HIP ENERGY CORPORATION

FORM 51-102F1

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the Three Month Period Ended February 28, 2011

April 29, 2011

The following discussion and analysis of our financial condition and results of operations for the quarterly period ended February 28, 2011 should be read in conjunction with our financial statements and related notes included in this interim report. Our financial statements included in this interim report were prepared in accordance with Canadian generally accepted accounting principles.

Information contained herein includes estimates and assumptions which management is required to make concerning future events, and may constitute forward-looking statements under applicable securities laws. Forward-looking statements include plans, expectations, estimates, forecasts and other comments that are not statements of fact. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential”, or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors that may cause our company’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

Although we believe that the expectations reflected in these forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, we do not intend to update any of these forward-looking statements to conform these statements to actual results.

The amounts included in the following discussion are expressed in U.S. dollars.

Historical Review of Business Operations:

On November 17, 2009, we changed our name from Bradner Ventures Ltd. (“Bradner”) to HIP Energy Corporation (“HIP”) and effected a five (5) for one (1) reverse stock-split of our issued and outstanding common stock. The name change and reverse stock-split were effected with the OTC Bulletin Board on November 19, 2009. Our trading symbol was changed from “BNVLF” to “HIPCF”. Also effective October 20, 2009, we effected an increase in our authorized capital to an unlimited number of common shares and an unlimited number of preferred shares. We received approval for the increase in authorized capital, reverse split and name-change at our annual general meeting of shareholders held on July 31, 2009.

On March 30, 2010, pursuant to the License Agreement, HIP Energy (Nevada) Corporation (“HIP Nevada”), a wholly-owned subsidiary of HIP, acquired from HIP Technology Limited (“HIP Tech”), an exclusive worldwide license for use of the HIP Downhole Process Technology. The HIP Downhole Process Technology is described in detail under the heading “Business Overview - HIP Downhole Process Technology”. The consideration for the acquisition of the HIP Downhole Process Technology was the issuance of 30 million common shares of HIP to Group Rich and a royalty payment.

Under the License Agreement, HIP Nevada was granted a worldwide exclusive license to the HIP Downhole Process Technology for the purpose of developing, producing, using, selling or otherwise

- 2 -

commercially exploiting all subject matter encompassed within the scope of the HIP Downhole Process Technology. The consideration for the acquisition of the HIP Downhole Process Technology was the issuance of 30 million common shares of HIP to Group Rich and the grant of an agreed royalty structure on certain non-China ventures by HIP.

The royalty payment varies depending on the project. HIP Tech and HIP, collectively, will split any proceeds from a non-China Joint Venture as follows:

(i) On all Non-China joint venture related projects or operations on which the HIP Downhole Process Technology are being applied, HIP agrees subject to (ii) below, pay to Group Rich and HIP Tech (together the “Licensor”) a royalty fee equal to 25% of the gross revenue received by HIP from oil and gas wells where cumulative gross production per well exceeds more than 20 barrels of oil equivalences per day (Bblsoepd) for each monthly period. In the event cumulative production per well is equal to or less than 20 Bblsoepd for each monthly period, then the royalty will be reduced to 20% of the gross revenue received by HIP for all such wells.

| Gross Average Production Per Well Per Day, calculated commencing from the day immediately after Well bore Commercialization | Percentage Payable to Licensor |

| Up to 20 barrels per well per day | 20% Gross Revenue |

| Greater than 20 barrels per well per day | 25% Gross Revenue |

(ii) Immediately upon HIP completing an equity or debt financing of US$1,000,000 or more, the gross royalty set out in (i) will be reduced to a flat 25% of all net revenue derived by HIP from projects on which the HIP Downhole Process Technology is being applied.

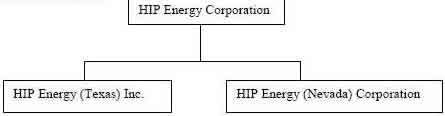

Organizational Structure

Our organizational structure is as follows:

HIP Texas is a wholly owned subsidiary that is governed by the laws of the state of Texas. It was incorporated for the purposes of holding title to the Well Bores.

HIP Nevada is a wholly owned subsidiary that is governed by the laws of the state of Nevada. It was incorporated for the purposes of holding our license to the HIP Downhole Process Technology.

Well Bore Acquisition Agreement:

On March 30, 2010, the Company acquired all rights, title and interest in and to 50 well bores located in West Texas, and 1 well bore (the “Opal Well”) located in Central Texas. In addition, the Company will,

- 3 -

within 12 months, be transferred title to an additional 41 wells and well bores located in East Texas and 60 wells and well bores located in West Louisiana. The Company issued 20,000,000 shares of common stock as consideration for the sale and transfer of the initial 52 well bores in West and Central Texas and the 41 East Texas and 60 Louisiana well bores. $5,000 was assigned as the purchase price of the well bores using carryover basis of accounting (being the amount that the well bores were carried in the accounts of the transferor) as the transferor, together with the transferor in the transaction discussed in Note 5 of the November 30, 2010 financial statements, control the Company subsequent to the transactions. In consideration of the transfer of the Opal Well, the Company agreed to pay consideration totalling $250,000 consisting of accrued development, equipment and lease operating costs incurred on the Opal Well. The Company paid $62,500 and the balance of these costs will be paid on a declining basis from any oil and gas production revenues received by the Company as generated on the Opal Well in excess of 20 bbl oil or gas equivalent per day, using the HIP Downhole Process Technology. The Company has not recorded an accrued liability for the balance of the costs owed given that they are contingent on oil and gas production.

Also as a condition of the Asset Purchase Agreement, the parties agreed to enter into a Non-Competition Agreement dated March 14, 2010 pursuant to which EEL and HIPER agreed, among other things, not to compete against the business of the Company for a period of four years from the date of the agreement. In addition, as the License Agreement grants HIP a worldwide exclusive license to the HIP Downhole Process Technology, EEL and HIPER will not be able to use the HIP Downhole Process Technology on any well or well bores, except as provided under the License Agreement.

HIP Energy –Discussion on its Technology

Traditional oil exploration involves acquiring exploration or drilling rights, conducting seismic and other subsurface studies to estimate if oil and gas is present, and then drilling of the properties in order to attempt to discover and extract the oil and gas. The process can be extremely expensive and time consuming. Costs for drilling a single well have escalated dramatically and can run into the hundreds of thousands of dollars. Further, a significant percentage of all traditional exploration wells drilled each year end-up being dry holes. Our business is to increase the production of proven but unproductive wells, or to increase production from damaged, uneconomical, and stripper well bores using the HIP Downhole Process Technology.

Our initial focus has been to concentrate our operations on applying the HIP Downhole Process Technology to an existing and historically producing but abandoned well bore, being the Opal Ward #1 well. With the beta testing of this single well having resulted in increased downhole pressures and production of oil and gas, although in uneconomic quantities, our goal is now to apply the HIP Downhole technology to a series of interconnected proven well bores and reservoirs that have become noncommercial, uneconomic, depleted or damaged. We intend to continue to demonstrate the value of the HIP Downhole Process Technology by improving the recovery of oil from well bores, after which we intend to acquire additional well bores that we believe, could have an increase in production if the HIP Downhole Process Technology was applied to the well bores. During the initial beta testing phase of the HIP Downhole technology that we can concentrate our efforts on the testing of company owned or acquired well bores. If successful we will then pursue both the development of company owned or controlled prospects and the licensing of the the HIP Downhole Process Technology to third parties. The licensing process may be applied to achieve more rapid development of the HIP Downhole Technology once we have achieved a sustainable, scalable and economic operating process. We believe the Company will benefit from increased industry recognition of the HIP Downhole Process Technology, while generating an ongoing and sustained cash flow from the increased recovery of hydrocarbons.

- 4 -

According to data provided to us by HIP Tech under the License Agreement, the HIP Downhole Process Technology has dissipated the barrier of 23 impediments that restricted or shut in the reservoirs located in the West Texas field, where the Texas Well Bores are located. According to data provided to us by HIP Tech, the HIP Process was applied on several of the Well Bores during the period from 1998 through 2004. These Well Bores experienced an increase in production after the HIP Downhole Process Technology was applied.

Current Period Operations

During the past year, the Company’s focus has been to undertake ongoing testing of its HIP Downhole Process Technology (the “HIP Technology”) on the Opal Ward #1 Well (the “Opal Well”), which is located in central Texas. The Company has been making the necessary design changes and modifications to the HIP Control Unit located on the Opal Well. These design modifications were successful in stimulating the well bore and during such testing periods resulted in the production of oil and gas from the Opal Well, which had been a dead or dormant wellbore. Having been encouraged by the testing results using the HIP Technology on the Opal Well, management proceeded to assemble a larger scale “test” project around various wellbores which it holds and has acquired in East Texas.

The Company has assembled a larger control area in which to test the scalability of the HIP Technology, which is comprised of oil and gas leases on approximately 6400 acres covering rights from the surface to the base of the Travis Peak formation. Within this larger control area, the Company also assembled 10 historically producing but dormant wellbores on which to test the HIP Technology. Of these wellbores, three were acquired previously from HIP Energy Resource Limited, and seven were purchased for $60,000 from Peak Energy Corp. of Dallas, Texas. The Company has completed construction of its 3 acre central facilities site on which the equipment necessary to test the HIP Technology (the “HIP Control Unit”) is being assembled. Pipeline connections of the HIP Control Unit to the 10 test wells are ongoing. To date, 8 of the 10 test wells have been piped to the HIP Control Unit, but the Company is waiting for the agreement of the Texas Parks and Wildlife Department before the well bore modifications and final hook-up of the wells can be completed. All of the wellheads required for each wellbore are also onsite and awaiting final modifications required for the HIP Down Hole Process. Phase 1 of the Company’s program will be to complete and to test at least five of the 10 wells within the next 12 months.

The Company estimates that it will require approximately $500,000 to complete construction and assembly of the HIP Technology control unit and to connect and finish modifications to the five phase 1 wells. Once completed, the Company expects that the cost of adding each of the remaining 5 wells will be approximately $40,000 per well.

Results of Operations

Three Month Period Ended February 28, 2011 Compared to the Three Month Period February 28, 2010

Our Company did not generate any revenues during the three months ended February 28, 2011. Expenses were $97,137 for the three months ended February 28, 2011, compared to $8,832 for the three months ended February 28, 2010. Expenses incurred in the three month period ended February 28, 2011 were primarily those required to maintain our continuous disclosure requirements as a public company while we seek to identify a suitable business opportunity or business combination.

Net loss was $97,137 or $(0.00) per share for the three months ended February 28, 2011, compared to a net loss of $8,832 or $(0.00) per share in the three months ended February 28, 2010. The increase in the net loss during our first quarter 2011 as compared to our first quarter 2010 was due to a general increase in operating expenses.

- 5 -

Selected Quarterly and Year-to-Date Financial Information

The following table provides selected quarterly financial information for the three months ended February 28, 2011 and February 28, 2010:

| | | Three Months Ended | | | Three Months Ended | |

| | | February 28, 2011 | | | February 28, 2010 | |

| | | | | | | |

| Revenue | $ | Nil | | $ | Nil | |

| | | | | | | |

| Net loss | | (97,137 | ) | | (8,832 | ) |

| | | | | | | |

| Net loss per share (basic and fully diluted) | | (0.00 | ) | | (0.00 | ) |

| | | As at February 28, 2011 | | | As at November 30, 2010 | |

| | | | | | | |

| Total assets | $ | 403,206 | | $ | 417,654 | |

| | | | | | | |

| Shareholders’ equity | | 186,277 | | | 283,414 | |

Summary of Quarterly Results

Quarterly Results of the Eight Quarters ended February 28, 2011

| | | 2011 | | | 2010 | |

| | | | | | | | | | | | | |

| | | February 28 | | | November 30 | | | August 31 | | | May 31 | |

| | | (unaudited) | | | (audited) | | | (unaudited) | | | (unaudited) | |

| | | | | | | | | | | | | |

| Revenues | $ | Nil | | $ | Nil | | $ | Nil | | $ | Nil | |

| | | | | | | | | | | | | |

| Net loss | | (97,137 | ) | | (192,806 | ) | | (354,099 | ) | | (203,575 | ) |

| | | | | | | | | | | | | |

| Basic and Diluted earnings (loss) per share | | (0.00 | ) | | (0.00 | ) | | (0.01 | ) | | (0.00 | ) |

| | | 2010 | | | 2009 | |

| | | | | | | | | | | | | |

| | | February 28 | | | November 30 | | | August 31 | | | May 31 | |

| | | (unaudited) | | | (audited) | | | (unaudited) | | | (unaudited) | |

| | | | | | | | | | | | | |

| Revenues | $ | Nil | | $ | Nil | | $ | Nil | | $ | Nil | |

| | | | | | | | | | | | | |

| Net loss | | (8,832 | ) | | (18,355 | ) | | (9,321 | ) | | (21,231 | ) |

| | | | | | | | | | | | | |

| Basic and Diluted earnings (loss) per share | | (0.00 | ) | | (0.00 | ) | | (0.00 | ) | | (0.00 | ) |

- 6 -

Liquidity

We had cash and other current assets of $31,413 as at February 28, 2011, compared to $43,911 as at November 30, 2010. Our company’s normal operating expenses for the quarter ended February 28, 2011 of $97,137 included bank charges and interest of $697, office and miscellaneous of $1,044, professional fees (accounting, administration and legal) of $14,741, management fees of $72,498, transfer agent and regulatory fees of $751, travel and promotion of $613, shareholder information of $240, amortization of $1,950 and loss on foreign exchange of $4,603.

Our Company has limited financing upon which to continue our operations, and we anticipate that it will require approximately $500,000 to complete construction and assembly of the HIP Technology control unit, and to connect and finish modifications to the five phase 1 wells referred to under “Current Operations” set out above. Once completed, the Company expects that the cost of adding each of the remaining 5 wells will be approximately $40,000 per well. We presently do not have any arrangements in place for the financing of our continued operations.

Operating Activities

Operating activities used cash of $14,539 for the quarter ended February 28, 2011, compared to $28,271 for the quarter ended February 28, 2010.

Investing Activities

We did not conduct any investing activities during the three months ended February 28, 2011 and 2010.

Financing Activities

During the three months period ended February 28, 2010, we received $Nil advances from directors compared to $23,603 received in the same period in 2010.

Capital Resources

Financing

We plan to focus on those areas that will result in the production of oil and gas in the shortest time frame. In pursuing this objective, we plan to raise funds as required with the intent of minimizing dilution and maximizing return on funds deployed. Until such time as the HIP Downhole Process Technology is further developed and results in revenues from production of oil and gas from applied wells, we plan to primarily rely on traditional equity markets and if available, debt instruments to raise our required funding. During the year ended November 30, 2010, we raised $1,129,000 through the sale of common stock. The Company has not undertaken any additional financings since.

Our Company has limited financing upon which to continue our operations, and we anticipate that we will require approximately $500,000 to complete construction and assembly of the HIP Technology control unit and to connect and finish modifications to the five phase 1 wells referred to under “Current Operations” set out above. Once completed, the Company expects that the cost of adding each of the remaining 5 wells will be approximately $40,000 per well. We presently do not have any arrangements in place for the financing of our continued operations.

- 7 -

Use of Funding

All funds received have been allocated to proving out the HIP Technology and for general working capital. If oil and gas production is attained from these low production or problematic wells using the HIP Process, we will then continue to expand our commercialization of the HIP Downhole Process Technology.

We plan on deploying monies in those prospect areas where we have the greatest understanding of the existing well bores and reservoirs. To this end, we plan to focus our initial efforts on using the HIP Process in well bores and basins in such regions as the Woodbine and Austin Chalk region of the U.S. These regions are low-risk and long-term energy producers. We will participate in such regions with landowners or companies that have access to leases located in geological trends that have demonstrated substantial historical production and have potential remaining reserves that can be exploited in a low-risk, systematic fashion.

Our initial project plan and budget was funded from earlier financing of $1.29 million.

Our sole tangible assets consists of the Well Bores and the exclusive worldwide license to the HIP Downhole Process Technology. It is however a requirement of the application of the HIP Downhole Process Technology that certain equipment and other fixed or other tangible assets be acquired or leased in order that any potential commercialization of the HIP Downhole Process Technology on any of the well bores can be realized. The equipment required as part of the HIP Downhole Process Technology in part forms the basis of the application patent relating to the HIP Downhole Process Technology and in other cases is readily available oilfield equipment. The availability of any specific equipment may affect our ability to carry out its operations in a timely and cost effective manner. As stated earlier, our short-term plan is to apply and test the HIP Downhole Process Technology on a number of wells and wellbores acquired from HIPER. The results of these tests and the ongoing development and application of the HIP Downhole Process Technology will directly affect the Companies ability to generate revenue and raise additional capital to further expand its programs and acquire any ongoing plant and equipment. As with any new technology applications there is inherent risk that the technology itself may not prove commercially viable or result in any economic production.

China Joint Venture

We have had preliminary discussion with the applicable parties to form a joint venture (a “China Joint Venture”). Our discussion to-date have focused on the development of an initial pilot program to prove the economic viability of the HIP Downhole Process Technology on an agreed number of “beta” test well bores within a designated oilfield in China. After the economic viability of the HIP Downhole Process Technology has been proven, the HIP Downhole Process Technology applied on a large scale. As of the date of this report, we have not signed any definitive agreements with JOC and they may cease discussions at any time. Further, although we are at an advanced stage of negotiations and agreement as to the financial terms, number of wells and contribution of the respective parties, we have not signed any letters of intent or memorandums of understanding regarding same at this time.

- 8 -

Off-balance Sheet Arrangements

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that are material to investors.

Transactions with Related Parties

The Company entered into the following transactions with related parties, which are measured at the exchange amount, being the amount established and agreed to by the related parties.

| | a) | During the three month period ended February 28, 2011, the Company incurred $72,498 (2010 – $482) for management fees to directors, officers and private companies controlled by them. |

| | | |

| | b) | During the three month period ended February 28, 2011, the Company incurred $3,000 (2010 – $Nil) in consulting fees to an officer. |

| | | |

| | c) | As at February 28, 2011, the Company owes $51,115 (CDN$50,000) (November 30, 2010 – $49,010 (CDN$50,000)) to a director for advances, which are unsecured, non-interest bearing and payable on demand. |

| | | |

| | d) | As at February 28, 2011, the Company owes $101,605 (November 30, 2010 – $25,762) to directors for accrued management fees, which are unsecured, non-interest bearing and payable on demand. |

| | | |

| | e) | As at February 28, 2011, the Company owes $15,335 (CDN$15,000) (November 30, 2010 – $14,704 (CDN$15,000)) to a private company owned by a shareholder for advances, which are unsecured, non-interest bearing and payable. |

Application of Critical Accounting Policies

The preparation of financial statements in conformity with Canadian generally accepted accounting principles requires our management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Significant areas requiring the use of management estimates relate to the impairment of mineral property interests and the determination of reclamation obligations. Actual results could differ from those estimates. By their nature, such estimates are subject to measurement uncertainty and the effect on the financial statements of changes in such estimates in future periods could be significant. The financial statements have, in management’s opinion, been properly prepared within the framework of the significant accounting policies summarized below.

Change in Functional Currency

On March 30, 2010, the Company completed the acquisition of certain Well Bores and a Technology License, both of which are located in the United States. Subsequent to the acquisitions, the Company’s operations, fundraising activities, and any future revenues will be denominated in United States (“US”) dollars. As a result of this change in circumstances, the Company undertook a review of the functional currency exposures of all of its business units according to CICA Section 1651 Foreign Currency Translation and concluded that the currency exposures of its Canadian and foreign operations are now predominately in US dollars. Prior to March 30, 2010, the Company’s functional currency was the Canadian dollar and the reporting currency was the Canadian dollar. Effective March 30, 2010, the Company’s functional and reporting currency is the US dollar. This results in all foreign currency impacts

- 9 -

of holding non-US dollar denominated financial assets and liabilities being recorded through the statement of earnings. The Company accounted for this change prospectively. The translated amounts on March 29, 2010 become the historical basis for all balance sheet items as at March 30, 2009, except for shareholders’ equity at historical cost.

Change in reporting currency

Prior year’s financial statements and all comparative financial information contained herein have been recast to reflect the Company’s results as if they had been historically reported in U.S. dollars. All revenues, expenses and cash flows for each period were translated into the reporting currency using average rates for the period, or the rates in effect at the date of the transaction for significant transactions. Assets and liabilities were translated using the exchange rate at the applicable balance sheet dates and stockholders’ equity was translated at historical rates. The resulting translation adjustment was recorded as accumulated foreign currency translation adjustment in accumulated other comprehensive income.

Recent Accounting Pronouncements

In 2006, the AcSB published a new strategic plan that will significantly affect financial reporting requirements for Canadian companies. The AcSB strategic plan outlines the convergence of Canadian GAAP with IFRS over an expected five year transitional period. In February 2008, the AcSB announced that 2011 is the changeover date for publicly-listed companies to use IFRS, replacing Canada’s own GAAP. The date is for interim and annual financial statements relating to fiscal years beginning on or after January 1, 2011. The transition date of January 1, 2011 will require the restatement for comparative purposes of amounts reported by the Company for the year ended November 30, 2011. While the Company has begun assessing the adoption of IFRS for 2011, the financial reporting impact of the transition to IFRS cannot be reasonably estimated at this time. The Company is currently assessing the impact of the above new accounting standards on the Company’s financial positions and results of operations.

The CICA handbook Section 1601, “Consolidated Financial Statements”, and Section 1602, “Non-controlling Interests”, replaces Section 1600. Section 1601 establishes standards for the preparation of consolidated financial statements. Section 1602 establishes standards for accounting, for a non-controlling interest in a subsidiary in consolidated financial statements, subsequent to a business combination. Section 1602 is equivalent to the corresponding provisions of International Financial Reporting Standard IAS 27, “Consolidated and Separate Financial Statements”. These standards are effective for the Company for interim and annual financial statements beginning on January 1, 2011. Early adoption is permitted. The Company has not yet determined the impact of the adoption of these changes on its financial statements.

The CICA handbook Section 1582, “Business Combinations”, which replaces Section 1581, “Business Combinations”, establishes standards for the accounting for a business combination. It is the Canadian GAAP equivalent to International Financial Reporting Standard IFRS 3, “Business Combinations”. This standard is effective for interim and annual financial statements beginning on January 1, 2011. Early adoption is permitted. The Company has not yet determined the impact of the adoption of these changes on its financial statements.

International financial reporting standards (‘IFRS”)

In 2006, the AcSB published a new strategic plan that will significantly affect financial reporting requirements for Canadian companies. The AcSB strategic plan outlines the convergence of Canadian GAAP with IFRS over an expected five year transitional period. In February 2008, the AcSB announced

- 10 -

that 2011 is the changeover date for publicly-listed companies to use IFRS, replacing Canada’s own GAAP. The date is for interim and annual financial statements relating to fiscal years beginning on or after January 1, 2011. The transition date of January 1, 2011 will require the restatement for comparative purposes of amounts reported by the Company for the year ended November 30, 2012. While the Company has begun assessing the adoption of IFRS for 2011, the financial reporting impact of the transition to IFRS cannot be reasonably estimated at this time. The Company does not expect the adoption of IFRS to have a material impact on the Company’s financial position and results of operations.

Disclosure Controls and Procedures and Internal Controls and Procedures

In contrast to the certificate required for non-venture issuers under National Instrument 52-109 Certification of Disclosure in Issuer’s Annual and Interim Filings (“NI 52-109”), the Company utilizes the Venture Issuer Basic Certificate which does not include representations relating to the establishment and maintenance of disclosure controls and procedures (“DC&P”) and internal control over financial reporting (“ICFR”), as defined in National Instrument NI 52-109. In particular, the Company’s certifying officers are not making any representations relating to the establishment and maintenance of:

(a) controls and other procedures designed to provide reasonable assurance that information required to be disclosed by the issuer in its annual filings, interim filings or other reports filed or submitted under securities legislation is recorded, processed, summarized and reported within the time periods specified in securities legislation; and

(b) a process to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with the issuer’s GAAP.

The Company’s certifying officers are responsible for ensuring that processes are in place to provide them with sufficient knowledge to support the representations they are making in their certifications. Investors should be aware that inherent limitations on the ability of certifying officers of a venture issuer to design and implement on a cost effective basis DC&P and ICFR as defined in NI 52-109 may result in additional risks to the quality, reliability, transparency and timeliness of interim and annual filings and other reports provided under securities legislation.

Financial Instruments – Recognition and Measurement

This standard requires all financial instruments within its scope, including derivatives, to be included on the balance sheet and measured either at fair value or, in certain circumstances when fair value may not be considered most relevant, at cost or amortized cost. Changes in fair value are to be recognized in either the Consolidated Statements of Operations or Comprehensive Loss.

In accordance with this standard, the Company has classified its financial instruments as follows:

The Company classifies and measures its financial instruments as follows:

Cash is classified as “held-for-trading” which is measured at fair value initially and in subsequent periods;

Accounts payable, accrued liabilities, due to related parties and advances payable are classified as other financial liabilities and are measured at fair value at inception. Subsequent valuations are recorded at amortized cost using the effective interest rate method.

Financial Instruments – Disclosures

In June 2009, the CICA amended Section 3862, Financial Instruments - Disclosures, to include additional disclosure requirements about fair value measurement for financial instruments and liquidity risk disclosures. These amendments require a three level hierarchy that reflects the significance of the inputs

- 11 -

used in making the fair value measurements. Fair value of assets and liabilities included in Level 1 are determined by reference to quoted prices in active markets for identical assets and liabilities. Assets and liabilities in Level 2 include valuations using inputs other than quoted prices for which all significant inputs are based on observable market data, either directly or indirectly. Level 3 valuations are based on inputs that are not based on observable market data. The amendments to Section 3862 apply for annualfinancial statements relating to fiscal years ending after September 30, 2009. The adoption of this standard did not have a significant impact on the Company’s consolidated financial statements.

Outstanding Securities

The authorized capital of our company consists of unlimited common and preferred shares without par value. As of February 28, 2011, there were 60,727,660 common shares issued and outstanding and no preference shares issued and outstanding in the capital of our company. The company has no options or warrants outstanding.

Additional Disclosure for Venture Issuers Without Significant Revenue

| | | Three Months | | | Three Months | |

| | | Ended | | | Ended | |

| | | February 28, 2011 | | | February 28, 2010 | |

| | | | | | | |

| General and Administrative Expenses | $ | 97,137 | | $ | 8,832 | |

Additional Information

Additional information relating to our company is available for viewing on the SEDAR website at www.sedar.com.