Exhibit A

FORDING CANADIAN COAL TRUST

ANNUAL INFORMATION FORM

March 14, 2008

TABLE OF CONTENTS

| | | | | |

| FORWARD-LOOKING INFORMATION ADVISORY | | | 1 | |

| DEFINED TERMS | | | 2 | |

| NON-GAAP FINANCIAL MEASURES | | | 2 | |

| CONVERSION TABLE | | | 2 | |

| REFERENCES TO CURRENCY | | | 2 | |

| CORPORATE STRUCTURE | | | 2 | |

| GENERAL DEVELOPMENT OF THE BUSINESS | | | 3 | |

| DESCRIPTION OF THE BUSINESS | | | 6 | |

| RESERVES AND RESOURCES | | | 20 | |

| RISK FACTORS | | | 26 | |

| OTHER INFORMATION REGARDING THE TRUST | | | 35 | |

| CAPITAL STRUCTURE | | | 40 | |

| MARKETS FOR SECURITIES | | | 45 | |

| GOVERNANCE | | | 45 | |

| CONFLICTS OF INTEREST | | | 50 | |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | | | 50 | |

| LEGAL PROCEEDINGS | | | 51 | |

| TRANSFER AGENT AND REGISTRAR | | | 51 | |

| MATERIAL CONTRACTS | | | 51 | |

| INTERESTS OF EXPERTS | | | 53 | |

| ADDITIONAL INFORMATION | | | 53 | |

| APPENDIX “A”: GENERAL GLOSSARY | | | A-1 | |

| APPENDIX “B”: GLOSSARY OF TECHNICAL TERMS | | | B-1 | |

| APPENDIX “C”: DEFINITIONS OF MINERAL RESERVES AND MINERAL RESOURCES | | | C-1 | |

| APPENDIX “D”: FORDING CANADIAN COAL TRUST AUDIT COMMITTEE CHARTER | | | D-1 | |

FORWARD-LOOKING INFORMATION ADVISORY

This annual information form (“Annual Information Form”) contains forward-looking information within the meaning of theUnited States Private Securities Litigation Reform Act of 1995relating, but not limited to, the Trust’s expectations, intentions, plans and beliefs. Forward-looking information can often be identified by forward-looking words such as “anticipate”, “believe”, “expect”, “goal”, “plan”, “intend”, “estimate”, “optimize”, “may”, and “will” or similar words suggesting future outcomes, or other expectations, beliefs, plans, objectives, assumptions, intentions or statements about future events or performance. This Annual Information Form contains forward-looking information, including in, but not limited to, the sections titled“General Development of the Business”,"Description of the Business”, “Reserves and Resources”and“Other Information Regarding the Trust".

Unitholders and prospective investors are cautioned not to place undue reliance on forward-looking information. By its nature, forward-looking information involves numerous assumptions, known and unknown risks and uncertainties, of both a general and specific nature, that could cause actual results to differ materially from those suggested by the forward-looking information or contribute to the possibility that predictions, forecasts or projections will prove to be materially inaccurate. For a further discussion of the risks and uncertainties relating to the forward-looking statements contained in this Annual Information Form please refer to the section titledRisk Factorson page 26.

The forward-looking statements contained in this Annual Information Form are based, in part, upon certain assumptions made by the Trust, including, but not limited to, the following: no material disruption in production; no material variation in anticipated coal sales volumes, coal prices or cost of product sold; no material variation in the forecasted yields, strip ratios, haul distances and productivity for each mine in which the Trust has an interest; no material increases in the global supply of hard coking coal other than what is currently projected by management; significant quantities of weaker coking coals will not be substituted for hard coking coal; continued strength in global steel markets; no material disruption in construction or operations at mine sites; no variation in availability or allocation of haul truck tires to Elk Valley Coal during 2008; an absence of labour disputes in the forecast period; no material variation in the anticipated cost of labour; no material variations in markets and pricing of metallurgical coal other than anticipated variations; no material variation in anticipated mining, energy or transportation costs; contracted levels of rail and port availability with no material disruption in rail service and port facilities; no material delays in the current timing for completion of ongoing projects; financing will be available on terms favourable to the Trust and Elk Valley Coal; no material variation in the operations of Elk Valley Coal’s customers which could impact coal purchases; no material variation in historical coal purchasing practises of customers; existing customer inventories will not result in decreased sales volumes; parties execute and deliver contracts currently under negotiation; and no material variations in the current taxation environment other than those that have already been announced.

The Trust cautions that the list of risks and assumptions set forth or referred to above is not exhaustive. Some of the risks, uncertainties and other factors which negatively affect the reliability of forward-looking information are discussed in the Trust’s public filings with the Canadian and United States securities regulatory authorities, including its most recent management information circular, annual report, management’s discussion and analysis, quarterly reports, material change reports and news releases. The Trust’s public filings are available through the Trust’s website at www.fording.ca. Copies of the Trust’s Canadian public filings are available on SEDAR at www.sedar.com. The Trust’s public filings, in the United States, including the Trust’s most recent annual report on form 40-F, as supplemented by its filings on form 6-K, are available at www.sec.gov. The Trust further cautions that information contained on, or accessible through, these websites is current only as of the date of such information and may be superseded by subsequent events or filings. The Trust undertakes no obligation to update publicly or otherwise revise any information, including any forward-looking information, whether as a result of new information, future events or other such factors that affect this information except as required by law.

DEFINED TERMS

The meanings of certain capitalized terms used in this Annual Information Form can be found in the General Glossary and the Glossary of Technical Terms set forth respectively at Appendix “A” and Appendix “B”.

NON-GAAP FINANCIAL MEASURES

Financial measures such as “Distributable Cash”, “Available Cash”, “cash available for distribution”, “sustaining capital expenditures” and “net income before unusual items, future income taxes and unrealized gains or losses on foreign exchange forward contracts” are not measures recognized under generally accepted accounting principles in Canada or the United States and do not have standardized meanings prescribed by GAAP. These measures may differ from those made by other issuers and, accordingly, may not be comparable to such measures as reported by other trusts or corporations. These measures, which have been derived from the Trust’s financial statements and applied on a consistent basis, are presented in this Annual Information Form because management of the Trust believes these non-GAAP measures are of assistance in understanding the Trust’s results of operations and financial position and are relevant measures of the ability of the Trust to earn and distribute cash to Unitholders.

Distributable Cash and Cash Available for Distribution

For a detailed description of the Trust’s interpretation of these terms please see the section titledCash Available for Distributionin the Trust’s MD&A which is incorporated into this document by reference. The Trust’s MD&A is available atwww.sedar.com,www.sec.gov and through the Trust’s website atwww.fording.ca.

CONVERSION TABLE

| | | | | |

| To Convert To | | From | | Multiply By |

| Cubic Yards | | Cubic metres | | 1.308 |

| Feet | | Metres | | 3.281 |

| Miles | | Kilometres | | 0.621 |

| Acres | | Hectares | | 2.471 |

| Pounds | | Kilograms | | 2.205 |

| Short Tons | | Tonnes | | 1.102 |

| Long tons | | Tonnes | | 0.984 |

| BTU/lb | | kJ/kg | | 0.430 |

REFERENCES TO CURRENCY

All references in this Annual Information Form to monetary amounts are expressed in Canadian dollars and “$” means Canadian dollars unless otherwise noted.

CORPORATE STRUCTURE

Name and Formation

Fording Canadian Coal Trust is an open-ended mutual fund trust governed by the Declaration of Trust and the laws of Alberta. The Trust’s head office is located at Suite 1000, 205 — 9th Avenue SE, Calgary, Alberta T2G 0R3.

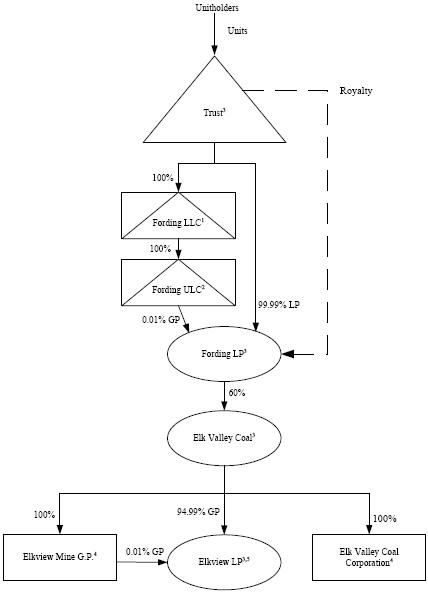

Intercorporate Relationships

The following chart sets forth all material subsidiaries of the Trust as at December 31, 2007, and indicates their respective jurisdictions of incorporation or organization and the ownership percentage of each such entity beneficially owned, or over which control or direction is exercised by the Trust.

2

Notes:

| | | |

| (1) | | Jurisdiction — Delaware |

| |

| (2) | | Jurisdiction — Nova Scotia |

| |

| (3) | | Jurisdiction — Alberta |

| |

| (4) | | Jurisdiction — Canada |

| |

| (5) | | Effective August 1, 2005, Elk Valley Coal contributed the Elkview mine to Elkview LP for a direct and indirect 95% partnership interest and subsidiaries of NSC and POSCO each acquired a 2.5% limited partnership interest by each contributing US$25 million. |

GENERAL DEVELOPMENT OF THE BUSINESS

Three-Year History

The Trust was established in connection with the 2003 Arrangement. The nature and development of the businesses in which the Trust has invested during the three most recently completed financial years is described in “Description of the Business”.

Achievement of Synergies

Elk Valley Coal was initially owned 65 percent by the Trust and 35 percent by Teck Cominco and certain affiliates of Teck Cominco. The EVC Partnership Agreement provided for an increase in Teck Cominco’s interest in Elk Valley Coal to a maximum of 40 percent in the event that Teck Cominco, as managing partner, was able to realize certain synergies as a result of the combination of the various mines and other properties comprising Elk Valley Coal. After discussions among the Partners and upon review of reports of various experts, the Partners determined that synergies had been achieved and that the Trust’s interest would be reduced to 62 percent effective April 1, 2004, to 61 percent on April 1, 2005, and to 60 percent on April 1, 2006. Teck Cominco’s entitlements increased correspondingly over the same period.

3

Please see the section titled“Introduction — The Trust”in the Trust’s MD&A for a further description of the achievement of synergies.

Elkview LP

Effective August 1, 2005, Elk Valley Coal contributed the Elkview operations to Elkview LP for a direct and indirect 95 percent partnership interest and subsidiaries of NSC and POSCO each acquired a 2.5 percent limited partnership interest by each contributing US$25 million. The proceeds of the NSC and POSCO contributions were used toward capital expenditures intended to increase the annual production capacity of the Elkview operations. In addition, NSC and POSCO each entered into ten-year sales agreements with Elk Valley Coal in connection with the transaction. Elkview Mine G.P. is the managing partner of Elkview LP and a wholly owned subsidiary of Elk Valley Coal. Pursuant to a management agreement, Elk Valley Coal provides management services to Elkview Mine G.P.

2005 Arrangement

At the 2005 Annual and Special Meeting, Unitholders approved a two-step reorganization of the Trust and its subsidiaries. The first step of the reorganization was completed on August 24, 2005 pursuant to the 2005 Arrangement. The 2005 Arrangement created a flow-through structure by transferring Fording Inc.’s partnership interest in Elk Valley Coal, to Fording LP, a new limited partnership, of which the Trust directly and indirectly owns all of the partnership interests. Fording ULC is the general partner of Fording LP and a wholly-owned subsidiary of the Trust. The 2005 Arrangement also resulted in the Trust directly and indirectly owning all of the securities of NYCO previously held by Fording Inc. The second step of the reorganization, whereby the Trust would further reorganize into a royalty trust at year end, was not completed because of delays resulting from the moratorium on advance tax rulings relating to income trusts by the Canada Revenue Agency in the fall of 2005. The purpose of reorganizing into a royalty trust was to allow the Trust to qualify for an exemption from a provision of the Tax Act that limits the level of Non-Resident ownership of units of income trusts.

Unitholders also approved a three-for-one split of the Units at the 2005 Annual and Special Meeting. The split became effective on September 6, 2005 with holders of record as at September 2, 2005 receiving two additional Units for each Unit held at that time.

A more detailed description of the 2005 Arrangement is contained in the Notice of Meeting and Management Information Circular dated April 2, 2005, that was mailed to Unitholders in advance of the 2005 Annual and Special Meeting and is available atwww.sedar.com,www.sec.gov and through the Trust’s website atwww.fording.ca.

Reorganization into a Royalty Trust

At the 2006 Annual and Special Meeting of the Trust, Unitholders approved a modified royalty reorganization structure. Subject to receiving a favourable advance tax ruling from the Canada Revenue Agency, the modified structure would have resulted in the creation of the Royalty and the reorganization of the assets and liabilities of the Trust under a new trust that, as a royalty trust, would have from the time of its creation qualified for an exemption from a provision of the Tax Act that limits the level of Non-Resident ownership of units of income trusts. Application for the advance tax ruling was made in February 2006 but the ruling had not been received by October 31, 2006 when the Federal Government announced proposed tax changes affecting income trusts, other than real estate investment trusts, including a tax on trust distributions effective January 1, 2007 for trusts whose units publicly trade for the first time after October 31, 2006. The Trustees decided not to proceed with the modified structure as it would have resulted in the new royalty trust being subject to the new tax on distributions beginning in 2007. Instead, the Trustees determined that it was in the best interests of Unitholders to reorganize the Trust into a royalty trust. The reorganization was completed effective January 1, 2007 following receipt of a favourable advance tax ruling from the Canada Revenue Agency. As a royalty trust, the Trust qualifies for an exemption from a provision of the Tax Act that limits the level of Non-Resident ownership of units of income trusts. The reorganization into a royalty trust did not change the distribution policy of the Trust or affect the amount of cash available for distribution to Unitholders.

4

Distribution Reinvestment Plan

The Trust has adopted a Distribution Reinvestment Plan (“DRIP”) that includes a Premium Distribution™ component. The DRIP allows eligible Unitholders of the Trust, generally residents of Canada or the United States, to direct that their cash distributions, net of any withholding taxes, be reinvested in additional Units issued from treasury at a five percent discount to the Average Market Price, as defined in the DRIP, on the applicable distribution payment date. The DRIP further allows eligible Unitholders, generally residents of Canada, to elect, under the Premium Distribution™ component of the DRIP, to have these additional Units delivered to the designated broker in exchange for a premium cash distribution equal to 102 percent of the cash distribution that such Unitholders would otherwise have received on the applicable distribution payment date. Canaccord Capital Corporation acts as the broker for the Premium Distribution™ component of the DRIP.

Unitholders who are residents of the United States or are otherwise considered “U.S. persons” under U.S. federal securities laws, or whose Units are held through the depository service operated by The Depository Trust Company, may not participate in the Premium Distribution™ component of the DRIP due to regulatory and operational restrictions.

The DRIP and a series of questions and answers related to the DRIP are available on the Trust’s website atwww.fording.ca in the section titled “Investor Relations” under the heading “DRIP”. Unitholders should carefully read the complete text of the DRIP before making any decisions regarding their participation in either of its components.

NYCO

The NYCO companies comprised the Trust’s industrial minerals operations, producing the industrial minerals wollastonite, a form of calcium oxide and silica, and tripoli, a form of crystalline silica. In 2007, the Trust decided to divest NYCO following an extensive review of strategic alternatives. The sale of NYCO was completed in June 2007.

Please see the section titled“Introduction — NYCO”in the Trust’s MD&A for a further description of the NYCO transaction.

Trust Announces Review of Strategic Alternatives

On December 5, 2007, the Trust announced that its Trustees had formed an independent committee to explore and make recommendations regarding strategic alternatives that may be available to the Trust to maximize value for its Unitholders. The Board of Directors of Fording ULC concurrently formed an independent committee with a similar mandate.

The independent committees have been given a broad mandate to consider a wide range of alternatives including an acquisition of all of the Trust’s outstanding Units by a third party, a sale of its assets, including its interest in the Elk Valley Coal Partnership, a combination, reorganization or similar form of transaction, or continuing with its current business plan. The independent committees have been given the authority to discuss possible transactions with interested parties and to make recommendations in that regard to the Trustees and Directors.

RBC Capital Markets has been engaged by the independent committees to assist them in their review.

The Trust anticipates it will make no further announcements regarding the strategic review unless and until the Trustees determine disclosure of a material change is required.

5

Changes to Applicable Tax Legislation

Withholding on Distributions to Non-Residents

The Tax Act was amended on May 13, 2005 to provide that, effective as of January 1, 2005, certain types of distributions made by an income trust to Non-Residents that were otherwise not subject to Canadian tax, including withholding tax, were subject to withholding under the Tax Act at a rate of 25 percent of the gross amount of the distribution subject to reduction under the provisions of any applicable tax treaty or conventions. Canadian withholding tax is generally 15 percent for U.S. holders.

Federal Government Announces Tax on Distributions from Income Trusts

On June 22, 2007, the Federal Government of Canada enacted new tax legislation that results in the taxation of income and royalty trusts that were publicly traded on October 31, 2006, other than certain real estate investment trusts, at effective rates similar to Canadian corporations commencing in 2011.

Please see the section titled“Other Information — Income Taxes”in the Trust’s MD&A for a further description of the changes to taxes on distributions.

DESCRIPTION OF THE BUSINESS

The Trust is an open-ended mutual fund trust existing under the laws of Alberta and governed by the Declaration of Trust. Its Units are publicly traded in Canada on the TSX (FDG.UN) and in the United States on the NYSE (FDG). The Trust is not a trust company and it is not registered under any trust and loan company legislation as it does not carry on or intend to carry on the business of a trust company.

The Trust was formed in connection with the 2003 Arrangement. Prior to August 24, 2005, the Trust held all of the shares and subordinated notes of its operating subsidiary company, Fording Inc. Effective August 24, 2005, the Trust reorganized its structure by way of the 2005 Arrangement under which substantially all of the assets of Fording Inc. were transferred to a new entity, Fording LP, and the Trust. The 2005 Arrangement created a flow-through structure whereby the Trust directly and indirectly owns all of the partnership interests of Fording LP, which holds the partnership interests in Elk Valley Coal previously held by the Fording Inc.

Effective January 1, 2007, the Trust reorganized into a royalty trust. As a royalty trust, current provisions of the Tax Act do not limit the level of foreign ownership of the Units of the Trust. The reorganization into a royalty trust did not change the distribution policy of the Trust or affect the amount of cash available for distribution to Unitholders.

The Trust is a flow-through structure and under currently applicable Canadian income tax regulations all taxable income of the Trust is distributed to the Unitholders without being taxed at the Trust level. The Trust does pay mineral taxes and Crown royalties to the provinces of British Columbia and Alberta. On June 22, 2007, the Federal Government of Canada enacted changes to Canadian income tax regulations that will result in the taxation of income and royalty trusts that were publicly traded as of October 31, 2006, other than certain real estate investment trusts, at effective rates similar to Canadian corporations commencing in 2011.

The Trust does not carry on any active business. The Trust directly and indirectly owns all of the interests of Fording LP, which holds a 60 percent interest in Elk Valley Coal. The Trust uses the cash it receives from its investments to make quarterly distributions to its Unitholders.

The principal asset of the Trust is its 60 percent interest in Elk Valley Coal, which was created in connection with the 2003 Arrangement. As part of the 2003 Arrangement the metallurgical coal mining operations and assets formerly owned by Old Fording (the public company that was the predecessor of the Trust prior to the 2003 Arrangement), Teck Cominco and/or its affiliates and the Luscar/CONSOL joint ventures were consolidated in Elk Valley Coal. Elk Valley Coal produces and distributes metallurgical coal from six mines located in British Columbia and Alberta, Canada.

6

Elk Valley Coal

Overview

Elk Valley Coal is a general partnership between Fording LP and Teck Cominco. Teck Cominco is the managing partner of Elk Valley Coal and is responsible for managing its business and affairs, subject to certain matters that require the agreement of all Partners.

Elk Valley Coal is the second-largest supplier of seaborne hard coking coal in the world. Hard coking coal is a type of metallurgical coal used primarily for making coke by integrated steel mills, which account for substantially all global production of primary (i.e. non-recycled) steel. The seaborne hard coking coal market is characterized by the global nature of international steel making, the relative concentration of quality metallurgical coal deposits in Australia, Canada and the United States and the comparatively low cost of seaborne transportation.

Summary of EVC Partnership Agreement

Elk Valley Coal is operated pursuant to the terms of the EVC Partnership Agreement, the material terms of which are summarized below.

Management of Elk Valley Coal

The managing partner supervises management of Elk Valley Coal and provides strategic direction. However, certain significant matters regarding Elk Valley Coal must be approved by a Special Resolution of the Partners.

The managing partner can resign as managing partner on 60 days advance notice to the other Partners. Further, the managing partner will be deemed to have resigned in certain circumstances (insolvency, reduction in its interest below 20 percent or wilful default of the EVC Partnership Agreement). In such circumstances, Partners holding a Distribution Entitlement of more than five percent (other than the resigning managing partner if the managing partner was deemed to have resigned due to insolvency or wilful default of the EVC Partnership Agreement) must unanimously select a new managing partner. Pending the selection of a new managing partner, the Partner then holding the largest Distribution Entitlement can designate a temporary managing partner.

The day-to-day operations of Elk Valley Coal are undertaken by officers of Elk Valley Coal and other management personnel designated by the managing partner.

Annual Budget Approval Process

The annual operation of Elk Valley Coal, including budgeting and capital spending, must be set out in the Capital and Operating Plan and Budget. The Capital and Operating Plan and Budget must be presented to the Partners by no later than November 15 of each year for the following calendar year and must be approved by a Special Resolution of the Partners.

The managing partner must use its best efforts to ensure that the business of Elk Valley Coal is conducted substantially in accordance with Capital and Operating Plan and Budget, except in certain extraordinary circumstances. Any material amendment or variation to such plans must also be approved by a Special Resolution of the Partners.

Special Resolution of the Partners Matters

In addition to the approval of the Capital and Operating Plan and Budget or any material amendment thereto, a Special Resolution of the Partners is required in a variety of other circumstances such as any change in the distribution policy of Elk Valley Coal, any proposed merger, arrangement or reorganization of Elk Valley Coal, the admission of new Partners (other than wholly-owned subsidiaries or affiliates of existing Partners) or the decision to institute bankruptcy or insolvency proceedings.

7

Distribution Entitlements

Each Partner is entitled to share in the profits and losses of Elk Valley Coal and to participate in the distribution of assets on liquidation or dissolution of Elk Valley Coal in proportion to its Distribution Entitlement. As at December 31, 2007, the Distribution Entitlements of the Partners were as follows:

| | | | | |

| | | Distribution | |

| Partner | | Entitlement | |

| Fording LP | | | 60.000 | % |

| Teck GP | | | 39.836 | % |

| QCP | | | 0.164 | % |

| | | | |

| | | | | |

| Total | | | 100.000 | % |

Reporting

Elk Valley Coal reports monthly to the Partners with respect to the operational results and financial performance of Elk Valley Coal. In addition, on a quarterly basis, the managing partner reports to the Board of Directors with respect to the operational results and financial performance of Elk Valley Coal and such other matters as the Board of Directors may reasonably request.

Elk Valley Coal is also required to provide to each Partner, within 55 days of the end of each calendar year, audited financial statements of Elk Valley Coal for the previous calendar year and such other financial information relating to such calendar year as the Partners may request.

Further, Elk Valley Coal is required to provide to each of the Partners such information as those Partners may require in order to satisfy their public company reporting obligations. In this regard, Elk Valley Coal is required to provide to the Partners a report of any material change in the affairs of Elk Valley Coal, quarterly and annual financial statements prepared in accordance with GAAP, management’s discussion and analysis for the relevant period covered by the aforementioned financial statements and such other documents as are customarily required in connection with the preparation and release of quarterly and annual financial information by public issuers in Canada and the United States.

Permitted Cash Calls

The managing partner will call for an additional cash contribution from the Partners in the event that the Partners agree the Partnership will experience a CCA shortfall as that term is defined in the EVC Partnership Agreement or the managing partner reasonably determines that an additional cash contribution of the Partners is the best way to fund capital expansion projects or rectify a capital cost allowance shortfall. All contributions made by the Partners in response to such a cash call shall be treated as additional contributions to the capital of Elk Valley Coal and the capital accounts of the Partners shall be adjusted accordingly.

Sale/Assignment of Partnership Interest

A Partner may sell, assign, transfer or dispose of its Elk Valley Coal interest to a subsidiary or affiliate. Pursuant to this provision, Teck Cominco and TBCI transferred their respective Elk Valley Coal interests to Teck GP as such a permitted transferee. Any intended sale, assignment, transfer or disposition to other than to such a permitted transferee is subject to a right of first offer to the other Partners. In addition, the sale by Teck Cominco and certain affiliates of Teck Cominco of their Elk Valley Coal interest, other than to such a permitted transferee, will be subject to the consent of the Independent Directors, such consent not to be unreasonably withheld.

8

Credit Agreement

The Trust and Elk Valley Coal entered into a joint credit agreement, as amended, which provides the Trust and Elk Valley Coal with revolving credit facilities. In connection with this agreement, Elk Valley Coal provided a guarantee of the obligations of the Trust.

Assets of Elk Valley Coal

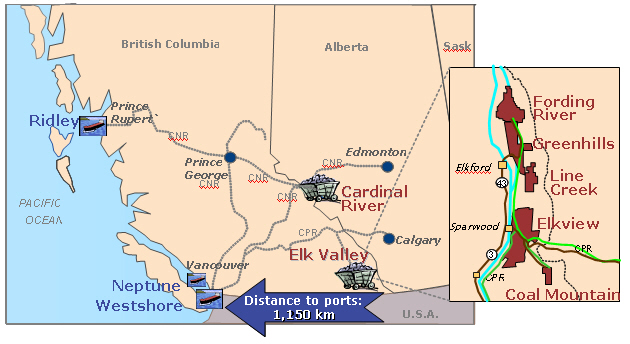

Elk Valley Coal has an interest in six active mining operations. The Fording River, Coal Mountain, Line Creek, Elkview and Greenhills operations are located in the Elk Valley region of southeast British Columbia. The Cardinal River operation is located in west-central Alberta.

The Fording River, Coal Mountain, Line Creek and Cardinal River operations are wholly owned. The Greenhills operation is a joint venture in which Elk Valley Coal has an 80 percent interest. Effective August 1, 2005, the Elkview operation was contributed to the Elkview Mine Limited Partnership in which Elk Valley Coal holds, directly and indirectly, a 95 percent general partnership interest.

All of Elk Valley Coal’s mines are open-pit, truck and shovel mining operations and are designed to operate year-round, 24 hours per day, seven days per week. However, the operating schedules can be varied depending on coal market conditions and shutdowns for maintenance activities. All of the mines are serviced by two-lane all weather roads. Elk Valley Coal’s reserves, facilities and overburden dumps are all proximate to its mine locations.

Elk Valley Coal also owns numerous coal resources in British Columbia as well as a 46 percent interest in Neptune Bulk Terminals (Canada) Ltd., a bulk facility located in North Vancouver, British Columbia.

The following map shows the location of Elk Valley Coal’s six operating mines:

9

Principal Products and Markets

Elk Valley Coal’s principal product is hard coking coal. Hard coking coal is a type of metallurgical coal, which is the term used to describe coal products suitable for making steel in the integrated steel mill process. Integrated steel mills account for substantially all global production of primary (i.e. non-recycled) steel. Integrated steel mills depend on metallurgical coal and iron ore as the two primary inputs for making steel. When making steel, two of the key raw ingredients are iron ore and coke. Coke is used to convert the iron ore into molten iron, which is further processed into steel. Coke is made by heating metallurgical coal to about 2,000°F (1,100°C) in the absence of oxygen in a coke oven. The lack of oxygen prevents the coal from burning. The coking process drives off various liquids, gases and volatile matter. The remaining solid matter forms coke, a solid mass of nearly pure carbon. Approximately 1.5 tonnes of metallurgical coal are needed to produce one tonne of coke, and for every one tonne of coke, the blast furnace produces about two to three tonnes of molten iron. Only certain types of metallurgical coal have the necessary characteristics required to make coke. These characteristics include caking properties (the ability to melt, swell and re-solidify when heated) and low impurity levels (e.g. moisture, ash, sulphur, etc.).

There are three main categories of metallurgical coal: (i) hard coking coal that forms high-strength coke; (ii) semi-soft coking coal that produces coke of lesser quality; and (iii) PCI coal. The categories are separated by reference to their chemical and physical properties. These differences, in turn, result in differentiation in pricing, which has become quite significant in recent years. Hard coking coals form high-strength coke, semi-soft coking coals produce coke of lesser quality and PCI is used for its heat value and is not typically a coking coal. Semi-soft and pulverized coals normally have lower sales values compared with hard coking coal due to marked differences in quality and broader availability. Recent trends in coal marketing and purchasing have led to the stratification of hard coking coals into quality groupings based on their chemical and physical properties, with prices varying significantly between these groups. The highest-quality hard coking coals are relatively scarce and, accordingly, command the highest prices. A key strategic priority for Elk Valley Coal is to maximize the quality and consistency of its products so that it continues to produce hard coking coals that are classified within the highest-quality groupings.

The following schematic outlines how steel is produced in an integrated steel mill.

The demand for hard coking coals is closely correlated with the steel production of integrated steel mills. However, other factors can influence demand. The substantially lower pricing for semi-soft and PCI encourages integrated steel mills to substitute these coals, to the extent their processes allow, in an attempt to reduce the total cost of steel production. This substitution tends to have technical limits. Use of semi-soft coals reduces the productivity of coke ovens and blast furnaces. Increased use of PCI reduces overall coking coal requirements but, in turn, necessitates the use of higher-quality hard coking coals. Therefore, substitution can increase when the steel mills operate at lower rates of productivity and when the price differential between hard coking and other coals widens. There is also an impact on hard coking coal demand when steel mills purchase supplies of finished coke. Approximately two-thirds of the hard coking coal needs of integrated steel mills and other producers of coke are met by domestic production or by production delivered overland. The remaining needs are satisfied by importing hard coking coal through seaborne trade.

There are currently no technologically feasible and cost-effective alternatives to using coking coal in the steel-making process. Changes to the steel-making process tend to occur gradually. Research into alternative technologies has been ongoing for many years, but to date the alternatives to using coking coal, such as direct smelting or hydrogen-reduction technologies, have generally not been feasible or cost-justified on a large commercial scale. However, the high prices and limited supplies of hard coking coals that have been experienced in recent years, combined with public pressure and government action to reduce carbon dioxide emissions, are expected to place increased focus on alternative technologies in the future. Alternative technologies may eventually displace some of the demand for hard coking coal, although the time frame for this change is expected to be relatively extended.

10

The demand side of the seaborne hard coking coal market is more fragmented than the supply side. However, the major steel producers have historically formed both formal and informal alliances to improve their bargaining leverage. In addition, there has been a trend toward consolidation among steel producers in recent years. In particular, the Mittal Group has acquired a number of other steel producers and has created the world’s largest steel company. Industry consolidation generally increases the purchasing power and bargaining strength of these customers although, recently, other factors including strong demand and perceived shortages of supply have sustained hard coking coal prices at historically high levels.

Since 2003, global steel production, and hence the demand for hard coking coal, has grown dramatically, driven primarily by rapid industrialization and economic development in the emerging economies of China, India, Russia and Brazil, commonly referred to as the “BRIC” countries. This is in contrast to the many years of relatively stable demand and stagnant prices for steel and hard coking coal that preceded 2003. The rapid development of the BRIC countries is expected to further increase the volatility of the global steel and hard coking coal markets in the future because these countries will likely experience sudden and irregular swings in their economic development. Accordingly, the Trust expects to experience increased volatility in its financial results in future years. A strategic priority for Elk Valley Coal is to position itself so that it can react appropriately and efficiently to sudden fluctuations in demand and prices. This will generally require increased flexibility across all of Elk Valley Coal’s business operations. For example, increased flexibility in its mine plans is required so that production levels and product mix can be adjusted more quickly in response to changing market conditions. It is anticipated that going forward Elk Valley Coal’s marketing strategies will be developed based on a presumption of increased volatility in sales prices and volumes. Also, flexibility in financing structures will be needed to accommodate the fluctuations and volatility in cash flows that may occur during these cycles.

China, in particular, is a key influence on the global steel and hard coking coal markets. The significant construction boom in China has required it to dramatically increase its domestic steel production capacity. China does not currently import a significant amount of seaborne hard coking coal because the requirements of its domestic steel mills can generally be met by Chinese coal producers and imports from Mongolia. In fact, China is the world’s largest producer of metallurgical coal, but it does not currently export significant quantities because domestic demand is so strong. However, an economic downturn in China could potentially cause its exports of hard coking coal to increase in the future. Elk Valley Coal does not currently sell significant quantities of coal to China, but it has benefitted indirectly from the growth in China because it sells coal to the large integrated steel mills elsewhere in Asia that help supply the Chinese market.

Principal Competition

Elk Valley Coal competes primarily with coal producers from Australia and the United States in the seaborne hard coking coal market. The supply of coal in the global markets and the demand for coal among the world’s steel producers has historically provided for a competitive seaborne market. Coal pricing is generally established in U.S. dollars and the competitive positioning among producers can be significantly affected by exchange rates. In addition, a number of steel producers deal with multiple coal suppliers in order to promote security of supply and further competitiveness in this market. Principal competitors to Elk Valley Coal are centered in Australia and include the BHP Billiton/Mitsubishi Alliance, Anglo American Plc./Mitsui & Co. Ltd., Xstrata Plc. and the Rio Tinto Group.

Competitive Position

Elk Valley Coal is the second-largest supplier of seaborne hard coking coal in the world, with approximately 15 percent of the global seaborne market in 2007. The other main producing regions of seaborne hard coking coal are Australia and the United States. New sources of supply of hard coking coal from Australia are expected to come into the market over the next few years. While not all of these new sources are expected to produce the highest quality hard coking coal, the supply will compete directly with some of Elk Valley Coal’s products.

Undeveloped reserves of high-quality metallurgical coal have been identified in Mongolia, Russia, Mozambique and other locations. These reserves have the potential to add a significant amount of supply in the longer term. There are significant economic, logistical and political challenges involved in developing these new reserves. However, the historically high prices and relative scarcity of high-quality hard coking coal experienced in recent years increases the likelihood that some of these high-quality deposits will be developed.

11

Nearly all of Elk Valley Coal’s production is hard coking coal, including a high proportion of high-quality hard coking coal products and a range of other products. Generally, these coal products are comparable in quality with those of Elk Valley Coal’s competitors and perform well when blended by customers with other coals. The varying chemical and physical properties of its coal products, their relative supply and demand in the marketplace and any differences in ocean freight costs into various markets result in differentiation in pricing between Elk Valley Coal’s various hard coking coal products. In response to trends toward increased stratification of hard coking coal qualities and, therefore prices, Elk Valley Coal is producing products and structuring its operations to preserve the value of its highest-quality coals. Approximately ten percent of Elk Valley Coal’s production is sold as thermal coal or as PCI to steel mills.

On the whole, the cost of production for Elk Valley Coal is competitive with that of the average Australian producer. However, that competitive position can depend on a number of factors, including the type of operations of a particular competitor and foreign currency exchange rates. Elk Valley Coal operates in mountainous regions whereas Australian metallurgical coal production is generally from open-pit mines in non-mountainous terrain using dragline and truck and shovel methods or from underground operations. Metallurgical coal production in the United States is generally from underground operations in the eastern states.

Transportation costs, including rail and port services, are significant to Elk Valley Coal and generally determine its competitiveness. Rail costs are high in comparison to Elk Valley Coal’s primary competitors in Australia because most of its coal is shipped through difficult terrain to west-coast ports that are over 1,100 kilometres from its mines. However, rail costs are also high because there are no cost-effective alternatives to Elk Valley Coal’s rail service providers, which impact its ability to negotiate competitive rates and service levels. These factors, combined with its high port costs, place Elk Valley Coal at a competitive disadvantage and result in it being a relatively high-cost producer compared with its peers in the global metallurgical coal industry. As a high-cost producer, Elk Valley Coal is subject to greater risks in a highly competitive market. Australian producers generally have a marked cost advantage over Elk Valley Coal because their mining operations are located much closer to tidewater, the rail lines run through more even terrain and because there are mechanisms that create a near competitive market for rail service.

Cyclical Nature of Seaborne Hard Coking Coal and Coal Markets

The market for hard coking coal was characterized by a large number of producers, excess capacity and low prices for almost two decades prior to 2003. Over time, slow but steady growth in the demand for seaborne hard coking coal absorbed much of the production capacity and with few new mines coming into production and some closing, supply and demand began to tighten in 2003.

Elk Valley Coal believes that the global metallurgical coal markets have entered a period of unprecedented volatility. Elk Valley Coal’s prices for the 2005 coal year (i.e. April 1, 2005 to March 31, 2006) reached historically high levels of approximately US$122 per tonne, which were more than double the prices for the 2004 coal year. The 2005 coal year prices reflected the confluence of strong growth in demand for steel, driven largely by the rapid industrialization and economic development of China and the other BRIC countries and coal production and delivery problems that constrained global supplies of hard coking coal at that time. Negotiations for the 2006 coal year were conducted under different circumstances. In late 2005, some integrated steel mills slowed deliveries of hard coking coal and substituted coals of lesser quality in response to the widening price gap between hard coking coal and semi soft coking coals. At the same time, the global supply of hard coking coal increased. As a result, prices came off historically high levels and Elk Valley Coal’s average prices for the 2006 coal year declined by 12 percent to approximately US$107 per tonne.

Leading into the 2007 coal year negotiations, continuing substitution of lesser quality coals and increasing global supply of hard coking coal caused further downward pressure on prices and Elk Valley Coal’s average prices fell by a further 13 percent to approximately US$93 per tonne for the 2007 coal year. The 2007 coal year prices represented a significant decline relative to the 2005 coal year, but in comparison to the many preceding years of low prices and slow growth in demand, the 2007 coal year prices remained relatively high. During 2007, the global metallurgical coal markets shifted dramatically and by the end of 2007 the market was in tight supply because of growing demand and lower than expected growth in exports from Australian suppliers. In late 2007, spot sales of hard coking coal by other coal producers were occurring at very high prices as many integrated steel mills faced critically low inventories.

12

Cyclical market conditions, along with normal variations in sales and operations, lead to a great deal of variability in Elk Valley Coal’s sales volume estimates for the calendar year. Rising steel prices and demand, or coal production or shipment interruptions in the global supply chain, could result in increased sales. However, a global oversupply of steel could result in lower sales.

Demand for hard coking coal is correlated to demand for steel. While demand is currently strong, it is expected that the BRIC countries will experience sudden and irregular swings in their economic development in the future, which will cause significant volatility in the global steel and hard coking coal markets. Dramatic swings in demand and prices for hard coking coal may be experienced from year to year. There is currently no commodity derivative market for metallurgical coal.

In the near term, a deep recession in the United States could impact the global economy and the demand for steel and metallurgical coal, especially if the economic problems in the United States impact the Chinese economy or other major growth areas.

For a further discussion of Elk Valley Coal’s markets please see the Trust’s MD&A.

Mining and Processing

Elk Valley Coal employs conventional open-pit mining techniques using large haul trucks and electric or hydraulic shovels. Overburden rock is drilled and blasted with explosives and is then loaded onto trucks by shovels and hauled outside of the mining area. Once the overburden is removed, the raw coal is typically recovered from the seam by bulldozers and is loaded onto haul trucks by front-end loaders and shovels for transport to the coal preparation plants. These plants employ breakers, which size the raw coal and remove large rocks, wash the raw coal of ash and impurities using conventional techniques and then dry the clean coal using dryers that utilize coal or natural gas for fuel.

Movement of rock overburden constitutes a significant portion of the unit cost of product sold because considerably more rock overburden must be blasted and moved outside of the active mining area compared with the volume of coal recovered from the underlying seams. Typically, more than 20 tonnes of rock must be moved for every tonne of coal produced, which equates to a strip ratio of approximately eight to nine bank cubic metres of rock overburden moved for each tonne of clean coal produced. Certain key variables are carefully managed with a view to the long-term economic viability of the coal reserve.

| | • | | Thestrip ratiois the average volume (bank cubic metres) of rock that must be moved for each tonne of clean coal produced and can vary from period to period around a long-term trend. The strip ratio impacts the size of the mining fleet, plant productivity and the cost of mining inputs such as labour, tires and fuel. A lower strip ratio normally reduces the unit cost of product sold. |

| |

| | • | | Thehaul distanceis the one-way distance the trucks, on average, have to travel to move the overburden. The haul distance impacts the size of the mining fleet, productivity in the mine and the cost of mining inputs such as labour, tires and fuel. Shorter haul distances normally result in lower cost of product sold. |

| |

| | • | | Totalmaterial productivityis a measure of operational efficiency, stated in the volume of rock and coal moved per eight-hour work shift. Higher productivity, which depends on such things as mine design, employee levels, size of the mining fleet, haul distance and equipment availability and capacity, normally reduces the unit cost of product sold. |

13

Changing technology and the use of larger equipment can reduce mining costs and increase productivity, which could make mining areas with higher strip ratios or longer haul distances economic and increase recoverable coal. The outlook for hard coking coal prices also helps to determine which strip ratios and haul distances can be economic. Mining costs are also impacted by the cost of various inputs such as labour, maintenance, fuel and other consumables. There has been significant inflation in mining input costs in recent years. Western Canada has been experiencing an economic boom and Elk Valley Coal operates in a very tight labour market. The availability of employees and contractors has been constrained, which has placed upward pressure on costs. The prices of diesel fuel and haul truck tires, which are also major cost drivers for Elk Valley Coal, have risen significantly.

Coal preparation plant processing includes the washing and drying of coal for sale. Washing coal removes impurities such as rock and ash. Drying the coal after washing reduces the moisture level of the coal in order to meet customers’ specifications. Certain key variables related to processing coal are also carefully managed with a long-term view to optimal mine operations.

| | • | | The percentage of clean product recovered compared with the amount of raw coal processed is referred to asplant yield. The yield achieved is a function of the physical characteristics of raw coal being processed and the amount of ash and impurities in the raw coal. In the cleaning process, ash in the raw coal is removed to acceptable levels for the production of coke for the steel-making process. Generally, a higher yield lowers the unit cost of product sold. |

| |

| | • | | Clean coal productivityis a measure of the overall operational efficiency of the coal preparation plant and minesite operations. It is stated as the amount of clean coal produced per eight-hour work shift. In addition to factors that affect productivity in the mining operations, productivity for coal preparation plants is dependent upon plant design and site employee levels. |

Mining and plant equipment and other infrastructure must be maintained. Scheduled shutdowns of operations, which are typically built into Elk Valley Coal’s production plans, may be taken at various times throughout the year to provide for employee vacations and allow for maintenance activities. Generally, scheduled shutdowns occur in July and August, which adversely impacts production volumes and unit costs in the third quarter.

Please see the section titled “2007compared with 2006 — Results of Operations”in the Trust’s MD&A for a detailed discussion of Elk Valley Coal’s mining costs.

Production and Quality Control

Coal seams are sampled and analyzed under the supervision of professional geologists and categorized by quality and coking potential. This data is then used to determine stockpiling and blending strategies. As a result, Elk Valley Coal has an available inventory of coal sources of varying qualities which can be combined, as required, to form blended products. In addition to sampling at source, coal is sampled at all stages of coal preparation, at the rail loadout and at the port to maintain quality standards.

Coal Transportation

Processed coal is conveyed to clean coal silos or other storage facilities for storage and loadout to rail cars. The loadout facilities are set up to load and weigh unit trains (each train carrying up to 13,000 tonnes). A spray system coats the coal in each rail car with a dust inhibitor to limit the escape of coal dust during transportation.

Elk Valley Coal transports approximately 90 percent of its coal to ports in Vancouver, British Columbia utilizing two rail service providers. CPR provides services to the five operations in the Elk Valley region in southeast British Columbia and CNR provides services to the Cardinal River operation in west-central Alberta. There are currently no cost-effective alternatives to these providers for the volume of coal produced by these mines, which affects Elk Valley Coal’s ability to negotiate competitive service rates. Elk Valley Coal has a five-year agreement with CPR for the westbound movement of its coal, which expires in March 2009. The rates under the agreement consist of a base rate and premiums if U.S. dollar coal prices and West Texas Intermediate crude oil prices are within certain parameters. The agreement with CNR expires in January 2009 and consists of a base rate plus a fuel surcharge.

14

Westshore Terminals in Vancouver handles most of the shipments loaded onto vessels. Neptune Terminals in North Vancouver, which is 46 percent owned by Elk Valley Coal, loads the balance of west-coast shipments. There are generally no cost-effective alternatives to these port facilities. Loading agreements with Westshore Terminals expire in March 2010 for the Elkview operation and in March 2012 for the Fording River, Greenhills and Coal Mountain operations. The agreement with Westshore Terminals for the Line Creek operation expired on March 31, 2007 and Elk Valley Coal is currently shipping under interim arrangements. The loading costs under the Westshore Terminals contracts are partially linked to the average Canadian dollar price that Elk Valley Coal receives for coal. Loading rates for Neptune Terminals are based on the actual costs allocated to the handling of coal at that facility.

Charges for demurrage by vessel owners for waiting times are incurred if there are loading problems or scheduling issues at the port or if there is a shortage of the specified coal at the port because of, for example, problems with the transportation of coal. Recently, vessel demurrage costs have increased significantly due to higher demurrage rates being charged by vessel owners as well as longer vessel wait times due to low inventories at the ports resulting from shortfalls in rail shipments. Ocean freight rates, including vessel demurrage rates, have increased significantly due to strong global demand for shipping services and rising fuel costs. Rising ocean freight rates, other than vessel demurrage rates, have little direct impact on Elk Valley Coal because the customer generally pays the ocean freight (either directly or through higher negotiated coal prices). Rising ocean freight costs can have an adverse indirect effect on Elk Valley Coal’s competitiveness because it increases the overall cost of its products, which could make other suppliers that are geographically closer to the customer more attractive.

Approximately ten percent of coal shipments are eastbound and delivered to North American customers by rail or by rail and ship via Thunder Bay Terminals in Thunder Bay, Ontario. CPR handles Elk Valley Coal’s eastbound rail transportation under a contract that expires in December 2009.

Coal Sales Contracts

Elk Valley Coal sells substantially all of its coal pursuant to evergreen contracts or long-term supply agreements. Evergreen contracts allow for pricing of specified volumes of coal to be set annually and require one or two year’s notice of termination by either party. Long-term supply agreements provide for the purchase of specified volumes of coal each year for a specified number of years, but allow prices to be set annually. Historically, less than ten percent of Elk Valley Coal’s sales have been based on spot market prices, which is typical for the seaborne hard coking coal market. Coal is generally priced on an annual basis for the 12 month period that starts April 1, referred to as the coal year. In other cases, coal is priced on a calendar year basis or another 12 month period that differs from the typical coal year.

Evergreen contracts and long-term supply agreements have traditionally been used to reduce some of the risk associated with sales and production volumes by providing more certainty and stability of sales volumes from year to year. However, within the calendar year the timing of coal sales is largely dependent on customers as they determine when vessels are nominated to receive shipments and it is not unusual for some sales volume to be carried over from one coal year into the next. In recent years, the amount of this carryover has increased. A strategic priority for Elk Valley Coal is to negotiate contract volumes that are more consistent with each customer’s underlying buying patterns in order to improve predictability.

The usual terms of sale for seaborne coking coal result in customers taking title to coal once it is loaded onto vessels at the shipping port. Elk Valley Coal’s customers typically arrange and pay for ocean freight and off-loading from vessels at the destination port. In some cases, Elk Valley Coal pays these costs, selling the coal on terms such that title to the coal transfers at the shipping destination. Higher prices are negotiated for these sales to cover the ocean freight rates and the costs of ocean freight are reflected in transportation costs.

Elk Valley Coal — The Last Three Years

For a description of the price volatility and revenue impacts of the hard coking coal market in the previous three years please see the section titled “Description of the Business — Elk Valley Coal — Cyclical Nature of Seaborne Hard Coking Coal and Coal Markets” in this Annual Information Form and the section titled“2007 Compared with 2006 — Results of Operations — Revenues”in the Trust’s MD&A.

15

Capital Expenditures

The Trust’s investing activities included capital expenditures of $49 million in 2007. Capital expenditures were $29 million and $119 million in 2006 and 2005, respectively. Capital spending in 2007 and 2006 was for sustaining capital requirements and included a small amount of expansion capital expenditures carried over from projects largely completed in 2005. Expansion capital expenditures in 2005 of $80 million were related to the development of the Cheviot pit at the Cardinal River operations and additions to production capacity at the Fording River and Elkview operations. The remaining $39 million of total capital expenditures related to sustaining capital.

Sustaining capital expenditures refers to expenditures in respect of capital asset additions, replacements or improvements required to maintain business operations at current production levels, the determination of which requires the judgment of management. Investments in sustaining capital are required on an ongoing basis and the Trust expects them to be funded primarily by cash flows from operating activities. Sustaining capital expenditures may vary by a considerable amount in any given year depending on the requirements to replace truck and shovel fleets and other support equipment.

Capital expenditures not identified by management to be sustaining in nature are classified as expansion capital. These expenditures are generally made in order to increase the production capacity of existing operations and to develop or acquire new mineral bodies or new mines.

Please see the section titled “Liquidity and Capital Resources”in the Trust’s MD&A.

Coal Sales by Geographical Area

Elk Valley Coal currently has approximately 45 customers around the world. Most of its customers are integrated steel mills, the largest of which are located in Korea and Japan. A breakdown of sales revenue by geographic region is as follows:

| | | | | | | | | | | | | |

| Elk Valley Coal sales by region (%) | | 2007 | | | 2006 | | | 2005 | |

| Asia | | | 45 | | | | 45 | | | | 45 | |

| Europe | | | 33 | | | | 35 | | | | 34 | |

| North America | | | 14 | | | | 11 | | | | 13 | |

| South America | | | 8 | | | | 9 | | | | 8 | |

16

Elk Valley Coal — Mines and Neptune Terminals

The following table sets forth the area, current production capacity, actual production and known reserve life of Elk Valley Coal’s mines:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | Known | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | Reserve | | | Date of | |

| | | | | | | Nominal Production | | | | | | | | | | | | | | | | | | | Life(3) | | | Initial | |

| | | | | | | Capacity(2,5) | | | Production(2) | | | (years) | | | Operation | |

| | | Mined or | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | to be | | | | | | | | | | | | �� | | | | | | Percent | | | | | | | |

| | | Mined(1) | | | Mine | | | Plant | | | 2007 | | | 2006 | | | 2005 | | | Change(4) | | | | | | | |

| Fording River | | | 4,220 | | | | 8.5 | | | | 10.0 | | | | 7.9 | | | | 7.7 | | | | 9.2 | | | | 3 | % | | | 27 | | | | 1969 | |

Elkview(6) | | | 4,100 | | | | 5.6 | | | | 7.0 | | | | 5.0 | | | | 4.7 | | | | 6.0 | | | | 6 | % | | | 47 | | | | 1969 | |

Greenhills(6) | | | 2,200 | | | | 5.0 | | | | 5.0 | | | | 4.1 | | | | 4.2 | | | | 5.0 | | | | (2 | %) | | | 22 | | | | 1981 | |

| Coal Mountain | | | 950 | | | | 2.7 | | | | 3.5 | | | | 2.1 | | | | 2.0 | | | | 2.3 | | | | 5 | % | | | 13 | | | | 1975 | |

| Line Creek | | | 1,150 | | | | 2.2 | | | | 3.5 | | | | 2.4 | | | | 2.3 | | | | 2.6 | | | | 4 | % | | | 7 | | | | 1981 | |

| Cardinal River | | | 2,350 | | | | 2.2 | | | | 2.8 | | | | 1.8 | | | | 1.7 | | | | 1.5 | | | | 6 | % | | | 23 | | | | 1969 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total | | | 14,970 | | | | 26.2 | (6) | | | 31.8 | (6) | | | 23.3 | | | | 22.6 | | | | 26.7 | | | | 3 | % | | | — | | | | — | |

Notes:

| | | |

| (1) | | Represents total hectares of coal lands where mining has occurred or is scheduled to occur. Numbers are rounded. |

| |

| (2) | | Million tonnes of saleable coal. |

| |

| (3) | | Years that reserves are projected to support mining are at 2007 production rates. |

| |

| (4) | | Percent change is for the production change from 2006 to 2007. |

| |

| (5) | | Production capacity is limited to approximately 25 million tonnes due to tire availability. |

| |

| (6) | | Values are 100% of capacity and include the NSC and POSCO combined five percent interest in Elkview LP and the 20% of Greenhills production which POSCO takes pursuant to POSCAN’s joint venture interest. |

Please see the section titled “Nature of Operations — The Steel and Metallurgical Coal Industries — Operating the Business — Mining Coal”in the Trust’s MD&A

All of Elk Valley Coal’s operations are accountable for long-term, socially responsible environmental stewardship. This means avoiding or mitigating potential negative impacts during operations as well as ensuring reclamation occurs to return the land to a pre-mining end land use. All operations have been, and continue to be, subject to extensive environmental assessment processes, which include public and Aboriginal consultation.

By the end of 2008, all Elk Valley Coal operations are expected to be ISO 14001 certified. At present, Fording River operations, Greenhills operations and Coal Mountain operations are certified, and Line Creek operations, Cardinal River operations and Elkview operations are planned to be certified by year end.

During 2007, three of the operations were recognized for significant Environmental Awards in their respective provinces. Fording River operations received the 2006 Reclamation Award for outstanding Reclamation Achievement and the Elkview operations won the Citation for Outstanding Achievement for Reclamation at a Coal Mine in British Columbia. The Cardinal River operation was recognized for its mine reclamation work with the Major Reclamation Award from the Alberta Chamber of Resources and Alberta Environment.

For information on Elk Valley Coal’s asset retirement obligations please see the section titledOther Information Regarding the Trust — Environment, Health and Safety — Reclamation Activities and Asset Retirement Obligationsin this Annual Information Form.

17

Fording River

The Fording River mine is located 29 kilometres northeast of Elkford, British Columbia. The mine was constructed in 1969 as a three million tonne per year operation and has been operated continuously since that time. It was contributed to Elk Valley Coal by Old Fording pursuant to the 2003 Arrangement. Coal produced at the Fording River mine is primarily metallurgical coal, although a very small amount of thermal coal is also produced. The majority of current production is derived from the Eagle Mountain pit.

Reclamation is integrated into the ongoing mining activities and is conducted continually on waste dumps and other disturbed sites. A total of 697 hectares of mined land has been reclaimed at Fording River to December 31, 2007, with 30 hectares being reclaimed during 2007.

The Fording River mine’s quality management system is in compliance with the ISO 9001 quality standard and its environmental management system is in compliance with the ISO 14001 environmental standard.

Elkview

The Elkview mine is located just outside Sparwood, British Columbia. The mine was constructed in 1969 by Kaiser Resources Ltd. and has been operating on a nearly continuous basis for over 35 years. The mine was operated by Kaiser Resources Ltd. until 1980 when it was sold to BC Coal Limited, a predecessor of Westar Mining Limited (“Westar”). The mine was purchased by Teck Cominco from the trustee in the bankruptcy of Westar in 1992 and has operated continuously since 1993. The Elkview mine was contributed to Elk Valley Coal by Teck Cominco pursuant to the 2003 Arrangement. Effective August 1, 2005, Elk Valley Coal contributed the Elkview mine to Elkview LP for a direct and indirect 95 percent partnership interest and subsidiaries of NSC and POSCO each acquired a 2.5 percent limited partnership interest by each contributing US$25 million. Please see the section titled “General Development of the Business — Three-Year History — Elkview LP” in this Annual Information Form.

Coal produced at the Elkview mine is primarily metallurgical coal of which approximately 15 percent is considered to be lower quality hard coking coal. The majority of current production is derived from seams in the area of the Baldy and Natal Ridge pits.

Reclamation is integrated into the ongoing mining activities and is conducted continually on waste dumps and other disturbed sites. A total of 971 hectares of mined land has been reclaimed at the Elkview mine to December 31, 2007. While reclamation work was ongoing during the year no areas were fully reclaimed during 2007.

The Elkview mine’s quality management system is in compliance with the ISO 9001 quality standards. Elkview anticipates that its environmental management system will be incompliance with the ISO 14001environmental standard by the end of 2008.

Greenhills

The Greenhills mine is located eight kilometres northeast of Elkford, British Columbia. The mine was constructed in the early 1980’s by BC Coal Limited, a predecessor of Westar. Old FCL purchased Westar’s 80 percent interest in the Greenhills mine from the trustee in bankruptcy of Westar in December 1992.

From 1993 to 2003, the Greenhills mine operated under a joint venture agreement (the “Greenhills Joint Venture Agreement”) among Old FCL and POSCAN, pursuant to which FCL had an 80 percent interest in the joint venture while POSCAN had a 20 percent interest. As part of the 2003 Arrangement, the 80 percent interest held by Old FCL was assigned to Elk Valley Coal. The mine equipment and coal preparation plant are owned by Elk Valley Coal and POSCAN in proportion to their respective joint venture interests. Elk Valley Coal and POSCAN bear all costs and expenses incurred in operating the mine in proportion to their respective joint venture interests. POSCAN, pursuant to a property rights grant, has a right to 20 percent of all of the coal mined at the Greenhills mine from certain defined lands until termination of the Greenhills Joint Venture Agreement on the earlier of the date the reserves on the defined lands have been depleted or March 31, 2015.

Coal mined at the Greenhills mine is primarily metallurgical coal, although a small amount of thermal coal is also produced. Production is derived from the Cougar reserve which is divided into two distinct pits, Cougar North and Cougar South.

18

Reclamation is integrated into the ongoing mining activities and is conducted continually on waste dumps and other disturbed sites. A total of 511 hectares of mined land has been reclaimed at the Greenhills mine to December 31, 2007, with 38 hectares being reclaimed during 2007.

The Greenhills mine’s quality management system is in compliance with the ISO 9001 quality standard and its environmental management system is in compliance with the ISO 14001 environmental standard.

Coal Mountain

The Coal Mountain mine is located 30 kilometres southeast of Sparwood, British Columbia. Old FCL purchased the mine in 1994 from Corbin Creek Resources Ltd. and contributed it to Elk Valley Coal at the time of the 2003 Arrangement. Corbin Creek Resources Ltd. acquired the mine in the early 1990’s from Esso Resources Canada Ltd. The Coal Mountain mine produces both metallurgical and thermal coal.

Reclamation is integrated into the ongoing mining activities and is conducted continually on waste dumps and other disturbed sites. A total of 105 hectares of mined land has been reclaimed at the Coal Mountain mine to December 31, 2007. While reclamation work was ongoing during the year no areas were fully reclaimed during 2007.

The Coal Mountain mine’s quality management system is in compliance with the ISO 9001 quality standard and its environmental management system is in compliance with the ISO 14001 environmental standard.

Line Creek

The Line Creek mine is located 22 kilometres north of Sparwood, British Columbia. The mine has operated continuously since its start up by Crowsnest Resources Limited in 1981. It was acquired by Manalta Coal Ltd. and subsequently acquired by the Luscar/CONSOL joint ventures in 1998 and was operated until 2003 when it was acquired by Fording Inc. and contributed to Elk Valley Coal pursuant to the 2003 Arrangement. The Line Creek mine produces both metallurgical and thermal coal.

Reclamation is integrated into the ongoing mining activities and is conducted continually on waste dumps and other disturbed sites. A total of 315 hectares of mined land has been reclaimed at the Line Creek mine to December 31, 2007, with eight hectares being reclaimed in 2007.

The Line Creek mine’s quality management system is in compliance with the ISO 9001 quality standard. Line Creek anticipates that its environmental management system will be incompliance with the ISO 14001environmental standard by the end of 2008.

Cardinal River

The Cardinal River mine is located 42 kilometres south of Hinton, Alberta and includes the Cheviot pit. The mine was owned by the Luscar/CONSOL joint ventures and their predecessors and has operated continuously since its start up in 1969. It was acquired by Fording Inc. and contributed to Elk Valley Coal pursuant to the 2003 Arrangement. The Cardinal River mine produces primarily metallurgical coal.

Pursuant to the 2003 Arrangement, Luscar and CONSOL each retain a net revenue royalty of 2.5 percent based on any coal mined after the effective date of the 2003 Arrangement from the Cheviot pit and certain other former Luscar properties.

Reclamation is integrated into the ongoing mining activities and is conducted continually on waste dumps and other disturbed sites. A total of 850 hectares of mined land has been reclaimed at the Cardinal River mine to December 31, 2007. While reclamation work was ongoing during the year no areas were fully reclaimed during 2007.

Production of Mines under Prior Ownership

Prior to being contributed to Elk Valley Coal pursuant to the 2003 Arrangement, the Elkview mine was operated by Teck Cominco and the Line Creek and Cardinal River mines were operated by Luscar.

19

Production at the Elkview mine was 5.5 million, 5.5 million and four million tonnes of coal for the years 2002, 2001 and 2000 respectively. Production at the Line Creek mine was three million, 2.8 million and 2.6 million tonnes of coal for the years 2002, 2001 and 2000 respectively. Production at the Cardinal River mine was 2.1 million, three million, and 2.7 million tonnes of coal for the years 2002, 2001 and 2000 respectively.

Neptune Terminals

Elk Valley Coal owns a 46 percent interest in Neptune Terminals, a corporation that owns and operates a multi-product bulk handling port facility located at North Vancouver, British Columbia. The shares of Neptune Terminals are owned by three of the facility’s users. Neptune Terminals has a long-term lease with the Vancouver Port Authority which expires on December 31, 2026. Shippers can access Neptune Terminal’s facilities from the CNR system and, through interconnection, from the CPR system. By agreement among the shareholders of Neptune Terminals, Elk Valley Coal and the other owners incur rates charged for the handling of coal and other products based on the actual costs allocated to the handling of each product.

Neptune Terminal’s shareholder agreement obligates Elk Valley Coal to Neptune Terminals for its respective interest in the facility’s outstanding bank indebtedness and asset retirement obligations. At December 31, 2007, the Trust’s share of these potential obligations was $16 million.

RESERVES AND RESOURCES

Estimates of mineral reserves and mineral resources of Elk Valley Coal as at December 31, 2007, have been prepared by Elk Valley Coal’s internal engineers and geologists in accordance with National Instrument 43-101 —Disclosure for Mineral Projects(“NI 43-101”), under the supervision of Mr. R. Pritchard, P.Eng., Elk Valley Coal’s Director, Engineering, and Mr. D. Mills, P.Geo., Elk Valley Coal’s Chief Geologist. Mr. Pritchard and Mr. Mills are “qualified persons” for the purposes of NI 43-101. Estimates are reviewed and updated periodically to reflect new data from mining experience, drilling results and analysis.

The Trust is subject to the provisions of NI 43-101 with respect to the manner in which it reports mineral reserves and mineral resources and it is also subject to United States securities laws. Accordingly, in this section, mineral reserves and mineral resources have been presented in tabular form in accordance with NI 43-101 and a paragraph has been included after each mineral reserve table reconciling such information for the purposes of SEC Guide 7.

Terminology

Effective December 30, 2005, NI 43-101 requires all disclosure of mineral resources and mineral reserves, including that of coal, to use the definitions and applicable mineral reserve and mineral resource categories prescribed by the Canadian Institute of Mining, Metallurgy and Petroleum, in the CIM Definition Standards on Mineral Resources and Mineral Reserves adopted by CIM Council, as those definitions may be amended (the “CIM Definition Standards”). In respect of coal, the Companion Policy to NI 43-101 provides that a qualified person estimating mineral resources or mineral reserves for coal may follow the guidelines of Paper 88-21 of the Geological Survey of Canada: A Standardized Coal Resource/Reserve Reporting System for Canada, as amended (“Paper 88-21”) but that the equivalent mineral resource and mineral reserve categories set out in the CIM Definition Standards should be used. Prior to 2006, the Trust reported its coal reserves and resources applying the definitions set out in Paper 88-21, and is now reporting all of its mineral reserves and mineral resources using the categories set out in the CIM Definition Standards.

The CIM Definition Standards definitions of “mineral reserve”, “proven mineral reserve”, “probable mineral reserve”, “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are set out for reference in Part One of Appendix “C”.

Part Two of Appendix “C” contains the definitions ascribed by SEC Guide 7 to the terms “Reserve”, “Proven Reserves” and “Probable Reserves”, which are applicable to the reporting by the Trust of mineral reserves, including coal, when being reported on in accordance with SEC Guide 7. Unlike NI 43-101, SEC Guide 7 does not recognize the reporting of mineral deposits which do not meet the SEC Article 7 definition of “Reserve”.

20

Assumptions