UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-09903 |

| | |

| | BNY Mellon Funds Trust | |

| | (Exact name of Registrant as specified in charter) | |

| | | |

| | c/o BNY Mellon Investment Adviser, Inc. 240 Greenwich Street New York, New York 10286 | |

| | (Address of principal executive offices) (Zip code) | |

| | | |

| | Deirdre Cunnane, Esq. 240 Greenwich Street New York, New York 10286 | |

| | (Name and address of agent for service) | |

| |

| Registrant's telephone number, including area code: | (212) 922-6400 |

| | |

Date of fiscal year end: | 08/31 | |

| Date of reporting period: | 08/31/23 | |

| | | | | | | |

FORM N-CSR

Item 1. Reports to Stockholders.

BNY Mellon Funds Trust

| |

BNY Mellon Income Stock Fund |

BNY Mellon Mid Cap Multi-Strategy Fund |

BNY Mellon Small Cap Multi-Strategy Fund |

BNY Mellon International Fund |

BNY Mellon Emerging Markets Fund |

BNY Mellon International Equity Income Fund |

BNY Mellon Asset Allocation Fund |

| | |

ANNUAL REPORT August 31, 2023 |

| |

Contents

THE FUNDS

FOR MORE INFORMATION

Back Cover

| |

| |

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.im.bnymellon.com and sign up for eCommunications. It’s simple and only takes a few minutes. |

| |

The views expressed herein are current to the date of this report. These views and the composition of the funds’ portfolios are subject to change at any time based on market and other conditions. |

| |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

DISCUSSION OF FUND PERFORMANCE (Unaudited)

For the period of September 1, 2022, through August 31, 2023, as provided by John C. Bailer, Brian C. Ferguson, and Keith Howell, Portfolio Managers of Newton Investment Management North America, LLC (NIMNA), the fund’s sub-adviser.

Market and Fund Performance Overview

For the 12-month period ended August 31, 2023, BNY Mellon Income Stock Fund’s (the “fund”) Class M shares produced a total return of 12.06%, Investor shares produced a total return of 11.93%, Class A shares produced a total return of 11.72%, Class C shares produced a total return of 11.00%, Class I shares produced a total return of 12.16% and Class Y shares produced a total return of 12.09%.1 In comparison, the fund’s benchmark, the Dow Jones U.S. Select Dividend™ Index (the “Index”), produced a total return of −1.56% for the same period.2

Income-oriented stocks lagged as investors favored more growth-oriented shares. But the fund outperformed the Index mostly due to favorable security selection.

The Fund’s Investment Approach

The fund seeks total return (consisting of capital appreciation and income). To pursue its goal, the fund normally invests at least 80% of its assets, plus any borrowings for investment purposes, in stocks. The fund seeks to focus on dividend-paying stocks and other investment techniques that produce income. We choose stocks through a disciplined investment process that combines quantitative modeling techniques, fundamental analysis and risk management. The fund emphasizes those stocks with value characteristics, although it may also purchase growth stocks. The fund may invest in the stocks of companies of any size, although it focuses on large-cap companies. The fund’s investment process is designed to provide investors with investment exposure to sector weightings and risk characteristics generally similar to those of the Index.

Market Supported by Easing Inflation, Economic Resilience

The reporting period was marked by a range of factors that affected returns. Early in the period, the dominant theme was the Federal Reserve’s (the “Fed”) continued monetary tightening policies aimed at curbing inflation. Added to this was the banking crisis that emerged early in 2023. Uncertainty about the outcome of the debt ceiling standoff in the Congress also weighed on markets, as did some weaker-than-expected performance of China’s economy. Easing inflation, continued economic growth, the anticipated end to the Fed’s rate hikes and the emergence of the artificial intelligence (“AI”) theme provided markets with support.

The Fed raised the federal funds rate seven times during the period but reduced the size of the increase from 75 basis points to just 25 basis points for the last four hikes. The smaller rate hikes late in the period disappointed markets somewhat, as many investors were hoping for an end to the hiking cycle, given some signs of economic slowing.

Economic data showed that as pricing pressures continued to weaken from their peak in June 2022, the labor market also began to soften. Though unemployment remained relatively low, some large technology companies announced layoffs or paused hiring amid a more cautious macroeconomic outlook.

The banking crisis that emerged early in 2023 gave investors another reason to believe the Fed’s tightening policy would not continue. Three regional banks—Silicon Valley Bank, Signature Bank and First Republic Bank—faced mounting losses in their long-dated bond holdings as interest rates rose. Uninsured depositors were alarmed by the headlines and lost confidence, choosing to move their money into larger money center banks.

In May 2023, the debate in Congress over the federal debt ceiling reached an apparent standoff, resulting in some market volatility. While an agreement was eventually reached, providing the market with some relief, the run-up caused some turmoil as the prospect of a default was threatened.

In addition to easing inflation and investors’ growing anticipation of the end to the Fed’s tightening cycle, the possibility the economy could avoid recession also provided some support as a widely expected recession failed to arrive. China’s weaker-than-expected rebound from its Zero-COVID policies, however, disappointed investors somewhat.

The market was also supported by the launch of ChatGPT by Open AI, which drew investors’ attention to the promise of artificial intelligence and its likely enhancement of productivity and economic growth. While the most immediate beneficiaries of this news were large-cap growth stocks in the information technology sector, their performance provided support to the market as a whole.

Performance Aided Largely by Stock Selection

The fund’s outperformance versus the Index benefited mainly from stock selection decisions, with asset allocations also contributing somewhat. The fund’s leading sector was utilities, where performance stemmed largely from a position in Constellation Energy Corp. This company is the largest owner and operator of nuclear power plants, and nuclear power will be the beneficiary of financial incentives passed in the 2022 Inflation Reduction Act. The company has also reported less volatile cash flows, resulting in a higher valuation. Stock selection in the information technology sector also added to the fund’s performance. Shares of Cisco Systems, Inc. a network hardware company, gained from the company’s robust backlog, which is twice the normal level, providing some assurance of revenues expected over the next two years. The fund’s position in Applied Materials, Inc. which is a semiconductor equipment manufacturer, also contributed positively. The company will be a beneficiary of the construction of semiconductor fabrication facilities in the U.S., funded in part by the CHIPS Act passed in 2022 to reduce the semiconductor industry’s dependence on China. Positions in the financials sector also boosted performance somewhat. Shares of insurance companies in particular, which benefit from higher interest rates, were advantageous. Shares of J.P.Morgan Chase & Co. also added to relative returns. The large bank was not hurt by the banking crisis early in the year, and it kept more cash on its balance sheet, which bolstered its financial results.

While all sectors generated positive returns, some lagged the Index, resulting in a drag on relative performance. But the fund’s relative returns were hindered most by certain stock selections.

2

In the consumer staples sector, which lagged the Index the most, the fund’s position in British American Tabacco PLC was a leading detractor. Shares slumped on concerns about the company’s exposure to the U.S. vaping market, where rival Philip Morris International will introduce a new product. Shares of Kenvue, Inc., a spin-off from Johnson & Johnson, also hampered relative returns. These shares performed poorly as arbitrageurs bought Johnson & Johnson and shorted Kenvue, Inc. In addition, Kenvue, Inc. is also exposed somewhat to legal liabilities related to a lawsuit regarding Johnson & Johnson’s talcum powder product. A lawsuit related to Tylenol may also have weighed on shares. Finally, two positions in the materials sector also detracted. Shares of two fertilizer companies, The Mosaic Co. and CF Industries Holdings, Inc., hampered performance as both companies were hurt by weak demand for potash.

Focused on Quality

In this uncertain and high interest-rate environment, we remain cautious. We believe inflation will remain relatively high for an extended period, in part due to deglobalization and also due to greater worker negotiating power, which should boost wages and support higher prices. As for interest rates, we believe that while short-term bond yields may come down, longer-term yields will remain steady.

In this environment, we remain focused on high-quality companies with strong balance sheets and less need to refinance existing debt. While some sectors, such as consumer staples, are highly leveraged, we are finding value elsewhere. We see opportunities among insurance companies, which typically benefit from higher interest rates. In addition, we are overweight in the energy sector, where balance sheets are stronger than in the past, and cash flows are strong. We also believe this sector will benefit as China continues to rebound. In addition, energy production in Russia will level off or decline because many oilfield services firms have exited the country as a result of sanctions by the U.S. and Europe. The need in the U.S. to refill the Strategic Petroleum Reserve could also boost demand for this sector.

Finally, we believe that market returns could be muted in the medium term, and that as a result, dividends will account for a larger portion of total returns in the equity market.

September 15, 2023

1 Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. The fund’s returns reflect the absorption of certain fund expenses by BNY Mellon Investment Adviser, Inc. pursuant to an agreement in effect through December 30, 2023, for Class A, Class C, Class I and Class Y, at which time it may be extended, terminated or modified. Had these expenses not been absorbed, the fund’s returns for those share classes would have been lower.

2 Source: Lipper Inc. – The Dow Jones U.S. Select Dividend™ Index is defined as all dividend-paying companies in the Dow Jones U.S. Index, excluding REITs, that have a non-negative, historical, five-year dividend-per-share growth rate, a five-year average dividend coverage ratio of greater than or equal to 167%, paid dividends in each of the previous five years, non-negative, trailing 12-month earnings-per-share (EPS), a float-adjusted market capitalization of at least U.S. $1 billion, and a three-month average daily trading volume of 200,000 shares. Investors cannot invest directly in any index.

Please note: the position in any security highlighted with italicized typeface was sold during the reporting period.

Investing in foreign denominated and/or domiciled securities involves special risks, including changes in currency exchange rates, political, economic, and social instability, limited company information, differing auditing and legal standards, and less market liquidity. These risks generally are greater with emerging market countries.

Equities are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

3

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

For the period from September 1, 2022, through August 31, 2023, as provided by Alicia Levine, Primary Portfolio Manager responsible for investment allocation decisions.

Market and Fund Performance Overview

For the 12-month period ended August 31, 2023, BNY Mellon Mid Cap Multi-Strategy Fund’s (the “fund”) Class M shares produced a total return of 10.50%, and Investor shares produced a total return of 10.18%.1 In comparison, the fund’s benchmark, the Russell Midcap® Index (the “Index”), produced a total return of 8.38% for the reporting period.2 The Russell Midcap® Growth Index and Russell Midcap® Value Index, the fund’s secondary benchmarks, produced total returns of 13.00% and 5.65%, respectively, for the same period.3,4

Mid-cap stocks gained ground over the reporting period as investors began to anticipate the end of the Federal Reserve’s (the “Fed”) monetary tightening program. The fund outperformed the Index due to outperformance by three of the underlying strategies.

The Fund’s Investment Approach

The fund seeks capital appreciation. The fund pursues its goal by normally investing at least 80% of its net assets in equity securities of mid-cap companies. The fund considers mid-cap companies to be those companies with market capitalizations that are within the market-capitalization range of companies comprising the Index. Furthermore, the fund normally allocates assets across multiple investment strategies employed by the investment adviser and unaffiliated sub-investment advisers that invest primarily in equity securities issued by mid-cap companies. The investment adviser determines the investment strategies and sets target allocations and ranges. The fund is designed to provide exposure to various investment strategies and styles, including the Mid Cap Tax-Sensitive Core Strategy, Opportunistic Mid Cap Value Strategy, Mid Cap Growth Strategy, Boston Partners Mid Cap Value Strategy and Geneva Mid Cap Growth Strategy, all as more particularly described in the fund’s prospectus.

Market Supported by Easing Inflation, Economic Resilience

The reporting period was marked by a range of factors that affected returns. Early in the period, the dominant theme was the Fed’s continued monetary tightening policies aimed at curbing inflation. Added to this was the banking crisis that emerged early in 2023. Uncertainty about the outcome of the debt ceiling standoff in the Congress also weighed on markets, as did some weaker-than-expected performance of China’s economy. Easing inflation, continued economic growth, the anticipated end to the Fed’s rate hikes and the emergence of the artificial intelligence (“AI”) theme provided markets with support.

The Fed raised the federal funds rate seven times during the period but reduced the size of the increase from 75 basis points to just 25 basis points for the last four hikes. The smaller rate hikes late in the period disappointed markets somewhat, as many investors were hoping for an end to the hiking cycle, given some signs of economic slowing.

Economic data showed that as pricing pressures continued to weaken from their peak in June 2022, the labor market also began to soften. Though unemployment remained relatively low, some large technology companies announced layoffs or paused hiring amid a more cautious macroeconomic outlook.

The banking crisis that emerged early in 2023 gave investors another reason to believe the Fed’s tightening policy would not continue. Three regional banks—Silicon Valley Bank, Signature Bank and First Republic Bank—faced mounting losses in their long-dated bond holdings as interest rates rose. Uninsured depositors were disconcerted by the headlines and lost confidence, choosing to move their money into larger money center banks.

In May 2023, the debate in Congress over the federal debt ceiling reached an apparent standoff, resulting in some market volatility. While an agreement was eventually reached, providing the market with some relief, the run-up caused some turmoil as the prospect of a default was threatened.

In addition to easing inflation and investors’ growing anticipation of the end to the Fed’s tightening cycle, the possibility the economy could avoid recession also provided some support as a widely expected recession failed to arrive. China’s weaker-than-expected rebound from its Zero-COVID policies, however, disappointed investors somewhat.

The market was also supported by the launch of ChatGPT by Open AI, which drew investors’ attention to the promise of artificial intelligence and its likely enhancement of productivity and economic growth. While the most immediate beneficiaries of this news were large-cap growth stocks in the information technology sector, their performance provided support to the market as a whole.

Three Strategies Contributed Positively

The fund’s relative performance was aided by three of the five underlying strategies. The primary contributor was the Boston Partners Mid Cap Value Strategy, which outperformed both the Index and the Russell Midcap Value benchmark. The Opportunistic Mid Cap Value Strategy also contributed positively. In the growth category, the Midcap Growth Strategy added to relative returns, outperforming both the Index and the category benchmark.

On the other hand, an underweight to the value-oriented category hindered returns somewhat, and two underlying strategies in two other categories also detracted from relative performance. In the growth-oriented category, the Geneva Midcap Growth Strategy posted a positive return but fell slightly short of the category benchmark. In the tax-sensitive category, the Mid Cap Tax-Sensitive Core Strategy lagged.

A Positive Outlook

We’ve become more constructive on the forward outlook. There are growing signs that the slowdown in earnings and economic activity is stabilizing, and leading indicators are turning higher. Resilient U.S. growth is diverging from the rest of world, especially China and Europe, leading to a stronger U.S. dollar. The U.S. labor market is cooling but remains strong and continues to support consumer spending. Further disinflation

4

could be more challenging due to sticky inflation in the services sector, higher commodity prices, and resilient U.S. growth. Sentiment and valuations are elevated, which could become a near-term headwind along with higher interest rates. The longer U.S. growth remains resilient, the greater likelihood that interest rates stay higher for longer. Key risks are China’s slowdown, the impact of credit tightening, and another uptick in inflation, especially if inflation in services remains sticky, oil prices continue to increase and growth stays resilient.

September 15, 2023

1 Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

2 Source: Lipper Inc. — The Russell Midcap® Index measures the performance of the mid-cap segment of the U.S. equity universe. The Russell Midcap® Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Russell Midcap® Index represents approximately 31% of the total market capitalization of the Russell 1000 companies. The Russell Midcap® Index is constructed to provide a comprehensive and unbiased barometer for the mid-cap segment. The Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true midcap opportunity set. Investors cannot invest directly in any index.

3 Source: Lipper Inc. — The Russell Midcap® Value Index measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies that are considered more value-oriented relative to the overall market as defined by Russell’s leading style methodology. The Russell Midcap Value® Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap value market. The Russell Midcap® Value Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap value market. Investors cannot invest directly in any index.

4 Source: Lipper Inc. — The Russell Midcap® Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with higher growth earning potential as defined by Russell’s leading style methodology. The Russell Midcap® Growth Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap growth market. The Russell Midcap® Growth Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap growth market. Investors cannot invest directly in any index.

Equities are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

Stocks of small- and/or mid-cap companies often experience sharper price fluctuations than stocks of large-cap companies.

5

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

For the period of September 1, 2022, through August 31, 2023, as provided by Alicia Levine, Primary Portfolio Manager responsible for investment allocation decisions.

Fund and Market Performance Overview

For the 12-month period ended August 31, 2023, BNY Mellon Small Cap Multi-Strategy Fund’s (the “fund”) Class M shares produced a total return of 2.15%, and Investor shares produced a total return of 1.88%.1 In comparison, the fund’s primary benchmark, the Russell 2000® Index (the “Index”), produced a total return of 4.65% for the same period.2 The Russell 2000® Growth Index and Russell 2000® Value Index, the fund’s secondary benchmarks, produced total returns of 6.78% and 2.17%, respectively, for the same period.3,4

Small-cap stocks gained ground over the reporting period as investors began to anticipate the end of the Federal Reserve’s (the “Fed) monetary tightening program. The fund lagged the Index, primarily due to the underperformance of two of the fund’s underlying strategies.

The Fund’s Investment Approach

The fund seeks capital appreciation. The fund pursues its goal by normally investing at least 80% of its net assets, plus any borrowings for investment purposes, in equity securities of small-cap companies. The fund currently considers small-cap companies to be those companies with market capitalizations that are equal to or less than the market capitalization of the largest company included in the Index. Furthermore, the fund normally allocates assets across multiple investment strategies employed by the investment adviser that invest primarily in equity securities issued by small-cap companies. The investment adviser determines the investment strategies and sets target allocations and ranges. The fund is designed to provide exposure to various investment strategies and styles, including the Opportunistic Small Cap Strategy, the Small Cap Value Strategy and the Small Cap Growth Strategy—all of which are more fully described in the fund’s prospectus.

Market Supported by Easing Inflation, Economic Resilience

The reporting period was marked by a range of factors that affected returns. Early in the period, the dominant theme was the Fed’s continued monetary tightening policies aimed at curbing inflation. Added to this was the banking crisis that emerged early in 2023. Uncertainty about the outcome of the debt ceiling standoff in the Congress also weighed on markets, as did some weaker-than-expected performance of China’s economy. Easing inflation, continued economic growth, the anticipated end to the Fed’s rate hikes and the emergence of the artificial intelligence (“AI”) theme provided markets with support.

The Fed raised the federal funds rate seven times during the period but reduced the size of the increase from 75 basis points to just 25 basis points for the last four hikes. The smaller rate hikes late in the period disappointed markets somewhat, as many investors were hoping for an end to the hiking cycle, given some signs of economic slowing.

Economic data showed that as pricing pressures continued to weaken from their peak in June 2022, the labor market also began to soften. Though unemployment remained relatively low, some large technology companies announced layoffs or paused hiring amid a more cautious macroeconomic outlook.

The banking crisis that emerged early in 2023 gave investors another reason to believe the Fed’s tightening policy would not continue. Three regional banks—Silicon Valley Bank, Signature Bank and First Republic Bank—faced mounting losses in their long-dated bond holdings as interest rates rose. Uninsured depositors were disconcerted by the headlines and lost confidence, choosing to move their money into larger money center banks.

In May 2023, the debate in Congress over the federal debt ceiling reached an apparent standoff, resulting in some market volatility. While an agreement was eventually reached, providing the market with some relief, the run-up caused some turmoil as the prospect of a default was threatened.

In addition to easing inflation and investors’ growing anticipation of the end to the Fed’s tightening cycle, the possibility the economy could avoid recession also provided some support as a widely expected recession failed to arrive. China’s weaker-than-expected rebound from its Zero-COVID policies, however, disappointed investors somewhat.

The market was also supported by the launch of ChatGPT by Open AI, which drew investors’ attention to the promise of artificial intelligence and its likely enhancement of productivity and economic growth. While the most immediate beneficiaries of this news were large-cap growth stocks in the information technology sector, their performance provided support to the market as a whole.

Two Underlying Funds Hindered Performance

The primary detractor in the fund’s relative performance was the Small Cap Growth Strategy. The fund’s decision to underweight this underlying strategy partially offset the effect of this lagging performance. An overweight allocation to the small cap value category also hindered relative returns. Although the underlying strategy in this category outperformed the Russell 2000® Value benchmark, it lagged the Index. The Opportunistic Small Cap Strategy also detracted somewhat as it slightly lagged the Index.

On the other hand, the strongest performance came from the underlying strategy in the Small Cap Value category. The underlying fund in this category significantly outperformed the Russell 2000® Value benchmark.

A Positive Outlook

We’ve become more constructive on the forward outlook. There are growing signs that the slowdown in earnings and economic activity is stabilizing, and leading indicators are turning higher. Resilient U.S. growth is diverging from the rest of world, especially China and Europe, leading to a stronger U.S. dollar. The U.S. labor market is cooling but remains strong and continues to support consumer spending. Further disinflation could be more challenging due to sticky inflation in the services sector, higher commodity prices and resilient U.S. growth. Sentiment and valuations are elevated, which could become a

6

near-term headwind along with higher interest rates. The longer U.S. growth remains resilient, the greater likelihood that interest rates stay higher for longer. Key risks are China’s slowdown, the impact of credit tightening and another uptick in inflation, especially if inflation in services remains sticky, oil prices continue to increase and growth stays resilient.

September 15, 2023

1 Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

2 Source: Lipper Inc. — The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® Index is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set. Investors cannot invest directly in any index.

3 Source: Lipper Inc. — The Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher growth earning potential as defined by Russell’s leading style methodology. The Russell 2000® Growth Index is constructed to provide a comprehensive and unbiased barometer for the small-cap growth segment. The Russell 2000® Growth Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set, and that the represented companies continue to reflect growth characteristics. Investors cannot invest directly in any index.

4 Source: Lipper Inc. — The Russell 2000® Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies that are considered more value-oriented relative to the overall market as defined by Russell’s leading style methodology. The Russell 2000 ®Value Index is constructed to provide a comprehensive and unbiased barometer for the small-cap value segment. The Russell 2000 ®Value Index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set, and that the represented companies continue to reflect value characteristics. Investors cannot invest directly in any index.

Equities are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

Stocks of small- and/or mid-cap companies often experience sharper price fluctuations than stocks of large-cap companies.

7

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

For the period of September 1, 2022, through August 31, 2023, as provided by portfolio manager, James A. Lydotes, of Newton Investment Management North America, LLC, sub-adviser.

Market and Fund Performance Overview

For the 12-month period ended August 31, 2023, BNY Mellon International Fund’s (the “fund”) Class M shares produced a total return of 21.91%, and Investor shares produced a total return of 21.64%.1 In comparison, the fund’s benchmark, the MSCI EAFE® Index (the “Index”), produced a total return of 17.92% for the same period.2

International equity markets posted gains as inflation eased, and investors began to anticipate an easing of tight monetary policy. The fund outperformed the Index primarily due to favorable stock selections.

The Fund’s Investment Approach

The fund seeks long-term capital growth. To pursue this goal, the fund normally invests at least 65% of its total assets in equity securities of foreign issuers. Foreign issuers are companies, organized under the laws of a foreign country, whose principal trading market is in a foreign country or with a majority of their assets or business outside the United States. The fund may invest in companies of any size. Though not specifically limited, the fund ordinarily will invest in a broad range of (and in any case at least five different) countries. The fund will limit its investments in any single company to no more than 5% of the fund’s assets at the time of purchase.

The stocks purchased may have value and/or growth characteristics. The portfolio managers employ a “bottom-up” investment approach, which emphasizes individual stock selection. The stock selection process is designed to produce a diversified portfolio that, relative to the Index, has a below-average price/earnings ratio and an above-average earnings growth trend.

Market Supported by Easing Inflation, Economic Resilience

The reporting period was marked by a range of factors that affected returns. Early in the period, the dominant theme was the Federal Reserve’s (the “Fed”) continued monetary tightening policies aimed at curbing inflation. Added to this was the banking crisis that emerged early in 2023. Uncertainty about the outcome of the debt ceiling standoff in the Congress also weighed on markets, as did some weaker-than-expected performance of China’s economy. Easing inflation, continued economic growth, the anticipated end to the Fed’s rate hikes and the emergence of the artificial intelligence (“AI”) theme provided markets with support.

The Fed raised the federal funds rate seven times during the period but reduced the size of the increase from 75 basis points to just 25 basis points for the last four hikes. The smaller rate hikes late in the period disappointed markets somewhat, as many investors were hoping for an end to the hiking cycle, given some signs of economic slowing.

Economic data showed that as pricing pressures continued to weaken from their peak in June 2022, the labor market also began to soften. Though unemployment remained relatively low, some large technology companies announced layoffs or paused hiring amid a more cautious macroeconomic outlook.

The banking crisis that emerged early in 2023 gave investors another reason to believe the Fed’s tightening policy would not continue. Three regional banks—Silicon Valley Bank, Signature Bank and First Republic Bank—faced mounting losses in their long-dated bond holdings as interest rates rose. Uninsured depositors were disconcerted by the headlines and lost confidence, choosing to move their money into larger money center banks.

In May 2023, the debate in Congress over the federal debt ceiling reached an apparent standoff, resulting in some market volatility. While an agreement was eventually reached, providing the market with some relief, the run-up caused some turmoil as the prospect of a default was threatened.

In addition to easing inflation and investors’ growing anticipation of the end to the Fed’s tightening cycle, the possibility the economy could avoid recession also provided some support as a widely expected recession failed to arrive. China’s weaker-than-expected rebound from its Zero-COVID policies, however, disappointed investors somewhat.

The market was also supported by the launch of ChatGPT by OpenAI, which drew investors’ attention to the promise of artificial intelligence and its likely enhancement of productivity and economic growth. While the most immediate beneficiaries of this news were large-cap growth stocks in the information technology sector, their performance provided support to the market as a whole.

Risk factors that drove performance during the period varied. While the dividend and value factors were very strong over the last year, momentum was quite weak. In addition, outside the U.S. market, the “big tech” narrative has played little role in performance as big technology companies make up only a small share of non-U.S. developed markets. As a result, the value/dividend trade continued to work very well during the period.

Finally, markets in Europe benefited from economic activity that was stronger than expected. A year ago, many were concerned that Europe’s dependence on Russian natural gas would result in shortages, causing economic activity to suffer. But these fears failed to materialize as a mild winter reduced natural gas demand.

Stock Selection Drove Results

The fund performed well relative to the Index over the period due primarily to favorable stock selection. Selections in the utilities sector were a key to relative outperformance, with positions in SSE PLC, based in the UK, and Enel SPA, based in Italy, contributing most. Both companies performed better than expected because the worst-case scenario, which included price caps on utilities, failed to materialize. A position in British defense contractor BAE Systems PLC also added to relative returns. Shares moved higher as a result of the conflict between Russia and Ukraine. The fund’s position in Germany’s Deutsche Post AG, a package delivery and logistics company, was also advantageous as the company benefited from better-than-expected economic activity in Europe. Finally, Ashtead Group PLC, UK-based industrial equipment rental company,

8

contributed positively as well. The U.S. market makes up the bulk of the company’s business, and that market segment has performed well.

On a less positive note, the health care sector was the primary laggard. A large position in Roche Holding AG, a Swiss pharmaceutical and diagnostics company, detracted from returns because the company’s drug pipeline proved to be disappointing during the reporting period. In the consumer discretionary sector, the fund’s position in Volkswagen AG also detracted, primarily because of its exposure to China. In the less expensive portion of that auto market, the company has faced increased competition.

Europe, Health Care and Communication Services Are Attractive

We continue to be constructive about the next six to 12 months for non-U.S. developed market equities. Although Europe remains dependent on Russia for natural gas, once this coming winter has passed, investors will find stocks in this region more attractive.

We remain overweight in the health care sector, driven largely by an overweight to the pharmaceutical industry. The sector’s underperformance over the past years stemmed largely from a rotation into more cyclical sectors, but we continue to view our position in health care as appropriate, given its defensive, consumer staples-like nature. In addition, the sector is home to many attractive businesses, and valuations are generally attractive. We are also overweight in the communication services sector. We especially see value in telecommunications companies and advertising agencies.

September 15, 2023

1 Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

2 Source: Lipper Inc. — Reflects reinvestment of net dividends and, where applicable, capital gain distributions. The MSCI EAFE® Index (Europe, Australasia, Far East) is a free float-adjusted, market capitalization-weighted index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. Investors cannot invest directly in any index.

Equities are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

The fund’s performance will be influenced by political, social and economic factors affecting investments in foreign companies. Special risks associated with investments in foreign companies include exposure to currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political instability and differing auditing and legal standards. These risks are enhanced in emerging market countries.

The fund may, but is not required to, use derivative instruments. A small investment in derivatives could have a potentially large impact on the fund’s performance. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in the underlying assets.

9

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

For the period from September 1, 2022, through August 31, 2023, as provided by Paul Birchenough, Ian Smith and Alex Khosla, portfolio managers, of Newton Investment Management Limited, sub-adviser.

Market and Fund Performance Overview

For the 12-month period ended August 31, 2023, BNY Mellon Emerging Markets Fund’s (the “fund”) Class M shares produced a total return of 1.02%, and Investor shares produced a total return of .87%.1 In comparison, the fund’s benchmark, the MSCI Emerging Markets Index (the “Index”), produced a total return of 1.25% for the same period.2

The reporting period was bookended by two down months for markets, as high inflation, higher-for-longer interest rates, geopolitical tensions and concerns about the strength of the Chinese economy dragged the Index down. This outweighed a period of more positive sentiment that persisted through much of the fourth quarter of 2022 and into the new year. The fund underperformed the Index, mainly due to stock selections in the consumer staples and information technology sectors.

The Fund’s Investment Approach

The fund seeks long-term capital growth. To pursue its goal, the fund invests at least 80% of its assets in equity securities of companies organized, or with a majority of assets or operations, in countries considered to be emerging markets. Emerging-markets countries generally include all countries represented by the Index. The fund may invest in companies of any size.

Normally, the fund will invest in a broad range of (and in any case, at least five different) emerging-markets countries. The stocks purchased may have value and/or growth characteristics. The portfolio managers employ a “bottom-up” investment approach, which emphasizes individual stock selection. The stock selection process is designed to produce a diversified portfolio that, relative to the Index, has a below-average price/earnings ratio and an above-average earnings growth trend.

Inflation, Geopolitical Concerns and the Chinese Economy Hinder Markets

The outlook for inflation and the trajectory of monetary policy continued to dominate the narrative within financial markets. The review period began with a large decline in the Index with the Federal Reserve (the “Fed”) raising interest rates by 75 basis points (bps), with a hawkish statement accompanying the rise, prompting investors to reassess their assumptions that rate hikes might have peaked. Meanwhile, the threat of nuclear escalation by Russia further unsettled markets.

In early October 2022, evidence of decelerating price growth in the U.S. ISM (Institute for Supply Management) manufacturing report raised hopes that inflation had peaked, ensuring risk assets got off to a flying start. Further positive momentum was injected the following month, when it was the turn of U.S. consumer price inflation to come in lower than expected. However, the resilience of the U.S. economy, particularly when viewed in terms of its labor market, necessitated further increases in interest rates through the review period, and also saw expectations for the terminal rate this cycle to move higher.

The other key factor that affected confidence was the initial positive reaction to the lifting of China’s strict COVID-19 restrictions at the beginning of 2023, despite rising infections. Sentiment was also bolstered by a government vaccination drive for the elderly population and the securities regulator’s decision to make raising equity easier for property developers. However, as we moved through the year, a series of weak macroeconomic data releases called into question the strength of the country’s post-COVID-19 recovery.

Meanwhile, U.S.-China relations continued to worsen. Despite well-received indications from the Chinese government that it would provide more support for the troubled real estate sector, pledge to boost consumption and address the market concerns about local government debt, the Chinese market widely underperformed the Index over the review period. An unexpected move by the central bank to reduce interest rates by the greatest amount since 2020 to support an economy facing further pressure from weak consumer spending, also failed to boost the market.

Performance Hindered by Stock Selection

The leading detractor for the period was in the consumer staples sector. Shares of China’s Foshan Haitian Flavouring & Food Co. Ltd. trended downwards after the release of results in which net profits and sales came in lower than the market expected. Investors were also worried that short-term economic headwinds could push retail and catering customers to cheaper non-branded offerings. The second leading detractor was in the information technology sector. Shares of LONGi Green Energy Technology Co. Ltd. declined, with the solar energy product manufacturer being affected by concerns around pricing pressure. Finally, Brazil’s second-largest private bank, Banco Bradesco SA, weakened over the period after reporting a fall in profits and raising its forecast for the amount of money it will set aside to cover bad loans.

The energy sector was a leading contributor to the fund’s outperformance. Having sold the position in October 2022, the fund’s zero weighting in Brazil’s largest oil and gas producer, Petroleo Brasileiro SA, was the top contributor to relative returns. Its share price plunged in December 2022 as Brazilian lawmakers approved changes to a law that shields state-controlled companies from political interference. In the information technology sector, the fund benefited from its holding in Japan-based automatic test equipment manufacturer Advantest Corp., which rode a wave of positive sentiment after U.S. chipmaker Nvidia released guidance that hugely exceeded market expectations, driven by significant demand for chips used in generative artificial intelligence systems. China-based Internet giant Tencent Holdings Ltd. also outperformed over the review period, largely in the latter part of 2022, on optimism that the economic reopening in China would boost economic growth. Another leading contributor was China Resources Sanjiu Medical & Pharmaceutical Co,, which the fund sold in October 2022 following strong performance.

Attractive Opportunities in the Consumer Staples and Industrial Sectors

We believe the longer-term opportunities in emerging markets are attractive. These are based on relatively higher levels of

10

income growth, rapid increases in product penetration and scope for industry consolidation. We believe there is a unique opportunity for emerging-markets companies that are well-exposed to reliable secular-growth trends and that can exploit this opportunity more than their peers, with their differentiated customer offering and execution. Accordingly, we believe that emerging-markets investors who can identify the right growth themes and companies should be rewarded over the long term.

On a sector basis, the fund is most overweight in the consumer staples and industrials sectors. On a country basis, the fund remains most overweight in India, as we believe the country offers many of the best investment cases in emerging markets over five years and beyond.

September 15, 2023

1 Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. The fund’s return reflects the absorption of certain fund expenses by BNY Mellon Investment Adviser, Inc. pursuant to an agreement in effect through April 1, 2024, at which time it may be extended, modified or terminated. Had these expenses not been absorbed, returns would have been lower.

2 Source: Lipper Inc. — Reflects reinvestment of net dividends and, where applicable, capital gain distributions. The MSCI Emerging Markets Index is a free float-adjusted, market capitalization-weighted index that is designed to measure equity market performance of emerging markets. Investors cannot invest directly in any index.

Please note: the position in any security highlighted with italicized typeface was sold during the reporting period.

Equities are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

The fund’s performance will be influenced by political, social and economic factors affecting investments in foreign companies. Special risks associated with investments in foreign companies include exposure to currency fluctuations, less liquidity, less developed, or less efficient trading markets, lack of comprehensive company information, political instability and differing auditing and legal standards. These risks are enhanced in emerging market countries.

The fund may, but is not required to, use derivative instruments. A small investment in derivatives could have a potentially large impact on the fund’s performance. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in the underlying assets.

11

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

For the period from September 1, 2022, through August 31, 2023, as provided by Peter D. Goslin, CFA, of Newton Investment Management North America, LLC, sub-adviser.

Market and Fund Performance Overview

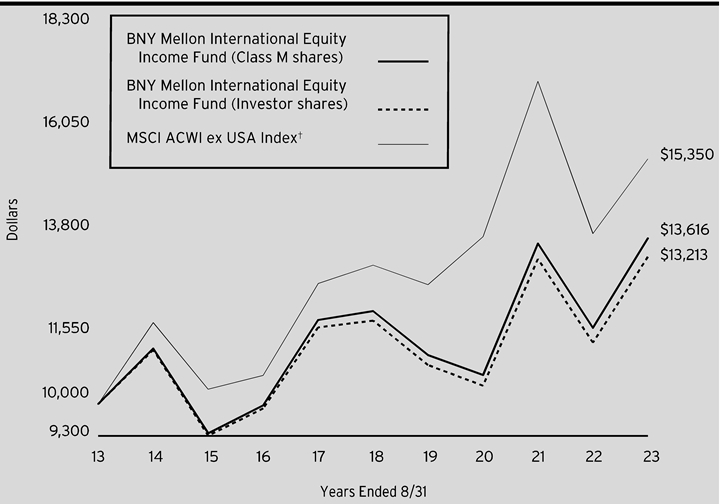

For the 12-month period ended August 31, 2023, BNY Mellon International Equity Income Fund’s (the “fund”) Class M shares produced a total return of 16.79%, and Investor shares produced a total return of 16.54%.1 In comparison, the fund’s benchmark, the MSCI ACWI ex USA Index (the “Index”), produced a total return of 11.89% for the same period.2

International equities generally rose during the period as economic growth and easing inflationary pressures outweighed concerns regarding elevated interest rates, slowing growth in China and heightened geopolitical tensions. The fund outperformed the Index during the period, largely due to its emphasis on high-dividend-paying stocks, which were favored by the market.

The Fund’s Investment Approach

The fund seeks total return (consisting of capital appreciation and income). To pursue its goal, the fund normally invests at least 80% of its net assets, plus any borrowings for investment purposes, in equity securities. The fund normally invests substantially all of its assets in the equity securities of issuers located outside the United States and diversifies broadly among developed- and emerging-markets countries. The fund focuses on dividend-paying stocks of foreign companies, including those of emerging-markets countries. The fund may invest in the stocks of companies of any market capitalization.

We select stocks through a disciplined investment process using proprietary, quantitative computer models that analyze a diverse set of characteristics to identify and rank stocks according to earnings quality. Based on this analysis, we generally select from the higher-ranked, dividend-paying securities that we believe will continue to pay above-average dividends. We seek to overweight higher-dividend-paying stocks, while maintaining country and sector weights generally similar to those of the Index.

High-Yielding, Developed-Markets Equities Outperform

The reporting period began on a negative note, as stocks broadly retreated in September and early October 2022 in the face of elevated rates of inflation, high energy prices and geopolitical concerns regarding the war in Ukraine. In the Eurozone, annual inflation was estimated at 10.0% in September, up from 9.1% a month earlier. While economic growth remained mildly positive, signs of economic weakening raised the specter of a recession. In much of Asia, shares were further hampered by slowing growth in China due to the spread of COVID-19 infections and fears of pandemic-related lockdowns.

Equities recovered broadly beginning in mid-October as inflationary pressures eased, and economic data reassured investors that a recession was not imminent. In Europe, equities showed surprising strength, bolstered by signs of easing global inflation, despite the war in Ukraine. In Asia, shares rose as China eased the pandemic restrictions that had been constraining economic growth, although China’s growth remained subdued through the remainder of the period. Most other emerging markets exhibited mild gains as well, due to lessening inflationary pressures and declining, relative U.S. dollar values, although energy producers were hurt by weak oil prices for much of the period. Over the entire reporting period, traditionally defensive, value-oriented and dividend-paying stocks tended to outperform growth-oriented shares by a wide margin, with high-dividend-paying stocks in the Index returning approximately 18%, while low-dividend-paying stocks gained approximately 2%. The best-performing sectors in the Index included information technology and industrials, while communication services and real estate lagged. Among countries, top performers included Turkey and Greece, while Qatar and Saudi Arabia were hurt by weak oil prices.

Gains Driven by a Focus on Dividend-Paying Stocks

The fund captured the outperformance of high-dividend-paying stocks, in line with its benchmark-driven, risk-controlled focus on maximizing dividend-yield exposure. Returns relative to the Index further benefited from good stock selection in industrials and financials, while disappointing selection in communication services and consumer staples detracted. From a country perspective, the fund saw strong returns from stock selections in Japan and Hong Kong, while positions in the UK and Denmark lagged. While individual holdings played only a minor role in the fund’s outperformance, given its broadly diversified profile, notably strong performers included Japan-based industrial conglomerate Sumitomo Corp., which posted strong earnings with inflation fueling strengthening margins; France-based global property and casualty insurance provider AXA SA, which reported better-than-expected earnings and revenues while exhibiting strong pricing power and repurchasing shares; and Ford Otomotiv Sanayi SA, a Turkey-based manufacturer, importer and distributor of Ford trucks, automobiles and commercial vehicles, which beat earnings expectations on strong domestic performance and issued improved guidance. Notably weak holdings included UK-based British American Tobacco PLC, which came under pressure from the increasing likelihood of a UK ban on disposable vaping products, and wireless telecommunications services provider Spark New Zealand Ltd., which declined after providing disappointing guidance and issuing uncharacteristically soft financial results.

Maintaining a Diversified, Risk-Controlled Portfolio

As of August 31, 2023, with inflation subsiding and economic growth remaining broadly positive despite the pressure from high interest rates, most observers now anticipate a soft landing, in which central banks manage to bring inflation under control without precipitating a global recession. However, risks remain as the impacts of high—and still increasing—interest rates continue to work their way through the real economy. Geopolitical risks remain a cause for concern as well, with Russia’s war in Ukraine ongoing and tensions simmering between the Western world and China over several issues. In this environment, we believe the fund is well positioned to provide investors with diversified access to international, high-dividend-paying stocks that reflect the geographic, sector and market-capitalization characteristics of the Index. While the fund maintains weightings similar to those of the Index, it does hold modest overweights and underweights in some areas. As of the

12

end of the reporting period, sector overweights included communication services and financials, while underweights included materials and industrials. Country overweights included Taiwan and Australia, with underweights in France and Denmark.

September 15, 2023

1 Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost.

2 Source: Lipper Inc. — Reflects reinvestment of net dividends and, where applicable, capital gain distributions. The MSCI ACWI ex USA Index captures large- and mid-cap representation across developed market (DM) countries (excluding the U.S.) and emerging market (EM) countries. Investors cannot invest directly in any index.

Equities are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

The fund may, but is not required to, use derivative instruments. A small investment in derivatives could have a potentially large impact on the fund’s performance. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in the underlying assets.

13

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

For the period from September 1, 2022, through August 31, 2023, as provided by Alicia Levine of BNY Mellon Investment Adviser, Inc., Primary Portfolio Manager responsible for investment allocation decisions.

Market and Fund Performance Overview

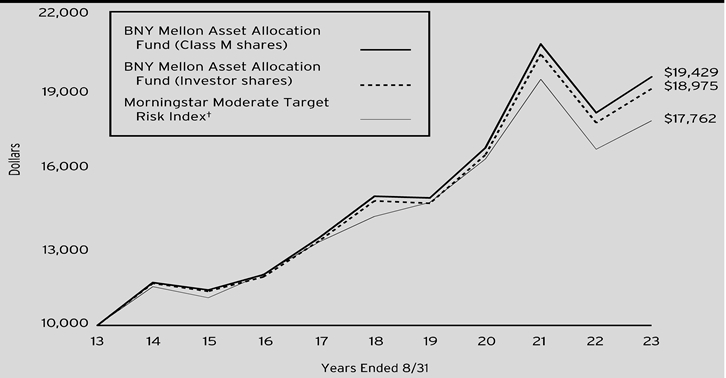

For the 12-month period ended August 31, 2023, BNY Mellon Asset Allocation Fund (the “fund”) produced a total return of 7.53% for Class M shares, and 7.29% for Investor shares.1 In comparison, the fund’s benchmark, the Morningstar Moderate Target Risk Index (the “Index”), produced a total return of 6.48% for the same period.2

Global equities gained ground during the reporting period as inflationary pressures eased, the U.S. Federal Reserve (the “Fed”) reduced the pace of interest-rate hikes and economic growth remained positive. Bonds produced mixed returns under pressure from rising interest rates. The fund outperformed the Index, largely due to the positive impact from fixed-income allocations and manager selection.

The Fund’s Investment Approach

The fund seeks long-term growth of principal in conjunction with current income. The fund may invest in both individual securities and other investment companies, including other BNY Mellon funds, funds in the BNY Mellon Investment Adviser, Inc. Family of Funds and unaffiliated open-end funds, closed-end funds and exchange-traded funds (collectively, the “underlying funds”). To pursue its goal, the fund currently intends to allocate its assets, directly and/or through investment in the underlying funds, to gain investment exposure to the following asset classes: large-cap equities, small-cap and mid-cap equities, developed international and global equities, emerging-markets equities, investment grade bonds, high yield bonds, emerging-markets debt, diversifying strategies and money market instruments.

BNY Mellon Investment Adviser, Inc. (“BNYM Investment Adviser”) allocates the fund’s investments among these asset classes using fundamental and quantitative analysis and its outlook for the economy and financial markets. The underlying funds are selected by BNYM Investment Adviser based on its investment objectives and management policies, portfolio holdings, risk/reward profiles, historical performance and other factors, including the correlation and covariance among the underlying funds.

Easing Inflation and Strong Economic Conditions Bolster Stocks and Bonds

Stocks and bonds broadly retreated in September and early October 2022 in the face of high levels of inflation and sharply rising interest rates. Although U.S. inflation appeared to peak before the period began, topping at over 9% in June, rates remained over 8% at the start of the period, well above the 2% target adopted by the Fed. The Fed responded with its third consecutive 0.75% increase to the federal funds rate in September, while indicating that additional increases were likely, increasing concerns of a possible recession. In Europe, inflation-related worries were exacerbated by Russia’s ongoing war in Ukraine, which increased energy prices and heightened regional geopolitical instability. In Asia, shares were further hampered by slowing growth in China due to the country’s “zero-COVID-19” lockdowns.

Equities and fixed-income assets began recovering broadly beginning in mid-October as inflationary pressures eased, and economic data reassured investors that a recession was not imminent. In the United States, inflation dropped steadily, dipping below 3% in June 2023 and remaining under 4% through the end of the period. While the Fed continued to hike rates, the scale of increases eased, with a fourth 0.75% increase in November, followed by a 0.50% increase in December and four subsequent 0.25% increases in 2023. At the same time, the U.S. economy continued to grow, bolstered by strong consumer spending, rising wages and robust levels of employment. Although European economic conditions proved less robust than those in the United States, European economies showed surprising strength despite the war in Ukraine, with warmer-than-expected winter temperatures limiting the impact of the conflict on energy prices. In addition, China began to emerge from pandemic-related lockdowns, although economic growth in the world’s second-largest economy remained sluggish. Generally, equity market returns remained positive despite a downturn in February and early March driven by renewed inflationary concerns, rising geopolitical tensions in Asia and concerns regarding a few inflation-driven regional bank failures in the United States. Over the entire reporting period, large-cap growth stocks tended to outperform value-oriented and smaller-capitalization shares. Bond prices improved as well from October through the end of the period, although fixed-income securities generated mixed returns overall. Shorter-duration fixed-income instruments tended to outperform their longer-duration counterparts, and lower-credit-rated securities generally outperformed higher credit ratings.

Fixed-Income Positions Enhance Relative Returns

While most of the fund’s total gains were driven by equity positions, particularly in the large-cap blend category, fixed-income positions provided the greatest contributions to relative performance, with positive attribution split between manager selection and asset allocation. From a manager selection perspective, investment grade fixed-income positions led relative returns, with nearly equal contributions from corporate bond and intermediate bond positions. From an asset allocation point of view, relative returns were bolstered by high yield bond positions.

The most significant detractors from relative performance came from equity positions, led by emerging-markets equity, followed by small-cap blend. Virtually all of the fund’s negative equity contribution resulted from asset allocation, with manager selection having little net effect.

We made several changes to the fund’s composition during the period. In September 2022, we reduced allocations to small-cap value and small-cap growth stocks, while increasing exposure to small-cap multi-strategy and short-term U.S. government securities. In January 2023, we used some of the fund’s cash to increase exposure to investment grade fixed-income direct and international equity, while selling a portion of the fund’s large-cap tax-managed equity to increase positions in income stock and, to a lesser extent, emerging-markets equity. In June, we sold positions in income stock and mid-cap equity multi-strategy,

14

while buying positions in research growth. Finally, in July, we trimmed positions in short-term U.S. government fixed income, small-cap equity multi-strategy and floating-rate income, while increasing large-cap tax-managed equity.

Adopting a More Constructive Outlook

In light of emerging economic developments, we have become more constructive on the market’s near- and mid-term prospects. Specifically, we see growing signs that the slowdown in earnings and economic activity is stabilizing, and leading indicators are turning higher. However, U.S. growth is diverging from the rest of world, leading to a stronger U.S. dollar, which could drive risk-off sentiment. From a monetary policy perspective, we see little likelihood of further substantial Fed rate increases. While rates may remain high for an extended period of time, the potential shock to the system has diminished. Nevertheless, elevated investor sentiment and equity price/earnings ratios could become near-term headwinds in an environment of high rates. Key risks over the coming months include China’s slowdown, the impact of credit tightening (which typically leads to lower earnings and growth) and the potential for another uptick in inflation if service prices remain high, and oil prices continue to increase.

As of the end of the period, the fund has allocated 64.3% of assets to equities and 33.1% to fixed income. The fund’s largest allocations by category are to large-cap blend equity and investment grade fixed income, while its smallest allocations by category are to alternatives and emerging-markets equity. By manager, the fund’s largest allocations are to tax-managed large-cap equity, investment grade fixed-income direct and intermediate bond, while its smallest allocations by manager are to small-cap growth, developed-markets REITs (real estate investment trusts), small-cap value, high yield and floating-rate income.

September 15, 2023

1 Total return includes reinvestment of dividends and any capital gains paid. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. The fund’s return reflects the absorption of certain fund expenses by BNY Mellon Investment Adviser, Inc. pursuant to an agreement in effect through December 30, 2023, at which time it may be extended, modified or terminated. Had these expenses not been absorbed, returns would have been lower.

2 Source: Morningstar Inc. — Morningstar Moderate Target Risk Index serves as a benchmark to help with target-risk, mutual fund selection and evaluation by offering an objective yardstick for moderate performance comparison. Investors cannot invest directly in any index.

Equities are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

Bonds are subject generally to interest-rate, credit, liquidity and market risks, to varying degrees, all of which are more fully described in the fund’s prospectus. Generally, all other factors being equal, bond prices are inversely related to interest-rate changes, and rate increases can cause price declines.

The underlying funds’ underlying strategies may use derivative instruments. A small investment in derivatives could have a potentially large impact on the fund’s performance. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in the underlying assets.

15

FUND PERFORMANCE (Unaudited)

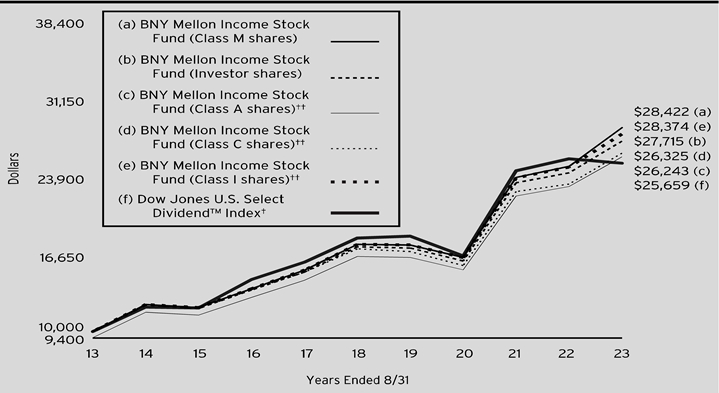

Comparison of change in value of a $10,000 investment in Class M shares, Investor shares, Class A shares, Class C shares and Class I shares of BNY Mellon Income Stock Fund with a hypothetical investment of $10,000 in the Dow Jones U.S. Select DividendTM Index (the “Index”).

† Source: Lipper Inc.

†† The total return figures presented for Class A shares, Class C shares and Class I shares of the fund reflect the performance of the fund’s Class M shares for the period prior to 5/31/16 (the inception date for Class A shares, Class C shares and Class I shares) adjusted to reflect each share class’ applicable sales charges, and the performance for the fund’s Class A shares, Class C shares and Class I shares thereafter.

Past performance is not predictive of future performance.

The above graph compares a hypothetical $10,000 investment made in each of the Class M shares, Investor shares, Class A shares, Class C shares and Class I shares of BNY Mellon Income Stock Fund on 8/31/13 to a hypothetical investment of $10,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account all applicable fees and expenses on all classes. The Index is defined as all dividend-paying companies in the Dow Jones U.S. Index, excluding REITs, that have a non-negative historical five-year dividend-per-share growth rate, a five-year average dividend coverage ratio of greater than or equal to 167%, paid dividends in each of the previous five years, non-negative trailing 12-month earnings-per-share (EPS), a float-adjusted market capitalization of at least US$1 billion, and three-month average daily trading volume of 200,000 shares. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

16

Comparison of change in value of a $1,000,000 investment in Class Y shares of BNY Mellon Income Stock Fund with a hypothetical investment of $1,000,000 in the Dow Jones U.S. Select DividendTM Index (the “Index”).

† Source: Lipper Inc.

†† The total return figures presented for Class Y shares for the period prior to 5/31/16 (the inception date for Class Y shares) adjusted to reflect each share class’ applicable sales charges, and the performance for the fund’s Class Y shares thereafter.

Past performance is not predictive of future performance.

The above graph compares a hypothetical investment of $1,000,000 made in Class Y shares of BNY Mellon Income Stock Fund on 8/31/13 to a hypothetical investment of $1,000,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account all applicable fees and expenses on Class Y shares. The Index is defined as all dividend-paying companies in the Dow Jones U.S. Index, excluding REITs, that have a non-negative historical five-year dividend-per-share growth rate, a five-year average dividend coverage ratio of greater than or equal to 167%, paid dividends in each of the previous five years, non-negative trailing 12-month earnings-per-share (EPS), a float-adjusted market capitalization of at least US$1 billion, and three-month average daily trading volume of 200,000 shares. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

17

FUND PERFORMANCE (Unaudited) (continued)

| | | | | | | | |

Average Annual Total Returns as of 8/31/2023 | | | |

| Inception Date | 1 Year | 5 Years | 10 Years |

Class M shares | 1/1/85 | 12.06% | 9.43% | 11.01% |

Investor shares | 7/11/01 | 11.93% | 9.17% | 10.73% |

Class A shares | | | | |

with maximum sales charge (5.75%) | 5/31/16 | 5.30% | 7.79% | 10.13%†† |

without sales charge | 5/31/16 | 11.72% | 9.08% | 10.78%†† |

Class C shares | | | | |

with applicable redemption charge† | 5/31/16 | 10.12% | 8.27% | 10.16%†† |

without redemption | 5/31/16 | 11.00% | 8.27% | 10.16%†† |

Class I shares | 5/31/16 | 12.16% | 9.40% | 10.99%†† |

Class Y shares | 5/31/16 | 12.09% | 9.41% | 11.00%†† |

Dow Jones U.S. Select Dividend TM Index | | -1.56% | 6.53% | 9.88% |

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the date of purchase.

†† The total return performance figures presented for Class A shares, Class C shares, Class I shares and Class Y shares of the fund reflect the performance of the fund’s Class M shares for the period prior to 5/31/16 (the inception date for Class A shares, Class C shares, Class I shares and Class Y shares) adjusted to reflect each share class’ applicable sales charges, and the performance for the fund’s Class A shares, Class C shares, Class I shares and Class Y shares thereafter.

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon redemption. Current performance may be lower or higher than the performance quoted. Go to www.im.bnymellon.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graphs and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

18

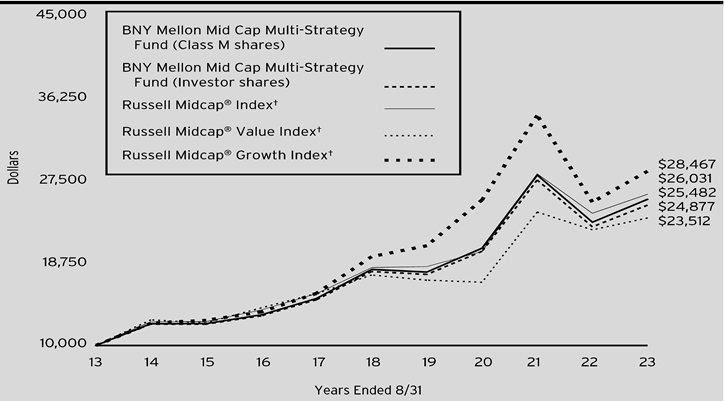

Comparison of change in value of a $10,000 investment in Class M shares and Investor shares of BNY Mellon Mid Cap Multi-Strategy Fund with a hypothetical investment of $10,000 in each of the Russell Midcap® Index, Russell Midcap® Value Index and Russell Midcap® Growth Index.

| | | | | |

Average Annual Total Returns as of 8/31/2023 | | | |

| | 1 Year | 5 Years | 10 Years |

Class M shares | | 10.50% | 7.13% | 9.81% |

Investor shares | | 10.18% | 6.88% | 9.54% |

Russell Midcap® Index | | 8.38% | 7.35% | 10.04% |

Russell Midcap® Value Index | | 5.65% | 6.12% | 8.93% |

Russell Midcap® Growth Index | | 13.00% | 7.95% | 11.03% |

† Source: Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a $10,000 investment made in Class M shares and Investor shares of BNY Mellon Mid Cap Multi-Strategy Fund on 8/31/13 to a hypothetical investment of $10,000 made in each of the (1) the Russell Midcap® Index, (2) the Russell Midcap® Value Index and (3) the Russell Midcap® Growth Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account all applicable fees and expenses for Class M shares and Investor shares. The Russell Midcap® Index measures the performance of the mid-cap segment of the U.S. equity universe. The Russell Midcap® Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Russell Midcap® Index represents approximately 31% of the total market capitalization of the Russell 1000 companies. The Russell Midcap® Index is constructed to provide a comprehensive and unbiased barometer for the mid-cap segment. The index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap opportunity set. The Russell Midcap® Value Index measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies that are considered more value-oriented relative to the overall market as defined by Russell’s leading style methodology. The Russell Midcap® Value Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap value market. The index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap value market. The Russell Midcap® Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with higher growth earning potential as defined by Russell’s leading style methodology. The Russell Midcap® Growth Index is constructed to provide a comprehensive and unbiased barometer of the mid-cap growth market. The index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true mid-cap growth market. Unlike a mutual fund, the indices are not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon redemption. Current performance may be lower or higher than the performance quoted. Go to www.im.bnymellon.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

19

FUND PERFORMANCE (Unaudited) (continued)

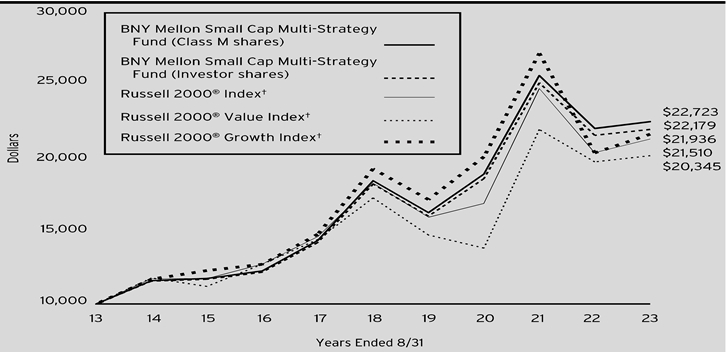

Comparison of change in value of a $10,000 investment in Class M shares and Investor shares of BNY Mellon Small Cap Multi-Strategy Fund with a hypothetical investment of $10,000 in each of the Russell 2000® Index, Russell 2000® Value Index and Russell 2000® Growth Index.

| | | | | |