UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 001-32594

HEARTLAND PAYMENT SYSTEMS, INC.

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 22-3755714 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

90 Nassau Street, Princeton, New Jersey 08542

(Address of principal executive offices) (Zip Code)

(609) 683-3831

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

| Common Stock, $0.001 par value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

NONE

(title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ YES x NO

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ YES x NO

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x YES ¨ NO

Indicate by check mark if disclosure of delinquent filer pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ YES x NO

The aggregate market value of the voting and non-voting common stock held by non-affiliates computed by reference to the price at which the common stock was last sold on the New York Stock Exchange on June 30, 2008 was approximately $674 million.

As of March 4, 2009, there were 37,442,292 shares of the registrant’s common stock, $0.001 par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Specifically identified portions of the registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A in connection with the 2009 annual meeting of shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K for fiscal year ended December 31, 2008.

Heartland Payment Systems, Inc.

Annual Report on Form 10-K

For the Year Ended

December 31, 2008

TABLE OF CONTENTS

FORWARD LOOKING STATEMENTS

Unless the context requires otherwise, references in this report to “the Company,” “we,” “us,” and “our” refer to Heartland Payment Systems, Inc. and our subsidiaries.

Some of the information in this Annual Report on Form 10-K may contain forward-looking statements that are based on our management’s beliefs and assumptions and on information currently available to our management. Forward-looking statements include the information concerning our possible or assumed future results of operations, the impact of the systems breach of our processing system, business strategies, financing plans, competitive position, industry environment, potential growth opportunities, the effects of future regulation and the effects of competition. Forward-looking statements include all statements that are not historical facts and can be identified by the use of forward-looking terminology such as the words “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate” or similar expressions.

Forward-looking statements involve risks, uncertainties and assumptions. Actual results may differ materially from those expressed in the forward-looking statements. You should understand that many important factors, in addition to those discussed elsewhere in this report, could cause our results to differ materially from those expressed in the forward-looking statements. Certain of these factors are described in Item 1A. Risk Factors and include, without limitation, the significantly unfavorable economic conditions facing the United States, the results and effects of the systems breach of our processing system including the outcome of our investigation, the extent of cardholder information compromised and the consequences to our business, including the effects on sales and costs in connection with the system breach, our competitive environment, the business cycles and credit risks of our merchants, chargeback liability, merchant attrition, problems with our bank sponsor, our reliance on other bank card payment processors, our inability to pass increased interchange fees along to our merchants, economic conditions, system failures and government regulation.

PART I

Overview of Our Company

Delaware Corporation

We were incorporated in Delaware in June 2000. Our headquarters are located at 90 Nassau Street, Princeton, NJ 08542, and our telephone number is (609) 683-3831.

Bank Card Payment Processing

Our primary business is to provide bank card payment processing services to merchants in the United States and Canada. This involves facilitating the exchange of information and funds between merchants and cardholders’ financial institutions, providing end-to-end electronic payment processing services to merchants, including merchant set-up and training, transaction authorization and electronic draft capture, clearing and settlement, merchant accounting, merchant assistance and support and risk management. Our merchant customers primarily fall into two categories: our core small and mid-sized merchants (referred to as Small and Midsized Enterprises, or “SME”) and large national merchants, primarily in the petroleum industry. We also provide additional services to our merchants, such as payroll processing, gift and loyalty programs, paper check processing, and we sell and rent point-of-sale devices and supplies.

At December 31, 2008, we provided our bank card payment processing services to approximately 168,850 active SME bank card merchants located across the United States. This represents a 9.1% increase over the 154,750 active SME bank card merchants at December 31, 2007. At December 31, 2008, we provided bank card payment processing services to approximately 82 large national merchants with approximately 55,761 locations. Our total bank card processing volume for the year ended December 31, 2008 was $66.9 billion, a 28.9% increase from the $51.9 billion processed during the year ended December 31, 2007. Bank card processing volume for 2008 includes $8.7 billion for large national merchants acquired with Network Services. Additionally, we provided bank card processing services to approximately 5,600 merchants in Canada.

On January 20, 2009, we announced the discovery of a criminal breach of our payment systems environment (referred to as the “Processing System Intrusion” in this document) that apparently had occurred during some portion of 2008. The Processing System Intrusion involved malicious software that appears to have been used to collect in-transit, unencrypted payment card data while it was being processed by Heartland during the transaction authorization process. Such data is not required to be encrypted while in transit under current payment card industry guidelines. Card data that was affected by the Processing System Intrusion included card numbers, expiration dates, and certain other information from the magnetic stripe on the back of the payment card (including, for a small percentage of transactions, the cardholder’s name). However, the cardholder information that we process does not include addresses or Social Security numbers. Also, we believe that no unencrypted PIN data was captured. We believe the breach has been contained and did not extend beyond 2008. Our investigation of the Processing System Intrusion is ongoing. See “— Processing System Intrusion” for more detail.

While we have determined that the Processing System Intrusion has triggered a loss contingency, to date an unfavorable outcome is not believed by us to be probable on those claims that are pending or have been threatened against us, or that we consider to be probable of assertion against us, and we do not have sufficient information to reasonably estimate the loss we would incur in the event of an unfavorable outcome on any such claim. Therefore, in accordance with SFAS No. 5,“Accounting for Contingencies,” no reserve/liability has been recorded with respect to any such claims as of December 31, 2008. As more information becomes available, if we should determine that an unfavorable outcome is probable on such a claim and that the amount of such unfavorable outcome is reasonably estimable, we will record a reserve for the claim in question. If and when we record such a reserve, it could be material and could adversely impact our results of operations, financial condition and cash flow. Costs we incurred related to investigations and remedial actions performed in December 2008 were not significant. Amounts we expect to incur for investigations, remedial actions, legal fees, and crisis management services related to the Processing System Intrusion that will be performed after December 31, 2008 will be recognized as incurred. Such costs are expected to be material and could adversely impact our results of operations, financial condition and cash flow.

1

According to The Nilson Report, in 2007 we were the 6th largest card acquirer in the United States ranked by purchase volume, which consists of both credit and debit Visa and MasterCard transactions. This ranking represented 2.4% of the total bank card processing market. In 2008, 2007 and 2006, our bank card processing volume was $66.9 billion, $51.9 billion and $43.3 billion, respectively.

In May 2008, we acquired the net assets of the Network Services Business unit (“Network Services”) of Alliance Data Network Services LLC (“Alliance”), for a cash payment of $92.5 million. The acquisition was financed through a combination of cash on hand and our credit facilities. Network Services provides processing of credit and debit cards to large national merchants, primarily in the petroleum industry. Network Services settled 604 million transactions representing over $17 billion of total annual Visa and MasterCard processing volume in 2007, and 600 million transactions representing $16.7 billion of bank card processing volume in 2008. In addition to settling Visa and MasterCard transactions, Network Services processes a wide range of payment transactions for its predominantly petroleum customer base, including providing approximately 2.6 billion transaction authorizations through its front-end card processing systems (primarily for Visa and MasterCard) in 2007. Network Services has added $8.7 billion to our bank card processing volume on 317 million transactions from the date we acquired it through December 31, 2008. Additionally, Network Services generated revenues on 1.6 billion transactions it authorized through its front-end card processing systems from the date we acquired it through December 31, 2008.

In March 2008, we acquired a majority interest in Collective Point of Sale Solutions Ltd. (“CPOS”) for a net cash payment of $10.1 million. CPOS is a Canadian provider of payment processing services and secure point-of-sale solutions. This acquisition added approximately 5,100 Canadian merchants to our customer base and provides us an entrance into the Canadian credit and debit card processing market. We are now able to service merchants that have locations in both the United States and Canada.

Our bank card processing revenue is recurring in nature. We typically enter into three-year service contracts with our SME merchants that, in order to qualify for the agreed-upon pricing, require the achievement of agreed bank card processing volume minimums from our merchants. Our SME gross bank card processing revenue is largely driven by Visa and MasterCard volume processed by merchants with whom we have processing contracts; as such, we also generally benefit from consumers’ increasing use of bank cards in place of cash and checks, and sales growth (if any) experienced by our retained bank card merchants. Most of our SME revenue is from gross processing fees, which are primarily a combination of a percentage of the dollar amount of each Visa and MasterCard transaction we process plus a flat fee per transaction. We make mandatory payments of interchange fees to card issuing banks through Visa and MasterCard and dues and assessment fees to Visa and MasterCard, and we retain the remainder of the revenue. For example, the allocation of funds resulting from a $100 transaction is depicted below.

Our bank card processing revenue from our large national merchants is also recurring in nature. In contrast to SME merchants, our processing revenues from large national merchants generally consist of a flat fee per transaction and thus are driven primarily by the number of transactions we process (whether settled, or only authorized), not bank card processing volume.

2

In December 2007, we signed a sales and servicing program agreement (“OnePoint”) with American Express Travel Related Services Company, Inc. (“American Express”) under which we will sign up and service new merchants on behalf of American Express. Under the terms of the program, we will act as American Express’s agent in: (a) providing solicitation services by signing merchants directly with American Express; and (b) providing transactional support services on behalf of American Express. OnePoint became available to our sales organization effective January 1, 2009. Under OnePoint, we will provide processing, settlement, customer support and reporting to merchants, in effect consolidating a merchant’s American Express card acceptance into the services we currently provide for their Visa and Master Card transactions. OnePoint also is open to our existing bank card merchants who do not currently accept American Express cards and who desire to add American Express card acceptance, so that we become their single point of contact for card processing.

In June 2008, we signed an agreement with DFS Services, LLC (formerly known as Discover Financial Services, LLC and referred to as “Discover” in this document) to offer bank card merchants a streamlined process that enables them to accept Discover Network cards on our processing platform. We plan to offer our new and existing customers an integrated processing solution that includes card acceptance pricing, funding, statement processing and customer service on one platform. Previously, to accept Discover Network cards, our merchants had to deal with two separate platforms - one for Discover and one for all other cards. Merchants who sign up for our program will, in turn, be able to offer their customers the added benefit of Discover Network card acceptance with greater ease. We expect this program to be available in the second quarter of 2009. Additionally, we will purchase the current Discover Network merchants that process through Heartland and convert them to the streamlined process mentioned previously.

Under our new agreement with Discover, which is expected to be implemented in the second quarter of 2009, our revenue model will be similar to Visa and MasterCard. The terms of the new American Express agreement have a compensation model which provides us a percentage-based residual on the American Express volume we process, plus fees for every transaction we process.

We sell and market our bank card payment processing services through a nationwide direct sales force of 1,725 sales professionals. Through this sales force we establish a local sales and servicing presence, which we believe provides for enhanced referral opportunities and helps mitigate merchant attrition. We compensate our sales force solely through commissions, based upon the performance of their merchant accounts. We believe that our sales force and our experience and knowledge in providing payment processing services gives us the ability to effectively evaluate and manage the payment processing needs and risks that are unique to these merchants. In 2008, our sales force generated over 63,500 bank card merchant applications and installed over 55,000 new bank card merchants. In 2007, our sales force generated over 62,500 bank card merchant applications and installed over 57,000 new bank card merchants.

We focus our sales efforts on low-risk bank card merchants and have developed systems and procedures designed to minimize our exposure to potential merchant losses. In 2008, 2007 and 2006, we experienced losses of 0.88 basis points (0.0088%), 0.54 basis points (0.0054%) and 0.45 basis points (0.0045%) of SME merchant bank card processing volume, respectively. We have developed significant expertise in industries that we believe present relatively low risks as the customers are generally present and the products or services are generally delivered at the time the transaction is processed. These industries include restaurants, brick and mortar retailers, convenience and liquor stores, automotive sales, repair shops and gas stations, professional service providers, lodging establishments and other. As of December 31, 2008, approximately 28.8% of our SME bank card merchants were restaurants, approximately 19.4% were brick and mortar retailers, approximately 10.9% were convenience and liquor stores, approximately 9.1% were automotive sales, repair shops and gas stations, approximately 9.0% were professional service providers and approximately 3.6% were lodging establishments. The Processing System Intrusion was the result of the insertion of malicious software into our processing system, and we believe that it was not the result of any failure of our sales efforts or systems and procedures described in this paragraph.

Since our inception, we have developed a number of proprietary Internet-based systems to increase our operating efficiencies and distribute our processing and merchant data to our three main constituencies: our sales force, our merchant base and our customer service staff. In 2001, we began providing authorization and data capture services to our SME bank card merchants through our own front-end processing system, HPS Exchange. In 2006, we began providing clearing, settlement and merchant accounting services through our own internally developed back-end processing system, Passport, to substantially all of our SME bank card merchants. Passport enables us to customize these services to the needs of our Relationship Managers and merchants. Currently, we are further developing HPS Exchange and Passport to process the large national merchants which we acquired with Network Services.

3

During the years ended December 31, 2008, 2007 and 2006, approximately 83%, 75% and 64%, respectively, of our SME merchant transactions were processed through HPS Exchange, which has decreased our operating costs per transaction. At December 31, 2008 and 2007, approximately 98% of total SME merchants were processing on Passport. At December 31, 2008, our internally developed systems are providing substantially all aspects of a merchant’s processing needs, excluding Network Services.

Payroll Processing Services

Through our wholly-owned subsidiary, Heartland Payroll Company, we operate a full-service nationwide payroll processing service, including check printing, direct deposit, related federal, state and local tax deposits and providing accounting documentation. At December 31, 2008, 2007 and 2006, we processed payroll for 7,738, 6,209 customers and 4,216 customers, respectively.

Our nationwide direct sales force also sells our payroll processing services solely on a commission basis. Beginning in 2006, we began providing additional training regarding our payroll processing products and increased the focus of our sales force on selling these products. As a result, in 2008, 2007 and 2006, we installed 4,406, 4,395 and 3,140 new payroll processing customers, respectively, compared to 1,117 new installs in 2005.

Other Products and Services

Other products and services which we offer, such as Electronic Check Processing Services and Micropayment and Campus Solutions, are discussed in “— Our Services and Products.”

Processing System Intrusion

In late October of 2008, we were alerted by Visa of suspicious activity surrounding certain cardholder accounts that appeared to certain card issuers to have been subjected to fraudulent activity shortly after those cards were used to make legitimate transactions that we processed. Our IT team worked with the major card brands (i.e., Visa, MasterCard, American Express, and Discover) (collectively, the “Card Brands”) to try to match the suspicious transactions with our processing activities, and we engaged multiple forensic auditors to investigate our payment card processing system. Ultimately, on January 12, 2009, informations that one of those auditors had provided our team with led us to the discovery of suspicious files, and on January 13, 2009, we discovered the malicious software that apparently had created those files. We promptly reported this discovery to law enforcement authorities and the Card Brands, and we continue to cooperate with the Card Brands and the criminal investigations relating to the Processing System Intrusion.

On January 20, 2009, we publicly announced the Processing System Intrusion. The Processing System Intrusion involved malicious software that appears to have been used to collect in-transit, unencrypted payment card data while it was being processed by us during the transaction authorization process. Such data is not required to be encrypted while in transit under current payment card industry guidelines. We had received confirmation of our compliance with the Payment Card Initiative Data Security Standard (PCI-DSS) from a third-party assessor each year since the standard was announced, including most recently in April 2008. Card data that was affected by the Processing System Intrusion included card numbers, expiration dates, and certain other information from the magnetic stripe on the back of the payment card (including, for a small percentage of transactions, the cardholder’s name). However, the cardholder information that we process does not include addresses or Social Security numbers. Also, we believe that no unencrypted PIN data was captured. We believe the breach has been contained and did not extend beyond 2008. Our investigation of the Processing System Intrusion is ongoing.

4

To date, we have had several lawsuits filed against us and we expect additional lawsuits will be filed. These include lawsuits which assert claims against us by cardholders (including various putative class actions seeking in the aggregate to represent all cardholders in the United States whose transaction information is alleged to have been placed at risk in the course of the Processing System Intrusion), and banks that issued payment cards to cardholders whose transaction information is alleged to have been placed at risk in the course of the Processing System Intrusion (including various putative class actions seeking to represent all financial institutions that issued payment cards to cardholders whose transaction information is alleged to have been placed at risk in the course of the Processing System Intrusion), seeking damages allegedly arising out of the Processing System Intrusion and other related relief. The actions generally assert various common-law claims such as claims for negligence and breach of contract, as well as, in some cases, statutory claims such as violation of the Fair Credit Reporting Act, state data breach notification statutes, and state unfair and deceptive practices statutes. The putative cardholder class actions seek various forms of relief including damages, injunctive relief, multiple or punitive damages, attorney’s fees and costs. The putative financial institution class actions seek compensatory damages, including recovery of the cost of issuance of replacement cards and losses by reason of unauthorized transactions, as well as injunctive relief, attorney’s fees and costs. In addition, we have been advised by the SEC that it has commenced an informal inquiry and we have been advised by the United States Attorney for the District of New Jersey that it has commenced an investigation, in each case to determine whether there have been any violations of the federal securities laws in connection with our disclosure of the Processing Systems Intrusion and the alleged trading in our securities by certain of our employees, including certain executive officers. A putative class action has been commenced against us and certain of our executive officers alleging violations of the federal securities laws in connection with our disclosures relative to the Processing System Intrusion and our computer system security and the alleged trading in our securities by four of our officers. The plaintiff in the putative federal securities law class action seeks to represent all purchasers of our securities between August 5, 2008 and February 23, 2009 and seeks to recover losses such purchasers allegedly incurred by reason of their purchases, as well as related costs and expenses. We also have been contacted by the Federal Financial Institutions Examination Council and informed that it will be making inquiries into the Processing System Intrusion, and the Federal Trade Commission, by letter dated February 19, 2009, has requested that we provide information about our information security practices. Additionally, we have received written or telephonic inquiries relating to the Processing System Intrusion from a number of state Attorneys General’s offices, including a Civil Investigative Demand from the Louisiana Department of Justice Office of the Attorney General, the Canadian Privacy Commission, and other government officials. We are cooperating with the government officials in response to each of these inquiries and investigations. We expect that additional lawsuits may be filed against us relating to the Processing System Intrusion and that additional inquiries from governmental agencies may be received or investigations by government agencies may be commenced.

Although we intend to defend the lawsuits, investigations and inquiries described above vigorously, we cannot predict the outcome of such lawsuits, investigations and inquiries. Apart from damages claimed in such lawsuits and/or in other lawsuits relating to the Processing System Intrusion that may be filed, we may be subject to fines or other obligations as a result of the government inquiries and investigations described above and/or other governmental inquiries or investigations relating to the Processing System Intrusion, and the Card Brands are also expected to assert claims seeking to impose fines, penalties, and/or other assessments against us or our sponsor banks (who would seek indemnification from us pursuant to our agreements with them) based upon the Processing System Intrusion. In that regard, we have been advised by Visa Inc. that based on Visa’s investigation of the Processing System Intrusion, Visa believes we are in violation of the Visa operating regulations and that, based on that belief, Visa has removed us from Visa’ published list of PCI-DSS compliant service providers until such time as we are re-certified as PCI-DSS compliant and the assessor’s report attesting to such re-certification has been reviewed and approved by Visa, intends to seek to impose fines on our sponsor banks, which fines (if successfully imposed) our sponsor banks could in turn seek to recover from us, intends to place us in a “probationary status” during the two years following our re-certification as being PCI-DSS compliant, during which time our failure to comply with the probationary requirements set forth by Visa or with the Visa operating regulations may result in Visa seeking to impose further risk conditions on us, including but not limited to our disconnection from VisaNet or our disqualification from the Visa payment system, and intends to treat some or all of the Visa accounts that Visa considers to have been placed at risk of compromise in the Processing System Intrusion as being eligible for Visa’s “Account Data Compromise Recovery” and “Data Compromise Recovery Solution” processes, which processes could result in Visa’s seeking to recover from our sponsor banks (and our sponsor banks in turn seeking to recover from us) amounts in respect of fraud losses and operating expenses that Visa believes Visa issuers to have incurred by reason of the Processing System Intrusion.

While we have determined that the Processing System Intrusion has triggered a loss contingency, to date an unfavorable outcome is not believed by us to be probable on those claims that are pending or have been threatened against us, or that we consider to be probable of assertion against us, and we do not have sufficient information to reasonably estimate the loss we would incur in the event of an unfavorable outcome on any such claim. Therefore, in accordance with SFAS No. 5, “Accounting for Contingencies,” no reserve/liability has been recorded with respect to any such claims as of December 31, 2008. As more information becomes available, if we should determine that an unfavorable outcome is probable on such a claim and that the amount of such unfavorable outcome is reasonably estimable, we will record a reserve for the claim in question. If and when we record such a reserve, it could be material and could adversely impact our results of operations, financial condition and cash flow. Costs we incurred related to investigations and remedial actions performed in December 2008 were not significant. Amounts we expect to incur for investigations, remedial actions, legal fees, and crisis management services related to the Processing System Intrusion that will be performed after December 31, 2008 will be recognized as incurred. Such costs are expected to be material and could adversely impact our results of operations, financial condition and cash flow. It is also possible that the publicity surrounding the Processing System Intrusion and the efforts of our competitors to capitalize on the Processing System Intrusion could have a material adverse impact on our ability to obtain new merchant customers and retain existing merchant customers which, in turn, could have a material adverse impact on our results of operations and financial condition.

Although we have insurance that we believe may cover some of the costs and losses that we may incur in connection with the above-described pending and potential lawsuits, inquiries, investigations and claims, we cannot now confirm that such coverage will, in fact, be provided or the extent of such coverage, if it is provided.

It is also possible that the publicity surrounding the Processing System Intrusion and the efforts of our competitors to capitalize on the Processing System Intrusion could have a material adverse impact on our ability to obtain new merchant customers and retain existing merchant customers which, in turn, could have a material adverse impact on our results of operations and financial condition.

Payment Processing Industry Overview

The payment processing industry provides merchants with credit, debit, gift and loyalty card and other payment processing services, along with related information services. The industry continues to grow as a result of wider merchant acceptance, increased consumer use of bank cards and advances in payment processing and telecommunications technology. According to The Nilson Report, total expenditures for all card type transactions by U.S. consumers were $3.3 trillion in 2007, and are expected to grow to $4.8 trillion by 2012.

5

From 2002 to 2007, the compound annual growth rate of card payments was 7%, and this rate is expected to increase to 8% for 2008 to 2012. The proliferation of bank cards has made the acceptance of bank card payments a virtual necessity for many businesses, regardless of size, in order to remain competitive. This use of bank cards, enhanced technology initiatives, efficiencies derived from economies of scale and the availability of more sophisticated products and services to all market segments has led to a highly competitive and specialized industry.

Segmentation of Merchant Service Providers

The payment processing industry is dominated by a small number of large, fully-integrated payment processors that sell directly to, and handle the processing needs of, the nation’s largest merchants. Large national merchants (i.e., those with multiple locations and high volumes of bank card transactions) typically demand and receive the full range of payment processing services at low per-transaction costs.

Payment processing services are generally sold to the SME merchant market segment through banks and Independent Sales Organizations that generally procure most of the payment processing services they offer from large payment processors. It is difficult, however, for banks and Independent Sales Organizations to customize payment processing services for the SME merchant on a cost-effective basis or to provide sophisticated value-added services. Accordingly, services to the SME merchant market segment historically have been characterized by basic payment processing without the availability of the more customized and sophisticated processing, information-based services or customer service that is offered to large merchants. The continued growth in bank card transactions is expected to cause SME merchants to increasingly value sophisticated payment processing and information services similar to those provided to large merchants.

The following table sets forth the typical range of services provided directly (in contrast to using outsourced providers) by fully integrated transaction processors, traditional Independent Sales Organizations and us.

| (a) | HPS Exchange: 84% of our bank card merchants |

Passport: 98% of our bank card merchants

We believe that the card-based payment processing industry will continue to benefit from the following trends:

Growth in Card Transactions

The proliferation in the uses and types of cards, including in particular debit and prepaid cards, the rapid growth of the Internet, significant technological advances in payment processing and financial incentives offered by issuers have contributed greatly to wider merchant acceptance and increased consumer use of such cards. The following chart illustrates the growth for card transactions for the periods indicated.

6

Source: The Nilson Report. Card purchase volume includes VISA / MasterCard (debit and credit), American Express, Discover and Diners Club.

Note: Percentages inside bar represent year-over-year growth.

According to The Nilson Report and the New York State Forum for Information Resource Management, sources of increased bank card payment volume include:

| | • | | increasing acceptance of electronic payments by merchants who previously did not do so, such as quick service restaurants, government agencies and businesses that provide goods and services to other businesses; |

| | • | | increasing consumer acceptance of alternative forms of electronic payments, as demonstrated by the dramatic growth of debit cards, electronic benefit transfer, and prepaid and gift cards; and |

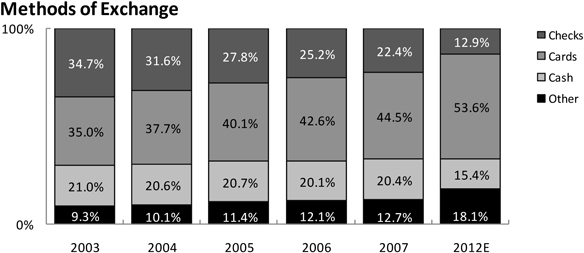

| | • | | continued displacement of checks with the use of cards and other methods of payment, including electronic, at the point of sale, as shown below. |

Source: The Nilson Report

7

Technology

At present, many large payment processors provide customer service and applications via legacy systems that are difficult and costly to alter or otherwise customize. In contrast to these systems, recent advances in scalable and networked computer systems, and relational database management systems, provide payment processors with the opportunity to deploy less costly technology that has improved flexibility and responsiveness. In addition, the use of fiber optic cables and advanced switching technology in telecommunications networks and competition among long-distance carriers, and the dramatic increase in merchants’ use of the Internet to process their transactions, further enhance the ability of payment processors to provide faster and more reliable service at lower per-transaction costs than previously possible.

Advances in personal computers and point-of-sale terminal technology, including integrated cash registers and networked systems, have increasingly allowed access to a greater array of sophisticated services at the point of sale and have contributed to the demand for such services. These trends have created the opportunity for payment processors to leverage technology by developing business management and other software application products and services.

Consolidation

The payment processing industry has undergone significant consolidation. The costs to convert from paper to electronic processing, merchant requirements for improved customer service, the risk of merchant fraud, and the demand for additional customer applications have made it difficult for community and regional banks to remain competitive in the merchant acquiring industry. Many of these providers are unwilling or unable to invest the capital required to meet these evolving demands, and have steadily exited the payment processing business or otherwise found partners to provide payment processing for their customers. Despite this consolidation, the industry remains fragmented with respect to the number of entities selling payment processing services, particularly to SME merchants.

Our Competitive Strengths

We believe our competitive strengths related to Bank Card Payment Processing include the following:

Large, Experienced, Efficient, Direct Sales Force

While many of our competitors rely on Independent Sales Organizations that often generate merchant accounts for multiple payment processing companies simultaneously, we market our services throughout the United States through our direct sales team of 1,725 Relationship Managers, Account Managers and sales managers who work exclusively for us. Our Relationship Managers have local merchant relationships and industry-specific knowledge that allow them to effectively compete for merchants. Our Relationship Managers are compensated solely on commissions, receiving signing bonuses and ongoing residual commissions for generating new merchant accounts. These commissions are based upon the gross margin we estimate that we will receive from their merchants, calculated by deducting interchange fees, dues, assessments and fees and all of our costs incurred in underwriting, processing, servicing and managing the risk of the account from gross processing revenue. Our Relationship Managers have considerable latitude in pricing a new account, but we believe that the shared economics motivate them to sign attractively priced contracts with merchants generating significant bank card processing volume. The residual commissions our Relationship Managers receive from their merchant accounts give them an incentive to maintain a continuing dialogue and servicing presence with their merchants; these relationships are also supported by our 293 Account Managers, who are focused on installing new merchants and responding to any ongoing servicing needs. We believe that our compensation structure is atypical in our industry and contributes to building profitable, long-term relationships with our merchants. Our sales compensation structure and marketing activities focus on recruiting and supporting our direct sales force, and we believe that the significant growth we have achieved in our merchant portfolio and bank card processing volume are directly attributable to these efforts.

8

Recurring and Predictable Revenue

We generate recurring revenue through our payment processing services. Our revenue is recurring in nature because we typically enter into three-year service contracts that require minimum volume commitments from our merchants to qualify for the agreed-upon pricing. Our recurring revenue grows as the number of transactions or dollar volume processed for a merchant increases or as our merchant count increases. In 2008, approximately 87% of our bank card processing volume came from merchants we installed in 2007 and earlier.

Internal Growth

While many of our competitors in the payment processing industry had relied on acquisitions to expand their operations and improve their profitability, from 2001 through 2007 we grew our business primarily through internal expansion by generating new merchant contracts submitted by our own direct sales force. Every merchant we processed during that time was originally underwritten by our staff, and we have substantial experience responding to their processing needs and the risks associated with them. We believe this both enhances our merchant retention and reduces our risks. We believe that internally generated merchant contracts generally are of a higher quality and generally are more predictable than contracts acquired from third parties, and the costs associated with such contracts are lower than the costs associated with contracts generally acquired from third parties.

While we continue to pursue internal growth, we were able to take advantage of acquisition opportunities in 2008 and expand into other markets that we previously did not have the technical capabilities to support. See “Pursue Strategic Acquisitions” and “Our Services and Products” later in this section for descriptions of these acquisitions.

Strong Position and Substantial Experience in Our Target Markets

As of December 31, 2008, we were providing payment processing services to approximately 168,850 active SMEs located across the United States. We believe our understanding of the needs of SMEs and the risks inherent in doing business with them, combined with our efficient direct sales force, provides us with a competitive advantage over larger service providers that access this market segment indirectly. We also believe that we have a competitive advantage over service providers of a similar or smaller size that may lack our extensive experience and resources and which do not benefit from the economies of scale that we have achieved.

Industry Expertise

Historically, we have focused our sales efforts on SME merchants who have certain key attributes and on industries in which we believe our direct sales model is most effective and the risks associated with bank card processing are relatively low. These attributes include owners who are typically on location, interact with customers in person, value a local sales and servicing presence and often consult with trade associations and other civic groups to help make purchasing decisions.

To further promote our products and services, we have entered into sponsoring arrangements with various trade associations, with an emphasis on state restaurant and hospitality groups. We believe that these sponsorships have enabled us to gain exposure and credibility within the restaurant industry and have provided us with opportunities to market our products to new merchants. In December 2008, the restaurant industry represented approximately 37.5% of our SME bank card processing volume and 52.1% of our SME transactions. In December 2007 and December 2006, the restaurant industry represented approximately 38.8% and 40.3% of our bank card processing volume and 53.3% and 54.8% of our transactions, respectively. We believe that the restaurant industry will remain an area of focus, though its growth will likely approximate the growth in the overall portfolio. Restaurants represent an attractive segment for us: according to a report by the National Restaurant Association, restaurant industry sales are expected to reach approximately $566 billion in 2009, which would represent a 2.5% increase over projected industry sales for 2008 and the eighteenth consecutive year of growth. The projected restaurant industry growth for 2009 is in spite of a challenging economy and this steady growth profile, combined with the industry’s low seasonality, makes restaurant merchant bank card processing volume very stable and predictable. In addition, the incidence of chargebacks is very low among

9

restaurants, as the service typically is provided before the card is used. Our industry focus not only differentiates us from other payment processors, but also allows us to forge relationships with key trade associations that attract merchants to our business. Our industry focus also allows us to better understand a merchant’s needs and tailor our services accordingly.

Although we have historically focused significant sales and marketing efforts on the restaurant industry, our SME merchant base also includes a broad range of brick and mortar retailers, lodging establishments, automotive repair shops, convenience and liquor stores and professional service providers. See “— Our Merchant Base” for detail on December 2008 bank card processing volume by merchant category.

Our historical focus on SME merchants has diversified our merchant portfolio and we believe has reduced the risks associated with revenue concentration. In 2008, no single SME merchant represented more than 0.56% of our total bank card processing volume. In 2007 and 2006, no single merchant represented more than 0.44% and 0.26% of our total bank card processing volume, respectively.

Our May 2008 acquisition of Network Services has further diversified our total merchant portfolio adding a substantial base of large national merchants, primarily in the petroleum industry.

Merchant Focused Culture

We have built a corporate culture and established practices that we believe improve the quality of services and products we provide to our merchants. This culture spans from our sales force, which maintains a local market presence to provide rapid, personalized customer service, through our service center which is segmented into regionalized teams to optimize responsiveness, and to our technology organization, which has developed a customer management interface and information system that alerts our Relationship Managers to any problems a merchant has reported and provides them with detailed information on the merchants in their portfolio. Additionally, we believe that we are one of the few companies that discloses and adheres to our pricing policies to merchants. Visa and MasterCard alter their interchange and other fees once or twice per year; we believe that we are one of the few companies that does not use such adjustments to increase our own margins. We think this is the best approach to building long-term merchant relationships. During 2006, we developed and endorsed The Merchant Bill of Rights, an advocacy initiative that details ten principles we believe should characterize all merchants’ processing relationships. The Merchant Bill of Rights allows our sales team to differentiate our approach to bank card processing from alternative approaches, and we believe that a focus on these principles by our merchants will enhance our merchant relationships. We believe that our culture and practices allow us to maintain strong merchant relationships and differentiate ourselves from our competitors in obtaining new merchants.

Scalable Operating Structure

Our scalable operating structure allows us to expand our operations without proportionally increasing our fixed and semi-fixed support costs. In addition, our technology platform, including both HPS Exchange and Passport, was designed with the flexibility to support significant growth and drive economies of scale with relatively low incremental costs. Most of our operating costs are related to the number of individuals we employ. We have in the past used, and expect in the future to use, technology to leverage our personnel, which should cause our personnel costs to increase at a slower rate than our bank card processing volume.

Advanced Technology

We employ information technology systems which use the Internet to improve management reporting, enrollment processes, customer service, sales management, productivity, merchant reporting and problem resolution.

In 2001, we began providing authorization and data capture services to our merchants through our internally-developed front-end processing system, HPS Exchange. This system incorporates real time reporting tools through, and interactive point-of-sale database maintenance via, the Internet. These tools enable merchants, and our employees, to change the messages on credit card receipts and to view sale and return transactions

10

entered into the point-of-sale device with a few second delay on any computer linked to the Internet. During the years ended December 31, 2008, 2007 and 2006, approximately 83%, 75% and 64%, respectively, of our SME transactions were processed through HPS Exchange.

In 2005, we began providing clearing, settlement and merchant accounting services through our own internally developed back-end processing system, Passport. Passport enables us to customize these services to the needs of our Relationship Managers and merchants. We completed converting substantially all of our SME bank card merchants to Passport during the second quarter of 2006. At December 31, 2008 and 2007, approximately 98% of total SME bank card merchants were processing on Passport. At December 31, 2008 and 2007, our internally developed systems have been providing substantially all aspects of a merchant’s processing needs for most of our SME merchants.

HPS Exchange, Passport and our other technology efforts have contributed to a reduction of our per-transaction processing costs and to a reduction of our costs of services as a percentage of our revenue. Many existing merchants will remain on TSYS Acquiring Solutions (“TSYS”) systems and those of our other third-party processors for front-end services for the duration of their relationship with us. However, we intend to install 85% to 95% of our new merchants on HPS Exchange, and to convert to HPS Exchange as many merchants on third party front ends as possible. Our Internet-based systems allow all of our merchant relationships to be documented and monitored in real time, which maximizes management information and customer service responsiveness. We believe that these systems help attract both new merchants and Relationship Managers and provide us with a competitive advantage over many of our competitors who rely on less flexible legacy systems.

Comprehensive Underwriting and Risk Management System

Through our experience in assessing risks associated with providing payment processing services to small- and medium-size merchants, we have developed procedures and systems that provide risk management and fraud prevention solutions designed to minimize losses. Our underwriting processes help us to evaluate merchant applications and balance the risks of accepting a merchant against the benefit of the bank card processing volume we anticipate the merchant will generate. We believe our systems and procedures enable us to identify potentially fraudulent activity and other questionable business practices quickly, thereby minimizing both our losses and those of our merchants. As evidence of our ability to manage these risks, we experienced losses of no more than 0.88 basis points of SME bank card processing volume for each of the years ended December 31, 2008, 2007 and 2006, which we believe is significantly lower than industry norms. The risks discussed in this paragraph are not the types of fraudulent card activity that has apparently resulted from the Processing System Intrusion.

Proven Management Team

We have a strong senior management team, each with at least a decade of financial services and payment processing experience. Our Chief Executive Officer, Robert O. Carr, was a founding member of the Electronic Transactions Association, the leading trade association of the bank card acquiring industry. Our management team has developed extensive contacts in the industry and with banks and value-added resellers. Our sales leaders have all sold merchant services for us prior to assuming management roles, and many have been with us throughout most of our first decade of existence. We believe that the strength and experience of our management team has helped us to attract additional sales professionals and add additional merchants, thereby contributing significantly to our growth.

11

Our Strategy

Our current growth strategy is to increase our market share as a provider of payment processing services to merchants in the United States and Canada. We believe that the increasing use of bank cards, combined with our sales and marketing approaches, will continue to present us with significant growth opportunities. Additionally, we intend to continue growing our payroll processing business, and enhance our other products such as Electronic Check Processing, Micro Payments and Campus Solutions. Key elements of our strategy include:

Expand Our Direct Sales Force

Unlike many of our competitors who rely on Independent Sales Organizations or salaried salespeople and telemarketers, we have built a direct, commission-only sales force. We have grown our sales force from 952 Relationship Managers as of December 31, 2006, to 1,117 and 1,166 Relationship Managers as of December 31, 2007 and 2008, respectively. We anticipate continued growth in our sales force in the next few years in order to increase our share of our target markets, and have targeted achieving a level of 2,000 Relationship Managers within the next three to four years. Our sales model divides the United States into four primary markets overseen by Executive Directors of Sales, and further into 17 primary geographic regions overseen by Regional Directors. The Regional Directors are primarily responsible for hiring Relationship Managers and increasing the number of installed merchants in their territory. Our Regional Directors’ compensation is directly tied to the compensation of the Relationship Managers in their territory, providing a significant incentive for them to grow the number and productivity of Relationship Managers in their territory.

Further Penetrate Existing Target Markets and Enter Into New Markets

We believe that we have an opportunity to grow our business by further penetrating the SME market through our direct sales force and alliances with local trade organizations, banks and value-added resellers. During 2007, according to The Nilson Report, we processed approximately 2.4% of the dollar volume of all Visa and MasterCard transactions in the United States, up from approximately 2.3% in 2006, 2.2% in 2005, 1.8% in 2004 and 1.4% in 2003. In December 2008, the restaurant industry represented approximately 37.5% of our bank card processing volume and 52.1% of our transactions. Our bank card merchant base also includes a wide range of merchants, including brick and mortar retailers, lodging establishments, automotive repair shops, convenience and liquor stores and professional service providers. We believe that our sales model, combined with our community-based strategy that involves our Relationship Managers building relationships with various trade groups and other associations in their territory, will enable our Relationship Managers to continuously add new merchants. We intend to further expand our bank card processing sales efforts into new target markets with relatively low risk characteristics, including markets that have not traditionally accepted electronic payment methods. These markets include governments, schools and the business-to-business market. In addition, the scale economies we have achieved by converting to our own platforms now allows us to profitably compete for the business of larger merchants, and we are now targeting merchants with annual processing volumes of up to $1 billion, compared to our prior maximum of $50-$100 million in processing volume.

Expand Our Services and Product Offerings

In recent years, we have focused on offering a broad set of payment-related products to our customers. In addition to payroll processing services (see “— Our Services and Products — Payroll Services” for a description of these services), our current product offerings include check processing services that allow merchants to computerize paper checks, and prepaid, gift and loyalty card product solutions. In 2006, we added electronic check services (see “— Our Services and Products — Electronic Check Processing Services” for a description of these services) and micropayment systems (see “— Our Services and Products — Micropayment Systems” for a description of these services) to our products. In 2007, we added Campus Solutions (see “— Our Services and Products — Campus Solutions” for a description of these services) to our products. In 2008, we added Collective Point of Sale Solutions Ltd., Network Services and Chockstone, Inc. (see “— Our Services and Products — Large National Merchant Bank Card processing, Collective Point of Sale Solutions Ltd., and Chockstone” for more information).

We also distribute products that will help our merchants reduce their costs and grow their businesses, such as age verification services that track driver’s license data to verify an individual’s age and identity. We may develop new products and services internally, enter into arrangements with third-party providers of these products or selectively acquire new technology and products. Many of these new service offerings are designed to work on the same point-of-sale devices that are currently in use, enabling merchants to purchase a greater volume of their services from us and eliminating their need to purchase additional hardware. We believe that these new products and services will enable us to leverage our existing infrastructure and create opportunities to cross-sell our products and services among our various merchant bases, as well as enhance merchant retention and increase processing revenue.

12

Leverage Our Technology

We intend to continue to leverage our technology to increase our operating efficiencies and provide real-time processing and account data to our merchants, Relationship Managers, Account Managers and customer service staff. Since our inception, we have been developing Internet-based systems to improve and streamline our information systems, including detailed customer-use reporting, management reporting, enrollment, customer service, sales management and risk management reporting tools. We are seeking to develop a significant initiative that will allow merchants to integrate their payment processing data into any of the major small business accounting software packages. We have also made significant investments in our payment processing capabilities, which we believe will allow us to offer a differentiated payment processing product that is faster and less expensive than many competing products.

Enhance Merchant Retention

By providing our merchants with a consistently high level of service and support, we strive to enhance merchant retention. While increased bank card use helps maintain our stable and recurring revenue base, we recognize that our ability to maintain strong merchant relationships is important to our continued growth. We believe that our practice of fully disclosing our pricing policies to our merchants creates goodwill. For example, in 2003, we believe we were one of the few companies that passed along to small- and medium-sized customers a reduction in debit interchange fees that resulted from the settlement of the so-called Wal-Mart lawsuit against Visa and MasterCard. During 2006, we developed and endorsed The Merchant Bill of Rights, an advocacy initiative that details ten principles we believe should characterize all merchants’ processing relationships. The Merchant Bill of Rights allows our sales team to differentiate our approach to bank card processing from alternative approaches, and we believe that a focus on these principles by our merchants will enhance our merchant relationships.

As discussed in “— Sales,” we have built a group of Account Managers who are teamed with Relationship Managers and handle field servicing responsibilities. We have developed a customer management interface that alerts our Relationship Managers and Account Managers to any problems an SME merchant has reported and provides them with detailed information on the merchants in their portfolio. In addition, we believe that the development of a more flexible back-end processing capability, such as Passport provides, will allow us to tailor our services to the needs of our sales force and merchants, which we believe will further enhance merchant retention. Passport will also allow us to enhance the information available to our merchants, and to offer new services to them.

Pursue Strategic Acquisitions

Although we intend to continue to pursue growth through the efforts of our direct sales force, we may also expand our merchant base or gain access to other target markets by acquiring complementary businesses, products or technologies, including other providers of payment processing. Our 2006 acquisition of Debitek, Inc. and 2007 acquisition of General Meters Corp, are examples of expanding by acquiring complementary businesses. In 2008, we acquired Collective Point of Sale Solutions Ltd., a Canadian provider of payment processing services and secure point-of-sale solutions that provided us with an entrance into the Canadian credit and debit card processing market. We are now able to service merchants that have locations in both the United States and Canada. In 2008, we also acquired the Network Services unit of Alliance Data Systems that handles a wide range of payment transactions for its predominantly petroleum customer base. Our latest acquisition of Chockstone in 2008 provided for expansion into the loyalty marketing and gift card solutions market.

Our Services and Products

SME Merchant Bank Card Payment Processing

We derive the majority of our SME processing revenues from fee income relating to Visa and MasterCard payment processing, which is primarily comprised of a percentage of the dollar amount of each transaction we process, as well as a flat fee per transaction. The percentage we charge is typically a fixed margin over interchange, which is the percentage set by Visa and MasterCard depending on the type of card used and the

13

way the transaction is handled by the merchant. On average, the gross revenue we generate from processing a Visa or MasterCard transaction equals approximately $2.47 for every $100 we process. We also receive fees from American Express, Discover, and JCB for facilitating their transactions with our SME merchants. The terms of our new American Express agreement have a compensation model which provides us percentage-based residual on the American Express volume we process, plus fees for every transaction we process. Under our new agreement with Discover, which is expected to be implemented in the second quarter of 2009, our revenue model will be similar to Visa and MasterCard.

We receive revenues as compensation for providing bank card payment processing services to merchants, including merchant set-up and training, transaction authorization and electronic draft capture, clearing and settlement, merchant accounting, merchant support and chargeback resolution. In 2005, we began providing clearing, settlement and accounting services through Passport, our own internally developed back-end processing system. Passport enables us to customize these services to the needs of our Relationship Managers and merchants. At December 31, 2008 and 2007, approximately 98% of our SME bank card merchants were processing on Passport. In addition, we sell and rent point-of-sale devices and supplies and provide additional services to our merchants, such as gift and loyalty programs, paper check authorization and chargeback processing. These payment-related services and products are described in more detail below:

Merchant Set-up and Training– After we establish a contract with a merchant, we create the software configuration that is downloaded to the merchant’s existing, newly purchased or rented point-of-sale terminal, cash register or computer. This configuration includes the merchant identification number, which allows the merchant to accept Visa and MasterCard as well as any other cards, such as American Express, Discover and JCB, provided for in the contract. The configuration might also accommodate check verification, gift and loyalty programs and allow the terminal or computer to communicate with a pin-pad or other device. Once the download has been completed by the Relationship Manager or Account Manager, we conduct a training session on use of the system. We also offer our merchants flexible low-cost financing options for point-of-sale terminals, including installment sale and monthly rental programs.

Authorization and Draft Capture– We provide electronic payment authorization and draft capture services for all major bank cards. Authorization generally involves approving a cardholder’s purchase at the point of sale after verifying that the bank card is not lost or stolen and that the purchase amount is within the cardholder’s credit or account limit. The electronic authorization process for a bank card transaction begins when the merchant “swipes” the card through its point-of-sale terminal and enters the dollar amount of the purchase. After capturing the data, the point-of-sale terminal transmits the authorization request through HPS Exchange or the third-party processor to the card-issuing bank for authorization. The transaction is approved or declined by the card-issuing bank and the response is transmitted back through HPS Exchange or the third-party processor to the merchant. At the end of each day, and, in certain cases, more frequently, the merchant will “batch out” a group of authorized transactions, transmitting them through us to Visa and MasterCard for payment.

We introduced HPS Exchange, our internally developed front-end processing system, in August 2001. During the years ended December 31, 2008, 2007 and 2006, approximately 83%, 75% and 64%, respectively, of our SME transactions were processed through HPS Exchange. The remainder of our front-end processing is outsourced to third-party processors, primarily TSYS Acquiring Solutions, but also including First Data Corporation, Chase Paymentech Solutions and Global Payments Inc. Although we will continue to install new SME merchants on TSYS’ and other third-party processors’ systems, we anticipate that the percentage of SME transactions that are outsourced to third-party processors will decline as we install a high percentage of new merchants on HPS Exchange, and convert merchants on third party systems to HPS Exchange.

Clearing and Settlement– Clearing and settlement processes, along with Merchant Accounting, represent the “back-end” of a transaction. Once a transaction has been “batched out” for payment, the payment processor transfers the merchant data to Visa or MasterCard who then collect funds from the card issuing banks. This is typically referred to as “clearing.” After a transaction has been cleared, the transaction is “settled” by Visa or MasterCard by payment of funds to the payment processor’s sponsor bank the next day. The payment processor creates an electronic payment file in ACH format for that day’s cleared activity and sends the ACH file to its sponsor bank. The ACH payments system generates a credit to the merchants’ bank accounts for the value of the file. The merchant thereby receives payment for the value of the purchased goods or services, generally two business days after the sale. Under the terms of the new Agreement with American Express and Discover, the

14

process will be substantially similar to the Visa and MasterCard process, and the merchant will receive one deposit for all cards accepted, in contrast to the existing arrangement, where an acceptor of Visa and MasterCard, American Express and Discover will receive three deposits.

Passport, our internally developed back-end system, enables us to customize these services to the needs of our merchants and Relationship Managers. For example, Passport enables us to provide Next Day Funding to our SME merchants who have banking relationships with certain banks. In January 2007 we commenced Next Day Funding for merchants who maintain a deposit relationship with TD BankNorth (acquired Commerce Bank, N.A.), in July 2007 we commenced Next Day Funding for merchants who maintain a deposit relationship with Bremer Bank, in December 2007 we commenced Next Day Funding for merchants who maintain a deposit relationship with Heartland Bank (an unrelated third party), in September 2008, we commenced Next Day Funding for merchants who maintain a deposit relationship with Central Pacific Bank, and in December 2008, we commenced Next Day Funding for merchants who maintain a deposit relationship with Gateway Bank. Under Next Day Funding, these merchants are paid for their transactions one day earlier than possible when we were processing on a third party back-end platform.

Merchant Accounting– Utilizing Passport, we organize our SME merchants’ transaction data into various files for merchant accounting and billing purposes. We send our SME merchants detailed monthly statements itemizing daily deposits and fees, and summarizing activity by bank card type. These detailed statements allow our SME merchants to monitor sales performance, control expenses, disseminate information and track profitability. We also provide information related to exception item processing and various other items of information, such as volume, discounts, chargebacks, interchange qualification levels and funds held for reserves to help them track their account activity. SME merchants may access this archived information through our customer service representatives or online through our internet-based customer service reporting system.

Merchant Support Services– We provide merchants with ongoing service and support for their processing needs. Customer service and support includes answering billing questions, responding to requests for supplies, resolving failed payment transactions, troubleshooting and repair of equipment, educating merchants on Visa and MasterCard compliance and assisting merchants with pricing changes and purchases of additional products and services. We maintain a toll-free help-line 24 hours a day, seven days a week, which is staffed by our customer service representatives and during 2008 answered an average of approximately 110,000 customer calls per month. The information access and retrieval capabilities of our intranet-based systems provide our customer service representatives prompt access to merchant account information and call history. This data allows them to quickly respond to inquiries relating to fees, charges and funding of accounts, as well as technical issues.

Chargeback Services – In the event of a billing dispute between a cardholder and a merchant, we assist the merchant in investigating and resolving the dispute as quickly and accurately as possible with card issuers or the bank card networks, which determine the outcome of the dispute. In most cases, before we process a debit to a merchant’s account for the chargeback, we offer the merchant the opportunity to demonstrate to the bank card network or the card issuer that the transaction was valid. If the merchant is unable to demonstrate that the transaction was valid and the dispute is resolved by the bank card network or the card issuer in favor of the cardholder, the transaction is charged back to the merchant. After a merchant incurs three chargebacks in a year, we typically charge our merchants a $25 fee for each subsequent chargeback they incur.

Large National Merchant Bank Card Payment Processing

In May 2008, we acquired Network Services from Alliance Data Systems Corporation. Network Services is a provider of payment processing solutions, serving large national merchants in a variety of industries such as petroleum, convenience store, parking and retail. Services include payment processing, prepaid services, POS terminal, helpdesk services and merchant bank card services. This acquisition provides us with a substantial portfolio of merchants in the petroleum industry segment. In addition to Visa and MasterCard transactions, Network Services handles a wide range of payment transactions for its predominantly petroleum customer base. Network Services continues to process authorizations of large national merchants transactions through Alliance Data Systems Corporation and processes settlement of large national merchant transactions through Fifth Third Bank.

15

Our bank card processing revenue from large national merchants is recurring in nature. In contrast to SME merchants, our processing revenues from large national merchants generally consist of a flat fee per transaction and thus are primarily driven by the number of transactions we process (whether settled, or only authorized), not processing volume.

Authorization and Draft Capture – Network Services provides electronic payment authorization and draft capture for all major bank cards, client private label cards and fleet cards. Authorization generally involves approving a cardholder’s purchase at the point of sale after verifying that the card is not lost or stolen and that the purchase amount is within the cardholder’s credit or account limit. The electronic authorization process for a card transaction begins when the merchant “swipes” the card through its point-of-sale terminal and enters the dollar amount of the purchase. Network Services offers two front-end processing hosts, VAPS and NWS. After capturing the data, the point-of-sale terminal transmits the authorization request through the VAPS or NWS hosts or the third-party processor to the card-issuing entity for authorization. The transaction is approved or declined by the card-issuing entity and the response is transmitted back through the VAPS/NWS host or the third-party processor to the merchant. At the end of each day, and, in certain cases, more frequently, the merchant will “batch out” a group of authorized transactions, transmitting them through us to Visa and MasterCard for payment.

VAPS and NWS provide distinct functionality and processing options for our large corporate customers. These hosts provide efficient transaction payment processing and real-time authorizations using fully redundant routing paths. Our merchants can rely on quick response times and high availability. We maintain two redundant data centers for our large national merchant transaction processing. If one site fails, the other site is capable of supporting 100% of the workload so this assures uninterrupted transaction processing. Each data center maintains direct connections to Visa, MasterCard, Discover, Fiserv and American Express. The Fiserv connection is our gateway for debit and EBT processing.

Clearing and Settlement – Clearing and settlement processes represent the “back-end” of a transaction. Once a transaction has been “batched out” for payment, we transfer the completed transaction detail file to Fifth Third Bank, which is our outsourced processor for clearing and settlement. During the “clearing” process, the transaction detail is split out and sent to Visa or MasterCard who then collect funds from the card issuing banks. After a transaction has been cleared, the transaction is “settled” by Visa or MasterCard by payment of funds to our sponsor bank, Sun Trust, the next day. HPS then creates an electronic payment file in ACH format for that day’s cleared activity and sends the ACH file to its sponsor bank. The ACH payments system generates a credit to the merchants’ bank accounts for the value of the file.

We provide deposit information to our large national merchants each day via our Internet-based settlement reporting system. Deposits are broken out by card type and show gross sales, less chargebacks, interchange, and miscellaneous adjustments.

Merchant Boarding –The Merchant Support area supports new site setup requests, changes to existing locations, and any deletions. In addition, we provide large national merchants with a web-based system, Prometheus, that allows merchants to manage their sites’ data in the mainframe database after their initial setup has been completed. The benefits of Prometheus include reducing complexity, decreasing delay in boarding, allowing merchants to control their data entry, and minimizing the learning curve and data entry. The only requirements are Windows and a user ID. Boarding merchants using Prometheus access allows direct connect into Prometheus through a TCP/IP connection.

Merchant Reporting –We provide three types of reporting options to large national merchants.

| | • | | Data Warehouse– Merchants interested in flexible reporting alternatives have been satisfied with our Data Warehouse. A data warehouse is an architecture that consists of various technologies, which include relational and multi-dimensional databases, file servers, extraction and transformation programs, user query and reporting tools, and more. Other than a suitable web browser, no additional software is required to access Data Warehouse. Users can access Data Warehouse from any location anywhere and at any time from any PC that has access to the Internet. |