Issuer Free Writing Prospectus

Filed Pursuant to Rule 433

Registration Statement No. 333-137902

Dated March 9, 2009

Expressing macro-economic views

through Interest Rate Structured Products

March 2009

Deutsche Bank Securities, Inc.

A Passion to Perform. [Deutsche Bank Logo]

slide00

|  |

Why Interest Rate Structured Products?

|X| One of the deepest and most liquid underlying derivatives markets

- Enables a wide array of products to be created and customized for

different requirements

|X| Ability to express views on fundamental macro economic variables and

drivers

- Short Term Rates

- Long Term Rates

- Yield Curve Slope, i.e. differential between long-term and short-term

rates

- Inflation

|X| Interest Rate Structured Products can serve multiple purposes within a core

portfolio

- Yield Enhancement

- Protecting Real Returns (Inflation linked structures)

- Hedging (E.g. Bearish Long Term Rate Structure for a Treasury

Portfolio)

[Deutsche Bank Logo]

slide01

|  |

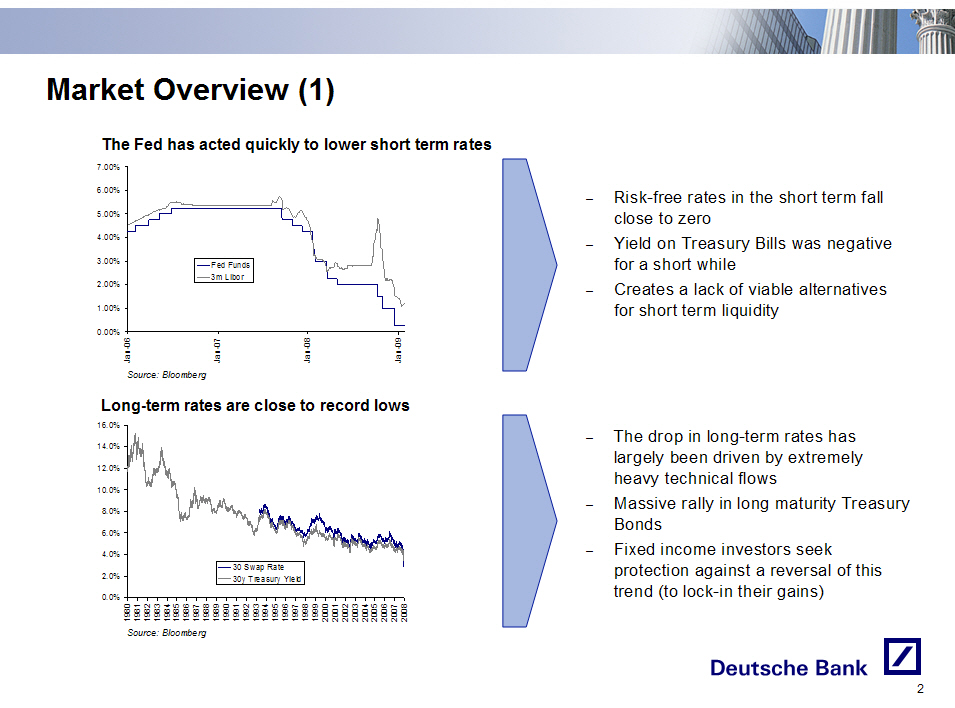

Market Overview (1)

The Fed has acted quickly to lower short term rates

[GRAPHIC OMITTED]

- Risk-free rates in the short term fall close to zero

- Yield on Treasury Bills was negative for a short while

- Creates a lack of viable alternatives for short term

liquidity

[GRAPHIC OMITTED]

- The drop in long-term rates has largely been driven by

extremely heavy technical flows

- Massive rally in long maturity Treasury Bonds

- Fixed income investors seek protection against a reversal

of this trend (to lock-in their gains)

[Deutsche Bank Logo]

slide02

|  |

Market Overview (2)

The inflation markets are pricing in significant deflation going forward

[GRAPHIC OMITTED]

- Market prices for TIPS and CPI Swaps imply years of

deflation

- Partly explained by commodity prices and economic

slowdown, but a large part is due to technical flows

(deleveraging)

- However a reversal could come quickly, given current

policy bias

- Investors seek to hedge their portfolios against a pickup

in inflation, taking advantage of attractive market levels

created by recent dislocation

[GRAPHIC OMITTED]

- Volatility spiked towards the end of 2008, but has come

down in the start of 2009

- Creates opportunities for investors depending on their

outlook on rates Selected Themes and Opportunities

[Deutsche Bank Logo]

slide03

|  |

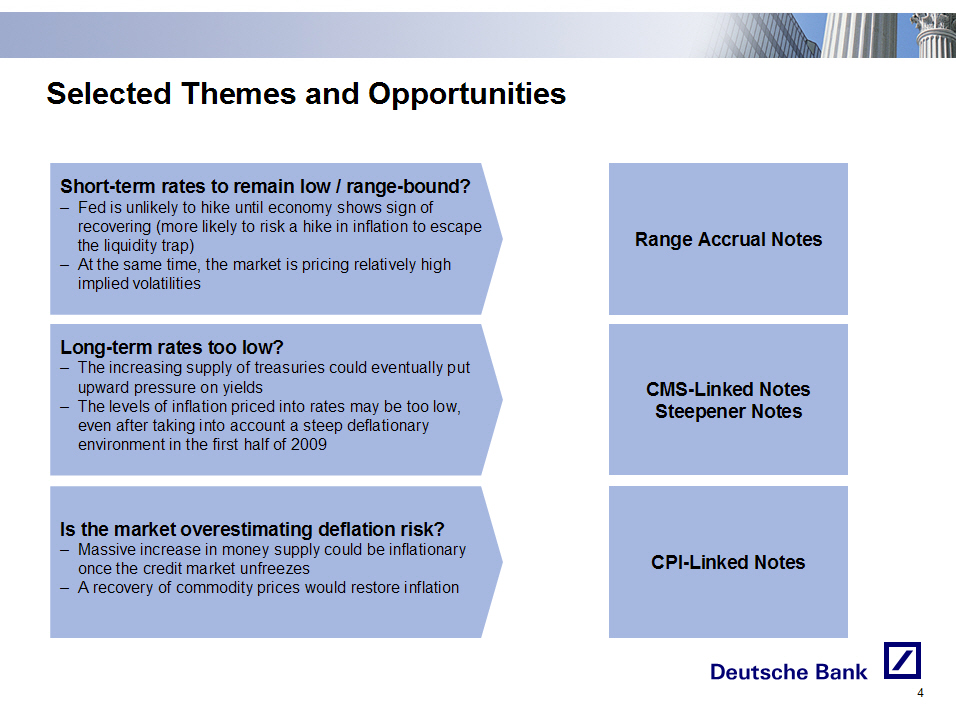

Selected Themes and Opportunities

Short-term rates to remain low / range-bound?

- - Fed is unlikely to hike until economy shows sign of recovering (more likely

to risk a hike in inflation to escape the liquidity trap)

- - At the same time, the market is pricing relatively high implied volatilities

Range Accrual Notes

Long-term rates too low?

- - The increasing supply of treasuries could eventually put upward pressure on

yields

- - The levels of inflation priced into rates may be too low, even after taking

into account a steep deflationary environment in the first half of 2009

CMS-Linked Notes

Steepener Notes

Is the market overestimating deflation risk?

- - Massive increase in money supply could be inflationary once the credit

market unfreezes

- - A recovery of commodity prices would restore inflation

CPI-Linked Notes

[Deutsche Bank Logo]

slide04

|  |

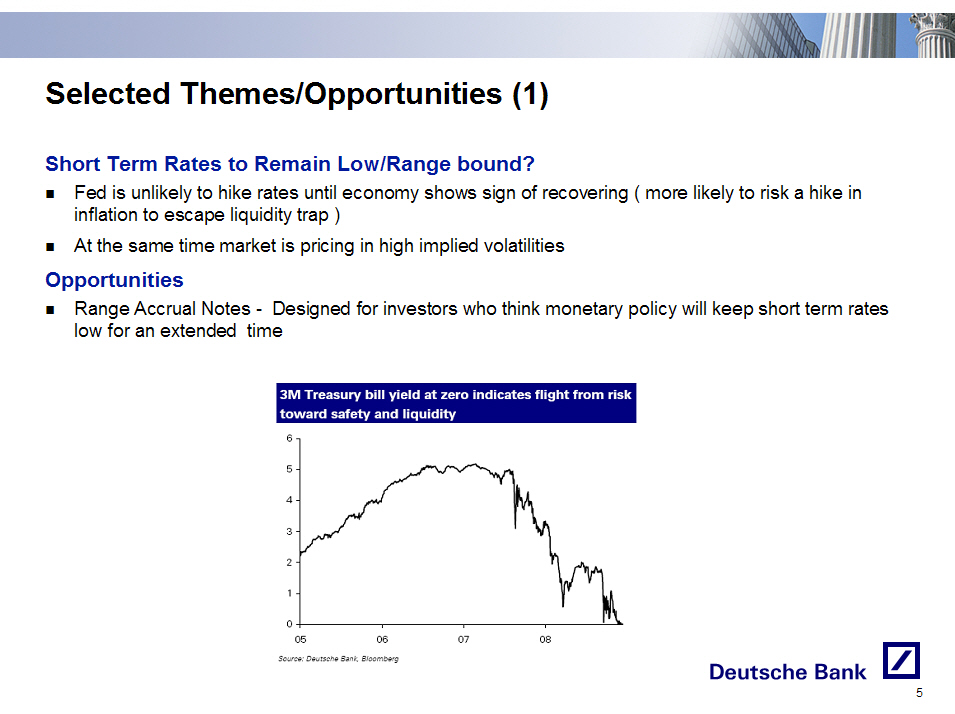

Selected Themes/Opportunities(1)

Short Term Rates to Remain Low/Range bound?

|X| Fed is unlikely to hike rates until economy shows sign of recovering (more

likely to risk a hike in inflation to escape liquidity trap)

|X| At the same time market is pricing in high implied volatilities

Opportunities

|X| Range Accrual Notes - Designed for investors who think monetary policy will

keep short term rates low for an extended time

[GRAPHIC OMITTED]

[Deutsche Bank Logo]

slide 05

|  |

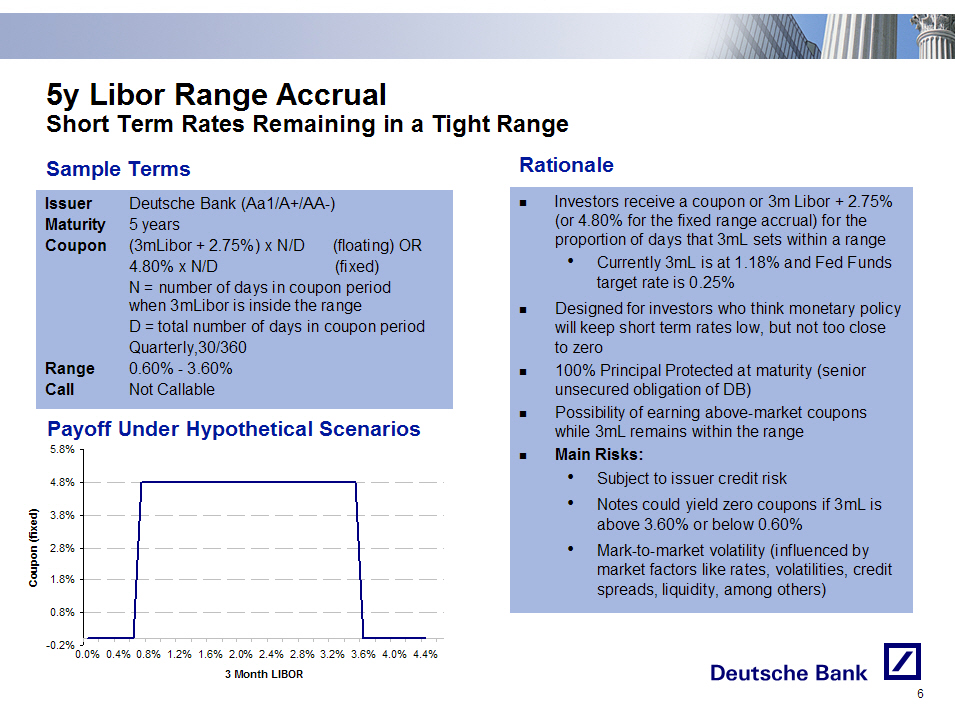

5y Libor Range Accrual

Short Term Rates Remaining in a Tight Range

Sample Terms

Issuer Deutsche Bank (Aa1/A+/AA-)

Maturity 5 years

Coupon (3mLibor + 2.75%) x N/D (floating) OR

4.80% x N/D (fixed)

N = number of days in coupon period

when 3mLibor is inside the range

D = total number of days in coupon period

Quarterly,30/360

Range 0.60% - 3.60%

Call Not Callable

Payoff Under Hypothetical Scenarios

[GRAPHIC OMITTED]

Rationale

|X| Investors receive a coupon or 3m Libor + 2.75% (or 4.80% for the fixed range

accrual) for the proportion of days that 3mL sets within a range

o Currently 3mL is at 1.18% and Fed Funds target rate is 0.25%

|X| Designed for investors who think monetary policy will keep short term rates

low, but not too close to zero

|X| 100% Principal Protected at maturity (senior unsecured obligation of DB)

|X| Possibility of earning above-market coupons while 3mL remains within the

range

|X| Main Risks:

o Subject to issuer credit risk

o Notes could yield zero coupons if 3mL is above 3.60% or below 0.60%

o Mark-to-market volatility (influenced by market factors like rates,

volatilities, credit spreads, liquidity, among others)

[Deutsche Bank Logo]

slide06

|  |

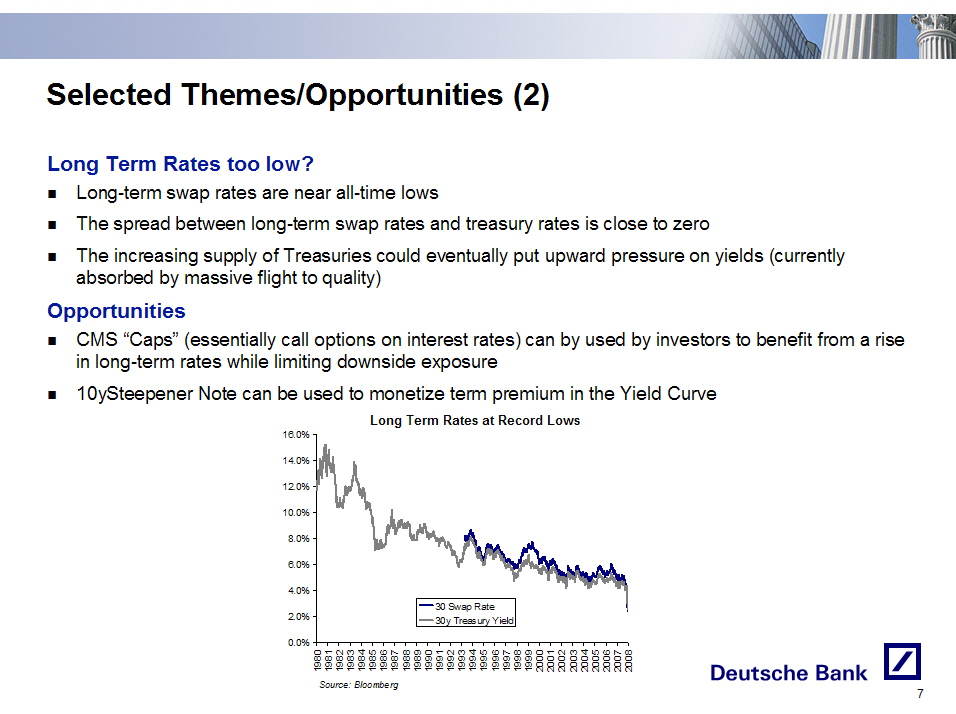

Selected Themes/Opportunities (2)

Long Term Rates too low?

|X| Long-term swap rates are near all-time lows

|X| The spread between long-term swap rates and treasury rates is close to zero

|X| The increasing supply of Treasuries could eventually put upward pressure on

yields (currently absorbed by massive flight to quality)

Opportunities

|X| CMS "Caps" (essentially call options on interest rates) can by used by

investors to benefit from a rise in long-term rates while limiting downside

xposure

|X| 10ySteepener Note can be used to monetize term premium in the Yield Curve

[GRAPHIC OMITTED]

[Deutsche Bank Logo]

slide07

|  |

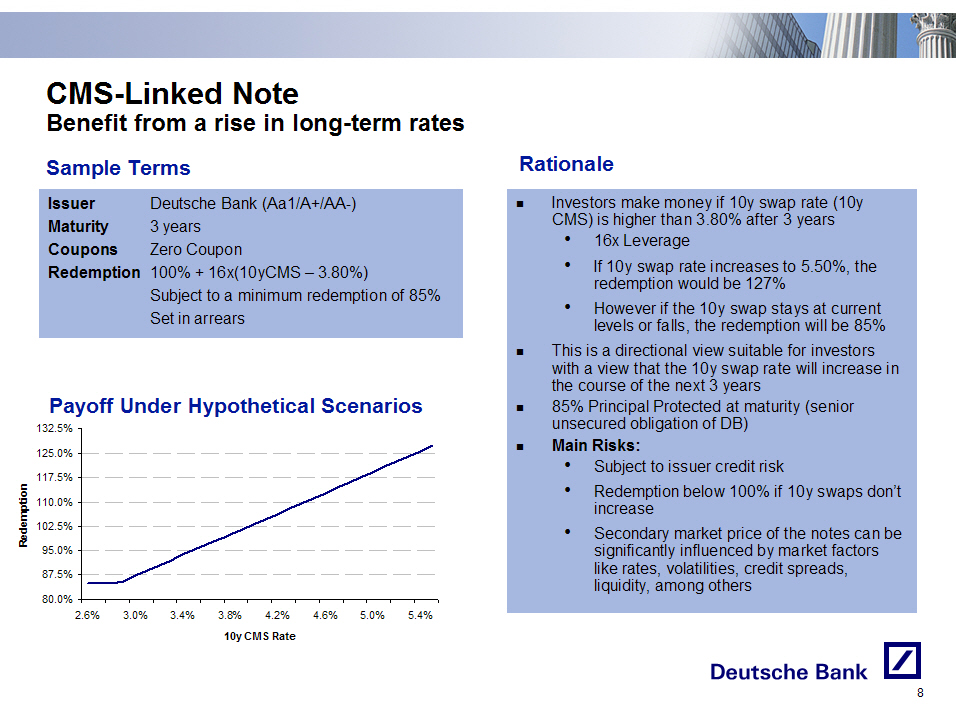

CMS-Linked Note

Benefit from a rise in long-term rates

Issuer Deutsche Bank (Aa1/A+/AA-)

Maturity 3 years

Coupons Zero Coupon

Redemption 100% + 16x(10yCMS - 3.80%)

Subject to a minimum redemption of 85%

Set in arrears

Payoff Under Hypothetical Scenarios

[GRAPHIC OMITTED]

Rationale

|X| Investors make money if 10y swap rate (10y CMS) is higher than 3.80% after

3 years

o 16x Leverage

o If 10y swap rate increases to 5.50%, the redemption would be 127%

o However if the 10y swap stays at current levels or falls, the

redemption will be 85%

|X| This is a directional view suitable for investors with a view that the

10y swap rate will increase in the course of the next 3 years

|X| 85% Principal Protected at maturity (senior unsecured obligation of DB)

|X| Main Risks:

o Subject to issuer credit risk

o Redemption below 100% if 10y swaps don't increase

o Secondary market price of the notes can be significantly influenced

by market factors like rates, volatilities, credit spreads,

liquidity, among others

[Deutsche Bank Logo]

SLIDE08

|  |

10y Steepener Note

Monetizing Term Premium in the Yield Curve

Sample Terms

Issuer Deutsche Bank (Aa1/A+/AA-)

Maturity 10 years

Coupon 7 x (10yCMS - 2yCMS)

Quarterly, 30/360

Capped at 9.50% and Floored at 0.00%

Set in arrears

Payoff Under Hypothetical Scenarios

[GRAPHIC OMITTED]

Rationale

|X| Investors receive coupons that are a multiple of the spread between the 10y

Swap (10yCMS) and the 2y swap (2yCMS)

o At the current spread of 1.32%, a multiple of 7x would deliver a coupon

of around 9.2%

o If the curve steepens further, investors can receive up to 9.5% coupons

|X| 100% Principal Protected at maturity (senior unsecured obligation of DB)

|X| Main Risks:

o Subject to issuer credit risk

o Notes can yield zero coupons if 10y swaps are equal or less than 2y

swaps

o Secondary market price can be influenced by market factors like

rates, volatilities, credit spreads, liquidity, among others)

[Deutsche Bank Logo]

slide09

|  |

Selected Themes/Opportunities (3)

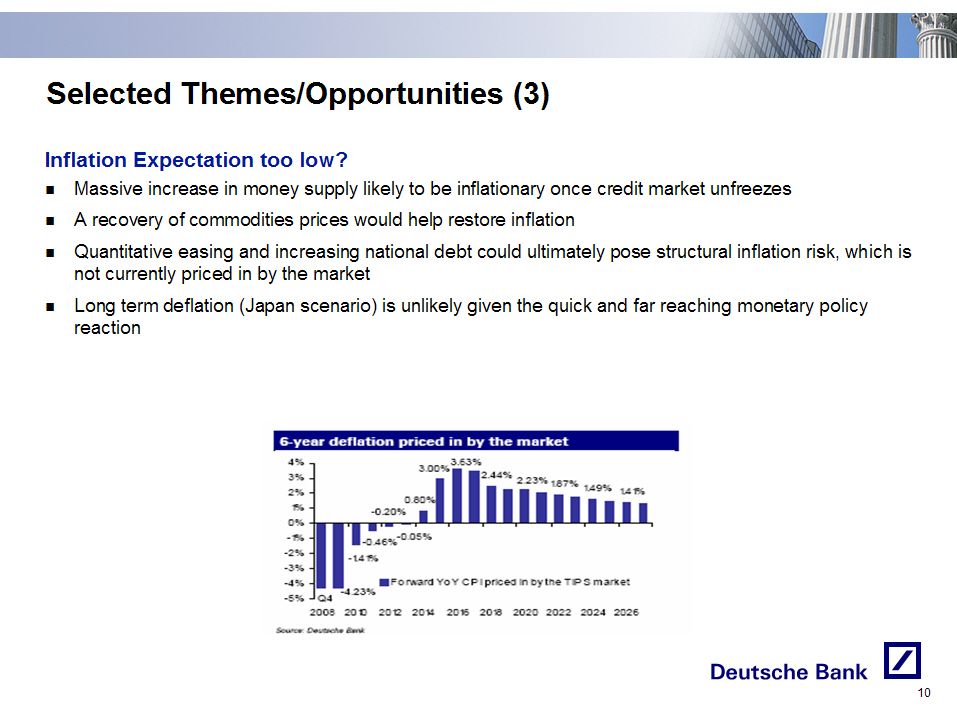

Inflation Expectation too low?

|X| Massive increase in money supply likely to be inflationary once credit

market unfreezes

|X| A recovery of commodities prices would help restore inflation

|X| Quantitative easing and increasing national debt could ultimately pose

structural inflation risk, which is not currently priced in by the market

|X| Long term deflation (Japan scenario) is unlikely given the quick and far

reaching monetary policy reaction

[GRAPHIC OMITTED]

[Deutsche Bank Logo]

slide10

|  |

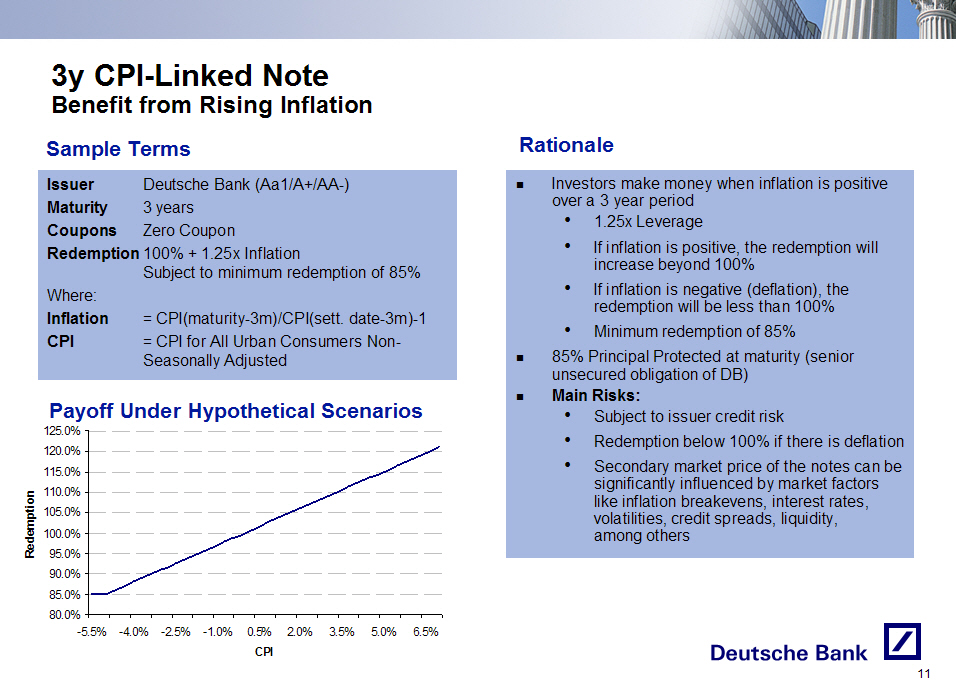

3y CPI-Linked Note

Benefit from Rising Inflation

Sample Terms

Issuer Deutsche Bank (Aa1/A+/AA-)

Maturity 3 years

Coupons Zero Coupon

Redemption 100% + 1.25x Inflation

Subject to minimum redemption of 85%

Where:

Inflation = CPI(maturity-3m)/CPI(sett. date-3m)-1

CPI = CPI for All Urban Consumers Non-

Seasonally Adjusted

Payoff Under Hypothetical Scenarios

[GRAPHIC OMITTED]

Rationale

|X| Investors make money when inflation is positive over a 3 year period

o 1.25x Leverage

o If inflation is positive, the redemption will increase beyond 100%

o If inflation is negative (deflation), the redemption will be less

than 100%

o Minimum redemption of 85%

|X| 85% Principal Protected at maturity (senior unsecured obligation of DB)

|X| Main Risks:

o Subject to issuer credit risk

o Redemption below 100% if there is deflation

o Secondary market price of the notes can be significantly influenced

by market factors like inflation breakevens, interest rates,

volatilities, credit spreads, liquidity, among others

[Deutsche Bank Logo]

slide11

|  |

Conclusion

|X| Macro economic parameters such as the level of interest rates, inflation

etc have a significant impact on any financial portfolio either through

first or second-order effects

|X| Interest rate linked products allow investors to directly express views on

these macro-economic variables and therefore should be a core part of an

investors structured product exposure

|X| These products can serve as a variety of purposes ranging from yield

enhancement to real return protection to hedging exposures in other parts of

the portfolio

|X| A deep and liquid underlying derivatives market combined with Deutsche

Bank's market leading product platform means that products can be easily

customised and efficiently tailored to investors specific requirements

[Deutsche Bank Logo]

slide12

|  |

Disclaimer

Copyright 2009 Deutsche Bank Securities Inc. All rights reserved. "Deutsche

Bank" means Deutsche Bank AG and its affiliated companies, as the context

requires.

The distribution of this document and the availability of some of the products

and services referred to herein may be restricted by law in certain

jurisdictions. Some products and services referred to herein are not eligible

for sale in all countries and in any event may only be sold to qualified

investors. Deutsche Bank will not offer or sell any products or services to any

persons prohibited by the law in their country of origin or in any other

relevant country from engaging in any such transactions.

Deutsche Bank or persons associated with Deutsche Bank an their affiliates may

maintain a long or short position in securities referred to herein, or in

related futures or options, purchase or sell, make a market in, trade

instruments economically related to or have investment banking or other

relationships with the issuers of or engage in any other transaction involving

such securities, and earn brokerage or other compensation. Any transaction that

may involve the products, services and strategies referred to in this

presentation will involve risks. You could lose your entire investment or incur

substantial loss. The products, services and strategies referred to herein may

not be suitable for all investors. The information contained in this

presentation is being provided on the basis that you have such knowledge and

experience in financial and business matters to be capable of evaluating the

merits and risks associated with such information. In contemplating any

transaction, you should consult with your own investment advisors. In any

discussion of a proposed transaction, Deutsche Bank would act at arm's length

and not in any advisory or fiduciary capacity.

The information contained in this presentation does not represent the rendering

of accounting, tax, legal or regulatory advice. It cannot be used or relied

upon for purposes of avoiding compliance with any accounting, tax, legal or

regulatory obligations or avoiding satisfaction of any U.S. federal income tax

penalties. You should consult with independent accounting, tax, legal and

regulatory counsel regarding such matters as they may apply to your particular

circumstances. Foreign currency rates of exchange may adversely affect the

value, price or income of any security or investment. Past performance is no

guarantee of future results.

Backtested, hypothetical or simulated performance results discussed herein have

inherent limitations. Unlike an actual performance record based on trading

actual client portfolios, simulated results are achieved by means of the

retroactive application of a backtested model itself designed with the benefit

of hindsight. Taking into account historical events the backtesting of

performance also differs from actual account performance because an actual

investment strategy may be adjusted any time, for any reason, including a

response to material, economic or market factors. The backtested performance

includes hypothetical results that do not reflect the reinvestment of dividends

and other earnings or the deduction of advisory fees, brokerage or other

commissions, and any other expenses that a client would have paid or actually

paid. No representation is made that any trading strategy or account will or is

likely to achieve profits or losses similar to those shown. Alternative

modeling techniques or assumptions might produce significantly different

results and prove to be more appropriate. Past hypothetical backtest results

are neither an indicator nor guarantee of future returns. Actual results will

vary, perhaps materially, from the analysis. Results represent the performance

of each basket on a back tested basis, tied to a structure whose economics are

determined by current economic factors such as current volatilities and

interest rates. There is no guarantee that a similar structure would have been

available at any point in the past and that such results could have been

achieved.

Options, structured securities and illiquid investments, such as private

investments, are complex instruments and are not be suitable for all investors.

Prior to buying or selling an option investors must review the Characteristics

and Risks of Standardized Options:

http://onn.theocc.com/publications/risks/riskstoc.pdf If you are unable to

access the website please contact Deutsche Bank AG at +1 (212) 250-7994 for a

copy of this important document.

These investments typically involve a high degree of risk, are not transferable

and typically will not be listed or traded on any exchange and are intended for

sale only to sophisticated investors who are capable of understanding and

assuming the risks involved. The market value of any structured security may be

affected by changes in economic, financial and political factors (including,

but not limited to, spot and forward interest and exchange rates), time to

maturity, market conditions and volatility. Any investor should conduct his/her

own investigation and analysis of the product and consult with its own

professional advisers as to the risks involved in making such a purchase;

since, it may be difficult to realize the investment prior to maturity, obtain

reliable information about the market value of such investments or the extent

of the risks to which they are exposed, including the risk of total loss of

capital.

Calculations of returns on instruments referred to herein may be linked to a

referenced index or interest rate. In such cases, the investments may not be

suitable for persons unfamiliar with such index or interest rate, or unwilling

or unable to bear the risks associated with the transaction. Products

denominated in a currency, other than the investor's home currency, will be

subject to changes in exchange rates, which may have an adverse effect on the

value, price or income return of the products. These products may not be

readily realizable investments and are not traded on any regulated market. The

securities referred to herein involve risk, which may include interest rate,

index, currency, credit, political, liquidity, time value, commodity and market

risk and is not suitable for all investors.

These instruments are not insured or guaranteed by the Federal Deposit

Insurance Corporation (FDIC) or any other U.S. governmental agency. These

instruments are not insured or guaranteed by any statutory scheme or

governmental agency of the United Kingdom. The distribution of this document

and availability of these products and services in certain jurisdictions may be

restricted by law.

Deutsche Bank AG has filed a registration statement (including a prospectus)

with the Securities and Exchange Commission, or SEC, for offerings to which

this communication relates. Before you invest, you should read the prospectus

in that registration statement and the other documents relating to such

offering that Deutsche Bank AG has filed with the SEC for more complete

information about Deutsche Bank AG and the offering. You may obtain these

documents without cost by visiting EDGAR on the SEC website at www.sec.gov.

Alternatively, Deutsche Bank AG, any agent or any dealer participating in the

offering will arrange to send you the prospectus if you so request by calling

toll-free 1-866-620-6443.

[Deutsche Bank Logo]

slide13

|  |