UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(X) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year endedMarch 31, 2009

Commission File Number1-7375

COMMERCE GROUP CORP.

(Exact name of registrant as specified in its charter)

WISCONSIN

39-6050862

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

6001 North 91st Street

Milwaukee, Wisconsin 53225-1795

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code:(414) 462-5310

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Name of each exchange on which registered

Common Shares $0.10 par value

Pink Sheets

Common Shares $0.10 par value

Over the Counter Bulletin Board (OTCBB)

Common Shares $0.10 par value

Berlin-Bremen Stock Exchange (C9G)

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ �� ] No [x]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [x]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [x] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [x]

1

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

Large accelerated filer [ ] | | Accelerated filer [ ] |

Non-accelerated filer [ ] | | Smaller reporting company [x] |

(Do not check if a smaller reporting company) | | |

Indicate by check mark whether the issuer is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [x]

The aggregate market value of the 19,505,778 registrant’s common shares held by nonaffiliates of the registrant based on the closing sale price of the OTC BB on July 24, 2009 was approximately $975,289.

At July 24, 2009 there were 30,750,869 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

2

COMMERCE GROUP CORP.

2009 FORM 10-K ANNUAL REPORT

For the Fiscal Year Ended March 31, 2009

TABLE OF CONTENTS

Page

PART I

Item 1.

Business

4

Item 1A.

Risk Factors

15

Item 2.

Properties

16

Item 3.

Legal Proceedings

28

Item 4.

Submission of Matters to a Vote of Security Holders

28

PART II

Item 5.

Market for the Company’s Common Stock and Related Stockholders’ Matters

29

Item 6.

Selected Financial Data

30

Item 7.

Management’s Discussion and Analysis of Financial Condition

and Results of Operations

31

Item 7(a).

Quantitative and Qualitative Disclosures About Market Risk

42

Item 8.

Financial Statements and Supplementary Data

44

Item 9.

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

77

Item 9(a).

Controls and Procedures

77

Item 9(b)

Other Information

79

PART III

Item 10.

Directors and Executive Officers of the Registrant

80

Item 11.

Executive Compensation

85

Item 12.

Security Ownership of Certain Beneficial Owners and Management

91

Item 13.

Certain Relationships and Related Transactions

92

Item 14.

Principal Accounting Fees and Services

95

PART IV

Item 15.

Exhibits, Financial Statement Schedules and Reports on Form 8-K

97

Subsidiaries

Consent of Chisholm, Bierwolf, Nilson & Morrill, LLC

Certification Pursuant to Section 302

Certification Pursuant to Section 302

Certification Pursuant to Section 906

Certification Pursuant to Section 906

3

PART I

Item 1. Business

Glossary of Selected Mining Terms

Cut-off Grade | The minimum grade of ore used to establish reserves. |

Doré | Unrefined gold and silver bullion consisting of approximately 90% precious metals that will be further refined to almost pure metal. |

Development Stage | A “development stage” project is one which is undergoing preparation of an established commercially mineable deposit for its extraction but which is not yet in production. This stage occurs after completion of a feasibility study. |

Exploration Stage | An “exploration stage” prospect is one which is not in either the development or production stage. |

Fault | A surface or zone of rock fracture along which there has been displacement. |

Feasibility Study | An engineering study designed to define the technical, economic, and legal viability of a mining project with a high degree of reliability. |

Formation | A distinct layer of sedimentary rock of similar composition. |

Grade | The metal content of ore, usually expressed in troy ounces per ton (2,000 pounds) or in grams per ton or metric tons which contain 2,204.6 pounds or 1,000 kilograms. This report refers to ounces per ton. |

Heap Leaching | A method of recovering gold or other precious metals from a heap of ore placed on an impervious pad, whereby a dilute leaching solution is allowed to percolate through the heap, dissolving the precious metal, which is subsequently captured and recovered. |

Mineralized Material | The term “mineralized material” refers to material that is not included in the reserve as it does not meet all of the criteria for adequate demonstration for economic or legal extraction. |

Mining | Mining is the process of extraction and beneficiation of mineral reserves to produce a marketable metal or mineral product. Exploration continues during the mining process and, in many cases, mineral reserves are expanded during the life of the mine operations as the exploration potential of the deposit is realized. |

4

Net Smelter Return Royalty | A defined percentage of the gross revenue from a resource extraction operation, less a proportionate share or transportation, insurance, and processing costs. |

Outcrop | That part of a geologic formation or structure that appears at the surface of the earth. |

Probable Reserves | Reserves for which quantity and grade and/or quality are computed from information similar to that used for Proven Reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for Proven Reserves, is high enough to assume continuity between points of observation. |

Production Stage | A “production stage” project is actively engaged in the process of extraction and beneficiation of mineral reserves to produce a marketable metal or mineral product. |

Proven Reserves | Reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling, and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well-defined that size, shape, depth and mineral content of reserves are well established. |

Reclamation | The process of returning land to another use after mining is completed. |

Recoverable | That portion of metal contained in ore that can be extracted by processing. |

Reserves | That part of a mineral deposit which could be economically and legally extracted or produced at the time of reserve determination. |

Run-of-Mine | Mined ore of a size that can be processed without further crushing. |

Strip Ratio | The ratio between tonnage of waste and ore in an open pit mine. |

Waste | Barren rock or mineralized material that is too low in grade to be economically processed. |

5

Cautionary Statement for Purposes of the “Safe Harbor” Provisions of the Private Securities Litigation Reform Act of 1995.

The matters discussed in this annual report on Form 10-K, when not historical matters, are forward-looking statements that involve a number of risks and uncertainties that could cause actual results to differ materially from projections or estimates contained herein. Such forward-looking statements include, among others, future expenditures, cash requirement predictions and the ability to finance continuing operations. Factors that could cause actual results to differ materially from these forward-looking statements include, among others, the factors described in this annual report on Form 10-K. Many of these factors are beyond our ability to control or predict. We disclaim any intent or obligation to update our forward-looking statements, either as a result of receiving new information, the occurrence of future events, or otherwise.

General

Commerce Group Corp. (“Commerce,” the “Company,” and/or the “Registrant” and reference to these identifications such as “we,” “our,” and “us” may be used herein to refer to Commerce or to any or all of wholly-owned subsidiaries of Commerce) is one of the only precious metals company that has produced gold and silver in the past twenty or more years in the Republic of El Salvador, Central America. Starting in 1968, for periods during the 1970's and 1980's Commerce was operative in the exploration, exploitation, development, and production of precious metals in El Salvador.

At the present time, Commerce is not in production and its permits from the Government of El Salvador to mine material, operate its mill facility and explore the concessions granted to it have been suspended. Commerce is involved in legal proceedings challenging the actions of the Government of El Salvador. Commerce’s current objectives are to restore its rights through the legal process, to restructure in order to obtain required financing, and to then continue with its plans to explore and to produce gold and silver.

Since the death of Commerce’s long-time Chairman Edward L. Machulak on October 21, 2007, the Company has been trying to find a compatible acquisition, merger, or other business arrangement that would enable it to proceed with its plans. On March 7, 2008, Commerce and Manti Holdings, LLC (Manti) entered into an agreement in which Manti was given an exclusive thirty-day option to conduct a review of Commerce’s San Sebastian property, with a view toward a pre-defined transaction. The general terms of the understanding reached between Commerce and Manti were stated in Exhibit 99.1 of Commerce’s Form 8-K filed on March 11, 2008. Since then, Manti decided not to continue its efforts to enter into a transaction relating to Commerce's San Sebastian Gold Mine in the Country of El Salvador. Therefore, Commerce's directors and officers continue to seek a compatible financial or business arrangemen t. Reference is made to Commerce’s Form 8-K filed on August 4, 2008.

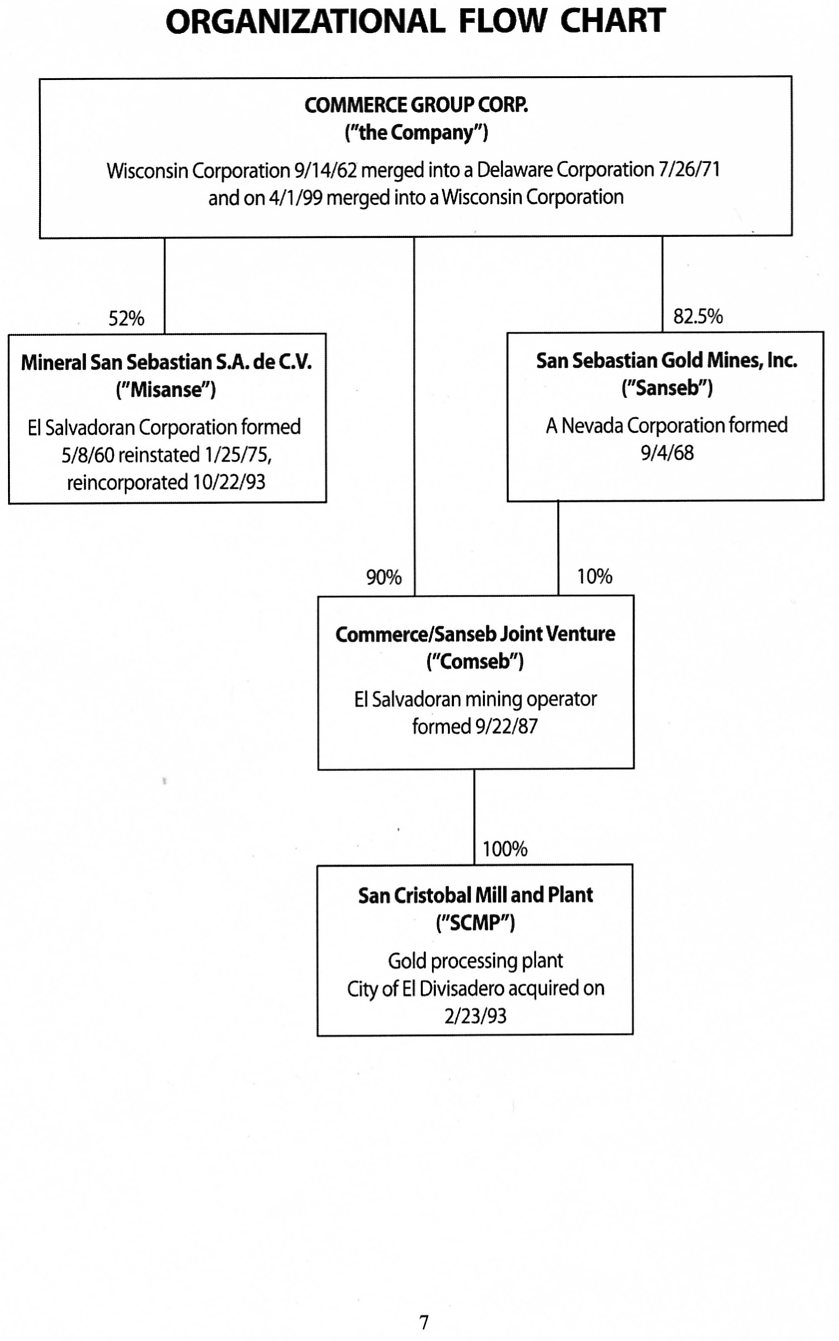

Commerce has been a Wisconsin-chartered corporation since its merger from a State of Delaware corporation on April 1, 1999, and its corporate headquarters since its inception has been based in Milwaukee, Wisconsin. Commerce was organized in 1962 and its common shares have been publicly traded since 1968. The Company’s shares have been trading on the Over the Counter Bulletin Board (OTCBB) under the trade symbol CGCO.OB, on the Pink Sheets under the trade symbol of CGCO.PK, and on the Berlin-Bremen Stock Exchange under the trade symbol of C9G since October 2006. The organizational chart on the following page reflects the mining organization in El Salvador as of March 31, 2009.

6

7

Company’s Website

Commerce has a website located at http://www.commercegroupcorp.com. This website can be used to access recent news releases, U.S. Securities and Exchange Commission filings, the Company’s Annual Report, Proxy Statement, Board Committee Charter, and other items of interest. The contents of the Company’s website are not incorporated into this document. The U.S. Securities and Exchange Commission filings, including supplemental schedules and exhibits can also be accessed free of charge through the U.S. Securities and Exchange Commission’s website at: http://www.sec.gov.

Precious Metal Mining

Commerce’s ultimate objective is to enhance the value of its shares by locating, developing and producing gold and silver in the Republic of El Salvador.

Commerce does business in the Republic of El Salvador through a joint venture with San Sebastian Gold Mines, Inc., a Nevada corporation. Commerce owns 82½% of the shares of San Sebastian Gold Mines, Inc., and owns a 90% interest in the joint venture. This joint venture was organized on September 22, 1987, and has been named the Commerce/Sanseb Joint Venture (“Joint Venture”).

In the past, Commerce produced gold and silver from material mined at the San Sebastian Gold Mine located near the city Santa Rosa de Lima. On July 23, 1987, Commerce secured the concession to operate at this 304-acre site from the El Salvadoran Department of Hydrocarbons and Mines.

In 1993, Commerce acquired a mill for processing gold and silver, known as the San Cristobal Mill and Plant. This facility is located on the Pan American Highway west of the city of El Divisadero. Commerce purchased the equipment on February 23, 1993 and signed a lease for the site on November 12, 1993.

On September 6, 2002, Commerce agreed to cancel the concession for the exploitation of the San Sebastian Gold Mine obtained on July 23, 1987, in exchange for a new concession. On August 18, 2003 the El Salvadoran Ministry of Economy issued a twenty-year concession. On May 20, 2004 the Government of El Salvador extended the exploitation concession at the San Sebastian Gold Mine for a period of thirty years.

Commerce applied for and received environmental permits to mine gold ore at the San Sebastian Gold Mine site, and process ore at the San Cristobal Mill and Plant. On October 15, 2002, the El Salvador Ministry of Environment and Natural Resources (“MARN”) issued an environmental permit for the San Cristobal Mill and Plant. On October 20, 2002, MARN issued an environmental permit under Resolution 493-2002 for the new San Sebastian Gold Mine exploitation concession. Financial security bonds were submitted as required.

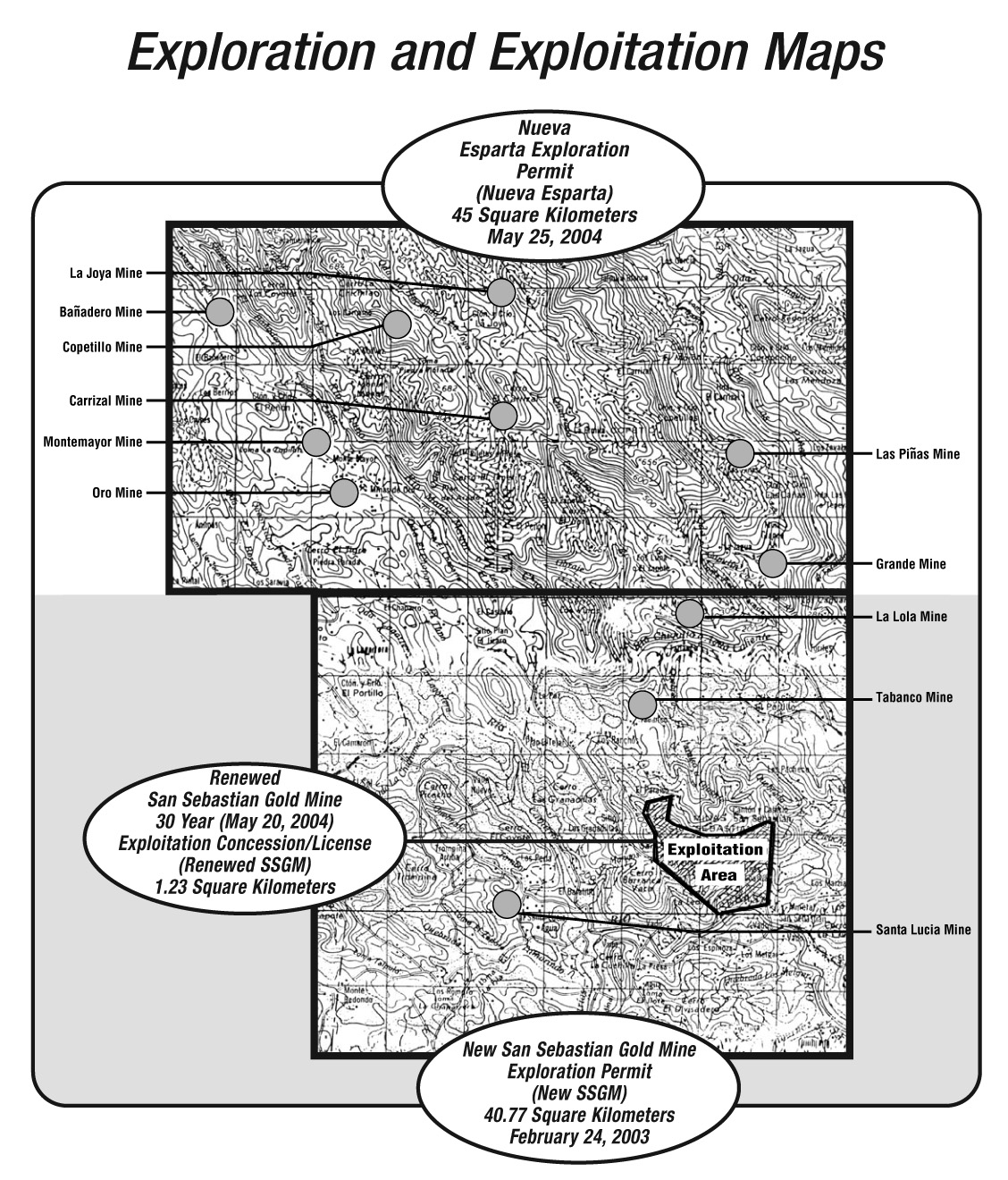

On March 3, 2003, the Government of El Salvador granted Commerce a new exploration license for a 41-square kilometer area (10,374 acres), which surrounded the site of the San Sebastian Gold Mine and included three other formerly-operated mines (the “New San Sebastian Exploration License”).

On May 25, 2004, the Government of El Salvador granted Commerce a new exploration license for an additional 45 square kilometers of area (11,115 acres) to the North of and abutting the New San Sebastian Exploration License area. This new license area encompassed eight formerly-operated gold and silver mines (the “Nueva Esparta Exploration License”).

8

Then, on or about September 13, 2006, MARN notified Commerce that it revoked the environmental permits issued for the San Sebastian Gold Mine exploitation concession and the San Cristobal Mill and Plant, effectively terminating Commerce right to operate. On October 10, 2006, Commerce applied to MARN for an environmental permit for its exploration of the New San Sebastian Exploration License and the Nueva Esparta License. MARN did not respond to the request and on March 8, 2007, Commerce applied to the El Salvador Ministry of Economy for an extension of these exploration licenses. On October 28, 2008, the Ministry of Economy denied Commerce’s application citing Commerce’s failure to secure an environment permit.

On December 6, 2006, Commerce’s legal counsel filed with the El Salvadoran Court of Administrative Litigation of the Supreme Court of Justice two complaints challenging the government’s revocation of Commerce’s permits for the San Sebastian Gold Mine and the other for the San Cristobal Mill and Plant. On January 20, 2009, Commerce’s legal counsel filed a challenge in the Courts to the government’s refusal to honor Commerce’s request to extend the New San Sebastian Exploration License and the Nueva Esparta License. On March 17, 2009, Commerce delivered a Notice of Intent to commence international arbitration proceedings against the Government of El Salvador under the Central America Free Trade Agreement-Dominican Republic (CAFTA-DR). The parties had 90 days to resolve their dispute amicably, after which the Company had the right to commence arbitration proceedings against the Go vernment of El Salvador to claim significant monetary damages. Since the Company received no response to the Notice of Intent, it submitted to the International Centre for Settlement of Investment Disputes (ICSID) a notice of arbitration to commence international arbitration proceedings against the Government of El Salvador under CAFTA-DR on July 2, 2009.

Operations

The Company is not producing gold or silver at the present time, and will not be able to continue in operation unless its permits are restored.

Commerce and San Sebastian Gold Mines, Inc. began producing gold at the San Sebastian Gold Mine site in 1968. In February, 1978, they suspended operations because of the war in El Salvador. The mill which had been constructed on site at the San Sebastian Gold Mine was destroyed during the war. Commerce returned to the site in 1985, and obtained a concession to resume production in 1987. In 1993, Commerce acquired the San Cristobal Mill and Plant, and from March 1995 through December 31, 1999 produced 22,710 ounces of bullion containing 13,305 ounces of gold and 4,667 ounces of silver at this facility, processing material from the San Sebastian Gold Mine.

From 2003 until about October 2008 when the Company was informed that extension of its exploration license would not be honored, the Company was performing limited exploration in the New San Sebastian Exploration and the Nueva Esparta Exploration License areas at the La Lola Mine, the Santa Lucia Mine, the Tabanco Mine, and the Montemayor Mine, and since 2005 until about October 2008 at the La Joya Mine.

Because the Company does not have a final feasibility study completed within the past five years, it cannot provide reserve estimates.

9

For the fiscal year ended March 31, 2009, the Company performed an impairment test over long-lived assets including mining resources and property, plant and equipment. Testing for impairment of long-lived assets requires significant management judgment regarding future cash flows, asset lives, and discount rates. The Company considered a number of factors including the cancellation of its permits by the Government of El Salvador, the fact that there has been no resolution of the Company’s legal challenges to this action initiated in El Salvador, the unwillingness of the El Salvadoran Government to engage in any discussions after the Company gave notice of its intent to file for arbitration under CAFTA-DR on March 17, 2009 (and consequently, the need to file for arbitration before the International Centre for Settlement of Investment Disputes (ICSID) on July 2, 2009), and public stat ements made by members of the Government of El Salvador elected in March 2009.

Given all of these factors and events, the Company determined that its assets have been impaired and the Company has made significant adjustments to account for impairment. A pre-tax charge of $21,213,950 was recognized in the fourth quarter ending March 31, 2009, fully impairing the mining resource assets. Additionally, a pre-tax charge of $4,835,353 was recognized in the fourth quarter ending March 31, 2009, related to impairment of plant and equipment. The Company has not impaired plant and equipment for the amount of $116,324 which the Company believes to be fully recoverable.

SSGM Joint Venture Arrangements

Commerce owns 82 1/2% of the authorized and issued common shares of San Sebastian Gold Mines, Inc. (“Sanseb”), a Nevada corporation formed on September 4, 1968. Approximately 200 unrelated shareholders hold the balance of Sanseb’s shares.

On September 22, 1987, Commerce and Sanseb entered into a joint venture agreement (named the “Commerce/Sanseb Joint Venture” and sometimes referred to herein as the “Joint Venture”) to formalize the relationship between Commerce and Sanseb with respect to the mining venture and to divide profits. The terms of this agreement authorize Commerce to supervise and control all of the business affairs of the Joint Venture. Under this agreement 90% of the net pre-tax profits of the Joint Venture will be distributed to Commerce and ten percent to Sanseb, and because Commerce owns 82 1/2% of the authorized and issued shares of Sanseb, Commerce in effect has an over 98% interest in the activities of the Joint Venture. In order to maintain current accounting between Commerce and Sanseb, the interest charges to Sanseb on advances made by Commerce are kept separately. Therefore, when profits are earned, the recorded interest due to Commerce will be paid from the cash distributions due and payable to Sanseb.

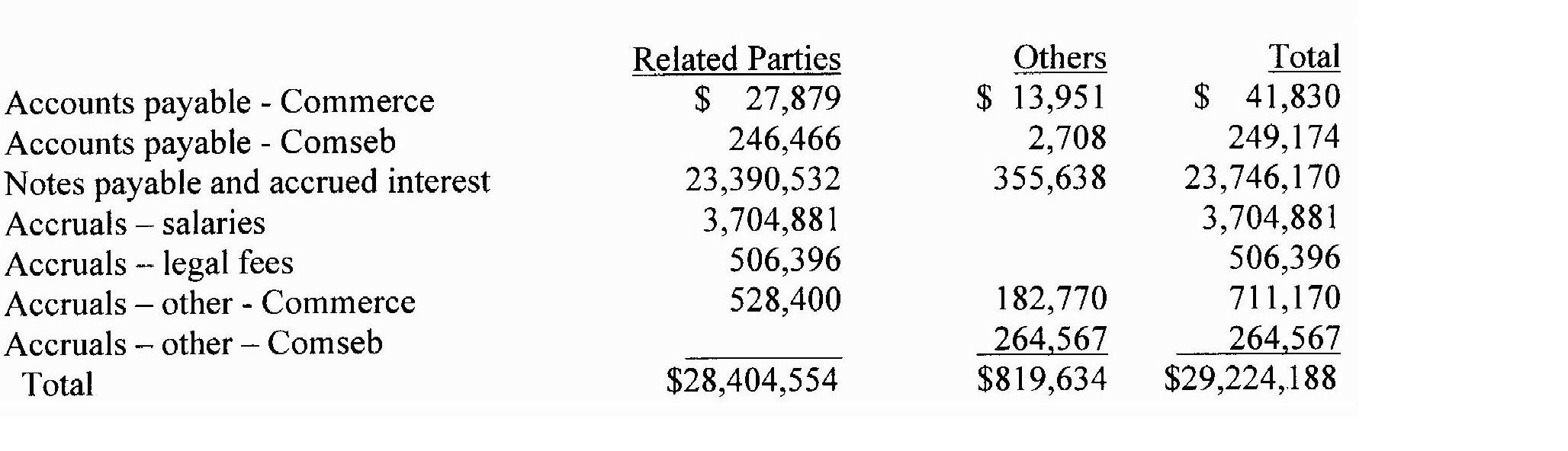

The Joint Venture leases the SSGM from the Company’s 52%-owned subsidiary, Mineral San Sebastian, S.A. de C.V. (“Misanse”), an El Salvadoran corporation. On January 14, 2003, the Company entered into an amended and renewed 30-year lease agreement with Mineral San Sebastian Sociedad Anomina de Capital Variable (Misanse) pursuant to the approval of the Misanse shareholders and Misanse directors at a meeting held on January 12, 2003. The renewed lease is for a period of time commencing and coinciding with the date that the Company received its Renewed San Sebastian Gold Mine Exploitation Concession, hereinafter identified as the “Renewed SSGM,” from the Ministry of Economy’s Director of El Salvador Department of Hydrocarbons and Mines (DHM). The lease is automatically extendible for one or more equal periods. The Company will pay to Misanse for the rental of this real estate the sum of five percent of the sales of the gold and silver produced from this real estate, however, the payment will not be less than $343.00 per month. The Company has the right to assign this lease without prior notice or permission from Misanse. This lease is pledged as collateral for loans made to related parties (Item 8. Financial Statements and Supplementary Data, Note 7).

10

The Joint Venture is registered as an operating entity to do business in the Republic of El Salvador, Central America. The Joint Venture Agreement authorizes Commerce to execute agreements on behalf of the Joint Venture.

Organizational Structure

The consolidated financial statements include the accounts of the Company, its majority-owned subsidiaries, and its Commerce/Sanseb Joint Venture, but it excludes its 52% ownership of Mineral San Sebastian S.A. de C.V. Mineral San Sebastian, S.A. de C.V. (Misanse) is not included in the consolidated statements as the Company does not have corporate control of Misanse because the majority of Misanse's elected directors must be El Salvadoran shareholders. Upon consolidation, all intercompany balances and transactions are eliminated.

| | | Charter/Joint Venture |

Included in the Consolidated Statements | % Ownership | Place | Date |

Homespan Realty Co., Inc. (“Homespan”) | 100.0 | Wisconsin | 02/12/1959 |

Ecomm Group Inc. (“Ecomm”) | 100.0 | Wisconsin | 06/24/1974 |

San Luis Estates, Inc. (“SLE”) | 100.0 | Colorado | 11/09/1970 |

San Sebastian Gold Mines, Inc. (“Sanseb”) | 82.5 | Nevada | 09/04/1968 |

Universal Developers, Inc. (“UDI”) | 100.0 | Wisconsin | 09/28/1964 |

Commerce/Sanseb Joint Venture (“Joint Venture”) | 90.0 | Wisconsin & El Salvador | 09/22/1987 |

Not included in the Consolidated Statements | | | |

Mineral San Sebastian, S.A. de C.V. (“Misanse”) | 52.0 | El Salvador | 05/08/1960 |

Commerce was originally formed as a Wisconsin corporation (September 14, 1962). It then merged into a Delaware corporation on July 26, 1971 and on April 1, 1999 it merged back into a Wisconsin corporation. It owns 52% of Misanse, an El Salvadoran corporation that was formed on May 8, 1960, reinstated on January 25, 1975 and reincorporated on October 22, 1993. Misanse previously had a mining concession with the government of El Salvador and is the owner of the SSGM real estate. At that time, Misanse had assigned the mining concession to Commerce Group Corp. and San Sebastian Gold Mines, Inc., the mining operator formed on September 22, 1987 and known as the Commerce/Sanseb Joint Venture (Joint Venture). It conducted exploration and operations at the SSGM starting in October 1968; it mined and sold gold from 1972 through March 1978 and from April 1, 1995 through December 1999. Commerce also owns 82 1/2% of the San Sebastian Gold Mines, Inc. (SSGM) which was chartered as a Nevada corporation on September 4, 1968.

11

World Gold Market Price, Customers and Competition

The price of gold and silver is unpredictable, volatile, and is affected by numerous factors beyond the Company’s control, including, but not limited to, expectations for inflation, the relative strength of the United States’ dollar in relation to other major worldwide currencies, political and economic conditions, central bank sales or purchases, inflation, and production costs in major gold-producing regions. The Company has not and does not expect in the foreseeable future to engage in hedging or other similar transactions to minimize the risk of fluctuations in gold prices or currencies. The Company’s past practice has been to sell its gold and silver at the world market spot prices. Gold and silver can be sold on numerous markets throughout the world, and the market price is readily ascertainable for such precious metals. There are many worldwide refiners and smelters available to refine these precious metals. Refined gold and silver can also be sold to a large number of precious metal dealers on a competitive basis. When it was producing doré, the Company’s SCMP sold the doré to a refinery located in the United States. During the past five years (March 31, 2004 to March 31, 2009) the London PM Fix gold price has fluctuated between a low of about $375 per ounce in May of 2004 and a high of over $1011 per ounce in March 2008.

At this time the Company believes that, due to its current financial capacity, it may not be a major gold producer based on the size of larger existing gold mining companies. At this time the Company believes no single gold-producing company could have a large impact to offset either the price or supply of gold in the world market. There are many mining entities in the world producing gold. Many of these companies have substantially greater technical and financial resources and larger gold ore reserves than the Company.

The Company’s profitability and viability are dependent upon, not only the price of gold in the world market (which can be unstable), but also upon the political stability of El Salvador, the cooperation of the Government of El Salvador in issuing needed environmental and other permits, and the availability of adequate funding for the SSGM open-pit, heap-leaching operation and for the exploration projects.

Seasonality

Seasonality does not have a material impact on the Company’s operations, but the rainy season in El Salvador (May through November) can subdue production.

Environmental Matters

The Company’s operations are subject to environmental laws and regulations adopted by various governmental authorities in the jurisdictions in which the Company operates. Accordingly, the Company has adopted policies, practices and procedures in the areas of pollution control, product safety, occupational health and the production, handling, storage, use and disposal of hazardous materials to prevent material environmental or other damage, and to limit the financial liability which could result from such events. However, some risk of environmental or other damage is inherent in the business of the Company, as it is with other companies engaged in similar businesses.

The Company is required to maintain environmental permits to operate in El Salvador. The issuance of these permits is under the jurisdiction of the El Salvador Ministry of Environment and Natural Resources Office (MARN). On October 15, 2002, MARN issued an environmental permit under Resolution 474-2002 for the SCMP. On October 20, 2002, MARN issued an environmental permit under Resolution 493-2002 for the Renewed SSGM Exploitation concession. Financial security bond(s) were submitted as required. These permits were renewed for a three-year period with the issuance of Resolution No. 3026-003-2006 dated January 4, 2006.

12

On or about September 13, 2006, without any prior notice, the El Salvador Ministry of Environment’s office delivered to Commerce’s El Salvadoran legal counsel, its revocation of the MARN Resolution dated July 6, 2006 which included its San Sebastian Gold Mine Exploitation and San Cristobal Mill and Plant environmental permits. These were the only permits of their kind issued in the Republic of El Salvador. The Company’s El Salvadoran legal counsel, after reviewing the two letters (one for the SSGM exploitation concession and the other for the SCMP), concluded that the revocation of these permits was arbitrary, illegal and unconstitutional and he so stated in a September 20, 2006 letter to the Ministry of Environment.

On or about December 6, 2006, the Company’s legal counsel filed with the El Salvadoran Court of Administrative Litigation of the Supreme Court of Justice two complaints contesting the revocation of the environmental permits: one for the San Sebastian Gold Mine and the other for the San Cristobal Mill and Plant. In these complaints the Company asserted:

1.

Violation of the Right to a Hearing and Due Process – pursuant to Articles 88 and 93 of the Environmental Law. On January 4, 2006 under MARN Resolution No. 3026-003-2006, the environmental permit was extended.

2.

Lack of legal foundation for the sanction – the Company was not in production, therefore, it could not be in violation. This fact was verified by a written MARN report after a site inspection on June 23, 2006.

3.

Excess of Authority – besides revoking the environmental permit, MARN ordered the closing of operations which said determination and authority are under the jurisdiction of the El Salvador Ministry of Economy’s office.

In October 2008 the Directorate of Mines notified the Company that it was not honoring the Company's previous request for an extension of the exploration permits at the San Sebastian and Nueva Esparta areas. The Company believes this notice is unwarranted and an appeal is pending.

All operations by the Company involving the exploration or the production of minerals are subject to existing laws and regulations relating to exploration procedures, safety precautions, employee health and safety, air quality standards, pollution of water sources, waste materials, odor, noise, dust and other environmental protection requirements adopted by the El Salvador governmental authorities. The Company was required to prepare and present to such authorities data pertaining to the effect or impact that any proposed exploration or production of minerals may have upon the environment. The requirements imposed by any such authorities may be costly, time consuming and may delay operations. Future legislation and regulations designed to protect the environment, as well as future interpretations of existing laws and regulations, may require substantial increases in equipment and operating costs to the Comp any and delays, interruptions, or a termination of operations. The Company cannot accurately predict or estimate the impact of any such future laws or regulations, or future interpretations of existing laws and regulations, on its operations.

13

Republic of El Salvador, Central America Information Sources

The most current information about El Salvador can be obtained from the following sources:

1.

General information can be obtained through the Internet from the following websites: http://www.usinfo.org.sv/eng/irc/svlinks.html and http://www.dirla.com/elsalvador2.html.

2.

The U.S. Embassy in El Salvador can also be contacted at Final Boulevard Santa Elena, Antiguo Cuscatlán, La Libertad, telephone (011) 503-2501-2999 and fax (011) 503-2501-2150 or at its website: http://sansalvador.usembassy.gov.

Operations, Other Than Mining

Commerce independently and through its partially and wholly-owned subsidiaries conducted other business activities, which at present are suspended. Previous operations consisted of the following: (1) land acquisition and real estate development through its wholly-owned subsidiaries, San Luis Estates, Inc. (“SLE”) and Universal Developers, Inc. (“UDI”); (2) real estate sales, through its wholly-owned subsidiary, Homespan Realty Co., Inc. (“Homespan”); and (3) advertising and various businesses, including Internet-related businesses, through its subsidiary, Ecomm Group Inc. (“Ecomm”).

Land Acquisition, Development, Ownership and Real Estate Sales

The Company has suspended its activities in the business of real estate development conducted principally through its subsidiaries San Luis Estates, Inc. (“SLE”), a Colorado corporation, and Universal Developers, Inc. (“UDI”), a Wisconsin corporation.

Misanse, the Company’s majority-owned subsidiary (52%) owns the SSGM real estate consisting of approximately 1,470 acres. This real estate is located approximately two and one-half miles northwest of the city of Santa Rosa de Lima, off of the Pan American Highway (a four-lane, first-class highway), about 108 miles southeast of the capital city of San Salvador, El Salvador, and is about 11 miles west from the border of the Country of Honduras. It is also about 26 miles from the city of La Union which has railroad and port facilities. The Company, on January 14, 2003, renewed its lease into a long-term lease arrangement with Misanse.

The Company currently leases approximately 166 acres of real estate on which it has its SCMP. These facilities are located on the Pan American Highway, near the City of El Divisadero.

The Company, through its late Chairman, owns approximately 63 acres of land on the Modesto Mine site which is located due north of the city of Paisnal and approximately 19 miles north of San Salvador, the capital city of El Salvador. This real estate is pledged as collateral for funds advanced to the Company. The Company also has permission from a number of property owners to explore, exploit and develop the Montemayor Mine in the Department of Morazan.

Reference is made to “Item 2. Properties,” for additional information.

Homespan, the local real estate marketing subsidiary of the Company, is presently inactive. It has no significant activity and is not material to the Company’s operation.

14

Employees

As of March 31, 2009, the Company and its wholly-owned subsidiaries employed approximately 25 to 30 full-time persons in El Salvador, which number may adjust seasonally. None of the Company’s employees are covered by collective bargaining agreements.

Patents, Trademarks, Licenses, Franchises, Concessions & Government Contracts

Other than concessions, licenses and interests in mining properties granted by the Government of El Salvador and permission from private landowners, the Company does not own any material patents, trademarks, licenses, franchises or non-mining concessions.

Significant Customers

The Company presently has no individual significant customers in which the loss of one or more would have an adverse effect on any segment of its operations or from whom the Company has received more than ten percent of its consolidated revenues, except for the sale of gold when the Joint Venture was mining gold. The gold in doré form was refined and then sold at the world market spot price to a refinery located in the United States. Given the marketability and liquidity of the precious metals sold and because of the large source of qualified buyers of gold and silver, the Company believes that a loss of its customers could be quickly replaced without any adverse affect.

Miscellaneous

Backlog orders at this time are not significant to either the Company’s or its majority-owned subsidiaries’ areas of operations, nor at this time is any portion of their operations subject to renegotiation of profits or termination of contracts at the election of the United States’ Government.

At this time, neither the Company nor its majority-owned subsidiaries conduct any material research and development activities, except as indicated in this report with respect to the Joint Venture and its mining exploration programs in the Republic of El Salvador, Central America.

The Company believes that the United States’ federal, state and local provisions regulating the discharge of materials into the environment should not have a substantial effect on the capital expenditures, earnings or competitive position of the Company or any of its majority-owned subsidiaries as the Company does not have any mining activity in the United States.

Item 1A. Risk Factors

The Company’s right to explore for gold and silver and to conduct mining at its properties in El Salvador is dependent upon permission from the Government of El Salvador. At the present time, the Government of El Salvador has for all intents and purposes, prohibited precious metal mining in the Republic of El Salvador. The Company is unable to predict if and when this policy will change. This has hampered not only mining activities, but also, the Company’s ability to find a suitable investment partner.

On or about September 13, 2006, the El Salvador Ministry of the Environment delivered to Commerce’s El Salvadoran legal counsel its revocation of the environmental permits issued for the SSGM and SCMP. The Company is contesting these actions in legal proceedings, but there can be no assurances as to what the outcome will be.

15

In October 2008 the Directorate of Mines notified the Company that it was not honoring the Company's previous request for an extension of the exploration permits at the San Sebastian and Nueva Esparta areas. The Company is contesting these actions in legal proceedings, but there can be no assurances as to what the outcome will be.

The Company’s main objective and plan has been to operate a moderate tonnage, low-grade, open-pit, heap-leaching operation to mine gold on its SSGM site. Since the death of Commerce’s long-time Chairman Edward L. Machulak on October 21, 2007, the Company has been directing most of its efforts toward finding a compatible acquisition, merger, or other business arrangement. At the present time, the Company cannot proceed with its plans because the government of El Salvador has revoked the necessary permits.

If the Company’s permits to conduct mining activity are restored, the Company will need to raise adequate funds from outside sources for its proposed operations. There have been and will be no revenues for so long as the Company is not in production.

The Company has recurring net losses, negative working capital and negative cash flow from operations, and is dependent upon raising capital to continue operations. The Company’s ability to continue as a going concern is subject to its ability to generate a profit and/or obtain necessary funding from outside sources, including obtaining additional funding from the sale of its securities, increasing sales or obtaining loans and grants from various financial institutions where possible. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Item 2. Properties: Mining Properties

The significant mining properties in which Commerce Group Corp. or the Joint Venture has an interest are summarized below. All of the properties are located in the Republic of El Salvador, Central America.

1.

San Sebastian Gold Mine

Property Description | San Sebastian Gold Mine located two and one-half miles northwest of the city of Santa Rosa de Lima and the Pan American Highway |

Nature of Interest | Mineral concession consisting of 100% ownership of the precious metals extracted from this mine. Environmental and exploration permits have been revoked but legal challenge is pending. |

Date Interest was Acquired | 1968 |

Cost of Interest | 5% of the gross precious metal proceeds or $343 a month whichever is higher. |

Amount of Funds to Make Property Operational | This is dependent on the scale of production that management decides to perform. The amount of investment could be from $5 million to $100 million. |

Date Mine will be Operational | No estimate at this time. |

2.

Modesto Mine

Property Description | Modesto Mine located near the city of Paisnal and about 19 miles north of San Salvador, the capital city. |

Nature of Interest | Land ownership through the Company’s late Chairman. |

Date Interest was Acquired | September 1993 |

Cost of Interest | No cost for interest. |

Amount of Funds to Make Property Operational | Not applicable. |

Date Mine will be Operational | Not applicable. |

3.

San Cristobal Mill and Plant

Property Description | San Cristobal Mill and Plant located on the Pan American Highway west of the city of El Divisadero. |

Nature of Interest | Mill and Plant owned by Joint Venture. The real estate is owned by an agency of the Government of El Salvador. Environmental permit has been revoked but legal challenge is pending. |

Date Interest was Acquired | Equipment was acquired on February 23, 1993; lease was acquired on November 12, 1993. |

Cost of Interest | Equipment purchased and extensive retrofitting was performed. The cost of the investment through March 31, 2009, including the crushing system located at the San Sebastian Gold Mine, is $7,203,820. |

Amount of Funds to Make Property Operational | To expand the plant, including a crushing system to a capacity of 500 tons per day; an estimated sum of up to $4 million may be required, all dependent on whether new or used equipment will be purchased. |

Date Plant will be Operational | Curbed production commenced March 1995; operations suspended on December 31, 1999. At the present time, the Company has no permit to operate the plant and is considering whether to terminate the lease and liquidate the equipment. |

16

4.

New San Sebastian Exploration License

Property Description | New San Sebastian Exploration License consisting of 41 square kilometers. |

Nature of Interest | Exploration license issued by the Government of El Salvador, which has been revoked, but is the subject of legal proceedings. |

Nature of Interest | Exploration license issued by the Government of El Salvador for the precious metals, which has been revoked, but is the subject of legal proceedings. |

Date Interest was Acquired | February 2003 |

Cost of Interest | Undetermined until negotiated with the surface rights’ owners. |

Amount of Funds to Make Property Operational | Undetermined until preliminary exploration at an estimated cost of $2 million is completed. |

Date Mine will be Operational | No estimate at this time. |

5.

Nueva Esparta Exploration License

Property Description | Nueva Esparta Exploration License consisting of 45 square kilometers. |

Nature of Interest | Exploration license issued by the Government of El Salvador, which has been revoked, but is the subject of legal proceedings. |

Date Interest was Acquired | May 2004 |

Cost of Interest | Undetermined until negotiated with the surface rights’ owners. |

Amount of Funds to Make Property Operational | Undetermined until preliminary exploration at an estimated cost of $2 million is completed.

|

Date Mine will be Operational | No estimate at this time. |

17

18

The San Sebastian Gold Mine

General Location and Accessibility

The SSGM is situated on a mountainous tract of land owned by Misanse in approximately 1,470 acres of explored and unexplored mining prospects. The SSGM is located approximately three miles off of the Pan American Highway, northwest of the city of Santa Rosa de Lima in the Department of La Union, El Salvador. The tract is typical of the numerous volcanic mountains of the coastal range of southeastern El Salvador. The topography is mountainous with elevations ranging from 300 to 1,500 feet above sea level. The mountain slopes are steep, the gulches are well defined, and the drainage is excellent.

There is good roadway access to the SSGM site. The Pan American Highway is a four lane road and runs from the city of San Salvador to the Honduran border. The city of Santa Rosa de Lima (approximately three miles from the SSGM) is one of the larger cities in the Eastern Zone. The SSGM is approximately 30 miles from the city of San Miguel, which is El Salvador’s third largest city, and approximately 108 miles southeast of El Salvador’s capital city, San Salvador. SSGM is also approximately 26 miles from the city of La Union which has port and railroad facilities. Major United States’ commercial airlines provide daily scheduled flights to the Comalapa Airport which is located on the outskirts of the city of San Salvador.

Because the Company does not have a final feasibility study completed within the past five years, a determination that the property contains valid reserve estimates is not possible at this time. The Company plans to develop reserves from mineralized material present at the SSGM.

At the turn of the twentieth century, the SSGM was rated as one of the richest gold mines in the world. The United Nations’ 1969 Mineral Survey Report states that “unquestionably the San Sebastian deposit was the jewel of the El Salvador mining industry and one of the most prolific gold mines in Central America.”

The Company estimates that at the SSGM it has 14.4 million tons of virgin mineralized material, including the dump waste material. The dump material and stope fill at the SSGM are the by-products of past mining operations. The dump material was mined in the past in the search for higher grades of gold ore and piled to the side of past excavations as it was considered at that time to be too low of a grade of ore to process economically; however, it was reserved for future processing when the price of gold is at a level to process it profitably. The stope fill that was available was in the past (1900 era) considered to be too low of a grade of mineralized material to process economically, therefore it was primarily used to fill the voids in the underground workings to accommodate the extraction of the higher grade of gold mineralized material in the past SSGM mining activities.

Misanse Mining Lease

The Company (previously through the Joint Venture) leases the SSGM from Mineral San Sebastian, S.A. de C.V. (“Misanse”), an El Salvadoran corporation. The Company owns 52% of the total of Misanse’s issued and outstanding shares. About 100 El Salvador, Central American and United States’ citizens own the balance of the shares. (Reference is made to Item 8. Financial Statements and Supplementary Data, Note 7, for related party interests.)

19

SSGM Mining Lease

On January 14, 2003, the Company entered into an amended and renewed lease agreement with Mineral San Sebastian Sociedad Anomina de Capital Variable (Misanse) pursuant to the approval of the Misanse shareholders and directors at a shareholders’ meeting and thereafter at a directors’ meeting both held on January 12, 2003. The renewed lease is for a period to coincide with the term of its Renewed SSGM concession, which it received on August 29, 2003 from the DHM. It was automatically amended on May 20, 2004 to coincide with the extension of the term of the Renewed SSGM Exploitation Concession from 20 to 30 years. The lease is automatically extendible for one or more equal periods. The Company will pay to Misanse for the rental of this real estate the sum of five percent of the sales of the gold and silver produced from this real estate, however, the payment will not be less than $343.00 per mo nth. The Company has the right to assign this lease without prior notice or permission from Misanse. This lease is pledged as collateral for loans made to related parties (Item 8. Financial Statements and Supplementary Data, Note 7).

Misanse Mineral Concession-Government of El Salvador

In El Salvador, the rights to minerals below the sub-surface are vested with the government. The government through concessions grants mineral rights. Reference is made to the exploration and exploitation maps included in this report.

On July 23, 1987, the Government of El Salvador delivered and granted to Misanse, possession of the mining concession. At that time this provided the right to extract minerals and export gold and silver for a term of 25 years (plus a 25-year renewal option) beginning on the first day of production from the real estate which encompasses the SSGM owned by Misanse. Misanse assigned this concession to the Joint Venture.

Effective February 1996, the Government of El Salvador passed a law which required mining companies to pay to it three percent of its gross gold sale receipts and an additional one percent is to be paid to the El Salvador municipality which has jurisdiction of the mine site. As of July 2001, a series of revisions to the El Salvador Mining Law were made. A principal change is that the fee payable to the GOES has been reduced to two percent of the gross gold and silver receipts.

20

Renewed San Sebastian Gold Mine Exploitation Concession under El Salvador Agreement Number 591 dated May 20, 2004 and delivered on June 4, 2004 (Renewed SSGM) - approximately 1.2306 square kilometers (304 acres) located in the Department of La Union, El Salvador, Central America

On September 6, 2002, at a meeting held with the El Salvadoran Minister of Economy and the Department of Hydrocarbons and Mines (DHM), it was agreed to submit an application for the Renewed SSGM concession for a 30-year term and to simultaneously cancel the concession obtained on July 23, 1987. On September 26, 2002, the Company filed this application. On February 28, 2003 (received March 3, 2003) the DHM admitted to the receipt of the application and the Company proceeded to file public notices as required by Article 40 of the El Salvadoran Mining Law and its Reform (MLIR). On April 16, 2003, the Company’s El Salvadoran legal counsel filed with the DHM notice that it believed that it complied with the requirements of Article 40, and that there were no objections; and requested that the DHM make its inspection as required by MLIR Article 42. An inspection by the DHM was made. The Company then pro vided a bond which was required by the DHM to protect third parties against any damage caused from the mining operations, and it simultaneously paid the annual surface tax. On August 29, 2003 the Office of the Ministry of Economy formally presented the Company with a twenty-year Renewed SSGM concession which was dated August 18, 2003. On May 20, 2004 (delivered June 4, 2004) the Government of El Salvador under this Agreement Number 591 extended the exploitation concession for a period of thirty (30) years. This Renewed SSGM concession replaces the collateral that the same parties held with the previous concession.

On or about September 13, 2006, the El Salvador Ministry of the Environment delivered to Commerce’s El Salvadoran legal counsel its revocation of the environmental permits issued for the SSGM and SCMP. The Company is contesting these actions.

New San Sebastian Exploration License under El Salvador Resolution Number 27 - approximately 40.7694 square kilometers (10,070 acres) located in the Departments of La Union and Morazan, El Salvador, Central America

On October 20, 2002, the Company applied to the Government of El Salvador through the DHM for the New San Sebastian Exploration License, which covers an area of 41 square kilometers and includes approximately 1.2306 square kilometers of the Renewed SSGM concession. The New San Sebastian Exploration License area is in the jurisdiction of the City of Santa Rosa de Lima in the Department of La Union, Republic of El Salvador, Central America. On February 24, 2003, the DHM issued the New San Sebastian Exploration License for a period of four years starting from the date of December 27, 2003, following the notification of this resolution which was received on March 3, 2003. The New San Sebastian Exploration License may be extended for two two-year periods, or for a total of eightyears. This license is in the process of being renewed for a period of four years. Besides the San Sebastian Gold Mine, th e following three other formerly operative gold and silver mines are included in the New San Sebastian Exploration License area: the La Lola Mine, the Tabanco Mine, and the Santa Lucia Mine. Historical data reflects the following:

A French company operated the La Lola Mine in 1920; they developed two quartz veins, which were named La Lola and Buena Vista. From 1950 through 1953, Mr. Amadeo Tinetti produced 1,850 ounces of gold and 66,000 ounces of silver.

21

The Tabanco Mine is south of the La Lola Mine. Records evidence and local citizens confirm that several levels of mining occurred. Isolated rich ore shoots reported to contain sulfides and silver chloride were encountered. The oxidized sulfide ore was mined from a width of three to six feet with a grade of 0.50 ounces per ton of gold and five ounces of silver. Records reflect that the Herrera family produced gold and silver beginning in the year 1780.

In the Tepeyac vein very high-grade ore in one to two foot widths was encountered. A United Nation’s team performed sampling and reported that in a sulfide bearing zone they found 0.31 ounces of gold and 4.52 ounces of silver in a 4.9 foot wide vein. The footwall host rock assayed at 0.22 ounces of gold and 41.29 ounces of silver. This footwall rock area location was not specifically identified, but the result lends strength to the recommendation that in any further sampling or mapping of veins in the epithermal environment, close attention will be directed to the wall rock.

The third mine in this exploration area is the Santa Lucia Mine in which Mr. Humberto Perla developed a 100 meter wide underground vein. This vein is the west continuation of the Granadilla and the Ano Nuevo veins located about two miles west of the SSGM property.

In October 2008 the Directorate of Mines notified the Company that it was not honoring the Company's previous request for an extension of the exploration permits at the San Sebastian and Nueva Esparta areas. The Company is contesting these actions.

Nueva Esparta Exploration License (Nueva Esparta) Resolution Number 271 - 45 square kilometers (11,115 acres) located in the Departments of La Union and Morazan, El Salvador, Central America

On or about October 20, 2002, the Company filed an application with the Government of El Salvador through the DHM for the Nueva Esparta, which consists of 45 square kilometers north and adjacent to the New San Sebastian Exploration License area. This rectangular area is in the Departments of La Union (east) and Morazan (west) and in the jurisdiction of the City of Santa Rosa de Lima, El Salvador, Central America. On May 25, 2004 (received June 4, 2004) the Government of El Salvador under Resolution Number 271 issued the exploration license for a period of four years with a right to request an additional four year extension. An important observation is that these mines form a belt of mineralization following a fault line from the SSGM to the Montemayor Mine for a distance of approximately five miles. Included in the Nueva Esparta are eight other formerly-operated gold and silver mines known as: t he Grande Mine, the Las Pinas Mine, the Oro Mine, the Montemayor Mine, the Banadero Mine, the Carrizal Mine, the La Joya Mine and the Copetillo Mine. Historical data reflects the following:

The Montemayor Mine has records that show that an English company commenced production of precious metals sometime about 1860. A report prepared by Mr. Fleury in 1878 stated that the area assayed approximately 48 ounces of silver and 0.85 ounces of gold per ton. Six underground workings were developed, but no records are available. A United Nation’s report reflects a possible grade of twelve ounces of silver and 0.29 ounces of gold from a section of the Montemayor vein stope. The Montañita, Tempique, Guarumo, Santa Gertrudis and El Indio vein findings support expanded exploration. The Company performed preliminary exploration in the Montemayor Mine area from 1995 through 1997. Its findings from the ore samples were very positive and encouraged additional exploration. Exploration will consist of locating workable ore within the known structures through mapping and sampling o f vein outcrops and reopening, mapping and sampling of underground work.

22

The El Banadero Mine is located near the Montemayor Mine. When in production, most of the mineralized material processed at the Montemayor mill came from this area and the quality of the precious metals appeared to have the highest values. The veins identified in the area are the Saravia, Borbollon, Caraguito 1 to 3, Eulalio and the Miserocordia.

At the La Joya Mine the Company, during previous exploration, discovered three parallel wide quartz veins averaging in width from six feet to 27 feet running northwest by southeast dipping at 42 degrees southwest. More exploration will be concentrated in this tract.

El Jimenito and Santa Teresa are two wide veins that the Company found at the Carrizal Mine. They are 1,920 to 2,560 feet apart. The local residents recollect that free gold was found in the Santa Teresa Vein Adit. This mine is located between the La Joya and Copetillo Mines.

One vein was discovered at the Copetillo Mine in an underground adit. It was developed into two sublevels connected to the south with one 100-foot shaft. Residents recall seeing free gold in the Canton Copetillo.

The Las Piñas Mine is located in the Canton Las Cañas and was in operation in 1935. It was developed for a five-year, 100-ton-per-day mill and plant. Records show that the average grade of silver was 5.10 ounces per ton and that the grade of gold averaged 0.06 ounces per ton.

The La Joya Mine is located in the Canton La Joya. Records relating to activities were not preserved. While exploring the region, the Company found three parallel wide quartz veins ranging from six to 25 feet running northwest to southeast for a distance of over one mile. The grass roots exploration suggests that this is an area with great ore potential.

At this time there is no available information about the Oro Mine. It is a short distance south of the Montemayor Mine. This should be a good exploration target.

In October 2008 the Directorate of Mines notified the Company that it was not honoring the Company's previous request for an extension of the exploration permits at the San Sebastian and Nueva Esparta areas. The Company is contesting these actions.

SSGM Current Status

The Company’s main objective and plan has been to operate a moderate tonnage, low-grade, open-pit, heap-leaching operation to mine gold on its SSGM site. Since the death of Commerce’s long-time Chairman Edward L. Machulak on October 21, 2007, the Company has been directing most of its efforts toward finding a compatible acquisition, merger, or other business arrangement. At the present time, the Company cannot proceed with its plans because the government of El Salvador has revoked the necessary permits.

SSGM Ownership of the Property

Misanse, a Salvadoran corporation, owns the San Sebastian Gold Mine real estate consisting of approximately 1,470 acres. The Company owns 52% of Misanse common shares that are issued and outstanding.

23

Modesto Mine

Modesto Mine Location

The Modesto Mine is located due north of the town of El Paisnal, approximately 19 miles north of the capital city, San Salvador, in the Republic of El Salvador, Central America.

Modesto Mine Present Status

The Joint Venture suspended exploration activities at this site in July 1997 when the Government of El Salvador awarded the concession of the property to another mining company. At the present time, the Government of El Salvador has suspended all mining in El Salvador. If the policies of the Government of El Salvador change, the Company believes that it will be in a good position to explore and develop this mining property because the Company’s late Chairman owns the title to the property.

Montemayor Mine (“Montemayor”)

The Joint Venture has obtained permission from a number of property owners to enter their property for the purpose of exploring, exploiting and developing the property and then, if feasible, to mine and extract minerals from this property. The Company believes that this real estate contains the “heart” of the mine. Montemayor is located about six miles northwest of the SSGM and about two and one-half miles east of the city of San Francisco Gotera in the Department of Morazan, Republic of El Salvador. Historical records evidence that the potential for the Montemayor to become an exploration and development silver-gold producing prospect is excellent. The Company will not be able to develop this mine unless it obtain required permits from the Government of El Salvador.

24

25

San Cristobal Mill and Plant (“SCMP”) Recovery and Processing System

SCMP Location

SCMP is located near the city of El Divisadero (bordering the Pan American Highway), and is approximately 13 miles east of the city of San Miguel, the third largest city in the Republic of El Salvador, Central America.

SCMP Lease Agreement

Although the Joint Venture owns the mill, plant and related equipment, it does not own the land and certain buildings.

On November 12, 1993, the Joint Venture entered into an agreement with Corporacion Salvadorena de Inversiones (“Corsain”), an El Salvadoran governmental agency, to lease for a period of ten years (expiring November 12, 2003), approximately 166 acres of land and buildings on which its gold processing mill, plant and related equipment (the SCMP) are located, and which is approximately 15 miles west of the SSGM site. The basic annual lease payment was U.S. $11,500, payable annually in advance, unless otherwise amended, and subject to an annual increase based on the annual United States’ inflation rate. As agreed, a security deposit of U.S. $11,500 was paid on the same date and this deposit was subject to increases based on any United States’ inflationary rate adjustments.

On April 26, 2004, a three-year lease, which includes an automatic additional three-year extension subject to Corsain’s review, was executed by and between Corsain and the Company. This lease is retroactive to November 12, 2003 and the monthly lease payments are $1,418.51 plus the El Salvadoran added value tax. The lease is subject to an annual increase based on the U.S. annual inflationary rate adjustments. The SCMP is strategically located to process mineralized material from other mining projects.

On March 25, 2008 a nineteen-month lease retroactive to November 12, 2006 was executed by and between Corsain and the Company. The total lease payment for this nineteen-month period is $18,608.21. Reference is made to Exhibit 10.16 of the Company’s Form 10-K for its fiscal year ended March 31, 2008, for a copy of this lease. The lease was renewed on June 12, 2008 for a six-month period to expire on December 11, 2008, with an option to subsequently renew it for additional three-month periods. The Company has chosen to exercise this option and has renewed the lease through June of 2009.

SCMP Mill and Plant Process Description

Current Status

The SCMP (a precious metal cyanidation carbon-in-leach system) has a capacity of processing up to 200 tons of virgin mineralized material per day. The following units of operation are required: crushing, grinding, thickening, agitated leaching and recovery of precious metals via a carbon-in-leach (CIL) system. The Company had planned to overhaul the SCMP to give it a production capacity of up to 500 tons per day.

26

On or about September 13, 2006, the El Salvador Ministry of the Environment delivered to Commerce’s El Salvadoran legal counsel its revocation of the environmental permits issued for the SSGM and SCMP. This Company’s legal counsel on December 6, 2006, filed with the El Salvadoran Court of Administrative Litigation of the Supreme Court of Justice two complaints relating to this matter. (See the Company’s discussion in the section entitled “Environmental Matters.”) These legal proceedings are pending.

Because of the length of time that the permit status of the SCMP has gone unresolved, the Company is now contemplating terminating its lease for the SCMP and liquidating its equipment.

SCMP Project Operating Plan

Current and Anticipated Schedule

In the past, the Company made substantial improvements to the SCMP, and used the facility to process material from the SSGM from April 1, 1995 through December 31, 1999. During this time, the gold mineralized material from the SSGM open-pit was loaded onto 20-25 ton dump trucks for transport to the SCMP. Trucks then hauled the gold mineralized material on the Pan American Highway approximately 15 miles from the SSGM. Mine employees were responsible for the mining activities including the determination of areas to be excavated, trucking and loading operations, head sampling and sample analysis.

The gold mineralized material was received at the SCMP where it was weighed, logged, and sampled. Weighing was performed utilizing a conveyor belt scale and/or a truck scale located on the SCMP site. The excess gold mineralized material was then unloaded at the SCMP site and stockpiled in an area which was developed to allow storage of more than 50,000 tons.

Environmental Matters

Reference is made to San Sebastian Gold Mine “Environmental Matters.” The same information applies. On March 15, 2006, the Office of the El Salvadoran Ministry of Environment and Natural Resources (MARN) issued an environmental permit (Resolution 3026-003-2006) relative to the Renewed SSGM Exploitation Concession and the San Cristobal Mill and Plant. On or about September 13, 2006, MARN revoked both permits. For more details, reference is made to “Environmental Matters” and to Item 3. Litigation.

The Joint Venture Laboratory

The Joint Venture has a laboratory located on real estate owned by the Company near the SSGM site. A total of 78,441 samples of exploration fire assays were logged through 2004. This total does not include the assays that were performed for production purposes. Assay work has not been performed at the laboratories since 2004.

27

Corporate Headquarters

The Company leases approximately 4,032 square feet of office space for its corporate headquarters on the second floor of the building known as the General Lumber Building located at 6001 North 91st Street, Milwaukee, Wisconsin, at a monthly rental charge of $2,789 on a month-to-month basis. The lessor is General Lumber & Supply Co., Inc. (“General Lumber”), a Wisconsin corporation. The Company’s late President, Edward L. Machulak, owns 55% of the common stock of General Lumber. Edward L. Machulak disclaims any interest in the balance of General Lumber common stock which is owned by relatives, his wife, and a trust formed for the benefit of his children. In addition, the Company shares proportionately any increase in real property taxes and any increase in general fire and extended coverage insurance on the property. In lieu of cash payment, the Lessor has agreed to apply the monthly rental payments owed to the secured open-ended, on-demand promissory note(s) due to it.

Item 3. Legal Proceedings

There is no pending litigation in the United States. However, in the Republic of El Salvador, Central America, the Company’s El Salvadoran legal counsel on December 6, 2006, filed a complaint with the El Salvadoran Supreme Court Administrative Division claiming that the El Salvadoran Office of the Ministry of Environment and Natural Resources, (MARN) has revoked its El Salvadoran environmental permits for mining exploitation, without any prior notice, without a right to a hearing and without the right of due process, based on misguided assertions, and contrary to El Salvadoran law. In addition, the Company’s legal counsel stated that there is a lack of legal foundation for the sanctions and excess authority exercised by MARN. For more details, reference is made to “Environmental Matters.” Also, in October 2008 the Directorate of Mines notified the Company that it was not honoring the Com pany's previous request for an extension of the exploration permits at the San Sebastian and Nueva Esparta areas. The Company believes this notice is unwarranted and an appeal is pending.

On March 17, 2009, the Company’s attorneys delivered a Notice of Intent to commence international arbitration proceedings against the Government of El Salvador under the Central America Free Trade Agreement-Dominican Republic (CAFTA-DR). The Company contends that the Government of El Salvador frustrated its effort to develop its mining interests in the country of El Salvador in violation of CAFTA-DR. The parties had 90 days to resolve their dispute amicably, after which the Company had the right to commence arbitration proceedings against the Government of El Salvador to claim significant monetary damages. Since the Company received no response to the Notice of Intent, it submitted to the International Centre for Settlement of Investment Disputes (ICSID) a notice of arbitration to commence international arbitration proceedings against the Government of El Salvador under CAFTA-DR on July 2, 2009.

Item 4. Submission of Matters to a Vote of Security Holders

No matters were brought to a vote of security holders in the fourth quarter ended March 31, 2009.

28

PART II

Item 5. Market for the Company’s Common Stock and Related Stockholders’ Matters

(a) Principal Market and Common Stock Price

The Company continues to be listed on the Over the Counter Bulletin Board (OTCBB) under the trade symbol CGCO.OB and on the Pink Sheets under the trade symbol CGCO.PK. Since October 21, 2005 its shares were traded on the Berlin-Bremen Stock Exchange under the trade symbol C9G. Prior to this time, the common shares were traded since 1968 on the Over the Counter, American Stock Exchange, Boston Stock Exchange and on the Nasdaq Smallcap.

The following table reflects the range of high and low trade prices of the common shares as reported by the OTCBB for the period ended March 31, 2009 and 2008, as well as the highest and lowest trade price during each quarter through the period ended March 31, 2009. The closing price on May 29, 2009 was $.175 a share.

For the period ended | March 31, 2009 | March 31, 2008 |

| | High | Low | High | Low |

First quarter ending June 30 | $0.32 | $0.12 | $0.40 | $0.10 |

Second quarter ending September 30 | $0.35 | $0.05 | $0.15 | $0.09 |

Third quarter ending December 31 | $0.10 | $0.01 | $0.30 | $0.05 |

Fourth quarter ending March 31 | $0.10 | $0.03 | $0.51 | $0.16 |

(b) Approximate Number of Holders of Common Shares

As of March 31, 2009, the Company believes that the common shares were held by approximately 3,600 shareholders; it is estimated that over 95% are United States’ residents.

As of March 31, 2009, the Company’s transfer agent and registrar certified that there were 1,584 shareholders of record. The number of shareholders of the Company who beneficially own shares in nominee or “street name” or through similar arrangements is estimated by the Company to be approximately 1,300.

As of March 31, 2009, there were issued and outstanding: (a) 30,750,869 shares of common stock; (b) no stock options were issued or outstanding to purchase common stock; and (c) no preferred shares or stock options are issued and outstanding.

(c) Equity Compensation Plans

None.

(d) Dividend History

Subject to the rights of holders of any outstanding series of preferred shares to receive preferential dividends, and to other applicable restrictions and limitations, holders of shares of common shares are entitled to receive dividends if and when declared by the Board of Directors out of funds legally available. No dividends were payable during the last fiscal year ended March 31, 2009. The declaration of future dividends will be determined by the Board of Directors in light of the Company’s earnings, cash requirements and other relevant considerations.

29

(e) Issue of Securities to Directors and Officers

No shares were issued to the Company’s Directors or Officers during the fiscal year ended March 31, 2009.

Item 6. Selected Financial Data

The following table presents certain selected financial information regarding the Company’s financial condition and results over the past five years:

| | | Year Ended March 31 ------------------------------------------------------------------------------------------- |

| |

2009 |

2008 | 2007 (Restated) | 2006 (Restated) | 2005 (Restated) |

Income statement data | | | | | |

Total revenue | $ 0 | $ 0 | $ 0 | $ 0 | $ 0 |

Income (loss) from continuing operations |

$(30,016,783) |

$(3,052,198) |

$(2,616,821) |

$(2,209,424) |

$(1,921,455) |

Income (loss) from continuing operations per share: | | | | | |

Basic and diluted | $ (0.98) | $ (.011) | $ (.010) | $ (.09) | $ (.09) |

Weighted average shares - basic and diluted |

30,723,711 |

28,401,086 |

25,457,052 |

23,834,988 |

22,581,814 |

Cash dividends per common share | $ 0 | $ 0 | $ 0 | $ 0 | $ 0 |

| | | | | | |

Balance sheet data | | | | | |

Working capital*1 | $ 200,975 | $ 545,618 | $ 605,787 | $ 798,753 | $ 496,977 |

Total assets | $ 689,595 | $26,485,002 | $25,889,065 | $25,236,806 | $24,559,123 |

Short-term obligations*1 | $ 29,224,187 | $25,006,311 | $21,790,176 | $18,851,934 | $16,178,620 |

Long-term obligations | $ 0 | $ 0 | $ 0 | $ 0 | $ 0 |

Shareholders’ equity (deficit) | $(28,534,592) | $ 1,478,691 | $ 4,098,889 | $ 6,384,872 | $ 8,380,503 |

| | | | | | |

*1

Although the majority of the short-term obligations are due on demand, some of these obligations have the attributes of being long-term as most of the debt is due to most of the related parties who have not called for a payment except for nominal amounts of their short-term loans during the past five or more years.

30

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion provides information on the results of operations for each of the three years ended March 31, 2009, 2008 and 2007 and the financial condition, liquidity and capital resources for March 31, 2009 and 2008. The financial statements of the Company and the notes thereto contain detailed information that should be referred to in conjunction with this discussion.

Overview

Today, Commerce is a company with great potential for developing gold and silver ore reserves. The Company is in the precious metals exploration business with all of its mining interests presently located in the Republic of El Salvador, Central America. The Company's objectives and goals are to increase shareholder value by finding a compatible acquisition, merger or other business arrangement by which gold and silver ore reserves within the concession/license areas granted to the Company by the Government of El Salvador (GOES) will be identified, developed and processed. Substantial capital expenditures are required to find, develop and process gold ore. The Company's geologists and engineers believe that it has potentially significant precious metal reserves, which can be identified and developed by continuous and expanded exploration. The strategies to accomplish these goals include, whether by Commerce or through an arrangement with another respected company, resolving its permit issues with the El Salvadoran Government, commencement of production of gold and silver when adequate funding is available, locating and identifying gold and silver ore reserves by a more aggressive exploration program, continuing the good relationship established over the past 39 years with its employees, earning profits and respecting the citizens surrounding its mining properties.