January 13, 2021

VIA EDGAR

==========

Samantha Brutlag

Division of Investment Management

Securities and Exchange Commission

Filing Desk

100 F Street, N.E.

Washington, DC 20549

| RE: | Hillman Capital Management Investment Trust; File No. 811-10085 |

Dear Ms. Brutlag,

On December 23, 2020, Hillman Capital Management Investment Trust (the “Trust” or the “Registrant”) filed a proxy statement on Schedule 14A (the “Proxy Statement”) with respect to the Hillman Value Fund (the “Fund”). On January 4, 2021, you provided oral comments to the Proxy Statement. Please find below a summary of those comments and the Registrant's responses, which the Registrant has authorized us to make on behalf of the Registrant.

Comment 1. Please supplementally explain the legal reasoning, including any no action letters on which you may have relied, for filing a proxy statement on Schedule 14A and not filing an N-14 with respect to the reorganization of the Fund into a new series (the “New Fund”) of the ALPs Series Trust (“AST) (the “Reorganization”).

Response. The use of Schedule 14A in lieu of Form N-14 in these circumstances is consistent with the announced positions of the Division of Investment Management (the “Staff”) regarding the scope of Rule 145(a)(2) and accepted market practice.

Rule 145 under the Securities Act of 1933, as amended (the “Securities Act”) generally requires the use of Form N-14 to register securities issued in connection with certain reclassifications, mergers, consolidations and transfers of assets. However, the preliminary note to Rule 145 explains that these transactions are subject to the registration requirements of the Securities Act only when a plan or agreement is submitted to shareholders under which they must “elect, on the basis of what is in substance a new investment decision, whether to accept a new or different security in exchange for their existing security”. Rule 145(a)(2), as interpreted by the Staff, provides an exception to the registration requirements of Rule 145 for certain mergers involving investment companies.

Many investment company reorganizations are structural in nature and do not fundamentally require investors to make a “new investment decision” (the “no-sale theory”). Such reorganizations can, and have been, implemented through the use of a Schedule 14A proxy statement and not through the registration of new securities via Form N-14 in reliance on Rule 145(a)(2). The Staff has recognized the applicability of the no-sale theory to certain investment company combinations and has issued a series of no-actions letters providing its view of the applicability of Rule 145(a)(2) in various circumstances similar to the proposed Reorganization. For example, the Staff has granted no-action relief in circumstances not involving a change in domicile where the investment adviser to the Fund is unchanged and the Fund’s principal investment objectives and policies do not materially change (see, Scudder Common Stock Fund, Inc. (pub. avail. Oct. 10, 1984); Putnam Convertible Fund, Inc. (pub. avail. April 28, 1982)). The Staff has also granted no-action relief in similar circumstances that also involved a change in the board and in non-advisory service providers (see, PEMCO (pub. avail. May 31, 1988); Advance Investors Corporation (pub. avail. Sept. 29, 1976)). Additionally, the Staff has taken the position that when changes in a fund's legal form do not materially change an investor's interests, no investor protection purpose would be served by requiring registration on Form N-14. (see Rydex Advisor Variable Annuity Account (pub. avail. September 28, 1998).

Further, as described more fully in the Proxy Statement, the investment objectives, principal investment strategies, risks and investment limitations of the Fund and the New Fund are identical. In the Registrant’s view, the Reorganization does not involve a new investment decision and can be implemented, consistent with Rule 145(a)(2), through the use of Schedule 14A. The Trust believes that this is consistent with the announced positions of the Staff.

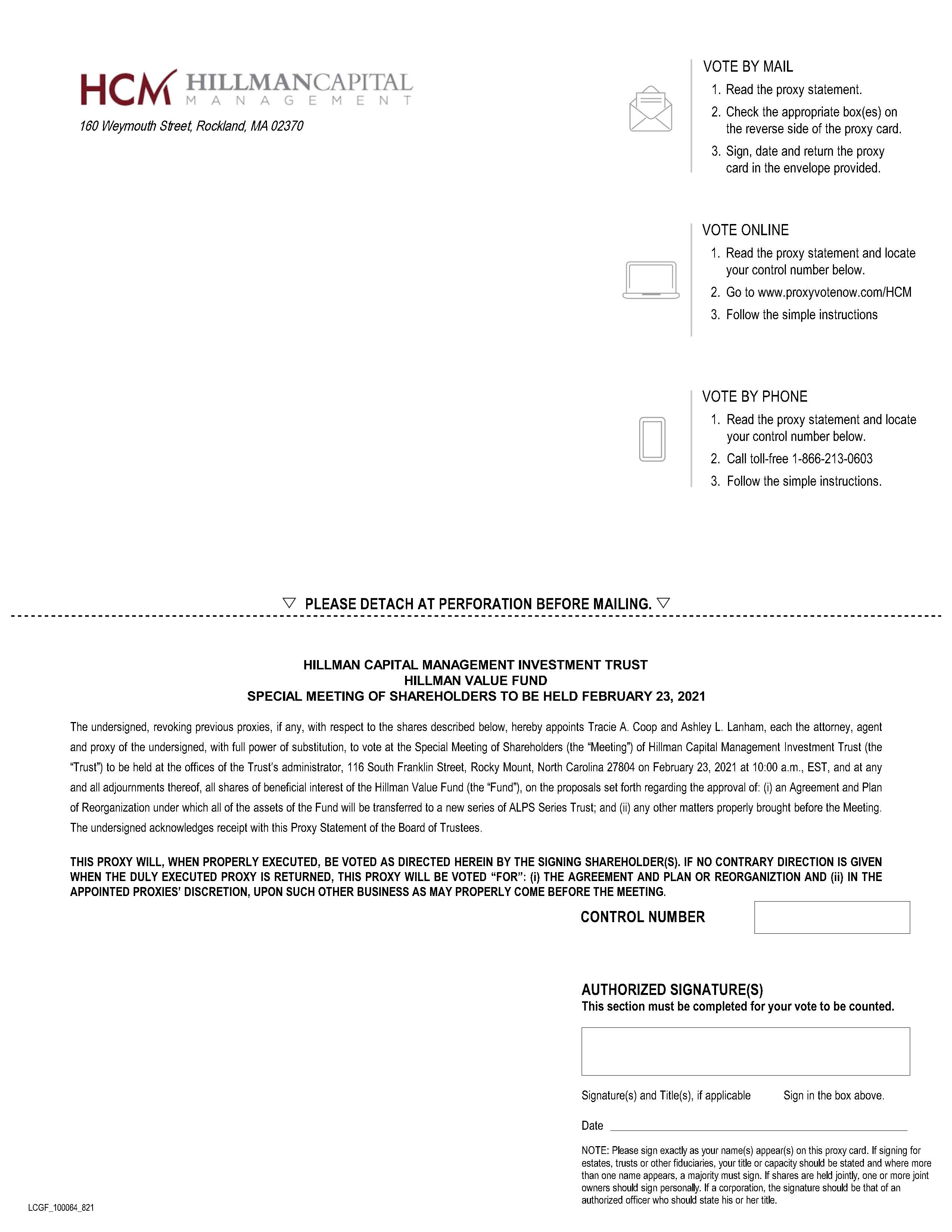

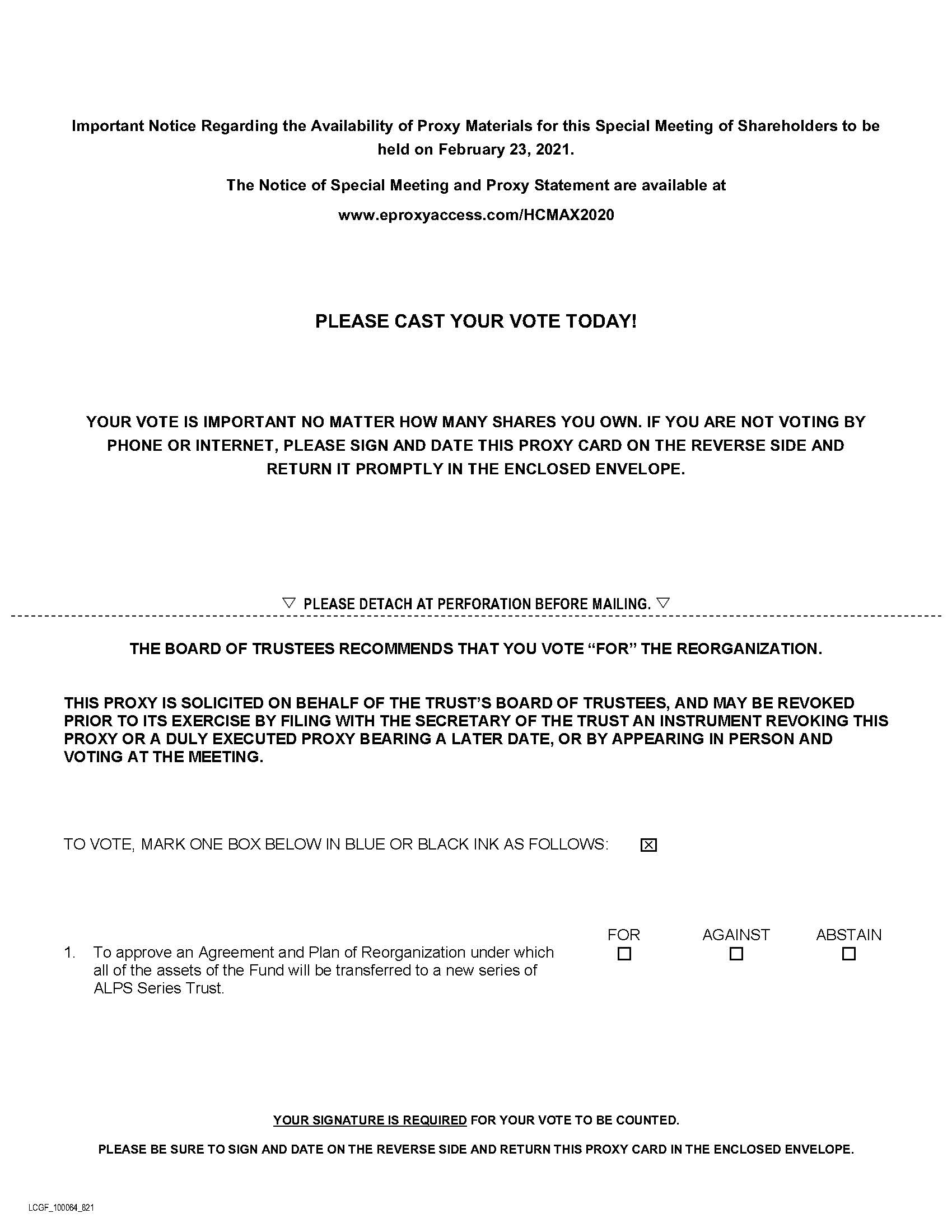

Comment 2. Please confirm that the proxy card will include boxes for shareholders to check to vote for, against, or abstain from voting on the Reorganization.

Response. The Registrant so confirms. The proxy card was cut off in the filing, so it has been attached hereto as an exhibit for your reference.

Comment 3. Please confirm that the New Fund will adopt the performance and financials of the Fund, and please provide the effective date of the registration statement for the New Fund.

Response. AST has confirmed to the Registrant that the New Fund will adopt the performance and financials of the Fund and that the effective date of the registration statement for the New Fund is expected to be February 3, 2021, which is before the shareholder meeting date.

Comment 4. Please confirm that the fundamental policies of the New Fund will be identical to those of the Fund.

Response. AST has confirmed to the Registrant that the fundamental policies of the New Fund will be identical to those of the Fund.

Comment 5. In the letter to shareholders, in the section “How Will Approval of the Reorganization Affect the Operation of the Existing Fund?”, please clarify whether the New Fund will have the same or lower gross expenses as the Fund in addition to the same or lower net expenses.

Response. AST has confirmed to the Registrant that it is anticipated that the New Fund will also have the same or lower gross expenses as the Fund at the time of the Reorganization, and the disclosure has been updated in the letter to shareholders accordingly.

Comment 6. Please provide the completed fee and expense table before effectiveness of the definitive proxy statement.

Response. The Registrant has provided the completed fee and expense table below:

Shareholder Fees

| Existing Fund

| New Fund

|

(fees paid directly from your investment)

| (Current)

| (Pro Forma)

|

Maximum Sales Charge (Load) Imposed on Purchases (as a percentage of offering price)

| None

| None

|

Maximum Deferred Sales Charge (Load) (as a % of the original purchase price)

| None

| None

|

Redemption Fee (as a % of amount redeemed)

| None

| None

|

| 0.85%

| 0.85%

|

Distribution and/or Service (12b-1) Fees

| None

| None

|

Other Expenses

| 0.46%

| 0.30%

|

Total Annual Fund Operating Expenses

| 1.31%

| 1.15%

|

| (0.36)%

| (0.20)%

|

Total Annual Fund Operating Expenses After Waiver1

| 0.95%

| 0.95%

|

(1) Restated to reflect current contractual management fee.

(2) HCM has entered into an expense limitation agreement with the Trust (the “Expense Limitation Agreement”) pursuant to which HCM has agreed to waive or reduce its management fees and to assume other expenses of the Fund, if necessary, in an amount that limits the Fund’s Total Annual Operating Expenses (exclusive of (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions; (iii) acquired fund fees and expenses; (iv) fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example option and swap fees and expenses); (v) borrowing costs (such as interest and dividend expense on securities sold short); (vi) taxes; and (vii) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees and contractual indemnification of Fund service providers (other than HCM)) to not more than 0.95% of the average daily net assets of the Fund. The contractual arrangement runs through January 31, 2022 for the Existing Fund and, for the New Fund, the later of February 3, 2022 or one year from the date on which the Reorganization is completed.

Comment 7. In the fee and expense table, there is a footnote regarding the expenses being restated for the Fund. Please confirm whether it also applies to the New Fund.

Response. The footnote also applies to the New Fund as reflected in the fee table provided in response to Comment 6 above.

Comment 8. Please confirm whether the NAV of the New Fund is expected to differ from that of the Fund due to any differences in the valuation policies of the New Fund compared to the Fund.

Response. AST has confirmed to the Registrant that the NAV of the New Fund is not expected to differ from that of the Fund due to any differences in the valuation policies of the New Fund compared to the Fund.

Comment 9. Please confirm that the Fund will be getting a legal opinion regarding the legality of the shares of the New Fund.

Response. The Registrant confirms that, as a condition of the Reorganization, it will receive an opinion of AST’s counsel that the New Fund’s shares are duly authorized and, upon delivery, will be validly issued and purchasers of the shares will not have any obligation to make payments to AST or its creditors solely by reason of the purchaser’s ownership of the shares.

* * *

If you have any questions or comments, please contact the undersigned at 214.665.3685. Thank you in advance for your consideration.

Sincerely,

/s/ Tanya L. Boyle

Tanya L. Boyle