Use these links to rapidly review the document

TABLE OF CONTENTS

Filed Pursuant to Rule 424(b)(3)

Registration Number 333-73020

PROSPECTUS SUPPLEMENT

(To Prospectus dated November 14, 2001)

Messer Griesheim Holding AG

10.375% Senior Notes Due 2011

Attached hereto and incorporated by reference herein are those sections of our Form 6-K relating to our financial results for the nine month period ended September 30, 2001. This Prospectus Supplement is not complete without, and may not be delivered or utilized except in connection with, the Prospectus, dated November 14, 2001, with respect to the 10.375% Senior Notes Due 2011, including any amendments or supplements thereto.

Investing in the notes involves a high degree of risk. See "Risk Factors" beginning on page 14 of the accompanying Prospectus for a discussion of certain factors that you should consider in connection with an investment in the notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these notes or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

This prospectus has been prepared for and will be used by Goldman, Sachs & Co. and Goldman Sachs International in connection with offers and sales of the notes in market-making transactions. These transactions may occur in the open market or may be privately negotiated, at prices related to prevailing market prices at the time of sale or at negotiated prices. Goldman, Sachs & Co. and Goldman Sachs International may act as principal or agent in these transactions. Messer Griesheim will not receive any of the proceeds of such sales of the notes.

Goldman, Sachs & Co.

Goldman Sachs International

December 17, 2001

2

REPORT FOR THE NINE MONTH PERIOD ENDED SEPTEMBER 30, 2001

The accounts being reported on are the consolidated results of Messer Griesheim Holding AG (the "Company"). Our obligation to file this report with The Bank of New York (the "Trustee"), for the benefit of our noteholders, and the U.S. Securities and Exchange Commission arises under the indenture, dated as of May 16, 2001, between the Company and the Trustee, pursuant to which the Company has issued its 10.375% Senior Notes due 2011.

This report may include forward-looking statements. In addition, from time to time, our representatives or we have made or may make forward-looking statements orally or in writing. All statements other than statements of historical facts included in this report regarding our financial condition, plans to increase revenues and statements regarding other future events or prospects, are forward-looking statements. We have used the words "may," "will," "expect," "anticipate," "believe," "estimate," "plan," "intend" or similar expressions in this report to identify forward-looking statements. We have based these forward-looking statements on our current views with respect to future events and financial performance. Actual results could differ materially from those projected in the forward-looking statements.

We are not obliged to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified to their entirety by the cautionary statements contained in this report and the more detailed discussion of risks in the section entitled "Risk Factors" on page 14 of the accompanying Prospectus. Because of these risks, uncertainties and assumptions, investors should not place undue reliance on forward-looking statements.

We are a producer and distributor of industrial gases, including oxygen, nitrogen, argon, carbon dioxide, hydrogen, helium, specialty gases and acetylene. The industrial gases we produce are used in a broad range of industries, including the steel, chemicals, electronics, pulp and paper, health-care, food and beverage, automotive, lighting and glass industries.

MANAGEMENT'S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion in conjunction with the Company's unaudited condensed consolidated financial statements included elsewhere herein. The Company's financial statements are prepared in accordance with the International Accounting Standards of the International Accounting Standards Committee, or IAS, which differ in certain significant respects from U.S. GAAP. You can find reconciliations of net income, shareholder's equity and other financial statement items and disclosures regarding differences between IAS and U.S. GAAP in note 20 to the Company's unaudited condensed consolidated financial statements.

We operate in nearly 60 countries through more than 500 facilities, including production plants, distribution and filling stations and research centers. We have an estimated global market share of approximately 5% of the total industrial gases market, making us the seventh largest industrial gas producer worldwide, and leading market shares in Germany and certain other countries in central and eastern Europe. We also have strong businesses in selected industrial areas of the United States and in selected niche markets in other western European countries. In 2001, we generated year-to-date net sales of E1,234 million and normalized EBITDA of E297 million.

3

Our primary or core markets are Germany, North America and the rest of Europe. Our two largest markets, Germany and North America, collectively accounted for 63.4% of our net sales and 75.7% of our normalized EBITDA for year-to-date 2001. Within each of our geographic markets, we generally organize our business based upon how we deliver industrial gases to our customers: delivery of large volumes from on-site production facilities or by pipeline, delivery in bulk tanks transported by truck or rail and delivery in gas cylinders. In addition to our core markets of Europe and North America, we also operate in Asia, Africa and Latin America. We intend to divest substantially all of the assets outside our core markets, along with certain non-strategic assets in our core markets, by year-end 2002.

The following is an overview of a number of significant factors that affect our results of operations or that may affect our future results of operations.

Acquisition Transactions, Refinancing and Divestiture Program

As discussed in note 3 to our unaudited interim condensed consolidated financial statements contained herein, the acquisition transactions have been accounted for at fair value and, accordingly, our assets and liabilities have been recorded at their estimated fair values as of April 30, 2001, the date of the acquisition transactions. As a result, the financial statements of Messer Griesheim for periods prior to the acquisition transactions are not comparable to our financial statements for periods subsequent to the acquisition transactions. To highlight this lack of comparability, a solid vertical line has been inserted, where applicable, between columns in the tables and schedules of this document, and in our financial statements to distinguish information pertaining to the pre-acquisition and post-acquisition periods.

The Acquisition of Messer Griesheim

Prior to the completion of the acquisition transactions described below, Messer Griesheim was owned:

- •

- 331/3% by the Messer family through a holding company, Messer Industrie GmbH, and

- •

- 662/3% by Hoechst AG, a subsidiary of Aventis S.A.. Aventis was formed in December 1999 as the result of the merger of Hoechst AG and Rhône-Poulenc S.A., two of Europe's largest chemical companies.

On December 31, 2000, Messer Industrie, Hoechst and our parent company Messer Griesheim Group GmbH (formerly named Cornelia Verwaltungsgesellschaft mbH), entered into certain acquisition transactions.

As a result of the acquisition transactions, the issuer owns 100% of Messer Griesheim and the issuer is wholly owned by Messer Griesheim Group. The issuer and Messer Griesheim Group are both holding companies with no material assets other than their direct or indirect interests in Messer Griesheim (and, in the issuer's case, the payments under the intercompany loan to Messer Griesheim). As a result of the completion of the acquisition transactions, Messer Griesheim Group is owned:

- •

- 32.67% by the Messer family, through Messer Industrie;

- •

- 33.665% by Allianz Capital Partners; and

- •

- 33.665% by six private equity funds managed by affiliates of The Goldman Sachs Group, Inc.

In connection with these acquisition transactions, the shareholders of Messer Griesheim Group entered into a shareholders' agreement governing their respective voting control and other ownership rights with respect to the issuer and Messer Griesheim.

4

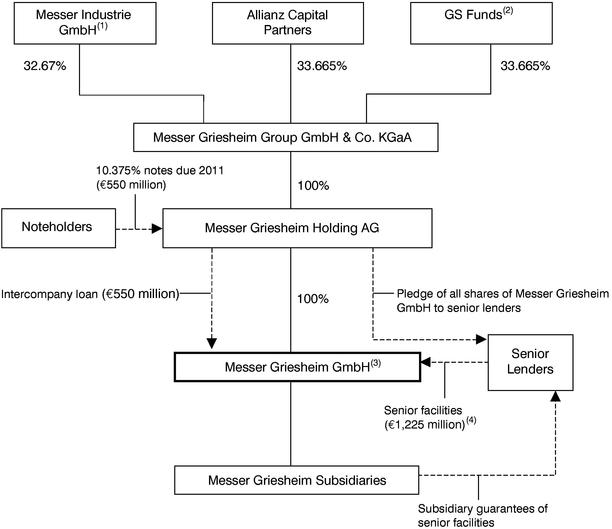

Transaction Structure

The following diagram shows our ownership structure and the structure of our principal indebtedness following completion of the acquisition transactions, and after the issuance of the notes and the refinancing of our indebtedness as have been completed, including repayment in full of the E400 million mezzanine bridge facility and repayment of E115 million of our senior term facilities:

- (1)

- The holding company for the Messer family's interests in Messer Griesheim.

- (2)

- Certain private equity funds managed by affiliates of The Goldman Sachs Group, Inc.

- (3)

- Principal operating company in Germany and holding company for the remainder of our operations.

- (4)

- E1,340 million is the initial aggregate amount of term loan facilities. We repaid E115 million principal amount of senior term facilities with a portion of the proceeds from the sale of the notes. E1,225 million is the aggregate amount of senior term facilities that remains. The senior facilities also include committed but not fully drawn funds totaling E310 million under revolving facilities. Certain of Messer Griesheim's subsidiaries are also direct borrowers under the senior facilities.

Refinancing Program

In connection with the acquisition transactions described above, substantially all of Messer Griesheim's existing indebtedness was refinanced through the senior facilities described below and the

5

notes. Upon the initial closing of the acquisition Messer Griesheim entered into a senior facilities agreement with aggregate available funds of E1,650 million (E1,340 million of term loan facilities and E310 million of revolving facilities) and a mezzanine bridge facility agreement in the aggregate amount of E400 million. Since that time Messer Griesheim has borrowed a portion of the term loans under the senior facilities and the entire mezzanine bridge facility. Upon the closing of the sale of the notes, the issuer made an intercompany loan to Messer Griesheim with the gross proceeds from the notes, and Messer Griesheim used the intercompany loan to repay the mezzanine bridge facility in full and repay E115 million principal amount of outstanding term borrowings under the senior facilities.

Net Sales

We primarily earn revenues from

- •

- sales of industrial gases and

- •

- sales of hardware related to industrial gas usage.

Our sales of industrial gases which amounts to greater than 90% of our total revenues are divided into three business units corresponding to their mode of delivery: on-site and pipeline sales, bulk delivery sales and cylinder delivery sales. Contracts in our on-site production and pipeline supply businesses in Europe and the United States typically have terms of 10 to 15 years and usually have "take-or-pay" minimum purchase provisions. In each of the last three years, the "take-or-pay" minimum purchase requirements in our on-site and pipeline supply contracts accounted for approximately 60% to 70% in Germany and 40% to 45% in the United States of the total amount of net sales that we generated under these contracts.

Contracts in our bulk business generally have terms of two to three years in Europe and five to seven years in the United States. Customers in our on-site and pipeline and bulk businesses have historically exhibited high renewal rates, with over 90% of customers whose contracts expired in the past five years renewing their contracts with us. Our on-site, pipeline and bulk businesses in Germany and the United States accounted for approximately 33% of our total net sales and approximately 50% of our normalized EBITDA in 2001. We generally sell our cylinder gases by purchase orders or by contracts with terms ranging between one to two years in Europe and three to five years in the United States.

The Company calculates normalized EBITDA as operating profit before depreciation and amortization, after adding back charges for impairment of intangible assets and property, plant and equipment and restructuring charges.

Normalized EBITDA is not a measure recognized by IAS or U.S. GAAP. This and similar measures are used by different companies for differing purposes and are often calculated in ways that reflect the unique situations of those companies. One should be very cautious in comparing the Company`s normalized EBITDA data to the EBITDA data of other companies. Normalized EBITDA is not a substitute for operating profit as a measure of operating results. Likewise, normalized EBITDA is not a substitute for cash flow as a measure of liquidity.

Our net sales are dependent on the economic conditions in the markets in which we operate. However, we believe that we have limited exposure to the cyclical nature in demand of any particular industry because of the wide diversity of industries represented by our customer base.

Although industrial gas prices appear to have recently stabilized in many of the markets in which we operate, prices have consistently decreased for at least the last 10 years, especially in the bulk and commodity gas cylinder segments, due to aggressive efforts by most producers to increase market share. The profit margin impact of this price erosion has been partially offset by efficiency improvements throughout the supply chain and regional consolidation among large participants in the industry,

6

permitting economies of scale. In addition, new applications for industrial gases have increased sales volumes and profit margins.

Cost of Sales

Our principal raw material is air, which is free and which we separate into its component gases. Cost of sales principally consists of:

- •

- capital costs of plants;

- •

- costs of energy required for production, and

- •

- labor costs relating to production.

Energy costs consist principally of electrical power costs. Energy costs accounted for approximately 25% of our total operating expenses in 2001. We are able to pass on a portion of increases in energy costs to many, but not all, of our on-site and pipeline customers with long-term supply contracts, although these adjustments in cost often occur only on an annual basis. The amount and other terms of these energy cost pass-through provisions vary by contract.

Labor costs relating to production consist principally of wages and salaries, social security contributions and other expenses related to employee benefits. Social security contributions include our portion of social security payments as well as our contributions to workers' insurance associations.

We depreciate fixed assets on a straight-line basis. Our depreciation rates assume a useful life of 10 to 50 years for buildings, 10 to 20 years for plant and machinery and 3 to 20 years for other plant, factory and office equipment.

Currency Translation

During the periods presented, our operations were conducted principally in Europe and the United States, and to a lesser extent in other regions of the world. On January 1, 2000, we adopted the E as our reporting currency and translated all amounts previously denominated in Deutsche Mark (DM) at the fixed exchange rate of E1.00 = DM 1.95583, applicable since January 1, 1999, for all prior periods presented.

The balance sheet items of our group companies located outside the European Monetary Union are translated from their relevant local currencies into E at the closing exchange rate on our balance sheet date. The items on our income statement are translated into E using average annual exchange rates. Foreign currency gains and losses from current assets and current liabilities denominated in a currency other than the functional currency are included in "other operating income" or "other operating expense". Accordingly, exchange rate fluctuations can have a material impact on our income statement and balance sheet as presented in E.

Impairment of Intangible Assets and Property, Plant and Equipment

In the event facts and circumstances indicate that our long-lived assets, including property, plant and equipment and intangible assets, may be impaired, an evaluation of recoverability is performed. If an evaluation is required, the recoverable amount of the asset is compared to the asset's carrying amount to determine whether a write-down to the recoverable amount is required. The recoverable amount is based on the discounted cash flows expected to arise from the continuing use of an asset and from its disposal at the end of its useful life. The write-down of current and non-current assets, except for goodwill, are reinstated to the extent factors giving rise to the write-down reasons no longer exist.

7

Discontinuing Operations

In December 1999, Messer Griesheim transferred its cutting & welding division to its minority shareholder, Messer Industrie GmbH. As a result of this transaction, the operating results of the cutting & welding division have been classified as discontinuing operations on Messer Griesheim's consolidated 2000 income statement.

Divestiture Program

Our core markets are Germany and elsewhere in Europe and the United States. In May 2001 immediately following our change in ownership that resulted from the acquisition transactions described elsewhere in this document, we adopted a divestiture program. Pursuant to the divestiture program, we are currently in negotiation to sell substantially all of our assets and operations in our non-core markets in Asia, Africa and Latin America, as well as certain non-strategic assets and operations in our core markets. Principally, the proceeds from this divestiture program will be used to reduce our consolidated debt.

We estimate that the operations to be divested accounted for approximately 24% of our net property, plant and equipment at year-end 2000 and 17% of our total net sales and 7% of normalized EBITDA for 2000. We expect our divestitures will permit us to reduce our consolidated debt by approximately E400 million. Delays in divesting these assets could prevent us from realizing the full benefit of our program to reduce our debt.

The divestiture of certain of our assets and operations may require additional expenditures prior to their divestiture.

Cost-Savings Plan

We are implementing a plan to reduce our operating costs, principally in Europe. This plan involves eliminating duplications in support positions for certain process functions, reducing energy costs, centralizing key process functions and simplifying our management structure. We have identified a number of specific cost savings measures that we expect will reduce the cost base of our operations in our core markets relative to its current level by E100 million by year-end 2003. To implement these measures, we expect to incur one-time costs of approximately E84 million over the next two years, principally to be applied towards severance payments and information technology improvements.

Taxation

In general, prior to 2001 retained (undistributed) German corporate income was initially subject to a federal corporation income tax at a rate of 40% for 2000 (40% for 1999 and 45% for 1998), plus a surcharge of 5.5% for each year. Giving effect to the surcharge, the federal corporate tax rate was 42.2% for 2000 (42.2% in 1999 and 47.475% in 1998). Upon distribution of certain retained earnings generated in Germany to stockholders in 2001, the corporate income tax rate on the earnings was adjusted to 30%, plus a solidarity surcharge of 5.5% for a total of 31.65% for each year, by means of a refund for taxes previously paid. Under the current German corporate tax system, during a 15 year transition period beginning on January 1, 2001, we will continue to receive a refund or pay additional taxes on the distribution of retained earnings which existed as of December 31, 2000.

Deferred taxes are recognized for the temporary differences between the carrying amount of assets or liabilities in the balance sheet and their associated tax bases. Deferred taxes are based on the rates enacted for the subsequent periods when the temporary differences are expected to reverse. A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the asset can be utilized.

8

Certain reclassifications have been made to the presentation of prior periods to conform to the current period classification. Consideration should be given to the effects of the acquisition transactions, the refinancing program, and the divestiture program, as discussed above, when comparing historical financial information for periods prior to April 30, 2001 to periods thereafter.

Four Months Ended April 30, 2001 and Five Months Ended September 30, 2001 Compared with Nine Months Ended September 30, 2000

The following table sets forth a summary of our results, which are unaudited, for the nine month period ended September 30, 2000, the four month period ended April 30, 2001 and the five month period ended September 30, 2001. Financial information for periods prior to and subsequent to the acquisition transactions have been separated in the following table by inserting a solid vertical line between the columns for such periods.

| | Predecessor | | |||||

|---|---|---|---|---|---|---|---|

| | Nine Months Ended September 30, 2000 | Four Months Ended April 30, 2001 | | ||||

| | Successor Five Months Ended September 30, 2001 Messer Griesheim Holding AG | ||||||

| | Messer Griesheim GmbH | ||||||

| | E (in millions) | E (in millions) | E (in millions) | ||||

| Net sales | 1,244.9 | 574.5 | 659.5 | ||||

| Cost of sales | (600.4 | ) | (293.4 | ) | (336.2 | ) | |

Gross profit | 644.5 | 281.1 | 323.3 | ||||

| Distribution and selling costs | (433.7 | ) | (177.2 | ) | (192.0 | ) | |

| General and administrative costs | (107.9 | ) | (45.0 | ) | (47.5 | ) | |

| Other, net(1) | (93.8 | ) | (12.4 | ) | (33.0 | ) | |

Operating profit | 9.1 | 46.5 | 50.8 | ||||

| Interest expense, net | (66.2 | ) | (36.4 | ) | (64.3 | ) | |

| Loss before income taxes and minority interests | (247.4 | ) | (6.6 | ) | (29.9 | ) | |

| Income tax benefit / (expense) | 57.3 | (4.8 | ) | (21.8 | ) | ||

| Net loss | (195.7 | ) | (13.5 | ) | (56.2 | ) | |

| Normalized EBITDA | 251.1 | 125.9 | 171.0 | ||||

- (1)

- Amounts include total net of research and development costs, other operating income, other operating expense, impairment of intangible assets and property, plant and equipment and restructuring charges.

As a result of the acquisition transactions, the refinancing program and the divestiture program, as described above, a comparison between the four months ended April 30, 2001 and the five months ended September 30, 2001 to the nine months ended September 30, 2000 is not meaningful. The acquisition transactions were accounted for in a manner similar to a "purchase" business combination and, accordingly, the cost of the acquisition has been allocated to the assets acquired and the liabilities assumed based on their fair values. The accounting treatment impacts our results of operations for the five months ended September 30, 2001 primarily by increasing amortization of goodwill, decreasing depreciation of property, plant and equipment, and reduced losses of disposals of subsidiaries and other assets included in the divestiture program and correspondingly decreasing our operating profit compared to all periods prior to April 30, 2001. The refinancing program increased our interest expense in the five months ended September 30, 2001 compared to all periods prior to April 30, 2001.

9

In addition, certain subsidiaries to be sold as part of our divestiture program have been deconsolidated and thus excluded from the results of operations for the five months ended September 30, 2001.

Notwithstanding the lack of comparability between the periods, net sales with respect to our continuing operations remained relatively constant in most of our operating regions, and operating profit with respect to our continuing operations, excluding impairment charges and restructuring charges, increased in Germany and Eastern Europe, remained stable in Western Europe (excluding Germany) and declined in North America.

Management believes that the following material trends have affected our net sales and operating profit with respect to our continuing operations for the nine months ended September 30, 2001, compared to the nine months ended September 30, 2000. Net sales and operating profit in Germany during 2001 benefited from increased sales volume in our gas business. This benefit was offset by lower prices resulting from ongoing competition in response to market conditions and the overall worsening economic conditions in Germany. Net sales and operating profit in North America declined, reflecting the adverse effects of the continuing economic downturn in U.S. markets, partially offset by the favorable effects of the appreciation of the dollar against the Euro. On a constant exchange rate basis, both net sales and operating profit decreased in North America. In Western Europe (other than Germany), net sales and operating profit remained selectively constant across all countries other than the United Kingdom, which experienced a slight decline in net sales due to lower sales to the food and beverage industry. Net sales and operating profit in Eastern Europe decreased, primarily resulting from a major devaluation of the Yugoslavian currency against the Euro.

Three Months Ended September 30, 2001 Compared with Three Months Ended September 30, 2000

The following table sets forth a summary of Messer Griesheim's results of operations for the three month periods ended September 30, 2000 and 2001, in terms of amounts as well as a percentage of net sales.

| | Predecessor Three Months Ended September 30, 2000 Messer Griesheim GmbH | Successor Three Months Ended September 30, 2001 Messer Griesheim Holding AG | |||||||

|---|---|---|---|---|---|---|---|---|---|

| | E (in millions) | % | E (in millions) | % | |||||

| Net sales | 397.7 | 100.0 | 393.6 | 100.0 | |||||

| Cost of sales | (183.3 | ) | (46.1 | ) | (206.1 | ) | (52.4 | ) | |

| Gross profit | 214.4 | 53.9 | 187.5 | 47,6 | |||||

Distribution and selling costs | (153.2 | ) | (38.5 | ) | (112.4 | ) | (28.6 | ) | |

| General and administrative costs | (31.7 | ) | (8.0 | ) | (28.7 | ) | (7.3 | ) | |

| Other, net(1) | (32.8 | ) | (8.2 | ) | (21.4 | ) | (5.4 | ) | |

| Operating profit (loss) | (3.3 | ) | (0.8 | ) | 25.0 | 6.4 | |||

| Interest expense, net | (25.5 | ) | (6.4 | ) | (40.1 | ) | (10.2 | ) | |

| Loss before income taxes and minority interests | (79.0 | ) | (19.9 | ) | (17.5 | ) | (4.5 | ) | |

| Income taxes | 18.2 | 4.6 | (20.9 | ) | (5.3 | ) | |||

| Net income (loss) | (63.2 | ) | (15.9 | ) | (41.3 | ) | (10.5 | ) | |

| Normalized EBITDA | 77.2 | 19.4 | 98.1 | 24.9 | |||||

- (1)

- Amounts include total net of research and development costs, other operating income, other operating expense, impairment of intangible assets and property, plant and equipment and restructuring charges.

10

Net sales. Net sales decreased 1.0% to E393.6 million in the third-quarter 2001 from E397.7 million in the same period 2000.

| | Predecessor Three Months Ended September 30, 2000 Messer Griesheim GmbH | Successor Three Months Ended September 30, 2001 Messer Griesheim Holding AG | ||

|---|---|---|---|---|

| | E (in millions) | E (in millions) | ||

| Net sales (Business Areas) | ||||

| Germany | 141.0 | 163.9 | ||

| Western Europe, excluding Germany | 61.1 | 64.7 | ||

| Eastern Europe | 51.1 | 54.2 | ||

| North America | 100.4 | 95.9 | ||

| Others | 50.4 | 14.7 | ||

| Reconciliation / Corporate | (6.3 | ) | 0.2 | |

| Total | 397.7 | 393.6 | ||

- •

- Net sales in Germany increased 16.2% to E163.9 million in the third quarter 2001 from E141.0 million in the same period 2000. This increase is principally due to increases in sales volumes. These sales volume increases were partially offset by falling gas prices. In general, prices in the German market fell in the third quarter 2001 due to increased competition in response to market conditions. However, overall price pressure declined in 2001 compared to 2000.

- •

- Net sales in North America decreased 4.5% to E95.9 million in the third quarter 2001 from E100.4 million in the same period 2000. This decrease is primarily due to lower sales volumes in all business areas as a result of the recession in the U.S. The decrease is partially offset of the appreciation of the U.S. dollar against the Euro in the third quarter 2001. On a constant exchange rate basis, net sales in North America decreased E8.7 million or 8.7% in the third-quarter 2001 compared to 2000. In order to make the figures comparable, the impact of the business disposal program on the third quarter 2001 sales was E6.3 million. Therefore, on a like-to-like basis, sales in the third quarter 2000 was E 94.1 million, which means ignoring exchange rates, sales of business included in both periods actually grew by 2.0%.

- •

- Net sales in Western Europe (excluding Germany) increased 5.9% to E64.7 million in the third-quarter 2001 from E 61.1million in the same period 2000. This increase is principally due to increased sales volumes in France, Italy, Switzerland and Spain. Furthermore, sales in the U.K. are driven by an extra engineering turnover this quarter. Further, sales benefited from various price developments. The downward trend in average selling price of LCO2 in the U.K. has been stopped. Similarly, the price war in the Italian market has declined compared to the same period 2000. However, we faced the first signs of business climate deterioration in France and Italy.

- •

- Net sales in Eastern Europe increased 6.1% to E54.2 million in the third-quarter 2001 from E51.1 million in the same period 2000. Sales volumes in almost all countries in the region increased compared to the same period 2000. In addition, the first-time consolidation of one of our Czech subsidiaries in September 2000 resulted in additional net sales of E1.6 million for 2001 compared to the prior year.

- •

- Net sales in Other Business Areas decreased by E35.7 million to E14.7 million in the third-quarter 2001 from E50.4 million in the same period 2000. However, numbers are not comparable owing to the de-consolidation of companies in Mexico, Brazil, Argentina, Peru, Venezuela, Trinidad &Tobago, South Africa, Singapore, Korea and Indonesia effective May 1, 2001.

11

Cost of sales. Cost of sales consists primarily of raw material costs, purchased parts and direct labor, as well as manufacturing overheads and depreciation. Cost of sales increased 12.4% to E206.1 million in the third-quarter 2001 from E183.3 million in the same period 2000. The cost of sales as a percentage of net sales increased to 52.4% in the third-quarter 2001 from 46.1% in the same period 2000. The increase primarily results from higher energy costs in the United States that could not be passed on to customers. Furthermore, our product mix in the third quarter was burdened by higher hardware-sales in the U.K. and Germany, which have below average margins.

Distribution and selling costs. Distribution and selling costs consist primarily of sales organization costs, transport of gases and cylinders from the production site or filling station to the customer, depreciation of the cylinders and tanks at the customer site, advertising and sales promotions, commissions and freight. Distribution and selling costs decreased 26.6% to E112.4 million in the third-quarter 2001 from E153.2 million in the same period 2000. This decrease is principally due to the successful implementation of the cost savings program. Distribution and selling costs as a percentage of net sales decreased to 28.6% in the third-quarter 2001 from 38.5% in the same period 2000.

General and administrative costs. General and administrative costs consist primarily of personnel costs attributable to general management, finance and human resources functions, as well as other corporate overheads. General and administrative expenses decreased 9.5% to E28.7 million in the third-quarter 2001 from E31.7 million in the same period 2000. This decrease is principally due to lower staff compensation costs and operating efficiencies in eastern Europe, resulting from the consolidation of local operations in the third-quarter 2001

Other, net. Other, net decreased 34.8% to E21.4 million in the third quarter 2001 from E32.8 million in the same period 2000. Other, net in the third quarter 2000 included impairment charges relating to property, plant and equipment (E32.3 million) which were not incurred in the three months ended September 30, 2001. This decrease was partially offset by the amortization of goodwill, which resulted from the accounting for the acquisition transactions (E11.2 million), restructuring and reorganisation charges (E5.0 million) and an increase of numerous other operating expenses for consulting services relating to the refinancing transaction in the second and third quarter 2001.

Operating profit (loss). Operating profit (loss) increased to a profit of E25.0 million in the third-quarter 2001 from a loss of E3.3 million in the same period 2000 based essentially on the factors described above.

| | Predecessor Three Months Ended September 30, 2000 Messer Griesheim GmbH | Successor Three Months Ended September 30, 2001 Messer Griesheim Holding AG | |||

|---|---|---|---|---|---|

| | E (in millions) | E (in millions) | |||

| Operating profit (loss) (Business Areas) | |||||

| Germany | 22.9 | 44.8 | |||

| Western Europe, excluding Germany | 5.7 | 5.8 | |||

| Eastern Europe | 10.1 | 9.9 | |||

| North America | 8.4 | 1.0 | |||

| Others | (41.1 | ) | 0.9 | ||

| Reconciliation / Corporate | (9.3 | ) | (37.4 | ) | |

| Total | (3.3 | ) | 25.0 | ||

12

- •

- Operating profit in Germany increased 95.6% to E44.8 million in the third-quarter 2001 from E22.9 million in the same period 2000. This increase was principally due to a decline in price pressure in the market. Furthermore, the on-going cost-saving program is showing its initial success by reducing our cost base.

- •

- In North America we incurred an operating profit of E1.0 million in the third-quarter 2001 compared to an operating profit of E8.4 million in the same period 2000. Operating profit in North America in the third-quarter 2001 reflects restructuring charges of E0.3 million. On a constant exchange rate basis and excluding the restructuring charges in the third-quarter 2001, operating profit in North America is E1.2 million. This decline was principally due to lower sales volume resulting from the recession in the U.S. and higher energy costs which impacts cost of sales as well as increasing distribution costs (fuel). In order to make the figures comparable, the impact of the divestiture program on the third quarter 2001 operating profit was E0.4 million. Therefore, on a like-to-like basis operating profit in the third quarter 2000 was E8.0 million or decreased by E7 million.

- •

- Operating profit in Western Europe increased 1.8% to E5.8 million in the third-quarter 2001 from E5.7 million in the same period 2000. Operating profit in Western Europe in the third-quarter 2001 reflects restructuring charges of E0.5 million. Excluding this item, operating profit increased by 10.5% to E6.3 million in the third-quarter 2001. This increase was principally due to higher sales volumes and generally stable pricing in the third-quarter 2001, the curtailment of the price war on the Italian market, successful start-up of the cylinder business in Spain and a continued decrease of the cost base in the U.K. in accordance with our cost savings program.

- •

- Operating profit in Eastern Europe decreased 2.0% to E9.9 million in the third-quarter 2001 from E10.1 million in the same period 2000. Included in the third quarter 2000 was non-recurring other income of approximately E1 million relating to our Hungarian affiliate. Operating profit in Eastern Europe in the third-quarter 2001 reflects restructuring charges of E0.4 million. The operating profit reflects an increase in net sales throughout most of the region other than Yugoslavia partially offset by the negative effects of the devaluation of the Yugoslavian currency. Additional contribution results from the effective cost management actions in Slovakia, Slovenia and Hungary.

- •

- Operating profit (loss) in Other Business Areas increased to a profit of E0.9 million in the third quarter 2001 from a loss of E41.1 million in the same period 2000. Operating loss in the third quarter 2000 reflects impairment charges of E32.1 million. Excluding this item, operating loss amounted to E9.0 million in the third quarter 2000. This improvement results primarily from sales from plants that came on stream in the same period 2000, partially offset by delays in the start-up of certain new plants in Latin America. These delays required us to make compensating gas purchases from competitors to meet our existing contractual obligations to our customers. However, numbers are not comparable owing to the de-consolidation of companies in Mexico, Brazil, Argentina, Peru, Venezuela, Trinidad & Tobago, South Africa, Singapore and Indonesia effective May 1, 2001.

- •

- Operating loss in Reconciliation / Corporate amounted to E37.4 million in the three months ended September 30, 2001 compared with an operating loss of E9.3 million in the period 2000. The increase in operating loss in the three months ended September 30, 2001 is mainly due to the amortization of goodwill and changes in fair value of subsidiaries held for sale.

Interest expense, net. Net interest expenses increased 57.3% to E40.1 million in the third-quarter 2001 from E25.5 million in the same period 2000. These expenses are principally the interest charges associated with Messer Griesheim's debt. This increase in the third-quarter 2001 is due to our higher long-term debt balance as a result of the refinancing program of the Messer Group following the

13

acquisition transactions. The average interest rate has increased from 6.5% to 8.3% per annum as a result of the aforementioned refinancing.

Income taxes. An income tax expense of E20.9 million was recorded in the third-quarter 2001, compared to an income tax benefit of E18.2 million in the same period 2000. This is principally due to the utilization of tax loss carryforwards in the third-quarter 2000. The income tax expenses for the 2001 period result from non tax deductible goodwill amortization due to the acquisition transactions and other non deductible expenses for tax purposes.

Liquidity and Capital Resources

Cash Flows for the Nine Month Period Ended September 30, 2000, the Four Month Period Ended April 30, 2001, and the Five Month Period Ended September 30, 2001

The following table summarizes our cash-flow activity during nine month period ended September 30, 2000, the four month period ended April 30, 2001 and the five month period ended September 30, 2001. The solid vertical line separates the information for periods prior to and subsequent to the acquisition transactions:

| | Predecessor | | |||||

|---|---|---|---|---|---|---|---|

| | Nine months ended September 30, 2000 | Four months ended April 30, 2001 | | ||||

| | Successor Five months ended September 30, 2001 Messer Griesheim Holding AG | ||||||

| | Messer Griesheim GmbH | ||||||

| | E (in millions) | ||||||

| Cash flow from (used in) operating activities | 167.0 | (8.9 | ) | 185.1 | |||

| Cash flow used in investing activities | (195.6 | ) | (66.0 | ) | (46.1 | ) | |

| Cash flow from (used in) financing activities | 37.9 | 247.6 | (88.9 | ) | |||

| Cash and cash equivalents, end of period | 59.3 | 226.6 | 258.3 | ||||

Consideration should be given to the effects of the acquisition transactions, the refinancing program, and the divestiture program when comparing historical financial information, for periods prior to April 30, 2001 to periods thereafter.

Cash flow from (used in) operating activities. Our cash flow from operations was E167.0 million in the nine-months ended September 2000 compared with cash used in operating activities of E8.9 million in the four-month period ended April 30, 2001 and cash flow from operating activities of E185.1 million in the five-month period ended September 30, 2001. The cash flow from operations for the nine-months ended September 2000 principally reflects a loss before income taxes and minority interests of E247.4 million which was offset mainly by depreciation and amortization of property, plant and equipment and intangible assets and by changes in provisions. For the four months ended April 30, 2001 cash flow from operating activities principally reflects a decrease due to the Singapore operations and changes in working capital in the four-month period ended April 30, 2001. The increase of cash flow from operating activities in the five months ended September 30, 2001 principally results from decreased losses and changes in working capital.

Cash flow used in investing activities. In the nine-months ended September 30, 2000, our net cash used in investing activities was E195.6 million, compared with net cash used in investing activities of E66.0 million in the four-month period ended April 30, 2001 and E46.1 million in the five month period ended September 30, 2001. The negative figure for the nine months ended September 30, 2000 principally reflects E180.9 million in purchases of property, plant and equipment and intangible assets. For the four-months ended April 30, 2001 and the five months ended September 30, 2001, the cash

14

used in investing activities principally reflects capital expenditure on property, plant and equipment as well as investments and loans to related parties.

Cash flow from (used in) financing activities. Our cash flow from financing activities was E37.9 million in the nine-months ended 2000 compared with E247.6 million in the four-month period ended April 30, 2001 and net cash used in financing activities of E88.9 million in the five-month period ended September 30, 2001. Cash flow from financing activities for the four months ended April 30, 2001 principally reflects additional borrowings that resulted in an increase of cash, which was used to refinance debt in addition to establishing restricted cash collateral on debt that was not refinanced in the five months ended September 30, 2001.

Anticipated Expenditures and Sources of Funds

Operational capital expenditures as a percentage of net sales was 14.5% in the nine-months ended 2000, as compared to 8.6% in the four-month period ended April 30, 2001 and 7.3% in the five-month period ended September 30, 2001. A core component of our strategy is to reduce Messer Griesheim's historically high levels of capital expenditure. However, we will require funds to meet scheduled debt repayments and to fund the acquisition, if and when it happens, of the China assets described in "Current Transactions-China Transactions", with a purchase price of E32 million and the assumption of existing debt of the ACIC joint ventures (approximately E17.3 million at September 30, 2001).

We had total indebtedness (including finance leases) of E1,743.3 million at September 30, 2001, of which E1,510.1 million was long-term indebtedness. The indebtedness was primarily due to banks and our bondholders and had an average rate of interest of approximately 7.8% at September 30, 2001.

Messer Griesheim's principal sources of funds have been cash flow from operations and borrowings from banks. We expect that, going forward, we will finance on-going operations and implement our cost-savings measures and information-technology improvements with a combination of bank borrowings and operating cash flows. We are dependent on the proceeds from our divestiture program to meet our contractually scheduled debt repayment under our senior facilities on April 30, 2003. We expect that our other cash requirements will be met through operating cash flows.

As of September 30, 2001, we had in place unused credit lines totaling E305.5 million. In addition, certain of our subsidiaries have unused available credit lines under local facilities.

Interest Rate Risk Management

We are exposed to interest rate risk mainly through our debt instruments. We manage interest rate risk on a group-wide basis with a combination of fixed and floating rate instruments designed to balance the fixed and floating interest rates. We have entered into interest rate swap agreements that effectively convert a major portion of our floating rate indebtedness to a fixed rate basis for the next three years, thus reducing the impact of interest rate changes on future interest expense.

Foreign Exchange Risk Management

We also are exposed to foreign currency exchange risk related to foreign currency denominated assets and liabilities and debt service payments denominated in foreign currencies. We manage foreign currency exchange risk on a group-wide basis using exchange forward contracts. Our current policy with respect to limiting foreign currency exposure is to economically hedge foreign currency exposures when appropriate.

The table below provides information about our significant derivative financial instruments that are sensitive to changes in interest and foreign currency exchange rates as of September 30, 2001. The table presents the notional amounts and the weighted average contractual foreign exchange rates. The terms

15

of our cross-currency exchange forward contracts generally do not exceed one year. At September 30, 2001, our interest rate swaps had remaining terms of nearly three years.

Derivative Financial Instruments

| | Contract notional amount | Contractual rates | Fair value September 30, 2001 | |||||

|---|---|---|---|---|---|---|---|---|

| | (equivalent in thousands, except for contractual rates) | |||||||

| | E'000 | | E'000 | |||||

| Interest rate cap contracts | ||||||||

| Euro | 25,565 | 5.50000 | 77 | |||||

| Interest rate swap contracts | ||||||||

| Euro | 89,250 | 4.45500 | (1,273 | ) | ||||

| Euro | 285,000 | 4.69500 | (5,855 | ) | ||||

| Euro | 55,000 | 4.73000 | (1,188 | ) | ||||

| Euro | 45,000 | 4.65250 | (918 | ) | ||||

| British pounds sterling | 28,855 | 5.81000 | (498 | ) | ||||

| U.S. dollar | 272,628 | 5.00000 | (8,034 | ) | ||||

| U.S. dollar | 27,788 | 4.96500 | (824 | ) | ||||

Forward exchange rate | ||||||||

| Foreign currency forward contracts | ||||||||

| Deutsche Mark/U.S. dollar | 304 | 2.29650 | 23 | |||||

| British pounds sterling/U.S. dollar | 3,992 | 1.45230 | 51 | |||||

Commodity Price Risk

We are exposed to commodity price risks through our dependence on various raw materials, such as chemical and energy prices. We seek to minimize these risks through our sourcing policies, operating procedures and pass through clauses in our product pricing agreements. We currently do not utilize derivative financial instruments to manage any remaining exposure to fluctuations in commodity prices.

Risk Identification and Analysis

The identification and analysis of risks relating to our operations is conducted through the application of an enterprise-wide risk management system, encompassing all of our activities worldwide. The goal of this risk management system is to foster a group-wide culture of risk management using a common set of objectives and standards in the measurement and treatment of risk. As with any risk management system, the results are based on individual assessments that may be subject to error. There is no guarantee that this system will consistently identify all of the important risks or provide an adequate assessment of their potential impact.

We are exposed to market risk through our commercial and financial operations as described above. We are implementing a policy of economic hedging against some of these exposures at present, but we may still incur losses as a result of changes in currency exchange rates, interest rates and commodity risk. We do not purchase or sell derivative financial instruments for trading purposes.

Our results as reported under IAS differ from our results as reconciled to U.S. GAAP, principally as a result of the different treatment under U.S. GAAP of:

- •

- allocation of purchase price to assets to be sold,

- •

- restructuring charges,

16

- •

- transaction costs incurred by our parent on our behalf

- •

- impairment of long lived assets

- •

- foreign currency gains and losses on borrowing costs directly attributable to construction

- •

- provisions for pensions and similar obligations, and

- •

- gains and losses related to financial instruments.

The significant differences between IAS and U.S. GAAP applicable to the historical financial statements are summarized below. Further discussion of significant differences between IAS and U.S. GAAP applicable to our historical financial statements are summarized in note 20 to our unaudited interim condensed consolidated financial statements contained in this document.

Three Months Ended September 31, 2001 Compared with Three Months Ended September 30, 2000

Net loss as reported under IAS was E41.3 million in third-quarter 2001 and E36.8 million as reconciled to U.S. GAAP, resulting in a reduction in net loss of E4.5 million as reconciled to U.S. GAAP. There were reconciling adjustments of E9.4 million in third quarter 2001 between IAS and U.S. GAAP relating to assets to be sold within one year of the date of the acquisition transaction. The remaining difference between net loss reported under IAS and net loss reported under U.S. GAAP is primarily due to the goodwill impact and thetax effect under U.S. GAAP associated with these adjustments.

In the third-quarter 2000, the net loss reported under IAS was E63.2 million and E58.9 million as reconciled to U.S. GAAP, resulting in a reduction in net loss of E4.3 million as reconciled to U.S. GAAP. During this period, the Group reported an impairment in accordance with IAS of E5.3 million related to a plant in Argentina, which is not impaired under U.S. GAAP. The remaining difference between net loss reported under IAS and net loss reported under U.S. GAAP is primarily due to financial instruments and to the tax effect under U.S. GAAP associated with these adjustments.

Five Months Ended September 30, 2001 and Four Months Ended April 30, 2001 Compared with Nine Months Ended September 30, 2000

Net loss as reported under IAS was E195.7 million in nine months ended September 2000 and E192.2 million as reconciled to U.S. GAAP, resulting in a reduction in net loss of E3.5 million as reconciled to U.S. GAAP. There were reconciling adjustments of E4.2 million in nine-months ended September 2000 between IAS and U.S. GAAP relating to property, plant and equipment. In addition, in the nine months ended September 2000 we recognized losses but not gains in the fair value of derivative financial instruments as required by IAS in effect prior to January 1, 2001. Under U.S. GAAP in effect prior to January 1, 2001, both the losses and gains on those instruments were recognized. This adjustment reflects the recognition of losses of E1.9 million in the nine month period ended September 2000. The remaining difference between net loss reported under IAS and net loss reported under U.S. GAAP is primarily due to the tax effect associated with these adjustments.

In the four-month period ended April 30, 2001 (prior to the acquisition transactions), the net loss reported under IAS and U.S. GAAP was E13.5 million with no significant differences.

In the five-month period ended September 30, 2001, the net loss reported under IAS was E56.2 million and E52.9 million as reconciled to U.S. GAAP, resulting in a reduction in net loss of E3.3 million as reconciled to U.S. GAAP. During this period, there were reconciling adjustments of E8.2 million between IAS and U.S. GAAP relating to assets to be sold within one year of the date of the business combination. The remaining difference between net loss under IAS and net loss reported under U.S. GAAP is primarily due to the goodwill impact and the tax effect under U.S. GAAP associated with these adjustments.

17

MESSER GRIESHEIM HOLDING AG ("SUCCESSOR")

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Amounts in E thousands, unless otherwise stated)

| | Successor July 1, 2001 to September 30, 2001 | Predecessor July 1, 2000 to September 30, 2000 | |||

|---|---|---|---|---|---|

| Net sales | 393,565 | 397,680 | |||

| Cost of sales | (206,074 | ) | (183,281 | ) | |

| Gross profit | 187,491 | 214,399 | |||

| Distribution and selling costs | (112,395 | ) | (153,242 | ) | |

| Research and development costs | (4,577 | ) | (8,323 | ) | |

| General and administrative costs | (28,669 | ) | (31,704 | ) | |

| Other operating income | 8,685 | 9,548 | |||

| Other operating expense | (20,505 | ) | (1,632 | ) | |

| Impairment of intangible assets and property, plant and equipment | — | (32,319 | ) | ||

| Restructuring and reorganisation charges | (4,997 | ) | — | ||

| Operating profit (loss) | 25,033 | (3,273 | ) | ||

| Equity method investments income, net | 2,676 | 1,379 | |||

| Other investment income/(expense), net | 3,088 | (11,842 | ) | ||

| Interest expense, net | (40,127 | ) | (25,470 | ) | |

| Changes in fair value of subsidiaries available for sale | (9,426 | ) | — | ||

| Other financial income, net | 1,232 | 2,020 | |||

| Non-operating expense | (42,557 | ) | (33,913 | ) | |

| Loss from disposal of discontinuing operations, net | — | (41,815 | ) | ||

| Loss before income taxes and minority interests | (17,524 | ) | (79,001 | ) | |

| Income tax benefit/(expense) | (20,914 | ) | 18,162 | ||

Loss before minority interests | (38,438 | ) | (60,839 | ) | |

Minority interests, net of income taxes | (2,868 | ) | (2,368 | ) | |

| Net loss | (41,306 | ) | (63,207 | ) |

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

18

MESSER GRIESHEIM HOLDING AG ("SUCCESSOR")

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Amounts in E thousands, unless otherwise stated)

| | | Predecessor | |||||

|---|---|---|---|---|---|---|---|

| | Successor May 1, 2001 to September 30, 2001 | ||||||

| | January 1, 2001 to April 30, 2001 | January 1, 2000 to September 30, 2000 | |||||

| Net sales | 659,538 | 574,463 | 1,244,934 | ||||

| Cost of sales | (336,171 | ) | (293,414 | ) | (600,426 | ) | |

| Gross profit | 323,367 | 281,049 | 644,508 | ||||

| Distribution and selling costs | (191,962 | ) | (177,182 | ) | (433,723 | ) | |

| Research and development costs | (6,748 | ) | (6,599 | ) | (18,942 | ) | |

| General and administrative costs | (47,514 | ) | (45,027 | ) | (107,993 | ) | |

| Other operating income | 9,498 | 10,242 | 24,176 | ||||

| Other operating expense | (26,623 | ) | (11,133 | ) | (21,034 | ) | |

| Impairment of intangible assets and property, plant and equipment | — | (2,356 | ) | (77,852 | ) | ||

| Restructuring and reorganisation charges | (9,255 | ) | (2,540 | ) | — | ||

| Operating profit | 50,763 | 46,454 | 9,140 | ||||

| Equity method investments expense, net | (5,302 | ) | (5,106 | ) | (163,303 | ) | |

| Other investment expense, net | (2,199 | ) | (4,544 | ) | (9,860 | ) | |

| Interest expense, net | (64,270 | ) | (36,364 | ) | (66,184 | ) | |

| Changes in fair value of subsidiaries available for sale | (8,192 | ) | — | — | |||

| Other financial expense, net | (656 | ) | (6,990 | ) | (93 | ) | |

| Non-operating expense | (80,619 | ) | (53,004 | ) | (239,440 | ) | |

| Loss from disposal of discontinuing operations | — | — | (17,120 | ) | |||

| Loss before income taxes and minority interests | (29,856 | ) | (6,550 | ) | (247,420 | ) | |

| Income tax benefit/(expenses) | (21,772 | ) | (4,813 | ) | 57,331 | ||

| Loss before minority interests | (51,628 | ) | (11,363 | ) | (190,089 | ) | |

| Minority interests, net of income taxes | (4,580 | ) | (2,135 | ) | (5,653 | ) | |

| Net loss | (56,208 | ) | (13,498 | ) | (195,742 | ) | |

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

19

MESSER GRIESHEIM HOLDING AG ("SUCCESSOR")

UNAUDITED INTERIM CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in E thousands, unless otherwise stated)

| | Successor | Predeccessor | |||||

|---|---|---|---|---|---|---|---|

| | As of September 30, 2001 | As of April 30, 2001 | As of December 31, 2000 | ||||

| Assets | |||||||

| Intangible assets | 750,418 | 126,190 | 130,817 | ||||

| Property, plant and equipment | 1,543,012 | 2,030,500 | 2,020,823 | ||||

| Equity method investments | 61,553 | 42,510 | 47,616 | ||||

| Cost method and other investments | 96,469 | 119,064 | 120,683 | ||||

| Deferred tax assets | 89,239 | 57,255 | 64,549 | ||||

| Other long-term receivables, net and other assets | 56,398 | 9,231 | 11,031 | ||||

Non-current assets | 2,597,089 | 2,384,750 | 2,395,519 | ||||

Inventories | 85,301 | 110,563 | 94,803 | ||||

| Trade accounts receivable, net | 306,432 | 322,844 | 320,031 | ||||

| Investments in subsidiaries available for sale | 64,723 | — | — | ||||

| Other receivables and other assets | 83,625 | 145,587 | 115,015 | ||||

| Cash and cash equivalents | 258,330 | 226,573 | 50,403 | ||||

Current assets | 798,411 | 805,567 | 580,252 | ||||

Total assets | 3,395,500 | 3,190,317 | 2,975,771 | ||||

Stockholders` equity and liabilities | |||||||

| Issued capital and reserves | 967,180 | 434,484 | 434,484 | ||||

| Accumulated deficit | (67,388 | ) | (93,327 | ) | (80,164 | ) | |

| Cumulative translation adjustment | (23,257 | ) | 87,726 | 84,204 | |||

Stockholders` equity | 876,535 | 428,883 | 438,524 | ||||

Minority interests | 88,988 | 87,021 | 86,594 | ||||

Provisions for pensions and similar obligations | 142,312 | 141,793 | 139,230 | ||||

| Other provisions | 75,727 | 71,949 | 76,522 | ||||

| Corporate debt, less current portion | 1,510,076 | 1,334,157 | 1,215,501 | ||||

| Deferred tax liabilities | 87,709 | 65,732 | 64,033 | ||||

| Other long-term liabilities | 27,700 | 25,892 | 22,715 | ||||

Non-current liabilities | 1,843,524 | 1,639,523 | 1,518,001 | ||||

Other provisions | 101,742 | 113,993 | 177,711 | ||||

| Corporate debt | 233,253 | 616,833 | 483,426 | ||||

| Trade accounts payable | 112,092 | 130,440 | 143,533 | ||||

| Miscellaneous liabilities | 139,366 | 106,662 | 127,982 | ||||

Current liabilities | 586,453 | 967,928 | 932,652 | ||||

Advance towards capital contribution | — | 66,962 | — | ||||

Total stockholders` equity and liabilities | 3,395,500 | 3,190,317 | 2,975,771 | ||||

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

20

MESSER GRIESHEIM HOLDING AG ("SUCCESSOR")

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY

(Amounts in E thousands, unless otherwise stated)

| | Predecessor | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | Subscribed capital | Additional paid-in capital | Accumulated deficit | Cumulative translation adjustment | Total stockholders` equity | ||||||

| Balance as of January 1, 2001 | 276,098 | 158,386 | (80,164 | ) | 84,204 | 438,524 | |||||

IAS 39 transition adjustment | — | — | 335 | — | 335 | ||||||

| Net loss | — | — | (13,498 | ) | — | (13,498 | ) | ||||

| Translation adjustment | — | — | — | 3,522 | 3,522 | ||||||

| Balance as of April 30, 2001 | 276,098 | 158,386 | (93,327 | ) | 87,726 | 428,883 | |||||

| | Successor | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | Subscribed capital | Additional paid-in capital | Accumulated deficit | Cumulative translation adjustment | Total stockholders` equity | ||||||

| Balance as of May 1, 2001 | 90 | 967,090 | 0 | 0 | 967,180 | ||||||

| Change in fair value of derivative financial instruments | — | — | (11,180 | ) | — | (11,180 | ) | ||||

| Net loss | — | — | (56,208 | ) | — | (56,208 | ) | ||||

| Translation adjustment | — | — | — | (23,257 | ) | (23,257 | ) | ||||

| Balance as of September 30, 2001 | 90 | 967,090 | (67,388 | ) | (23,257 | ) | 876,535 | ||||

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

21

MESSER GRIESHEIM HOLDING AG ("SUCCESSOR")

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(Amounts in E thousands, unless otherwise stated)

| | Successor | | | ||||||

|---|---|---|---|---|---|---|---|---|---|

| | Predecessor | ||||||||

| | Five-months ended September 30, 2001 | ||||||||

| | Four-months ended April 30, 2001 | Nine-months ended September 30, 2000 | |||||||

| Loss before income taxes and minority interests | (29,856 | ) | (6,550 | ) | (247,420 | ) | |||

| Income taxes (paid) refunded | (8,147 | ) | 6,964 | 11,944 | |||||

| Results of discontinuing operations | — | — | 17,120 | ||||||

| Depreciation and amortization of property, plant and equipment and intangible assets | 111,011 | 76,923 | 241,919 | ||||||

| Changes in fair value of subsidiaries available for sale | 8,192 | — | — | ||||||

| Reversal of write-down of property, plant and equipment and investments | — | — | (1,026 | ) | |||||

| Losses/gains on disposals of property, plant and equipment and investments | — | 7,186 | (13,706 | ) | |||||

| Non-cash changes in equity method investments | 31,396 | (5,106 | ) | 41,056 | |||||

| Interest expense, net | 64,270 | 36,364 | 66,184 | ||||||

| Other financial expenses, net | 656 | 6,990 | 93 | ||||||

| Changes in inventories | 8,726 | (10,474 | ) | (13,458 | ) | ||||

| Changes in receivables and other assets | 20,692 | (25,464 | ) | (18,442 | ) | ||||

| Changes in provisions | (29,150 | ) | (68,752 | ) | 126,398 | ||||

| Changes in accounts payable and other liabilities | 7,349 | (26,991 | ) | (43,618 | ) | ||||

Cash flow from (used in) operating activities | 185,139 | (8,910 | ) | 167,044 | |||||

Purchases of property plant and equipment and intangible assets | (47,979 | )(1) | (49,467 | ) | (180,928 | ) | |||

| Purchases of investments and loans to related parties | (60,973 | ) | (35,429 | ) | (71,926 | ) | |||

| Proceeds from the sales of property plant and equipment and intangible assets | 30,916 | 68 | 26,887 | ||||||

| Proceeds from the sales of investments | 19,630 | 13,746 | 23,989 | ||||||

| Interest received | 12,293 | 5,086 | 6,398 | ||||||

Cash flow used in investing activities | (46,113 | ) | (65,996 | ) | (195,580 | ) | |||

Capital increases | 30 | 66,962 | — | ||||||

| Net proceeds from additions to non-current corporate debt | 553,747 | 118,656 | 82,961 | ||||||

| Net (repayment of) proceeds from current corporate debt | (547,277 | ) | 133,407 | 27,600 | |||||

| Dividends paid | — | (4,012 | ) | — | |||||

| Interest paid | (47,300 | ) | (60,469 | ) | (72,582 | ) | |||

| Increase in cash collateral | (47,400 | ) | — | — | |||||

| Other financial expenses, net | (656 | ) | (6,990 | ) | (93 | ) | |||

| Cash flow from (used in) financing activities | (88,856 | ) | 247,554 | 37,886 | |||||

| Cash flow from operating, investing and financing activities activities | 50,170 | 172,648 | 9,350 | ||||||

| Effect of exchange rate changes on cash | (3,601 | ) | 3,522 | 2,201 | |||||

| Cash balances included in investments in subsidiaries available for sale | (14,812 | ) | — | — | |||||

| Changes in cash and cash equivalents | 31,757 | 176,170 | 11,551 | ||||||

| Cash and cash equivalents | |||||||||

| at beginning of reporting period | 226,573 | 50,403 | (2) | 47,718 | |||||

| at end of reporting period | 258,330 | 226,573 | 59,269 | ||||||

Supplemental cash flow information: | |||||||||

| Non-cash financing and investing activities | |||||||||

| Transfer of Cutting & Welding Division | — | — | 37,912 | ||||||

| Fair value of assets acquired in acquisitions, other than cash | 2,732,025 | — | — | ||||||

| Fair value of liabilities assumed in acquisitions | 2,734,628 | — | — | ||||||

| Increase in stockholders' equity | 967,180 | — | — | ||||||

- (1)

- Exclusive of commitments for capital expenditures of E26.2 million at September 30, 2001.

- (2)

- Cash and cash equivalents existing as of April 30, 2001 in the Predecessor financial statements is reflected as cash and cash equivalents at the beginning of the period. No other cash was transferred at the time of acquisition (see note 3).

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

22

MESSER GRIESHEIM HOLDING AG

NOTES TO UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts in E thousands, unless otherwise stated)

1. Background and basis of presentation

Messer Griesheim Holding AG ("the Company" or "Successor") is a supplier of industrial gases. The Company produces and markets industrial gases (including oxygen, nitrogen, argon, helium, carbon dioxide, hydrogen and rare and high-purity gases), gas application processes and customer-site gas production systems. The Company's primary customers include major industrial, chemical and pharmaceutical manufacturers, and the food processing and waste treatment industries.

The Successor, incorporated on November 6, 1996, was a dormant company until April 30, 2001, when it was activated to become the holding company for the shares of Messer Griesheim GmbH ("MGG" or "Predecessor"). As of December 31, 2000, the Successor had net assets aggregating E44.9, represented by current assets of E50.7 and current liabilities of E5.8. The Predecessor was recapitalized to effect the acquistion transactions discussed in note 3. As discussed in note 3, the acquisition transactions have been accounted for at fair value and, accordingly, the assets and liabilities of the Group have been recorded at their estimated fair values as of April 30, 2001, the date of the acquisition transactions. As a result, the financial statements of the Group for periods prior to the acquisition are not comparable to the Group's financial statements for periods subsequent to the acquisition. To highlight this lack of comparability, a solid line has been inserted, where applicable, to distinguish information pertaining to the pre-acquisition and post-acquisition periods. The refinancing transactions and the divestiture program adopted by the Group are described in notes 4 and 10, respectively.

The unaudited condensed consolidated financial statements have been prepared in accordance with International Accounting Standards ("IAS") as adopted by the International Accounting Standards Board (formerly known as the International Accounting Standards Committee or "IASC"), and include the accounts of all companies which the Successor or Predecessor controls (collectively, "the Messer Group", "Messer" or "the Group").

The condensed consolidated financial statements include, in the opinion of management, all adjustments of a normal, recurring nature necessary to present fairly the financial position, results of operations and cash flows for the periods presented. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with IAS have been condensed or omitted. These condensed consolidated financial statements should be read in conjunction with the Predecessor's December 31, 2000 financial statements and notes thereto. The results of operations for the interim 2001 periods presented are not necessarily indicative of the operating results to be expected for the full year.

The preparation of condensed consolidated financial statements in conformity with IAS requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of financial statements, and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Additionally, as discussed in note 3, the allocation of the purchase price in the acquisition transactions to the assets acquired and liabilities assumed is preliminary, and certain revisions to such allocation may be necessary upon completion of the allocation process.

Certain reclassifications have been made to the presentation of prior periods to conform to the current period classification.

23

2. New IAS accounting standards

The Group has adopted each of the following standards effective January 1, 2001. Unless otherwise stated, adoption of these standards did not have a material impact on the Group's financial position or results of operations.

In 1998 the IASC issued IAS 39"Financial Instruments: Recognition and Measurement". IAS 39 was effective for fiscal periods beginning after December 31, 2000. The standard significantly increases the use of fair values in accounting for financial instruments. In addition, it establishes specific criteria relating to hedge accounting. Adoption of this standard on January 1, 2001 resulted in a E335 cumulative effect of change in accounting principles, net of deferred taxes totaling E223.

In 2000 the IASC revised IAS 19"Employee Benefits". IAS 19 (revised 2000) was effective for fiscal periods beginning on or after January 1, 2001. The standard changes the definition of plan assets and introduces recognition, measurement and disclosure requirements for reimbursements.

3. Acquisition transactions

On December 31, 2000, Aventis S.A. (parent company to Hoechst AG ("Hoechst")) entered into an agreement with Allianz Capital Partners ("ACP") and six private equity funds managed by affiliates of The Goldman Sachs Group, Inc. (the "GS Funds"), regarding the purchase of Hoechst's shares in MGG. The transaction was consummated on April 30, 2001.

In order to facilitate the purchase of Hoechst's shares in MGG by ACP and the GS Funds, Hoechst transferred its 662/3% share interest in MGG to the Company on April 30, 2001. In addition, on the same date Messer Industrie GmbH ("MIG") transferred its 331/3% equity interest in MGG to the Company for nominal cash and a 331/3% equity interest in the Company. As explained in the following paragraph, 100% of the Company was then immediately acquired by Messer Griesheim Group GmbH.

ACP and the GS funds formed a new company, Messer Griesheim Group GmbH. On April 30, 2001, through Messer Griesheim Group GmbH, ACP and the GS Funds acquired Hoechst's share of the Company for E618 million, payable in cash (E388 million) and deferred notes (E230 million). The E230 million note is due from Messer Griesheim Group GmbH on November 11, 2011, together with interest which, although not currently payable, will accrue thereon at a rate of 250 basis points above the three month EURIBOR. In certain circumstances, the deferred purchase price may be payable earlier. Further, Hoechst has been issued 300,000 bonds (E300) which are convertible into 3% of the equity shares of Messer Griesheim Group GmbH upon the occurrence of certain events at a nominal conversion price. In addition, MIG transferred its share in the Company for a 32.67% share in Messer Griesheim Group GmbH and cash of E33.2 million. MIG is also entitled to receive additional cash consideration of up to E35.8 million upon the occurrence of certain events. As a result of the foregoing transactions, the Company is 100% owned by Messer Griesheim Group GmbH, which in turn is owned by ACP (33.665%), the GS Funds (collectively 33.665%) and Messer Industrie GmbH (32.67%).

Also as a result of the foregoing transactions, the Company owns 100% of MGG.

The foregoing transactions have been accounted for in a manner similar to an acquisition of MGG. Accordingly, the purchase consideration for the acquisition transaction has been allocated to the

24

assets acquired and liabilities assumed as of April 30, 2001, the date of consummation of the transactions, based on their estimated fair values. The Company has engaged the services of an outside specialist to assist in allocating its purchase price, and the results of the outside specialist's work is not expected to be complete until early 2002. Finalization of the purchase price allocation, which is expected to be completed within one year from April 30, 2001, may result in certain adjustments to such allocations. The initial purchase price allocation was as follows:

| Cash paid and notes issued to Aventis/Hoechst | 618,000 | ||

| Cash paid and equity issued to Messer Industrie | 349,180 | ||

| 967,180 | |||

| Current assets (including cash of E226,573) | 805,567 | ||

| Non-current assets, including other intangibles | 2,153,031 | ||

| Goodwill | 743,210 | ||

| Total assets | 3,701,808 | ||

| Current liabilities | 1,012,253 | ||

| Non-current liabilities | 1,722,375 | ||

| Equity | 967,180 | ||

| Total liabilities and equity | 3,701,808 | ||

Goodwill represents the excess of the cost of the acquisition transaction over the fair value of the assets acquired and liabilities assumed. Goodwill arising from the acquisition transaction is being amortized on a straight-line basis over an estimated useful life of 15 years.

4. Financing transactions

Refinancing transactions

Pursuant to the debt covenants, a substantial portion of MGG's existing debt became due and payable upon the change in control, which occurred on April 30, 2001 (see note 3). As a result, MGG entered into refinancing transactions with a consortium of banks during April and May 2001. The refinancing transactions involved borrowings under a senior facilities agreement with aggregate available funds of E1,650 million (E1,340 million of term loan facilities and E310 million under a revolving facility), and a mezzanine bridge facility in the aggregate amount of E400 million.

The amounts borrowed under the refinancing agreement (E1,160.32 million) and under the mezzanine bridge facility (E400 million) were used to repay MGG's existing debt obligations of E1,302.86 million. As the existing debt was repaid in connection with the acquisition transactions, the prepayment penalties aggregating E19.1 million have been reflected as part of the purchase accounting adjustments. No part of the existing debt or the refinanced debt was used to finance the acquisition transactions. Refinancing costs of E91.0 million were capitalized, and are being amortized over the period of maturities of the borrowings using the effective interest rate method.

25

The senior facilities agreement contains certain covenants that require MGG, among other things, to maintain certain specified financial ratios, to observe capital expenditure limits, and to ensure that the combination of the repayment of the senior term disposal facility and the assumption of indebtedness by third parties in connection with the divestment of assets will result in the reduction of the aggregate indebtedness of MGG and its consolidated subsidiaries by at least E255 million by April 2003.

Senior Notes

On May 16, 2001, the Company issued E550 million principal amount of 10.375% Senior Notes maturing on June 1, 2011. At any time prior to June 1, 2006, the Company may redeem all but not part of the Senior Notes at a redemption price equal to 100% of the principal amount thereof, plus a redemption premium and unpaid interest, and special interest, if any, to the redemption date. At any time on or after June 1, 2006, the Company may redeem all or part of the Senior Notes at specific redemption prices, expressed as percentages of the principal amount, accrued and unpaid interest, special interest, if any, and additional amounts, if any, to the applicable redemption date on a sliding scale. In addition, prior to June 1, 2004, the Company may redeem up to 35% of the Senior Notes with the proceeds of one or more public equity offerings of its or its parent company's equity at a redemption price equal to 110.375% of the principal amount of the Senior Notes redeemed.