Project Maple Tree Presentation to the Special Committee February 24, 2007 Exhibit (c)(5) |

1 Table of Contents Sections 1. Introduction 2. Offer Overview 3. Financial Analysis 4. Fairness Considerations Appendix 1. Overview of Hub International |

Introduction |

3 Introduction • This Scotia Capital presentation to the Special Committee (the “Committee”) of the board of directors (the “Board”) of Hub International Limited (“Hub” or the “Company”) will: Provide an overview of the current proposal (the “Offer”) by Apax Partners LLP (“Apax”) and Morgan Stanley Principal Investments, Inc. (“Morgan Stanley”) (together, the “Sponsors”) to acquire Hub (the “Transaction”) Provide our views with respect to the value of Hub Provide our views on certain other factors we considered in assessing the fairness, from a financial point of view, of the consideration to be paid to the shareholders of Hub (the “Public Shareholders”) other than members of the Company’s senior management team who will be rolling-over their interests • Scotia Capital’s analysis is for illustrative purposes only, and does not constitute a formal valuation of the Company Introduction |

Offer Overview |

5 Key Terms of the Offer Offer Overview • “Go-shop” provision 22 day initial period to obtain non-binding expressions of interest Additional 22 days to obtain a binding proposal • Fiduciary out for superior proposal • Break fee 1.25% of equity value during “Go-shop” period 3.00% of equity value outside of “Go-shop” period Support Agreement • Acquisition of 100% of the outstanding common shares of the Company • All cash • $40.00 per Share Offer Stated Offer Price Form of Consideration Structure Terms |

6 Assessment of the Offer Offer Overview (1) Based on company reports and management projections, includes all outstanding contingency payments. (2) Estimates from I/B/E/S. (3) 2006E pro forma run-rate EBITDA and EPS from acquisitions. 2007E EBITDA management projections, adjusted for 2007E related acquisitions. Implied Capitalization (US$, million except per share amounts) Offer Price $40.00 Recent Share Price $34.20 % Premium 17.0% Basic Shares Outstanding 39.5 Add: In-the-Money Options 1.0 Add: Restricted Share Units 2.0 FD Shares Outstanding 42.5 FD Market Capitalization at Offer Price $1,698.1 Add: Debt $144.6 Add: Contingent Payments (1) $83.3 Less: Cash ($99.2) Less: Cash from options ($15.7) Enterprise Value $1,811.2 Implied Values Financial Overview EBITDA EPS EBITDA EPS 2006E $147.8 $1.56 $160.7 $1.69 2007E $179.2 $1.94 $173.4 $1.85 Multiples Implied by Offer EV/EBITDA P/E EV/EBITDA P/E 2006E 12.3x 25.6x 11.3x 23.6x 2007E 10.1x 20.6x 10.4x 21.7x December 31, 2006 Street Estimates (2) Management (3) |

Financial Analysis |

8 Methodology • The subject matter of the Opinion will be valued in accordance with the following: Fair Market Value: “The monetary consideration that, in an open and unrestricted market, a prudent and informed buyer would pay to a prudent and informed seller, each acting at arm’s length with the other and under no compulsion to act” No downward adjustment to reflect liquidity, the effect of the transaction, or the lack of a controlling interest • Several valuation methodologies will be considered in determining a range of fair market values for the Company’s shares Financial Analysis • Relevance varies with the comparability of the target companies, time period and industry dynamics • Useful for checking the relevance of DCF results Medium Precedent Transactions • Analysis is only as good as the comparables • Ability to use relevant universe of pure-play public companies Low Publicly-Traded Comparable Companies • Compares the offer price relative to historical trading levels of the Company’s shares as well as volume weighted cost basis • While not a primary valuation methodology, this analysis provides insights into market reaction to the Offer Medium Trading Analysis High Relevance • Explicitly takes into account the amount, timing and relative certainty of future cash flows for each of Hub’s business segments • Ability to account for changing industry dynamics and trends Preliminary Observations Discounted Cash Flow Valuation Methodology |

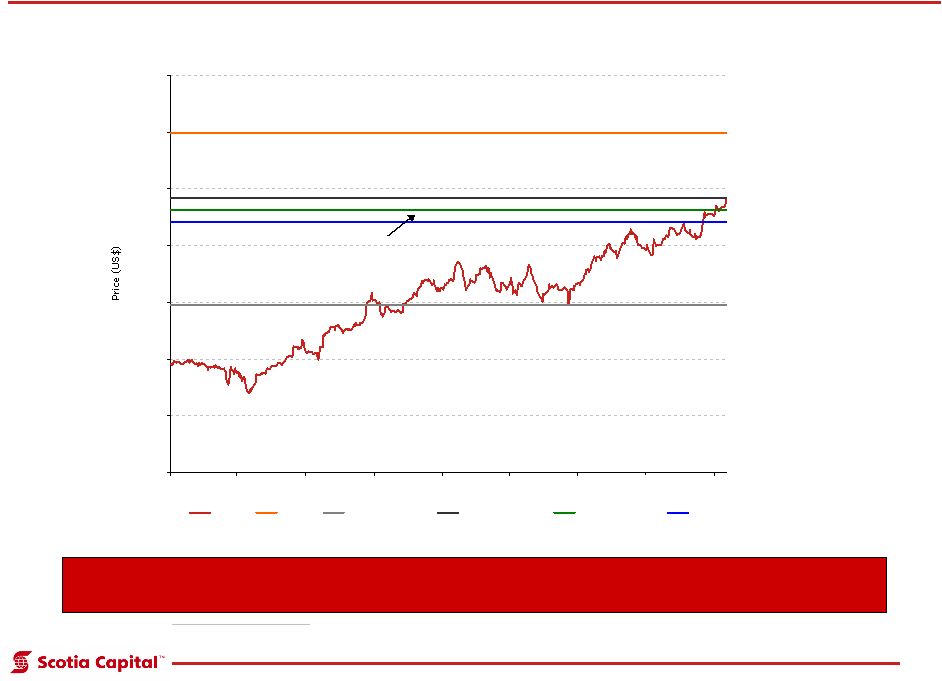

9 Trading Analysis – Historical Share Price A $40.00 cash offer represents a 17% premium to the recently achieved 52-week high Hub Trading Analysis (1) Financial Analysis Source: Bloomberg. (1) VWAP calculated using NYSE volume and price. $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00 $45.00 Feb-05 May-05 Aug-05 Nov-05 Feb-06 May-06 Aug-06 Nov-06 Feb-07 Price Offer 52-Week Low 52-Week High 20-Day VWAP 60-Day VWAP Implied Premium $40.00 $24.80 $34.20 $33.18 $32.14 $34.20 17.0% 61.3% 17.0% 20.6% 24.4% 52-week High 60-day VWAP 52-week Low 20-day VWAP Offer Price |

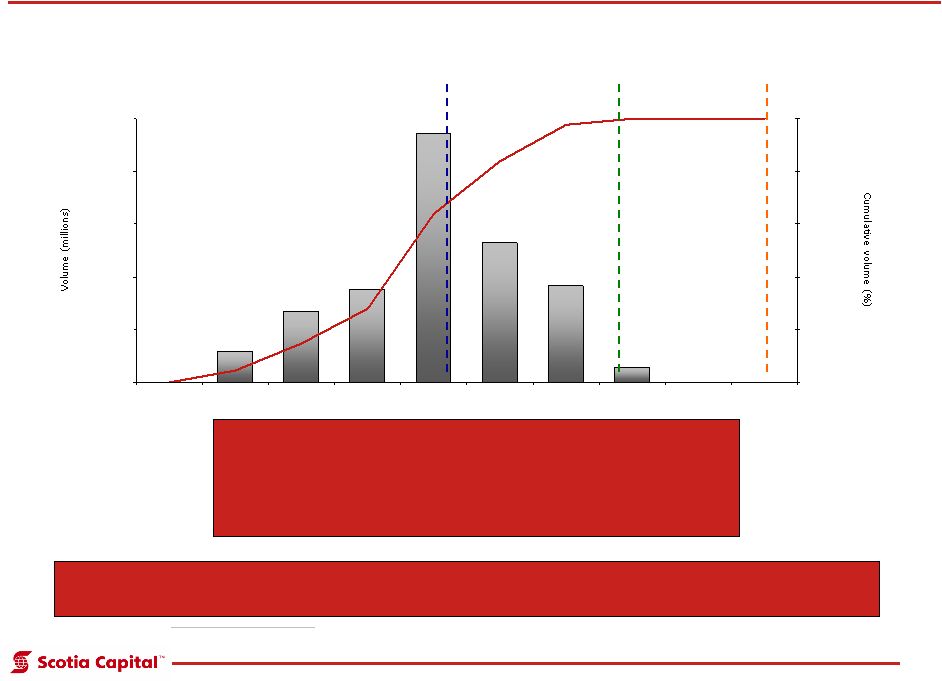

10 - 1.2 2.7 3.5 9.5 5.3 3.7 - - 0.6 0.0 2.0 4.0 6.0 8.0 10.0 $16.00 - $18.50 $18.50 - $21.00 $21.00 - $23.50 $23.50 - $26.00 $26.00 - $28.50 $28.50 - $31.00 $31.00 - $33.50 $33.50 - $36.00 $36.00 - $38.50 $38.50 - $41.00 0% 20% 40% 60% 80% 100% Trading Analysis – Float Turnover One Turn of Market Float (1) July 27, 2005 to February 22, 2007 Float Outstanding (1) : 26,480,720 Average Daily Volume (NYSE/TSX): 62,560/4,306 Volume-Weighted Average Close (2) : US$27.48 Number of Days: 396 (1) Float calculated using basic shares outstanding less management and Fairfax ownership. Aggregate of NYSE and TSX volume. (2) VWAP based on NYSE price and volume. The Sponsors’ offer represents a premium of approximately 45% to the volume- weighted average close over the float turnover period VWAP: $27.48 Current Price: $34.20 Offer Price: $40.00 Financial Analysis |

11 Publicly Traded Comparable Companies • Scotia Capital reviewed a series of publicly traded North American insurance brokers • Multiples of publicly traded companies do not represent en bloc value (i.e. control) • Hub’s operational performance and financial situation is slightly better than that of peers as acquisitions and margin improvement are forecasted to drive earnings growth that exceeds that of peers • Hub’s trading multiples appear lower than North American peers Based on a selected range of multiples of 8.0x–10.0x and 15.0x-20.0x for EV/EBITDA and P/E respectively, the implied value of Hub would be $27.70-$38.18 per share (1) 2007E Management projections, adjusted for 2007E related acquisitions. Financial Analysis (US$) Selected Multiples Implied Per Share Value Low High Low High EV/2007E EBITDA (1) 8.0x 10.0x $30.01 $38.18 P/2007E EPS (1) 15.0x 20.0x $27.70 $36.93 |

12 Selected Publicly Traded Comparable Companies Financial Analysis (1) Enterprise value includes regulatory settlements and pension related liabilities. Adjusted for after-tax proceeds from Putnam sale. (2) Pro forma shares repurchased in Q4/06. Enterprise value includes securitization and pension and related liabilities. (3) Market capitalization net of shares repurchased in Q4/06. (4) Enterprise value includes future contingency payments. (5) Pro forma January 2007 acquisitions. Enterprise value includes earnouts payable and off-balance sheet commitments. (6) Enterprise value includes litigation related liabilities. (7) Estimates from I/B/E/S. (8) Based on company information, estimates from management projections, adjusted for acquisitions. 07/08 Net Debt/ Share Market EBITDA Margins EPS 2007E (US$ millions, except share price) Price Cap. EV 2007E 2008E 2007E 2008E 2007E 2008E Growth EBITDA 22-Feb-07 Marsh & McLennan Companies (1) $29.98 $16,549 $18,431 9.4x 8.9x 17.0x 14.6x 17.0% 17.6% 17.0% 1.0x Aon Corp. (2) $38.66 $12,217 $16,989 10.3x 9.5x 14.5x 12.7x 17.8% 18.5% 14.1% 2.9x Willis Group Holdings (3) $40.22 $6,203 $6,740 9.7x 8.9x 14.9x 13.0x 26.6% 27.4% 14.8% 0.7x Brown & Brown (4) $28.33 $3,992 $4,319 11.1x 9.8x 19.4x 17.7x 39.5% 40.9% 9.6% 0.8x Arthur J Gallagher & Co. (5) $29.06 $2,908 $2,799 10.1x 9.2x 16.0x 15.8x 16.5% 17.8% 1.0% (0.4x) Hilb Rogal & Hobbs Co. (6) $46.40 $1,708 $1,815 8.6x 8.1x 17.6x 16.7x 26.5% 26.0% 5.7% 0.5x Average 9.9x 9.1x 16.6x 15.1x 24.0% 24.7% 10.4% 0.9x Hub International (7) $34.20 $1,452 $1,565 8.7x n.a. 17.7x n.a. 27.7% n.a. n.a. 0.6x Hub International (at offer price) (8) $40.00 $1,698 $1,811 10.4x 9.8x 21.7x 20.4x 28.7% 29.5% 6.3% 0.7x EV / EBITDA Price/Earnings |

13 Selected Precedent Transactions Analysis • Precedent transactions analysis is based upon the multiples implied by prior transactions in the North American insurance broker sector Prior transactions by Hub were also reviewed • Scotia Capital reviewed certain public information regarding industry transactions and considered a range of multiples that are appropriate for assessing Hub Such multiples implicitly reflect a premium for control • In identifying appropriate transactions, Scotia Capital considered, among other things, size, nature of the business model, margins and recent and future growth prospects Scotia Capital is of the view that there are relatively few truly meaningful and recent comparable transactions based on the aforementioned criteria We have nonetheless observed transaction multiples of approximately 10.0x – 11.0x LTM EBITDA Financial Analysis |

14 Selected Precedent Transactions Analysis (1) LTM financial results adjusted for one-time charges and pro forma acquisitions made during the LTM period. Forward for year-end 2007. 1-day prior premium based on October 24, 2006 share price when USIH announced formation of special committee. Includes mid-point of estimated contingent payments. (2) LTM financials 2006E. Transaction value includes preferred shares. (3) Consortium included Actis Capital, Caisse de Depot et Placement and Ontario Teachers Pension Plan. Financials shown in US$. Premiums to prices prior to June 7, 2006, date on which the company announced sale process. (4) Transaction value and multiples from street research. (5) Financials from company press release and street research. Forward for year-end 2002. (6) Forward multiples based on 2001 estimates from street research. Premium to 1-day prior share price though review of strategic alternative announced November 2000. (7) C$, forward for year-end 2000. (8) Transaction value from press release. Financials are historical from Willis Group Holdings initial public offering documents, June, 2001. Premium based on ADR. (9) Transaction value includes restricted share units. Multiples based on financials from Management projections adjusted for acquisitions. Premiums to January 25, 2007. Source: Company reports, Bloomberg, Capital IQ, estimates from street research There are relatively few public acquisitions of comparable size to Hub’s transaction Financial Analysis (US$, millions unless otherwise noted) Date Target Acquiror Enterprise Value LTM Revenue Forward Revenue LTM EBITDA Forward EBITDA LTM EPS Forward EPS 1-Day Prior 20-Days Prior Jan-07 (1) USI Holdings Corp GS Capital Partners $1,347.0 2.4x 2.1x 10.4x 9.6x 31.7x 13.2x 15.0% 23.7% Nov-06 (2) Clark, Inc. AEGON $596.7 2.1x 2.0x 10.4x 9.2x 33.1x 21.3x 32.4% 45.2% Oct-06 (3) Alexander Forbes Ltd. Consortium $884.9 1.2x 1.3x 7.3x n.a. 15.0x 11.7x 15.9% 4.8% Feb-05 (4) Hull & Co, Inc. Brown & Brown Inc. $175.0 2.8x n.a. 7.9x n.a. 15.3x n.a. n.a. n.a. Sep-04 Summit Global Partners USI Holdings Corp. $123.9 0.9x n.a. n.a. n.a. n.a. n.a. n.a. n.a. May-02 (5) Hobbs Group, LLC Hilb, Rogal & Hamilton $274.0 2.9x 2.5x 11.2x 7.8x n.a. n.a. n.a. n.a. Apr-01 (6) EW Blanch Holdings Benfield Group Ltd. $179.4 n.a. 0.9x n.a. n.a. n.a. 13.5x 68.3% 45.9% Aug-00 (7) Equisure Financial Network ING Groep NV C$172.1 2.2x 2.2x 16.0x 9.9x 31.5x 32.1x 42.9% 45.8% Jul-98 (8) Willis Corroon Group plc KKR $1,416.4 1.2x 1.1x 7.4x 9.3x n.a. n.a. 12.0% 29.6% Average 2.0x 1.7x 10.1x 9.2x 25.3x 18.3x 31.1% 32.5% Average (excl. min/max) 2.0x 1.7x 9.5x 9.4x 26.2x 16.0x 26.5% 36.1% Jan-07 (9) Hub International Apax Partners $1,811.2 3.1x 3.0x 11.3x 10.4x 23.6x 21.7x 21.6% 28.7% Price Transaction Value Bid Premium |

15 USI Holdings Implied Valuation • On January 16, 2007, Goldman Sachs Capital Partners announced a bid for USI Holdings • USI Holdings had previously announced expressions of interest from potential bidders in October 2006 • USI Holdings represents the most comparable precedent transaction USI Holdings is a mid-market brokerage Private equity buyer (1) 2006E Pro forma run-rate EBITDA and EPS from acquisitions. (2) 2007E EBITDA management projections, adjusted for 2007E related acquisitions. Source: Management projections. The Sponsors’ offer implies a premium to the multiple paid by Goldman Sachs to acquire USI Holdings Financial Analysis (US$, millions) 2006E 2007E EBITDA $160.7 $173.4 USI Holdings Multiple 10.4x 9.6x Enterprise Value $1,674.6 $1,666.3 Less: Debt ($144.6) ($144.6) Less: Contingent Payments (2) ($83.3) ($83.3) Add: Cash $99.2 $99.2 Add: Cash from options $15.7 $15.7 Equity Value $1,561.6 $1,553.3 FD Shares Outstanding 42.5 42.5 Equity Value Per Share $36.78 $36.59 Implied Hub Equity Value (1) (2) |

16 DCF Analysis • The DCF approach takes into account the amount, timing and relative certainty of projected cash flows • The analysis involves several steps: Developing a long-term forecast of the unlevered free cash flows (“UFCF”) of the business; Calculating a terminal value to capture value beyond the forecast period; and Discounting the cash flows and terminal value at the weighted average cost of capital (“WACC”) to arrive at an enterprise value in current dollars at December 31, 2006 • In developing its 15-year forecast for the fiscal period going from December 31, 2006 to 2021, Scotia Capital based its analysis on information and forecasts provided by Hub management 2007 Budget and Summary Management Projections (2007-2011) Actual results for year ending December 31, 2006 Hub business plans Other internal documents and spreadsheets • In addition to this, we discussed with senior management of Hub the Company’s business model, its strategic plan and prospects for each business segment • Projections were also developed through discussions on key assumptions with management and vetted for reasonableness Insurance sector pricing trends Continued strategy for acquisitions of hub brokerages and fold-in brokerages Financial Analysis |

17 DCF Analysis – Segmented Business Model • For the purpose of our analysis, UFCFs are defined as after-tax operating cash flows adjusted for working capital requirements, capital expenditures and future acquisition costs After-tax operating cash flows exclude all interest payments and assume a long-term corporate tax rate of 37.5% • Forecasts of sales and earnings before interest, taxes, depreciation and amortization (“EBITDA”) were modeled for each individual hub based on the following drivers: Commissions & Fees revenue growth rates by product line Contingent Commissions, Interest Income and Other Income grown as per management forecast Expense margins grown as a percentage of total revenue and in line with management projections Future acquisitions as per management forecast • Other key considerations included: Review of Hub’s competitive positioning within each of its segments Pool of potential acquisition/consolidation targets Financial Analysis |

18 DCF Analysis – Consolidated Business Model • Consolidated forecasts were obtained by combining results from each hub and adjusting for corporate expenses • Additional considerations included: Potential outcome of class action litigation concerning contingent commissions Related party transactions with Fairfax • From the information gathered during our due diligence process, neither of the additional considerations necessitated adjustments to value Financial Analysis |

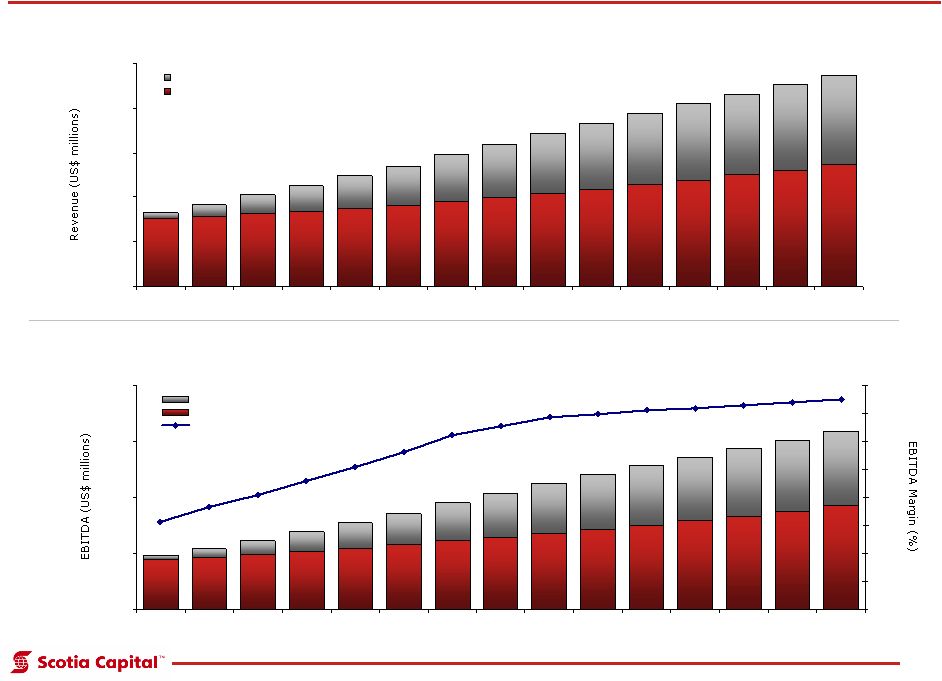

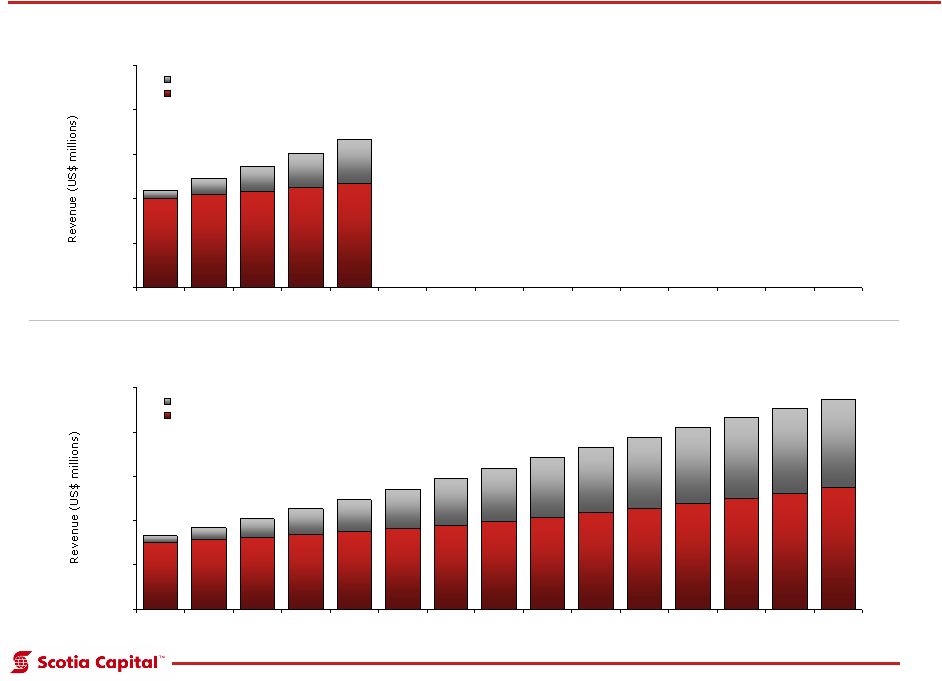

19 Summary of Projections Total Revenue (2007E – 2021E) Total EBITDA (2007E – 2021E) Financial Analysis $605 $626 $648 $672 $698 $726 $757 $791 $827 $866 $907 $951 $997 $1,047 $1,099 $54 $111 $169 $230 $293 $358 $426 $487 $544 $597 $645 $690 $730 $765 $796 $660 $737 $817 $902 $990 $1,084 $1,183 $1,278 $1,371 $1,462 $1,552 $1,641 $1,727 $1,812 $1,895 $0 $400 $800 $1,200 $1,600 $2,000 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Acquisition Organic $176 $186 $195 $205 $217 $230 $244 $257 $272 $285 $300 $315 $332 $350 $368 $16 $33 $51 $70 $91 $113 $137 $158 $179 $197 $214 $229 $243 $256 $267 $192 $218 $246 $276 $308 $343 $381 $416 $450 $482 $514 $544 $575 $605 $635 29.1% 29.7% 30.1% 30.6% 31.1% 31.6% 32.2% 32.5% 32.9% 33.0% 33.1% 33.2% 33.3% 33.4% 33.5% $0 $200 $400 $600 $800 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 26% 27% 28% 29% 30% 31% 32% 33% 34% Acquisition Organic EBITDA Margin |

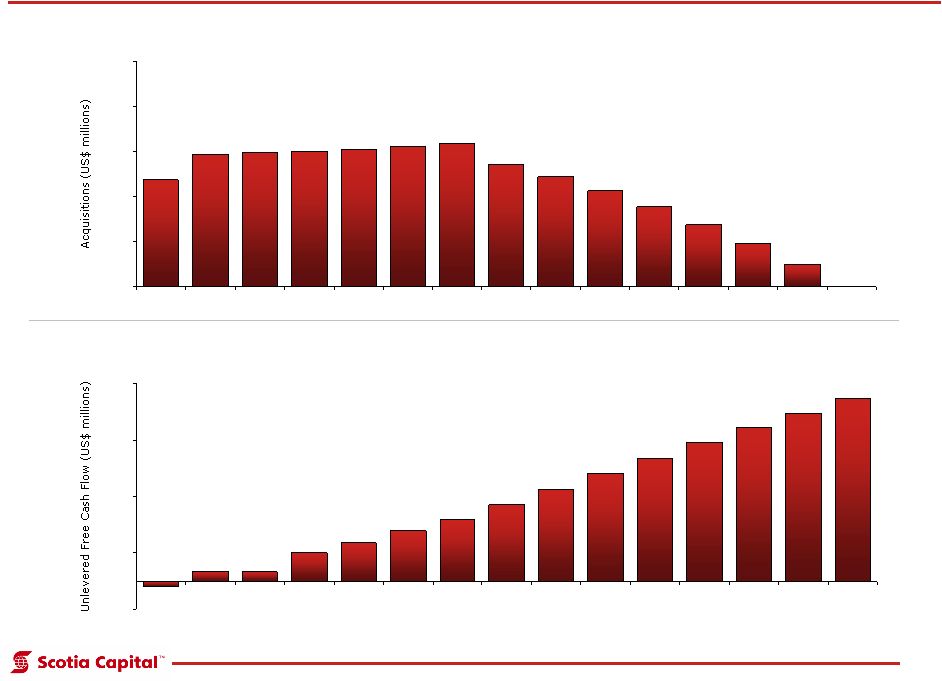

20 Summary of Projections Unlevered Free Cash Flow (2007E – 2021E) Cost of Acquisitions (2007E – 2021E) Financial Analysis $71 $88 $89 $91 $92 $94 $95 $81 $73 $63 $53 $41 $28 $15 $0 $0 $30 $60 $90 $120 $150 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E -$10 $17 $17 $50 $68 $89 $108 $136 $162 $192 $219 $246 $272 $297 $323 ($50) $50 $150 $250 $350 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E |

21 Key DCF Assumptions – Revenue • The revenue forecast is segmented into revenue generated by the existing organic business, and augmented by revenue generated by future acquisitions Forecasts for organic and acquired revenue from management projections • Organic revenue is segmented into four main revenue drivers calculated on a hub-by-hub basis: Commission and Fees income, Contingent Profit Sharing, Interest Income and Other Income Commission and Fees income is further broken down by major business line Financial Analysis Consolidated Revenue Forecast 2006A 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Organic Revenue Commissions & Fees Personal Lines $94.8 $104.0 $108.1 $112.4 $116.8 $121.4 $126.2 $131.2 $136.4 $141.9 $147.4 $153.2 $159.3 $165.6 $172.1 $179.0 Commercial Lines $256.9 $289.3 $301.0 $313.1 $325.8 $339.0 $352.7 $367.1 $382.0 $397.6 $413.9 $430.9 $448.6 $467.1 $486.5 $506.6 Wholesale $67.6 $72.9 $74.2 $75.6 $76.9 $78.3 $79.7 $81.2 $82.7 $84.2 $85.8 $87.4 $89.0 $90.6 $92.3 $94.1 Life/Grp/Investment Products $69.0 $76.0 $79.1 $82.4 $85.9 $89.5 $93.2 $97.2 $101.3 $105.5 $110.0 $114.7 $119.5 $124.6 $130.0 $135.5 Financial Institutions $9.4 $11.3 $11.7 $12.0 $12.4 $12.7 $13.1 $13.5 $13.9 $14.3 $14.8 $15.2 $15.7 $16.1 $16.6 $17.1 ICBC $21.6 $23.0 $23.9 $24.9 $25.9 $26.9 $28.0 $29.1 $30.3 $31.5 $32.8 $34.1 $35.4 $36.8 $38.3 $39.8 Reinsurance $7.1 $7.1 $7.4 $7.7 $8.0 $8.3 $8.6 $9.0 $9.3 $9.7 $10.1 $10.5 $10.9 $11.4 $11.8 $12.3 Sub-Broker Commission Expense ($43.1) ($46.7) ($48.5) ($50.3) ($52.2) ($54.2) ($56.3) ($58.4) ($60.6) ($63.0) ($65.4) ($67.9) ($70.5) ($73.2) ($76.0) ($78.9) Total Commissions & Fees $483.2 $537.0 $556.9 $577.7 $599.4 $621.9 $645.4 $669.9 $695.3 $721.9 $749.4 $778.1 $808.0 $839.2 $871.6 $905.5 YOY Growth - % n.a. 11.1% 3.7% 3.7% 3.7% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.9% 3.9% 3.9% Contingent Profit Sharing/Volume Overrides $44.7 $47.0 $48.2 $48.2 $48.2 $48.2 $48.7 $50.5 $52.5 $54.6 $56.7 $59.0 $61.4 $63.8 $66.4 $69.0 Interest Income $7.2 $10.6 $9.3 $10.3 $12.0 $14.8 $18.5 $23.1 $28.8 $35.7 $44.0 $53.6 $64.5 $76.8 $90.4 $105.4 Total Other Income $8.5 $10.8 $11.4 $11.8 $12.3 $12.8 $13.3 $13.8 $14.4 $14.9 $15.5 $16.1 $16.8 $17.5 $18.2 $18.9 Total Organic Revenue $543.6 $605.4 $625.8 $648.1 $671.9 $697.7 $725.9 $757.3 $791.0 $827.1 $865.7 $906.8 $950.7 $997.2 $1,046.6 $1,098.8 YOY Growth - % n.a. 11.4% 3.4% 3.6% 3.7% 3.8% 4.0% 4.3% 4.4% 4.6% 4.7% 4.8% 4.8% 4.9% 4.9% 5.0% New Acquired Revenue $0.0 $54.4 $54.2 $54.0 $53.9 $53.8 $53.8 $53.8 $43.8 $37.5 $31.3 $25.0 $18.8 $12.5 $6.3 $0.0 Growth in Acquired Revenue $0.0 $0.0 $56.5 $115.1 $175.9 $238.9 $304.3 $372.3 $443.1 $506.3 $565.4 $620.5 $671.2 $717.5 $759.1 $795.9 Total Acquired Revenue $0.0 $54.4 $110.7 $169.1 $229.7 $292.6 $358.1 $426.1 $486.8 $543.8 $596.7 $645.5 $690.0 $730.0 $765.3 $795.9 YOY Growth - % n.a. n.a. 103.6% 52.8% 35.8% 27.4% 22.4% 19.0% 14.3% 11.7% 9.7% 8.2% 6.9% 5.8% 4.8% 4.0% Total Revenue $543.6 $659.7 $736.5 $817.2 $901.6 $990.3 $1,083.9 $1,183.4 $1,277.8 $1,370.8 $1,462.3 $1,552.3 $1,640.6 $1,727.2 $1,811.9 $1,894.7 YOY Growth - % n.a. 21.4% 11.6% 11.0% 10.3% 9.8% 9.5% 9.2% 8.0% 7.3% 6.7% 6.2% 5.7% 5.3% 4.9% 4.6% |

22 Key DCF Assumptions – Revenue • Revenue growth rates are based on management’s forecast, and then adjusted based on discussions held with management Base case commission and fees revenue growth of 4.0% for all product lines except wholesale, which is grown at 2.0% All commission and fees growth rates increased by 2.0% in the Pacific and Fortun hubs, and decreased by 1.0% and 2.0% in the Midwest and Ontario hubs respectively Financial Analysis Key Revenue Growth Assumptions 2006A 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Organic Revenue Growth Commissions & Fees Personal Lines n.a. 9.8% 3.9% 3.9% 3.9% 4.0% 4.0% 4.0% 4.0% 4.0% 3.9% 3.9% 3.9% 4.0% 4.0% 4.0% Commercial Lines n.a. 12.6% 4.0% 4.0% 4.0% 4.1% 4.1% 4.1% 4.1% 4.1% 4.1% 4.1% 4.1% 4.1% 4.1% 4.1% Wholesale n.a. 7.9% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.8% 1.9% 1.9% 1.9% 1.9% 1.9% Life/Grp/Investment Products n.a. 10.1% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2% 4.3% 4.3% 4.3% 4.3% Financial Institutions n.a. 20.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% ICBC n.a. 6.4% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% Reinsurance n.a. 0.5% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% Sub-Broker Commission Expense n.a. 8.4% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.9% 3.9% Total Commissions & Fees n.a. 11.1% 3.7% 3.7% 3.7% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.9% 3.9% 3.9% YOY Growth - % n.a. 11.1% 3.7% 3.7% 3.7% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.8% 3.9% 3.9% 3.9% Contingent Profit Sharing/Volume Overrides n.a. 5.1% 2.5% 0.1% (0.0%) (0.1%) 1.1% 3.8% 3.8% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% Interest Income n.a. 47.2% (11.8%) 10.2% 16.3% 23.3% 25.1% 25.2% 24.7% 24.0% 23.1% 21.8% 20.4% 19.0% 17.7% 16.6% Total Other Income n.a. 27.1% 5.6% 3.5% 4.2% 4.1% 3.9% 3.8% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% Organic Revenue Growth n.a. 11.4% 3.4% 3.6% 3.7% 3.8% 4.0% 4.3% 4.4% 4.6% 4.7% 4.8% 4.8% 4.9% 4.9% 5.0% Overall Revenue Growth Total Acquired Revenue Growth n.a. n.a. 103.6% 52.8% 35.8% 27.4% 22.4% 19.0% 14.3% 11.7% 9.7% 8.2% 6.9% 5.8% 4.8% 4.0% Growth of Previously Acquired Revenue n.a. n.a. 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% Total Revenue Growth n.a. 21.4% 11.6% 11.0% 10.3% 9.8% 9.5% 9.2% 8.0% 7.3% 6.7% 6.2% 5.7% 5.3% 4.9% 4.6% |

23 Key DCF Assumptions – Expenses • Organic expenses as per 2007E management budget and grown as a percentage of revenue in line with management forecast Acquired expense assumptions in line with organic margin forecasts Financial Analysis Consolidated Expenses Forecast 2006A 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Organic Expenses Compensation $295.9 $326.4 $334.4 $344.5 $355.3 $366.8 $378.5 $391.5 $406.3 $422.2 $440.8 $460.5 $482.1 $504.9 $528.8 $554.5 Selling $21.7 $21.7 $21.6 $21.5 $21.3 $20.9 $21.2 $21.5 $22.3 $23.1 $24.1 $25.1 $26.2 $27.5 $28.7 $30.1 Occupancy $25.3 $26.5 $28.0 $29.7 $31.4 $33.3 $34.8 $36.3 $38.0 $39.8 $41.6 $43.6 $45.7 $47.9 $50.1 $52.6 Administration $54.1 $50.3 $51.4 $52.6 $53.9 $55.3 $57.5 $59.7 $62.7 $65.7 $69.0 $72.4 $76.0 $79.7 $83.5 $87.5 Corporate Expenses $0.0 $4.1 $4.9 $4.8 $4.6 $4.5 $4.3 $4.2 $4.4 $4.6 $4.8 $5.0 $5.2 $5.5 $5.8 $6.0 Total Organic Expenses $396.9 $429.0 $440.3 $453.1 $466.5 $480.8 $496.3 $513.3 $533.6 $555.3 $580.3 $606.6 $635.2 $665.3 $697.0 $730.7 Acquired Expenses $0.0 $38.1 $77.0 $117.0 $157.9 $199.8 $242.7 $286.5 $325.7 $362.1 $396.7 $428.2 $457.2 $483.0 $505.5 $524.9 Corporate Expenses $0.0 $0.4 $0.9 $1.2 $1.6 $1.9 $2.1 $2.3 $2.7 $3.0 $3.3 $3.6 $3.8 $4.0 $4.2 $4.4 Total Acquired Expenses $0.0 $38.5 $77.9 $118.2 $159.5 $201.7 $244.8 $288.8 $328.4 $365.1 $400.0 $431.8 $461.0 $487.0 $509.7 $529.3 Total Compensation, Selling & Occupancy $396.9 $467.5 $518.1 $571.3 $626.0 $682.5 $741.0 $802.1 $862.0 $920.4 $980.2 $1,038.3 $1,096.2 $1,152.4 $1,206.6 $1,260.0 Key Expense Margin Assumptions 2006A 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Organic Expenses as a % of Organic Revenue Compensation 54.4% 53.9% 53.4% 53.2% 52.9% 52.6% 52.1% 51.7% 51.4% 51.0% 50.9% 50.8% 50.7% 50.6% 50.5% 50.5% Selling 4.0% 3.6% 3.5% 3.3% 3.2% 3.0% 2.9% 2.8% 2.8% 2.8% 2.8% 2.8% 2.8% 2.8% 2.7% 2.7% Occupancy 4.7% 4.4% 4.5% 4.6% 4.7% 4.8% 4.8% 4.8% 4.8% 4.8% 4.8% 4.8% 4.8% 4.8% 4.8% 4.8% Administration 9.9% 8.3% 8.2% 8.1% 8.0% 7.9% 7.9% 7.9% 7.9% 7.9% 8.0% 8.0% 8.0% 8.0% 8.0% 8.0% Corporate Expenses 0.0% 0.7% 0.8% 0.7% 0.7% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% Total Organic Expenses 73.0% 70.9% 70.3% 69.9% 69.4% 68.9% 68.4% 67.8% 67.5% 67.1% 67.0% 66.9% 66.8% 66.7% 66.6% 66.5% Acquired Expenses as a % of Acquired Revenue Acquired Expenses n.a. 70.2% 69.6% 69.2% 68.7% 68.3% 67.8% 67.2% 66.9% 66.6% 66.5% 66.3% 66.3% 66.2% 66.0% 66.0% Corporate Expenses n.a. 0.7% 0.8% 0.7% 0.7% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% 0.6% Total Acquired Expenses n.a. 70.9% 70.3% 69.9% 69.4% 68.9% 68.4% 67.8% 67.5% 67.1% 67.0% 66.9% 66.8% 66.7% 66.6% 66.5% Total Expenses (as a % of Total Revenue) 73.0% 70.9% 70.3% 69.9% 69.4% 68.9% 68.4% 67.8% 67.5% 67.1% 67.0% 66.9% 66.8% 66.7% 66.6% 66.5% |

24 Key DCF Assumptions – Acquisitions • Annual acquired revenue in line with management projections Average revenue per target based on the average revenue of acquisitions in 2006 (adjusted for the high and low of the group) • EBITDA margin of acquisitions in line with forecasted organic margins • Purchase price as a multiple of EBITDA estimated at 6.0x in 2007, 7.0x from 2008 to 2013, and increasing by 0.22x per year throughout the remainder of the forecast period (8.5x by 2020) 1.5x EBITDA allocated for earnout, which is subsequently paid out over a 3-year period (initial payment occurring in the year of acquisition) • All acquisitions and earnout payments are made with cash Financial Analysis Acquisition Forecast 2006A 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Acquisitions per Year n.a. 25.2 25.1 25.0 25.0 24.9 24.9 24.9 20.3 17.4 14.5 11.6 8.7 5.8 2.9 0.0 Growth - % of Prior Year Total Revenue n.a. 10.0% 8.2% 7.3% 6.6% 6.0% 5.4% 5.0% 3.7% 2.9% 2.3% 1.7% 1.2% 0.8% 0.4% 0.0% EBITDA Margin of Acquisitions - % n.a. 29.1% 29.7% 30.1% 30.6% 31.1% 31.6% 32.2% 32.5% 32.9% 33.0% 33.1% 33.2% 33.3% 33.4% 33.5% Acquired EBITDA n.a. $15.8 $16.1 $16.2 $16.5 $16.7 $17.0 $17.3 $14.2 $12.3 $10.3 $8.3 $6.2 $4.2 $2.1 $0.0 Acquisition EBITDA Multiple n.a. 6.0x 7.0x 7.0x 7.0x 7.0x 7.0x 7.0x 7.2x 7.4x 7.7x 7.9x 8.1x 8.3x 8.5x 8.5x Earnout Component (EBITDA Multiple) n.a. 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x 1.5x Initial Outlay for Business (EBITDA Multiple) n.a. 4.5x 5.5x 5.5x 5.5x 5.5x 5.5x 5.5x 5.7x 5.9x 6.2x 6.4x 6.6x 6.8x 7.0x 7.0x Amortization of Earnout (Annual Payment) n.a. 0.50x 0.50x 0.50x 0.50x 0.50x 0.50x 0.50x 0.50x 0.50x 0.50x 0.50x 0.50x 0.50x 0.75x 0.75x Cash Outlay for Acquisitions n.a. $71.2 $88.3 $89.4 $90.5 $91.9 $93.5 $95.3 $81.4 $73.2 $63.5 $52.8 $41.1 $28.4 $14.7 $0.0 Earnout (Incl. Prior Years' Earnout) n.a. $7.9 $15.9 $24.1 $24.4 $24.7 $25.1 $25.5 $24.3 $21.9 $18.4 $15.5 $12.4 $9.3 $6.8 $3.6 Annual Cash Outlay for Acquisitions n.a. $79.2 $104.2 $113.4 $114.9 $116.6 $118.6 $120.8 $105.7 $95.1 $81.9 $68.3 $53.5 $37.7 $21.5 $3.6 Earnouts from Pre-Forecast Acquisitions n.a. $42.4 $13.4 $20.7 $4.2 $2.7 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 Total Earnout n.a. $50.3 $29.3 $44.8 $28.6 $27.4 $25.1 $25.5 $24.3 $21.9 $18.4 $15.5 $12.4 $9.3 $6.8 $3.6 |

25 Revenue Projections Financial Analysis Management Revenue Forecast (2007E – 2011E) Revised Revenue Forecast (2007E – 2021E) $605 $626 $648 $672 $698 $726 $757 $791 $827 $866 $907 $951 $997 $1,047 $1,099 $54 $111 $169 $230 $293 $358 $426 $487 $544 $597 $645 $690 $730 $765 $796 $660 $737 $817 $902 $990 $1,084 $1,183 $1,278 $1,371 $1,462 $1,552 $1,641 $1,727 $1,812 $1,895 $0 $400 $800 $1,200 $1,600 $2,000 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Acquisition Organic $603 $625 $650 $676 $705 $55 $111 $169 $229 $292 $658 $737 $819 $905 $997 $0 $300 $600 $900 $1,200 $1,500 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Acquisition Organic |

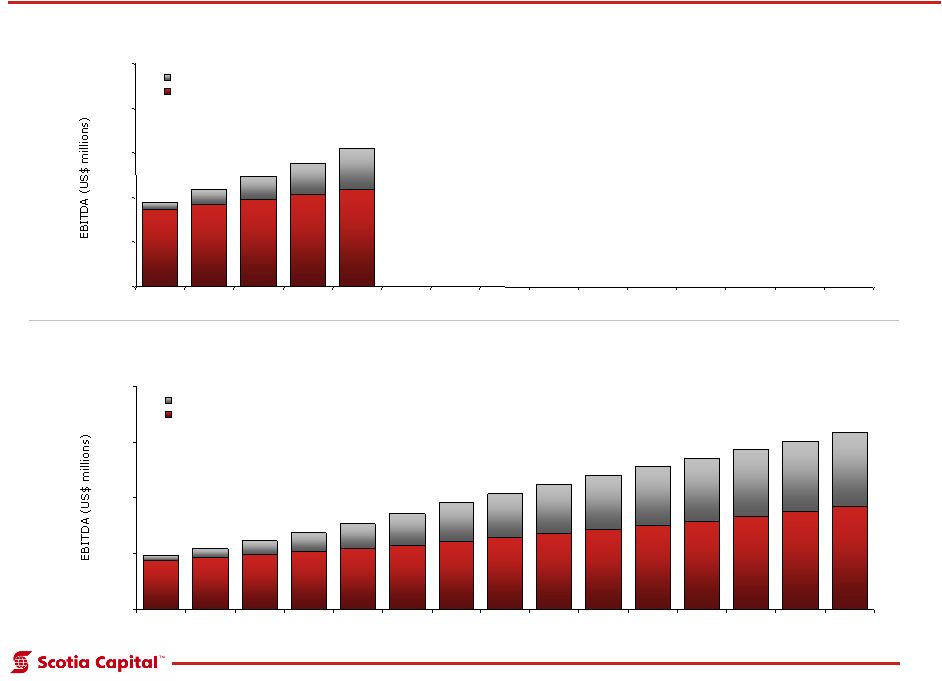

26 EBITDA Projections Management EBITDA Forecast (2007E – 2011E) Revised EBITDA Forecast (2007E – 2021E) Financial Analysis $176 $186 $195 $205 $217 $230 $244 $257 $272 $285 $300 $315 $332 $350 $368 $16 $33 $51 $70 $91 $113 $137 $158 $179 $197 $214 $229 $243 $256 $267 $192 $218 $246 $276 $308 $343 $381 $635 $605 $575 $544 $514 $482 $450 $416 $0 $200 $400 $600 $800 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Acquisition Organic $173 $184 $195 $206 $218 $16 $33 $51 $70 $91 $189 $217 $246 $276 $309 $0 $100 $200 $300 $400 $500 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Acquisition Organic |

27 Unlevered Free Cash Flows – Standalone Financial Analysis (US$ millions) 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Unlevered Free Cash Flow 21.4% 11.6% 11.0% 10.3% 9.8% 9.5% 9.2% 8.0% 7.3% 6.7% 6.2% 5.7% 5.3% 4.9% 4.6% Organic Revenue (0% Dis-Synergies) $605.4 $625.8 $648.1 $671.9 $697.7 $725.9 $757.3 $791.0 $827.1 $865.7 $906.8 $950.7 $997.2 $1,046.6 $1,098.8 Acquisition Revenue $54.4 $110.7 $169.1 $229.7 $292.6 $358.1 $426.1 $486.8 $543.8 $596.7 $645.5 $690.0 $730.0 $765.3 $795.9 Total Revenue $659.7 $736.5 $817.2 $901.6 $990.3 $1,083.9 $1,183.4 $1,277.8 $1,370.8 $1,462.3 $1,552.3 $1,640.6 $1,727.2 $1,811.9 $1,894.7 Organic EBITDA $176.3 $185.6 $195.0 $205.4 $216.8 $229.6 $244.0 $257.4 $271.8 $285.4 $300.2 $315.5 $331.9 $349.6 $368.1 Acquisition EBITDA $15.8 $32.8 $50.9 $70.2 $91.0 $113.3 $137.3 $158.4 $178.7 $196.7 $213.7 $228.9 $243.0 $255.7 $266.6 EBITDA $192.2 $218.4 $245.9 $275.6 $307.8 $342.9 $381.3 $415.8 $450.5 $482.1 $514.0 $544.4 $574.9 $605.3 $634.7 Margin -% 29.1% 29.7% 30.1% 30.6% 31.1% 31.6% 32.2% 32.5% 32.9% 33.0% 33.1% 33.2% 33.3% 33.4% 33.5% Add: SG&A Synergies (0%) $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 Add: Corporate Synergies (0%) $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 Less: Interest Income from Cash ($4.4) ($3.3) ($3.5) ($4.4) ($6.4) ($9.3) ($13.1) ($17.9) ($24.0) ($31.4) ($40.2) ($50.4) ($61.9) ($74.7) ($89.0) Adjusted EBITDA $187.8 $215.1 $242.4 $271.2 $301.4 $333.6 $368.2 $397.9 $426.5 $450.7 $473.7 $494.0 $513.0 $530.6 $545.7 Margin -% 28.5% 29.2% 29.7% 30.1% 30.4% 30.8% 31.1% 31.1% 31.1% 30.8% 30.5% 30.1% 29.7% 29.3% 28.8% Less: Depreciation and Amortization ($40.3) ($44.0) ($47.8) ($52.0) ($56.2) ($63.0) ($68.8) ($65.0) ($67.9) ($71.0) ($73.8) ($76.3) ($78.2) ($79.6) ($80.5) EBIT $147.5 $171.0 $194.6 $219.2 $245.1 $270.6 $299.4 $333.0 $358.6 $379.7 $399.9 $417.8 $434.8 $450.9 $465.3 Income Tax Rate 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% Less: Taxes ($55.3) ($64.1) ($73.0) ($82.2) ($91.9) ($101.5) ($112.3) ($124.9) ($134.5) ($142.4) ($150.0) ($156.7) ($163.0) ($169.1) ($174.5) Unlevered Net Income $92.2 $106.9 $121.6 $137.0 $153.2 $169.1 $187.1 $208.1 $224.1 $237.3 $249.9 $261.1 $271.7 $281.8 $290.8 Less: Capital Expenditures ($14.7) ($15.6) ($16.4) ($18.0) ($19.9) ($21.7) ($23.9) ($26.0) ($28.2) ($30.2) ($32.2) ($34.1) ($36.0) ($37.9) ($39.7) Less: Cost of Acquisitions (Incl. Earnout) ($121.5) ($117.6) ($134.1) ($119.1) ($119.3) ($118.6) ($120.8) ($105.7) ($95.1) ($81.9) ($68.3) ($53.5) ($37.7) ($21.5) ($3.6) Less: Investment in Working Capital ($5.9) ($0.7) ($1.4) ($2.0) ($2.2) ($2.7) ($3.2) ($5.8) ($6.2) ($4.1) ($4.7) ($3.9) ($4.3) ($4.7) ($4.4) Add: Depreciation and Amortization $40.3 $44.0 $47.8 $52.0 $56.2 $63.0 $68.8 $65.0 $67.9 $71.0 $73.8 $76.3 $78.2 $79.6 $80.5 Unlevered Free Cash Flow ($9.7) $17.0 $17.5 $49.8 $68.1 $89.1 $108.1 $135.5 $162.5 $192.1 $218.7 $245.9 $271.9 $297.4 $323.5 Growth - % n.a. nmf 2.9% 184.8% 36.7% 30.8% 21.3% 25.4% 19.9% 18.2% 13.8% 12.5% 10.6% 9.4% 8.8% |

28 DCF Analysis – Terminal Value • Hub’s terminal value was modeled using the: Capitalization of “steady-state” cash flows into perpetuity using a constant revenue growth rate Multiple of EBITDA (as a check for reasonableness for the above) • Certain “normalizing” adjustments were made in the terminal year Capital expenditures maintained as a percentage of EBITDA in line with 2021E forecast Tax depreciation assumed to be equal to the amount of capital expenditures (net of acquisitions) No acquisitions estimated in the terminal period 37.5% tax rate consistent with historical Working capital consistent with 2021E as a percentage of total revenue • The capitalized free cash flow growth rate approach assumed revenue growth of 3.5% in perpetuity Consistent with forecast organic growth as per management forecast • The multiple of EBITDA approach assumed a range of 7.5x – 8.5x Financial Analysis |

29 DCF Analysis – WACC • The WACC was determined in reference to an optimal capital structure based upon risk/volatility parameters and our review of the capital structure of other similar corporate entities • Cash flows were discounted between 10.5% and 11.5%, based on the following: (1) 10-year U.S. Treasury as of February 9, 2007. (2) Based on sales weighted average of U.S. and Canadian equity risk premiums (7.1% and 5.3% respectively). (3) Re-levered beta calculated from unlevered betas of comparable North American insurance brokers. (4) Based on Ibbotson Low Cap 6th decile size premium. (5) Estimate based on spread of comparable North American insurance brokers with public debt. (6) Based on comparable North American insurance brokers. WACC Range Low High Cost of Equity Risk-Free Rate (1) 4.8% 4.8% Risk Premium (2) 6.7% 6.7% Re-Levered Beta (3) 0.90 1.00 Size Premium (4) 1.7% 1.7% Cost of Equity 12.5% 13.2% Cost of Debt Risk-Free Rate 4.8% 4.8% Spread Over Risk-Free Bonds (5) 1.5% 2.0% Long-Term Income Tax Rate 37.5% 37.5% Cost of Debt (After-Tax) 3.9% 4.2% Weighted Average Cost of Capital Equity Weighting 75.0% 85.0% Cost of Equity 12.5% 13.2% Debt Weighting (6) 25.0% 15.0% Cost of Debt (After-Tax) 3.9% 4.2% Calculated Weighted Average Cost of Capital 10.4% 11.8% Selected Weighted Average Cost of Capital 10.5% 11.5% Financial Analysis |

30 DCF Analysis – Implied Value (1) Includes $144.6 million of debt, $99.2 million of cash, and $15.7 million from the exercise of in-the-money options. (2) Including in-the-money outstanding options and restricted share units. (3) As at February 22, 2007. The DCF analysis indicates an equity value per share for Hub of $34.37 to $41.67 Financial Analysis US$ millions, except per share data Low High Selected weighted average cost of capital 11.5% 10.5% Present value of unlevered free cash flows $695.2 $760.6 Terminal Value Methodology: Capitalization of UFCF Unlevered free cash flow - selected terminal growth rate 3.5% 3.5% Present value of terminal value $793.5 $1,038.1 Enterprise Value $1,488.8 $1,798.8 Percentage of enterprise value from terminal period 53.3% 57.7% Capitalization Net Debt (1) ($29.7) ($29.7) Implied Equity $1,459.1 $1,769.1 Shares Outstanding - FD (2) 42.5 42.5 Implied Equity Value per Share $34.37 $41.67 Current Share Price (3) $34.20 $34.20 Premium Over Current Share Price - % 0.5% 21.8% |

31 Synergies Analysis • We understand that the Sponsors intend to operate Hub as a “standalone” entity The Sponsors have no intentions on merging Hub with any other portfolio company • It is possible that potential synergies exist with other potential strategic buyers • Estimated synergies include 25% of selling expenses and 50% of administration expenses • Other potential revenue or “best practices” synergies may be realizable in the future, although difficult to quantify and risk assess at this time • We have estimated that a purchaser would pay for half the synergies ($16 million of 2007E pre-tax savings included in the forecast) Financial Analysis 2007E Annual Savings Present Value 10.5% 11.5% Public Company Costs $2.1 $20.1 $18.4 Selling, General & Administrative $32.5 $423.2 $371.4 Net Present Value $443.3 $389.7 Less: One-time costs ($32.5) ($32.5) Net Present Value of Synergies (100%) $410.8 $357.3 |

32 Synergies Analysis - Contingent Commissions • As Hub generates a significant level of contingent commission revenue, it is possible that certain strategic buyers may suffer dis-synergies in effecting an acquisition of Hub In 2004/2005, in response to actions commenced by the New York State Attorney General and the Superintendent of the New York State Insurance Department, Marsh & McLennan Cos., Aon Corp., Willis Group Holdings, and Arthur J. Gallagher & Co., agreed to forego contingent commissions Furthermore, a number of insurance carriers, including St. Paul Travelers, Zurich Financial, Chubb Corp., and Metropolitan Life have agreed to no longer pay some or all contingent fees • Recent initiatives by those in the industry directly affected by the loss of contingent commissions may have created a solution to partially replace the losses of contingent commission revenue Industry participants, including Chubb and St. Paul Travelers have effectively developed a “fixed commission” structure tied to producer performance, which is similar in nature to contingent commissions, and has received the approval of the New York State Attorney General According to a recent Chubb agreement, a fixed commission paid to a producer, set prior to the sale of a particular insurance product, and that may be based on, among other things, the prior year's performance of the producer'' is not considered contingent compensation and thus is permitted • Notwithstanding the foregoing, the remaining uncertainty around contingent commissions may suggest the most logical strategic buyers (Marsh & McLennan Cos., Aon Corp., Willis Group Holdings, and Arthur J. Gallagher & Co.,) may be hesitant to acquire any insurance brokerage that currently earns contingent commission revenue Financial Analysis |

33 Revenue Dis-Synergies • In addition to cost savings, strategic acquirors may face the potential loss of revenue from the departure of brokers and the associated insurance contracts Contracts often reside with the relationship, not with the Company • In our analysis we have assumed that Hub would lose 10% of top-line organic commission revenue • The potential enterprise value impact of revenue dis-synergies is $127 million to $147 million Financial Analysis Present Value Adjustment 10.5% 11.5% Total Revenue ($53.6) Total EBITDA ($18.2) NPV of Dis-Synergies $127.3 $147.2 |

34 Unlevered Free Cash Flows –Synergies/Dis-Synergies Financial Analysis (US$ millions) 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E Unlevered Free Cash Flow 11.5% 12.2% 11.5% 10.8% 10.2% 9.8% 9.5% 8.2% 7.4% 6.8% 6.2% 5.8% 5.3% 4.9% 4.6% Organic Revenue (10% Dis-Synergies) $551.7 $569.2 $588.9 $610.1 $633.1 $658.4 $686.8 $717.3 $750.1 $785.2 $822.7 $862.7 $905.2 $950.4 $998.3 Acquisition Revenue $54.4 $110.7 $169.1 $229.7 $292.6 $358.1 $426.1 $486.8 $543.8 $596.7 $645.5 $690.0 $730.0 $765.3 $795.9 Total Revenue $606.1 $679.9 $758.1 $839.8 $925.8 $1,016.5 $1,112.9 $1,204.2 $1,293.9 $1,381.9 $1,468.2 $1,552.7 $1,635.2 $1,715.7 $1,794.1 Organic EBITDA $158.4 $166.5 $174.8 $183.9 $194.0 $205.3 $218.2 $230.1 $242.9 $255.1 $268.4 $282.0 $296.9 $312.9 $329.7 Acquisition EBITDA $15.6 $32.4 $50.2 $69.2 $89.6 $111.7 $135.4 $156.2 $176.1 $193.8 $210.6 $225.6 $239.4 $252.0 $262.8 EBITDA $174.0 $198.9 $225.0 $253.1 $283.6 $317.0 $353.6 $386.3 $419.0 $448.9 $478.9 $507.6 $536.3 $564.9 $592.5 Margin -% 28.7% 29.3% 29.7% 30.1% 30.6% 31.2% 31.8% 32.1% 32.4% 32.5% 32.6% 32.7% 32.8% 32.9% 33.0% Add: SG&A Synergies (50%) $16.2 $15.5 $17.1 $18.7 $20.4 $22.1 $24.1 $26.2 $28.4 $30.6 $32.7 $34.8 $36.8 $38.8 $40.6 Add: Corporate Synergies (100%) $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 $2.1 Less: Interest Income from Cash ($4.4) ($2.8) ($2.6) ($3.1) ($4.6) ($6.9) ($10.1) ($14.4) ($19.8) ($26.5) ($34.6) ($43.9) ($54.5) ($66.4) ($79.7) Adjusted EBITDA $187.9 $213.7 $241.6 $270.9 $301.6 $334.3 $369.7 $400.2 $429.8 $455.0 $479.2 $500.7 $520.7 $539.3 $555.5 Margin -% 31.0% 31.4% 31.9% 32.3% 32.6% 32.9% 33.2% 33.2% 33.2% 32.9% 32.6% 32.2% 31.8% 31.4% 31.0% Less: Depreciation and Amortization ($40.0) ($43.3) ($46.7) ($50.6) ($54.5) ($61.1) ($66.6) ($62.8) ($65.6) ($68.6) ($71.4) ($73.7) ($75.5) ($76.8) ($77.5) EBIT $147.9 $170.3 $194.8 $220.3 $247.1 $273.2 $303.1 $337.4 $364.1 $386.4 $407.9 $427.0 $445.2 $462.5 $478.0 Income Tax Rate 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% 37.5% Less: Taxes ($55.5) ($63.9) ($73.1) ($82.6) ($92.6) ($102.5) ($113.7) ($126.5) ($136.5) ($144.9) ($152.9) ($160.1) ($167.0) ($173.4) ($179.2) Unlevered Net Income $92.4 $106.5 $121.8 $137.7 $154.4 $170.8 $189.4 $210.9 $227.6 $241.5 $254.9 $266.9 $278.3 $289.1 $298.7 Less: Capital Expenditures ($13.3) ($14.2) ($15.0) ($16.6) ($18.3) ($20.1) ($22.1) ($24.2) ($26.2) ($28.1) ($30.0) ($31.8) ($33.6) ($35.3) ($37.1) Less: Cost of Acquisitions (Incl. Earnout) ($120.4) ($116.2) ($132.6) ($117.5) ($117.6) ($116.9) ($119.1) ($104.2) ($93.8) ($80.7) ($67.3) ($52.7) ($37.1) ($21.1) ($3.6) Less: Investment in Working Capital ($2.5) ($0.6) ($1.0) ($1.5) ($1.7) ($2.2) ($2.7) ($5.1) ($5.5) ($3.5) ($4.1) ($3.4) ($3.8) ($4.2) ($4.0) Add: Depreciation and Amortization $40.0 $43.3 $46.7 $50.6 $54.5 $61.1 $66.6 $62.8 $65.6 $68.6 $71.4 $73.7 $75.5 $76.8 $77.5 Unlevered Free Cash Flow ($3.8) $18.8 $20.0 $52.7 $71.3 $92.6 $112.1 $140.2 $167.7 $197.8 $225.0 $252.7 $279.2 $305.1 $331.6 Growth - % n.a. nmf 6.1% 163.8% 35.4% 29.9% 21.1% 25.1% 19.6% 18.0% 13.7% 12.3% 10.5% 9.3% 8.7% |

35 DCF Analysis – Implied Value The DCF analysis indicates an equity value per share for Hub of $35.57 to $43.07 Financial Analysis (1) Includes $144.6 million of debt, $99.2 million of cash, and $15.7 million from the exercise of in-the-money options. (2) Including in-the-money outstanding options and restricted share units. (3) As at February 22, 2007. US$ millions, except per share data Low High Selected weighted average cost of capital 11.5% 10.5% Present value of unlevered free cash flows $725.9 $793.4 Terminal Value Methodology: Capitalization of UFCF Unlevered free cash flow - selected terminal growth rate 3.5% 3.5% Present value of terminal value $814.0 $1,064.9 Enterprise Value $1,539.9 $1,858.3 Percentage of enterprise value from terminal period 52.9% 57.3% Capitalization Net Debt (1) ($29.7) ($29.7) Implied Equity $1,510.2 $1,828.6 Shares Outstanding - FD (2) 42.5 42.5 Implied Equity Value per Share $35.57 $43.07 Current Share Price (3) $34.20 $34.20 Premium Over Current Share Price - % 4.0% 25.9% |

36 DCF Analysis – Sensitivity Analysis (1) Assumes WACC of 11.0% and terminal growth rate of 3.5%. (2) Represents initial EBITDA multiple paid for acquisitions from 2008 to 2013. EBITDA multiple in 2007 1.0x less than base case, and constant annual multiple increase of from base case of 0.22x from 2014 to 2021. Financial Analysis Revenue Growth +/- 1% $37.76 (3.0%) (2.0%) (1.0%) 0.0% 1.0% 2.0% 3.0% -2.0% $19.91 $24.12 $28.84 $34.15 $40.11 $46.79 $54.30 -1.0% $21.25 $25.60 $30.47 $35.95 $42.10 $49.01 $56.76 0.0% $22.59 $27.07 $32.11 $37.76 $44.10 $51.22 $59.21 1.0% $23.93 $28.55 $33.74 $39.56 $46.09 $53.43 $61.67 2.0% $25.27 $30.03 $35.37 $41.36 $48.09 $55.65 $64.13 Valuation Implied Share Price (US$) WACC $37.76 9.5% 10.0% 10.5% 11.0% 11.5% 12.0% 12.5% 3.00% $49.00 $44.13 $39.95 $36.35 $33.20 $30.44 $28.01 3.25% $50.27 $45.15 $40.78 $37.03 $33.77 $30.92 $28.41 3.50% $51.64 $46.24 $41.67 $37.76 $34.37 $31.42 $28.83 3.75% $53.12 $47.43 $42.63 $38.53 $35.01 $31.95 $29.27 4.00% $54.74 $48.71 $43.65 $39.37 $35.69 $32.51 $29.74 WACC $45.98 9.5% 10.0% 10.5% 11.0% 11.5% 12.0% 12.5% 7.0x $42.00 $39.60 $37.34 $35.23 $33.26 $31.41 $29.67 7.5x $43.65 $41.13 $38.78 $36.58 $34.51 $32.58 $30.77 8.0x $45.30 $42.67 $40.22 $37.92 $35.77 $33.76 $31.87 8.5x $46.95 $44.21 $41.66 $39.26 $37.03 $34.93 $32.97 9.0x $48.59 $45.75 $43.09 $40.61 $38.28 $36.10 $34.07 Operational (1) Implied Share Price (US$) % of Planned Acquisition Revenue (Per Year) $37.76 25.0% 50.0% 75.0% 100.0% 125.0% 150.0% 175.0% 6.0x $32.49 $34.83 $37.17 $39.53 $41.89 $44.27 $46.65 6.5x $32.27 $34.38 $36.51 $38.64 $40.78 $42.93 $45.06 7.0x $32.05 $33.94 $35.85 $37.76 $39.67 $41.58 $43.43 7.5x $31.83 $33.50 $35.18 $36.87 $38.56 $40.20 $41.79 8.0x $31.61 $33.06 $34.52 $35.99 $37.44 $38.81 $40.13 |

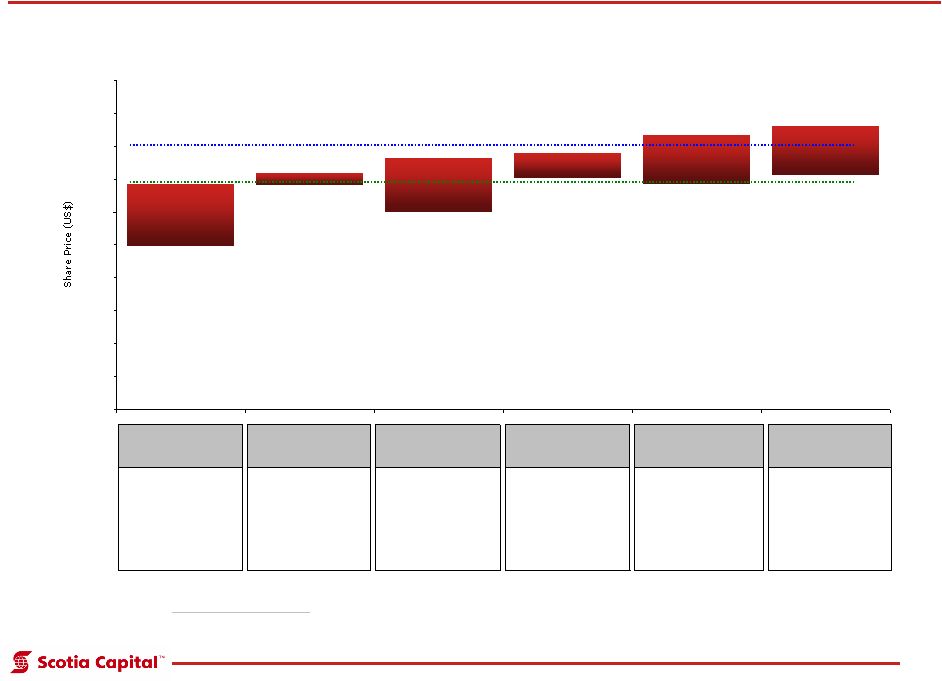

37 Trading History Research Analyst Price Targets Comparable Companies Precedent Transactions Discounted Cash Flow Discounted Cash incl. Synergies 52-week Analyst EV/2007E EV/2006PF WACC: 10.5% - 11.5% WACC: 10.5% - 11.5% High/Low 1-Year Price EBITDA EBITDA: TGR: 3.5% TGR: 3.5% 8.0x - 10.0x 10.0x - 11.0x Implied EV/ Implied EV/ 2007E 2006PF 2006PF EBITDA: 2006PF EBITDA: EBITDA EBITDA 9.3x-11.2x 9.5x-11.5x $173.4 million $160.7 million $34.00 $30.01 $35.19 $34.37 $35.57 $24.80 $34.20 $36.00 $38.18 $38.98 $41.67 $43.07 $0.00 $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 $40.00 $45.00 $50.00 Current Share Price: $34.20 Offer Price: $40.00 Summary of Methodologies (3) (2) (1) Financial Analysis (1) Price as at February 22, 2007. (2) 2007E EBITDA management projections, adjusted for 2007E related acquisitions. (3) Pro forma 2006 acquisitions per management presentation. (3) (3) |

Fairness Considerations |

39 Key Factors • Voting agreement with Fairfax demonstrate arm’s length negotiation of value Voting Agreement • Public Shareholders are expecting procedural fairness and some degree of comfort that other potential bidders have not been unreasonably excluded • “Go-shop” clause may provide a credible market test Length of period and break fee appear to be consistent with precedents Procedural Fairness • We understand that current senior management intend to sell 50% of their equity interest in Hub and roll-over the remainder as part of the proposed transaction Related-Party Transactions • We understand that Apax approached Hub’s CEO in early January and expressed an initial interest in acquiring Hub, suggesting a 20% premium to market (approx $37.67 per share) • After Hub deemed the initial offer inadequate, Apax, now in partnership with Morgan Stanley, tabled a second offer of $40.00 per share • The management of Hub has indicated their support for the revised proposal • The special committee has negotiated terms with the Sponsors including a “Go-shop” provision upon public announcement of the transaction Considerations Process Leading to Apax Offer Key Factors • In assessing the fairness of the consideration offered to Public Shareholders, from a financial point of view, Scotia Capital has considered the following factors: Fairness Considerations |

40 Observations • After reviewing the key factors, Scotia Capital observed the following: The offer price reflects a significant premium over the recent and historical trading price The consideration offered is within the assessment range The implied transaction multiples are in line with precedent transaction multiples The offer provides the Public Shareholders with immediate liquidity Fairness Considerations |

Overview of Hub International Appendix 1 |

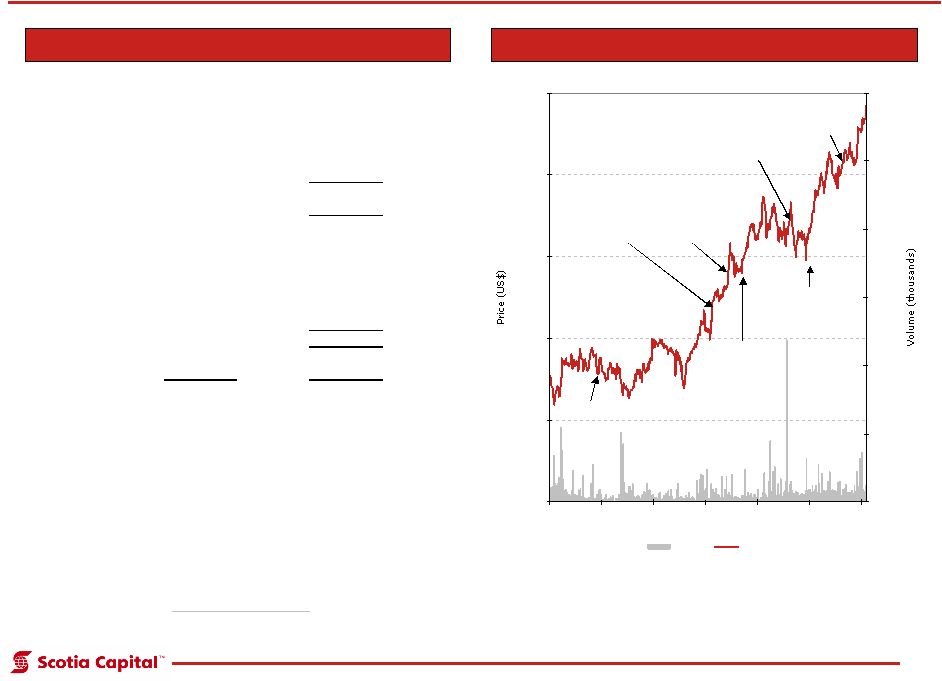

42 Market Profile Trading Performance Capitalization and Implied Valuation (1) Excludes trust cash. (2) Management projection including contingent payments. (3) Estimates from I/B/E/S. Overview of Hub International $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 Feb-04 Aug-04 Feb-05 Aug-05 Feb-06 Aug-06 Feb-07 0 500 1,000 1,500 2,000 2,500 3,000 Volume Price Jul. 27, 2006 Reports strong Q2 06 results indicating a 38% increase in net revenue year over year Dec. 13, 2005 Hub, in partnership with Wellpoint Health Services, announces launch of new healthcare program May 12, 2006 Announces that it will offe 4,000,000 common share in a public offering Oct. 26, 2006 Reports Q3 06 results with $0.17/sh vs. ($0.01)/sh in the prior year Sep. 1, 2005 Announces the fold- in acquisition of The Innovators Insurance Agencies May 3, 2005 Announces acquisition of THB Intermediaries Inc. Oct. 26, 2005 Reports Q3 05 results indicating 7% revenue growth of which 5% is organic Jul. 29, 2004 Reports Q2 06 results demonstrating an 11% increase in revenues year over year (US$, million except share price) Recent Share Price $34.20 Basic Shares Outstanding 39.5 Add: In-the-Money Options 1.0 Add: Restricted Share Units 2.0 FD Shares Outstanding 42.5 Market Capitalization $1,451.9 Add: Debt (1) $144.6 Add: Contingent Payments (2) $83.3 Less: Cash ($99.2) Less: Cash from options ($15.7) Enterprise Value $1,564.9 Base (3) Multiple Revenue 2006E $550.1 2.8x 2007E $646.3 2.4x EV/EBITDA 2006E $147.8 10.6x 2007E $179.2 8.7x P/E 2006E $1.56 21.9x 2007E $1.94 17.7x |

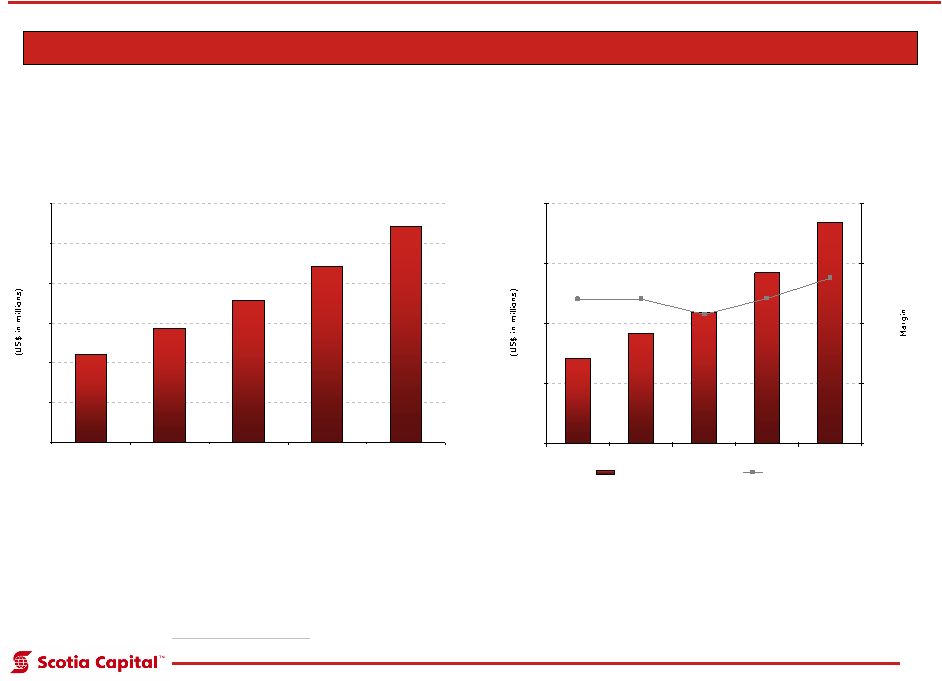

43 Financial Results Revenue EBITDA Hub has expanded EBITDA margins while growing revenues organically and via acquisitions Source: Management presentation. Overview of Hub International $56 $73 $87 $114 $147 26% 26% 25% 26% 27% $0 $40 $80 $120 $160 2002 2003 2004 2005 2006E 16.0% 20.0% 24.0% 28.0% 32.0% EBITDA EBITDA Margin $220 $286 $355 $443 $544 $0 $100 $200 $300 $400 $500 $600 2002 2003 2004 2005 2006E |

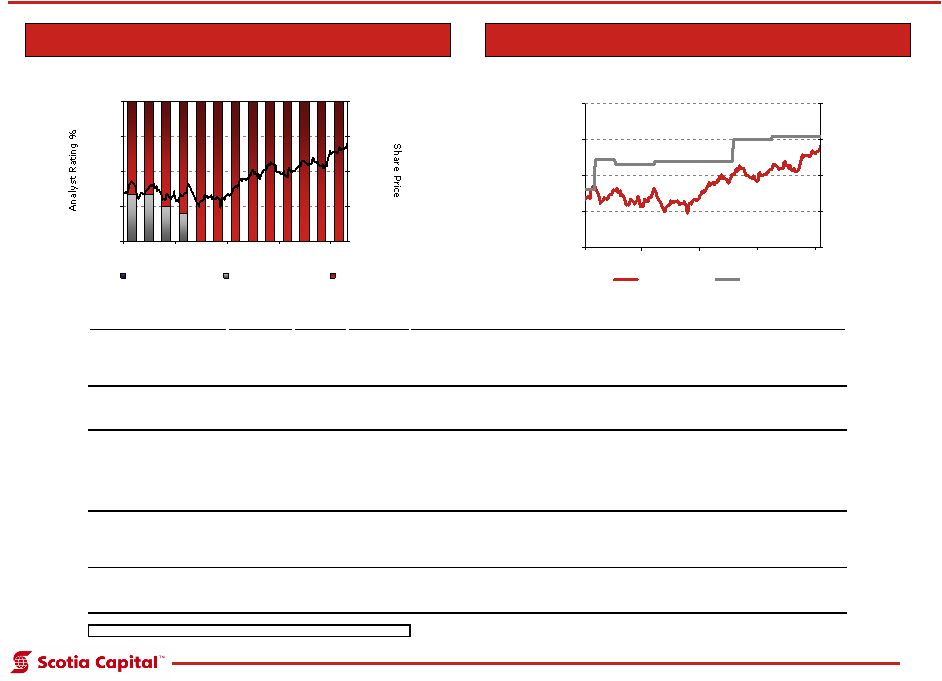

44 Research Analyst Views Historical Analyst Views Share Price vs. Target Price Overview of Hub International Firm/Date/Analyst Rating Target Price Premium to Current Price Analyst Comments Wachovia Securities Outperform n.a. n.a. November 21, 2006 Lara Devieux Keefe, Bruyette & Woods Outperform $36.00 5.3% December 8, 2006 Dean Evans Cochran Caronia Waller Outperform $34.00 -0.6% October 27, 2006 Adam Klauber TD Newcrest Buy $35.00 2.3% October 27, 2006 Doug Young Ferris Baker Watts Buy $36.00 5.3% October 26, 2006 John B Keefe Average $35.25 3.1% "We continue to believe that over time, if HBG can achieve its 4-5% organic growth target, supplement this with acquisitions and through gaining scale hit its 50-150bps margin expansion target, the discount at which it trades to its peers should continue to shrink. We believe that HBG is an attractive small cap financial services company." n.a. "Our Outperform rating on HBG shares is based on (1) strong revenue and earnings growth prospects, largely driven by acquisitions and margin expansion; and (2) valuation, with the stock trading below the broker peer group average." n.a. "The third quarter showed why Hub is the only brokerage stock we are recommending to buy. The key is and will continue to be acquisitions. Management's ability to attract deals in a competitive environment gives us comfort that Hub will produce a materially higher growth rate going forward." "Revenue growth of 29% for the quarter was 3x to 4x more than growth being produced by other regional brokers." 0% 25% 50% 75% 100% Feb-06 May-06 Aug-06 Nov-06 Feb-07 $20.00 $25.00 $30.00 $35.00 $40.00 Sell Hold Buy # of Analysts 3 3 5 5 5 5 5 5 5 5 5 5 4 $20.00 $25.00 $30.00 $35.00 $40.00 Feb-06 May-06 Aug-06 Nov-06 Feb-07 $20.00 $25.00 $30.00 $35.00 $40.00 Price Target Price |

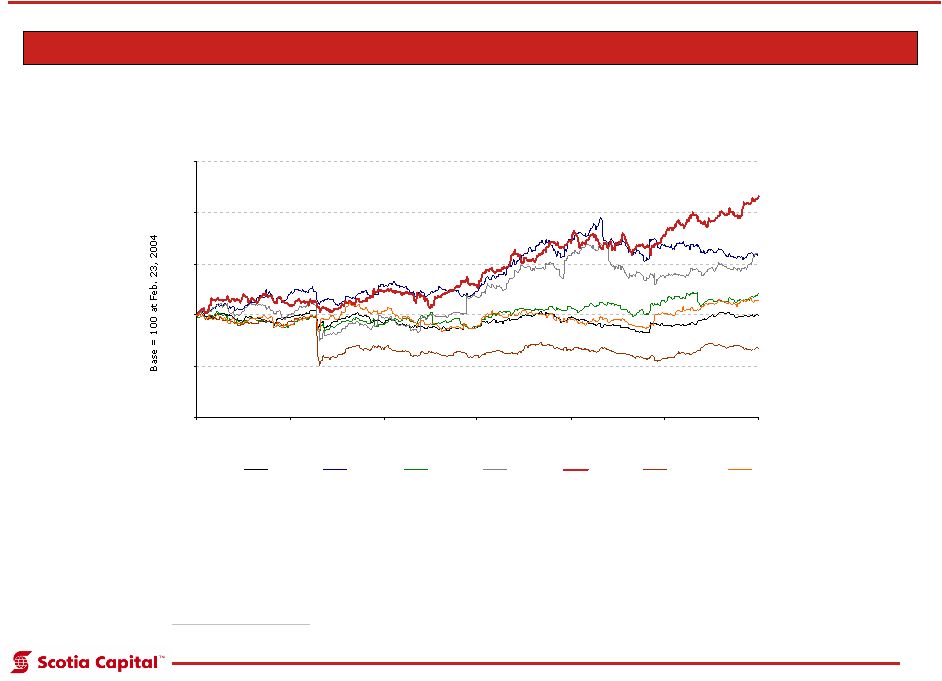

45 0 50 100 150 200 250 Feb-04 Aug-04 Feb-05 Aug-05 Feb-06 Aug-06 Feb-07 AJG BRO HRH AOC HBG MMC WSH -0.3% 58.5% 27.5% 59.1% 118.0% -32.3% 12.7% Relative Share Price Performance Hub has significantly outperformed peers over the past three years Overview of Hub International Source: Bloomberg. |

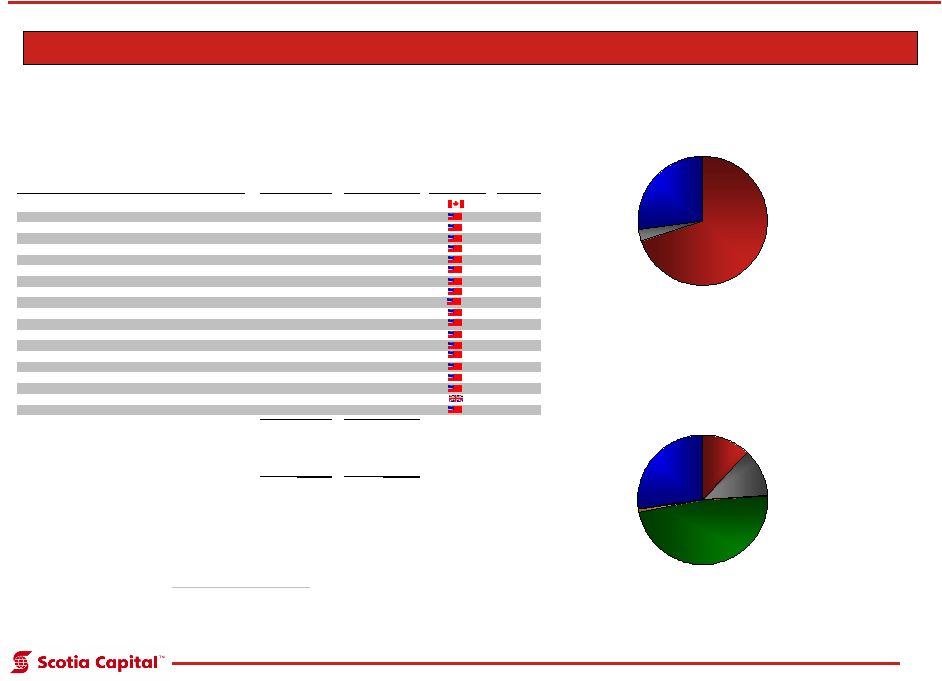

46 Shareholder Profile Shareholders by Geography (4) Top 20 Institutional Shareholders (1) As a percentage of basic shares outstanding. (2) Based on SEC filings as at February 14, 2007. (3) Company information. (4) As a percentage of float outstanding. Source: LionShare and company filings. Note: Value may not add due to rounding. U.S. institutions comprise the bulk of Hub’s shareholder base Shareholders by Investing Style (4) Overview of Hub International U.S. Institutions 70% International Institutions 3% Retail & Unidentified Institutions 27% GARP 12% Value 12% Growth 48% Yield 1% Retail & Unidentified Institutions 27% Institution Shares Held Percent Ownership (1) Country Style FAIRFAX FINANCIAL HOLDINGS LTD (2) 10.3 26.2% n.a. LORD ABBETT & CO. LLC 2.2 5.6% Growth WASATCH ADVISORS, INC. 2.2 5.5% Growth ARTISAN PARTNERS LP 1.4 3.5% Growth T. ROWE PRICE ASSOCIATES, INC. 1.3 3.2% Growth TRUSCO CAPITAL MANAGEMENT INC. 0.8 2.0% Growth EAGLE ASSET MANAGEMENT, INC. 0.8 1.9% Value MUNDER CAPITAL MANAGEMENT 0.7 1.8% Growth INVESTMENT COUNSELORS OF MARYLAND LLC 0.7 1.7% Growth TCW ASSET MANAGEMENT CO. 0.6 1.6% GARP CARDINAL CAPITAL MGMT, L.L.C. 0.6 1.6% Value PZENA INVESTMENT MANAGEMENT LLC 0.5 1.3% Growth PUTNAM INVESTMENT MANAGEMENT, INC. 0.5 1.2% GARP Amber Capital LP 0.4 1.1% GARP ROYCE & ASSOCIATES LLC 0.4 1.0% Value ENDEAVOUR CAPITAL ADVISORS, INC. 0.4 1.0% Value FRIESS ASSOCIATES LLC 0.4 0.9% Growth KALMAR INVESTMENTS, INC. 0.4 0.9% Growth F&C ASSET MANAGEMENT PLC. 0.3 0.9% GARP SILVERCREST ASSET MANAGEMENT GROUP LLC 0.3 0.8% GARP Top 20 Institutional Total 25.2 63.8% Other Identified Institutions 4.5 11.3% Insiders (3) 2.7 6.8% Retail and Unidentified Institutions 7.2 18.2% Total Basic Shares Outstanding 39.5 100.0% |