UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

[ ] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) or 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year endedDecember 31, 2012

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[ ] SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number000-30087

ADIRA ENERGY LTD.

(Exact name of Registrant specified in its charter)

CANADA

(Jurisdiction of incorporation or organization)

120 Adelaide Street West, Suite 1204

Toronto, Ontario

Canada M5H 1T1

(Address of principal executive offices)

Contact Person: Gadi Levin

Address: 120 Adelaide Street West, Suite 1204

Toronto, Ontario M5H 1T1

Email: glevin@adiraenergy.com

Telephone: (416) 250-1955, Facsimile: (416) 250-6330

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of each exchange on which registered |

| None | Not applicable |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

COMMON SHARES

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:None

i

Number of outstanding shares of the Company’s only class of capital or common stock as at December 31, 2012 was

180,781,093 common shares.

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

If this is an annual report or a transition report, indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes [ ] No [X]

Indicate by check mark whether Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [ ] No [ ]

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (check one):

Large accelerated filer [ ] Accelerated filer [ ] Non-accelerated filer [X]

Indicate by check mark which basis of accounting the Registrant has used to prepare the financial statements included in this filing:

| | International Financial Reporting Standards as issued | |

| U.S. | by the International Accounting Standards Board | |

| GAAP [ ] | [X] | Other [ ] |

If “other” has been checked in response to the previous question, indicate by check mark which financial statement item the Registrant has elected to follow:

Item 17 [ ] Item 18 [ ]

If this is an annual report, indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by checkmark whether the Registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

YES [ ] NO [ ]

ii

TABLE OF CONTENTS

iii

iv

GENERAL

This Form 20-F is being filed as an annual report under the Exchange Act.

In this Form 20-F, references to:

“Adira” means Adira Energy Ltd., a Canadian federal corporation (formerly AMG Oil Ltd.);

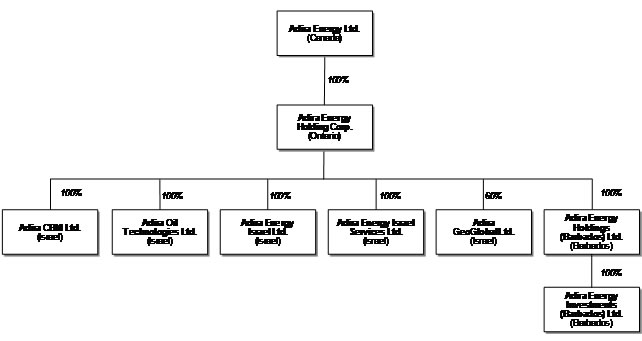

“Adira Group” means Adira Energy Ltd. (formerly AMG Oil Ltd.) together with: (a) its wholly-owned subsidiary, Adira Energy Holding Corp.; (b) its wholly-owned indirect (through Adira Energy) subsidiaries, Adira Energy Israel Ltd., Adira Energy Israel Services Ltd., Adira Oil Technologies Ltd., Adira Energy CBM Ltd., and Adira Energy Holdings (Barbados) Ltd., which wholly owns Adira Energy Investments (Barbados) Ltd.; and (c) Adira’s 60% indirect (through Adira Energy) subsidiary, Adira Geo Global Ltd.;

“Adira Energy” means Adira Energy Holding Corp., an Ontario corporation (formerly Adira Energy Corp.);

“Adira Israel” means Adira Energy Israel Ltd., an Israeli corporation;

“Adira Services” means Adira Energy Israel Services Ltd., an Israeli corporation;

“We”, “us”, “our”, and the “Company” mean Adira Group; and

“AMG” refers to AMG Oil Ltd. which was the name of the Company prior to its change of name to Adira Energy Ltd. on December 17, 2009.

Adira and Adira Energy have historically used U.S. dollar as their reporting currency. All references in this document to “dollars” or “$” are to United States dollars and all references to “CDN$” are to Canadian dollars, unless otherwise indicated.

Except as noted, the information set forth in this Form 20-F is as of December 31, 2012 and all information included in this document should only be considered correct as of such date.

- 1 -

NOTE REGARDING FORWARD LOOKING STATEMENTS

Much of the information included in this Form 20-F includes or is based upon estimates, projections or other “forward looking statements”. Such forward looking statements include any projections or estimates made by us and our management in connection with our business operations. These statements relate to future events or our future financial performance. Generally, any statements contained herein that are not statements of historical facts may be forward–looking statements. In some cases you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue or the negative of those terms or other comparable terminology. While these forward-looking statements, and any assumptions upon which they are based, are made in good faith and reflect our current judgment regarding the direction of our business, actual results will almost always vary, sometimes materially, from any estimates, predictions, projections, assumptions or other future performance suggested herein. Such estimates, projections or other forward looking statements involve various risks and uncertainties and other factors, including the risks in the section titled “Risk Factors” below, that may cause our actual results, levels of activities, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. We caution the reader that important factors in some cases have affected and, in the future, could materially affect actual results and cause actual results to differ materially from the results expressed in any such estimates, projections or other forward looking statements. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform those statements to actual results.

In particular, without limiting the generality of the foregoing disclosure, the statements contained in Item 4.B. – “Business Overview”, Item 5 – “Operating and Financial Review and Prospects” and Item 11 – “Quantitative and Qualitative Disclosures About Market Risk” are inherently subject to a variety of risks and uncertainties that could cause actual results, performance or achievements to differ significantly.

PART I

ITEM 1 - IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2 - OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3 - KEY INFORMATION

A. Selected Financial Data

Adira Energy

On August 31, 2009, Adira acquired Adira Energy by issuing 39,040,001 common shares of Adira to Adira Energy’s shareholders on a one-for-one basis. As the shareholders of Adira Energy obtained control of Adira, the share exchange is considered to be a reverse takeover transaction. Accordingly, for accounting purposes, Adira Energy is the acquirer.

Adira Energy’s predecessor is Adira Israel, which was incorporated in Israel on October 26, 2008. In order to facilitate tax planning, all of the issued and outstanding shares of Adira Israel were registered in the name of Adira Africa Corp. (“Adira Africa”), a privately-owned Canadian corporation, as a trustee for and on behalf of a corporation to be incorporated in Ontario – namely, Adira Energy, which was subsequently incorporated on April 8, 2009 – pursuant to a Declaration of Trust dated November 16, 2008 (the “Declaration of Trust”). In December 2008, upon application to Ministry of Energy and Water Resources (formerly the Ministry of National Infrastructures) of the State of Israel (the “Ministry” or “MNI”), Adira Israel obtained Eitan License No. 356, covering 31,060 acres (125.7 square kilometers) in the Hula Valley in Northern Israel (the “Eitan License”), for no consideration other than the payment of a nominal stamp duty in the amount of $3,544. Upon the incorporation of Adira Energy on April 8, 2009, Adira Africa transferred the shares of Adira Israel to Adira Energy for no consideration, as contemplated by the Declaration of Trust.

- 2 -

The only activity undertaken in Adira Israel from December 2008 to April 8, 2009 was the application for, and the receipt of, the Eitan License, and, pursuant to the Declaration of Trust, Adira Energy is in substance treated as the owner of the Adira Israel shares since the inception of Adira Israel. Further, the carrying amount of the single asset owned by Adira Israel, the Eitan License (there were no material liabilities), was recorded in the accounts of Adira Israel as of April 8, 2009 in its nominal amount of the stamp duty. Therefore, under International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (the “IASB”), the carrying amount of the Adira Israel shares transferred to Adira Energy on that date was of the same nominal amount. Subsequent to April 7, 2009, all activities of the Company are reflected in the consolidated financial statements of Adira.

As disclosed elsewhere in this annual report, we have now plugged and abandoned the first well that we drilled on the Eitan License (the “Eitan #1 Well”), and we have surrendered the Eitan License in accordance with the Israeli Petroleum Law (as defined below). However, we continue to hold interests in certain other oil and gas licenses located offshore Israel.

The selected historical information presented in the table below for the years ended December 31, 2012 and 2011 are derived from the audited consolidated financial statements of Adira for such period, and have been prepared in accordance with IFRS as issued by the IASB. The selected historical financial information presented in the table below for the 267-day period ended December 31, 2009 comprises the operating data of Adira Energy and its subsidiary companies from April 8, 2009 (date of incorporation of Adira Energy) and that of Adira (formerly AMG Oil Ltd) from September 1, 2009, and have also been prepared in accordance with IFRS as issued by the IASB. The selected financial information presented below should be read in conjunction with the audited consolidated financial statements and the notes thereto of Adira Group, and with the information appearing under each of Item 4 – “Information on the Company” and Item 5 – “Operating and Financial Review and Prospects” of this Form 20-F. All financial data presented in this Form 20-F are qualified in their entirety by reference to the consolidated financial statements and their notes.

U.S. dollars in thousands, except share and per share data

| | Year Ended December 31, |

| | 2012 | 2011 | 2010 | 2009 |

| | ($ thousands) |

| Balance Sheet Data | | | | |

| Cash and cash equivalents | 2,394 | 8,094 | 8,686 | 2,044 |

| Total Assets | 15,340 | 10,247 | 18,610 | 2,437 |

| Total Liabilities | 10,330 | 1,421 | 7,373 | 227 |

| Total Shareholders’ Equity | 5,010 | 8,826 | 11,237 | 2,437 |

- 3 -

| | | Year ended December 31 | | | 267-day period | |

| | | | | | | | | | | | ended | |

| | | | | | | | | | | | December 31 | |

| | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

| | | $ | | | $ | | | $ | | | $ | |

| Operating Data | | | | | | | | | | | | |

| Revenues and other income | | 1,889 | | | 1,323 | | | 1,707 | | | - | |

| | | | | | | | | | | | | |

| Expenses: | | | | | | | | | | | | |

| Exploration expenses | | 1,026 | | | 5,018 | | | 1,624 | | | 195 | |

| General and administrative expenses | | 5,304 | | | 5,031 | | | 3,067 | | | 1,639 | |

| Impairment charge | | 7,810 | | | 1,226 | | | - | | | - | |

| | | | | | | | | | | | | |

| Total expenses | | 14,140 | | | 11,275 | | | 4,691 | | | 1,834 | |

| | | | | | | | | | | | | |

| Operating loss | | (12,251 | ) | | (9,952 | ) | | (2,984 | ) | | (1,834 | ) |

| | | | | | | | | | | | | |

| Financing income | | 2,480 | | | 43 | | | - | | | 15 | |

| Financing expense | | (745 | ) | | (109 | ) | | (5 | ) | | - | |

| Issuance expenses | | - | | | - | | | - | | | (4,902 | ) |

| | | | | | | | | | | | | |

| Loss before income taxes | | (10,516 | ) | | (10,018 | ) | | (2,989 | ) | | (6,721 | ) |

| | | | | | | | | | | | | |

| Income taxes | | (41 | ) | | (33 | ) | | (15 | ) | | (1 | ) |

| | | | | | | | | | | | | |

| Net loss and comprehensive loss | | (10,557 | ) | | (10,051 | ) | | (3,004 | ) | | (6,722 | ) |

| | | | | | | | | | | | | |

| Basic and diluted net loss per share attributable to equity holders of the parent | | (0.06 | ) | | (0.10 | ) | | (0.05 | ) | | (0.14 | ) |

| Weighted average number of Ordinary shares used in computing basic and diluted net loss per share | | 132,940,856 | | | 99,813,334 | | | 65,653,700 | | | 49,184,720 | |

We previously prepared our financial statements in accordance with Canadian generally accepted accounting principles (“Canadian GAAP”). The consolidated financial statements included in our transition report on Form 20-F for the period from October 1, 2010 to December 31, 2010, as filed with the SEC on February 27, 2012, were our Company’s first annual financial statements reported in accordance with IFRS. “IFRS 1, First-time Adoption of International Financial Reporting Standards,” was applied to such consolidated financial statements; the impact of the transition to reporting in accordance with IFRS on our Company's financial statements was detailed in Note 19 to those financial statements.

The selected balance sheet data presented in the table below for Adira Israel as of April 7, 2009, and the related changes in equity for the 164-day period from its incorporation (October 26, 2008) to April 7, 2009, are derived from the audited financial statements of Adira Israel for such period, which are included in Amendment No. 1 to our annual report on Form 20-F for the year ended September 30, 2010, as filed with the SEC on November 21, 2011. Adira Israel’s financial statements do not include a statement of operations and statement of cash flows for the 164-day period ended April 7, 2009, as there were no revenues, expenses or cash transactions during this period. The selected financial information presented below should be read in conjunction with the audited financial statements and the notes thereto of Adira Israel.

- 4 -

Under Israeli GAAP (U.S. dollars in thousands)

| | | As at April 7 | |

| | | 2009 | |

| | | $ | |

| Balance Sheet Data | | | |

| Exploration and evaluation asset | | 3,544 | |

| Total Assets | | 3,544 | |

| Total Liabilities | | 3,541 | |

| Total Shareholders’ Equity | | 3 | |

| Changes in Equity | | Share Capital | | | Total | |

| | | Number | | | Amount | | | Equity | |

| | | | | | | | | | |

| Balance at October 26, 2008 (date of incorporation) | | - | | $ | - | | $ | - | |

| | | | | | | | | | |

| Shares issued | | 1,000 | | | 3 | | | 3 | |

| | | | | | | | | | |

| Balance at April 7, 2009 | | 1,000 | | $ | 3 | | $ | 3 | |

As noted in Note 4 to the audited financial statements of Adira Israel, which are included in Amendment No. 1 to our annual report on Form 20-F for the year ended September 30, 2010, as filed with the SEC on November 21, 2011, there are no differences between Israeli GAAP and US GAAP in respect of the financial position and results of operations of Adira Israel for the period presented.

We have never declared or paid any cash or other dividends.

- 5 -

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

An investment in our securities is highly speculative and involves a high degree of risk. Our Company may face a variety of risks that may affect our operations or financial results and many of those risks are driven by factors that we cannot control or predict. Before investing in our company’s securities, investors should carefully consider the following risks. The risks and uncertainties described below are not the only risks and uncertainties that we face or that an investment in our securities entails. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business operations. Any of the following risks could materially and adversely affect our business, financial condition, prospects and results of operations. In that case, investors may lose all or a part of their investment. The risks discussed below also include forward-looking statements and the out actual results may differ substantially from those discussed in these forward-looking statements. See ‘‘Note Regarding Forward Looking Statements” and “Operating and Financial Review and Prospects”.

Risks Associated with the Company

Our independent auditors have referred to circumstances which might result in doubt about our ability to continue as a going concern, which may hinder our ability to obtain future financing.

Adira incurred a net loss of $10.6 million for the year ended December 31, 2012. At December 31, 2012, Adira had an accumulated deficit of $29 million. These circumstances raise doubt about our ability to continue as a going concern, as described in the Note 1 to our consolidated financial statements for the period ended December 31, 2012, which are included herein. Although our consolidated financial statements refer to circumstances which might raise doubt about our ability to continue as a going concern, they do not reflect any adjustments that might result if we are unable to continue our business.

We are an early-stage oil and gas exploration company without significant revenues. Our ability to continue in business depends upon our continued ability to obtain significant financing from external sources and the success of our exploration efforts and any production efforts resulting therefrom, none of which can be assured.

We are an early-stage oil and gas exploration company without any significant revenues, and there can be no assurance of our ability to develop and operate our projects profitably. We have historically depended entirely upon capital infusion from the issuance of equity securities to provide the cash needed to fund our operations, but we cannot assure you that we will be able to continue to do so. Our ability to continue in business depends upon our continued ability to obtain significant financing from external sources and the success of our exploration efforts and any production efforts resulting therefrom. Any reduction in our ability to raise equity capital in the future would force us to reallocate funds from other planned uses and could have a significant negative effect on our business plans and operations, including our ability to continue our current exploration activities and maintain ownership of our current licenses.

While we may in the future generate additional working capital through the development, operation, sale or possible syndication of our current property or any future properties, there is no assurance that our Company will be successful in generating positive cash flow, or if successful, that any such funds will be available for distribution to shareholders or to fund further exploration and development programs.

We have had negative cash flows from operations, and there is no assurance that our current liquidity or capital resources will be sufficient to fund our operations on an ongoing basis. Our business operations may fail if our actual cash requirements exceed our estimates and we are not able to obtain further financing.

- 6 -

We will require significant capital to complete our drill test wells, and to build the necessary infrastructure to commence operations if our exploration activities result in the discovery of sufficient oil and gas reserves to justify their exploitation and development.

Since inception, we have not earned any significant revenues from operations, and due to the length of time between the discovery of oil and gas reserves and their exploitation and development, we do not anticipate earning significant revenues from operation in the near future. We have incurred and will continue to incur significant expenses. As noted above, at December 31, 2012, we had cash and equivalents on hand of $2.4 million. We will have to seek additional financing to fund the advanced exploration on our assets, if warranted. Further, we cannot assure you that our actual cash requirements will not exceed our estimates, and in any case we will require additional financing to bring our interests into commercial operation, finance working capital, meet our contractual minimum expenditures and pay for operating expenses and capital requirements until we achieve a positive cash flow. Additional capital also may be required in the event we incur any significant unanticipated expenses.

In light of our operating history, and under the current capital and credit market conditions, we may not be able to obtain additional equity or debt financing on acceptable terms if and when needed. Even if financing is available, it may not be available on terms that are favorable to us or in sufficient amounts to satisfy our requirements.

If we require, but are unable to obtain, additional financing in the future, we may be unable to implement our business plan and our growth strategies, respond to changing business or economic conditions, withstand adverse operating results, and compete effectively. More importantly, if we are unable to raise further financing when required, our planned exploration activities may have to be scaled down or even ceased, and our ability to generate revenues in the future would be negatively affected.

As a holding company, our ability to make payments will eventually depend on the cash flows of our subsidiaries.

We are a holding company and conduct substantially all of our operations through our subsidiaries incorporated outside North America. We have no direct operations and no significant assets other than the shares of our subsidiaries and cash proceeds received from any financings, which cash is subsequently provided to our subsidiaries. Assuming our holding company structure remains, we will be dependent on the cash flows from our subsidiaries to meet our obligations, including payment of principal and interest on any debt we incur. The ability of certain of our subsidiaries to provide us with payments may be constrained by the following factors:

the cash flows generated by operations, investment activities and financing activities; and

the level of taxation, particularly corporate profits and withholding taxes.

In addition, we cannot guarantee that the current fiscal regime that allows for repatriation of funds in each of the countries where we do business will remain in effect, nor can we guarantee that arbitrary changes in exchange controls in each of the countries where we do business will not take place, which may adversely impact on the ability of investors to recover their investment.

If we are unable to receive sufficient cash from our subsidiaries, we may be required to refinance any indebtedness we incur, raise funds in a public or private equity or debt offering or sell some or all of our assets. We can provide no assurances that an offering of our debt or equity or a refinancing of our debt can or will be completed on satisfactory terms or that it would be sufficient to enable us to make payment with respect to our debt. The foregoing events could have an adverse impact on our future cash flows, earnings, results of operations and financial condition.

- 7 -

The majority of our assets are outside the United States, with the result that it may be difficult for investors to enforce within the United States any judgments obtained against us or some of our directors or officers.

The majority of our assets are located outside the United States. In addition, some of our directors and officers are nationals and/or residents of countries other than the United States, and all or a substantial portion of such persons’ assets are located outside the United States.

As a result, it may be difficult for investors to enforce within the United States any judgments obtained against us or our officers or directors, including judgments predicated upon the civil liability provisions of the securities laws of the United States or any state thereof. Consequently, investors may be effectively prevented from pursuing remedies under United States federal securities laws against them.

We may be adversely affected by current global financial conditions.

Current global financial conditions have been characterized by increased volatility and several financial institutions have either gone into bankruptcy or have had to be rescued by governmental authorities. Access to public financing and bank credit has been negatively impacted by both the rapid decline in value of sub-prime mortgages and the liquidity crisis affecting the asset-backed commercial paper market. These and other factors may affect our ability to obtain equity or debt financing in the future on favorable terms. Additionally, these factors, as well as other related factors, may cause decreases in our asset values that may be other than temporary, which may result in impairment losses. If such increased levels of volatility and market turmoil continue, or if more extensive disruptions of the global financial markets occur, our operations could be adversely impacted and the market value of our common shares may be adversely affected.

Currency fluctuations could have an adverse effect on our business.

Our earnings and cash flow may also be affected by fluctuations in the exchange rate between the U.S. dollar and other currencies, such as the New Israeli Shekel (“NIS”) and the Canadian dollar. Our consolidated financial statements are expressed in U.S. dollars. Our sales of oil and gas, if any, will be denominated in U.S. dollars, while exploration costs and operating costs are, in part, denominated in Israel Shekels, U.S. dollars and Canadian dollars

Fluctuations in exchange rates between the U.S. dollar and other currencies may give rise to foreign exchange currency exposures, both favorable and unfavorable, which have impacted and in the future may materially impact our future financial results. We do not utilize a hedging program to limit the adverse effects of foreign exchange rate fluctuations.

Conditions in Israel may affect our operations.

Our subsidiaries conduct their principal operations in Israel, and therefore are directly affected by the political, economic, and military conditions affecting Israel and the Middle East. Armed conflicts between Israel and its neighboring countries and territories occur periodically and a protracted state of hostility, varying in degree and intensity over time, has in the past led to security and economic difficulties for Israel. These hostilities, any escalation thereof or any future armed conflict or violence in the region, could adversely affect our subsidiaries’ operations. In addition, we could be adversely affected by other events or factors affecting Israel such as the interruption or curtailment of trade between Israel and its present trading partners, a significant downturn in the economic or financial condition of Israel, a significant downgrading of Israel’s international credit rating, labor disputes and strike actions and political instability.

- 8 -

Our financial reporting may be subject to weaknesses in internal controls.

Internal controls over financial reporting are procedures designed to provide reasonable assurance that transactions are properly authorized, assets are safeguarded against unauthorized or improper use, and transactions are properly recorded and reported. A control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance with respect to the reliability of financial reporting and financial statement preparation.

We cannot be certain that current expected expenditures and completion/testing programs will be realized.

We believe that the costs used to prepare internal budgets are reasonable, however, there are assumptions, uncertainties, and risk that may cause our allocated funds on a per well basis to change as a result of having to alter certain activities from those originally proposed or programmed to reduce and mitigate uncertainties and risks. These assumptions, uncertainties, and risks are inherent in the completion and testing of wells and can include but are not limited to: pipe failure, casing collapse, unusual or unexpected formation pressure, environmental hazards, and other operating or production risk intrinsic in oil and/or gas activities. Any of the above may cause a delay in the Company’s completion program and its ability to determine reserve potential.

Our lack of diversification increases the risk of an investment, and our financial condition and results of operations may deteriorate if we fail to diversify.

Our business focus is on oil and gas exploration on three properties in Israel within close proximity. As a result, we lack diversification, in terms of both the nature and geographic scope of our business. We will likely be impacted more acutely by factors affecting our industry or the regions in which we operate than we would if our business were more diversified. If we cannot diversify our operations, our financial condition and results of operations could deteriorate.

We may not effectively manage the growth necessary to execute our business plan.

Our business plan anticipates a significant increase in the number of our contractors, strategic partners and equipment suppliers. Such growth, if any, will place significant strain on our current personnel, systems and resources. We expect that we will be required to hire qualified consultants and employees to help manage our growth effectively. We believe that we will also be required to improve our management, technical, information and accounting systems, controls and procedures. We may not be able to maintain the quality of our operations, control our costs, continue complying with all applicable regulations and expand our internal management, technical information and accounting systems to support our desired growth. If we fail to manage our anticipated growth effectively, our business could be adversely affected.

We have agreed to indemnify our directors against liabilities incurred by them as directors.

We have agreed to indemnify our directors from and against all costs, charges and expenses reasonably incurred by them in respect of any civil, criminal or administrative action or proceeding to which they are made a party or with which they are threatened by reason of being or having been a director of Adira, provided that (a) they have acted honestly and in good faith with a view to the best interests of Adira; and (b) in the case of a criminal or administrative action or proceeding that is enforced by a monetary penalty, they had reasonable grounds for believing that their conduct was lawful. This indemnity may reduce the likelihood of derivative litigation against our directors and may discourage or deter our shareholders from suing the directors.

Risks Associated with Our Business

We have not discovered any oil and gas reserves, and we cannot assure you that we or our venture ever will.

We are in the business of exploring for oil and natural gas, and the development and exploitation of any significant reserves that are found. Oil and gas exploration involves a high degree of risk that the exploration will not yield positive results. These risks are more acute in the early stages of exploration. We have not discovered any reserves, and we cannot guarantee you that we ever will. Even if we succeed in discovering oil or gas reserves, these reserves may not be in commercially viable quantities or locations. Until we discover such reserves, we will not be able to generate any revenues from their exploitation and development. If we are unable to generate revenues from the development and exploitation of oil and gas reserves, we will be forced to change our business or cease operations.

- 9 -

Our business will suffer if we cannot obtain or maintain necessary licenses.

Our operations require licenses, permits and in some cases renewals of licenses and permits from various governmental authorities. Specifically, the licenses awarded to us by the Government of Israel have terms of three years and must be renewed in order to extend the license beyond this initial term. Although certain licenses have received one extension, there can be no assurance that we will be able to secure any additional extensions, if necessary. The Offshore Licenses require us to meet certain minimum commitments with respect to our activities on those licenses. We may apply to extend the timing for the commitments associated with the Offshore Licenses, but there can be no assurance that we will be able to secure any amendments to the commitment dates associated with the licenses, if necessary.

As of the date hereof, we have missed two Ministry milestones on the Samuel License; namely we have not signed a drilling contract by March 31, 2013, and we have not spud a well by April 30, 2013. We have requested an extension of both milestones and await a formal response from the Ministry. There is no assurance that the Ministry will grant our requests.

Among other factors, our ability to obtain, sustain or renew such licenses and permits on acceptable terms is subject to change in regulations and policies and to the discretion of the applicable governments. Our inability to obtain, maintain or acquire extensions for these licenses or permits could hamper our ability to produce revenues from operations. Other oil and gas companies may seek to acquire property leases and licenses that we will need to operate our business. This competition has become increasingly intense as the price of oil on the commodities markets has risen in recent years. This competition may prevent us from obtaining licenses we deem necessary for our business, or it may substantially increase the cost of obtaining these licenses.

We may not meet the timing commitments with respect to the Offshore Licenses.

We have formally applied to revise only certain of the minimum commitments with respect to the Offshore Licenses. We understand that rig availability in the eastern-Mediterranean region is in low supply and, accordingly, we may not be able to secure drilling rig contracts for drilling on our licenses. As such, even if we have funds available to proceed with the work programs on our licenses, we may not be able to source and secure a rig to begin drilling. Moreover, in the event that our joint venture, farm-out and/or other co-participants related to each of the Offshore Licenses are unable to meet their obligations under their respective agreements related to the Offshore Licenses or in the event that certain unforeseen circumstances occur, the timing commitments under the Offshore Licenses may not be met. If in the future we are required to apply for a formal extension from the Ministry from certain of the timing commitments with respect to the Offshore Licenses, we can make no guarantee that the Ministry will provide such extensions relating to the Offshore Licenses. If the Ministry does not provide such extensions, the Ministry could then begin a process to retract the applicable license or licenses from us.

Disagreements among Gabriella License co-participants may prevent the continued operations on the Gabriella License or result in the loss of our working interest in the Gabriella License.

We are a party to various contracts with Modi’in Energy Limited Partnership (“MELP) and Brownstone Energy Inc. (“Brownstone”) related to the Gabriella License and the joint operations to explore for hydrocarbons on that license. These contracts include the Farmout Agreement, dated January 26, 2010; the International Operating Agreement, dated March 10, 2011 (as amended on August 24, 2012); the Memorandum of Understanding, dated June 12, 2011; and the Letter Agreement, dated December 20, 2012. In addition, MELP entered into a rig/drilling contract with Noble International Limited dated July 19, 2012 (as amended three times). In connection with the License and the contracts just mentioned, (i) MELP alleges in letters and oral communications that we breached obligations under the contracts listed above, including failure to transfer funds required to meet various financial obligations; and (ii) we allege similar claims against MELP. In addition, both MELP and Adira have accused the other of various defaults under the joint operating agreement (the “Gabriella JOA”) relating to the Gabriella License, to which each of MELP, Adira and Brownstone are parties. The Gabriella JOA provides that certain “Defaults,” if not cured, will result in a party’s removal from the Gabriella JOA, and forfeiture of any working interest in the Gabriella License. Aspects of the Memorandum of Understanding and the Letter Agreement listed above contain a similar mechanism that would, if triggered, strip us of any interest in the Gabriella License, cause the loss of our right to receive management fees, royalty rights, and other payments and rights due to it from MELP and from MELP’s general partner.

- 10 -

Thus far, accusations to and from MELP have been in the form of letters and oral communications, not legal action. If either party initiates legal action, then the other will likely respond with counter-claims, and we cannot provide any assurance that we would prevail on any of the matters in dispute. If legal action is pursued by either side, and if we are ultimately found to be in breach of our obligations, this could result in the loss of our entire interest in the Gabriella License, and the loss of all associated royalty rights, options to purchase an interest in the Yam Hadera License, management fees, and operator fees.

In addition, even if we were to prevail in any legal action against MELP, that could mean that a 70% share of the total funding obligations with respect to the Gabriella License would have to be met pro rata (50/50) by Adira and Brownstone, or new Gabriella License participants would have to agree to take on a large portion of the funding. This would further exacerbate the challenges with regards to liquidity, capital resources and funding that are mentioned in other Risk Factors in this filing, unless new investors were located, or third parties were interested in taking a working interest in the Gabriella License directly. Finally, rather than initiating or responding to court action filed by MELP or Adira, the parties may reach an amicable settlement of their current disagreements. Such settlement may result in additional changes to Adira’s rights, obligations, or working interest on the Gabriella License that are not yet known to the Company.

We may be liable to pay operating expenditures respecting our licenses exceeding our pro rata share of such expenditures.

We are a party to certain joint operation and farm-out agreements respecting our licenses pursuant to which we have agreed to pay our pro rata share of operating expenditures in connection with the licenses. In accordance with the terms and conditions of such agreements, if a party fails to pay its pro rata share of the expenditures, we may be liable to cover such defaulting party’s pro rata share of the expenditures based on our interest in the license to ensure compliance with the terms and expenditure requirements under the work plan. If we do not have sufficient funds to cover the defaulting party’s pro rata share of expenditures, we may not be able to maintain our licenses in good standing, causing them to be revoked, suspended or cancelled, which would have a material adverse effect on us.

Adira is owed an aggregate of $3 million of operating costs on the Samuel License from GGRI and Emmanuelle under the Joint Operating Agreement, or “JOA,” for that license, made up as follows: Emanuelle and GGRI owe an aggregate of $2.8 million through their direct interest in the license, as JOA signatories and GGRI owes an additional $0.2 million, indirectly, through its 40% interest in Adira GeoGlobal. The three parties are currently discussing a plan to ensure the reimbursement to Adira for such costs. If GGRI and Emanuelle do not repay Adira for the costs owed through their direct interest in the Samuel License, then in accordance with the JOA, Adira may seek reimbursement of these costs from the other Samuel License participants in proportion to their respective interests in the Samuel License, and all of the participants, including Adira, will each receive a proportionate increase in their interests in the Samuel License. In addition, if GGRI does not repay Adira for the costs owed through GGRI’s 40% ownership interest in Adira GeoGlobal, Adira may have to seek reimbursement through continued negotiation or litigation.

We might incur debt in order to fund our exploration and development activities, which would continue to reduce our financial flexibility and could have a material adverse effect on our business, financial condition or results of operation.

It is possible that we might incur debt in order to fund our exploration and development activities, which would continue to reduce our financial flexibility and could have a material adverse effect on our business, operations and results of operations and financial condition. General economic conditions, oil and gas prices and financial, business and other factors affect our operations and future performance. Many of these factors are beyond our control. No assurances can be made that we will be able to generate sufficient cash flow to pay the interest on its debt or that future working capital, borrowings or equity financing will be available to pay or refinance such debt. Factors that will affect its ability to raise cash through an offering of Common Shares or other types of equity securities, or a refinancing of debt include financial market conditions, the value of its assets and performance at the time we need capital. No assurances can be made that we will have sufficient funds to make such payments. If we do not have sufficient funds and are otherwise unable to negotiate renewals of our borrowings or arrange new financing, we might be required to sell significant assets. Any such sale could have a material adverse effect on our business, financial condition and results of operations.

Our assets and operations are subject to government regulation in Israel.

Our interests and operations in Israel may be affected in varying degrees by government regulations relating to the oil and gas industry. Any changes in regulations or shifts in political conditions are beyond the control of the Company and may adversely affect our business. Our operations may be affected in varying degrees by new government regulations and changes to existing regulations, including those with respect to restrictions on exploration and production, price controls, export controls, income taxes, employment, land use, water use, environmental legislation and safety regulations. On April 10, 2011, the Petroleum Profits Taxation Law, 5771-2011 (the “Petroleum Taxation Law”) was published based largely on the conclusions and recommendations of the Sheshinski Committee, a government appointed committee in Israel which was tasked with examining the fiscal system prevailing in Israel in respect of petroleum and gas resources and proposing an updated fiscal policy. The Petroleum Taxation Law imposes a progressive levy (the “Levy”) on profits derived from petroleum reserve, in addition to the 12.5% royalty payable under the old tax regime which remains unchanged. The Levy is designed to capitalize on the economic benefits from each individual reservoir and is imposed only after the investment in exploration, development and construction are fully returned, plus a yield that reflects, among other things, the developer’s risk and required financial expenses. As a result of the Levy, the aggregate government take from oil and gas revenue is expected to increase from approximately 33% to about 52% to 62%. The implementation of the Petroleum Taxation Law may have an adverse effect on our business, financial conditions and results as our business matures.

- 11 -

Our future success depends upon our ability to find, develop and acquire additional oil and natural gas reserves that are economically recoverable.

In the event that we are able to find and develop oil and natural gas reserves which are economically recoverable, the rate of production from those reservoirs will decline as reserves are depleted. As a result, we must locate and develop or acquire new oil and natural gas reserves to replace those being depleted by production. We must do this even during periods of low oil and natural gas prices when it is difficult to raise the capital necessary to finance activities. Without successful exploration or acquisition activities, our reserves and revenues will decline. We may not be able to find and develop or acquire additional reserves at an acceptable cost or have necessary financing for these activities.

Oil and natural gas drilling is a high-risk activity.

Our future success will depend on the success of our exploration and drilling programs. In addition to the numerous operating risks described in more detail below, these activities involve the risk that no commercially productive oil or natural gas reservoirs will be discovered. In addition, we are uncertain as to the future cost or timing of drilling, completing and producing wells. Furthermore, our drilling operations may be curtailed, delayed or cancelled as a result of a variety of factors, including, but not limited to, the following: unexpected drilling conditions; pressure or irregularities in formations; equipment failures or accidents; adverse weather conditions; inability to comply with governmental requirements; and shortages or delays in the availability of drilling rigs and the delivery of equipment. If we experience any of these problems, our ability to conduct operations could be adversely affected.

Our success depends on our ability to attract and retain qualified personnel.

Recruiting and retaining qualified personnel is critical to our success. The number of persons skilled in the acquisition, exploration and development of oil and gas properties is limited and competition for such persons is intense. As our business activity grows, it will require additional key financial, administrative and qualified technical personnel as well as additional operations staff. Although we believe that we will be successful in attracting, training and retaining qualified personnel, there can be no assurance of such success. If we are not successful in attracting and training qualified personnel, the efficiency of our operations could be affected, which could have an adverse impact on our future cash flows, earnings, results of operations and financial condition. Our development now and in the future will also depend on the efforts of key management figures. The loss of any of these key people could have a material adverse effect on our business. We do not currently maintain key-man life insurance on any of our key employees.

We face strong competition from other energy companies that may negatively affect our ability to carry on operations.

We operate in the highly competitive area of oil and natural gas exploration, development and production. Factors which affect our ability to successfully compete in the marketplace include, but are not limited to, the following: the availability of funds and information relating to a property; the standards established by us for the minimum projected return on investment; the availability of alternate fuel sources; and the transportation of gas.

Our competitors include major integrated oil companies, substantial independent energy companies, affiliates of major pipeline companies, and national and local natural gas gatherers. Many of these competitors possess greater financial and other resources than we do.

- 12 -

We might not be able to determine reserve potential, identify liabilities associated with the properties or obtain protection from sellers against them, which could cause us to incur losses.

Although we believe we have reviewed and evaluated our properties in Israel in a manner consistent with industry practices, such review and evaluation might not necessarily reveal all existing or potential problems. This is also true for any future acquisitions made by us. Inspections may not always be performed on every well, and environmental problems, such as groundwater contamination, are not necessarily observable even when an inspection is undertaken. Even when problems are identified, a seller may be unwilling or unable to provide effective contractual protection against all or part of those problems, and we often assume environmental and other risks and liabilities in connection with the acquired properties.

You should not place undue reliance on reserve information because reserve information represents estimates.

There are numerous uncertainties inherent in estimating quantities of proved reserves and cash flows from such reserves, including factors beyond our control and the control of engineers. Reserve engineering is a subjective process of estimating underground accumulations of oil and natural gas that cannot be measured in an exact manner. The accuracy of an estimate of quantities of reserves, or of cash flows attributable to these reserves, is a function of many factors, including, but not limited to, the following: available data; assumptions regarding future oil and natural gas prices; estimates of future production rates; expenditures for future development and exploitation activities; and engineering and geological interpretation and judgment.

Reserves and future cash flows may also be subject to material downward or upward revisions based upon production history, development and exploitation activities and oil and natural gas prices. Actual future production, revenue, taxes, development expenditures, operating expenses, quantities of recoverable reserves and value of cash flows from those reserves may vary significantly from the estimates. In addition, reserve engineers may make different estimates of reserves and cash flows based on the same available data.

The nature of oil and gas exploration makes the estimates of costs uncertain, and our operations may be adversely affected if we underestimate such costs.

It is difficult to project the costs of implementing an exploratory drilling program. Complicating factors include the inherent uncertainties of drilling in unknown formations, the costs associated with encountering various drilling conditions, such as over-pressured zones and tools lost in the hole, and changes in drilling plans and locations as a result of prior exploratory wells or additional seismic data and interpretations thereof. If we underestimate the costs of such programs, we may be required to seek additional funding, shift resources from other operations or abandon such programs.

Losses and liabilities arising from uninsured or under-insured hazards could have a material adverse effect on our business.

If we develop and exploit oil and gas reserves, those operations will be subject to the customary hazards of recovering, transporting and processing hydrocarbons, such as fires, explosions, gaseous leaks, migration of harmful substances, blowouts and oil spills. An accident or error arising from these hazards might result in the loss of equipment or life, as well as injury, property damage or other liability. We cannot assure you that we will obtain insurance on reasonable terms or that any insurance we may obtain will be sufficient to cover any such accident or error. Our operations could be interrupted by natural disasters or other events beyond our control. Losses and liabilities arising from uninsured or under-insured events could have a material adverse effect on our business, financial condition and results of operations.

Compliance with environmental and other government regulations could be costly and could negatively impact production.

All phases of the oil and gas business present environmental risks and hazards and are subject to environmental regulation pursuant to a variety of laws and regulations. Our operations are subject to laws and regulations governing the discharge of materials into the environment or otherwise relating to environmental protection. The recent trend toward stricter standards in environmental legislation and regulation is likely to continue. The enactment of stricter legislation or the adoption of stricter regulation could have a significant impact on our operating costs, as well as on the oil and natural gas industry in general.

- 13 -

Our existing property, and any future properties that we may acquire, may be subject to pre-existing environmental liabilities.

Pre-existing environmental liabilities may exist on the property in which we currently hold an interest or on properties that may be subsequently acquired by us which are unknown to the Company and which have been caused by previous or existing owners or operators of the properties. In such event, we may be required to remediate these properties and the costs of remediation could be substantial. Further, in such circumstances, we may not be able to claim indemnification or contribution from other parties. In the event we were required to undertake and fund significant remediation work, such event could have a material adverse effect upon the Company and the value of our common shares.

Penalties we may incur could impair our business.

Failure to comply with government regulations could subject us to civil and criminal penalties, could require us or our venture to forfeit property rights or licenses, and may affect the value of our assets. We may also be required to take corrective actions, such as installing additional equipment, which could require substantial capital expenditures. We could also be required to indemnify our employees in connection with any expenses or liabilities that they may incur individually in connection with regulatory action against them. As a result, our future business prospects could deteriorate due to regulatory constraints, and our profitability could be impaired by our obligation to provide such indemnification to our employees.

Strategic relationships upon which we may rely are subject to change, which may diminish our ability to conduct our operations.

Our ability to successfully acquire additional licenses, to discover reserves, to participate in drilling opportunities and to identify and enter into commercial arrangements depends on developing and maintaining close working relationships with industry participants and government officials and on our ability to select and evaluate suitable properties and to consummate transactions in a highly competitive environment. We may not be able to establish these strategic relationships, or if established, we may not be able to maintain them. In addition, the dynamics of our relationships with strategic partners may require us to incur expenses or undertake activities we would not otherwise be inclined to undertake in order to fulfill our obligations to these partners or maintain our relationships. If our strategic relationships are not established or maintained, our business prospects may be limited, which could diminish our ability to conduct our operations.

Political instability or fundamental changes in the leadership or in the structure of the governments in the jurisdictions in which the Company operates could have a material negative impact on the Company.

Our interests may be affected by political and economic upheavals. Although we currently operate in jurisdictions that welcome foreign investment and are generally stable, there is no assurance that the current economic and political situation in these jurisdictions will not change drastically in coming years. Local, regional and world events could cause the jurisdictions in which we operate to change the applicable resource laws, tax laws, foreign investment laws, or to revise their policies in a manner that renders our current and future projects non-economic.

Even if we discover and then develop oil and gas reserves, we may have difficulty distributing our production.

If our exploration activities result in the discovery of oil and gas reserves, and if we are able to successfully develop and exploit such reserves, we will have to make arrangements for storage and distribution of oil and gas. We would have to rely on local infrastructure and the availability of transportation for storage and shipment of oil and gas products, but any readily available infrastructure and storage and transportation facilities may be insufficient or not available at commercially acceptable terms. The marketability of our production, if any, will depend in part upon the availability, proximity, and capacity of oil and natural gas pipelines, crude oil trucking, natural gas gathering systems and processing facilities. This could be particularly problematic to the extent that operations are conducted in remote areas that are difficult to access, such as areas that are distant from shipping or pipeline facilities. Furthermore, weather conditions or natural disasters, actions by companies doing business in one or more of the areas in which we or our venture will operate, or labor disputes may impair the distribution of oil and gas. In addition, Israel has little or no storage capacity and the currently available distribution infrastructure is limited. These factors may affect the ability to explore and develop properties and to store and transport oil and gas and may increase our expenses to a degree that has a material adverse effect on operations.

- 14 -

Our inability to obtain necessary facilities could hamper our operations.

Oil and gas exploration activities depend on the availability of equipment, transportation, power and technical support in the particular areas where these activities will be conducted, and our access to these facilities may be limited. Demand for such limited equipment and other facilities or access restrictions may affect the availability of such equipment to us and may delay exploration and development activities. The quality and reliability of necessary facilities may also be unpredictable and we may be required to make efforts to standardize our facilities, which may entail unanticipated costs and delays. Shortages or the unavailability of necessary equipment or other facilities will impair our activities, either by delaying our activities, increasing our costs or otherwise.

Factors beyond our control affect our ability to market oil and gas.

Our ability to market oil and natural gas from ourwells, in the event we discover and exploit oil and natural gas, depends upon numerous factors beyond our control. These factors include, but are not limited to, the following: the level of domestic production and imports of oil and gas; the volatility of both oil and natural gas pricing; the proximity of natural gas production to natural gas facilities, pipelines and other means of transportation; the availability of pipeline capacity or other means of transportation; the demand for oil and natural gas by utilities and other end users; the availability of alternate fuel sources; the effect of inclement weather; and government regulation of oil and natural gas marketing.

If these factors were to change dramatically, our ability to market oil and natural gas or obtain favourable prices for our oil and natural gas could be adversely affected.

Prices and markets for oil are unpredictable and tend to fluctuate significantly, which could reduce profitability, growth and the value of our business if we or our ventures ever begin exploitation of reserves.

Our future financial condition, results of operations and the carrying value of our oil and natural gas properties depend primarily upon the prices we receive for our oil and natural gas production, if any. Oil and natural gas prices historically have been volatile and likely will continue to be volatile in the future, especially given current world economic conditions. Significant changes in long-term price outlooks for crude oil could by the time that we start exploiting oil and gas reserves, if we ever discover and exploits such reserves, have a material adverse effect on revenues as well as the value of licenses or other assets.

Future cash flow from operations, if any, will be highly dependent on the prices that we receive for oil and natural gas. This price volatility also affects the amount of our cash flow available for capital expenditures and our ability to borrow money or raise additional capital. The prices for oil and natural gas are subject to a variety of additional factors that are beyond our control. These factors include: the level of consumer demand for oil and natural gas; the domestic and foreign supply of oil and natural gas; the ability of the members of the Organization of Petroleum Exporting Countries to agree to and maintain oil price and production controls; the price of foreign oil and natural gas; the price and availability of alternative fuel sources; governmental regulations; weather conditions; market uncertainty; political conditions in oil and natural gas producing regions, including Israel and the Middle East; war, or the threat of war, in oil producing regions; and worldwide economic conditions.

- 15 -

These factors and the volatility of the energy markets generally make it extremely difficult to predict future oil and natural gas price movements with any certainty. Also, oil and natural gas prices do not necessarily move in tandem. Declines in oil and natural gas prices would not only reduce revenue, but could reduce the amount of oil and natural gas that we can produce economically and, as a result, could have a material adverse effect upon our financial condition, cash flows, results of operations, oil and natural gas reserves, the carrying values of our oil and natural gas properties and the amounts we can borrow under any bank credit facilities we may obtain in the future.

Operating hazards may adversely affect our ability to conduct business.

Our future operations, if any, will be subject to risks inherent in the oil and natural gas industry, including, but not limited to, the following: blowouts; cratering; explosions; uncontrollable flows of oil, natural gas or well fluids; fires; pollution; and other environmental risks.

These risks could result in substantial losses to us from injury and loss of life, damage to and destruction of property and equipment, pollution and other environmental damage and suspension of operations. Governmental regulations may impose liability for pollution damage or result in the interruption or termination of operations.

We may enter into hedging agreements but may not be able to hedge against all such risks.

If we are able to discover commercially exploitable quantities of oil or gas and is able to enter into commercial production, from time to time we may enter into agreements to receive fixed or a range of prices on its oil and natural gas production to offset the risk of revenue losses if commodity prices decline; however, if commodity prices increase beyond the levels set in such agreements, we will not benefit from such increases. Similarly, from time to time we may enter into agreements to fix the exchange rate of certain currencies to US dollars in order to offset the risk of revenue losses if the other currencies increase in value compared to the US dollar; however, if other currencies decline in value compared to the US dollar, we will not benefit from the fluctuating exchange rate. In addition to the potential of experiencing an opportunity cost, other potential costs or losses associated with hedging include the risk that the other party to a hedge transaction does not perform its obligations under a hedge agreement, the hedge is imperfect or our hedging policies and procedures are not followed.

Our Company is organized under the laws of Canada.

Our Company is a Canadian corporation governed by theCanada Business Corporations Actand as such, its corporate structure, the rights and obligations of shareholders and its corporate bodies may be different from those of the home countries of international investors. Furthermore, non-Canadian residents may find it more difficult and costly to exercise shareholder rights. International investors may also find it costly and difficult to effect service of process and enforce their civil liabilities against the Company or some of its directors, controlling persons and officers.

To the extent that we establish natural gas and oil reserves, we will be required to replace, maintain or expand these natural gas and oil reserves in order to prevent reserves and production from declining, which could adversely affect cash flows and income.

In general, production from natural gas and oil properties declines over time as reserves are depleted, with the rate of decline depending on reservoir characteristics. If we establish reserves, of which there is no assurance, and are not successful in its subsequent exploration and development activities or in subsequently acquiring properties containing proved reserves, our proved reserves will decline as reserves are produced. Our future natural gas and oil production is highly dependent upon its ability to economically find, develop or acquire reserves in commercial quantities.

To the extent cash flow from operations, if any, is reduced, either by a decrease in prevailing production volume prices for natural gas and oil or an increase in finding and development costs, and external sources of capital become limited or unavailable, our ability to make the necessary capital investment to maintain or expand its asset base of natural gas and oil reserves would be impaired. Even with sufficient available capital, our future exploration and development activities may not result in additional proved reserves, and we might not be able to drill productive wells at acceptable costs.

- 16 -

We may be treated as a U.S. corporation and taxed by the U.S. on our worldwide income.

We continued from Nevada to Canada in 2008. Such continuance is for corporate purposes a migration of us from Nevada to Canada. Transactions whereby a U.S. corporation migrates to a foreign jurisdiction are considered by the U.S. Congress to be a potential abuse of the U.S. tax rules because thereafter the foreign entity is not subject to U.S. tax on its worldwide income. As a result, Section 7874(b) of the Internal Revenue Code of 1986, as amended, was enacted to address this potential abuse. Section 7874(b) provides generally that a corporation that migrates from the U.S. will nonetheless remain subject to U.S. tax on its worldwide income unless the migrating entity has substantial business activities in the foreign country in which it is migrating when compared to its total business activities.

If Section 7874(b) were to apply to our migration from Nevada to Canada, it would cause us to be subject to U.S. federal income taxation on our worldwide income. Section 7874(b) of the Code will apply to our migration unless we had substantial business activities in Canada when compared to our total business activities at the time of our migration.

Based on the fact that substantially all of our activities were taking place in Canada and all of our assets were located in Canada at the time of our migration, we have taken the position that we had substantial business activity in Canada in relation to our worldwide activities at the time of the migration and that Section 7874(b) did not apply to cause us, after the migration, to be subject to U.S. federal income tax on our worldwide income. There is limited guidance as to what “substantial business activity” is “when compared to our worldwide activities.” Accordingly, the position adopted by us may be challenged by the U.S. tax authorities with the result that we may be subject to U.S. federal income taxes on our worldwide activities. In addition to U.S. federal income taxes, were Section 7874(b) to apply to us, we could be subject to penalties for failure to file U.S. federal income tax returns, late fees and interest on past due taxes. Furthermore, if Section 7874(b) were to apply to us, our non-U.S. shareholders may be subject to adverse U.S. federal income tax consequences such as the assessment of U.S. federal income withholding taxes on dividends paid by us. Each shareholder should consult its own tax advisor regarding the foregoing rules.

Risks Associated with our Common Shares

The market price of the common shares of our corporation may be volatile

The market price of our common shares may experience significant volatility. For the 12 months preceding the date of this annual report, the trading price of our common shares on the TSXV (as defined below) has ranged from a low of CDN$0.02 per share to a high of CDN$0.30 per share. Numerous factors, including many over which we have no control, may have a significant impact on the market price of our common shares including, among other things: regulatory developments in target markets affecting us, our customers or our competitors; actual or anticipated fluctuations in our quarterly operating results; changes in financial estimates or other material comments by securities analysts relating to us, our competitors or the industry in general; announcements by other companies in the industry relating to their operations, strategic initiatives, financial condition or financial performance or to the industry in general; announcements of acquisitions or consolidations involving industry competitors or industry suppliers; addition or departure of our executive officers; and sales or perceived sales of additional common shares of Adira.In addition, the stock market in recent years has experienced extreme price and trading volume fluctuations that often have been unrelated or disproportionate to the operating performance of individual companies. These broad market fluctuations may adversely affect the price of the common shares of Adira regardless of our operating performance. There can be no assurance that an active market for the Common Shares will be established or persist and the share price may decline.

The value of securities issued by us might be affected by matters not related to our operating performance.

The value of securities issued by us may be affected by matters not related to our operating performance or underlying value for reasons that include the following: general economic conditions in Canada, the US, Israel and globally; industry conditions, including fluctuations in the price of oil and natural gas; governmental regulation of the oil and gas industry, including environmental regulation; fluctuation in foreign exchange or interest rates; liabilities inherent in oil and natural gas operations; geological, technical, drilling and processing problems; assuming we achieve production, unanticipated operating events which can reduce production or cause production to be shut-in or delayed; failure to obtain industry partner and other third party consents and approvals, when required; stock market volatility and market valuations; competition for, among other things, capital, acquisition of reserves, undeveloped land and skilled personnel; the need to obtain required approvals from regulatory authorities; worldwide supplies and prices of and demand for natural gas and oil; political conditions and developments in Israel, Canada, the US, and globally; political conditions in natural gas and oil producing regions; revenue and operating results failing to meet expectations in any particular period; investor perception of the oil and gas industry; limited trading volume of our common shares; change in environmental and other governmental regulations; announcements relating to our business or the business of our competitors; our liquidity; and our ability to raise additional funds.

- 17 -

In the past, companies that have experienced volatility in their value have been the subject of securities class action litigation. We might become involved in securities class action litigation in the future. Such litigation often result in substantial costs and diversion of management’s attention and resources and could have a material adverse effect on our business, financial condition and results of operation.

An investment in our Company will likely be diluted.

We may issue a substantial number of our common shares without investor approval to raise additional financing and we may consolidate the current outstanding common shares. Any such issuance or consolidation of our securities in the future could reduce an investor’s ownership percentage and voting rights in the Company and further dilute the value of your investment.

If we are a “passive foreign investment company” at any time that a U.S. shareholder holds our common shares, such U.S. shareholder may be subject to adverse U.S. federal income tax consequences

Acquiring, holding or disposing of our common shares may have tax consequences under the laws of Canada and the United States that are not disclosed in this Form 20-F. In particular, potential investors that are U.S. taxpayers should be aware that we may be considered a “passive foreign investment company” under Section 1297(a) of the U.S. Internal Revenue Code (a “PFIC”) with respect to U.S. shareholders. If the Company is or becomes a PFIC during any time that a U.S. shareholder holds our common shares, any gain recognized on the sale of our common shares and any excess distributions paid on our common shares must be ratably allocated to each day in a U.S. taxpayer’s holding period for our common shares and any excess distributions paid on our common shares must be ratably allocated to each day in a U.S. taxpayer’s holding period for our common shares. The amounts allocated to the taxable year of disposition and to years before we became a PFIC would be taxed as ordinary income. The amount allocated to each other taxable year would be subject to tax at the highest rate applicable to ordinary income in effect for that taxable year for individuals or corporations, as appropriate, and an interest charge would be imposed on the tax attributable to the allocated amount, calculated as if such tax liability had been due in each such prior year. This risk factor is qualified in its entirety by the discussion set forth under the heading “Certain United States Federal Income Tax Considerations.” Shareholders should consult their own tax advisors as to the PFIC rules and the other tax consequences of the acquisition, ownership, and disposition of our common shares.

We do not expect to pay dividends for the foreseeable future.

We do not intend to declare dividends for the foreseeable future, as we anticipate that we will reinvest any future earnings in the development and growth of our business. Therefore, investors will not receive any funds unless they sell their Common Shares, and shareholders may be unable to sell their shares on favorable terms or at all. We cannot assure you of a positive return on investment or that you will not lose the entire amount of your investment in our Common Shares. Prospective investors seeking or needing dividend income or liquidity should not purchase our

- 18 -

ITEM 4 INFORMATION ON THE COMPANY

We are a Canadian corporation existing under theCanada Business Corporations Act (the “CBCA”) which conducts business as an oil and gas exploration company with operations in the State of Israel. We have been granted certain petroleum licenses from the State of Israel, as more particularly described below in Item 4B – “Business Overview”.

The Company presently does not have any oil and gas reserves, does not produce any oil or gas and does not earn any significant revenues.

A. History and Development of the Company

Name

Our legal and commercial name is Adira Energy Ltd.