital stock outstanding) | | | 100.0 | % | | | | | | $ | 1,260,326,686 | | |

Note: Percentages indicated are based on the net assets of the fund.

See accompanying notes to financial statements.

9

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

STATEMENT OF ASSETS AND LIABILITIES

June 30, 2007 (Unaudited)

| ASSETS: | |

| Investments in securities, at value (Identified cost—$855,446,651) | | $ | 1,252,146,770 | | |

| Receivable for investment securities sold | | | 7,979,667 | | |

| Dividends receivable | | | 4,495,564 | | |

| Receivable for fund shares sold | | | 3,669,515 | | |

| Total Assets | | | 1,268,291,516 | | |

| LIABILITIES: | |

| Payable for dividends declared | | | 2,720,108 | | |

| Payable for investment securities purchased | | | 2,384,255 | | |

| Payable for fund shares redeemed | | | 2,030,547 | | |

| Payable for manager fees | | | 793,115 | | |

| Payable for directors' fees | | | 6,326 | | |

| Other liabilities | | | 30,479 | | |

| Total Liabilities | | | 7,964,830 | | |

| NET ASSETS applicable to 24,206,054 shares of $0.001 par value of common stock outstanding | | $ | 1,260,326,686 | | |

| NET ASSET VALUE PER SHARE: | |

| ($1,260,326,686 ÷ 24,206,054 shares outstanding) | | $ | 52.07 | | |

| NET ASSETS consist of: | |

| Paid-in-capital | | $ | 762,712,467 | | |

| Dividends in excess of net investment income | | | (10,065,337 | ) | |

| Accumulated undistributed net realized gain on investments | | | 110,979,437 | | |

| Net unrealized appreciation on investments | | | 396,700,119 | | |

| | | $ | 1,260,326,686 | | |

See accompanying notes to financial statements.

10

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

STATEMENT OF OPERATIONS

For the Six Months Ended June 30, 2007 (Unaudited)

| Investment Income: | |

| Dividend income (net of $64,576 of foreign withholding tax) | | $ | 9,638,340 | | |

| Interest income | | | 570,364 | | |

| Total Income | | | 10,208,704 | | |

| Expenses: | |

| Management fees | | | 5,168,988 | | |

| Registration and filing fees | | | 38,982 | | |

| Directors' fees and expenses | | | 31,150 | | |

| Line of credit fees and expenses | | | 11,926 | | |

| Miscellaneous | | | 9,789 | | |

| Total Expenses | | | 5,260,835 | | |

| Reduction of Expenses | | | (91,847 | ) | |

| Net Expenses | | | 5,168,988 | | |

| Net Investment Income | | | 5,039,716 | | |

| Net Realized and Unrealized Gain (Loss) on Investments: | |

| Net realized gain on investments | | | 112,388,724 | | |

| Net change in unrealized appreciation on investments | | | (213,422,374 | ) | |

| Net realized and unrealized loss on investments | | | (101,033,650 | ) | |

| Net Decrease in Net Assets Resulting from Operations | | $ | (95,993,934 | ) | |

See accompanying notes to financial statements.

11

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

STATEMENT OF CHANGES IN NET ASSETS (Unaudited)

| | | For the

Six Months Ended

June 30, 2007 | | For the

Year Ended

December 31, 2006 | |

| Change in Net Assets: | |

| From Operations: | |

| Net investment income | | $ | 5,039,716 | | | $ | 14,825,242 | | |

| Net realized gain on investments | | | 112,388,724 | | | | 175,828,980 | | |

| Net change in unrealized appreciation on investments | | | (213,422,374 | ) | | | 177,345,967 | | |

Net increase (decrease) in net assets resulting from

operations | | | (95,993,934 | ) | | | 368,000,189 | | |

| Dividends and Distributions to Shareholders from: | |

| Net investment income | | | (15,105,053 | ) | | | (15,437,505 | ) | |

| Net realized gain on investments | | | — | | | | (101,394,447 | ) | |

| Tax return of capital | | | — | | | | (7,820,597 | ) | |

| Total dividends and distributions to shareholders | | | (15,105,053 | ) | | | (124,652,549 | ) | |

| Capital Stock Transactions: | |

| Increase in net assets from fund share transactions | | | 29,249,330 | | | | 86,764,476 | | |

| Total increase (decrease) in net assets | | | (81,849,657 | ) | | | 330,112,116 | | |

| Net Assets: | |

| Beginning of period | | | 1,342,176,343 | | | | 1,012,064,227 | | |

| End of perioda | | $ | 1,260,326,686 | | | $ | 1,342,176,343 | | |

a Includes dividends in excess of net investment income of $10,065,337 and $0, respectively.

See accompanying notes to financial statements.

12

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

FINANCIAL HIGHLIGHTS (Unaudited)

The following table includes selected data for a share outstanding throughout each period and other performance information derived from the financial statements. It should be read in conjunction with the financial statements and notes thereto.

| | | For the Six

Months Ended | | For the Year Ended December 31, | |

| Per Share Operating Performance: | | June 30, 2007 | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| Net asset value, beginning of period | | $ | 56.49 | | | $ | 45.56 | | | $ | 45.47 | | | $ | 37.34 | | | $ | 29.41 | | | $ | 30.97 | | |

| Income from investment operations: | |

| Net investment income | | | 0.21 | | | | 0.70 | | | | 0.81 | | | | 0.99 | | | | 1.10 | | | | 1.28 | | |

Net realized and unrealized

gain (loss) on investments | | | (4.00 | ) | | | 15.87 | | | | 5.77 | | | | 13.11 | | | | 9.78 | | | | (0.28 | ) | |

Total income (loss) from

investment operations | | | (3.79 | ) | | | 16.57 | | | | 6.58 | | | | 14.10 | | | | 10.88 | | | | 1.00 | | |

Less dividends and distributions to

shareholders from: | |

| Net investment income | | | (0.63 | ) | | | (0.70 | ) | | | (0.81 | ) | | | (0.99 | ) | | | (1.10 | ) | | | (1.29 | ) | |

| Net realized gain on investments | | | — | | | | (4.59 | ) | | | (5.36 | ) | | | (4.80 | ) | | | (1.53 | ) | | | (1.23 | ) | |

| Tax return of capital | | | — | | | | (0.35 | ) | | | (0.32 | ) | | | (0.18 | ) | | | (0.32 | ) | | | (0.04 | ) | |

Total dividends and

distributions to

shareholders | | | (0.63 | ) | | | (5.64 | ) | | | (6.49 | ) | | | (5.97 | ) | | | (2.95 | ) | | | (2.56 | ) | |

| Net increase (decrease) in net assets | | | (4.42 | ) | | | 10.93 | | | | 0.09 | | | | 8.13 | | | | 7.93 | | | | (1.56 | ) | |

| Net asset value, end of period | | $ | 52.07 | | | $ | 56.49 | | | $ | 45.56 | | | $ | 45.47 | | | $ | 37.34 | | | $ | 29.41 | | |

| Total investment return | | | –6.77 | %a | | | 37.15 | % | | | 14.70 | % | | | 38.78 | % | | | 38.04 | % | | | 3.06 | % | |

| Ratios/Supplemental Data: | |

| Net assets, end of period (in millions) | | $ | 1,260.3 | | | $ | 1,342.2 | | | $ | 1,012.1 | | | $ | 1,006.2 | | | $ | 888.7 | | | $ | 615.7 | | |

Ratio of expenses to average

daily net assets

(before expense reduction) | | | 0.76 | %b | | | 0.77 | % | | | 0.76 | % | | | 0.76 | % | | | 0.77 | % | | | 0.76 | % | |

Ratio of expenses to average

daily net assets

(net of expense reduction) | | | 0.75 | %b | | | 0.75 | % | | | 0.75 | % | | | 0.75 | % | | | 0.75 | % | | | 0.75 | % | |

Ratio of net investment income to

average daily net assets

(before expense reduction) | | | 0.72 | %b | | | 1.26 | % | | | 1.65 | % | | | 2.23 | % | | | 3.24 | % | | | 4.06 | % | |

Ratio of net investment income to

average daily net assets

(net of expense reduction) | | | 0.73 | %b | | | 1.28 | % | | | 1.67 | % | | | 2.24 | % | | | 3.26 | % | | | 4.07 | % | |

| Portfolio turnover rate | | | 32 | %a | | | 46 | % | | | 34 | % | | | 29 | % | | | 35 | % | | | 38 | % | |

a Not annualized.

b Annualized.

See accompanying notes to financial statements.

13

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

NOTES TO FINANCIAL STATEMENTS (Unaudited)

Note 1. Significant Accounting Policies

Cohen & Steers Institutional Realty Shares, Inc. (the fund) was incorporated under the laws of the State of Maryland on October 13, 1999 and is registered under the Investment Company Act of 1940, as amended, as a nondiversified, open-end management investment company. The fund's investment objective is total return.

The following is a summary of significant accounting policies consistently followed by the fund in the preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America (GAAP). The preparation of the financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Portfolio Valuation: Investments in securities that are listed on the New York Stock Exchange are valued, except as indicated below, at the last sale price reflected at the close of the New York Stock Exchange on the business day as of which such value is being determined. If there has been no sale on such day, the securities are valued at the mean of the closing bid and asked prices for the day or, if no asked price is available, at the bid price.

Securities not listed on the New York Stock Exchange but listed on other domestic or foreign securities exchanges or admitted to trading on the National Association of Securities Dealers Automated Quotations, Inc. (Nasdaq) national market system are valued in a similar manner. Securities traded on more than one securities exchange are valued at the last sale price on the business day as of which such value is being determined as reflected on the tape at the close of the exchange representing the principal market for such securities.

Readily marketable securities traded in the over-the-counter market, including listed securities whose primary market is believed by Cohen & Steers Capital Management, Inc. (the manager) to be over-the-counter, but excluding securities admitted to trading on the Nasdaq National List, are valued at the official closing prices as reported by Nasdaq, the National Quotation Bureau, or such other comparable sources as the Board of Directors deems appropriate to reflect their fair market value. If there has been no sale on such day, the securities are valued at the mean of the closing bid and asked prices for the day, or if no asked price is available, at the bid price. Where securities are traded on more than one exchange and also over-the-counter, the securities will generally be valued using the quotations the Board of Directors believes most closely reflect the value of such securities.

Securities for which market prices are unavailable, or securities for which the manager determines that bid and/or asked price does not reflect market value, will be valued at fair value pursuant to procedures approved by the fund's Board of Directors. Circumstances in which market prices may be unavailable include, but are not limited to, when trading in a security is suspended, the exchange on which the security is traded is subject to an unscheduled close or disruption or material events occur after the close of the exchange on which the security is principally traded. In these circumstances, the fund determines fair value in a manner that fairly reflects the market value of the security on the valuation date based on consideration of any information or factors it deems

14

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

NOTES TO FINANCIAL STATEMENTS (Unaudited)—(Continued)

appropriate. These may include recent transactions in comparable securities, information relating to the specific security and developments in the markets.

The fund's use of fair value pricing may cause the net asset value of fund shares to differ from the net asset value that would be calculated using market quotations. Fair value pricing involves subjective judgments and it is possible that the fair value determined for a security may be materially different than the value that could be realized upon the sale of that security.

Short-term debt securities, which have a maturity date of 60 days or less, are valued at amortized cost, which approximates value.

Security Transactions and Investment Income: Security transactions are recorded on trade date. Realized gains and losses on investments sold are recorded on the basis of identified cost. Interest income is recorded on the accrual basis. Discounts are accreted and premiums are amortized over the life of the respective securities. Dividend income is recorded on the ex-dividend date. The fund records distributions received in excess of income from underlying investments as a reduction of cost of investments and/or realized gain. Such amounts are based on estimates if actual amounts are not available and actual amounts of income, realized gain and return of capital may differ from the estimated amounts. The fund adjusts the estimated amounts of the components of distributions (and consequently its net investment income) as an increase to unrealized appreciation/(depre ciation) and realized gain/(loss) on investments as necessary once the issuers provide information about the actual composition of the distributions.

Dividends and Distributions to Shareholders: Dividends from net investment income and capital gain distributions are determined in accordance with U.S. federal income tax regulations, which may differ from GAAP. Dividends from net investment income are declared and paid quarterly. Net realized capital gains, unless offset by any available capital loss carryforward, are distributed to shareholders annually. Dividends and distributions to shareholders are recorded on the ex-dividend date and are automatically reinvested in full and fractional shares of the fund based on the net asset value per share at the close of business on the ex-dividend date unless the shareholder has elected to have them paid in cash.

Distributions paid by the fund are subject to recharacterization for tax purposes. Based upon the results of operations for the six months ended June 30, 2007, the manager considers it likely that a portion of the dividends will be reclassified to return of capital and distributions of net realized capital gains upon the final determination of the fund's taxable income for the year.

Federal Income Taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interest of the shareholders, by complying with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies, and by distributing substantially all of its taxable earnings to its shareholders. Accordingly, no provision for federal income or excise tax is necessary.

15

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

NOTES TO FINANCIAL STATEMENTS (Unaudited)—(Continued)

Note 2. Investment Management Fees and Other Transactions with Affiliates

Investment Management Fees: The manager serves as the fund's investment manager, pursuant to a management agreement (the management agreement). Under the terms of the management agreement, the manager provides the fund with the day-to-day investment decisions and generally manages the fund's investments in accordance with the stated policies of the fund, subject to the supervision of the fund's Board of Directors. For the services provided to the fund, the manager receives a fee, accrued daily and paid monthly, at the annual rate of 0.75% of the average daily net assets of the fund.

The manager is also responsible, under the management agreement, for the performance of certain administrative functions for the fund. Additionally, the manager pays certain expenses of the fund, including administration and custody fees, transfer agent fees, professional fees, and reports to shareholders.

The manager has contractually agreed to reimburse the fund so that its total annual operating expenses do not exceed 0.75% of the average daily net assets. This commitment will remain in place for the life of the fund.

Directors' and Officers' Fees: Certain directors and officers of the fund are also directors, officers, and/or employees of the manager. The fund does not pay compensation to any affiliated directors and officers.

Note 3. Purchases and Sales of Securities

Purchases and sales of securities, excluding short-term investments, for the six months ended June 30, 2007 totaled $453,673,215 and $433,464,522, respectively.

Note 4. Income Tax Information

As of June 30, 2007, the federal tax cost and net unrealized appreciation were as follows:

| Cost for federal income tax purposes | | $ | 855,446,651 | | |

| Gross unrealized appreciation | | $ | 411,824,486 | | |

| Gross unrealized depreciation | | | (15,124,367 | ) | |

| Net unrealized appreciation | | $ | 396,700,119 | | |

16

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

NOTES TO FINANCIAL STATEMENTS (Unaudited)—(Continued)

Note 5. Capital Stock

The fund is authorized to issue 100 million shares of capital stock at a par value of $0.001 per share. The Board of Directors of the fund is authorized to reclassify and issue any unissued shares of the fund without shareholder approval. Transactions in fund shares were as follows:

| | | For the

Six Months Ended

June 30, 2007 | | For the

Year Ended

December 31, 2006 | |

| | | Shares | | Amount | | Shares | | Amount | |

| Sold | | | 5,354,887 | | | $ | 311,703,615 | | | | 8,760,054 | | | $ | 463,867,464 | | |

Issued as reinvestment of dividends

and distributions | | | 180,088 | | | | 9,850,406 | | | | 1,806,418 | | | | 98,124,763 | | |

| Redeemed | | | (5,086,845 | ) | | | (292,304,691 | ) | | | (6,403,435 | ) | | | (344,369,988 | ) | |

| Redeemed in kinda | | | — | | | | — | | | | (2,618,726 | ) | | | (130,857,763 | ) | |

| Net increase (decrease) | | | 448,130 | | | $ | 29,249,330 | | | | 1,544,311 | | | $ | 86,764,476 | | |

a During the year ended December 31, 2006, certain shareholders of the fund were permitted to redeem shares in-kind. As a result, the fund realized a net gain of $73,498,001 for financial reporting purposes.

Note 6. Borrowings

The fund, in conjunction with other Cohen & Steers funds, is a party to a $150,000,000 syndicated credit agreement (the credit agreement) with State Street Bank and Trust Company, as administrative agent and operations agent, and the lenders identified in the credit agreement, which expires December 2007. The fund pays a commitment fee of 0.10% per annum on its proportionate share of the unused portion of the credit agreement.

During the six months ended June 30, 2007, the fund did not utilize the line of credit.

Note 7. Other

In the normal course of business, the fund enters into contracts that provide general indemnifications. The fund's maximum exposure under these arrangements is dependent on claims that may be made against the fund in the future and, therefore, cannot be estimated; however, based on experience, the risk of material loss from such claims is considered remote.

17

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

NOTES TO FINANCIAL STATEMENTS (Unaudited)—(Continued)

Note 8. New Accounting Pronouncements

In July 2006, the Financial Accounting Standards Board (FASB) issued Interpretation 48, Accounting for Uncertainty in Income Taxes—an interpretation of FASB Statement 109 (FIN 48). FIN 48 clarifies the accounting for income taxes by prescribing the minimum recognition threshold a tax position must meet before being recognized in the financial statements. FIN 48 is effective for fiscal years beginning after December 15, 2006. An assessment of the fund's tax positions has been made and it has been determined that there is no impact to the fund's financial statements.

In September 2006, Statement of Financial Accounting Standards No. 157, Fair Value Measurements (SFAS 157), was issued and is effective for fiscal years beginning after November 15, 2007. SFAS 157 defines fair value, establishes a framework for measuring fair value and expands disclosures about fair value measurements. Management is currently evaluating the impact the adoption of SFAS 157 will have on the fund's financial statements.

18

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

OTHER INFORMATION

A description of the policies and procedures that the fund uses to determine how to vote proxies relating to portfolio securities is available (i) without charge, upon request, by calling 800-330-7348, (ii) on our Web site at cohenandsteers.com or (iii) on the Securities and Exchange Commission's Web site at http://www.sec.gov. In addition, the fund's proxy voting record for the most recent 12-month period ended June 30 is available (i) without charge, upon request, by calling 800-330-7348 or (ii) on the SEC's Web site at http://www.sec.gov.

The fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The fund's Forms N-Q are available (i) without charge, upon request by calling 800-330-7348, or (ii) on the SEC's Web site at http://www.sec.gov. In addition, the Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330.

Please note that the distributions paid by the fund to shareholders are subject to recharacterization for tax purposes. The fund may also pay distributions in excess of the fund's net investment company taxable income and this excess would be a tax-free return of capital distributed from the fund's assets. The final tax treatment of all distributions is reported to shareholders on their 1099-DIV forms, which are mailed after the close of each calendar year.

19

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

APPROVAL OF MANAGEMENT AGREEMENT

The board of directors of the fund, including a majority of the directors who are not parties to the fund's Management Agreement, or interested persons of any such party ("Independent Directors"), has the responsibility under the 1940 Act to approve the fund's Management Agreement for its initial two year term and its continuation annually thereafter at a meeting of the board called for the purpose of voting on the approval or continuation. At a meeting held in person on March 6, 2007, the Management Agreement was discussed and was unanimously continued for a one-year term by the fund's board, including the Independent Directors. The Independent Directors were represented by independent counsel who assisted them in their deliberations during the meeting and executive session.

In considering whether to continue the Management Agreement, the board reviewed materials provided by the fund's investment manager (the "Investment Manager") and fund counsel which included, among other things, fee, expense and performance information compared to peer funds ("Peer Funds") prepared by an independent data provider, supplemental performance and summary information prepared by the Investment Manager, sales and redemption data for the fund and memoranda outlining the legal duties of the board. The board also spoke directly with representatives of the independent data provider and met with investment advisory personnel. In addition, the board considered information provided from time to time by the Investment Manager throughout the year at meetings of the board, including presentations by portfolio managers relating to the investment performance of the fund and the investment strategies used in pursuing the fund's objective. In p articular, the board considered the following:

(i) The nature, extent and quality of services to be provided by the Investment Manager: The board reviewed the services that the Investment Manager provides to the fund, including, but not limited to, making the day-to-day investment decisions for the fund, and generally managing the fund's investments in accordance with the stated policies of the fund. The board also discussed with officers and portfolio managers of the fund the amount of time the Investment Manager dedicates to the fund and the types of transactions that were being done on behalf of the fund. Additionally, the board took into account the services provided by the Investment Manager to its other funds, including those that invest substantially in real estate securities and have investment objectives and strategies similar to the fund.

The board next considered the education, background and experience of the Investment Manager's personnel, noting particularly that the favorable history and reputation of the portfolio managers for the fund has had, and would likely continue to have, a favorable impact on the success of the fund. The board further noted the Investment Manager's ability to attract quality and experienced personnel. After consideration of the above factors, among others, the board concluded that the nature, quality and extent of services provided by the Investment Manager are adequate and appropriate.

(ii) Investment performance of the fund and the Investment Manager: The board considered the investment performance of the fund compared to Peer Funds and compared to relevant benchmarks. The board noted that the fund had outperformed the Peer Funds and benchmark during the one, three and five year periods In particular, the board noted that among the Peer Funds, the fund ranked second in total returns for each of the

20

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

3- and 5-year periods and third in total returns for the one-year period, placing the fund in the first quartile among its Peer Funds over all periods. The board also considered the Investment Manager's performance in managing other real estate funds. The board then determined that fund performance, in light of all the considerations noted above, was satisfactory.

(iii) Cost of the services to be provided and profits to be realized by the Investment Manager from the relationship with the fund: Next, the board considered the advisory fees payable by the fund as well as total expense ratios. As part of their analysis, the board gave substantial consideration to the fee and expense analyses provided by the independent data provider. The board noted that the advisory fee was at the median and that the total expense ratio (on a gross and net basis) was below the median and in the first quartile versus the Peer Funds. The board further noted that the Investment Manager has contractually agreed to reimburse the fund so that its total annual operating expenses never exceed 0.75% of average daily net assets. In light of the considerations above, the board concluded that the fund's expense structure was competitive in the peer group.

The board also reviewed information regarding the profitability to the Investment Manager of its relationship with the fund. The board considered the level of the Investment Manager's profits and whether the profits were reasonable for the Investment Manager. The board took into consideration other benefits to be derived by the Investment Manager in connection with the Management Agreement, noting particularly the research and related services, within the meaning of Section 28(e) of the Securities Exchange Act of 1934, as amended, that the Investment Manager receives by allocating the fund's brokerage transactions.

(iv) The extent to which economies of scale would be realized as the fund grows and whether fee levels would reflect such economies of scale: The board noted that the Investment Manager pays certain operating costs of the fund and reimburses the fund to the extent that total expenses exceed the advisory fee rate; thus, the shareholders only incur the advisory fee costs. Consequently, the board determined that there were not at this time significant economies of scale that were not being shared with shareholders.

(v) Comparison of services rendered and fees paid to those under other investment advisory contracts, such as contracts of the same and other investment advisers or other clients: As discussed above in (i) and (iii), the board compared both the services rendered and the fees paid under the Management Agreement to those under other investment advisory contracts of other investment advisers managing Peer Funds. The board was also provided with an industry study analyzing differences between funds and institutional accounts and the services and fees associated with each and compared the services rendered, fees paid and profitability under the Management Agreement to the Investment Manager's other advisory contracts with institutional and other clients with similar investment mandates. The board determined that on a comparative basis the fees under the Management Agre ement were reasonable in relation to the services provided.

No single factor was cited as determinative to the decision of the board. Rather, after weighing all of the considerations and conclusions discussed above, the board, including the Independent Directors, unanimously approved the continuation of the Management Agreement.

21

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

Meet the Cohen & Steers family of open-end funds:

COHEN & STEERS

REALTY SHARES

• Designed for investors seeking maximum total return, investing primarily in REITs

• Symbol: CSRSX

COHEN & STEERS

REALTY INCOME FUND

• Designed for investors seeking high current income, investing primarily in REITs

• Symbols: CSEIX, CSBIX, CSCIX, CSDIX

COHEN & STEERS

INTERNATIONAL REALTY FUND

• Designed for investors seeking maximum total return, investing primarily in international real estate securities

• Symbols: IRFAX, IRFCX, IRFIX

COHEN & STEERS

DIVIDEND VALUE FUND

• Designed for investors seeking high current income and long-term growth of income and capital appreciation, investing primarily in dividend paying common stocks and preferred stocks

• Symbols: DVFAX, DVFCX, DVFIX

COHEN & STEERS

INSTITUTIONAL GLOBAL REALTY SHARES

• Designed for investors seeking maximum total return, investing primarily in global real estate securities

• Symbol: GRSIX

COHEN & STEERS

INSTITUTIONAL REALTY SHARES

• Designed for institutional investors seeking maximum total return, investing primarily in REITs

• Symbol: CSRIX

COHEN & STEERS

REALTY FOCUS FUND

• Designed for investors seeking maximum capital appreciation, investing in a limited number of REITs and other real estate securities

• Symbols: CSFAX, CSFBX, CSFCX, CSSPX

COHEN & STEERS

UTILITY FUND

• Designed for investors seeking maximum total return, investing primarily in utilities

• Symbols: CSUAX, CSUBX, CSUCX, CSUIX

COHEN & STEERS

ASIA PACIFIC REALTY SHARES

• Designed for investors seeking maximum total return, investing primarily in real estate securities located in the Asia Pacific region

• Symbols: APFAX, APFCX, APFIX

COHEN & STEERS

EUROPEAN REALTY SHARES

• Designed for investors seeking maximum total return, investing primarily in real estate securities located in Europe

• Symbols: EURAX, EURCX, EURIX

Please consider the investment objectives, risks, charges and expenses of the fund carefully before investing. A prospectus containing this and other information can be obtained by calling 800-330-7348 or by visiting cohenandsteers.com. Please read the prospectus carefully before investing.

Cohen & Steers Securities, LLC, Distributor

22

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

OFFICERS AND DIRECTORS

Robert H. Steers

Director and co-chairman

Martin Cohen

Director and co-chairman

Bonnie Cohen

Director

George Grossman

Director

Richard E. Kroon

Director

Richard J. Norman

Director

Frank K. Ross

Director

Willard H. Smith Jr.

Director

C. Edward Ward, Jr.

Director

Adam M. Derechin

President and chief executive officer

Joseph M. Harvey

Vice president

James S. Corl

Vice president

John E. McLean

Secretary

James Giallanza

Treasurer and chief financial officer

Lisa D. Phelan

Chief compliance officer

KEY INFORMATION

Manager

Cohen & Steers Capital Management, Inc.

280 Park Avenue

New York, NY 10017

(212) 832-3232

Fund Subadministrator and Custodian

State Street Bank and Trust Company

One Lincoln Street

Boston, MA 02111

Transfer Agent

Boston Financial Data Services, Inc.

2 Heritage Drive

North Quincy, MA 02171

(800) 437-9912

Legal Counsel

Stroock & Stroock & Lavan LLP

180 Maiden Lane

New York, NY 10038

Distributor

Cohen & Steers Securities, LLC

280 Park Avenue

New York, NY 10017

Nasdaq Symbol: CSRIX

Web site: cohenandsteers.com

This report is authorized for delivery only to shareholders of Cohen & Steers Institutional Realty Shares, Inc. unless accompanied or preceded by the delivery of a currently effective prospectus setting forth details of the fund. Past performance is of course no guarantee of future results and your investment may be worth more or less at the time you sell.

23

COHEN & STEERS

INSTITUTIONAL REALTY SHARES

280 PARK AVENUE

NEW YORK, NY 10017

SEMIANNUAL REPORT

JUNE 30, 2007

Item 2. Code of Ethics.

Not applicable.

Item 3. Audit Committee Financial Expert.

Not applicable.

Item 4. Principal Accountant Fees and Services.

Not applicable.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Schedule of Investments.

Included in Item 1 above.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

None.

Item 11. Controls and Procedures.

(a) The registrant’s principal executive officer and principal financial officer have concluded, based upon their evaluation of the registrant’s disclosure controls and procedures as conducted within 90 days of the filing date of this report, that these disclosure controls and procedures provide reasonable assurance that material information required to be disclosed by the registrant in the report it files or submits on Form N-CSR is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange Commission’s rules and forms

and that such material information is accumulated and communicated to the registrant’s management, including its principal executive officer and principal financial officer, as appropriate, in order to allow timely decisions regarding required disclosure.

(b) There were no changes in the registrant’s internal control over financial reporting that occurred during the second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the registrant’s internal control over financial reporting.

Item 12. Exhibits.

(a)(1) Not applicable.

(a)(2) Certifications of principal executive officer and principal financial officer as required by Rule 30a-2(a) under the Investment Company Act of 1940.

(a)(3) Not applicable.

(b) Certifications of principal exec utive officer and principal financial officer as required by Rule 30a- 2(b) under the Investment Company Act of 1940.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

COHEN & STEERS INSTITUTIONAL REALTY SHARES, INC.

| By: | /s/ Adam M. Derechin | | |

| Name: Adam M. Derechin |

| Title: President and Chief Executive Officer |

| |

| Date: August 29, 2007 | | |

| | | | | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By: | /s/ Adam M. Derechin | |

| Name: | Adam M. Derechin |

| Title: | President and Chief Executive Officer |

| | (principal executive officer) |

| | |

| By: | /s/ James Giallanza | |

| Name: | James Giallanza |

| Title: | Treasurer |

| | (principal financial officer) |

| | |

| | |

| Date: August 29, 2007 |

| | | | | | |