QuickLinks -- Click here to rapidly navigate through this document

We are

growingin

gastroenterology

| DISEASES OF THE LIVER Liver and biliary diseases affect one in every ten Americans. Cholestatic liver diseases, conditions in which the bile flow is impaired, include Primary Biliary Cirrhosis (PBC), Primary Sclerosing Cholangitis (PSC) and many others. | DISEASES OF THE PANCREAS Common diseases of the pancreas, the "hidden organ" include Diabetes, Chronic Pancreatitis, Cystic Fibrosis, pancreatic enzyme deficiency, and pancreatic cancer. | DISEASES OF THE BOWEL Inflammatory Bowel Diseases (IBD) affect people of any gender, age or race and cause mild to debilitating symptoms including abdominal pain, cramping, fatigue and diarrhea. | GASTROINTESTINAL (GI) AND GI-RELATED CANCER Digestive cancers, affecting the colon and rectum, the esophagus and stomach and the liver and pancreas, have the world's highest incidence and mortality rate of cancer. | OTHER GI DISEASES AND DISORDERS Peptic ulcers, a sore on the lining of the stomach or duodenum, Irritable Bowel Syndrome (IBS), a disorder interfering with the normal functions of the colon, and hemorrhoids are common occurrences. |

A new era of growth...

Building on its solid base of five core therapeutic areas, Axcan is poised for expansion into larger GI markets with innovative products. Our commitment and dedication to improving quality of care and treatment of patients suffering from gastrointestinal diseases and disorders, are stronger than ever.

AXCAN PROUDLY PRESENTS ITS 9TH ANNUAL REPORT

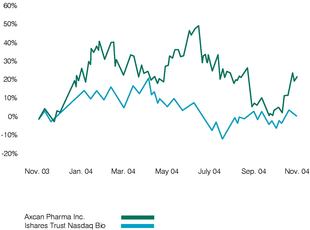

NASDAQ INDEX VS AXCAN

On November 24, 2003, Axcan was added to the NASDAQ Biotechnology Index joining biomedical industry leaders in their respective areas, and gaining increased visibility in the U.S. financial markets.

FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements for either the Company or certain of its subsidiaries. These forward-looking statements, by their nature, necessarily involve risks and uncertainties that could cause actual results to differ materially from those contemplated by the forward-looking statements. The Company considers the assumptions on which these forward-looking statements are based to be reasonable at the time they were prepared, but cautions the reader that these assumptions regarding future events, many of which are beyond the control of the Company and its subsidiaries, may ultimately prove to be incorrect. Factors and risks, which could cause actual results to differ materially from current expectations, are discussed on page 44 of this Annual Report as well as in the Company's Annual Information Form for the year ended September 30, 2004. The Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events, or otherwise.

| TABLE OF CONTENTS | PAGE | |

|---|---|---|

| Financial and Operating Highlights | 04 | |

| Five-Year Financial Data | 06 | |

| Letter to Our Shareholders | 08 | |

| Our Five Core Gastroenterology Franchises | 14 | |

| ITAX, a Novel Gastroprokinetic Drug for Motility Disorders | 26 | |

| HEPENAX, a Novel Treatment for Hepatic Encephalopathy | 28 | |

| A Deep Pipeline | 30 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 32 | |

| Consolidated Financial Statements — U.S. GAAP | 47 | |

| Consolidated Financial Statements — Canadian GAAP | 75 | |

| Corporate Governance | 100 | |

| Board of Directors | 102 | |

| Management Team | 104 |

2

Axcan is a leading specialty pharmaceutical company focused in the field of gastroenterology.

The Company markets a broad line of prescription products sold for the treatment of symptoms in a number of gastrointestinal diseases and disorders such as Inflammatory Bowel Disease, Irritable Bowel Syndrome, cholestatic liver diseases, and complications related to Cystic Fibrosis. Axcan's products are marketed by its own sales force in North America and Europe. Today, the Company counts more than 450 employees worldwide.

Headquartered in Mont-St-Hilaire, Quebec, Canada, Axcan's common shares are traded on the Toronto Stock Exchange under the symbol "AXP" and on the NASDAQ National Market under the symbol "AXCA".

3

FINANCIAL AND OPERATING HIGHLIGHTS

A PROVEN TRACK RECORD

For the last five years, our dedication to executing our growth strategy has proven to be fruitful. We have further developed our core capabilities through multiple acquisitions and licensing agreements, smoothly integrating the merged entities while successfully filing Investigational New Drug Applications (INDs) and New Drug Applications (NDAs). We have also achieved another year of profitability and growth.

A SOUND BUSINESS MODEL

Successful integration of recently acquired companies, products and product lines allowed us to build a solid international infrastructure. Today, we are in a favorable position to leverage our strong foundation by adding new products through development or acquisitions, translating into higher margins.

4

5

Years ended September 30

(All amounts are stated in thousands of U.S. dollars, except share-related data, percentages and ratios)

| | 2004 | 2003 | 2002 | 2001 | 2000 | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | $ | $ | $ | $ | $ | |||||||

| OPERATING DATA | ||||||||||||

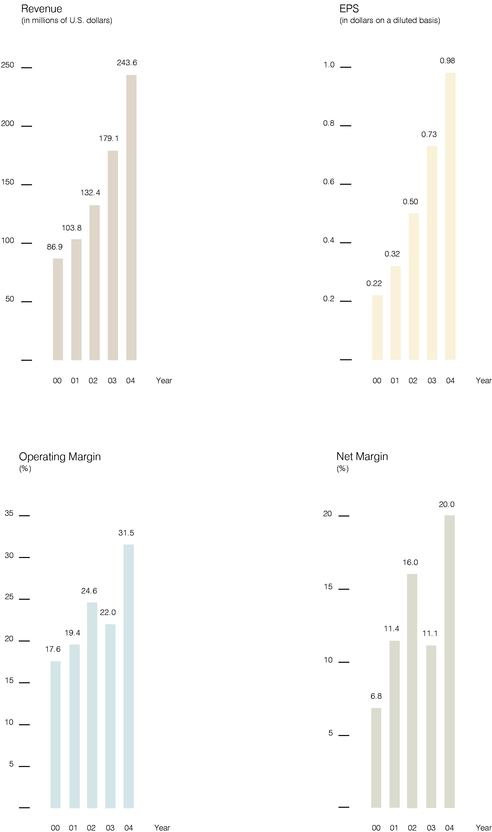

Revenue | 243,634 | 179,084 | 132,404 | 103,814 | 86,869 | |||||||

Expenses | ||||||||||||

| Cost of goods sold | 54,247 | 44,459 | 34,039 | 26,381 | 22,268 | |||||||

| Research and development | 19,886 | 12,098 | 8,855 | 7,243 | 7,066 | |||||||

| Selling and administrative | 76,365 | 63,084 | 49,392 | 38,185 | 31,821 | |||||||

| Depreciation and amortization | 16,359 | 8,063 | 7,546 | 11,829 | 10,410 | |||||||

Operating income | 76,797 | 39,380 | 32,572 | 20,176 | 15,304 | |||||||

| Net income | 48,728 | 19,925 | 21,188 | 11,825 | 5,936 | |||||||

| Net income, excluding one-time charges(1) | 48,728 | 33,350 | 21,188 | 11,825 | 5,936 | |||||||

Per share data, excluding one-time charges(1) | ||||||||||||

| Basic net income | 1.08 | 0.74 | 0.51 | 0.32 | 0.22 | |||||||

| Diluted net income | 0.98 | 0.73 | 0.50 | 0.32 | 0.22 | |||||||

| Weighted average number of common shares outstanding (000s) (diluted) | 52,788 | 45,608 | 42,528 | 36,531 | 26,792 | |||||||

FINANCIAL POSITION | ||||||||||||

Cash, cash equivalents and short-term investments | 37,901 | 170,885 | 80,717 | 16,515 | 20,911 | |||||||

| Total assets | 609,644 | 545,349 | 367,006 | 246,484 | 250,943 | |||||||

| Long-term debt (including convertible subordinated notes) | 129,694 | 131,002 | 8,603 | 2,919 | 50,006 | |||||||

| Shareholders' equity | 392,076 | 331,011 | 294,787 | 200,431 | 156,667 | |||||||

COMMON SHARE PERFORMANCE(2) | ||||||||||||

Market capitalization (000s) | 708,494 | 612,059 | 430,238 | 411,010 | 377,151 | |||||||

| Closing share price on NASDAQ National Market | 15.55 | 13.60 | 9.59 | 10.70 | 10.93 | |||||||

| Closing share price on Toronto Stock Exchange (CDN$) | 19.62 | 18.28 | 15.11 | 16.95 | 16.80 | |||||||

| Closing number of common shares issued and outstanding (000s) | 45,562 | 45,004 | 44,863 | 38,412 | 34,506 | |||||||

CASH FLOWS | ||||||||||||

Cash flows from operating activities | 23,360 | 51,496 | 35,331 | 16,390 | 11,285 | |||||||

| Acquisition of intangible assets | 149,628 | 76,093 | 1,561 | 1,892 | 19,886 | |||||||

| Net issuance of common shares | 4,900 | 1,103 | 65,039 | 30,969 | 83,466 | |||||||

| Issuance of long-term debt | 2,212 | 126,064 | 1,506 | — | — | |||||||

| Net increase (decrease) in cash and cash equivalents | (15,794 | ) | 17,796 | 3,462 | 5,391 | (16,398 | ) | |||||

RATIOS | ||||||||||||

Gross margin | 77.7% | 75.2% | 74.3% | 74.6% | 74.4% | |||||||

| Operating margin | 31.5% | 22.0% | 24.6% | 19.4% | 17.6% | |||||||

| Net margin | 20.0% | 11.1% | 16.0% | 11.4% | 6.8% | |||||||

| Return on equity | 13.5% | 6.4% | 8.6% | 6.6% | 5.5% | |||||||

| Revenue growth | 36.0% | 35.3% | 27.5% | 19.5% | 131.3% | |||||||

- (1)

- One-time charges consisting of take-over bid expenses, acquired in-process research and related income taxes, a non-GAAP measure (see page 37).

- (2)

- As of September 30

6-7

"Significant investments were made over the

last several years to create the impending new product flow that

will translate into sustained growth for the future."

8

LETTER TO OUR SHAREHOLDERS

FISCAL 2004 was a determining year for your company. It was a year that culminated five full years of solid growth and profitability. More importantly, 2004 marked the beginning of a new era for Axcan that will ensure its future growth. Over the course of the last 20 fiscal quarters, the company consistently executed its growth strategy, delivering repeated strong financial performances and achieving its major corporate objectives. Throughout this time, Axcan continued to successfully expand its core gastroenterology franchises by extending product lines, maintaining market share for its key products and increasing global market penetration. Axcan also in-licensed key later-stage products that hold tremendous promise for the future.

Today, Axcan is well positioned to build on its solid base of five core gastro-intestinal (GI) franchises and expand into larger GI markets with patented new products. One of these products continues to command a huge amount of attention. Indeed, ITAX (itopride hydrochloride) oral tablets may prove to be the answer to a major unmet clinical need since no safe and effective therapy exists for Functional Dyspepsia. There is no doubt that if approved, ITAX will be, by far, the largest drug in our portfolio. The launch of ITAX will encompass North America (Canada and the United States) as well as major markets in Europe (France, the United Kingdom and Germany). The launch of ITAX is expected to take place in 2007. It is planned to be followed by the launch of several other innovative GI products including HEPENAX (L-ornithine L-aspartate) in 2008, ursodeoxycholic acid-disulfate (SUDCA) in 2009 and others.

Significant investments have been made by our company over the course of the last several years in order to create the impending new product flow that will translate into solid, sustained growth for the future.

9

This year we were also pleased to inaugurate our new expanded corporate offices in Mont-St-Hilaire, to celebrate our 22 years of service to the stakeholders and patients afflicted with GI disorders and diseases. Within our newly expanded premises, we will endeavor to meet new challenges and discover new treatments in order to fulfill unmet medical needs in gastroenterology.

As part of the inauguration ceremony, we hosted a very special Analyst & Investor Luncheon featuring a R&D Update. This included presentations by world-renowned experts in their respective fields. We were honored to have such high quality speakers: Dr. Richard H. Hunt from the McMaster University Medical Center, Dr. Rajiv Jalan from the University College London Medical School, Dr. Kenneth D. Setchell from the Cincinnati Children's Hospital Medical Center, Dr. Steve Pereira from the University College Medical School and Mr. Alan Brownstein, Chairman of the American Liver Foundation.

They discussed the disease states that underlie four selected, high potential Axcan projects: ITAX (itopride hydrochloride) for the treatment of Functional Dyspepsia, HEPENAX (L-ornithine L-aspartate) in the treatment of Hepatic Encephalopathy, ursodeoxycholic acid-disulfate (SUDCA) in Liver Disease and Organ Preservation in Liver Transplant and finally PHOTOFRIN (porfimer sodium) in the treatment of Cholangiocarcinoma. As part of their presentations, the authors featured ground-breaking hitherto unpublished clinical data related to these topics as well as the clinical implications thereof.

FINANCIAL PERFORMANCE

Over the last five years, Axcan has had a remarkable track record with an annual compounded growth rate of 28% in revenue and 45% in diluted income per share. For the fiscal year 2004, our financial goals included growth of total revenue to $242.0 million, net income to $47.4 million, a solid improvement of our gross margin as well as EPS growth of 27.0%.

For the fiscal year ended September 30, 2004, the Company reported revenue growth of 36.0% to $243.6 million and net income of $48.7 million, a 46.1%(1) increase compared to the previous year. Gross margin amounted to 77.7% of revenue for the year 2004 compared to 75.2% of revenue in 2003. We achieved $0.98 in earnings per share on a fully diluted basis for the fiscal year 2004, representing a 34.2%(1) increase in comparison to fiscal year 2003.

The increase in revenue primarily resulted from $41.8 million in additional North American sales of the AVAX product line, which was acquired in November 2003 from Aventis S.A. and strong sales of CANASA in the United States. Revenues from sales made by our French subsidiary, following the acquisitions of DELURSAN as well as the PANZYTRAT product line, also contributed positively. Our overall gross margin was enhanced due to a product mix effect and generally improved margins in Europe.

- (1)

- Before one-time charges consisting of takeover-bid expenses, acquired in-process research and related income taxes, a non-GAAP measure (see page 37)

10

Research and development expenses increased by $7.8 million to $19.9 million for the year ended September 30, 2004, a 64.5% increase from the preceding fiscal year. This increase is mainly due to the acceleration of our ITAX development program for the treatment of Functional Dyspepsia.

Axcan is in a solid financial position with a healthy balance sheet, almost $40 million in cash, cash equivalents and short term investments and working capital of almost $90 million. Axcan also has access to credit facilities totaling $125 million. The company therefore maintains the flexibility to actively pursue strategic opportunities including revenue generating accretive product acquisitions and to continue advancing its current development programs. Given its strong balance sheet and excluding any large transactions, the company does not foresee requiring the issue of additional securities.

GROWING IN GASTROENTEROLOGY

Consistent with the execution of our business strategy, we continue to actively pursue acquisition opportunities that represent accretive extensions to Axcan's product portfolio. At the beginning of the year, we completed the acquisition of a group of gastrointestinal products from Aventis: CARAFATE and BENTYL for the U.S. market and SULCRATE, BENTYLOL and PROCTOSEDYL for the Canadian market, further consolidating our core revenue stream and leveraging our North American sales and marketing infrastructure.

We continue to successfully develop line extensions, either improvements or new indications for our key products, in order to strengthen their competitive positions and increase our global market penetration. This year, we obtained approval by the U.S. Food and Drug Administration (FDA) for a unique, double-strength tablet (500mg) of ursodiol for the treatment of Primary Biliary Cirrhosis. We also launched this new dosage form of ursodiol in the U.S., marketed under the brand name URSO Forte, and distributed through major independent and retail pharmacies. We also expect to receive approval shortly for a new, 750mg tablet dosage of SALOFALK (Canada) for the treatment of Ulcerative Colitis. Just recently, we received FDA approval for the use of a 1-gram mesalamine suppository dosage form in the treatment of Ulcerative Proctitis, for which we have been granted a 3-year market exclusivity for the new strength and dosing regimen.

Last, we obtained our first European approval for PHOTOBARR for the treatment of High-Grade Dysplasia associated with Barrett's Esophagus. This approval was very important demonstrating our ability to navigate the European regulatory process.

Continuously assessing the market opportunities and environment for each product in development, we believe that HELIZIDE will have good potential in export markets, where the incidence of gastric cancers is highest and the "test and treat" approach is systematic. We continue to pursue the process of qualifying a new North American manufacturer of biskalcitrate potassium (bismuth salt), a component of our HELIZIDE combination therapy for the eradication ofHelicobacter pylori bacterium. We have realigned the timelines for this product candidate and now aim for an FDA re-submission by the middle of calendar year 2005.

11

ADVANCING THE PIPELINE

On the Research and Development front, fiscal year 2004 was marked by crucial advancement in the development program for our potential "blockbuster" gastroprokinetic drug, ITAX. Further to positive Phase II efficacy and safety results for ITAX in the treatment of Functional Dyspepsia, Axcan initiated Phase III clinical trials in North America and Western Europe. Enrollment for the two Phase III studies is well underway and is expected to be completed in the second half of calendar year 2005.

More recently, the positive results of a cardiac safety study conducted in Montreal, with 162 healthy volunteers, strengthened our confidence in the safety profile of this new prokinetic drug. We intend to aggressively pursue the ITAX development program and remain confident that we can achieve our goal of an early 2007 launch in the U.S., Canada, Germany, the United Kingdom and France.

Other advances in our development programs include the completion of three Phase III studies to confirm the efficacy and safety of a new 4-gram, patented, mesalamine rectal gel for the treatment of Distal Ulcerative Colitis. In addition, we initiated a clinical research program for HEPENAX (L-ornithine L-aspartate), a very promising treatment for Porto-Systemic Encephalopathy. During the year, we also achieved positive animal study results for the new sulfated version of ursodiol as a potent chemopreventive agent in colorectal cancer, for which we will initiate animal toxicity studies in the second half of fiscal 2005.

BUILDING A STRONG AND EXPERIENCED MANAGEMENT TEAM

During the year, Axcan strengthened its existing core management team with the addition of Jean-François Hébert, appointed Vice President, Manufacturing Operations. Mr. Hébert, formerly with Abbott Laboratories where he assumed positions of increasing responsibility and received awards for operations and leadership, brings to Axcan more than 15 years of successful international business experience in the pharmaceutical and food industries.

A number of individuals also evolved within our growing organization and assumed new roles and challenges at Axcan. Jocelyn Pelchat was promoted to Senior Vice President, International Commercial Operations, with responsibility for building the Company's GI business in the European Union and other select markets outside North America. Richard Tarte assumed the position of Vice President, Corporate Development and General Counsel, with the goal of identifying, evaluating and negotiating new business opportunities for the Company, and Michael Thiel, in addition to his responsibilities as Vice President of Marketing for North American Commercial Operations, was appointed Global Project Leader — ITAX, responsible for planning, directing, and coordinating the development and commercialization of this product candidate.

We also enhanced the structure of our North American Commercial Operations and made new appointments there. A Sales Operations Department was created to manage Axcan's broad range of large accounts and to direct the sales support functions. Our Sales and Marketing structure was also realigned to further develop our capabilities to compete successfully in the future and to assure the effective commercialization of ITAX. Michael Pasternak was promoted to Vice President of Sales Operations, North America, while Paul Smith was appointed Vice President of Sales, North America. Having worked together for the last 14 years, they combine more than 50 years of pharmaceutical experience.

12

INVESTING FOR THE FUTURE

The end of fiscal year 2004 is marked by our stronger than ever commitment to advance our innovative pipeline of product candidates. ITAX, which could be the biggest product in Axcan's history, will receive special focus in the coming year.

Nevertheless, we will continue to build on our successes and continue to develop our core competencies to ensure Axcan's long-term profitability and growth. To leverage our existing infrastructure, acquisitions of value-added and carefully selected products remain a key element of our business strategy.

With our successfully established gastroenterology franchises, or products for five therapeutic areas, we believe that Axcan is ready to transition towards developing more innovative, IP-protected gastroenterology products, with an emphasis on hepatology diseases. This will allow attainment of better margins and provide higher growth potential for the Company. We will continue to address unmet therapeutic needs and help improve the quality of life of people suffering from GI diseases and disorders.

Axcan is already a specialty pharmaceutical world leader in the field of gastroenterology. By building our product portfolio and extending our market reach in both North America and Europe, we expect to enhance this position. As we continue to apply our proven three-pronged business model based on organic sales growth of our current products, in-licensing or acquisition of new products and continued product development, Axcan's growth potential is very promising. Since 2001, our compounded annual growth rate of diluted income per share has been 45%, an eloquent testimony to the effectiveness of our strategy.

In achieving our growth objectives, Axcan has taken great care to foster strict corporate governance practices. The Corporate Governance and Nominating Committee of Axcan's Board of Directors, comprised solely of independent directors, has a broad mandate to assure efficient and appropriate relations between senior management and the Board of Directors. In addition, at every level of the company, Axcan insists on a high standard of ethical business behavior, be it in scientific development, manufacturing, sales, or administration. Moreover, we are committed to transparent and ongoing communications with you, our shareholder.

The continued remarkable performance of Axcan in terms of top-line growth and profitability is in large measure the result of the commitment of our employees and their devotion to serving the needs of patients with GI diseases and disorders. On behalf of the Board of Directors and the entire Management team, I would like to take this opportunity to thank the Axcan employees who now number some 450 people in North America and in Europe and salute their role in helping make Axcan Pharma a recognized leader in gastroenterology.

I also want to express my gratitude to the members of the Board of Directors for their ongoing guidance and strategic, constructive counsel in this period of rapid growth.

Last, I would like to thank you, our shareholder, for believing in this Company as we do, and for your continuing support.

Léon F. Gosselin Chairman of the Board, President and Chief Executive Officer |

13

AXCAN HAS BUILT A STRONG MULTI-PRODUCT GASTROINTESTINAL BASE FOCUSING ON UNMET THERAPEUTIC NEEDS.OUR CORE BUSINESS, ALWAYS GEARED TOWARDS GASTROENTEROLOGY, REVOLVES AROUND FIVE THERAPEUTIC AREAS.

14

| GI | DISEASES OF THE LIVER DISEASES OF THE PANCREAS DISEASES OF THE BOWEL GASTRO-INTESTINAL (GI) AND GI-RELATED CANCER OTHER GASTRO-INTESTINAL DISEASES AND DISORDERS |

15

GI DISEASES OF THE LIVER

Liver diseases affect one in every ten Americans

According to the American Liver Foundation (ALF), 25 million Americans are or have been afflicted with liver and biliary diseases. Furthermore, 25,000 Americans die each year from chronic liver disease and cirrhosis, and 300,000 people are hospitalized each year due to cirrhosis.

Cholestatic liver diseases are conditions in which the bile flow from the liver is impaired. Such conditions include Primary Biliary Cirrhosis (PBC), Primary Sclerosing Cholangitis (PSC) and many others. Axcan markets URSO 250 and URSO Forte in the United States for the treatment of PBC, as well as URSO DS in Canada and DELURSAN in France for the treatment of cholestatic liver diseases.

16

The only ursodiol approved for PBC

URSO (ursodeoxycholic acid), a therapeutic bile acid available in 500mg and 250mg film-coated tablets for oral administration, is the only ursodiol approved by the FDA for the treatment of patients with PBC, a chronic liver disease that slowly destroys the ducts that drain bile in the liver.

More than 10 years of clinical studies

The effectiveness and safety of URSO have been proven. It delays the progression of PBC, normalizes liver function tests, decreases the incidence of esophageal varices by 60%, and significantly improves transplant-free survival to the point that non-cirrhotic PBC patients have a survival rate similar to that of the general population.

PBC, a chronic liver disease

The disease causes slow, progressive destruction of bile ducts in the liver. This destruction interferes with the excretion of bile. Continued liver inflammation causes scarring and eventually leads to cirrhosis. Ursodeoxycholic acid is a life-saving, safe, and approved therapy.

Women are affected 10 times more frequently than men

Studies show that women are affected 10 times more commonly than men. PBC is usually diagnosed in patients between the ages of 35 and 60. The illness is chronic and can lead to liver failure and other life-threatening complications. Despite the fact that scientists and physicians have known about PBC for more than 100 years, the basic cause is still unknown.

| URSO 250, URSO Forte | URSO DS | DELURSAN | ||

|---|---|---|---|---|

| Tablets | Tablets | Tablets | ||

| United States | Canada | France | ||

| Primary Biliary Cirrhosis | Cholestatic liver diseases | Cholestatic liver diseases |

17

GI DISEASES OF THE PANCREAS

The pancreas is vital to good health

The pancreas, located deep in the abdomen behind the stomach, produces juices and enzymes that flow into the intestine, where they mix with food. The enzymes digest fat, protein, and carbohydrates so that they can be absorbed by the intestine. Pancreatic juices, therefore, play an important role in maintaining good health. The organ also produces insulin, important in regulating the amount of glucose in the blood. Common diseases of the pancreas include Diabetes, Chronic Pancreatitis, Cystic Fibrosis, pancreatic enzyme deficiency (like Steatorrhea), and pancreatic cancer, among others.

18

Thanks to medical development, the average life-span of cystic fibrosis patients is now approximately 33 years

Cystic Fibrosis (CF) is a genetic disease characterized by excessive secretions of certain glands, causing pancreatic insufficiency and pulmonary disorders. Mucus blocks the pancreatic ducts, which normally secrete the digestive enzymes that allow food to be digested in the small intestine. In order to aid digestion, patients need pancreatic enzyme supplements, specifically formulated multivitamin supplements, and hypercaloric formulas that may help weight maintenance.

Axcan's commitment to the CF community

Patients suffering from Cystic Fibrosis need the support of an extended family. Along with family members, friends, specialized caregivers and not-for-profit organizations, Axcan Pharma supports the CF community, providing quality products and services.

Quality products

Axcan provides a vast array of products in this field such as ULTRASE (pancrelipase), indicated for patients with partial or complete exocrine pancreatic insufficiency caused by Cystic Fibrosis, Chronic Pancreatitis, Pancreatectomy, and Shwachman's Syndrome. Pancrelipase capsules are also effective in controlling Steatorrhea (maldigestion of fat in the feces). VIOKASE (pancrelipase, USP) is indicated for the treatment of exocrine pancreatic insufficiency as associated with, but not limited to, Cystic Fibrosis, Chronic Pancreatitis, Pancreatectomy, or obstruction of the pancreas ducts. Other products for CF patients include ADEKs, SCANDISHAKE, SCANDICAL and FLUTTER.

Axcan sponsors programs to help make a difference

For CF patients, caregivers, and centers, Axcan implemented the following programs to help make a difference in the lives of patients and their families: CareFirst for CF, an innovative program to help ease the financial burden of infant patients diagnosed with CF; Comprehensive Care Program for CF, to provide additional support for CF patients by helping reduce the cost of therapy while providing better quality of care; the Rx Cost Reduction Program, a prescription rebate program to assist patients with the cost of treatment; and the CF Direct Connect Program, providing a dedicated Axcan resource to help ensure that the needs of the CF centers and caregivers are met.

| ULTRASE | VIOKASE | PANZYTRAT | ||

|---|---|---|---|---|

| Capsules | Tablets and powder | Microtablets | ||

| United States and Canada | United States and Canada | Worldwide | ||

| Partial or complete exocrine pancreatic insufficiency | Partial or complete exocrine pancreatic insufficiency | Partial or complete exocrine pancreatic insufficiency |

19

GI DISEASES OF THE BOWEL

Abdominal pain, cramping, fatigue and diarrhea

These are the main symptoms of Inflammatory Bowel Diseases (IBDs), a term used to describe two similar, yet distinct conditions: Crohn's Disease and Ulcerative Colitis. These diseases affect the digestive system and cause intestines to become inflamed, ulcerated, bleed easily, scar and lose the normal smoothness of the inner lining. Axcan markets a wide range of products used to treat inflammation associated with IBD therefore relieving these mild to debilitating symptoms.

20

Crohn's Disease

Affects any part of the gastrointestinal tract, from the mouth to the anus, and is characterized by patches of inflammation with healthy tissue between the diseased areas. The inflammation can extend through every layer of affected bowel tissue. No drug or surgery can cure the disease, although either or both can relieve the symptoms.

Ulcerative Colitis

Affects only the colon, and only a single layer of bowel tissue, the inner lining. The disease always starts in the portion of the colon called the rectum, and may extend as continuous inflammation from there to the rest of the colon. Usually, the disease can be controlled by medication.

IBD affects people regardless of gender, age or race

Most frequently, people are diagnosed between the ages of 15 and 25 years, or 45 and 55 years. No one knows what causes IBD. Also, IBD is unpredictable and many people experience "flare-ups" following which the disease seemingly goes away.

Improving treatment

Axcan is committed to developing novel forms of mesalamine (5-ASA) in order to improve the quality of life for IBD patients. A 1-gram suppository of mesalamine, a once-a-day formulation greatly improving convenience for the patient, has recently been approved by the U.S. Food and Drug Administration. Also, Axcan has recently completed Phase III clinical trials for a patented 4-gram rectal gel formulation of mesalamine for the topical treatment of Distal Ulcerative Colitis. The new formulation should be better tolerated by patients and prove to be easier to administer.

| CANASA | SALOFALK | CORTENEMA | ||

|---|---|---|---|---|

| Suppositories | Suppositories, tablets and enemas | Enemas | ||

| United States | Canada | Canada | ||

| Active ulcerative proctitis | Ulcerative proctitis Distal ulcerative colitis Acute ulcerative colitis | Adjunct in the treatment of non-specific inflammatory bowel diseases |

21

GI GASTRO-INTESTINAL (GI) AND GI-RELATED CANCER

Digestive cancers, the highest incidence and mortality of cancer worldwide

According to the International Digestive Cancer Alliance, in 2004, there will be approximately 3 million new cases of digestive cancers globally, with 2.2 million deaths. Digestive cancers affect the colon and rectum, the esophagus and stomach, and the liver and pancreas.

22

Barrett's esophagus, major risk factor for esophageal adenocarcinoma

Barrett's esophagus is a condition in which the normal lining of the lower part of the esophagus is replaced over time by another type of lining, normally present in the stomach. Usually Barrett's esophagus develops during the process of healing after a chronic injury to the esophageal mucosa such as caused by reflux of gastric juice (GERD) in the esophagus. Continued reflux may cause dysplastic changes progressing from Low-Grade to High-Grade Dysplasia. Such dysplasia may lead to esophageal adenocarcinoma, which is a life-threatening condition. The National Digestive Diseases Information Clearinghouse (NDDIC)(3) estimates that the risk of developing adenocarcinoma is 30 to 125 times greater in people who have Barrett's esophagus than in people who do not.

First Photodynamic Therapy (PDT) indicated for ablation of High-Grade Dysplasia in Barrett's esophagus

PHOTOFRIN (porfimer sodium) for injection is a photosensitizing agent used in the Photodynamic Therapy of tumors. It uses a combination of a photoactive drug and light from a laser, allowing the doctor to specifically target and destroy cells with High-Grade Dysplasia associated with Barrett's esophagus while limiting damage to surrounding healthy tissue. PHOTOFRIN was granted an orphan drug designation for this indication, which guarantees a 7-year marketing exclusivity.

Palliation of other cancers

PDT with PHOTOFRIN is also indicated for palliation of patients with completely or partially obstructing esophageal cancer, completely or partially obstructing endobronchial Non-Small Cell Lung Cancer (NSCLC) and papillary bladder cancer. Patients with NSCLC for whom surgery and radiotherapy are not indicated can also benefit from PHOTOFRIN.

- (3)

- The National Digestive Diseases Information Clearinghouse (NDDIC) is a service of the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK). The NIDDK is part of the National Institutes of Health under the U.S. Department of Health and Human Services.

| PHOTOFRIN | PHOTOBARR | |

|---|---|---|

| Powder for solution for injection | Powder for solution for injection | |

| Canada and Unites States | Worldwide | |

| Ablation of HGD in Barrett's esophagus | Ablation of HGD in Barrett's esophagus | |

| Palliative treatment of esophageal cancer | Palliative treatment of esophageal cancer | |

| Palliative and curative treatment of NSCLC | Palliative and curative treatment of NSCLC | |

| Papillary bladder cancer (Canada) |

23

GI OTHER GASTRO-INTESTINAL DISEASES AND DISORDERS

One in 10 Americans develops an ulcer at some time in his or her life.

A peptic ulcer is a sore on the lining of the stomach or duodenum, which is the beginning of the small intestine. A common occurrence, one cause of peptic ulcer is bacterial infection, but some ulcers are caused by long-term use of Non-Steroidal Anti-Inflammatory Drugs (NSAIDs), like aspirin and ibuprofen. In a few cases, cancerous tumors in the stomach or pancreas can cause ulcers. Peptic ulcers are not caused by stress or eating spicy foods, but these can make ulcers worse.

Effective treatment of active duodenal ulcers

CARAFATE is the U.S. brand, and SULCRATE, the Canadian brand of a sulcrafate-based product indicated for the treatment of active duodenal ulcers. Both of these products are currently available in suspension and tablet dosage forms.

24

One in five Americans has IBS

Irritable Bowel Syndrome (IBS) is a disorder that interferes with the normal functions of the large intestine (colon). Characterized by a group of symptoms such as cramps and abdominal pain, bloating, constipation, and diarrhea, IBS is one of the most common disorders diagnosed by doctors. It occurs more often in women than in men, usually beginning around age 20. IBS causes a great deal of discomfort and distress, but it does not permanently harm the intestines and does not lead to intestinal bleeding or to any serious disease such as cancer. Most people can control their symptoms with diet, stress management, and medications prescribed by their physician. But for some people, IBS can be disabling. They may be unable to work, attend social events, or travel even short distances.

Relieving symptoms of IBS

BENTYL and BENTYLOL (dicyclomine hydrochloride) are antispasmodic and anticholinergic drugs mainly used for the relief of gastrointestinal symptoms associated with Irritable Bowel Syndrome. These products are available in the U.S. and Canada.

About half of the population has hemorrhoids by age 50

The term hemorrhoids refers to a condition in which the veins around the anus or lower rectum are swollen and inflamed. Hemorrhoids may result from straining to move stool. Other contributing factors include pregnancy, aging, chronic constipation, diarrhea, etc. Hemorrhoids are either inside the anus (internal) or under the skin around the anus (external).

Relieving symptoms of hemorrhoids

PROCTOSEDYL (hydrocortisone acetate) is indicated for the reduction of swelling, pain and inflammation of hemorrhoids and other rectal lesions. This product is available in ointment and suppository dosage forms.

| CARAFATE | SULCRATE | BENTYL | BENTYLOL | PROCTOSEDYL | TAGAMET | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Tablets, suspensions United States Active duodenal ulcers | Tablets, suspensions Canada Duodenal and non-malignant gastric ulcers | Tablets, syrup and solution for intra-muscular injection United States Functional bowel and irritable bowel syndrome | Tablets, syrup Canada Irritable Bowel Functional bowel and irritable bowel syndrome | Ointment, suppositories Canada Hemorrhoids and rectal lesions | Tablets France Gastric and duodenal ulcers Esophagitis |

25

ITAX

(itopride hydrochloride) A NOVEL PROKINETIC DRUG TO TREAT MOTILITY DISORDERS

Up to 25% of the population is affected by dyspepsia

Functional Dyspepsia, a disorder of the upper gastrointestinal tract, affects up to 25% of the North American population annually and accounts for up to 5% of all visits to primary care physicians(4). Dyspepsia can be defined as pain or discomfort centered in the upper abdomen, characterized by abdominal fullness, early satiety, bloating, or nausea. The term functional dyspepsia refers to relapsing or chronic dyspepsia in patients without evidence of organic disease to explain the symptoms.

Dual mode of action

ITAX improves GI motility by a dual action mechanism. First, it acts as a dopamine antagonist on D2-receptors thereby increasing the secretion of acetylcholine; and secondly, it prevents hydrolysis of the released acetylcholine by the acetycholinesterase enzyme in the smooth muscles of the upper GI tract. This specific dual action on acetylcholine in the GI tract, by enhancing the acetylcholine-induced gastric contraction, effectively controls the gastric symptoms. ITAX has also been shown to have antiemetic properties.

Superior safety profile

Results from Axcan's recent high dose safety study on ITAX in healthy subjects showed no cardiac adverse drug reaction. Because it is metabolized by a Flavine-dependent Mono-Oxygenase (FMO) enzyme rather than by the Cytochrome P450 enzyme system, responsible for most drug metabolism, metabolic interactions and cardiotoxi-city are not expected from Itopride.

Therapeutic void for a distressing disorder

Currently in North America, there is no safe and efficacious treatment for Functional Dyspepsia. The void left by the first generation of gastroprokinetic drugs has yet to be filled because of significant cardiac side effects and other serious side effects. Currently, there is no FDA-approved drug for the treatment of motility disorders such as Functional Dyspepsia and Diabetic Gastroparesis. To date, the patients living with these distressing disorders have no satisfying therapeutic option available to them.

Itopride Hydrochloride in the Treatment of Functional Dyspepsia

Dr. Richard H. Hunt, Professor, Division of Gastroenterology,

McMaster University, Hamilton, Canada

Some of the most important developments in the treatment of gastrointestinal disease over the past thirty years have been for patients with upper gastrointestinal disorders. The principal areas of clinical need are for disorders of gastric statis and delayed gastric emptying such as may occur in patients with Diabetes Mellitus and Functional Dyspepsia and in patients with Gastroesophageal Reflux Disease especially those without heartburn or who experience regurgitation or high volume reflux. Itopride is a prokinetic drug, which also has antiemetic properties and has been available in Japan since 1995. In Caucasian populations, initial studies with Itopride suggest that it is safe and effective in patients with Functional Dyspepsia with a significant benefit for symptoms of pain and fullness and with a significant positive impact on quality of life.

September 17, 2004

Itopride in the treatment of Functional Dyspepsia

Scientific presentation of Dr. Richard Hunt

Mont-St-Hilaire, Quebec

- (4)

- Talley et al Gastroenterology 1992:102;1259-1268

26

ITAX Clinical Program on Track

Enrollment for the two Phase III studies, being conducted in 90 North American centers and in 75 Western European centers, is underway and is expected to be completed in the third quarter of fiscal year 2005. More recently, a cardiac safety study, to examine ITAX in doses of up to 400mg three times a day, was completed, and results showed no cardiac adverse drug reaction. Axcan hopes to have results eight weeks after the final day of recruitment, which would allow filing an NDA, NDS and EMEA by the end of the first quarter of fiscal year 2006.

In addition, Axcan aims to study ITAX as a treatment for Diabetic Gastroparesis, a very serious condition that greatly affects quality of life.

ITAX for the Treatment of Diabetic Gastroparesis

Pursuing another unmet need

Diabetic Gastroparesis is the secondary indication that Axcan intends to pursue for ITAX. Gastroparesis is a neuromuscular disease characterized by delayed or absent emptying of the stomach. Gastroparesis occurs when the stomach's enteric nerves and/or muscle cells become damaged or destroyed. In addition, the disease can occur primarily as a result of nerve or muscle damage further down the digestive tract, which causes gastric contents to back up and pool in the stomach. The most prevalent secondary cause of Gastroparesis is Diabetes. Symptoms can include severe stomach muscle spasm, heartburn, nausea, vomiting and significant weight loss.

Almost 50% of Type I and Type II Diabetics have Gastroparesis

Gastroparesis occurs in Diabetes as a result of high blood glucose levels creating chemical and structural changes in the nerves and muscles of the stomach. Other secondary causes of the disease include Parkinson's Disease, migraine, connective tissue diseases (such as lupus and scleroderma) or failed gas-trectomy (a procedure now used to attempt to alleviate obesity). A recent study estimates that more than 5 million people in the U.S. suffer from either the primary or secondary form of Gastroparesis. In Diabetes, Gastroparesis is a significant contributor to loss of blood glucose control and diabetic crisis.

27

HEPENAX

(L-ornithine L-aspartate) A NOVEL TREATMENT FOR HEPATIC ENCEPHALOPATHY

When the liver fails, no other organ can take over its role

The liver performs a number of vital functions such as converting food into energy for the body's growth and maintenance as well as removing and converting toxins for elimination. Repeated or extensive damage to the liver caused by diseases such as alcoholism and Hepatitis C may ultimately result in cirrhosis, a severe degenerative disorder in which liver cells are destroyed and replaced by scar tissue, thus impairing its regenerative capacity.

PSE, a frequent and debilitating complication of cirrhosis

Porto-Systemic Encephalopathy (PSE) is a term used for Hepatic Encephalopathy (HE) in cirrhotic patients and, more rarely, in patients with portosystemic shunting without liver disease. HE, present in more than 28% of patients with cirrhosis, is the result of a diminished hepatic reservoir and inability to detoxify some toxins that originate in the bowel.

Ammonia is believed to be the main cause of HE

Ammonia is naturally produced by bacterial degradation of food proteins in the intestine. Normally, it is converted to urea by the liver and then excreted in the urine. However, because of the liver's impaired detoxifying capacity, increased ammonia levels enter the systemic circulation causing a wide variety of signs and symptoms. The most typical are changes in consciousness, intellectual function, and behavior as well as neuromuscular abnormalities. In severe cases, the symptoms can range from brain oedema to coma and even death.

No safe and effective therapy exists

Today, no available therapies have conclusively proven to be safe and effective in the treatment of HE. The conventional treatments have included protein intake restriction; use of non-absorbable disaccharides limited by the occurrence of flatulence, cramps and diarrhea; and antibiotics such as neomycin, which are associated with nephrotoxicity and ototoxicity.

28

Efficacy shown in seven Phase II studies

Developed and marketed by Merz Pharmaceuticals GmbH, L-ornithine L-aspartate (LOLA) has an excellent safety profile and has been shown to reduce ammonia blood levels and improve mental function in patients with HE. LOLA is believed to reduce ammonia levels by 1) enhancing the rate of the urea cycle, 2) acting as a substrate for the enzyme asparagine synthetase, which catalyses the reaction between ammonia and aspartate in the cells, and 3) acting as a substrate for glutamine synthetase, an enzyme which utilizes ammonia in the muscle for the synthesis of glutamine, thereby lowering blood ammonia concentration.

L-ornithine L-aspartate in the Management of Porto-Systemic Encephalopathy

Dr. Rajiv Jalan, Institute of Hepatology,

University College London Medical School, London, U.K.

Worldwide, deaths from cirrhosis, are increasing. Hepatic Encephalopathy (HE) is one of the most debilitating complications of cirrhosis. Currently, there are no available therapies that have been conclusively shown successful in the treatment of encephalopathy. The studies so far provide a compelling argument for L-ornithine L-aspartate (LOLA) in the treatment of HE. From the pathophysiological perspective, LOLA enhances the body's ability to detoxify ammonia in the muscle, central to the pathogenesis of HE. The current clinical plan by Axcan is likely to provide data required for approval by the FDA.

September 17, 2004

L-ornithine L-aspartate in the Management of Porto-Systemic Encephalopathy

Scientific Presentation of Dr. Rajiv Jalan

Mont-St-Hilaire, Quebec

29

A DEEP PIPELINE

PHOTOFRIN PDT in the Treatment of Cholangiocarcinoma

Dr. Steve Pereira, University College Medical School, London, U.K.

Cholangiocarcinoma (cancer of the bile ducts) and cancer of the gall bladder are tumors of the biliary tract that are considered as one pathological entity (biliary tract carcinoma, BTC). Recently published, a multicentre, randomised, controlled trial of repeated PDT with stenting versus stenting alone for unresectable, advanced cholangiocarcinoma was discontinued early by the monitoring committee after 39 patients had been randomised as there was a dramatic five-fold survival advantage in the PDT group, with an average survival at the time of publication of 493 days compared with 98 days in the stent alone group. Further multicentre studies, to confirm these exciting results and to define the likely important role of PDT in relation to best supportive care and other cancer therapies, are underway.

September 17, 2004

PHOTOFRIN PDT in the Treatment of Cholangiocarcinoma

Scientific Presentation of Dr. Steve Pereira

Mont-St-Hilaire, Quebec

Ursodeoxycholic Acid-disulfate in Liver Disease and Transplant

Kenneth D.R. Setchell(2), Nigel D. Heaton(2), Hector Vilca-Melendez(2), Clinical Mass Spectrometry Department, Cincinnati Children's Hospital Medical Center, Cincinnati, Ohio, U.S.A.(1), and Liver Transplant Surgical Service, King's College Hospital, London, U.K.(2)

(...) results from the successful completion of a 2-year study using an animal model of colon cancer were reported this year and showed that ursodiol disulfate (SUDCA) is significantly superior to ursodiol (UDCA) in colon cancer prevention in this model. Oral administration of SUDCA led to a 50% reduction in tumor burden, and 55% of animals were without tumors when challenged with the potent carcinogen, azoymethane. Completion of this proof-of-concept study justifies continuing evaluation of SUDCA in humans at risk for colon cancer.

Since SUDCA is highly hydrophilic it is ideally suited to intravenous use. In the last year we have initiated studies aimed at investigating the choleretic properties of SUDCA in an experimental pig model for human liver transplantation as a prelude to performing studies in human donors. The goal was to first demonstrate that SUDCA has a marked stimulatory effect on bile-flow that will be beneficial in improving initial function of the transplanted liver and later we will examine whether the highly hydrophilic property of SUDCA can protect the liver from ischemic damage that occurs during organ retrieval. Initial bile-flow following transplantation has been found to be associated with better graft function in humans and for this reason this has been first examined. (...) Based on these preliminary studies, we conclude that SUDCA is a potent choleretic bile acid, superior to UDCA, and its aqueous solubility makes it a potentially useful therapeutic agent for intravenous use in human liver transplantation. Its role as a protective agent from ischemia-reperfusion injury is presently under investigation.

September 17, 2004

Ursodeoxycholic Acid-disulfate in Liver Disease and Transplant

Scientific presentation of Dr. Kenneth D.R. Setchell

Mont-St-Hilaire, Quebec

30

| PRODUCT | INDICATION | STAGE OF DEVELOPMENT | TIMELINES | |||

|---|---|---|---|---|---|---|

| CANASA (4-gram mesalamine rectal gel) | Treatment of Distal Ulcerative Colitis | Phase III study results Launch | Q2 2005 H2 2006 | |||

ITAX (itopride hydrochloride, 100mg oral tablets) | Treatment of Functional Dyspepsia Treatment of Diabetic Gastroparesis | Cardiac Safety Study NDA, NDS and EMEA filing Launch Launch | Q1 2005 Q1 2006 H1 2007 FY 2008 | |||

PHOTOFRIN (porfimer sodium) | Treatment of Cholangiocarcinoma | Start of Phase III study | Q1 2005 | |||

HEPENAX (L-ornithine L-aspartate) | Treatment of Porto-Systemic Encephalopathy | Dose ranging study Phase III study (ies) NDA, NDS and EMEA filing Launch | Q4 2005 H2 2007 Q4 2007 H2 2008 | |||

URSODIOL DISULFATE (SUDCA) (oral tablets) | Chemoprevention of Colorectal Polyps | Animal toxicity studies Phase I study | Q2 2005 FY 2005 | |||

URSODIOL DISULFATE (SUDCA) (injectable formulation) | Total Parental Nutrition (TPN) Cholestatis Organ Preservation in Liver Transplant | — — | — — | |||

NCX-1000 (nitric oxide-releasing derivative of ursodiol) | Treatment of Portal Hypertension | Phase II studies | FY 2005 | |||

NMK-150 (high protease pancrelipase) | Pain Management in the Treatment of Chronic Small Duct Pancreatitis | Start of clinical development | FY 2005 | |||

NMK-250 (bacterial lipase) | Steatorrhea | Formulation work | Q2 2005 |

31

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This discussion should be read in conjunction with the information contained in Axcan's consolidated financial statements and the related notes thereto. All amounts are in U.S. dollars.

OVERVIEW

Axcan is a leading specialty pharmaceutical company concentrating in the field of gastroenterology, with operations in North America and Europe. Axcan markets and sells pharmaceutical products used in the treatment of a variety of gastrointestinal diseases and disorders. The Company seeks to expand its gastrointestinal franchise by in-licensing products and acquiring products or companies, as well as developing additional products and expanding indications for existing products. Axcan's current products include ULTRASE, PANZYTRAT and VIOKASE for the treatment of certain gastrointestinal symptoms, related to cystic fibrosis in the case of ULTRASE and PANZYTRAT; URSO and DELURSAN for the treatment of certain cholestatic liver diseases; SALOFALK and CANASA for the treatment of certain inflammatory bowel diseases; and PHOTOFRIN for the treatment of certain types of gastrointestinal cancers and other conditions. In addition, as at September 30, 2004, Axcan had one product pending approval, a new formulation for a product currently marketed in the United States. Axcan also has a number of other pharmaceutical projects in all phases of development including ITAX for the treatment of functional dyspepsia. Axcan reported revenue of $243.6 million and operating income of $76.8 million for the year ended September 30, 2004.

Much of Axcan's recent sales growth is derived from sales in the United States and from sales by its French subsidiary, following recent acquisitions. During the first quarter of fiscal 2003, Axcan acquired the worldwide rights to the PANZYTRAT enzyme product line from Abbott Laboratories ("Abbott") and the rights to DELURSAN, an ursodiol 250mg tablet, from Aventis Pharma S.A. ("Aventis") for the French market. During the first quarter of fiscal 2004, Axcan acquired the rights to a group of products from Aventis for a cash purchase price of $145.0 million. These products are CARAFATE and BENTYL for the U.S. market and SULCRATE, BENTYLOL and PROCTOSEDYL for the Canadian market (collectively, "AVAX" product line). Revenue from sales of Axcan's products in the United States was $166.7 million (68.4% of total revenue) for the year ended September 30, 2004, compared to $113.9 million (63.6% of total revenue) for fiscal 2003 and $100.1 million for fiscal 2002. In Canada, revenue was $28.0 million (11.5% of total revenue) for the year ended September 30, 2004, compared to $20.6 million (11.5% of total revenue) for fiscal 2003 and $17.4 million for fiscal 2002. In Europe, revenue was $48.7 million (20.0% of total revenue) for the year ended September 30, 2004, compared to $44.5 million (24.8% of total revenue) for fiscal 2003 and $14.8 million for fiscal 2002.

Axcan's revenue historically has been and continues to be principally derived from sales of pharmaceutical products to large pharmaceutical wholesalers and large chain pharmacies. Axcan utilizes a "pull-through" marketing approach that is typical of pharmaceutical companies. Under this approach, Axcan's sales representatives demonstrate the features and benefits of its products to gastroenterologists who may write their patients prescriptions for Axcan's products. The patients, in turn, take the prescriptions to pharmacies to be filled. The pharmacies then place orders with the wholesalers or, in the case of large chain pharmacies, their distribution centres, to whom Axcan sells its products.

Axcan's expenses are comprised primarily of selling and administrative expenses (including marketing expenses), cost of goods sold (including royalty payments to those companies from whom Axcan licenses some of its products), research and development expenses as well as depreciation and amortization.

Axcan's annual and quarterly operating results are primarily affected by three factors: wholesaler buying patterns; the level of acceptance of Axcan's products by gastroenterologists and their patients; and the extent of Axcan's control over the marketing of its products. Wholesaler buying patterns, including a tendency to increase inventory levels prior to an anticipated or announced price increase, affect Axcan's operating results by shifting revenue between quarters. To maintain good relations with wholesalers, Axcan typically gives prior notice of price increases. The level of patient and physician acceptance of Axcan's products, as well as the availability of similar therapies, which may be less effective but also less expensive than some of Axcan's products, impact Axcan's revenues by driving the level and timing of prescriptions for its products.

32

CRITICAL ACCOUNTING POLICIES

Axcan's consolidated financial statements are prepared in accordance with generally accepted accounting principles in the United States of America ("U.S. GAAP"), applied on a consistent basis. Axcan's critical accounting policies include the use of estimates, revenue recognition, the recording of research and development expenses and the determination of the useful lives or fair value of goodwill and intangible assets. Some of our critical accounting policies require the use of judgment in their application or require estimates of inherently uncertain matters. Although our accounting policies are in compliance with U.S. GAAP, a change in the facts and circumstances of an underlying transaction could significantly change the application of our accounting policies to that transaction, which could have an effect on our financial statements. Discussed below are those policies that we believe are critical and require the use of complex judgment in their application.

USE OF ESTIMATES

The preparation of financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the recorded amounts of assets and liabilities, the disclosure of contingent assets and liabilities as of the date of the financial statements and the disclosure of recognized amounts of revenues and expenses during the year. Significant estimates and assumptions made by management include the allowance for accounts receivable and inventories, reserves for product returns, rebates and chargebacks, the classification of intangible assets between finite and indefinite life, useful lives of long-lived assets, the expected cash flows used in evaluating long-lived assets, goodwill and investments for impairment, contingency provisions and other accrued charges. These estimates were made using the historical information available to management. The Company reviews all significant estimates affecting the financial statements on a recurring basis and records the effect of any adjustment when necessary. Actual results could differ from those estimates.

REVENUE RECOGNITION

Revenue is recognized when the product is shipped to the Company's customer, provided the Company has not retained any significant risks of ownership or future obligations with respect to the product shipped. Revenue from product sales is recognized net of sales discounts, allowances, returns, rebates and chargebacks. In certain circumstances, returns or exchanges of products are allowed under the Company's policy, and provisions are maintained accordingly. Amounts received from customers as prepayments for products to be shipped in the future are reported as deferred revenue.

GOODWILL AND INTANGIBLE ASSETS

Axcan's goodwill and intangible assets are stated at cost, less accumulated amortization. Since October 1, 2001, the Company does not amortize goodwill and intangible assets with an indefinite life. However, management evaluates the value of the unamortized portion of goodwill and intangible assets annually, by comparing the carrying value to the future benefits of the Company's activities or the expected sale of pharmaceutical products. Should there be a permanent impairment in value or if the unamortized balance exceeds recoverable amounts, a write-down will be recognized for the current year. To date, Axcan has not recognized any significant permanent impairment in value except for an amount of $83,000 of goodwill for the year ended September 30, 2004. Intangible assets with finite life are amortized over their estimated useful lives.

RESEARCH AND DEVELOPMENT EXPENSES

Research and development expenses are charged to operations in the year they are incurred. Acquired in-process research and development having no alternative future use is written off at the time of acquisition. The cost of intangibles that are acquired from others for a particular research and development project, with no alternative use, is written off at the time of acquisition.

ACQUISITION OF COMPANIES

On November 7, 2001, Axcan acquired all the outstanding shares of Laboratoires Entéris S.A.S. ("Entéris"), a company specializing in the distribution of gastrointestinal products in France. The acquisition cost, including transaction expenses, amounted to $23.0 million and was paid in cash.

33

On April 17, 2002, Axcan acquired all of the oustanding shares and certain related assets of Laboratoire du Lactéol du Docteur Boucard S.A. ("Lactéol"). Lactéol specializes in the manufacturing and distribution of gastrointestinal products in France. The acquisition cost, including transaction expenses, amounted to $13.1 million and was paid through the issuance of 365,532 common shares of the Company and the payment of $8.4 million in cash.

The acquisition costs for both transactions have been allocated to the assets and liabilities acquired according to their estimated fair values at the acquisition dates. The operating results of Entéris and Lactéol have been included in the consolidated financial statements from their respective acquisition dates.

ACQUISITION OF PRODUCTS

On November 18, 2003, the Company acquired the rights to the AVAX product line from Aventis. The $145.0 million purchase price was paid out of Axcan's cash on hand.

On August 29, 2003, the Company acquired an exclusive license for North America, the European Union and Latin America, from Abbott to develop, manufacture and market ITAX, a patented gastroprokinetic drug. Under the terms of this license agreement, the Company paid $10 million in cash and assumed $2 million in research contract liability. This product is in development, has not reached technological feasibility and has no known alternative uses; therefore, its acquisition was deemed to be acquired in-process research and was expensed in the period of acquisition.

On December 10, 2002, the Company acquired the rights to the Ursodiol 250mg tablets DELURSAN for the French market from Aventis, for a cash purchase price of $22.8 million.

On December 3, 2002, the Company acquired the worldwide rights to the PANZYTRAT enzyme product line from Abbott for a cash purchase price of $45.0 million.

During a transition period, the seller in each of these acquisition transactions acts as selling agent for the management of these products. For the year ended September 30, 2004, sales of these products were still managed in part by the sellers. Axcan includes in its revenue the net sales from such products less corresponding cost of goods sold and other seller related expenses. Consequently, although net sales of such products for the year ended September 30, 2004, were $7,667,940 ($14,255,979 in 2003), the Company only included in its revenue an amount of $4,685,673 ($9,463,645 in 2003) representing the net sales less cost of goods sold and other seller related expenses.

RESULTS OF OPERATIONS

The following table sets forth, for the years indicated, the percentage of revenue represented by items in Axcan's consolidated statements of operations:

| For the years ended September 30 | 2004 | 2003 | 2002 | ||||

|---|---|---|---|---|---|---|---|

| | % | % | % | ||||

| Revenue | 100.0 | 100.0 | 100.0 | ||||

| Cost of goods sold | 22.2 | 24.8 | 25.7 | ||||

| Selling and administrative expenses | 31.4 | 35.2 | 37.3 | ||||

| Research and development expenses | 8.2 | 6.8 | 6.7 | ||||

| Acquired in-process research | — | 6.7 | — | ||||

| Depreciation and amortization | 6.7 | 4.5 | 5.7 | ||||

| 68.5 | 78.0 | 75.4 | |||||

| Operating income | 31.5 | 22.0 | 24.6 | ||||

| Financial expenses | 2.8 | 2.4 | 0.7 | ||||

| Interest income | (0.3 | ) | (0.9 | ) | (0.7 | ) | |

| Loss (gain) on foreign exchange | (0.1 | ) | — | 0.2 | |||

| Takeover-bid expenses | — | 2.1 | — | ||||

| 2.4 | 3.6 | 0.2 | |||||

| Income before income taxes | 29.1 | 18.4 | 24.4 | ||||

| Income taxes | 9.1 | 7.3 | 8.4 | ||||

| Net income | 20.0 | 11.1 | 16.0 | ||||

34

QUARTERLY RESULTS

(amounts in thousands of dollars, except share related data)

| | | | Net income (loss) per share | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Quarter | | Net income (loss) | |||||||

| Revenue | Basic | Diluted | |||||||

| | $ | $ | $ | $ | |||||

| 2004 | |||||||||

| First | 57,565 | 10,435 | 0.23 | 0.23 | |||||

| Second | 63,192 | 12,421 | 0.27 | 0.24 | |||||

| Third | 62,005 | 12,552 | 0.28 | 0.25 | |||||

| Fourth | 60,872 | 13,320 | 0.29 | 0.26 | |||||

2003 | |||||||||

| First | 37,846 | 6,557 | 0.15 | 0.14 | |||||

| Second | 45,621 | 8,933 | 0.20 | 0.20 | |||||

| Third | 46,877 | 6,339 | 0.14 | 0.14 | |||||

| Fourth | 48,740 | (1,904 | ) | (0.04 | ) | (0.04 | ) | ||

YEAR ENDED SEPTEMBER 30, 2004

COMPARED TO YEAR ENDED SEPTEMBER 30, 2003

REVENUE

For the year ended September 30, 2004, revenue was $243.6 million compared to $179.1 million for the preceding fiscal year, an increase of 36.0%. This increase in revenue primarily resulted from $41.8 million in U.S. and Canadian sales of the AVAX product line which was acquired in November 2003 and strong sales of CANASA in the U.S. Revenues from sales made by the French subsidiary, following the acquisition of DELURSAN as well as the PANZYTRAT product line, also contributed to the increase.

PRODUCT SALES

Key sales figures for fiscal 2004 are as follows:

- •

- Worldwide sales of pancreatic enzymes (ULTRASE, PANZYTRAT and VIOKASE) amounted to $57.6 million, a decrease of 1.0% over fiscal 2003 sales of pancreatic enzymes. PANZYTRAT acquired in the first quarter of fiscal 2003, accounted for $10.2 million of these sales in fiscal 2003 and $13.5 million in fiscal 2004;

- •

- Worldwide sales of ursodiol (URSO 250, URSO DS and DELURSAN) increased 4.0% to $56.1 million. DELURSAN acquired in the second quarter of fiscal 2003 accounted for $6.9 million of these sales in fiscal 2003 and $ 10.8 million in fiscal 2004;

- •

- Sales of mesalamine (CANASA and SALOFALK) amounted to $50.3 million, a 92.0% increase from the prior year. This increase offsets the 24% decrease announced last year and reflects not only the increase in prescriptions but also the fluctuations in wholesalers buying patterns. Often, customers will buy in advance of pre-announced price increases or in anticipation of price increases, thus shifting revenue from one period to another.

- •

- Sales of the AVAX product line amounted to $41.8 million. The AVAX product line was acquired in November 2003.

- •

- Sales of PHOTOFRIN and other products in North America amounted to $14.1 million, the same total as for the prior year.

- •

- Sales of other products in Europe, mainly LACTÉOL and TAGAMET amounted to $23.7 million, a 14% decrease over the prior year. This decrease is mainly due to lower sales of TAGAMET following changes in the regulatory rules applicable to this product.

COST OF GOODS SOLD

Cost of goods sold consists principally of costs of raw materials, royalties and manufacturing costs. Axcan outsources most of its manufacturing requirements. Cost of goods sold increased $9.7 million (21.8%) to $54.2 million for the year ended September 30, 2004, from $44.5 million for the preceding fiscal year. As a percentage of revenue, cost of goods sold for the year ended September 30, 2004, decreased as compared to the preceding fiscal year from 24.8% to 22.2%. This decrease in the cost of goods sold as a percentage of revenue was due to the increase in sales of products with a higher margin in the United States and an improved margin in Europe.

35

SELLING AND ADMINISTRATIVE EXPENSES

Selling and administrative expenses consist principally of salaries and other costs associated with Axcan's sales force and marketing activities Selling and administrative expenses increased $13.3 million (21.1%) to $76.4 million for the year ended September 30, 2004, from $63.1 million for the preceding fiscal year. This increase is mainly due to an increase in our sales force as a result of the recent acquisition of additional products.

RESEARCH AND DEVELOPMENT EXPENSES

Research and development expenses consist principally of fees paid to outside parties that Axcan uses to conduct clinical studies and to submit governmental approval applications on its behalf as well as the salaries and benefits paid to its personnel involved in research and development projects. Excluding acquired in-process research, research and development expenses increased $7.8 million (64.5%) to $19.9 million for the year ended September 30, 2004, from $12.1 million for the preceding fiscal year. This increase is mainly due to the development of ITAX, acquired in August 2003, for the treatment of functional dyspepsia.

ACQUIRED IN-PROCESS RESEARCH

The acquired in-process research of $12.0 million for the year ended September 30, 2003, was a result of the acquisition of an exclusive license for North America, the European Union and Latin America, from Abbott to develop, manufacture and market ITAX, a patented gastroprokinetic drug. Under the terms of this license agreement, Axcan paid $10.0 million and assumed $2.0 million in research liability. As this product had not reached technological feasibility and had no known alternative use, it was considered to be acquired in-process research and was expensed in the fourth quarter of the year ended September 30, 2003, the period of acquisition.

DEPRECIATION AND AMORTIZATION

Depreciation and amortization consists principally of the amortization of intangible assets with a finite life. Intangible assets include trademarks, trademark licenses and manufacturing rights. Depreciation and amortization increased $8.3 million (102.5%) to $16.4 million for the year ended September 30, 2004, from $8.1 million for the preceding fiscal year. The increase is mainly due to the amortization of the AVAX product line acquired from Aventis on November 18, 2003, and of TAGAMET which was reclassified from intangible assets with an indefinite life to intangible assets with a finite life on October 1, 2003.

FINANCIAL EXPENSES

Financial expenses consist principally of interest and fees paid in connection with money borrowed for acquisitions. Financial expenses increased $2.6 million (60.5%) to $6.9 million for the year ended September 30, 2004, from $4.3 million for the preceding fiscal year. This increase is mainly due to the Company recognizing a full year's worth of interest expense on the $125.0 million aggregate principal amount of 41/4% convertible subordinated notes due 2008 which were issued on March 5, 2003, and amortization of deferred debt issue expenses.

TAKEOVER-BID EXPENSES

On April 10, 2003, Axcan made an unsolicited cash tender offer of $8.75 per share for all of the outstanding shares of common stock of Salix Pharmaceuticals Inc. ("Salix"), which was subsequently increased to $10.50 per share. On June 27, 2003, the offer for all outstanding shares of Salix expired without acceptance or extension. Total costs related to the offer were $3.7 million and were expensed during the quarter ended June 30, 2003, thus reducing net income by approximately $2.4 million, or $0.05 per share for the year ended September 30, 2003.

INCOME TAXES

Income taxes amounted to $22.3 million for the year ended September 30, 2004, compared to $13.0 million for the year ended September 30, 2003. The effective tax rates were 31.4% for the year ended September 30, 2004, and 39.5% for the year ended September 30, 2003. The acquired in-process research is deductible at a lower rate than most operating expenses. As discussed below in "net income", excluding acquired in-process research and takeover-bid expenses, the effective tax rate was 31.4% for the year ended September 30, 2003.

36

NET INCOME

Net income was $48.7 million or $1.08 of basic income per share and $0.98 of diluted income per share, for the year ended September 30, 2004, compared to $19.9 million or $0.44 of both basic and diluted income per share for the preceding year. The weighted average number of common shares outstanding used to establish the basic per share amounts increased from 44.9 million for the year ended September 30, 2003, to 45.3 million for the year ended September 30, 2004, following the exercise of options previously granted pursuant to Axcan's stock option plan. The weighted average number of common shares used to establish the diluted per share amounts increased from 45.6 million for the year ended September 30, 2003, to 52.8 million for the year ended September 30, 2004, because the shares issuable under the convertible subordinated notes are included because a trigger event giving holders the right to convert their notes occurred in each of the second, third and fourth quarters of this fiscal year as a result of the stock trading price exceeding 110% of the conversion price of the convertible notes.

Net income (in thousands of dollars), basic income per share and diluted income per share excluding takeover-bid expenses, acquired in-process research and related income taxes for the years ended September 30, 2004, and 2003, were as follows:

| | For the years ended September 30 | |||||

|---|---|---|---|---|---|---|

| | 2004 | 2003 | ||||

| | $ | $ | ||||

| Net income in accordance with U.S. GAAP | 48,728 | 19,925 | ||||

| Plus: Takeover-bid expenses | — | 3,697 | ||||

| Acquired in-process research | — | 12,000 | ||||

| Less: Related income taxes | — | (2,272 | ) | |||

| Net income excluding takeover-bid expenses, acquired in-process research and related income taxes | 48,728 | 33,350 | ||||

| Income per share excluding takeover-bid expenses, acquired in-process research and related income taxes | ||||||

| Basic | 1.08 | 0.74 | ||||

| Diluted | 0.98 | 0.73 | ||||

This measure of net income, basic income per share and diluted income per share excluding certain items is a non-GAAP measure that does not have a standardized meaning and, as such, is not necessarily comparable to similarly titled measures presented by other companies. This measure is provided to assist our investors in assessing Axcan's operating performance. We believe the presentation of this non-GAAP measure provides useful information because it eliminates certain expenses unrelated to our operations and because it provides similar information for period-to-period comparisons. Investors should consider this non-GAAP measure in the context of Axcan's U.S. and Canadian GAAP results of operations.

Excluding takeover-bid expenses, acquired in-process research and related income taxes, net income for the year ended September 30, 2004, was $48.7 million or $1.08 of basic income per share and $0.98 of diluted income per share compared to $33.4 million of net income or $0.74 of basic income per share and $0.73 of diluted income per share for the year ended September 30, 2003.

YEAR ENDED SEPTEMBER 30, 2003, COMPARED TO YEAR ENDED SEPTEMBER 30, 2002

REVENUE

Revenue increased $46.7 million (35.3%) to $179.1 million for the year ended September 30, 2003, from $132.4 million for the preceding fiscal year. This increase in revenue resulted primarily from sales generated by Axcan's French subsidiary, following the acquisitions of Entéris and Lactéol and the PANZYTRAT and DELURSAN product lines. Strong sales of URSO in North America also contributed to the increase. Revenue from Europe, including domestic and foreign sales, amounted to $44.5 million for the year ended September 30, 2003, compared to $14.8 million for the year ended September 30, 2002.

37

PRODUCT SALES

Key sales figures for fiscal 2003 are as follows:

- •

- Worldwide sales of pancreatic enzymes (ULTRASE, PANZYTRAT and VIOKASE) amounted to $57.9 million, an increase of 47% over fiscal 2002 sales of pancreatic enzymes. PANZYTRAT acquired in the first quarter of fiscal 2003, accounted for $10.2 million of these sales;

- •

- Worldwide sales of ursodiol (URSO 250, URSO DS and DELURSAN) increased 79% to $53.9 million. DELURSAN acquired in the second quarter of fiscal 2003 accounted for $6.9 million of these sales;

- •

- Sales of mesalamine (CANASA and SALOFALK) amounted to $26.2 million, a 24% decrease from the prior year. This decrease was mainly due to the resolution of short product supply, that occurred in fiscal 2002, for a product competing with CANASA in an associated indication.

- •

- Sales of PHOTOFRIN and other products in North America amounted to $14.1 million, an increase of 3%.

- •

- Sales of other products in Europe, mainly LACTÉOL and TAGAMET, amounted to $27.6 million, a 76% increase over the prior year.

COST OF GOODS SOLD