QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. 1)

| Filed by the Registrantý | |||

Filed by a Party other than the Registranto | |||

Check the appropriate box: | |||

o | Preliminary Proxy Statement | ||

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | ||

ý | Definitive Proxy Statement | ||

o | Definitive Additional Materials | ||

o | Soliciting Material Pursuant to §240.14a-12 | ||

BEACON POWER CORPORATION | ||||

(Name of Registrant as Specified In Its Charter) | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

ý | No fee required. | |||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

o | Fee paid previously with preliminary materials. | |||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

(1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

BEACON POWER CORPORATION

65 Middlesex Road

Tyngsboro, MA 01879

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

To be Held June 11, 2009

To the Stockholders of

Beacon Power Corporation:

We are hereby notifying you that Beacon Power Corporation will be holding its Annual Meeting of Stockholders at our corporate headquarters located at 65 Middlesex Road, Tyngsboro, Massachusetts 01879, on Thursday, June 11, 2009 at 1:00 p.m., local time, for the following purposes:

- (1)

- To elect six members of our Board of Directors for the ensuing year and until each of their successors is duly elected and qualified;

- (2)

- To amend our Sixth Amended and Restated Certificate of Incorporation to increase the authorized number of shares of common stock of the Company to 400,000,000;

- (3)

- To approve the issuance and sale of shares of common stock to Seaside 88, LP, pursuant to a Common Stock Purchase Agreement between Seaside and us dated February 19, 2009, in an amount greater than 19.9% of our outstanding shares of common stock as of the date of such agreement, for the purpose of complying with Nasdaq Marketplace Rules 5635(b) and 5635(d);

- (4)

- To ratify the selection of Miller Wachman LLP as independent auditors to audit our books and accounts for the fiscal year ending December 31, 2009; and

- (5)

- To transact such other business as may properly come before the meeting or any adjournment thereof.

Approval of the issuance of Common Stock in excess of the stated amounts (Proposal 3) is expressly conditioned on approval of the amendment to our Certificate of Incorporation to increase our common stock authorized for issuance (Proposal 2). Your vote is important. Whether or not you plan to attend the meeting, please vote as soon as possible. You may vote by mailing a completed proxy card, by telephone, or over the Internet. For specific voting instructions, please refer to the information provided with your proxy card and in this proxy statement.

| By Order of the Board of Directors, | ||

Beacon Power Corporation | ||

James M. Spiezio |

May 1, 2009

Tyngsboro, Massachusetts

| | Page | ||

|---|---|---|---|

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | 3 | ||

PROXY STATEMENT | 4 | ||

Introduction | 4 | ||

Methods of Voting | 4 | ||

Solicitation of Proxies | 4 | ||

Voting Rights | 5 | ||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 6 | ||

SECTION 16(a) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE | 8 | ||

PROPOSAL 1—ELECTION OF DIRECTORS | 9 | ||

CORPORATE GOVERNANCE | 11 | ||

Executive Officers | 11 | ||

Director Independence | 13 | ||

Limitation of Liability and Indemnification | 13 | ||

Communication with Our Board of Directors | 13 | ||

AUDIT COMMITTEE REPORT | 14 | ||

DIRECTOR AND EXECUTIVE OFFICER COMPENSATION | 15 | ||

Compensation Discussion and Analysis | 15 | ||

Report of the Compensation Committee | 28 | ||

Summary Compensation Table | 29 | ||

Grants of Plan-Based Awards | 33 | ||

Outstanding Equity Awards at Fiscal Year-End | 34 | ||

Potential Payments Upon Termination or Change in Control | 37 | ||

Director Compensation | 45 | ||

COMPENSATION COMMITTEE INTERLOCKS AND INSIDER PARTICIPATION | 46 | ||

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 47 | ||

PROPOSAL 2—AMENDMENT TO CERTIFICATE OF INCORPORATION | 49 | ||

Reasons for the Proposed Amendment | 49 | ||

Vote Required for Approval | 51 | ||

Effectiveness of Share Amendments | 51 | ||

PROPOSAL 3—SHARE ISSUANCE | 52 | ||

Background | 52 | ||

Reasons for Seeking Stockholder Approval | 53 | ||

Effect on Existing Stockholders | 54 | ||

Amendment to Rights Agreement | 56 | ||

Effect of Failure of Stockholders to Approve | 57 | ||

PROPOSAL 4—RATIFICATION OF SELECTION OF AUDITORS | 58 | ||

Principal Accounting Fees and Services | 58 | ||

Audit Fees | 58 | ||

Audit-Related Fees | 58 | ||

Tax Fees | 58 | ||

All Other Fees | 58 | ||

Audit Committee Pre-Approval Requirements | 59 | ||

Required Vote and Board of Directors Recommendation | 59 | ||

OTHER MATTERS | 59 | ||

INCORPORATION BY REFERENCE | 59 | ||

ANNUAL REPORT AND OTHER SEC FILINGS | 59 | ||

HOUSEHOLDING OF PROXY MATERIALS | 59 | ||

STOCKHOLDER PROPOSALS FOR 2010 ANNUAL MEETING | 60 | ||

APPENDIX A—Proposed Amendment to Sixth Amended and Restated Certificate of Incorporation | A-1 | ||

APPENDIX B—Common Stock Purchase Agreement | B-1 | ||

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

| This Proxy Statement may include statements that are not historical facts and are considered "forward-looking" statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements reflect Beacon Power Corporation's current views about future events and financial performances. These "forward-looking" statements are identified by the use of terms and phrases such as "believe," "expect," "plan," "anticipate," and similar expressions identifying forward-looking statements. Investors should not rely on forward-looking statements because they are subject to a variety of risks, uncertainties, and other factors that could cause actual results to differ materially from Beacon Power Corporation's expectation. These factors include: a short operating history; a history of losses and anticipated continued losses from operations; a need to raise additional capital combined with a questionable ability to do so, especially in view of the current situation in the financial markets and the evolving global economic crisis; the complexity and other challenges of arranging project financing and resources for one or more frequency regulation power plants, including uncertainty about whether we will be successful in obtaining DOE loan guarantee support for our New York facility; conditions in target markets, including the fact that some ISOs have been slow to comply with the FERC's requirement to update market rules to include new technology such as ours; our ability to obtain site interconnection approval, landlord approvals, or other zoning and construction approvals in a timely manner; limited experience manufacturing commercial products or supplying frequency regulation services on a commercial basis; limited commercial contracts for sales to date; the dependence of revenues on the achievement of product optimization, manufacturing and commercialization milestones; the uncertainty of the political and economic climate, and the different electrical grid characteristics and requirements of any foreign countries into which we hope to sell or operate, including the uncertainty of enforcing contracts, the different market structures, and the potential substantial fluctuation in currency exchange rates in those countries; dependence on third-party suppliers; intense competition from companies with greater financial resources, especially from companies that are already in the frequency regulation market; possible government regulation that would impede the ability to market products or services or affect market size; possible product liability claims and the negative publicity which could result; any failure to protect intellectual property, or any possible infringement of third party patents; retaining key executives and the possible need in the future to hire and retain key executives; and the historical volatility of our stock price, as well as the volatility of the stock price of other companies in the energy sector, especially in view of the current situation in the equity and debt financial markets. Such statements made by us fall within the safe harbors provided by Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These factors are elaborated upon and other factors are described in the section of our Annual Report on Form 10-K titled "Risk Factors Relating to Our Business." We disclaim any obligation to update any forward-looking statements contained herein after the date of this Proxy Statement. |

Important Notice Regarding the Availability of Proxy Materials for the Stockholder Meeting to be Held on June 11, 2009. Our proxy statement and annual report to security holders for the fiscal year ended December 31, 2008 are available atwww.beaconpower.com/proxy/.

If you plan to attend the shareholder meeting in person, please visit our website for directions to our corporate headquarters at 65 Middlesex Road, Tyngsboro, Massachusetts 01879. The website address for directions iswww.beaconpower.com/contact/visitingbeacon.htm. You may also contact our investor relations department to obtain directions at (978) 694-9121.

3

BEACON POWER CORPORATION

FOR THE ANNUAL MEETING OF STOCKHOLDERS

On June 11, 2009

This Proxy Statement is furnished in connection with the solicitation of proxies by the Board of Directors of Beacon Power Corporation ("we", "us", "Beacon", "our", or the "Company") for use at the Annual Meeting of Stockholders to be held on June 11, 2009 beginning at 1:00 p.m. at our corporate headquarters located at 65 Middlesex Road, Tyngsboro, Massachusetts 01879, and at any adjournment or postponement of that meeting.

We are furnishing you with this Proxy Statement in connection with the solicitation of proxies to be used at the Annual Meeting of Beacon to be held on June 11, 2009 and at any adjournment of the Annual Meeting, for the purposes set forth in the accompanying notice of the meeting. All holders of record of our Common Stock at the close of business on April 24, 2009 will be entitled to vote at this meeting and any adjournments thereof. The stock transfer books have not been closed.

This Proxy Statement, our Annual Report on Form 10-K for the fiscal year ended December 31, 2008 and the accompanying proxy card were mailed to our stockholders on or about May 1, 2009.

You may vote by mail, by telephone, over the Internet or in person at the Annual Meeting.

Voting by Mail. By signing and returning the proxy card in the enclosed prepaid and addressed envelope, you are authorizing the individuals named on the proxy card to vote your shares at the Annual Meeting in the manner you indicate. We encourage you to sign and return the proxy card even if you plan to attend the meeting. Please sign and return your proxy card to ensure that all of your shares are voted.

Voting by Telephone. To vote by telephone, please follow the instructions included on your proxy card. If you vote by telephone, you do not need to complete and mail your proxy card.

Voting over the Internet. To vote over the Internet, please follow the instructions included on your proxy card. If you vote over the Internet, you do not need to complete and mail your proxy card.

Voting in Person at the Annual Meeting. If you plan to attend the Annual Meeting and vote in person, we will provide you with a ballot at the meeting. If your shares are registered directly in your name, you are considered the stockholder of record and you have the right to vote in person at the Annual Meeting. If your shares are held in the name of your broker or other nominee, you are considered the beneficial owner of shares held in street name. As a beneficial owner, if you wish to vote at the meeting, you will need to bring to the meeting a legal proxy from your broker or other nominee authorizing you to vote such shares.

We are soliciting proxies in the form enclosed on behalf of the Board of Directors. We will vote any such signed proxy, if received in time for the voting and not revoked, at the Annual Meeting according to your directions. We will vote any proxy that fails to specify a choice on any matter to be acted upon FOR the election of each nominee for director and FOR each other proposal to be acted upon. If you submit a signed proxy in the form enclosed, you will have the power to revoke it at any time before we use it by filing a later proxy with us, by attending the Annual Meeting and voting in person, or by notifying us of the revocation in writing addressed to the Secretary of Beacon Power Corporation at 65 Middlesex Road, Tyngsboro, MA 01879.

4

We will pay for all expenses of preparing, assembling, printing and mailing the material used in the solicitation of proxies by the Board. Officers and regular Beacon employees may solicit proxies on behalf of the Board by telephone, telegram or personal interview, and we will bear the expenses of such efforts. We also may make arrangements with brokerage houses and other custodians, nominees and fiduciaries to forward soliciting materials to the beneficial owners of stock held of record by such persons at our expense. We have retained Georgeson Shareholder Communications, Inc. to assist in the solicitation of proxies for a fee of $8,500 plus reasonable out-of-pocket expenses.

As of April 24, 2009, we had 114,490,887 shares of our common stock, $0.01 par value ("Common Stock"), issued and outstanding. You may vote your shares of Beacon Common Stock at the Annual Meeting if you were a stockholder of record as the close of business on April 24, 2009. Each share of Common Stock that you held as of the record date entitles you to one vote on each matter to be voted upon at the Annual Meeting. All holders of Common Stock vote together as one class.

The presence at the Annual Meeting, either in person or by proxy, of the holders of a majority of the issued and outstanding shares of Common Stock on the record date is necessary to constitute a quorum to transact business at the Annual Meeting. If a quorum is not present, it is expected that the Annual Meeting will be adjourned or postponed in order to solicit additional proxies. Shares of Common Stock represented at the Annual Meeting but not voted, including shares of Common Stock for which proxies have been received but for which the holders have abstained, will be treated as present at the Annual Meeting for purposes of determining the presence or absence of a quorum for the transaction of all business.

Assuming a quorum is established, directors will be elected (under Proposal 1) by a plurality of votes cast. If a vote is withheld regarding the election of directors, such vote will have no effect because the directors receiving a plurality of votes are elected.

To approve the amendment to the Sixth Amended and Restated Certificate of Incorporation (Proposal 2), stockholders holding more than fifty percent (50%) of our issued and outstanding shares of Common Stock that are entitled to vote must vote FOR such Proposal.

To approve the issuance of shares of common stock to Seaside 88, LP (Seaside) in excess of amounts that would otherwise be permissible under applicable Nasdaq continued listing rules (Proposal 3), a majority of the shares cast on the Proposal must be voted FOR the Proposal. Shares already issued to Seaside under the Common Stock Purchase Agreement will not be voted on this Proposal. In addition, approval of Proposal 3 is expressly conditioned upon approval of the amendment to our Sixth Amended and Restated Certificate of Incorporation (Proposal 2).

Approval of Proposal 4, the ratification of auditors, requires the affirmative vote of a majority of shares represented at the meeting.

If you return your proxy with instructions to abstain from voting on any of the proposals, your shares will be counted for purposes of determining whether a quorum is present at the Annual Meeting and for purposes of determining the total number of votes cast on each proposal described in this Proxy Statement. Other than with respect to the election of directors proposal, an abstention with respect to the other proposals has the legal effect of a vote "AGAINST" the proposal. Brokers and banks holding shares in street name have the authority to vote in favor of all the nominees for director and in favor of ratifying auditors when they have not received contrary instructions from the beneficial owners. However, if your shares are held by your broker in "street name" and you do not vote your shares, your brokerage firm does not have the authority to vote your unvoted shares held by the firm on Proposal 2 or Proposal 3. Since the broker non-votes are not considered cast on the Proposals, they will not have any effect on the outcome of Proposal 3. However, under Delaware law, to determine whether Proposals 2 and 4 have received the necessary number of affirmative votes, broker non-votes, like abstentions will have the same effect as a vote AGAINST Proposals 2 and 4.

5

No Appraisal Rights

There are no appraisal rights associated with any of the proposals being considered at the Annual Meeting.

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

The following table sets forth, as of April 22, 2009, certain information concerning the ownership of shares of our Common Stock by:

- •

- Each person or group that we know beneficially owns more than five percent of the issued and outstanding shares of common stock

- •

- Each director

- •

- Our Senior Managers; and

- •

- All of our directors and executive officers as a group. Except as otherwise indicated, each person named has sole investment and voting power with respect to his, her or its shares of common stock shown.

Each beneficial owner other than Capital Ventures International, Enable Growth Partners, LP and Seaside 88, LP has an address c/o Beacon Power Corporation, 65 Middlesex Road, Tyngsboro, Massachusetts 01879.

Name and Address of Beneficial Owner | Amount and nature of beneficial ownership(1) | Percent of Class | |||||

|---|---|---|---|---|---|---|---|

| Stephen P. Adik (2) | 290,843 | * | |||||

| F. William Capp (2) | 2,647,623 | 2.3 | % | ||||

| Daniel E. Kletter (2) | 135,583 | * | |||||

| Matthew L. Lazarewicz (2) | 1,260,194 | 1.1 | % | ||||

| Virgil G. Rose (2) | 129,650 | * | |||||

| Jack P. Smith (2) | 327,149 | * | |||||

| James M. Spiezio (2) | 1,199,993 | * | |||||

| Edward A. Weihman (2) | 112,984 | * | |||||

5% Shareholder | |||||||

| Capital Ventures International (3) Heights Capital Management, Inc. One Capitol Place Grand Cayman, Cayman Islands British West Indies | 10,648,953 | 8.5 | % | ||||

Enable Growth Partners, L.P. (4) Enable Capital Management LLC One Ferry Building, Suite 255 San Francisco, CA 94111. | 8,600,730 | 7.5 | % | ||||

Seaside 88, LP (5) 750 Ocean Royale Way, Suite 805 North Palm Beach, FL 33408 | 7,465,161 | 6.5 | % | ||||

All directors and executive officers as a group (8 persons) | 6,104,019 | 5.1 | % | ||||

- *

- Less than 1%.

- (1)

- The number of shares beneficially owned by each stockholder is determined under rules issued by the Securities and Exchange Commission and includes voting or investment power with respect to

6

those securities. Under these rules, beneficial ownership includes any shares as to which the individual or entity has sole or shared voting power or investment power and includes any shares as to which the individual or entity has the right to acquire beneficial ownership within 60 days after April 22, 2009 through the exercise of any warrant, stock option or other right. The inclusion in this joint proxy statement of these shares, however, does not constitute an admission that the named stockholder is a direct or indirect beneficial owner of those shares. The number of shares of Beacon common stock outstanding used in calculating the percentage for each listed person includes the shares of Beacon common stock underlying options or restricted stock units held by that person that are exercisable or convertible within 60 days of April 22, 2009, but excludes shares of Beacon common stock underlying options or restricted stock units held by any other person.

- (2)

- Includes the following shares of the Company's Common Stock which the indicated executive officer or director had the right to acquire within 60 days after April 22, 2009, through the exercise of stock options or restricted stock units: Mr. Adik, 290,843; Mr. Capp, 2,135,045; Mr. Kletter, 135,583; Mr. Lazarewicz, 888,590; Mr. Rose, 129,650; Mr. Smith, 324,149; Mr. Spiezio, 951,062; and Mr. Weihman 112,984.

- (3)

- Heights Capital Management, Inc., the authorized agent of Capital Ventures International ("CVI"), has discretionary authority to vote and dispose of the shares held by Capital Ventures International and may be deemed to be the beneficial owner of these shares. The address for Heights Capital Management, Inc. is 101 California Street, Suite 3250, San Francisco, CA 94111. Martin Kobinger, in his capacity as Investment Manager of Heights Capital Management, Inc., may also be deemed to have investment discretion and voting power over the shares held by CVI. Mr. Kobinger disclaims any such beneficial ownership of the shares. According to the Schedule 13G filing referenced below, this amount does not include 447,973 shares underlying warrants to purchase Common Stock, which warrants are not exercisable to the extent that the shares then beneficially owned by the reporting persons would exceed 4.99% of our outstanding Common Stock. Information regarding the number of shares of common stock held by CVI is based solely on information contained in a Schedule 13G filed with the SEC jointly with Heights Capital Management, Inc. on February 13, 2009.

- (4)

- Enable Capital Management, LLC ("ECM") is the general partner and/or investment manager of Enable Growth Partners, L.P. ("EGP") and Mitchell S. Levine ("Levine"), is managing member and majority owner of Enable Capital Management, LLC. ECM and Levine may, therefore, be deemed to beneficially own the Securities owned by EGP and such other investment limited partnerships for the purposes of Rule 13d-3 of the Securities Exchange Act of 1934, as amended, insofar as they may be deemed to have the power to direct the voting or disposition of those securities. Each of ECM and Levine disclaims beneficial ownership as to the securities, except to the extent of his or its pecuniary interests therein. Information regarding the number of shares of common stock held by ECM, EGP and Levine is based solely on information contained in the Schedules 13G each filed with the SEC on February 10, 2009.

- (5)

- Seaside 88, LP ("Seaside") is a Florida limited partnership for which Seaside 88 Advisors, LLC serves as general partner. William J. Ritger and Denis M. O'Donnell are managing members of the general partner of Seaside. Each may therefore be deemed to beneficially own the shares owned by Seaside for the purposes of Rule 13d-3 of the Securities Exchange Act of 1934, as amended, insofar as they may be deemed to have the power to direct the voting or disposition of those shares. Each disclaims beneficial ownership as to the shares. The number of shares beneficially owned represents the 7,465,161 shares sold to Seaside in February, March and April 2009, and assumes none have been sold since their purchase. The amounts reported in the table do not reflect shares that may be acquired by Seaside in the two monthly closings that are scheduled to occur within 60 days of April 22, 2009, because there are conditions to such closings outside of the control of Beacon and Seaside, and because the number of shares to be issued in such closings is dependent upon the market price at the time of sale and cannot be determined at

7

this time. The maximum number of shares that could be purchased by Seaside during such 60 day period is 10,000,000. If the maximum amount of shares were purchased in the next two monthly closings, Seaside's ownership percentage would be approximately 14.0%.

Equity Compensation Plan Information. The following table gives information about equity awards under our stock option plan and employee stock purchase plan, as of December 31, 2008.

Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | (a) | (b) | (c) | |||||||

Equity compensation plans approved by security holders | 11,238,470 | $ | 1.18 | 7,478,264 | ||||||

Equity compensation plans not approved by security holders | 100,000 | $ | 1.18 | — | ||||||

Total | 11,338,470 | $ | 1.18 | 7,478,264 | ||||||

For additional information concerning our equity compensation plans, see discussion in footnotes 2 and 9 to our consolidated financial statements in our Annual Report on Form 10-K filed with the SEC on March 16, 2009 and under the caption "Compensation Discussion and Analysis" in this proxy statement for the Annual Meeting of Stockholders.

SECTION 16(a) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE

Section 16(a) of the Securities Exchange Act of 1934 (the "Exchange Act") requires our directors and officers, and persons who beneficially own more than ten percent of a registered class of our equity securities, to file with the SEC initial reports of ownership and reports of changes in ownership of our Common Stock. Directors, officers and greater than ten percent stockholders are required by SEC regulation to furnish us with copies of all Section 16(a) forms they file.

To our knowledge, during our fiscal year ended December 31, 2008, all Section 16(a) filing requirements applicable to our directors, officers and ten percent stockholders were satisfied.

8

PROPOSAL 1

ELECTION OF DIRECTORS

Our Board of Directors has nominated the persons named below for election at the 2009 Annual Meeting as directors. The directors who are elected will hold office until their successors shall have been duly elected and qualified as of the 2010 Annual Meeting of stockholders. In accordance with the Delaware General Corporation Law, each nominee for director requires a plurality of the votes of shares present in person or represented by proxy at the Annual Meeting in order to gain election.

The nominees are members of our present Board of Directors. The nominees for director have consented to being named nominees in this Proxy Statement and have agreed to serve as directors, if elected at the Annual Meeting. The Common Stock represented by proxies will be voted for the election of directors of the nominees unless we receive contrary instructions. If any of the nominees is unwilling or unable to serve, favorable and uninstructed proxies will be voted for a substitute nominee designated by our Board of Directors. If a suitable substitute is not available, our Board of Directors will reduce the number of directors to be elected.

We encourage our directors to attend each of our Annual Meetings of Stockholders. At our 2008 Annual Meeting of Stockholders, all of our then current directors were present.

OUR BOARD RECOMMENDS A VOTE "FOR" THE NOMINEES FOR DIRECTOR LISTED BELOW.

F. William Capp, age 60 (director since 2001)

Mr. Capp has served as our President, Chief Executive Officer and Board member since December 1, 2001 when he joined the Company. Mr. Capp received a Bachelor of Science in Aeronautical Engineering from Purdue University, a Master of Business Administration and a Masters Degree in Mechanical Engineering from the University of Michigan.

Stephen P. Adik, age 65 (director since 2004)

Audit Committee

Compensation Committee

Finance Committee

Mr. Adik served as Vice Chairman at NiSource Inc. (NYSE: NI), a Fortune 500 electric, natural gas and pipeline company, from December 2000 until his retirement in December 2003. He served on the Board of NiSource from December 2000 to May 2005. He is a member of the Board of Directors and Chairman of the Audit Committee of NorthWestern Corporation, an electric and natural gas company. He is also a member of the Board of Directors of the Chicago South Shore and South Bend Railroad, a regional railroad company and the Dearborn Mid-West Conveyor Company, a supplier of material handling equipment to the automotive and bulk materials industry. Mr. Adik received a Bachelor of Science degree in Mechanical Engineering from the Stevens Institute of Technology, and an MBA degree in Finance from Northwestern University.

9

Daniel E. Kletter, age 70 (director since October 2006)

Audit Committee

Finance Committee

Nominating and Governance Committee

Mr. Kletter is an independent consultant with more than 29 years of operating management, acquisition and director experience. From 1999 to 2001 he was with ING-BARINGS/ABN-AMRO, where he was Managing Director in the Industrial Manufacturing and Technology Group. Mr. Kletter serves on the Board of Directors of Power Curbers, Inc. Mr. Kletter received a Bachelor of Science in Mechanical Engineering from the University of Notre Dame, and a Masters Degree in Business Administration from Northwestern University.

Virgil G. Rose, age 63 (director since January 2007)

Compensation Committee

Nominating and Governance Committee

Mr. Rose has been an independent consultant providing advisory services that include working with the United States Department of Energy, California Energy Commission, California ISO, Bonneville Power Authority, National Labs, and numerous west coast utilities since 2004. From 2001 to 2004, Mr. Rose was Senior Vice President and Director of Energy Delivery and Management at Nexant, an international energy industry consulting company. Mr. Rose has 38 years of experience in the electric utility industry in various consulting, engineering, system operation, and management capacities, including 27 years with Pacific Gas & Electric (PG&E), where he served as Senior Vice President of Electric Supply. Mr. Rose received a Bachelor of Science in Electrical Engineering from Fresno State University, a Master of Science in Electrical Engineering from Santa Clara University, and has completed the Advanced Management Program at Harvard University.

Jack P. Smith, age 60 (director since 2001)

Compensation Committee

Nominating and Governance Committee

Mr. Smith is Chairman, Director and co-owner of Silversmith Inc., a producer of natural gas well metering and automated data reporting systems. Mr. Smith co-founded Silversmith Inc. in 2003. Prior to his current engagement with Silversmith, Mr. Smith was President and CEO of Holland Neway International, a leading producer of commercial vehicle suspensions and brake systems. Mr. Smith also serves on the Board of Directors of Bissell Corporation in Grand Rapids, Michigan, SRAM Corporation in Chicago and Weasler Engineering in Wisconsin. He is a Trustee of Grand Valley State University Foundation. Mr. Smith received a Bachelor of Science and Masters Degree in Mechanical Engineering and a Masters Degree in Business Administration from the University of Michigan.

Edward A. Weihman, age 60 (director since 2007)

Audit Committee

Finance Committee

Mr. Weihman is currently President of Kirkwood, Weihman & Co., LLC, a consulting firm serving the oil and gas industry. He was a Managing Director at Dresdner Kleinwort and a predecessor firm, Wasserstein Perella, from 1995 to 2006, where he was engaged in the mergers and acquisitions business for the firm's natural Resources and Utility clients. Mr. Weihman received a Bachelor of Arts degree from Williams College and a Masters Degree in Business Administration from Columbia University.

10

The names, ages, current positions and principal occupations during the last five years of our current Executive Officers are described below.

Name | Age | Position | |||

|---|---|---|---|---|---|

F. William Capp | 60 | President and Chief Executive Officer | |||

Matthew L. Lazarewicz | 58 | Vice President of Engineering and Chief Technical Officer | |||

James M. Spiezio | 61 | Vice President of Finance, Chief Financial Officer, Treasurer and Secretary | |||

F. William Capp

Mr. Capp has served as our President, Chief Executive Officer and member of the Board since December 1, 2001 when he joined the Company. Mr. Capp received his Bachelor of Science in Aeronautical Engineering from Purdue University, a Master of Business Administration and a Master's Degree in Mechanical Engineering from the University of Michigan.

Matthew L. Lazarewicz

Mr. Lazarewicz has served as our Vice President of Engineering since February 1999, and was named our Chief Technical Officer in September of 2001. Mr. Lazarewicz is a Registered Professional Engineer in the Commonwealth of Massachusetts and received both Bachelor's and Master's Degrees in Mechanical Engineering from the Massachusetts Institute of Technology. Mr. Lazarewicz also completed his Master's Degree in Management at the Massachusetts Institute of Technology Sloan School of Management.

James M. Spiezio

Mr. Spiezio joined our Company in May 2000. He has served as Vice President of Finance, Chief Financial Officer and Treasurer since July 2000, Secretary since March 2001, and was our Corporate Controller from May 2000 to July 2000. He has over twenty-seven years of diversified manufacturing and financial management experience. Mr. Spiezio is a graduate of the Indiana University School of Business.

Board of Directors' Meetings and Committees

Meetings. During the fiscal year ended December 31, 2008, our Board of Directors held 15 meetings. Each director attended more than 75% of the aggregate of (i) the total number of meetings of our Board of Directors held during the period for which he has been a director and (ii) the total number of meetings held by all committees of our Board of Directors on which he served during the period.

11

Committees. Our Board of Directors has established four standing committees: the Audit Committee, the Compensation Committee, Finance Committee and the Nominating and Governance Committee. No member of any of these committees is an employee of Beacon. Effective February 1, 2009, the membership of each committee is listed below.

| Audit | Compensation | Nominating and Governance | Finance Committee | |||

|---|---|---|---|---|---|---|

| Stephen P. Adik,Chair | Jack P. Smith,Chair | Virgil G. Rose,Chair | Daniel E. Kletter,Chair | |||

| Edward A. Weihman | Stephen P. Adik | Daniel E. Kletter | Stephen P. Adik | |||

| Daniel E. Kletter | Virgil G. Rose | Jack P. Smith | Edward A. Weihman |

Audit Committee. Under rules of the Nasdaq Stock Market, our Audit Committee must have at least three members, all of whom must be "independent." All members of our Audit Committee qualify as "independent" as defined in the Nasdaq Stock Market and SEC rules. Mr. Adik and Mr. Kletter are each qualified as an Audit Committee Financial Expert, as defined by the SEC. The Audit Committee is appointed by and reports to our Board of Directors. Its responsibilities include, but are not limited to, the appointment, compensation and dismissal of our independent auditors, review of the scope and results of our independent auditors' audit activities, evaluation of the independence of our independent auditors and review of our accounting controls and policies, financial reporting practices and internal audit control procedures and related reports. During the last fiscal year, the Audit Committee held 7 meetings. The Audit Committee's charter can be found on our website atwww.beaconpower.com.

Compensation Committee. Our Compensation Committee has the authority to set the compensation of our Chief Executive Officer and all other executive officers and has the responsibility to review the design, administration and effectiveness of all programs and policies concerning executive compensation and establishing and reviewing general policies relating to compensation and benefits of employees. The Compensation Committee administers our Third Amended and Restated 1998 Stock Incentive Plan and Employee Stock Purchase Plan. Messrs. Adik, Smith and Rose are non-employee directors who have no interlocking relationships as defined by the SEC, and are all independent pursuant to the rules of the Nasdaq Stock Exchange applicable to members of this committee. The Compensation Committee held 7 meetings during the last fiscal year. The Compensation Committee's charter can be found on our website atwww.beaconpower.com.

Nominating and Governance Committee. The Nominating and Governance Committee recommends to the Board corporate governance guidelines applicable to the Board and to the Company and oversees the effectiveness of our corporate governance in accordance with those guidelines. The committee also identifies individuals qualified to become Board members, reviews the qualifications of nominee directors and recommends to the Board the director nominees for annual meetings of stockholders and candidates to fill vacancies on the Board. Additionally, the committee recommends to the Board the directors to be appointed to Board committees. A stockholder may nominate a person for election as a director by complying with Section 2.2 of our By-Laws, which provides that advance notice of a nomination must be delivered to us and must contain the name and certain information concerning the nominee and the stockholders who support the nominee's election. A copy of this By-Law provision may be obtained by writing to Beacon Power Corporation, Attn: James M. Spiezio, Secretary, 65 Middlesex Road, Tyngsboro, Massachusetts 01879. Director nominees submitted by our stockholders will be considered on the same terms as other nominees. All members of our Nominating and Governance Committee qualify as "independent" pursuant to the rules of the Nasdaq Stock Market. The Nominating and Governance Committee held 6 meetings during the last fiscal year. The charter for our Nominating and Governance Committee can be found on our web site atwww.beaconpower.com.

12

Finance Committee. The Finance Committee is appointed by the Board of Directors (the "Board") to assist the Board in monitoring material financial matters involving: (1) debt undertaken by the Company; (2) equity raised by the Company; (3) terms and conditions related to debt or equity for the Company; (4) payoff of debt by the Company; (5) share splits or retirement of shares by the Company; (6) cash dividends or share dividends issued by the Company; (7) terms and conditions offered by outside resources for debt or equity related transactions; (8) acquisitions and divestures; (9) significant changes in Company ownership; (10) project finance for the Company and/or for affiliates that it may sponsor; and (11) such other matters as are similar or related thereto, or which the Board considers to be necessary or advisable. While the Committee has the responsibilities and powers set forth in its Charter, it is not the duty of the Committee to plan or conduct financial transactions nor does the Committee have any oversight responsibility with respect to the Company's financial reporting. The Finance Committee held 6 meetings during the last fiscal year. The Finance Committee's Charter can be found on our website atwww.beaconpower.com.

There are no family relationships among any of our directors or executive officers. Messrs. Adik, Smith, Kletter, Weihman and Rose, representing a majority of our directors, are independent under the rules of the Nasdaq Stock Market. Our board holds regularly scheduled meetings at which only these independent directors are present.

Limitation of Liability and Indemnification

Our Certificate of Incorporation limits the liability of our directors, officers and various other parties whom we have requested to serve as directors, officers, trustees or in similar capacities with other entities to us or our stockholders for any liability arising from an action to which such persons are a party by reason of the fact that they were serving Beacon or at our request to the fullest extent permitted by the Delaware General Corporation Law.

We have entered into indemnification agreements with our directors and Executive Officers. Subject to certain limited exceptions, under these agreements, we will be obligated, to the fullest extent not prohibited by the Delaware General Corporation Law, to indemnify such directors and officers against all expenses, judgments, fines and penalties incurred in connection with the defense or settlement of any actions brought against them by reason of the fact that they were Beacon directors or Executive Officers. We also maintain liability insurance for our directors and Executive Officers in order to limit our exposure to liability for indemnification of our directors and Executive Officers.

Communication with Our Board of Directors

Our Board of Directors provides a process for our stockholders and other interested parties to send communications directly to our non-employee directors. Any person who desires to contact the non-employee directors may do so by writing to: Board of Directors, c/o Beacon Power Corporation, 65 Middlesex Road, Tyngsboro, Massachusetts 01879.

Communications received will be forwarded directly to the Chair of the Nominating and Governance Committee. The Chair of the Nominating and Governance Committee will, in his discretion, forward such communications to other directors, members of our management or such other persons as he deems appropriate. The Chair of the Nominating and Governance Committee, or, if appropriate, our management, will respond in a timely manner to any substantive communications from a stockholder or interested party.

Our Audit Committee also provides a process to send communications directly to the committee about our accounting, internal accounting controls or auditing matters. Any person who desires to contact the Audit Committee regarding such matters may do so by writing to Audit Committee of the

13

Board of Directors, c/o Beacon Power Corporation, 65 Middlesex Road, Tyngsboro, Massachusetts 01879.

Communications received by mail will be forwarded directly to the Chair of the Audit Committee. The Chair of the Audit Committee, in his discretion, will forward such communications to other directors, members of our management or such other persons as he deems appropriate. The Chair of the Audit Committee, or, if appropriate, our management, will respond in a timely manner to any substantive communications from a stockholder or an interested party.

The Audit Committee of our Board of Directors is composed of three members and acts under a written charter first adopted and approved by our Board of Directors on October 18, 2000. All members of the Audit Committee are independent directors, as defined by its charter and the rules of the Securities and Exchange Commission and Nasdaq Stock Market.

In connection with the preparation and filing of our Annual Report on Form 10-K for the year ended December 31, 2008, the Audit Committee (i) reviewed and discussed the audited financial statements with management, (ii) discussed with Miller Wachman LLP, our independent auditors for the fiscal year ending December 31, 2008, the matters required to be discussed by Statement of Auditing Standards 61 (as modified or supplemented) and (iii) received the written disclosures and the letter from Miller Wachman LLP required by applicable requirements of the Public Company Accounting Oversight board regarding Miller Wachman LLP's communications with the audit committee concerning independence, and has discussed the independence of Miller Wachman LLP with such firm. Based on the review and discussions referred to above, among other things, the Audit Committee recommended to our Board of Directors that the audited financial statements be included in our Annual Report on Form 10-K for the year ended December 31, 2008.

| Submitted by the Audit Committee: | ||

Stephen P. Adik,Chair Daniel E. Kletter Edward A. Weihman |

14

DIRECTOR AND EXECUTIVE OFFICER COMPENSATION

Compensation Discussion and Analysis

Executive Summary

Our executive compensation and benefit program has been designed to encourage our named Executive Officers (CEO, CFO and CTO) to pursue our strategic objectives while effectively managing the risks and challenges inherent in a development stage company transitioning into a commercial company. We created a compensation package that combines short and long-term components through a mix of base salary, bonus and equity compensation, in the proportions we believe are most appropriate to incentivize and reward our Executive Officers for achieving our strategic objectives. Moreover, the program is designed to be competitive with comparable employers and to align management's incentives with the long-term interests of our stockholders. Our compensation-setting process consists of establishing targeted overall compensation for each Executive Officer and then allocating that compensation among fixed and variable elements. At the executive level, we design the incentive compensation to reward company-wide performance, shareholder value creation, and the achievement of specific financial, operational and strategic objectives.

Our compensation program is a performance-oriented structure exemplified by the elements of compensation that are at risk for our Executive Officers. For example over 58% of our CEO's targeted total compensation in 2008 was variable and based on performance of the Company.

In 2008 our Executive Officers performance relative to strategic objectives resulted in a 78% payout of the targeted bonus amount. The objectives for 2008 had four primary components: fund raising, improving market rules and tariffs, deployment of flywheel systems and completion of the 25kWh system design. In determining the payout percentage the Committee assessed performance in the key areas as follows:

- •

- On fund raising, the amount of funds raised was below targeted amounts; however in consideration of the difficult equity market conditions, the fact that sufficient funds were raised to support operations was considered a positive performance.

- •

- On market rules and tariffs, 2008 was a very successful year with significant progress in modifying rules and tariffs in each of the ISOs to allow energy storage to compete with conventional generators.

- •

- On deployment of flywheel systems progress was made but deployment was less than desired.

- •

- On completion of the 25kWh systems design, overall the efforts were successful, however, completion was behind the targeted completion dates.

Role of Our Compensation Committee

Our Compensation Committee approves, administers and interprets our executive compensation policies. Our Compensation Committee is appointed by our Board of Directors, and consists entirely of directors who are "outside directors" for purposes of Section 162(m) of the Internal Revenue Code, "non-employee directors" for purposes of Rule 16b-3 under the Exchange Act and "independent directors" for purposes of the rules of the Nasdaq Stock Market. Our Compensation Committee has three members: Mr. Stephen P. Adik, and Mr. Virgil G. Rose and is chaired by Mr. Jack P. Smith.

Our Compensation Committee reviews and makes recommendations to our Board of Directors to ensure that our compensation program is consistent with our compensation philosophy and corporate governance guidelines and, subject to the approval of our Board (without the participation of the CEO), establishes the compensation paid or granted to our Executive Officers, which include our CEO,

15

CFO and CTO. The Compensation Committee also establishes an overall pool of compensation for Senior Management and other employees.

Messrs. Adik, Smith and Rose are non-employee directors who have no interlocking relationships as defined by the SEC, and are all independent pursuant to the rules of the Nasdaq Stock Market applicable to members of this committee.

Role of Compensation Consultant

The Compensation Committee generally engages an independent compensation consultant to provide a market perspective on executive compensation matters. Watson Wyatt has served as the Compensation Committee's consultant since 2005. During that time, the Compensation Committee has utilized Watson Wyatt for various activities, including but not limited to peer group development, competitive market analysis, incentive plan design and assistance in pay determination. The Compensation Committee expects to continue to engage an outside advisor in the development of programs and pay setting activities.

Role of our Executive Officers

The role of the CEO and CFO is to allocate the compensation pool approved by the Compensation Committee among all our other employees and to provide recommendations to the Compensation Committee in regard to any equity compensation to be granted to other employees.

During the transition from development stage to commercial, we have aligned the compensation structure of all other employees to the same company-wide strategic objectives and performance as the Executive Officers' compensation. As we transition to commercialization, we expect to design the incentive compensation for the employees to reward the achievement of specific operational goals within areas under the control of the relevant employees as well as company-wide performance.

Evolution of our Compensation Strategy

Our compensation strategy is necessarily tied to our stage of development. Accordingly, the specific direction, emphasis and components of our executive compensation program will continue to evolve in parallel with the evolution of our business strategy. For example, as we transition from development stage to commercial operations with more predictable financial resources, our compensation programs may also evolve, reflecting the changing needs of the business and available resources. Similarly, our goals may be modified to incorporate changing requirements expected of us as a result of regulatory, operational, competitive or other factors. Our Compensation Discussion and Analysis will, in the future, describe these evolutionary changes, if any.

Program Participants

Our Executive Officers are:

- •

- F. William Capp, Chief Executive Officer (CEO)

- •

- James M. Spiezio, Chief Financial Officer (CFO)

- •

- Matthew L. Lazarewicz, Chief Technical Officer (CTO)

16

Development of a Formal Compensation Program

Our Compensation Committee has taken the following steps to ensure that our compensation and benefit programs for Executive Officers are consistent with our compensation philosophy and our corporate governance guidelines:

- •

- Beginning in 2005, engaged and directed Watson Wyatt, as our independent executive compensation and benefits consultant, to assess the competitiveness of our compensation program, and provide a high-level review of our long-term incentive plan

- •

- With the assistance of ongoing input from Watson Wyatt, we have developed appropriate compensation packages by targeting a competitive level of pay as measured against our peer group described below

- •

- We have maintained a practice of reviewing the performance and determining the total compensation earned, paid or awarded to our Chief Executive Officer independent of input from him

- •

- We have developed compensation guidelines for our Chief Financial Officer and Chief Technical Officer with assistance from our Chief Executive Officer, and determined what we believe to be appropriate total compensation based on competitive levels as measured against our peer group

- •

- We have maintained the practice of holding executive sessions, without executive officers present, at every Compensation Committee meeting; and

- •

- For the remainder of the team the Compensation Committee and Executive Officers review the compensation program to insure consistency with our compensation philosophy and governance guidelines.

Based on these efforts and examinations, the Compensation Committee developed a compensation program intended to be in place for the next several years and continues to monitor this program to insure its effectiveness.

Market Referencing

To test the competitiveness of our compensation program, Watson Wyatt was engaged to compare our compensation practices and levels to a group of specific peer companies, representative of companies of similar size and industry. As our company continues to grow, Watson Wyatt analyzes and updates the compensation benchmarking peer group where appropriate. The recommended changes, if any, in the peer group is then presented to the Compensation Committee for approval. In late 2007, Watson Wyatt helped us to select a comparison group for 2008 compensation decisions. In selecting the peer comparison group, the following criteria were used:

- •

- Publicly-traded companies subject to disclosure requirements governed by the SEC

- •

- Companies that operate in the capital goods sectors or select companies in the Jeffries Clean Technology index

- •

- Companies that are similar in size to the company:

- •

- Market capitalization—generally within a range of .5X - 2.5X of our own

- •

- Revenue—within a range of $0 to $50 million

- •

- Companies that are generally in a similar business stage

17

Using the above screening criteria, the 2008 peer comparison group was determined to have the following 11 companies:

- •

- Active Power Inc.

- •

- Akeena Solar Inc.

- •

- Ascent Solar Technologies

- •

- Capstone Turbine Corporation

- •

- Daystar Technologies Inc.

- •

- Evergreen Energy Inc.

- •

- Hoku Scientific Inc.

- •

- Ocean Power Technologies Inc.

- •

- Satcon Technology Corporation

- •

- Spire Corporation

- •

- UQM Technologies, Inc.

A majority of the above companies operate in our assigned sub-sector, electrical equipment, and compete against each other for executive talent.

With the assistance of Watson Wyatt, we compared the following aspects of our compensation program to those of our peer group members:

| | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Study | | Overview | | Purpose | | ||||||

| Current Landscape | Summarizes current programs and trends in the marketplace | Provide an overview of the current compensation environment, competitive market practices and emerging trends | ||||||||||

| Total Direct Compensation | Competitive assessment of all compensation including base salaries, annual incentives and the fair value of long-term incentives | Determines whether compensation opportunities were competitive with market levels and are delivering an appropriate mix of pay, both fixed and variable | ||||||||||

| Usage, Dilution & Plan Expense | Usage: Number of shares and options being granted as a percentage of shares outstanding Dilution: Number of shares currently outstanding and available for grant in the current equity program | Considered the relative competitiveness, from a share number perspective, that the equity program has offered historically and the resulting potential shareholder dilution | ||||||||||

In 2006, the committee made the decision to shift a portion of short-term incentive opportunity to long-term incentives to appropriately balance near term operational goals with longer term shareholder value creation. Specifically, we reduced each Executive Officer's short-term incentive targets and introduced a portfolio approach to delivering long-term incentives, comprised of stock options,

18

restricted stock units (RSUs) and performance stock units (PSUs). The structure developed as a result of those analyses and subsequent discussions serves as the foundation for our executive compensation program going forward. Based on our most recent analysis in 2007, we believe it was appropriate to maintain this compensation structure for 2008.

We intend to continue our strategy of providing competitive compensation opportunity to our Executive Officers, through programs that emphasize performance-based incentive compensation in the form of cash and equity. To that end, total executive compensation is structured to ensure that, due to the nature of our business, there is an equal focus on our financial performance and stockholder return. For 2008, we targeted total compensation opportunity levels to our Executive Officers generally between the 50th and 60th percentiles of our peer group. We believe that the positioning of our Executive Officer compensation was consistent with our financial performance, the individual performance of each of our executives and the interests of our stockholders. We also believe that the total compensation was reasonable in the aggregate. Further, in light of our compensation philosophy, we believe that the total compensation package for our Executive Officers should continue to consist of base salary, annual cash incentive awards (bonuses), long-term equity-based incentive compensation, and certain other benefits.

The competitive posture of our total annual direct compensation will vary from year to year based on our results and individual performance versus the performance of the peer group companies and their respective level of annual performance bonus awards made to their executives.

Components of Compensation Program

Our performance-driven compensation program has both short-term and long-term components. Our Executive Officers' compensation is defined in the Executive Agreements (which are further detailed in the section titled "Executive Officer Employment Agreements" below.) All of our other employees are employees at will. However, all of our employees participate in the compensation programs as noted below.

Current Compensation Components

We utilize current compensation components that include base salary and cash bonuses to motivate and reward our employees, including our Executive Officers, in accordance with our defined objectives. Our Compensation Committee has established this program to set and refine management objectives and to measure performance against those objectives. The Compensation Committee reviews its conclusions on short term compensation with the Board (without the participation of the CEO), and once a consensus is reached, the short term compensation decisions are presented to the Executive Officers.

Base Salary

Base salary will typically be used to reward the experience, skills, knowledge and responsibilities required of each of our Executive Officers, as well as competitive market conditions. In establishing the 2008 base salaries for other employees, our Compensation Committee considered the proposals made by the Executive Officers and the recommendations made by Watson Wyatt, who were retained to do an update of their findings for executive officers from the prior year. The factors considered in determining salary and annual increases to salary, which are adjusted effective January 1 of each year, were:

- •

- Seniority

- •

- Functional role

- •

- Level of responsibility

19

- •

- Performance and accomplishments

- •

- Comparisons against market benchmarks described earlier in this discussion

- •

- Trends in compensation for the geographic region

- •

- Professional effectiveness including leadership, commitment, creativity and team building

- •

- Knowledge, skills, attitude and focus

- •

- Competitive market for corresponding positions within comparable geographic areas and industries

Using the same criteria outlined above, our Compensation Committee works directly with its independent compensation consultant to determine the compensation recommendations that our Compensation Committee makes to our Board of Directors regarding specific compensation actions for the Executive Officers. Executive Officers' base salaries changes in 2008 were as follows:

| | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Executive Officer | | 2007 Base Salary | | 2008 Base Salary | | % Increase | | |||||||||||

| F. William Capp | $ | 257,500 | $ | 296,125 | 15.0 | % | ||||||||||||

| James M. Spiezio | 202,705 | 210,813 | 4.0 | % | ||||||||||||||

| Matthew L. Lazarewicz | 182,000 | 189,280 | 4.0 | % | ||||||||||||||

The Compensation Committee evaluates each Executive Officer's base salary in terms of his individual performance and his relative percentile performance to the peer group. The 2008 base salary increases for the CFO and CTO reflect comparable performance to expectations and base salaries being in line with the committee's guidelines relative to the peer group. In the case of the CEO, the base salary increase was higher than the other Executive Officers to bring base salary in line with the committee's guidelines relative to the peer group (as 2007 base salary was below the peer 25th percentile).

Annual Incentives

Performance Bonus

Overview of Performance Bonus Program

Awards under the program are based on a quantitative and qualitative review of all of the facts and circumstances related to the Company and each executive's or employee's performance. An Executive Officer may receive awards from zero to 100% of his target bonus based on the review of results. Additional awards of up to 50% of the potential bonus may be awarded for performance at levels above targeted goals and objectives or improvement in the timing of achieving certain results. The criteria for these potential additions to the bonus are clearly defined as part of establishing the potential bonus structure each year.

On an individual level, the Compensation Committee attempts to set clearly defined goals for each Executive Officer, focusing on the categories mentioned below, with an emphasis on quantifiable and achievable goals. Once the defined goals have been identified, the Compensation Committee engages in a collaborative process with the Executive Officers to reach agreement on the following aspects of the short term goals:

- •

- Agreement that the goals formulated are viewed by the Executive Officers as the correct drivers for the business from their perspectives

- •

- Consistency of these goals with our short and long term strategies

- •

- Timing, measurability and relative values that should be ascribed to each goal; and

20

- •

- Agreement that the goals are difficult yet realistically attainable.

The Compensation Committee sees this process both as the optimal means of assembling accurate information regarding the expectation and realization of performance, as well as an integral part of our culture of collaborative, team-oriented management.

Discretionary Bonus

Additional discretionary awards of up to approximately 35% of the potential bonus may be awarded for performance to targets that emerge subsequent to the establishment of the year's bonus program or other achievements not previously identified, or performance to existing targets that is greater or more timely than the target.

The Compensation Committee evaluates each Executive Officer as well as our other key employees once each year based on the achievement of set goals. This review is typically done during the first quarter of the year. We review final results for the year versus pre-determined objectives and begin discussions regarding performance objectives for the current fiscal year. Performance bonuses, at the discretion of the Compensation Committee, may be awarded in the form of cash or RSUs and equity-based awards.

Total compensation for our Executive Officer may vary significantly from year to year, based on the percentage of achievement of goals. In addition, the value of equity awards in either RSUs or stock options may vary significantly in value based on the performance of our stock's price.

2008 Performance Bonus and Resulting Bonus Payout

Our business strategy is to become a leader in providing frequency regulation services to the electrical grid. We intend to build our service business through our internal research efforts, our use of proprietary technologies, expansion of manufacturing capabilities and our deployment of facilities dedicated to providing economically-viable frequency regulation services to the electrical grid. In order to accomplish these goals, we will need to expand manufacturing capabilities, acquire appropriate locations for installation of our flywheel systems and raise additional financing. We must also focus on continually strengthening our management and technical teams, in order to provide the human resources necessary to carry out our business objectives.

21

In 2008, we made progress in executing our strategic plan. For 2008, the target performance goals and results were as follows:

| | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Description of Goal | | Potential Value (% of Bonus Award)* | | Value Awarded Based on Achievement (% of Bonus Award) | | Comment on Results | | ||||||||||

| 25kWh Flywheel Development: metrics relate to progress on cost reduction, and having production tooling and equipment in place to meet production goals. | 20 | 10 | Goals related to cost reduction partially achieved. Goals related to having production tooling and equipment in place met. | |||||||||||||||

| Deployment of units and payment for services: metrics relate to having a specified number of units operational and producing revenue by specified dates, as well as making progress having additional sites ready to install additional MW of service. | 30 | 23 | Goals partially achieved. Manufacturing of initial units completed, but later than initially planned. 1 MW system is operational and began earning revenue under the ISO-NE Pilot Program during Q4 2008. Goals met related to progress at additional sites (beyond Tyngsboro). | |||||||||||||||

| Funding: metrics relate to completion of the DOE loan application, DOE loan guarantee award, and obtaining new equity or debt financing other than the DOE loan. | 25 | 15 | Goals partially met. | |||||||||||||||

| Market Access: metrics relate to efforts to obtain favorable market rules in the various ISOs, establishment of the New England Pilot Program, development of marketing materials, and exploring markets outside of the United States. | 15 | 20 | The Board awarded additional points in this category because we exceeded our goals. | |||||||||||||||

| Government Contracts/Other: metrics relate to maintaining investor awareness, resolution of outstanding litigation, safety, and progress on the completion of existing contracts. | 5 | 5 | Goals achieved. | |||||||||||||||

| New Revenue: metrics relate to achievement of new contracts from State or Federal agencies and closing on the Mass Development loan. | 5 | 5 | We have been notified of two new awards for which documents were pending at year end. Goals relating to the Mass Development loan achieved. | |||||||||||||||

| Target Bonus: Note that additional points could be earned in most categories for exceeding certain goals. | 100 | 78 | ||||||||||||||||

| Stretch Goals: Additional bonus amounts could be awarded for exceeding certain targets relating to fundraising and other revenue-related contracts. | 35 | 0 | Not met. Contract offered, but judged not attractive. | |||||||||||||||

| Maximum Bonus: | 135 | 78 | ||||||||||||||||

22

Based on these goals and the resulting attainment, each Executive Officer was judged to have achieved 78% of his goals. Accordingly, for our Executive Officers, the Target and actual bonuses paid in February 2009 for our 2008 Performance Plan were as follows:

| | |||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Name | | 2008 Base Salary | | Bonus Potential as a % Salary | | 2008 Target Bonus Potential | | Bonus Percent Awarded (as a % of Target) | | Bonus Amount Earned | | |||||||||||||||||

| F. William Capp | $ | 296,125 | 50.0 | % | $ | 148,063 | 78.0 | % | $ | 115,489 | |||||||||||||||||||

| James M. Spiezio | 210,813 | 35.0 | % | 73,785 | 78.0 | % | 57,552 | ||||||||||||||||||||||

| Matthew L. Lazarewicz | 189,280 | 35.0 | % | 66,248 | 78.0 | % | 51,673 | ||||||||||||||||||||||

The bonus potential as a percent of salary was defined in the Executive Officers' Employment Agreements with the Company. These agreements are further described below.

The Compensation Committee is working with the Executives to set targets for 2009.

Long-term Compensation

At present, our long-term compensation for Executive Officers consists of a combination of common stock options and RSUs, all with a three year vesting period, and performance stock units (PSUs) tied to achieving specific longer term objectives. We believe this strategy of utilizing a combination of options, RSUs and PSUs is appropriate for aligning the interests of our Executive Officers with those of our stockholders over the long-term, focuses on attaining key operational milestones, and provides an effective retention feature. All Options, RSUs and PSUs are granted under our Third Amended and Restated 1998 Stock Incentive Plan. Details as to the valuation of these grants are included in our Notes to Consolidated Financial Statements included in our Annual Report on Form 10-K filed with the SEC on March 16, 2009, and are incorporated here by reference. Equity grant practices, including recent changes, are detailed in a subsequent section of this discussion. Our practice is to grant stock options and RSUs on an annual basis at the time of annual performance review. The typical target expected value of the annual long term incentive grant is 100% of base salary for the CEO and 55% of base salary for the CFO and CTO. PSUs were granted in 2006 as a special grant to motivate the executives to achieve specific long-term financial objectives.

Common Stock Option Grants

Our common stock option grants are designed to align our executives' performance objectives with the interests of our stockholders. We believe that these options provide an important component of executive compensation which is fully aligned with our shareholder's interests whereby the impact of any business setbacks, whether Company-specific or industry based, achievement of objectives or other performance matters impacts the Executive Officers as well as shareholders directly. Our Compensation Committee also grants options to key employees based on this same rationale which enables these key employees to participate in the long term appreciation of our stockholder value. In addition, all new permanent, full-time employees are granted options when they join the Company. We further believe that our option grants provide a means to assist in the retention of key employees, inasmuch as they are in almost all cases subject to vesting over an extended period of time.

We analyze the following external market comparisons when we set the number of options or RSUs to be granted to each executive. On an individual basis, we compare:

- •

- The fair value of the grants using a Black-Scholes valuation for equity awards that is consistent with SFAS 123(R)

- •

- The number of common stock options and RSUs granted by position; and

23

- •

- The competitive level of our equity-based compensation practices versus the market, including levels, share usage levels, dilution and overall equity plan expense.

In 2008, options vesting over three years granted to our Executive Officers pursuant to the Executive Agreements were as follows: Mr. Capp, 291,279 options; Mr. Spiezio, 114,098 options; and Mr. Lazarewicz, 102,426 options. These options had exercise prices based on the stock closing price on the date of grant, which was $1.25.

We have used the Black-Scholes valuation model in determining the number of options or RSUs to be granted our executives as well as the remainder of the Company's employees. In light of the volatile stock market, the Compensation Committee is evaluating whether the Black Scholes model is the best method to use to calculate grant size going forward. Accordingly, the committee has engaged its compensation consultant, Watson Wyatt, to review and possibly restructure our incentive stock compensation arrangements for our Executive Officers.

Restricted Stock Unit Grants

RSUs were granted to our Executive Officers pursuant to the Executive Agreements. Our issuance of RSUs is a further effort to align management's performance objectives with the interest of shareholders by having the same attributes as our vesting stock options with the additional alignment of each Executive Officer owning actual shares. These RSUs vest quarterly over a three year period, and are generally converted to common stock on the vesting dates. The numbers of RSUs issued to each of the Executive Officers based upon the 2008 Executive Agreements were as follows: Mr. Capp, 32,350 units, Mr. Spiezio, 12,678 units; and Mr. Lazarewicz, 11,366 units. The compensation value of these RSUs was calculated using the stock closing price on the date of grant, which was $1.25.

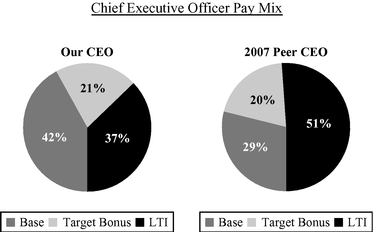

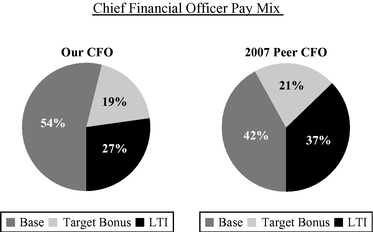

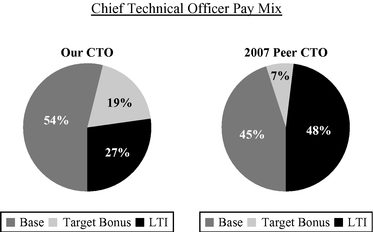

The charts below show long term incentive (LTI) grants as a percentage of base salary for 2008:

| | |||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Name | | 2008 Base Salary | | Fair Value of Options Granted | | Value of RSUs Granted | | Total LTI | | LTI as % Base Salary | | |||||||||||||||||

| F. William Capp | $ | 296,125 | $ | 224,285 | $ | 40,438 | $ | 264,723 | 89 | % | |||||||||||||||||||

| James M. Spiezio | 210,813 | 87,855 | 15,848 | 103,703 | 49 | % | |||||||||||||||||||||||

| Matthew L. Lazarewicz | 189,280 | 78,868 | 14,208 | 93,076 | 49 | % | |||||||||||||||||||||||

Performance Stock Unit Grants

Our Performance Stock Units (PSUs) are also designed to align management's performance objectives to shareholder interest by providing stock grants that cliff-vest upon achievement of specific longer term objectives of interest to our investors.

The Executive Officers were granted PSUs as part of the Executive Agreements in 2006 to incentivize the Executive team to maintain a sustained drive and focus on moving the development-stage company successfully into production. The PSUs were structured to provide Mr. Capp with potential awards valued at $1,000,000 and Mr. Spiezio and Mr. Lazarewicz with awards valued at $500,000 each, where the unit price used to calculate the number of units was based on the average of the high and the low stock price on the date of grant, $1.58. This equates to a potential award of 632,911 shares to Mr. Capp and 316,456 shares each to Mr. Spiezio and Mr. Lazarewicz. There were no additional PSUs granted in 2007 or 2008.

The 2006 PSUs cliff vest only upon achievement of certain conditions:

- a.

- Achievement of the following Adjusted EBITDA goals for either of the fiscal years ending in 2009 or 2010. (Adjusted EBITDA is defined as net earnings before Interest, Taxes,

24

Depreciation, Amortization and Stock Compensation Expense.) We believed that a multiplier of EBITDA has a direct correlation with common stock valuations and that achieving the EBITDA goals would maximize shareholder value in the 2009 - 2010 timeframe.

The scale for potential awards was set as follows:

| | ||||||||

|---|---|---|---|---|---|---|---|---|

| | Size of Adjusted EBITDA: | | Number of RSUs in the Actual Award | | ||||

| Under $2,000,000 | No Award | |||||||

| $2,000,000 | 50% of the Potential Award | |||||||

| $2,000,000 to $4,000,000 | (Potential Award X Adjusted EBITDA)/4,000,000 | |||||||

| Over $4,000,000 | 100% of the Potential Award | |||||||

- b.