UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-10067 |

|

Eaton Vance Variable Trust |

(Exact name of registrant as specified in charter) |

|

The Eaton Vance Building, 255 State Street, Boston, Massachusetts | | 02109 |

(Address of principal executive offices) | | (Zip code) |

|

Alan R. Dynner The Eaton Vance Building, 255 State Street, Boston, Massachusetts 02109 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (617) 482-8260 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2005 | |

| | | | | | | | | |

Item 1. Reports to Stockholders

Annual Report December 31, 2005

EATON VANCE

VT

FLOATING-

RATE

INCOME

FUND

IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS, AND PROXY VOTING

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy ("Privacy Policy") with respect to nonpublic personal information about its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer's account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer's account (i.e., fund shares) is held in the name of a third-party financial adviser/broker-dealer, it is likely that only such adviser's privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance's Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission (the "SEC") permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called "householding" and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and its underlying Portfolio (if applicable) will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the Securities and Exchange Commision's website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC's public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds' and Portfolios' Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to Portfolio securities during the most recent 12 month period ended June 30, without charge, upon request, by calling 1-800-262-1122. This description is also available on the SEC's website at www.sec.gov.

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

MANAGEMENT'S DISCUSSION OF FUND PERFORMANCE

The Fund

Performance for the year ended December 31, 2005

• The Fund distributed $0.402 in income dividends during the year ended December 31, 2005. Based on a $10.08 net asset value on December 31, 2005, the Fund had a distribution rate of 4.82%.(1) The Fund’s SEC 30-day yield at December 31, 2005 was 4.81%.(2)

• The Fund had a total return of 3.86% during the year ended December 31, 2005.(3) That return was the result of a decrease in net asset value per share to $10.08 on December 31, 2005 from $10.10 on December 31, 2004 and the reinvestment of all dividends.

• For comparison, the S&P/LSTA Leveraged Loan Index – an unmanaged loan market index – had a return of 5.06% for the year ended December 31, 2005.(4)

Investment Environment

• Loan market fundamentals remained relatively strong during the fiscal year ended December 31, 2005. Despite historically low credit spreads, default rates remained below historical averages. Technical factors, meanwhile, have also been favorable. Demand outstripped supply for much of the period; however, in recent months, increasing supply has brought demand/supply into better balance.

• The Federal Reserve continued to push short-term interest rates higher, raising its Federal Funds rate – a short-term interest rate benchmark – by 25 basis points (0.25%) on eight occasions during the year ended December 31, 2005. With their interest rate reset provisions, floating-rate loans have historically generated higher income returns in response to increases in the short-term interest rate level.

The Fund’s Investments

• The Fund’s investment objective is to provide a high level of current income. To do so, the Fund invests primarily in income producing, floating rate loans and other floating rate debt securities.

• The Fund’s investments included 254 borrowers at December 31, 2005, ranging across 35 different industries. The Fund’s average loan size was just 0.35% of net assets, and no industry constituted more than 6% of the Fund. Building and development (including manufacturers of building products and companies that manage/own apartments, shopping malls and commercial office buildings, among others), chemicals and plastics, health care, telecommunications and containers and glass were the Fund’s largest industry weightings.*

• The loan market performed well, as short-term interest rates rose throughout the fiscal year. The London-Interbank Offered Rate (LIBOR) – the benchmark over which loan interest rates are typically set – kept pace with the Federal Reserve’s rate hikes; and, yield spreads narrowed to just below their historical range.

• In the wake of Hurricanes Katrina and Rita, management identified several companies that were directly impacted by the storms. While these loans suffered very little price impact, management nonetheless reduced exposure to the hardest-hit companies, generally at prices above par. The hurricanes had little initial overall impact on the Fund.

• We continued to emphasize the importance of rigorous credit selection, discipline and careful monitoring. We believe that the difference in performance between the Fund and the S&P/LSTA Leveraged Loan Index was the result of our more defensive stance versus this unmanaged Index; a stance, we believe, that may produce higher and more stable risk-adjusted total returns over time.(4)

* Holdings and industry weightings are subject to change due to active management.

The views expressed in this report are those of the portfolio managers and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for an Eaton Vance fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund.

(1) The Fund’s distribution rate represents actual distributions paid to shareholders and is calculated daily by dividing the last distribution per share (annualized) by the net asset value.

(2) The Fund’s SEC yield is calculated by dividing the net investment income per share for the 30-day period by the net asset value at the end of the period and annualizing the result.

(3)There is no sales charge. Insurance-related charges are not included in calculations of returns. Please refer to the report for your insurance contract for performance data reflecting insurance-related charges.

(4) It is not possible to invest directly in an Index. The Index’s total return does not reflect the commissions or expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested. Yield will vary.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to www.eatonvance.com.

2

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

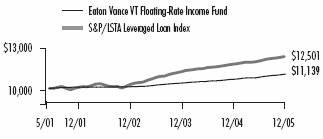

FUND PERFORMANCE

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of the Fund with that of the S&P/LSTA Leveraged Loan Index, an unmanaged loan market index. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of the Fund and the S&P/LSTA Leveraged Loan Index. The table includes the total returns of the Fund at net asset value. There is no sales charge. Insurance-related sales charges are not included in calculations of returns. Please refer to the report for your insurance contract for performance data reflecting insurance-related charges.

Performance(1)

Average Annual Total Return (at net asset value) | | | |

| | | |

One Year | | 3.86 | % |

Life of Fund (5/2/01) | | 2.40 | |

(1) The Fund has no sales charge. Returns do not include insurance-related charges.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to www.eatonvance.com.

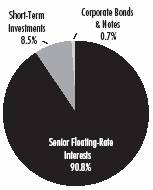

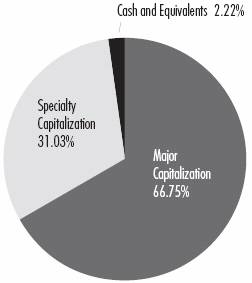

Fund Allocations(2)

By total investments

(2) Fund Allocations are shown as a percentage of total investments as of December 31, 2005. Allocations may not be representative of current or future investments and are subject to change due to active management.

Comparison of Change in Value of a $10,000 Investment in Eatan Vance VT Floating-Rate Income Fund vs. the S&P/LSTA Leveraged Loan Index*

May 31, 2001 – December 31, 2005

* Sources: Thomson Financial; Bloomberg, L.P.; Fund operations commenced 5/2/01.

It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Because Index is based on month-end data, chart begins on 5/31/01.

Diversification by Industries(3)

By total investments

Building & Development | | 5.9 | % |

Chemicals & Plastics | | 5.2 | |

Telecommunications | | 5.1 | |

Health Care | | 4.7 | |

Containers & Glass Products | | 4.6 | |

Publishing | | 4.5 | |

Cable & Satellite Television | | 4.3 | |

Leisure Goods/Activities/Movies | | 3.9 | |

Radio & Television | | 3.7 | |

Lodging & Casinos | | 3.5 | |

Retailers (Except Food & Drug) | | 3.3 | |

Business Equip. & Services | | 3.1 | |

Aerospace & Defense | | 3.1 | |

Food Products | | 3.1 | |

Utilities | | 2.9 | |

Oil & Gas | | 2.8 | |

Forest Products | | 2.8 | |

Conglomerates | | 2.8 | |

Automotive | | 2.7 | % |

Financial Intermediaries | | 2.7 | |

Electronics/Electrical | | 2.6 | |

Nonferrous Metals/Minerals | | 1.7 | |

Food Service | | 1.6 | |

Beverage & Tobacco | | 1.5 | |

Industrial Equipment | | 1.3 | |

Home Furnishings | | 1.3 | |

Equipment Leasing | | 1.2 | |

Food/Drug Retailers | | 1.2 | |

Insurance | | 1.1 | |

Ecological Services & Equip. | | 1.0 | |

Rail Industries | | 0.7 | |

Farming/Agriculture | | 0.4 | |

Drugs | | 0.4 | |

Cosmetics/Toiletries | | 0.3 | |

Air Transport | | 0.3 | |

Surface Transport | | 0.2 | |

(3) Reflects the Fund’s investments as of December 31, 2005. Industries are shown as a percentage of the Fund’s total investments. Statistics may not be representative of current or future investments and are subject to change due to active management.

3

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

FUND EXPENSES

Example: As a shareholder of the Fund, you incur ongoing costs, including transaction costs; management fees; distribution or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2005 – December 31, 2005).

Actual Expenses: The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as insurance-related charges, sales charges (loads) or redemption fees (if applicable). Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Eaton Vance VT Floating-Rate Income Fund

| | Beginning Account Value | | Ending Account Value | | Expenses Paid During Period* | |

| | (7/1/05) | | (12/31/05) | | (7/1/05 – 12/31/05) | |

| | | | | | | |

Actual | | | | | | | |

| | $ | 1,000.00 | | $ | 1,022.60 | | $ | 6.37 | |

| | | | | | | |

Hypothetical | | | | | | | |

(5% return before expenses) | | | | | | | |

| | $ | 1,000.00 | | $ | 1,018.90 | | $ | 6.36 | |

* Expenses are equal to the Fund’s annualized expense ratio of 1.25%, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2005. |

4

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

PORTFOLIO OF INVESTMENTS

| Senior, Floating Rate Interests — 87.4%(1) | | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Aerospace and Defense — 3.0% | | | |

| Delta Air Lines, Inc. | |

| $ | 250,000 | | | Term Loan, 11.01%, Maturing March 27, 2008 | | $ | 259,583 | | |

| Dresser Rand Group, Inc. | | | |

| | 687,639 | | | Term Loan, 6.28%, Maturing October 29, 2011 | | | 699,566 | | |

| DRS Technologies, Inc. | | | |

| | 226,344 | | | Term Loan, 5.94%, Maturing November 4, 2010 | | | 228,466 | | |

| Hexcel Corp. | | | |

| | 452,222 | | | Term Loan, 5.88%, Maturing March 1, 2012 | | | 456,744 | | |

| K&F Industries, Inc. | | | |

| | 395,614 | | | Term Loan, 6.28%, Maturing November 18, 2012 | | | 400,374 | | |

| Mid-Western Aircraft Systems, Inc. | | | |

| | 398,000 | | | Term Loan, 6.78%, Maturing December 31, 2011 | | | 403,929 | | |

| Transdigm, Inc. | | | |

| | 490,000 | | | Term Loan, 6.58%, Maturing July 22, 2010 | | | 496,814 | | |

| | | | | | | $ | 2,945,476 | | |

| Air Transport — 0.3% | | | |

| United Airlines, Inc. | |

| $ | 250,000 | | | DIP Loan, 0.00%, Maturing March 31, 2006(2) | | $ | 251,562 | | |

| | | | | | | $ | 251,562 | | |

| Automotive — 2.6% | | | |

| Accuride Corp. | |

| $ | 385,252 | | | Term Loan, 6.55%, Maturing January 31, 2012 | | $ | 388,904 | | |

| Affina Group, Inc. | |

| | 281,914 | | | Term Loan, 7.10%, Maturing November 30, 2011 | | | 279,870 | | |

| Dayco Products, LLC | |

| | 147,224 | | | Term Loan, 5.94%, Maturing June 23, 2011 | | | 148,604 | | |

| Exide Technologies, Inc. | |

| | 83,895 | | | Term Loan, 9.38%, Maturing May 5, 2010 | | | 84,315 | | |

| | 83,982 | | | Term Loan, 9.38%, Maturing May 5, 2010 | | | 84,402 | | |

| Federal-Mogul Corp. | |

| | 350,000 | | | Term Loan, 8.14%, Maturing December 9, 2006 | | | 350,875 | | |

| TI Automotive, Ltd. | |

| | 69,841 | | | Term Loan, 7.94%, Maturing June 30, 2011 | | | 69,143 | | |

| Trimas Corp. | |

| | 267,439 | | | Term Loan, 8.02%, Maturing December 31, 2009 | | | 270,114 | | |

| TRW Automotive, Inc. | |

| | 148,875 | | | Term Loan, 6.00%, Maturing October 31, 2010 | | | 149,545 | | |

| | 411,969 | | | Term Loan, 5.25%, Maturing June 30, 2012 | | | 414,061 | | |

| United Components, Inc. | |

| | 346,187 | | | Term Loan, 7.28%, Maturing June 30, 2010 | | | 350,947 | | |

| | | | | | | $ | 2,590,780 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Beverage and Tobacco — 1.4% | | | |

| Constellation Brands, Inc. | |

| $ | 313,111 | | | Term Loan, 5.66%, Maturing November 30, 2011 | | $ | 316,927 | | |

| Culligan International Co. | | | |

| | 346,500 | | | Term Loan, 6.87%, Maturing September 30, 2011 | | | 351,264 | | |

| National Dairy Holdings, L.P. | | | |

| | 397,000 | | | Term Loan, 7.39%, Maturing March 15, 2012 | | | 399,233 | | |

| Southern Wine & Spirits of America, Inc. | | | |

| | 338,688 | | | Term Loan, 6.03%, Maturing May 31, 2012 | | | 342,075 | | |

| | | | | | | $ | 1,409,499 | | |

| Building and Development — 5.7% | | | |

| Biomed Realty, L.P. | |

| $ | 295,000 | | | Term Loan, 6.54%, Maturing May 31, 2010 | | $ | 295,737 | | |

| Epco/Fantome, LLC | | | |

| | 250,000 | | | Term Loan, 7.90%, Maturing November 23, 2010 | | | 250,000 | | |

| General Growth Properties, Inc. | | | |

| | 698,961 | | | Term Loan, 6.35%, Maturing November 12, 2008 | | | 704,670 | | |

| Kyle Acquisition Group, LLC | | | |

| | 300,000 | | | Term Loan, 6.50%, Maturing July 20, 2010 | | | 301,687 | | |

| Landsource Communities, LLC | | | |

| | 251,000 | | | Term Loan, 6.88%, Maturing March 31, 2010 | | | 253,745 | | |

| Lion's Gables Realty Limited | | | |

| | 234,342 | | | Term Loan, 6.19%, Maturing September 30, 2006 | | | 235,587 | | |

| LNR Property Corp. | | | |

| | 342,990 | | | Term Loan, 7.27%, Maturing February 3, 2008 | | | 344,812 | | |

| LNR Property Holdings | | | |

| | 75,000 | | | Term Loan, 8.77%, Maturing February 3, 2008 | | | 75,750 | | |

| Mueller Group, Inc. | | | |

| | 249,375 | | | Term Loan, 6.54%, Maturing October 3, 2012 | | | 252,737 | | |

| Newkirk Master, L.P. | | | |

| | 316,514 | | | Term Loan, 6.05%, Maturing August 11, 2008 | | | 319,184 | | |

| Nortek, Inc. | | | |

| | 325,875 | | | Term Loan, 6.95%, Maturing August 27, 2011 | | | 329,174 | | |

| Ply Gem Industries, Inc. | | | |

| | 24,513 | | | Term Loan, 6.16%, Maturing February 12, 2011 | | | 24,666 | | |

| | 141,817 | | | Term Loan, 6.40%, Maturing February 12, 2011 | | | 142,704 | | |

| St. Marys Cement, Inc. | | | |

| | 343,000 | | | Term Loan, 6.53%, Maturing December 4, 2010 | | | 348,359 | | |

| Stile Acquisition Corp. | | | |

| | 327,246 | | | Term Loan, 6.43%, Maturing April 6, 2013 | | | 324,366 | | |

| Stile U.S. Acquisition Corp. | | | |

| | 327,804 | | | Term Loan, 6.43%, Maturing April 6, 2013 | | | 324,918 | | |

| Sugarloaf Mills, L.P. | | | |

| | 400,000 | | | Term Loan, 6.12%, Maturing April 7, 2007 | | | 402,000 | | |

See notes to financial statements

5

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Building and Development (continued) | | | |

| TE / Tousa Senior, LLC | | | |

| $ | 200,000 | | | Term Loan, 7.94%, Maturing July 29, 2008 | | $ | 201,750 | | |

| Tru 2005 Re Holding Co. | | | |

| | 450,000 | | | Term Loan, 7.46%, Maturing December 9, 2008 | | | 449,344 | | |

| | | | | | | $ | 5,581,190 | | |

| Business Equipment and Services — 3.0% | | | |

| Affinion Group, Inc. | |

| $ | 229,535 | | | Term Loan, 7.10%, Maturing October 17, 2012 | | $ | 226,307 | | |

| Buhrmann US, Inc. | |

| | 295,500 | | | Term Loan, 6.20%, Maturing December 31, 2010 | | | 300,056 | | |

| DynCorp International, LLC | |

| | 104,475 | | | Term Loan, 7.13%, Maturing February 11, 2011 | | | 105,084 | | |

| Iron Mountain, Inc. | |

| | 537,052 | | | Term Loan, 6.19%, Maturing April 2, 2011 | | | 542,003 | | |

| | 198,000 | | | Term Loan, 6.71%, Maturing April 2, 2011 | | | 199,609 | | |

| N.E.W. Holdings I, LLC | |

| | 271,296 | | | Term Loan, 6.52%, Maturing July 1, 2011 | | | 275,195 | | |

| Sungard Data Systems, Inc. | |

| | 1,288,525 | | | Term Loan, 6.81%, Maturing February 11, 2013 | | | 1,298,524 | | |

| | | | | | | $ | 2,946,778 | | |

| Cable and Satellite Television — 4.2% | | | |

| Adelphia Communications Corp. | | | |

| $ | 288,471 | | | DIP Loan, 6.31%, Maturing March 31, 2006 | | $ | 289,913 | | |

| Atlantic Broadband Finance, LLC | | | |

| | 350,000 | | | Term Loan, 7.20%, Maturing September 1, 2011 | | | 355,031 | | |

| Bresnan Communications, LLC | | | |

| | 300,000 | | | Term Loan, 7.83%, Maturing March 31, 2010 | | | 303,375 | | |

| Persona Communications | | | |

| | 344,750 | | | Term Loan, 7.53%, Maturing July 30, 2011 | | | 349,706 | | |

| Charter Communications Operating, LLC | | | |

| | 1,034,442 | | | Term Loan, 7.50%, Maturing April 27, 2011 | | | 1,038,362 | | |

| Insight Midwest Holdings, LLC | | | |

| | 343,000 | | | Term Loan, 6.56%, Maturing December 31, 2009 | | | 347,824 | | |

| MCC Iowa, LLC | | | |

| | 308,000 | | | Term Loan, 5.76%, Maturing March 31, 2010 | | | 307,725 | | |

| Mediacom Illinois, LLC | | | |

| | 198,000 | | | Term Loan, 6.57%, Maturing March 31, 2013 | | | 200,908 | | |

| NTL, Inc. | | | |

| | 300,000 | | | Term Loan, 7.14%, Maturing April 13, 2012 | | | 301,525 | | |

| UGS Corp. | | | |

| | 373,177 | | | Term Loan, 7.28%, Maturing March 31, 2012 | | | 378,308 | | |

| UPC Broadband Holdings B.V. | | | |

| | 210,000 | | | Term Loan, 6.80%, Maturing September 30, 2012 | | | 212,156 | | |

| | | | | | | $ | 4,084,833 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Chemicals and Plastics — 5.0% | | | |

| Basell Af S.A.R.L. | |

| $ | 125,000 | | | Term Loan, 6.91%, Maturing August 1, 2013 | | $ | 127,168 | | |

| | 25,000 | | | Term Loan, 6.91%, Maturing August 1, 2013 | | | 25,350 | | |

| | 125,000 | | | Term Loan, 6.82%, Maturing August 1, 2014 | | | 127,168 | | |

| | 25,000 | | | Term Loan, 7.24%, Maturing August 1, 2014 | | | 25,386 | | |

| Brenntag AG | |

| | 250,000 | | | Term Loan, 7.83%, Maturing February 27, 2012 | | | 250,792 | | |

| Celanese Holdings, LLC | |

| | 277,900 | | | Term Loan, 6.53%, Maturing April 6, 2011 | | | 281,061 | | |

| Hercules, Inc. | |

| | 393,748 | | | Term Loan, 5.88%, Maturing October 8, 2010 | | | 398,768 | | |

| Huntsman International, LLC | |

| | 578,413 | | | Term Loan, 6.12%, Maturing August 16, 2012 | | | 582,073 | | |

| Innophos, Inc. | |

| | 284,075 | | | Term Loan, 6.71%, Maturing August 13, 2010 | | | 287,626 | | |

| Invista B.V. | |

| | 98,582 | | | Term Loan, 6.13%, Maturing April 29, 2011 | | | 99,629 | | |

| | 229,409 | | | Term Loan, 6.69%, Maturing April 29, 2011 | | | 231,846 | | |

| Kraton Polymer, LLC | |

| | 255,367 | | | Term Loan, 7.02%, Maturing December 23, 2010 | | | 259,037 | | |

| Mosaic Co. | |

| | 198,500 | | | Term Loan, 5.95%, Maturing February 21, 2012 | | | 200,386 | | |

| Nalco Co. | |

| | 925,338 | | | Term Loan, 6.32%, Maturing November 4, 2010 | | | 938,467 | | |

| PQ Corp. | |

| | 397,995 | | | Term Loan, 5.91%, Maturing February 11, 2012 | | | 402,804 | | |

| Rockwood Specialties Group, Inc. | |

| | 407,950 | | | Term Loan, 6.22%, Maturing December 10, 2012 | | | 412,826 | | |

| Solo Cup Co. | |

| | 297,706 | | | Term Loan, 7.03%, Maturing February 27, 2011 | | | 300,187 | | |

| | | | | | | $ | 4,950,574 | | |

| Conglomerates — 2.7% | | | |

| Amsted Industries, Inc. | |

| $ | 523,785 | | | Term Loan, 6.68%, Maturing October 15, 2010 | | $ | 532,296 | | |

| Goodman Global Holdings, Inc. | |

| | 84,516 | | | Term Loan, 6.38%, Maturing December 23, 2011 | | | 85,801 | | |

| Jarden Corp. | |

| | 114,347 | | | Term Loan, 6.28%, Maturing January 24, 2012 | | | 114,776 | | |

| | 199,102 | | | Term Loan, 6.53%, Maturing January 24, 2012 | | | 200,240 | | |

| Johnson Diversey, Inc. | |

| | 407,452 | | | Term Loan, 6.80%, Maturing December 16, 2011 | | | 411,679 | | |

| Polymer Group, Inc. | |

| | 275,000 | | | Term Loan, 6.77%, Maturing November 22, 2012 | | | 277,922 | | |

| PP Acquisition Corp. | |

| | 332,584 | | | Term Loan, 6.56%, Maturing November 12, 2011 | | | 331,060 | | |

See notes to financial statements

6

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Conglomerates (continued) | | | |

| Rexnord Corp. | |

| $ | 508,773 | | | Term Loan, 6.15%, Maturing December 31, 2011 | | $ | 515,345 | | |

| Roper Industries, Inc. | |

| | 135,455 | | | Term Loan, 5.48%, Maturing December 13, 2009 | | | 135,991 | | |

| | | | | | | $ | 2,605,110 | | |

| Containers and Glass Products — 4.5% | | | |

| Berry Plastics Corp. | |

| $ | 471,678 | | | Term Loan, 6.45%, Maturing December 2, 2011 | | $ | 477,820 | | |

| BWAY Corp. | |

| | 152,059 | | | Term Loan, 6.56%, Maturing June 30, 2011 | | | 153,865 | | |

| Dr. Pepper/Seven Up Bottling Group, Inc. | |

| | 290,102 | | | Term Loan, 6.20%, Maturing December 19, 2010 | | | 294,490 | | |

| Graham Packaging Holdings Co. | |

| | 509,850 | | | Term Loan, 6.48%, Maturing October 7, 2011 | | | 516,422 | | |

| Graphic Packaging International, Inc. | |

| | 482,443 | | | Term Loan, 6.60%, Maturing August 8, 2010 | | | 488,895 | | |

| IPG (US), Inc. | |

| | 345,625 | | | Term Loan, 6.13%, Maturing July 28, 2011 | | | 350,665 | | |

| JSG Acquisitions | |

| | 195,000 | | | Term Loan, 7.11%, Maturing December 31, 2013 | | | 194,902 | | |

| | 195,000 | | | Term Loan, 7.61%, Maturing December 13, 2014 | | | 194,902 | | |

| Kranson Industries, Inc. | |

| | 49,250 | | | Term Loan, 7.28%, Maturing July 30, 2011 | | | 49,866 | | |

| Owens-Illinois, Inc. | |

| | 500,000 | | | Term Loan, 6.10%, Maturing April 1, 2007 | | | 502,708 | | |

| | 91,983 | | | Term Loan, 6.15%, Maturing April 1, 2008 | | | 92,702 | | |

| Pregis Corp. | |

| | 299,250 | | | Term Loan, 6.37%, Maturing October 12, 2011 | | | 301,806 | | |

| Smurfit-Stone Container Corp. | |

| | 42,866 | | | Term Loan, 2.35%, Maturing November 1, 2010 | | | 43,315 | | |

| | 450,544 | | | Term Loan, 6.69%, Maturing November 1, 2011 | | | 455,261 | | |

| | 249,834 | | | Term Loan, 6.69%, Maturing November 1, 2011 | | | 252,450 | | |

| | | | | | | $ | 4,370,069 | | |

| Cosmetics/Toiletries — 0.3% | | | |

| Prestige Brands, Inc. | |

| $ | 294,750 | | | Term Loan, 6.31%, Maturing April 7, 2011 | | $ | 297,820 | | |

| | | | | | | $ | 297,820 | | |

| Drugs — 0.4% | | | |

| Warner Chilcott Corp. | |

| $ | 95,634 | | | Term Loan, 7.28%, Maturing January 18, 2012 | | $ | 95,677 | | |

| | 44,180 | | | Term Loan, 7.28%, Maturing January 18, 2012 | | | 44,200 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Drugs (continued) | | | |

| $ | 237,335 | | | Term Loan, 7.28%, Maturing January 18, 2012 | | $ | 237,441 | | |

| | | | | | | $ | 377,318 | | |

| Ecological Services and Equipment — 0.9% | | | |

| Alderwoods Group, Inc. | |

| $ | 86,789 | | | Term Loan, 6.25%, Maturing September 29, 2009 | | $ | 87,793 | | |

| Allied Waste Industries, Inc. | |

| | 221,984 | | | Term Loan, 6.18%, Maturing January 15, 2012 | | | 223,447 | | |

| | 86,184 | | | Term Loan, 6.59%, Maturing January 15, 2012 | | | 86,747 | | |

| Envirocare of Utah, LLC | |

| | 259,091 | | | Term Loan, 6.95%, Maturing April 15, 2010 | | | 262,707 | | |

| Environmental Systems, Inc. | |

| | 251,845 | | | Term Loan, 5.55%, Maturing December 12, 2008 | | | 256,646 | | |

| | | | | | | $ | 917,340 | | |

| Electronics/Electrical — 2.5% | | | |

| AMI Semiconductor, Inc. | |

| | 248,748 | | | Term Loan, 5.89%, Maturing April 1, 2012 | | $ | 250,406 | | |

| Aspect Software, Inc. | |

| | 250,000 | | | Term Loan, 6.56%, Maturing September 22, 2010 | | | 253,125 | | |

| Avago Technologies Finance PTE | |

| | 250,000 | | | Term Loan, 6.82%, Maturing December 1, 2012 | | | 251,484 | | |

| Fairchild Semiconductor Corp. | |

| | 442,884 | | | Term Loan, 6.31%, Maturing December 31, 2010 | | | 446,205 | | |

| Invensys International Holdings Ltd. | |

| | 197,586 | | | Term Loan, 7.79%, Maturing September 4, 2009 | | | 200,994 | | |

| Rayovac Corp. | |

| | 447,622 | | | Term Loan, 6.44%, Maturing February 7, 2012 | | | 450,887 | | |

| Security Co., Inc. | |

| | 98,501 | | | Term Loan, 9.25%, Maturing June 30, 2010 | | | 99,240 | | |

| Telcordia Technologies, Inc. | |

| | 474,125 | | | Term Loan, 6.64%, Maturing September 15, 2012 | | | 470,273 | | |

| | | | | | | $ | 2,422,614 | | |

| Equipment Leasing — 1.1% | | | |

| Ashtead Group, PLC | |

| $ | 198,000 | | | Term Loan, 6.13%, Maturing November 12, 2009 | | $ | 199,691 | | |

| The Hertz Corp. | |

| | 48,182 | | | Term Loan, 0.00%, Maturing December 21, 2012(2) | | | 48,841 | | |

| | 41,111 | | | Term Loan, 5.88%, Maturing December 21, 2012 | | | 41,673 | | |

| | 280,707 | | | Term Loan, 8.50%, Maturing December 21, 2012 | | | 284,544 | | |

| United Rentals, Inc. | |

| | 91,876 | | | Term Loan, 6.03%, Maturing February 14, 2011 | | | 92,979 | | |

| | 451,342 | | | Term Loan, 6.03%, Maturing February 14, 2011 | | | 456,758 | | |

| | | | | | | $ | 1,124,486 | | |

See notes to financial statements

7

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Farming/Agriculture — 0.4% | | | |

| Central Garden & Pet Co. | |

| $ | 395,965 | | | Term Loan, 5.57%, Maturing May 15, 2009 | | $ | 401,657 | | |

| | | | | | | $ | 401,657 | | |

| Financial Intermediaries — 2.6% | | | |

| AIMCO Properties, L.P. | |

| $ | 125,000 | | | Term Loan, 6.03%, Maturing November 2, 2009 | | $ | 126,758 | | |

| | 600,000 | | | Term Loan, 6.23%, Maturing November 2, 2009 | | | 609,188 | | |

| Corrections Corp. of America | |

| | 496,250 | | | Term Loan, 6.02%, Maturing March 31, 2008 | | | 504,004 | | |

| Fidelity National Information Solutions, Inc. | |

| | 528,000 | | | Term Loan, 6.11%, Maturing March 9, 2013 | | | 530,728 | | |

| Geo Group, Inc. | |

| | 299,250 | | | Term Loan, 5.77%, Maturing September 14, 2011 | | | 301,868 | | |

| The Macerich Partnership, L.P. | |

| | 500,000 | | | Term Loan, 5.81%, Maturing April 25, 2010 | | | 503,229 | | |

| | | | | | | $ | 2,575,775 | | |

| Food Products — 3.0% | | | |

| Acosta, Inc. | |

| $ | 400,000 | | | Term Loan, 6.60%, Maturing December 6, 2012 | | $ | 404,500 | | |

| American Seafoods Group, LLC | |

| | 493,750 | | | Term Loan, 6.28%, Maturing September 30, 2011 | | | 500,848 | | |

| BF Bolthouse Holdco, LLC | |

| | 200,000 | | | Term Loan, 8.75%, Maturing December 16, 2012 | | | 203,208 | | |

| Chiquita Brands, LLC | |

| | 298,500 | | | Term Loan, 6.38%, Maturing June 28, 2012 | | | 301,983 | | |

| Dole Food Company, Inc. | |

| | 177,555 | | | Term Loan, 6.06%, Maturing April 18, 2012 | | | 178,461 | | |

| Michael Foods, Inc. | |

| | 319,463 | | | Term Loan, 6.66%, Maturing November 21, 2010 | | | 323,922 | | |

| Nash-Finch Co. | |

| | 198,843 | | | Term Loan, 6.69%, Maturing November 12, 2010 | | | 200,334 | | |

| Pinnacle Foods Holdings Corp. | |

| | 313,515 | | | Term Loan, 7.32%, Maturing November 25, 2010 | | | 317,982 | | |

| Reddy Ice Group, Inc. | |

| | 500,000 | | | Term Loan, 5.87%, Maturing August 9, 2012 | | | 505,157 | | |

| | | | | | | $ | 2,936,395 | | |

| Food Service — 1.6% | | | |

| AFC Enterprises, Inc. | |

| $ | 258,700 | | | Term Loan, 6.81%, Maturing May 11, 2011 | | $ | 261,934 | | |

| Burger King Corp. | |

| | 298,500 | | | Term Loan, 6.31%, Maturing June 30, 2012 | | | 302,441 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Food Service (continued) | | | |

| Domino's, Inc. | |

| $ | 262,794 | | | Term Loan, 6.06%, Maturing June 25, 2010 | | $ | 266,025 | | |

| Jack in the Box, Inc. | |

| | 343,875 | | | Term Loan, 5.69%, Maturing January 8, 2011 | | | 347,529 | | |

| Weight Watchers International, Inc. | |

| | 343,000 | | | Term Loan, 6.25%, Maturing March 31, 2010 | | | 347,573 | | |

| | | | | | | $ | 1,525,502 | | |

| Food/Drug Retailers — 1.1% | | | |

| General Nutrition Centers, Inc. | |

| $ | 84,358 | | | Term Loan, 7.39%, Maturing December 7, 2009 | | $ | 85,518 | | |

| Giant Eagle, Inc. | |

| | 200,000 | | | Term Loan, 6.35%, Maturing November 7, 2012 | | | 201,063 | | |

| Roundy's, Inc. | |

| | 350,000 | | | Term Loan, 7.33%, Maturing November 3, 2011 | | | 348,425 | | |

| The Jean Coutu Group (PJC), Inc. | |

| | 484,221 | | | Term Loan, 6.50%, Maturing July 30, 2011 | | | 489,433 | | |

| | | | | | | $ | 1,124,439 | | |

| Forest Products — 2.7% | | | |

| Appleton Papers, Inc. | |

| $ | 278,966 | | | Term Loan, 6.58%, Maturing June 11, 2010 | | $ | 281,930 | | |

| Boise Cascade Holdings, LLC | |

| | 388,821 | | | Term Loan, 6.26%, Maturing October 29, 2011 | | | 394,410 | | |

| Buckeye Technologies, Inc. | |

| | 229,243 | | | Term Loan, 6.19%, Maturing March 15, 2008 | | | 231,010 | | |

| NewPage Corp. | |

| | 498,750 | | | Term Loan, 7.56%, Maturing May 2, 2011 | | | 504,984 | | |

| RLC Industries Co. | |

| | 435,909 | | | Term Loan, 6.03%, Maturing February 24, 2010 | | | 438,088 | | |

| Xerium Technologies, Inc. | |

| | 796,000 | | | Term Loan, 6.70%, Maturing November 19, 2011 | | | 801,224 | | |

| | | | | | | $ | 2,651,646 | | |

| Healthcare — 4.6% | | | |

| Colgate Medical, Ltd. | |

| $ | 49,402 | | | Term Loan, 5.68%, Maturing December 30, 2008 | | $ | 49,896 | | |

| Community Health Systems, Inc. | |

| | 438,678 | | | Term Loan, 6.16%, Maturing August 19, 2011 | | | 444,755 | | |

| Concentra Operating Corp. | |

| | 250,000 | | | Term Loan, 6.62%, Maturing September 30, 2011 | | | 253,333 | | |

| Conmed Corp. | |

| | 160,206 | | | Term Loan, 6.62%, Maturing December 31, 2007 | | | 162,209 | | |

See notes to financial statements

8

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Healthcare (continued) | | | |

| Davita, Inc. | |

| $ | 723,188 | | | Term Loan, 6.73%, Maturing October 5, 2012 | | $ | 733,784 | | |

| Encore Medical IHC, Inc. | |

| | 225,901 | | | Term Loan, 7.46%, Maturing October 4, 2010 | | | 228,443 | | |

| Healthsouth Corp. | |

| | 248,750 | | | Term Loan, 6.89%, Maturing June 14, 2007 | | | 250,072 | | |

| Kinetic Concepts, Inc. | |

| | 455,590 | | | Term Loan, 6.28%, Maturing August 11, 2010 | | | 460,336 | | |

| Leiner Health Products, Inc. | |

| | 236,319 | | | Term Loan, 7.70%, Maturing May 27, 2011 | | | 239,347 | | |

| Lifepoint Hospitals, Inc. | |

| | 771,903 | | | Term Loan, 6.19%, Maturing April 15, 2012 | | | 777,370 | | |

| Magellan Health Services, Inc. | |

| | 97,222 | | | Term Loan, 4.19%, Maturing August 15, 2008 | | | 98,316 | | |

| | 121,528 | | | Term Loan, 6.74%, Maturing August 15, 2008 | | | 122,895 | | |

| Select Medical Holding Corp. | |

| | 299,246 | | | Term Loan, 6.12%, Maturing February 24, 2012 | | | 299,724 | | |

| Sybron Dental Management, Inc. | |

| | 100,585 | | | Term Loan, 6.23%, Maturing June 6, 2009 | | | 101,465 | | |

| VWR International, Inc. | |

| | 241,533 | | | Term Loan, 6.69%, Maturing April 7, 2011 | | | 245,232 | | |

| | | | | | | $ | 4,467,177 | | |

| Home Furnishings — 1.2% | | | |

| Knoll, Inc. | |

| $ | 139,650 | | | Term Loan, 6.53%, Maturing October 3, 2012 | | $ | 141,505 | | |

| National Bedding Company, LLC | |

| | 300,000 | | | Term Loan, 6.17%, Maturing August 31, 2011 | | | 302,775 | | |

| Sealy Mattress Co. | |

| | 431,540 | | | Term Loan, 6.13%, Maturing April 6, 2012 | | | 436,732 | | |

| Simmons Co. | |

| | 319,695 | | | Term Loan, 5.87%, Maturing December 19, 2011 | | | 323,341 | | |

| | | | | | | $ | 1,204,353 | | |

| Industrial Equipment — 1.2% | | | |

| Alliance Laundry Holdings, LLC | |

| | 177,000 | | | Term Loan, 5.86%, Maturing January 27, 2012 | | $ | 179,655 | | |

| Douglas Dynamics Holdings, Inc. | |

| | 299,247 | | | Term Loan, 6.28%, Maturing December 16, 2010 | | | 301,491 | | |

| Flowserve Corp. | |

| | 241,042 | | | Term Loan, 6.36%, Maturing August 10, 2012 | | | 244,243 | | |

| MTD Products, Inc. | |

| | 496,222 | | | Term Loan, 6.06%, Maturing June 1, 2010 | | | 500,564 | | |

| | | | | | | $ | 1,225,953 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Insurance — 1.1% | | | |

| Conseco, Inc. | |

| | 280,917 | | | Term Loan, 6.28%, Maturing June 22, 2010 | | $ | 283,258 | | |

| Hilb, Rogal & Hobbs Co. | |

| | 636,448 | | | Term Loan, 5.88%, Maturing June 30, 2007 | | | 644,006 | | |

| U.S.I. Holdings Corp. | |

| | 104,213 | | | Term Loan, 6.80%, Maturing August 11, 2008 | | | 104,668 | | |

| | | | | | | $ | 1,031,932 | | |

| Leisure Goods/Activities/Movies — 3.8% | | | |

| AMF Bowling Worldwide, Inc. | |

| | 202,247 | | | Term Loan, 7.28%, Maturing August 27, 2009 | | $ | 204,080 | | |

| Cinemark, Inc. | |

| | 393,000 | | | Term Loan, 6.53%, Maturing March 31, 2011 | | | 398,207 | | |

| Loews Cineplex Entertainment Corp. | |

| | 448,085 | | | Term Loan, 6.45%, Maturing July 30, 2011 | | | 450,955 | | |

| Metro-Goldwyn-Mayer Holdings, Inc. | |

| | 880,000 | | | Term Loan, 6.78%, Maturing April 8, 2012 | | | 886,900 | | |

| Regal Cinemas Corp. | |

| | 381,061 | | | Term Loan, 6.53%, Maturing November 10, 2010 | | | 385,771 | | |

| Riddell Bell Holdings, Inc. | |

| | 248,115 | | | Term Loan, 7.03%, Maturing September 30, 2011 | | | 252,096 | | |

| Six Flags Theme Parks, Inc. | |

| | 459,901 | | | Term Loan, 6.67%, Maturing June 30, 2009 | | | 465,979 | | |

| Universal City Development Partners, Ltd. | |

| | 346,500 | | | Term Loan, 7.28%, Maturing June 9, 2011 | | | 351,048 | | |

| WMG Acquisition Corp. | |

| | 318,917 | | | Term Loan, 6.41%, Maturing February 28, 2011 | | | 322,676 | | |

| | | | | | | $ | 3,717,712 | | |

| Lodging and Casinos — 3.3% | | | |

| Alliance Gaming Corp. | |

| $ | 313,132 | | | Term Loan, 11.00%, Maturing September 4, 2009 | | $ | 313,670 | | |

| Ameristar Casinos, Inc. | |

| | 250,000 | | | Term Loan, 6.56%, Maturing November 10, 2012 | | | 251,875 | | |

| Boyd Gaming Corp. | |

| | 369,375 | | | Term Loan, 5.86%, Maturing June 30, 2011 | | | 374,108 | | |

| CCM Merger, Inc. | |

| | 199,000 | | | Term Loan, 6.49%, Maturing July 13, 2012 | | | 200,642 | | |

| Globalcash Access, LLC | |

| | 129,740 | | | Term Loan, 6.64%, Maturing March 10, 2010 | | | 131,686 | | |

| Isle of Capri Casinos, Inc. | |

| | 391,050 | | | Term Loan, 6.06%, Maturing February 4, 2011 | | | 395,449 | | |

| Marina District Finance Co., Inc. | |

| | 247,500 | | | Term Loan, 6.14%, Maturing October 20, 2011 | | | 249,408 | | |

See notes to financial statements

9

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Lodging and Casinos (continued) | | | |

| Penn National Gaming, Inc. | |

| $ | 635,408 | | | Term Loan, 6.05%, Maturing October 3, 2012 | | $ | 643,797 | | |

| Resorts International Holdings, LLC | |

| | 288,189 | | | Term Loan, 7.53%, Maturing April 26, 2012 | | | 289,540 | | |

| Venetian Casino Resort, LLC | |

| | 259,679 | | | Term Loan, 6.28%, Maturing June 15, 2011 | | | 261,667 | | |

| | 53,542 | | | Term Loan, 6.78%, Maturing June 15, 2011 | | | 53,952 | | |

| Wynn Las Vegas, LLC | |

| | 100,000 | | | Term Loan, 6.53%, Maturing December 14, 2011 | | | 101,167 | | |

| | | | | | | $ | 3,266,961 | | |

| Nonferrous Metals/Minerals — 1.7% | | | |

| Alpha Natural Resources, LLC | |

| $ | 300,000 | | | Term Loan, 6.32%, Maturing October 26, 2012 | | $ | 302,375 | | |

| Foundation Coal Corp. | |

| | 285,106 | | | Term Loan, 6.35%, Maturing July 30, 2011 | | | 289,898 | | |

| ICG, LLC | |

| | 18,600 | | | Term Loan, 7.13%, Maturing November 5, 2010 | | | 18,693 | | |

| International Mill Service, Inc. | |

| | 248,748 | | | Term Loan, 5.81%, Maturing December 31, 2010 | | | 251,236 | | |

| Murray Energy Corp. | |

| | 347,375 | | | Term Loan, 7.39%, Maturing January 28, 2010 | | | 348,895 | | |

| Novelis, Inc. | |

| | 275,972 | | | Term Loan, 6.01%, Maturing January 6, 2012 | | | 279,249 | | |

| | 159,873 | | | Term Loan, 6.95%, Maturing January 6, 2012 | | | 161,772 | | |

| | | | | | | $ | 1,652,118 | | |

| Oil and Gas — 2.7% | | | |

| Citgo Petroleum Corp. | |

| $ | 500,000 | | | Term Loan, 5.68%, Maturing November 15, 2012 | | $ | 504,219 | | |

| Dresser, Inc. | |

| | 123,780 | | | Term Loan, 6.28%, Maturing March 31, 2007 | | | 125,637 | | |

| El Paso Corp. | |

| | 409,750 | | | Term Loan, 4.00%, Maturing November 23, 2009 | | | 411,600 | | |

| | 260,925 | | | Term Loan, 7.31%, Maturing November 23, 2009 | | | 262,411 | | |

| Epco Holdings, Inc. | |

| | 247,500 | | | Term Loan, 6.52%, Maturing August 18, 2010 | | | 251,270 | | |

| Targa Resources, Inc. | |

| | 175,000 | | | Term Loan, 6.83%, Maturing October 31, 2007 | | | 175,656 | | |

| | 38,226 | | | Term Loan, 4.40%, Maturing October 31, 2012 | | | 38,572 | | |

| | 236,182 | | | Term Loan, 6.64%, Maturing October 31, 2012 | | | 238,323 | | |

| Universal Compression, Inc. | |

| | 297,751 | | | Term Loan, 6.03%, Maturing February 15, 2012 | | | 301,100 | | |

| Williams Production RMT Co. | |

| | 343,000 | | | Term Loan, 6.62%, Maturing May 30, 2008 | | | 346,859 | | |

| | | | | | | $ | 2,655,647 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Publishing — 4.3% | | | |

| American Media Operations, Inc. | |

| $ | 317,952 | | | Term Loan, 6.28%, Maturing April 1, 2007 | | $ | 320,204 | | |

| Dex Media West, LLC | |

| | 117,128 | | | Term Loan, 6.05%, Maturing March 9, 2010 | | | 117,907 | | |

| Endurance Business Media, Inc. | |

| | 160,000 | | | Term Loan, 6.62%, Maturing March 8, 2012 | | | 161,500 | | |

| Herald Media, Inc. | |

| | 296,807 | | | Term Loan, 7.28%, Maturing July 22, 2011 | | | 298,662 | | |

| Journal Register Co. | |

| | 385,000 | | | Term Loan, 5.69%, Maturing August 12, 2012 | | | 387,346 | | |

| Liberty Group Operating, Inc. | |

| | 250,000 | | | Term Loan, 8.25%, Maturing February 28, 2012 | | | 252,422 | | |

| Medianews Group, Inc. | |

| | 407,491 | | | Term Loan, 5.64%, Maturing August 25, 2010 | | | 408,680 | | |

| Merrill Communications, LLC | |

| | 197,547 | | | Term Loan, 6.82%, Maturing July 30, 2009 | | | 199,152 | | |

| Nebraska Book Co., Inc. | |

| | 343,875 | | | Term Loan, 6.52%, Maturing March 4, 2011 | | | 347,314 | | |

| Newspaper Holdings, Inc. | |

| | 300,000 | | | Term Loan, 6.19%, Maturing August 24, 2012 | | | 302,063 | | |

| R.H. Donnelley Corp. | |

| | 12,851 | | | Term Loan, 6.15%, Maturing December 31, 2009 | | | 12,911 | | |

| | 443,868 | | | Term Loan, 6.15%, Maturing June 30, 2011 | | | 446,536 | | |

| Source Media, Inc. | |

| | 91,176 | | | Term Loan, 6.63%, Maturing January 30, 2006 | | | 92,259 | | |

| SP Newsprint Co. | |

| | 87,208 | | | Term Loan, 6.43%, Maturing January 9, 2010 | | | 88,462 | | |

| | 225,556 | | | Term Loan, 6.43%, Maturing January 9, 2010 | | | 228,798 | | |

| Sun Media Corp. | |

| | 315,679 | | | Term Loan, 6.81%, Maturing February 7, 2009 | | | 317,258 | | |

| Xsys US, Inc. | |

| | 132,027 | | | Term Loan, 6.77%, Maturing December 31, 2012 | | | 133,182 | | |

| | 134,855 | | | Term Loan, 7.27%, Maturing December 31, 2013 | | | 136,710 | | |

| | | | | | | $ | 4,251,366 | | |

| Radio and Television — 3.3% | | | |

| Adams Outdoor Advertising, L.P. | |

| $ | 310,265 | | | Term Loan, 6.20%, Maturing November 18, 2012 | | $ | 314,855 | | |

| DirecTV Holdings, LLC | |

| | 340,000 | | | Term Loan, 5.87%, Maturing April 13, 2013 | | | 343,506 | | |

| Emmis Operating Co. | |

| | 200,383 | | | Term Loan, 6.12%, Maturing November 10, 2011 | | | 201,579 | | |

| Entravision Communications Corp. | |

| | 250,000 | | | Term Loan, 5.55%, Maturing September 29, 2013 | | | 251,875 | | |

| Nexstar Broadcasting, Inc. | |

| | 160,137 | | | Term Loan, 6.28%, Maturing October 1, 2012 | | | 161,271 | | |

| | 163,011 | | | Term Loan, 6.28%, Maturing October 1, 2012 | | | 164,166 | | |

See notes to financial statements

10

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Radio and Television (continued) | | | |

| PanAmSat Corp. | |

| $ | 792,989 | | | Term Loan, 6.49%, Maturing August 20, 2011 | | $ | 803,298 | | |

| Rainbow National Services, LLC | |

| | 187,439 | | | Term Loan, 9.02%, Maturing March 31, 2012 | | | 189,149 | | |

| Raycom TV Broadcasting, Inc. | |

| | 360,000 | | | Term Loan, 6.44%, Maturing February 24, 2012 | | | 361,350 | | |

| Spanish Broadcasting System | |

| | 173,688 | | | Term Loan, 6.53%, Maturing June 10, 2012 | | | 176,293 | | |

| Young Broadcasting, Inc. | |

| | 248,750 | | | Term Loan, 6.70%, Maturing November 3, 2012 | | | 250,110 | | |

| | | | | | | $ | 3,217,452 | | |

| Rail Industries — 0.6% | | | |

| Kansas City Southern Industries, Inc. | |

| $ | 344,768 | | | Term Loan, 5.80%, Maturing March 30, 2008 | | $ | 346,779 | | |

| Railamerica, Inc. | |

| | 28,922 | | | Term Loan, 6.69%, Maturing September 29, 2011 | | | 29,386 | | |

| | 244,663 | | | Term Loan, 9.02%, Maturing September 29, 2011 | | | 248,588 | | |

| | | | | | | $ | 624,753 | | |

| Retailers (Except Food and Drug) — 3.1% | | | |

| Advance Stores Company, Inc. | |

| $ | 94,643 | | | Term Loan, 5.89%, Maturing September 30, 2010 | | $ | 95,797 | | |

| | 56,261 | | | Term Loan, 5.91%, Maturing September 30, 2010 | | | 56,823 | | |

| Alimentation Couche-Tard, Inc. | |

| | 309,032 | | | Term Loan, 6.19%, Maturing December 17, 2010 | | | 312,895 | | |

| Coinmach Laundry Corp. | |

| | 375,000 | | | Term Loan, 6.38%, Maturing December 19, 2012(2) | | | 380,625 | | |

| Harbor Freight Tools USA, Inc. | |

| | 228,723 | | | Term Loan, 6.94%, Maturing July 15, 2010 | | | 231,182 | | |

| Josten's Corp. | |

| | 375,402 | | | Term Loan, 6.80%, Maturing October 4, 2010 | | | 380,846 | | |

| Oriental Trading Co., Inc. | |

| | 216,325 | | | Term Loan, 6.81%, Maturing August 4, 2010 | | | 217,677 | | |

| Rent-A-Center, Inc. | |

| | 298,460 | | | Term Loan, 6.27%, Maturing June 30, 2010 | | | 301,818 | | |

| Savers, Inc. | |

| | 249,367 | | | Term Loan, 7.53%, Maturing August 4, 2009 | | | 252,796 | | |

| School Specialty, Inc. | |

| | 550,000 | | | Term Loan, 6.71%, Maturing September 29, 2012 | | | 550,000 | | |

| Travelcenters of America, Inc. | |

| | 300,000 | | | Term Loan, 6.28%, Maturing November 30, 2008 | | | 303,375 | | |

| | | | | | | $ | 3,083,834 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Surface Transport — 0.2% | | | |

| Sirva Worldwide, Inc. | |

| $ | 164,354 | | | Term Loan, 8.16%, Maturing December 1, 2010 | | $ | 157,780 | | |

| | | | | | | $ | 157,780 | | |

| Telecommunications — 4.5% | | | |

| Alaska Communications Systems Holdings, Inc. | |

| $ | 300,000 | | | Term Loan, 6.53%, Maturing February 11, 2012 | | $ | 303,375 | | |

| Cellular South, Inc. | |

| | 249,367 | | | Term Loan, 6.04%, Maturing May 4, 2011 | | | 252,484 | | |

| Centennial Cellular Operating Co., LLC | |

| | 320,833 | | | Term Loan, 6.62%, Maturing February 9, 2011 | | | 325,119 | | |

| Cincinnati Bell, Inc. | |

| | 249,375 | | | Term Loan, 5.90%, Maturing August 31, 2012 | | | 250,934 | | |

| Consolidated Communications, Inc. | |

| | 296,250 | | | Term Loan, 5.93%, Maturing July 27, 2015 | | | 299,213 | | |

| Fairpoint Communications, Inc. | |

| | 340,000 | | | Term Loan, 6.31%, Maturing February 8, 2012 | | | 341,403 | | |

| Hawaiian Telcom Communications, Inc. | |

| | 300,000 | | | Term Loan, 6.78%, Maturing October 31, 2012 | | | 302,063 | | |

| Intelsat, Ltd. | |

| | 596,992 | | | Term Loan, 5.81%, Maturing July 28, 2011 | | | 603,336 | | |

| Iowa Telecommunications Services | |

| | 450,000 | | | Term Loan, 6.13%, Maturing November 23, 2011 | | | 454,711 | | |

| Nextel Partners Operation Corp. | |

| | 340,000 | | | Term Loan, 5.91%, Maturing May 31, 2012 | | | 341,204 | | |

| Qwest Corp. | |

| | 100,000 | | | Term Loan, 9.02%, Maturing June 4, 2007 | | | 102,488 | | |

| Syniverse Holdings, Inc. | |

| | 298,702 | | | Term Loan, 6.28%, Maturing February 15, 2012 | | | 302,809 | | |

| Triton PCS, Inc. | |

| | 322,246 | | | Term Loan, 7.64%, Maturing November 18, 2009 | | | 324,502 | | |

| Valor Telecom Enterprise, LLC | |

| | 203,000 | | | Term Loan, 6.02%, Maturing February 14, 2012 | | | 204,063 | | |

| | | | | | | $ | 4,407,704 | | |

| Utilities — 2.8% | | | |

| Allegheny Energy Supply Co., LLC | |

| $ | 484,812 | | | Term Loan, 5.86%, Maturing March 8, 2011 | | $ | 490,973 | | |

| Cogentrix Delaware Holdings, Inc. | |

| | 261,190 | | | Term Loan, 6.28%, Maturing April 14, 2012 | | | 263,992 | | |

| Covanta Energy Corp. | |

| | 110,569 | | | Term Loan, 6.02%, Maturing June 24, 2012 | | | 112,366 | | |

| | 74,573 | | | Term Loan, 7.51%, Maturing June 24, 2012 | | | 75,785 | | |

See notes to financial statements

11

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Utilities (continued) | | | |

| Energy Transfer Company, L.P. | |

| $ | 248,750 | | | Term Loan, 7.44%, Maturing June 16, 2012 | | $ | 249,714 | | |

| NRG Energy, Inc. | |

| | 177,528 | | | Term Loan, 4.43%, Maturing December 24, 2011 | | | 178,268 | | |

| | 223,536 | | | Term Loan, 6.26%, Maturing December 24, 2011 | | | 224,468 | | |

| Pike Electric, Inc. | |

| | 185,220 | | | Term Loan, 6.13%, Maturing July 1, 2012 | | | 187,535 | | |

| Plains Resources, Inc. | |

| | 299,250 | | | Term Loan, 6.40%, Maturing July 23, 2010 | | | 302,430 | | |

| Reliant Energy, Inc. | |

| | 174,042 | | | Term Loan, 6.09%, Maturing December 22, 2010 | | | 173,825 | | |

| Texas Genco, LLC | |

| | 142,592 | | | Term Loan, 6.37%, Maturing December 14, 2011 | | | 143,060 | | |

| | 344,355 | | | Term Loan, 6.37%, Maturing December 14, 2011 | | | 345,485 | | |

| | | | | | | $ | 2,747,901 | | |

| | Total Senior, Floating Rate Interests

(identified cost $85,311,569) | | | | | $ | 85,803,506 | | |

| Floating Rate Notes — 0.7% | | | |

Principal Amount

(000's omitted) | | Security | | Value | |

| Radio and Television — 0.3% | | | |

| Paxson Communications Corp., Variable Rate | |

| $ | 300 | | | 6.90%, 1/15/10(3) | | $ | 302,250 | | |

| | | | | | | $ | 302,250 | | |

| Telecommunications — 0.4% | | | |

| Qwest Corp., Variable Rate | |

| $ | 300 | | | 7.741%, 6/15/13(3) | | $ | 325,125 | | |

| Rogers Wireless, Inc., Variable Rate | |

| | 93 | | | 7.616%, 12/15/10 | | | 96,487 | | |

| | | | | | | $ | 421,612 | | |

| | Total Floating Rate Notes

(identified cost $693,000) | | | | | $ | 723,862 | | |

| Short-Term Investments — 8.2% | | | |

Principal

Amount | | Maturity

Date | | Borrower | | Rate | | Amount | |

| $ | 1,906,000 | | | 01/04/06 | | Abbey National North

America, LLC | | | 4.33 | % | | $ | 1,905,312 | | |

| | 1,653,000 | | | 01/03/06 | | General Electric

Capital Corp. | | | 4.20 | % | | | 1,652,614 | | |

| | 1,908,000 | | | 01/03/06 | | Investors Bank and Trust

Company, Time Deposit | | | 4.23 | % | | | 1,908,000 | | |

| | 1,039,000 | | | 01/06/06 | | Old Line Funding, LLC | | | 4.35 | % | | | 1,038,372 | | |

| | 1,500,000 | | | 01/03/06 | | Yorktown Capital, LLC | | | 4.35 | % | | | 1,499,638 | | |

Total Short-Term Investments

(at amortized cost) | | $ | 8,003,936 | | |

Total Investments — 96.3%

(identified cost $94,008,505) | | $ | 94,531,304 | | |

Less Unfunded Loan

Commitments — (0.5)% | | $ | (521,866 | ) | |

Net Investments — 95.8%

(identified cost $93,486,639) | | $ | 94,009,438 | | |

| Other Assets, Less Liabilities — 4.2% | | $ | 4,173,761 | | |

| Net Assets — 100.0% | | $ | 98,183,199 | | |

(1) Senior floating-rate interests often require prepayments from excess cash flows or permit the borrower to repay at its election. The degree to which borrowers repay, whether as a contractual requirement or at their election, cannot be predicted with accuracy. As a result, the actual remaining maturity may be substantially less than the stated maturities shown. However, it is anticipated that the senior floating-rate interests will have an expected average life of approximately two to three years. The stated interest rate represents the weighted average interest rate of all contracts within the senior loan facility. Senior Loans typically have rates of interest which are redetermined either daily, monthly, quarterly or semi-annually by reference to a base lending rate, plus a premium. These base lending rates are primarily the London - -Interbank Offered Rate ("LIBOR"), and secondarily the prime rate offered by one or more major United States banks (the "Prime Rate") and the certificate of deposit ("CD") rate or other base lending rates used by commercial lenders.

(2) Unfunded loan commitments. See Note 1E for description.

(3) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in transactions exempt from registration, normally to qualified institutional buyers. At December 31, 2005, the aggregate value of the securities is $627,375 or 0.7% of the Fund's net assets.

See notes to financial statements

12

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

FINANCIAL STATEMENTS

Statement of Assets and Liabilities

As of December 31, 2005

| Assets | |

| Investments, at value (identified cost, $93,486,639) | | $ | 94,009,438 | | |

| Cash | | | 1,518,667 | | |

| Receivable for investments sold | | | 29,927 | | |

| Receivable for Fund shares sold | | | 2,403,424 | | |

| Interest receivable | | | 428,659 | | |

| Prepaid expenses | | | 3,507 | | |

| Total assets | | $ | 98,393,622 | | |

| Liabilities | |

| Payable to affiliate for investment advisory fees | | $ | 46,387 | | |

| Dividends payable | | | 24,819 | | |

| Payable to affiliate for administration fees | | | 20,168 | | |

| Payable for Fund shares redeemed | | | 2,245 | | |

| Payable to affiliate for Trustees' fees | | | 1,930 | | |

| Accrued expenses | | | 114,874 | | |

| Total liabilities | | $ | 210,423 | | |

| Net Assets for 9,744,054 shares of beneficial interest outstanding | | $ | 98,183,199 | | |

| Sources of Net Assets | |

| Paid-in capital | | $ | 97,959,801 | | |

| Accumulated net realized loss (computed on the basis of identified cost) | | | (321,514 | ) | |

| Accumulated undistributed net investment income | | | 22,112 | | |

| Net unrealized appreciation (computed on the basis of identified cost) | | | 522,800 | | |

| Total | | $ | 98,183,199 | | |

Net Asset Value, Offering Price and

Redemption Price Per Share | |

| ($98,183,199 ÷ 9,744,054 shares of beneficial interest outstanding) | | $ | 10.08 | | |

Statement of Operations

For the Year Ended

December 31, 2005

| Investment Income | |

| Interest | | $ | 4,668,937 | | |

| Total investment income | | $ | 4,668,937 | | |

| Expenses | |

| Investment adviser fee | | $ | 508,858 | | |

| Administration fee | | | 221,243 | | |

| Trustees' fees and expenses | | | 7,116 | | |

| Service fees | | | 221,243 | | |

| Custodian fee | | | 96,621 | | |

| Legal and accounting services | | | 40,350 | | |

| Transfer and dividend disbursing agent fees | | | 10,902 | | |

| Printing and postage | | | 4,700 | | |

| Registration fees | | | 4,055 | | |

| Miscellaneous | | | 13,852 | | |

| Total expenses | | $ | 1,128,940 | | |

Deduct —

Reduction of custodian fee | | $ | 25,741 | | |

| Total expense reductions | | $ | 25,741 | | |

| Net expenses | | $ | 1,103,199 | | |

| Net investment income | | $ | 3,565,738 | | |

| Realized and Unrealized Gain (Loss) | |

Net realized gain (loss) —

Investment transactions (identified cost basis) | | $ | (233,885 | ) | |

| Net realized loss | | $ | (233,885 | ) | |

Change in unrealized appreciation (depreciation) —

Investments (identified cost basis) | | $ | (9,239 | ) | |

| Net change in unrealized appreciation (depreciation) | | $ | (9,239 | ) | |

| Net realized and unrealized loss | | $ | (243,124 | ) | |

| Net increase in net assets from operations | | $ | 3,322,614 | | |

See notes to financial statements

13

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

FINANCIAL STATEMENTS CONT'D

Statements of Changes in Net Assets

Increase (Decrease)

in Net Assets | | Year Ended

December 31, 2005 | | Year Ended

December 31, 2004 | |

From operations —

Net investment income | | $ | 3,565,738 | | | $ | 1,621,678 | | |

Net realized loss from

Investment transactions | | | (233,885 | ) | | | (87,629 | ) | |

Net change in unrealized

appreciation (depreciation)

from investments | | | (9,239 | ) | | | 278,521 | | |

| Net increase in net assets from operations | | $ | 3,322,614 | | | $ | 1,812,570 | | |

Distributions to shareholders —

From net investment income | | $ | (3,564,220 | ) | | $ | (1,622,175 | ) | |

| Total distributions to shareholders | | $ | (3,564,220 | ) | | $ | (1,622,175 | ) | |

Transactions in shares of beneficial interest —

Proceeds from sale of shares | | $ | 37,756,714 | | | $ | 47,887,259 | | |

Net asset value of shares issued to

shareholders in payment of

distributions declared | | | 3,471,078 | | | | 1,622,162 | | |

| Cost of shares redeemed | | | (17,786,686 | ) | | | (20,128,267 | ) | |

Net increase in net assets from

Fund share transactions | | $ | 23,441,106 | | | $ | 29,381,154 | | |

| Net increase in net assets | | $ | 23,199,500 | | | $ | 29,571,549 | | |

| Net Assets | |

| At beginning of year | | $ | 74,983,699 | | | $ | 45,412,150 | | |

| At end of year | | $ | 98,183,199 | | | $ | 74,983,699 | | |

Accumulated

undistributed net

investment income

included in net assets | |

| At end of year | | $ | 22,112 | | | $ | 20,594 | | |

See notes to financial statements

14

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

FINANCIAL STATEMENTS CONT'D

Financial Highlights

| | | Year Ended December 31, | |

| | | 2005(1) | | 2004(1) | | 2003 | | 2002(1) | | 2001(1)(2) | |

| Net asset value — Beginning of year | | $ | 10.100 | | | $ | 10.070 | | | $ | 10.000 | | | $ | 10.000 | | | $ | 10.000 | | |

| Income (loss) from operations | |

| Net investment income | | $ | 0.406 | | | $ | 0.257 | | | $ | 0.222 | | | $ | 0.031 | | | $ | 0.129 | | |

| Net realized and unrealized gain (loss) | | | (0.024 | ) | | | 0.026 | | | | 0.070 | | | | — | | | | — | | |

| Total income from operations | | $ | 0.382 | | | $ | 0.283 | | | $ | 0.292 | | | $ | 0.031 | | | $ | 0.129 | | |

| Less distributions | |

| From net investment income | | $ | (0.402 | ) | | $ | (0.253 | ) | | $ | (0.222 | ) | | $ | (0.031 | ) | | $ | (0.129 | ) | |

| Total distributions | | $ | (0.402 | ) | | $ | (0.253 | ) | | $ | (0.222 | ) | | $ | (0.031 | ) | | $ | (0.129 | ) | |

| Net asset value — End of year | | $ | 10.080 | | | $ | 10.100 | | | $ | 10.070 | | | $ | 10.000 | | | $ | 10.000 | | |

| Total Return(3) | | | 3.86 | % | | | 2.82 | % | | | 2.93 | % | | | 0.31 | % | | | 1.29 | % | |

| Ratios/Supplemental Data† | |

| Net assets, end of year (000's omitted) | | $ | 98,183 | | | $ | 74,984 | | | $ | 45,412 | | | $ | 36,552 | | | $ | 15,789 | | |

| Ratios (As a percentage of average daily net assets): | |

| Net expenses | | | 1.27 | % | | | 1.27 | % | | | 1.36 | % | | | 1.47 | % | | | 1.26 | %(4) | |

| Net expenses after custodian fee reduction | | | 1.25 | % | | | 1.26 | % | | | 1.36 | % | | | 1.47 | % | | | 1.26 | %(4) | |

| Net investment income | | | 4.03 | % | | | 2.55 | % | | | 2.18 | % | | | 0.31 | % | | | 1.37 | %(4) | |

| Portfolio Turnover | | | 60 | % | | | 61 | % | | | 65 | % | | | 0 | % | | | — | | |

† The operating expenses of the Fund reflect a reduction of the investment advisor fee. Had such action not been taken, the ratios and net investment gain per share would have been as follows:

| Ratios (As a percentage of average daily net assets): | |

| Expenses | | | 1.28 | %(4) | |

| Expenses after custodian fee reduction | | | 1.28 | %(4) | |

| Net investment income | | | 1.35 | %(4) | |

| Net investment income per share | | $ | 0.127 | | |

(1) Net investment income per share was computed using average shares outstanding.

(2) For the period from the start of business, May 2, 2001, to December 31, 2001.

(3) Returns are historical and are calculated by determining the percentage change in net asset value with all distributions reinvested. Total return is not computed on an annualized basis.

(4) Annualized.

See notes to financial statements

15

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

NOTES TO FINANCIAL STATEMENT

1 Significant Accounting Policies

Eaton Vance VT Floating-Rate Income Fund (the Fund) is a non-diversified series of Eaton Vance Variable Trust (the Trust). The Trust, which was organized under Massachusetts law on August 14, 2000, is an entity of the type commonly known as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The Fund seeks to provide a high level of current income by investing primarily in income producing floating rate loans. The Fund is made available only to separate accounts issued by participating insurance companies. The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America.

A Investment Valuations — Certain Senior Loans are deemed to be liquid because reliable market quotations are readily available for them. Liquid Senior Loans are valued on the basis of prices furnished by a pricing service. Other Senior Loans are valued at fair value by the Fund's investment adviser, Eaton Vance Management (EVM), under procedures approved by the Trustees. In connection with determining the fair value of a Senior Loan, the investment adviser makes an assessment of the likelihood that the borrower will make a full repayment of the Senior Loan. The primary factors considered by the investment adviser when making this assessment are (i) the creditworthiness of the borrower, (ii) the value of the collateral backing the Senior Loan, and (iii) the priority of th e Senior Loan versus other creditors of the borrower. If, based on its assessment, the investment adviser believes there is a reasonable likelihood that the borrower will make a full repayment of the Senior Loan, the investment adviser will determine the fair value of the Senior Loan using a matrix pricing approach that considers the yield on the Senior Loan relative to yields on other loan interests issued by companies of comparable credit quality. If, based on its assessment, the investment adviser believes there is not a reasonable likelihood that the borrower will make a full repayment of the Senior Loan, the investment adviser will determine the fair value of the Senior Loan using analyses that include, but are not limited to (i) a comparison of the value of the borrower's outstanding equity and debt to that of comparable public companies; (ii) a discounted cash flow analysis; or (iii) when the investment adviser believes it is likely that a borrower will be liquidated or sold, an analysis of the terms of such liquidation or sale. In certain cases, the investment adviser will use a combination of analytical methods to determine fair value, such as when only a portion of a borrower's assets are likely to be sold. In conducting its assessment and analyses for purposes of determining fair value of a Senior Loan, the investment adviser will use its discretion and judgment in considering and appraising such factors, data and information and the relative weight to be given thereto as it deems relevant, including without limitation, some or all of the following: (i) the fundamental characteristics of and fundamental analytical data relating to the Senior Loan, including the cost, size, current interest rate, maturity and base lending rate of the Senior Loan, the terms and conditions of the Senior Loan and any related agreements, and the position of the Senior Loan in the Borrower's debt structure; (ii) the nature, adequacy and value of the co llateral securing the Senior Loan, including the Fund's rights, remedies and interests with respect to the collateral; (iii) the creditworthiness of the Borrower, based on an evaluation of, among other things, its financial condition, financial statements and information about the Borrower's business, cash flows, capital structure and future prospects; (iv) information relating to the market for the Senior Loan, including price quotations for and trading in the Senior Loan and interests in similar Senior Loans and the market environment and investor attitudes towards the Senior Loan and interests in similar Senior Loans; (v) the experience, reputation, stability and financial condition of the agent and any intermediate participants in the Senior Loan; and (vi) general economic and market conditions affecting the fair value of the Senior Loan.

Debt obligations (other than short-term obligations maturing in sixty days or less), including listed securities and securities for which price quotations are available and forward contracts, will normally be valued on the basis of market valuations furnished by dealers or pricing services. Financial futures contracts listed on commodity exchanges and exchange-traded options are valued at closing settlement prices. Over-the-counter options are valued at the mean between the bid and asked prices provided by dealers. Marketable securities listed on the NASDAQ National Market System are valued at the NASDAQ official closing price. The value of interest rate swaps will be based upon a dealer quotation. Short-term obligations and money market securities maturing in sixty days or less are valued at amortized cost which approximates value. Investments for which reliable market quotations are unavailable are valued at fair value using m ethods determined in good faith by or at the direction of the Trustees of the Fund. Occasionally, events affecting the value of foreign securities may occur between the time trading is completed abroad and the close of the Exchange which will not be reflected in the computation of the

16

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2005

NOTES TO FINANCIAL STATEMENT CONT'D

Fund's net asset value (unless the Fund deems that such event would materially affect its net asset value in which case an adjustment would be made and reflected in such computation). The Fund may rely on an independent fair valuation service in making any such adjustment.

B Income — Interest income from Senior Loans is recorded on the accrual basis at the then-current interest rate, while all other interest income is determined on the basis of interest accrued, adjusted for amortization of premium or discount. Facility fees received are recognized as income over the expected term of the loan.

C Income Taxes — The Fund has elected to be treated as a regulated investment company (RIC) for United States federal tax purposes. The Fund's policy is to comply with the provisions of Section 817-(h) of the Internal Revenue Code regarding Variable Trusts. No provision is made by the Fund for federal or state taxes on any taxable income of the Fund because each separate account in the Fund is ultimately responsible for the payment of any taxes. The Fund will distribute at least annually all of the Fund's net investment income and net realized capital gains, if any. At December 31, 2005, the Fund, for federal income tax purposes, had a capital loss carryover of $296,534, which will reduce the Fund's taxable income arising from future net realized gains on investments, if any, to the extent permitted by the Internal Revenue Code and thus will reduce the amount of distributions to shareholders which would otherwise be necessary to relieve the Fund of any liability for federal income tax. Such capital loss carryover expires on December 31, 2012, $48,462 and December 31, 2013, $248,072. Additionally, at December 31, 2005, the Fund had a net capital loss of $24,980 attributable to security transactions incurred after October 31, 2005. This capital loss is treated as arising on the first day of the Fund's taxable year ending December 31, 2006.

D Expense Reduction — Investors Bank & Trust Company (IBT) serves as custodian to the Fund. Pursuant to the custodian agreement, IBT receives a fee reduced by credits which are determined based on the average daily cash balance the Fund maintains with IBT. All credit balances used to reduce the Fund's custodian fees are reported as a reduction of total expenses in the Statement of Operations.

E Unfunded Loan Commitments — The Fund may enter into certain credit agreements all or a portion of which may be unfunded. The Fund is obligated to fund these loan commitments at the borrower's discretion. These commitments are disclosed in the accompanying Portfolio of Investments.

F Use of Estimates — The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expense during the reporting period. Actual results could differ from those estimates.