UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-10067 |

|

Eaton Vance Variable Trust |

(Exact name of registrant as specified in charter) |

|

The Eaton Vance Building, 255 State Street, Boston, Massachusetts | | 02109 |

(Address of principal executive offices) | | (Zip code) |

|

Alan R. Dynner The Eaton Vance Building, 255 State Street, Boston, Massachusetts 02109 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (617) 482-8260 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2007 | |

| | | | | | | | |

Item 1. Reports to Stockholders

Annual Report December 31, 2007

EATON VANCE

VT

FLOATING-

RATE

INCOME

FUND

IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS, AND PROXY VOTING

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy ("Privacy Policy") with respect to nonpublic personal information about its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer's account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer's account (i.e., fund shares) is held in the name of a third-party financial adviser/broker-dealer, it is likely that only such adviser's privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance's Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission (the "SEC") permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called "householding" and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and its underlying Portfolio (if applicable) will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC's website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC's public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds' and Portfolios' Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to Portfolio securities during the most recent 12 month period ended June 30, without charge, upon request, by calling 1-800-262-1122. This description is also available on the SEC's website at www.sec.gov.

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

FUND EXPENSES

Example: As a shareholder of the Fund, you incur ongoing costs including management fees, distribution or service fees, and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2007 – December 31, 2007).

Actual Expenses: The first section of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed annual rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect expenses and charges which are, or may be, imposed under your variable annuity contract or variable life insurance policy ("variable contracts") (if applicable). Therefore, the second line of the table is useful in comparing ongoing costs associated with an investment in vehicles which fund benefits under variable contracts, and will not help you determine the relative total costs of owning different funds. In addition, if these expenses and charges imposed under the variable contracts were included, your costs would have been higher.

Eaton Vance VT Floating-Rate Income Fund

| | | Beginning Account Value

(7/1/07) | | Ending Account Value

(12/31/07) | | Expenses Paid During Period*

(7/1/07 – 12/31/07) | |

| Actual | | $ | 1,000.00 | | | $ | 986.70 | | | $ | 5.71 | | |

| Hypothetical | |

| (5% return per year before expenses) | | $ | 1,000.00 | | | $ | 1,019.50 | | | $ | 5.80 | | |

* Expenses are equal to the Fund's annualized expense ratio of 1.14% multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2007. Expenses shown do not include insurance-related charges.

4

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

ManagEMEnt’s DisCussion of funD PERFORMANCE

Scott H. Page, CFA

Co-Portfolio Manager

Craig R. Russ, CFA

Co-Portfolio Manager

Economic and Market Conditions

· The loan market underwent an unprecedented price dislocation in the second half of 2007, during which loan prices fell, on average, approximately 4-5%. The decline began as a reaction to the unrelated but growing subprime problem. The decline was further compounded by technical pressures, as significant new loan supply faced weakening demand from loan investors, who pulled back in the face of falling prices. As the subprime problems widened, their impact on the economy became a growing concern and added further pressure on the bank loan market.

· Management believes that the fundamentals of the asset class remain sound. According to Standard & Poor’s Leveraged Commentary and Data, the lagging 12-month default rate remained at a historical low of 0.24%, by principal, at December 31, 2007. Further, in the second half of 2007, public filers in the S&P/LSTA Leveraged Loan Index continued to perform well. Credit losses for the year were minimal. Many loan market participants believe that credit defaults may revert, over time, to the mean of approximately 3%, which management believes is consistent with the historical performance of this asset class.

Management Discussion

· The Fund’s investment objective is to seek to provide a high level of current income. To do so, the Fund invests primarily in senior floating rate loans (“Senior Loans”). The Fund normally invests at least 80% of its net assets in income producing floating rate loans and other floating rate debt securities.

· The Fund’s investments included senior loans to 477 borrowers spanning 39 industries at December 31, 2007, with an average loan size of 0.20% of total investments, and no industry constituting more than 10% of total investments. Health care, business equipment and services, chemicals and plastics, publishing, and cable and satellite television were the largest industry weightings. The Fund is diversified in terms of industry, market and geography – a strategy management believes may help the Fund weather an economic downturn.

· The Fund had a less than 1% exposure to home builders during the period. Home builders have struggled in the recent economic climate; however, management believes that these loans may benefit from the security and collateral that back these exposures. The Fund did not have any direct exposure to subprime or prime mortgage lenders during the period ended December 31, 2007.

· The Fund’s net asset value reflected the market correction, declining in July and August, before temporarily rebounding slightly in September and October. The Fund’s net asset value fell again toward year-end, as the dimensions of the credit crisis widened.

Eaton Vance Vt floating-rate income fund Total return Performance 12/31/06 – 12/31/07 | | | |

The Fund - at Net Asset Value (NAV)(1) | | 1.62 | % |

S&P/LSTA Leveraged Loan Index(2) | | 2.02 | % |

(1) | There is no sales charge. Insurance-related charges are not included in the calculations of returns. Such expenses would reduce the overall returns shown. Please refer to the report for your insurance contract for performance data reflecting insurance-related charges. |

(2) | It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. The S&P/LSTA Leveraged Loan Index is an unmanaged loan market index. |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to www.eatonvance.com.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

1

· Effective January 30, 2008, Andrew Sveen assumed portfolio management responsibilities for Eaton Vance VT Floating-Rate Income Fund. Mr. Sveen joined Eaton Vance in 1991 as a senior financial analyst in the bank loan group, and has been Head Trader for floating-rate funds since 2001. He also manages other Eaton Vance floating-rate loan funds and/or portfolios. Previously, Mr. Sveen worked as a corporate lending officer at State Street Bank.

Portfolio Composition

Top Ten Holdings(1)

By total investments

Charter Communications Operating, LLC | | 1.0 | % |

Community Health Systems, Inc. | | 0.9 | |

HCA, Inc. | | 0.9 | |

Univision Communications, Inc. | | 0.9 | |

SunGard Data Systems, Inc. | | 0.8 | |

Georgia-Pacific Corp. | | 0.8 | |

Insight Midwest Holdings LLC | | 0.7 | |

Idearc, Inc. | | 0.7 | |

UPC Broadband Holding B.V. | | 0.7 | |

Nielsen Finance LLC | | 0.7 | |

(1) | Reflects the Fund’s investments as of 12/31/07. Top Ten Holdings represented 8.1% of the Fund’s total investments and are shown as a percentage of the Fund’s total investments. |

Top Five Industries(2)

By total investments

Health Care | | 8.9 | % |

Business Equipment and Services | | 6.8 | |

Publishing | | 5.8 | |

Chemicals and Plastics | | 5.6 | |

Cable and Satellite Television | | 4.8 | |

(2) Reflects the Fund’s investments as of 12/31/07. Industries are shown as a percentage of the Fund’s total investments.

Credit Quality Ratings for

Total Loan Investments(3)

By total loan investments

Baa | | 1.7 | % |

Ba | | 59.3 | |

B | | 34.4 | |

Caa | | 0.2 | |

Non-Rated(4) | | 4.4 | |

(3) | Credit Quality ratings are those provided by Moody’s Investors Service, Inc., a nationally recognized bond rating service, as of 12/31/07. As a percentage of the Fund’s total loan investments as of 12/31/07. |

| |

(4) | Certain loans in which the Fund invests are not rated by a rating agency. In management’s opinion, such securities are comparable to loans rated by an independent rating agency in one of the categories listed above. |

The views expressed in this report are those of the portfolio managers and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and the investment adviser disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund. In addition, fund information provided in the report may not be representative of the Fund’s current or future investments and may change due to active management.

2

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

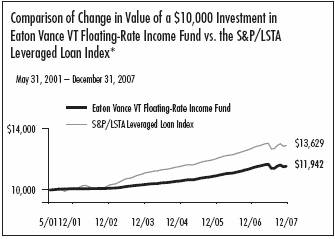

funD PERFORMANCE

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of the Fund with that of the S&P/LSTA Leveraged Loan Index, an unmanaged loan market index. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of the Fund and the S&P/LSTA Leveraged Loan Index. The table includes the total returns of the Fund at net asset value. There is no sales charge. The performance presented below does not reflect the deduction of insurance-related sales charges or of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares. Please refer to the report for your insurance contract for performance data reflecting insurance-related charges.

Performance(1) | | | |

| | | |

Average Annual Total Return (at net asset value) | | | |

One Year | | 1.62 | % |

Five Years | | 3.34 | |

Life of Fund† | | 2.74 | |

†Inception date: 5/2/01

(1) | The Fund has no sales charge. Insurance-related charges are not included in the calculation of returns. Such expenses would reduce the overall returns shown. |

Total Annual

Operating Expenses(2)

(2) From the Fund’s Prospectus dated 5/1/07.

* | Sources: Thomson Financial; Bloomberg, L.P.; Investment operations commenced on 5/2/01. |

| |

| The graph does not reflect the deduction of insurance-related charges or taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The Index’s total return does not reflect any commissions or expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. It is not possible to invest directly in an Index. Index performance is available as of month end only. |

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

3

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS

| Senior Floating-Rate Interests — 95.1%(1) | | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Aerospace and Defense — 2.0% | | | |

| ACTS Aero Technical Support & Service, Inc. | | | |

| $ | 479,865 | | | Term Loan, 8.47%, Maturing October 5, 2014 | | $ | 458,272 | | |

| AWAS Capital, Inc. | | | |

| | 215,991 | | | Term Loan, 6.69%, Maturing March 22, 2013 | | | 202,221 | | |

| BE Aerospace, Inc. | | | |

| | 125,000 | | | Term Loan, 6.73%, Maturing August 24, 2012 | | | 124,713 | | |

| DAE Aviation Holdings, Inc. | | | |

| | 834,528 | | | Term Loan, 7.80%, Maturing July 31, 2009 | | | 834,006 | | |

| | 377,787 | | | Term Loan, 8.74%, Maturing July 31, 2014 | | | 376,429 | | |

| | 286,022 | | | Term Loan, 8.75%, Maturing July 31, 2014 | | | 284,994 | | |

| Evergreen International Aviation | | | |

| | 376,510 | | | Term Loan, 8.38%, Maturing October 31, 2011 | | | 363,332 | | |

| Hawker Beechcraft Acquisition | | | |

| | 218,230 | | | Term Loan, 6.83%, Maturing March 26, 2014 | | | 208,137 | | |

| | 2,559,742 | | | Term Loan, 6.83%, Maturing March 26, 2014 | | | 2,441,354 | | |

| Hexcel Corp. | | | |

| | 213,766 | | | Term Loan, 6.51%, Maturing March 1, 2012 | | | 210,560 | | |

| IAP Worldwide Services, Inc. | | | |

| | 171,500 | | | Term Loan, 11.13%, Maturing December 30, 2012 | | | 154,693 | | |

| PGS Solutions, Inc. | | | |

| | 1,889,481 | | | Term Loan, 7.27%, Maturing February 14, 2013 | | | 1,802,093 | | |

| Spirit AeroSystems, Inc. | | | |

| | 809,585 | | | Term Loan, 6.90%, Maturing December 31, 2011 | | | 802,501 | | |

| TransDigm, Inc. | | | |

| | 500,000 | | | Term Loan, Maturing June 23, 2013(2) | | | 490,000 | | |

| | 1,925,000 | | | Term Loan, 6.86%, Maturing June 23, 2013 | | | 1,884,606 | | |

| Vought Aircraft Industries, Inc. | | | |

| | 1,867,377 | | | Term Loan, 7.34%, Maturing December 17, 2011 | | | 1,836,253 | | |

| Wesco Aircraft Hardware Corp. | | | |

| | 413,313 | | | Term Loan, 7.08%, Maturing September 29, 2013 | | | 407,629 | | |

| Wyle Laboratories, Inc. | | | |

| | 992,500 | | | Term Loan, 7.96%, Maturing January 28, 2011 | | | 977,612 | | |

| | | | | | | $ | 13,859,405 | | |

| Air Transport — 0.5% | | | |

| Delta Air Lines, Inc. | | | |

| $ | 696,500 | | | Term Loan, 8.08%, Maturing April 30, 2014 | | $ | 665,655 | | |

| Northwest Airlines, Inc. | | | |

| | 1,000,000 | | | DIP Loan, Maturing August 21, 2008(2) | | | 947,500 | | |

| | 1,693,000 | | | DIP Loan, 6.97%, Maturing August 21, 2008 | | | 1,601,311 | | |

| | | | | | | $ | 3,214,466 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Automotive — 4.0% | | | |

| Accuride Corp. | | | |

| $ | 3,098,258 | | | Term Loan, 8.50%, Maturing January 31, 2012 | | $ | 3,036,293 | | |

| Adesa, Inc. | | | |

| | 3,383,000 | | | Term Loan, 7.08%, Maturing October 18, 2013 | | | 3,183,643 | | |

| Affina Group, Inc. | | | |

| | 268,350 | | | Term Loan, 7.96%, Maturing November 30, 2011 | | | 260,299 | | |

| Allison Transmission, Inc. | | | |

| | 2,025,000 | | | Term Loan, 7.96%, Maturing September 30, 2014 | | | 1,895,544 | | |

| Chrysler Financial | | | |

| | 1,000,000 | | | Term Loan, Maturing August 1, 2014(2) | | | 964,091 | | |

| Dana Corp. | | | |

| | 1,500,000 | | | Term Loan, 7.36%, Maturing March 30, 2008 | | | 1,495,446 | | |

| Dayco Products, LLC | | | |

| | 500,000 | | | Term Loan, Maturing June 21, 2011(2) | | | 475,000 | | |

| | 474,931 | | | Term Loan, 9.53%, Maturing June 21, 2011 | | | 452,708 | | |

| Delphi Corp. | | | |

| | 1,000,000 | | | DIP Loan, 8.63%, Maturing July 1, 2008 | | | 998,375 | | |

| | 1,000,000 | | | DIP Loan, 9.13%, Maturing July 1, 2008 | | | 998,646 | | |

| Dollar Thrifty Automotive Group, Inc. | | | |

| | 597,000 | | | Term Loan, 6.85%, Maturing June 15, 2014 | | | 571,627 | | |

| Ford Motor Co. | | | |

| | 1,463,991 | | | Term Loan, 8.00%, Maturing December 15, 2013 | | | 1,358,350 | | |

| General Motors Corp. | | | |

| | 2,683,487 | | | Term Loan, 7.62%, Maturing November 29, 2013 | | | 2,513,523 | | |

| Goodyear Tire & Rubber Co. | | | |

| | 3,425,000 | | | Term Loan, 6.43%, Maturing April 30, 2010 | | | 3,222,713 | | |

| Keystone Automotive Operations, Inc. | | | |

| | 495,000 | | | Term Loan, 8.55%, Maturing January 12, 2012 | | | 452,100 | | |

| LKQ Corp. | | | |

| | 675,000 | | | Term Loan, 7.46%, Maturing October 12, 2014 | | | 673,312 | | |

| Tenneco Automotive, Inc. | | | |

| | 525,000 | | | Term Loan, 6.75%, Maturing March 17, 2014 | | | 500,062 | | |

| The Hertz Corp. | | | |

| | 379,938 | | | Term Loan, 4.91%, Maturing December 21, 2012 | | | 372,704 | | |

| | 2,106,454 | | | Term Loan, 6.89%, Maturing December 21, 2012 | | | 2,066,351 | | |

| TriMas Corp. | | | |

| | 187,500 | | | Term Loan, 6.79%, Maturing August 2, 2011 | | | 184,453 | | |

| | 802,344 | | | Term Loan, 7.23%, Maturing August 2, 2013 | | | 789,306 | | |

| TRW Automotive, Inc. | | | |

| | 920,375 | | | Term Loan, 6.69%, Maturing February 2, 2014 | | | 900,242 | | |

| United Components, Inc. | | | |

| | 1,014,224 | | | Term Loan, 6.91%, Maturing June 30, 2010 | | | 978,727 | | |

| | | | | | | $ | 28,343,515 | | |

See notes to financial statements

5

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Beverage and Tobacco — 0.3% | | | |

| Constellation Brands, Inc. | | | |

| $ | 620,000 | | | Term Loan, 6.60%, Maturing June 5, 2013 | | $ | 605,146 | | |

| Culligan International Co. | | | |

| | 1,811,313 | | | Term Loan, 7.09%, Maturing November 24, 2014 | | | 1,523,767 | | |

| Southern Wine & Spirits of America, Inc. | | | |

| | 331,863 | | | Term Loan, 6.34%, Maturing May 31, 2012 | | | 331,448 | | |

| | | | | | | $ | 2,460,361 | | |

| Brokers, Dealers and Investment Houses — 0.1% | | | |

| AmeriTrade Holding Corp. | | | |

| $ | 728,837 | | | Term Loan, 6.35%, Maturing December 31, 2012 | | $ | 711,279 | | |

| | | | | | | $ | 711,279 | | |

| Building and Development — 3.1% | | | |

| AIMCO Properties, L.P. | | | |

| $ | 1,225,000 | | | Term Loan, 6.37%, Maturing March 23, 2011 | | $ | 1,200,118 | | |

| Beacon Sales Acquisition, Inc. | | | |

| | 296,250 | | | Term Loan, 7.21%, Maturing September 30, 2013 | | | 269,587 | | |

| Brickman Group Holdings, Inc. | | | |

| | 1,290,250 | | | Term Loan, 7.14%, Maturing January 23, 2014 | | | 1,225,737 | | |

| Building Materials Corp. of America | | | |

| | 792,030 | | | Term Loan, 7.94%, Maturing February 22, 2014 | | | 670,397 | | |

| Capital Automotive (REIT) | | | |

| | 325,592 | | | Term Loan, 6.98%, Maturing December 16, 2010 | | | 319,117 | | |

| Contech Construction Products | | | |

| | 787,873 | | | Term Loan, 7.12%, Maturing January 13, 2013 | | | 752,419 | | |

| Epco/Fantome, LLC | | | |

| | 230,000 | | | Term Loan, 7.59%, Maturing November 23, 2010 | | | 228,850 | | |

| General Growth Properties, Inc. | | | |

| | 348,684 | | | Term Loan, 6.50%, Maturing February 24, 2011 | | | 332,957 | | |

| LNR Property Corp. | | | |

| | 1,750,000 | | | Term Loan, 7.63%, Maturing July 3, 2011 | | | 1,674,531 | | |

| Mueller Water Products, Inc. | | | |

| | 1,000,000 | | | Term Loan, Maturing May 24, 2014(2) | | | 953,750 | | |

| | 915,853 | | | Term Loan, 6.73%, Maturing May 24, 2014 | | | 863,117 | | |

| NCI Building Systems, Inc. | | | |

| | 200,893 | | | Term Loan, 6.71%, Maturing June 18, 2010 | | | 189,844 | | |

| Nortek, Inc. | | | |

| | 319,275 | | | Term Loan, 7.10%, Maturing August 27, 2011 | | | 297,724 | | |

| Panolam Industries Holdings, Inc. | | | |

| | 1,707,000 | | | Term Loan, 7.59%, Maturing September 30, 2012 | | | 1,621,650 | | |

| PLY GEM Industries, Inc. | | | |

| | 1,076,343 | | | Term Loan, 7.58%, Maturing August 15, 2011 | | | 985,392 | | |

| | 33,667 | | | Term Loan, 7.58%, Maturing August 15, 2011 | | | 30,822 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Building and Development (continued) | | | |

| Re/Max International, Inc. | | | |

| $ | 66,667 | | | Term Loan, 0.00%, Maturing January 23, 2008(3) | | $ | 66,167 | | |

| Realogy Corp. | | | |

| | 548,758 | | | Term Loan, 4.97%, Maturing September 1, 2014 | | | 481,687 | | |

| | 2,038,242 | | | Term Loan, 8.24%, Maturing September 1, 2014 | | | 1,789,124 | | |

| Standard Pacific Corp. | | | |

| | 450,000 | | | Term Loan, 6.66%, Maturing May 5, 2013 | | | 334,500 | | |

| Stile Acquisition Corp. | | | |

| | 320,652 | | | Term Loan, 7.03%, Maturing April 6, 2013 | | | 292,729 | | |

| Stile U.S. Acquisition Corp. | | | |

| | 321,198 | | | Term Loan, 7.03%, Maturing April 6, 2013 | | | 293,227 | | |

| TRU 2005 RE Holding Co. | | | |

| | 4,450,000 | | | Term Loan, 8.23%, Maturing December 9, 2008 | | | 4,299,350 | | |

| Wintergames Acquisition ULC | | | |

| | 2,489,825 | | | Term Loan, 4.40%, Maturing April 24, 2008 | | | 2,471,152 | | |

| | | | | | | $ | 21,643,948 | | |

| Business Equipment and Services — 6.9% | | | |

| ACCO Brands Corp. | | | |

| $ | 1,640,175 | | | Term Loan, 6.79%, Maturing August 17, 2012 | | $ | 1,582,769 | | |

| Activant Solutions, Inc. | | | |

| | 998,109 | | | Term Loan, 6.95%, Maturing May 1, 2013 | | | 936,975 | | |

| | 997,494 | | | Term Loan, 8.00%, Maturing May 1, 2013 | | | 936,397 | | |

| Acxiom Corp. | | | |

| | 1,306,250 | | | Term Loan, 6.63%, Maturing September 15, 2012 | | | 1,263,797 | | |

| Affiliated Computer Services | | | |

| | 687,228 | | | Term Loan, 6.87%, Maturing March 20, 2013 | | | 669,564 | | |

| | 1,553,844 | | | Term Loan, 7.04%, Maturing March 20, 2013 | | | 1,513,905 | | |

| Affinion Group, Inc. | | | |

| | 1,223,414 | | | Term Loan, 7.48%, Maturing October 17, 2012 | | | 1,181,105 | | |

| Allied Security Holdings, LLC | | | |

| | 334,091 | | | Term Loan, 7.83%, Maturing June 30, 2010 | | | 330,750 | | |

| Buhrmann US, Inc. | | | |

| | 333,017 | | | Term Loan, 6.97%, Maturing December 31, 2010 | | | 326,357 | | |

| | 193,803 | | | Term Loan, 7.00%, Maturing December 31, 2010 | | | 189,927 | | |

| Cellnet Group, Inc. | | | |

| | 499,853 | | | Term Loan, 6.86%, Maturing July 22, 2011 | | | 484,077 | | |

| DynCorp International, LLC | | | |

| | 707,451 | | | Term Loan, 6.88%, Maturing February 11, 2011 | | | 682,690 | | |

| Education Management, LLC | | | |

| | 3,270,081 | | | Term Loan, 6.63%, Maturing June 1, 2013 | | | 3,139,278 | | |

| Info USA, Inc. | | | |

| | 990,000 | | | Term Loan, 6.83%, Maturing February 14, 2012 | | | 975,150 | | |

See notes to financial statements

6

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Business Equipment and Services (continued) | | | |

| Information Resources, Inc. | | | |

| $ | 926,161 | | | Term Loan, 6.77%, Maturing May 7, 2014 | | $ | 861,330 | | |

| Intergraph Corp. | | | |

| | 1,674,762 | | | Term Loan, 7.07%, Maturing May 29, 2014 | | | 1,614,052 | | |

| iPayment, Inc. | | | |

| | 1,713,895 | | | Term Loan, 6.87%, Maturing May 10, 2013 | | | 1,585,353 | | |

| Iron Mountain, Inc. | | | |

| | 1,666,625 | | | Term Loan, 6.59%, Maturing April 16, 2014 | | | 1,658,292 | | |

| Kronos, Inc. | | | |

| | 790,286 | | | Term Loan, 7.08%, Maturing June 11, 2014 | | | 746,820 | | |

| Mitchell International, Inc. | | | |

| | 1,488,750 | | | Term Loan, 6.84%, Maturing March 28, 2014 | | | 1,384,537 | | |

| N.E.W. Holdings I, LLC | | | |

| | 1,162,820 | | | Term Loan, 7.49%, Maturing May 22, 2014 | | | 1,081,422 | | |

| Protection One, Inc. | | | |

| | 1,033,472 | | | Term Loan, 7.21%, Maturing March 31, 2012 | | | 994,717 | | |

| Quintiles Transnational Corp. | | | |

| | 2,412,050 | | | Term Loan, 6.83%, Maturing March 31, 2013 | | | 2,330,643 | | |

| RiskMetrics Group Holdings, LLC | | | |

| | 1,538,375 | | | Term Loan, 7.08%, Maturing January 11, 2014 | | | 1,505,685 | | |

| Sabre, Inc. | | | |

| | 3,190,795 | | | Term Loan, 6.96%, Maturing September 30, 2014 | | | 2,917,765 | | |

| Safenet, Inc. | | | |

| | 746,250 | | | Term Loan, 7.75%, Maturing April 12, 2014 | | | 686,550 | | |

| Serena Software, Inc. | | | |

| | 500,000 | | | Term Loan, Maturing March 10, 2013(2) | | | 486,250 | | |

| | 460,000 | | | Term Loan, 7.18%, Maturing March 10, 2013 | | | 438,550 | | |

| Sitel (Client Logic) | | | |

| | 1,022,133 | | | Term Loan, 7.29%, Maturing January 29, 2014 | | | 919,920 | | |

| Solera Nederland Holdings | | | |

| | 1,481,255 | | | Term Loan, 7.06%, Maturing May 15, 2014 | | | 1,414,598 | | |

| SunGard Data Systems, Inc. | | | |

| | 5,941,620 | | | Term Loan, 6.90%, Maturing February 11, 2013 | | | 5,751,304 | | |

| TDS Investor Corp. | | | |

| | 995,000 | | | Term Loan, 7.08%, Maturing August 23, 2013 | | | 947,116 | | |

| | 1,367,022 | | | Term Loan, 7.08%, Maturing August 23, 2013 | | | 1,301,021 | | |

| | 274,294 | | | Term Loan, 7.08%, Maturing August 23, 2013 | | | 261,051 | | |

| Transaction Network Services, Inc. | | | |

| | 424,197 | | | Term Loan, 7.48%, Maturing May 4, 2012 | | | 417,834 | | |

| URS Corp. | | | |

| | 458,972 | | | Term Loan, 7.59%, Maturing May 15, 2013 | | | 459,164 | | |

| Valassis Communications, Inc. | | | |

| | 1,600,347 | | | Term Loan, 6.58%, Maturing March 2, 2014 | | | 1,508,327 | | |

| VWR International, Inc. | | | |

| | 1,175,000 | | | Term Loan, 7.33%, Maturing June 28, 2013 | | | 1,116,250 | | |

| West Corp. | | | |

| | 2,476,288 | | | Term Loan, 7.30%, Maturing October 24, 2013 | | | 2,363,926 | | |

| | | | | | | $ | 48,965,218 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Cable and Satellite Television — 4.9% | | | |

| Atlantic Broadband Finance, LLC | | | |

| $ | 1,635,018 | | | Term Loan, 7.08%, Maturing February 10, 2011 | | $ | 1,589,033 | | |

| Bragg Communications, Inc. | | | |

| | 972,563 | | | Term Loan, 7.58%, Maturing August 31, 2014 | | | 972,562 | | |

| Bresnan Broadband Holdings, LLC | | | |

| | 2,700,000 | | | Term Loan, 6.96%, Maturing March 29, 2014 | | | 2,585,812 | | |

| | 1,300,000 | | | Term Loan, 7.18%, Maturing March 29, 2014 | | | 1,245,020 | | |

| Cequel Communications, LLC | | | |

| | 2,977,500 | | | Term Loan, 7.21%, Maturing November 5, 2013 | | | 2,791,406 | | |

| Charter Communications Operating, Inc. | | | |

| | 7,434,441 | | | Term Loan, 6.99%, Maturing April 28, 2013 | | | 6,960,852 | | |

| CSC Holdings, Inc. | | | |

| | 3,276,737 | | | Term Loan, 6.90%, Maturing March 29, 2013 | | | 3,102,368 | | |

| CW Media Holdings, Inc. | | | |

| | 448,875 | | | Term Loan, 8.08%, Maturing February 15, 2015 | | | 446,631 | | |

| DirecTV Holdings, LLC | | | |

| | 1,807,557 | | | Term Loan, 6.36%, Maturing April 13, 2013 | | | 1,790,486 | | |

| Insight Midwest Holdings, LLC | | | |

| | 5,500,000 | | | Term Loan, 7.00%, Maturing April 6, 2014 | | | 5,319,721 | | |

| MCC Iowa, LLC | | | |

| | 194,250 | | | Term Loan, 6.54%, Maturing March 31, 2010 | | | 183,748 | | |

| Mediacom Broadband Group | | | |

| | 997,481 | | | Term Loan, 6.69%, Maturing January 31, 2015 | | | 924,985 | | |

| | 247,500 | | | Term Loan, 6.69%, Maturing January 31, 2015 | | | 229,512 | | |

| Mediacom Illinois, LLC | | | |

| | 443,025 | | | Term Loan, 6.69%, Maturing January 31, 2015 | | | 414,070 | | |

| NTL Investment Holdings, Ltd. | | | |

| | 677,570 | | | Term Loan, 7.22%, Maturing March 30, 2012 | | | 648,139 | | |

| UPC Broadband Holding B.V. | | | |

| | 5,500,000 | | | Term Loan, 7.13%, Maturing December 31, 2014 | | | 5,219,846 | | |

| | | | | | | $ | 34,424,191 | | |

| Chemicals and Plastics — 5.7% | | | |

| AZ Chem US, Inc. | | | |

| $ | 992,500 | | | Term Loan, 7.08%, Maturing February 28, 2013 | | $ | 903,175 | | |

| Brenntag Holding GmbH and Co. KG | | | |

| | 255,273 | | | Term Loan, 7.39%, Maturing December 23, 2013 | | | 244,424 | | |

| | 1,044,727 | | | Term Loan, 7.39%, Maturing December 23, 2013 | | | 1,000,326 | | |

| Celanese Holdings, LLC | | | |

| | 1,000,000 | | | Term Loan, Maturing April 2, 2014(2) | | | 967,500 | | |

| | 2,860,612 | | | Term Loan, 6.98%, Maturing April 2, 2014 | | | 2,764,693 | | |

| Cognis GmbH | | | |

| | 975,000 | | | Term Loan, 6.99%, Maturing September 15, 2013 | | | 915,484 | | |

| Columbian Chemicals Acquisition | | | |

| | 1,473,446 | | | Term Loan, 6.58%, Maturing March 16, 2013 | | | 1,396,090 | | |

See notes to financial statements

7

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Chemicals and Plastics (continued) | | | |

| Foamex L.P. | | | |

| $ | 1,217,647 | | | Term Loan, 7.46%, Maturing February 12, 2013 | | $ | 1,120,235 | | |

| Georgia Gulf Corp. | | | |

| | 1,325,938 | | | Term Loan, 7.76%, Maturing October 3, 2013 | | | 1,277,596 | | |

| Hercules, Inc. | | | |

| | 261,490 | | | Term Loan, 6.71%, Maturing October 8, 2010 | | | 260,836 | | |

| Hexion Specialty Chemicals, Inc. | | | |

| | 497,500 | | | Term Loan, 7.13%, Maturing May 5, 2012 | | | 481,603 | | |

| | 409,141 | | | Term Loan, 7.13%, Maturing May 5, 2013 | | | 396,068 | | |

| | 1,690,895 | | | Term Loan, 7.19%, Maturing May 5, 2013 | | | 1,636,866 | | |

| | 1,888,239 | | | Term Loan, 7.50%, Maturing May 5, 2013 | | | 1,827,904 | | |

| Huish Detergents, Inc. | | | |

| | 597,000 | | | Term Loan, 6.83%, Maturing April 26, 2014 | | | 522,375 | | |

| Huntsman International, LLC | | | |

| | 1,000,000 | | | Term Loan, Maturing August 16, 2012(2) | | | 983,750 | | |

| | 2,629,268 | | | Term Loan, 6.62%, Maturing August 16, 2012 | | | 2,587,552 | | |

| INEOS Group | | | |

| | 661,500 | | | Term Loan, 7.36%, Maturing December 14, 2013 | | | 642,827 | | |

| | 661,500 | | | Term Loan, 7.86%, Maturing December 14, 2014 | | | 642,827 | | |

| Innophos, Inc. | | | |

| | 612,782 | | | Term Loan, 7.08%, Maturing August 10, 2010 | | | 602,058 | | |

| Invista B.V. | | | |

| | 196,000 | | | Term Loan, 6.33%, Maturing April 30, 2010 | | | 188,650 | | |

| | 161,531 | | | Term Loan, 6.33%, Maturing April 29, 2011 | | | 157,022 | | |

| | 85,623 | | | Term Loan, 6.33%, Maturing April 29, 2011 | | | 83,233 | | |

| ISP Chemco, Inc. | | | |

| | 2,786,000 | | | Term Loan, 6.78%, Maturing June 4, 2014 | | | 2,659,237 | | |

| Kleopatra | | | |

| | 1,175,000 | | | Term Loan, 7.74%, Maturing January 3, 2016 | | | 1,004,625 | | |

| Kranton Polymers, LLC | | | |

| | 1,782,032 | | | Term Loan, 7.25%, Maturing May 12, 2013 | | | 1,695,158 | | |

| Lucite International Group Holdings | | | |

| | 322,805 | | | Term Loan, 7.10%, Maturing July 7, 2013 | | | 309,691 | | |

| | 911,689 | | | Term Loan, 7.10%, Maturing July 7, 2013 | | | 874,652 | | |

| MacDermid, Inc. | | | |

| | 2,371,882 | | | Term Loan, 6.83%, Maturing April 12, 2014 | | | 2,265,147 | | |

| Millenium Inorganic Chemicals | | | |

| | 875,000 | | | Term Loan, 7.08%, Maturing April 30, 2014 | | | 809,375 | | |

| Momentive Performance Material | | | |

| | 1,138,500 | | | Term Loan, 7.13%, Maturing December 4, 2013 | | | 1,092,756 | | |

| Mosaic Co. | | | |

| | 82,095 | | | Term Loan, 6.63%, Maturing December 21, 2012 | | | 81,824 | | |

| MSCI, Inc. | | | |

| | 1,000,000 | | | Term Loan, 7.95%, Maturing November 5, 2014 | | | 1,002,813 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Chemicals and Plastics (continued) | | | |

| Nalco Co. | | | |

| $ | 2,756,520 | | | Term Loan, 6.92%, Maturing November 4, 2010 | | $ | 2,715,938 | | |

| Propex Fabrics, Inc. | | | |

| | 154,532 | | | Term Loan, 11.25%, Maturing July 31, 2012 | | | 124,398 | | |

| Rockwood Specialties Group, Inc. | | | |

| | 2,869,370 | | | Term Loan, 6.46%, Maturing December 10, 2012 | | | 2,774,520 | | |

| Solo Cup Co. | | | |

| | 185,837 | | | Term Loan, 8.48%, Maturing February 27, 2011 | | | 184,443 | | |

| Solutia, Inc. | | | |

| | 945,138 | | | DIP Loan, 8.06%, Maturing March 31, 2008 | | | 944,252 | | |

| | | | | | | $ | 40,141,923 | | |

| Clothing / Textiles — 0.3% | | | |

| Hanesbrands, Inc. | | | |

| $ | 1,290,045 | | | Term Loan, 6.78%, Maturing September 5, 2013 | | $ | 1,260,481 | | |

| The William Carter Co. | | | |

| | 1,046,697 | | | Term Loan, 6.43%, Maturing July 14, 2012 | | | 1,015,296 | | |

| | | | | | | $ | 2,275,777 | | |

| Conglomerates — 2.6% | | | |

| Amsted Industries, Inc. | | | |

| $ | 2,500,716 | | | Term Loan, 7.21%, Maturing October 15, 2010 | | $ | 2,458,517 | | |

| | 468,632 | | | Term Loan, 7.01%, Maturing April 5, 2013 | | | 461,017 | | |

| Doncasters (Dunde HoldCo 4 Ltd.) | | | |

| | 681,731 | | | Term Loan, 7.48%, Maturing July 13, 2015 | | | 657,461 | | |

| | 681,731 | | | Term Loan, 7.98%, Maturing July 13, 2015 | | | 659,166 | | |

| Gentek, Inc. | | | |

| | 688,743 | | | Term Loan, 7.00%, Maturing February 28, 2011 | | | 676,690 | | |

| Goodman Global Holdings, Inc. | | | |

| | 143,593 | | | Term Loan, 6.59%, Maturing December 23, 2011 | | | 142,427 | | |

| Jarden Corp. | | | |

| | 2,188,880 | | | Term Loan, 6.58%, Maturing January 24, 2012 | | | 2,117,741 | | |

| | 87,599 | | | Term Loan, 6.58%, Maturing January 24, 2012 | | | 84,752 | | |

| | 997,494 | | | Term Loan, 7.33%, Maturing January 24, 2012 | | | 976,297 | | |

| Johnson Diversey, Inc. | | | |

| | 1,254,899 | | | Term Loan, 6.88%, Maturing December 16, 2011 | | | 1,232,546 | | |

| Polymer Group, Inc. | | | |

| | 1,546,921 | | | Term Loan, 7.09%, Maturing November 22, 2012 | | | 1,515,982 | | |

| RBS Global, Inc. | | | |

| | 500,000 | | | Term Loan, Maturing July 19, 2013(2) | | | 493,125 | | |

| | 1,197,500 | | | Term Loan, 7.40%, Maturing July 19, 2013 | | | 1,166,066 | | |

| | 1,901,639 | | | Term Loan, 7.58%, Maturing July 19, 2013 | | | 1,845,471 | | |

| RGIS Holdings, LLC | | | |

| | 117,327 | | | Term Loan, 7.35%, Maturing April 30, 2014 | | | 106,963 | | |

| | 2,346,545 | | | Term Loan, 7.47%, Maturing April 30, 2014 | | | 2,139,267 | | |

See notes to financial statements

8

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Conglomerates (continued) | | | |

| US Investigations Services, Inc. | | | |

| $ | 1,321,679 | | | Term Loan, 7.91%, Maturing February 21, 2015 | | $ | 1,250,639 | | |

| Vertrue, Inc. | | | |

| | 573,563 | | | Term Loan, 7.83%, Maturing August 16, 2014 | | | 547,752 | | |

| | | | | | | $ | 18,531,879 | | |

| Containers and Glass Products — 2.6% | | | |

| Berry Plastics Corp. | | | |

| $ | 3,725,616 | | | Term Loan, 7.16%, Maturing April 3, 2015 | | $ | 3,492,765 | | |

| Bluegrass Container Co. | | | |

| | 758,152 | | | Term Loan, 7.08%, Maturing June 30, 2013 | | | 753,729 | | |

| | 226,849 | | | Term Loan, 7.09%, Maturing June 30, 2013 | | | 225,525 | | |

| Consolidated Container Co. | | | |

| | 744,375 | | | Term Loan, 7.23%, Maturing March 28, 2014 | | | 633,960 | | |

| Crown Americas, Inc. | | | |

| | 490,000 | | | Term Loan, 6.62%, Maturing November 15, 2012 | | | 480,200 | | |

| Graham Packaging Holdings Co. | | | |

| | 3,976,231 | | | Term Loan, 7.50%, Maturing October 7, 2011 | | | 3,830,228 | | |

| Graphic Packaging International, Inc. | | | |

| | 4,023,258 | | | Term Loan, 7.10%, Maturing May 16, 2014 | | | 3,884,122 | | |

| IPG (US), Inc. | | | |

| | 205,625 | | | Term Loan, 8.24%, Maturing July 28, 2011 | | | 204,340 | | |

| JSG Acquisitions | | | |

| | 195,000 | | | Term Loan, 7.12%, Maturing December 31, 2013 | | | 187,322 | | |

| | 195,000 | | | Term Loan, 7.37%, Maturing December 13, 2014 | | | 188,297 | | |

| Kranson Industries, Inc. | | | |

| | 296,669 | | | Term Loan, 7.09%, Maturing July 31, 2013 | | | 288,511 | | |

| Owens-Brockway Glass Container | | | |

| | 406,938 | | | Term Loan, 6.43%, Maturing June 14, 2013 | | | 397,578 | | |

| Pregis Corp. | | | |

| | 293,250 | | | Term Loan, 7.08%, Maturing October 12, 2011 | | | 282,986 | | |

| Smurfit-Stone Container Corp. | | | |

| | 505,255 | | | Term Loan, 5.02%, Maturing November 1, 2011 | | | 495,290 | | |

| | 597,272 | | | Term Loan, 7.06%, Maturing November 1, 2011 | | | 585,492 | | |

| | 1,499,236 | | | Term Loan, 7.15%, Maturing November 1, 2011 | | | 1,470,422 | | |

| | 242,645 | | | Term Loan, 7.25%, Maturing November 1, 2011 | | | 237,981 | | |

| Tegrant Holding Corp. | | | |

| | 992,500 | | | Term Loan, 7.60%, Maturing March 8, 2013 | | | 890,769 | | |

| | | | | | | $ | 18,529,517 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Cosmetics / Toiletries — 0.4% | | | |

| American Safety Razor Co. | | | |

| $ | 2,191,313 | | | Term Loan, 7.51%, Maturing July 31, 2013 | | $ | 2,136,530 | | |

| Bausch & Lomb, Inc. | | | |

| | 80,000 | | | Term Loan, 0.00%, Maturing April 30, 2015(3) | | | 79,775 | | |

| | 320,000 | | | Term Loan, 8.08%, Maturing April 30, 2015 | | | 319,100 | | |

| Prestige Brands, Inc. | | | |

| | 253,711 | | | Term Loan, 6.98%, Maturing April 7, 2011 | | | 248,796 | | |

| | | | | | | $ | 2,784,201 | | |

| Drugs — 1.2% | | | |

| Chattem, Inc. | | | |

| $ | 855,035 | | | Term Loan, 6.97%, Maturing January 2, 2013 | | $ | 846,485 | | |

| Graceway Pharmaceuticals, LLC | | | |

| | 1,087,500 | | | Term Loan, 7.58%, Maturing May 3, 2012 | | | 1,027,959 | | |

| Pharmaceutical Holdings Corp. | | | |

| | 336,875 | | | Term Loan, 8.10%, Maturing January 30, 2012 | | | 330,980 | | |

| Royal Pharma Finance Trust | | | |

| | 496,250 | | | Term Loan, 7.10%, Maturing April 16, 2013 | | | 494,286 | | |

| Stiefel Laboratories, Inc. | | | |

| | 216,748 | | | Term Loan, Maturing December 28, 2013(2) | | | 211,871 | | |

| | 283,252 | | | Term Loan, Maturing December 28, 2013(2) | | | 276,879 | | |

| | 858,106 | | | Term Loan, 7.50%, Maturing December 28, 2013 | | | 834,768 | | |

| | 1,121,894 | | | Term Loan, 7.50%, Maturing December 28, 2013 | | | 1,091,382 | | |

| Warner Chilcott Corp. | | | |

| | 230,952 | | | Term Loan, Maturing January 18, 2012(2) | | | 226,910 | | |

| | 769,048 | | | Term Loan, Maturing January 18, 2012(2) | | | 755,590 | | |

| | 625,327 | | | Term Loan, 6.83%, Maturing January 18, 2012 | | | 604,572 | | |

| | 1,820,313 | | | Term Loan, 6.85%, Maturing January 18, 2012 | | | 1,758,789 | | |

| | | | | | | $ | 8,460,471 | | |

| Ecological Services and Equipment — 1.3% | | | |

| Allied Waste Industries, Inc. | | | |

| $ | 799,549 | | | Term Loan, 5.50%, Maturing January 15, 2012 | | $ | 766,749 | | |

| | 1,329,840 | | | Term Loan, 6.59%, Maturing January 15, 2012 | | | 1,275,286 | | |

| Big Dumpster Merger Sub, Inc. | | | |

| | 1,030,650 | | | Term Loan, 7.08%, Maturing February 5, 2013 | | | 961,081 | | |

| Casella Waste Systems, Inc. | | | |

| | 994,857 | | | Term Loan, 7.22%, Maturing April 28, 2010 | | | 969,364 | | |

| Energy Solutions, LLC | | | |

| | 733,491 | | | Term Loan, 7.22%, Maturing June 7, 2013 | | | 713,320 | | |

| IESI Corp. | | | |

| | 2,000,000 | | | Term Loan, 6.61%, Maturing January 20, 2012 | | | 1,927,500 | | |

| Sensus Metering Systems, Inc. | | | |

| | 13,550 | | | Term Loan, 6.88%, Maturing December 17, 2010 | | | 13,313 | | |

| | 208,561 | | | Term Loan, 7.04%, Maturing December 17, 2010 | | | 204,911 | | |

See notes to financial statements

9

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Ecological Services and Equipment (continued) | | | |

| Synagro Technologies, Inc. | | | |

| $ | 746,250 | | | Term Loan, 6.89%, Maturing June 21, 2012 | | $ | 720,131 | | |

| Waste Services, Inc. | | | |

| | 963,649 | | | Term Loan, 7.40%, Maturing March 31, 2011 | | | 941,967 | | |

| Wastequip, Inc. | | | |

| | 433,958 | | | Term Loan, 7.08%, Maturing February 5, 2013 | | | 404,666 | | |

| | | | | | | $ | 8,898,288 | | |

| Electronics / Electrical — 3.5% | | | |

| AMI Semiconductor, Inc. | | | |

| $ | 1,091,919 | | | Term Loan, 6.85%, Maturing April 1, 2012 | | $ | 1,070,080 | | |

| Aspect Software, Inc. | | | |

| | 1,149,267 | | | Term Loan, 7.94%, Maturing July 11, 2011 | | | 1,114,789 | | |

| Baldor Electric Co. | | | |

| | 863,111 | | | Term Loan, 6.96%, Maturing January 31, 2014 | | | 849,265 | | |

| EnerSys Capital, Inc. | | | |

| | 491,222 | | | Term Loan, 6.74%, Maturing March 17, 2011 | | | 478,327 | | |

| Fairchild Semiconductor Corp. | | | |

| | 566,375 | | | Term Loan, 6.33%, Maturing June 26, 2013 | | | 543,720 | | |

| Freescale Semiconductor, Inc. | | | |

| | 3,370,975 | | | Term Loan, 6.98%, Maturing December 1, 2013 | | | 3,131,848 | | |

| Infor Enterprise Solutions Holdings | | | |

| | 497,500 | | | Term Loan, 7.95%, Maturing July 28, 2012 | | | 468,894 | | |

| | 1,460,902 | | | Term Loan, 8.58%, Maturing July 28, 2012 | | | 1,406,119 | | |

| | 762,210 | | | Term Loan, 8.58%, Maturing July 28, 2012 | | | 733,627 | | |

| Invensys International Holding | | | |

| | 1,472,222 | | | Term Loan, 6.90%, Maturing December 15, 2010 | | | 1,437,871 | | |

| | 527,778 | | | Term Loan, 7.24%, Maturing January 15, 2011 | | | 525,139 | | |

| Network Solutions, LLC | | | |

| | 896,419 | | | Term Loan, 7.33%, Maturing March 7, 2014 | | | 844,875 | | |

| Open Solutions, Inc. | | | |

| | 2,186,292 | | | Term Loan, 7.28%, Maturing January 23, 2014 | | | 2,048,282 | | |

| Sensata Technologies Finance Co. | | | |

| | 2,580,452 | | | Term Loan, 6.76%, Maturing April 27, 2013 | | | 2,458,802 | | |

| Spectrum Brands, Inc. | | | |

| | 500,000 | | | Term Loan, Maturing March 30, 2013(2) | | | 489,375 | | |

| | 96,487 | | | Term Loan, 5.09%, Maturing March 30, 2013 | | | 93,641 | | |

| | 1,898,754 | | | Term Loan, 9.12%, Maturing March 30, 2013 | | | 1,838,616 | | |

| SS&C Technologies, Inc. | | | |

| | 1,576,297 | | | Term Loan, 6.83%, Maturing November 23, 2012 | | | 1,529,008 | | |

| TTM Technologies, Inc. | | | |

| | 212,500 | | | Term Loan, 7.26%, Maturing October 27, 2012 | | | 210,375 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Electronics / Electrical (continued) | | | |

| VeriFone, Inc. | | | |

| $ | 500,000 | | | Term Loan, Maturing October 31, 2013(2) | | $ | 488,750 | | |

| | 552,250 | | | Term Loan, 6.71%, Maturing October 31, 2013 | | | 537,194 | | |

| Vertafore, Inc. | | | |

| | 2,233,167 | | | Term Loan, 7.52%, Maturing January 31, 2012 | | | 2,155,006 | | |

| | | | | | | $ | 24,453,603 | | |

| Equipment Leasing — 0.2% | | | |

| Maxim Crane Works, L.P. | | | |

| $ | 621,875 | | | Term Loan, 7.23%, Maturing June 29, 2014 | | $ | 581,453 | | |

| United Rentals, Inc. | | | |

| | 302,133 | | | Term Loan, 5.32%, Maturing February 14, 2011 | | | 295,335 | | |

| | 716,399 | | | Term Loan, 7.11%, Maturing February 14, 2011 | | | 700,280 | | |

| | | | | | | $ | 1,577,068 | | |

| Farming / Agriculture — 0.4% | | | |

| BF Bolthouse HoldCo, LLC | | | |

| $ | 500,000 | | | Term Loan, Maturing December 16, 2012(2) | | $ | 488,750 | | |

| | 937,078 | | | Term Loan, 7.50%, Maturing December 16, 2012 | | | 914,197 | | |

| Central Garden & Pet Co. | | | |

| | 245,625 | | | Term Loan, 6.50%, Maturing February 28, 2014 | | | 214,308 | | |

| United Agri Products, Inc. | | | |

| | 1,226,932 | | | Term Loan, 7.90%, Maturing June 8, 2012 | | | 1,225,398 | | |

| | | | | | | $ | 2,842,653 | | |

| Financial Intermediaries — 1.5% | | | |

| Citco III, Ltd. | | | |

| $ | 750,000 | | | Term Loan, Maturing June 30, 2014(2) | | $ | 723,750 | | |

| | 1,400,000 | | | Term Loan, 6.97%, Maturing June 30, 2014 | | | 1,348,313 | | |

| E.A. Viner International Co. | | | |

| | 666,600 | | | Term Loan, 7.33%, Maturing July 31, 2013 | | | 656,601 | | |

| Grosvenor Capital Management | | | |

| | 1,703,513 | | | Term Loan, 7.19%, Maturing December 5, 2013 | | | 1,652,408 | | |

| INVESTools, Inc. | | | |

| | 300,000 | | | Term Loan, 8.09%, Maturing August 13, 2012 | | | 294,000 | | |

| LPL Holdings, Inc. | | | |

| | 2,197,588 | | | Term Loan, 6.83%, Maturing December 18, 2014 | | | 2,111,058 | | |

| Nuveen Investments, Inc. | | | |

| | 500,000 | | | Term Loan, Maturing November 2, 2014(2) | | | 492,500 | | |

| | 1,050,000 | | | Term Loan, 7.86%, Maturing November 2, 2014 | | | 1,043,800 | | |

| Oxford Acquisition III, Ltd. | | | |

| | 1,859,640 | | | Term Loan, 6.90%, Maturing May 24, 2014 | | | 1,755,035 | | |

| The Geo Group, Inc. | | | |

| | 333,416 | | | Term Loan, 6.38%, Maturing January 24, 2014 | | | 332,583 | | |

| | | | | | | $ | 10,410,048 | | |

See notes to financial statements

10

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Food Products — 3.0% | | | |

| Acosta, Inc. | | | |

| $ | 2,918,075 | | | Term Loan, 7.10%, Maturing July 28, 2013 | | $ | 2,790,409 | | |

| Advance Food Company, Inc. | | | |

| | 66,667 | | | Term Loan, 0.00%, Maturing March 16, 2014(3) | | | 63,000 | | |

| | 231,583 | | | Term Loan, 6.58%, Maturing March 16, 2014 | | | 218,846 | | |

| Advantage Sales & Marketing, Inc. | | | |

| | 1,726,782 | | | Term Loan, 6.88%, Maturing March 29, 2013 | | | 1,643,681 | | |

| | 299,174 | | | Term Loan, 6.88%, Maturing March 29, 2013 | | | 284,777 | | |

| American Seafoods Group, LLC | | | |

| | 369,950 | | | Term Loan, 6.58%, Maturing September 30, 2011 | | | 357,695 | | |

| | 1,182,203 | | | Term Loan, 6.58%, Maturing September 30, 2012 | | | 1,143,043 | | |

| B&G Foods, Inc. | | | |

| | 1,500,000 | | | Term Loan, 7.06%, Maturing February 23, 2013 | | | 1,471,875 | | |

| Birds Eye Foods, Inc. | | | |

| | 1,288,750 | | | Term Loan, 6.58%, Maturing March 22, 2013 | | | 1,225,923 | | |

| Chiquita Brands, LLC | | | |

| | 1,792,231 | | | Term Loan, 7.88%, Maturing June 28, 2012 | | | 1,758,627 | | |

| Dean Foods Co. | | | |

| | 3,476,244 | | | Term Loan, 6.58%, Maturing April 2, 2014 | | | 3,287,619 | | |

| Del Monte Corp. | | | |

| | 492,500 | | | Term Loan, 6.49%, Maturing February 8, 2012 | | | 488,267 | | |

| Dole Food Company, Inc. | | | |

| | 93,660 | | | Term Loan, 5.16%, Maturing April 12, 2013 | | | 87,081 | | |

| | 207,048 | | | Term Loan, 7.16%, Maturing April 12, 2013 | | | 192,503 | | |

| | 690,160 | | | Term Loan, 7.22%, Maturing April 12, 2013 | | | 641,676 | | |

| Michael Foods, Inc. | | | |

| | 252,790 | | | Term Loan, 6.85%, Maturing November 21, 2010 | | | 248,524 | | |

| Nash-Finch Co. | | | |

| | 474,800 | | | Term Loan, 7.81%, Maturing November 12, 2010 | | | 453,434 | | |

| National Dairy Holdings, L.P. | | | |

| | 358,771 | | | Term Loan, 6.98%, Maturing March 15, 2012 | | | 346,214 | | |

| Pinnacle Foods Finance, LLC | | | |

| | 3,109,375 | | | Term Loan, 7.93%, Maturing April 2, 2014 | | | 2,933,695 | | |

| Reddy Ice Group, Inc. | | | |

| | 1,675,000 | | | Term Loan, 7.00%, Maturing August 9, 2012 | | | 1,633,125 | | |

| | | | | | | $ | 21,270,014 | | |

| Food Service — 2.1% | | | |

| AFC Enterprises, Inc. | | | |

| $ | 168,010 | | | Term Loan, 7.13%, Maturing May 23, 2009 | | $ | 165,490 | | |

| Aramark Corp. | | | |

| | 268,485 | | | Term Loan, 5.20%, Maturing January 26, 2014 | | | 255,832 | | |

| | 3,752,339 | | | Term Loan, 6.83%, Maturing January 26, 2014 | | | 3,575,510 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Food Service (continued) | | | |

| Buffets, Inc. | | | |

| $ | 169,102 | | | Term Loan, 7.83%, Maturing May 1, 2013 | | $ | 140,439 | | |

| | 1,266,451 | | | Term Loan, 7.98%, Maturing November 1, 2013 | | | 1,051,788 | | |

| Burger King Corp. | | | |

| | 1,271,988 | | | Term Loan, 6.38%, Maturing June 30, 2012 | | | 1,254,896 | | |

| CBRL Group, Inc. | | | |

| | 1,564,401 | | | Term Loan, 6.40%, Maturing April 27, 2013 | | | 1,489,440 | | |

| Denny's, Inc. | | | |

| | 123,333 | | | Term Loan, 7.12%, Maturing March 31, 2012 | | | 120,867 | | |

| | 508,409 | | | Term Loan, 6.85%, Maturing March 31, 2012 | | | 498,241 | | |

| JRD Holdings, Inc. | | | |

| | 460,156 | | | Term Loan, 7.74%, Maturing June 26, 2014 | | | 448,652 | | |

| NPC International, Inc. | | | |

| | 920,000 | | | Term Loan, 6.69%, Maturing May 3, 2013 | | | 865,950 | | |

| OSI Restaurant Partners, LLC | | | |

| | 254,791 | | | Term Loan, 7.31%, Maturing May 9, 2013 | | | 234,726 | | |

| | 3,123,585 | | | Term Loan, 7.13%, Maturing May 9, 2014 | | | 2,877,603 | | |

| QCE Finance, LLC | | | |

| | 987,475 | | | Term Loan, 7.37%, Maturing May 5, 2013 | | | 929,735 | | |

| Sagittarius Restaurants, LLC | | | |

| | 245,625 | | | Term Loan, 7.08%, Maturing March 29, 2013 | | | 224,133 | | |

| Weight Watchers International, Inc. | | | |

| | 990,000 | | | Term Loan, 6.38%, Maturing January 26, 2014 | | | 964,631 | | |

| | | | | | | $ | 15,097,933 | | |

| Food / Drug Retailers — 2.0% | | | |

| General Nutrition Centers, Inc. | | | |

| $ | 1,811,313 | | | Term Loan, 7.26%, Maturing September 16, 2013 | | $ | 1,666,408 | | |

| Krispy Kreme Doughnut Corp. | | | |

| | 396,582 | | | Term Loan, 7.71%, Maturing February 16, 2014 | | | 373,778 | | |

| Pantry, Inc. (The) | | | |

| | 611,111 | | | Term Loan, 0.00%, Maturing May 15, 2014(3) | | | 571,007 | | |

| | 2,128,194 | | | Term Loan, 6.60%, Maturing May 15, 2014 | | | 1,988,532 | | |

| Rite Aid Corp. | | | |

| | 1,000,000 | | | Term Loan, Maturing June 1, 2014(2) | | | 972,500 | | |

| | 3,650,000 | | | Term Loan, 6.80%, Maturing June 1, 2014 | | | 3,383,969 | | |

| Roundy's Supermarkets, Inc. | | | |

| | 3,315,529 | | | Term Loan, 7.91%, Maturing November 3, 2011 | | | 3,258,545 | | |

| Supervalu, Inc. | | | |

| | 1,635,154 | | | Term Loan, 6.40%, Maturing June 1, 2012 | | | 1,606,084 | | |

| | | | | | | $ | 13,820,823 | | |

See notes to financial statements

11

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Forest Products — 1.8% | | | |

| Appleton Papers, Inc. | | | |

| $ | 895,500 | | | Term Loan, 6.74%, Maturing June 5, 2014 | | $ | 847,527 | | |

| Boise Cascade Holdings, LLC | | | |

| | 488,240 | | | Term Loan, 6.38%, Maturing April 30, 2014 | | | 482,869 | | |

| | 3,326,773 | | | Term Loan, 6.38%, Maturing April 30, 2014 | | | 3,290,179 | | |

| Domtar Corp. | | | |

| | 803,750 | | | Term Loan, 6.40%, Maturing March 7, 2014 | | | 773,322 | | |

| Georgia-Pacific Corp. | | | |

| | 990,000 | | | Term Loan, 6.84%, Maturing December 20, 2012 | | | 944,919 | | |

| | 4,878,230 | | | Term Loan, 6.87%, Maturing December 20, 2012 | | | 4,656,095 | | |

| Newpage Corp. | | | |

| | 1,025,000 | | | Term Loan, 8.69%, Maturing December 5, 2014 | | | 1,020,676 | | |

| Xerium Technologies, Inc. | | | |

| | 713,914 | | | Term Loan, 7.58%, Maturing May 18, 2012 | | | 661,263 | | |

| | | | | | | $ | 12,676,850 | | |

| Healthcare — 9.1% | | | |

| Accellent, Inc. | | | |

| $ | 1,479,874 | | | Term Loan, 7.79%, Maturing November 22, 2012 | | $ | 1,331,887 | | |

| Advanced Medical Optics, Inc. | | | |

| | 744,375 | | | Term Loan, 6.95%, Maturing April 2, 2014 | | | 697,386 | | |

| American Medical Systems | | | |

| | 707,975 | | | Term Loan, 7.54%, Maturing July 20, 2012 | | | 676,116 | | |

| AMN Healthcare, Inc. | | | |

| | 1,091,807 | | | Term Loan, 6.58%, Maturing November 2, 2011 | | | 1,065,194 | | |

| AMR HoldCo, Inc. | | | |

| | 1,432,164 | | | Term Loan, 7.14%, Maturing February 10, 2012 | | | 1,397,703 | | |

| Biomet, Inc. | | | |

| | 1,995,000 | | | Term Loan, 7.86%, Maturing December 26, 2014 | | | 1,976,297 | | |

| Cardinal Health 409, Inc. | | | |

| | 2,388,000 | | | Term Loan, 7.08%, Maturing April 10, 2014 | | | 2,228,799 | | |

| Carestream Health, Inc. | | | |

| | 2,999,503 | | | Term Loan, 7.00%, Maturing April 30, 2013 | | | 2,763,292 | | |

| Community Health Systems, Inc. | | | |

| | 324,826 | | | Term Loan, 0.00%, Maturing July 25, 2014(3) | | | 313,136 | | |

| | 6,458,623 | | | Term Loan, 7.33%, Maturing July 25, 2014 | | | 6,226,177 | | |

| Concentra, Inc. | | | |

| | 472,625 | | | Term Loan, 7.08%, Maturing June 25, 2014 | | | 443,480 | | |

| ConMed Corp. | | | |

| | 692,924 | | | Term Loan, 6.34%, Maturing April 13, 2013 | | | 675,601 | | |

| CRC Health Corp. | | | |

| | 1,703,443 | | | Term Loan, 7.09%, Maturing February 6, 2013 | | | 1,633,176 | | |

| | 772,506 | | | Term Loan, 7.09%, Maturing February 6, 2013 | | | 740,641 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Healthcare (continued) | | | |

| DaVita, Inc. | | | |

| $ | 3,056,280 | | | Term Loan, 6.55%, Maturing October 5, 2012 | | $ | 2,952,782 | | |

| DJO Finance, LLC | | | |

| | 550,000 | | | Term Loan, 7.83%, Maturing May 15, 2014 | | | 544,729 | | |

| Fresenius Medical Care Holdings | | | |

| | 1,264,760 | | | Term Loan, 6.27%, Maturing March 31, 2013 | | | 1,221,623 | | |

| Hanger Orthopedic Group, Inc. | | | |

| | 307,236 | | | Term Loan, 7.09%, Maturing May 30, 2013 | | | 294,946 | | |

| HCA, Inc. | | | |

| | 6,400,462 | | | Term Loan, 7.08%, Maturing November 18, 2013 | | | 6,176,177 | | |

| Health Management Association, Inc. | | | |

| | 4,134,596 | | | Term Loan, 6.58%, Maturing February 28, 2014 | | | 3,868,716 | | |

| HealthSouth Corp. | | | |

| | 2,616,113 | | | Term Loan, 7.75%, Maturing March 10, 2013 | | | 2,504,928 | | |

| Iasis Healthcare, LLC | | | |

| | 440,461 | | | Term Loan, 6.63%, Maturing March 14, 2014(3) | | | 418,622 | | |

| | 117,456 | | | Term Loan, 6.63%, Maturing March 14, 2014 | | | 111,632 | | |

| | 1,279,414 | | | Term Loan, 7.06%, Maturing March 14, 2014 | | | 1,215,977 | | |

| Ikaria Acquisition, Inc. | | | |

| | 308,797 | | | Term Loan, 7.08%, Maturing March 28, 2013 | | | 301,077 | | |

| IM U.S. Holdings, LLC | | | |

| | 1,344,497 | | | Term Loan, 6.84%, Maturing June 26, 2014 | | | 1,282,314 | | |

| Invacare Corp. | | | |

| | 1,185,990 | | | Term Loan, 7.17%, Maturing February 12, 2013 | | | 1,142,998 | | |

| inVentiv Health, Inc. | | | |

| | 942,722 | | | Term Loan, Maturing July 6, 2014(2) | | | 902,656 | | |

| | 57,278 | | | Term Loan, Maturing July 6, 2014(2) | | | 54,844 | | |

| | 40,000 | | | Term Loan, 0.00%, Maturing July 6, 2014(3) | | | 37,327 | | |

| | 656,700 | | | Term Loan, 6.58%, Maturing July 6, 2014 | | | 612,796 | | |

| Leiner Health Products, Inc. | | | |

| | 231,521 | | | Term Loan, 9.65%, Maturing May 27, 2011 | | | 195,519 | | |

| LifePoint Hospitals, Inc. | | | |

| | 1,449,394 | | | Term Loan, 6.72%, Maturing April 15, 2012 | | | 1,385,206 | | |

| Magellan Health Services, Inc. | | | |

| | 375,000 | | | Term Loan, 5.13%, Maturing August 15, 2008 | | | 367,500 | | |

| | 93,750 | | | Term Loan, 6.74%, Maturing August 15, 2008 | | | 91,875 | | |

| Matria Healthcare, Inc. | | | |

| | 461,899 | | | Term Loan, 6.83%, Maturing January 19, 2012 | | | 448,042 | | |

| | 892,954 | | | Term Loan, 6.91%, Maturing January 19, 2012 | | | 866,166 | | |

| MultiPlan Merger Corp. | | | |

| | 351,111 | | | Term Loan, 7.35%, Maturing April 12, 2013 | | | 340,688 | | |

| | 1,329,191 | | | Term Loan, 7.35%, Maturing April 12, 2013 | | | 1,289,731 | | |

| Mylan, Inc. | | | |

| | 400,000 | | | Term Loan, 8.24%, Maturing October 2, 2014 | | | 396,583 | | |

See notes to financial statements

12

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Healthcare (continued) | | | |

| National Mentor Holdings, Inc. | | | |

| $ | 73,271 | | | Term Loan, 5.32%, Maturing June 29, 2013 | | $ | 71,806 | | |

| | 1,210,657 | | | Term Loan, 6.73%, Maturing June 29, 2013 | | | 1,186,444 | | |

| National Rental Institutes, Inc. | | | |

| | 234,141 | | | Term Loan, 7.13%, Maturing March 31, 2013 | | | 227,703 | | |

| Physiotherapy Associates, Inc. | | | |

| | 585,167 | | | Term Loan, 8.12%, Maturing June 27, 2013 | | | 550,057 | | |

| Psychiatric Solutions Inc. | | | |

| | 996,084 | | | Term Loan, 6.79%, Maturing May 31, 2014 | | | 958,109 | | |

| RadNet Management, Inc. | | | |

| | 496,251 | | | Term Loan, 8.65%, Maturing November 15, 2012 | | | 496,251 | | |

| ReAble Therapeutics Finance, LLC | | | |

| | 3,826,545 | | | Term Loan, 7.11%, Maturing November 16, 2013 | | | 3,649,568 | | |

| Renal Advantage, Inc. | | | |

| | 803,628 | | | Term Loan, 7.47%, Maturing October 5, 2012 | | | 770,479 | | |

| Select Medical Holding Corp. | | | |

| | 1,000,000 | | | Term Loan, Maturing February 24, 2012(2) | | | 950,000 | | |

| | 1,283,038 | | | Term Loan, 6.99%, Maturing February 24, 2012 | | | 1,213,653 | | |

| Sunrise Medical Holdings, Inc. | | | |

| | 720,201 | | | Term Loan, 8.92%, Maturing May 13, 2010 | | | 648,181 | | |

| United Surgical Partners International | | | |

| | 161,290 | | | Term Loan, 7.35%, Maturing April 19, 2014(3) | | | 152,016 | | |

| | 832,419 | | | Term Loan, 7.38%, Maturing April 19, 2014 | | | 784,555 | | |

| Vanguard Health Holding Co., LLC | | | |

| | 982,631 | | | Term Loan, 7.10%, Maturing September 23, 2011 | | | 952,333 | | |

| Viant Holdings, Inc. | | | |

| | 398,000 | | | Term Loan, 7.08%, Maturing June 25, 2014 | | | 359,693 | | |

| | | | | | | $ | 64,165,187 | | |

| Home Furnishings — 1.7% | | | |

| Hunter Fan Co. | | | |

| $ | 30,000 | | | Term Loan, 0.00%, Maturing April 16, 2014(3) | | $ | 26,550 | | |

| | 291,275 | | | Term Loan, 7.38%, Maturing April 16, 2014 | | | 257,778 | | |

| Interline Brands, Inc. | | | |

| | 1,698,582 | | | Term Loan, 6.59%, Maturing June 23, 2013 | | | 1,662,487 | | |

| | 1,173,952 | | | Term Loan, 6.59%, Maturing June 23, 2013 | | | 1,149,005 | | |

| National Bedding Co., LLC | | | |

| | 3,772,737 | | | Term Loan, 6.91%, Maturing August 31, 2011 | | | 3,436,334 | | |

| | 290,884 | | | Term Loan, Maturing August 31, 2012(2) | | | 264,704 | | |

| Oreck Corp. | | | |

| | 492,386 | | | Term Loan, 7.66%, Maturing February 2, 2012(4) | | | 285,584 | | |

| Sealy Mattress Co. | | | |

| | 1,975,000 | | | Term Loan, 6.34%, Maturing August 25, 2011 | | | 1,935,500 | | |

| | 300,000 | | | Term Loan, 6.36%, Maturing August 25, 2012 | | | 295,500 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Home Furnishings (continued) | | | |

| Simmons Co. | | | |

| $ | 1,000,000 | | | Term Loan, Maturing December 19, 2011(2) | | $ | 965,000 | | |

| | 1,808,978 | | | Term Loan, 7.11%, Maturing December 19, 2011 | | | 1,717,574 | | |

| | | | | | | $ | 11,996,016 | | |

| Industrial Equipment — 2.1% | | | |

| Aearo Technologies, Inc. | | | |

| $ | 945,250 | | | Term Loan, 7.08%, Maturing July 2, 2014 | | $ | 939,342 | | |

| Alliance Laundry Holdings, LLC | | | |

| | 464,894 | | | Term Loan, 7.63%, Maturing January 27, 2012 | | | 460,245 | | |

| Brand Energy and Infrastructure Services, Inc. | | | |

| | 548,625 | | | Term Loan, 8.13%, Maturing February 7, 2014 | | | 539,024 | | |

| Bucyrus International, Inc. | | | |

| | 498,750 | | | Term Loan, 6.49%, Maturing May 4, 2014 | | | 491,269 | | |

| CEVA Group PLC U.S. | | | |

| | 246,299 | | | Term Loan, 7.83%, Maturing January 4, 2014 | | | 240,141 | | |

| | 747,742 | | | Term Loan, 8.09%, Maturing January 4, 2014 | | | 729,049 | | |

| Colfax Corp. | | | |

| | 1,470,283 | | | Term Loan, 7.13%, Maturing May 30, 2009 | | | 1,450,986 | | |

| EPD Holdings (Goodyear Engineering Products) | | | |

| | 131,250 | | | Term Loan, 7.35%, Maturing July 13, 2014 | | | 126,492 | | |

| | 916,453 | | | Term loan, 7.46%, Maturing July 13, 2014 | | | 883,232 | | |

| Flowserve Corp. | | | |

| | 231,408 | | | Term Loan, 6.40%, Maturing August 10, 2012 | | | 225,719 | | |

| Generac Acquisition Corp. | | | |

| | 1,292,000 | | | Term Loan, 7.73%, Maturing November 7, 2013 | | | 1,168,799 | | |

| Gleason Corp. | | | |

| | 336,936 | | | Term Loan, 6.85%, Maturing June 30, 2013 | | | 321,352 | | |

| | 174,893 | | | Term Loan, 6.85%, Maturing June 30, 2013 | | | 166,805 | | |

| Itron, Inc. | | | |

| | 443,823 | | | Term Loan, 6.84%, Maturing April 18, 2014 | | | 434,809 | | |

| Jason, Inc. | | | |

| | 298,500 | | | Term Loan, 7.53%, Maturing April 30, 2010 | | | 283,575 | | |

| John Maneely Co. | | | |

| | 1,490,283 | | | Term Loan, 8.43%, Maturing December 8, 2013 | | | 1,335,134 | | |

| Kinetek Acquisition Corp. | | | |

| | 472,500 | | | Term Loan, 7.33%, Maturing November 10, 2013 | | | 463,050 | | |

| | 47,250 | | | Term Loan, 7.35%, Maturing November 10, 2013 | | | 46,305 | | |

| Loan Acquisitions Corp. | | | |

| | 362,045 | | | Term Loan, 7.35%, Maturing July 11, 2014 | | | 356,615 | | |

| | 135,682 | | | Term Loan, 7.41%, Maturing July 11, 2014 | | | 133,647 | | |

| Polypore, Inc. | | | |

| | 2,163,909 | | | Term Loan, 7.10%, Maturing July 3, 2014 | | | 2,098,992 | | |

| Sequa Corp. | | | |

| | 500,000 | | | Term Loan, 8.08%, Maturing November 30, 2014 | | | 491,875 | | |

See notes to financial statements

13

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Industrial Equipment (continued) | | | |

| Terex Corp. | | | |

| $ | 492,500 | | | Term Loan, 6.58%, Maturing July 13, 2013 | | $ | 491,269 | | |

| TFS Acquisition Corp. | | | |

| | 1,209,688 | | | Term Loan, 8.33%, Maturing August 11, 2013 | | | 1,185,494 | | |

| | | | | | | $ | 15,063,220 | | |

| Insurance — 1.7% | | | |

| Alliant Holdings I, Inc. | | | |

| $ | 698,250 | | | Term Loan, 7.83%, Maturing August 21, 2014 | | $ | 670,320 | | |

| Amwins Group, Inc. | | | |

| | 497,500 | | | Term Loan, 7.81%, Maturing June 8, 2013 | | | 422,875 | | |

| Applied Systems, Inc. | | | |

| | 997,475 | | | Term Loan, 7.42%, Maturing September 26, 2013 | | | 967,551 | | |

| CCC Information Services Group, Inc. | | | |

| | 785,685 | | | Term Loan, 7.36%, Maturing February 10, 2013 | | | 775,864 | | |

| Conseco, Inc. | | | |

| | 4,457,490 | | | Term Loan, 6.85%, Maturing October 10, 2013 | | | 4,106,463 | | |

| Crawford & Company | | | |

| | 880,357 | | | Term Loan, 7.58%, Maturing October 31, 2013 | | | 853,946 | | |

| Crump Group, Inc. | | | |

| | 725,518 | | | Term Loan, 7.83%, Maturing August 4, 2014 | | | 714,635 | | |

| Hub International Holdings, Inc. | | | |

| | 287,448 | | | Term Loan, 6.07%, Maturing June 13, 2014(3) | | | 272,716 | | |

| | 1,280,331 | | | Term Loan, 7.33%, Maturing June 13, 2014 | | | 1,214,714 | | |

| U.S.I. Holdings Corp. | | | |

| | 1,792,247 | | | Term Loan, 7.58%, Maturing May 4, 2014 | | | 1,709,355 | | |

| | | | | | | $ | 11,708,439 | | |

| Leisure Goods / Activities / Movies — 4.7% | | | |

| AMC Entertainment, Inc. | | | |

| $ | 2,664,558 | | | Term Loan, 6.62%, Maturing January 26, 2013 | | $ | 2,556,102 | | |

| AMF Bowling Worldwide, Inc. | | | |

| | 497,500 | | | Term Loan, 7.68%, Maturing June 8, 2013 | | | 470,138 | | |

| Bombardier Recreational Products | | | |

| | 501,266 | | | Term Loan, 7.70%, Maturing June 28, 2013 | | | 483,304 | | |

| Carmike Cinemas, Inc. | | | |

| | 750,000 | | | Term Loan, Maturing May 19, 2012(2) | | | 741,562 | | |

| | 291,058 | | | Term Loan, 8.50%, Maturing May 19, 2012 | | | 277,373 | | |

| | 446,656 | | | Term Loan, 8.65%, Maturing May 19, 2012 | | | 437,165 | | |

| Cedar Fair, L.P. | | | |

| | 3,706,171 | | | Term Loan, 6.85%, Maturing August 30, 2012 | | | 3,517,157 | | |

| Cinemark, Inc. | | | |

| | 1,000,000 | | | Term Loan, Maturing October 5, 2013(2) | | | 950,000 | | |

| | 2,950,946 | | | Term Loan, 6.67%, Maturing October 5, 2013 | | | 2,797,227 | | |

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Leisure Goods / Activities / Movies (continued) | | | |

| Dave & Buster's, Inc. | | | |

| $ | 73,125 | | | Term Loan, 7.10%, Maturing March 8, 2013 | | $ | 71,663 | | |

| | 122,813 | | | Term Loan, 7.10%, Maturing March 8, 2013 | | | 120,356 | | |

| Deluxe Entertainment Services | | | |

| | 59,055 | | | Term Loan, 7.08%, Maturing January 28, 2011 | | | 54,035 | | |

| | 1,232,528 | | | Term Loan, 7.08%, Maturing January 28, 2011 | | | 1,127,763 | | |

| | 113,929 | | | Term Loan, 7.08%, Maturing January 28, 2011 | | | 104,245 | | |

| DW Funding, LLC | | | |

| | 776,450 | | | Term Loan, 7.10%, Maturing April 30, 2011 | | | 760,921 | | |

| Easton-Bell Sports, Inc. | | | |

| | 1,974,893 | | | Term Loan, 6.85%, Maturing March 16, 2012 | | | 1,893,429 | | |

| Fender Musical Instruments Corp. | | | |

| | 208,333 | | | Term Loan, 6.97%, Maturing June 9, 2014 | | | 192,188 | | |

| | 415,625 | | | Term Loan, 7.16%, Maturing June 9, 2014 | | | 383,414 | | |

| Mega Blocks, Inc. | | | |

| | 1,480,587 | | | Term Loan, 7.25%, Maturing July 26, 2012 | | | 1,354,737 | | |

| Metro-Goldwyn-Mayer Holdings, Inc. | | | |

| | 251,141 | | | Term Loan, Maturing April 8, 2012(2) | | | 233,333 | | |

| | 1,000,000 | | | Term Loan, Maturing April 8, 2012(2) | | | 927,500 | | |

| | 124,859 | | | Term Loan, Maturing April 8, 2012(2) | | | 116,743 | | |

| | 862,062 | | | Term Loan, 8.11%, Maturing April 8, 2012 | | | 801,787 | | |

| National CineMedia, LLC | | | |

| | 2,400,000 | | | Term Loan, 6.87%, Maturing February 13, 2015 | | | 2,260,687 | | |

| Regal Cinemas Corp. | | | |

| | 2,962,500 | | | Term Loan, 6.33%, Maturing November 10, 2010 | | | 2,820,602 | | |

| Revolution Studios Distribution Co., LLC | | | |

| | 679,667 | | | Term Loan, 8.60%, Maturing December 21, 2014 | | | 669,472 | | |

| Six Flags Theme Parks, Inc. | | | |

| | 2,089,500 | | | Term Loan, 7.25%, Maturing April 30, 2015 | | | 1,923,790 | | |

| Universal City Development Partners, Ltd. | | | |

| | 796,080 | | | Term Loan, 6.84%, Maturing June 9, 2011 | | | 780,656 | | |

| WMG Acquisition Corp. | | | |

| | 3,977,496 | | | Term Loan, 7.07%, Maturing February 28, 2011 | | | 3,808,452 | | |

| Zuffa, LLC | | | |

| | 995,000 | | | Term Loan, 6.94%, Maturing June 20, 2016 | | | 850,725 | | |

| | | | | | | $ | 33,486,526 | | |

| Lodging and Casinos — 2.7% | | | |

| Ameristar Casinos, Inc. | | | |

| $ | 736,228 | | | Term Loan, 7.43%, Maturing November 10, 2012 | | $ | 727,025 | | |

| Bally Technologies, Inc. | | | |

| | 1,231,744 | | | Term Loan, 8.39%, Maturing September 5, 2009 | | | 1,230,461 | | |

| CCM Merger, Inc. | | | |

| | 195,002 | | | Term Loan, 6.90%, Maturing April 25, 2012 | | | 187,689 | | |

See notes to financial statements

14

Eaton Vance VT Floating-Rate Income Fund as of December 31, 2007

PORTFOLIO OF INVESTMENTS CONT'D

Principal

Amount | | Borrower/Tranche Description | | Value | |

| Lodging and Casinos (continued) | | | |

| Green Valley Ranch Gaming, LLC | | | |

| $ | 1,255,154 | | | Term Loan, 6.99%, Maturing February 16, 2014 | | $ | 1,189,259 | | |

| Herbst Gaming, Inc. | | | |

| | 70,892 | | | Term Loan, 9.24%, Maturing December 2, 2011 | | | 68,378 | | |

| | 1,712,350 | | | Term Loan, 9.49%, Maturing December 2, 2011 | | | 1,651,614 | | |

| Isle of Capri Casinos, Inc. | | | |

| | 435,547 | | | Term Loan, 0.00%, Maturing November 30, 2013(3) | | | 404,696 | | |

| | 1,396,876 | | | Term Loan, 6.58%, Maturing November 30, 2013 | | | 1,297,931 | | |

| | 558,751 | | | Term Loan, 6.58%, Maturing November 30, 2013 | | | 519,173 | | |

| LodgeNet Entertainment Corp. | | | |

| | 1,492,500 | | | Term Loan, 6.83%, Maturing April 4, 2014 | | | 1,439,330 | | |

| New World Gaming Partners, Ltd. | | | |

| | 750,000 | | | Term Loan, 8.75%, Maturing June 30, 2014 | | | 690,000 | | |

| | 150,000 | | | Term Loan, 8.75%, Maturing June 30, 2014 | | | 138,000 | | |

| Penn National Gaming, Inc. | | | |