Use these links to rapidly review the document

TABLE OF CONTENTS

Filed Pursuant to Rule 424(b)(3)

Registration Number 333-73020

PROSPECTUS SUPPLEMENT

(To Prospectus dated May 9, 2002)

Messer Griesheim Holding AG

10.375% Senior Notes Due 2011

Attached hereto and incorporated by reference herein are those sections of our Form 6-K relating to our financial results for the three month period ended March 31, 2002. This Prospectus Supplement is not complete without, and may not be delivered or utilized except in connection with, the Prospectus, dated May 9, 2002, with respect to the 10.375% Senior Notes Due 2011, including any amendments or supplements thereto.

Investing in the notes involves a high degree of risk. See "Risk Factors" beginning on page 14 of the accompanying Prospectus for a discussion of certain factors that you should consider in connection with an investment in the notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these notes or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

This prospectus has been prepared for and will be used by Goldman, Sachs & Co. and Goldman Sachs International in connection with offers and sales of the notes in market-making transactions. These transactions may occur in the open market or may be privately negotiated, at prices related to prevailing market prices at the time of sale or at negotiated prices. Goldman, Sachs & Co. and Goldman Sachs International may act as principal or agent in these transactions. Messer Griesheim will not receive any of the proceeds of such sales of the notes.

Goldman, Sachs & Co.

Goldman Sachs International

May 30, 2002

In this document:

"Messer Holding", "the Company", "we", "us" and "our" refers to Messer Griesheim Holding AG and, unless the context otherwise requires, its consolidated subsidiaries;

"Messer Griesheim" refer to the Messer Griesheim Holding AG's subsidiary, Messer Griesheim GmbH, which is the operating company whose business and results of operations are described in this Form 6-K, including, unless the context otherwise requires, its consolidated subsidiaries;

"Messer Griesheim Group" and "the Group" refer to the parent of Messer Griesheim Holding AG, Messer Griesheim Group GmbH & Co. KGaA, a German Partnership limited by shares, or Messer Griesheim Group GmbH prior to its conversion on November 1, 2001 to Messer Griesheim Group GmbH & Co. KGaA;

"Messer Employee GmbH" refers to Messer Employee GmbH & Co. KG, a company through which employees participating on our share purchase and option plan are to hold shares in Messser Griesheim Group.

"Messer Industrie" and "MIG" refers to Messer Industrie GmbH, a holding company for the Messer family's minority interest in Messer Griesheim Group.

2

REPORT FOR THE THREE MONTH PERIOD ENDED MARCH 31, 2002

The accounts being reported on are the consolidated results of Messer Griesheim Holding AG. Our obligation to file this report with The Bank of New York (the "Trustee"), for the benefit of our noteholders, and the U.S. Securities and Exchange Commission arises under the indenture, dated as of May 16, 2001, between the Company and the Trustee, pursuant to which the Company has issued its 10.375% Senior Notes due 2011.

This document includes forward-looking statements. We have based these forward-looking statements on our current expectations and projections about future events. Although we believe that our expectations are based on reasonable assumptions, we cannot assure you that actual results will not be materially different from our expectations. Factors that could cause our actual results to differ materially from our expectations include, among other things:

- •

- the amount of proceeds that we realize from our divestiture program;

- •

- the timing of the receipt of proceeds that we realize from our divestiture program;

- •

- the amount of savings in operational costs that Messer Griesheim is able to achieve as a result of its cost-savings program;

- •

- the costs of implementing Messer Griesheim's cost-savings program;

- •

- the timing to achieve benefits of our cost-savings program;

- •

- anticipated trends and conditions in our industry, including regulatory developments;

- •

- our capital needs; and

- •

- our ability to compete.

We are under no obligation to update or revise publicly any forward-looking statement. The forward-looking events discussed in this document might not happen. In addition, you should not interpret statements regarding past trends or activities as promises that those trends or activities will continue in the future. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by this cautionary statement and the more detailed discussion of risks in the section entitled "Risk Factors" of the Company's Post-Effective Amendment No. 1 to its Registration Statement on Form F-4 filed with the Securities and Exchange Commission on April 30, 2002. Some numbers that appear in this document (including percentage amounts) have been rounded. Numbers in tables may not sum precisely to the totals shown due to rounding.

Investors are cautioned that forward-looking statements contained in this section involve both risk and uncertainty. Several important factors could cause actual results to differ materially from those anticipated by these statements. Many of these statements are macroeconomic in nature and are, therefore, beyond the control of management.

We are a producer and distributor of industrial gases, including oxygen, nitrogen, argon, helium, carbon dioxide, hydrogen, helium, specialty gases and acetylene. The industrial gases we produce are used in a broad range of industries, such as the industrial, chemical and pharmaceutical manufacturers, and the food processing and waste treatment industries.

3

MANAGEMENT'S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion in conjunction with the Company's unaudited interim condensed consolidated financial statements included elsewhere herein. The Company's financial statements are prepared in accordance with the International Accounting Standards of the International Accounting Standards Board, or IAS, which differ in certain significant respects from U.S. GAAP. You can find reconciliations of net income, and shareholders' equity and disclosures regarding differences between IAS and U.S. GAAP in note 19 to the Company's unaudited interim condensed consolidated financial statements.

The Company calculates normalized EBITDA as operating profit before depreciation and amortization, after adding back charges for impairment of intangible assets and property, plant and equipment, restructuring and reorganization charges.

Normalized EBITDA is not a measure recognized by IAS or U.S. GAAP. This and similar measures are used by different companies for differing purposes and are often calculated in ways that reflect the unique situations of those companies. We urge you to be very cautious in comparing our normalized EBITDA data to the EBITDA data of other companies. Normalized EBITDA is not a substitute for operating profit as a measure of operating results. Likewise, normalized EBITDA is not a substitute for cash flow as a measure of liquidity.

We operate in 48 countries through more than 419 facilities, including production plants, distribution and filling stations and research centers. We have an estimated global market share of approximately 5% of the total industrial gases market, making us the seventh largest industrial gas producer worldwide, and leading market shares in Germany and certain other countries in central and eastern Europe. We also have strong businesses in selected industrial areas of the United States and in selected niche markets in other Western European countries. In the first quarter 2002, we generated net sales of EURO386.4 million and normalized EBITDA of EURO97.3 million.

Our primary or core markets are Europe and North America. Our two largest markets, Germany and North America, collectively accounted for 65.0% of our net sales and 74.5% of our normalized EBITDA for the first quarter 2002. Within each of our geographic markets, we generally organize our business based upon how we deliver industrial gases to our customers: delivery of large volumes from on-site production facilities or by pipeline, delivery in bulk tanks transported by truck or rail and delivery in gas cylinders. In addition to our core markets of Europe and North America, we also operate in Asia, Africa and Latin America. We are in the process of divesting substantially all of the assets outside our core markets, along with certain non-strategic assets in our core markets. Other than our joint ventures in China, we anticipate completing these divestitures by year end 2002.

Acquisition Transactions, Refinancing and Divestiture Program

As discussed elsewhere in this document, the acquisition transactions have been accounted for at fair value and, accordingly, our assets and liabilities have been recorded at their estimated fair values as of April 30, 2001, the date of the acquisition transactions. As a result, the financial statements of Messer Griesheim for periods prior to the acquisition transactions are not comparable to our financial statements for periods subsequent to the acquisition transactions. To highlight this lack of comparability, a solid vertical line has been inserted, where applicable, between columns in the tables and schedules of this document, and in our unaudited interim condensed consolidated financial statements to distinguish information pertaining to the pre-acquisition and post-acquisition periods.

4

The Acquisition of Messer Griesheim

Prior to the completion of the acquisition transactions described below, Messer Griesheim was owned:

- •

- 331/3% by the Messer family through a holding company, Messer Industrie GmbH, and

- •

- 662/3% by Hoechst AG, a subsidiary of Aventis S.A. Aventis was formed in December 1999 as the result of the merger of Hoechst AG and Rhône-Poulenc S.A., two of Europe's largest chemical companies.

On December 31, 2000, Messer Industrie, Hoechst and our parent company Messer Griesheim Group GmbH (formerly named Cornelia Verwaltungsgesellschaft mbH), entered into certain acquisition transactions.

As a result of the acquisition transactions, Messer Holding owns 100% of Messer Griesheim and Messer Holding is directly or indirectly wholly owned by Messer Griesheim Group. Messer Holding and Messer Griesheim Group are both holding companies with no material assets other than their direct or indirect interests in Messer Griesheim (and, in Messer Holding's case, the payments under the intercompany loan to Messer Griesheim). During the three month period ended March 31, 2002, our employees purchased shares through the share purchase and option plan. They hold their shares through Messer Employee GmbH & Co. KG. Consequently, Messer Griesheim Group is owned as of March 31, 2002:

- •

- 32.18% by the Messer family, through Messer Industrie;

- •

- 33.17% by Allianz Capital Partners;

- •

- 33.17% by six private equity funds managed by affiliates of The Goldman Sachs Group, Inc.; and

- •

- 1.48% by Messer Employee GmbH & Co. KG reflecting ownership interests of our employee participants in the share purchase and option plan.

In connection with these acquisition transactions, the main shareholders of Messer Griesheim Group entered into a shareholders' agreement governing their respective voting control and other ownership rights with respect to the issuer and Messer Griesheim.

Due to certain antitrust related considerations relating to the equity interest of Allianz AG in a competitor of Messer Griesheim, the agreement generally allocates the rights of the financial sponsors relating to corporate governance and management to the GS Funds until such time as the antitrust related considerations are no longer relevant. Accordingly, until then, members of the shareholders' committee appointed by the GS Funds will represent all votes of the financial sponsors constituting 66.34% of all votes in the shareholders' committee. Thereafter, the rights will be shared by Allianz Capital Partners and the GS Funds, with Allianz Capital Partners having a deciding vote in the event of a lack of consensus between Allianz Capital Partners and the GS Funds, subject to certain exceptions.

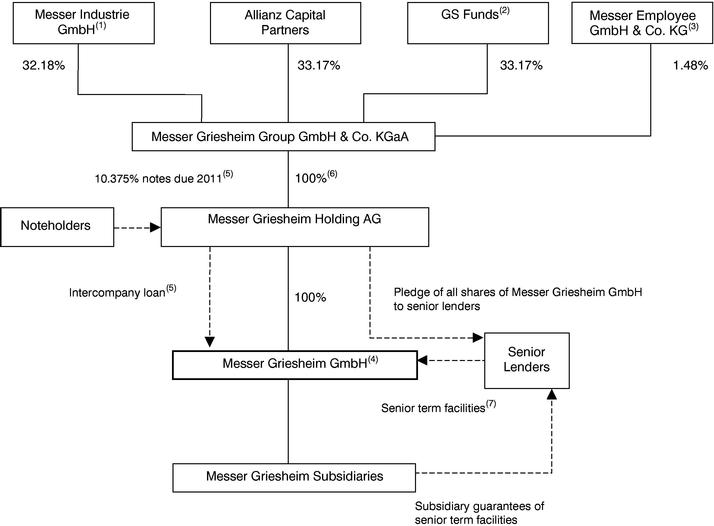

Transaction Structure

The following diagram shows our ownership structure and the structure of our principal indebtedness as of March 31, 2002 following completion of the acquisition transactions on or about April 30, 2001, reflecting the issuance of the senior notes and the refinancing or repayment of our indebtedness to the extent completed, including repayment in full of the EURO400 million mezzanine bridge facility and repayment of EURO115 million of our senior term facilities and subsequent share purchases by our employees through the share purchase and option plan mentioned above.

5

- (1)

- The holding company for the Messer family's interests in Messer Griesheim.

- (2)

- Certain private equity funds managed by affiliates of The Goldman Sachs Group, Inc.

- (3)

- The employees participating in the stock option plan hold their shares through Messer Employee GmbH & Co. KG. The participant's voting rights are exercised by the managing partner of this company.

- (4)

- Principal operating company in Germany and holding company for the remainder of our operations.

- (5)

- EURO550.0 million aggregate principal amount.

- (6)

- Messer Griesheim Group owns 100% of Messer Holding, 33.33% of which is owned directly and 66.67% of which is owned through the wholly owned subsidiary DIOGENES 20. Vermögensverwaltung GmbH.

- (7)

- EURO1,340 million was the initial aggregate amount of senior term loan facilities. Messer Griesheim GmbH repaid EURO115 million principal amount of senior term facilities on or about May 16, 2001 with a portion of the proceeds from the sale of the senior notes. As of March 31, 2002, EURO922.9 million aggregate principal amount remained outstanding under the senior term facilities. The senior term facilities also include committed but undrawn funds totaling EURO297 million under revolving facilities. Certain of Messer Griesheim's subsidiaries are also direct borrowers under the senior term facilities.

Refinancing Program

In connection with the acquisition transactions described above, substantially all of Messer Griesheim's existing indebtedness was refinanced through the senior term facilities and the senior notes. Upon the initial closing of the acquisition, Messer Griesheim entered into a senior term

6

facilities agreement with aggregate available funds of EURO1,650 million ( EURO1,340 million of term loan facilities and EURO310 million of revolving facilities) and a mezzanine bridge facility agreement in the aggregate amount of EURO400 million. On May 16, 2001, the Company issued EURO550 million principal amount of 10.375% senior notes maturing on June 1, 2011. Upon the closing of the sales of the senior notes, Messer Holding made an intercompany loan to Messer Griesheim with the gross proceeds from the senior notes, and Messer Griesheim used the intercompany loan to repay the mezzanine bridge facility in full and repay EURO115 million principal amount of the outstanding term borrowings under the facilities.

We believe the following selected business practices are important for a proper understanding of financial reporting risks.

Net Sales

We primarily earn revenues from:

- •

- sales of industrial gases and, to a lesser extent,

- •

- sales of hardware related to industrial gas usage.

Our sales of industrial gases, which amount to greater than 90% of our total revenue, are divided into three business units corresponding to their mode of delivery: on-site and pipeline sales, bulk delivery sales and cylinder delivery sales. Contracts in our on-site production and pipeline supply businesses in Europe and the United States typically have terms of 10 to 15 years and usually have "take-or-pay" minimum purchase provisions. In each of the last three years, the "take-or-pay" minimum purchase requirements in our on-site and pipeline supply contracts accounted for approximately 60% to 70% in Germany and 40% to 45% in the United States of the total amount of net sales that we generated under these contracts.

Contracts in our bulk business generally have terms of two to three years in Europe and five to seven years in the United States. Customers in our on-site and pipeline and bulk businesses have historically exhibited high renewal rates, with over 90% of customers whose contracts expired in the past five years renewing their contracts with us. Our on-site, pipeline and bulk businesses in Germany and the United States accounted for approximately 39% of our total net sales and approximately 51% of our normalized EBITDA in the first quarter 2002. We generally sell our cylinder gases by purchase orders or by contracts with terms ranging between one to two years in Europe and three to five years in the United States.

Our net sales are dependent on the economic conditions in the markets in which we operate. However, we believe that we have limited exposure to the cyclical nature in demand of any particular industry because of the wide diversity of industries represented by our customer base.

Although industrial gas prices appear to have recently stabilized in many of the markets in which we operate, prices have consistently decreased for at least the last 10 years, especially in the bulk and commodity gas cylinder segments, due to aggressive efforts by most producers to increase market share. The profit margin impact of this price erosion has been partially offset by efficiency improvements throughout the supply chain and regional consolidation among large participants in the industry, permitting economies of scale. In addition, new applications for industrial gases have increased sales volumes and profit margins.

7

Cost of Sales

Our principal raw material is air, which is free and which we separate into its component gases. Cost of sales principally consists of:

- •

- capital costs of plants;

- •

- costs of energy required for production; and

- •

- labor costs relating to production.

Energy costs consist principally of electrical power costs. Electricity represents approximately 27% of cost of sales in the first quarter of 2002. We are able to pass on a portion of increases in energy costs to many, but not all, of our on-site and pipeline customers with long-term supply contracts, although these adjustments in cost often occur only on an annual basis. The amount and other terms of these energy cost pass-through provisions vary by contract.

Labor costs relating to production consist principally of wages and salaries, social security contributions and other expenses related to employee benefits. Social security contributions include our portion of social security payments as well as our contributions to workers' insurance associations.

We depreciate fixed assets on a straight-line basis. Our depreciation rates assume a useful lives ranging from 10 to 50 years for buildings, 10 to 20 years for plant and machinery and 3 to 20 years for other plant, factory and office equipment.

Divestiture Program

Our core markets are Europe and North America. In May 2001, immediately following our change of ownership resulting from the acquisition transactions described elsewhere in this document, we adopted a divestiture program. Pursuant to the divestiture program, we intend to sell substantially all of our assets and operations in our non-core markets in Asia, Africa and Latin America, as well as certain non-strategic assets and operations in our core markets. The proceeds from this divestiture program will be used to reduce our consolidated debt.

Pursuant to the divestiture program, as of March 31, 2002, we have completed disposals of our home care business in Germany, our health care business in Canada and our non-cryogenic plant production operations in Germany, the United States, Italy and China. We also have completed disposals of our operations in Argentina, Brazil, Mexico, South Africa, South Korea and Venezuela, our nitric oxide business in Germany, our carbon dioxide business in the United States and our nitrogen services business in the United Kingdom. Subsequent to March 31, 2002 we disposed of our activities in Egypt and Trinidad & Tobago which enabled us to repay our senior term disposal facility.

The remaining divestiture of certain of our assets and operations may require additional expenditures prior to their disposal.

Cost-Savings Plan

We are implementing a plan to reduce our operating costs, principally in Europe. This plan involves eliminating duplication in support positions for certain process functions, reducing energy costs, centralizing key process functions and simplifying our management structure. We have identified most of the specific cost savings measures that we anticipate to achieve by year-end 2003. We expect that these measures will reduce the cost base of our operations in our core markets relative to its level for the year 2000 by approximately EURO100 million by year-end 2003. To implement these measures, we expect to spend in total approximately EURO84 million between April 30,

8

2001 and year end 2003, principally to be applied towards severance payments and efficiency improvements.

For the eight month period ended December 31, 2001, we have reduced the cost base of our operations in our core markets relative to its level for the year 2000 by EURO27.0 million. As a result of implementation of these measures, we incurred total one time costs of approximately EURO25.7 million (excluding EURO12.5 million of costs that were included as part of the purchase price accounting adjustments) for the eleven month period ended March 31, 2002, of which EURO0.4 million was recorded in the first quarter of 2002. We expect to incur an additional EURO46.2 million of one-time costs by year end 2003.

Critical Accounting Policies

The results of our operations and financial condition are dependent upon the utilization of accounting methods, assumptions and estimates that are used as a basis for the preparation of the unaudited interim condensed consolidated financial statements. We have identified the following critical accounting policies and related assumptions, estimates and uncertainties, which management believes are essential to understanding the underlying financial reporting risks and the impact that these accounting methods, assumptions, estimates and uncertainties have on our reported financial results. This information should be read in conjunction with the unaudited interim condensed consolidated financial statements.

Purchase Accounting

We accounted for the acquisition transactions similar to that of an acquisition of Messer Griesheim by Messer Holding. The accounting for this acquisition resulted in significant amount of long-lived intangible assets. Our accounting policy relating to purchase business combinations requires the use of the purchase method whereby the purchase price is allocated to identifiable tangible and intangible assets based upon their fair value. The allocation of purchase price is judgmental and requires the extensive use of estimates and fair value assumptions, which can have a significant impact on operating results. Changes in the industry conditions, technological advances and other economic factors could result in revisions to the judgments, estimates and valuation techniques utilized in the application of purchase accounting. Such differing allocations could impact future operating results.

Recoverability of Long-Lived Assets

Our business is capital intensive and, historically, required a significant investment in property, plant and equipment. At March 31, 2002, the carrying value of our property, plant and equipment was EURO1,676 million. At March 31, 2002 long-lived intangible assets amounted to EURO843 million. We review long-lived assets, including intangible assets, for impairment whenever events or changes in circumstances indicate that the carrying value of an asset may not be recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying value of an asset to future net cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment recognized is measured by the amount by which the carrying value of the assets exceeds the fair value of the assets. Estimated fair value is generally based on either appraised value or by discounted estimated future cash flows.

A continuation of the currently competitive economic conditions in the industrial gas industry could result in an increasingly adverse pricing environment due to significant industry over-capacity. This could result in decreased production and reduced capacity utilization. Such events could result in reductions of future estimates of net cash flows expected to be generated to the extent that both

9

long-lived tangible and intangible assets could be considered impaired, negatively impacting future operating results.

Recoverability of Investments in Subsidiaries Available for Sale

We have made a series of investments in, and advances to, companies that are principally engaged in the manufacture, sale and distribution of industrial gases which are located in regional markets which we no longer consider part of our core markets. At March 31, 2002, the carrying amounts of investments in subsidiaries available for sale aggregate EURO45 million. Our accounting policy is to record an impairment of such investments to net realizable value when the decline in fair value below carrying value is other than temporary. In determining if a decline in value is other than temporary, we consider the length of time and magnitude of excess of carrying value, the forecasted results of the investee, the economic environment in the regional market and our ability and intent to hold the investment.

A slump in demand for industrial gases could adversely impact the operations of these investments to generate future net cash flows. Furthermore, since these investments are not publicly traded, further judgments and estimates are required to determine their fair value. As a result, potential impairment charges to write-down such investments to net realizable value could adversely affect future operating results.

Realization of Deferred Tax Assets

At March 31, 2002, we had total deferred tax assets (net of valuation allowance) of approximately EURO193 million. Included in this total are the benefit of net operating loss and tax credit carry forwards of approximately EURO129 million. Such tax loss and credit carry forwards generally do not expire under current law, except certain amounts attributable to operations in the United States that expire in 20 years. Realization of these amounts are dependent upon the generation of future taxable income at a level sufficient to absorb the loss and credit carry forwards. These deferred tax assets were recognized to the extent that it is probable that future taxable profit will be available. The amount of total deferred tax assets considered realizable prospectively could be reduced if our estimates of projected future taxable income are lowered from present levels or changes in current tax regulations are revised which could impose restrictions on the time or extent of our ability to utilize tax loss and credit carry forwards in the future.

Restructuring Charges

Subsequent to the acquisition transactions, the management approved plans to restructure the Group and reduce costs. These changes were intended to, among other things, improve operational efficiencies and improve profitability. While the management approved a detailed restructuring plan, the calculation of the provision requires the use of estimates and management judgment. Additionally, if industry conditions continue to deteriorate or an economic downturn is experienced in the future, further restructuring charges may be incurred. Resulting variances from estimates previously utilized may adversely impact future financial results.

Reclassifications

Certain reclassifications have been made to the presentation of the prior period to conform to the current period classifications.

10

When comparing the three month periods ended March 31, 2002 and 2001, consideration should be given to the impact on comparability arising from the acquisition transaction, the refinancing program, the divestiture program and the other developments described above. As a result of these events, comparability is impacted by a number of factors, the most significant of which are (i) the new cost base of the Company's assets and liabilities as a result of the acquisition program, (ii) the refinancing program and the resulting impact on financing costs and (iii) the divestiture program. All of these factors impacted the results presented for the three month period ended March 31, 2002.

To highlight this lack of comparability, a solid vertical line has been inserted, where applicable, between columns in the tables below, in our interim condensed consolidated financial statements and elsewhere in this document in order to distinguish information pertaining to the pre-acquisition and post-acquisition periods.

Three Months Ended March 31, 2002 Compared with Three Months Ended March 31, 2001

The following table sets forth a summary of the results of operations for the three month periods ended March 31, 2002 and 2001, in terms of amounts as well as a percentage of net sales.

| | Three Months Ended March 31, 2002 Messer Griesheim Holding AG | Three Months Ended March 31, 2001 Messer Griesheim GmbH | |||||||

|---|---|---|---|---|---|---|---|---|---|

| | EURO (in millions) | % | EURO (in millions) | % | |||||

| Net sales | 386.4 | 100.0 | 435.1 | 100.0 | |||||

| Cost of sales | (194.6 | ) | (50.4 | ) | (220.8 | ) | (50.7 | ) | |

| Gross profit | 191.8 | 49.6 | 214.3 | 49.3 | |||||

| Distribution and selling costs | (117.6 | ) | (30.4 | ) | (135.1 | ) | (31.1 | ) | |

| General and administrative costs | (35.7 | ) | (9.2 | ) | (34.5 | ) | (7.9 | ) | |

| Other, net(1) | (10.4 | ) | (2.7 | ) | (10.7 | ) | (2.5 | ) | |

| Operating profit | 28.1 | 7.3 | 34.0 | 7.8 | |||||

| Interest expense, net | (35.2 | ) | (9.1 | ) | (25.1 | ) | (5.8 | ) | |

| Profit (loss) before income taxes and minority interests | (7.7 | ) | (2.0 | ) | (0.8 | ) | (0.2 | ) | |

| Income taxes | (3.2 | ) | (0.8 | ) | (3.9 | ) | (0.9 | ) | |

| Net loss | (13.4 | ) | (3.5 | ) | (6.7 | ) | (1.5 | ) | |

| Normalized EBITDA | 97.3 | 25.2 | 91.9 | 21.1 | |||||

- (1)

- Amounts include total net of research and development costs, other operating income, other operating expense and restructuring and reorganization charges.

11

Net sales. Net sales decreased 11.2% to EURO386.4 million in the first quarter 2002 from EURO435.1 million in the same period 2001 based essentially on the factors described below.

| | Three Months Ended March 31, 2002 Messer Griesheim Holding AG | Three Months Ended March 31, 2001 Messer Griesheim GmbH | ||

|---|---|---|---|---|

| | EURO (in millions) | EURO (in millions) | ||

| Net sales (Business Areas) | ||||

| Germany | 157.4 | 173.1 | ||

| Western Europe, excluding Germany | 66.2 | 64.2 | ||

| Eastern Europe | 54.0 | 53.5 | ||

| North America | 93.6 | 98.5 | ||

| Others | 14.1 | 45.4 | ||

| Reconciliation/Corporate | 1.1 | 0.4 | ||

| Total | 386.4 | 435.1 | ||

- •

- Net sales in Germany decreased 9.1% to EURO157.4 million in the first quarter 2002 from EURO173.1 million in the same period 2001. The first quarter 2001 included EURO7.2 million of sales from the disposed businesses Homecare and Mahler. Excluding this effect, net sales for Germany decreased by 5.1% or EURO8.5 million, of which EURO6.5 million resulted from our industrial gas business and the remainder of the decrease resulted from our specialty gas business subsidiary for the semiconductor industry. This decrease is due to lower demand caused by an overall downturn in the business climate in Germany.

- •

- Net sales in Western Europe (excluding Germany) increased 3.1% to EURO66.2 million in the first quarter 2002 from EURO64.2 million in the same period 2001. This increase is primarily due to higher sales volumes from our activities in Spain and Italy more than offsetting lower sales in Benelux and the United Kingdom. In the first quarter 2002, the region benefited from our entering into the cylinder business in Spain and increased bulk CO2 sales in Italy. Lower sales occurred in the United Kingdom due to a decline in the beverage business and in Benelux from the cylinder business.

- •

- Net sales in Eastern Europe increased 0.9% to EURO54.0 million in the first quarter 2002 from EURO53.5 million in the same period 2001. The first quarter 2001 included a sale from an on-site plant in Austria amounting to EURO2.6 million. Excluding this effect, net sales for the region increased from EURO50.9 million in the first quarter 2001 by EURO3.1 million or 6.1% to EURO54.0 million in the same period 2002. Sales volumes in almost all countries in the region increased compared to the same period 2001. The only exception was Bulgaria where we had a temporary shortfall in product sourcing. The main sales increases arose from our businesses in Finland, Hungary, the Czech Republic and Yugoslavia, where new business was generated. This development confirms our leading position in Eastern Europe.

- •

- Net sales in North America decreased 5.0% to EURO93.6 million in the first quarter 2002 from EURO98.5 million in the same period 2001. This decrease results from the EURO12.2 million reduction in net sales as a result of the business disposals pursuant to the divestiture program (the sale of Generon, Healthcare Canada and CO2 business) and is partially offset by EURO4.6 million by the appreciation of the U.S. dollar against the Euro in the first quarter 2002. Excluding the effects of the business disposals in the first quarter 2002 and

12

- •

- Net sales in Other Business Areas decreased 68.9% to EURO14.1 million in the first quarter 2002 from EURO45.4 million in the same period 2001. This decrease primarily results from the divestiture program which resulted in the de-consolidation of our subsidiaries in Mexico, Brazil, Argentina, Peru, Venezuela, Trinidad & Tobago, South Africa, Singapore, Korea and Indonesia as of April 30, 2001. Therefore, the figures are not comparable.

appreciation of the U.S. dollar net sales increased by 3.1% from EURO86.3 million in the first quarter 2001 to EURO89.0 million in the first quarter 2002. This increase reflects an improving business climate in the U.S. and successful pricing increases, particularly within the bulk and pipeline business.

Cost of sales. Cost of sales decreased 11.9% to EURO194.6 million in the first quarter 2002 from EURO220.8 million in the same period 2001. Cost of sales consist primarily of raw material costs (e.g. energy), purchased parts and direct labor, as well as manufacturing overheads and depreciation.

The change in cost of sales is influenced by an amount of EURO2.4 million representing additional depreciation due to step ups related to the purchase method of accounting. Excluding the impact of the purchase method of accounting, cost of sales decreased by 13% to EURO192.2 million in the first quarter 2002. This decrease is caused by lower sales as compared to the first quarter 2002 and by the effect of the de-consolidation.

Furthermore, the decrease in cost of sales also results from our successful cost saving initiatives as the gross margin improved from 49.3% to 49.6% (50.3% excluding the impact from purchase accounting).

Distribution and selling costs. Distribution and selling costs decreased 13% to EURO117.6 million in the first quarter 2002 from EURO135.1 million in the same period 2001. Distribution and selling costs consist primarily of sales organization costs, transport of gases and cylinders from the production site or filling station to the customer, depreciation of the cylinders and tanks at the customer site, advertising and sales promotions, commissions and freight.

The change in distribution and selling costs is influenced by an amount of EURO9.7 million representing additional depreciation due to step ups related to the purchase method of accounting. Excluding the impact of the purchase accounting, distribution and selling costs decreased by 20.1% to EURO107.9 million in the first quarter 2002. This decrease is caused by lower sales as compared to the first quarter 2002 and by the effect of the de-consolidation. Additionally, the decrease in distribution and selling costs results from our successful cost saving initiatives as distribution and selling costs in relation to sales decreased from 31.1% to 30.4% (27.9% excluding the impact from purchase accounting).

General and administrative costs. General and administrative expenses increased by 3.5% to EURO35.7 million in the first quarter 2002 from EURO34.5 million in the same period 2001. General and administrative costs consist primarily of personnel costs attributable to general management, finance and human resources functions, as well as other corporate overhead charges.

13

Operating profit. Operating profit decreased to EURO28.1 million in the first quarter 2002 from EURO34.0 million in the same period 2001 based essentially on the factors described below.

| | Three Months Ended March 31, 2002 Messer Griesheim Holding AG | Three Months Ended March 31, 2001 Messer Griesheim GmbH | |||

|---|---|---|---|---|---|

| | EURO (in millions) | EURO (in millions) | |||

| Operating profit (loss) (Business Areas) | |||||

| Germany | 24.3 | 32.5 | |||

| Western Europe, excluding Germany | 2.1 | 4.4 | |||

| Eastern Europe | 7.3 | 6.8 | |||

| North America | 4.7 | 5.8 | |||

| Others | 2.4 | (4.1 | ) | ||

| Reconciliation/Corporate | (12.7 | ) | (11,4 | ) | |

| Total | 28.1 | 34.0 | |||

- •

- In Germany, the operating profit amounted to EURO24.3 million in the first quarter 2002 as compared to an operating profit of EURO32.5 million in the same period 2001. The operating profit in the first quarter 2002 includes additional depreciation and amortization of EURO11.4 million related to the purchase accounting. Excluding this effect, operating profit increased from EURO32.5 million by 9.8% to EURO35.7 million. This increase results primarily from cost savings more than offsetting the negative impact of lower sales.

- •

- In Western Europe, excluding Germany, the operating profit amounted to EURO2.1 million in the first quarter 2002 compared to an operating profit of EURO4.4 million in the same period 2001. The operating profit in the first quarter 2002 includes additional depreciation and amortization of EURO2.2 million related to the purchase method of accounting. Excluding this effect, operating profit decreased slightly by EURO0.1 million or 2.3% to EURO4.3 million in the first quarter 2002 compared to EURO4.4 million in the first quarter 2001. This decrease is primarily due to decreased margins in Switzerland.

- •

- In Eastern Europe, the operating profit amounted to EURO7.3 million in the first quarter 2002 compared to an operating profit of EURO6.8 million in the same period 2001. The operating profit in the first quarter 2002 included additional depreciation and amortization of EURO1.8 million related to the purchase accounting. The operating profit in the first quarter 2001 included a restructuring expense of EURO0.3 million which did not occur in the same period 2002. Excluding these effects, operating profit increased by EURO2.0 million or 28.2% to EURO9.1 million in the first quarter 2002 compared to EURO7.1 million in the same period 2001.

- •

- In North America, the operating profit amounted to EURO4.7 million in the first quarter 2002 as compared to EURO5.8 million in the same period 2001. The operating profit in the first quarter 2002 includes additional depreciation and amortization of EURO4.5 million related to the purchase accounting. In addition, the operating profit in the first quarter 2001 included restructuring expenses of EURO1.5 million which did not occur in the same period 2002. Excluding these effects, plus EURO0.4 million resulting from the effect of the appreciation of the U.S. dollar against the Euro in the first quarter 2002, operating profit increased by EURO1.5 million or 20.5% to EURO8.8 million in the first quarter 2002 as compared to EURO7.3 million for

14

- •

- Operating profit (loss) in Other Business Areas improved to a profit of EURO2.4 million in the first quarter 2002 compared to a loss of EURO4.1 million in the same period 2001. This improvement results primarily from the deconsolidation of loss making companies as well as a more efficient utilization of new plants in Asia which commenced operations during 2001. However, these figures are generally not comparable as a result of the de-consolidation of companies in Mexico, Brazil, Argentina, Peru, Venezuela, Trinidad & Tobago, South Africa, Singapore and Indonesia.

the same period in 2001. This increase reflects the beginning of an improving business climate in the U.S.

Interest expense, net. Net interest expense increased 40.2% to EURO35.2 million in the first quarter 2002 from EURO25.1 million in the same period 2001. This increase is due to our refinancing program following the acquisition transactions which resulted in an increase in the average interest rate from 6.5% to 8.2% per annum.

Income taxes. In the first quarter 2002 the Group recorded income tax expense of EURO3.2 million, compared to an income tax expense of EURO3.9 million in the same period 2001. This expense in 2002, despite our operating loss, is mainly due to non deductible interest expense and goodwill amortization.

Liquidity and Capital Resources

Cash Flows for the Three Month Period Ended March 31, 2002 and the Three Month Period Ended March 31, 2001

The following table summarizes our cash-flow activity during the three month period ended March 31, 2002 and the three month period ended March 31, 2001. Consideration should be given to the effects of the acquisition transactions, the refinancing program, and the divestiture program when comparing historical financial information, for periods prior to April 30, 2001 to periods thereafter. The solid vertical line separates the information for periods prior to and subsequent to the acquisition transactions:

| | Three Months Ended March 31, 2002 Messer Griesheim Holding AG | Three Months Ended March 31, 2001 Messer Griesheim GmbH | |||

|---|---|---|---|---|---|

| | EURO (in millions) | EURO (in millions) | |||

| Cash flow from operating activities | 85.8 | 6.8 | |||

| Cash flow used in investing activities | (21.6 | ) | (40.9 | ) | |

| Cash flow from (used in) financing activities | (37.5 | ) | 39.7 | ||

| Cash and cash equivalents, end of period | 214.0 | 57.4 |

15

Cash flow from operating activities. The cash flows from operating activities increased to EURO85.8 million from EURO6.8 million. Operating cash flows in the first quarter of 2002 reflects a net loss of EURO13.4 million, consisting of EBIT (earnings before income taxes) of EURO25.0, net of interest and taxes of EURO35.2 and EURO3.2, respectively. Operating cash flows in the first quarter of 2001 reflects a net loss of EURO6.7 million, consisting of EBIT of EURO22.3 million, net of interest and taxes of EURO25.1 million and EURO3.9 million, respectively. Significant non-cash items impacting operating activities included an increase in depreciation and amortization totaling EURO68.8 million in the first quarter of 2002, compared with EURO55.8 million in the first quarter of 2001.

Cash flow from investing activities. The cash flow used in investing activities decreased to EURO21.6 million from EURO40.9 million. The decrease mainly resulted from reductions in capital expenditures for property plant and equipment and intangible assets to EURO23.2 million from EURO31.8 million, and from reductions in investments in and loans to related parties and subsidiaries available for sale to EURO8.5 million from EURO13.2 million during the first quarter of 2002 and 2001, respectively. In addition, investing cash flows during the first quarter of 2002 includes EURO6.9 million of proceeds from sales of investments and property plant and equipment and intangible assets.

Cash flow from financing activities. The company used EURO37.5 million in cash for financing activities during the first quarter of 2002, and generated EURO39.7 million during the first quarter of 2001. Cash flows for financing activities during the first quarter of 2002 included interest paid of EURO30.6 million and principal reductions of corporate debt of EURO5.1 million, whereas financing cash flows during the first quarter of 2001 include EURO74.0 of cash received arising from increases in corporate debt, reduced by interest paid of EURO25.3 million.

Contractual Obligations

The following table summarizes our contractual obligations as of December 31, 2001:

| | Payments Due by Period | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | Less than 1 year | 1-3 years | 4-5 years | After 5 years | Total | |||||

| | EURO (in millions) | EURO (in millions) | EURO (in millions) | EURO (in millions) | EURO (in millions) | |||||

| Contractual Obligations | ||||||||||

| Long-Term Debt | 42.6 | 103.2 | 112.6 | 1,266.3 | 1,524.7 | |||||

| Capital Lease Obligations(1) | 15.7 | 49.1 | 59.5 | 47.5 | 171.8 | |||||

| Operating Lease Obligations | 8.1 | 16.3 | 14.8 | 52.0 | 91.2 | |||||

| Commitments | ||||||||||

| Other Long-Term Obligations(2) | 32.0 | |||||||||

| ACIC Joint Ventures | 32.0 | |||||||||

| Financial Guarantees(3) | 206.7 | |||||||||

| Long-Term Purchase Agreements | 68.6 | |||||||||

| Other(4) | 22.8 | |||||||||

- (1)

- The capital lease obligations include an interest portion of EURO32.8 million.

- (2)

- Other financial obligations not included in the consolidated balance sheet relate to long-term commitments for capital expenditures of EURO32.0 million at December 31, 2001.

- (3)

- Financial guarantees mainly include guarantees for third party debt of deconsolidated subsidiaries included in assets available for sale from the divestiture program of EURO149.6 million and other at equity consolidated subsidiaries of EURO28.4 million.

- (4)

- Commitments for capital to be funded to equity and cost method investees totaled EURO22.8 million at December 31, 2001.

16

Anticipated Uses/Expenditures and Sources of Funds

Capital expenditures in our core markets as a percentage of net sales was 6.0% in the three-month period ended March 31, 2002, as compared to 7.3% in the same period 2001. A core component of our strategy is to reduce Messer Griesheim's historically high levels of capital expenditure. However, we will require funds to meet scheduled debt repayments and to fund the acquisition, if and when it happens, of the China assets as elsewhere stated in this Form 6-K, with a purchase price of EURO32 million and the assumption of existing debt of the ACIC joint ventures (approximately EURO16.5 million at March 31, 2002).

We had total indebtedness (including finance leases) of EURO1,660.2 million at March 31, 2002, of which EURO1,610.6 million was long-term indebtedness. The indebtedness was primarily due to banks and our bondholders and had an average rate of interest of approximately 8.2% at March 31, 2002.

Messer Griesheim's principal sources of funds have been cash flow from operations and borrowings from banks. We expect that, going forward, we will finance on-going operations and implement our cost-savings measures and information-technology improvements with a combination of existing cash balances and operating cash flows, and available funds from our credit lines. We are dependent on the proceeds from our divestiture program to meet our contractually scheduled debt repayment under our senior facilities on April 30, 2003. We expect that our other cash requirements will be met through operating cash flows.

As of March 31, 2002, we had in place unused credit lines totaling EURO297.0 million. In addition, certain of our subsidiaries have unused available credit lines under local facilities.

Interest Rate Risk Management

We are exposed to interest rate risk mainly through our debt instruments. We manage interest rate risk on a group-wide basis with a combination of fixed and floating rate instruments designed to balance the fixed and floating interest rates. We have entered into interest rate swap agreements that effectively convert a major portion of our floating rate indebtedness to a fixed rate basis for the next two and one half years, thus reducing the impact of interest rate changes on future interest expense.

As of March 31, 2002, approximately 90% of our debt facilities were hedged to comply with the terms of our senior facilities agreement. The remaining 10% of our multicurrency debt facilities have floating rates. With respect to such portion of the debt facilities for each fluctuation in market interest rates of 1%, the interest expense related to such portion of the debt facilities would fluctuate by EURO1.5 million.

Foreign Exchange Risk Management

We also are exposed to foreign currency exchange risk related to foreign currency denominated assets and liabilities and debt service payments denominated in foreign currencies. We manage foreign currency exchange risk on a group-wide basis using exchange forward contracts. Our current policy with respect to limiting foreign currency exposure is to economically hedge foreign currency exposures when appropriate.

For the majority of our operations, we have local production facilities which generate cash flows in local currencies. These cash flows generally match local expenditures and debt service of these operations, resulting in a 95% or greater "natural hedge" as of March 31, 2002.

The most significant foreign exchange rate risks exist in Central America, Eastern Europe and China where we produce locally. A portion of our debt serviced by these facilities is in Euros and U.S. dollars. Accordingly, we depend on the stability of currencies in these countries in order to

17

service these debts. The total Euro and US dollar denominated debt in these countries is EURO29 million. The single largest debt is approximately EURO9 million in Poland. An increase or decrease of 10% of the PLN Zloty against the Euro would result in an impact of approximately EURO1 million on our results of operations. If all the currencies in these countries depreciate against the Euro and the U.S. Dollar, a 10% change would impact our consolidated net results by approximately EURO3 million on a pretax basis.

Our reporting currency is the Euro. The net assets outside the "Euro zone" are subject to currency fluctuations against the Euro. The most volatile currencies are those of Eastern Europe, China and Central America. Normally, we do not hedge the net assets of foreign subsidiaries. Except for our subsidiary located in Yugoslavia, a hyperinflationary economy, in the event the Euro significantly increases in value relative to other currencies, the accounting treatment would result in a charge against our equity without any effect on net income.

Derivative Financial Instruments

The table below provides information about our significant derivative financial instruments that are sensitive to changes in interest and foreign currency exchange rates as of March 31, 2002. The table presents the notional amounts and the weighted average contractual foreign exchange rates. The terms of our cross-currency exchange forward contracts generally do not exceed one year. At March 31, 2002, our interest rate swaps had remaining terms of two and one half years.

| | Contract Notional Amount | Contractual Rates | Fair value March 31, 2002 | |||||

|---|---|---|---|---|---|---|---|---|

| | ( EURO equivalent in thousands, except for contractual rates) | |||||||

| | EURO'000 | % | EURO'000) | |||||

| Interest rate cap contracts | ||||||||

| Euro | 25,565 | 5.50000 | % | 115 | (1) | |||

Interest rate swap contracts | ||||||||

| Euro | 87,911 | 4.45500 | % | 70 | ||||

| Euro | 285,000 | 4.69500 | % | (1,469 | ) | |||

| Euro | 54,175 | 4.73000 | % | (278 | ) | |||

| British pounds sterling | 28,956 | 5.81000 | % | (323 | ) | |||

| U.S. dollar | 286,895 | 5.00000 | % | (4,659 | ) | |||

| U.S. dollar | 28,804 | 4.96500 | % | (413 | ) | |||

| Euro | 44,325 | 4.65250 | % | (185 | ) | |||

Forward exchange rate | ||||||||

| Foreign currency forward contracts | ||||||||

| Euro/U.S. dollar | 28,689 | 0.87590 | 346 | (1) | ||||

| British pounds sterling/U.S. dollar | 4,201 | 1.42008 | 12 | (1) | ||||

- (1)

- Free standing derivatives, which are marked-to-market through earnings.

Commodity Price Risk

We are exposed to commodity price risks through our dependence on various raw materials, such as chemical and energy prices. We seek to minimize these risks through our sourcing policies, operating procedures and pass through clauses in our product pricing agreements. We

18

currently do not utilize derivative financial instruments to manage any remaining exposure to fluctuations in commodity prices.

Risk Identification and Analysis

The identification and analysis of risks relating to our operations is conducted through the application of an enterprise-wide risk management system, encompassing all of our activities worldwide. The goal of this risk management system is to foster a group-wide culture of risk management using a common set of objectives and standards in the measurement and treatment of risk. As with any risk management system, the results are based on individual assessments that may be subject to error. There is no guarantee that this system will consistently identify all of the important risks or provide an adequate assessment of their potential impact.

We are exposed to market risk through our commercial and financial operations as described above. We are implementing a policy of economic hedging against some of these exposures at present, but we may still incur losses as a result of changes in currency exchange rates, interest rates and commodity risk. We do not purchase or sell derivative financial instruments for trading purposes.

Initial Adoption of Accounting Policies

Effective July 1, 2001, the Group adopted Statement 141"Business Combinations" and certain provisions of SFAS 142"Goodwill and Other Intangible Assets". The Group adopted SFAS 142 in its entirety on January 1, 2002. SFAS 141 requires that the purchase method of accounting be used for all business combinations initiated after June 30, 2001, as well as all purchase method business combinations completed after June 30, 2001. SFAS 141 also specifies criteria intangible assets acquired in a purchase method business combination must meet to be recognized and reported separately from goodwill, and also indicates that any purchase price allocable to an assembled workforce may not be accounted for separately. Additionally, SFAS 141 required, upon adoption of SFAS 142 in its entirety, that the Group evaluate its existing intangible assets and goodwill that were acquired in a prior purchase business combination, and to make any necessary reclassifications in order to conform with the new criteria in SFAS 141 for recognition apart from goodwill. SFAS 142 requires that goodwill and intangible assets with indefinite useful lives no longer be amortized, but instead will be tested for impairment annually (or more frequently if impairment indicators arise) in accordance with the provisions of SFAS 142. Intangible assets with definite useful lives will be amortized over their respective estimated useful lives to their estimated residual values, and reviewed for impairment in accordance with SFAS 144"Accounting for the Impairment or Disposal of Long-Lived Assets".

In August 2001, the FASB approved for issuance SFAS 144. This Statement addresses financial accounting and reporting for the impairment or disposal of long-lived assets. This Statement supersedes SFAS 121 and the accounting and reporting provisions of APB Opinion No. 30"Reporting the Results of Operations—Reporting the Effects of Disposal of a Segment of a Business, and Extraordinary, Unusual and Infrequently Occurring Events and Transactions", for the disposal of a segment of a business (as previously defined in that Opinion). This Statement also amends ARB No. 51"Consolidated Financial Statements" to eliminate the exception to consolidation for a subsidiary for which control is likely to be temporary. The Group adopted the provisions of this Statement on January 1, 2002. The adoption of the new pronouncement did not have a material effect on the unaudited interim condensed consolidated financial statements. However, the Group has noted that certain provisions of SFAS 144 will potentially impact its accounting and reporting for the remaining subsidiaries to be sold under its divestiture program. The Group has also noted that

19

the provisions of SFAS 144 would supersede certain provisions of EITF 87-11 as they relate to allocation of purchase price in a business combination where the acquirer intends to sell a portion of the operations of the acquired enterprise (see note 40a) and, as a result, had SFAS 144 been applied in accounting for the acquisition transactions, certain of the differences between U.S. GAAP and IAS relating to operations and entities included in the divestiture program would not have occurred.

Main Differences

Our results as reported under IAS differ from our results as reconciled to U.S. GAAP, principally as a result of the different treatment under U.S. GAAP of:

- •

- allocation of purchase price to assets to be sold,

- •

- restructuring costs,

- •

- transaction costs incurred by our parent on our behalf,

- •

- impairment of long lived assets,

- •

- assembled workforce (intangible asset),

- •

- foreign currency gains and losses on borrowing costs directly attributable to construction,

- •

- provisions for pensions and similar obligations, and

- •

- gains and losses related to financial instruments.

The significant differences between IAS and U.S. GAAP applicable to the historical financial statements are summarized below. Significant differences between IAS and U.S. GAAP applicable to our historical financial statements are further discussed elsewhere in this document.

Three Months Ended March 31, 2002 compared with Three Months Ended March 31, 2001

Net loss as reported under IAS was EURO13.4 million in first quarter 2002 and EURO5.3 million as reconciled to U.S. GAAP. There were reconciling adjustments of EURO0.7 million in first quarter 2002 between IAS and U.S. GAAP relating to assets to be sold within one year of the date of the acquisition transaction. The remaining difference between net loss reported under IAS and net loss reported under U.S. GAAP is primarily due to the discontinuation of goodwill amortization under U.S. GAAP upon adoption of SFAS 142 and the tax effect under U.S. GAAP associated with these adjustments.

In the first quarter 2001, the net loss reported under IAS was EURO6.7 million and EURO6.6 million as reconciled to U.S. GAAP. The difference between net loss reported under IAS and net loss reported under U.S. GAAP is primarily due to property, plant and equipment, provisions for pension and similar obligations and to the tax effect under U.S. GAAP associated with these adjustments.

20

MESSER GRIESHEIM HOLDING AG

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Amounts in EURO thousands, unless otherwise stated)

| | | Successor | Predecessor | ||||

|---|---|---|---|---|---|---|---|

| | Note | January 1, 2002 to March 31, 2002 | January 1, 2001 to March 31, 2001 | ||||

| Net sales | 386,420 | 435,150 | |||||

| Cost of sales | (194,628 | ) | (220,869 | ) | |||

| Gross profit | 191,792 | 214,281 | |||||

| Distribution and selling costs | (117,573 | ) | (135,119 | ) | |||

| Research and development costs | (3,787 | ) | (5,089 | ) | |||

| General and administrative costs | (35,655 | ) | (34,529 | ) | |||

| Other operating income | 6,636 | 6,256 | |||||

| Other operating expense | (12,870 | ) | (9,724 | ) | |||

| Restructuring and reorganization charges | 8 | (408 | ) | (2,123 | ) | ||

| Operating profit | 28,135 | 33,953 | |||||

| Equity method investments expense, net | (10 | ) | (2,993 | ) | |||

| Other investment income, net | 309 | 767 | |||||

| Interest expense, net | 4 | (35,234 | ) | (25,078 | ) | ||

| Changes in fair value of investments in subsidiaries available for sale | 9 | (692 | ) | — | |||

| Other financial expense, net | (220 | ) | (7,447 | ) | |||

| Non-operating expense | (35,847 | ) | (34,751 | ) | |||

| Loss before income taxes and minority interests | (7,712 | ) | (798 | ) | |||

| Income tax expense | (3,246 | ) | (3,872 | ) | |||

| Loss before minority interests | (10,958 | ) | (4,670 | ) | |||

| Minority interests, net of income taxes | (2,436 | ) | (2,023 | ) | |||

| Net loss | (13,394 | ) | (6,693 | ) | |||

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

21

MESSER GRIESHEIM HOLDING AG

UNAUDITED INTERIM CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in EURO thousands, unless otherwise stated)

| | Note | As of March 31, 2002 | As of December 31, 2001 | ||||

|---|---|---|---|---|---|---|---|

| Assets | |||||||

| Intangible assets | 842,745 | 852,809 | |||||

| Property, plant and equipment | 1,675,587 | 1,697,679 | |||||

| Equity method investments | 19,199 | 19,186 | |||||

| Cost method and other investments | 57,984 | 59,347 | |||||

| Deferred tax assets | 4,741 | 4,546 | |||||

| Other long-term receivables, net and other assets | 11 | 37,805 | 43,081 | ||||

| Non-current assets | 2,638,061 | 2,676,648 | |||||

| Inventories | 12 | 83,719 | 80,098 | ||||

| Trade accounts receivable, net | 293,205 | 290,743 | |||||

| Investments in subsidiaries available for sale | 9 | 45,122 | 42,183 | ||||

| Other receivables and other assets | 74,332 | 71,796 | |||||

| Cash and cash equivalents | 13 | 214,015 | 188,018 | ||||

| Current assets | 710,393 | 672,838 | |||||

| Total assets | 3,348,454 | 3,349,486 | |||||

| Stockholders` equity and liabilities | |||||||

| Issued capital and reserves | 967,180 | 967,180 | |||||

| Accumulated deficit | (82,925 | ) | (69,531 | ) | |||

| Cumulative other comprehensive income | 18,891 | 5,740 | |||||

| Stockholders` equity | 903,146 | 903,389 | |||||

| Minority interests | 90,238 | 88,138 | |||||

| Provisions for pensions and similar obligations | 168,514 | 166,356 | |||||

| Other provisions | 4 | 45,812 | 53,344 | ||||

| Corporate debt, less current portion | 1,542,526 | 1,540,312 | |||||

| Deferred tax liabilities | 140,711 | 135,933 | |||||

| Other liabilities | 27,443 | 25,353 | |||||

| Non-current liabilities | 1,925,006 | 1,921,298 | |||||

| Other provisions | 4 | 146,568 | 159,215 | ||||

| Corporate debt | 38,125 | 40,927 | |||||

| Trade accounts payable | 110,019 | 118,344 | |||||

| Miscellaneous liabilities | 135,352 | 118,175 | |||||

| Current liabilities | 430,064 | 436,661 | |||||

| Total stockholders` equity and liabilities | 3,348,454 | 3,349,486 | |||||

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

22

MESSER GRIESHEIM HOLDING AG

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY

(Amounts in EURO thousands, unless otherwise stated)

| | Predecessor | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | | Other comprehensive income | | | |||||||||

| | | | | Cumulative other comprehensive income | | ||||||||||

| | Subscribed capital | Additional paid-in capital | Accumulated deficit | Hedging reserve | Translation reserve | Total stockholders' Equity | |||||||||

| Balance as of December 31, 2000 | 276,098 | 158,386 | (80,164 | ) | — | 84,204 | 84,204 | 438,524 | |||||||

| IAS 39 transition adjustment | — | — | 335 | — | — | — | 335 | ||||||||

| Net loss | — | — | (6,693 | ) | — | — | — | (6,693 | ) | ||||||

| Cumulative translation adjustment | — | — | — | — | 403 | 403 | 403 | ||||||||

| Balance as of March 31, 2001 | 276,098 | 158,386 | (86,522 | ) | — | 84,607 | 84,607 | 432,569 | |||||||

| | Successor | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | | Other comprehensive income | | | |||||||||

| | | | | Cumulative other comprehensive income | | ||||||||||

| | Subscribed capital | Additional paid-in capital | Accumulated deficit | Hedging reserve | Translation reserve | Total stockholders' Equity | |||||||||

| Balance as of December 31, 2001 | 90 | 967,090 | (69,531 | ) | (9,199 | ) | 14,939 | 5,740 | 903,389 | ||||||

| Change in fair value of derivatives | — | — | — | 4,817 | — | 4,817 | 4,817 | ||||||||

| Net loss | — | — | (13,394 | ) | — | — | — | (13,394 | ) | ||||||

| Cumulative translation adjustment | — | — | — | — | 8,334 | 8,334 | 8,334 | ||||||||

| Balance as of March 31, 2002 | 90 | 967,090 | (82,925 | ) | (4,382 | ) | 23,273 | 18,891 | 903,146 | ||||||

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

23

MESSER GRIESHEIM HOLDING AG

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in EURO thousands, unless otherwise stated)

| | Successor | Predecessor | |||

|---|---|---|---|---|---|

| | January 1, 2002 to March 31, 2002 | January 1, 2001 to March 31, 2001 | |||

| Losses before income taxes and minority interests | (7,712 | ) | (798 | ) | |

| Income taxes (paid) refunded | (3,784 | ) | 827 | ||

| Depreciation and amortization of property, plant and equipment and intangible assets | 68,755 | 55,843 | |||

| Changes in fair value of investments in subsidiaries available for sale | 692 | — | |||

| Write-down of investments | 803 | — | |||

| (Gain)/losses on disposals of property, plant and equipment and investments | (363 | ) | 398 | ||

| Non-cash changes in equity method investments | 10 | 2,993 | |||

| Interest expense, net | 35,234 | 25,078 | |||

| Other financial expense, net | 220 | 7,447 | |||

| Changes in inventories | (3,378 | ) | (12,461 | ) | |

| Changes in receivables and other assets | 2,849 | (26,605 | ) | ||

| Changes in provisions | (11,145 | ) | (28,354 | ) | |

| Changes in accounts payable and other liabilities | 3,605 | (17,575 | ) | ||

| Cash flow from operating activities | 85,786 | 6,793 | |||

| Purchases of property plant and equipment and intangible assets | (23,189 | ) | (31,796 | ) | |

| Purchases of investments and loans to related parties | (2,846 | ) | (13,152 | ) | |

| Investments in subsidiaries available for sale for extinguishment of debt | (5,655 | ) | — | ||

| Proceeds from the sales of property plant and equipment and intangible assets | 1,666 | 59 | |||

| Proceeds from the sales of investments | 5,272 | 20 | |||

| Interest received | 3,115 | 3,930 | |||

| Cash flow used in investing activities | (21,637 | ) | (40,939 | ) | |

| Net proceeds from additions to non-current corporate debt | — | 12,041 | |||

| Repayments of non-current corporate debt | (1,854 | ) | — | ||

| Net (repayment of) proceeds from current corporate debt | (3,247 | ) | 61,914 | ||

| Dividends paid to minorities | (1,514 | ) | (1,514 | ) | |

| Interest paid | (30,620 | ) | (25,308 | ) | |

| Other financial expenses, net | (220 | ) | (7,447 | ) | |

| Cash flow from (used in) financing activities | (37,455 | ) | 39,686 | ||

| Cash flow from operating, investing and financing activities | 26,694 | 5,540 | |||

| Effect of exchange rate changes on cash and cash equivalents | (697 | ) | 1,448 | ||

| Changes in cash and cash equivalents | 25,997 | 6,988 | |||

| Cash and cash equivalents | |||||

| at beginning of reporting period | 188,018 | 50,403 | |||

| at end of reporting period | 214,015 | 57,391 |

The accompanying notes are an integral part of these unaudited interim condensed consolidated financial statements.

24

MESSER GRIESHEIM HOLDING AG

NOTES TO UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts in EURO thousands, unless otherwise stated)

1. Background and basis of presentation

Messer Griesheim Holding AG ("the Company" or "Successor") is a supplier of industrial gases. The Company produces and markets industrial gases (including oxygen, nitrogen, argon, helium, carbon dioxide, hydrogen and rare and high-purity gases), gas application processes and customer-site gas production systems. The Company's primary customers include major industrial, chemical and pharmaceutical manufacturers, and the food processing and waste treatment industries. Messer Griesheim Group GmbH & Co. KGaA owns 100% of the shares of Messer Griesheim Holding AG, 33.33% of which is owned directly and 66.67% which is owned through the wholly owned Diogenes 20.Vermögensverwaltung GmbH.

The unaudited interim condensed consolidated financial statements have been prepared in accordance with International Accounting Standards ("IAS") as adopted by the International Accounting Standards Board and include the accounts of all companies which it controls (collectively, "the Messer Group", "Messer" or "Messer Griesheim GmbH" or the "Group").

The Successor, incorporated on November 6, 1996, was a dormant company until April 30, 2001, when it was activated to become the holding company for the shares of Messer Griesheim GmbH ("Predecessor"). As of December 31, 2000, the Successor had net assets aggregating EURO44.9, represented by current assets of EURO50.7 and current liabilities of EURO5.8. As discussed in note 3 the Predecessor was recapitalized to effect the acquistion transactions which have been accounted for at fair value. Accordingly, the assets and liabilities of the Group have been recorded at their estimated fair values as of April 30, 2001, the date of the acquisition transactions. As a result, the financial statements of the Group for periods prior to the acquisition are not comparable to the Group's financial statements for periods subsequent to the acquisition. To highlight this lack of comparability, a solid line has been inserted, where applicable, to distinguish information pertaining to the pre-acquisition and post-acquisition periods. The refinancing transactions and the divestiture program adopted by the Group are described in notes 4 and 9, respectively.

The unaudited interim condensed consolidated financial statements include, in the opinion of management, all adjustments of a normal, recurring nature necessary to present fairly the financial position, results of operations and cash flows for the periods presented. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with IAS have been condensed or omitted. These unaudited interim condensed consolidated financial statements have been prepared using similar accounting principles and should, therefore, be read in conjunction with the successors's December 31, 2001 consolidated financial statements and notes thereto. The results of operations for the interim 2002 periods presented are not necessarily indicative of the operating results to be expected for the full year.

The preparation of unaudited interim condensed consolidated financial statements in conformity with IAS requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Certain reclassifications have been made to the presentation of prior periods to conform to the current period classification.

25

2. New IAS accounting standards

The Group has adopted each of the following standards effective January 1, 2001. Unless otherwise stated, adoption of these standards did not have a material impact on the Group's financial position or results of operations.

In 1998 the IASC issued IAS 39"Financial Instruments: Recognition and Measurement". IAS 39 was effective for fiscal periods beginning after December 31, 2000. The standard significantly increases the use of fair values in accounting for financial instruments. In addition, it establishes specific criteria relating to hedge accounting. Adoption of this standard on January 1, 2001 resulted in a EURO335 cumulative effect of change in accounting principles, net of deferred taxes totaling EURO223, reported in other comprehensive income.

In 2000 the IASC issued IAS 40 "Investment Property". IAS 40 was effective for financial statements covering periods beginning on or after January 1, 2001. IAS 40 prescribes the accounting treatment for investment property and related disclosure requirements and replaces previous requirements in IAS 25 "Accounting for Investments". Under IAS 40, investment property is defined as property held to earn rentals or for capital appreciation or both rather than for use in the production or supply of goods or services or for administrative purposes or for sale in the ordinary course of business. The Group has opted for the cost model under which investment property is measured at depreciated cost less any impairment losses.

In 2000 the IASC revised IAS 19"Employee Benefits". IAS 19 (revised 2000) was effective for fiscal periods beginning on or after January 1, 2001. The standard changes the definition of plan assets and introduces recognition, measurement and disclosure requirements for reimbursements. The standard prescribes the accounting and disclosure by employers for employee benefits, post employment benefits, other long-term employee benefits, termination benefits and equity compensation benefits.

3. Acquisition transactions

On December 31, 2000, Aventis S.A. (parent company to Hoechst AG ("Hoechst")) entered into an agreement with Allianz Capital Partners ("ACP") and six private equity funds managed by affiliates of The Goldman Sachs Group, Inc. (the "GS Funds"), regarding the purchase of Hoechst's shares in Messer Griesheim. The transaction was consummated on April 30, 2001.

In order to facilitate the purchase of Hoechst's shares in Messer Griesheim by ACP and the GS Funds, Hoechst transferred its 662/3% share interest in Messer Griesheim to the Company. On April 30, 2001 Messer Industrie GmbH ("MIG") transferred its 331/3% equity interest in Messer Griesheim to the Company for nominal cash and a 331/3% equity interest in the Company. As explained in the following paragraph, the Company was then immediately acquired by Messer Griesheim Group GmbH.

ACP and the GS funds formed a new company, Messer Griesheim Group GmbH & Co KGaA. On April 30, 2001, through Messer Griesheim Group GmbH & Co KGaA, ACP and the GS Funds acquired Hoechst's share of the Company for EURO618 million, payable in cash ( EURO388 million) and deferred notes ( EURO230 million). The EURO230 million note is due from Messer Griesheim Group GmbH & Co KGaA on November 11, 2011, together with interest which, although not currently payable, will accrue thereon at a rate of 250 basis points above the three month EURIBOR. In certain

26

circumstances, the deferred purchase price may be payable earlier. Further, Hoechst has been issued 300,000 bonds ( EURO300) which are convertible into 3% of the equity shares of Messer Griesheim Group GmbH & Co KGaA upon the occurrence of certain events at a nominal conversion price. In addition, MIG transferred its share in the Company for a 32.67% share in Messer Griesheim Group GmbH & Co KGaA and cash of EURO33.2 million. MIG is also entitled to receive additional cash consideration of up to EURO35.8 million upon the occurrence of certain events. As a result of the foregoing transactions, the Company was 100% owned by Messer Griesheim Group GmbH & Co KGaA, which in turn is owned by ACP (33.665%), the GS Funds (collectively 33.665%) and Messer Industrie GmbH (32.67%) at April 30, 2001.

Also as a result of the foregoing transactions, the Company owns 100% of Messer Griesheim.

The foregoing transactions have been accounted for in a manner similar to an acquisition of Messer Griesheim. Accordingly, the purchase consideration for the acquisition transaction has been allocated to the assets acquired and liabilities assumed as of April 30, 2001, the date of consummation of the acquisition transactions, based on their estimated fair values.