UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE l4A

PROXY STATEMENT PURSUANT TO SECTION 14(A) OF THE SECURITIES

EXCHANGE ACT OF 1934

Filed by the Registrant ¨

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| þ | Definitive Additional Materials |

| ¨ | Soliciting Material Under Rule l4a-l2 |

ATLAS AIR WORLDWIDE HOLDINGS, INC. | ||||

| (Name of Registrant As Specified In Its Charter) | ||||

N/A | ||||

| (Name of Person(s) Filing Proxy statement, if Other Than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

| þ | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules l4a-6(i)(4) and 0-11 | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| ||||

| (2) | Aggregatenumber of securities to which transaction applies:

| |||

| ||||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth in the amount on which the filing fee is calculated and state how it was determined):

| |||

| ||||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| ||||

| (5) | Total fee paid:

| |||

| ||||

| ¨ | Fee paid previously with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a) (2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| ||||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| ||||

| (3) | Filing Party:

| |||

| ||||

| (4) | Date Filed:

| |||

| ||||

Shareholder Engagement Shareholder Engagement Proxy Season 2014 Proxy Season 2014 |

Executive Summary 2 We seek shareholder feedback and welcome your thoughts on corporate governance and executive compensation Following our 2013 annual meeting, we reached out to holders of nearly 80% of shares, and made significant changes to our compensation program following this engagement We have performed well in an environment of global uncertainty and are ready to capitalize on market improvements We continue to execute a strategic plan that enables us to grow over the long term and deliver value to our investors A significant portion of our compensation is performance-based. We use objective metrics in our annual bonus program, our RSUs vest over 4 years, and PSUs pay out zero to twice target based on absolute company performance Alignment of executive compensation with company performance drives a highly engaged and tenured executive team This has resulted in a strong operating and financial performance over the 2009-2013 period We have a strong level of independent oversight of our compensation program and adherence to corporate governance best practices We have made recent enhancements to our practices, including the adoption of majority voting for Directors in uncontested elections and appointment of a new independent Chairman in 2014 Shareholder Outreach and Responsiveness Business Performance Pay Program Aimed at Aligning Pay with Performance Effective Compensation Program Commitment to Best Practices |

We value our shareholders’ input and continue to solicit feedback In 2013, we reached out to holders of almost 80% of our outstanding shares to discuss executive compensation and other issues of importance to shareholders, and met with holders of about 55% of our outstanding shares We made changes to our compensation program in 2013 and early 2014 in response to feedback given by shareholders during these meetings (See slides #4 and #5 for a detailed description of changes) We continue to engage extensively with our investors to solicit their points of view and consider further improvement We are committed to linking pay and performance, as we believe this is a key driver in aligning company, executive and shareholder interests Shareholder Outreach and Responsiveness 3 |

Compensation Program Changes in Response to Shareholder Feedback 4 ©2012 Atlas Air Worldwide Holdings, Inc. Area of Focus What We Heard from Investors How We Responded in 2013-14 CEO Compensation Benchmarking CEO’s pay should be targeted at median For all future CEO pay decisions, total direct compensation targeted at median of peers CEO LTI plan target award reduced by 100 percentage points, from 475% to 375% of base salary CEO Annual Bonus Payout Consider negative discretion to reflect special circumstances in addition to operating performance The Compensation Committee used downward discretion to reduce the bonus payout in 2013 by an additional $673,000 (an additional 65 percentage points), to 80% of target (performance against stated objectives would have resulted in CEO bonus at 145% of target) This is 40% below prior year payout all based on special circumstances of this year Annual Bonus Performance Metrics Objective performance criteria should have greater weighting in annual incentive program Decreased weighting of individual strategic metrics for all participants to 30% in 2013 Further decreased individual performance metrics for the CEO to 20% in 2014 Peer Group Compensation benchmark group includes peers with significantly larger revenues, requiring regression, and certain companies in automotive industry For 2014 compensation decisions, the Committee revised the peer group to consist of 20 companies in industries similar to ours, with median revenue size approximately equal to AAWW revenues (including revenues of Polar) |

Compensation Program Changes in Response to Shareholder Feedback (cont’d) 5 ©2012 Atlas Air Worldwide Holdings, Inc. Area of Focus What We Heard from Investors How We Responded in 2013-14 Multiple Peer Groups Use of separate peer groups for benchmarking pay and measuring performance is confusing We used a single new representative and relevant peer group to benchmark 2014 compensation We moved in 2014 to absolute metrics to measure performance for LTI plan awards Metrics used in AIP and LTI plan should be more relevant to value enhancement In 2013, AIP metric moved to Adjusted EPS to better diversify from LTI plan metrics and to incentivize and reward tax planning efforts of management In 2013, LTI plan EBT metric changed to EBITDA as a better indicator of cash flow and more relevant measure of underlying profit potential while keeping ROIC In 2014, LTI plan metrics changed from relative to absolute measure Clawback Lack of compensation clawback policy New AIP clawback policy adopted beginning in 2014 Change-in-Control/Double Trigger Single-trigger vesting upon change of control not considered ‘best practice’ LTI awards granted beginning in 2014 have double triggers Majority Voting Standard A majority voting standard would strengthen the director election process Incentive Plans Performance Metrics Amendment to our By-Laws establishes a majority voting standard in uncontested director elections beginning with our Annual Meeting in 2015 |

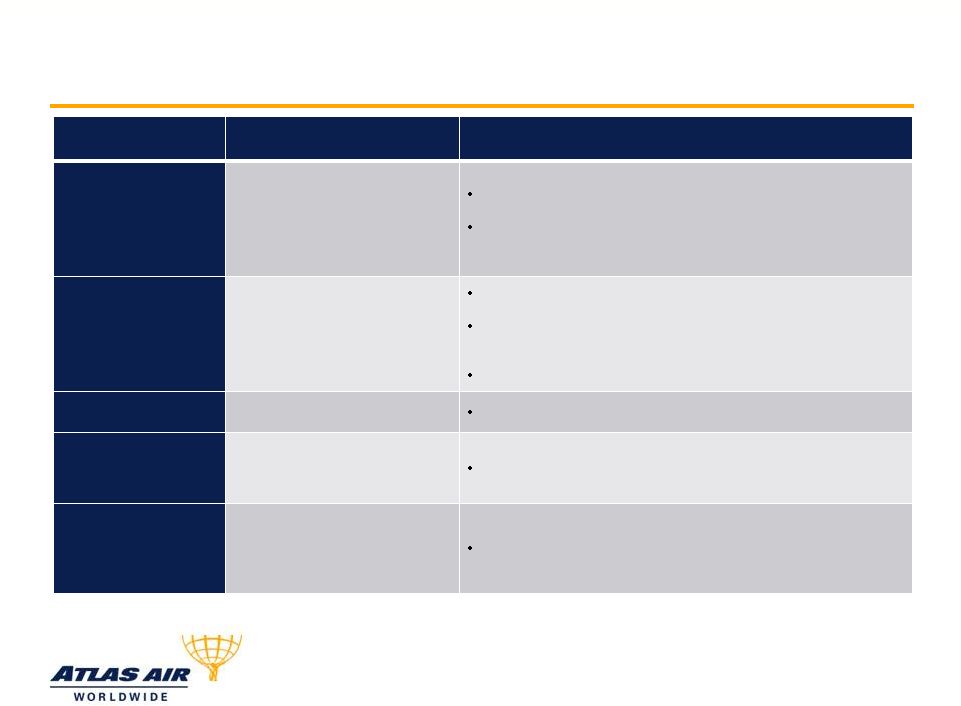

~70% of AAWW block hours Provide outsourced cargo aircraft solutions, including provision of an aircraft, crew, maintenance and insurance, including DHL Express and Qantas, among others Most competitors are private companies ~10-15% of AAWW block hours Provide cargo and passenger aircraft charters to customers, including brokers, cruise-ship operators, freight forwarders, direct shippers and airlines Large, fragmented, competitive market; is a component of many freight companies’ business ~10-15% of AAWW block hours Provide cargo and passenger aircraft charter services for the U.S. military Mostly small, domestic competitors; private companies, many of which have recently experienced bankruptcy Significantly growing part of our business Revenue not tied to block hours Provide cargo and passenger aircraft and engine leasing solutions We are a leading global provider of outsourced aircraft and aviation operating services, managing and operating the world’s largest fleet of Boeing 747 freighters through several diverse business segments A Diverse Service Provider with Solid Business Performance 6 ACMI (Aircraft, Crew, Maintenance, and Insurance) Commercial Charter AMC (Air Mobility Command) Charter Services Dry Leasing |

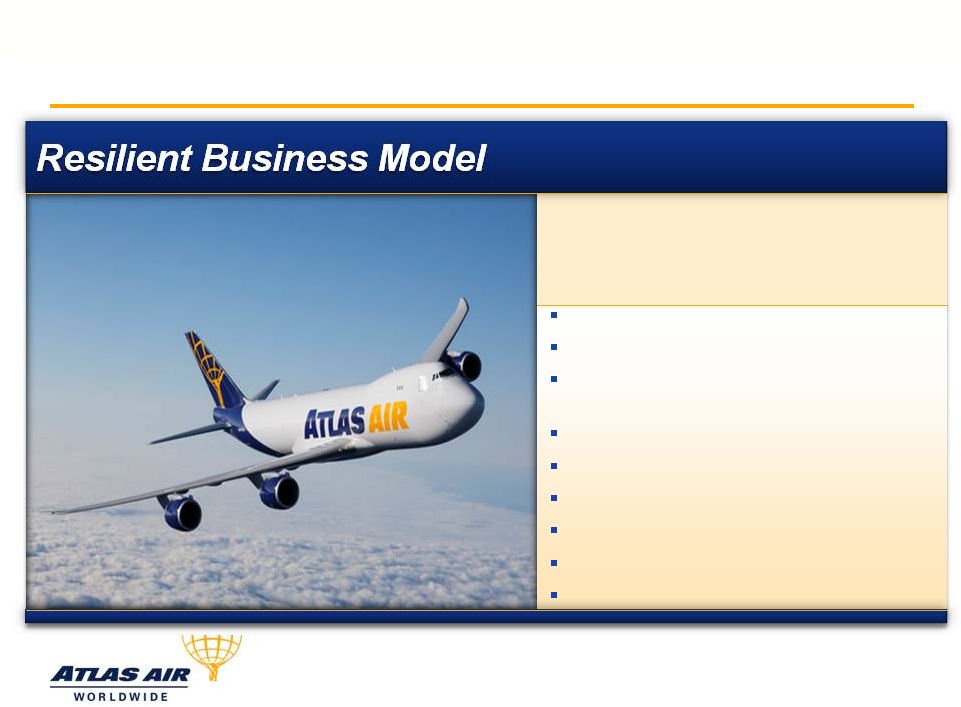

Underlying Core Strength and Growth 7 Resilient Business Model Modern fleet: New 747-8Fs Higher ACMI and CMI volume Added AMC and Commercial Charter Pax flying Added 777Fs for Dry Leasing Expanding 767 platform Added Passenger flying Operating efficiencies Meaningful earnings Return of capital Executing our plan Increasing contribution from business investments |

|

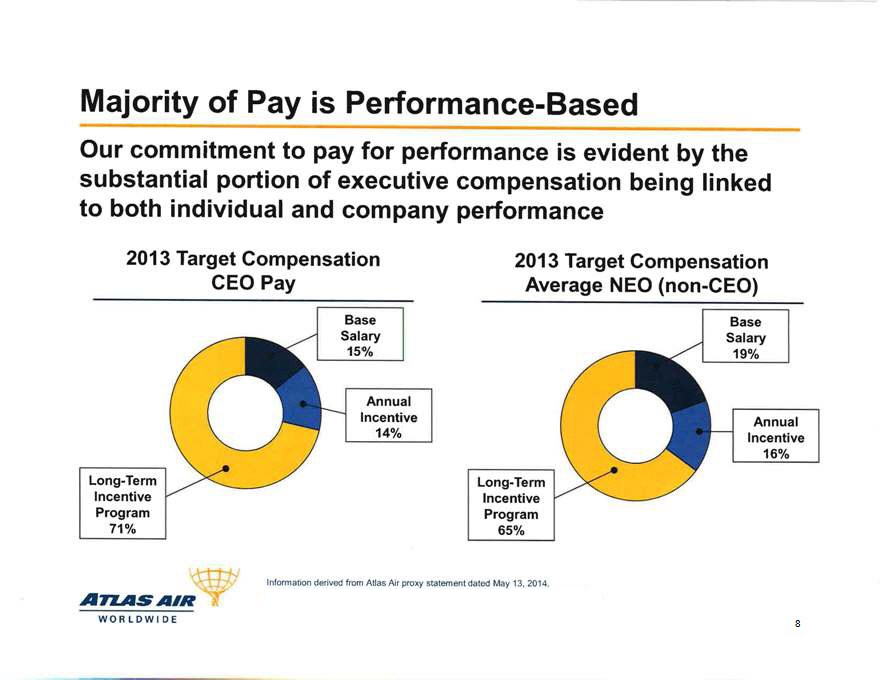

Majority of pay performance-based

Our community to pay for performance is evidence by the substantial portion of executive compensation being linked to both individual and company performance

2013 target compensation CEO Pay

Base salary 15%

Long-term incentive program 71%

Annual Incentive 14%

2013 Target Compensation Average NEO (non-CEO)

Base Salary 19%

Long-Term Incentive Program 65%

Annual Incentive 16%

Information derived from Atlas Air proxy statement dated May 13, 2014

8

Atlas Air is a unique company in the public markets It is not appropriate to compare Atlas Air directly with passenger airlines, door-to-door freight delivery providers or leasing companies (many of these companies are our customers), Most direct competitors are private companies with different capital structures and executive compensation arrangements, much of which is undisclosed There are 5 primary competitors in our core ACMI business – All are private companies; several closely held or private equity owned – 2 recently came out of bankruptcy We offer a complex number of services on a truly global scale – 300+ cities, 100+ countries last year – Most customers outside the U.S. – Running a safe, secure, compliant airline with large complex assets – Lean management team and challenging business requires broad skillsets and deep experience Our Unique Comparator Considerations 9 A Unique Company with Limited Number of Direct Peers Global Scale; Business Complexity; Competition for Business and Talent |

Completely Revamped Peer Group for 2014 10 • We now use one peer group consisting of 20 companies in industries similar to ours, with median revenue size approximately equal to AAWW revenues (including Polar revenues) to benchmark compensation • Regression of revenues is no longer necessary • PSU performance is now measured using absolute metrics, eliminating the need for a second peer group. • We had previously used two carefully structured groups of comparator companies to benchmark compensation: Before … 2014 and Beyond … Towers Watson Aerospace/Defense Automotive and Transportation Industries database for Base Salary, Annual Incentive Compensation and Long-Term Incentive Compensation Specially constructed peer group for PSU performance purposes • Many shareholders found the use of two peer groups confusing and felt that use of the Towers Watson database was inappropriate as it contained peers with significantly larger revenues (requiring revenue regression) and certain companies in the automotive industry |

Our Revised CEO Benchmarking Practice In response to shareholder feedback, all future CEO pay decisions will be targeted at the median of benchmarking peer group, rather than between the 50 th – 75 th percentile 11 Base Salary Bonus Equity (50% RSU / 50% PSU) Targeted at median of benchmarking peer group 2014 and beyond |

Effective Compensation Policies and Procedures 12 Substantial levels of variable compensation No excise tax gross-ups Long-term performance metrics aligned with company value creation Payments in the event of change of control do not exceed 3x for all executives No share recycling Minimum stock ownership requirements are in place for officers and directors Prohibition of hedging and pledging AAWW shares Do not provide excessive perquisites Independent Oversight of Pay Sound Compensation Practices Independent Chairman of the Board Independent Compensation Committee Independent Compensation Consultant |

Annually elected directors Majority voting for uncontested Director elections; adopted new voting standard, effective at our 2015 annual meeting Strong independent Chairman role; appointed a new Chairman, Frederick McCorkle as of May 2014 Separate CEO and Chairman positions All board committees are 100% independent All directors are independent (except our CEO) No poison pill in place Ongoing dialogue with shareholders Continued Commitment to Corporate Governance Best Practices 13 1 2 3 4 5 6 7 8 *Recent Changes |

As of our annual meeting of shareholders, our Board will consist of seven directors, one of whom is our CEO. We have a talented group of directors who bring differing perspectives and backgrounds to the boardroom Given the diversity of our operations, it is important to bring experience from all areas key to understanding our business Experienced and Well-Rounded Board Leadership 14 Mergers and Acquisitions Strategic Planning Finance and Capital Structure Civil and Governmental Aviation Legal, Regulatory and Government Affairs Corporate Governance International Operations Transportation and Security Accounting International and National Trade Military Affairs Procurement and Distribution Atlas Air’s Board of Directors’ Expertise |

Appendix 15 |

2009 – 2013 Performance Metrics ($ Millions Ex BHs, EPS, Stock Price, ROIC) 2009 2013 CAGR Block Hours 108,969 158,937 9.9% Operating Revenues 1,061.5 1,656.9 11.8% Adjusted Pretax Income 118.5 142.3 4.7% Adjusted EPS 3.40 3.78 2.7% Free Cash Flow 172.2 273.1 12.2% Stock Price per Share 18.90 41.15 21.5% Four-Year ROIC 59.8% 16 Free Cash Flow = Cash Flows from Operations – Base Capex – Capitalized Interest ROIC = Net Operating Profit After Tax/Average Invested Capital |

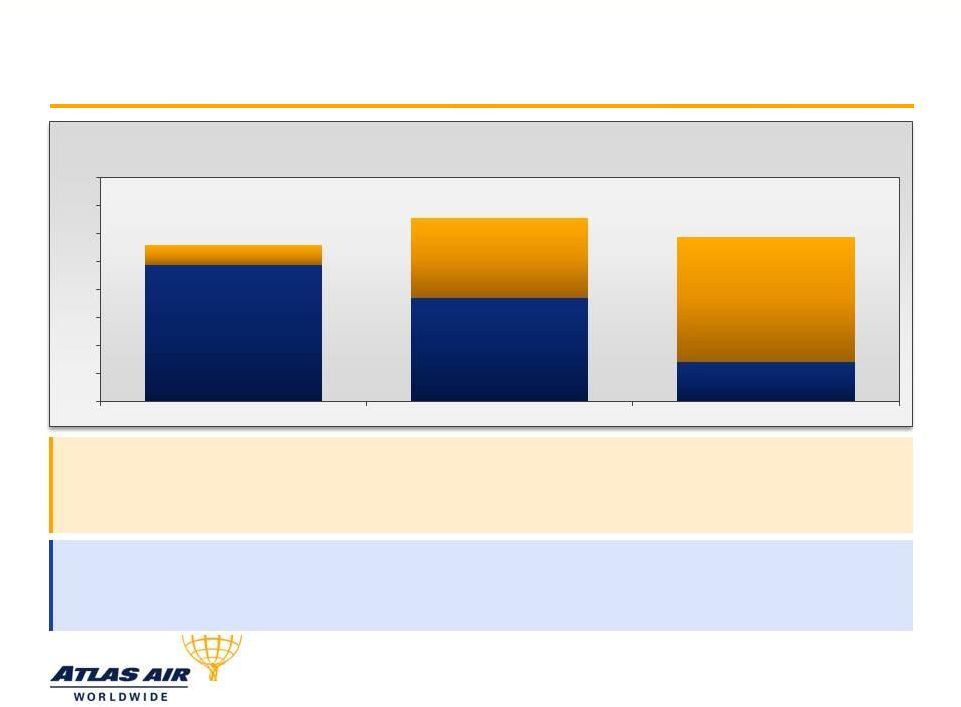

Business Investments Driving Business Resilience 17 Business Investments: ACMI 747-8Fs, AMC and Commercial Charter Passenger Operations, CMI Operations, 767 platform, 777Fs for Dry Leasing Established Business: Primarily due to significant declines in AMC and Commercial Charter Cargo Operations Challenging Airfreight Environment $0 $50 $100 $150 $200 $250 $300 $350 $400 2011 2012 2013 Direct Contribution ($ Millions) |

Business Segments % of 2013 Block Hours (1) Description ACMI (2) CMI (3) 73 Offers aircraft that are crewed, maintained, and insured by Atlas for lease on a long-term basis Customers assume fuel, demand and yield risk Provides outsourced CMI operating solutions for passenger and freighter operations Air Mobility Command (AMC) Charter 11 AMC Charter provides full planeload cargo and passenger charter flights to the U.S. military Cost-plus business Commercial Charter 16 Commercial Charter segment provides full planeload cargo and passenger charter services to charter brokers, freight forwarders, direct shippers, and airlines Dry Leasing -- Provides aircraft and engine dry leasing solutions to third parties Other Services -- Selected by the U.S. government to train pilots who fly the President on Air Force One Core Business Segments Note: (1) Excludes ferry block hours (2) Aircraft, Crew, Maintenance, Insurance. (3) Crew, Maintenance, Insurance 18 |

747-8F Financings in Place 2012 record-low fixed-rate coupons of: 19 In aggregate: $200+ million in cash from deliveries Under 3% coupon IRR in excess of 30% 2013 and 2014 fixed-rate coupons of: 1.83% 2.67% 2.02%, 1.73%, 1.56%, and 1.48% |

Capital Allocation Strategy Committed to creating, enhancing, returning value to our stockholders Repurchased 1,723,577 shares, 6.5% of outstanding stock, in 2013 Current authorization to repurchase up to $60 million Cash prioritization: – Balance sheet maintenance – Business investment – Share repurchases 20 |

Deliver superior service quality to our customers Expand our ACMI and CMI business Maximize our AMC and Commercial Charter business opportunities Achieve Continuous Improvement savings and efficiencies Develop Titan (dry leasing) platform Execute share repurchase program 2014 Operational Goals and Objectives 21 In other words… Drive Value for Stockholders |