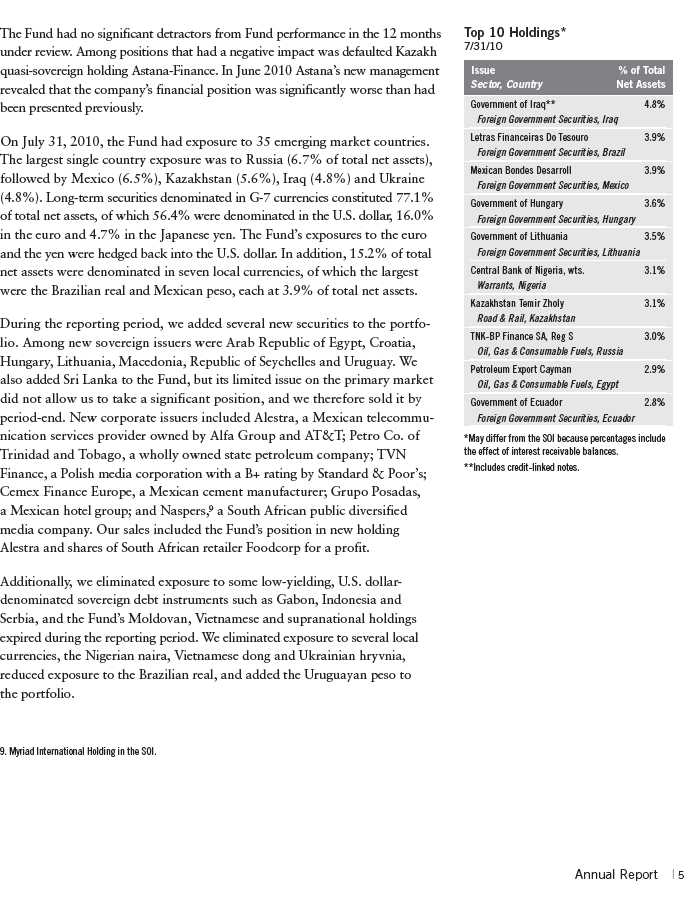

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT

COMPANIES

Investment Company Act file number 811-10157

Franklin Global Trust

(Exact name of registrant as specified in charter)

One Franklin Parkway, San Mateo, CA 94403-1906

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant's telephone number, including area code: 650 312-2000

Date of fiscal year end: 7/31

Date of reporting period: 7/31/10

Item 1. Reports to Stockholders.

FRANKLIN

GLOBAL REAL ESTATE FUND

| | | | | | | |

| | Contents | | | | | |

| Shareholder Letter | 1 | Annual Report | | Financial Highlights and | | Tax Designation | 35 |

| | | Franklin Global | | Statement of Investments | 13 | Board Members and Officers | 36 |

| | | Real Estate Fund | 3 | Financial Statements | 19 | Shareholder Information | 41 |

| | | Performance Summary | 7 | Notes to Financial Statements | 23 | | |

| | | Your Fund’s Expenses | 11 | Report of Independent | | | |

| | | | | Registered Public | | | |

| | | | | Accounting Firm | 34 | | |

Annual Report

Franklin Global Real Estate Fund

| | |

| Top 10 Holdings | | |

| 7/31/10 | | |

| |

| Company | % of Total | |

| Sector/Industry, Country | Net Assets | |

| Simon Property Group Inc. | 5.5 | % |

| Retail REITs, U.S. | | |

| Unibail-Rodamco SE | 4.5 | % |

| Retail REITs, France | | |

| Westfield Group, ord. & 144A | 4.1 | % |

| Retail REITs, Australia | | |

| Boston Properties Inc. | 3.8 | % |

| Office REITs, U.S. | | |

| Equity Residential | 3.5 | % |

| Residential REITs, U.S. | | |

| Host Hotels & Resorts Inc. | 3.3 | % |

| Specialized REITs, U.S. | | |

| Vornado Realty Trust | 3.0 | % |

| Diversified REITs, U.S. | | |

| Ventas Inc. | 2.9 | % |

| Specialized REITs, U.S. | | |

| Public Storage | 2.7 | % |

| Specialized REITs, U.S. | | |

| Stockland, ord. & 144A | 2.5 | % |

| Diversified REITs, Australia | | |

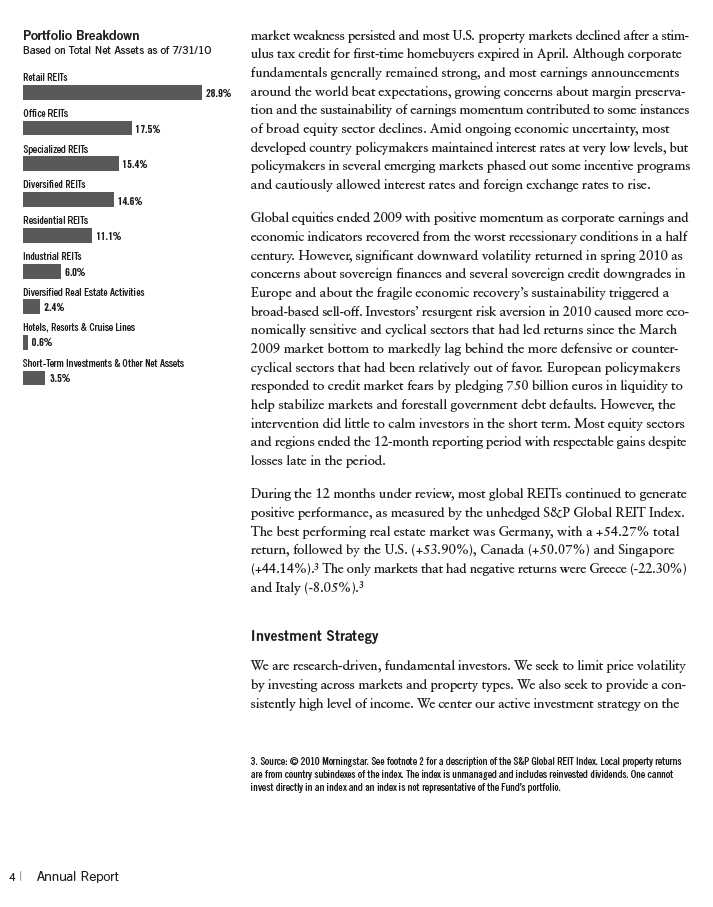

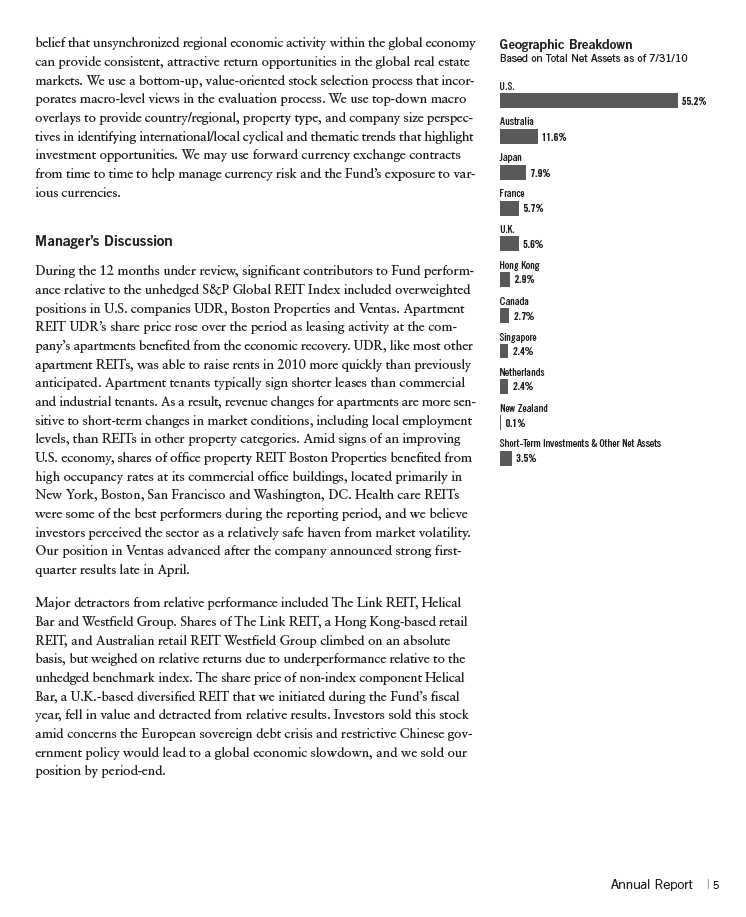

Thank you for your continued participation in Franklin Global Real Estate Fund. We look forward to serving your future investment needs.

Portfolio Management Team

Franklin Global Real Estate Fund

The foregoing information reflects our analysis, opinions and portfolio holdings as of July 31, 2010, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

6 | Annual Report

Performance Summary as of 7/31/10

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

| | | | | | | | |

| Price and Distribution Information | | | | | | |

| Class A (Symbol: FAGRX) | | | | Change | | 7/31/10 | | 7/31/09 |

| Net Asset Value (NAV) | | | +$ | 1.33 | $ | 6.40 | $ | 5.07 |

| Distributions (8/1/09–7/31/10) | | | | | | | | |

| Dividend Income | $ | 0.2370 | | | | | | |

| Class C (Symbol: n/a) | | | | Change | | 7/31/10 | | 7/31/09 |

| Net Asset Value (NAV) | | | +$ | 1.32 | $ | 6.35 | $ | 5.03 |

| Distributions (8/1/09–7/31/10) | | | | | | | | |

| Dividend Income | $ | 0.1992 | | | | | | |

| Advisor Class (Symbol: FVGRX) | | | | Change | | 7/31/10 | | 7/31/09 |

| Net Asset Value (NAV) | | | +$ | 1.34 | $ | 6.42 | $ | 5.08 |

| Distributions (8/1/09–7/31/10) | | | | | | | | |

| Dividend Income | $ | 0.2528 | | | | | | |

Annual Report | 7

Performance Summary (continued)

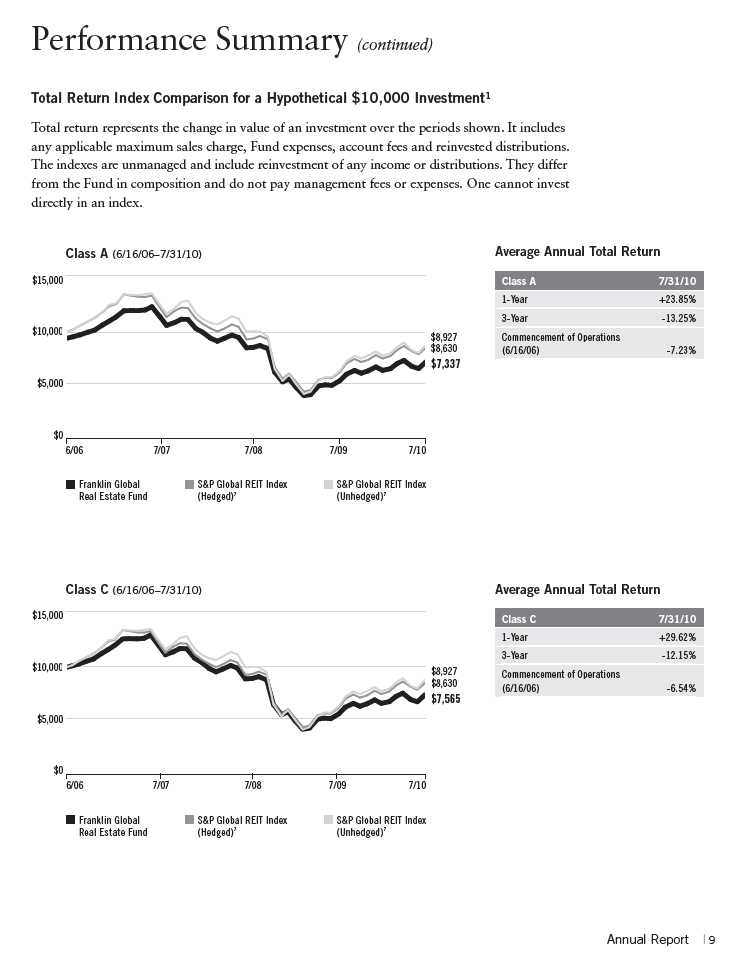

Performance1

Cumulative total return excludes sales charges. Average annual total returns and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class C: 1% contingent deferred sales charge in first year only; Advisor Class: no sales charges.

| | | | | | | | | | | |

| | | | | | | | | | | Commencement | |

| | | | | | | | | | | of Operations | |

| Class A | | | | 1-Year | | | 3-Year | | | (6/16/06 | ) |

| Cumulative Total Return2 | | | + | 31.43 | % | | -30.74 | % | | -22.15 | % |

| Average Annual Total Return3 | | | + | 23.85 | % | | -13.25 | % | | -7.23 | % |

| Value of $10,000 Investment4 | | | $ | 12,385 | | $ | 6,529 | | $ | 7,337 | |

| Avg. Ann. Total Return (6/30/10)5 | | | + | 21.88 | % | | -17.90 | % | | -9.50 | % |

| Total Annual Operating Expenses6 | | | | | | | | | | | |

| Without Waiver | 1.75 | % | | | | | | | | | |

| With Waiver | 1.35 | % | | | | | | | | | |

| | | | | | | | | | | Commencement | |

| | | | | | | | | | | of Operations | |

| Class C | | | | 1-Year | | | 3-Year | | | (6/16/06 | ) |

| Cumulative Total Return2 | | | + | 30.62 | % | | -32.21 | % | | -24.35 | % |

| Average Annual Total Return3 | | | + | 29.62 | % | | -12.15 | % | | -6.54 | % |

| Value of $10,000 Investment4 | | | $ | 12,962 | | $ | 6,779 | | $ | 7,565 | |

| Avg. Ann. Total Return (6/30/10)5 | | | + | 27.56 | % | | -16.87 | % | | -8.79 | % |

| Total Annual Operating Expenses6 | | | | | | | | | | | |

| Without Waiver | 2.44 | % | | | | | | | | | |

| With Waiver | 2.04 | % | | | | | | | | | |

| | | | | | | | | | | Commencement | |

| | | | | | | | | | | of Operations | |

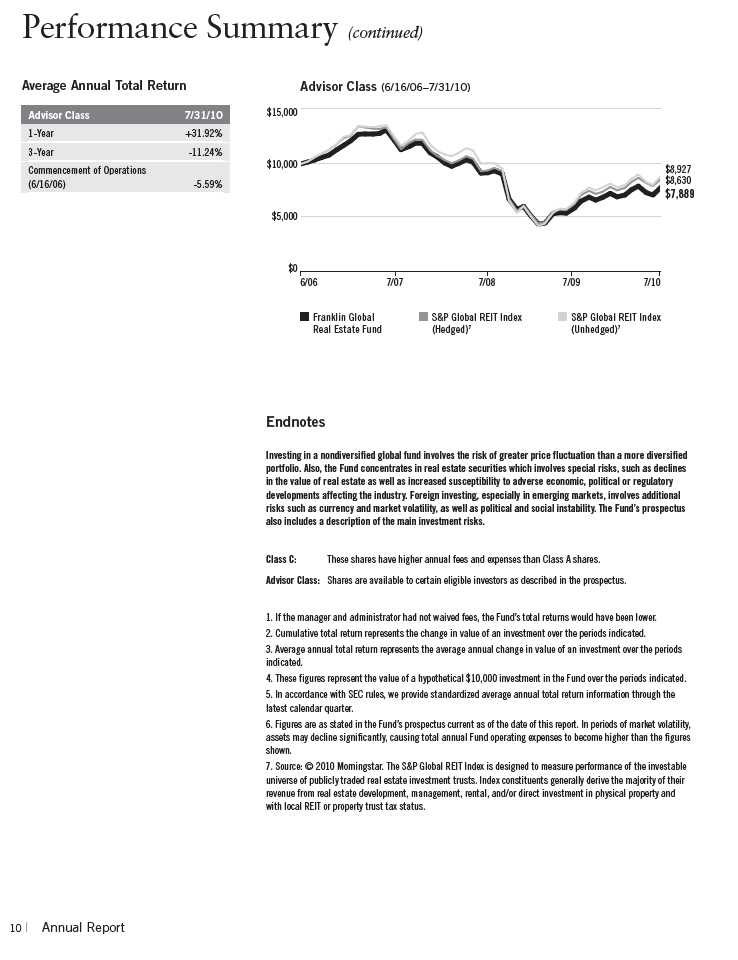

| Advisor Class | | | | 1-Year | | | 3-Year | | | (6/16/06 | ) |

| Cumulative Total Return2 | | | + | 31.92 | % | | -30.08 | % | | -21.11 | % |

| Average Annual Total Return3 | | | + | 31.92 | % | | -11.24 | % | | -5.59 | % |

| Value of $10,000 Investment4 | | | $ | 13,192 | | $ | 6,992 | | $ | 7,889 | |

| Avg. Ann. Total Return (6/30/10)5 | | | + | 29.70 | % | | -16.03 | % | | -7.89 | % |

| Total Annual Operating Expenses6 | | | | | | | | | | | |

| Without Waiver | 1.45 | % | | | | | | | | | |

| With Waiver | 1.05 | % | | | | | | | | | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

The investment manager and administrator have co ntractually agreed to waive or limit their respective fees and to assume as their own expense certain expenses otherwise payable by the Fund so that common expenses (i.e., a combinatio n of invest-ment management fees, fund administration fees, and other expenses, but excluding Rule 12b-1 fees) for each class of the Fund do not exceed 1.05% (other than certain nonroutine expenses or costs, including those relating to litigation, indemnifi-cation, reorganizations and liquidations) until 11/30/10.

8 | Annual Report

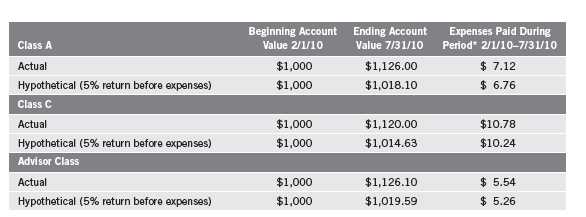

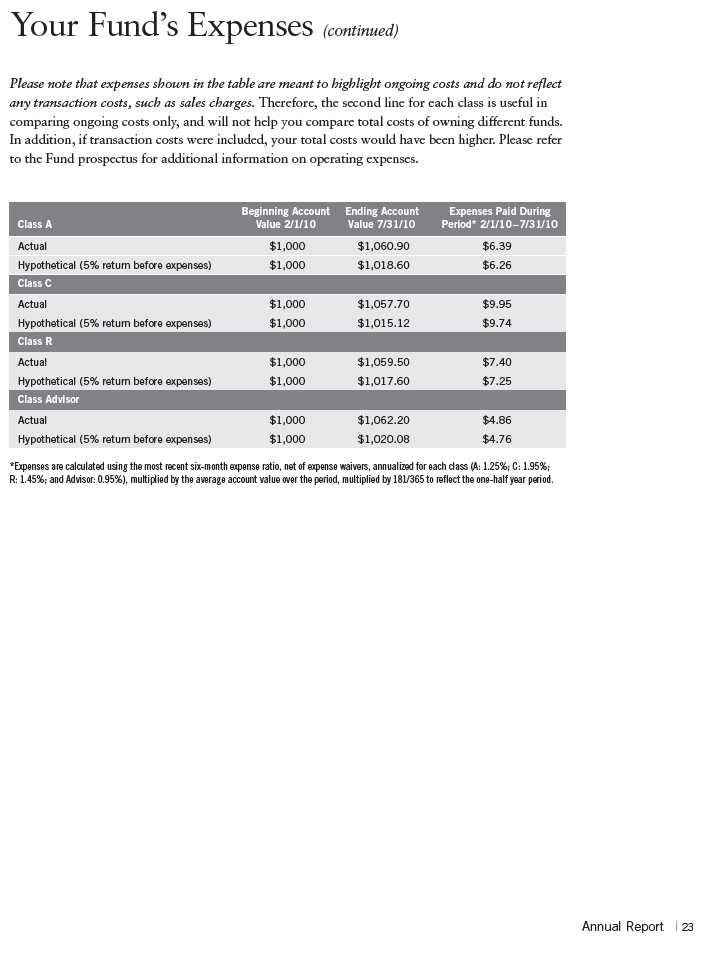

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| | If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| | If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Annual Report | 11

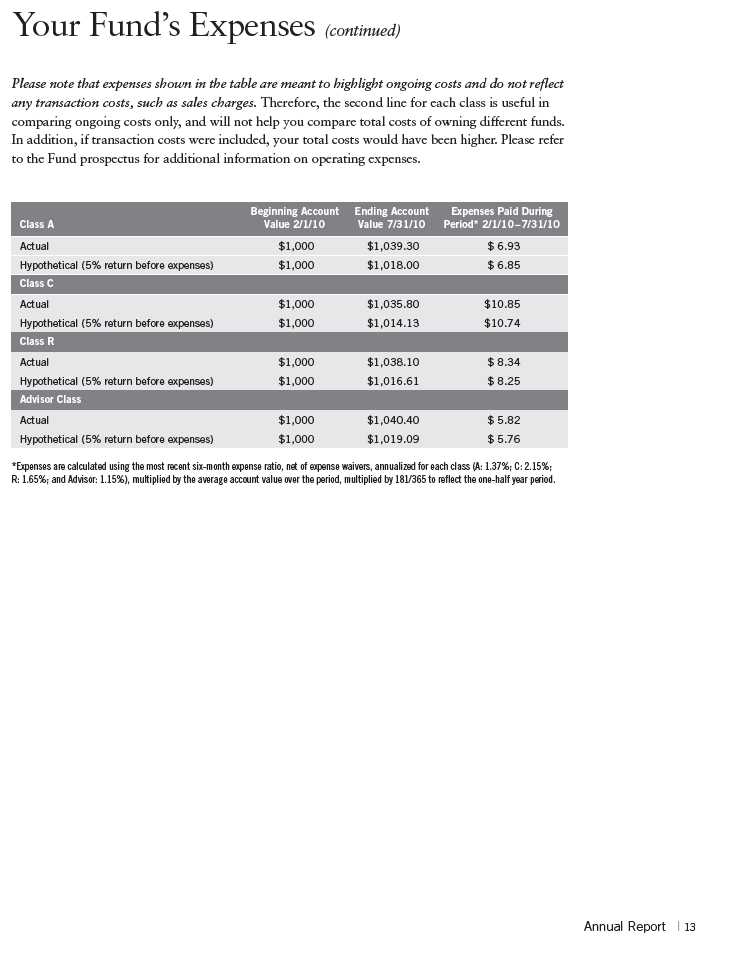

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

*Expenses are calculated using the most recent six-month expense ratio, net of expense waivers, annualized for each class (A: 1.35%; C: 2.05%; and Advisor: 1.05%), multiplied by the average account value over the period, multiplied by 181/365 to reflect the one-half year period.

12 | Annual Report

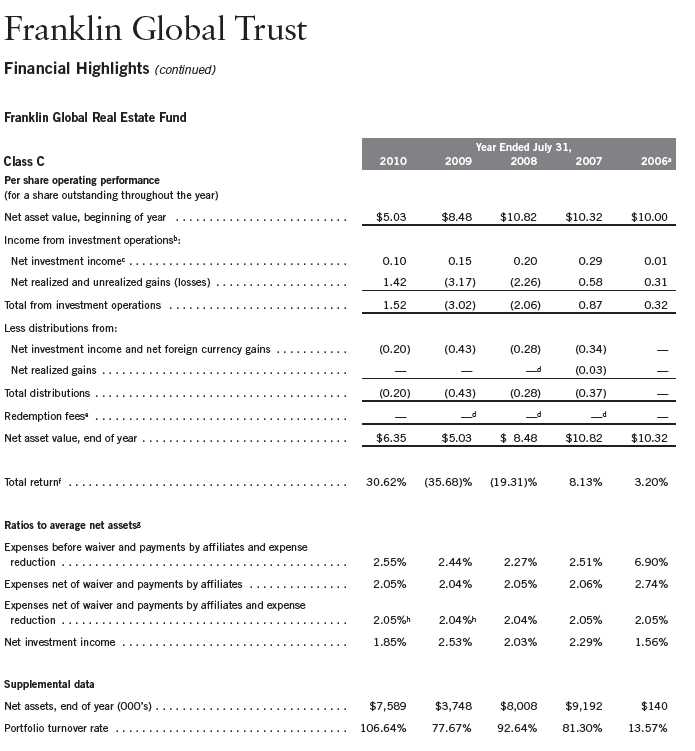

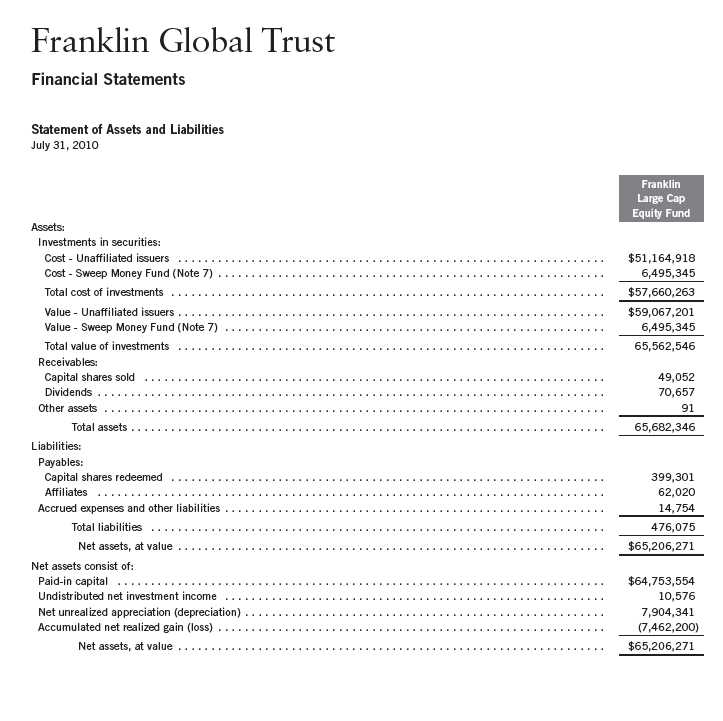

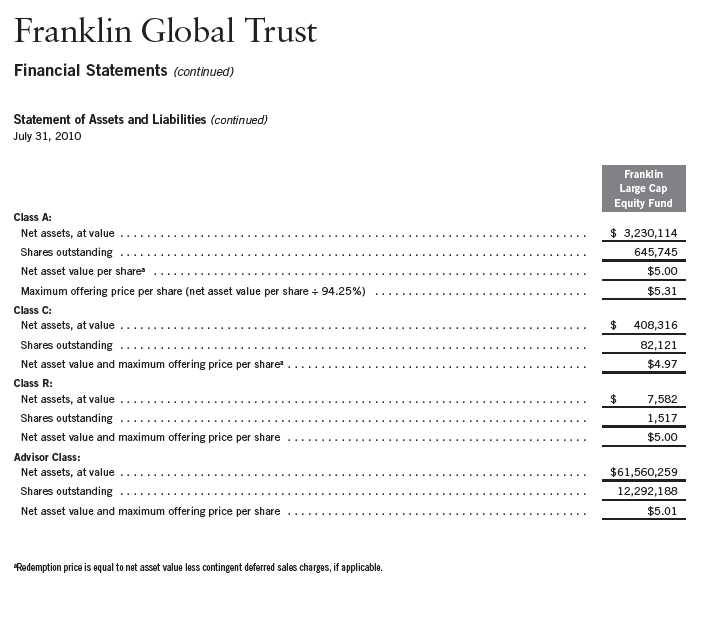

Annual Report | The accompanying notes are an integral part of these financial statements. | 13

Annual Report | The accompanying notes are an integral part of these financial statements. | 15

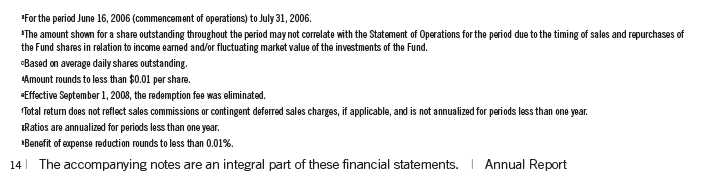

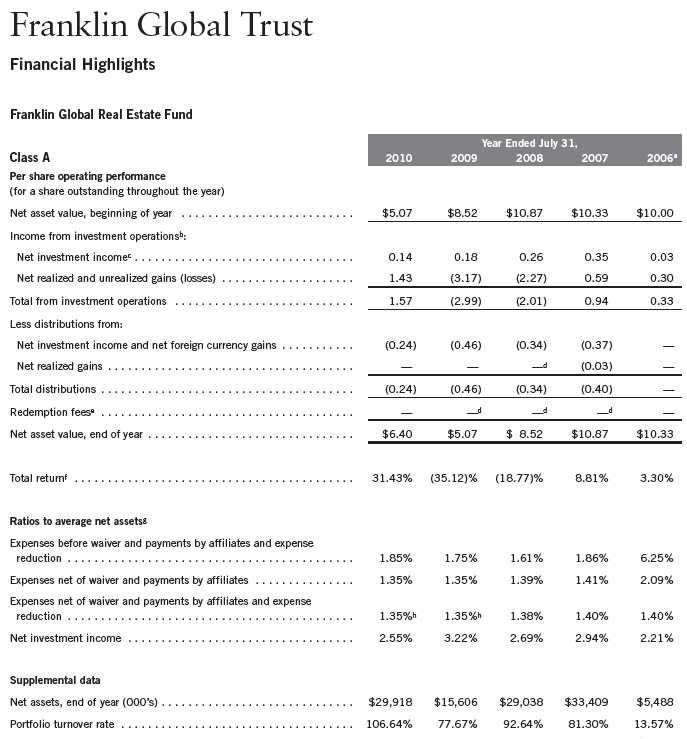

See Abbreviations on page 33.

aNon-income producing.

18 | The accompanying notes are an integral part of these financial statements. | Annual Report

Annual Report | The accompanying notes are an integral part of these financial statements. | 19

20 | The accompanying notes are an integral part of these financial statements. | Annual Report

Annual Report | The accompanying notes are an integral part of these financial statements. | 21

22 | The accompanying notes are an integral part of these financial statements. | Annual Report

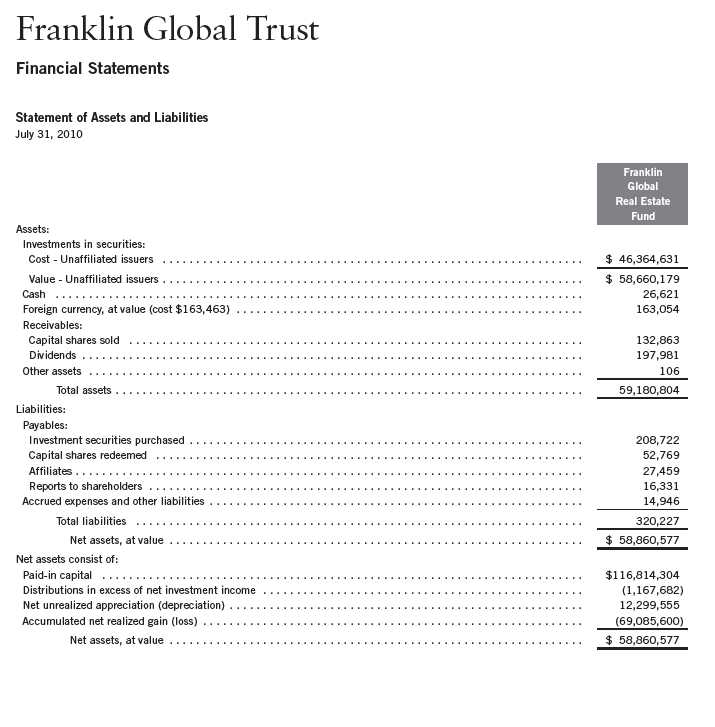

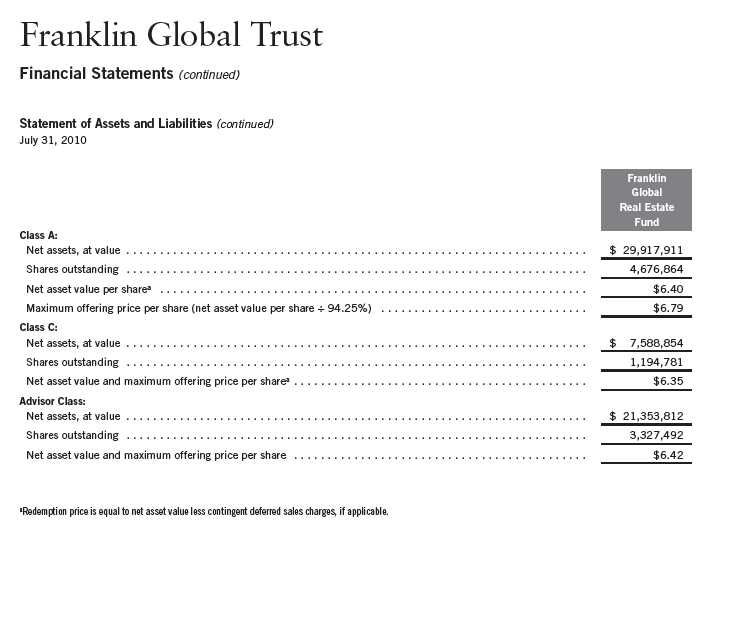

Franklin Global Trust

Notes to Financial Statements

Franklin Global Real Estate Fund

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Franklin Global Trust (Trust) is registered under the Investment Company Act of 1940, as amended, (1940 Act) as an open-end investment company, consisting of five separate funds. The Franklin Global Real Estate Fund (Fund) is included in this report. The financial statements of the remaining funds in the Trust are presented separately. The Fund offers three classes of shares: Class A, Class C, and Advisor Class. Each class of shares differs by its initial sales load, contingent deferred sales charges, distribution fees, voting rights on matters affecting a single class and its exchange privilege.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund values its investments in securities and other assets and liabilities carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. Under procedures approved by the Fund’s Board of Trustees, the Fund may utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.

Equity securities listed on an exchange or on the NASDAQ National Market System are valued at the last quoted sale price or the official closing price of the day, respectively. Foreign equity securities are valued as of the close of trading on the foreign stock exchange on which the security is primarily traded, or the NYSE, whichever is earlier. The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the day that the value of the security is determined. Over-the-counter securities are valued within the range of the most recent quoted bid and ask prices. Securities that trade in multiple markets or on multiple exchanges are valued according to the broadest and most representative market. Certain equity securities are valued based upon fundamental characteristics or relationships to similar securities. Time deposits are valued at cost, which approximates market val ue.

The Fund has procedures to determine the fair value of securities and other financial instruments for which market prices are not readily available or which may not be reliably priced. Under these procedures, the Fund primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. The Fund may also use an income-based valuation approach in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed.

Annual Report | 23

Franklin Global Trust

Notes to Financial Statements (continued)

Franklin Global Real Estate Fund

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| a. | Financial Instrument Valuation (continued) |

Trading in securities on foreign exchanges and over-the-counter markets may be completed before the daily close of business on the NYSE. Occasionally, events occur between the time at which trading in a foreign security is completed and the close of the NYSE that might call into question the reliability of the value of a portfolio security held by the Fund. As a result, differences may arise between the value of the Fund’s portfolio securities as determined at the foreign market close and the latest indications of value at the close of the NYSE. In order to minimize the potential for these differences, the investment manager monitors price movements following the close of trading in foreign stock markets through a series of country specific market proxies (such as baskets of American Depository Receipts, futures contracts and exchange traded funds). These price movements are measured against established trigger thresholds for ea ch specific market proxy to assist in determining if an event has occurred that may call into question the reliability of the values of the foreign securities held by the Fund. If such an event occurs, the securities may be valued using fair value procedures, which may include the use of independent pricing services.

b. Foreign Currency Translation

Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars based on the exchange rate of such currencies against U.S. dollars on the date of valuation. The Fund may enter into foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of securities, income and expense items denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date. Occasionally, events may impact the availability or reliability of foreign exchange rates used to convert the U.S. dollar equivalent value. If such an event occurs, the foreign exchange rate will be valued at fair value using procedures established and approved by Fund’s Board of Trustees.

The effect of changes in foreign exchange rates from changes in market prices on securities held are included in net realized and unrealized gain or loss from investments on the Statement of Operations. Realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest, and foreign withholding taxes and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in foreign exchange rates on foreign denominated assets and liabilities other than investments in securities held at the end of the reporting period. These realized and unrealized foreign exchange gains or losses are reported in foreign currency transactions and translation of other assets and liabilities denominated in foreign currencies on the Statement of Operations.

24 | Annual Report

Franklin Global Trust

Notes to Financial Statements (continued)

Franklin Global Real Estate Fund

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| c. | Derivative Financial Instruments |

The Fund invests in derivative financial instruments (derivatives) in order to manage risk or gain exposure to various other investments or markets. Derivatives are financial contracts based on an underlying or notional amount, require no initial investment or an initial net investment that is smaller than would normally be required to have a similar response to changes in market factors, and require or permit net settlement. Derivatives may contain various risks including the potential inability of the counterparty to fulfill their obligations under the terms of the contract, the potential for an illiquid secondary market, and the potential for market movements which expose the Fund to gains or losses in excess of the amounts shown on the Statement of Assets and Liabilities. Realized gain and loss and unrealized appreciation and depreciation on these contracts for the period are included in the Statement of Operations.

The Fund enters into forward exchange contracts primarily to manage and/or gain exposure to certain foreign currencies. A forward exchange contract is an agreement between the Fund and a counterparty to buy or sell a foreign currency for a specific exchange rate on a future date. Pursuant to the terms of the forward exchange contracts, cash or securities may be required to be deposited as collateral. Unrestricted cash may be invested according to the Fund’s investment objectives.

See Note 7 regarding other derivative information.

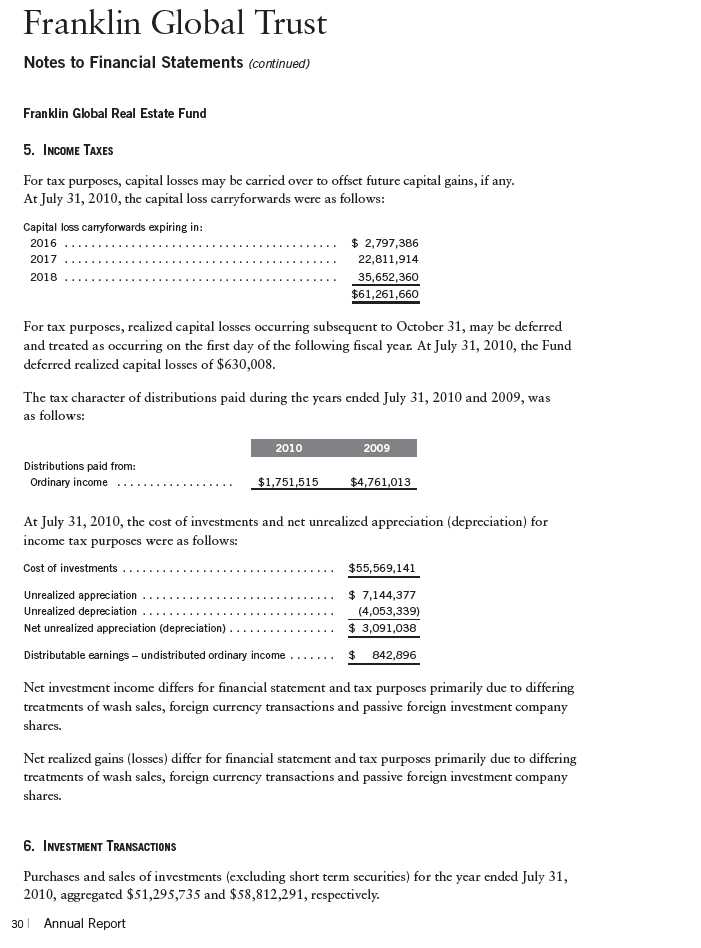

d. Income Taxes

It is the Fund’s policy to qualify as a regulated investment company under the Internal Revenue Code and to distribute to shareholders substantially all of its taxable income and net realized gains. As a result, no provision for federal income taxes is required. The Fund files U.S. income tax returns as well as tax returns in certain other jurisdictions. As of July 31, 2010, and for all open tax years, the Fund has determined that no provision for income tax is required in the Fund’s financial statements. Open tax years are those that remain subject to examination by such taxing authorities, which in the case of the U.S. is three years after the filing of a fund’s tax return.

Foreign securities held by the Fund may be subject to foreign taxation on dividend income received. Foreign taxes, if any, are recorded based on the tax regulations and rates that exist in the foreign markets in which the Fund invests.

Annual Report | 25

Franklin Global Trust

Notes to Financial Statements (continued)

Franklin Global Real Estate Fund

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| h. | Guarantees and Indemnifications |

Under the Trust’s organizational documents, its officers and trustees are indemnified by the Trust against certain liabilities arising out of the performance of their duties to the Trust. Additionally, in the normal course of business, the Trust, on behalf of the Fund, enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred. Currently, the Trust expects the risk of loss to be remote.

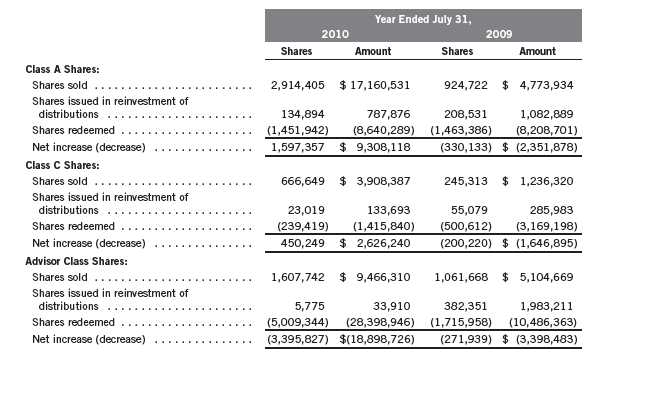

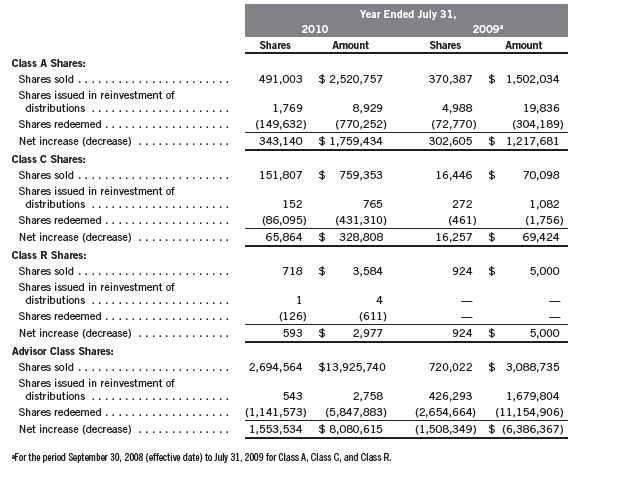

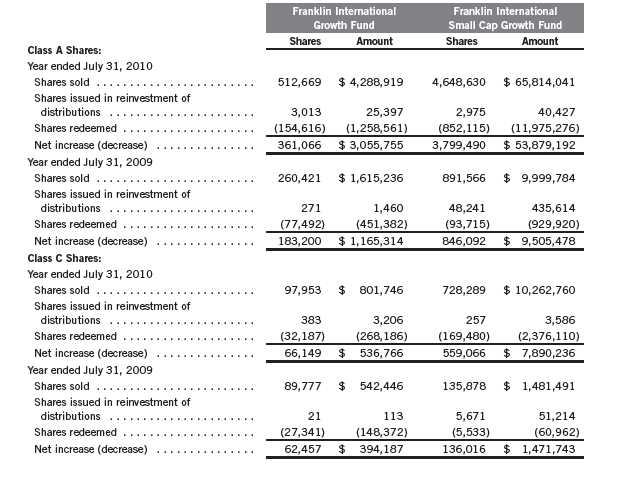

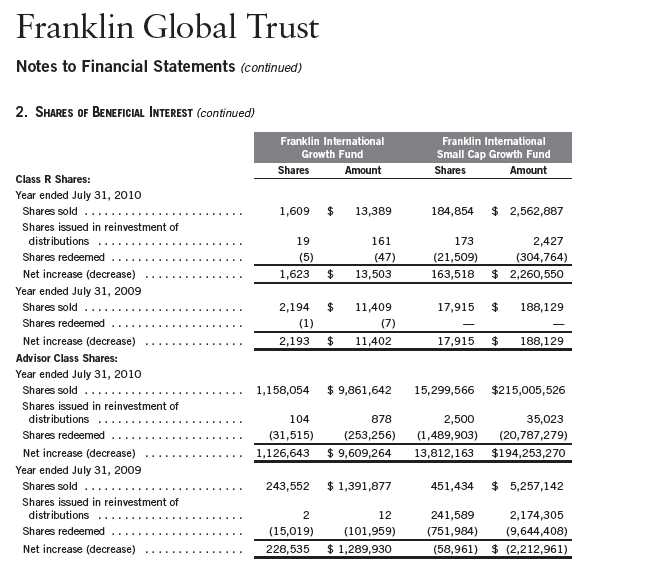

2. SHARES OF BENEFICIAL INTEREST

At July 31, 2010, there were an unlimited number of shares authorized (without par value).

Transactions in the Fund’s shares were as follows:

Annual Report | 27

Franklin Global Trust

Notes to Financial Statements (continued)

Franklin Global Real Estate Fund

3. TRANSACTIONS WITH AFFILIATES

Franklin Resources, Inc. is the holding company for various subsidiaries that together are referred to as Franklin Templeton Investments. Certain officers and trustees of the Fund are also officers and/or directors of the following subsidiaries:

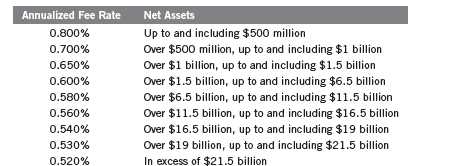

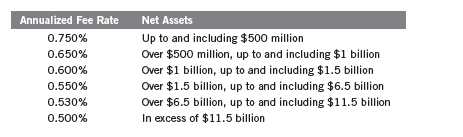

a. Management Fees

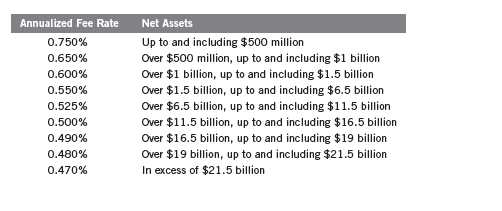

The Fund pays an investment management fee to FT Institutional based on the average daily net assets of the Fund as follows:

b. Administrative Fees

The Fund pays an administrative fee to FT Services of 0.20% per year of the average daily net assets of the Fund.

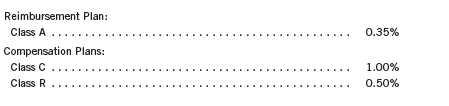

c. Distribution Fees

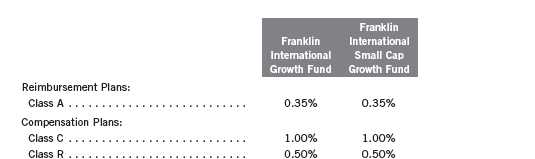

The Fund’s Board of Trustees has adopted distribution plans for each share class, with the exception of Advisor Class shares, pursuant to Rule 12b-1 under the 1940 Act. Under the Fund’s Class A reimbursement distribution plan, the Fund reimburses Distributors for costs incurred in connection with the servicing, sale and distribution of the Fund’s shares up to the maximum annual plan rate. Under the Class A reimbursement distribution plan, costs exceeding the maximum for the current plan year cannot be reimbursed in subsequent periods.

In addition, under the Fund’s Class C compensation distribution plan, the Fund pays Distributors for costs incurred in connection with the servicing, sale and distribution of the Fund’s shares up to the maximum annual plan rate.

28 | Annual Report

Franklin Global Trust

Notes to Financial Statements (continued)

Franklin Global Real Estate Fund

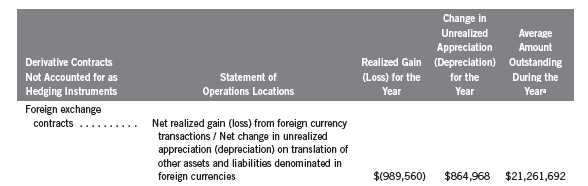

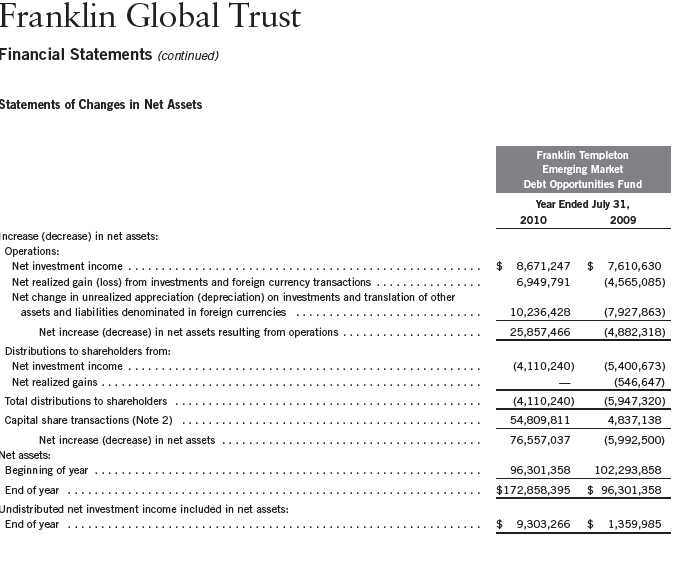

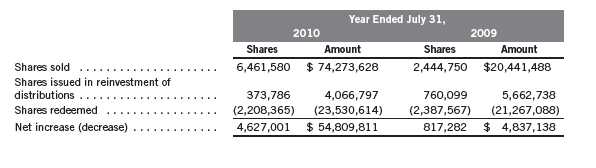

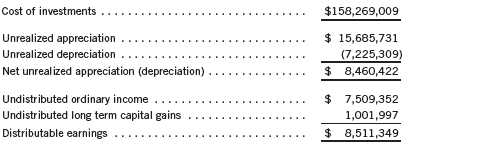

7. OTHER DERIVATIVE INFORMATION

For the year ended July 31, 2010, the effect of derivative contracts on the Fund’s Statement of Operations was as follows:

aRepresents the average notional amount for other derivative contracts outstanding during the period. For derivative contracts denominated in foreign currencies, notional amounts are converted into U.S. dollars.

See Note 1(c) regarding derivative financial instruments.

8. SPECIAL SERVICING AGREEMENT

The Fund, which is an eligible underlying investment of one or more of the Franklin Templeton Fund Allocator Series Funds (Allocator Funds), participates in a Special Servicing Agreement (SSA) with the Allocator Funds and certain service providers of the Fund and the Allocator Funds. Under the SSA, the Fund may pay a portion of the Allocator Funds’ expenses (other than any asset allocation, administrative, and distribution fees) to the extent such payments are less than the amount of the benefits realized or expected to be realized by the Fund (e.g., due to reduced costs associated with servicing accounts) from the investment in the Fund by the Allocator Funds. The Allocator Funds are either managed by Franklin Advisers, Inc. or administered by FT Services, affiliates of the fund. For the year ended July 31, 2010, the Fund was held by one or more of the Allocator Funds and was allocated expenses as noted in the Statement of Oper ations. At July 31, 2010, the Fund was no longer held by any of the Allocator Funds.

9. CREDIT FACILITY

The Fund, together with other U.S. registered and foreign investment funds (collectively “Borrowers”), managed by Franklin Templeton Investments, are borrowers in a joint syndicated senior unsecured credit facility totaling $750 million (Global Credit Facility) which matures on January 21, 2011. This Global Credit Facility provides a source of funds to the Borrowers for temporary and emergency purposes, including the ability to meet future unanticipated or unusually large redemption requests.

Annual Report | 31

Franklin Global Trust

Notes to Financial Statements (continued)

Franklin Global Real Estate Fund

9. CREDIT FACILITY (continued)

Under the terms of the Global Credit Facility, the Fund shall, in addition to interest charged on any borrowings made by the Fund and other costs incurred by the Fund, pay its share of fees and expenses incurred in connection with the implementation and maintenance of the Global Credit Facility, based upon its relative share of the aggregate net assets of all of the Borrowers, including an annual commitment fee of 0.10% based upon the unused portion of the Global Credit Facility, which is reflected in other expenses on the Statement of Operations. During the year ended July 31, 2010, the Fund did not use the Global Credit Facility.

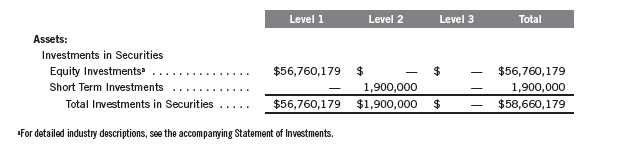

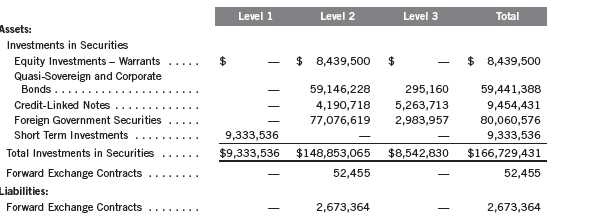

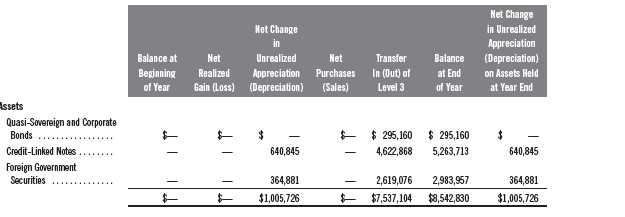

10. FAIR VALUE MEASUREMENTS

The Fund follows a fair value hierarchy that distinguishes between market data obtained from independent sources (observable inputs) and the Fund’s own market assumptions (unobservable inputs). These inputs are used in determining the value of the Fund’s investments and are summarized in the following fair value hierarchy:

- Level 1 – quoted prices in active markets for identical securities

- Level 2 – other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speed, credit risk, etc.)

- Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

For movements between the levels within the fair value hierarchy, the Fund has adopted a policy of recognizing the transfers as of the date of the underlying event which caused the movement.

32 | Annual Report

Franklin Global Trust

Notes to Financial Statements (continued)

Franklin Global Real Estate Fund

10. FAIR VALUE MEASUREMENTS (continued)

The following is a summary of the inputs used as of July 31, 2010, in valuing the Fund’s assets and liabilities carried at fair value:

11. SUBSEQUENT EVENTS

The Fund has evaluated subsequent events through the issuance of the financial statements and determined that no events have occurred that require disclosure.

ABBREVIATIONS

Selected Portfolio

REIT - Real Estate Investment Trust

Annual Report | 33

Franklin Global Trust

Report of Independent Registered Public Accounting Firm

Franklin Global Real Estate Fund

To the Board of Trustees and Shareholders of Franklin Global Trust

In our opinion, the accompanying statement of assets and liabilities, including the statement of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Franklin Global Real Estate Fund (one of the funds constituting Franklin Global Trust, hereafter referred to as the “Fund”) at July 31, 2010, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financ ial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at July 31, 2010 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

San Francisco, California

September 16, 2010

34 | Annual Report

Franklin Global Trust

Tax Designation (unaudited)

Franklin Global Real Estate Fund

Under Section 854(b)(2) of the Internal Revenue Code (Code), the Fund designates the maximum amount allowable but no less than $467,153 as qualified dividends for purposes of the maximum rate under Section 1(h)(11) of the Code for the fiscal year ended July 31, 2010. Distributions, including qualified dividend income, paid during calendar year 2010 will be reported to shareholders on Form 1099-DIV in January 2011. Shareholders are advised to check with their tax advisors for information on the treatment of these amounts on their individual income tax returns.

Annual Report | 35

Franklin Global Trust

Shareholder Information

Franklin Global Real Estate Fund

Board Review of Investment Management Agreement

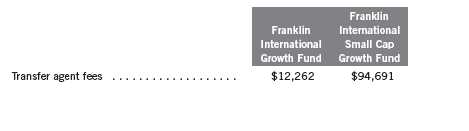

At a meeting held February 23, 2010, the Board of Trustees (Board), including a majority of non-interested or independent Trustees, approved renewal of the investment management agreements for each of the separate funds within Franklin Global Trust including Franklin Global Real Estate Fund (Fund(s)). In reaching this decision, the Board took into account information furnished throughout the year at regular Board meetings, as well as information prepared specifically in connection with the annual renewal review process. Information furnished and discussed throughout the year included investment performance reports and related financial information for each Fund, as well as periodic reports on shareholder services, legal, compliance, pricing, brokerage commissions and execution and other services provided by the Investment Manager (Manager) and its affiliates. Information furnished specifically in connection with the renewal process i ncluded a report for each Fund prepared by Lipper, Inc. (Lipper), an independent organization, as well as additional material, including a Fund profitability analysis report prepared by management. The Lipper report compared a Fund’s investment performance and expenses with those of other mutual funds deemed comparable to the Fund as selected by Lipper. The Fund profitability analysis report discussed the profitability to Franklin Templeton Investments from its overall U.S. fund operations, as well as on an individual fund-by-fund basis. Included with such profitability analysis report was information on a fund-by-fund basis listing portfolio managers and other accounts they manage, as well as information on management fees charged by the Manager and its affiliates to U.S. mutual funds and other accounts, including management’s explanation of differences where relevant and a three-year expense analysis with an explanation for any increase in expense ratios. Additional material accompanying such rep ort was a memorandum prepared by management describing project initiatives and capital investments relating to the services provided to the Funds by the Franklin Templeton Investments organization, as well as a memorandum relating to economies of scale and a comparative analysis concerning transfer agent fees charged each Fund.

In considering such materials, the independent Trustees received assistance and advice from and met separately with independent counsel. While the investment management agreements for all Funds were considered at the same Board meeting, the Board dealt with each Fund separately. In approving continuance of the investment management agreement for each Fund, the Board, including a majority of independent Trustees, determined that the existing management fee structure was fair and reasonable and that continuance of the investment management agreement was in the best interests of the Funds and their shareholders. While attention was given to all information furnished, the following discusses some primary factors relevant to the Board’s decision.

NATURE, EXTENT AND QUALITY OF SERVICES. The Board was satisfied with the nature and quality of the overall services provided by the Manager and its affiliates to the Fund and its shareholders. In addition to investment performance and expenses discussed later, the Board’s opinion was based, in part, upon periodic reports furnished it showing that the investment policies

Annual Report | 41

Franklin Global Trust

Shareholder Information (continued)

Franklin Global Real Estate Fund

Board Review of Investment Management Agreement (continued)

and restrictions for the Fund were consistently complied with as well as other reports periodically furnished the Board covering matters such as the compliance of portfolio managers and other management personnel with the code of ethics adopted throughout the Franklin Templeton fund complex, the adherence to fair value pricing procedures established by the Board, and the accuracy of net asset value calculations. The Board also noted the extent of benefits provided Fund shareholders from being part of the Franklin Templeton family of funds, including the right to exchange investments between the same class of funds without a sales charge, the ability to reinvest Fund dividends into other funds and the right to combine holdings in other funds to obtain a reduced sales charge. Favorable consideration was given to management’s continuous efforts and expenditures in establishing back-up systems and recovery procedures to function in the event of a natural disaster, it being noted that such systems and procedures had functioned smoothly during the Florida hurricanes and blackouts experienced in recent years. Among other factors taken into account by the Board were the Manager’s best execution trading policies, including a favorable report by an independent portfolio trading analytical firm. Consideration was also given to the experience of the Fund’s portfolio management team, the number of accounts managed and general method of compensation. In this latter respect, the Board noted that a primary factor in management’s determination of a portfolio manager’s bonus compensation was the relative investment performance of the funds he or she managed and that a portion of such bonus was required to be invested in a predesignated list of funds within such person’s fund management area so as to be aligned with the interests of Fund shareholders. The Board also took into account the quality of transfer agent and sharehol der services provided Fund shareholders by an affiliate of the Manager, noting continuing expenditures by management to increase and improve the scope of such services, periodic favorable reports on such service conducted by third parties, and the continuous enhancements to and high industry ranking given the Franklin Templeton website. Particular attention was given to management’s conservative approach and diligent risk management procedures, including continuous monitoring of counterparty credit risk and attention given to derivatives and other complex instruments. The Board also took into account, among other things, management’s efforts in establishing a global credit facility for the benefit of the Fund and other accounts managed by Franklin Templeton Investments to provide a source of cash for temporary and emergency purposes or to meet unusual redemption requests as well as the strong financial position of the Manager’s parent company and its commitment to the mutual fund business as e videnced by its subsidization of money market funds. The Board also noted management’s efforts to minimize any negative impact on the nature and quality of services provided the Fund arising from Franklin Templeton Investments’ implementation of a hiring freeze and employee reductions in response to market conditions during the latter part of 2008 and early 2009.

INVESTMENT PERFORMANCE. The Board placed significant emphasis on the investment performance of the Fund in view of its importance to shareholders. While consideration was given to performance reports and discussions with portfolio managers at Board meetings throughout the

42 | Annual Report

Franklin Global Trust

Shareholder Information (continued)

Franklin Global Real Estate Fund

Board Review of Investment Management Agreement (continued)

year, particular attention in assessing performance was given to the Lipper reports furnished for the agreement renewal. The Lipper reports prepared for the Fund showed the investment performance of the largest share class of the Fund in comparison to a performance universe selected by Lipper. Comparative performance for the Fund was shown for the one-year period ended December 31, 2009, and for additional periods ended that date depending on when the Fund commenced operations. The performance universe for the Fund consisted of the Fund and all retail and institutional global real estate funds as selected by Lipper. The Fund has been in operation for only three full years at the date of the Lipper report, which showed the total return of the Fund’s Class A shares to be in the lowest quintile of such performance universe in 2009, the highest quintile of such performance universe in 2008 and the second-lowest quintile of such univ erse in 2007. While noting that the Fund’s brief period of existence limited the meaningfulness of such performance record, the Board discussed with management steps being taken to improve its performance including appointment of an additional portfolio manager. The Board was satisfied with management’s response and efforts being made to improve performance and intends to continue monitoring the Fund’s performance results.

COMPARATIVE EXPENSES. Consideration was given to the management fee and total expense ratios of the dominant share class of the Fund with those of a comparative share class within a group of funds selected by Lipper as its appropriate Lipper expense group. Lipper expense data is based upon information taken from each fund’s most recent annual report, which reflects historical asset levels that may be quite different from those currently existing, particularly in a period of market volatility. While recognizing such inherent limitation and the fact that expense ratios generally increase as assets decline and decrease as assets grow, the Board believed the independent analysis conducted by Lipper to be an appropriate measure of comparative expenses. In reviewing comparative costs, Lipper provides information on the Fund’s management fee i n comparison with the contractual investment management fee that would have been charged by other funds within its Lipper expense group assuming they were similar in size to the Fund, as well as the actual total expenses of the Fund in comparison with those of its Lipper expense group. The Lipper contractual investment management fee analysis includes the advisory and administrative fees directly charged to the Fund as being part of the management fee. The contractual investment management fee rate for the Fund was above the median of its Lipper expense group, but the actual total expense ratio was in the lowest quintile of such expense group. The Board found the expenses of the Fund to be acceptable, noting they were subsidized by management.

MANAGEMENT PROFITABILITY. The Board also considered the level of profits realized by the Manager and its affiliates in connection with the operation of the Fund. In this respect, the Board reviewed the Fund profitability analysis that addresses the overall profitability of Franklin Templeton’s U.S. fund business, as well as its profits in providing management and other services to the Fund during the 12-month period ended September 30, 2009, being the most recent fiscal year-end for Franklin Resources, Inc., the Manager’s parent. In reviewing the analysis, attention

Annual Report | 43

Franklin Global Trust

Shareholder Information (continued)

Franklin Global Real Estate Fund

Board Review of Investment Management Agreement (continued)

was given to the methodology followed in allocating costs to the Fund, it being recognized that allocation methodologies are inherently subjective and various allocation methodologies may each be reasonable while producing different results. In this respect, the Board noted that, while being continuously refined and reflecting changes in the Manager’s own cost accounting, the allocation methodology was consistent with that followed in profitability report presentations for the Fund made in prior years and that the Fund’s independent registered public accounting firm had been engaged by the Manager to review the reasonableness of the allocation methodologies solely for use by the Fund’s Board in reference to the profitability analysis. In reviewing and discussing such analysis, management discussed with the Board its belief that costs incurred in establishing the infrastructure necessary for the type of mutual fund oper ations conducted by the Manager and its affiliates may not be fully reflected in the expenses allocated to the Fund in determining its profitability, as well as the fact that the level of profits, to a certain extent, reflected operational cost savings and efficiencies initiated by management. The Board also took into account management’s expenditures in improving shareholder services provided the Fund, as well as the need to meet additional regulatory and compliance requirements resulting from the Sarbanes-Oxley Act and recent SEC and other regulatory requirements. In addition, the Board considered a third-party study comparing the profitability of the Manager’s parent on an overall basis to other publicly held managers broken down to show profitability from management operations exclusive of distribution expenses, as well as profitability including distribution expenses. The Board also considered the extent to which the Manager and its affiliates might derive ancillary benefits from fund operatio ns, including potential benefits resulting from allocation of fund brokerage and the use of commission dollars to pay for research. Based upon its consideration of all these factors, and taking into account the fact that the expenses of the Fund were being subsidized through fee waivers, the Board determined that the level of profits realized by the Manager and its affiliates from providing services to the Fund was not excessive in view of the nature, quality and extent of services provided.

ECONOMIES OF SCALE. The Board also considered whether economies of scale are realized by the Manager as the Fund grows larger and the extent to which this is reflected in the level of management fees charged. While recognizing that any precise determination is inherently subjective, the Board noted that based upon the Fund profitability analysis, it appears that as some funds get larger, at some point economies of scale do result in the Manager realizing a larger profit margin on management services provided such a fund. The Board believed it unlikely that economies of scale existed in the management of the Fund, based on its relatively small asset size on December 31, 2009.

44 | Annual Report

Franklin Global Trust

Shareholder Information (continued)

Franklin Global Real Estate Fund

Proxy Voting Policies and Procedures

The Trust’s investment manager has established Proxy Voting Policies and Procedures (Policies) that the Trust uses to determine how to vote proxies relating to portfolio securities. Shareholders may view the Trust’s complete Policies online at franklintempleton.com. Alternatively, shareholders may request copies of the Policies free of charge by calling the Proxy Group collect at (954) 527-7678 or by sending a written request to: Franklin Templeton Companies, LLC, 500 East Broward Boulevard, Suite 1500, Fort Lauderdale, FL 33394, Attention: Proxy Group. Copies of the Trust’s proxy voting records are also made available online at franklintempleton.com and posted on the U.S. Securities and Exchange Commission’s website at sec.gov and reflect the most recent 12-month period ended June 30.

Quarterly Statement of Investments

The Trust files a complete statement of investments with the U.S. Securities and Exchange Commission for the first and third quarters for each fiscal year on Form N-Q. Shareholders may view the filed Form N-Q by visiting the Commission’s website at sec.gov. The filed form may also be viewed and copied at the Commission’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling (800) SEC-0330.

Householding of Reports and Prospectuses

You will receive the Fund’s financial reports every six months as well as an annual updated summary prospectus (prospectus available upon request). To reduce Fund expenses, we try to identify related shareholders in a household and send only one copy of the financial reports and summary prospectus. This process, called “householding,” will continue indefinitely unless you instruct us otherwise. If you prefer not to have these documents householded, please call us at (800) 632-2301. At any time you may view current prospectuses/summary prospectuses and financial reports on our website. If you choose, you may receive these documents through electronic delivery.

Annual Report | 45

This page intentionally left blank.

This page intentionally left blank.

This page intentionally left blank.

Sign up for electronic delivery

on franklintempleton. com

Annual Report and Shareholder Letter

FRANKLIN GLOBAL REAL ESTATE FUND

Investment Manager

Franklin Templeton Institutional, LLC

Distributor

Franklin Templeton Distributors, Inc.

(800) DIAL BEN®

franklintempleton. com

Shareholder Services

(800) 632-2301

Authorized for distribution only when accompanied or preceded by a summary prospectus and/or prospectus. Investors should carefully consider a fund’s investment goals, risks, charges and expenses before investing. A prospectus contains this and other information; please read it carefully before investing.

To ensure the highest quality of service, telephone calls to or from our service departments may be monitored, recorded and accessed. These calls can be identified by the presence of a regular beeping tone.

- 2010 Franklin Templeton Investments. All rights reserved.

- A 09/10

FRANKLIN

LARGE CAP EQUITY FUND

| | | | | | | |

| | Contents | | | | | |

| |

| Shareholder Letter | 1 | Annual Report | | Financial Highlights and | | Report of Independent | |

| | | | | Statement of Investments | 15 | Registered Public | |

| | | Franklin Large Cap | | | | | |

| | | | | | | Accounting Firm | 35 |

| | | Equity Fund | 3 | Financial Statements | 22 | | |

| | | | | | | Tax Designation | 36 |

| | | Performance Summary | 8 | Notes to | | | |

| | | | | Financial Statements | 26 | Board Members and Officers | 37 |

| | | Your Fund’s Expenses | 13 | | | | |

| | | | | | | Shareholder Information | 42 |

Annual Report

Franklin Large Cap Equity Fund

Your Fund’s Goal and Main Investments: Franklin Large Cap Equity Fund seeks long-term growth of principal and income through investing at least 80% of its net assets in equity securities of large capitalization companies with market capitalizations within the top 50% of companies in the Russell 1000® Index, or of more than $5 billion, at the time of purchase.1 The Fund attempts to keep taxable capital gain distributions relatively low.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

This annual report for Franklin Large Cap Equity Fund covers the fiscal year ended July 31, 2010.

Performance Overview

Franklin Large Cap Equity Fund – Class A delivered a +7.47% cumulative total return for the 12 months ended July 31, 2010. The Fund underperformed its benchmark, the Standard & Poor’s 500 Index (S&P 500), which posted a +13.84% total return during the same period.2 You can find other Fund performance data in the Performance Summary beginning on page 8.

Economic and Market Overview

During the 12-month period ended July 31, 2010, the U.S. economy recovered unevenly from the depths of the recession, supported by a combination of fundamental improvement in business conditions and government intervention and stimulus. Economic activity as measured by gross domestic product (GDP) expanded at a 5.0% annualized rate in 2009’s fourth quarter. As the effects of temporary stimulus measures faded and construction and industrial production

1. The Russell 1000 Index is market capitalization weighted and measures performance of the largest companies in the Russell 3000 Index, which represents the majority of the U.S. market’s total capitalization.

2. Source: © 2010 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. The S&P 500 is a market capitalization-weighted index of 500 stocks designed to measure total U.S. equity market performance. STANDARD & POOR’S®, S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC. Standard & Poor’s does not sponsor, endorse, sell or promote any S&P index-based product. The index is unmanaged and includes reinvested distributions. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

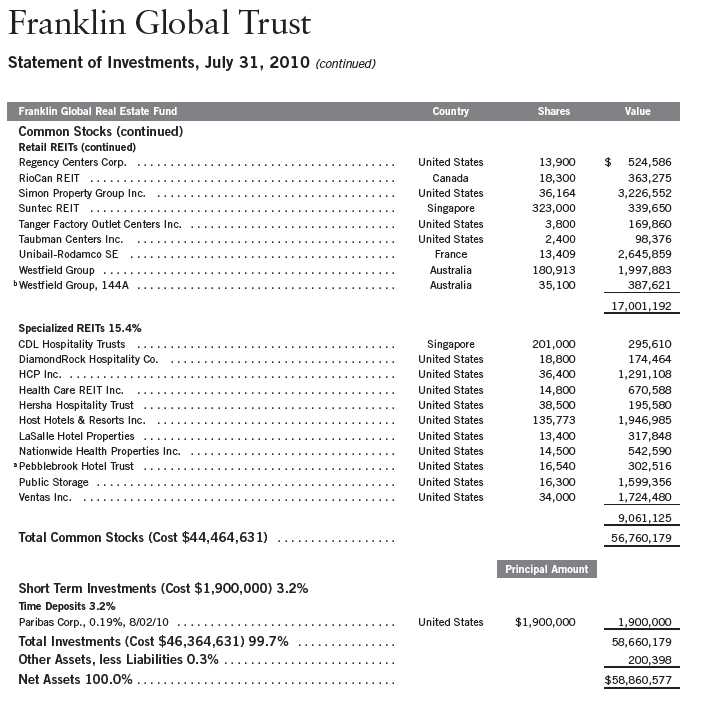

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 19.

Annual Report | 3

| | |

| Portfolio Breakdown | | |

| 7/31/10 | | |

| | % of Total | |

| Sector/Industry | Net Assets | |

| Oil, Gas & Consumable Fuels | 6.2 | % |

| Pharmaceuticals | 6.2 | % |

| Aerospace & Defense | 5.4 | % |

| Textiles, Apparel & Luxury Goods | 5.1 | % |

| Beverages | 4.6 | % |

| Computers & Peripherals | 4.4 | % |

| Biotechnology | 4.2 | % |

| Food Products | 4.1 | % |

| IT Services | 4.1 | % |

| Energy Equipment & Services | 3.9 | % |

| Capital Markets | 3.5 | % |

| Communications Equipment | 3.4 | % |

| Electronic Equipment, Instruments | | |

| & Components | 3.3 | % |

| Insurance | 3.3 | % |

| Chemicals | 2.9 | % |

| Software | 2.9 | % |

| Other | 23.0 | % |

| Short-Term Investments and | | |

| Other Net Assets | 9.5 | % |

cooled somewhat, GDP growth slowed to an annualized 3.7% pace in 2010’s first quarter and an estimated annualized 1.6% pace in the second quarter.

Challenges such as mixed economic data, elevated debt concerns surrounding the U.S. budget deficit and a growing lack of job prospects for the unemployed also hindered consumer confidence and the economy’s advance. During much of the period, home prices rose in most regions due to record-low interest rates, a first-time homebuyer tax credit program, and prices dipping to levels that lured buyers. The housing sector overall remained weak, however, as foreclosures jumped to new highs, and the pace of home sales and housing starts failed to gain traction.

Amid signs of a demand-led recovery, crude oil prices rose from $69 per barrel at the end of July 2009 to a period high of nearly $87 in early April. When mixed economic data began to indicate a slow recovery during the spring, oil prices dipped to $66 in late May before recovering to $79 by the end of July 2010. With scant evidence of pricing pressure in the economy, the July 2010 inflation rate as gauged by the Consumer Price Index (CPI) was an annualized 1.2%.3 Core CPI, which excludes food and energy costs, hovered near a 44-year low by period-end, rising only 0.9% since July 2009.3

Given few inflationary concerns and an economic recovery the Federal Reserve Board (Fed) characterized as “unusually uncertain,” the Federal Open Market Committee announced it intended to hold the federal funds target rate in the 0% to 0.25% range “for an extended period.” As some economic data improved in early 2010, the Fed began withdrawing some of the extraordinary support policies it had provided in response to the 2008 financial crisis. Despite a lack of significant job gains, the unemployment rate, which had jumped from 9.4% at the beginning of the period to a 26-year high of 10.1% by October 2009, dropped to 9.5% through June and July 2010 as the labor force participation rate fell.3

Investor confidence improved from depressed levels in response to strong corporate profits, renewed business activity and encouraging, though mixed, economic data, which helped equity markets rally for most of the year under review. However, the markets became quite volatile later in the period, partially stemming from concerns about many European countries’ creditworthiness and growing doubts about the U.S. and global economic recoveries. Many investors sought the relative safety of U.S. Treasury securities, even at times when the stock market was climbing. For the 12 months under review, the blue chip

3. Source: Bureau of Labor Statistics.

4 | Annual Report

stocks of the Dow Jones Industrial Average delivered a +17.28% total return, while the broader S&P 500 posted a +13.84% total return and the technology-heavy NASDAQ Composite Index produced a +14.99% return.4 All major industry groups advanced during the period, led by the industrials, consumer discretionary and financials sectors.

Investment Strategy

We are research-driven, fundamental investors, pursuing a blend of growth and value strategies. We use a top-down analysis of macroeconomic trends, market sectors (with some attention to the sector weightings in the Fund’s comparative index) and industries combined with a bottom-up analysis of individual securities. In selecting investments for the Fund, we look for companies we believe are positioned for growth in revenues, earnings or assets, and are selling at reasonable prices. We also consider the level of dividends a company has paid. We employ a thematic approach to identify sectors that may benefit from longer term dynamic growth. Within these sectors, we consider the basic financial and operating strength and quality of a company and company management. The Fund, from time to time, may have significant positions in particular sectors such as technology or industrials. We also seek to identify c ompanies that we believe are temporarily out of favor with investors, but have a good intermediate-or long-term outlook.

Manager’s Discussion

During the year under review, the Fund’s large-cap bias hurt performance as large-cap stocks significantly lagged their mid-cap and small-cap counterparts during the past year. The S&P 100 Index, which comprises the largest U.S. companies, returned +8.76%.5 The S&P 1000 Index, composed of mid- and small-cap companies, returned +21.68%.6 Clearly during the past year, as the equity markets rebounded from financial turmoil and subsequent recession, owning stocks in mid- and small-cap companies was generally more rewarding.

4. Source: © 2010 Morningstar. The Dow Jones Industrial Average is price weighted based on the average market price of 30 blue chip stocks that are generally industry leaders. See footnote 2 for a description of the S&P 500. The NASDAQ Composite Index is a broad-based market capitalization-weighted index designed to measure all NASDAQ domestic and international based common type stocks listed on the NASDAQ Stock Market.

5. Source: © 2010 Morningstar. The S&P 100 Index is market capitalization weighted and consists of the larger and more stable companies in the S&P 500. Securities included in the S&P 100 Index must have individual stock options available.

6. Source: © 2010 Morningstar. The S&P 1000 Index combines two leading indices — the S&P MidCap 400 and the S&P SmallCap 600 — to form an investable benchmark for the mid-small cap universe of the U.S. equity market.

| | |

| Top 10 Equity Holdings | | |

| 7/31/10 | | |

| |

| Company | % of Total | |

| Sector/Industry | Net Assets | |

| Exxon Mobil Corp. | 2.9 | % |

| Oil, Gas & Consumable Fuels | | |

| Nestle SA (Switzerland) | 2.6 | % |

| Food Products | | |

| JPMorgan Chase & Co. | 2.3 | % |

| Diversified Financial Services | | |

| Wells Fargo & Co. | 2.2 | % |

| Commercial Banks | | |

| General Electric Co. | 2.2 | % |

| Industrial Conglomerates | | |

| Gilead Sciences Inc. | 2.2 | % |

| Biotechnology | | |

| Apple Inc. | 2.2 | % |

| Computers & Peripherals | | |

| NIKE Inc., B | 2.2 | % |

| Textiles, Apparel & Luxury Goods | | |

| BorgWarner Inc. | 2.2 | % |

| Auto Components | | |

| EMC Corp. | 2.2 | % |

| Computers & Peripherals | | |

Annual Report | 5

| | |

| Geographic Breakdown | | |

| 7/31/10 | | |

| | % of Total | |

| | Net Assets | |

| U.S. | 76.4 | % |

| U.K. | 3.7 | % |

| Switzerland | 3.6 | % |

| Hong Kong | 1.8 | % |

| South Korea | 1.7 | % |

| Israel | 1.4 | % |

| Brazil | 1.0 | % |

| Taiwan | 0.9 | % |

| Short-Term Investments & Other | | |

| Net Assets | 9.5 | % |

The consumer discretionary and consumer staples sectors had strong results and benefited performance relative to the S&P 500 over the past 12 months.7 In both sectors, foreign companies were major contributors. Among consumer discretionary stocks, Li & Fung,8 a worldwide distributor of consumer products, and Hyundai Motor,8 a South Korean auto manufacturer, helped Fund performance. Another c onsumer discretionary sector holding, BorgWarner, a U.S.-based auto components company, also benefited Fund performance. In the consumer staples sector, two international companies that were leading contributors to performance were Cadbury, a British candy company acquired by Kraft, and Nestle, a Swiss food producer and long-term Fund holding during the period. Hansen Natural, a U.S.-based beverage maker, aided performance as well. In addition, U.S. technology company Polycom, an architect of high definition telepresence, video and voice solutions, boosted performance. We sold Cadbury and Polycom during the period.

In contrast, stock selection in the financials and health care sectors detracted from relative performance over the period, offset somewhat by our underweighting in financials stocks.9 Asset management company BlackRock8 lost value and weighed on performance. Life and health insurance company Aflac performed well over the 12-month period, but we sold it during the period and held it too briefly to fully benefit the Fund. In the health care sector, biopharmaceutical companies Celgene, Roche Holding and Gilead Sciences weighed on Fund performance. We continued to hold Ce lgene and Gilead at period-end as our analysis reinforced their long-term potential. Elsewhere, key detractors were telecommunications firm Singapore Telecom and offshore drilling contractor Transocean, whose deepwater oil rig leased to British Petroleum was involved in the recent Gulf of Mexico oil spill. By period-end, we sold Roche Holding, Singapore Telecom and Transocean.

7. The consumer discretionary sector comprises auto components; automobiles; distributors; specialty retail; and textiles, apparel and luxury goods in the SOI. The consumer staples sector comprises beverages, food and staples retailing, and food products in the SOI.

8. This holding is not a component of the S&P 500.

9. The financials sector comprises capital markets, commercial banks, diversified financial services, insurance, and thrifts and mortgage finance in the SOI. The health care sector comprises biotechnology, health care providers and services, and pharmaceuticals in the SOI.

6 | Annual Report

Thank you for your continued participation in Franklin Large Cap Equity Fund.

We look forward to serving your future investment needs.

Portfolio Management Team

Franklin Large Cap Equity Fund

The foregoing information reflects our analysis, opinions and portfolio holdings as of July 31, 2010, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Annual Report | 7

Performance Summary as of 7/31/10

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

| | | | | | | | |

| Price and Distribution Information | | | | | | |

| Class A (Symbol: n/a) | | | | Change | | 7/31/10 | | 7/31/09 |

| Net Asset Value (NAV) | | | +$ | 0.33 | $ | 5.00 | $ | 4.67 |

| Distributions (8/1/09–7/31/10) | | | | | | | | |

| Dividend Income | $ | 0.0188 | | | | | | |

| Class C (Symbol: n/a) | | | | Change | | 7/31/10 | | 7/31/09 |

| Net Asset Value (NAV) | | | +$ | 0.31 | $ | 4.97 | $ | 4.66 |

| Distributions (8/1/09–7/31/10) | | | | | | | | |

| Dividend Income | $ | 0.0058 | | | | | | |

| Class R (Symbol: n/a) | | | | Change | | 7/31/10 | | 7/31/09 |

| Net Asset Value (NAV) | | | +$ | 0.33 | $ | 5.00 | $ | 4.67 |

| Distributions (8/1/09–7/31/10) | | | | | | | | |

| Dividend Income | $ | 0.0120 | | | | | | |

| Advisor Class (Symbol: FLCIX) | | | | Change | | 7/31/10 | | 7/31/09 |

| Net Asset Value (NAV) | | | +$ | 0.34 | $ | 5.01 | $ | 4.67 |

| Distributions (8/1/09–7/31/10) | | | | | | | | |

| Dividend Income | $ | 0.0300 | | | | | | |

8 | Annual Report

Performance Summary (continued)

Performance1

Cumulative total return excludes sales charges. Average annual total returns and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class C: 1% contingent deferred sales charge in first year only; Class R/Advisor Class: no sales charges.

| | | | | | | | | | | |

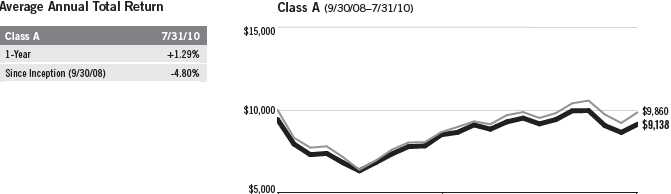

| Class A | | | | | | | 1-Year | | | Inception (9/30/08) | |

| Cumulative Total Return2 | | | | | | + | 7.47 | % | | -3.05 | % |

| Average Annual Total Return3 | | | | | | + | 1.29 | % | | -4.80 | % |

| Value of $10,000 Investment4 | | | | | | $ | 10,129 | | $ | 9,138 | |

| Avg. Ann. Total Return (6/30/10)5 | | | | | | + | 4.06 | % | | -8.00 | % |

| Total Annual Operating Expenses6 | | | | | | | | | | | |

| Without Waiver | 1.57 | % | | | | | | | | | |

| With Waiver | 1.28 | % | | | | | | | | | |

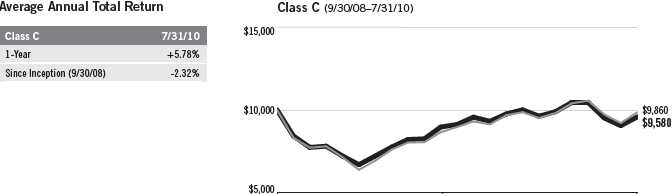

| Class C | | | | | | | 1-Year | | | Inception (9/30/08) | |

| Cumulative Total Return2 | | | | | | + | 6.78 | % | | -4.20 | % |

| Average Annual Total Return3 | | | | | | + | 5.78 | % | | -2.32 | % |

| Value of $10,000 Investment4 | | | | | | $ | 10,578 | | $ | 9,580 | |

| Avg. Ann. Total Return (6/30/10)5 | | | | | | + | 8.68 | % | | -5.50 | % |

| Total Annual Operating Expenses6 | | | | | | | | | | | |

| Without Waiver | 2.27 | % | | | | | | | | | |

| With Waiver | 1.98 | % | | | | | | | | | |

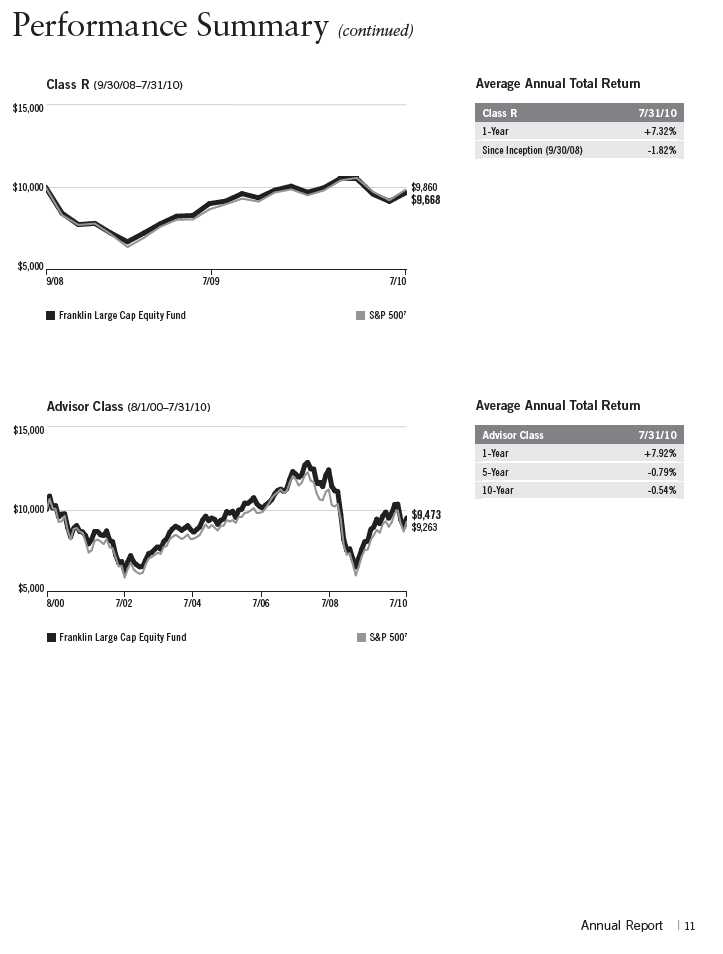

| Class R | | | | | | | 1-Year | | | Inception (9/30/08) | |

| Cumulative Total Return2 | | | | | | + | 7.32 | % | | -3.32 | % |

| Average Annual Total Return3 | | | | | | + | 7.32 | % | | -1.82 | % |

| Value of $10,000 Investment4 | | | | | | $ | 10,732 | | $ | 9,668 | |

| Avg. Ann. Total Return (6/30/10)5 | | | | | | + | 10.26 | % | | -4.98 | % |

| Total Annual Operating Expenses6 | | | | | | | | | | | |

| Without Waiver | 1.77 | % | | | | | | | | | |

| With Waiver | 1.48 | % | | | | | | | | | |

| Advisor Class | | | | 1-Year | | | 5-Year | | | 10-Year | |

| Cumulative Total Return2 | | | + | 7.92 | % | | -3.88 | % | | -5.27 | % |

| Average Annual Total Return3 | | | + | 7.92 | % | | -0.79 | % | | -0.54 | % |

| Value of $10,000 Investment4 | | | $ | 10,792 | | $ | 9,612 | | $ | 9,473 | |

| Avg. Ann. Total Return (6/30/10)5 | | | + | 10.65 | % | | -1.02 | % | | -1.44 | % |

| Total Annual Operating Expenses6 | | | | | | | | | | | |

| Without Waiver | 1.27 | % | | | | | | | | | |

| With Waiver | 0.98 | % | | | | | | | | | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

The investment manager and administrator have contractually agreed to waive or limit their respective fees and to assume as their own expense certain expenses otherwise payable by the Fund so that common expenses (i.e., a combination of investment management fees, fund administration fees, and other expenses, but excluding Rule 12b-1 fees and acquired fund fees and expenses) for each class of the Fund do not exceed 0.95% (other than certain nonroutine expenses or costs, including those relating to litigation, indemnification, reorganizations and liquidations) until 11/30/10.

Annual Report | 9

Performance Summary (continued)

Total Return Index Comparison for a Hypothetical $10,000 Investment1

Total return represents the change in value of an investment over the periods shown. It includes any applicable maximum sales charge, Fund expenses, account fees and reinvested distributions. The unmanaged index includes reinvestment of any income or distributions. It differs from the Fund in composition and does not pay management fees or expenses. One cannot invest directly in an index.

| | |

| 9/08 | 7/09 | 7/10 |

| Franklin Large Cap Equity Fund | | S&P 500 7 |

| | |

| 9/08 | 7/09 | 7/10 |

| Franklin Large Cap Equity Fund | | S&P 500 7 |

10 | Annual Report

Performance Summary (continued)

Endnotes

While stocks have historically outperformed other asset classes over the long term, they tend to fluctuate more dramatically over the short term. There are special risks involved with significant exposure to a particular sector, including increased susceptibility related to economic, business, or other developments affecting that sector, which may result in increased volatility. The Fund’s investments in foreign company stocks involve special risks including currency fluctuations and political uncertainty. The Fund’s prospectus also includes a description of the main investment risks.

| |

Class C: Class R: | These shares have higher annual fees and expenses than Class A shares. Shares are available to certain eligible investors as described in the prospectus. These shares have higher annual fees than Class A shares. |

Advisor Class: | Shares are available to certain eligible investors as described in the prospectus. |

1. If the manager and administrator had not waived fees, the Fund’s total returns would have been lower. 2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated. 4. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

5. In accordance with SEC rules, we provide standardized average annual total return information through the latest calendar quarter.

6. Figures are as stated in the Fund’s prospectus current as of the date of this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

7. Source: © 2010 Morningstar. The S&P 500 is a market capitalization-weighted index of 500 stocks designed to measure total U.S. equity market performance.

12 | Annual Report

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases, if applicable; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, if appli- cable, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| | If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| | If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Annual Report | 13

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

| | | | | | |

| | | Beginning Account | | Ending Account | | Expenses Paid During |

| Class A | | Value 2/1/10 | | Value 7/31/10 | | Period* 2/1/10–7/31/10 |

| Actual | $ | 1,000 | $ | 997.40 | $ | 6.19 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,018.60 | $ | 6.26 |

| Class C | | | | | | |

| Actual | $ | 1,000 | $ | 995.10 | $ | 9.65 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,015.12 | $ | 9.74 |

| Class R | | | | | | |

| Actual | $ | 1,000 | $ | 997.10 | $ | 7.18 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,017.60 | $ | 7.25 |

| Advisor Class | | | | | | |

| Actual | $ | 1,000 | $ | 1,000.50 | $ | 4.71 |

| Hypothetical (5% return before expenses) | $ | 1,000 | $ | 1,020.08 | $ | 4.76 |

*Expenses are calculated using the most recent six-month expense ratio, net of expense waivers, annualized for each class (A: 1.25%; C: 1.95%; R: 1.45%; and Advisor: 0.95%), multiplied by the average account value over the period, multiplied by 181/365 to reflect the one-half year period.

14 | Annual Report

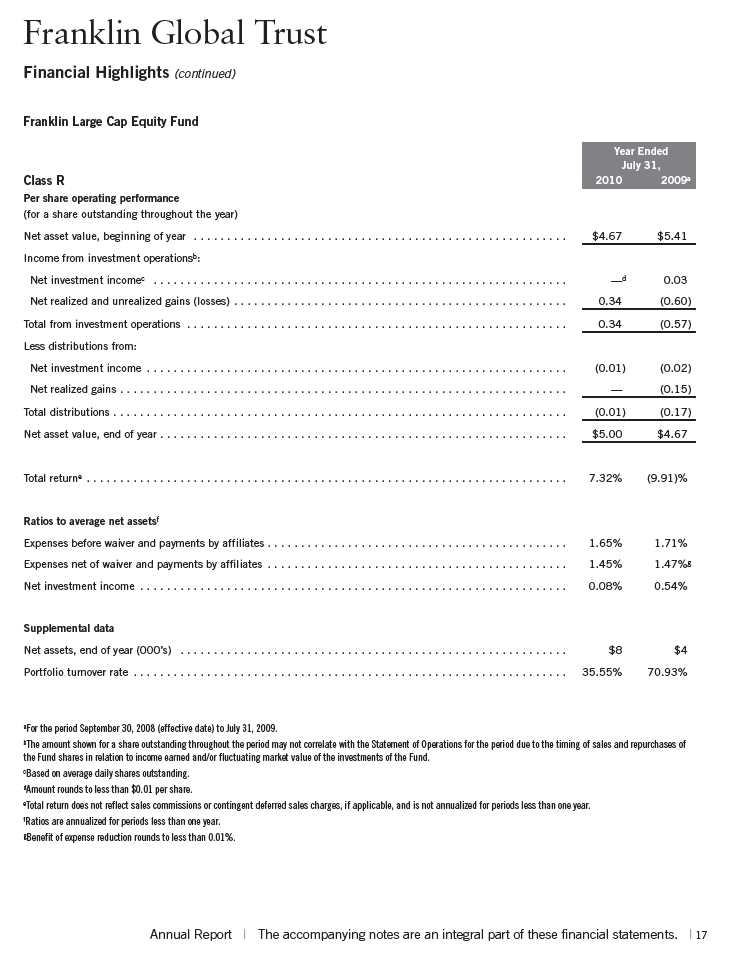

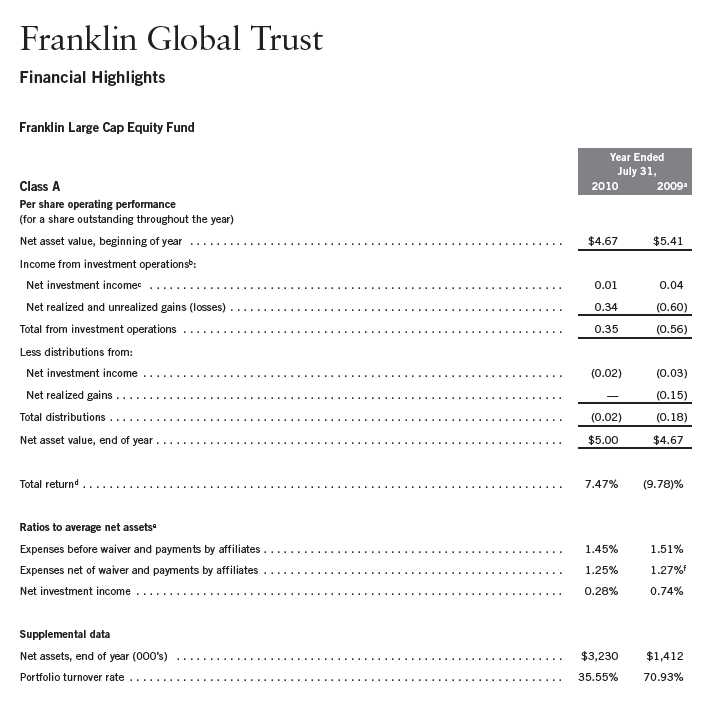

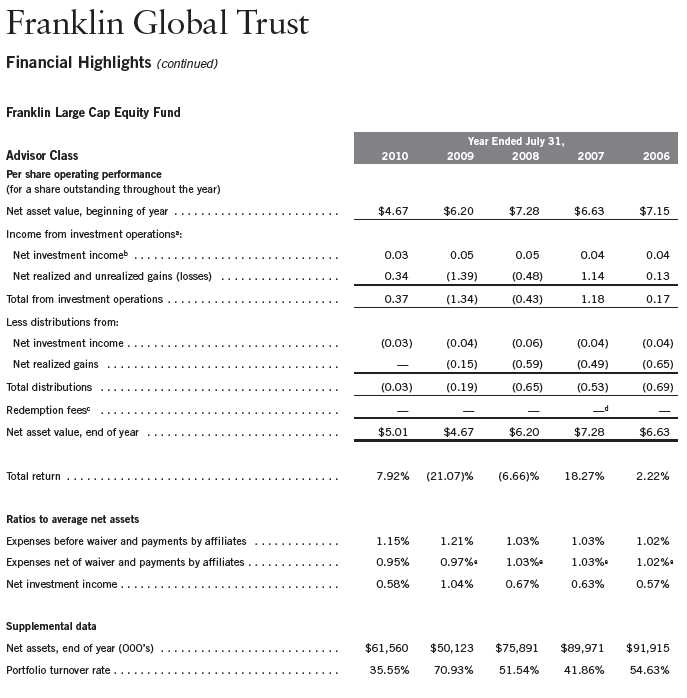

aFor the period September 30, 2008 (effective date) to July 31, 2009. bThe amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and repurchases of the Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund. cBased on average daily shares outstanding. dTotal return does not reflect sales commissions or contingent deferred sales charges, if applicable, and is not annualized for periods less than one year. eRatios are annualized for periods less than one year. fBenefit of expense reduction rounds to less than 0.01%.

Annual Report | The accompanying notes are an integral part of these financial statements. | 15

16 | The accompanying notes are an integral part of these financial statements. | Annual Report

18 | The accompanying notes are an integral part of these financial statements. | Annual Report

| | | | |

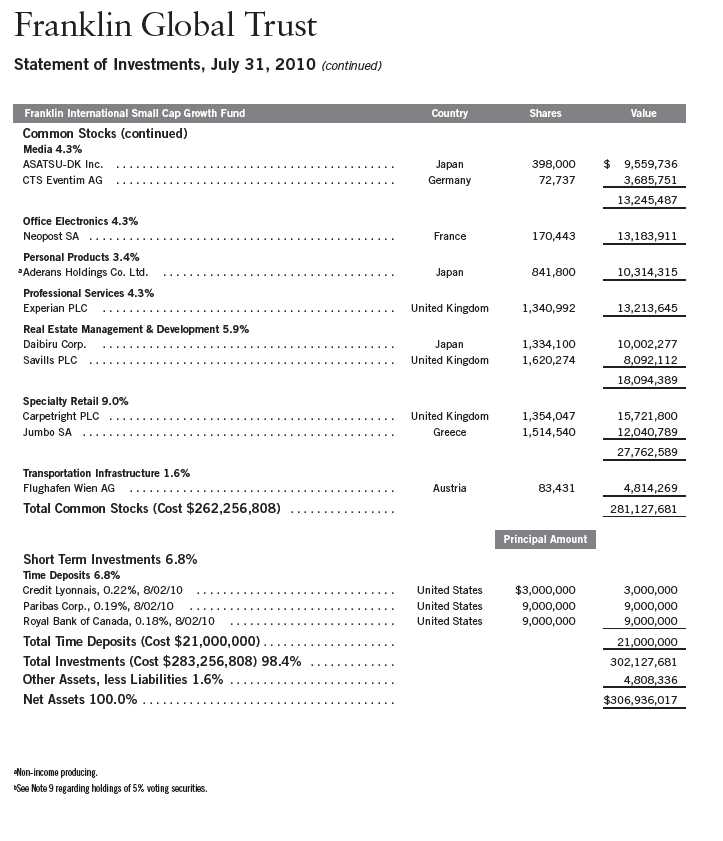

| Franklin Global Trust | | | | |

| |

| Statement of Investments, July 31, 2010 | | | | |

| |

| Franklin Large Cap Equity Fund | Country | Shares | | Value |

| Common Stocks 90.5% | | | | |

| Aerospace & Defense 5.4% | | | | |

| General Dynamics Corp. | United States | 14,200 | $ | 869,751 |

| Precision Castparts Corp. | United States | 11,200 | | 1,368,528 |

| United Technologies Corp. | United States | 18,300 | | 1,301,130 |

| | | | | 3,539,409 |

| Auto Components 2.2% | | | | |

| aBorgWarner Inc. | United States | 32,700 | | 1,434,222 |

| Automobiles 1.8% | | | | |

| bHyundai Motor Co., GDR, Reg S | South Korea | 55,000 | | 1,142,900 |

| Beverages 4.6% | | | | |

| Diageo PLC, ADR | United Kingdom | 17,500 | | 1,222,900 |

| aHansen Natural Corp. | United States | 16,800 | | 703,752 |

| PepsiCo Inc. | United States | 16,700 | | 1,083,997 |

| | | | | 3,010,649 |

| Biotechnology 4.2% | | | | |

| aCelgene Corp. | United States | 23,100 | | 1,273,965 |

| aGilead Sciences Inc. | United States | 43,800 | | 1,459,416 |

| | | | | 2,733,381 |

| Capital Markets 3.5% | | | | |

| BlackRock Inc. | United States | 7,700 | | 1,212,673 |

| Invesco Ltd. | United States | 53,700 | | 1,049,298 |

| | | | | 2,261,971 |

| Chemicals 2.9% | | | | |

| Air Products and Chemicals Inc. | United States | 14,100 | | 1,023,378 |

| The Mosaic Co. | United States | 17,600 | | 838,640 |

| | | | | 1,862,018 |

| Commercial Banks 2.2% | | | | |

| Wells Fargo & Co. | United States | 52,900 | | 1,466,917 |

| Communications Equipment 3.4% | | | | |

| aCisco Systems Inc. | United States | 56,200 | | 1,296,534 |

| QUALCOMM Inc. | United States | 24,400 | | 929,152 |

| | | | | 2,225,686 |

| Computers & Peripherals 4.4% | | | | |

| aApple Inc. | United States | 5,600 | | 1,440,600 |

| aEMC Corp. | United States | 71,700 | | 1,418,943 |

| | | | | 2,859,543 |

| Distributors 1.8% | | | | |

| Li & Fung Ltd. | Hong Kong | 253,500 | | 1,165,097 |

| Diversified Financial Services 2.3% | | | | |