| Three months ended | | Twelve months ended |

SELECTED FINANCIAL RESULTS | December 31, | | December 31, |

| | 2016 | | 2015 | | | 2016 | | 2015 |

Financial (000’s) | | | | | | | | | | | | | |

Adjusted Funds Flow(4) | $ | | 107,730 | | $ | 102,674 | | | $ | 305,605 | | $ | 493,101 |

Dividends to Shareholders | | | 7,214 | | | 22,717 | | | | 35,439 | | | 131,955 |

Net Income/(Loss) | | | 840,325 | | | (624,987) | | | | 397,416 | | | (1,523,403) |

Debt Outstanding, net of Cash and Restricted Cash | | | 375,520 | | | 1,216,184 | | | | 375,520 | | | 1,216,184 |

Capital Spending | | | 57,462 | | | 89,490 | | | | 209,135 | | | 493,403 |

Property and Land Acquisitions | | | 118,452 | | | 8,794 | | | | 126,126 | | | 9,552 |

Property Divestments | | | 389,750 | | | 83,236 | | | | 670,364 | | | 286,614 |

Debt to Adjusted Funds Flow Ratio(4) | | | 1.2x | | | 2.5x | | | | 1.2x | | | 2.5x |

| | | | | | | | | | | | | |

Financial per Weighted Average Shares Outstanding | | | | | | | | | | | | | |

Net Income/(Loss) - Basic | | $ | 3.49 | | $ | (3.03) | | | $ | 1.75 | | $ | (7.39) |

Net Income/(Loss) - Diluted | | | 3.43 | | | (3.03) | | | | 1.72 | | | (7.39) |

Weighted Average Number of Shares Outstanding (000’s) | | | 240,483 | | | 206,517 | | | | 226,530 | | | 206,205 |

| | | | | | | | | | | | | |

Selected Financial Results per BOE(1)(2) | | | | | | | | | | | | | |

Oil & Natural Gas Sales(3) | | $ | 32.81 | | $ | 23.81 | | | $ | 25.88 | | $ | 27.07 |

Royalties and Production Taxes | | | (7.60) | | | (4.75) | | | | (5.77) | | | (5.63) |

Commodity Derivative Instruments | | | 1.12 | | | 7.50 | | | | 2.36 | | | 7.40 |

Cash Operating Expenses | | | (7.22) | | | (8.68) | | | | (7.31) | | | (8.75) |

Transportation Costs | | | (3.44) | | | (2.98) | | | | (3.14) | | | (2.95) |

General and Administrative Expenses | | | (1.63) | | | (1.75) | | | | (1.75) | | | (2.09) |

Cash Share-Based Compensation | | | (0.17) | | | 0.16 | | | | (0.09) | | | (0.02) |

Interest, Foreign Exchange and Other Expenses | | | (0.97) | | | (2.94) | | | | (1.28) | | | (2.78) |

Current Tax Recovery | | | 0.26 | | | 0.07 | | | | 0.07 | | | 0.43 |

| | | | | | | | | | | | | |

Adjusted Funds Flow(4) | | $ | 13.16 | | $ | 10.44 | | | $ | 8.97 | | $ | 12.68 |

| | | | | | | | | | | | | |

| Three months ended | | Twelve months ended |

SELECTED OPERATING RESULTS | December 31, | | December 31, |

| | 2016 | | 2015 | | | 2016 | | 2015 |

Average Daily Production(2) | | | | | | | | | | | | | |

Crude Oil (bbls/day) | | | 37,128 | | | 41,135 | | | | 38,353 | | | 41,639 |

Natural Gas Liquids (bbls/day) | | | 4,413 | | | 5,092 | | | | 4,903 | | | 4,763 |

Natural Gas (Mcf/day) | | | 284,515 | | | 364,065 | | | | 299,214 | | | 360,733 |

Total (BOE/day) | | | 88,960 | | | 106,905 | | | | 93,125 | | | 106,524 |

| | | | | | | | | | | | | |

% Crude Oil and Natural Gas Liquids | | | 47% | | | 43% | | | | 46% | | | 44% |

| | | | | | | | | | | | | |

Average Selling Price(2)(3) | | | | | | | | | | | | | |

Crude Oil (per bbl) | | $ | 53.91 | | $ | 43.04 | | | $ | 44.84 | | $ | 48.43 |

Natural Gas Liquids (per bbl) | | | 21.31 | | | 16.61 | | | | 15.29 | | | 18.06 |

Natural Gas (per Mcf) | | | 2.89 | | | 1.89 | | | | 2.06 | | | 2.15 |

| | | | | | | | | | | | | |

Net Wells Drilled | | | 5 | | | 2 | | | | 25 | | | 46 |

| | | | | | | | | | | | | |

| (1) | | Non‑cash amounts have been excluded. |

| (2) | | Based on Company interest production volumes. See “Basis of Presentation” section in the following MD&A. |

| (3) | | Before transportation costs, royalties and commodity derivative instruments. |

| (4) | | These non‑GAAP measures may not be directly comparable to similar measures presented by other entities. See “Non‑GAAP Measures” section in the following MD&A. |

ENERPLUS 2016 FINANCIAL SUMMARY 1

| | | | | | | | | | | | | |

| Three months ended | | Twelve months ended |

| December 31, | | December 31, |

Average Benchmark Pricing | | 2016 | | 2015 | | | 2016 | | 2015 |

WTI crude oil (US$/bbl) | | $ | 49.29 | | $ | 42.18 | | | $ | 43.32 | | $ | 48.80 |

AECO natural gas – monthly index (CDN$/Mcf) | | | 2.81 | | | 2.65 | | | | 2.09 | | | 2.77 |

AECO natural gas – daily index (CDN$/Mcf) | | | 3.09 | | | 2.47 | | | | 2.16 | | | 2.69 |

NYMEX natural gas – last day (US$/Mcf) | | | 2.98 | | | 2.27 | | | | 2.46 | | | 2.66 |

US/CDN average exchange rate | | | 1.33 | | | 1.34 | | | | 1.32 | | | 1.28 |

| | | | | | |

Share Trading Summary | | CDN(1) – ERF | | U.S.(2) – ERF |

For the twelve months ended December 31, 2016 | | (CDN$) | | (US$) |

High | | $ | 13.55 | | $ | 10.33 |

Low | | $ | 2.68 | | $ | 1.84 |

Close | | $ | 12.74 | | $ | 9.48 |

(1) TSX and other Canadian trading data combined.

(2) NYSE and other U.S. trading data combined.

| | | | |

2016 Dividends per Share | | CDN$ | | US$(1) |

First Quarter Total | $ | 0.09 | $ | 0.07 |

Second Quarter Total | $ | 0.03 | $ | 0.02 |

Third Quarter Total | $ | 0.03 | $ | 0.02 |

Fourth Quarter Total | $ | 0.03 | $ | 0.02 |

Total Year to Date | $ | 0.18 | $ | 0.13 |

| (1) | | CDN$ dividends converted at the relevant foreign exchange rate on the payment date. |

2 ENERPLUS 2016 FINANCIAL SUMMARY

Financial and Operational Highlights

| · | | Fourth quarter 2016 production averaged 88,960 BOE per day, bringing annual average 2016 production to 93,125 BOE per day, in line with guidance of 93,000 BOE per day. Fourth quarter 2016 crude oil and natural gas liquids production averaged 41,541 barrels per day, impacted by severe weather in North Dakota during the quarter. Annual average 2016 liquids production was 43,256 barrels per day, within the guidance range of 43,000 to 44,000 barrels per day. |

| · | | Enerplus realized strong value from its non-core divestments in 2016, selling 13,500 BOE per day (60% natural gas) of production for aggregate proceeds of $670.4 million. |

| · | | The Company reported fourth quarter 2016 net income of $840.3 million, or $3.43 per diluted share. Net income was impacted by a gain on the sale of the Company’s non-operated North Dakota properties of $339.4 million, and a non-cash deferred tax recovery of $567.8 million primarily as a result of the reversal of a portion of the valuation allowance on the Company’s deferred tax asset. For the year ended December 31, 2016, Enerplus reported net income of $397.4 million, or $1.72 per diluted share, compared with a net loss of $1,523.4 million, or $7.39 per share, for the comparable 2015 period. |

| · | | Enerplus generated fourth quarter 2016 adjusted funds flow of $107.7 million, an increase of 34% from the previous quarter as a result of stronger commodity prices in the fourth quarter. The Company generated full year 2016 adjusted funds flow of $305.6 million, down 38% from the comparable 2015 period due to lower average commodity prices and lower hedging gains in 2016. |

| · | | Enerplus delivered strong operating cost performance in 2016 reflecting efficiency improvements and the divestment of higher cost properties. Fourth quarter operating expenses were $7.15 per BOE, a reduction of 18% compared to the same period in 2015. Full year 2016 operating expenses were $7.27 per BOE, a reduction of 17% compared to 2015. |

| · | | Fourth quarter 2016 cash G&A expenses were $1.63 per BOE, a reduction of 7% compared to the same period in 2015. Full year 2016 cash G&A expenses were $1.75 per BOE, a reduction of 16% compared to 2015. Enerplus’ lower G&A cost structure is, in part, a result of a reduction in staffing levels related to non-core asset divestments. |

| · | | Transportation expense in the fourth quarter of 2016 was $3.44 per BOE, up slightly from the previous quarter. Full year 2016 transportation expense was $3.14 per BOE, a 6% increase from the prior year period. |

| · | | Capital spending in the fourth quarter of 2016 was $57.5 million, with approximately 71% allocated to North Dakota. Full year 2016 capital spending totaled $209.1 million, slightly below annual 2016 guidance of $215.0 million. |

| · | | Enerplus significantly strengthened its balance sheet during 2016 having reduced its total debt, net of cash and restricted cash, by 69%, or $840.7 million, over the twelve-month period. Total debt, net of cash and restricted cash, at December 31, 2016 was $375.5 million, and was comprised of $23.2 million of bank indebtedness and $745.6 million of senior notes less $393.3 million in cash, including $392.0 million in restricted cash. The restricted cash balance reflects proceeds from the sale of the Company’s non-operated North Dakota properties which were placed in escrow in order to facilitate possible future like-kind transactions in accordance with U.S. federal tax regulations. Net debt to adjusted funds flow at year-end was 1.2 times. |

Reserves Highlights

| · | | Replaced 126% of 2016 production, adding 42.6 MMBOE (42% crude oil and natural gas liquids) of proved plus probable (“2P”) reserves from development activities (including revisions). |

| · | | Material reserves growth was realized in Enerplus’ North Dakota and Marcellus assets. The Company replaced 207% of 2016 North Dakota production, excluding production from Enerplus’ non-operated North Dakota assets which were sold at the end of 2016, adding 17.5 MMBOE of 2P reserves (including revisions). The Company also replaced 175% of 2016 Marcellus production, adding 125.0 Bcf of 2P reserves (including revisions). |

| · | | Finding and development (“F&D”) costs for proved developed producing (“PDP”) reserves decreased by 60% to $4.77 per BOE for 2016, generating a PDP reserves recycle ratio of 2.0 times based on a 2016 operating netback (before hedging) of $9.66 per BOE. Enerplus’ three-year average PDP reserves F&D cost was $10.37 per BOE. |

ENERPLUS 2016 FINANCIAL SUMMARY 3

| · | | F&D costs for 2P reserves decreased by 43% to $4.82 per BOE for 2016, including future development costs (“FDC”), generating a 2P reserves recycle ratio of 2.0 times. Enerplus’ three-year average 2P reserves F&D cost, including FDC, was $8.11 per BOE. |

| · | | Enerplus sold various non-core properties in 2016 representing 37.3 MMBOE of 2P reserves at a combined value of $20.38 per BOE. Total 2P reserves, net of divestments, were 382.5 MMBOE at year-end 2016, representing a 6% decrease from year-end 2015. Excluding acquisitions and divestments, 2P reserves increased by 2% in 2016. |

| · | | 2P reserves were comprised of 51% crude oil and natural gas liquids and 49% natural gas at year-end 2016. |

| · | | Total proved reserves account for 70% of 2P reserves. PDP reserves represent 71% of total proved reserves and 50% of 2P reserves. |

4 ENERPLUS 2016 FINANCIAL SUMMARY

EXHIBIT 99.3

Management’s Discussion and Analysis (“MD&A”)

The following discussion and analysis of financial results is dated February 23, 2017 and is to be read in conjunction with the audited Consolidated Financial Statements (the “Financial Statements”) of Enerplus Corporation (“Enerplus” or the “Company”), as at December 31, 2016 and 2015 and for the years ended December 31, 2016, 2015 and 2014.

The following MD&A contains forward-looking information and statements. We refer you to the end of the MD&A under “Forward‑Looking Information and Statements” for further information. The following MD&A also contains financial measures that do not have a standardized meaning as prescribed by accounting principles generally accepted in the United States of America (“U.S. GAAP”). See “Non‑GAAP Measures” at the end of this MD&A for further information.

BASIS OF PRESENTATION

The Financial Statements and notes have been prepared in accordance with U.S. GAAP, including the prior period comparatives. All amounts are stated in Canadian dollars unless otherwise specified and all note references relate to the notes included with the Financial Statements. Certain prior period amounts have been restated to conform with current period presentation.

Where applicable, natural gas has been converted to barrels of oil equivalent (“BOE”) based on 6 Mcf:1 BOE and oil and natural gas liquids (“NGL”) have been converted to thousand cubic feet of gas equivalent (“Mcfe”) based on 0.167 bbl:1 Mcfe. The BOE and Mcfe rates are based on an energy equivalent conversion method primarily applicable at the burner tip and do not represent a value equivalent at the wellhead. Given that the value ratio based on the current price of natural gas as compared to crude oil is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value. Use of BOE and Mcfe in isolation may be misleading. All production volumes are presented on a company interest basis, being the Company’s working interest share before deduction of any royalties paid to others, plus the Company’s royalty interests, unless otherwise stated. Company interest is not a term defined in Canadian National Instrument 51‑101– Standards of Disclosure for Oil and Gas Activities (“NI 51‑101”) and may not be comparable to information produced by other entities.

In accordance with U.S. GAAP, oil and natural gas sales are presented net of royalties in the Financial Statements. Under International Financial Reporting Standards, industry standard is to present oil and natural gas sales before deduction of royalties and as such this MD&A presents production, oil and natural gas sales, and BOE measures before deduction of royalties to remain comparable with our peers.

The following table provides a reconciliation of our production volumes:

| | | | | | |

| | Year ended December 31, |

Average Daily Production Volumes | 2016 | 2015 | 2014 |

Company interest production volumes | | | | | | |

Crude oil (bbls/day) | | 38,353 | | 41,639 | | 40,208 |

Natural gas liquids (bbls/day) | | 4,903 | | 4,763 | | 3,565 |

Natural gas (Mcf/day) | | 299,214 | | 360,733 | | 356,142 |

Company interest production volumes (BOE/day) | | 93,125 | | 106,524 | | 103,130 |

| | | | | | |

Royalty volumes | | | | | | |

Crude oil (bbls/day) | | 7,198 | | 7,471 | | 7,731 |

Natural gas liquids (bbls/day) | | 932 | | 971 | | 775 |

Natural gas (Mcf/day) | | 50,270 | | 59,077 | | 55,114 |

Royalty volumes (BOE/day) | | 16,508 | | 18,288 | | 17,692 |

| | | | | | |

Net production volumes | | | | | | |

Crude oil (bbls/day) | | 31,155 | | 34,168 | | 32,477 |

Natural gas liquids (bbls/day) | | 3,971 | | 3,792 | | 2,790 |

Natural gas (Mcf/day) | | 248,944 | | 301,656 | | 301,028 |

Net production volumes (BOE/day) | | 76,617 | | 88,236 | | 85,438 |

ENERPLUS 2016 FINANCIAL SUMMARY 5

2016 FOURTH QUARTER OVERVIEW

Fourth quarter production averaged 88,960 BOE/day, in line with our target of 89,000 BOE/day, and a decrease of 3,117 BOE/day compared to third quarter production of 92,077 BOE/day. In the U.S. production during the fourth quarter was impacted by approximately 1,700 BOE/day of price related curtailments in the Marcellus and fewer on-streams in North Dakota along with severe winter weather. Canadian production was consistent with the prior quarter, with production from our November asset acquisition of a Canadian waterflood property offsetting price related shut-ins and minor non-core asset divestments. Operating costs increased somewhat in the fourth quarter, to $58.5 million or $7.15/BOE from $56.2 million or $6.64/BOE in the third quarter, due to additional weather related costs in December.

We reported net income of $840.3 million and adjusted funds flow of $107.7 million in the fourth quarter compared to a net loss of $100.7 million and adjusted funds flow of $80.1 million in the third quarter. Both net income and adjusted funds flow benefited from a $29.1 million or 15% increase in net oil and natural gas sales compared to the third quarter, with improved pricing offsetting the impact of lower production volumes. Net income also increased as a result of a non-cash deferred tax recovery of $567.8 million due to the reversal of a portion of the valuation allowance on our deferred tax asset and a $339.4 million gain on the sale of non-operated North Dakota properties.

On November 15, 2016, we closed the previously announced purchase of a Canadian waterflood property for proceeds of $110.3 million.

On December 30, 2016, we closed the previously announced sale of our non-operated North Dakota properties with production of approximately 5,000 BOE/day for proceeds of $392.0 million.

Selected Fourth Quarter Canadian and U.S. Financial Results

| | | | | | | | | | | | | | | | | | | |

| | Three months ended | | | Three months ended |

| | December 31, 2016 | | | December 31, 2015 |

(millions, except per unit amounts) | | Canada | | U.S. | | Total | | | Canada | | U.S. | | Total |

Average Daily Production Volumes(1) | | | | | | | | | | | | | | | | | | | |

Crude oil (bbls/day) | | | 12,417 | | | 24,711 | | | 37,128 | | | | 13,790 | | | 27,345 | | | 41,135 |

Natural gas liquids (bbls/day) | | | 1,160 | | | 3,253 | | | 4,413 | | | | 1,771 | | | 3,321 | | | 5,092 |

Natural gas (Mcf/day) | | | 68,437 | | | 216,078 | | | 284,515 | | | | 135,898 | | | 228,167 | | | 364,065 |

Total average daily production (BOE/day) | | | 24,983 | | | 63,977 | | | 88,960 | | | | 38,210 | | | 68,695 | | | 106,905 |

| | | | | | | | | | | | | | | | | | | |

Pricing(2) | | | | | | | | | | | | | | | | | | | |

Crude oil (per bbl) | | $ | 48.44 | | $ | 56.66 | | $ | 53.91 | | | $ | 38.11 | | $ | 45.53 | | $ | 43.04 |

Natural gas liquids (per bbl) | | | 36.33 | | | 15.96 | | | 21.31 | | | | 28.77 | | | 10.13 | | | 16.61 |

Natural gas (per Mcf) | | | 3.13 | | | 2.82 | | | 2.89 | | | | 2.46 | | | 1.55 | | | 1.89 |

Capital Expenditures | | | | | | | | | | | | | | | | | | | |

Capital spending | | $ | 10.2 | | $ | 47.3 | | $ | 57.5 | | | $ | 26.8 | | $ | 62.7 | | $ | 89.5 |

Acquisitions | | | 111.2 | | | 7.2 | | | 118.4 | | | | 0.7 | | | 8.1 | | | 8.8 |

Divestments | | | (1.5) | | | (388.3) | | | (389.8) | | | | 0.9 | | | (84.1) | | | (83.2) |

Netback(3) Before Hedging | | | | | | | | | | | | | | | | | | | |

Oil and natural gas sales | | $ | 78.9 | | $ | 189.7 | | $ | 268.6 | | | $ | 84.0 | | $ | 150.2 | | $ | 234.2 |

Royalties | | | (11.0) | | | (40.1) | | | (51.1) | | | | (9.0) | | | (25.8) | | | (34.8) |

Production taxes | | | (0.4) | | | (10.6) | | | (11.0) | | | | (1.5) | | | (10.5) | | | (12.0) |

Cash operating expenses | | | (30.7) | | | (28.4) | | | (59.1) | | | | (54.4) | | | (30.9) | | | (85.3) |

Transportation costs | | | (3.2) | | | (25.0) | | | (28.2) | | | | (5.2) | | | (24.1) | | | (29.3) |

| | | | | | | | | | | | | | | | | | | |

Netback before hedging | | $ | 33.6 | | $ | 85.6 | | $ | 119.2 | | | $ | 13.9 | | $ | 58.9 | | $ | 72.8 |

| | | | | | | | | | | | | | | | | | | |

Other Expenses | | | | | | | | | | | | | | | | | | | |

Commodity derivative instruments loss/(gain) | | $ | 33.0 | | $ | — | | $ | 33.0 | | | $ | (31.1) | | $ | — | | $ | (31.1) |

General and administrative expense(4) | | | 21.0 | | | 7.0 | | | 28.0 | | | | 10.4 | | | 8.1 | | | 18.5 |

Current income tax recovery | | | — | | | (2.1) | | | (2.1) | | | | (0.4) | | | (0.3) | | | (0.7) |

(1)Company interest volumes.

(2)Before transportation costs, royalties and the effects of commodity derivative instruments.

(3)See “Non‑GAAP Measures” section in this MD&A.

(4)Includes share‑based compensation.

6 ENERPLUS 2016 FINANCIAL SUMMARY

Comparing the fourth quarter of 2016 with the same period in 2015:

| · | | Average daily production was 88,960 BOE/day, down 17% or approximately 17,945 BOE/day from 106,905 BOE/day in 2015 primarily due to our non-core Canadian asset divestments and lower capital spending. |

| · | | Despite a significant reduction in capital spending, U.S. production declined only modestly over the period as a result of strong well performance. This was offset somewhat by the divestment of 1,000 BOE/day of our non-operated North Dakota properties during the fourth quarter of 2015. U.S. crude oil production decreased 10% or 2,634 BOE/day from the fourth quarter of 2016 to the fourth quarter of 2015, while natural gas production decreased 5% or 2,015 BOE/day over the same period. |

| · | | Capital spending decreased to $57.5 million compared to $89.5 million in the fourth quarter of 2015. The majority of our capital investment in the fourth quarter was focused on our core areas, with spending of $41.1 million on our North Dakota crude oil properties, $10.2 million on our Canadian crude oil waterflood properties and $4.2 million on our Marcellus natural gas properties. |

| · | | Operating expenses decreased to $58.5 million ($7.15/BOE) compared to $85.6 million ($8.71/BOE) in the fourth quarter of 2015 as a result of ongoing cost efficiencies and the divestment of higher operating cost Canadian properties throughout 2016. |

| · | | Cash general and administrative (“G&A”) expenses decreased to $13.4 million ($1.63/BOE) compared to $17.2 million ($1.75/BOE) in 2015 due to reductions in staffing levels and the success of our ongoing cost saving initiatives. |

| · | | We reported net income of $840.3 million in the fourth quarter of 2016 compared to a net loss of $625.0 million in the fourth quarter of 2015. The improvement year over year was primarily the result of a non-cash deferred tax recovery of $567.8 million due to the reversal of a portion of our valuation allowance on our deferred tax asset, compared to a non-cash deferred tax provision of $294.4 million on our deferred tax asset in the same period of 2015. Net income also benefitted from a gain of $339.4 million on the sale of our non-operated North Dakota property and a $221.0 million decrease in the non-cash impairment charge on our crude oil and natural gas assets compared to the fourth quarter of 2015. |

| · | | Adjusted funds flow increased to $107.7 million compared to $102.7 million in the fourth quarter of 2015. The increase in adjusted funds flow was a result of significantly higher commodity prices, which were offset in part by lower production volumes and a $64.1 million decrease in cash gains on commodity hedges. |

2016 OVERVIEW AND 2017 OUTLOOK

| | | | | | | | | |

| | | | | | | | | |

Summary of Guidance and Results | | Original 2016 Guidance | | Revised 2016 Guidance | | 2016 Results | | 2017 Guidance | |

Capital spending ($ millions) | | $ 200 | | $ 215 | | $ 209 | | $ 450 | |

Average annual production (BOE/day) | | 90,000 - 94,000 | | 93,000 | | 93,125 | | 86,000 – 90,000 | |

Crude oil and natural gas liquids volumes (bbls/day) | | 43,000 - 45,000 | | 43,000 - 44,000 | | 43,256 | | 40,000 – 43,000 | |

Average royalty and production tax rate (% of oil and natural gas sales) | | 23% | | 22% | | 22% | | 23% | |

Operating expenses (per BOE) | | $ 9.50 | | $ 7.50 | | $ 7.27 | | $ 7.85 | |

Transportation costs (per BOE) | | $ 3.30 | | $ 3.15 | | $ 3.14 | | $ 3.90 | |

Cash G&A expenses (per BOE) | | $ 2.10 | | $ 1.80 | | $ 1.75 | | $ 1.80 | |

| | | | | | | | | |

2016 Overview

We improved our financial position in 2016 despite the weakness and volatility in commodity prices. We achieved this through ongoing cost reductions, strong operational results, a disciplined capital program and a successful non-core asset divestment program.

Average annual production was 93,125 BOE/day, consistent with our guidance of 93,000 BOE/day. Crude oil and liquids volumes were 43,256 bbls/day, within our guidance range of 43,000 – 44,000 bbls/day.

ENERPLUS 2016 FINANCIAL SUMMARY 7

Our capital spending for the year totaled $209.1 million, slightly below our guidance of $215 million due to weather related deferrals of spending in the fourth quarter.

Operating expenses and cash G&A expenses came in under our guidance, at $7.27/BOE and $1.75/BOE, respectively, compared to guidance of $7.50/BOE and $1.80/BOE, respectively. The outperformance was a result of our ongoing cost saving initiatives and our continued effort to focus our business through the sale of higher cost, non-core assets.

Net income for 2016 was $397.4 million, a significant increase from our net loss of $1,523.4 million in 2015 primarily due to a $1,051.3 million decrease in non-cash asset impairments, along with $578.5 million in realized gains on asset divestments and senior note prepayments.

Adjusted funds flow decreased 38% to $305.6 million in 2016 from $493.1 million in 2015. This was due to a $161.7 million decrease in net oil and gas sales over the period as a result of lower production volumes and weaker commodity prices, along with a $207.4 million decrease in realized gains on commodity hedges. These reductions were offset by significant cost savings in operating, interest and cash G&A expenses.

We continued to focus our portfolio during 2016, divesting of certain non-operated crude oil assets in the U.S. and lower margin crude oil and natural gas assets in Canada for aggregate proceeds of $670.4 million. These assets had associated production of approximately 13,500 BOE/day.

On May 31, 2016, we completed an equity financing of 33,350,000 common shares at a price of $6.90 per share for gross proceeds of $230.1 million ($220.4 million net of issue costs).

Proceeds from both the asset divestments and equity financing were used to reduce our total debt, net of cash and restricted cash, by 69% or $840.7 million compared to the prior year. Net debt at December 31, 2016 was $375.5 million, comprised of $23.2 million of bank indebtedness and $745.6 million of senior notes less $393.3 million in cash and restricted cash. At December 31, 2016, we were approximately 3% drawn on our $800 million senior unsecured bank credit facility.

2017 Outlook

Our focus for 2017 is to deliver profitable growth and generate strong returns on capital while maintaining our balance sheet strength. Accordingly, we have increased our capital budget for 2017 to $450 million, with the majority directed to our North Dakota crude oil properties. We expect this spending level to generate significant liquids growth, with a 25% increase in liquids production from the beginning of 2017 to the fourth quarter of 2017, driven by 50% growth in our total North Dakota production over the same period.

Annual 2017 production is expected to average between 86,000 – 90,000 BOE/day, with crude oil and natural gas liquids production expected to average between 40,000 – 43,000 bbls/day. Following a limited completions program in North Dakota in the fourth quarter of 2016, capital spending is forecast to begin to ramp-up in the first half of 2017, driving strong liquids production growth in the back half of the year. Total fourth quarter production is expected to average 92,000 – 97,000 BOE/day, with a fourth quarter liquids production target of 45,000 - 50,000 bbls/day.

To support our 2017 capital program, we have increased our 2017 crude oil hedging program to 63% of our forecast crude oil production volumes, after royalties, and 23% of our natural gas production, after royalties. We have also added crude oil hedges in 2018 and 2019 on approximately 44% and 14%, respectively, based on our forecasted 2017 net crude oil production.

Operating expenses are expected to average approximately $7.85/BOE in 2017, modestly higher than 2016 levels as we expect to increase our corporate weighting of liquids production in 2017.

We expect cash G&A expenses in 2017 to average approximately $1.80/BOE. Although we expect total costs to decrease year over year, our per BOE expenses will remain flat due to lower production volumes.

Transportation costs are expected to average $3.90/BOE in 2017, an increase from 2016 levels. The increase is largely attributable to additional firm transportation commitments in the Marcellus that came into effect in August 2016 that deliver to higher priced markets, along with lower production volumes due to the non-operated year-end 2016 divestment and a weaker Canadian dollar projected in 2017 compared to 2016.

8 ENERPLUS 2016 FINANCIAL SUMMARY

RESULTS OF OPERATIONS

Production

| | | | | | | | | |

Average Daily Production Volumes | | | 2016 | | | 2015 | | | 2014 |

Crude oil (bbls/day) | | | 38,353 | | | 41,639 | | | 40,208 |

Natural gas liquids (bbls/day) | | | 4,903 | | | 4,763 | | | 3,565 |

Natural gas (Mcf/day) | | | 299,214 | | | 360,733 | | | 356,142 |

Total daily sales (BOE/day) | | | 93,125 | | | 106,524 | | | 103,130 |

Production in 2016 averaged 93,125 BOE/day, in line with our guidance of 93,000 BOE/day. Crude oil and liquids volumes were 43,256 bbls/day, within our guidance range of 43,000 – 44,000 bbls/day. The 13% decrease in average production compared to the prior year was primarily due to the sale of non-core properties during the fourth quarter of 2015 and throughout the first three quarters of 2016 with associated production of approximately 11,800 BOE/day, and our reduced capital spending program compared to the prior year.

Our U.S. production decreased a modest 2% compared to 2015 despite our reduced capital spending. The decrease was primarily due to a 1,200 BOE/day or 4% reduction in Marcellus natural gas production due to lower investment and price related production curtailments during the year. In North Dakota, strong production from our crude oil properties offset the impact of decline and the fourth quarter 2015 sale of a portion of our non-operated properties.

Canadian production volumes decreased 12,310 BOE/day or 31% compared to the prior year, largely due to asset divestments. Price related shut-ins and asset declines also impacted Canadian production, but were offset somewhat by our November, 2016 acquisition of a Canadian waterflood property.

Our crude oil and natural gas liquids production accounted for 46% of our total average daily production in 2016, compared to 44% in 2015.

In 2015, production increased 3% over 2014 to average 106,524 BOE/day. Crude oil production increased 4% from the prior year due to 6,000 BOE/day or 28% growth in our North Dakota crude oil volumes. Our natural gas production was relatively consistent with 2014 at 360,733 Mcf/day, with 8% growth in our Marcellus production offset by decline in Canadian natural gas volumes over the same period.

2017 Guidance

We expect annual average production for 2017 of 86,000 – 90,000 BOE/day, including 40,000 – 43,000 bbls/day of crude oil and natural gas liquids. As a result of our increased capital spending program of $450 million, we expect strong production growth in the second half of the year, with liquids production expected to grow 25% from the beginning of 2017 to the end of the year. Accordingly, we are providing fourth quarter total average production guidance of 92,000 – 97,000 BOE/day and fourth quarter liquids production guidance of 45,000 – 50,000 bbls/day. This guidance includes the full year impact of our 2016 acquisitions and divestments, including the December 30, 2016 sale of 5,000 BOE/day non‑operated North Dakota properties and the November 15, 2016 acquisition of a Canadian waterflood property.

ENERPLUS 2016 FINANCIAL SUMMARY 9

Pricing

The prices received for our crude oil and natural gas production directly impact our earnings, adjusted funds flow and financial condition. The following table summarizes our average selling prices, benchmark prices and differentials:

| | | | | | | | | |

Pricing (average for the period) | | 2016 | | 2015 | | 2014 |

Benchmarks | | | | | | | | | |

WTI crude oil (US$/bbl) | | $ | 43.32 | | $ | 48.80 | | $ | 93.00 |

AECO natural gas – monthly index ($/Mcf) | | | 2.09 | | | 2.77 | | | 4.42 |

AECO natural gas – daily index ($/Mcf) | | | 2.16 | | | 2.69 | | | 4.51 |

NYMEX natural gas – last day (US$/Mcf) | | | 2.46 | | | 2.66 | | | 4.41 |

US/CDN average exchange rate | | | 1.32 | | | 1.28 | | | 1.10 |

US/CDN period end exchange rate | | | 1.34 | | | 1.38 | | | 1.16 |

Enerplus selling price(1) | | | | | | | | | |

Crude oil ($/bbl) | | $ | 44.84 | | $ | 48.43 | | $ | 86.28 |

Natural gas liquids ($/bbl) | | | 15.29 | | | 18.06 | | | 51.72 |

Natural gas ($/Mcf) | | | 2.06 | | | 2.15 | | | 3.94 |

Average differentials | | | | | | | | | |

MSW Edmonton – WTI (US$/bbl) | | $ | (3.21) | | $ | (3.93) | | $ | (7.17) |

WCS Hardisty – WTI (US$/bbl) | | | (13.84) | | | (13.52) | | | (19.40) |

Transco Leidy monthly – NYMEX (US$/Mcf) | | | (1.15) | | | (1.52) | | | (1.95) |

TGP Z4 300L monthly – NYMEX (US$/Mcf) | | | (1.21) | | | (1.58) | | | (2.04) |

AECO monthly – NYMEX (US$/Mcf) | | | (0.89) | | | (0.50) | | | (0.41) |

Enerplus realized differentials(1) | | | | | | | | | |

Canada crude oil – WTI (US$/bbl) | | $ | (13.21) | | $ | (13.34) | | $ | (17.36) |

Canada natural gas – NYMEX (US$/Mcf) | | | (0.80) | | | (0.44) | | | (0.34) |

Bakken crude oil – WTI (US$/bbl) | | | (7.46) | | | (9.44) | | | (12.94) |

Marcellus natural gas – NYMEX (US$/Mcf) | | | (0.93) | | | (1.37) | | | (1.43) |

| (1) | | Before transportation costs, royalties and commodity derivative instruments. |

CRUDE OIL AND NATURAL GAS LIQUIDS

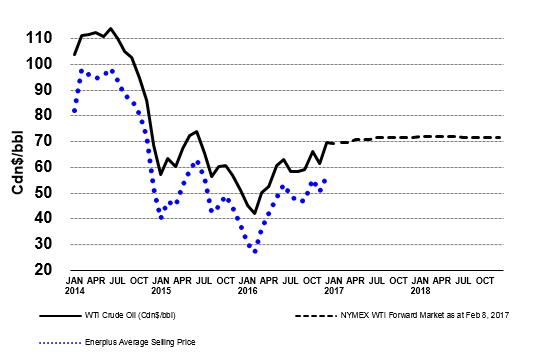

Our realized crude oil price in 2016 averaged $44.84/bbl, a 7% decrease compared to 2015. Benchmark WTI crude oil prices fell by 11% versus 2015 due to the continued oversupply of crude oil in the global markets for most of the year. In the fourth quarter of 2016, the Organization of the Petroleum Exporting Countries (“OPEC”) and certain non-OPEC nations agreed to reduce production by approximately 1.8 million bbls/day through June 2017, which resulted in WTI prices strengthening at the end of the year to US$53.72/bbl.

Our Bakken sales price differential improved by 21% year over year, averaging US$7.46/bbl below WTI due to declining regional production and stronger local refinery demand. With the Dakota Access Pipeline expected to be completed and in service around mid-year 2017, increasing regional takeaway capacity, we are expecting our 2017 Bakken crude oil differential to improve to US$4.50/bbl below WTI, from our previous guidance of US$6.00/bbl below WTI. Canadian light sweet crude prices also improved, resulting in our Canadian realized price differentials to WTI narrowing slightly compared to the prior year.

We realized an average of $15.29/bbl on our natural gas liquids production, which was 15% lower than 2015 and largely in line with changes in underlying crude oil prices.

NATURAL GAS

Our realized natural gas price averaged $2.06/Mcf in 2016, a 4% decrease from 2015 realized prices but considerably stronger than the changes in benchmark prices during the period. NYMEX prices fell by 8% and AECO monthly prices fell by 25% compared to 2015 in response to excess inventories due to a warm winter in early 2016. However, with lower production levels and warmer than average summer temperatures in the U.S., NYMEX prices improved substantially over the course of the year and into 2017. In Alberta, concerns over congestion on regional pipelines due to continued production growth resulted in AECO prices averaging US$0.89/Mcf below NYMEX in 2016 compared to US$0.50/Mcf below NYMEX in 2015. Our overall realized natural gas price outperformed the benchmarks due to much stronger Marcellus basis differentials and the positive impact of our term AECO physical sales with fixed basis differentials at prices much narrower than where AECO basis market prices averaged.

In the Marcellus, the Tennessee Gas Pipeline Zone 4 - 300 Leg and Transco Leidy monthly benchmark differentials averaged US$1.21/Mcf and US$1.15/Mcf below NYMEX compared to US$1.58/Mcf and US$1.52/Mcf below NYMEX in 2015. The strengthening in local Marcellus prices was due to additional pipeline capacity coming into service, as well as higher weather

10 ENERPLUS 2016 FINANCIAL SUMMARY

related demand in the region. Our realized sales price benefitted from August to December 2016 as we began to transport 30,000 Mcf/day of production to markets south of the Marcellus producing region, allowing us to realize sales prices closer to NYMEX pricing. This resulted in an average Marcellus realized sales price differential before transportation costs of US$0.93/Mcf below NYMEX, a 32% improvement from 2015.

We expect our realized Marcellus differentials in 2017 to continue to improve due to further pipeline capacity additions and stronger regional demand alleviating some of the constraints in the region. There is the potential for differentials to widen in certain periods of the year as seasonal demand falls and until sufficient pipeline capacity is built to fully relieve the congestion. We expect our Marcellus natural gas realized differential to average US$0.90/Mcf below NYMEX in 2017.

Monthly Crude Oil Prices

Monthly Natural Gas Prices

FOREIGN EXCHANGE

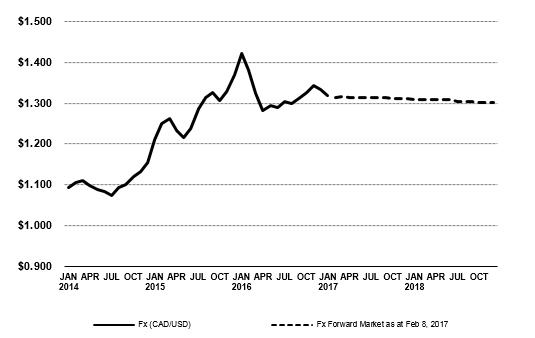

The Canadian dollar was volatile throughout 2016, beginning the year near a thirteen year low of 1.47 USD/CDN and strengthening to 1.25 USD/CDN in late April before closing the year at 1.34 USD/CDN. Overall, the Canadian dollar weakened relative to the U.S. dollar, averaging 1.32 USD/CDN. The majority of our oil and natural gas sales are based on U.S. dollar denominated indices, and a weaker Canadian dollar relative to the U.S. dollar increases the amount of our realized sales. Because we report in Canadian dollars, the weaker Canadian dollar also increases our U.S. dollar denominated costs, capital spending and the cost of our U.S. dollar denominated senior notes.

ENERPLUS 2016 FINANCIAL SUMMARY 11

Monthly USD/CDN Exchange Rate

Price Risk Management

We have a price risk management program that considers our overall financial position, the economics of our capital program and potential acquisitions.

As of February 23, 2017, we have hedged approximately 18,000 bbls/day of our crude oil production for 2017, which represents approximately 63% of our forecasted 2017 crude oil production, after royalties. For 2018, we have hedged 12,500 bbls/day, which represents approximately 44% of our forecasted 2017 crude oil production, after royalties. We have also added hedges through 2019 to protect the long term economics of a portion of our capital program. Our crude oil hedges are predominantly three way collars, which consist of a sold put, a purchased put and a sold call. When WTI prices settle below the sold put strike in any given month, the three way collars provide a limited amount of protection above the WTI index prices equal to the difference between the strike price of the purchased and sold puts. Overall, we continue to expect our crude oil hedge contracts to protect a significant portion of our adjusted funds flow.

As of February 23, 2017, we have hedged approximately 50,000 Mcf/day of our natural gas production for 2017 using NYMEX three way collars. This represents approximately 23% of our 2017 forecasted 2017 natural gas production, after royalties. When NYMEX prices settle below the sold put strike price in any given month, the three way collars provide a limited amount of protection above the NYMEX index prices equal to the value between the strike price of the purchased and sold puts.

12 ENERPLUS 2016 FINANCIAL SUMMARY

The following is a summary of our financial contracts in place at February 23, 2017, expressed as a percentage of our anticipated production volumes, after royalties, for 2017:

| | | | | | | | | | | | | |

| | WTI Crude Oil (US$/bbl)(1) | | NYMEX Natural Gas (US$/Mcf)(1) | |

| | Jan 1, 2017 – | | Jul 1, 2017 – | | Jan 1, 2018 – | | Jan 1, 2019 – | | Apr 1, 2019 – | | Jan 1, 2017 – | |

| | Jun 30, 2017 | | Dec 31, 2017 | | Dec 31, 2018 | | Mar 31, 2019 | | Dec 31, 2019 | | Dec 31, 2017 | |

Swaps | | | | | | | | | | | | | |

Sold Swaps | | $ 53.50 | | $ 53.50 | | $ 53.73 | | $ 53.73 | | - | | - | |

% | | 7% | | 7% | | 11% | | 11% | | - | | - | |

| | | | | | | | | | | | | |

Three Way Collars | | | | | | | | | | | | . | |

Sold Puts | | $ 38.94 | | $ 39.62 | | $ 43.13 | | $ 45.00 | | $ 43.75 | | $ 2.06 | |

% | | 49% | | 63% | | 33% | | 3% | | 14% | | 23% | |

Purchased Puts | | $ 50.29 | | $ 50.61 | | $ 54.00 | | $ 56.00 | | $ 54.69 | | $ 2.75 | |

% | | 49% | | 63% | | 33% | | 3% | | 14% | | 23% | |

Sold Calls | | $ 61.14 | | $ 60.33 | | $ 63.09 | | $ 70.00 | | $ 66.18 | | $ 3.41 | |

% | | 49% | | 63% | | 33% | | 3% | | 14% | | 23% | |

| | | | | | | | | | | | | |

| (1) | | Based on weighted average price (before premiums) assuming average annual production of 88,000 BOE/day for 2017, less royalties and production taxes of 23%. |

We did not have any foreign exchange contracts in place during 2016. In comparison, during 2015, we recorded realized foreign exchange losses of $39.2 million on foreign exchange costless collars and foreign exchange gains of $39.9 million and $3.3 million, respectively, on the unwind of our US$175 million foreign exchange swap and the final settlement of the foreign exchange swap on our US$54 million senior notes.

ACCOUNTING FOR PRICE RISK MANAGEMENT

| | | | | | | | | |

Commodity Risk Management Gains/(Losses) | | | | | | | | | |

($ millions) | | 2016 | | 2015 | | 2014 |

Cash gains/(losses): | | | | | | | | | |

Crude oil | | $ | 75.0 | | $ | 217.2 | | $ | 7.0 |

Natural gas | | | 5.3 | | | 70.5 | | | (3.5) |

| | | | | | | | | |

Total cash gains/(losses) | | $ | 80.3 | | $ | 287.7 | | $ | 3.5 |

| | | | | | | | | |

Non-cash gains/(losses): | | | | | | | | | |

Crude oil | | $ | (96.2) | | $ | (99.8) | | $ | 182.0 |

Natural gas | | | (13.5) | | | (45.2) | | | 48.9 |

Total non-cash gains/(losses) | | $ | (109.7) | | $ | (145.0) | | $ | 230.9 |

Total gains/(losses) | | $ | (29.4) | | $ | 142.7 | | $ | 234.4 |

| | | | | | | | | |

(Per BOE) | | 2016 | | 2015 | | 2014 |

Total cash gains/(losses) | | $ | 2.36 | | $ | 7.40 | | $ | 0.09 |

Total non-cash gains/(losses) | | | (3.22) | | | (3.73) | | | 6.14 |

| | | | | | | | | |

Total gains/(losses) | | $ | (0.86) | | $ | 3.67 | | $ | 6.23 |

During 2016, we realized cash gains of $75.0 million on our crude oil contracts and $5.3 million on our natural gas contracts. In comparison, in 2015 we realized cash gains of $217.2 million on our crude oil contracts and $70.5 million on our natural gas contracts. During 2014, we realized cash gains of $7.0 million on our crude oil contracts and cash losses of $3.5 million on our natural gas contracts. The cash gains in each year were due to contracts which provided floor protection above market prices, while cash losses were a result of natural gas prices rising above our fixed price swap positions.

As the forward markets for crude oil and natural gas fluctuate and new contracts are executed and existing contracts are realized, changes in fair value are reflected as either a non‑cash charge or gain to earnings. The fair value of our crude oil and natural gas contracts represented net loss positions of $28.8 million and $9.5 million, respectively, at December 31, 2016, and net gain positions of $67.4 million and $4.0 million, respectively, at December 31, 2015. The change in fair value of our crude oil and natural gas contracts represented losses of $96.2 million and $13.5 million, respectively, during 2016 and losses of $99.8 million and $45.2 million, respectively, during 2015.

ENERPLUS 2016 FINANCIAL SUMMARY 13

Revenues

| | | | | | | | | |

($ millions) | | 2016 | | 2015 | | 2014 |

Oil and natural gas sales | | $ | 882.1 | | $ | 1,052.4 | | $ | 1,849.3 |

Royalties | | | (159.4) | | | (168.0) | | | (323.1) |

Oil and natural gas sales, net of royalties | | $ | 722.7 | | $ | 884.4 | | $ | 1,526.2 |

Oil and natural gas sales revenue for 2016 totaled $882.1 million, a decrease of 16% from $1,052.4 million in 2015. The decrease in revenue was a result of the continued decline in commodity prices compared to the prior year along with lower production due to non-core asset divestments and lower capital spending.

In 2015, oil and natural gas sales revenue decreased 43% to $1,052.4 million from $1,849.3 million in 2014 as a result of weak commodity prices, offset somewhat by growth in production volumes.

Royalties and Production Taxes

| | | | | | | | | | |

($ millions, except per BOE amounts) | | 2016 | | 2015 | | 2014 | |

Royalties | | $ | 159.4 | | $ | 168.0 | | $ | 323.1 | |

Per BOE | | $ | 4.67 | | $ | 4.32 | | $ | 8.58 | |

| | | | | | | | | | |

Production taxes | | $ | 37.4 | | $ | 50.9 | | $ | 81.5 | |

Per BOE | | $ | 1.10 | | $ | 1.31 | | $ | 2.17 | |

Royalties and production taxes | | $ | 196.8 | | $ | 218.9 | | $ | 404.6 | |

Per BOE | | $ | 5.77 | | $ | 5.63 | | $ | 10.75 | |

| | | | | | | | | | |

Royalties and production taxes (% of oil and natural gas sales) | | | 22% | | | 21% | | | 22% | |

Royalties are paid to government entities, land owners and mineral rights owners. Production taxes include state production taxes, Pennsylvania impact fees, freehold mineral taxes and Saskatchewan resource surcharges. A large percentage of our production is from U.S. properties where royalty rates are generally not as sensitive to commodity price levels.

Royalties and production taxes were in line with our guidance for 2016, averaging 22% of oil and natural gas sales, before transportation. Royalties and production taxes decreased to $196.8 million in 2016 from $218.9 million in 2015 primarily due to lower production volumes, a decrease in realized crude oil and natural gas prices and a 1.5% rate reduction of production taxes in North Dakota. In 2015, royalties and production taxes decreased to $218.9 million from $404.6 million in the prior year primarily due to decreased realized crude oil and natural gas prices.

2017 Guidance

We expect royalty and production taxes in 2017 to average 23% of our oil and gas sales, before transportation. The increase compared to 2016 is due to the higher percentage of U.S. production as a result of additional capital spending and growth in our U.S. assets, as well as the divestment of our non-core Canadian properties during 2016.

Operating Expenses

| | | | | | | | | |

($ millions, except per BOE amounts) | | 2016 | | 2015 | | 2014 |

Cash operating expenses | | $ | 249.0 | | $ | 340.1 | | $ | 347.3 |

Non-cash (gains)/losses(1) | | | (1.1) | | | 0.4 | | | 1.3 |

Total operating expenses | | $ | 247.9 | | $ | 340.5 | | $ | 348.6 |

Per BOE | | $ | 7.27 | | $ | 8.76 | | $ | 9.26 |

| (1) | | Non-cash (gains)/losses on fixed price electricity swaps. |

Operating expenses during 2016 were $247.9 million or $7.27/BOE, beating our guidance of $7.50/BOE, largely due to higher than expected production volumes from our lower operating cost Marcellus properties during the fourth quarter. Compared to 2015, expenses decreased $92.6 million or 27% primarily due to successful cost saving initiatives, lower repairs and maintenance costs and the divestment of higher operating cost Canadian properties throughout 2016.

Operating expenses during 2015 were $340.5 million or $8.76/BOE compared to $348.6 million or $9.26/BOE in 2014. The improvement resulted mainly from cost savings and a continued increase in the U.S. weighting of production, which has lower

14 ENERPLUS 2016 FINANCIAL SUMMARY

operating metrics. This was offset in part by the impact of a weaker Canadian dollar on our U.S. dollar denominated operating expenses.

2017 Guidance

We expect operating expenses of $7.85/BOE in 2017. The modest increase from 2016 is a result of the expected increase in the corporate weighting of our liquids production.

Transportation Costs

| | | | | | | | | |

($ millions, except per BOE amounts) | | 2016 | | 2015 | | 2014 |

Transportation costs | | $ | 107.1 | | $ | 114.7 | | $ | 101.2 |

Per BOE | | $ | 3.14 | | $ | 2.95 | | $ | 2.69 |

Transportation costs increased on a per BOE basis throughout the year to average $3.14/BOE in 2016, consistent with our guidance of $3.15/BOE and a 6% increase compared to $2.95/BOE in 2015. The increase was primarily due to the increased weighting of U.S. production with higher associated transportation costs and additional firm transportation commitments in the Marcellus, effective August 2016.

Transportation costs increased to $2.95/BOE in 2015 compared to $2.69/BOE in 2014 as a result of increasing U.S. production and costs associated with securing U.S. pipeline capacity. The impact of a weakening Canadian dollar on our U.S. transportation costs further increased our total reported expense.

2017 Guidance

We expect transportation costs of $3.90/BOE in 2017. The increase from 2016 is largely attributable to additional firm transportation commitments in the Marcellus that came into effect in August 2016 to deliver production to higher priced markets, lower production volumes due to the year-end 2016 divestment of non-operated North Dakota properties and a weaker Canadian dollar projected in 2017.

Netbacks

The crude oil and natural gas classifications below contain properties according to their dominant production category. These properties may include associated crude oil, natural gas or natural gas liquids volumes which have been converted to the equivalent BOE/day or Mcfe/day and as such, the revenue per BOE or per Mcfe may not correspond with the average selling price under the “Pricing” section of this MD&A. Certain prior period amounts have been reclassified to conform with current period presentation.

ENERPLUS 2016 FINANCIAL SUMMARY 15

| | | | | | | | | |

| Year ended December 31, 2016 |

Netbacks by Property Type | | Crude Oil | | Natural Gas | | Total |

Average Daily Production | | | 47,206 BOE/day | | | 275,538 Mcfe/day | | | 93,125 BOE/day |

Netback(1) $ per BOE or Mcfe | | | (per BOE) | | | (per Mcfe) | | | (per BOE) |

Oil and natural gas sales | | $ | 37.86 | | $ | 2.26 | | $ | 25.88 |

Royalties and production taxes | | | (9.38) | | | (0.34) | | | (5.77) |

Cash operating expenses | | | (10.29) | | | (0.72) | | | (7.31) |

Transportation costs | | | (1.97) | | | (0.72) | | | (3.14) |

Netback before hedging | | $ | 16.22 | | $ | 0.48 | | $ | 9.66 |

Cash gains/(losses) | | | 4.34 | | | 0.05 | | | 2.36 |

Netback after hedging | | $ | 20.56 | | $ | 0.53 | | $ | 12.02 |

Netback before hedging ($ millions) | | $ | 280.4 | | $ | 48.8 | | $ | 329.2 |

Netback after hedging ($ millions) | | $ | 355.3 | | $ | 54.2 | | $ | 409.5 |

| | | | | | | | | |

| Year ended December 31, 2015 |

Netbacks by Property Type | | Crude Oil | | Natural Gas | | Total |

Average Daily Production | | | 49,069 BOE/day | | | 344,730 Mcfe/day | | | 106,524 BOE/day |

Netback(1) $ per BOE or Mcfe | | | (per BOE) | | | (per Mcfe) | | | (per BOE) |

Oil and natural gas sales | | $ | 43.67 | | $ | 2.15 | | $ | 27.07 |

Royalties and production taxes | | | (10.54) | | | (0.24) | | | (5.63) |

Cash operating expenses | | | (11.98) | | | (1.00) | | | (8.75) |

Transportation costs | | | (1.84) | | | (0.65) | | | (2.95) |

Netback before hedging | | $ | 19.31 | | $ | 0.26 | | $ | 9.74 |

Cash gains/(losses) | | | 12.13 | | | 0.56 | | | 7.40 |

Netback after hedging | | $ | 31.44 | | $ | 0.82 | | $ | 17.14 |

Netback before hedging ($ millions) | | $ | 345.7 | | $ | 33.0 | | $ | 378.7 |

Netback after hedging ($ millions) | | $ | 562.9 | | $ | 103.5 | | $ | 666.4 |

| | | | | | | | | |

| Year ended December 31, 2014 |

Netbacks by Property Type | | Crude Oil | Natural Gas | | Total |

Average Daily Production | | | 45,225 BOE/day | | | 347,430 Mcfe/day | | | 103,130 BOE/day |

Netback(1) $ per BOE or Mcfe | | | (per BOE) | | | (per Mcfe) | | | (per BOE) |

Oil and natural gas sales | | $ | 79.12 | | $ | 4.28 | | $ | 49.13 |

Royalties and production taxes | | | (19.78) | | | (0.61) | | | (10.75) |

Cash operating expenses | | | (11.76) | | | (1.21) | | | (9.23) |

Transportation costs | | | (1.89) | | | (0.55) | | | (2.69) |

Netback before hedging | | $ | 45.69 | | $ | 1.91 | | $ | 26.46 |

Cash gains/(losses) | | | 0.42 | | | (0.03) | | | 0.09 |

Netback after hedging | | $ | 46.11 | | $ | 1.88 | | $ | 26.55 |

Netback before hedging ($ millions) | | $ | 754.3 | | $ | 241.9 | | $ | 996.2 |

Netback after hedging ($ millions) | | $ | 761.3 | | $ | 238.4 | | $ | 999.7 |

| (1) | | See “Non‑GAAP Measures” in this MD&A. |

Crude oil and natural gas netbacks per BOE after hedging were lower during 2016 compared to 2015 and 2014 primarily due to the weakness in commodity prices compared to both the prior years and lower realized hedging gains compared to 2015, partially offset by significant improvements in our operating costs. During 2016, our crude oil properties accounted for 85% and 87% of our netback before and after hedging, respectively.

16 ENERPLUS 2016 FINANCIAL SUMMARY

General and Administrative Expenses

Total G&A expenses include cash G&A expenses and share‑based compensation (“SBC”) charges related to our long‑term incentive plans (“LTI plans”) and our stock option plan. See Note 10 and Note 14 to the Financial Statements for further details.

| | | | | | | | | |

($ millions) | | 2016 | | 2015 | | 2014 |

Cash: | | | | | | | | | |

G&A expense | | $ | 59.8 | | $ | 81.3 | | $ | 83.5 |

Share-based compensation expense | | | 3.1 | | | 0.9 | | | (1.2) |

| | | | | | | | | |

Non-Cash: | | | | | | | | | |

Share-based compensation expense | | | 27.0 | | | 19.6 | | | 13.4 |

Equity swap loss/(gain) | | | (3.6) | | | 2.1 | | | 9.3 |

Total G&A expenses | | $ | 86.3 | | $ | 103.9 | | $ | 105.0 |

| | | | | | | | | |

(Per BOE) | | 2016 | | 2015 | | 2014 |

Cash: | | | | | | | | | |

G&A expense | | $ | 1.75 | | $ | 2.09 | | $ | 2.22 |

Share-based compensation expense | | | 0.09 | | | 0.02 | | | (0.03) |

| | | | | | | | | |

Non-Cash: | | | | | | | | | |

Share-based compensation expense | | | 0.80 | | | 0.51 | | | 0.36 |

Equity swap loss/(gain) | | | (0.11) | | | 0.05 | | | 0.24 |

Total G&A expenses | | $ | 2.53 | | $ | 2.67 | | $ | 2.79 |

Cash G&A expenses in 2016 totaled $59.8 million ($1.75/BOE), outperforming our guidance of $1.80/BOE and a decrease of 26% from $81.3 million ($2.09/BOE) in 2015. The reduction from 2015 was primarily due to continued cost savings initiatives and the impact of ongoing staff reductions as we continue to divest of non-core assets and focus our business.

Our share price increased significantly during 2016, resulting in cash SBC expense of $3.1 million ($0.09/BOE) compared to an expense of $0.9 million ($0.02/BOE) in 2015. Following the settlement of the final grants of our cash-settled Restricted Share Unit (“RSU”) plans during the year, the Director Share Unit (“DSU”) plan is our only remaining LTI plan that we intend to settle in cash. We recorded non‑cash SBC of $27.0 million ($0.80/BOE) in 2016 compared to $19.6 million ($0.51/BOE) in 2015. The increase in non‑cash SBC was a result of an improvement in our performance multiplier based on our relative return in the Toronto Stock Exchange Oil and Gas Producers Index, along with additional grants issued under the treasury-settled LTI plans rather than the cash-settled plans.

Cash G&A expenses in 2015 were $81.3 million ($2.09/BOE) compared to $83.5 million ($2.22/BOE) in 2014. The decrease in cash G&A expenses compared to 2014 was primarily due to a 20% reduction in staff levels offset by one‑time severance charges. Cash SBC expense was $0.9 million ($0.02/BOE) in 2015 compared to a recovery of $1.2 million ($0.03/BOE) in 2014. We recorded non‑cash SBC of $19.6 million ($0.51/BOE) in 2015 compared to $13.4 million ($0.36/BOE) in 2014. The increase in non‑cash SBC was a result of additional grants issued under the treasury‑settled LTI plans.

We have hedged a portion of the outstanding cash‑settled units under our LTI plans. We recorded a non‑cash mark‑to‑market gain of $3.6 million on these hedges in 2016 (2015 - $2.1 million loss; 2014 – $9.3 million loss). As of December 31, 2016, we have 470,000 units hedged at a weighted average price of $16.89/share.

2017 Guidance

We expect our cash G&A expense to be approximately $1.80/BOE in 2017, consistent with 2016 despite lower expected production levels.

ENERPLUS 2016 FINANCIAL SUMMARY 17

Interest Expense

| | | | | | | | | |

($ millions) | | 2016 | | 2015 | | 2014 |

Interest on senior notes and bank facility | | $ | 45.4 | | $ | 66.5 | | $ | 62.2 |

Non-cash interest expense | | | - | | | - | | | 0.6 |

Total interest expense | | $ | 45.4 | | $ | 66.5 | | $ | 62.8 |

Interest on our senior notes and bank credit facility in 2016 decreased 32% to $45.4 million compared to $66.5 million in 2015. The decrease in interest expense corresponds to a decrease in the aggregate principal amount of our outstanding senior notes following our repurchase of US$267 million of senior notes during the first half of 2016. The repurchase was funded by asset divestment proceeds and lower interest rate bank debt, which was repaid following our May 31, 2016 equity financing and the closing of our second quarter Canadian non-core asset divestment.

Interest expense increased to $66.5 million in 2015 from $62.8 million in 2014 due to the impact of a weaker Canadian dollar on our U.S. dollar denominated interest payments and an increased weighting of senior notes with higher interest rates compared to our bank credit facility following our US$200 million private placement in September 2014. Non-cash amounts recorded in 2014 consisted of unrealized losses on the interest component of our cross currency interest rate swap. See Note 11 to the Financial Statements for further details.

At December 31, 2016, approximately 97% of our debt consisted of fixed interest rate senior notes and approximately 3% was floating bank debt with weighted average interest rates of 5.0% and 2.6%, respectively.

Foreign Exchange

| | | | | | | | | |

($ millions) | | 2016 | | 2015 | | 2014 |

Realized loss/(gain) | | $ | 0.1 | | $ | (8.7) | | $ | 11.2 |

Unrealized loss/(gain) | | | (40.6) | | | 182.6 | | | 45.9 |

Total foreign exchange loss/(gain) | | $ | (40.5) | | $ | 173.9 | | $ | 57.1 |

US/CDN average exchange rate | | | 1.32 | | | 1.28 | | | 1.10 |

US/CDN period end exchange rate | | | 1.34 | | | 1.38 | | | 1.16 |

We recorded a net foreign exchange gain of $40.5 million in 2016 compared to losses of $173.9 million and $57.1 million in 2015 and 2014, respectively. Our foreign exchange exposure relates to fluctuations in the Canadian and U.S. dollar exchange rate.

In 2016, we recorded a realized loss of $0.1 million on day‑to‑day transactions denominated in foreign currencies, compared to a gain of $8.7 million and a loss of $11.2 million in 2015 and 2014, respectively. In 2015, realized foreign exchange included a gain of $39.9 million on the unwind of our US$175 million foreign exchange swaps and a gain of $3.3 million on the final settlement of our US$54 million senior notes and the corresponding foreign exchange swap. These gains were offset by cumulative losses of $39.2 million on our foreign exchange collars with final settlements in December 2015. In 2014, we recorded a $15.8 million loss on the final settlement of our cross currency interest rate swap and a gain of $0.7 million on our costless collars.

Unrealized foreign exchange gains and losses are recorded on the translation of our U.S. dollar denominated debt and working capital at each period end. Comparing December 31, 2016 to December 31, 2015, the Canadian dollar strengthened relative to the U.S. dollar and we reduced our U.S. dollar denominated senior notes by 33%, resulting in an unrealized gain of $40.6 million. See Note 12 to the Financial Statements for further details.

18 ENERPLUS 2016 FINANCIAL SUMMARY

Capital Investment

| | | | | | | | | |

($ millions) | | 2016 | | 2015 | | 2014 |

Capital spending | | $ | 209.1 | | $ | 493.4 | | $ | 811.0 |

Office capital | | | 1.5 | | | 4.5 | | | 7.0 |

Sub-total | | | 210.6 | | | 497.9 | | | 818.0 |

Property and land acquisitions | | $ | 126.1 | | $ | 9.5 | | $ | 18.5 |

Property divestments | | | (670.4) | | | (286.6) | | | (203.6) |

Sub-total | | | (544.3) | | | (277.1) | | | (185.1) |

Total | | $ | (333.7) | | $ | 220.8 | | $ | 632.9 |

2016

Capital spending in 2016 totaled $209.1 million, slightly below our revised guidance of $215 million due to some weather related deferrals of spending during the fourth quarter. We continued to focus capital on our core areas during 2016, spending $136.4 million on our North Dakota crude oil properties, $44.4 million on our Canadian crude oil waterflood properties and $24.3 million on our Marcellus natural gas assets. Through our capital program in 2016 we added 43 MMBOE of gross proved plus probable reserves, replacing 126% of our 2016 production, before accounting for acquisitions and divestments.

We recorded net divestment proceeds of $670.4 million in 2016. In Canada, we sold properties for combined proceeds of $281.0 million with production of approximately 8,500 BOE/day. Sold properties consisted mainly of natural gas assets, and included certain Deep Basin natural gas properties with production of 5,400 BOE/day and non-core properties in northwest Alberta with production of 2,300 BOE/day. Divestments resulted in a $35.6 million reduction to future asset retirement obligations. On December 30, 2016, we closed the sale of our non-operated assets in North Dakota with production of approximately 5,000 BOE/day for proceeds of $392.0 million, which was reported as restricted cash at December 31, 2016.

Property and land acquisitions in 2016 totaled $126.1 million, largely due to our acquisition of a Canadian waterflood property for a purchase price of $110.3 million, net of closing adjustments.

2015

Capital spending in 2015 totaled $493.4 million and included spending of $302.3 million on our North Dakota crude oil properties, $115.7 million on our Canadian crude oil properties, $32.2 million on our Marcellus assets and $40.4 million on our Deep Basin properties in Canada. Through our capital program in 2015 we added 42 MMBOE of gross proved plus probable reserves, replacing 108% of our 2015 production, before accounting for acquisitions and divestments.

During 2015, we recorded net divestment proceeds of $286.6 million. In Canada, we divested of assets for combined proceeds of $198.9 million with production of approximately 4,900 BOE/day including the sale of our Pembina waterflood assets and certain non-core shallow gas assets with production of 2,700 BOE/day. In the U.S., we divested of assets for combined proceeds of $87.7 million with production of approximately 1,250 BOE/day, including the sale of a portion of our non‑operated North Dakota properties for proceeds of $80.4 million, and our operated Marcellus assets for proceeds of $3.5 million.

Property and land acquisitions in 2015 totaled $9.5 million and included minor acquisitions of leases and undeveloped land.

2014

Capital spending in 2014 totaled $811.0 million and included spending of $343.7 million on our North Dakota crude oil properties, $176.6 million on our Canadian crude oil properties, $158.8 million on our Marcellus assets and $124.5 million on our deep gas properties in Canada. Through our capital program in 2014 we added 75 MMBOE of gross proved plus probable reserves, replacing over 200% of our 2014 production.

Property divestments in 2014 totaled $203.6 million. In Canada we divested of natural gas properties in the Deep Basin area with production of approximately 3,100 BOE/day for proceeds of $91.0 million and recognized the remaining $65.8 million of proceeds on the 2013 sale of our undeveloped Montney acreage. During the first quarter, we sold our gross overriding royalty interest in the Jonah natural gas property in Wyoming with production of approximately 400 BOE/day for proceeds of $44.0 million, after closing adjustments. Property and land acquisitions in 2014 totaled $18.5 million and included several minor acquisitions across our core areas.

ENERPLUS 2016 FINANCIAL SUMMARY 19

2017 Guidance

To re-position ourselves for growth in 2017, we are increasing our capital spending guidance to $450 million, more than twice our spending levels in 2016. We will continue to focus our spending on our core areas, with $330 million currently allocated to North Dakota crude oil properties, $60 million to Canadian waterflood crude oil properties and $60 million to the Marcellus natural gas properties.

Gain on Asset Sales and Note Repurchases

We recorded gains of $559.2 million on asset divestments during 2016, including a gain of $339.4 million on the fourth quarter sale of our non-operated North Dakota property. No gains were recorded on asset sales in 2015 or 2014. Under full cost accounting rules, divestments of oil and natural gas properties are generally accounted for as adjustments to the full cost pool with no recognition of a gain or loss. However, if not recognizing a gain or loss on the transaction would significantly alter the relationship between a cost centre’s capitalized costs and proved reserves, then a gain or loss must be recognized. Gains and losses are evaluated on a case by case basis for each asset sale, and future sales may or may not result in such treatment.

During the first half of 2016, we recorded a total gain of $19.3 million on the repurchase of US$267 million of outstanding senior notes at prices between 90% of par and par value.

Depletion, Depreciation and Accretion (“DD&A”)

| | | | | | | | | |

($ millions, except per BOE amounts) | | 2016 | | 2015 | | 2014 |

DD&A expense | | $ | 329.0 | | $ | 508.2 | | $ | 567.7 |

Per BOE | | $ | 9.65 | | $ | 13.06 | | $ | 15.08 |

DD&A of property, plant and equipment (“PP&E”) is recognized using the unit‑of‑production method based on proved reserves. DD&A has decreased from 2014 to 2016 primarily due to the quarterly asset impairments recorded during 2015 and 2016 under the U.S. GAAP full cost ceiling test methodology.

Impairments

PP&E

| | | | | | | | | |

($ millions) | | 2016 | | 2015 | | 2014 |

Canada cost centre | | $ | 89.4 | | $ | 286.7 | | $ | — |

U.S. cost centre | | | 211.8 | | | 1,065.7 | | | — |

Total Impairments | | $ | 301.2 | | $ | 1,352.4 | | $ | — |

Under U.S. GAAP, the full cost ceiling test is performed on a country‑by‑country cost centre basis using estimated after‑tax future net cash flows discounted at 10% from proved reserves using SEC constant prices (“Standardized Measure”). SEC prices are calculated as the unweighted average of the trailing twelve first‑day‑of‑the‑month commodity prices. Standardized Measure is not related to our capital spending investment criteria and is not a fair value based measurement, but rather a prescribed accounting calculation. Under U.S. GAAP impairments are not reversed in future periods.

The trailing twelve month average crude oil and natural gas prices have decreased significantly in 2016 and 2015, resulting in non‑cash impairments totaling $301.2 million and $1,352.4 million (before tax), respectively. We did not record any impairments on our oil and natural gas properties in 2014.

The following table outlines the twelve month average trailing benchmark prices and exchange rates used in our ceiling test at December 31, 2016, 2015 and 2014:

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | AECO Natural |

| | WTI Crude Oil | | Exchange Rate | | Edm Light Crude | | U.S. Henry Hub | | Gas Spot |

Year | | US$/bbl | | US/CDN | | CDN$/bbl | | Gas US$/Mcf | | CDN$/Mcf |

2016 | | $ | 42.75 | | 1.32 | | $ | 52.26 | | $ | 2.49 | | $ | 2.17 |

2015 | | $ | 50.28 | | 1.27 | | $ | 59.38 | | $ | 2.58 | | $ | 2.69 |

2014 | | $ | 94.99 | | 1.09 | | $ | 94.84 | | $ | 4.30 | | $ | 4.60 |

20 ENERPLUS 2016 FINANCIAL SUMMARY

Many factors influence the allowed ceiling value versus our net capitalized cost base, making it difficult to predict with reasonable certainty the value of impairment losses from future ceiling tests. For the next year, the primary factors include future first‑day‑of‑the‑month commodity prices, reserves revisions, our capital expenditure levels and timing, acquisition and divestment activity, as well as production levels, which affect DD&A expense. Although the twelve month average trailing commodity prices are below current levels, there is the potential for prices to decline further, impacting the ceiling value which could result in further non-cash impairments.

Goodwill

Goodwill impairment testing is performed annually or more frequently if events or changes in circumstances indicate that goodwill may be impaired. We perform a qualitative assessment of goodwill by evaluating potential indicators of impairment, and if it is more likely than not that the fair value of the reporting unit is less than its carrying value we perform quantitative impairment tests. If the carrying value of the reporting unit exceeds its fair value, goodwill is written down to its implied fair value with an offsetting charge to earnings in the consolidated statements of income/(loss) in the Financial Statements.

Our annual goodwill impairment assessments as at December 31, 2016 and 2015 indicated no impairment.

Asset Retirement Obligation

In connection with our operations, we incur abandonment and reclamation costs related to assets, such as surface leases, wells, facilities and pipelines. Total asset retirement obligations included on our balance sheet are based on management’s estimate of our net ownership interest, costs to abandon and reclaim and the timing of the costs to be incurred in future periods.

We have estimated the net present value of our asset retirement obligation to be $181.7 million at December 31, 2016, compared to $206.4 million at December 31, 2015. The decrease was largely due to the removal of $35.6 million of asset retirement obligations related to asset divestments during 2016. See Note 8 to the Financial Statements for further information.

We take an active approach to managing our abandonment, reclamation and remediation obligations. During 2016, we spent $8.4 million (2015 – $14.9 million) on our asset retirement obligations and we expect to spend approximately $13.1 million in 2017. The majority of our abandonment and reclamation costs are expected to be incurred between 2025 and 2055. We do not reserve cash or assets for the purpose of funding our future asset retirement obligations. Any abandonment and reclamation costs are anticipated to be funded out of cash flow and available credit facilities.

Income Taxes

| | | | | | | | | |

($ millions) | | 2016 | | 2015 | | 2014 |

Current tax expense/(recovery) | | $ | (2.4) | | $ | (16.9) | | $ | 5.0 |

Deferred tax expense/(recovery) | | | (234.8) | | | (150.6) | | | 132.8 |

Total tax expense/(recovery) | | $ | (237.2) | | $ | (167.5) | | $ | 137.8 |

Our current tax recovery mainly relates to a refund of U.S. Alternative Minimum Tax (“AMT”) from a prior period.

The total tax recovery in 2016 was $237.2 million, compared to $167.5 million in 2015. The increased recovery in 2016 is due primarily to the removal of a portion of our valuation allowance recorded in 2015 due to higher future taxable income projected this year compared to 2015. We assess the recoverability of our deferred income tax assets each period to determine whether it is more likely than not all or a portion of our deferred income tax assets will be realized. We have considered available positive and negative evidence, including future taxable income and reversing existing temporary differences in making this assessment. This assessment is primarily the result of projecting future taxable income using December 30 benchmark forward prices for 2017, held constant and adjusted for other significant items affecting taxable income. Had we utilized forecast prices and costs to estimate future taxable income we expect that all of our deferred income tax assets would be realized and no valuation allowance would be required. Our overall deferred income tax asset, net of valuation allowance, is $733.4 million as at December 31, 2016 (2015 - $516.1 million).

In 2015, our total tax recovery was $167.5 million compared to an expense of $137.8 million in 2014. The recovery in 2015 was due primarily to lower income, which was impacted by a $1,352.4 million non‑cash charge for asset impairments and a valuation allowance recorded against a portion of our deferred income tax asset.

ENERPLUS 2016 FINANCIAL SUMMARY 21

Our estimated tax pools at December 31, 2016 are as follows:

| | | |

Pool Type ($ millions) | | 2016 |

Canada | | | |

Canadian development expenditures (“CDE”) | | $ | 63 |

Canadian exploration expenditures (“CEE”) | | | 236 |

Undepreciated capital costs (“UCC”) | | | 166 |

Non-capital losses and other credits | | | 397 |

| | $ | 862 |

U.S. | | | |

Alternative minimum tax credit (“AMT”) | | $ | 112 |

Net operating losses | | | 894 |

Depletable and depreciable assets | | | 1,370 |

| | $ | 2,376 |

Total tax pools and credits | | $ | 3,238 |

Capital losses | | $ | 1,224 |

Capital losses reflect the balance of unused capital losses available for carry‑forward in Canada. These capital losses have an indefinite carry‑forward period however can only be used to offset capital gains. We do not anticipate future capital gains that will allow us to utilize the capital losses. Therefore, a full valuation allowance has been applied to the deferred tax asset in respect of these capital losses.

LIQUIDITY AND CAPITAL RESOURCES

There are numerous factors that influence how we assess our liquidity and leverage including commodity price cycles, capital spending levels, acquisition and divestment plans, hedging and dividend levels. We also assess our leverage relative to our most restrictive debt covenant, which is a maximum senior debt to earnings before interest, taxes, depreciation, amortization, impairment and other non-cash charges (“adjusted EBITDA”) ratio of 3.5x for a period of up to six months, after which it drops to 3.0x. At December 31, 2016, our senior debt to adjusted EBITDA ratio was 0.8x and our net debt to adjusted funds flow ratio was 1.2x, a significant improvement from 2.2x and 2.5x, respectively, at December 31, 2015. Although it is not included in our debt covenants, the net debt to adjusted funds flow ratio is often used by investors and analysts to evaluate our liquidity.

We strengthened our financial position significantly in 2016, reducing our net debt by 69% over the twelve month period. The overall reduction in debt was funded through proceeds from our May 2016 equity issuance and our ongoing non-core asset divestment program. On May 31, 2016, we completed an equity financing for 33,350,000 common shares at a price of $6.90 per share for gross proceeds of $230.1 million ($220.4 million, net of issue costs). Asset divestments throughout 2016 resulted in aggregate divestment proceeds of $670.4 million. This additional liquidity was used to repay our bank credit facility, repurchase US$267 million of senior notes during the first half of 2016, at prices ranging from 90% of par to par value, and purchase our Canadian waterflood property in November for $110.3 million.

Net acquisition and divestment proceeds include $392.0 million from the sale of non-operated North Dakota properties, which were classified as restricted cash on the December 31, 2016 balance sheet. As of the date of this report, we expect to continue to hold these funds in escrow for a period of up to 180 days from the date of closing to facilitate possible future like-kind transactions in accordance with U.S. federal tax regulations.

Total debt, net of cash and restricted cash, at December 31, 2016 was $375.5 million compared to $1,216.2 million at December 31, 2015. Total debt was comprised of $23.2 million of bank indebtedness and $745.6 million of senior notes less $393.3 million in cash, including restricted cash. Our next scheduled senior notes repayment of US$22 million is due in June 2017 with remaining maturities extending to 2026.

Our adjusted payout ratio, which is calculated as cash dividends plus capital and office expenditures divided by adjusted funds flow, was 80% for 2016 compared to 128% in 2015. After adjusting for net acquisition and divestment proceeds, our funding surplus for the year ended December 31, 2016 was $603.8 million compared to $144.8 million in 2015. We expect to continue to pay monthly dividends to our shareholders of $0.01 per share, however, if economic conditions change we may make adjustments.

Our working capital deficiency, excluding cash and current deferred financial and tax balances, decreased to $94.4 million at December 31, 2016 from $104.0 million at December 31, 2015. We expect to finance our working capital deficit and our ongoing

22 ENERPLUS 2016 FINANCIAL SUMMARY

working capital requirements through cash, adjusted funds flow and our bank credit facility. In addition, we have sufficient liquidity to meet our financial commitments for the near term, as disclosed under “Commitments” below.