UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

100 F ST., N.E.

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

S ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2008,

OR

£ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM TO

| | | | |

Commission

File Number | | Registrants, State of Incorporation,

Address, and Telephone Number | | I.R.S. Employer

Identification No. |

001-09120 | | PUBLIC SERVICE ENTERPRISE GROUP INCORPORATED

(A New Jersey Corporation)

80 Park Plaza, P.O. Box 1171

Newark, New Jersey 07101-1171

973 430-7000

http://www.pseg.com | | 22-2625848 |

000-49614 | | PSEG POWER LLC

(A Delaware Limited Liability Company)

80 Park Plaza—T25

Newark, New Jersey 07102-4194

973 430-7000

http://www.pseg.com | | 22-3663480 |

001-00973 | | PUBLIC SERVICE ELECTRIC AND GAS COMPANY

(A New Jersey Corporation)

80 Park Plaza, P.O. Box 570

Newark, New Jersey 07101-0570

973 430-7000

http://www.pseg.com | | 22-1212800 |

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

Registrant | | Title of Each Class | | Name of Each Exchange

On Which Registered |

Public Service Enterprise

Group Incorporated | | Common Stock without

par value | | New York Stock

Exchange |

| | | | | | | | | | |

Registrant | | Title of Each Class | | Title of Each Class | | Name of Each Exchange

On Which Registered |

Public Service Electric

and Gas Company | | Cumulative Preferred Stock

$100 par value Series: | | First and Refunding

Mortgage Bonds: | | |

| | | | | | Series | | Due | | |

| | 4.08% | | 91/4% | | CC | | 2021 | | |

| | 4.18% | | 63/4% | | VV | | 2016 | | New York Stock Exchange |

| | 4.30% | | 8% | | | | 2037 | | |

| | 5.05% | | 5% | | | | 2037 | | |

| | 5.28% | | | | | | | | |

(Cover continued on next page)

(Cover continued from previous page)

| | | | |

Registrant | | Title of Each Class | | Name of Each Exchange

On Which Registered |

PSEG Power LLC | | 85/8% Senior Notes, due 2031 | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

| | |

Registrant | | Title of Class |

PSEG Power LLC | | Limited Liability Company Membership Interest |

| | |

Public Service Electric and Gas Company | | 6.92% Cumulative Preferred Stock $100 par value

Medium-Term Notes, Series A

Medium-Term Notes, Series B

Medium-Term Notes, Series C

Medium-Term Notes, Series D

Medium-Term Notes, Series E

Medium-Term Notes, Series F |

Indicate by check mark whether each registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| | | | |

Public Service Enterprise Group Incorporated | | | | YesS | | | | | No£ | |

PSEG Power LLC | | | | Yes£ | | | | | NoS | |

Public Service Electric and Gas Company | | | | YesS | | | | | No£ | |

Indicate by check mark if each of the registrants is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes£ NoS

Indicate by check mark whether each of the registrants (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. YesS No£

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.S

Indicate by check mark whether each registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | |

Public Service Enterprise Group Incorporated | | Large accelerated filerS | | Accelerated filer£ | | Non-accelerated filer£ | | Smaller reporting company£ |

PSEG Power LLC | | Large accelerated filer£ | | Accelerated filer£ | | Non-accelerated filerS | | Smaller reporting company£ |

Public Service Electric

and Gas Company | | Large accelerated filer£ | | Accelerated filer£ | | Non-accelerated filerS | | Smaller reporting company£ |

Indicate by check mark whether any of the registrants is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes£ NoS

The aggregate market value of the Common Stock of Public Service Enterprise Group Incorporated held by non-affiliates as of June 30, 2008 was $23,326,705,042 based upon the New York Stock Exchange Composite Transaction closing price.

The number of shares outstanding of Public Service Enterprise Group Incorporated’s sole class of Common Stock as of January 30, 2009 was 505,996,093.

PSEG Power LLC is a wholly owned subsidiary of Public Service Enterprise Group Incorporated and meets the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K and is filing its Annual Report on Form 10-K with the reduced disclosure format authorized by General Instruction I.

As of January 30, 2009, Public Service Electric and Gas Company had issued and outstanding 132,450,344 shares of Common Stock, without nominal or par value, all of which were privately held, beneficially and of record by Public Service Enterprise Group Incorporated.

DOCUMENTS INCORPORATED BY REFERENCE

| | |

Part of Form 10-K of

Public Service

Enterprise

Group Incorporated | | Documents Incorporated by Reference |

III | | Portions of the definitive Proxy Statement for the 2009 Annual Meeting of Stockholders of Public Service Enterprise Group Incorporated, which definitive Proxy Statement is expected to be filed with the Securities and Exchange Commission on or about March 9, 2009, as specified herein. |

TABLE OF CONTENTS

i

FORWARD-LOOKING STATEMENTS

Certain of the matters discussed in this report constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to risks and uncertainties, which could cause actual results to differ materially from those anticipated. Such statements are based on management’s beliefs as well as assumptions made by and information currently available to management. When used herein, the words “anticipate,” “intend,” “estimate,” “believe,” “expect,” “plan,” “hypothetical,” “potential,” “forecast,” “project,” variations of such words and similar expressions are intended to identify forward-looking statements. Factors that may cause actual results to differ are often presented with the forward-looking statements themselves. Other factors that could cause actual results to differ materially from those contemplated in any forward-looking statements made by us herein are discussed in Item 1A. Risk Factors, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A), Item 8. Financial Statements and Supplementary Data—Note 11. Commitments and Contingent Liabilities and other factors discussed in filings we make with the United States Securities and Exchange Commission (SEC). These factors include, but are not limited to:

|

• | | | | Adverse changes in energy industry policies and regulation, including market structures and rules. |

|

• | | | | Any inability of our energy transmission and distribution businesses to obtain adequate and timely rate relief and regulatory approvals from federal and state regulators. |

|

• | | | | Changes in federal and state environmental regulations that could increase our costs or limit operations of our generating units. |

|

• | | | | Changes in nuclear regulation and/or developments in the nuclear power industry generally that could limit operations of our nuclear generating units. |

|

• | | | | Actions or activities at one of our nuclear units that might adversely affect our ability to continue to operate that unit or other units at the same site. |

|

• | | | | Any inability to balance our energy obligations, available supply and trading risks. |

|

• | | | | Any deterioration in our credit quality. |

|

• | | | | Availability of capital and credit at reasonable pricing terms and our ability to meet cash needs. |

|

• | | | | Any inability to realize anticipated tax benefits or retain tax credits. |

|

• | | | | Increases in the cost of, or interruption in the supply of, fuel and other commodities necessary to the operation of our generating units. |

|

• | | | | Delays or cost escalations in our construction and development activities. |

|

• | | | | Adverse investment performance of our decommissioning and defined benefit plan trust funds and changes in discount rates and funding requirements. |

|

• | | | | Changes in technology and increased customer conservation. |

Additional information concerning these factors are set forth under Item 1A. Risk Factors.

All of the forward-looking statements made in this report are qualified by these cautionary statements and we cannot assure you that the results or developments anticipated by management will be realized, or even if realized, will have the expected consequences to, or effects on, us or our business prospects, financial condition or results of operations. Readers are cautioned not to place undue reliance on these forward-looking statements in making any investment decision. Forward-looking statements made in this report only apply as of the date of this report. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if internal estimates change, unless otherwise required by applicable securities laws.

The forward-looking statements contained in this report are intended to qualify for the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

ii

FILING FORMAT AND GLOSSARY

This combined Annual Report on Form 10-K is separately filed by Public Service Enterprise Group Incorporated (PSEG), PSEG Power LLC (Power) and Public Service Electric and Gas Company (PSE&G). Information relating to any individual company is filed by such company on its own behalf. Power and PSE&G each is only responsible for information about itself and its subsidiaries.

Discussions throughout the document refer to PSEG and its principal operating subsidiaries, Power, PSE&G and PSEG Energy Holdings L.L.C. (Energy Holdings). Depending on the context of each section, references to “we,” “us,” and “our” relate to the specific company or companies being discussed. In addition, certain key acronyms and definitions are summarized in a glossary beginning on page 233.

WHERE TO FIND MORE INFORMATION

PSEG, Power and PSE&G file annual, quarterly and special reports, proxy statements and other information with the U.S. Securities and Exchange Commission (SEC). You may read and copy any document that we file at the Public Reference Room of the SEC at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. You may also obtain our filed documents from commercial document retrieval services, the SEC’s internet website at www.sec.gov or our website at www.pseg.com. Information contained on our website should not be deemed incorporated into or as a part of this report. Our Common Stock is listed on the New York Stock Exchange under the ticker symbol PEG. You can obtain information about us at the offices of the New York Stock Exchange, 20 Broad Street, New York, New York 10005.

PART I

ITEM 1. BUSINESS

We were incorporated under the laws of the State of New Jersey in 1985 and our principal executive offices are located at 80 Park Plaza, Newark, New Jersey 07102. We conduct our business through three direct wholly owned subsidiaries, Power, PSE&G and Energy Holdings, each of which also has its principal executive offices at 80 Park Plaza, Newark, New Jersey 07102. PSEG Services Corporation (Services), our wholly owned subsidiary, provides us and these operating subsidiaries with certain management, administrative and general services at cost.

1

| | | | |

PSEG |

|

We are an energy company with a diversified business mix. Our operations are located primarily in the Northeastern and Mid Atlantic United States. Our business approach focuses on operational excellence, financial strength and disciplined investment. As a holding company, our profitability depends significantly on our subsidiaries’ operating capabilities. Below are descriptions of our principal operating subsidiaries. |

|

Power | | PSE&G | | Energy Holdings |

|

A Delaware limited liability company formed in 1999 that integrates its generating asset operations with its wholesale energy sales, fuel supply, energy trading and marketing and risk management functions.

Earns revenues from selling under contract or on the spot market a range of diverse products such as electricity, natural gas, capacity, emissions credits, congestion credits and a series of energy-related products used to optimize the operation of the energy grid.

Owns approximately 13,600 megawatts (MWs) of generation capacity located in the Northeast and Mid Atlantic regions of the U.S. in some of the country’s largest and most developed electricity markets. | | A New Jersey corporation, incorporated in 1924, which is a regulated public utility providing transmission and distribution of electric energy and natural gas in New Jersey. It is also the provider of last resort for gas and electric commodity service for end users in its service territory.

Earns revenue from its regulated rate tariffs under which it provides electric transmission and electric and gas distribution to residential, commercial and industrial customers in its service territory. It also offers appliance services and repairs to customers throughout its service territory.

Provides service to 2.1 million electric customers and 1.7 million gas customers in a service area that covers approximately 2,600 square miles running diagonally across New Jersey where approximately 5.5 million people, or about 70% of the State’s population, resides. Serves the most heavily populated, commercialized and industrialized territory in New Jersey, including its six largest cities and approximately 300 suburban and rural communities. | | A New Jersey limited liability company (formed as successor to a company which was incorporated in 1989) that invests and operates through its two primary subsidiaries.

Earns revenues from the operation of generation projects and passive energy-related investments.

Owns approximately 2,400 MW of generation capacity, mostly in Texas.

Also owns and manages a $2 billion diversified portfolio of passive investments, which consists mainly of energy-related leveraged leases. |

The majority of our earnings are derived from the operations of Power, which has contributed at least 70% of our Income from Continuing Operations over the past three years. While this part of the business has produced significant earnings over that period, its operations are subject to higher risks resulting from volatility in the energy markets. PSE&G has continued to produce stable earnings contributions for us. Earnings from Energy Holdings have declined in recent years as we have significantly reduced our investment in international projects. Energy Holdings’ earnings have also been impacted by gains and losses on its asset sales and other charges and impairments taken on its remaining investments.

2

| | | | | | |

|

Earnings (Losses) in millions | | 2008 | | 2007 | | 2006 |

|

Power | | | $ | | 1,050 | | | | $ | | 949 | | | | $ | | 515 | |

PSE&G | | | | 364 | | | | | 380 | | | | | 265 | |

Energy Holdings | | | | (403 | ) | | | | | 63 | | | | | (30 | ) | |

Other | | | | (28 | ) | | | | | (67 | ) | | | | | (77 | ) | |

| | | | | | |

PSEG Income from Continuing Operations | | | $ | | 983 | | | | $ | | 1,325 | | | | $ | | 673 | |

| | | | | | |

The following is a more detailed description of our business, including a discussion of our:

|

• | | | | Business Operations and Strategy |

|

• | | | | Competitive Environment |

|

• | | | | Employee Relations |

|

• | | | | Regulatory Issues |

|

• | | | | Environmental Matters |

BUSINESS OPERATIONS AND STRATEGY

Power

Through Power, we seek to produce low-cost energy by efficiently operating our nuclear, coal and gas-fired generation facilities, while balancing generation production, fuel requirements and supply obligations through energy portfolio management. We use commodity and financial instruments, combined with our owned generation, to cover our commitments for Basic Generation Service (BGS) in New Jersey and other bilateral contract agreements.

Products and Services

As a merchant generator, our profit is derived from selling a range of products and services under contract to power marketers and to load-serving entities, such as investor-owned and municipal utilities, and to aggregators who resell energy to retail consumers, or on the spot market. These products and services include:

|

• | | | | Energy—is the electrical output produced by generation plants that is ultimately delivered to customers for use in lighting, heating, air conditioning and operation of other electrical equipment. Energy is our principal product and is priced on a usage basis, typically in cents per kWh or dollars per MWh. |

|

• | | | | Capacity—a product distinct from energy, is a market commitment that a given unit will be available to an Independent System Operator (ISO) for dispatch if it is needed to meet system demand. Capacity is typically priced in dollars per MW for a given sale period. |

|

• | | | | Ancillary Services—are related activities supplied by generation unit owners to the wholesale market, required by the ISO to ensure the safe and reliable operation of the bulk power system. Owners of generation units may bid units into the ancillary services market in return for compensatory payments. Costs to pay generators for ancillary services are recovered through charges imposed on market participants. |

|

• | | | | Emissions Allowances and Congestion Credits—Emissions Allowances (or credits) represent the right to emit a specific amount of certain pollutants. Allowance trading is used to control air pollution by providing economic incentives for achieving reductions in the emissions of pollutants. Congestion credits (or Financial Transmission Rights) are financial instruments that entitle the holder |

3

| | | | to a stream of revenues (or charges) based on the hourly congestion price differences across a transmission path. |

Power also sells wholesale natural gas, primarily through a full requirements Basic Gas Supply Service (BGSS) contract with PSE&G to meet the gas supply requirements of PSE&G’s gas customers. The current BGSS contract runs through March 31, 2012.

About 42% of PSE&G’s peak daily gas requirements comes from our firm transportation, which is available every day of the year. We satisfy the remainder of PSE&G’s requirements from our field storage, liquefied natural gas, seasonal purchases, contract peaking supply, propane and refinery and landfill gas. Based upon availability, we also sell gas to others.

How Power Operates

We have ownership interests in five nuclear generating units: Salem Units 1 and 2, each owned 57.41% by us and 42.59% by Exelon Generation and which we operate; Hope Creek, 100% owned and operated by us; and Peach Bottom Units 2 and 3, each of which is operated by Exelon Generation and owned 50% by us and 50% by Exelon Generation. Salem 1 and 2 and Hope Creek are located at the same site. We also have ownership interests in fossil-fueled generating stations in the Northeast and Mid Atlantic U.S. These units use coal, natural gas and oil for electric generation.

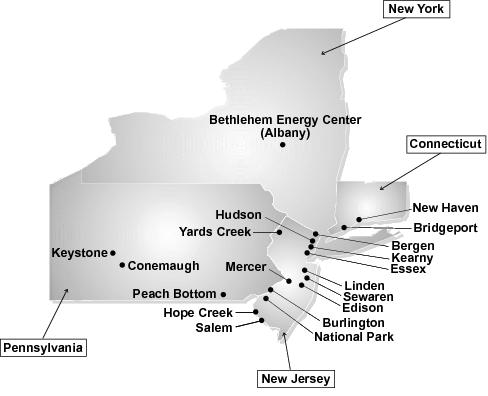

The map below shows the locations of Power’s generation facilities. For additional information, see Item 2. Properties.

4

| | | Generation Capacity | Our installed capacity is comprised of a diverse mix of fuels: 45% gas, 27% nuclear, 17% coal, 9% oil and 2% pumped storage. This fuel diversity serves to mitigate risks associated with fuel price volatility and market demand cycles. Our total generating output in 2008 was approximately 55,300 GWh, which was the highest level of generating output achieved in a year by our facilities. We anticipate that our 2009 electric output will be approximately 58,000 GWh. The following table indicates the proportionate share of generating output by fuel type.

| | | | Generation by Fuel Type | | Actual 2008 | | Estimated 2009 (A) |

Nuclear: | | | | |

New Jersey facilities | | | | 36 | % | | | | | 35 | % | |

Pennsylvania facilities | | | | 17 | % | | | | | 16 | % | |

Fossil: | | | | |

Coal: | | | | |

New Jersey facilities | | | | 8 | % | | | | | 11 | % | |

Pennsylvania facilities | | | | 11 | % | | | | | 10 | % | |

Connecticut facilities | | | | 5 | % | | | | | 5 | % | |

Oil and Natural Gas: | | | | |

New Jersey facilities | | | | 18 | % | | | | | 17 | % | |

New York facilities | | | | 5 | % | | | | | 6 | % | |

| | | | |

Total | | | | 100 | % | | | | | 100 | % | |

| | | | |

|

(A) | | | | No assurances can be given that actual 2009 output by source will match estimates. |

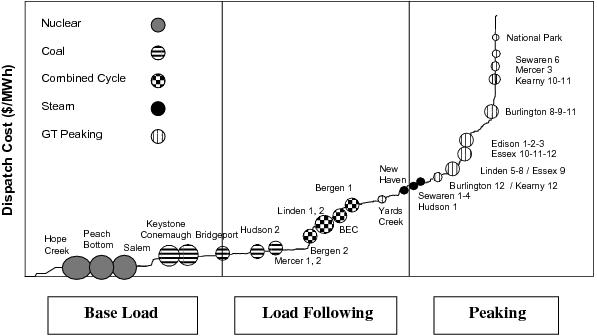

| | | Generation Dispatch | Our generation units are typically characterized as serving one or more of the three general energy market segments: base load; load following; and peaking, based on their operating capability and performance. On a capacity basis, our portfolio of generation assets consists of 35% base load, 43% load following and 22% peaking. This diversity serves to reduce the risk associated with market demand cycles and allows us to participate in the market at each segment of the dispatch curve.

| | | Base Load Unitsare the largest and most efficient units that we operate. These units operate whenever they are available. These units generally derive revenues from energy and capacity sales. Operating costs are low due to the combination of high efficiency and the use of coal and nuclear fuels, which have generally been lower in cost relative to oil or natural gas. Performance is generally measured by the unit’s “capacity factor,” or the ratio of the actual output to the theoretical maximum output. During 2008, our base load coal unit average capacity factor was 86.2%. Our base load nuclear unit capacity factors were as follows: | | | Unit | | Capacity

Factor |

Salem Unit 1 | | | | 89.9 | % | |

Salem Unit 2 | | | | 81.2 | % | |

Hope Creek | | | | 100.8 | % | |

Peach Bottom Unit 2 | | | | 87.4 | % | |

Peach Bottom Unit 3 | | | | 98.2 | % | |

No assurances can be given that these capacity factors will be achieved in the future.

5

|

¡ | | | | Load Following Unitsare generally less efficient than base load units. These units generally operate between 20% and 80% of the time. The operating costs are generally higher per unit of output due to lower efficiency and/or the use of higher cost fuels such as oil and natural gas. They operate less frequently than base load units and generally derive revenues from energy, capacity and ancillary services. |

|

¡ | | | | Peaking Unitsare the least efficient units, run the least amount of time, and generally utilize higher-priced fuels. These units generally operate less than 20% of the time. Costs per unit of output tend to be much higher than that of base load units. The majority of a peaking unit’s revenues is from capacity and ancillary service sales. The characteristics of these units enable them to capture energy revenues during periods of high energy prices. |

|

| | | | In the energy markets in which we operate, owners of power plants generally specify to the ISO prices at which they are prepared to generate and sell energy based on the marginal cost of generating energy from each individual unit. The ISOs will generally dispatch in merit order, calling on the lowest variable cost units first and dispatching progressively higher-cost units until the point that the entire system demand for power (known as the system “load”) is satisfied. Base load units are generally dispatched first, with load following units next, followed by peaking units. The following illustrative chart depicts the order of dispatch of our units based on their dispatch cost: |

Our Generation Facilities Along Dispatch Curve

The bid price of the last unit dispatched by an ISO establishes the energy market-clearing price. In PJM, after considering the market-clearing price and the effect of transmission, congestion and other factors, the ISO calculates the locational marginal pricing (LMP) for every generation facility. The ISO pays all units that are dispatched their respective LMP for each MWh of energy produced, regardless of their specific bid prices. Since bids generally approximate the marginal cost of production, units with lower marginal costs generate higher operating profits than units with comparatively higher marginal costs.

During periods when one or more parts of the transmission grid are operating at full capability, resulting in a constraint on the transmission system, it may not be possible to dispatch units in merit order without violating transmission reliability standards. Under such circumstances, the ISO will dispatch higher-cost

6

generation out of merit order within the congested area and power suppliers will be paid an increased LMP in congested areas, reflecting the bid prices of those higher-cost generation units.

This method of determining supply and pricing creates an environment in the markets in which Power participates where natural gas prices have often had a major impact on the price that generators will receive for their output, especially in periods of relatively strong demand. As such, significant changes in the price of natural gas will often translate into significant changes in the price of electricity.

For example, the price of natural gas at the Henry Hub terminal increased from an average of about $3 per MMBtu in 2002 to about $9 per MMBtu on average in 2008. Similarly, the electricity spot price quoted at the PJM West market increased from an average of about $25 per MWh for 2002 to an average of about $70 per MWh in 2008. The prices at which transactions are entered into for future delivery of these products also are volatile, as evidenced by the market for forward contracts at points such as PJM West. The historical annual spot prices and forward calendar prices as averaged over a year are reflected in the graphs below.

7

The prices reflected in the tables above do not necessarily illustrate our contract prices, but they are representative of market prices at relatively liquid hubs, with nearer-term forward pricing generally resulting from more liquid markets than pricing for later years. In addition, the prices do not reflect locational differences resulting from congestion or other factors which can be considerable. While these prices provide some perspective on past and future prices, the forward prices are highly volatile and there is no assurance that such prices will remain in effect nor that we will be able to contract output at these forward prices.

Fuel Supply

|

• | | | | Nuclear Fuel Supply—To run our nuclear units we have long-term contracts for nuclear fuel. These contracts provide for: |

| | | purchase of uranium (concentrates and uranium hexafluoride); | |

¡ | | | | conversion of uranium concentrates to uranium hexafluoride; |

|

¡ | | | | enrichment of uranium hexafluoride; and |

|

¡ | | | | fabrication of nuclear fuel assemblies. |

|

• | | | | Coal Supply—Coal is the primary fuel for our Hudson, Mercer, Keystone, Conemaugh and Bridgeport stations. We have contracts with numerous suppliers. Coal is delivered to our units through a combination of rail, truck, barge or ocean shipments. |

|

| | | | In order to minimize emissions levels, our Bridgeport 3 and Hudson units use a specific type of coal obtained from Indonesia. If the supply from Indonesia or equivalent coal from other sources was not available for these facilities, their near-term operations would be adversely impacted. In the longer-term, additional material capital expenditures would be required to modify our Bridgeport 3 station to enable it to operate using a broader mix of coal sources. |

|

| | | | Recent volatility in the price of coal has prompted action by coal suppliers to attempt to renegotiate contracts. In particular, the Indonesian government requested that one of its domestic suppliers renegotiate its contracts with us to reflect more current market prices based on certain coal indexes. We reached an agreement with this supplier, which has resulted in an adjustment to the pricing, volumes and term of our contract. |

|

| | | | We are constructing pollution control equipment at Hudson and Mercer that is designed to provide more flexibility in the types of coal we can use at those stations. |

|

• | | | | Gas Supply—Natural gas is the primary fuel for the bulk of our load following and peaking fleet. We purchase gas directly from natural gas producers and marketers. These supplies are transported to New Jersey by four interstate pipelines with whom we have contracted. |

|

| | | | We have one billion cubic feet-per-day of firm transportation capacity under contract to meet the primary gas supply needs of our generation fleet and our obligations under the BGSS contract. We supplement that supply with a total storage capacity of 80 billion cubic feet. |

|

• | | | | Oil—Oil is used as the primary fuel for two load following steam units and nine combustion turbine peaking units and can be used as an alternate fuel by several load following and peaking units that have dual-fuel capability. Oil is purchased on the spot market and delivered by truck, barge, or pipeline. |

We expect to be able to meet the fuel supply demands of our customers and our own operations. However, the ability to maintain an adequate fuel supply could be affected by several factors not within our control, including changes in prices and demand, curtailments by suppliers, severe weather and the availability of feedstocks for the production of supplements to the natural gas supply. For additional information, see Item 7. MD&A—Overview of 2008 and Future Outlook and Note 11. Commitments and Contingent Liabilities.

8

Markets and Market Pricing

In the Northeast and Mid Atlantic U.S., there are three centralized, competitive electricity markets now being operated by ISO organizations:

|

• | | | | PJM Regional Transmission Organization—PJM conducts the largest centrally dispatched energy market in North America. It serves nearly 17% of the total U.S. population and has a peak demand of over 139,000 MW. The PJM Interconnection coordinates the movement of electricity through all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia. All of Power’s generating stations, except for the Bethlehem Energy Center (BEC) and the Bridgeport and New Haven stations, operate in PJM. |

|

• | | | | New York—The New York ISO is the market coordinator for New York State and is now responsible for managing the New York power pool and for administering its energy marketplace. This service area has a population of about 19 million and a peak demand of over 32,000 MW. Power’s BEC operates in New York. |

|

• | | | | New England—ISO New England is responsible for managing the New England Power Pool which covers Maine, New Hampshire, Vermont, Massachusetts, Connecticut and Rhode Island. This service area has a population of about 14 million and a peak demand of over 26,000 MW. Power’s Bridgeport and New Haven stations operate in Connecticut. |

The pricing of electricity varies by location in each of these markets. Depending upon our production and our obligations, these price differentials can serve to increase or decrease our profitability.

Commodity prices, such as electricity, gas, coal and emissions, as well as the availability of our diverse fleet of generation units to produce these products also have a considerable effect on our profitability. These commodity prices have been, and continue to be, highly volatile.

Since the majority of the power we generate is sourced from lower-cost nuclear and coal units, the rise in electric prices in recent years has yielded higher margins for us. Over a longer-term horizon, if these higher prices are sustained at the levels indicated by the current forward markets, we expect to have an attractive environment in which to contract for the sale of our anticipated output. However, higher prices also increase the cost of replacement power, thereby placing us at risk should any of our generating units fail to function effectively or otherwise become unavailable.

In addition to energy sales, we also earn revenue from capacity payments, through which we are compensated for committing that a portion of our capacity be available to the ISO for dispatch at its discretion. Capacity payments reflect the value to the ISO that at any time there is assurance that sufficient generating capacity is available to meet system reliability and energy requirements. Currently, there is sufficient capacity in the markets in which we operate. However, in certain areas of these markets there are transmission system constraints, raising concerns about reliability and creating a more acute need for capacity. Some generators, including us, announced the retirement of certain older generating facilities in these constrained areas due to insufficient revenues to support their continued operation. To enable the continued availability of these facilities, in separate instances, both PJM and the New England Power Pool (NEPOOL) agreed to enter into Reliability-Must-Run (RMR) contracts to compensate us for those units’ contribution to reliability. By providing for such a payment structure, the ISOs have acknowledged that these units provide a reliability service that is not otherwise compensated for in the existing markets.

Through the implementation of the Reliability Pricing Model (RPM) (the market design for capacity payments in PJM) and the Forward Capacity Market (FCM) (in NEPOOL), the markets in which we operate have changed to provide for a more structured, forward-looking, transparent pricing mechanism. This change is aimed at providing greater clarity regarding the value of capacity, resulting in an improved pricing signal to prospective investors in new generating facilities so as to encourage expansion of capacity to meet future market demands.

9

The prices to be received by generating units in PJM for capacity have been set through RPM base residual auctions based on the zone in which the generating unit is located. The majority of our PJM generating units are located in zones where the following prices have been set.

| | | | |

Delivery Year | | MW-day | | kW-yr |

June 2007 to May 2008 | | | $ | | 197.67 | | | | $ | | 72.15 | |

June 2008 to May 2009 | | | $ | | 148.80 | | | | $ | | 54.31 | |

June 2009 to May 2010 | | | $ | | 191.32 | | | | $ | | 69.83 | |

June 2010 to May 2011 | | | $ | | 174.29 | | | | $ | | 63.62 | |

June 2011 to May 2012 | | | $ | | 110.00 | | | | $ | | 40.16 | |

The zone in which our Keystone and Conemaugh units are located experienced fewer constraints on the system, resulting in prices lower than the prices for the rest of our generating assets in the first three auctions. This was not the case for the periods from June 2010 to May 2012 when identical prices were set for all zones.

The price that must be paid by an entity serving load in the various zones is also set through these auctions. These prices can be higher or lower than the prices noted in the table above due to import and export capability to and from lower-priced areas.

The majority of our generating capacity has experienced increases in value from the recent changes in market designs, resulting in significant additional revenue. We cannot determine the long-term sustainability of these market design changes.

On a prospective basis, many factors will affect the capacity pricing in PJM, including but not limited to:

|

• | | | | changes in load and demand; |

|

• | | | | changes in the available amounts of demand response resources; |

|

• | | | | changes in available generating capacity (including retirements, additions, derates, forced outage rates, etc.); |

|

• | | | | increases in transmission capability between zones; and |

|

• | | | | changes to the pricing mechanism, including increasing the potential number of zones to create more pricing sensitivity to changes in supply and demand, as well as other potential changes that PJM may propose over time. |

For additional information on our collection of RMR payments in PJM and NEPOOL and the RPM and FCM proposals, see Regulatory Issues—Federal Regulation.

Hedging Strategy

In an attempt to mitigate volatility in our results, we seek to contract in advance for a significant portion of our anticipated electric output, capacity and fuel needs. We seek to sell a portion of our anticipated lower-cost nuclear and coal-fired generation over a multi-year forward horizon, normally over a period of two to three years. We believe this hedging strategy increases stability of earnings.

Among the ways in which we hedge our output are: (1) sales at PJM West and (2) BGS contracts. The BGS-Fixed Price contract, a full requirements contract that includes energy and capacity, ancillary and other services, is awarded for three-year periods through an auction process managed by the New Jersey Board of Public Utilities (BPU). The volume of BGS contracts and the electric utilities our generation operations will serve vary from year to year. Pricing for the BGS contracts for recent and future periods by purchasing utility, including a capacity component, is as follows:

10

| | | | | | | | | | |

Load Zone ($/MWh) | | 2005-2008 | | 2006-2009 | | 2007-2010 | | 2008-2011 | | 2009-2012 |

PSE&G | | | $ | | 65.41 | | | | $ | | 102.51 | | | | $ | | 98.88 | | | | $ | | 111.50 | | | | $ | | 103.72 | |

Jersey Central Power and Light | | | $ | | 65.70 | | | | $ | | 100.44 | | | | $ | | 99.64 | | | | $ | | 114.09 | | | | $ | | 103.51 | |

Atlantic City Electric | | | $ | | 66.48 | | | | $ | | 103.99 | | | | $ | | 99.59 | | | | $ | | 116.50 | | | | $ | | 105.36 | |

Rockland Electric Company | | | $ | | 71.79 | | | | $ | | 111.14 | | | | $ | | 109.99 | | | | $ | | 120.49 | | | | $ | | 112.70 | |

A portion of our total generation capacity is allocated in the BGS contract through the BGS auctions. On average, tranches won in the BGS auctions require 100 MW to 120 MW of capacity on a daily basis. In addition, we hedged a portion of our generation capacity with forward capacity sales contracts.

The capacity prices we contracted for in the 2005-2008 BGS auctions and through some of the forward sales contracts were set prior to the implementation of RPM capacity auctions and therefore do not reflect the capacity prices determined more recently in the RPM capacity auctions. As a result, we were unable to fully realize such pricing for some of our generating capacity. As these older contracts expire, we expect revenues to increase as we realize the RPM auction pricing.

We have obtained price certainty for all of our PJM and New England capacity through May 2012 through these mechanisms.

To support our contracted sales of energy, we also entered into contracts for the future purchase and delivery of nuclear fuel and coal, which include some market-based pricing components. As of February 10, 2009, we had contracted for the following percentages of our nuclear and coal generation output and related fuel supplies for the next three years with modest amounts beyond 2011.

| | | | | | |

Nuclear and Coal Generation | | 2009 | | 2010 | | 2011 |

Generation Sales | | 100% | | 70%-80% | | 30%-50% |

Nuclear Fuel | | 100% | | 100% | | 100% |

Coal Supply and Transportation | | 90%-100% | | 15%-25% | | 0%-25% |

We take a more opportunistic approach in hedging our anticipated natural gas-fired generation. The generation from these units is less predictable, as these units are generally dispatched when aggregate market demand has exceeded the supply provided by lower-cost units. The natural gas-fired units have generally provided a lower contribution to our margin than either the nuclear or coal units. We purchase natural gas when gas-fired generation is required to supply forward sale commitments.

In a changing market environment, this hedging strategy may cause our realized prices to differ materially from current market prices. In a rising price environment, this strategy normally results in lower margins than would have been the case if little or no hedging activity had been conducted. Alternatively, in a falling price environment, this hedging strategy will tend to create margins higher than those implied by the then current market.

11

PSE&G

Our regulated public utility, PSE&G, distributes electric energy and gas to customers within a designated service territory running diagonally across New Jersey where approximately 5.5 million people, or about 70% of the State’s population, reside.

Products and Services

Our utility operations primarily earn margins through the transmission and distribution of electricity and the distribution of gas.

|

• | | | | Transmission—is the movement of electricity at high voltage from generating plants to substations and transformers, where it is then reduced to a lower voltage for distribution to homes, businesses and industrial customers. Our revenues for these services are based upon tariffs approved by the Federal Energy Regulatory Commission (FERC). |

|

• | | | | Distribution—is the delivery of electricity and gas to the retail customer’s home, business or industrial facility. Our revenues for these services are based upon tariffs approved by the BPU. |

We also earn margins through non-tariff competitive services, such as appliance repair services. The commodity supply portion of our utility business’ electric and gas sales are managed by BGS and BGSS suppliers. Pricing for those services are set by the BPU as a pass-through, resulting in no margin for our utility operations.

In addition to our current utility products and services, we have proposed several programs to improve efficiencies in customer energy use and increase the level of renewable generation to be constructed and owned by us including:

|

¡ | | | | a program approved in 2008 to help finance the installation of 30 MW of solar power systems throughout our electric service area, |

|

¡ | | | | a new proposal to develop 120 MW of solar power systems over five years, |

12

|

¡ | | | | a proposed energy efficiency stimulus initiative to encourage conservation and energy efficiency and to provide energy and money saving measures directly to businesses and families, and |

|

¡ | | | | a small scale carbon abatement program designed to promote energy efficiency. |

For additional information concerning these proposed programs and the components of our tariffs, see Regulatory Issues.

How PSE&G Operates

Transmission

In September 2008, we received FERC approval to use formula transmission rates, effective October 1, 2008, for our existing and future transmission investments. Formula-type rates provide a method of rate recovery where the transmission owner annually determines its revenue requirements through a fixed formula which considers Operations and Maintenance expenditures, Rate Base and capital investments and applies an approved return on equity (ROE). Currently, approved rates provide for a ROE of 11.68% on existing and new transmission investment. FERC has also approved incentive rate treatment for the Susquehanna-Roseland line, which when added to the approved base ROE, will yield a ROE of 12.93% for this particular project. We will also earn this ROE on Construction Work In Progress (CWIP) dollars spent on this project.

| | | | |

Transmission Statistics |

December 31, 2008 | | Historical Annual

Growth 2004-2008 |

Network Circuit Miles | | Billing Peak (MW) |

1,429 | | 10,654 | | 1.60% |

For more information on current transmission construction activities, see Regulatory Issues, Federal Regulation—Transmission Regulation.

Distribution

All electric and gas customers in New Jersey have the ability to choose their own electric energy and/or gas supplier. However, pursuant to BPU requirements, we serve as the supplier of last resort for electric and gas customers within our service territory who have no other supplier. As a practical matter, this means we are obligated to provide supply to a vast majority of residential customers and a smaller portion of commercial and industrial customers.

The percentage of customers we serve as compared to that served by third party suppliers has been reasonably stable over the past several years. As shown in the table below, we continue to provide the electric energy and gas supply for the majority of the customers in our service territory for the year ended December 31, 2008.

| | | | | | | | |

| | Electric | | Gas |

| | GWh | | % | | Million

Therms | | % |

PSE&G | | | | 33,702 | | | | | 77 | % | | | | | 2,139 | | | | | 62 | % | |

Third Party Suppliers | | | | 10,018 | | | | | 23 | % | | | | | 1,302 | | | | | 38 | % | |

| | | | | | | | |

Total Delivered | | | | 43,720 | | | | | 100 | % | | | | | 3,441 | | | | | 100 | % | |

| | | | | | | | |

13

Our load requirements were split during 2008 among residential, commercial and industrial customers, described below. We believe that we have all the non-exclusive franchise rights (including consents) necessary for our electric and gas distribution operations in the territory we serve.

| | | | |

Customer Type | | % of Sales |

| | Electric | | Gas |

Commercial | | | | 57 | % | | | | | 36 | % | |

Residential | | | | 31 | % | | | | | 60 | % | |

Industrial | | | | 12 | % | | | | | 4 | % | |

| | | | |

Total | | | | 100 | % | | | | | 100 | % | |

| | | | |

We procure the supply to meet our BGS obligations through two concurrent auctions authorized by the BPU for New Jersey’s total BGS requirement. These auctions take place annually in February. Results of these auctions determine which energy suppliers are authorized to supply BGS to New Jersey’s electric distribution companies (EDCs). Once validated by the BPU, electricity prices for BGS service are set.

BGSS is the mechanism approved by the BPU designed to recover all gas costs related to the supply for residential customers. BGSS filings are made annually by June 1 of each year, with an effective date of October 1. PSE&G has a full requirements contract through 2012 with Power to meet the supply requirements of our default service gas customers. Gas commodity costs under this contract are recovered from our customers. Any difference between rates charged under the BGSS contract and rates charged to our residential customers is deferred and collected or refunded through adjustments in future rates.

While our customer base has remained steady, electric load has been fairly flat and gas load has declined, as illustrated:

| | | | | | |

Electric and Gas Distribution Statistics |

| | | December 31, 2008 | | Historical Annual

Load Growth

2004-2008 |

| | Number of

Customers | | Electric Sales and Gas

Sold and Transported |

Electric | | | | 2.1 Million | | | 43,720 GWh | | | | 0.08 | % | |

Gas | | | | 1.7 Million | | | 3,441 Million Therms | | | | -3.50 | % | |

Markets and Market Pricing

There continues to be significant volatility in commodity prices. Such volatility can have a considerable impact on us since a rising commodity price environment results in higher delivered electric and gas rates for customers. This may result in decreased demand for both electricity and gas, increased regulatory pressures and greater working capital requirements as the collection of higher commodity costs may be deferred under our regulated rate structure. For additional information see Item 7. MD&A.

Energy Holdings

Through Energy Holdings, we own domestic generation outside of the Mid Atlantic region and own and manage passive energy-related investments. We are also pursuing an offshore wind project and a modest amount of solar and other renewable projects, primarily in our core markets.

Products and Services

We own 2,395 MW of domestic capacity in areas outside of the Mid Atlantic region, of which 2,000 MW comes from two 1,000 MW gas-fired, combined cycle generation facilities in Texas. The majority of our investments in international generation and distribution projects have been sold.

14

Our passive energy-related investments consist primarily of leveraged leases. As of December 31, 2008, the single largest lease investment represented 13% of total leveraged leases.

How Energy Holdings Operates

Approximately 37% of the expected output of our Texas facilities for 2009 has been sold via bilateral agreements. Additional bilateral sales for peak and off-peak services are expected to be signed as the year progresses. Any remaining uncommitted economic output will be offered in the Texas spot market. Included in these bilateral agreements is a 350 MW daily capacity call option at Odessa that expires on December 31, 2010.

In August 2008, we invested in a joint venture to further develop compressed air energy storage (CAES) technology. CAES technology stores energy in the form of compressed air by injection into underground caverns or above ground storage facilities which can then be released to generate electricity through specialized turbine equipment. This technology could be used to optimize an intermittent energy source, such as wind, by storing energy at night and releasing this stored energy during the day when customers need power. Our plan is to use the technology to develop CAES power plants and sell licenses to third parties to implement CAES technology.

In October 2008, the New Jersey Office of Clean Energy (OCE) awarded a $4 million grant to a joint venture owned equally by one of our subsidiaries and an unaffiliated private developer, to advance the development of a 350 MW wind farm to be located approximately 16 miles off the shore of southern New Jersey. An offshore wind farm has not yet been developed and constructed in the U.S. Numerous issues, including federal and state permitting, environmental impacts, power output sale arrangements, construction approach and expected maintenance costs, will need to be worked through in order to successfully develop such a project. If these issues are satisfactorily addressed and the joint venture decides to proceed, the wind farm could be fully operational in 2013.

Our leasing portfolio is designed to provide a fixed rate of return. Income on leveraged leases is recognized by a method which produces a constant rate of return on the outstanding investment in the lease, net of the related deferred tax liability, in the years in which the net investment is positive. Any gains or losses incurred as a result of a lease termination are recorded as Operating Revenues as these events occur in the ordinary course of business of managing the investment portfolio.

Leveraged lease investments involve three parties: an owner/lessor, a creditor and a lessee. In a typical leveraged lease financing, the lessor purchases an asset to be leased. The purchase price is typically financed 80% with debt provided by the creditor and the balance comes from equity funds provided by the lessor. The creditor provides long-term financing to the transaction secured by the property subject to the lease. Such long-term financing is non-recourse to the lessor and, with respect to our lease investments, is not presented in our Consolidated Balance Sheets.

The lessor acquires economic and tax ownership of the asset and then leases it to the lessee for a period of time no greater than 80% of its remaining useful life. As the owner, the lessor is entitled to depreciate the asset under applicable federal and state tax guidelines. The lessor receives income from lease payments made by the lessee during the term of the lease and from tax benefits associated with interest and depreciation deductions with respect to the leased property. The ability to realize these tax benefits is dependent on operating gains generated by our other operating subsidiaries and allocated pursuant to the consolidated tax sharing agreement between us and our operating subsidiaries. During 2008, we recorded after-tax charges of $490 million related to tax deductions previously claimed for certain of these leases that were recently disallowed by the Internal Revenue Service (IRS). See Note 11. Commitments and Contingent Liabilities for further discussion.

Lease rental payments are unconditional obligations of the lessee and are set at levels at least sufficient to service the non-recourse lease debt. The lessor is also entitled to any residual value associated with the leased asset at the end of the lease term. An evaluation of the after-tax cash flows to the lessor determines the return on the investment. Under GAAP, the lease investment is recorded net of non-recourse debt and income is recognized as a constant return on the net unrecovered investment.

15

For additional information on leases, including the credit, tax and accounting risks related to certain lessees, see Item 1A. Risk Factors, Item 7. MD&A—Results of Operations—Energy Holdings, Item 7A. Qualitative and Quantitative Disclosures About Market Risk—Credit Risk—Energy Holdings and Note 11. Commitments and Contingent Liabilities.

Markets and Market Pricing

Our generation business in Texas is a merchant generation business located in the Electric Reliability Council of Texas (ERCOT) market. In balancing energy and ancillary service markets, an ISO will generally dispatch the lowest bids first unless local transmission congestion requires units to be dispatched out of merit order. The price that all dispatched units receive is set by the last, or marginal bidder that is dispatched. Our Texas generation assets are combined cycle gas-fired generation units and generally have lower variable costs than less efficient single cycle gas and oil-fired generation units. As a result, during on-peak periods, the price of power in ERCOT is frequently set by generation units with higher variable costs than our Texas generation assets. Unlike the other markets in which we compete, ERCOT does not have a capacity market, and as a result, all generators are compensated solely through energy revenues and revenues for ancillary services, which are subject to substantial volatility as power prices fluctuate.

ERCOT has decided to delay a proposed transition from a zonal market to a nodal wholesale market until the fourth quarter of 2010 at the earliest. As proposed, the redesigned grid will consist of more than 4,000 nodes replacing the current four congestion management zones. The implementation of the new design is expected to deliver improved price signals, improved dispatch efficiencies and direct assignment of local congestion. We will continue to evaluate the potential impact this change will have on our Texas generation facilities once implemented.

COMPETITIVE ENVIRONMENT

Power

Various market participants compete with us and one another in buying and selling in wholesale power pools, entering into bilateral contracts and selling to aggregated retail customers. Our competitors include:

|

• | | | | merchant generators, |

|

• | | | | domestic and multi-national utility generators, |

|

• | | | | energy marketers, |

|

• | | | | banks, funds and other financial entities, |

|

• | | | | fuel supply companies, and |

|

• | | | | affiliates of other industrial companies. |

Our business is also under competitive pressure due to demand side management (DSM) and other efficiency efforts aimed at changing the quantity and patterns of usage by consumers which could result in a reduction in load requirements. A reduction in load requirements can also be caused by economic cycles and factors. It is also possible that advances in technology, such as distributed generation, will reduce the cost of alternative methods of producing electricity to a level that is competitive with that of most central station electric production. To the extent that additions to the transmission system relieve or reduce congestion in eastern PJM where most of our plants are located, our revenues could be adversely affected. In addition, pressures from renewable resources, such as wind and solar, could increase over time, especially if government incentive programs continue to grow.

We are also at risk if one or more states in which we operate should decide to turn away from competition and allow regulated utilities to continue to own or reacquire and operate generating stations in a regulated and potentially uneconomical manner, or to encourage rate-based generation for the construction of new base load units. This has occurred in certain states. The lack of consistent rules in energy markets can negatively impact the competitiveness of our plants. Also, regional inconsistencies in environmental regulations, particularly those related to emissions, have put some of our plants which are located in the

16

Northeast, where rules are more stringent, at an economic disadvantage compared to our competitors in certain Midwest states.

Also, environmental issues such as restrictions on carbon dioxide (CO2) emissions and other pollutants may have a competitive impact on us to the extent it is more expensive for our plants to remain compliant, thus affecting our ability to be a lower-cost provider compared to competitors without such restrictions.

PSE&G

The electric and gas transmission and distribution business has minimal risks from competitors. Our transmission and distribution business is minimally impacted when customers choose alternate electric or gas suppliers since we earn our return by providing transmission and distribution service, not by supplying the commodity. The demand for electric energy and gas by customers is affected by customer conservation, economic conditions, weather and other factors not within our control.

Energy Holdings

New additions of lower cost or more efficient generation capacity in Texas could make our plants in the region less economical in the future. A number of competitors have announced plans to build additional coal-fired and gas-fired generation capacity in ERCOT. Although it is not clear if this capacity will be built or, if so, what the economic impact will be, such additions could impact market prices and our competitiveness.

Over the past several years, substantial amounts of wind generation capacity have been constructed in ERCOT, particularly in western Texas, where our Odessa generation facility is located. At the end of 2008, ERCOT had approximately 8,000 MW of installed wind capacity. Given the favorable wind conditions in western Texas, these wind generation facilities are able to produce power during a substantial period of the year, resulting in an additional source of base load power in western Texas, especially during off-peak seasons.

While numerous competitors have announced plans to build substantial amounts of new wind generation capacity, an issue impacting the likelihood of these projects being built is the constrained amount of transmission capacity between western Texas, where wind generation units are typically sited but where power demand is relatively low, and the rest of Texas.

The Public Utility Commission of Texas (PUCT) has designated five Competitive Renewable Energy Zones in western Texas and the Texas Panhandle in an effort to address the constraint issue. The PUCT has requested that ERCOT develop transmission construction options within these zones that would allow for much greater levels of delivery of wind power from western Texas to customers throughout the ERCOT grid. Although it is not clear if these efforts at transmission expansion will be successful or, if so, what the economic impact will be, it is possible that substantial additional amounts of wind generation will be built in ERCOT as a result of such potential transmission expansion, which could impact market prices and our competitiveness.

EMPLOYEE RELATIONS

The following table provides summarized information about our employees as of December 31, 2008. We believe that we maintain satisfactory relationships with our employees.

| | | | | | | | |

Employees as of December 31, 2008 |

| | Power | | PSE&G | | Energy

Holdings | | Services |

Non-Union | | | | 1,126 | | | | | 1,231 | | | | | 112 | | | | | 1,032 | |

Union | | | | 1,412 | | | | | 4,838 | | | | | — | | | | | 98 | |

| | | | | | | | |

Total Employees | | | | 2,538 | | | | | 6,069 | | | | | 112 | | | | | 1,130 | |

| | | | | | | | |

Number of Union Groups | | | | 3 | | | | | 4 | | | | | n/a | | | | | 1 | |

Bargaining Agreement Expiration Year | | | | 2011 | | | | | 2011 | | | | | n/a | | | | | 2011 | |

17

REGULATORY ISSUES

Federal Regulation

FERC

The FERC is an independent federal agency that regulates the transmission of electric energy and gas in interstate commerce and the sale of electric energy and gas at wholesale pursuant to the Federal Power Act (FPA) and the Natural Gas Act. PSE&G and certain subsidiaries of Power and Energy Holdings are public utilities as defined by the FPA. By virtue of its regulation of (a) interstate electric and gas transmission and (b) wholesale sales of electricity and gas, the FERC has extensive oversight over “public utilities” as defined by the FPA. FERC approval is usually required when a “public utility” company seeks to: sell or acquire an asset that is regulated by the FERC (such as a transmission line or a generating station); collect costs from customers associated with a new transmission facility; charge a rate for wholesale sales under a contract or tariff; or engage in certain mergers and internal corporate reorganizations.

The FERC also regulates generating facilities known as qualifying facilities (QFs). QFs are cogeneration facilities that produce electricity and another form of useful thermal energy, or small power production facilities where the primary energy source is renewable, biomass, waste, or geothermal resources. QFs must meet certain ownership, operating and efficiency criteria established by the FERC. Through Energy Holdings, we own several QF plants. QFs are subject to many, but not all, of the same FERC requirements as public utilities.

For us, the major effects of FERC regulation fall into four general categories:

|

• | | | | Regulation of Wholesale Sales—Generation/Market Issues |

|

• | | | | Capacity Market Issues |

|

• | | | | Transmission Regulation |

|

• | | | | Compliance |

Regulation of Wholesale Sales—Generation/Market Issues

|

• | | | | Market Power—Under FERC regulations, public utilities must receive FERC authorization to sell power in interstate commerce. They can sell power at cost-based rates or apply to the FERC for authority to make market based rate (MBR) sales. For a requesting company to receive MBR authority, the FERC must first make a determination that the requesting company lacks market power in the relevant markets. The FERC requires that holders of MBR tariffs file an update every three years demonstrating that they continue to lack market power. |

|

| | | | PSE&G and certain subsidiaries of Power and Energy Holdings have received MBR authority from the FERC. Retention of MBR authority is critical to the maintenance of our generation business’ revenues. |

|

| | | | Under new MBR rules issued in 2007, the FERC may look at sub-markets to analyze whether a company possesses market power. Applying these new rules in October 2008, the FERC granted both PSE&G and PSEG Energy Resources & Trade LLC continued MBR authority and granted both PSEG Fossil LLC and PSEG Nuclear LLC initial MBR authority. |

|

• | | | | Cost-Based RMR Agreements—The FERC has permitted public utility generation owners to enter into RMR agreements that provide cost-based compensation to a generation owner when a unit proposed for retirement is asked to continue operating for reliability purposes. Our Hudson 1 generating station is currently operating under an RMR agreement which expires September 2010. However, pursuant to the request of PJM, we will be extending this agreement until September 2011. For additional information, see Note 11. Commitments and Contingent Liabilities. |

18

|

| | | | In NEPOOL, many owners of generation facilities have also filed for RMR treatment. We currently collect FERC-approved monthly payments for the Bridgeport Harbor Station Unit 2 and the New Haven Harbor Station. These agreements are scheduled to expire in June 2010. |

|

| | | | RMR treatment has enabled these units to continue to operate. Various parties have challenged the continuation of RMR payments in NEPOOL, and thus, there is risk that such payments may be terminated prior to the end of the contract terms. |

|

• | | | | Reactive Power—Reactive power encompasses certain ancillary services necessary to maintain voltage support and operate the system. In May 2008, we filed with FERC to increase our annual fixed revenues by $18 million to reflect our provision of reactive power support in PJM. In November 2008, FERC accepted our reactive power rate filing retroactive to May 2008. |

Capacity Market Issues

RPM is a locational installed capacity market design for the PJM region, including a forward auction for installed capacity. Under RPM, generators located in constrained areas within PJM are paid more for their capacity as an incentive to locate in areas where generation capacity is most needed. PJM’s RPM has been challenged in court.

In early 2006, certain interested market participants in New England agreed to a settlement that establishes the design of the region’s market for installed capacity and which is being implemented gradually over four years. Commencing in December 2006, all generators in New England began receiving fixed capacity payments that escalate gradually over the transition period. The market design consists of a forward-looking auction for installed capacity that is intended to recognize the locational value of generators on the system and contains incentive mechanisms to encourage generator availability during generation shortages. Capacity market rules in both PJM and in New England may change in the future.

Transmission Regulation

The FERC has exclusive jurisdiction to establish the rates and terms and conditions of service for interstate transmission. We currently have FERC-approved formula rates in effect to recover the costs of our transmission facilities. Under this formula, rates are put into effect in January of each year based upon our internal forecast of annual expenses and capital expenditures. Rates are then trued up the following year to reflect actual annual expenses/capital expenditures. Our allowed ROE is 11.68% for both existing and new transmission investments, and we have received incentive rates—affording a higher return on equity—for specific transmission investments.

|

• | | | | Transmission Expansion—In June 2007, PJM approved the construction of the Susquehanna-Roseland line, a new 500 kV transmission line intended to maintain the reliability of the electrical grid serving New Jersey customers. PJM assigned construction responsibility for the new line to us and PPL for the New Jersey and Pennsylvania portions of the project, respectively. The estimated cost of our portion of this construction project is approximately $750 million, and PJM has directed that the line be placed into service by June 2012. We have recently filed with the BPU to obtain authorization to construct the Susquehanna-Roseland line. For further discussion, see State Regulation—Energy Policy—Susquehanna-Roseland BPU Petition. |

|

| | | | Construction of the Susquehanna-Roseland line is contingent upon obtaining all necessary federal, state, municipal and landowner permits and approvals. The construction of the line has encountered local opposition. Should the line be cancelled for reasons beyond our control, we will be entitled to recover 100% of prudently-incurred abandonment costs. |

|

| | | | PJM has also approved the construction of a 500 kV transmission line running from Virginia through Maryland and Delaware and is still considering approval of the portion terminating in Salem Township, New Jersey. We will be responsible for constructing and operating a portion of this line, known as the Mid-Atlantic Pathway Project (MAPP), if approved. We have asked the FERC to approve a 150 basis point ROE adder for this project, 100% recovery of abandonment costs and the ability to transfer the project to an affiliate. Several state consumer advocates, including the New |

19

| | | | Jersey Division of Rate Counsel, have opposed the incentive rate filing and have requested that the FERC set the matter for hearing. This filing is pending at the FERC. |

|

| | | | In December 2008, PJM approved another transmission project, including two additional 500 kV transmission lines. The first would run from Branchburg to Roseland, and the second from Roseland to Hudson. These lines are still in the design phase. |

|

| | | | U.S. Department of Energy (DOE) Congestion Study—National Interest Electric Transmission Corridors and FERC Back-Stop Siting Authority—By virtue of the Energy Policy Act enacted by Congress in 2005, the DOE has the ability to designate transmission corridors in areas found to be critical congestion areas, which then gives the FERC the ability to site transmission projects within these corridors should certain events occur. |

|

| | | | In October 2007, the DOE acted to designate transmission corridors within these critical congestion areas. One of the designated corridors is the Mid-Atlantic Area National Corridor. Thus, entities seeking to build transmission within the Mid-Atlantic Area Corridor, which includes New Jersey, most of Pennsylvania and New York, may be able to use the FERC’s back-stop siting authority in the future under certain circumstances, if necessary, to site transmission, including with respect to the Susquehanna-Roseland line. On February 18, 2009, the United States Court of Appeals for the Fourth Circuit narrowed the scope of the FERC’s back-stop siting authority, which may lead to future legislative changes in this area. |

Compliance

|

• | | | | Reliability Standards—Congress has required the FERC to put in place, through the North American Electric Reliability Council (NERC), national and regional reliability standards to ensure the reliability of the U.S. electric transmission and generation system and to prevent major system blackouts. Many reliability standards have been developed and approved. Since these standards are mandatory and applicable to, among other entities, transmission owners and generation owners and operators, and thus several of our operating subsidiaries, we are obligated to comply with the standards and to ensure continuing compliance. In 2008, our Texas generation plants were audited for NERC Reliability Standards and were found to be in compliance. PSE&G was also audited for NERC Reliability Standards compliance in November 2008, and we are awaiting a final determination on the audit. |

|

• | | | | FERC Standards of Conduct—On October 16, 2008, FERC issued a revised rule governing the interaction between transmission provider employees and wholesale merchant employees, which revises FERC’s Standards of Conduct by abandoning the “corporate” separation approach to regulating these interactions and instead adopting an “employee function” approach, which focuses on an individual employee’s job functions in determining how the rules will apply. The effect of these rules will be to permit more affiliate communication with respect to corporate and strategic planning, to loosen restrictions on senior officers and directors and to permit necessary operational communications between those employees engaged in transmission system operations and planning and those employees engaged in generating plant operations. This rule became effective in November 2008, with full compliance required by the FERC during the first quarter of 2009. We expect to be able to comply with these new rules. |

Nuclear Regulatory Commission (NRC)

Our operation of nuclear generating facilities is subject to comprehensive regulation by the NRC, a federal agency established to regulate nuclear activities to ensure protection of public health and safety, as well as the security and protection of the environment. Such regulation involves testing, evaluation and modification of all aspects of plant operation in light of NRC safety and environmental requirements. Continuous demonstration to the NRC that plant operations meet requirements is also necessary. The NRC has the ultimate authority to determine whether any nuclear generating unit may operate. We anticipate filing for

20

extensions of operating licenses for the Salem and Hope Creek facilities in 2009. The current operating licenses of our nuclear facilities expire in the years shown below:

| | |

Unit | | Year |

Salem Unit 1 | | | | 2016 | |

Salem Unit 2 | | | | 2020 | |

Hope Creek | | | | 2026 | |

Peach Bottom Unit 2 | | | | 2033 | |

Peach Bottom Unit 3 | | | | 2034 | |

State Regulation

Since our operations are primarily located within New Jersey, our main state regulator is the BPU. The BPU is the regulatory authority that oversees electric and natural gas distribution companies in New Jersey. PSE&G is subject to comprehensive regulation by the BPU including, among other matters, regulation of retail electric and gas distribution rates and service and the issuance and sale of certain types of securities. BPU regulation can also have a direct or indirect impact on our power generation business as it relates to energy supply agreements and energy policy in New Jersey.

We are also subject to some state regulation in California, Connecticut, Hawaii, New Hampshire, New York, Pennsylvania and Texas due to our ownership of generation and transmission facilities in those states.

Rates

|

• | | | | Electric and Gas Base Rates—We must file electric and gas base rate cases with the BPU in order to change PSE&G’s base rates. The BPU also has authority to seek to adjust rates downward if it believes the rates are no longer just and reasonable. Under our current BPU Order, we may not seek new base rates to be effective prior to November 15, 2009. We also must file a joint electric and gas petition for any future base rate increases. We expect to file a joint electric and gas rate case by mid 2009 with a request that rates become effective in 2010. |

|

• | | | | Rate Adjustment Clauses—In addition to base rate determinations, we recover certain costs from customers pursuant to mechanisms, known as adjustment clauses. These permit, at set intervals, the flow-through of costs to customers related to specific programs, outside the context of base rate case proceedings. Recovery of these costs are subject to BPU approval. Costs associated with these programs are deferred when incurred and amortized to expense when recovered in revenues. Delays in the pass-through of costs under these clauses can result in significant changes in cash flow. Our SBC and NGC clauses are detailed in the following table: |

| | | | |

Rate Clause | | 2008 Revenue | | (Over) Under Recovered

Balance

as of December 31, 2008 |

| | | | Millions |

Energy Efficiency and Renewable Energy | | | $ | | 179 | | | | $ | | 9 | |

RAC | | | | 16 | | | | | 134 | |

USF | | | | 152 | | | | | 34 | |

Social Programs | | | | 33 | | | | | 32 | |

| | | | |

Total SBC | | | | 380 | | | | | 209 | |

NGC | | | | 59 | | | | | (9 | ) | |

| | | | |

Total | | | $ | | 439 | | | | $ | | 200 | |

| | | | |

|

| | | | Societal Benefits Charges (SBC)—The SBC is a mechanism designed to ensure recovery of costs associated with activities required to be accomplished to achieve specific government-mandated |

21