SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

Amendment No. 1

(Mark One)

| x | Annual Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2007

or

| ¨ | Transition Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934 |

COMMISSION FILE NUMBER 000-27915

GENIUS PRODUCTS, INC.

(Exact name of registrant as specified in its charter)

| DELAWARE | 33-0852923 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

3301 EXPOSITION BLVD., SUITE 100, SANTA MONICA, CALIFORNIA | 90404 |

| (Address of principal executive offices) | (Zip Code) |

(310) 401-2200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

COMMON STOCK, PAR VALUE $0.0001

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-KSB or any amendment to this Form 10-KSB. Yes o No x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of voting stock held by non-affiliates of the registrant was $146,169,528 as of June 30, 2007 (computed by reference to the average of the bid and asked price of a share of the registrant’s common stock on that date as reported by the Over the Counter Bulletin Board). For purposes of this computation, it has been assumed that the shares beneficially held by directors and officers of registrant were “held by affiliates”; this assumption is not to be deemed to be an admission by such persons that they are affiliates of registrant.

There were 67,709,094 shares of the registrant’s common stock outstanding as of February 29, 2008.

EXPLANATORY NOTE

During meetings held on October 8, 2008 and November 13, 2008, the Audit Committee of the Board of Directors of Genius Products, Inc. (the “Company”), acting on a recommendation from the Company’s management, determined that it was necessary to restate (i) the Company’s unaudited consolidated financial statements and other financial information as of and for the three months ended September 30, 2006, March 31, June 30 and September 30, 2007 and March 31 and June 30, 2008, and (ii) the audited consolidated financial statements and other financial information of the Company and Genius Products, LLC (the “Distributor”) as of December 31, 2006 and 2007 and for the periods then ended.

The aforementioned restatements relate to (i) an error in the application of generally accepted accounting principles with respect to the recognition in the Company’s financial statements of costs paid on its behalf by the Distributor and (ii) an error in the application of generally accepted accounting principles with respect to the accounting classification and measurement of certain redemption rights of the holders of the Distributor’s Class W Units.

The Company’s prior accounting methodology with respect to costs paid on its behalf by the Distributor was based on the view that such costs should be recognized in the Company’s financial statements to the extent of the Company’s economic participation and ownership interest in the Distributor. The Company has now determined that it should recognize all such costs incurred on its behalf by the Distributor in the Company’s financial statements.

The Distributor’s prior accounting methodology with respect to the accounting classification and measurement of the aforementioned redemption rights did not properly classify and measure the Distributor’s Class W Units as redeemable securities. The Distributor will now recognize, as an asset, the fair market value of such redemption rights in the Distributor’s financial statements. In addition, the Distributor has now recorded the redeemable Class W Units outside of permanent equity in its financial statements. This accounting change in the Distributor’s financial statements has also resulted in the need to restate the Company’s financial statements to reflect a corresponding liability related to the aforementioned redemption rights at the end of each of the aforementioned reporting periods.

The impact of these restatements (i) as of and for the periods ended December 31, 2006 and December 31, 2007 and (ii) as of and for the three months ended September 30, 2006 and March 31, June 30 and September 30, 2007, are further discussed in Note 3 to the audited consolidated financial statements of the Company and the Distributor included herein.

This amendment is being filed for the purpose of amending and restating Item 1 and 1A of Part I and Item 6 and 7 of Part II and Item 15 of Part IV of the Company’s Annual Report on Form 10-K originally filed with the Securities and Exchange Commission on March 19, 2008, solely to the extent necessary (i) to reflect the restatement of the Company’s audited consolidated financial statements as of and for the periods ended December 31, 2007 and December 31, 2006, as described in Note 3 to the audited consolidated financial statements of the Company and the Distributor, (ii) to reflect the restatement of the Company’s unaudited consolidated financial statements as of and for the three months ended September 30, 2006 and March 31, June 30 and September 30, 2007, (iii) to make revisions to “Management’s Discussion and Analysis of Financial Condition and Results of Operations” as warranted by the restatements, (iv) to update the certifications required by the Sarbanes-Oxley Act of 2002, and (v) to update the exhibits.

| Page | ||

| PART I | ||

| 1 | ||

| 7 | ||

| 10 | ||

| 10 | ||

| 11 | ||

| 12 | ||

| PART II | ||

| 13 | ||

| 16 | ||

| 18 | ||

| 30 | ||

| 30 | ||

| 30 | ||

| 31 | ||

| 33 | ||

| PART III | ||

| 34 | ||

| 38 | ||

| 49 | ||

| 51 | ||

| 53 | ||

| PART IV | ||

| 54 | ||

| 54 | ||

This Annual Report on Form 10-K includes “forward-looking statements”. To the extent that the information presented in this Annual Report discusses financial projections, information or expectations about our business plans, results of operations, products or markets, or otherwise makes statements about future events, such statements are forward-looking. Such forward-looking statements can be identified by the use of words such as “intends”, “anticipates”, “believes”, “estimates”, “projects”, “forecasts”, “expects”, “plans” and “proposes”.

Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from such forward-looking statements. These include, among others, the cautionary statements in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of this Annual Report. These cautionary statements identify important factors that could cause actual results to differ materially from those described in the forward-looking statements.

When considering forward-looking statements in this Annual Report, you should keep in mind the cautionary statements in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections, and other sections of this Annual Report. Except as required by law, we do not intend to update our forward-looking statements, whether written or oral, to reflect events or circumstances after the date of this Annual Report.

PART I

BUSINESS

Overview

Genius Products, Inc. (the “Company” or “Management”), through our 30%-owned subsidiary, Genius Products, LLC (the “Distributor”), is a leading independent home entertainment products company that acquires, produces and licenses an extensive library of motion pictures, television programming, and trend entertainment that is primarily sold on digital versatile disks (“DVD”) and digitally. The Distributor works in partnership with major retailers to distribute widely recognized home entertainment brands to a diversified customer base. The remaining 70% of the Distributor is owned by The Weinstein Company Holdings LLC (“TWC Holdings”) (which includes a 1% percentage interest owned indirectly through its wholly-owned subsidiary, W-G Holding Corp (“W-G Holding”)). TWC Holdings is the parent company of The Weinstein Company LLC (“TWC”), the largest provider of content for our library.

Through the Distributor, for which the Company serves as managing member, we produce and distribute a vast and growing content library that encompasses approximately 3,550 feature films and documentaries and 4,000 hours of television programming. This library includes feature films and television programming from critically acclaimed producers such as The Weinstein Company®, for which the Distributor has the exclusive U.S. home video distribution rights, and RHI Entertainment™ (Hallmark library). Additional content, such as independent films, sports, family, and lifestyle productions, come from partnerships with established consumer brands: IFC®, ESPN®, World Wrestling Entertainment®, Classic Media, Sesame Workshop®, Discovery Kids™, Animal Planet and The Learning Channel (TLC™).

The Distributor has developed a fully integrated direct-to-retail distribution platform that parallels the home entertainment divisions of the major Hollywood studios. This platform provides direct sales and marketing, inventory management and state-of-the-art supply-chain services. In collaboration with leading replicators and third-party logistics and supply-chain companies, we have rapidly scaled this network, which has helped to facilitate our rapid growth in revenues.

We primarily sell to major national retailers including Wal-Mart, Blockbuster Entertainment, Best Buy, Circuit City, Kmart, Target, Netflix, Costco, Sam’s Club, Amazon, Barnes & Noble, Borders, Toys R Us and Columbia House. We co-produce programming with our branded content partners and mitigate the impact of our production costs through minimum guarantees from our revenue share partner, Blockbuster. We believe that the strong relationships we have developed with these well-known retailers and branded content partners help promote and enhance consumer awareness of our programs.

We collaborate with our retail and content partners to create sales programs that exploit their widely recognized brands and endorse related content. These sales programs focus on brands to provide the retailer with solutions that simplify the retailer’s buying process, improve shelf-space utilization, and help consumers quickly make informed purchase decisions. Our ability to deliver unique, innovative solutions that improve the sales and rentals of our content has enabled us to compete successfully and maintain strong relationships with our retail and content partners.

We currently distribute our library on DVDs, next-generation DVDs, and electronically in a digital format. We plan to continue to expand the distribution of our theatrical and non-theatrical products through the diverse and emerging digital distribution markets including: Video-on-Demand (“VOD”) and Electronic Sell-Through (“EST”) on the Internet to companies such as Amazon, Apple, MovieLink and Microsoft, Internet-based subscription VOD customers (such as NetFlix) and direct-to-television peer-to-peer network solutions. Through our partnerships, we have released 128 theatrical and non-theatrical titles since inception (including ninety titles released in 2007). The Distributor distributes products to basic channels distributed on cable, Direct Broadcast Satellite (“DBS”) and Internet Protocol Television (“IPTV”), which delivers television programming to households via a broadband connection using Internet protocols. Further, we are exploring kiosk-based distribution with retailers.

1

Industry Overview

The traditional and Internet markets for entertainment products such as DVDs and compact discs (“CDs”) are highly competitive. We face significant competition with respect to the number of products currently available in the marketplace and in securing distribution at retail outlets. The costs of entry into the retail and Internet markets for competitive products are low, and there are no significant barriers to entry.

Established companies who compete with the Distributor include major studios such as Buena Vista (Disney), Fox (who distributes MGM and Lions Gate home entertainment products), Paramount, Sony, Warner Bros. and Universal Studios, as well as certain independent studios and suppliers, such as Image Entertainment. The Distributor’s portfolio of owned and distributed content from The Weinstein Company®, ESPN®, World Wrestling Entertainment®, Sesame Workshop®, Classic Media and others provides the Distributor with a high volume of major studio quality, theatrically released feature films and direct-to-video releases, which we believe provides the Distributor with a strong competitive position in the marketplace.

Changes in the distribution, sale and use of home entertainment products have created significant business opportunities. We believe these changes have driven the demand for branded content, and that this demand will grow based on several recent trends, including the following:

| · | We believe that owners of major consumer entertainment brands are increasingly recognizing the retail channel as a critical component of their sales growth strategy. This is due in part to the large installed base of 95.3 million DVD set-top households in the U.S. as at year-end 2007 (according to Adams Research, Hollywood After Market January 31, 2008 Newsletter, Vol. 14, No. 6) and the consolidation of retailers by national retail chains which offer exposure to a large population of consumers, as well as the emergence of new retailers who service their customer base through the Internet; |

| · | We believe that national retail chains, including Wal-Mart, Best Buy and Target, have focused on branded content for their retail environment in order to improve the sales and profitability of their largest retail categories, including home entertainment. |

Home entertainment is the largest sector of filmed entertainment. In 2007 DVD units sold to consumers were 1.1 billion. Consumer spending on DVD purchases was $15.9 billion, a decline of 3.2% from 2006. In addition, consumer spending on rental transactions was $8.2 billion (2.5 billion rental transactions, a decline of 2.2% from 2006). Total home video consumer spending in 2007 was $24.1 billion (all data according to Adams Research, Hollywood After Market January 31, 2008 Newsletter, Vol. 14, No. 6).

Management believes that, with the end of the high definition format war, any lingering doubts about the strong near-term future of home video will be mitigated. The impact should translate into reduced consumer confusion and an increase in high definition demand. The Distributor plans to release titles on the Blu-Ray format in 2008.

Distribution/Supply Chain

Direct-to-Retail Distribution Platform

Through the Distributor, we have relationships with and are a direct supplier to nearly every major retailer or major wholesaler of entertainment-based products. These relationships provide more control over our inventory, the ability to customize our distribution strategies for a large number of retail locations and independence from third-party wholesalers. Through the Distributor, we provide Vendor Managed Inventory (“VMI”) services and contract with merchandisers to assist several of our most important retail partners in merchandising and managing their inventory. Through our VMI system, we manage store level placement and replenishment of shelves. Our in-store displays effectively highlight and promote our products and brands to the consumer. We customize store-level distribution and replenishment strategies based upon analysis of each product relative to the retailer’s inventory plan, store traits, seasonal trends and forecasted store traffic, as well as the buying patterns, habits and demographics of consumers to whom the products are targeted.

2

Strong Relationships with Key Retailers

Our direct-to-retail distribution capabilities and independence from major film studios enable us to work with our retail and content partners to develop innovative programs. We believe our retail-centric focus builds deeper relationships and gives us the opportunity to connect major brands with retailers and their customers, thereby increasing our level of business with our partners. We work with both our retail and content partners to develop promotional plans, re-pricing strategies and volume forecasts for catalog as well as recently released titles. We utilize tools to measure project effectiveness and customer feedback that enable us to develop unique programs to improve the level of service for our partners.

Wide Range of Diverse Retailers

Our ability to reach a wide variety of retailers enables us to access a broad spectrum of customer demographics through which we have attracted major brand partners and thereby enabled us to develop a diversified portfolio of content. We currently distribute directly to a mixture of retailers, including:

| · | Mass retail stores: Wal-Mart, Target, Kmart, Costco and Sam’s Club |

| · | Electronics stores: Best Buy, Fry’s and Circuit City |

| · | Bookstores: Borders and Barnes & Noble |

| · | Music retailers: Trans World Entertainment and Virgin |

| · | Emerging retailers: Amazon.com, Netflix, iTunes, Microsoft and MovieLink |

| · | Rental outlets: Blockbuster, Hollywood Video and Movie Gallery |

| · | Direct marketing companies: QVC and Columbia House |

We also sell through key select wholesale distribution companies, including Ingram, Alliance Entertainment Corp., Video Products Distributors, and Baker & Taylor.

Content Partnerships

Our retail marketing and distribution expertise has attracted widely recognized brand content partners from major competitors. For example, we were granted the exclusive home video distribution rights for ESPN®, which is owned by The Walt Disney Company. We utilize widely recognized consumer branded content to improve customer recognition and purchase of our products, encourage repeat purchases, and manage marketing costs (which are typically lower for branded content than for comparable content not associated with a brand). Our content strategy is primarily driven by our focus on retail partners’ requirements, which has led us to identify our four core content categories, which we call “Content Verticals”:

| · | Theatrical/Independent Films (includes Independent Film Channel (IFC)® , RHI Entertainment™ (Hallmark library), Tartan, The Weinstein Company® and Wellspring™) |

| · | Sports (includes ESPN® and World Wrestling Entertainment® (“WWE”)) |

| · | Lifestyle (includes Animal Planet and The Learning Channel (TLC™)) |

| · | Family/Faith (includes Classic Media, Discovery Kids™, Entertainment Rights and Sesame Workshop®) |

We believe that the breadth of our content portfolio allows us to compete effectively with the major studios in almost every major content segment.

The Distributor has released over 95 TWC theatrical titles on DVD, including the following recent or forthcoming releases:

Released Titles:

| · | Halloween, directed by Rob Zombie |

| · | The Nanny Diaries, starring Scarlett Johansson and Laura Linney |

| · | Who’s Your Caddy?, directed by Don Michael Paul |

| · | Sicko, directed by Michael Moore (Fahrenheit 911) |

3

| · | Planet Terror, directed by Robert Rodriguez and starring Josh Brolin |

| · | 1408, based on a short story by Stephen King and starring John Cusack and Samuel L. Jackson |

Upcoming Titles:

| · | The Hunting Party, starring Richard Gere and Terrence Howard | |

| · | Grace is Gone, starring John Cusack |

| · | Awake, starring Hayden Christensen and Jessica Alba |

| · | The Mist, starring Thomas James and Marcia Gay Hayden |

| · | Control, starring Sam Riley and Samantha Morton |

| · | Pete Seeger: The Power of Song, documentary by Jim Brown |

| · | Dedication, starring Billy Crudup and Mandy Moore |

The following selection of content releases and upcoming releases with the Distributor’s other major content partners demonstrates the breadth of the Distributor’s expanding film library:

Released Titles: | Partner | ||

| · | The Christmas Card, starring Ed Asner, John Newton and Alice Evans | RHI Entertainment™ | |

| · | Avenging Angel, starring Kevin Sorbo and Cynthia Watros | RHI Entertainment™ | |

| · | John Cena: My Life | WWE | |

| · | Rey Mysterio: The Biggest Little Man | WWE | |

| · | The Bronx is Burning | ESPN® | |

| · | Ultimate NASCAR | ESPN® | |

| · | Little People, Big World | Discovery/TLC™ | |

| · | Meerkat Manor | Animal Planet | |

| · | Flight 27 Down | Discovery Kids™ | |

| · | Kenny the Shark | Discovery Kids™ | |

| · | Sesame Street: Ready for School! | Sesame Workshop® | |

| · | Casper’s Scare School | Classic Media | |

Upcoming Titles: | |||

| · | Ten Commandments, starring Ben Kingsley, Christian Slater, Alfred Molina and Elliott Gould | Promenade Pictures | |

| · | Tin Man, starring Zooey Deschanel, Alan Cumming, Neal McDonough and Richard Dreyfuss | RHI Entertainment™ | |

| · | Hogfather, based on the novel by Terry Pratchett | RHI Entertainment™ | |

| · | The Legacy of Stone Cold Steve Austin | WWE® | |

| · | The Rock: The Most Electrifying Man in Sports Entertainment | WWE® | |

| · | Sesame Street: Dinosaurs | Sesame Workshop® | |

| · | Elmo’s Christmas Countdown | Sesame Workshop® | |

| · | Jeff Corwin Experience | Animal Planet | |

| · | Gorillas on the Brink | Animal Planet | |

| · | LA Ink | TLC™ | |

| · | Trading Spaces: The Specials | TLC™ | |

| · | Turok: Son of Stone | Classic Media | |

| · | Pat the Bunny Playdates | Classic Media | |

Proven Management Team

Our management team is comprised of seasoned home entertainment industry executives, some of whom have been involved in the home entertainment distribution industry with major Hollywood studios from its inception. Additionally, our senior financial professionals have sophisticated media investment banking experience in capital markets transactions, content acquisitions and production financing. We have attracted experienced personnel in home entertainment, acquisition, sales, marketing, distribution and finance.

4

Vision and Execution

A key driver of our business strategy is to exploit our extensive relationships with retailers and branded content providers to increase our share of the home video market and other entertainment products. Our growth strategy centers on capitalizing from our direct-to-retail distribution platform to (i) increase business with existing and new content partners, (ii) engage in profitable production and licensing of new content, (iii) continue to expand into new markets and complementary businesses including digital distribution, interactive software (video games) and (iv) license our partners’ proprietary brands and content. To achieve these goals, we intend to:

Further Penetrate Existing Retail and Content Partner Relationships

Our retail and content partner relationships and broad distribution and marketing capabilities offer multiple opportunities to increase business with our existing retail and content partners. We actively pursue these opportunities through increasing the number of co-productions with our content partners, extending a successful project to other divisions of our retail partners, and fostering relationships built in one part of our retail partners’ organizations to win business opportunities in other divisions.

Co-Produce Content with Brand Partners

Some of our key distribution agreements, including those with ESPN®, WWE®, Sesame Street®, Classic Media and RHI Entertainment™, provide the opportunity to co-produce content in which we will own either a portion of or the entire copyright, earn a distribution fee and/or share in the profits of such content. We anticipate that we will increase the number of co-productions to improve gross margins and expand our owned-content library.

Pursue Strategic Alternatives to Take Advantage of Fixed-Cost Infrastructure

We have built a fully integrated distribution and marketing infrastructure to deliver superior service to our retail and content partners. We now plan to take advantage of our distribution and marketing infrastructure, as well as the expertise of our third-party supply-chain partners, to expand our home entertainment distribution business into: (i) other geographical markets such as Canada; (ii) the interactive software/video game distribution business, which is complementary to our existing supply-chain, retail and content partnerships; and (iii) licensing and marketing services for our branded content partners and retail customers. While our focus is on internal growth, we may selectively pursue acquisitions that accomplish a previously identified strategic goal where acquiring that capability is more cost-effective than building it internally. As an example, in April 2007, we acquired Castalian Music (as defined in Item 7), a direct response music and video company, from EMI. The acquisition of Castalian Music enables us to provide our content partners an additional consumer channel.

The Weinstein Company Transaction

On July 21, 2006 (the “Closing Date”), the Company completed a transaction (the “TWC Transaction”) with TWC Holdings and W-G Holding (two subsidiaries of TWC) pursuant to which we launched the Distributor to exploit the exclusive U.S. home video distribution rights to feature film and direct-to-video releases owned or controlled by TWC. On the Closing Date, the Company contributed substantially all of its assets (except for $1 million in cash and certain liabilities), its employees, and its existing businesses to the Distributor.

Thus, the Distributor is owned 70% by TWC Holdings and W-G Holding and 30% by the Company. The 70% interest in the Distributor held by TWC Holdings and W-G Holding consists of Class W Units and is redeemable, at TWC Holdings’ and W-G Holding’s option commencing at any time from July 21, 2007 for up to 70% of the Company’s outstanding common stock, or with TWC Holdings’ and W-G Holding’s approval, cash. The redemption value of the Class W Units may not be less than $60.0 million. The Company’s 30% membership interest in the Distributor consists of the Distributor’s Class G Units.

In addition, the Company issued an aggregate of 100 shares of its Series W Preferred Stock to TWC Holdings and W-G Holding in connection with the TWC Transaction. The Series W Preferred Stock provides the holders thereof with (i) the right to elect five of the seven directors on our Board of Directors, of which two are currently TWC Holdings executives, (ii) majority voting power over other actions requiring approval of our stockholders, and (iii) the right to approve certain specified actions. The Series W Preferred Stock has no rights to receive dividends and minimal liquidation value.

5

On the Closing Date, the Company also entered into a Registration Rights Agreement with TWC Holdings and W-G Holding pursuant to which the Company agreed to register for resale the shares of the Company’s common stock issuable upon redemption of Class W Units in the Distributor currently held by them. The Company and/or the Distributor entered into the following agreements on the Closing Date: (i) an Amended and Restated Limited Liability Company Agreement for the Distributor, (ii) a Video Distribution Agreement between the Distributor and TWC (the “TWC Distribution Agreement”), (iii) a Services Agreement between the Company and the Distributor and (iv) an Assignment and Assumption Agreement.

From December 5, 2005 through the Closing Date, the Company operated under an interim distribution agreement with TWC and recorded the results from titles we released for TWC on our financial statements. After the Closing Date, substantially all of the operating activities we previously conducted, as well as the results from releasing TWC product, are reflected in the financial statements of the Distributor.

For a full description of the TWC Transaction, please see our Current Report on Form 8-K filed with the Securities and Exchange Commission (the “SEC”) on July 26, 2006.

Suppliers and Compliance with Environmental Laws

We are not aware of any environmental laws that materially affect our business or the business of the Distributor.

Internet Business

Consumers who visit our website at www.geniusproducts.com can learn about us and the Distributor’s products. We are also creating a business-to-business section that will allow retailers to gain access to promotional and marketing materials. We believe that a continued Internet presence is desirable because it aids in consumer sales, business-to-business sales, brand exposure and retail sales.

Corporate Information

Genius Products, Inc. was incorporated in the State of Nevada on January 8, 1996 under the name Salutations, Inc. In October 1999, we changed our name to Genius Products, Inc. to reflect our primary business of producing, publishing, licensing and distributing audio and video products under our “Baby Genius” brand. In March 2005, we changed our state of incorporation to Delaware.

Genius Products, LLC was formed in the State of Delaware on May 10, 2005 as a wholly-owned subsidiary of The Weinstein Company Holdings LLC, and was originally named The Weinstein Company Funding LLC. The company was renamed Genius Products, LLC on July 21, 2006 in connection with the TWC Transaction.

Our principal executive offices are located at 2230 Broadway, Santa Monica, California 90404, and our telephone number is (310) 453-1222. Our Internet address is www.geniusproducts.com.

EMPLOYEES

As of December 31, 2007, the Company had 2 employees and the Distributor had 219 full-time employees and one part-time employee.

None of the Distributor’s employees are represented by an organized labor union. We believe that the Distributor’s relationship with its employees is good, and neither the Company nor the Distributor has experienced an employee-related work stoppage.

INTERNET ACCESS TO OUR SEC REPORTS

Our Internet address is www.geniusproducts.com. Through our website, we make available, free of charge, the following reports as soon as reasonably practicable after electronically filing them with, or furnishing them to, the SEC: our Annual Reports on Form 10-K; our Quarterly Reports on Form 10-Q; our Current Reports on Form 8-K; and amendments to those reports. Our Proxy Statements for our Stockholder Meetings are also available through our website. Our website and the information contained therein or connected thereto are not intended to be incorporated into this Annual Report on Form 10-K.

6

We have a history of significant losses, and we may never achieve or sustain profitability.

The Company has incurred operating losses in all but two quarters since we commenced operations. As of December 31, 2007, we had an accumulated deficit of $46.4 million. Our net loss for the year ended December 31, 2007 was $14.9 million. Our net loss before extraordinary gain for the year ended December 31, 2006 was $47.0 million. Our net loss for the year ended December 31, 2005 was $17.2 million. Neither we nor the Distributor may ever achieve or sustain profitability in the future. Our continued operating losses may have a material adverse effect upon the value of our common stock and may jeopardize our ability to continue our operations.

Our business, results of operations and financial condition depend principally on the success of the Distributor.

In July 2006 we contributed substantially all of our assets to the Distributor in exchange for a 30% interest in that entity. As a result of that transaction, our business substantially consists of acting as the managing member of, and holding a membership interest in, the Distributor. Accordingly, our business results of operations and financial condition depend almost exclusively on the successful operations of the Distributor. Further, in the past the Distributor has provided and we expect the Distributor in the future to continue providing, funds to pay our operating costs, including the cost of preparing and filing reports with the SEC. If the Distributor does not continue to provide these funds, our overhead may increase and our net income may decline as a percentage of revenues.

Failure to achieve and maintain effective disclosure controls or internal controls would have a material adverse effect on our ability to report our financial results timely and accurately.

Effective internal controls are necessary for us to produce reliable financial reports and are important in our effort to prevent financial fraud. We are required to periodically evaluate the effectiveness of the design and operation of our internal controls. These evaluations may result in the conclusion that enhancements, modifications or changes to our internal controls are necessary or desirable. Company management has concluded that several material weaknesses relating to the internal controls and related structure existed as of December 31, 2007 at both the Company and the Distributor. While Company management evaluates the effectiveness of our internal controls on a regular basis, we cannot provide absolute assurance that these controls will be remediated timely, and be considered effective, nor can we give any assurance that the controls, accounting processes, procedures and underlying assumptions will not be subject to revision. As such, until remediated, these weaknesses could adversely affect the accuracy or timing of future filings with the SEC and other regulatory authorities. There are also inherent limitations on the effectiveness of internal controls and financial reporting practices, including collusion, management override, and failure of human judgment. Because of this, control procedures and financial reporting practices are designed to reduce rather than eliminate business risks. If we fail to maintain an effective system of internal control over financial reporting or if and for so long as management or our independent registered public accounting firm were to discover material weaknesses in our internal control over financial reporting (or if our system of controls and audits result in a change of practices or new information or conclusions about our financial reporting) like the disclosed material weakness, we may be unable to produce reliable financial reports or prevent fraud and it could harm our financial condition and results of operations and result in loss of investor confidence and a decline in our stock price. A discussion of these material weaknesses and our remediation efforts can be found in Item 9A. Controls and Procedures — Management’s Report on Internal Control Over Financial Reporting.

If the Distributor continues to grow at a rapid pace, it may not be able to manage that growth effectively.

Initially the Company, then through its transfer of assets and operations to the Distributor in mid 2006, have each expanded operations rapidly since inception. Net revenues increased from $22.3 million in fiscal 2005 (for the Company), to $274.6 million in fiscal 2006 (for the Company and Distributor combined), and to $474.1 million in fiscal 2007 (for the Distributor). This substantial growth has placed a significant strain on management systems and resources. The Distributor is currently investing in new management information systems and related technology, increasing the number of employees in the affected areas, and improving processes. However, if the Distributor’s operations continue to grow at this rate, the Distributor could experience serious operating difficulties in these and other areas (including difficulties in hiring, training and managing an increasing number of employees, difficulties in obtaining manufacturing capacity to produce products, and delays in production and shipments), which could result in a material adverse effect on the Distributor and us.

7

The Distributor’s business depends upon the success of its relationship with TWC and our other key content suppliers.

A significant amount of the Distributor’s net revenue is derived from the distribution rights accorded to the Distributor under its distribution agreements with TWC and other key content suppliers. Specifically, 67% of the Distributor’s net revenue in fiscal year 2007 was derived from TWC-controlled titles, compared to 84% in fiscal year 2006. The Distributor’s results of operations and financial condition depend principally on the success of the relationships with TWC and other content suppliers. To grow its business, the Distributor is reliant on the quantity and quality of theatrical and direct-to-video releases provided by TWC and its other content partners. The failure of the Distributor to maintain its relationships with TWC and other key content suppliers would have a material adverse effect on the Distributor and us.

The motion picture industry is rapidly evolving, and recent trends have shown that audience response to both traditional and emerging distribution channels is volatile and difficult to predict.

The entertainment industry in general and the motion picture industry in particular continue to undergo significant changes, due both to shifting consumer tastes and to technological developments. New technologies, such as video-on-demand and Internet distribution of films, have provided motion picture companies with new channels through which to distribute their films. Accurately forecasting both the changing expectations of movie audiences and market demand within these new channels have proven challenging.

We cannot accurately predict the overall effect shifting audience tastes, technological change or the availability of alternative forms of entertainment may have on the Distributor. In addition to uncertainty regarding the DVD market, there is uncertainty as to whether other developing distribution channels and formats, including video-on-demand, Internet distribution of films and high-definition, will attain expected levels of public acceptance or, if such channels or formats are accepted by the public, whether the Distributor will be successful in exploiting the business opportunities they provide. Moreover, to the extent that these emerging distribution channels and formats gain popular acceptance, the demand for delivery through DVDs may decrease.

The Distributor faces intense competition.

The market for entertainment products, including DVDs and CDs, is highly competitive. The Distributor faces significant competition from both Hollywood studios and other independent distributors with respect to the number of titles currently available and in securing distribution at retail outlets. The costs of entry into the retail and Internet markets for competitive products are low, and there are no significant barriers to entry. Many of the Distributor’s competitors are larger with established brand names, greater resources and access to established distribution channels, and therefore may be able to adapt more quickly to changes in customer requirements, devote greater resources to marketing and sale of their products, generate greater brand recognition or adopt more aggressive pricing policies than the Distributor. As a result, the revenues, results of operation and financial position of the Distributor may be materially adversely affected.

The unauthorized use of the Distributor’s intellectual property rights may reduce revenues.

The success of the Distributor’s business is highly dependent on the maintenance by our content partners of intellectual property rights in the entertainment products the Distributor distributes. New technologies such as peer-to-peer technology, high speed digital transmissions (including digital distribution of theatrical films) and some features of digital video recorders have made infringement of intellectual property in films and television programming easier and faster and enforcement of intellectual property rights more challenging. Unauthorized use of intellectual property rights in the entertainment industry generally is a significant and rapidly growing phenomenon. These developments may result in a loss of revenues as a result of sales of unauthorized products.

The loss of any major customer would harm us.

The Distributor does not have long-term agreements with its customers, nor is it an exclusive supplier to any of its retail customers. If any customer were to reduce or cancel a significant order, it would have a material adverse effect on its business, results of operations and financial condition. For 2007, Wal-Mart and Blockbuster Entertainment accounted for 34% and 20%, respectively, of the Distributor’s net revenues. For the period from July 22, 2006 through December 31, 2006, Wal-Mart accounted for 31% of the Distributor’s net revenues. At December 31, 2007, Wal-Mart and Target comprised 36% and 12% of the Distributor’s accounts receivable after allowances, respectively, while at December 31, 2006, Wal-Mart and Best Buy comprised 50% and 7% of the Distributor’s accounts receivable after allowances, respectively.

Substantially all of the Distributor’s revenues are derived from the distribution rights accorded to the Distributor under its distribution agreements with TWC and other key content suppliers. Specifically, 84% of the Distributor’s net revenue for the period from July 22, 2006 through December 31, 2006, and 67% of the Distributor’s net revenue for fiscal 2007 were derived from its agreement with TWC. The Distributor’s business, operational results and financial condition depend principally on the success of the relationships between it and these content suppliers.

8

The Distributor’s products are subject to returns.

The Distributor’s products are subject to return. While we anticipate a certain level of returns, if product returns experienced by the Distributor are significantly greater than anticipated, it will negatively impact the business of the Distributor and us. If the actual amount of customer returns significantly exceeds historic return rates, it would have an adverse effect upon the Distributor and our results of operations.

The Distributor’s cash flow may not be sufficient to meet its operational needs.

At December 31, 2007, the Distributor had cash balances of $3.1 million, with an additional $7.8 million of short-term and $3.3 million of long-term restricted cash. The $7.8 million is part of the Distributor’s short-term liquid cash that had accumulated in a central lockbox account and can only be disbursed weekly pursuant to the terms of the “Allocation of Accounts Receivable and Intercreditor Agreement” entered into by and among the Distributor, The Weinstein Company, LLC and Société Générale dated August 10, 2007. The $3.3 million is comprised of: (i) $3 million in a money market account, which is restricted pursuant to our credit facility with Société Générale and (ii) $0.3 million in a certificate of deposit which is securing a letter of credit on the Distributor’s Broadway lease. The Distributor may need or choose to obtain additional financing to fund its activities in the future. Funds could be raised by selling securities or by entering into credit agreements. The Distributor may not be able to obtain additional funds on acceptable terms, or at all. In addition, the Distributor’s ability to borrow funds in excess of certain agreed upon thresholds is subject to the approval of TWC Holdings. If adequate funds are not available, the Distributor may be required to curtail its operations.

Inventory obsolescence may adversely affect the Distributor’s business.

The Distributor maintains a substantial investment in its DVD inventory, and if it overestimates the demand for a particular title, it may have to destroy excess inventory. Further, the Distributor’s agreements with content providers may limit its ability to sell such titles at discounted prices. The Distributor’s estimated allowances for obsolete or unmarketable inventory are based upon management’s understanding of market conditions and forecasts of future product demand, which are subject to change. The Distributor reviews inventory for excess or obsolete product on a quarterly basis. Obsolescence is determined by taking the total inventory on hand less the 12 months projected sales. Any inventories in excess of 12 months are deemed 100% obsolete and a corresponding charge for obsolescence is recorded. Obsolescence is calculated only on inventory for which the Distributor is responsible on a title-by-title basis, which includes all theatrical and direct-to-video titles.

The Distributor’s revenues and results of operations may fluctuate significantly.

The Distributor’s revenues and results of operations (and consequently our 30% equity interest in the Distributor) depend significantly upon the success of the motion pictures and television programming delivered by our content partners that we distribute and which cannot be predicted with certainty. Accordingly, our revenues and results of operations may fluctuate significantly from period to period. The results of one period may not be indicative of the results of any future period. Our revenues and results are also significantly influenced by seasonality and in particular the all-important fourth quarter gift-giving season. Any quarterly fluctuations that we report in the future may not match the expectations of market analysts and investors. This could cause the price of our common stock to fluctuate significantly.

Litigation may harm our business and the Distributor or otherwise distract management.

Substantial, complex or extended litigation could cause us and the Distributor to incur large expenditures and could distract management. For example, lawsuits by licensors, employees or stockholders could be very costly and disrupt business. While disputes from time to time are not uncommon, we may not be able to resolve such disputes on terms favorable to us and the Distributor.

Our business would be adversely affected if the Distributor lost key members of its executive management team.

We are highly dependent on the efforts and performance of the Distributor’s executive management team. The loss of any key members of this team could result in our inability to manage our operations effectively or to execute our business strategy. The failure to maintain or replace any such individuals could have a material adverse effect on the Distributor and us.

9

If we cease to serve as the managing member of the Distributor, we could become subject to the Investment Company Act of 1940.

The Amended and Restated Limited Liability Company Agreement of the Distributor (the “Distributor LLC Agreement”) contemplates that TWC Holdings or its designee will become the managing member of the Distributor, instead of the Company, if we become insolvent or bankrupt, if we violate the membership interest transfer restrictions in the Distributor LLC Agreement or if a lender forecloses on a security interest granted with respect to our Class G Units in the Distributor. If we cease to serve as the managing member of the Distributor, then we could become subject to the Investment Company Act of 1940 (the “1940 Act”), which could have a material adverse effect on our business.

Under the 1940 Act, a company may be deemed to be an investment company if it owns investment securities with a value exceeding 40% of its total assets, subject to certain exclusions. If we ceased to serve as the managing member of the Distributor and were deemed an investment company, we would become subject to the requirements of the 1940 Act. As a consequence, among other things, we would likely incur significant expenses and could be prohibited from engaging in our business or issuing our securities as we have in the past.

Revenues and results of operations are at risk from competition from major motion picture studios, music and game distributors, and other independent content suppliers for limited retail shelf space. The failure by the Distributor to successfully compete for and procure retail shelf space for its products could have a material adverse effect on the Distributor and us.

None.

On December 31, 2007, the Distributor entered into a lease commitment (the “New Maguire Lease”) with Maguire Properties – 3301 Exposition, LLC (“Maguire LLC”), pursuant to which the Distributor will rent approximately 40,520 square feet of office space in Santa Monica, California. When complete, this facility will be the consolidated home office of the Company and the Distributor, housing all employees currently located at the Company’s and the Distributor’s Santa Monica offices.

The initial term of the New Maguire Lease is ten (10) years, commencing five (5) months after the completion of certain tenant improvements to be constructed by Maguire LLC (the “Occupancy Date”), which Occupancy Date is currently projected to be in July, 2008. The Distributor has an option to extend the term of the New Maguire Lease for two (2) additional five (5) year terms, subject to the satisfaction of certain conditions specified in the New Maguire Lease.

As security for its obligations under the New Maguire Lease, the Distributor has delivered to Maguire LLC an irrevocable letter of credit in the amount of $1.5 million. The aforementioned tenant improvements are being constructed at Maguire LLC’s expense in accordance with an agreed upon space plan and subject to certain conditions specified in the New Maguire Lease.

Also on December 31, 2007, the Distributor and Maguire Properties, L.P. (“Maguire LP”) amended the lease agreement, dated January 23, 2007 (the “Old Maguire Lease”), under which the Distributor currently rents approximately 14,000 square feet of office space located in Santa Monica, California. Under the amendment to the Old Maguire Lease, Maguire L.P. agreed to waive the Distributor’s monthly rent for a period commencing on January 1, 2008 through the Occupancy Date under the New Maguire Lease. The Distributor has the right to terminate the Old Maguire Lease at any time upon five (5) business days’ prior written notice. The Distributor’s accounting and finance departments are currently housed in this office space.

10

On October 12, 2007, Castalian, LLC, a wholly owned subsidiary of the Distributor (“Castalian”), entered into a lease agreement with 2800 OBI, LP (the “Castalian landlord”), under which Castalian rents approximately 6,465 square feet of office space in Santa Monica, California. This lease has a three (3) year term commencing on November 23, 2007. Castalian also has the option to extend the lease for an additional three (3) year term upon the expiration of the initial term.

On January 5, 2007, the Distributor entered into a sublease agreement with The Advantage Network, LLC, under which the Distributor subleased to The Advantage Network, LLC its leasehold interest in a 5,603 square foot facility located in Solana Beach, California. This sublease is for a term commencing February 1, 2007 and ending December 31, 2008. Until March 2006, we used this facility as our principal executive offices pursuant to a sublease agreement entered into in November 2003. The November 2003 sublease is for a five-year term which commenced in January 2004, and was assigned to the Distributor as part of the TWC Transaction.

On March 18, 2006, we entered into a five-year lease agreement for a 17,400 square foot facility located in Santa Monica, California. This lease was assigned to the Distributor as part of the TWC Transaction. This facility has been used as our, and the Distributor’s, principal executive offices.

On March 22, 2005, as part of the acquisition of American Vantage Media Corporation and Wellspring Media, Inc., we assumed office space in New York and Santa Monica on a month-to-month basis. Effective as of April 30, 2006, we terminated our lease for the Santa Monica space. Effective as of the Closing Date of the TWC Transaction, the Distributor assumed all of our rights and obligations under the New York lease, and continues to occupy the New York space.

On October 15, 2004, we entered into a sublease agreement for a 1,670 square foot facility located in Bentonville, Arkansas. This sublease has a five-year term and expires in October 2009. This sublease was assigned to the Distributor as part of the TWC Transaction.

Except as described below, neither we nor the Distributor are a party to any legal or administrative proceedings, other than routine litigation incidental to our business and that of the Distributor that we do not believe, individually or in the aggregate, would be likely to have a material adverse effect on our, or the Distributor’s, financial condition or results of operations.

FALCON PICTURE GROUP MATTER

On October 3, 2005, Falcon Picture Group, LLC (“Falcon”) commenced litigation against the Company in the Circuit Court of Cook County, Illinois, Case No. 05H16850 (the “Illinois Proceeding”), based upon allegations, among other things, that the Company breached the terms of a license agreement between Falcon and the Company by refusing to pay certain royalties to which Falcon allegedly was entitled. On or about July 2007, Falcon was granted leave to file an amended complaint alleging further that the Company interfered with Falcon’s current and potential business relationships. Falcon seeks damages resulting from the interference claim of approximately $0.4 million as well as $0.8 million relating to the claim for breach of the license agreement. The court’s decision to grant leave to amend is not indicative of the merits of such amended claims as leave to amend proceedings in the early stages of litigation are routine procedural matters.

The Company has asserted various affirmative defenses to Falcon’s complaint, including, among other things, that Falcon in fact breached the license agreement by delivering defective content to the Company, double billed for content and failed to honor provisions in the license agreement requiring Falcon to indemnify the Company in the event of claims by third parties that the Company did not possess the legal right to sell Falcon content. The Company has also asserted that the additional claims in Falcon’s amended complaint are unfounded, and that the damages asserted by the Company pursuant to its own claims will substantially exceed the damages sought by Falcon. The Company believes that the evidence will demonstrate that there was no monetary default on its part under the license agreement insofar as, at the time of the alleged default, Falcon was indebted to the Company for an amount substantially in excess of the sum Falcon claims was past due. Accordingly, the Company has commenced litigation against Falcon and its owner, Carl Amari, in the form of a counter claim seeking damages of approximately $1.5 million, exclusive of any award of attorneys’ fees, costs of suit and punitive damages to which the Company may also be entitled to recover. Discovery is in its final stages but a trial date has not yet been scheduled. The Company plans to continue to vigorously defend against Falcon’s allegations and to pursue its counter claim against Falcon.

11

ENTERTAINMENT RESOURCE MATTER

In June 2007, Larry S. Hyman, as assignee for Entertainment Resource, Inc. (“ERI”), commenced litigation against the Company in the Circuit Court of Broward County, Florida, Case No. 06-012249 CACE 05, based upon allegations, among other things, that the Company owes ERI for products delivered and sold to the Company by ERI between September 2005 and January 2006. ERI seeks an award of $0.9 million. The Company plans to vigorously defend against ERI’s allegations and has denied ERI’s allegations in response to their complaint. Among other defenses, the Company plans to provide evidence that ERI owes to the Company approximately $1 million for products sold and delivered by the Company to ERI, which amount should be set-off against any amounts owing by the Company to ERI. Discovery is in its early stages and the action has not been scheduled for trial.

On October 31, 2007, stockholders of the Company holding voting rights equivalent to seventy percent (70%) of the outstanding shares of our common stock executed written consents in lieu of a special meeting approving a reverse stock split of the Company’s common stock in an exchange ratio of (i) one-for-five, (ii) one-for-six, (iii) one-for-seven, or (iv) one-for-eight (the “Reverse Stock Split”), with the Company’s Board of Directors retaining the discretion of whether to implement the Reverse Stock Split and which exchange ratio to implement. The Company’s Board of Directors approved the proposed Reverse Stock Split on September 28, 2007, but the Board of Directors has not yet determined whether to implement the Reverse Stock Split or which exchange ratio to implement. A complete description of the proposed Reverse Stock Split is included in the Company’s Definitive Information Statement filed with the SEC on October 31, 2007.

Our 2007 Annual Meeting of Stockholders was held on December 5, 2007. Of the 67,673,344 shares eligible to vote, 50,161,285 appeared by proxy and established a quorum for the meeting. The singular matter considered at the annual meeting was the election of directors, with the holders of our common stock entitled to appoint two directors and the holders of our Series W Preferred Stock entitled to appoint five directors. The items listed in the table below were approved by, respectively, a majority of the common stockholders appearing at the meeting and a majority of the Series W Preferred stockholders appearing at the meeting.

| VOTES FOR | VOTES AGAINST | VOTES WITHHELD | NOT VOTED | ||||||||||||||||

| 1. | Election of Directors by Common Stockholders | ||||||||||||||||||

| Stephen K. Bannon | 45,401,109 | 126,000 | 4,634,176 | 0 | |||||||||||||||

| Trevor Drinkwater | 45,526,109 | 1,000 | 4,634,176 | 0 | |||||||||||||||

| VOTES FOR | VOTES AGAINST | VOTES WITHHELD | NOT VOTED | ||||||||||||||||

| 2. | Election of Directors by Series W Preferred Stockholders | ||||||||||||||||||

| Bradley A. Ball | 100 | 0 | 0 | 0 | |||||||||||||||

| James G. Ellis | 100 | 0 | 0 | 0 | |||||||||||||||

| Herbert Hardt | 100 | 0 | 0 | 0 | |||||||||||||||

| Larry Madden | 100 | 0 | 0 | 0 | |||||||||||||||

| Irwin Reiter | 100 | 0 | 0 | 0 | |||||||||||||||

12

Our stock trades on the over-the-counter bulletin board (“OTCBB”) under the symbol “GNPI”. The market represented by the OTCBB is extremely limited and the price for our common stock quoted on the OTCBB is not necessarily a reliable indication of the value of our common stock. The following table sets forth the high and low bid prices for shares of our common stock for the periods noted, as reported on the OTCBB. Quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions.

| YEAR | PERIOD | HIGH | LOW | ||||||

| Calendar Year 2006 | First Quarter | $ | 2.35 | $ | 1.62 | ||||

| Second Quarter | 2.08 | 1.55 | |||||||

| Third Quarter | 2.12 | 1.63 | |||||||

| Fourth Quarter | 2.72 | 1.78 | |||||||

| Calendar Year 2007 | First Quarter | $ | 3.30 | $ | 2.53 | ||||

| Second Quarter | 3.32 | 2.63 | |||||||

| Third Quarter | 2.96 | 2.30 | |||||||

| Fourth Quarter | 2.85 | 1.59 | |||||||

Our common stock is subject to Rules 15g-1 through 15g-9 under the Securities Exchange Act of 1934, as amended, which impose certain sales practice requirements on broker-dealers who sell our common stock to persons other than established customers and “accredited investors” (generally, individuals with a net worth in excess of $1,000,000 or an annual income exceeding $200,000 individually or $300,000 together with their spouses). For transactions covered by this rule, a broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction prior to the sale.

13

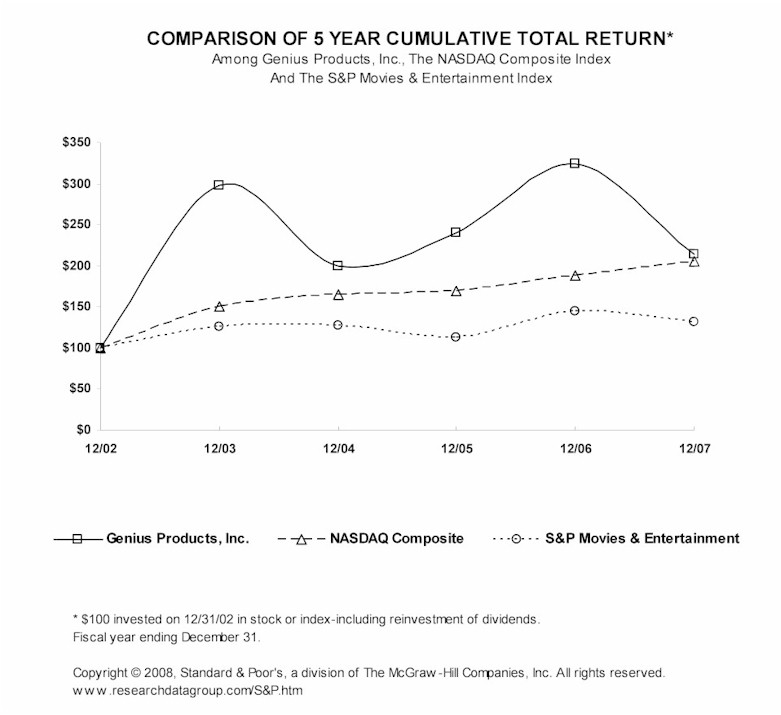

Stock Performance Graph

The following graph compares the performance of our common stock over the five preceding fiscal years to the weighted average performance over the same period of the stock of companies included in the NASDAQ Composite Index and the S&P Movies and Entertainment Index. The graph assumes $100 was invested at the close of trading on December 31, 2002 in our common stock and in each of the indices and that all dividends were reinvested. The stockholder return shown on the graph below should not be considered indicative of future stockholder returns, and we will not make or endorse any predictions of future stockholder returns.

Stockholders

As of February 29, 2008, we had 67,709,094 shares of common stock issued and outstanding which were held by 184 stockholders of record, including the holders that have their shares held in a depository trust in “street” name. The transfer agent for our common stock is Interwest Transfer Company, 1981 East 4800 South, Suite 100, Salt Lake City, Utah 84117.

14

Equity Compensation Plans

The following table provides information concerning our equity compensation plans as of December 31, 2007.

| (Securities in thousands) | ||||||

Number of securities to be issued Upon exercise of outstanding options, warrants and rights (a) | Weighted-average exercise price of outstanding options, warrants and rights (b) | Number of securities remaining available for future issuance under Equity Compensation Plans (excluding securities reflected in column (a)) (c) | ||||

| Equity compensation plans approved by security holders | 28,196 | $ | 2.06 | 8,290 | ||

| Equity compensation plans not approved by security holders | — | — | — | |||

| Total | 28,196 | $ | 2.06 | 8,290 | ||

Dividend Policy

Our Board of Directors determines any payment of dividends. We have never declared or paid cash dividends on our common or preferred stock. We do not expect to authorize the payment of cash dividends on our shares of common or preferred stock in the foreseeable future. Any future decision with respect to dividends will depend on future earnings, operations, capital requirements and availability, restrictions in future financing agreements and other business and financial considerations.

Sales of Unregistered Securities

On March 2, 2005, we engaged in a private placement of 6,518,987 shares of our common stock and five-year warrants to purchase 1,303,797 shares of common stock, half at an exercise price of $2.56 per share and half at an exercise price of $2.78 per share. The transaction closed on March 3, 2005 and we realized gross proceeds of $10.3 million from the financing, before deducting commissions and other expenses. We agreed to register for resale the shares of common stock issued in the private placement and shares issuable upon exercise of warrants. Such registration statement became effective on May 11, 2005.

On March 22, 2005, in connection with the Company’s acquisition of American Vantage Corporation from American Vantage Companies (“AVC”), the Company issued to AVC (i) 7,000,000 shares of the Company’s common stock valued at $2.27 per share and (ii) warrants to purchase 1,400,000 shares of the Company’s common stock, half at an exercise price of $2.56 per share and half at an exercise price of $2.78 per share.

In May 2005, we engaged in a private placement of 3,000,000 shares of our common stock and five-year warrants to purchase 270,000 shares of our common stock at an exercise price of $2.56 per share. The transaction closed on May 20, 2005, and we realized gross proceeds of $5.25 million from the financing before deducting commissions and other expenses.

On December 5, 2005, we engaged in a private placement of 16,000,000 shares of our common stock and five-year warrants to purchase 4,800,000 shares of common stock with an exercise price of $2.40 per share. The transaction closed on December 6, 2005 and we realized gross proceeds of $32 million from the financing, before deducting commissions and other expenses.

On October 4, 2005, we entered into a Note and Warrant Purchase Agreement with a group of investors (collectively, the “Investors”). Under the Note and Warrant Purchase Agreement, the Investors loaned a total of $4.0 million to the Company in exchange for (i) promissory notes in favor of the Investors with a total principal balance of $4.0 million and (ii) five-year warrants to purchase a total of 280,000 shares of our common stock at an exercise price of $1.88 per share.

15

From time to time, the Company has awarded stock options to certain individuals outside of the Company’s stock option plans.

The aforementioned sales of securities were not registered under the Securities Act of 1933, as amended (the “Act”), or any state securities laws, and were sold in private transactions exempt from registration pursuant to Section 4(2) of the Act and Regulation D promulgated thereunder.

You should read the financial data set forth below in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (included in Item 7) and our consolidated financial statements and the related notes included in this Annual Report.

Genius Products, Inc.

| (In thousands), except per share data | Years Ended December 31, | |||||||||||||||||||

2007 *, ^ (Restated) | 2006 *, ^ (Restated) | 2005 | 2004 | 2003 | ||||||||||||||||

| Statement of Operations data: | ||||||||||||||||||||

| Revenues, net of sales returns, discounts and allowances | $ | - | $ | 119,011 | $ | 22,328 | $ | 16,630 | $ | 3,069 | ||||||||||

| Cost of revenues | - | 130,870 | 22,883 | 13,893 | 2,150 | |||||||||||||||

| Gross profit (loss) | - | (11,859 | ) | (555 | ) | 2,737 | 919 | |||||||||||||

| Operating expenses (income): | ||||||||||||||||||||

| General and administrative | 5,248 | 20,752 | 14,747 | 8,231 | 3,531 | |||||||||||||||

| Restructuring | - | - | 2,745 | - | - | |||||||||||||||

| Gain on sale, related party | - | (63 | ) | (1,352 | ) | - | - | |||||||||||||

| Equity in net loss from Distributor | 10,565 | 7,989 | - | - | - | |||||||||||||||

| Total operating expenses | 15,813 | 28,678 | 16,140 | 8,231 | 3,531 | |||||||||||||||

| Loss from operations | (15,813 | ) | (40,537 | ) | (16,695 | ) | (5,494 | ) | (2,612 | ) | ||||||||||

| Net interest income (expense) | (797 | ) | 853 | (465 | ) | (551 | ) | (130 | ) | |||||||||||

| Loss before provision for income taxes | (16,610 | ) | (39,684 | ) | (17,160 | ) | (6,045 | ) | (2,742 | ) | ||||||||||

| Provision (benefit) for income taxes | (1,730 | ) | 7,304 | 1 | 1 | 1 | ||||||||||||||

| Loss before extraordinary item | (14,880 | ) | (46,988 | ) | (17,161 | ) | (6,046 | ) | (2,743 | ) | ||||||||||

| Extraordinary gain, net of taxes | - | 54,203 | - | - | - | |||||||||||||||

| Net income (loss) | $ | (14,880 | ) | $ | 7,215 | $ | (17,161 | ) | $ | (6,046 | ) | $ | (2,743 | ) | ||||||

| Basic and diluted earnings per common shares | ||||||||||||||||||||

| Loss before extraordinary item | $ | (0.22 | ) | $ | (0.77 | ) | $ | (0.42 | ) | $ | (0.25 | ) | $ | (0.16 | ) | |||||

| Extraordinary item | - | 0.89 | - | - | - | |||||||||||||||

| Net income (loss) | $ | (0.22 | ) | $ | 0.12 | $ | (0.42 | ) | $ | (0.25 | ) | $ | (0.16 | ) | ||||||

| Basic and diluted weighted average common shares | 66,222 | 60,949 | 40,400 | 23,827 | 17,574 | |||||||||||||||

| Balance Sheet data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 1,757 | $ | 3,745 | $ | 30,597 | $ | 1,224 | $ | 941 | ||||||||||

| Working capital | 1,669 | 3,707 | 21,441 | 60 | 1,150 | |||||||||||||||

| Investment in Distributor | 73,002 | 87,694 | - | - | - | |||||||||||||||

| Total assets | 83,060 | 92,326 | 76,365 | 12,996 | 5,575 | |||||||||||||||

| Redeemable common stock | - | - | 414 | 395 | 491 | |||||||||||||||

| Deferred gain, related party | - | - | 1,212 | - | - | |||||||||||||||

| Total stockholders' equity | 65,897 | 73,858 | 55,188 | 4,432 | 2,723 | |||||||||||||||

*For 2007 and 2006, the financial data reflects results from the Company's venture with The Weinstein Company, and will not be comparable to prior years. 2006 results reflect operations of Genius Products, Inc. from January 1 through July 21, 2006 and the Company's equity in net loss from the Distributor from July 22 through December 31, 2006. During 2007, the Company had no operations. Its operating loss is comprised of general and administrative expenses and equity in net loss from the Distributor for the fiscal year.

^ The aforementioned restatements relate to (i) an error in the application of generally accepted accounting principles with respect to the recognition in the Company’s financial statements of costs paid on its behalf by the Distributor and (ii) an error in the application of generally accepted accounting principles with respect to the accounting classification and measurement of certain redemption rights of the holders of the Distributor’s Class W Units. See Note 3 to each of the Company’s and the Distributor’s financial statements for further details regarding the restatements.

16

Genius Products LLC

| (In thousands) | Years Ended December 31, | |||||||

2007 ^ (Restated) | 2006 * | |||||||

| Statement of Operations data: | ||||||||

| Revenues, net of sales returns, discounts and allowances | $ | 474,087 | $ | 155,591 | ||||

| Cost of revenues | 451,597 | 168,044 | ||||||

| Gross profit (loss) | 22,490 | (12,453 | ) | |||||

| Operating expenses: | ||||||||

| General and administrative | 38,440 | 7,566 | ||||||

| Total operating expenses | 38,440 | 7,566 | ||||||

| Loss from operations | (15,950 | ) | (20,019 | ) | ||||

| Other income (expense) | (2,882 | ) | 309 | |||||

| Net loss | $ | (18,832 | ) | $ | (19,710 | ) | ||

| * For 2006, the financial data reflects results from July 22 through December 31, 2006 | ||||||||

^ See comment above

17

THE WEINSTEIN COMPANY TRANSACTION.

On July 21, 2006 (the “Closing Date”), the Company completed a transaction (the “TWC Transaction”) with TWC Holdings and W-G Holding (two subsidiaries of TWC) pursuant to which we launched the Distributor to exploit the exclusive U.S. home video distribution rights to feature film and direct-to-video releases owned or controlled by TWC. On the Closing Date, the Company contributed substantially all of its assets (except for $1 million in cash and certain liabilities), its employees, and its existing businesses to the Distributor.

Thus, the Distributor is owned 70% by TWC Holdings and W-G Holding and 30% by the Company. The 70% interest in the Distributor held by TWC Holdings and W-G Holding consists of Class W Units and is redeemable, at TWC Holdings’ and W-G Holding’s option commencing at any time from July 21, 2007 for up to 70% of the Company’s outstanding common stock, or with TWC Holdings’ and W-G Holding’s approval, cash. The redemption value of the Class W Units may not be less than $60.0 million. The Company’s 30% membership interest in the Distributor consists of the Distributor’s Class G Units. (see Equity Investment in Distributor section below).

In addition, the Company issued an aggregate of 100 shares of the Company’s Series W Preferred Stock to TWC Holdings and W-G Holding in connection with the TWC Transaction. The Series W Preferred Stock provides the holders thereof with (i) the right to elect five of the seven directors on the Company’s Board of Directors, of which two are currently TWC executives, (ii) majority voting power over other actions requiring approval of our stockholders, and (iii) the right to approve certain specified actions. The Series W Preferred Stock has no rights to receive dividends and minimal liquidation value.

On the Closing Date, the Company entered into a Registration Rights Agreement with TWC Holdings and W-G Holding pursuant to which we agreed to register for resale the shares of our common stock issuable upon redemption of Class W Units in the Distributor currently held by them. The Company and/or the Distributor also entered into the following agreements on the Closing Date: (i) an Amended and Restated Limited Liability Company Agreement of the Distributor, (ii) a Video Distribution Agreement (the “TWC Distribution Agreement”), (iii) a Services Agreement, and (iv) an Assignment and Assumption Agreement.

From December 5, 2005 through the Closing Date, the Company operated under an interim distribution agreement with TWC and recorded the results from titles we released for TWC on our consolidated financial statements. After the Closing Date, substantially all of the operating activities we previously conducted, as well as the results from releasing TWC product, are reflected in the financial statements of the Distributor.

For a full description of the TWC Transaction, please see our Current Report on Form 8-K filed with the Securities and Exchange Commission (the “SEC”) on July 26, 2006.

For the period from July 22, 2006 through December 31, 2007 (after the Closing Date), we accounted for our investment in the Distributor using the equity method of accounting. Under the equity method of accounting, only the Company’s investment in and amounts due to and from the Distributor are included in our consolidated balance sheet. As a result, we recorded an asset on our balance sheet related to our investment interest in the Distributor. In our statement of operations, we recorded our 30% share of the Distributor’s loss as equity in net losses from the Distributor. We recorded an extraordinary gain on sale of $54.2 million, after taxes, upon consummation of the TWC Transaction based on the difference between the fair market value of assets contributed and their net book value, reduced for the portion of the gain associated with our retained economic interest in the Distributor. We entered into a master contribution agreement related to the TWC Transaction effective December 5, 2005 and operated under an interim distribution agreement with TWC through July 21, 2006. During that period, we recorded the results from releasing TWC titles in our financial statements. After the Closing Date, substantially all of the operating activities that we previously conducted, including releasing TWC products, are reflected in the financial statements of the Distributor.

The information in this Annual Report pertaining to our business operations reflects the operations of the Company prior to the Closing Date and the operations of the Distributor after the Closing Date. In addition, we are including stand-alone financial statements and footnotes of the Distributor, which are located immediately following the footnotes for the Company.

CRITICAL ACCOUNTING POLICIES

NOTE: THE FOLLOWING CRITICAL ACCOUNTING POLICIES ARE CONSISTENTLY APPLIED BY BOTH THE COMPANY AND THE DISTRIBUTOR (For further details, refer to Note 2 in the Financial Notes and Disclosure section incorporated herein by reference)

ALLOWANCE FOR SALES RETURNS, PRICE PROTECTION, CUSTOMER DISCOUNTS, CUSTOMER DEDUCTIONS AND BAD DEBTS.

We calculate the allowance for doubtful accounts and provision for sales returns based on management’s estimate of the amount expected to be uncollectible or returned on specific accounts. We provide for future returns and price protection for releases of home video product at the time the products are sold. We calculate an estimate of future returns of product by analyzing units shipped, units returned and point of sale data to ascertain consumer purchases and inventory remaining with retail to establish anticipated returns. Price protection is calculated on a title by title basis. The objective of price protection is to mitigate returns by providing retailers with credits to ensure maximum consumer sales. Price protection is granted to retailers after they have presented the company an affidavit of existing inventory.

Other factors are taken into consideration in the calculation of future returns such as title genre, historical returns, projections of consumer demands, box office and other research. We allow for future returns on non-theatrical titles by analyzing a combination of historical returns, point of sale data and product seasonality.

18

We provide for customer discounts based on arrangements entered into on a customer-by-customer basis. We set aside reserves for bad debts and customer deductions based on management’s estimate of the amounts expected to be uncollectible on specific accounts.

INVENTORIES.