U.S. Securities and Exchange Commission

Washington, DC 20549

NOTICE OF EXEMPT SOLICITATION

1. Name of the Registrant: Charles River Laboratories International, Inc.

2. Name of person relying on exemption: JANA Partners LLC

3. Address of person relying on exemption: 767 Fifth Avenue, 8th Floor, New York, New York 10153

4. Written materials. Attach written material required to be submitted pursuant to Rule 14a-6(g)(1)

Supplemental Materials for ISS: Response to Charles River

Laboratories’ ISS Presentation Follow-Up Materials

Laboratories’ ISS Presentation Follow-Up Materials

July 22, 2010

2

THESE MATERIALS ARE FOR GENERAL INFORMATIONAL PURPOSES FOR ISS GROUP ONLY. THEY DO NOT HAVE REGARD TO THE

SPECIFIC INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY, OR THE PARTICULAR NEED OF ANY SPECIFIC PERSON WHO

MAY RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. THESE

MATERIALS DO NOT RECOMMEND THE PURCHASE OR SALE OF ANY SECURITY. THE VIEWS EXPRESSED HEREIN REPRESENT THE

OPINIONS OF JANA PARTNERS LLC ("JANA PARTNERS"), WHICH OPINIONS MAY CHANGE AT ANY TIME AND ARE BASED ON PUBLICLY

AVAILABLE INFORMATION WITH RESPECT TO CHARLES RIVER LABORATORIES INTERNATIONAL INC. AND WUXI PHARMATECH (CAYMAN)

INC. (THE “ISSUERS”). CERTAIN FINANCIAL INFORMATION AND DATA USED HEREIN HAVE BEEN DERIVED OR OBTAINED FROM FILINGS

MADE WITH THE SECURITIES AND EXCHANGE COMMISSION (“SEC”) BY THE ISSUERS OR OTHER COMPANIES JANA PARTNERS

CONSIDERS COMPARABLE, AND FROM OTHER THIRD PARTY REPORTS.

SPECIFIC INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY, OR THE PARTICULAR NEED OF ANY SPECIFIC PERSON WHO

MAY RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. THESE

MATERIALS DO NOT RECOMMEND THE PURCHASE OR SALE OF ANY SECURITY. THE VIEWS EXPRESSED HEREIN REPRESENT THE

OPINIONS OF JANA PARTNERS LLC ("JANA PARTNERS"), WHICH OPINIONS MAY CHANGE AT ANY TIME AND ARE BASED ON PUBLICLY

AVAILABLE INFORMATION WITH RESPECT TO CHARLES RIVER LABORATORIES INTERNATIONAL INC. AND WUXI PHARMATECH (CAYMAN)

INC. (THE “ISSUERS”). CERTAIN FINANCIAL INFORMATION AND DATA USED HEREIN HAVE BEEN DERIVED OR OBTAINED FROM FILINGS

MADE WITH THE SECURITIES AND EXCHANGE COMMISSION (“SEC”) BY THE ISSUERS OR OTHER COMPANIES JANA PARTNERS

CONSIDERS COMPARABLE, AND FROM OTHER THIRD PARTY REPORTS.

QUOTATION OF ANALYSTS HEREIN DOES NOT NECESSARILY INDICATE THAT SUCH ANALYSTS SUPPORT THE VIEWS EXPRESSED

HEREIN. JANA PARTNERS HAS NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO THE USE OF PREVIOUSLY

PUBLISHED INFORMATION AND ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF

SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN. NO WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED

OR OBTAINED FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE.

HEREIN. JANA PARTNERS HAS NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO THE USE OF PREVIOUSLY

PUBLISHED INFORMATION AND ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT OF

SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN. NO WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED

OR OBTAINED FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE.

JANA PARTNERS SHALL NOT BE RESPONSIBLE OR HAVE ANY LIABILITY FOR ANY MISINFORMATION CONTAINED IN ANY SEC FILING OR

THIRD PARTY REPORT. THERE IS NO ASSURANCE OR GUARANTEE WITH RESPECT TO THE PRICES AT WHICH ANY SECURITIES OF THE

ISSUERS WILL TRADE, AND SUCH SECURITIES MAY NOT TRADE AT PRICES THAT MAY BE IMPLIED HEREIN. THE ESTIMATES,

PROJECTIONS, PRO FORMA INFORMATION AND POTENTIAL IMPACT OF TRANSACTIONS DISCUSSED HEREIN ARE BASED ON

ASSUMPTIONS WHICH JANA PARTNERS BELIEVES TO BE REASONABLE, BUT THERE CAN BE NO ASSURANCE OR GUARANTEE THAT

ACTUAL RESULTS OR PERFORMANCE OF THE ISSUERS WILL NOT DIFFER, AND SUCH DIFFERENCES MAY BE MATERIAL. JANA

PARTNERS DISCLAIMS ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN.

THIRD PARTY REPORT. THERE IS NO ASSURANCE OR GUARANTEE WITH RESPECT TO THE PRICES AT WHICH ANY SECURITIES OF THE

ISSUERS WILL TRADE, AND SUCH SECURITIES MAY NOT TRADE AT PRICES THAT MAY BE IMPLIED HEREIN. THE ESTIMATES,

PROJECTIONS, PRO FORMA INFORMATION AND POTENTIAL IMPACT OF TRANSACTIONS DISCUSSED HEREIN ARE BASED ON

ASSUMPTIONS WHICH JANA PARTNERS BELIEVES TO BE REASONABLE, BUT THERE CAN BE NO ASSURANCE OR GUARANTEE THAT

ACTUAL RESULTS OR PERFORMANCE OF THE ISSUERS WILL NOT DIFFER, AND SUCH DIFFERENCES MAY BE MATERIAL. JANA

PARTNERS DISCLAIMS ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN.

JANA PARTNERS AND ITS AFFILIATES CURRENTLY HOLD A SUBSTANTIAL AMOUNT OF SHARES OF COMMON STOCK OF CHARLES RIVER

LABORATORIES INTERNATIONAL INC. AND JANA PARTNERS IS IN THE BUSINESS OF INVESTING IN AND TRADING SECURITIES. JANA

PARTNERS AND ITS AFFILIATES MAY FROM TIME TO TIME SELL ALL OR A PORTION OF SUCH SHARES IN OPEN MARKET TRANSACTIONS

OR OTHERWISE (INCLUDING VIA SHORT SALES), BUY ADDITIONAL SHARES (IN OPEN MARKET OR PRIVATELY NEGOTIATED

TRANSACTIONS OR OTHERWISE), OR TRADE IN OPTIONS, PUTS, CALLS OR OTHER DERIVATIVE INSTRUMENTS RELATING TO SUCH

SHARES. JANA PARTNERS ALSO RESERVES THE RIGHT TO TAKE ANY ACTIONS WITH RESPECT TO ITS INVESTMENT IN CHARLES RIVER

LABORATORIES INTERNATIONAL INC. AS IT MAY DEEM APPROPRIATE, INCLUDING, BUT NOT LIMITED TO, COMMUNICATING WITH

MANAGEMENT, THE BOARD OF DIRECTORS AND OTHER INVESTORS.

LABORATORIES INTERNATIONAL INC. AND JANA PARTNERS IS IN THE BUSINESS OF INVESTING IN AND TRADING SECURITIES. JANA

PARTNERS AND ITS AFFILIATES MAY FROM TIME TO TIME SELL ALL OR A PORTION OF SUCH SHARES IN OPEN MARKET TRANSACTIONS

OR OTHERWISE (INCLUDING VIA SHORT SALES), BUY ADDITIONAL SHARES (IN OPEN MARKET OR PRIVATELY NEGOTIATED

TRANSACTIONS OR OTHERWISE), OR TRADE IN OPTIONS, PUTS, CALLS OR OTHER DERIVATIVE INSTRUMENTS RELATING TO SUCH

SHARES. JANA PARTNERS ALSO RESERVES THE RIGHT TO TAKE ANY ACTIONS WITH RESPECT TO ITS INVESTMENT IN CHARLES RIVER

LABORATORIES INTERNATIONAL INC. AS IT MAY DEEM APPROPRIATE, INCLUDING, BUT NOT LIMITED TO, COMMUNICATING WITH

MANAGEMENT, THE BOARD OF DIRECTORS AND OTHER INVESTORS.

NOTHING CONTAINED IN THIS PRESENTATION IS INTENDED TO BE, NOR SHOULD IT BE CONSTRUED OR USED AS, INVESTMENT, TAX,

LEGAL OR FINANCIAL ADVICE, AN OPINION OF THE APPROPRIATENESS OF ANY SECURITY OR INVESTMENT, OR AN OFFER, OR THE

SOLICITATION OF ANY OFFER, TO BUY OR SELL ANY SECURITY OR INVESTMENT.

LEGAL OR FINANCIAL ADVICE, AN OPINION OF THE APPROPRIATENESS OF ANY SECURITY OR INVESTMENT, OR AN OFFER, OR THE

SOLICITATION OF ANY OFFER, TO BUY OR SELL ANY SECURITY OR INVESTMENT.

3

„ In its latest attempt to justify the proposed acquisition of WuXi (“WX”) in the face of significant

shareholder opposition, Charles River (“CRL”) has resorted to inaccurate and misleading analysis

shareholder opposition, Charles River (“CRL”) has resorted to inaccurate and misleading analysis

„ Overstating potential synergies to be generated by proposed WuXi acquisition

„ Understating premium proposed to be paid to WuXi shareholders

„ Relying on unrealistically optimistic assumptions for WuXi, while also using unrealistically low trough

assumptions for Charles River (thus mirroring the proposed transaction, which overvalues WuXi and

shortchanges Charles River shareholders by using undervalued Charles River stock)

assumptions for Charles River (thus mirroring the proposed transaction, which overvalues WuXi and

shortchanges Charles River shareholders by using undervalued Charles River stock)

„ Abandoning previous assertions that no longer suit their purpose

„ Including irrelevant analyses such as PEG ratios and growth/margin improvements which say nothing

about whether a combination with WuXi would create any incremental value

about whether a combination with WuXi would create any incremental value

„ Charles River’s attempt to show that the proposed WuXi acquisition would generate more

shareholder value than other strategic alternatives is highly flawed, and when properly adjusted in

fact demonstrates the opposite

shareholder value than other strategic alternatives is highly flawed, and when properly adjusted in

fact demonstrates the opposite

„ Charles River continues to rely on extremely aggressive growth and margin assumptions for WuXi

and highly speculative revenue synergy projections which run counter to market perception and

industry dynamics

and highly speculative revenue synergy projections which run counter to market perception and

industry dynamics

„ Either Charles River’s board relied on this flawed and misleading analysis in approving the proposed

acquisition, or has now manufactured it to salvage this acquisition. Either is unacceptable

acquisition, or has now manufactured it to salvage this acquisition. Either is unacceptable

Summary

4

„ Synergy value overstated to appear more valuable to CRL shareholders than premium offered to WX shareholders

§ 100% of claimed synergy value is compared to WX deal premium. However, CRL shareholders would only benefit from

78% of this value (because WX shareholders would own 22% of CRL), overstating synergy value by $89MM—$116MM

78% of this value (because WX shareholders would own 22% of CRL), overstating synergy value by $89MM—$116MM

§ Revenue synergies valued in 2013 dollars (when assumed to be fully realized) instead of present value, yet are compared

to today’s deal premium. Assuming 12% discount rate,(1) this overstates revenue synergies by $65MM—$100MM

to today’s deal premium. Assuming 12% discount rate,(1) this overstates revenue synergies by $65MM—$100MM

§ Despite CRL’s prior objection to using an EBITDA multiple to value WX,(2) CRL now relies on a blended EBITDA multiple

to value synergies. In other words, CRL first objected that such multiple overstates WX’s valuation, but now relies on it to

calculate synergy value

to value synergies. In other words, CRL first objected that such multiple overstates WX’s valuation, but now relies on it to

calculate synergy value

„ Premium paid to WX is significantly larger than CRL claims

§ Premium to market analysis only focuses on 28% premium to 4/23/10 announcement date closing price, whereas prior

CRL presentations cite the higher premium to 30 day average closing price of 38%. Adjusting for this adds $125MM to the

proposed premium to be paid by CRL

CRL presentations cite the higher premium to 30 day average closing price of 38%. Adjusting for this adds $125MM to the

proposed premium to be paid by CRL

§ Premium to DCF value is based on extremely aggressive 2010-2012 standalone WX assumptions (which are well ahead

of the Street), with the vast majority of the DCF value coming from projections in future years that have not been disclosed

in CRL’s proxy but can reasonably be assumed to be equally aggressive. Such projections assume reversal of negative

trends in growth rates and margins and robust results from unproven new businesses

of the Street), with the vast majority of the DCF value coming from projections in future years that have not been disclosed

in CRL’s proxy but can reasonably be assumed to be equally aggressive. Such projections assume reversal of negative

trends in growth rates and margins and robust results from unproven new businesses

„ CRL continues to rely upon unrealistic synergy estimates and highly aggressive WX assumptions

§ Despite widespread industry consensus that the claimed revenue synergies are highly speculative, such revenue

synergies (assumed to be achieved in 2013) have been fully valued at the same 10.5x EBITDA multiple as the base

businesses rather than appropriately discounted for the higher risk to their realization

synergies (assumed to be achieved in 2013) have been fully valued at the same 10.5x EBITDA multiple as the base

businesses rather than appropriately discounted for the higher risk to their realization

§ Cost synergies are suspect given that some derive from SG&A synergies when WX brings a minimal sales force and

generating cross-selling revenue synergies would likely require CRL to expand its sales force

generating cross-selling revenue synergies would likely require CRL to expand its sales force

Inaccurate Synergy and Premium Analysis

(1) Midpoint of rate used to value synergies in DCF analysis as disclosed in CRL proxy.

(2) “For you to compare relative pre-tax EBITDA multiples is misleading given WuXi’s significantly lower effective tax rate than Charles River.” Letter from James C. Foster to JANA

Partners LLC in Charles River Form DEFA14A filed with the SEC on June 14, 2010.

Partners LLC in Charles River Form DEFA14A filed with the SEC on June 14, 2010.

Charles River Assertion: “The Value of Synergies is Greater than the Premium Paid for WuXi” (page 4 of CRL materials)

Fact: CRL relies on highly misleading and inaccurate analysis to support this incorrect assertion

5

„ CRL’s attempt to justify WX acquisition on basis of relative PEG ratio is unsupportable

§ We are unaware of a single analyst who uses PEG to value CRL or WX. According to Lazard today, “[V]aluations based

upon PEG ratios are extremely sensitive to changes and we would not use them for this purpose.”(1)

upon PEG ratios are extremely sensitive to changes and we would not use them for this purpose.”(1)

§ As we previously noted in our letter to CRL dated June 16, 2010, it is not useful to rely on a “consensus” long-term

growth rate given it is comprised of wide-ranging growth forecasts based on inconsistent time frames including LTM

growth in earnings (which do not capture future growth), NTM growth in earnings and projections for multi-year growth in

earnings. Not surprisingly, analyst estimates for CRL's long-term growth rate ranged from 8% to 26% per Bloomberg (at

June 16, 2010), which would result in a PEG range from below 1.0x to above 2.0x

growth rate given it is comprised of wide-ranging growth forecasts based on inconsistent time frames including LTM

growth in earnings (which do not capture future growth), NTM growth in earnings and projections for multi-year growth in

earnings. Not surprisingly, analyst estimates for CRL's long-term growth rate ranged from 8% to 26% per Bloomberg (at

June 16, 2010), which would result in a PEG range from below 1.0x to above 2.0x

„ Using a P/E multiple is misleading since EPS fails to capture meaningful differences between CRL and WX

§ Does not equalize for WX’s lower tax rate (roughly 14%) stemming from current government incentives which may be

temporary (absent such incentives tax rate would be 25% Chinese statutory rate, similar to CRL’s current effective rate)

temporary (absent such incentives tax rate would be 25% Chinese statutory rate, similar to CRL’s current effective rate)

§ WX outflows for capex are substantially higher than depreciation expense (with opposite being true for CRL as it harvests

years of investment); adjusting EPS for this meaningful cash flow mismatch nearly doubles WX’s P/E and PEG

multiple(2)

years of investment); adjusting EPS for this meaningful cash flow mismatch nearly doubles WX’s P/E and PEG

multiple(2)

„ PEG ratio analysis pro forma for synergies relies on 2011 multiples and earnings growth rates, yet includes full

realization of cost and revenue synergies that will not be achieved until 2013

realization of cost and revenue synergies that will not be achieved until 2013

Irrelevant and Misleading Analyses

(1) “CRL: Four new slides added to justify WX valuation; ISS assessment expected to be released Friday or Monday; BUY”; Stephen Unger and William Hite; Lazard Capital Markets,

July 22, 2010. Quotation of analysts herein does not necessarily indicate that such analysts support the views expressed herein

July 22, 2010. Quotation of analysts herein does not necessarily indicate that such analysts support the views expressed herein

(2) See JANA’s letter to CRL in its Schedule 13D filed with the SEC on June 16, 2010.

Charles River Assertion: “The Purchase Price is Attractive on a PEG Ratio Basis” (page 5 of CRL materials)

Fact: This is an irrelevant and misleading metric

Charles River Assertion: “Proposed Transaction with WuXi Will Significantly Improve Charles River’s Revenue Growth and

Margins” (page 6 of CRL materials)

Margins” (page 6 of CRL materials)

Fact: This too is irrelevant given that it says nothing about whether combination with WX would generate any incremental value

„ It is obvious that acquiring a company with higher growth and margins would enhance CRL’s growth rates and

margins, and CRL shareholders attracted to WX are always free to buy WX stock without paying a premium

margins, and CRL shareholders attracted to WX are always free to buy WX stock without paying a premium

6

„ CRL’s standalone earnings prospects are highly attractive given recovery from cyclical low in preclinical (and

minimal reinvestment requirements), yet CRL relies on overly conservative assumptions to understate this potential

minimal reinvestment requirements), yet CRL relies on overly conservative assumptions to understate this potential

§ “Consensus” I/B/E/S long-term growth rate is inconsistently applied. WX’s 17.2% rate is used in WX projections, but

CRL’s 12.6% rate (which is cited by CRL in its analysis on page 5 and is consistent with CRL’s disclosed internal

forecast) is discarded in projecting CRL earnings growth(1)

CRL’s 12.6% rate (which is cited by CRL in its analysis on page 5 and is consistent with CRL’s disclosed internal

forecast) is discarded in projecting CRL earnings growth(1)

§ CRL standalone growth rate assumptions of 0% or 5% for both revenues and EPS are preposterous given that CRL’s

own standalone high single-digit revenue growth guidance suggests double-digit EPS growth with operational leverage,

and that consensus estimates and CRL’s own standalone 2011 EPS forecast of $2.70 have a higher EPS growth

trajectory

own standalone high single-digit revenue growth guidance suggests double-digit EPS growth with operational leverage,

and that consensus estimates and CRL’s own standalone 2011 EPS forecast of $2.70 have a higher EPS growth

trajectory

§ Also, implied core earnings would decline under 0% revenue growth case, which is indefensible given that the preclinical

business is at a cyclical low and that debt pay downs and growth in balance sheet cash will also drive earnings growth

business is at a cyclical low and that debt pay downs and growth in balance sheet cash will also drive earnings growth

„ However, CRL uses highly aggressive WX assumptions to inflate potential earnings accretion from a WX acquisition

§ WX 2010-2012 projections were prepared by WX without any adjustment from CRL and are well above Street projections

§ CRL applies 17.2% long-term growth rate to these already aggressive 2012 WX estimates, yet the average growth in

2012-2015 operating EPS for analysts who project this period is only 12%(2)

2012-2015 operating EPS for analysts who project this period is only 12%(2)

§ CRL assumes that only WX will benefit from operating leverage, with projections assuming material operating leverage

(2012 revenue growth of 15% compared to operating income growth of 21%)

(2012 revenue growth of 15% compared to operating income growth of 21%)

„ Buyback assumptions understate earnings potential of standalone buyback

§ Share repurchase scenario (which provides for a substantially larger 2011 buyback than share repurchase combined with

a WX transaction scenario given debt limitation) is assumed to occur at $41.75 (5% premium to CRL’s 4/23/10 stock

price), which is a staggering 23% premium to CRL’s current stock price. A buyback at a 5% premium to 7/21/10 price

increases standalone buyback scenario 2015 EPS accretion by 12%-15% leaving all other assumptions constant

a WX transaction scenario given debt limitation) is assumed to occur at $41.75 (5% premium to CRL’s 4/23/10 stock

price), which is a staggering 23% premium to CRL’s current stock price. A buyback at a 5% premium to 7/21/10 price

increases standalone buyback scenario 2015 EPS accretion by 12%-15% leaving all other assumptions constant

Invalid and Unreasonable Assumptions

(1) See CRL 8-K filed with the SEC on June 25, 2010 for internal forecast.

(2) Based on Goldman Sachs, Morgan Stanley and Jefferies 2012-2015 growth rates of 19%, 12%, and 6% respectively.

Charles River Assertion: “The Transaction Adds Meaningfully to CRL’s Standalone Long-Term Earnings Growth ” (page 7)

Fact: Higher projected earnings from WX transaction are derived from invalid and unreasonable assumptions

7

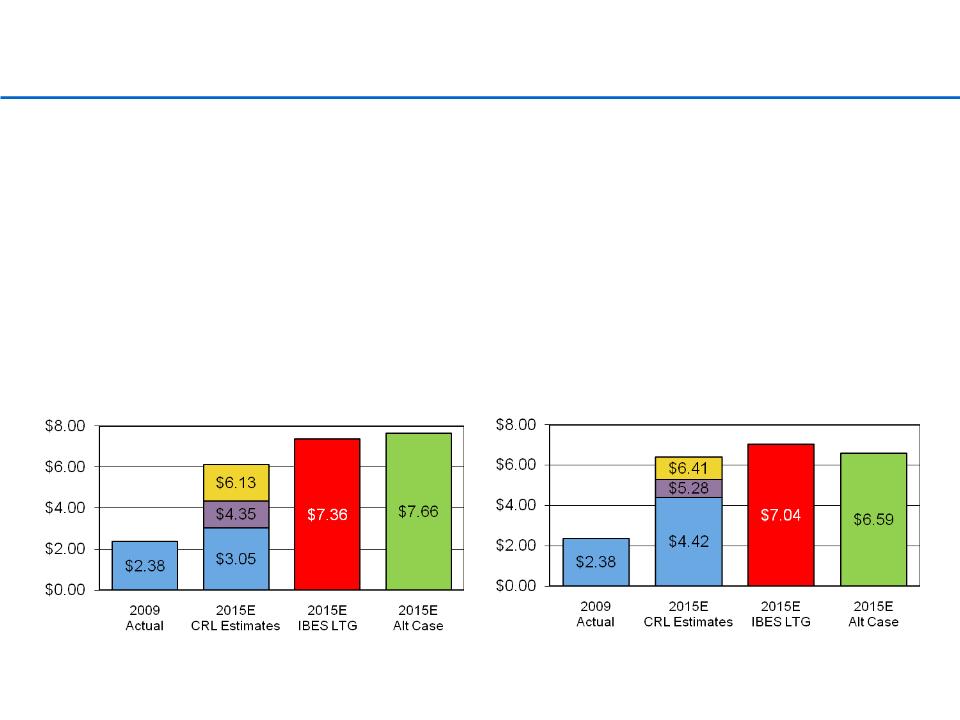

Invalid and Unreasonable Assumptions (cont.)

(1) See CRL 8-k filed with the SEC on June 25, 2010.

(2) 2015 Alt Case based on CRL analysis adjusted to assume CRL EPS growth rate per IBES estimates, initial share repurchase based on 5% premium to July 21, 2010 closing price

and realization of 50% of CRL/WX stated synergies.

and realization of 50% of CRL/WX stated synergies.

(3) 2015E CRL Estimates per CRL 0%, 5% and 10% EPS growth cases. 2015E IBES LTG based on CRL analysis adjusted to assume EPS growth of 12.6% per IBES long-term growth

rate.

rate.

„ While CRL claims on page 7 of its analysis to have demonstrated that a WX acquisition would generate greater EPS

growth than a standalone CRL share repurchase, this analysis when appropriately conducted actually demonstrates

the opposite

growth than a standalone CRL share repurchase, this analysis when appropriately conducted actually demonstrates

the opposite

§ Adjusting just one of the many unreasonable and inconsistent assumptions CRL employs in attempting to justify the

transaction demonstrates that a standalone share repurchase would create more value than acquiring WX followed by

share repurchases

transaction demonstrates that a standalone share repurchase would create more value than acquiring WX followed by

share repurchases

§ The “2015 IBES LTG” analysis below assumes a CRL earnings growth rate of 12.6% based on the long-term

earnings growth in earnings which CRL previously cited in justifying the proposed WX acquisition and which is

consistent with the growth rate relied on by CRL in formulating their recently disclosed 2009-2012 forecast(1)

earnings growth in earnings which CRL previously cited in justifying the proposed WX acquisition and which is

consistent with the growth rate relied on by CRL in formulating their recently disclosed 2009-2012 forecast(1)

§ Adjusting further for additional aggressive CRL assumptions (the “Alt Case” analysis below) results in 16% higher 2015

EPS in the standalone repurchase case than would be achieved combining a WX acquisition with ongoing repurchases,

again without the elevated operational and financial risk of a WX transaction(2)

EPS in the standalone repurchase case than would be achieved combining a WX acquisition with ongoing repurchases,

again without the elevated operational and financial risk of a WX transaction(2)

CRL Standalone, with Stock Repurchases(2)(3)

WuXi Transaction, with Stock Repurchases(2)(3)