Exhibit 1.3

SIERRA WIRELESS, INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

DATED March 7, 2013

MANAGEMENT’S DISCUSSION AND ANALYSIS

Table of Contents

MANAGEMENT’S DISCUSSION AND ANALYSIS | 1 |

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS | 2 |

OVERVIEW | 3 |

Business Overview | 3 |

Strategy | 4 |

Annual Overview - Financial Highlights | 5 |

Outlook | 10 |

Disposition of AirCard Business | 11 |

CONSOLIDATED ANNUAL RESULTS OF OPERATIONS | 13 |

Year ended December 31, 2012 Compared to Year Ended December 31, 2011 | 13 |

Year ended December 31, 2011 Compared to Year Ended December 31, 2010 | 16 |

SEGMENTED INFORMATION | 18 |

FOURTH QUARTER OVERVIEW | 19 |

SUMMARY OF QUARTERLY RESULTS OF OPERATIONS | 21 |

LIQUIDITY AND CAPITAL RESOURCES | 22 |

NON-GAAP FINANCIAL MEASURES | 25 |

OFF-BALANCE SHEET ARRANGEMENTS | 27 |

TRANSACTIONS BETWEEN RELATED PARTIES | 27 |

CRITICAL ACCOUNTING POLICIES AND ESTIMATES | 28 |

OUTSTANDING SHARE DATA | 33 |

IMPACT OF ACCOUNTING PRONOUNCEMENTS AFFECTING FUTURE PERIODS | 33 |

DISCLOSURE CONTROLS | 33 |

INTERNAL CONTROL OVER FINANCIAL REPORTING | 34 |

LEGAL PROCEEDINGS | 35 |

RISKS AND UNCERTAINTIES | 38 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) provides information for the year ended December 31, 2012, and up to and including March 7, 2013. This MD&A should be read together with our audited consolidated financial statements and the accompanying notes for the year ended December 31, 2012 (“the consolidated financial statements”). The consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). Except where otherwise specifically indicated, all amounts in this MD&A are expressed in United States dollars.

We have prepared this MD&A with reference to National Instrument 51-102 “Continuous Disclosure Obligations” of the Canadian Securities Administrators. Under the U.S./Canada Multijurisdictional Disclosure System, we are permitted to prepare this MD&A in accordance with the disclosure requirements of Canada, which requirements are different than those of the United States.

Certain statements in this MD&A constitute forward-looking statements or forward-looking information within the meaning of applicable securities laws. You should carefully read the cautionary note in this MD&A regarding forward-looking statements and should not place undue reliance on any such forward-looking statements. See “Cautionary Note Regarding Forward-Looking Statements”.

Throughout this document, references are made to certain non-GAAP financial measures that are not measures of performance under U.S. GAAP. Management believes that these non-GAAP financial measures provide useful information to investors regarding the Company’s financial condition and results of operations as they provide additional measures of its performance. These non-GAAP financial measures do not have any standardized meaning prescribed by U.S. GAAP and are therefore unlikely to be comparable to similar measures presented by other issuers. These non-GAAP financial measures are defined and reconciled to their nearest GAAP measure in “Non-GAAP Financial Measures”.

Additional information about the Company, including our most recent consolidated financial statements and our Annual Information Form, is available on our website at www.sierrawireless.com, or on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Cautionary Note Regarding Forward-looking Statements

Certain statements and information in this MD&A are not based on historical facts and constitute forward-looking statements or forward-looking information within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and Canadian securities laws (“forward-looking statements”), including our business outlook for the short and longer term and our strategy, plans and future operating performance. Forward-looking statements are provided to help you understand our views of our short and longer term prospects. We caution you that forward-looking statements may not be appropriate for other purposes. We will not update or revise our forward-looking statements unless we are required to do so by securities laws. Forward-looking statements:

· Typically include words and phrases about the future such as “outlook”, “may”, “estimates”, “intends”, “believes”, “plans”, “anticipates” and “expects”;

· Are not promises or guarantees of future performance. They represent our current views and may change significantly;

· Are based on a number of material assumptions, including those listed below, which could prove to be significantly incorrect:

· Our ability to develop, manufacture and sell new products and services that meet the needs of our customers and gain commercial acceptance;

· Our ability to continue to sell our products and services in the expected quantities at the expected prices and expected times;

· Expected cost of goods sold;

· Expected component supply constraints;

· Our ability to “win” new business;

· Expected deployment of next generation networks by wireless network operators;

· Our operations are not adversely disrupted by component shortages or other development, operating or regulatory risks; and

· Expected tax rates and foreign exchange rates.

· Are subject to substantial known and unknown material risks and uncertainties. Many factors could cause our actual results, achievements and developments in our business to differ significantly from those expressed or implied by our forward-looking statements, including, without limitation, the following factors which are discussed in greater detail under “Risks and Uncertainties” and in our other regulatory filings with the U.S. Securities and Exchange Commission (the “SEC”) in the United States and the provincial securities commissions in Canada.

· We may experience higher than anticipated costs; disruption of, and demands on, our ongoing business; diversion of management’s time and attention; adverse effects on existing business relationships with suppliers and customers and employee issues in connection with the divestiture of the AirCard assets and operations;

· Actual sales volumes or prices for our products and services may be lower than we expect for any reason including, without limitation, continuing uncertain economic conditions, price and product competition, different product mix, the loss of any of our significant customers, or competition from new or established wireless communication companies;

· The cost of products sold may be higher than planned or necessary component supplies may not be available, are delayed or are not available on commercially reasonable terms;

· We may be unable to enforce our intellectual property rights or may be subject to litigation that has an adverse outcome;

· The development and timing of the introduction of our new products may be later than we expect or may be indefinitely delayed; and

· Transition periods associated with the migration to new technologies may be longer than we expect.

Investors are cautioned not to place undue reliance on these forward-looking statements. No forward-looking statement is a guarantee of future results.

OVERVIEW

On January 28, 2013, we announced a definitive agreement for the sale of substantially all of the assets and operations related to our AirCard business. The transaction is expected to close in early April 2013, subject to customary closing conditions.

In accordance with U.S. GAAP, assets and liabilities associated with the sale have been recorded as “held for sale” in our consolidated balance sheet as at December 31, 2012 and the results of operations of the AirCard business as discontinued operations in our consolidated statements of operations for the three years ended December 31, 2012. The selected financial information has been retrospectively adjusted to reflect the presentation of the AirCard business as discontinued operations (refer to the section on “Disposition of AirCard business”).

Business Overview

Sierra Wireless Inc. (“Sierra Wireless” or the “Company”) is a global leader in wireless technology and solutions for the machine-to-machine (“M2M”) and connected device markets. We offer a comprehensive portfolio of value added wireless devices and related software products that dramatically simplify the integration of wireless communications and enable customers to more easily build, deploy and operate their M2M applications.

Our continuing business includes our AirPrime™ Embedded Wireless Modules, AirLink™ Intelligent Gateways, and AirVantage™ M2M Cloud products. Effective August 1, 2012, our continuing business also includes the M2M business that we acquired from Sagemcom (refer to the section on “Acquisition of M2M business of Sagemcom”). Sagemcom products are part of the AirPrime portfolio.

· AirPrime Embedded Wireless Modules - AirPrime Embedded Wireless Modules are used to wirelessly enable products and solutions made by our OEM customers. Our M2M OEM customers cover a broad range of industries, including automotive, networking equipment, energy, security, sales and payment, industrial control and monitoring, fleet management, field service, healthcare, and consumer electronics. Our PC OEM customers integrate AirPrime modules into notebooks, tablets, and other mobile computing devices, to provide mobile broadband connectivity. The AirPrime product portfolio spans 2G, 3G and 4G LTE technologies and includes

robust remote device management capability, as well as supports on-board embedded applications with the OpenATÒ Application Framework.

· AirLink Intelligent Gateways - AirLink Intelligent Gateways are rugged, industrial-grade wireless terminals for M2M and mobile applications. They are designed for use in mission critical deployments, where reliability and security are essential, and are sold to public safety, transportation, field service, energy, industrial, and financial organizations around the world. The AirLink product portfolio includes 2G, 3G and 4G LTE terminals, supported by cloud-based remote device management tools. AirLink gateways can be easily configured for almost any type of application, and also support on-board embedded applications with the ALEOS Application Framework.

· AirVantage M2M Cloud - The AirVantage M2M Cloud provides a secure, scalable, device-to-cloud infrastructure for M2M applications. The AirVantage Enterprise Platform can be used to collect, transmit, and store machine data, and process and schedule events, from any number of devices, across any network operator around the world. M2M solution developers can use the latest cloud API standards to quickly integrate that machine data with their own enterprise applications and back-end systems. The AirVantage Management Service can be used to centrally deploy and monitor M2M devices, including configuring device settings, delivering firmware and embedded application updates, and administering airtime subscriptions across global networks making managing a million wireless devices as easy as managing ten.

Strategy

According to Machina Research, an independent research firm, the number of connected devices in operation was 1.4 billion in 2011. This number is expected to grow significantly in the coming years to over 12 billion by 2020. Adoption of M2M and connected device solutions is driven by a number of enablers, such as lower wireless connectivity costs, higher wireless connection speeds, new devices and tools to simplify development of M2M applications, and increased focus and investment from network operators, infrastructure vendors and other wireless ecosystem players. Key benefits for customers deploying M2M solutions, such as the ability to generate new revenue streams, improve cost efficiencies through remote access to data, gather important customer and market intelligence, as well as regulatory and security requirements, are also driving demand for M2M connectivity.

Management believes these factors create a substantial growth opportunity for the Company. We are the global market share leader in M2M embedded devices today, with 34% of the global M2M embedded wireless module market (source: ABI Research, 2011). Going forward, we plan to build on this leadership position and expand our business across the value chain in M2M and connected device solutions. We intend to:

· Complete our transformation into a pure play leader in M2M and connected device solutions;

· Maintain our leadership position as we continue to innovate — making it easier, faster, and cheaper for our customers to build, deploy and manage their M2M solutions;

· Drive organic revenue growth and improve profitability by leveraging our cost structure;

· Build on organic investments in the development of value-added services and solutions to provide more value to customers and improve margins; and

· Accelerate revenue and profitability growth through an active acquisition strategy focused on M2M opportunities.

Annual Overview — Financial highlights

Revenue and profitability in 2012 improved significantly compared to 2011. This was primarily driven by significant growth in M2M sales, including contribution from the M2M business of Sagemcom acquired on August 1, 2012, and strong growth in sales to PC OEMs. This revenue growth, combined with improved gross margins due to product cost reductions and favourable shifts in product mix, drove the significant improvement in profitability year-over-year.

Financial highlights for year ended December 31, 2012:

Continuing operations

· Revenue of $397.3 million, up 19.3%, compared to $333.2 million in 2011

· Gross margin improved to 31.5% in 2012, compared to 30.5% in 2011

· Non-GAAP operating earnings were $0.9 million, up from a loss of $22.4 million in 2011

Continuing and discontinued operations

· Revenue was $644.2 million, 11.4% year-over-year growth

· Non-GAAP operating earnings were $36.3 million, up significantly from $2.9 million in 2011

· Net earnings of $27.2 million and diluted earnings per share of $0.88, improved significantly from net loss of $29.3 million and loss per share of $0.94 in 2011. Net earnings, including discontinued operations, in 2012 included a favorable income tax adjustment associated with the pending sale of the AirCard business. Net loss in 2011 included an asset impairment charge of $11.2 million related to a write-down of an intangible asset.

· Non-GAAP net earnings of $33.4 million, or $1.08 per diluted share, in 2012, up from $3.6 million, or $0.12 per diluted share, in 2011

· Cash flow from operations of $40.5 million in 2012, up from $23.7 million in 2011

Selected Annual Financial information:

(in thousands of U.S. dollars, except where otherwise stated)

|

| 2012 |

| 2011 (2) |

| 2010 (2) |

| |||

Statement of Operations data: |

|

|

|

|

|

|

| |||

Revenue (GAAP and Non-GAAP) |

| $ | 397,321 |

| $ | 333,175 |

| $ | 358,005 |

|

|

|

|

|

|

|

|

| |||

Gross Margin |

|

|

|

|

|

|

| |||

- GAAP |

| $ | 125,274 |

| $ | 101,740 |

| $ | 121,406 |

|

- Non-GAAP (1) |

| 125,578 |

| 102,125 |

| 121,897 |

| |||

|

|

|

|

|

|

|

| |||

Gross Margin % |

|

|

|

|

|

|

| |||

- GAAP |

| 31.5 | % | 30.5 | % | 33.9 | % | |||

- Non-GAAP (1) |

| 31.6 | % | 30.7 | % | 34.0 | % | |||

|

|

|

|

|

|

|

| |||

Earnings (loss) from operations |

|

|

|

|

|

|

| |||

- GAAP |

| $ | (22,206 | ) | $ | (54,253 | ) | $ | (42,717 | ) |

- Non-GAAP (1) |

| 898 |

| (22,390 | ) | (10,904 | ) | |||

|

|

|

|

|

|

|

| |||

Net earnings (loss) from continuing operations |

|

|

|

|

|

|

| |||

- GAAP |

| $ | (4,202 | ) | $ | (50,710 | ) | $ | (34,973 | ) |

- Non-GAAP (1) |

| (444 | ) | (18,681 | ) | (1,206 | ) | |||

|

|

|

|

|

|

|

| |||

Net earnings from discontinued operations |

|

|

|

|

|

|

| |||

- GAAP |

| $ | 31,401 |

| $ | 21,338 |

| $ | 20,174 |

|

- Non-GAAP (1) |

| 33,796 |

| 22,289 |

| 21,125 |

| |||

|

|

|

|

|

|

|

| |||

Net earnings (loss) attributable to the Company |

|

|

|

|

|

|

| |||

- GAAP |

| $ | 27,199 |

| $ | (29,315 | ) | $ | (14,541 | ) |

- Non-GAAP (1) |

| 33,352 |

| 3,633 |

| 19,996 |

| |||

|

|

|

|

|

|

|

| |||

Share and per share data: |

|

|

|

|

|

|

| |||

Basic and diluted earnings (loss) per share (in dollars) - GAAP |

|

|

|

|

|

|

| |||

- GAAP |

| $ | 0.88 |

| $ | (0.94 | ) | $ | (0.47 | ) |

- Non-GAAP (1) |

| $ | 1.08 |

| $ | 0.12 |

| $ | 0.64 |

|

|

|

|

|

|

|

|

| |||

Common shares (in thousands) |

|

|

|

|

|

|

| |||

At period-end |

| 30,592 |

| 31,307 |

| 31,223 |

| |||

Weighed average - basic and diluted |

| 30,788 |

| 31,275 |

| 31,083 |

| |||

|

|

|

|

|

|

|

| |||

Balance sheet data: |

|

|

|

|

|

|

| |||

Cash and cash equivalents and short-term investments |

| $ | 63,646 |

| $ | 110,722 |

| $ | 111,848 |

|

Total assets |

| 464,763 |

| 422,887 |

| 469,568 |

| |||

Total long-term liabilities |

| 26,826 |

| 25,379 |

| 26,130 |

| |||

(1) Non-GAAP results exclude the impact of stock-based compensation expense, acquisition amortization, impairment, acquisition and disposition costs, integration costs, restructuring costs, foreign exchange gains or losses on foreign currency contracts and translation of balance sheet accounts, and certain tax adjustments. Refer to the section on “Non-GAAP financial measures” for additional details.

(2) Selected financial information for fiscal years 2011 and 2010 have been retrospectively adjusted to reflect the presentation of the AirCard business as discontinued operations.

See discussion under “Consolidated Annual Results of Operations” for factors that have caused period to period variations.

Acquisition of M2M business of Sagemcom

On August 1, 2012, we completed the acquisition of the M2M business of Sagemcom. The acquisition included the purchase of substantially all of the assets of the M2M business of Sagemcom for €44.9 million ($55.2 million) in cash consideration plus assumed liabilities of €3.9 million ($4.8 million).

Sagemcom is a France-based technology company active in broadband, telecom, energy, and document management. Its M2M business included 2G and 3G wireless modules, as well as industry-leading rugged terminals for railway applications. This acquisition extends our global leadership position in the growing M2M market as it provides us with a significantly enhanced market position in key segments, including payment, transportation and railways, as well as new geographical expansion into Brazil.

The acquired business’ results of operations and estimated fair value of assets acquired and liabilities assumed have been included in our consolidated financial statements from the date of acquisition, August 1, 2012. The M2M business of Sagemcom contributed $20.1 million to our consolidated revenues during 2012.

Closure of Newark, California facility

Our Newark, California facility was closed, effective December 31, 2012, to drive greater efficiency and leverage. Our AirLink marketing, research and development, and customer support activities were transferred primarily to our Richmond, British Columbia facilities and our manufacturing facilities were transferred to our manufacturing partners in Suzhou, China. We recorded $2.0 million in total severance and other costs associated with this initiative during 2012.

Other key business highlights for the year ended December 31, 2012 include:

AirPrime Embedded Wireless Modules

· We announced that PSA Peugeot Citroen, in collaboration with Bouygues Telecom, selected the Company to provide an innovative 3G USB key that powers the new Peugeot Connect Apps system. Designed specifically for automotive use, this key incorporates 3G wireless connectivity, global positioning, and advanced processing capabilities in a compact, plug-and-play form factor. When the 3G key is plugged into the vehicle, it provides the driver with real-time information on traffic conditions, weather, and navigation, as well as information about services nearby.

· We announced the availability of the industry leading Open AT Application Framework, which is used in millions of our 2G products, on select 3G AirPrime embedded wireless modules, including the SL808x. This allows customers to build M2M application software once and deploy it in nearly any market worldwide on 2G or 3G networks — significantly lowering overall system cost and accelerating time to market.

· We announced the launch of the AirPrime Q2698 embedded wireless module, an important addition to the AirPrime Q Series. The AirPrime Q2698 provides our AirPrime Q Series customers with a seamless migration path from 2G to 3G, using the same hardware platform and embedded applications they had developed for earlier products. In addition, the AirPrime Q2698 is compatible with networks worldwide, making it ideal for global deployments.

· We introduced the AirPrime SL9090, a new, multimode product in the AirPrime SL Series of compact, industrial-grade embedded wireless modules. The multimode module gives device manufacturers the ability to operate on networks that use either HSPA+ or EV-DO cellular standards with a single product design. It is designed for use in fixed or mobile M2M deployments in the industrial, field service, energy, networking and transportation sectors. It has design and operational characteristics that make it particularly well-suited for use in harsh environments. In December, the AirPrime SL9090 was named among the Best of 2012 by Electronics Design Magazine.

· We introduced our second generation of 4G LTE AirPrime embedded wireless modules for notebooks, ultraportable notebooks, and tablets. The six new additions to the AirPrime MC Series and EM Series support 4G LTE networks worldwide and are compatible with the Windows® 8 operating system. All of the new MC and EM Series modules are optimized for low power consumption, to enable longer battery life in their host devices. The AirPrime EM7355, AirPrime EM7305, and AirPrime EM7330 are the first AirPrime modules built to the new PCI Express M.2 module standard, making them even thinner and smaller than the AirPrime EM7700 module introduced earlier in the year. Each module offers multi-operator LTE support with sets of frequency bands for specific regions — one for North America, one for EMEA and Australia, and one for Japan.

· We unveiled the world’s thinnest 4G LTE embedded wireless module. The AirPrime EM7700 is only 2.5 millimeters thick and is designed for use in ultraportable notebooks, tablets, and other devices where thickness is a critical design constraint. We are working with leading OEMs to integrate the AirPrime EM7700 into a variety of connected devices.

· Panasonic Corporation selected our AirPrime MC series embedded wireless modules to provide 4G LTE mobile-broadband connectivity for its new rugged Toughpad A1 tablet in North America.

· Beeldhorloge (Timer B.V.), based in the Netherlands, selected our AirPrime embedded wireless module to provide wireless connectivity for its Pictowatch, which is designed to assist individuals with cognitive disorders in managing daily routines.

AirLink Intelligent Gateways

· We announced that our AirLink GX440 4G LTE rugged wireless gateway received certification on both the Verizon 4G LTE and AT&T 4G LTE networks. The AirLink GX440 delivers the durability and high bandwidth required by applications such as high-quality wireless video surveillance, multi-data stream connections to branch locations, and mobile office applications for public safety and field service activities.

· We released the ALEOS Application Framework, which enables our customers to create customized embedded applications that run on AirLink intelligent gateways. Available first in our AirLink GX400 and AirLink GX440 gateways, the ability to run applications directly on the AirLink devices provides important cost and operational advantages for our customers.

AirVantage M2M Cloud Platform

· We launched the next-generation of our AirVantage M2M Cloud, a faster, more cost-effective way to build, deploy, and manage large M2M applications. The AirVantage M2M Cloud provides secure two-way communication between connected devices and the enterprise, enabling innovation in products, services, and revenue streams. In conjunction with this new release of AirVantage, we joined the Amazon Web Services Partner Network as an APN Technology Partner. This collaboration with Amazon will make it easy for customers to use the AirVantage APIs to build M2M applications that run seamlessly on the Amazon Web Services cloud infrastructure. The joint solution eliminates the need for any on-premise IT infrastructure and further accelerates time-to-market and improving scalability.

· We announced that Nestle Nespresso SA, the pioneer and market leader in high-quality portioned premium coffee, selected Sierra Wireless to provide a comprehensive M2M cloud platform and hardware solution for remote connectivity and monitoring within its range of professional coffee machines.

· We have successfully integrated AirVantage subscription management with eight additional network operators during the year, enabling multi-operator provisioning on a global basis. Through a common interface, our customers can securely access each operator’s activation infrastructure to perform activation/deactivation, billing plan management and subscription life cycle management for their M2M solution.

Outlook

In the first quarter of 2013, we expect revenue to be down sequentially following the exceptionally strong fourth quarter of 2012. We expect gross margin to be similar or slightly lower than fourth quarter 2012 levels, and operating expenses to increase as a result of higher new product certification costs combined with the negative impact of a strengthening Euro. Looking forward to the second quarter of 2013, we expect a return to solid sequential and year-over-year revenue growth and modest profitability. As a result of the expected sale of the AirCard business, Sierra Wireless will have a cost structure to support higher revenue levels. Management believes operating expenses should change relatively little as our revenue grows, resulting in improved profitability.

Macroeconomic pressure in Europe continues to dampen near-term growth in our M2M business. However, we continue to believe that the market for wireless M2M and connected devices solutions has strong growth prospects. We anticipate strong growth in the number and type of devices being wirelessly connected, driven by a number of enablers, such as lower wireless connectivity costs, higher wireless connection speeds, new devices and tools to simplify development of M2M applications, and increased focus and investment from network operators, infrastructure vendors and other wireless ecosystem players. More importantly, we see strong customer demand in many of our target verticals driven by increasing recognition of the value created by deploying M2M solutions, such as new revenue streams, improve cost efficiencies, and better customer insight.

Key factors that we expect will affect our results in the near term are the strong competitive position of our products in the market; the timely ramp up of sales of our new products recently launched or currently under development; the level of success our OEM customers achieve with sales of embedded solutions to end users; our ability to secure future design wins with both existing and new customers; wireless technology transitions and the timing of deployment of mobile broadband networks by wireless

operators; the availability of components from key suppliers; general economic conditions in the markets we serve; and seasonality in demand. We expect that product and price competition from other wireless device manufacturers will continue to play a role in the M2M embedded wireless module market. As a result of these factors, we may experience volatility in our results on a quarter to quarter basis. Gross margin percentage may fluctuate from quarter to quarter depending on product and customer mix, competitive selling prices and product costs.

Disposition of AirCard Business

On January 28, 2013, we announced a definitive agreement for the sale of substantially all of the assets and operations related to our AirCard business to Netgear, Inc. (“Netgear”) for $138 million in cash plus assumed liabilities. Netgear is a leading global provider of networking products for the home, businesses and operators. We expect to realize net cash proceeds of approximately $100 million from the divesture after related taxes, expenses and retention for the purposes of indemnification. The transaction is expected to close in early April 2013, subject to customary closing conditions. Approximately 160 employees, primarily in sales, marketing and research and development, will be transferred to Netgear, as well as certain facilities in Carlsbad, California and Richmond, British Columbia.

In accordance with U.S. GAAP, assets and liabilities associated with the sale have been recorded as “held for sale” in our consolidated balance sheet as at December 31, 2012 and the results of operations of the AirCard business as discontinued operations in our consolidated statements of operations for the three years ended December 31, 2012. The historical consolidated statements of operations and related selected financial information have been retrospectively adjusted to distinguish between continuing operations and discontinued operations.

Summarized results from discontinued operations for the years ended December 31 were as follows:

|

| 2012 |

| 2011 |

| 2010 |

| |||

Revenue |

| $ | 246,845 |

| $ | 245,010 |

| $ | 292,336 |

|

Cost of goods sold |

| 177,147 |

| 183,300 |

| 223,377 |

| |||

Gross margin |

| $ | 69,698 |

| $ | 61,710 |

| $ | 68,959 |

|

Gross margin % |

| 28.2 | % | 25.2 | % | 23.6 | % | |||

Expenses |

| 36,653 |

| 37,368 |

| 36,608 |

| |||

Earnings from operations |

| 33,045 |

| 24,342 |

| 32,351 |

| |||

Net earnings from discontinued operations |

| $ | 31,401 |

| $ | 21,338 |

| $ | 20,174 |

|

During the year ended December 31, 2012, Sprint and AT&T each accounted for more than 10% of our aggregated revenue, from continuing and discontinued operations, and on a combined basis, accounted for 25% of the aggregated revenue. During the year ended December 31, 2011, Sprint, AT&T and Telstra each accounted for more than 10% of our aggregated revenue, from continuing and discontinued operations, and on a combined basis, accounted for 36% of the aggregated revenue.

Key business highlights for discontinued operations for the year ended December 31, 2012 include:

AirCard® Mobile Broadband Devices

· We introduced our newest family of AirCard mobile hotspots for 4G LTE networks in early 2012. The new AirCard 760S, AirCard 762S, and AirCard 763S offer several feature enhancements to earlier generations, including an improved user interface, longer battery life, and expanded frequency band support across the product family, providing compatibility with most common frequency band combinations around the world. These hotspots are now available from Telstra in Australia, NetIndex in Japan, Rogers and Bell in Canada, as well as DNA in Finland.

· We launched the Sierra Wireless 4G LTE Tri-Fi Hotspot launched on the Sprint network. The 4G LTE Tri-Fi is the first and only mobile hotspot to support 4G LTE, 4G WiMAX, and 3G EVDO.

CONSOLIDATED ANNUAL RESULTS OF OPERATIONS

(in thousands of U.S. dollars, except where otherwise stated)

|

| 2012 |

| 2011 (1) |

| 2010 (1) |

| ||||||

|

|

|

| % of |

|

|

| % of |

|

|

| % of |

|

|

| $ |

| Revenue |

| $ |

| Revenue |

| $ |

| Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

| 397,321 |

| 100.0 | % | 333,175 |

| 100.0 | % | 358,005 |

| 100.0 | % |

Cost of goods sold |

| 272,047 |

| 68.5 | % | 231,435 |

| 69.5 | % | 236,599 |

| 66.1 | % |

Gross margin |

| 125,274 |

| 31.5 | % | 101,740 |

| 30.5 | % | 121,406 |

| 33.9 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales and marketing |

| 37,067 |

| 9.3 | % | 37,188 |

| 11.2 | % | 42,472 |

| 11.9 | % |

Research and development |

| 61,785 |

| 15.6 | % | 60,903 |

| 18.3 | % | 60,890 |

| 17.0 | % |

Administration |

| 32,777 |

| 8.2 | % | 33,716 |

| 10.1 | % | 36,021 |

| 10.1 | % |

Acquisition |

| 3,182 |

| 0.8 | % | — |

| 0.0 | % | — |

| 0.0 | % |

Restructuring |

| 2,251 |

| 0.6 | % | 837 |

| 0.2 | % | 7,640 |

| 2.1 | % |

Integration |

| — |

| 0.0 | % | 1,426 |

| 0.4 | % | 5,110 |

| 1.4 | % |

Impairment of intangible asset |

| — |

| 0.0 | % | 11,214 |

| 3.4 | % | — |

| — |

|

Amortization |

| 10,418 |

| 2.6 | % | 10,709 |

| 3.2 | % | 11,990 |

| 3.3 | % |

|

| 147,480 |

| 37.1 | % | 155,993 |

| 46.8 | % | 164,123 |

| 45.8 | % |

Loss from operations |

| (22,206 | ) | -5.6 | % | (54,253 | ) | -16.3 | % | (42,717 | ) | -11.9 | % |

Foreign exchange gain (loss) |

| 3,326 |

|

|

| (460 | ) |

|

| (7,000 | ) |

|

|

Other income (expense) |

| (196 | ) |

|

| 35 |

|

|

| (241 | ) |

|

|

Loss before income taxes |

| (19,076 | ) |

|

| (54,678 | ) |

|

| (49,958 | ) |

|

|

Income tax recovery |

| (14,874 | ) |

|

| (3,968 | ) |

|

| (14,985 | ) |

|

|

Net loss from continuing operations |

| (4,202 | ) |

|

| (50,710 | ) |

|

| (34,973 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net earnings from discontinued operations |

| 31,401 |

|

|

| 21,338 |

|

|

| 20,174 |

|

|

|

Net earnings (loss) |

| 27,199 |

|

|

| (29,372 | ) |

|

| (14,799 | ) |

|

|

Less: non-controlling interest |

| — |

|

|

| (57 | ) |

|

| (258 | ) |

|

|

Net earnings (loss) attributable to the Company |

| 27,199 |

|

|

| (29,315 | ) |

|

| (14,541 | ) |

|

|

Net earnings (loss) per share attributable to the Company Basic and diluted (in dollars) |

| 0.88 |

|

|

| (0.94 | ) |

|

| (0.47 | ) |

|

|

(1) Financial information for fiscal years 2011 and 2010 has been retrospectively adjusted to reflect the presentation of the AirCard business as discontinued operations.

Year Ended December 31, 2012 Compared to Year Ended December 31, 2011

Revenue

Revenue for the year ended December 31, 2012 was $397.3 million, compared to $333.2 million for the year ended December 31, 2011. The 19.3 percent year-over-year revenue increase was driven by significant growth in M2M sales, including a $20.1 million contribution from the recently acquired M2M business of Sagemcom, along with strong growth in sales to PC OEMs.

Our M2M business has a considerable revenue base in Europe and while we have experienced weakness in our European sales, revenues from other regions, particularly Asia and the Americas, have been rising.

Our geographic revenue mix for the years ended December 31, 2012 and 2011 was as follows:

Gross margin

Gross margin was 31.5% of revenue for the year ended December 31, 2012, compared to gross margin of 30.5% of revenue in 2011. The increase in gross margin was primarily related to product cost reductions, favorable product mix, and higher than average gross margin contribution from the M2M business of Sagemcom. Gross margin included $0.3 million of stock-based compensation expense in 2012 compared to $0.4 million in 2011.

Sales and marketing

Sales and marketing expenses decreased $0.1 million, or 0.3%, to $37.1 million in 2012, compared to 2011. Sales and marketing expenses included $1.2 million of stock-based compensation expense in 2012 compared to $1.1 million in 2011.

Research and development

Research and development (“R&D”) expenses increased by $0.9 million, or 1.4%, to $61.8 million in 2012, compared to 2011. The increase in R&D expenses was primarily related to the additional R&D expenses we incurred as a result of the Sagemcom acquisition, partially offset by the positive impact of foreign exchange rates.

R&D expenses in 2012 included stock-based compensation expense of $1.3 million and acquisition amortization of $5.6 million. R&D expenses in 2011 included stock-based compensation expense of $1.1 million and acquisition amortization of $6.9 million.

Administration

Administration expense decreased by $0.9 million, or 2.8%, in 2012, compared to 2011. Administration expenses included stock-based compensation expense of $3.0 million and $2.9 million in 2012 and 2011, respectively.

Acquisition

Acquisition costs related to the acquisition of the M2M business of Sagemcom were $3.2 million during 2012. Acquisition costs in 2011 were $nil.

Restructuring

Restructuring costs were $2.3 million in 2012 compared to $0.8 million in 2011. Restructuring costs in 2012 related primarily to the closure of our Newark, California facility. Restructuring costs in 2011 represented the additional costs incurred for reductions related to the new organizational structure announced in September 2010.

Integration costs

Integration costs were $nil during 2012, compared to $1.4 million in 2011. Integration costs in 2011 were primarily related to office space optimization in France.

Impairment of intangible asset

Impairment of intangible asset was $nil during 2012 compared to $11.2 million in 2011. The impairment charge in 2011 primarily related to a software development program we acquired through the acquisition of Wavecom, S.A. (“Wavecom”) which we abandoned in 2011.

Amortization

Amortization expense decreased by $0.3 million, or 2.7%, in 2012 compared to 2011. Amortization expense in 2012 included $6.3 million of acquisition amortization compared to $6.0 million in 2011.

Foreign exchange gain (loss)

Foreign exchange gain was $3.3 million in 2012 compared to foreign exchange loss of $0.5 million in 2011. Foreign exchange gain in 2012 included a net foreign exchange gain of $2.7 million on revaluation of an intercompany loan to a self-sustaining subsidiary and a loss of $1.8 million related to the settlement of foreign currency forward exchange contracts that we had entered into in connection with the acquisition of the M2M business of Sagemcom.

Foreign exchange rate changes also impacted our Euro and Canadian dollar denominated revenue and operating expenses. We estimate that changes in exchange rates between 2011 and 2012 negatively impacted our 2012 revenues by approximately $2.4 million. We estimate that the favorable impact on operating expenses during 2012 was approximately $3.6 million.

Income tax recovery

Income tax recovery increased by $10.9 million in 2012 compared to 2011, primarily driven by the recognition of certain tax assets that will be realizable as a result of the sale of the AirCard business.

Net loss from continuing operations

Net loss from continuing operations improved by $46.5 million to a net loss of $4.2 million in 2012, compared to 2011. This improvement reflects the positive impact of higher revenue and gross margin, combined with lower operating expenditures, as well as the impact of favorable foreign exchange and tax recoveries in 2012.

Net loss from continuing operations in 2012 included stock-based compensation expense of $5.8 million and acquisition amortization of $11.9 million. Net loss from continuing operations in 2011 included stock-based compensation expense of $5.5 million, acquisition amortization of $12.9 million, and an after-tax

impairment charge of $11.2 million.

Net earnings (loss) attributable to the Company

Net earnings attributable to the Company increased by $56.5 million to net earnings of $27.2 million in 2012, compared to 2011. This increase reflects the increase in net earnings from continuing operations, combined with a $10.1 million increase in net earnings from discontinued operations.

Weighted average number of shares

The weighted average basic and diluted number of shares outstanding was 30.8 million for the year ended December 31, 2012, compared to 31.3 million for the year ended December 31, 2011.

The number of shares outstanding was 30.6 million at December 31, 2012, compared to 31.3 million at December 31, 2011. The reduction in number of shares outstanding was primarily due to purchases of 800,000 of the Company’s common shares on the Toronto Stock Exchange (“TSX”) and NASDAQ under our normal course issuer bid approved on December 13, 2011.

Year Ended December 31, 2011 Compared to Year Ended December 31, 2010

Revenue

Revenue in 2011 decreased by $24.8 million, or 6.9% as a result of a significant reduction in embedded wireless module sales to Barnes & Noble for their e-book reader ($0.7 million in 2011 compared to $64.2 million in 2010). This was partially offset by continued growth in sales to PC OEMs and our core M2M business, excluding Barnes & Noble.

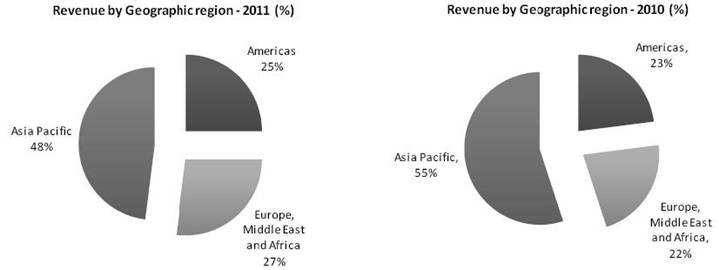

Our geographic revenue mix for the years ended December 31, 2011 and 2010 was as follows:

Gross margin

Gross margin was 30.5% of revenue for the year ended December 31, 2011, compared to 33.9% of revenue in 2010. The decrease in gross margin percentage was primarily related to product mix within our M2M business. Gross margin included $0.4 million of stock-based compensation expense in 2011, compared to $0.5 million in 2010.

Sales and marketing

Sales and marketing expenses decreased by $5.3 million, or 12.4%, and were 11.2% of revenue in 2011 compared to 11.9% in 2010. The decrease in sales and marketing expenses was due primarily to cost reduction initiatives, including the final stages of integration of Sierra Wireless and Wavecom. Sales and

marketing expenses included $1.1 million of stock-based compensation expense in 2011, compared to $1.2 million in 2010.

Research and development

R&D expenses in 2011 were comparable to 2010 at $60.9 million. R&D expenses for 2011 included stock-based compensation expense of $1.1 million and acquisition amortization of $6.9 million, compared to stock-based compensation expense of $0.9 million and acquisition amortization of $6.3 million in 2010.

Administration

Administration expenses decreased by $2.3 million, or 6.4%, in 2011, compared to 2010. The decrease was primarily due to cost reduction initiatives that were implemented in 2011. Administration expenses included $2.9 million of stock-based compensation expense in each of 2011 and 2010.

Restructuring

Restructuring costs decreased by $6.8 million, or 89.0%, to $0.8 million during 2011, compared to 2010. Restructuring costs in 2011 primarily represented the additional costs incurred for reductions in our workforce resulting from the implementation of the new organizational structure announced in September 2010. Restructuring costs in 2010 were related to reductions in our workforce resulting from the September 2010 organizational structure change.

Integration costs

Integration costs decreased by $3.7 million, or 72.1%, in 2011 compared to 2010. Integration costs in 2011 were primarily related to office space optimization in France. Integration costs in 2010 included costs for the integration of our Enterprise Resource Planning (“ERP”) system and employees retained for integration activities.

Impairment of intangible asset

We recorded an $11.2 million impairment charge in 2011, primarily related to a software development program we acquired through the acquisition of Wavecom which we abandoned in 2011. The program was not part of the Company’s strategic plan and its termination had no impact on our future operations. There was no impairment charge recorded in 2010.

Amortization

Amortization expense decreased by $1.3 million or 10.7%, in 2011 compared to 2010. Amortization expense in 2011 included $6.0 million of acquisition amortization compared to $7.3 million in 2010.

Foreign exchange gain (loss)

Foreign exchange loss decreased by $6.5 million in 2011 to $0.5 million. Foreign exchange loss for 2011 included a net foreign exchange loss of $0.1 million on intercompany balances. Foreign exchange loss for 2010 included a loss of $4.7 million on an intercompany balance that the parent company had with its self-sustaining foreign operations that arose as a result of the Wavecom acquisition.

Foreign exchange rate changes also impacted our Euro and Canadian dollar denominated operating expenses. We estimate that changes in exchange rates between 2010 and 2011 positively impacted our revenues by approximately $0.6 million and negatively impacted operating expenses by approximately $1.0 million in 2011.

Income tax recovery

Income tax recovery decreased by $11.0 million, or 73.5%, in 2011, compared to 2010, primarily driven by changes in the effective tax rate as a result of a shift in earnings among our numerous tax jurisdictions.

Net loss from continuing operations

Net loss from continuing operations increased by $15.7 million in 2011, compared to 2010. This was primarily due to a higher after-tax loss from operations of $50.7 million in 2011, compared to $35.0 million in 2010.

Net loss from continuing operations for the year ended December 31, 2011 included stock-based compensation of $5.5 million, acquisition amortization of $12.9 million, and an after-tax impairment charge of $11.2 million. Net loss for the year ended December 31, 2010 included stock-based compensation of $6.0 million, acquisition amortization of $13.6 million, and no after-tax impairment charge.

Net earnings (loss) attributable to the Company

Net loss attributable to the Company increased by $14.8 million in 2011, compared to 2010. This was primarily due to $15.7 million higher net loss from continuing operations, partially offset by higher net earnings from discontinued operations.

Weighted average number of shares

The weighted average basic and diluted number of shares outstanding was 31.3 million for the year ended December 31, 2011, compared to 31.1 million for the year ended December 31, 2010. The number of shares outstanding was 31.3 million at December 31, 2011, compared to 31.2 million at December 31, 2010.

SEGMENTED INFORMATION

Revenue and gross margin by segment for the years ending December 31 were as follows:

(in thousands of U.S. dollars)

|

| 2012 |

| 2011 |

| 2010 |

| |||

M2M |

|

|

|

|

|

|

| |||

Revenue (1) |

| $ | 335,990 |

| $ | 293,219 |

| $ | 332,445 |

|

Cost of goods sold |

| 224,229 |

| 198,271 |

| N/A |

| |||

Gross margin |

| $ | 111,761 |

| $ | 94,948 |

| $ | N/A |

|

Gross margin % |

| 33.3 | % | 32.4 | % | N/A |

| |||

|

|

|

|

|

|

|

| |||

Mobile Computing (2) |

|

|

|

|

|

|

| |||

Revenue |

| $ | 61,331 |

| $ | 39,956 |

| $ | 25,560 |

|

Cost of goods sold |

| 47,818 |

| 33,164 |

| N/A |

| |||

Gross margin |

| $ | 13,513 |

| $ | 6,792 |

| $ | N/A |

|

Gross margin % |

| 22.0 | % | 17.0 | % | N/A |

| |||

(1) Barnes and Noble contributed $nil in M2M revenue in 2012 compared to $0.7 million in 2011 and $64.2 million in 2010. Includes revenue generated from the acqusition of the M2M business of Sagemcom from the date of acquisition on August 1, 2012 to December 31, 2012 of $20.1 million.

(2) Excludes revenue, cost of goods sold, and gross margin related to the discontinued operations of the AirCard business.

Product line revenue by segment for the years ending December 31 was as follows:

(in thousands of U.S. dollars)

|

| 2012 |

| 2011 |

| 2010 |

| |||

M2M |

|

|

|

|

|

|

| |||

Air Prime Embedded Wireless Modules for M2M (1) |

| $ | 279,324 |

| $ | 242,791 |

| $ | 274,964 |

|

AirLink Intelligent Gateways |

| 46,699 |

| 39,013 |

| 48,626 |

| |||

AirVantage M2M Cloud Platform and Other |

| 9,967 |

| 11,415 |

| 8,855 |

| |||

|

| $ | 335,990 |

| $ | 293,219 |

| $ | 332,445 |

|

Mobile Computing (2) |

|

|

|

|

|

|

| |||

AirPrime Embedded Wireless Modules for PC OEM and Other |

| $ | 61,331 |

| $ | 39,956 |

| $ | 25,560 |

|

(1) Barnes and Noble contributed $nil in M2M revenue in 2012 compared to $0.7 million in 2011 and $64.2 million in 2010. Includes revenue generated from the acqusition of the M2M business of Sagemcom from the date of acquisition on August 1, 2012 to December 31, 2012 of $20.1 million.

(2) Excludes revenue related to the discontinued operations of the AirCard business.

Our M2M revenue increased $42.8 million, or 14.6%, to $336.0 million in 2012 compared to 2011. Revenue from AirPrime Embedded Wireless Modules for M2M increased $36.5 million, or 15.0%, in 2012 compared to 2011. This increase was due to $20.1 million in revenue generated from the M2M business of Sagemcom acquired on August 1, 2012 along with solid organic growth in the Americas and Asia, partially offset by continued weakness in European markets. Revenue from AirLink Intelligent Gateways increased $7.7 million, or 19.7%, in 2012 compared to 2011. The increase was primarily driven by sales related to the launch of new 4G gateways during the year.

Our Mobile Computing revenue, consisting primarily of sales of AirPrime Embedded Wireless Modules for PC OEM increased by $21.4 million, or 53.5%, to $61.3 million in 2012 compared to 2011. The increase was largely driven by strong demand for both existing 3G modules, as well as new 4G LTE modules launched during the year.

FOURTH QUARTER OVERVIEW

Fourth quarter 2012 was exceptionally strong. Revenues increased from quarter three as a result of a full quarter of contribution from the recently acquired M2M business of Sagemcom. Gross margin percentage was slightly higher, reflecting favorable product mix and contribution from the M2M business of Sagemcom and operating expenses were at comparable levels to third quarter levels. Operating expenses in the fourth quarter of 2012 included a full quarter of expenses related to the M2M business of Sagemcom and a benefit from one time project funding from a partner.

Financial highlights for the fourth quarter of 2012:

· Revenue of $109.4 million, 32.8 percent year-over-year growth, and non-GAAP operating earnings from continuing operations of $3.7 million

· Gross margin was 33.1%, up from 31.0% in the third quarter of 2012

· Non-GAAP earnings from operations were $3.7 million compared to $0.3 million in the third quarter of 2012

· Net earnings from continuing operations of $15.5 million and diluted earnings per share of $0.50 compared to net loss from continuing operations of $3.6 million and diluted loss per share of $0.12 in the third quarter of 2012. A favorable income tax recovery contributed to the sequentially stronger net earnings from continuing operations

· Non-GAAP net earnings from continuing operations were $4.5 million, or $0.15 per diluted share, in the fourth quarter of 2012 compared to Non-GAAP net earnings from continuing operations of $1.3 million, or $0.04 per diluted share, in the third quarter of 2012.

CONSOLIDATED FOURTH QUARTER RESULTS OF OPERATIONS

(in thousands of U.S. dollars, except where otherwise stated)

|

| Three months ended December 31, |

| ||||||

|

| 2012 |

| 2011 (1) |

| ||||

|

|

|

| % of |

|

|

| % of |

|

|

| $ |

| Revenue |

| $ |

| Revenue |

|

|

|

|

|

|

|

|

|

|

|

Revenue |

| 109,405 |

| 100.0 | % | 82,391 |

| 100.0 | % |

Cost of goods sold |

| 73,172 |

| 66.9 | % | 57,206 |

| 69.4 | % |

Gross margin |

| 36,233 |

| 33.1 | % | 25,185 |

| 30.6 | % |

|

|

|

|

|

|

|

|

|

|

Expenses |

|

|

|

|

|

|

|

|

|

Sales and marketing |

| 10,176 |

| 9.3 | % | 8,886 |

| 10.8 | % |

Research and development |

| 16,294 |

| 14.9 | % | 14,801 |

| 18.0 | % |

Administration |

| 7,743 |

| 7.1 | % | 7,694 |

| 9.3 | % |

Acquisition |

| 387 |

| 0.4 | % | — |

| 0.0 | % |

Restructuring |

| 42 |

| 0.0 | % | (19 | ) | 0.0 | % |

Integration |

| — |

| 0.0 | % | — |

| 0.0 | % |

Impairment of intangible asset |

| — |

| 0.0 | % | 11,214 |

| 13.6 | % |

Amortization |

| 3,107 |

| 2.8 | % | 2,620 |

| 3.2 | % |

|

| 37,749 |

| 34.5 | % | 45,196 |

| 54.9 | % |

Loss from operations |

| (1,516 | ) | -1.4 | % | (20,011 | ) | -24.3 | % |

Foreign exchange gain (loss) |

| 1,608 |

|

|

| (507 | ) |

|

|

Other income |

| 35 |

|

|

| 20 |

|

|

|

Earnings (loss) before income taxes |

| 127 |

|

|

| (20,498 | ) |

|

|

Income tax recovery |

| (15,396 | ) |

|

| (68 | ) |

|

|

Net earnings (loss) from continuing operations |

| 15,523 |

|

|

| (20,430 | ) |

|

|

Net earnings from discontinued operations |

| 4,083 |

|

|

| 6,668 |

|

|

|

Net earnings (loss) attributable to the Company |

| 19,606 |

|

|

| (13,762 | ) |

|

|

Net earnings (loss) per share attributable to the Company - Basic and diluted (in dollars) Continuing operations |

| 0.50 |

|

|

| (0.65 | ) |

|

|

Discontinued operations |

| 0.14 |

|

|

| 0.21 |

|

|

|

|

| 0.64 |

|

|

| (0.44 | ) |

|

|

(1) Financial information for fiscal year 2011 has been retrospectively adjusted to reflect the presentation of the AirCard business as discontinued operations.

SUMMARY OF QUARTERLY RESULTS OF OPERATIONS

The following tables highlight selected financial information for each of the eight most recent quarters that, in management’s opinion, have been prepared on a basis consistent with the audited consolidated financial statements for the year ended December 31, 2012. The selected financial information presented below reflects all adjustments, consisting primarily of normal recurring adjustments, which are, in the opinion of management, necessary for a fair presentation of results for the interim periods. These results are not necessarily indicative of results for any future period. You should not rely on these results to predict future performance.

(in thousands of U.S. dollars, except where otherwise stated)

|

| 2012 (1) |

| 2011 (1) |

| ||||||||||||||||||||

|

| Q4 |

| Q3 |

| Q2 |

| Q1 |

| Q4 |

| Q3 |

| Q2 |

| Q1 |

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Revenue |

| $ | 109,405 |

| $ | 100,183 |

| $ | 95,398 |

| $ | 92,335 |

| $ | 82,391 |

| $ | 85,363 |

| $ | 85,863 |

| $ | 79,558 |

|

Cost of goods sold |

| 73,172 |

| 69,097 |

| 65,317 |

| 64,461 |

| 57,206 |

| 57,855 |

| 60,713 |

| 55,661 |

| ||||||||

Gross margin |

| 36,233 |

| 31,086 |

| 30,081 |

| 27,874 |

| 25,185 |

| 27,508 |

| 25,150 |

| 23,897 |

| ||||||||

Gross margin % |

| 33.1 | % | 31.0 | % | 31.5 | % | 30.2 | % | 30.6 | % | 32.2 | % | 29.3 | % | 30.0 | % | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Sales and marketing |

| 10,176 |

| 8,572 |

| 8,998 |

| 9,321 |

| 8,886 |

| 9,082 |

| 9,318 |

| 9,902 |

| ||||||||

Research and development |

| 16,294 |

| 15,886 |

| 14,674 |

| 14,931 |

| 14,801 |

| 15,528 |

| 14,873 |

| 15,701 |

| ||||||||

Administration |

| 7,743 |

| 8,013 |

| 8,562 |

| 8,459 |

| 7,694 |

| 8,346 |

| 8,635 |

| 9,041 |

| ||||||||

Restructuring costs |

| 42 |

| 498 |

| 1,531 |

| 180 |

| (19 | ) | 881 |

| (350 | ) | 325 |

| ||||||||

Integration costs |

| — |

| — |

| — |

| — |

| — |

| 121 |

| 765 |

| 540 |

| ||||||||

Acquisition costs |

| 387 |

| 2,196 |

| 599 |

| — |

| — |

| — |

| — |

| — |

| ||||||||

Impairment of intangible asset |

| — |

| — |

| — |

| — |

| 11,214 |

| — |

| — |

| — |

| ||||||||

Amortization |

| 3,107 |

| 2,649 |

| 2,275 |

| 2,387 |

| 2,620 |

| 2,447 |

| 2,794 |

| 2,848 |

| ||||||||

|

| 37,749 |

| 37,814 |

| 36,639 |

| 35,278 |

| 45,196 |

| 36,405 |

| 36,035 |

| 38,357 |

| ||||||||

Operating income (loss) from continuing operations |

| (1,516 | ) | (6,728 | ) | (6,558 | ) | (7,404 | ) | (20,011 | ) | (8,897 | ) | (10,885 | ) | (14,460 | ) | ||||||||

Foreign exchange gain (loss) |

| 1,608 |

| 1,176 |

| 336 |

| 206 |

| (507 | ) | (154 | ) | (221 | ) | 422 |

| ||||||||

Other income (expense) |

| 35 |

| (70 | ) | 10 |

| (171 | ) | 20 |

| 68 |

| (13 | ) | (40 | ) | ||||||||

Earnings (loss) from continuing operations before income tax |

| 127 |

| (5,622 | ) | (6,212 | ) | (7,369 | ) | (20,498 | ) | (8,983 | ) | (11,119 | ) | (14,078 | ) | ||||||||

Income tax expense (recovery) |

| (15,396 | ) | (2,010 | ) | 2,656 |

| (124 | ) | (68 | ) | (1,632 | ) | (327 | ) | (1,941 | ) | ||||||||

Net earnings (loss) from continuing operations |

| 15,523 |

| (3,612 | ) | (8,868 | ) | (7,245 | ) | (20,430 | ) | (7,351 | ) | (10,792 | ) | (12,137 | ) | ||||||||

Net earnings (loss) from discontinued operations |

| 4,083 |

| 7,279 |

| 12,449 |

| 7,590 |

| 6,668 |

| 6,353 |

| 4,013 |

| 4,304 |

| ||||||||

Net earnings (loss) |

| 19,606 |

| 3,667 |

| 3,581 |

| 345 |

| (13,762 | ) | (998 | ) | (6,779 | ) | (7,833 | ) | ||||||||

Non-controlling interest |

| — |

| — |

| — |

| — |

| — |

| — |

| (13 | ) | (44 | ) | ||||||||

Net earnings (loss) attributable to the Company |

| $ | 19,606 |

| $ | 3,667 |

| $ | 3,581 |

| $ | 345 |

| $ | (13,762 | ) | $ | (998 | ) | $ | (6,766 | ) | $ | (7,789 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Earnings (loss) per share - GAAP in dollars |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Basic |

| $ | 0.64 |

| $ | 0.12 |

| $ | 0.12 |

| $ | 0.01 |

| $ | (0.44 | ) | $ | (0.03 | ) | $ | (0.22 | ) | $ | (0.25 | ) |

Diluted |

| $ | 0.64 |

| $ | 0.12 |

| $ | 0.12 |

| $ | 0.01 |

| $ | (0.44 | ) | $ | (0.03 | ) | $ | (0.22 | ) | $ | (0.25 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Weighted average number of shares (in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Basic |

| 30,591 |

| 30,573 |

| 30,817 |

| 31,175 |

| 31,298 |

| 31,297 |

| 31,267 |

| 31,237 |

| ||||||||

Diluted |

| 30,774 |

| 30,573 |

| 30,817 |

| 31,175 |

| 31,298 |

| 31,297 |

| 31,267 |

| 31,237 |

| ||||||||

(1) Quarterly information has been retrospectively adjusted to reflect the presentation of the AirCard business as discontinued operations.

Our quarterly results may fluctuate from quarter to quarter, driven by variation in sales volume, product mix and the combination of variable and fixed operating expenses. The impact of significant items incurred during the first three interim periods of year ended December 31, 2012 are discussed in more detail and disclosed in our quarterly reports and management’s discussion and analysis. Factors affecting our quarterly results in 2012 were as follows:

In the first quarter of 2012, net earnings attributable to the company increased $14.1 million, or $0.45 per common share, from the fourth quarter of 2011. The increase was primarily due to growth in our

AirPrime embedded wireless module business, for both M2M and PC OEM applications, combined with the absence of $11.2 million impairment charge related to intangible assets which occurred in the fourth quarter of 2012.

In the second quarter of 2012, net earnings attributable to the company increased by $3.2 million, or $0.11 per common share, from the first quarter of 2012. This increase was driven by higher revenues in the second quarter largely due to strong sales growth in both M2M and PC OEM segments of our AirPrime embedded wireless module business, combined with higher gross margin resulting from lower product costs.

In the third quarter of 2012, net earnings attributable to the company of $3.7 million, or $0.12 per common share, were comparable to the second quarter of 2012. Strong growth in AirPrime embedded wireless module sales to M2M customers was offset by modestly higher operating expenses incurred as a result of the acquisition of the M2M business of Sagemcom.

In the fourth quarter of 2012, net earnings attributable to the company increased $15.9 million, or $0.52 per common share, from the third quarter of 2012. The increase was primarily related to unusually high revenues from AirPrime embedded wireless module sales to M2M customers combined with steady growth in AirLink intelligent gateways. The fourth quarter also included an income tax recovery related to the recognition of certain assets that will be realizable upon the sale of the AirCard business.

LIQUIDITY AND CAPITAL RESOURCES

Selected Financial Information

(in thousands of U.S. dollars)

|

| 2012 |

| 2011 |

| 2010 |

| |||

|

|

|

|

|

|

|

| |||

Cash flows provided before changes in non-cash working capital: |

| $ | 49,070 |

| $ | 17,814 |

| $ | 22,970 |

|

|

|

|

|

|

|

|

| |||

Changes in non-cash working capital |

|

|

|

|

|

|

| |||

Accounts receivable |

| (616 | ) | 9,067 |

| (35,671 | ) | |||

Inventories |

| (4,019 | ) | 5,664 |

| (11,399 | ) | |||

Prepaid expense and other |

| (14,543 | ) | 4,248 |

| 7,104 |

| |||

Accounts payable and accrued liabilities |

| 10,997 |

| (13,783 | ) | 12,116 |

| |||

Deferred revenue and credits |

| (422 | ) | 733 |

| 480 |

| |||

|

| (8,603 | ) | 5,929 |

| (27,370 | ) | |||

Cash flows provided by (used in): |

|

|

|

|

|

|

| |||

Operating activities |

| 40,467 |

| 23,743 |

| (4,400 | ) | |||

|

|

|

|

|

|

|

| |||

Investing activities |

| (64,184 | ) | (2,706 | ) | (17,521 | ) | |||

Acquisition of M2M business of Sagemcom |

| (55,218 | ) | — |

| — |

| |||

Capital expenditures and increase in intangible assets |

| (18,452 | ) | (18,008 | ) | (16,556 | ) | |||

Net change in short-term investments |

| 9,347 |

| 17,058 |

| 489 |

| |||

Purchase of Wavecom S.A. shares |

| — |

| (1,787 | ) | (1,553 | ) | |||

|

|

|

|

|

|

|

| |||

Financing activities |

| (9,365 | ) | (4,858 | ) | (1,541 | ) | |||

Repurchase of common shares for cancellation |

| (6,312 | ) | — |

| — |

| |||

Purchase of treasury shares for RSU distribution |

| (2,489 | ) | (4,472 | ) | — |

| |||

Operating Activities

Cash provided by operating activities increased $16.7 million to $40.5 million during the year ended December 31, 2012, compared to the same period of 2011. The increase in cash was primarily due to higher operating earnings in the year ended December 31, 2012 compared to the same period of 2011. This was partially offset by higher working capital requirements in 2012.

Investing Activities

Cash used for investing activities increased $61.5 million to $64.2 million during the year ended December 31, 2012, compared to the same period of 2011. The increase in investing activities was largely related to the acquisition of the M2M business of Sagemcom and net change in short-term investments.

Cash used for the purchase of capital equipment was primarily for production and tooling equipment, research and development equipment, computer equipment and software, while cash used for intangible assets was driven primarily by patent registration costs and software licenses.

Financing Activities

Cash used for financing activities increased $4.5 million to $9.4 million during the year ended December 31, 2012, compared to 2011. The increase was primarily related to the use of cash during 2012 to purchase 800,000 of our common shares on the TSX and NASDAQ in connection with our normal course issuer bid approved on December 13, 2011 and 336,638 of our common shares to satisfy obligations under our restricted share unit plan, in the amounts of $6.3 million and $2.5 million, respectively.

Cash Requirements

Our near-term cash requirements are primarily related to funding our operations, capital expenditures, intellectual property (“IP”) licenses, and other obligations discussed below. On August 1, 2012, we completed the acquisition of the M2M business of Sagemcom, a transaction that was funded by $55.2 million in cash. We continue to believe our cash and cash equivalents balance of $63.6 million at December 31, 2012 and cash generated from continuing operations will be sufficient to fund our expected working capital requirements for at least the next twelve months based on current business plans. Our capital expenditures during the first quarter of 2013 are expected to be primarily for research and development equipment, tooling, leasehold improvements, software licenses and patents. However, we cannot be certain that our actual cash requirements will not be greater than we currently expect. Following closing of the sale of the AirCard business in early April 2013, we expect to continue to purchase back our common shares under our Normal Course Issuer Bid.

The following table presents the aggregate amount of future cash outflows for contractual obligations as of December 31, 2012.

Payments due by period |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| Thereafter |

| ||||||

Operating lease obligations |

| $ | 4,429 |

| $ | 4,092 |

| $ | 3,630 |

| $ | 3,597 |

| $ | 3,487 |

| $ | 10,876 |

|

Capital lease obligations |

| 305 |

| 231 |

| 153 |

| 30 |

| — |

| — |

| ||||||

Purchase obligations (1) |

| 54,850 |

| — |

| — |

| — |

| — |

| — |

| ||||||

Other long-term liabilities (2) |

| — |

| 24,887 |

| — |

| — |

| — |

| 1,225 |

| ||||||

Total |

| $ | 59,584 |

| 29,210 |

| $ | 3,783 |

| $ | 3,627 |

| $ | 3,487 |

| $ | 12,101 |

| |

(1) Purchase obligations represent obligations with certain contract manufacturers to buy minimum amount of designated products between January, 2013 and March, 2013. In certain of these arrangements, we may be required to acquire and pay for such products up to the prescribed minimum or forecasted purchases.

(2) Other long-term liabilities include the long-term portions of accrued royalties.

Capital Resources

|

| 2012 |

| 2011 |

| ||||||||||||||||||||

(In thousands of dollars) |

| Dec 31 |

| Sept 30 |

| June 30 |

| Mar 31 |

| Dec 31 |

| Sept 30 |

| June 30 |

| Mar 31 |

| ||||||||

Cash and cash equivalents |

| $ | 63,646 |

| $ | 59,528 |

| $ | 123,159 |

| $ | 106,773 |

| $ | 101,375 |

| $ | 100,662 |

| $ | 101,685 |

| $ | 86,197 |

|

Short-term investments |

| — |

| — |

| 2,153 |

| — |

| 9,347 |

| — |

| 17,470 |

| 24,559 |

| ||||||||

|

| 63,646 |

| 59,528 |

| 125,312 |

| 106,773 |

| 110,722 |

| 100,662 |

| 119,155 |

| 110,756 |

| ||||||||

Unused credit facilities |

| 50,000 |

| 10,000 |

| 10,000 |

| 10,000 |

| 10,000 |

| 10,000 |

| 10,000 |

| 10,000 |

| ||||||||

Total |

| $ | 113,646 |

| $ | 69,528 |

| $ | 135,312 |

| $ | 116,773 |

| $ | 120,722 |

| $ | 110,662 |

| $ | 129,155 |

| $ | 120,756 |

|

Credit Facilities

On October 31, 2012 we cancelled our then existing revolving facility (“Old Revolving Facility”) of $10 million which was to expire on January 28, 2013, and replaced it with a new revolving facility with the Toronto Dominion Bank and the Canadian Imperial Bank of Commerce in the amount of $50 million which will expire on October 31, 2013. The revolving facility is for working capital requirements and is secured by a pledge against all of our assets, including assets related to discontinued operations, and is subject to borrowing base limitations. The new revolving facility contains covenants and security substantially similar to the Old Revolving Facility. There were no borrowings under the revolving facility as at December 31, 2012. We are presently reviewing the impact of the proposed sale of the assets and operations of our AirCard business on the availability of the entire $50 million of the facility.

Letters of Credit

We have entered into a standby letter of credit facility agreement under which we have issued three performance bonds to third party customers in accordance with specified terms and conditions. At December 31, 2012, we had two Euro denominated performance bonds amounting to €50,000 expiring in June 2014 and a performance bond of $176,000 expiring in May 2013 (December 2011 - $176,000). We also have a letter of credit in the amount of $1.3 million expiring in May 2013 issued to a third party vendor with specified terms and conditions. These instruments approximate their fair market value.

Normal Course Issuer Bids

During the year ended December 31, 2012, we purchased 800,000 common shares in the open market for cancellation at an average price of $7.89 per share pursuant to a normal course issuer bid approved December 13, 2011. These purchases were completed in the first half of 2012.

On February 6, 2013, we received approval from the TSX of our Notice of Intention to make a Normal Course Issuer Bid (the “2013 Bid”). Pursuant to the 2013 Bid, we can purchase for cancellation up to 1,529,687 of our common shares, or approximately 5% of the common shares outstanding as of the date of the announcement. The 2013 Bid commenced on February 14, 2013 and will terminate on the earlier of: (i) February 13, 2014, (ii) the date the Company completes its purchases pursuant to the Notice of Intention filed with the TSX, or (iii) the date of notice by the Company of termination of the 2013 Bid. As of March 7, 2013, we had purchased 124,300 common shares at an average price of $11.08 per share.

NON-GAAP FINANCIAL MEASURES

Our consolidated financial statements are prepared in accordance with U.S. GAAP on a basis consistent for all periods presented. In addition to results reported in accordance with U.S. GAAP, we use non-GAAP financial measures as supplemental indicators of our operating performance. The term “non-GAAP financial measure” is used to refer to a numerical measure of a company’s historical or future financial performance, financial position or cash flows that: (i) excludes amounts, or is subject to adjustments that have the effect of excluding amounts, that are included in the most directly comparable measure calculated and presented in accordance with U.S. GAAP in a company’s statement of earnings, balance sheet or statement of cash flows; or (ii) includes amounts, or is subject to adjustments that have the effect of including amounts, that are excluded from the most directly comparable measure so calculated and presented.