U.S. Securities and Exchange Commission

Washington, DC 20549

NOTICE OF EXEMPT SOLICITATION

1. Name of the Registrant: Charles River Laboratories International, Inc.

2. Name of person relying on exemption: JANA Partners LLC

3. Address of person relying on exemption: 767 Fifth Avenue, 8th Floor, New York, New York 10153

4. Written materials. Attach written material required to be submitted pursuant to Rule 14a-6(g)(1)

Presentation to ISS Group: Proposed Acquisition of WuXi

Pharmatech (“WX”) by Charles River Laboratories (“CRL”)

Pharmatech (“WX”) by Charles River Laboratories (“CRL”)

July 20, 2010

2

THIS PRESENTATION IS FOR GENERAL INFORMATIONAL PURPOSES FOR ISS GROUP ONLY. IT DOES NOT HAVE REGARD TO

THE SPECIFIC INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY, OR THE PARTICULAR NEED OF ANY SPECIFIC PERSON

WHO MAY RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION.

THIS PRESENTATION DOES NOT RECOMMEND THE PURCHASE OR SALE OF ANY SECURITY. THE VIEWS EXPRESSED HEREIN

THE SPECIFIC INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY, OR THE PARTICULAR NEED OF ANY SPECIFIC PERSON

WHO MAY RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION.

THIS PRESENTATION DOES NOT RECOMMEND THE PURCHASE OR SALE OF ANY SECURITY. THE VIEWS EXPRESSED HEREIN

REPRESENT THE OPINIONS OF JANA PARTNERS LLC ("JANA PARTNERS"), WHICH OPINIONS MAY CHANGE AT ANY TIME AND ARE BASED

ON PUBLICLY AVAILABLE INFORMATION WITH RESPECT TO CHARLES RIVER LABORATORIES INTERNATIONAL INC. AND WUXI

PHARMATECH (CAYMAN) INC. (THE “ISSUERS”). CERTAIN FINANCIAL INFORMATION AND DATA USED HEREIN HAVE BEEN DERIVED OR

OBTAINED FROM FILINGS MADE WITH THE SECURITIES AND EXCHANGE COMMISSION (“SEC”) BY THE ISSUERS OR OTHER COMPANIES

JANA PARTNERS CONSIDERS COMPARABLE, AND FROM OTHER THIRD PARTY REPORTS.

QUOTATION OF ANALYSTS HEREIN DOES NOT NECESSARILY INDICATE THAT SUCH ANALYSTS SUPPORT THE VIEWS EXPRESSED

HEREIN. JANA PARTNERS HAS NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO THE USE OF PREVIOUSLY

PUBLISHED INFORMATION AND ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF

SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN. NO WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED

OR OBTAINED FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE.

HEREIN. JANA PARTNERS HAS NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO THE USE OF PREVIOUSLY

PUBLISHED INFORMATION AND ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF

SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN. NO WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED

OR OBTAINED FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE.

JANA PARTNERS SHALL NOT BE RESPONSIBLE OR HAVE ANY LIABILITY FOR ANY MISINFORMATION CONTAINED IN ANY SEC FILING OR

THIRD PARTY REPORT. THERE IS NO ASSURANCE OR GUARANTEE WITH RESPECT TO THE PRICES AT WHICH ANY SECURITIES OF THE

ISSUERS WILL TRADE, AND SUCH SECURITIES MAY NOT TRADE AT PRICES THAT MAY BE IMPLIED HEREIN. THE ESTIMATES,

PROJECTIONS, PRO FORMA INFORMATION AND POTENTIAL IMPACT OF TRANSACTIONS DISCUSSED HEREIN ARE BASED ON

ASSUMPTIONS WHICH JANA PARTNERS BELIEVES TO BE REASONABLE, BUT THERE CAN BE NO ASSURANCE OR GUARANTEE THAT

ACTUAL RESULTS OR PERFORMANCE OF THE ISSUERS WILL NOT DIFFER, AND SUCH DIFFERENCES MAY BE MATERIAL. JANA

PARTNERS DISCLAIMS ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN.

THIRD PARTY REPORT. THERE IS NO ASSURANCE OR GUARANTEE WITH RESPECT TO THE PRICES AT WHICH ANY SECURITIES OF THE

ISSUERS WILL TRADE, AND SUCH SECURITIES MAY NOT TRADE AT PRICES THAT MAY BE IMPLIED HEREIN. THE ESTIMATES,

PROJECTIONS, PRO FORMA INFORMATION AND POTENTIAL IMPACT OF TRANSACTIONS DISCUSSED HEREIN ARE BASED ON

ASSUMPTIONS WHICH JANA PARTNERS BELIEVES TO BE REASONABLE, BUT THERE CAN BE NO ASSURANCE OR GUARANTEE THAT

ACTUAL RESULTS OR PERFORMANCE OF THE ISSUERS WILL NOT DIFFER, AND SUCH DIFFERENCES MAY BE MATERIAL. JANA

PARTNERS DISCLAIMS ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN.

JANA PARTNERS AND ITS AFFILIATES CURRENTLY HOLD A SUBSTANTIAL AMOUNT OF SHARES OF COMMON STOCK OF CHARLES RIVER

LABORATORIES INTERNATIONAL INC. AND JANA PARTNERS IS IN THE BUSINESS OF INVESTING IN AND TRADING SECURITIES. JANA

PARTNERS AND ITS AFFILIATES MAY FROM TIME TO TIME SELL ALL OR A PORTION OF SUCH SHARES IN OPEN MARKET TRANSACTIONS

OR OTHERWISE (INCLUDING VIA SHORT SALES), BUY ADDITIONAL SHARES (IN OPEN MARKET OR PRIVATELY NEGOTIATED

TRANSACTIONS OR OTHERWISE), OR TRADE IN OPTIONS, PUTS, CALLS OR OTHER DERIVATIVE INSTRUMENTS RELATING TO SUCH

SHARES. JANA PARTNERS ALSO RESERVES THE RIGHT TO TAKE ANY ACTIONS WITH RESPECT TO ITS INVESTMENT IN CHARLES RIVER

LABORATORIES INTERNATIONAL INC. AS IT MAY DEEM APPROPRIATE, INCLUDING, BUT NOT LIMITED TO, COMMUNICATING WITH

MANAGEMENT, THE BOARD OF DIRECTORS AND OTHER INVESTORS.

LABORATORIES INTERNATIONAL INC. AND JANA PARTNERS IS IN THE BUSINESS OF INVESTING IN AND TRADING SECURITIES. JANA

PARTNERS AND ITS AFFILIATES MAY FROM TIME TO TIME SELL ALL OR A PORTION OF SUCH SHARES IN OPEN MARKET TRANSACTIONS

OR OTHERWISE (INCLUDING VIA SHORT SALES), BUY ADDITIONAL SHARES (IN OPEN MARKET OR PRIVATELY NEGOTIATED

TRANSACTIONS OR OTHERWISE), OR TRADE IN OPTIONS, PUTS, CALLS OR OTHER DERIVATIVE INSTRUMENTS RELATING TO SUCH

SHARES. JANA PARTNERS ALSO RESERVES THE RIGHT TO TAKE ANY ACTIONS WITH RESPECT TO ITS INVESTMENT IN CHARLES RIVER

LABORATORIES INTERNATIONAL INC. AS IT MAY DEEM APPROPRIATE, INCLUDING, BUT NOT LIMITED TO, COMMUNICATING WITH

MANAGEMENT, THE BOARD OF DIRECTORS AND OTHER INVESTORS.

NOTHING CONTAINED IN THIS PRESENTATION IS INTENDED TO BE, NOR SHOULD IT BE CONSTRUED OR USED AS, INVESTMENT, TAX,

LEGAL OR FINANCIAL ADVICE, AN OPINION OF THE APPROPRIATENESS OF ANY SECURITY OR INVESTMENT, OR AN OFFER, OR THE

SOLICITATION OF ANY OFFER, TO BUY OR SELL ANY SECURITY OR INVESTMENT.

LEGAL OR FINANCIAL ADVICE, AN OPINION OF THE APPROPRIATENESS OF ANY SECURITY OR INVESTMENT, OR AN OFFER, OR THE

SOLICITATION OF ANY OFFER, TO BUY OR SELL ANY SECURITY OR INVESTMENT.

Overview

4

JANA Partners Strongly Opposes the Proposed Acquisition of WuXi

„ Purported strategic rationale of combining preclinical and discovery services has

found almost no support

found almost no support

„ Proposed synergies are highly speculative and run counter to established industry

dynamics, and significant integration risk makes realization of even limited

synergies challenging

dynamics, and significant integration risk makes realization of even limited

synergies challenging

„ Charles River’s poor track record of integration and overall history of capital

allocation has been highly disappointing

allocation has been highly disappointing

„ WuXi valuation is excessive and relies on highly aggressive assumptions

„ Even assuming synergies were realistic and that Charles River can overcome

significant integration risk and its own history, and accepting aggressive WuXi

growth and margin assumptions, the proposed acquisition would still generate

inadequate returns

significant integration risk and its own history, and accepting aggressive WuXi

growth and margin assumptions, the proposed acquisition would still generate

inadequate returns

„ There are much more promising avenues to create immediate and certain

shareholder value, after years of significant underperformance

shareholder value, after years of significant underperformance

Lack of Supportable Strategic Rationale and Significant Risks

6

Street Reaction

“We still see the valuation premium applied as aggressive and the rationale for combination lacking

enough supporting evidence to assuage all concerns. We do believe that the combined entity will be

competitively differentiated, but we’re unconvinced that it will be materially competitively advantaged.” - R.W.

Baird, May 12, 2010

enough supporting evidence to assuage all concerns. We do believe that the combined entity will be

competitively differentiated, but we’re unconvinced that it will be materially competitively advantaged.” - R.W.

Baird, May 12, 2010

“[WuXi] stands to benefit from this transaction more than [Charles River].” - Lazard, June 15, 2010

“[W]e continue to see the proposed WX acquisition reducing the value of CRL shares.” - Lazard, July 15,

2010

2010

“During our conversations with industry participants, the subject of the Charles River-Wuxi proposed merger

often emerged. From the strategic perspective of synergies between discovery services and existing

preclinical capabilities, we did not encounter a single individual who agreed with the transaction

and/or thought that it would clearly provide a benefit to the resulting entity. In our view, this further validates

investor concerns over the merits of the transaction.” - - Raymond James, June 17, 2010

often emerged. From the strategic perspective of synergies between discovery services and existing

preclinical capabilities, we did not encounter a single individual who agreed with the transaction

and/or thought that it would clearly provide a benefit to the resulting entity. In our view, this further validates

investor concerns over the merits of the transaction.” - - Raymond James, June 17, 2010

[R]evenue synergies tend to be elusive in nature and particularly hard to capture relative to service based

transactions. Therefore, we expect shareholders to discount the revenue synergy potential of the

transaction and remain generally against the proposed [WuXi] transaction.” - Deutsche Bank, July 13, 2010

transactions. Therefore, we expect shareholders to discount the revenue synergy potential of the

transaction and remain generally against the proposed [WuXi] transaction.” - Deutsche Bank, July 13, 2010

“Neuberger Berman has been a patient long term stockholder of CRL, waiting for a reasonable return on the

investment made on behalf of our clients ... In our opinion, the proposed transaction with WuXi represents an

unacceptable elevation of financial and operational risks to CRL, and therefore, our investment.” - Neuberger

Berman LLC, June 16, 2010

investment made on behalf of our clients ... In our opinion, the proposed transaction with WuXi represents an

unacceptable elevation of financial and operational risks to CRL, and therefore, our investment.” - Neuberger

Berman LLC, June 16, 2010

Note: Quotation of analysts and investment firms herein does not necessarily indicate that such analysts or investment firms support the views expressed herein. Please see end

notes at the end of this presentation for full citation list.

notes at the end of this presentation for full citation list.

7

„ Customer and drug research process not well suited for integrated WuXi / Charles River Offering and

WuXi’s discovery offering too far removed from Charles River’s toxicology offering to generate significant

cross-selling opportunities

WuXi’s discovery offering too far removed from Charles River’s toxicology offering to generate significant

cross-selling opportunities

Expert Reaction

The research process is very complex which is why the pharmaceutical industry has kept separate decision makers at each

stage. Discovery scientists do not make decisions on preclinical work and vice versa. Moreover, they are usually in different

buildings, if not different cities or countries. - Former CEO of diversified preclinical CRO

stage. Discovery scientists do not make decisions on preclinical work and vice versa. Moreover, they are usually in different

buildings, if not different cities or countries. - Former CEO of diversified preclinical CRO

CROs do not sell everything to just one chief scientific professor. ‘A lot of times biologists don’t even talk to chemists.’ At my

company, there are a few decision makers for the range of preclinical work. Preclinical outsourcing decisions are made at a

lower level in the organization because they are less critical. Charles River does not have experience managing a discovery

business which increases risk of transaction. - - Executive in preclinical development at leading biotechnology company

company, there are a few decision makers for the range of preclinical work. Preclinical outsourcing decisions are made at a

lower level in the organization because they are less critical. Charles River does not have experience managing a discovery

business which increases risk of transaction. - - Executive in preclinical development at leading biotechnology company

CROs selection is based on particular service needed. Breadth of service not an important factor. Decision making is

decentralized and based on individual project/team. Do not think Charles River / WuXi combination will change sales process.

- Executive in Medical Affairs at leading pharmaceutical company

decentralized and based on individual project/team. Do not think Charles River / WuXi combination will change sales process.

- Executive in Medical Affairs at leading pharmaceutical company

WuXi combo is highly unproven. WuXi is too early in process to hook into a toxicology sale. Does not make sense to buy

toxicology services years in advance. Also potential to lose contact with molecule after discovery chemistry when it is brought

back in-house by some customers for further work, so low probability of cross sell to Charles River’s toxicology. - Former

senior executive of leading preclinical CRO

toxicology services years in advance. Also potential to lose contact with molecule after discovery chemistry when it is brought

back in-house by some customers for further work, so low probability of cross sell to Charles River’s toxicology. - Former

senior executive of leading preclinical CRO

It does not make sense to bundle chemistry (WuXi) and toxicology (Charles River) together. - Senior project manager for drug

development at leading pharmaceutical company, formerly project manager at a CRO

development at leading pharmaceutical company, formerly project manager at a CRO

Note: Excerpts presented here are summaries and do not purport to be direct quotes. The use of such summaries herein does not necessarily indicate that such individuals support the

views expressed herein.

views expressed herein.

JANA engaged with 20+ experts including several current and former executives at preclinical CROs,

several current and former executives in drug development and outsourcing at pharmaceutical and

biotechnology companies, and private investors in CROs, many of whom voiced similar concerns.

several current and former executives in drug development and outsourcing at pharmaceutical and

biotechnology companies, and private investors in CROs, many of whom voiced similar concerns.

8

„ Any success with integrated offering will come at the expense of lower pricing and margins

„ WuXi’s core business is facing increased competition and further standalone growth will be much

more challenging without the combination with Charles River

more challenging without the combination with Charles River

Expert Reaction (cont.)

When entering an arrangement for a broader offering with a CRO, we look for across the board pricing improvement.

- Executive managing outsourcing for leading pharmaceutical company

Shanghai is becoming quite expensive for chemistry professionals and how do they grow revenue? WuXi’s core strength

is in an area (medicinal chemistry) that is becoming commoditized. - Former executive in strategic sourcing/outsourcing for

preclinical development at leading pharmaceutical company

is in an area (medicinal chemistry) that is becoming commoditized. - Former executive in strategic sourcing/outsourcing for

preclinical development at leading pharmaceutical company

Without Charles River, WuXi will take a while to grow pharmacology / toxicology on its own. Chemistry outsourcing is

driven by cost and volume. - Senior executive responsible for outsourcing at leading pharmaceutical company

driven by cost and volume. - Senior executive responsible for outsourcing at leading pharmaceutical company

Note: Excerpts presented here are summaries and do not purport to be direct quotes. The use of such summaries herein does not necessarily indicate that such individuals support the

views expressed herein.

views expressed herein.

9

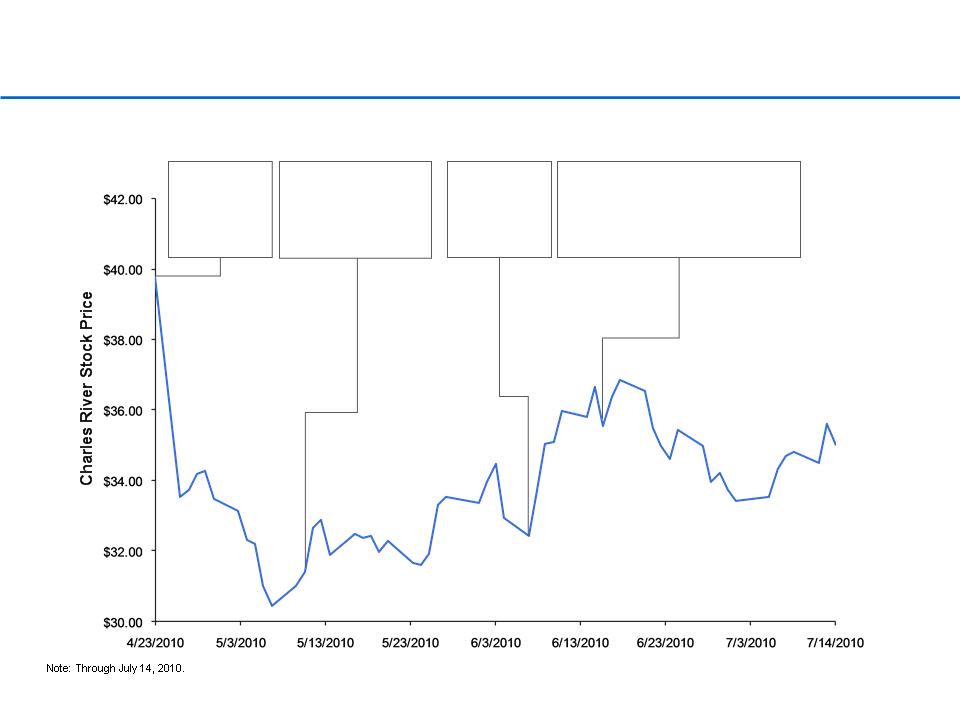

Charles River stock price dropped 16% on deal announcement … Recovery corresponds to rise in

shareholder opposition to WX transaction.

shareholder opposition to WX transaction.

Market Reaction

(1) “We know that there is a large contingent of shareholders unhappy with the valuation and strategy.”; Eric W. Coldwell, Nicholas Juhle; Robert W. Baird & Co., May 12, 2010.

CRL/WX

announced

JANA 13D

filing

filing

Neuberger Berman 13D filing

… Followed by Relational

opposition

… Followed by Relational

opposition

Reports of

Opposition to WX

Transaction (1)

Opposition to WX

Transaction (1)

10

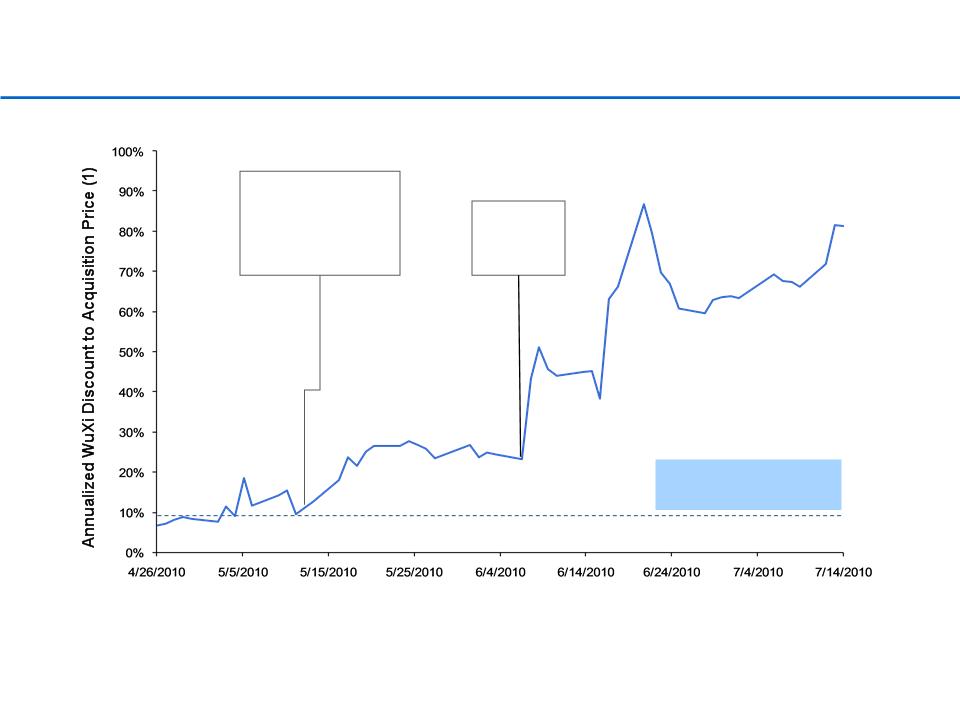

Market Reaction (cont.)

The market viewed the deal unfavorably even before public shareholder opposition surfaced.

Note: Through July 14, 2010.

(1)Assumes 12/31/2010 transaction close.

(2)“We know that there is a large contingent of shareholders unhappy with the valuation and strategy.”; Eric W. Coldwell, Nicholas Juhle; Robert W. Baird & Co., May 12, 2010.

(3)Per Barclays Capital research. As of July 2, 2010.

JANA

13D filing

13D filing

Current Median Deal

Spread(3)

Spread(3)

Reports of

Opposition to WX

Transaction (2)

Opposition to WX

Transaction (2)

Expanding deal spread illustrates market does not subscribe to deal rationale.

11

Market Reaction (cont.)

Note: Through June 8, 2010.

(1) “We know that there is a large contingent of shareholders unhappy with the valuation and strategy.”; Eric W. Coldwell, Nicholas Juhle; Robert W. Baird & Co., May 12, 2010.

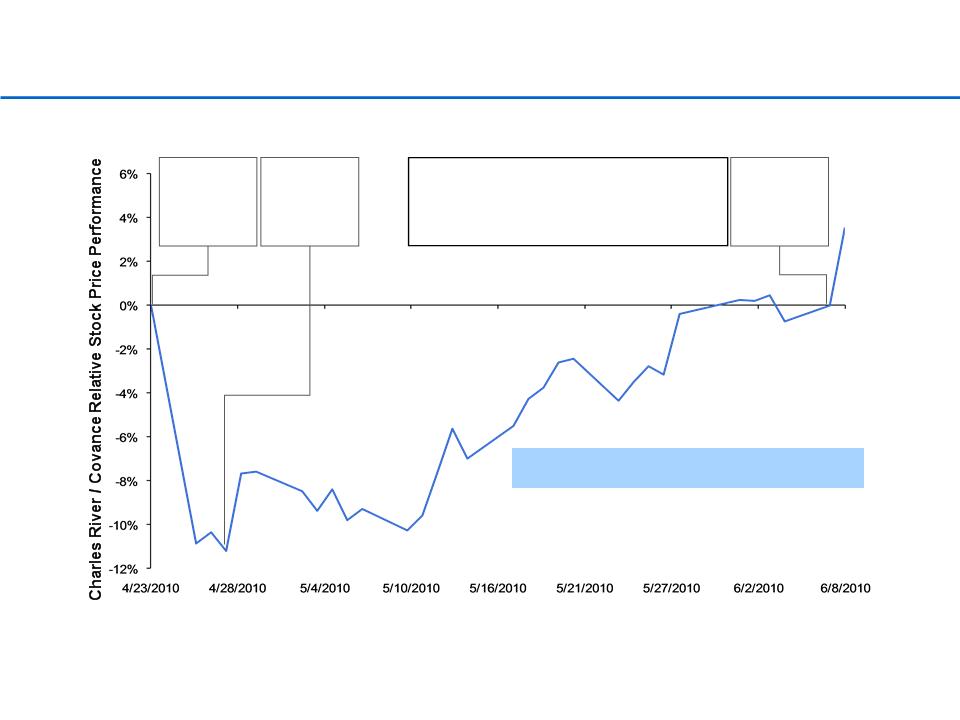

Charles River underperformance continued after market digested Covance’s worse earnings

report and only reversed as opposition to the deal spread through the market after May 12th.

report and only reversed as opposition to the deal spread through the market after May 12th.

Charles River materially underperforms peer Covance even after factoring in reaction to each

company’s Q1 earnings.

company’s Q1 earnings.

CRL/WX

announced

Covance

earnings

earnings

§ Reports of Opposition to WX

Transaction(1)

Transaction(1)

§ JANA due diligence and acquiring 7%

position

position

JANA 13D

filing

filing

Stock Price Performance pre/post Deal Opposition | ||

April 23 - May 12 | May 12 - June 8 | |

S&P 500 | (4)% | (10)% |

Charles River | (22)% | 3% |

Covance | (11)% | (11)% |

Highly Questionable Strategic Merits and Significant Integration Risk

13

While some Charles River investors may be drawn to China, the proposed combination with WuXi fails

to provide Charles River shareholders with any material incremental benefits.

to provide Charles River shareholders with any material incremental benefits.

„Integrated offering of discovery and preclinical services unlikely to yield material cross-selling synergies

because not a logical cross-sell

because not a logical cross-sell

§ Fragmented R&D process means customers not set up to buy integrated offering of unrelated processes

§ Separate decisions often made by different decision makers with different scientific expertise often

separated by facility, city or even country

separated by facility, city or even country

§ Significant time lapse (often years) between discovery and preclinical work greatly reduces likelihood that

discovery and preclinical outsourcing decisions will be made at the same time

discovery and preclinical outsourcing decisions will be made at the same time

Claimed Benefits Run Counter to Industry Dynamics and

Experience, Present Significant Risks

Experience, Present Significant Risks

Chart Source: Pharmaceutical Industry Profile 2008 (PhRMA, March 2008, p.4).

Integrated discovery and preclinical offering is unlikely to generate significant revenue synergies.

3-6 Years

6-7 Years

½ -2 Years

Clinical Trials

Drug Discovery

Preclinical

FDA Review

Lg-Scale Mfg

One FDA-

Approved

Drug

Approved

Drug

5

250

5,000-10,000

Compounds

Compounds

14

„ Revenue synergies notoriously difficult to generate in this sector(1)

„ Client consideration of reducing number of suppliers has been gradual and is mostly in the clinical sector

(not discovery or preclinical) where there are dozens of CROs and modest barriers to entry(2)

(not discovery or preclinical) where there are dozens of CROs and modest barriers to entry(2)

„ Even when integrated offering leads to cross-sale, usually combined sale made through “purchasing

department” leading to discounting

department” leading to discounting

§ Integrated sale leads to pricing pressure along with having to reconcile the companies’ differential pricing

models(3)

models(3)

„ Cross-selling challenging to sales force given high degree of specialization / distinct pricing model for each

company’s offering

company’s offering

§ Charles River’s sales force will be stretched having to sell three highly specialized offerings (discovery,

research models and preclinical services) given WuXi brings along a minimal sales effort

research models and preclinical services) given WuXi brings along a minimal sales effort

„ Unlikely to achieve announced SG&A cost synergies given WuXi has minimal sales force and achieving

cross-selling revenue synergies from specialized discovery sales would require CRL to expand its sales

force

cross-selling revenue synergies from specialized discovery sales would require CRL to expand its sales

force

(1) For example, Deutsche Bank has noted that “[R]evenue synergies tend to be elusive in nature and particularly hard to capture relative to service based transactions.” “CRL updates

synergy target and receives 2nd request from FTC”; Ross Muken, Michael Cherny and Vijay Kumar; Deutsche Bank Securities Inc., July 13, 2010.

synergy target and receives 2nd request from FTC”; Ross Muken, Michael Cherny and Vijay Kumar; Deutsche Bank Securities Inc., July 13, 2010.

(2) Survey of clinical providers and sponsors as performed by the Avoca Group and presented on July 1, 2010 on a Jefferies & Company Inc. conference call.

(3) Bank of America Merrill Lynch for example has expressed concerns regarding “potential cannibalization of sales from having a different pricing model in the US/EU vs. Asia.” “Merger

assumptions leave little room for error”; Eric Lo, Eric H. Chang; Bank of America Merrill Lynch, June 2, 2010.

assumptions leave little room for error”; Eric Lo, Eric H. Chang; Bank of America Merrill Lynch, June 2, 2010.

Significant integration risk, plus risk of margin erosion from any successful combined offering.

Claimed Benefits Run Counter to Industry Dynamics and

Experience, Present Significant Risks (cont.)

Experience, Present Significant Risks (cont.)

15

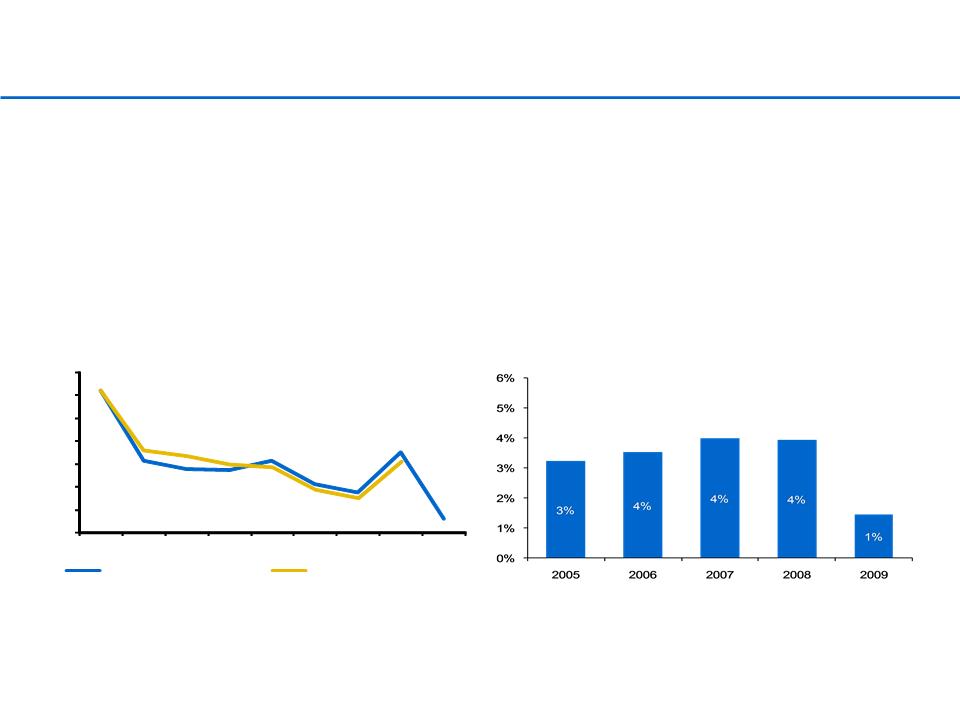

CRL has Struggled to Generate Appropriate Returns and

With Integration

With Integration

Margin Comparison (CRL PCS - Covance Early Stage)(1)

Charles River Preclinical Return on Investment(2)

-

8%

-

6%

-

4%

-

2%

0%

2%

4%

6%

2002

2003

2004

2005

2006

2007

2008

2009

1Q10

EBIT Margin Diff

EBITDA Margin Diff

„ $1.5 billion acquisition of Inveresk in 2004 was meant to enhance existing preclinical offering and generate cross-selling

synergies from Inveresk’s late stage outsourced offering. However CRL failed to successfully integrate Inveresk’s late stage

offering, selling it for a substantial loss

synergies from Inveresk’s late stage outsourced offering. However CRL failed to successfully integrate Inveresk’s late stage

offering, selling it for a substantial loss

„ Despite a high degree of experience in the preclinical business, Charles River significantly overpaid for Inveresk, ultimately

resulting in a $700 million write-down of preclinical goodwill

resulting in a $700 million write-down of preclinical goodwill

„ Despite substantial scale benefits from Inveresk acquisition and over $600 million in additional investment over the past five

years, poor integration resulted in combined preclinical margin deterioration at a time when a close peer exhibited margin

expansion and the business never generated an acceptable return

years, poor integration resulted in combined preclinical margin deterioration at a time when a close peer exhibited margin

expansion and the business never generated an acceptable return

„ That CRL misjudged the acquisition of a business they knew well (preclinical) raises questions about their ability to evaluate

a business they do not know (discovery)

a business they do not know (discovery)

(1) Charles River margins pro forma to include Inveresk prior to transaction close. Margins exclude acquisition related expenses, impairment and write-downs.

(2) (1) Tax-effected segment operating income at assumed 30% tax rate divided by (2) period end segment long-term assets, adding back goodwill write-downs and including other intangible assets.

(3) ”Putting on its Marketing Hat”; David Windley, Timothy C. Evans, Andrew Hilgenbrink, Ph.D.; Jefferies & Company, Inc., June 2, 2010.

(4) “Charles River Laboratories”; Eric W. Coldwell, Nicholas Juhle; Robert W. Baird & Co., May 12, 2010.

"Investors must bet against history to believe that [Charles River] can integrate [WuXi] without a stumble."(3)

“Past acquisitions haven’t been [CRL’s] strong point, nor have the majority panned out across the industry.”(4)

High Valuation and Inadequate Returns

17

WuXi: Excessive Valuation on Aggressive Assumptions

„ Proposed WX acquisition price is excessive at 16x 2010 EBITDA — nearly 56x “cash” earnings(1) — and

relative to CRL’s high single-digit EBITDA multiple valuation

relative to CRL’s high single-digit EBITDA multiple valuation

§ Compounded by issuing stock well below intrinsic value(2) and when preclinical earnings down 50%

§ WX CEO sold stock more than 50% below CRL offer price; offer price is minimal premium to post-IPO

private equity investor initial cost, suggesting future standalone business prospects are very

challenging

private equity investor initial cost, suggesting future standalone business prospects are very

challenging

„ Despite raising 2010 guidance, WX projections are aggressive, requiring reversal of negative trends and

robust results from unproven businesses

robust results from unproven businesses

§ Assume reacceleration in revenue growth (after deceleration) and margin improvement (gross margin

declining annually since 2003 with management guiding a further decline for 2010) despite labor cost

inflation in China pressuring margins

declining annually since 2003 with management guiding a further decline for 2010) despite labor cost

inflation in China pressuring margins

§ “To reach expectations will require sustainable Lab services growth and successful execution in two

relatively early stage businesses (tox and manufacturing) while driving margin expansion in the face of

pricing pressure.”(3)

relatively early stage businesses (tox and manufacturing) while driving margin expansion in the face of

pricing pressure.”(3)

§ “WX's new guidance is still well below the forecasts given…This makes the 6/1 proxy forecasts

aggressive.”(4)

aggressive.”(4)

„ WX’s primary competitive advantages of scale and cost and are not sustainable, putting projections at risk

§ Chinese competitors reaching scale (#2 competitor employing almost half the chemists as WX)

impacting WX margins

impacting WX margins

§ India offers a promising new geography given lower labor costs and highly skilled workforce

(1) See JANA 13D, June 16, 2010 for “cash” earnings calculation.

(2) “[A] split of CRL could unlock shareholder value that is equivalent to $47 per share”; “CRL: Time to unlock value; we see $6/share from recap, $11/share from an RMS/PCS split”;

Stephen Unger, William Hite; Lazard Capital Markets, Inc., June 17, 2010.

Stephen Unger, William Hite; Lazard Capital Markets, Inc., June 17, 2010.

(3) “Merger assumptions leave little room for error”; Eric Lo, Eric H. Chang; Bank of America Merrill Lynch, June 2, 2010.

(4) “Pre-announcement Adds Arrow to CRL Quiver”; David Windley, Timothy C. Evans, Andrew Hilgenbrink; Jefferies & Company Inc., July, 15 2010.

Even assuming strategic benefits from the WuXi deal, excessive price destroys shareholder value.

18

(1) Midpoint of JPMorgan calculated WX WACC per latest CRL proxy.

(2) Charles River has previously communicated to shareholders a mid teens return requirement on investments.

(3) $350MM of additional revenue synergies (beyond the newly announced revenue synergies) which would be required to achieve return requirement, assuming a 30% operating margin and a 25% tax rate.

Note: Please see the end notes at the end of this presentation for returns calculation information.

Returns Inadequate Even Under Most Optimistic

Scenarios

Scenarios

Even if one assumes synergies are realistic and that Charles River can overcome significant

integration risk and its own history, and accepting aggressive WuXi growth and margin

assumptions, the proposed acquisition would still fail to return its 12% cost of capital(1) by 2015.

integration risk and its own history, and accepting aggressive WuXi growth and margin

assumptions, the proposed acquisition would still fail to return its 12% cost of capital(1) by 2015.

To achieve CRL’s 15% return requirement by 2015 requires $350MM of additional revenue synergies.(2)(3)

19

„ Charles River has much more promising and straightforward means to create greater and more immediate

shareholder value than a WuXi acquisition

shareholder value than a WuXi acquisition

„ For example, could employ the same amount of leverage it would assume in a WuXi acquisition to

repurchase 30% of its undervalued shares at a 10% premium to current share price, without any integration

risk

repurchase 30% of its undervalued shares at a 10% premium to current share price, without any integration

risk

§ Would result in accretion to 2011 earnings per share of approximately 14% based on recent share prices,

with accretion continuing to grow thereafter

with accretion continuing to grow thereafter

§ Leverage would likely instill greater capital discipline

„ Given history as a leveraged buyout, robust private equity activity in the CRO space, minimal synergies

between its research models and preclinical segments and recent published reports, a sale or break-up

potentially represents another means of creating greater shareholder value

between its research models and preclinical segments and recent published reports, a sale or break-up

potentially represents another means of creating greater shareholder value

More Promising Means to Create Shareholder Value

20

End Notes

Page 6 Full Citations:

- “Charles River Laboratories”; Eric W. Coldwell, Nicholas Juhle; Robert W. Baird & Co., May 12, 2010.

- “CRL: Argument for WX completion continues to evolve; does management intend to change the terms and avoid vote?”; Stephen Unger and

William Hite; Lazard Capital Markets, June 15, 2010.

William Hite; Lazard Capital Markets, June 15, 2010.

- Neuberger Berman Group LLC, Schedule 13D, filed with the SEC June 16, 2010.

- “DIA: Exhibitor Conversation Takeaways”; Alexander Y. Draper and Jake Hausman; Raymond James & Associates; June 17, 2010.

- “CRL updates synergy target and receives 2nd request from FTC”; Ross Muken, Michael Cherny and Vijay Kumar; Deutsche Bank Securities

Inc.; July 13, 2010.

Inc.; July 13, 2010.

- “CRL: Too little, too late? CRL is trying very hard to get shareholders comfortable; a ‘No’ vote looks imminent; BUY”; Stephen Unger and William

Hite; Lazard Capital Markets, July 15, 2010.

Hite; Lazard Capital Markets, July 15, 2010.

Note: Quotation of analysts and investment firms herein does not necessarily indicate that such analysts or investment firms support the views

expressed herein.

expressed herein.

Page 18 Return Calculation Details:

- Returns calculated by dividing (1) the sum of GAAP net income and depreciation & amortization by (2) the sum of Charles River stock and cash

consideration, conversion of WuXi options, WuXi net debt assumed, deal related expenses and WuXi capital expenditures. Synergies (a)

incorporate the announced $20MM of pre-tax cost synergies taxed at a 25% tax rate in 2011 and thereafter, (b) assume a one-time pre-tax

restructuring charge of $30MM which is included in invested capital and (c) include newly announced revenue synergies of $100MM in 2013 (the

high-end of Charles River synergy guidance) and initial revenue synergies of $33MM in 2011 and $67MM in 2012, in each case at an assumed

30% operating margin, growing in-line with operating income projections thereafter and taxed at a 25% tax rate. WuXi GAAP net income through

2012 based on adjusted operating income projections per Charles River’s latest proxy statement, 14% tax rate per midpoint of WuXi 2010

guidance, and assumes $9MM reduction for after tax share based compensation per 2009 actual results. 2013-2015 WuXi operating income

growth rate based on Jefferies’ research projected growth rate of operating income for the same period. Depreciation expense through 2012

based on difference between WuXi adjusted EBITDA and operating income estimates per Charles River’s latest proxy statement; thereafter

assumed to grow in-line with capital expenditure growth rate. 2011-2015 capital expenditures per Jefferies’ research estimates. Charles River

stock consideration valued per Charles River transaction presentations, using Charles River closing price of 4/23/2010 (closing price prior to

transaction announcement) and based on 75MM diluted WuXi shares, for a total stock and cash consideration of $1.6 billion. Conversion of WuXi

options valued at $39MM per Charles River proxy. Deal related expenses include Credit Suisse seller advisory fee (not disclosed but assumed to

be equivalent to $12MM JP Morgan buyer advisory fee) and assumed $24MM in financing fees related to Charles River’s $1.2bn credit facility.

consideration, conversion of WuXi options, WuXi net debt assumed, deal related expenses and WuXi capital expenditures. Synergies (a)

incorporate the announced $20MM of pre-tax cost synergies taxed at a 25% tax rate in 2011 and thereafter, (b) assume a one-time pre-tax

restructuring charge of $30MM which is included in invested capital and (c) include newly announced revenue synergies of $100MM in 2013 (the

high-end of Charles River synergy guidance) and initial revenue synergies of $33MM in 2011 and $67MM in 2012, in each case at an assumed

30% operating margin, growing in-line with operating income projections thereafter and taxed at a 25% tax rate. WuXi GAAP net income through

2012 based on adjusted operating income projections per Charles River’s latest proxy statement, 14% tax rate per midpoint of WuXi 2010

guidance, and assumes $9MM reduction for after tax share based compensation per 2009 actual results. 2013-2015 WuXi operating income

growth rate based on Jefferies’ research projected growth rate of operating income for the same period. Depreciation expense through 2012

based on difference between WuXi adjusted EBITDA and operating income estimates per Charles River’s latest proxy statement; thereafter

assumed to grow in-line with capital expenditure growth rate. 2011-2015 capital expenditures per Jefferies’ research estimates. Charles River

stock consideration valued per Charles River transaction presentations, using Charles River closing price of 4/23/2010 (closing price prior to

transaction announcement) and based on 75MM diluted WuXi shares, for a total stock and cash consideration of $1.6 billion. Conversion of WuXi

options valued at $39MM per Charles River proxy. Deal related expenses include Credit Suisse seller advisory fee (not disclosed but assumed to

be equivalent to $12MM JP Morgan buyer advisory fee) and assumed $24MM in financing fees related to Charles River’s $1.2bn credit facility.