UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-10487

Hotchkis & Wiley Funds

(Exact name of registrant as specified in charter)

601 South Figueroa Street, 39th Floor

Los Angeles, California 90017-5704

(Address of principal executive offices) (Zip code)

Anna Marie Lopez

Hotchkis & Wiley Capital Management, LLC

601 South Figueroa Street, 39th Floor

Los Angeles, California 90017-5704

(Name and address of agent for service)

Copies to:

Maureen A. Miller, Esq.

Joseph M. Mannon, Esq.

Vedder Price P.C.

222 North LaSalle Street, 26th Floor

Chicago, Illinois 60601

(Counsel for the registrant)

(213) 430-1000

Registrant's telephone number, including area code

Date of fiscal year end: June 30, 2022

Date of reporting period: June 30, 2022

Item 1. Reports to Stockholders.

Hotchkis & Wiley Funds

Annual Report

JUNE 30, 2022

DIVERSIFIED VALUE FUND

LARGE CAP VALUE FUND

MID-CAP VALUE FUND

SMALL CAP VALUE FUND

SMALL CAP DIVERSIFIED VALUE FUND

GLOBAL VALUE FUND

INTERNATIONAL VALUE FUND

INTERNATIONAL SMALL CAP DIVERSIFIED VALUE FUND

VALUE OPPORTUNITIES FUND

HIGH YIELD FUND

SHAREHOLDER LETTER | | | 1 | | |

FUND INFORMATION | | | 4 | | |

FUND PERFORMANCE DATA | | | 6 | | |

SCHEDULE OF INVESTMENTS: | |

DIVERSIFIED VALUE FUND | | | 16 | | |

LARGE CAP VALUE FUND | | | 18 | | |

MID-CAP VALUE FUND | | | 20 | | |

| SMALL CAP VALUE FUND | | | 23 | | |

| SMALL CAP DIVERSIFIED VALUE FUND | | | 26 | | |

| GLOBAL VALUE FUND | | | 33 | | |

| INTERNATIONAL VALUE FUND | | | 35 | | |

| INTERNATIONAL SMALL CAP DIVERSIFIED VALUE FUND | | | 37 | | |

| VALUE OPPORTUNITIES FUND | | | 43 | | |

| HIGH YIELD FUND | | | 46 | | |

STATEMENTS OF ASSETS & LIABILITIES | | | 53 | | |

STATEMENTS OF OPERATIONS | | | 55 | | |

STATEMENTS OF CHANGES IN NET ASSETS | | | 57 | | |

FINANCIAL HIGHLIGHTS | | | 62 | | |

NOTES TO THE FINANCIAL STATEMENTS | | | 67 | | |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 81 | | |

| FUND EXPENSE EXAMPLES | | | 82 | | |

BOARD CONSIDERATIONS IN APPROVING CONTINUATION OF

INVESTMENT ADVISORY AGREEMENTS | | | 84 | | |

STATEMENT REGARDING LIQUIDITY RISK MANAGEMENT

PROGRAM | | | 86 | | |

| MANAGEMENT | | | 87 | | |

INFORMATION ABOUT THE FUNDS | | | BACK COVER | | |

DEAR SHAREHOLDER:

The following investment review and shareholder report relates to the activities of the Hotchkis & Wiley Funds for the 12 months ended June 30, 2022.

OVERVIEW

In the 12-month period ended June 30, 2022, the S&P 500® Index returned –11%, the MSCI World Index returned –14%, and the ICE BofA U.S. High Yield Index (high yield market) returned –13%. Several economic developments have sparked fears of a recession. The most recent real GDP growth was negative quarter-over-quarter, the war in Ukraine showed little signs of abating, inflation increased by the largest amount in more than 40 years, and an increasingly hawkish Federal Open Market Committee (FOMC) raised the Fed Funds rate by 150 basis points via three hikes over the past year (from 0.25% to 1.75%, upper bound). The Fed signaled further rate increases going forward to combat inflation. Other major central banks have raised rates also, and like the Fed, signaled further rate hikes going forward. Higher rates are generally bad for equities. It becomes more costly to borrow, increasing the cost of capital, which is the rate used to discount future cash flows. Higher rates impair long-duration equities disproportionately because most of the intrinsic value is derived from a terminal value estimate far into the future. In general, growth stocks are longer duration securities than value stocks. Unsurprisingly, value has outperformed growth in periods of elevated inflation and interest rates historically.

Value held up better than growth over the 12-month period. From a global sector perspective, energy was the best performer of the year by a large magnitude, returning +33%. The three least economically sensitive sectors — utilities, health care, and consumer staples — were next best, returning +4%, –2%, and –3%, respectively. All other sectors declined more than –10%. Communication services (–29%), consumer discretionary (–27%), and information technology (–19%) were the worst performers. These sectors comprise considerably larger portions of growth indexes. Combined, the three sectors averaged nearly two-thirds of the MSCI World Growth Index's total weight over the past year. This highlights growth indexes unusual concentration, the likes of which we have not observed since the tech bubble.

We are finding attractive equity opportunities in a variety of market segments. We are partial to select large cap software companies, which are not inexpensive on typical valuation metrics like price-to-earnings, enterprise value to earnings before interest and taxes, price-to-book, etc. They represent fantastic businesses, however trade at large discounts to our estimate of intrinsic value. Common traits among our positions are high returns on capital, captive customer bases, good balance sheets, and a substantial return of capital to shareholders. The stocks also trade at large discounts to other parts of the market generally viewed as high quality businesses, e.g., consumer staples, though with superior growth prospects. We also find many opportunities in energy and financials, across the market cap spectrum. Within energy, valuations remain uncommonly attractive despite the sector's significant outperformance recently, because valuations are coming off such a low base. Higher commodity prices have translated into strong free cash flow. Historically, elevated cash flows

in energy were routinely used to reinvest in new exploration projects. Recently, however, cash has been used to pay down considerable amounts of debt, de-risking the sector significantly. Dividends and share repurchases have also ramped up meaningfully. With balance sheets improved and cash flow still strong, we expect share repurchases to increase even further going forward — an accretive use of capital considering the still attractive valuations. Additionally, energy has been the best inflation hedge of all sectors dating back to the 1970s. In financials, we find banks unusually attractive. The Funds' banks trade at compelling valuations both relative to normal earnings power and tangible book values. The attractive valuations reflect the market's recession worries and the credit losses that typically coincide with economic slowdowns. Yet the capital position in the industry is such that even severe regulatory stress tests (most recently in June) are passed largely without comment. Banks also experience an earnings benefit should interest rates continue to climb — financials have been the best interest rate hedge of all sectors dating back to the 1970s.

Value continues to trade at a large discount to growth, despite its recent outperformance. The Funds' valuations represent larger-than-normal discounts to their respective benchmarks. We view a reversion toward a more normal valuation relationship as more likely than not, which would represent a conducive environment for our long-term fundamental value approach.

The high yield market's decline has resulted in yields and spreads increasing to levels we have not observed in some time. Spreads over treasuries widened to 587 basis points as of June 30, 2022, with more than a tenth of the market trading at spreads greater than 1,000 basis points. The high yield market's yield-to-worst closed the period at 8.9%, a function of both rising rates and spread widening. The number of attractive valuation opportunities has increased over the past year, though it took a negative market to get here. Nonetheless, we are more optimistic about our prospect to add value going forward than we were a year ago. We will continue to adhere to our competitive research advantage, particularly in small and mid cap credits, with a focus on strong asset coverage.

HOTCHKIS & WILEY DIVERSIFIED VALUE FUND

The Fund's Class I shares had a total return of –8.27% for the year ended June 30, 2022 compared to the Russell 1000® Value Index return of –6.82%.

Stock selection in consumer discretionary, industrials, and consumer staples detracted from performance in the period. The underweight exposure to non-cyclical sectors also hurt, as the Fund was underexposed to health care, consumer staples, and utilities. The overweight position and positive stock selection in energy was a significantly positive contributor. Positive stock selection in information technology and financials also helped. The largest detractors to relative performance in the 12-month period were General Electric, Citigroup, General Motors, Magna International, and Warner Bros. Discovery. The largest positive contributors were Marathon Oil, APA Corp., AIG, Elevance Health, and Shell.

1

HOTCHKIS & WILEY LARGE CAP VALUE FUND

The Fund's Class I shares had a total return of –9.31% for the year ended June 30, 2022 compared to the Russell 1000® Value Index return of –6.82%.

Over the 12-month period ended June 30, 2022, stock selection in consumer discretionary, industrials, and communication services detracted from relative performance. The underweight positions in health care, consumer staples, and utilities also hurt, along with the overweight exposure to information technology. The overweight position in energy, along with positive stock selection in the same sector helped relative performance. The underweight exposure to communication services and stock selection in financials were also positive contributors. The largest individual detractors to performance in the period were General Electric, General Motors, Citigroup, Magna International, and Warner Bros. Discovery; the largest positive contributors were Marathon Oil, APA Corp., Elevance Health, AIG, and Shell.

HOTCHKIS & WILEY MID-CAP VALUE FUND

The Fund's Class I shares had a total return of –2.34% for the year ended June 30, 2022 compared to the Russell Midcap® Value Index return of –10.00%.

Energy was the best-performing sector in the period by a wide margin. The Fund's overweight position and positive stock selection in the sector drove most of the outperformance. Positive stock selection in industrials was also a significant contributor. The underweight position and stock selection in consumer staples hurt relative performance. Stock selection in consumer discretionary and the underweight position in real estate detracted from performance. The largest positive contributors to relative performance in the 12-month period were Kosmos Energy, APA Corp., Fluor, Capricorn Energy, and Marathon Oil; the largest detractors were Royal Mail, CommScope, ODP Corp., Credit Suisse, and Adient.

HOTCHKIS & WILEY SMALL CAP VALUE FUND

The Fund's Class I shares had a total return of –3.42% for the year ended June 30, 2022 compared to the Russell 2000® Value Index return of –16.28%.

Positive stock selection drove most of the outperformance over the 12-month period. Stock selection was most positive in industrials, consumer discretionary, and communication services. The overweight position in energy and underweight position in health care also helped. Stock selection in real estate and the underweight positions in utilities and consumer staples detracted from performance. The largest positive contributors to relative performance were Range Resources, Fluor, Kosmos Energy, Meritor, and Points.com; the largest detractors were Seritage Growth Properties, Telos Corp., TrueBlue, Hanger, and Armstrong Flooring.

HOTCHKIS & WILEY SMALL CAP DIVERSIFIED VALUE FUND

The Fund's Class I shares had a total return of –9.34% for the year ended June 30, 2022 compared to the Russell 2000® Value Index return of –16.28%.

Stock selection was positive in 7 of the 11 GICS® sectors which helped relative performance. It was most positive in financials, industrials, and materials. The underweight positions in health care and communication services also helped, along with the overweight position in energy. Stock selection in energy, real estate, and consumer staples detracted from performance. The overweight position in consumer discretionary, along with the underweight positions in utilities, real estate, and consumer staples detracted from performance.

HOTCHKIS & WILEY GLOBAL VALUE FUND

The Fund's Class I shares had a total return of –11.86% for the year ended June 30, 2022 compared to the MSCI World Index return of –14.34%.

Both the overweight position in energy, and positive stock selection in the sector helped relative performance in the period. Positive stock selection in health care, financials, and information technology also helped. The underweight position in consumer discretionary and information technology, along with the overweight position in financials were positive contributors. Stock selection in consumer discretionary, consumer staples, and real estate detracted from performance. The underweight exposure to health care and no exposure to utilities hurt, as these were the best performing sectors for the benchmark after energy. The largest positive contributors to relative performance were Suncor Energy, Cenovus Energy, BAE Systems, Elevance Health, and AIG; the largest detractors were General Electric, Royal Mail, Credit Suisse, General Motors, and Warner Bros. Discovery.

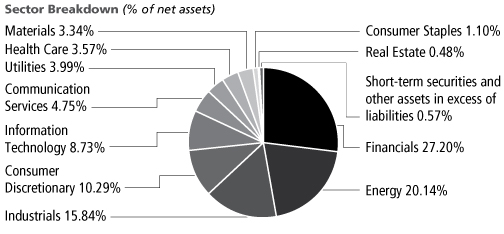

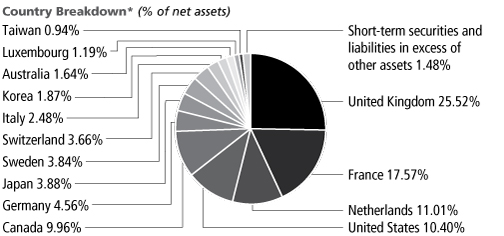

HOTCHKIS & WILEY INTERNATIONAL VALUE FUND

The Fund's Class I shares had a total return of –9.82% for the year ended June 30, 2022 compared to the MSCI World ex-USA Index return of –16.76%.

The index's only positive sector in the period was energy. The Fund's overweight position combined with positive stock selection in the sector were positive contributors to relative performance in the period. Positive stock selection in consumer discretionary and industrials also helped, along with the overweight exposure to financials. The underweight position and stock selection in health care detracted from performance. Stock selection in consumer staples also hurt. The largest positive contributors to relative performance were Cenovus Energy, BAE Systems, Kosmos Energy, Suncor Energy, and Points.com; the largest detractors were Royal Mail, Credit Suisse, Ericsson, Philips, and Magna International.

HOTCHKIS & WILEY INTERNATIONAL SMALL CAP DIVERSIFIED VALUE FUND

The Fund's Class I shares had a total return of –14.28% for the year ended June 30, 2022 compared to the MSCI World ex-USA Small Cap Index return of –23.02%.

Stock selection was positive in all 11 GICS® sectors, which drove most of the Fund's outperformance over the period. It was most positive in information technology, consumer discretionary, and financials. The overweight position in energy and financials also helped. The underweight exposure to real estate, utilities, and consumer staples detracted from performance.

2

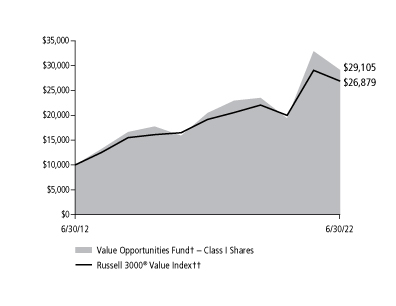

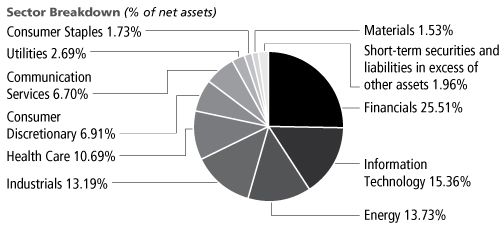

HOTCHKIS & WILEY VALUE OPPORTUNITIES FUND

The Fund's Class I shares had a total return of –11.50% for the year ended June 30, 2022 compared to the Russell 3000® Value return of –7.46%.

The overweight exposure to information technology was the Fund's largest detractor over the 12-month period, though this was more than offset by positive security selection in the sector. Security selection in real estate hurt performance, along with the underweight exposure to health care and utilities, and the overweight exposure to communication services. The overweight position in energy was a large positive contributor in the period. Positive security selection in health care also helped. The largest detractors to relative performance in the period were General Electric, Seritage Growth Properties, Credit Suisse, Royal Mail, and General Motors; the largest positive contributors were Range Resources, Triple-S Management, NOV, Inc., Kosmos Energy, and AIG.

HOTCHKIS & WILEY HIGH YIELD FUND

The Fund's Class I shares had a total return of –11.12% for the year ended June 30, 2022 compared to the ICE BofA BB-B U.S. High Yield Constrained Index return of –12.20%.

Positive credit selection in small cap credits contributed to relative performance in the period. Much of this was in energy, where positive credit selection was significantly positive. Positive credit selection in basic industry and services also helped, along with an underweight allocation to telecommunications. Credit selection in retail, leisure, and media detracted from performance in the period.

CONCLUSION

We appreciate your continued support of the Hotchkis & Wiley Funds, and we look forward to serving your investment needs in the future.

Sincerely,

| |

| |

| |

Anna Marie Lopez

President | | George Davis

Fund Manager | | Scott McBride

Fund Manager | |

| |

| |

| |

Patty McKenna

Fund Manager | | James Miles

Fund Manager | | Stan Majcher

Fund Manager | |

| |

| |

| |

David Green

Fund Manager | | Judd Peters

Fund Manager | | Ray Kennedy

Fund Manager | |

| |

| |

| |

Mark Hudoff

Fund Manager | | Patrick Meegan

Fund Manager | | Scott Rosenthal

Fund Manager | |

| |

| |

| |

Richard Mak

Fund Manager | | Ryan Thomes

Fund Manager | | Hunter Doble

Fund Manager | |

3

ABOUT FUND PERFORMANCE

The Diversified Value Fund, Large Cap Value Fund, Mid-Cap Value Fund, Small Cap Value Fund, Small Cap Diversified Value Fund, Global Value Fund, International Value Fund, Value Opportunities Fund and High Yield Fund have four authorized classes of shares (Class I, Class A, Class C and Class Z). The International Small Cap Diversified Value Fund has three authorized classes of shares (Class I, Class A and Class Z). Each share class has its own sales charge and expense structure, allowing you to invest in the way that best suits your needs. Currently, the International Value Fund and International Small Cap Diversified Value Fund are not offering Class A shares to investors; the Small Cap Diversified Value Fund, Global Value Fund and International Value Fund are not offering Class C shares to investors; and the Diversified Value Fund, Global Value Fund, International Value Fund and International Small Cap Diversified Value Fund are not offering Class Z shares to investors.

Class I shares have no initial sales charge and bear no ongoing distribution and service fees under a 12b-1 plan. Class I shares are available only to eligible investors.

Class A shares incur a maximum initial sales charge of 5.25% for the Diversified Value Fund, Large Cap Value Fund, Mid-Cap Value Fund, Small Cap Value Fund, Small Cap Diversified Value Fund, Global Value Fund, International Value Fund, International Small Cap Diversified Value Fund and Value Opportunities Fund and 3.75% for the High Yield Fund and an annual distribution and service fee of 0.25%.

Class C shares are subject to an annual distribution and service fee of 1.00%. In addition, Class C shares are subject to a 1.00% contingent deferred sales charge (CDSC) if redeemed within one year after purchase. Class C shares automatically convert to Class A shares approximately eight years after purchase and will then be subject to lower annual distribution and service fees.

Class Z shares have no initial sales charge and bear no ongoing distribution and service fees under a 12b-1 plan. Class Z shares are available only to eligible investors (provided that no compensation, administrative payments, sub-transfer agency payments and service payments are required).

FUND RISKS

Mutual fund investing involves risk; loss of principal is possible. The Mid-Cap Value Fund, Small Cap Value Fund, Small Cap Diversified Value Fund, Global Value Fund, International Value Fund, International Small Cap Diversified Value Fund and Value Opportunities Fund invest in small- and mid-capitalization companies which tend to have limited liquidity and greater price volatility than large-capitalization companies. The Value Opportunities Fund is a non-diversified fund which involves greater risk than investing in a diversified fund because a loss resulting from the decline in the value of one security may represent a greater portion of the total assets of a non-diversified fund. Growth stocks typically are more volatile than value stocks; however, value stocks have a lower expected growth rate in earnings and sales. The Value Opportunities Fund and High Yield Fund invest in debt securities that typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment by the Value Opportunities Fund and High Yield Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. The Value Opportunities Fund

and High Yield Fund may utilize derivative instruments, which derive their performance from the performance of an underlying asset, index, interest rate or currency exchange rate. Derivatives can be volatile and involve various types and degrees of risks. Depending upon the characteristics of particular derivatives, they can suddenly become illiquid. Investments by the High Yield Fund in asset-backed and mortgage-backed securities include additional risks that investors should be aware of such as credit risk, extension risk, prepayment risk, and default risk, as well as increased susceptibility to adverse economic developments. The Funds may invest in foreign securities, including developed and emerging markets, which involve greater volatility and political, economic, and currency risks.

MARKET INDEXES

The following are definitions for indexes used in the shareholder letter and the fund performance data on the following pages. These indexes are unmanaged and include the reinvestment of dividends, but do not reflect the payment of transaction costs and advisory and other fees associated with an investment in the Funds. The securities that comprise these indexes may differ substantially from the securities in the Funds' portfolios. The Funds' value disciplines may prevent or restrict investments in securities included in the benchmark indexes. It is not possible to invest directly in an index. Each index named is not the only index which may be used to characterize performance of a specific Fund and other indexes may portray different comparative performance.

S&P 500® Index, a capital weighted, unmanaged index, represents the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange.

Russell 1000® Index, an unmanaged index, measures the performance of the 1,000 largest companies in the Russell 3000® Index.

Russell 1000® Value Index measures the performance of those Russell 1000® companies with lower price-to-book ratios and lower forecasted growth values.

Russell Midcap® Index, an unmanaged index, measures the performance of the 800 smallest companies in the Russell 1000® Index.

Russell Midcap® Value Index measures the performance of those Russell Midcap® companies with lower price-to-book ratios and lower forecasted growth values.

Russell 2000® Index, an unmanaged index, measures the performance of the 2,000 smallest companies in the Russell 3000® Index.

Russell 2000® Value Index measures the performance of those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values.

Russell 3000® Index, an unmanaged index, is comprised of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

Russell 3000® Value Index measures the performance of those Russell 3000® companies with lower price-to-book ratios and lower forecasted growth values.

MSCI World Index is a free float-adjusted weighted index capturing large and mid cap representation across 23 Developed Markets (DM) countries.

4

MSCI World Growth Index is the growth investment style of the MSCI World Index. The growth investment style characteristics for index construction are defined using five variables: long-term forward EPS growth rate, short-term forward EPS growth rate, current internal growth rate and long-term historical EPS growth trend and long-term historical sales per share growth trend.

MSCI World ex-USA Index is a free float-adjusted weighted index capturing large and mid cap representation across 22 of 23 Developed Markets (DM) countries, excluding the United States.

MSCI World ex-USA Small Cap Index is a free float-adjusted weighted index capturing small cap representation across 22 of 23 Developed Markets (DM) countries, excluding the United States.

ICE BofA BB-B U.S. High Yield Constrained Index contains all securities in the ICE BofA U.S. High Yield Index rated BB+ through B- by S&P (or equivalent as rated by Moody's or Fitch), but caps issuer exposure at 2%. Index constituents are capitalization-weighted, based on their current amount outstanding, provided the total allocation to an individual issuer does not exceed 2%.

ICE BofA U.S. High Yield Index tracks the performance of below investment grade, but not in default, U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market, and includes issues with a credit rating of BBB or below, as rated by Moody's and S&P.

DISCLOSURE

Past performance does not guarantee future results.

The shareholder letter reflects opinions of Fund managers as of June 30, 2022. They are subject to change and any forecasts made cannot be guaranteed. The Funds might not continue to hold any securities mentioned and have no obligation to disclose purchases or sales in these securities. Please refer to the Schedule of Investments in this report for a complete list of Fund holdings for June 30, 2022. Indexes do not incur expenses or sales loads and are not available for investment.

The Global Industry Classification Standard (GICS®) was developed by MSCI, an independent provider of global indices and benchmark-related products and services, and Standard & Poor's (S&P), an independent international financial data and investment services company.

The GICS methodology has been widely accepted as an industry analysis framework for investment research, portfolio management and asset allocation. The GICS structure consists of 11 sectors, 24 industry groups, 69 industries and 158 sub-industries. Each stock that is classified will have a coding at all four of these levels.

Investing in value stocks presents the risk that value stocks may fall out of favor with investors and underperform other asset types during a given period.

Each type of asset class or investment product has a different risk-return profile, which should be considered when investing. All investments contain risk and may lose value.

Basis point (bp) is a unit equal to 1/100th of 1% (0.01%) and is used to denote the change in a financial instrument.

Market capitalization of a company is calculated by multiplying the number of outstanding shares by the current market price of a share.

Yield-to-worst is the lowest possible yield from owning a bond considering all potential call dates prior to maturity.

Credit Quality weights by rating were derived from the highest bond rating as determined by S&P, Moody's or Fitch. Bond ratings are grades given to bonds that indicate their credit quality as determined by private independent rating services such as S&P, Moody's and Fitch. These firms evaluate a bond issuer's financial strength, or its ability to pay a bond's principal and interest in a timely fashion. Ratings are expressed as letters ranging from 'AAA', which is the highest grade, to 'D', which is the lowest grade. In limited situations when none of the three rating agencies have issued a formal rating, the Advisor will classify the security as nonrated.

During the year ended June 30, 2022, the Value Opportunities Fund held futures contracts, which resulted in realized gains and unrealized losses, and purchased put options, which resulted in realized losses and unrealized gains.

5

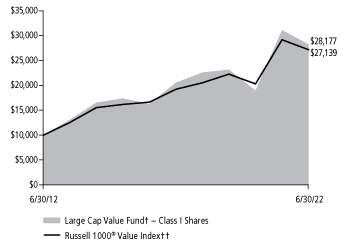

DIVERSIFIED VALUE FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | 10 Years | | Since

8/30/04* | |

Class I | |

Average annual total return | | | –8.27 | % | | | 7.23 | % | | | 10.97 | % | | | 7.21 | % | |

Class A | |

Average annual total return (with sales charge) | | | –13.31 | % | | | 5.82 | % | | | 10.09 | % | | | 6.62 | % | |

Average annual total return (without sales charge) | | | –8.49 | % | | | 6.97 | % | | | 10.69 | % | | | 6.94 | % | |

Class C | |

Average annual total return (with CDSC) | | | –10.10 | % | | | 6.16 | % | | | 9.86 | % | | | 6.16 | % | |

Average annual total return (without CDSC) | | | –9.20 | % | | | 6.16 | % | | | 9.86 | % | | | 6.16 | % | |

Russell 1000® Value Index†† | |

Average annual total return | | | –6.82 | % | | | 7.17 | % | | | 10.50 | % | | | 7.79 | % | |

Russell 1000® Index†† | |

Average annual total return | | | –13.04 | % | | | 11.00 | % | | | 12.82 | % | | | 9.45 | % | |

Average annual total returns with sales charge and CDSC shown for Class A and Class C shares, respectively, have been adjusted to reflect the applicable sales charges of each specific class. Returns for Class A reflect the maximum initial sales charge of 5.25%. Class C shares have no adjustment for sales charges, but redemptions within one year of purchase may be subject to a CDSC of 1%. Average annual total returns without sales charge or CDSC do not reflect the sales charges. Had the sales charge or CDSC been included, the Fund's returns would have been lower.

† The Fund invests primarily in equity securities of companies with market capitalizations similar to the Russell 1000® Index.

†† See index descriptions in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I, Class A and Class C.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 1.01% for Class I shares, 1.22% for Class A shares and 1.98% for Class C shares, respectively.

6

LARGE CAP VALUE FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | 10 Years | | Since

6/24/87* | |

Class I | |

Average annual total return | | | –9.31 | % | | | 6.56 | % | | | 10.91 | % | | | 8.81 | % | |

Class A | |

Average annual total return (with sales charge) | | | –14.28 | % | | | 5.15 | % | | | 10.04 | % | | | 8.39 | % | |

Average annual total return (without sales charge) | | | –9.53 | % | | | 6.29 | % | | | 10.64 | % | | | 8.56 | % | |

Class C | |

Average annual total return (with CDSC) | | | –11.07 | % | | | 5.53 | % | | | 9.82 | % | | | 7.75 | % | |

Average annual total return (without CDSC) | | | –10.17 | % | | | 5.53 | % | | | 9.82 | % | | | 7.75 | % | |

Class Z | |

Average annual total return | | | –9.22 | % | | | 6.63 | % | | | 10.95 | % | | | 8.82 | % | |

Russell 1000® Value Index†† | |

Average annual total return | | | –6.82 | % | | | 7.17 | % | | | 10.50 | % | | | 9.48 | % | |

Russell 1000® Index†† | |

Average annual total return | | | –13.04 | % | | | 11.00 | % | | | 12.82 | % | | | 9.88 | % | |

Returns shown for Class A, Class C, and Class Z shares for the periods prior to their inception are derived from the historical performance of Class I shares of the Fund during such periods and have been adjusted to reflect the higher total annual operating expenses of Class A and Class C shares. (Inception dates: Class A — 10/26/01; Class C — 2/4/02; Class Z — 9/30/19.)

Average annual total returns with sales charge and CDSC shown for Class A and Class C shares, respectively, have been adjusted to reflect the applicable sales charges of each specific class. Returns for Class A reflect the maximum initial sales charge of 5.25%. Class C shares have no adjustment for sales charges, but redemptions within one year of purchase may be subject to a CDSC of 1%. Average annual total returns without sales charge or CDSC do not reflect the sales charges. Had the sales charge or CDSC been included, the Fund's returns would have been lower.

† The Fund invests primarily in equity securities of companies with market capitalizations similar to the Russell 1000® Index.

†† See index descriptions in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I is 6/24/87. Average annual total return for the Russell 1000® Value Index reflects a beginning date of 6/30/87.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 0.97% for Class I shares, 1.18% for Class A shares, 1.91% for Class C shares and 0.86% for Class Z shares, respectively.

7

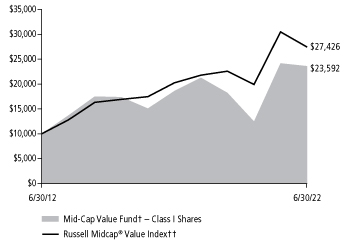

MID-CAP VALUE FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | 10 Years | | Since

1/2/97* | |

Class I | |

Average annual total return | | | –2.34 | % | | | 4.88 | % | | | 8.96 | % | | | 10.72 | % | |

Class A | |

Average annual total return (with sales charge) | | | –7.65 | % | | | 3.53 | % | | | 8.12 | % | | | 10.22 | % | |

Average annual total return (without sales charge) | | | –2.54 | % | | | 4.66 | % | | | 8.71 | % | | | 10.45 | % | |

Class C | |

Average annual total return (with CDSC) | | | –4.26 | % | | | 3.86 | % | | | 7.89 | % | | | 9.65 | % | |

Average annual total return (without CDSC) | | | –3.29 | % | | | 3.86 | % | | | 7.89 | % | | | 9.65 | % | |

Class Z | |

Average annual total return | | | –2.23 | % | | | 4.96 | % | | | 9.00 | % | | | 10.73 | % | |

Russell Midcap® Value Index†† | |

Average annual total return | | | –10.00 | % | | | 6.27 | % | | | 10.62 | % | | | 9.77 | % | |

Russell Midcap® Index†† | |

Average annual total return | | | –17.30 | % | | | 7.96 | % | | | 11.29 | % | | | 9.76 | % | |

Returns shown for Class A, Class C, and Class Z shares for the periods prior to their inception are derived from the historical performance of Class I shares of the Fund during such periods and have been adjusted to reflect the higher total annual operating expenses of Class A and Class C shares. (Inception dates: Class A, Class C — 1/2/01; Class Z — 9/30/19.)

Average annual total returns with sales charge and CDSC shown for Class A and Class C shares, respectively, have been adjusted to reflect the applicable sales charges of each specific class. Returns for Class A reflect the maximum initial sales charge of 5.25%. Class C shares have no adjustment for sales charges, but redemptions within one year of purchase may be subject to a CDSC of 1%. Average annual total returns without sales charge or CDSC do not reflect the sales charges. Had the sales charge or CDSC been included, the Fund's returns would have been lower.

† The Fund invests primarily in equity securities of companies with market capitalizations similar to the Russell Midcap® Index.

†† See index descriptions in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 1.01% for Class I shares, 1.21% for Class A shares, 1.97% for Class C shares and 0.87% for Class Z shares, respectively.

8

SMALL CAP VALUE FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | 10 Years | | Since

9/20/85* | |

Class I | |

Average annual total return | | | –3.42 | % | | | 6.30 | % | | | 10.37 | % | | | 10.91 | % | |

Class A | |

Average annual total return (with sales charge) | | | –8.62 | % | | | 4.94 | % | | | 9.52 | % | | | 10.50 | % | |

Average annual total return (without sales charge) | | | –3.56 | % | | | 6.08 | % | | | 10.11 | % | | | 10.66 | % | |

Class C | |

Average annual total return (with CDSC) | | | –5.21 | % | | | 5.30 | % | | | 9.30 | % | | | 9.86 | % | |

Average annual total return (without CDSC) | | | –4.25 | % | | | 5.30 | % | | | 9.30 | % | | | 9.86 | % | |

Class Z | |

Average annual total return | | | –3.22 | % | | | 6.41 | % | | | 10.42 | % | | | 10.92 | % | |

Russell 2000® Value Index†† | |

Average annual total return | | | –16.28 | % | | | 4.89 | % | | | 9.05 | % | | | 10.27 | % | |

Russell 2000® Index†† | |

Average annual total return | | | –25.20 | % | | | 5.17 | % | | | 9.35 | % | | | 9.24 | % | |

Returns shown for Class A, Class C, and Class Z shares for the periods prior to their inception are derived from the historical performance of Class I shares of the Fund during such periods and have been adjusted to reflect the higher total annual operating expenses of Class A and Class C shares. (Inception dates: Class A — 10/6/00; Class C — 2/4/02: Class Z — 9/30/19.)

Average annual total returns with sales charge and CDSC shown for Class A and Class C shares, respectively, have been adjusted to reflect the applicable sales charges of each specific class. Returns for Class A reflect the maximum initial sales charge of 5.25%. Class C shares have no adjustment for sales charges, but redemptions within one year of purchase may be subject to a CDSC of 1%. Average annual total returns without sales charge or CDSC do not reflect the sales charges. Had the sales charge or CDSC been included, the Fund's returns would have been lower.

† The Fund invests primarily in equity securities of companies with market capitalizations similar to the Russell 2000® Index.

†† See index descriptions in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I is 9/20/85. Average annual total return for the Russell 2000® Value Index reflects a beginning date of 9/30/85.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 1.06% for Class I shares, 1.21% for Class A shares, 1.94% for Class C shares and 0.86% for Class Z shares, respectively.

9

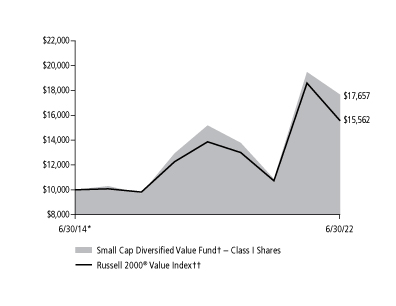

SMALL CAP DIVERSIFIED VALUE FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | Since

6/30/14* | |

Class I | |

Average annual total return | | | –9.34 | % | | | 6.44 | % | | | 7.37 | % | |

Class A | |

Average annual total return (with sales charge) | | | –14.31 | % | | | 5.05 | % | | | 6.38 | % | |

Average annual total return (without sales charge) | | | –9.57 | % | | | 6.19 | % | | | 7.09 | % | |

Class Z | |

Average annual total return | | | –9.38 | % | | | 6.44 | % | | | 7.36 | % | |

Russell 2000® Value Index†† | |

Average annual total return | | | –16.28 | % | | | 4.89 | % | | | 5.68 | % | |

Russell 2000® Index†† | |

Average annual total return | | | –25.20 | % | | | 5.17 | % | | | 5.98 | % | |

Returns shown for Class Z shares for the periods prior to its inception are derived from the historical performance of Class I shares of the Fund during such periods. (Inception date: Class Z — 9/30/19.)

Average annual total returns with sales charge shown for Class A shares have been adjusted to reflect the applicable sales charge of the class. Returns for Class A reflect the maximum initial sales charge of 5.25%. Average annual total returns without sales charge do not reflect the sales charge. Had the sales charge been included, the Fund's returns would have been lower.

† The Fund invests primarily in equity securities of companies with market capitalizations similar to the Russell 2000® Index.

†† See index descriptions in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I and Class A.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 0.87% for Class I shares, 1.15% for Class A shares and 0.76% for Class Z shares, respectively.

10

GLOBAL VALUE FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | Since

12/31/12* | |

Class I | |

Average annual total return | | | –11.86 | % | | | 3.71 | % | | | 7.44 | % | |

Class A | |

Average annual total return (with sales charge) | | | –16.69 | % | | | 2.34 | % | | | 6.57 | % | |

Average annual total return (without sales charge) | | | –12.07 | % | | | 3.45 | % | | | 7.18 | % | |

MSCI World Index†† | |

Average annual total return | | | –14.34 | % | | | 7.67 | % | | | 9.01 | % | |

Returns shown for Class A shares for the periods prior to its inception are derived from the historical performance of Class I shares of the Fund during such periods and have been adjusted to reflect the higher total annual operating expenses of the class. (Inception date: Class A — 8/30/13.)

Average annual total returns with sales charge shown for Class A shares have been adjusted to reflect the applicable sales charge of the class. Returns for Class A reflect the maximum initial sales charge of 5.25%. Average annual total returns without sales charge do not reflect the sales charge. Had the sales charge been included, the Fund's returns would have been lower.

† The Fund invests primarily in U.S. and non-U.S. companies.

†† See index description in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 1.22% for Class I shares and 1.46% for Class A shares, respectively.

11

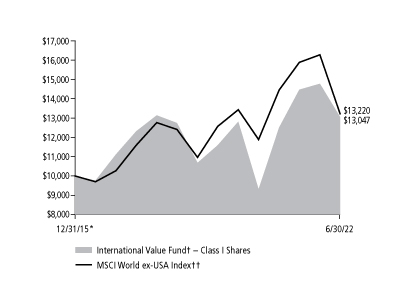

INTERNATIONAL VALUE FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | Since

12/31/15* | |

Class I | |

Average annual total return | | | –9.82 | % | | | 1.17 | % | | | 4.18 | % | |

MSCI World ex-USA Index†† | |

Average annual total return | | | –16.76 | % | | | 2.66 | % | | | 4.39 | % | |

† The Fund invests primarily in non-U.S. companies.

†† See index description in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 4.87% for Class I shares.

12

INTERNATIONAL SMALL CAP DIVERSIFIED VALUE FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Period ended June 30, 2022 | | 1 Year | | Since

6/30/20* | |

Class I | |

Average annual total return | | | ��14.28 | % | | | 13.99 | % | |

MSCI World ex-USA Small Cap Index†† | |

Average annual total return | | | –23.02 | % | | | 4.65 | % | |

† The Fund invests primarily in equity securities of non-U.S. companies with market capitalizations similar to the MSCI World ex-USA Small Cap Index.

†† See index description in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 4.23% for Class I shares.

13

VALUE OPPORTUNITIES FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | 10 Years | | Since

12/31/02* | |

Class I | |

Average annual total return | | | –11.50 | % | | | 7.31 | % | | | 11.27 | % | | | 11.42 | % | |

Class A | |

Average annual total return (with sales charge) | | | –16.34 | % | | | 5.89 | % | | | 10.40 | % | | | 10.88 | % | |

Average annual total return (without sales charge) | | | –11.72 | % | | | 7.03 | % | | | 11.00 | % | | | 11.18 | % | |

Class C | |

Average annual total return (with CDSC) | | | –13.11 | % | | | 6.26 | % | | | 10.18 | % | | | 10.34 | % | |

Average annual total return (without CDSC) | | | –12.34 | % | | | 6.26 | % | | | 10.18 | % | | | 10.34 | % | |

Class Z | |

Average annual total return | | | –11.40 | % | | | 7.36 | % | | | 11.30 | % | | | 11.43 | % | |

Russell 3000® Value Index†† | |

Average annual total return | | | –7.46 | % | | | 7.01 | % | | | 10.39 | % | | | 8.76 | % | |

Russell 3000® Index†† | |

Average annual total return | | | –13.87 | % | | | 10.60 | % | | | 12.57 | % | | | 10.02 | % | |

Returns shown for Class C and Class Z shares for the periods prior to their inception are derived from the historical performance of Class I shares of the Fund during such periods and have been adjusted to reflect the higher total annual operating expenses of Class C shares. (Inception dates: Class C — 8/28/03; Class Z — 9/30/19.)

Average annual total returns with sales charge and CDSC shown for Class A and Class C shares, respectively, have been adjusted to reflect the applicable sales charges of each specific class. Returns for Class A reflect the maximum initial sales charge of 5.25%. Class C shares have no adjustment for sales charges, but redemptions within one year of purchase may be subject to a CDSC of 1%. Average annual total returns without sales charge or CDSC do not reflect the sales charge. Had the sales charge or CDSC been included, the Fund's returns would have been lower.

† The Fund invests primarily in securities of companies with strong capital appreciation potential.

†† See index descriptions in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I and Class A.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 0.94% for Class I shares, 1.20% for Class A shares, 1.91% for Class C shares and 0.86% for Class Z shares, respectively.

14

HIGH YIELD FUND

Total Return Based on a $10,000 Investment

Comparative Results†††

For Periods ended June 30, 2022 | | 1 Year | | 5 Years | | 10 Years | | Since

3/31/09* | |

Class I | |

Average annual total return | | | –11.12 | % | | | 1.06 | % | | | 3.95 | % | | | 7.43 | % | |

Class A | |

Average annual total return (with sales charge) | | | –14.61 | % | | | 0.02 | % | | | 3.28 | % | | | 6.79 | % | |

Average annual total return (without sales charge) | | | –11.28 | % | | | 0.78 | % | | | 3.67 | % | | | 7.10 | % | |

Class C | |

Average annual total return (with CDSC) | | | –12.79 | % | | | 0.08 | % | | | 2.92 | % | | | 6.37 | % | |

Average annual total return (without CDSC) | | | –11.94 | % | | | 0.08 | % | | | 2.92 | % | | | 6.37 | % | |

Class Z | |

Average annual total return | | | –11.04 | % | | | 1.14 | % | | | 3.99 | % | | | 7.46 | % | |

ICE BofA BB-B U.S. High Yield Constrained Index†† | |

Average annual total return | | | –12.20 | % | | | 2.07 | % | | | 4.34 | % | | | 7.76 | % | |

Returns shown for Class A, Class C, and Class Z shares for the periods prior to their inception are derived from the historical performance of Class I shares of the Fund during such periods and have been adjusted to reflect the higher total annual operating expenses of Class A and Class C shares. (Inception dates: Class A — 5/29/09; Class C — 12/31/12; Class Z — 3/29/18.)

Average annual total returns with sales charge and CDSC shown for Class A and Class C shares, respectively, have been adjusted to reflect the applicable sales charges of each specific class. Returns for Class A reflect the maximum initial sales charge of 3.75%. Class C shares have no adjustment for sales charges, but redemptions within one year of purchase may be subject to a CDSC of 1%. Average annual total returns without sales charge or CDSC do not reflect the sales charges. Had the sales charge or CDSC been included, the Fund's returns would have been lower.

† The Fund invests primarily in high yield securities.

†† See index description in the Fund Information section.

††† Fund returns during certain periods shown reflect a fee waiver and/or expense reimbursement. Without waiver/reimbursement, returns would have been lower. Returns shown include the reinvestment of all dividends.

* Commencement of Class I.

Past performance is not indicative of future results and the graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, access our website at www.hwcm.com.

The gross expense ratio for the year ended June 30, 2022 is 0.77% for Class I shares, 0.98% for Class A shares, 1.77% for Class C shares and 0.65% for Class Z shares, respectively.

15

Schedule of Investments — June 30, 2022

Hotchkis & Wiley Diversified Value Fund

Largest Equity Holdings | | Percent of

net assets | |

Citigroup, Inc. | | | 4.85 | % | |

General Electric Company | | | 4.76 | % | |

Wells Fargo & Company | | | 3.91 | % | |

American International Group, Inc. | | | 3.76 | % | |

Microsoft Corp. | | | 2.94 | % | |

Alphabet, Inc. | | | 2.78 | % | |

Oracle Corp. | | | 2.77 | % | |

The Goldman Sachs Group, Inc. | | | 2.71 | % | |

Elevance Health, Inc. | | | 2.70 | % | |

PPL Corp. | | | 2.66 | % | |

COMMON

STOCKS — 99.20% | | Shares

Held | | Value | |

COMMUNICATION SERVICES — 9.77%

Entertainment — 1.74% | |

Warner Bros. Discovery, Inc. (a) | | | 108,900 | | | $ | 1,461,438 | | |

Interactive Media & Services — 2.78% | |

Alphabet, Inc. (a) | | | 1,070 | | | | 2,331,808 | | |

Media — 3.90% | |

Comcast Corp. | | | 39,100 | | | | 1,534,284 | | |

News Corp. | | | 57,000 | | | | 888,060 | | |

Omnicom Group, Inc. | | | 6,100 | | | | 388,021 | | |

Paramount Global | | | 18,700 | | | | 461,516 | | |

| | | | 3,271,881 | | |

Wireless Telecommunication Services — 1.35% | |

Vodafone Group PLC — ADR | | | 72,963 | | | | 1,136,764 | | |

TOTAL COMMUNICATION SERVICES | | | 8,201,891 | | |

CONSUMER DISCRETIONARY — 6.60%

Auto Components — 3.27% | |

Adient PLC (a) | | | 8,974 | | | | 265,899 | | |

Aptiv PLC (a) | | | 7,000 | | | | 623,490 | | |

The Goodyear Tire & Rubber Company (a) | | | 20,600 | | | | 220,626 | | |

Magna International, Inc. | | | 29,800 | | | | 1,636,020 | | |

| | | | 2,746,035 | | |

Automobiles — 2.64% | |

General Motors Company (a) | | | 69,900 | | | | 2,220,024 | | |

Hotels, Restaurants & Leisure — 0.69% | |

Booking Holdings, Inc. (a) | | | 330 | | | | 577,167 | | |

TOTAL CONSUMER DISCRETIONARY | | | 5,543,226 | | |

CONSUMER STAPLES — 1.72%

Personal Products — 1.72% | |

Unilever PLC — ADR | | | 31,600 | | | | 1,448,228 | | |

TOTAL CONSUMER STAPLES | | | 1,448,228 | | |

| | | Shares

Held | | Value | |

ENERGY — 11.99%

Energy Equipment & Services — 3.66% | |

Baker Hughes Company | | | 14,000 | | | $ | 404,180 | | |

Halliburton Company | | | 32,700 | | | | 1,025,472 | | |

NOV, Inc. | | | 75,600 | | | | 1,278,396 | | |

Schlumberger NV | | | 10,300 | | | | 368,328 | | |

| | | | 3,076,376 | | |

Oil, Gas & Consumable Fuels — 8.33% | |

APA Corp. | | | 46,700 | | | | 1,629,830 | | |

Cenovus Energy, Inc. | | | 28,800 | | | | 547,488 | | |

Hess Corp. | | | 8,900 | | | | 942,866 | | |

Marathon Oil Corp. | | | 77,900 | | | | 1,751,192 | | |

Murphy Oil Corp. | | | 20,200 | | | | 609,838 | | |

Shell PLC — ADR | | | 28,962 | | | | 1,514,423 | | |

| | | | 6,995,637 | | |

TOTAL ENERGY | | | 10,072,013 | | |

FINANCIALS — 25.03%

Banks — 11.02% | |

Citigroup, Inc. | | | 88,574 | | | | 4,073,518 | | |

Citizens Financial Group, Inc. | | | 23,900 | | | | 852,991 | | |

First Citizens BancShares, Inc. | | | 1,592 | | | | 1,040,818 | | |

Wells Fargo & Company | | | 83,834 | | | | 3,283,778 | | |

| | | | 9,251,105 | | |

Capital Markets — 7.34% | |

The Bank of New York Mellon Corp. | | | 44,000 | | | | 1,835,240 | | |

Credit Suisse Group AG — ADR | | | 102,400 | | | | 580,608 | | |

The Goldman Sachs Group, Inc. | | | 7,650 | | | | 2,272,203 | | |

State Street Corp. | | | 24,000 | | | | 1,479,600 | | |

| | | | 6,167,651 | | |

Diversified Financial Services — 0.47% | |

Equitable Holdings, Inc. | | | 15,100 | | | | 393,657 | | |

The accompanying notes are an integral part of these financial statements.

16

Schedule of Investments — June 30, 2022

Hotchkis & Wiley Diversified Value Fund

| | | Shares

Held | | Value | |

Insurance — 6.20% | |

American International Group, Inc. | | | 61,700 | | | $ | 3,154,721 | | |

The Hartford Financial Services Group, Inc. | | | 21,300 | | | | 1,393,659 | | |

The Travelers Companies, Inc. | | | 3,900 | | | | 659,607 | | |

| | | | 5,207,987 | | |

TOTAL FINANCIALS | | | 21,020,400 | | |

HEALTH CARE — 10.99%

Health Care Equipment & Supplies — 1.59% | |

Medtronic PLC | | | 8,882 | | | | 797,159 | | |

Zimmer Biomet Holdings, Inc. | | | 5,100 | | | | 535,806 | | |

| | | | 1,332,965 | | |

Health Care Providers & Services — 7.66% | |

Centene Corp. (a) | | | 14,600 | | | | 1,235,306 | | |

CVS Health Corp. | | | 13,200 | | | | 1,223,112 | | |

Elevance Health, Inc. | | | 4,700 | | | | 2,268,126 | | |

HCA Healthcare, Inc. | | | 4,600 | | | | 773,076 | | |

Humana, Inc. | | | 2,000 | | | | 936,140 | | |

| | | | 6,435,760 | | |

Pharmaceuticals — 1.74% | |

GSK PLC — ADR | | | 15,300 | | | | 666,009 | | |

Sanofi — ADR | | | 15,800 | | | | 790,474 | | |

| | | | 1,456,483 | | |

TOTAL HEALTH CARE | | | 9,225,208 | | |

INDUSTRIALS — 13.52%

Aerospace & Defense — 2.22% | |

The Boeing Company (a) | | | 7,000 | | | | 957,040 | | |

Raytheon Technologies Corp. | | | 9,400 | | | | 903,434 | | |

| | | | 1,860,474 | | |

Air Freight & Logistics — 2.51% | |

FedEx Corp. | | | 9,300 | | | | 2,108,403 | | |

Construction & Engineering — 0.35% | |

Fluor Corp. (a) | | | 12,200 | | | | 296,948 | | |

Industrial Conglomerates — 4.76% | |

General Electric Company | | | 62,737 | | | | 3,994,465 | | |

Machinery — 3.68% | |

| CNH Industrial NV | | | 90,500 | | | | 1,048,895 | | |

Cummins, Inc. | | | 5,700 | | | | 1,103,121 | | |

Iveco Group NV (a) (v) | | | 20,620 | | | | 109,173 | | |

PACCAR, Inc. | | | 10,100 | | | | 831,634 | | |

| | | | 3,092,823 | | |

TOTAL INDUSTRIALS | | | 11,353,113 | | |

INFORMATION TECHNOLOGY — 15.59%

Communications Equipment — 3.50% | |

F5, Inc. (a) | | | 13,000 | | | | 1,989,520 | | |

Telefonaktiebolaget LM Ericsson — ADR | | | 127,600 | | | | 944,240 | | |

| | | | 2,933,760 | | |

| | | Shares

Held | | Value | |

Electronic Equipment, Instruments & Components — 2.27% | |

Corning, Inc. | | | 33,300 | | | $ | 1,049,283 | | |

TE Connectivity Ltd. | | | 7,600 | | | | 859,940 | | |

| | | | 1,909,223 | | |

IT Services — 1.09% | |

Cognizant Technology Solutions Corp. | | | 7,000 | | | | 472,430 | | |

Fiserv, Inc. (a) | | | 5,000 | | | | 444,850 | | |

| | | | 917,280 | | |

Semiconductors & Semiconductor Equipment — 0.98% | |

Micron Technology, Inc. | | | 14,800 | | | | 818,144 | | |

Software — 7.75% | |

Microsoft Corp. | | | 9,600 | | | | 2,465,568 | | |

Oracle Corp. | | | 33,300 | | | | 2,326,671 | | |

Workday, Inc. (a) | | | 12,300 | | | | 1,716,834 | | |

| | | | 6,509,073 | | |

TOTAL INFORMATION TECHNOLOGY | | | 13,087,480 | | |

MATERIALS — 1.33%

Chemicals — 0.94% | |

Olin Corp. | | | 17,000 | | | | 786,760 | | |

Containers & Packaging — 0.39% | |

International Paper Company | | | 7,900 | | | | 330,457 | | |

TOTAL MATERIALS | | | 1,117,217 | | |

UTILITIES — 2.66%

Electric Utilities — 2.66% | |

PPL Corp. | | | 82,300 | | | | 2,232,799 | | |

TOTAL UTILITIES | | | 2,232,799 | | |

Total common stocks

(Cost $79,535,935) | | | | | 83,301,575 | | |

Total long-term investments

(Cost $79,535,935) | | | | | 83,301,575 | | |

SHORT-TERM

INVESTMENTS — 0.80% | | Principal

Amount | | | |

Time Deposits — 0.80% | |

Barclays PLC, 0.91%, 07/01/2022* | | $ | 670,660 | | | | 670,660 | | |

Total short-term investments

(Cost $670,660) | | | 670,660 | | |

Total investments — 100.00%

(Cost $80,206,595) | | | | | 83,972,235 | | |

Liabilities in excess of other assets — 0.00% | | | | | (3,984 | ) | |

Net assets — 100.00% | | $ | 83,968,251 | | |

(a) — Non-income producing security.

(v) — Security was fair valued as a result of market movements following the close of local trading using a third-party vendor's proprietary fair value pricing model. The total market value of these securities was $109,173, which represented 0.13% of net assets. See Security Valuation in Note 1 in Notes to the Financial Statements.

ADR — American Depositary Receipt

* — Invested through a cash management account administered by Brown Brothers Harriman & Co.

The accompanying notes are an integral part of these financial statements.

17

Schedule of Investments — June 30, 2022

Hotchkis & Wiley Large Cap Value Fund

Largest Equity Holdings | | Percent of

net assets | |

General Electric Company | | | 4.88 | % | |

Citigroup, Inc. | | | 4.86 | % | |

Wells Fargo & Company | | | 3.91 | % | |

American International Group, Inc. | | | 3.70 | % | |

General Motors Company | | | 3.37 | % | |

Elevance Health, Inc. | | | 3.17 | % | |

F5, Inc. | | | 3.13 | % | |

Oracle Corp. | | | 3.12 | % | |

The Goldman Sachs Group, Inc. | | | 2.97 | % | |

FedEx Corp. | | | 2.85 | % | |

COMMON

STOCKS — 98.04% | | Shares

Held | | Value | |

COMMUNICATION SERVICES — 6.70%

Entertainment — 2.03% | |

Warner Bros. Discovery, Inc. (a) | | | 611,400 | | | $ | 8,204,988 | | |

Interactive Media & Services — 0.97% | |

Alphabet, Inc. (a) | | | 1,800 | | | | 3,922,668 | | |

Media — 2.20% | |

Comcast Corp. | | | 227,000 | | | | 8,907,480 | | |

Wireless Telecommunication Services — 1.50% | |

Vodafone Group PLC — ADR | | | 390,944 | | | | 6,090,908 | | |

TOTAL COMMUNICATION SERVICES | | | 27,126,044 | | |

CONSUMER DISCRETIONARY — 6.91%

Auto Components — 2.76% | |

Adient PLC (a) | | | 44,891 | | | | 1,330,120 | | |

Magna International, Inc. | | | 179,300 | | | | 9,843,570 | | |

| | | | 11,173,690 | | |

Automobiles — 3.37% | |

General Motors Company (a) | | | 430,300 | | | | 13,666,328 | | |

Hotels, Restaurants & Leisure — 0.78% | |

Booking Holdings, Inc. (a) | | | 1,800 | | | | 3,148,182 | | |

TOTAL CONSUMER DISCRETIONARY | | | 27,988,200 | | |

CONSUMER STAPLES — 1.73%

Personal Products — 1.73% | |

Unilever PLC — ADR | | | 152,500 | | | | 6,989,075 | | |

TOTAL CONSUMER STAPLES | | | 6,989,075 | | |

ENERGY — 13.73%

Energy Equipment & Services — 4.17% | |

Baker Hughes Company | | | 70,100 | | | | 2,023,787 | | |

Halliburton Company | | | 109,500 | | | | 3,433,920 | | |

NOV, Inc. | | | 508,200 | | | | 8,593,662 | | |

Schlumberger NV | | | 79,300 | | | | 2,835,768 | | |

| | | | 16,887,137 | | |

| | | Shares

Held | | Value | |

Oil, Gas & Consumable Fuels — 9.56% | |

APA Corp. | | | 236,400 | | | $ | 8,250,360 | | |

Hess Corp. | | | 54,100 | | | | 5,731,354 | | |

Marathon Oil Corp. | | | 431,200 | | | | 9,693,376 | | |

Murphy Oil Corp. | | | 90,570 | | | | 2,734,308 | | |

Shell PLC — ADR | | | 160,872 | | | | 8,411,997 | | |

Suncor Energy, Inc. | | | 110,000 | | | | 3,857,700 | | |

| | | | 38,679,095 | | |

TOTAL ENERGY | | | 55,566,232 | | |

FINANCIALS — 25.51%

Banks — 10.27% | |

Citigroup, Inc. | | | 427,788 | | | | 19,673,970 | | |

Citizens Financial Group, Inc. | | | 169,700 | | | | 6,056,593 | | |

Wells Fargo & Company | | | 403,863 | | | | 15,819,314 | | |

| | | | 41,549,877 | | |

Capital Markets — 8.04% | |

The Bank of New York Mellon Corp. | | | 228,000 | | | | 9,509,880 | | |

Credit Suisse Group AG — ADR (l) | | | 535,500 | | | | 3,036,285 | | |

The Goldman Sachs Group, Inc. | | | 40,500 | | | | 12,029,310 | | |

State Street Corp. | | | 129,200 | | | | 7,965,180 | | |

| | | | 32,540,655 | | |

Diversified Financial Services — 0.50% | |

Equitable Holdings, Inc. | | | 77,600 | | | | 2,023,032 | | |

Insurance — 6.70% | |

American International Group, Inc. | | | 292,900 | | | | 14,975,977 | | |

The Hartford Financial Services Group, Inc. | | | 120,200 | | | | 7,864,686 | | |

The Travelers Companies, Inc. | | | 25,300 | | | | 4,278,989 | | |

| | | | 27,119,652 | | |

TOTAL FINANCIALS | | | 103,233,216 | | |

HEALTH CARE — 10.69%

Health Care Equipment & Supplies — 2.47% | |

Medtronic PLC | | | 73,400 | | | | 6,587,650 | | |

Zimmer Biomet Holdings, Inc. | | | 32,700 | | | | 3,435,462 | | |

| | | | 10,023,112 | | |

The accompanying notes are an integral part of these financial statements.

18

Schedule of Investments — June 30, 2022

Hotchkis & Wiley Large Cap Value Fund

| | | Shares

Held | | Value | |

Health Care Providers & Services — 5.91% | |

CVS Health Corp. | | | 67,000 | | | $ | 6,208,220 | | |

Elevance Health, Inc. | | | 26,600 | | | | 12,836,628 | | |

HCA Healthcare, Inc. | | | 29,000 | | | | 4,873,740 | | |

| | | | 23,918,588 | | |

Pharmaceuticals — 2.31% | |

GSK PLC — ADR | | | 121,300 | | | | 5,280,189 | | |

Sanofi — ADR | | | 81,200 | | | | 4,062,436 | | |

| | | | 9,342,625 | | |

TOTAL HEALTH CARE | | | 43,284,325 | | |

INDUSTRIALS — 13.19%

Aerospace & Defense — 0.64% | |

Huntington Ingalls Industries, Inc. | | | 11,800 | | | | 2,570,276 | | |

Air Freight & Logistics — 2.85% | |

FedEx Corp. | | | 50,900 | | | | 11,539,539 | | |

Industrial Conglomerates — 4.88% | |

General Electric Company | | | 310,387 | | | | 19,762,340 | | |

Machinery — 4.82% | |

| CNH Industrial NV | | | 486,700 | | | | 5,640,853 | | |

Cummins, Inc. | | | 33,800 | | | | 6,541,314 | | |

Iveco Group NV (a) (v) | | | 109,000 | | | | 577,104 | | |

PACCAR, Inc. | | | 56,300 | | | | 4,635,742 | | |

Stanley Black & Decker, Inc. | | | 20,200 | | | | 2,118,172 | | |

| | | | 19,513,185 | | |

TOTAL INDUSTRIALS | | | 53,385,340 | | |

INFORMATION TECHNOLOGY — 15.36%

Communications Equipment — 4.74% | |

F5, Inc. (a) | | | 82,900 | | | | 12,687,016 | | |

Telefonaktiebolaget LM Ericsson — ADR | | | 876,500 | | | | 6,486,100 | | |

| | | | 19,173,116 | | |

Electronic Equipment, Instruments & Components — 2.42% | |

Corning, Inc. | | | 160,800 | | | | 5,066,808 | | |

TE Connectivity Ltd. | | | 41,600 | | | | 4,707,040 | | |

| | | | 9,773,848 | | |

IT Services — 2.44% | |

Amdocs Ltd. | | | 25,600 | | | | 2,132,736 | | |

Euronet Worldwide, Inc. (a) | | | 54,100 | | | | 5,441,919 | | |

Fiserv, Inc. (a) | | | 25,900 | | | | 2,304,323 | | |

| | | | 9,878,978 | | |

Software — 5.76% | |

Microsoft Corp. | | | 41,600 | | | | 10,684,128 | | |

Oracle Corp. | | | 180,900 | | | | 12,639,483 | | |

| | | | 23,323,611 | | |

TOTAL INFORMATION TECHNOLOGY | | | 62,149,553 | | |

| | | Shares

Held | | Value | |

MATERIALS — 1.53%

Chemicals — 0.96% | |

Olin Corp. | | | 84,400 | | | $ | 3,906,032 | | |

Containers & Packaging — 0.57% | |

International Paper Company | | | 54,800 | | | | 2,292,284 | | |

TOTAL MATERIALS | | | 6,198,316 | | |

UTILITIES — 2.69%

Electric Utilities — 2.69% | |

PPL Corp. | | | 401,700 | | | | 10,898,121 | | |

TOTAL UTILITIES | | | 10,898,121 | | |

Total common stocks

(Cost $372,190,241) | | | | | 396,818,422 | | |

Total long-term investments

(Cost $372,190,241) | | | | | 396,818,422 | | |

COLLATERAL FOR SECURITIES ON LOAN — 0.16% | |

Money Market Funds — 0.16% | |

Invesco Short-Term Investments Trust

Government & Agency Portfolio —

Institutional Class, 1.38%^ | | | 638,435 | | | | 638,435 | | |

Total collateral for securities on loan

(Cost $638,435) | | | 638,435 | | |

SHORT-TERM

INVESTMENTS — 1.91% | | Principal

Amount | | | |

Time Deposits — 1.91% | |

Barclays PLC, 0.91%, 07/01/2022* | | $ | 7,730,917 | | | | 7,730,917 | | |

Citigroup, Inc., (0.78)%, 07/01/2022* | | EUR | 97 | | | | 102 | | |

Total short-term investments

(Cost $7,731,022) | | | 7,731,019 | | |

Total investments — 100.11%

(Cost $380,559,698) | | | | | 405,187,876 | | |

Liabilities in excess of other assets — (0.11)% | | | | | (464,055 | ) | |

Net assets — 100.00% | | $ | 404,723,821 | | |

(a) — Non-income producing security.

(l) — All or a portion of this security is on loan. The total market value of securities on loan was $621,267. The remaining contractual maturity of all of the securities lending transactions is overnight and continuous.

(v) — Security was fair valued as a result of market movements following the close of local trading using a third-party vendor's proprietary fair value pricing model. The total market value of these securities was $577,104, which represented 0.14% of net assets. See Security Valuation in Note 1 in Notes to the Financial Statements.

ADR — American Depositary Receipt

^ — Rate shown is the 7-day yield as of June 30, 2022.

* — Invested through a cash management account administered by Brown Brothers Harriman & Co.

The accompanying notes are an integral part of these financial statements.

19

Schedule of Investments — June 30, 2022

Hotchkis & Wiley Mid-Cap Value Fund

Largest Equity Holdings | | Percent of

net assets | |

Kosmos Energy Ltd. | | | 5.21 | % | |

Popular, Inc. | | | 4.82 | % | |

Fluor Corp. | | | 4.56 | % | |

First Citizens BancShares, Inc. | | | 4.28 | % | |

Citizens Financial Group, Inc. | | | 3.54 | % | |

APA Corp. | | | 3.29 | % | |

American International Group, Inc. | | | 3.18 | % | |

Adient PLC | | | 2.96 | % | |

Vistra Corp. | | | 2.57 | % | |

State Street Corp. | | | 2.44 | % | |

COMMON

STOCKS — 99.43% | | Shares

Held | | Value | |

COMMUNICATION SERVICES — 4.75%

Entertainment — 2.10% | |

Warner Bros. Discovery, Inc. (a) | | | 678,100 | | | $ | 9,100,102 | | |

Media — 2.65% | |

News Corp. | | | 225,500 | | | | 3,513,290 | | |

Omnicom Group, Inc. | | | 61,200 | | | | 3,892,932 | | |

Paramount Global | | | 166,800 | | | | 4,116,624 | | |

| | | | 11,522,846 | | |

TOTAL COMMUNICATION SERVICES | | | 20,622,948 | | |

CONSUMER DISCRETIONARY — 10.29%

Auto Components — 6.47% | |

Adient PLC (a) | | | 433,100 | | | | 12,832,753 | | |

The Goodyear Tire & Rubber Company (a) | | | 447,800 | | | | 4,795,938 | | |

Lear Corp. | | | 11,400 | | | | 1,435,146 | | |

Magna International, Inc. | | | 163,900 | | | | 8,998,110 | | |

| | | | 28,061,947 | | |

Automobiles — 0.32% | |

Harley-Davidson, Inc. | | | 43,900 | | | | 1,389,874 | | |

Household Durables — 1.72% | |

Tri Pointe Homes, Inc. (a) | | | 58,900 | | | | 993,643 | | |

Whirlpool Corp. | | | 41,800 | | | | 6,473,566 | | |

| | | | 7,467,209 | | |

Specialty Retail — 1.78% | |

The Gap, Inc. | | | 126,000 | | | | 1,038,240 | | |

The ODP Corp. (a) | | | 221,145 | | | | 6,687,425 | | |

| | | | 7,725,665 | | |

TOTAL CONSUMER DISCRETIONARY | | | 44,644,695 | | |

CONSUMER STAPLES — 1.10%

Personal Products — 1.10% | |

Herbalife Nutrition Ltd. (a) | | | 233,000 | | | | 4,764,850 | | |

TOTAL CONSUMER STAPLES | | | 4,764,850 | | |

| | | Shares

Held | | Value | |

ENERGY — 20.14%

Energy Equipment & Services — 2.38% | |

Expro Group Holdings NV (a) | | | 73,983 | | | $ | 852,284 | | |

Halliburton Company | | | 135,600 | | | | 4,252,416 | | |

NOV, Inc. | | | 310,000 | | | | 5,242,100 | | |

| | | | 10,346,800 | | |

Oil, Gas & Consumable Fuels — 17.76% | |

APA Corp. | | | 409,600 | | | | 14,295,040 | | |

Capricorn Energy PLC (a) (v) | | | 3,741,475 | | | | 9,946,269 | | |

Cenovus Energy, Inc. | | | 250,700 | | | | 4,765,807 | | |

Kosmos Energy Ltd. (a) | | | 3,655,220 | | | | 22,625,812 | | |

Murphy Oil Corp. | | | 220,900 | | | | 6,668,971 | | |

Oasis Petroleum, Inc. | | | 49,300 | | | | 5,997,345 | | |

PDC Energy, Inc. | | | 140,500 | | | | 8,656,205 | | |

Range Resources Corp. (a) | | | 165,800 | | | | 4,103,550 | | |

| | | | 77,058,999 | | |

TOTAL ENERGY | | | 87,405,799 | | |

FINANCIALS — 27.20%

Banks — 13.41% | |

Citizens Financial Group, Inc. | | | 430,900 | | | | 15,378,821 | | |

First Citizens BancShares, Inc. | | | 28,387 | | | | 18,558,853 | | |

First Horizon Corp. | | | 151,600 | | | | 3,313,976 | | |

Popular, Inc. | | | 272,200 | | | | 20,940,346 | | |

| | | | 58,191,996 | | |

Capital Markets — 4.88% | |

Credit Suisse Group AG — ADR (l) | | | 1,067,600 | | | | 6,053,292 | | |

Lazard Ltd. | | | 42,000 | | | | 1,361,220 | | |

Northern Trust Corp. | | | 33,000 | | | | 3,183,840 | | |

State Street Corp. | | | 172,100 | | | | 10,609,965 | | |

| | | | 21,208,317 | | |

Consumer Finance — 1.37% | |

SLM Corp. | | | 373,400 | | | | 5,951,996 | | |

The accompanying notes are an integral part of these financial statements.

20

Schedule of Investments — June 30, 2022

Hotchkis & Wiley Mid-Cap Value Fund

| | | Shares

Held | | Value | |

Insurance — 7.54% | |

American International Group, Inc. | | | 270,300 | | | $ | 13,820,439 | | |

CNO Financial Group, Inc. | | | 450,000 | | | | 8,140,500 | | |

Enstar Group Ltd. (a) | | | 23,300 | | | | 4,985,734 | | |

The Hartford Financial Services Group, Inc. | | | 88,100 | | | | 5,764,383 | | |

| | | | 32,711,056 | | |

TOTAL FINANCIALS | | | 118,063,365 | | |