Filed pursuant to Rule 433

Registration Statement No. 333-137902

Dated March 20, 2009

Private Wealth Management

Deutsch Bank

Deutsche Bank Commodity Harvest Indices

March 2009

The instruments described in this presentation are hybrid instruments under the

Commodity Exchange Act ("CEA").

As such, the instruments are not contracts of sale of a commodity for future

delivery (or options on such contracts) and are not subject to the CEA.

[GRAPHIC OMITTED]

|  |

Private Wealth Management

Risks

Commodities are speculative and highly volatile. The risk of loss in trading

commodities can be substantial. Commodity prices may be subject to substantial

and unpredictable fluctuations over short periods of time and may be affected

by, among other things, a wide variety of regulatory, monetary and/or economic

developments and policies. Prospective investors must independently assess the

appropriateness of an investment in commodities in light of their own financial

situation and investment objectives.

The price of an instrument and the commodities which comprise the index may be

affected by numerous market factors, including events in the market for

commodities, the equity markets, the bond market and the foreign exchange

market, fluctuations in interest rates, and world economic, political and

regulatory events. A rise in the value of one commodity may be offset by a fall

in the value of one or more of the other commodities comprising the index.

Commodity prices can be highly volatile and may impact negatively the value of

an instrument. Volatility around the time of maturity could have a significant

impact on the overall performance of an investment.

The value of any instrument linked to the index described herein will depend

on, among other things, fluctuations in interest rates, the value of the

commodities underlying the index, the time remaining to the maturity date, and

associated options markets and hedging costs of the issuer. The value of any

instrument may start to decline significantly if the value of the index at a

given time is below the level of the index on the issue date of the instrument.

Price movements may also be caused by changes in the credit spread of the

issuer.

The receipt by the investor of monies owed under instruments linked to the

index described herein is subject to and dependent on the issuer's abilities to

pay such monies. Consequently, investors are subject to a counterparty risk and

are susceptible to risks relating to the creditworthiness of the issuer.

page 2

|  |

Private Wealth Management

Risks

Investing in instruments linked to the index involves certain risks. Inherent

in the index is the risk that the forward curves for the underlying futures

contracts will unexpectedly move from a contangoed curve and remain as either a

less contangoed curve or a backwardated curve after long positions have been

taken in such futures contracts. This switch would result in negative carry at

a time when the optimum yield methodology has presumed that the underlying

futures contract would result in positive carry. Further, because the index is

composed of long and short positions, there is a risk that these positions

could cancel each other out if the long "booster" position were identical to

the short position in the GSCI Light Energy Index. This would occur if the

optimum yield methodology selects the same futures contract for an underlying

commodity as the fixed roll methodology used by the GSCI Light Energy Index

which would result in flat returns for the index for that respective component.

The DB Commodity Harvest 3.5 TV Index attempts to achieve a realized volatility

of 3.5%. Adjustments are made to the participation in the DB Commodity Harvest

Index based on realized volatility of the DB Commodity Harvest Index. The

realized volatility of the DB Commodity Harvest Index may differ --- perhaps

significantly --- from its historical realized volatility. It is also possible

that the DB Commodity Harvest 3.5 TV Index will achieve realized volatility

that differs --- possibly significantly --- from the target volatility of 3.5%.

page 3

|  |

Private Wealth Management

Contents

DB Commodity Harvest Index

o Executive Summary

o Sources of Return in Commodities / Commodity Index

o Concept and Construction

o Performance and Descriptive Statistics

DB Commodity Harvest 3.5 TV "Target Volatility" Index

o Executive Summary

o Risk Control by Targeting Volatility

o Exhibit I - Weights and Contracts

page 4

|  |

Private Wealth Management

Deutsch Bank

DB Commodity Harvest Index

|  |

Private Wealth Management

Executive Summary

Why invest in the DB Commodity Harvest Index?

The DB Commodity Harvest Index tracks a long/short rule-based strategy that

uses the concept of "carry" to generate returns without directional exposure to

the commodity markets.

Rule Based Index

o The DB Commodity Harvest Index provides access to commodity "carry"

through the application of a futures "optimum roll" strategy relative to a

"fixed roll" strategy in the same underlying commodities

o Monthly rebalancing of the two strategies keeps the Index's market

exposure neutral and non- directional. Weights of each commodity are reset

annually to match the S&P GSCITM Light Energy Index ("the benchmark

index")

o Investing via an index frees the investor from the mechanics of rolling

the 24 underlying futures contracts

o Carry trades may offer an attractive investment in both absolute return

and portfolio diversification

Past performance is not indicative of future results

page 6

|  |

Private Wealth Management

Sources of Return in Commodities

Commodity indices invest in futures contracts and are subject to the impact of

"roll return."

Spot Return: Return resulting from the change in the value of a commodity

futures contract

Roll Return: Return from the change in value of a commodity futures contract

resulting from its movement over time along its forward curve -

also known as "roll yield" or "carry"

Backwardation:* The roll return (carry) is Positive

o Negative slope or inverted "backward" forward curve

o Supply disruption price elasticity

o Risk premium at near-term delivery - "convenience yield" theory

Contango:* The roll return (carry) is Negative

o Positive slope or "normal" upward forward curve

o Typically reflects markets that are not as price elastic to supply shocks

o Market participants pay a "cost of carry" for deferred payment and

delivery

o Time value of money, storage costs and delivery are all priced into the

deferred premium

*Definitions:

Backwardation: market condition where the futures price is lower in the distant

delivery months than in the near delivery months

Contango: market condition where the future price for distant delivery is

higher than near delivery months, often due to the costs of storing and

insuring the underlying commodity; opposite of backwardation

page 7

|  |

Private Wealth Management

Sources of Return in Commodities

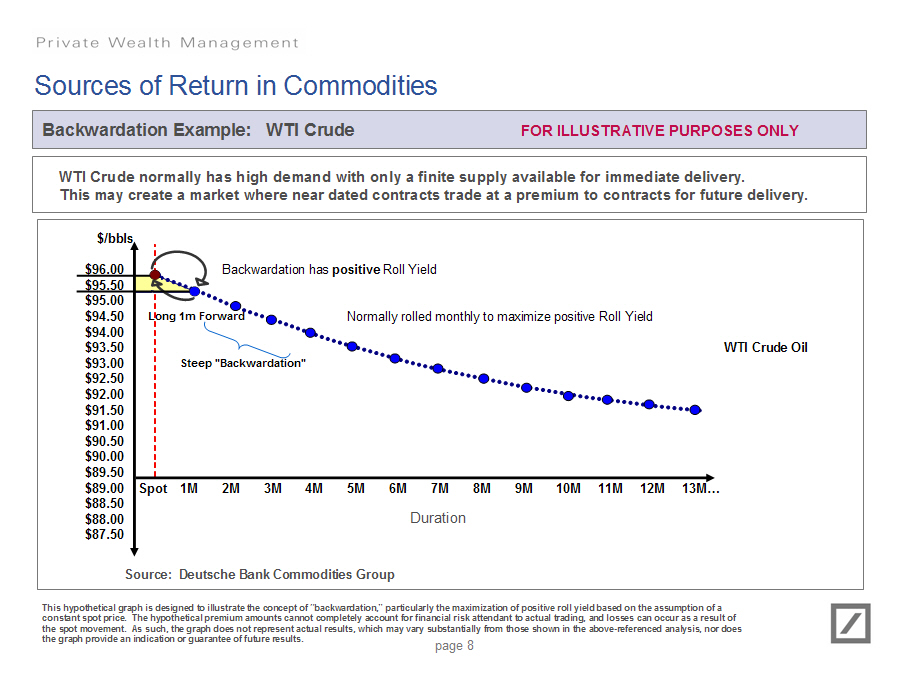

Backwardation Example: WTI Crude FOR ILLUSTRATIVE PURPOSES ONLY

WTI Crude normally has high demand with only a finite supply available for

immediate delivery. This may create a market where near dated contracts trade

at a premium to contracts for future delivery.

[GRAPHIC OMITTED]

This hypothetical graph is designed to illustrate the concept of

"backwardation," particularly the maximization of positive roll yield based on

the assumption of a constant spot price. The hypothetical premium amounts

cannot completely account for financial risk attendant to actual trading, and

losses can occur as a result of the spot movement. As such, the graph does not

represent actual results, which may vary substantially from those shown in the

above-referenced analysis, nor does the graph provide an indication or

guarantee of future results.

page 8

|  |

Private Wealth Management

Sources of Return in Commodities

Contango Example: Gold FOR ILLUSTRATIVE PURPOSES ONLY

Gold normally has insurance and storage costs associated with future delivery.

This may create a market where future dated contracts trade at a premium to

contracts for immediate delivery.

[GRAPHIC OMITTED]

Source: Deutsche Bank Commodities Group

This hypothetical graph is designed to illustrate the concept of "contango,"

particularly the maximization of negative roll yield based on the assumption of

a constant spot price. The hypothetical premium amounts cannot completely

account for financial risk attendant to actual trading, and losses can occur as

a result of the spot movement. As such, the graph does not represent actual

results, which may vary substantially from those shown in the above-referenced

analysis, nor does the graph provide an indication or guarantee of future

results.

page 9

|  |

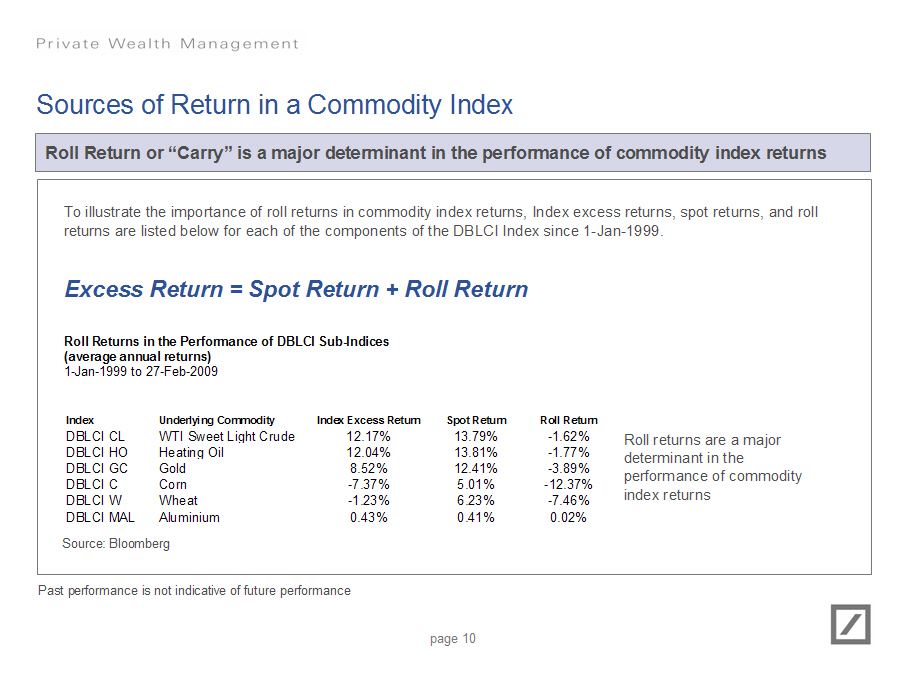

Private Wealth Management

Sources of Return in a Commodity Index

Roll Return or "Carry" is a major determinant in the performance of commodity

index returns

To illustrate the importance of roll returns in commodity index returns, Index

excess returns, spot returns, and roll returns are listed below for each of the

components of the DBLCI Index since 1-Jan-1999.

Excess Return = Spot Return + Roll Return

Roll Returns in the Performance of DBLCI Sub-Indices

(average annual returns)

1-Jan-1999 to 27-Feb-2009

Index Underlying Commodity Index Excess Return Spot Return Roll Return

DBLCI CL WTI Sweet Light Crude 12.17% 13.79% -1.62% Roll returns are a major

DBLCI HO Heating Oil 12.04% 13.81% -1.77% determinant in the

DBLCI GC Gold 8.52% 12.41% -3.89% performance of commodity

DBLCI C Corn -7.37% 5.01% -12.37% index returns

DBLCI W Wheat -1.23% 6.23% -7.46%

DBLCI MAL Aluminium 0.43% 0.41% 0.02%

Source: Bloomberg

Past performance is not indicative of future performance

page 10

|  |

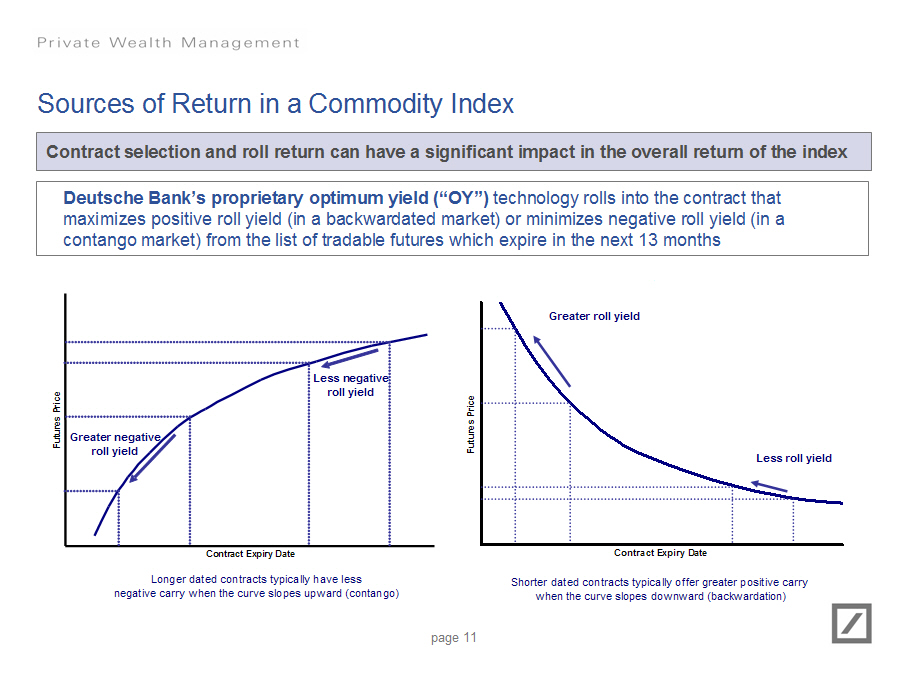

Private Wealth Management

Sources of Return in a Commodity Index

Contract selection and roll return can have a significant impact in the overall

return of the index

Deutsche Bank's proprietary optimum yield ("OY") technology rolls into the

contract that maximizes positive roll yield (in a backwardated market) or

minimizes negative roll yield (in a contango market) from the list of tradable

futures which expire in the next 13 months

[GRAPHIC OMITTED] [GRAPHIC OMITTED]

Longer dated contracts typically have Shorter dated contracts typically

less negative carry when the curve offer greater positive carry when

slopes upward (contango) the curve slopes downward

(backwardation)

page 11

|  |

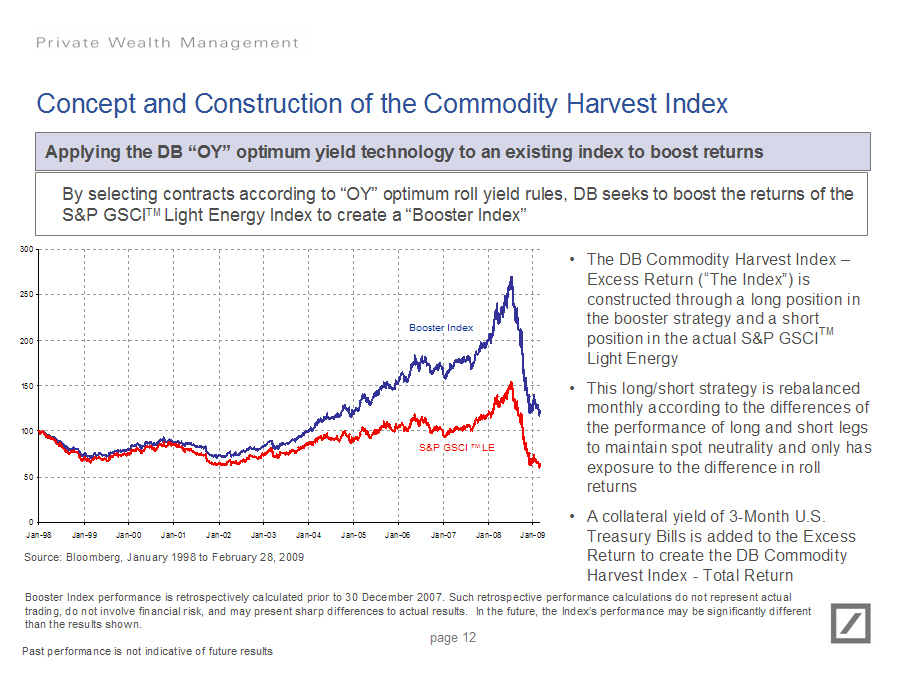

Private Wealth Management

Concept and Construction of the Commodity Harvest Index

Applying the DB "OY" optimum yield technology to an existing index to boost

returns

By selecting contracts according to "OY" optimum roll yield rules, DB seeks to

boost the returns of the S&P GSCITM Light Energy Index to create a "Booster

Index"

[GRAPHIC OMITTED]

o The DB Commodity Harvest Index - Excess Return ("The Index") is

constructed through a long position in the booster strategy and a shortTM

position in the actual S&P GSCI Light Energy

o This long/short strategy is rebalanced monthly according to the

differences of the performance of long and short legs to maintain spot

neutrality and only has exposure to the difference in roll returns

o A collateral yield of 3-Month U.S. Treasury Bills is added to the Excess

Return to create the DB Commodity Harvest Index - Total Return

Source: Bloomberg, January 1998 to February 28, 2009

Booster Index performance is retrospectively calculated prior to 30 December

2007. Such trading, do not involve financial risk, and may present sharp

differences to actual results. than the results shown.

Past performance is not indicative of future results

page 12

|  |

Private Wealth Management

Concept and Construction of the Commodity Harvest Index

Performance of the DB Commodity Harvest Index TR

The DB Commodity Harvest Index rebalances mechanically in order to extract

alpha and reduce spot market risk.

[GRAPHIC OMITTED]

o The Index is rebalanced every month to reduce spot price exposure created

by performance differences between long and short legs.

o Additional reweighting occurs annually to match the annual reweighting of

the S&P GSCITM Light Energy

o The Index is diversified among 24 underlying commodities

(see Exhibit I for weightings)

Source: Bloomberg, Jan 1998 to February 28, 2009

Booster Index performance is retrospectively calculated prior to 30 December

2007. Such retrospective performance calculations do not represent actual

trading, do not involve financial risk, and may present sharp differences to

actual results. In the future, the Index's performance may be significantly

different than the results shown.

page 13

Past performance is not indicative of future results

|  |

Past performance is not indicative of future results

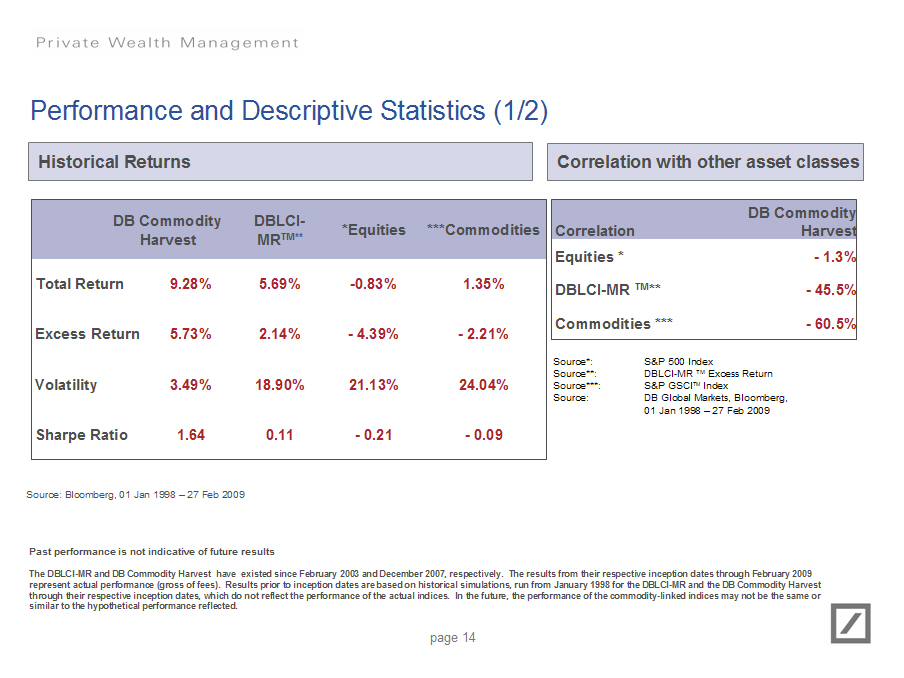

Performance and Descriptive Statistics (1/2)

Historical Returns

- --------------------------------------------------------------------

DB Commodity DBLCI- *Equities ***Commodities

Harvest MR TM**

Total Return 9.28% 5.69% -0.83% 1.35%

Excess Return 5.73% 2.14% -4.39% -2.21%

Volatility 3.49% 18.90% 21.13% 24.04%

Sharpe Ratio 1.64 0.11 - 0.21 -0.09

- --------------------------------------------------------------------

Source: Bloomberg, 01 Jan 1998 - 27 Feb 2009

Correlation with other asset classes

- -------------------------------

DB Commodity

Correlation Harvest

Equities * - 1.3%

DBLCI-MR TM** - 45.5%

Commodities *** - 60.5%

- -------------------------------

Source*: S&P 500 Index

Source**: DBLCI-MR TM Excess Return

Source***: S&P GSCITM Index

Source: DB Global Markets, Bloomberg,

01 Jan 1998 - 27 Feb 2009

Past performance is not indicative of future results

The DBLCI-MR and DB Commodity Harvest have existed since February 2003 and

December 2007, respectively. The results from their respective inception dates

through February 2009 represent actual performance (gross of fees). Results

prior to inception dates are based on historical simulations, run from January

1998 for the DBLCI-MR and the DB Commodity Harvest through their respective

inception dates, which do not reflect the performance of the actual indices. In

the future, the performance of the commodity-linked indices may not be the same

or similar to the hypothetical performance reflected.

page 14

|  |

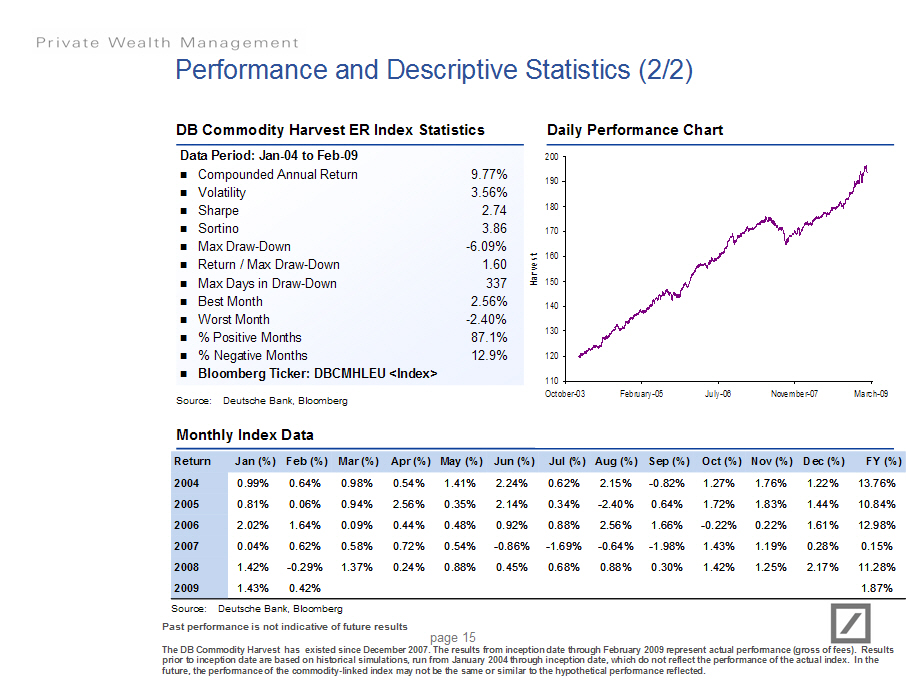

Performance and Descriptive Statistics (2/2)

DB Commodity Harvest ER Index Statistics

Data Period: Jan-04 to Feb-09

Compounded Annual Return 9.77%

Volatility 3.56%

Sharpe 2.74

Sortino 3.86

Max Draw-Down -6.09%

Return / Max Draw-Down 1.60

Max Days in Draw-Down 337

Best Month 2.56%

Worst Month -2.40%

% Positive Months 87.1%

% Negative Months 12.9%

Bloomberg Ticker: DBCMHLEU (Index)

Source: Deutsche Bank, Bloomberg

Daily Performance Chart

[GRAPHIC OMITTED]

Monthly Index Data

Return Jan (%)Feb (%) Mar (%) Apr (%) May (%) Jun (%) Jul (%)

2004 0.99% 0.64% 0.98% 0.54% 1.41% 2.24% 0.62%

2005 0.81% 0.06% 0.94% 2.56% 0.35% 2.14% 0.34%

2006 2.02% 1.64% 0.09% 0.44% 0.48% 0.92% 0.88%

2007 0.04% 0.62% 0.58% 0.72% 0.54% -0.86% -1.69%

2008 1.42% -0.29% 1.37% 0.24% 0.88% 0.45% 0.68%

2009 1.43% 0.42%

- --------------------------------------------------------------------------------

Aug (%) Sep (%) Oct (%) Nov (%) Dec (%) FY (%)

2.15% -0.82% 1.27% 1.76% 1.22% 13.76%

-2.40% 0.64% 1.72% 1.83% 1.44% 10.84%

2.56% 1.66% -0.22% 0.22% 1.61% 12.98%

-0.64% -1.98% 1.43% 1.19% 0.28% 0.15%

0.88% 0.30% 1.42% 1.25% 2.17% 11.28%

1.87%

- ------------------------------------------------------------

Source: Deutsche Bank, Bloomberg

Past performance is not indicative of future results

The DB Commodity Harvest has existed since December 2007. The results from

inception date through February 2009 represent actual performance (gross of

fees). Results prior to inception date are based on historical simulations, run

from January 2004 through inception date, which do not reflect the performance

of the actual index. In the future, the performance of the commodity-linked

index may not be the same or similar to the hypothetical performance reflected.

page 15

|  |

DB Commodity Harvest 3.5 TV Index

page 16

|  |

Executive Summary

Why invest in the DB Commodity Harvest 3.5 TV Index?

The DB Commodity Harvest Index seeks to generate alpha through a long/short

index strategy. However, there are no controls for volatility. The DB

Commodity Harvest 3.5 TV Index is an allocation strategy based on the DB

Commodity Harvest Index that aims at maintaining a target volatility of

3.5%

Rules-Based Index

o The DB Commodity Harvest 3.5 TV Index dynamically controls the exposure to

the DB Commodity Harvest Excess Return Index ("the Underlying Index") in

order to target realized volatility of close to 3.5%

o Rebalancing occurs monthly, at which time the participation of the DB

Commodity Harvest 3.5 TV Index in the Underlying Index is reset to the

ratio of Target Volatility / Realized Volatility

o Participation in the Underlying Index increases when the realized

volatility of the Underlying Index has gone down and vice-versa

o Volatility targeting can reduce the cost of options when there is a large

divergence between realized (historical) and implied (expected)

volatility, as reflected by the option price

Past performance is not indicative of future results

page 17

|  |

Index Construction (Harvest 3.5 TV Index)

Applying volatility targeting to potentially control risk

Monthly rebalancing

Calculated on 3rd last business day of the month, effective on the last business

day

Step I

Monitor Realized Volatility (Based on Last 90 Days Returns)

Step II

Calculate Index Participation Participation = Target Volatility / Realized

Volatility, subject to a maximum participation of 300%

Step III

Harvest 3.5 TV Index Return = Participation x Underlying Index

return

Numerical

Example:

Volatility Target =

3.5%

90 Day Realized Underlying Vol Target

Month Volatility Participation (%) Index Return Return

(Annualized %) (%) (%)

12 3.50 100.00 +5.00 +5.00

13 10.50 33.33 -1.00 -0.33

14 2.50 140.00 +3.00 +4.20

15 2.00 175.00 -2.00 -3.50

16 1.50 233.33 +5.00 +11.66

17 3.00 116.67 +1.00 +1.16

18 3.50 100.00 +10.00 +10.00

- ------------------------- ------------------ ------------- ----------

page 18

|  |

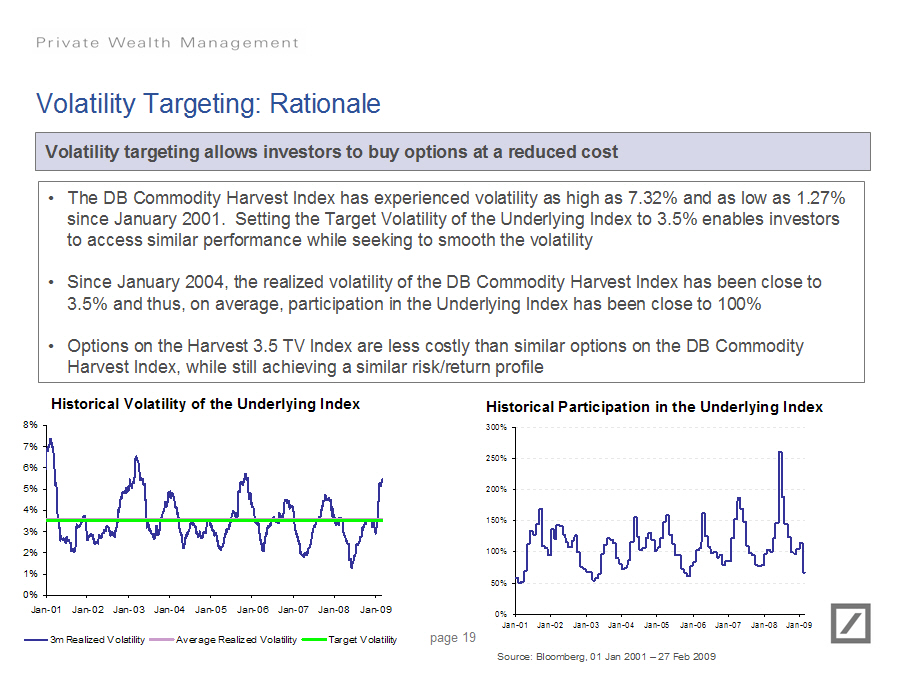

Volatility Targeting: Rationale

Volatility targeting allows investors to buy options at a reduced cost

o The DB Commodity Harvest Index has experienced volatility as high as 7.32%

and as low as 1.27% since January 2001. Setting the Target Volatility of

the Underlying Index to 3.5% enables investors to access similar

performance while seeking to smooth the volatility

o Since January 2004, the realized volatility of the DB Commodity Harvest

Index has been close to 3.5% and thus, on average, participation in the

Underlying Index has been close to 100%

o Options on the Harvest 3.5 TV Index are less costly than similar options on

the DB Commodity Harvest Index, while still achieving a similar risk/return

profile

Historical Volatility of the Underlying Index

[GRAPHIC OMITTED]

3m Realized Volatility Average Realized Volatility Target Volatility

Historical Participation in the Underlying Index

[GRAPHIC OMITTED]

Source: Bloomberg, 01 Jan 2001 - 27 Feb 2009

page 19

|  |

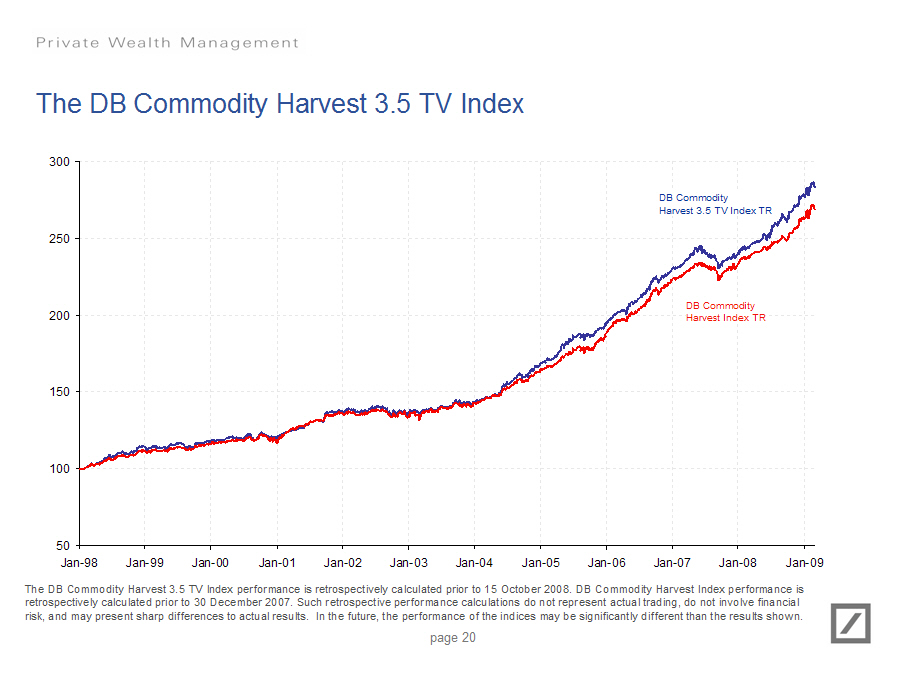

The DB Commodity Harvest 3.5 TV Index

[GRAPHIC OMITTED]

The DB Commodity Harvest 3.5 TV Index performance is retrospectively calculated

prior to 15 October 2008. DB Commodity Harvest Index performance is

retrospectively calculated prior to 30 December 2007. Such retrospective

performance calculations do not represent actual trading, do not involve

financial risk, and may present sharp differences to actual results. In the

future, the performance of the indices may be significantly different than the

results shown.

page 20

|  |

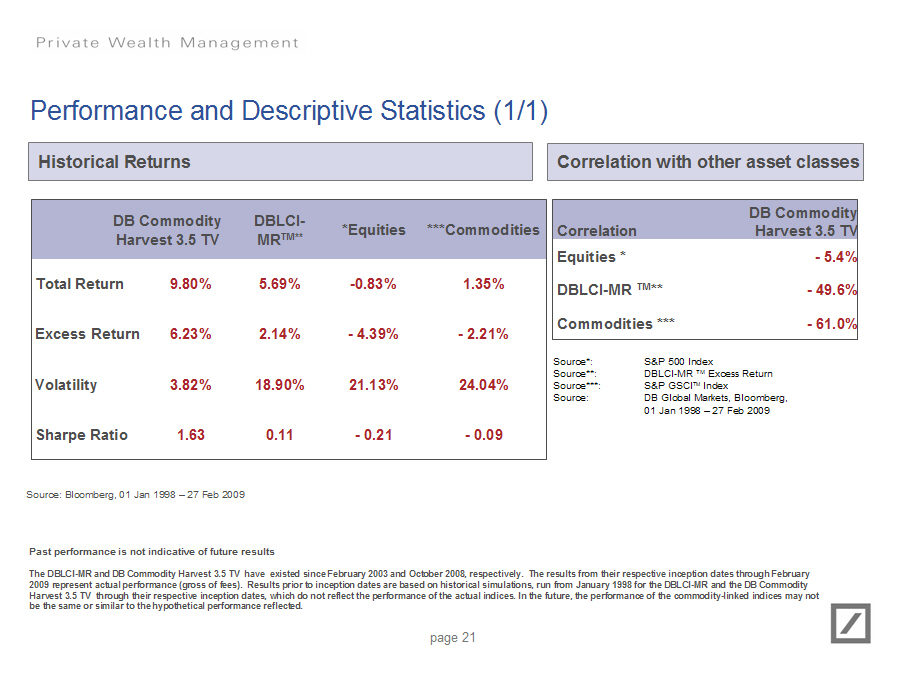

Performance and Descriptive Statistics (1/1)

Historical Returns

------------------------------------------------------------------

DB Commodity DBLCI- *Equities ***Commodities

Harvest 3.5 TV MRTM**

Total Return 9.80% 5.69% -0.83% 1.35%

Excess Return 6.23% 2.14% -4.39% -2.21%

Volatility 3.82% 18.90% 21.13% 24.04%

Sharpe Ratio 1.63 0.11 -0.21 -0.09

------------------------------------------------------------------

Source: Bloomberg, 01 Jan 1998 - 27 Feb 2009

Correlation with other asset classes

- ------------------------------------------------------------

DB Commodity

Correlation Harvest 3.5 TV

Equities * - 5.4%

DBLCI-MR TM** - 49.6%

Commodities *** - 61.0%

- ------------------------------------------------------------

Source*: S&P 500 Index

Source**: DBLCI-MR TM Excess Return

Source***: S&P GSCITM Index

Source: DB Global Markets, Bloomberg,

01 Jan 1998 - 27 Feb 2009

Past performance is not indicative of future results

The DBLCI-MR and DB Commodity Harvest 3.5 TV have existed since February 2003

and October 2008, respectively. The results from their respective inception

dates through February 2009 represent actual performance (gross of fees).

Results prior to inception dates are based on historical simulations, run from

January 1998 for the DBLCI-MR and the DB Commodity Harvest 3.5 TV through their

respective inception dates, which do not reflect the performance of the actual

indices. In the future, the performance of the commodity-linked indices may not

be the same or similar to the hypothetical performance reflected.

page 21

|  |

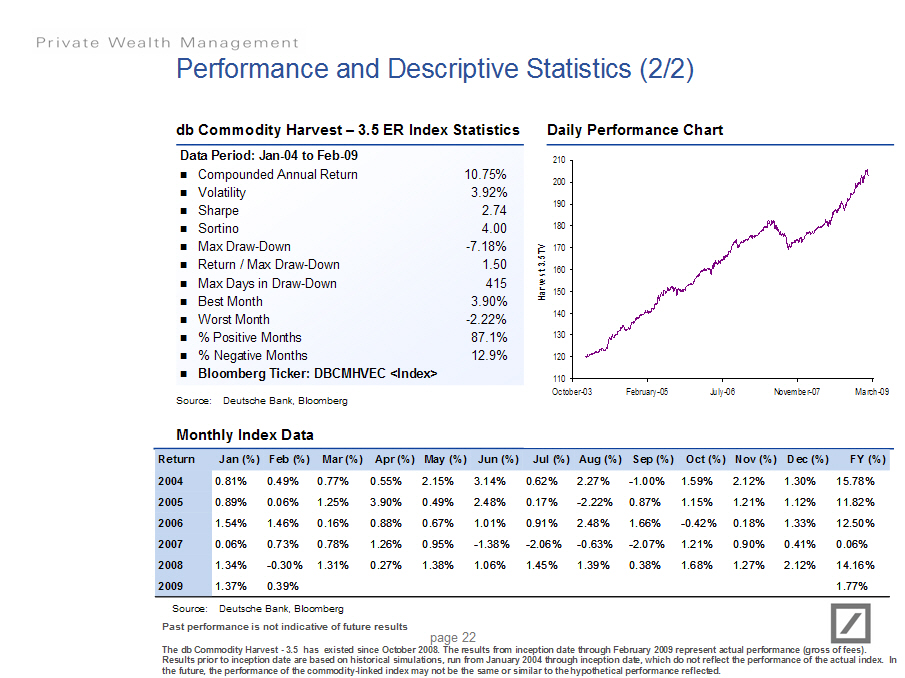

Performance and Descriptive Statistics (2/2)

db Commodity Harvest - 3.5 ER Index Statistics

Data Period: Jan-04 to Feb-09

o Compounded Annual Return 10.75%

o Volatility 3.92%

o Sharpe 2.74

o Sortino 4.00

o Max Draw-Down -7.18%

o Return / Max Draw-Down 1.50

o Max Days in Draw-Down 415

o Best Month 3.90%

o Worst Month -2.22%

o % Positive Months 87.1%

o % Negative Months 12.9%

o Bloomberg Ticker: DBCMHVEC (Index)

Daily Performance Chart

[GRAPHIC OMITTED]

Monthly Index Data

Return Jan (%) Feb (%) Mar (%) Apr (%) May (%) Jun (%) Jul (%) Aug (%)

2004 0.81% 0.49% 0.77% 0.55% 2.15% 3.14% 0.62% 2.27%

2005 0.89% 0.06% 1.25% 3.90% 0.49% 2.48% 0.17% -2.22%

2006 1.54% 1.46% 0.16% 0.88% 0.67% 1.01% 0.91% 2.48%

2007 0.06% 0.73% 0.78% 1.26% 0.95% -1.38% -2.06% -0.63%

2008 1.34% -0.30% 1.31% 0.27% 1.38% 1.06% 1.45% 1.39%

2009 1.37% 0.39%

- ---------------------------------------------------------------------------------

Sep (%) Oct (%) Nov (%) Dec (%) FY (%)

-1.00% 1.59% 2.12% 1.30% 15.78%

0.87% 1.15% 1.21% 1.12% 11.82%

1.66% -0.42% 0.18% 1.33% 12.50%

-2.07% 1.21% 0.90% 0.41% 0.06%

0.38% 1.68% 1.27% 2.12% 14.16%

1.77%

Source: Deutsche Bank, Bloomberg

Past performance is not indicative of future results

The db Commodity Harvest - 3.5 has existed since October 2008. The results from

inception date through February 2009 represent actual performance (gross of

fees). Results prior to inception date are based on historical simulations, run

from January 2004 through inception date, which do not reflect the performance

of the actual index. In the future, the performance of the commodity-linked

index may not be the same or similar to the hypothetical performance reflected.

page 22

|  |

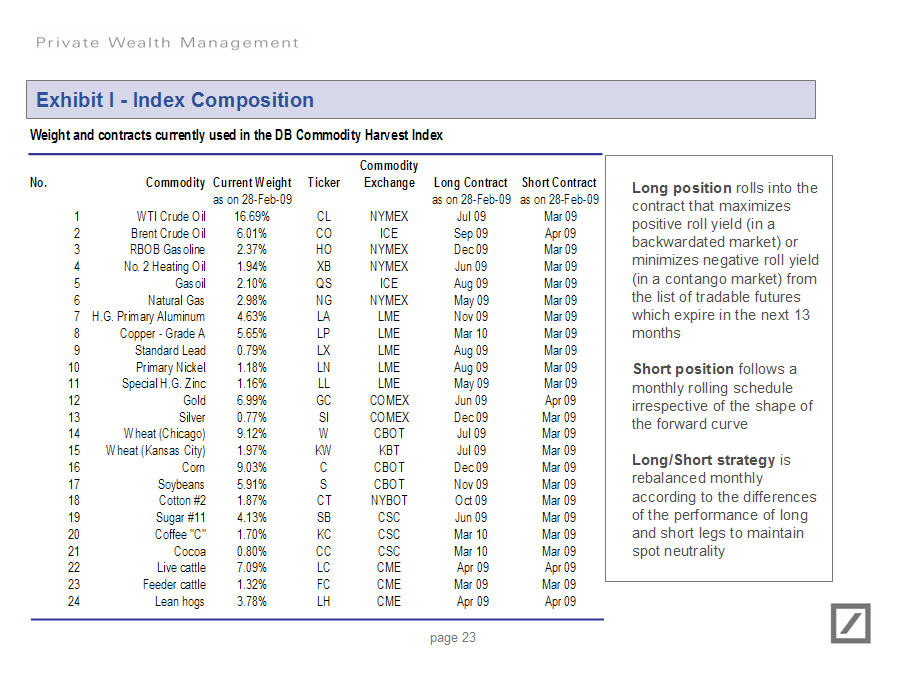

Exhibit I - Index Composition

Weight and contracts currently used in the DB Commodity Harvest Index

- -------------------------------------------------------------------------------------------------------

Commodity

No. Commodity Current Weight Ticker Exchange Long Contract Short Contract

as on 28-Feb-09 as on 28-Feb-09 as on 28-Feb-09

1 WTI Crude Oil 16.69% CL NYMEX Jul 09 Mar 09

2 Brent Crude Oil 6.01% CO ICE Sep 09 Apr 09

3 RBOB Gasoline 2.37% HO NYMEX Dec 09 Mar 09

4 No. 2 Heating Oil 1.94% XB NYMEX Jun 09 Mar 09

5 Gasoil 2.10% QS ICE Aug 09 Mar 09

6 Natural Gas 2.98% NG NYMEX May 09 Mar 09

7 H.G. Primary Aluminum 4.63% LA LME Nov 09 Mar 09

8 Copper - Grade A 5.65% LP LME Mar 10 Mar 09

9 Standard Lead 0.79% LX LME Aug 09 Mar 09

10 Primary Nickel 1.18% LN LME Aug 09 Mar 09

11 Special H.G. Zinc 1.16% LL LME May 09 Mar 09

12 Gold 6.99% GC COMEX Jun 09 Apr 09

13 Silver 0.77% SI COMEX Dec 09 Mar 09

14 Wheat (Chicago) 9.12% W CBOT Jul 09 Mar 09

15 Wheat (Kansas City) 1.97% KW KBT Jul 09 Mar 09

16 Corn 9.03% C CBOT Dec 09 Mar 09

17 Soybeans 5.91% S CBOT Nov 09 Mar 09

18 Cotton #2 1.87% CT NYBOT Oct 09 Mar 09

19 Sugar #11 4.13% SB CSC Jun 09 Mar 09

20 Coffee "C" 1.70% KC CSC Mar 10 Mar 09

21 Cocoa 0.80% CC CSC Mar 10 Mar 09

22 Live cattle 7.09% LC CME Apr 09 Apr 09

23 Feeder cattle 1.32% FC CME Mar 09 Mar 09

24 Lean hogs 3.78% LH CME Apr 09 Apr 09

- -------------------------------------------------------------------------------------------------------

Long position rolls into the contract that maximizes positive roll yield (in a

backwardated market) or minimizes negative roll yield (in a contango market)

from the list of tradable futures which expire in the next 13 months

Short position follows a monthly rolling schedule irrespective of the shape of

the forward curve

Long/Short strategy is rebalanced monthly according to the differences of the

performance of long and short legs to maintain spot neutrality

page 23

|  |

Market Data Sources

Bloomberg Tickers:

DB Commodity Harvest - Total Return DBCMHLTU (Index)

DB Commodity Harvest - Excess Return DBCMHLEU (Index)

DB Commodity Harvest 3.5 TV - Total Return DBCMHVTC (Index)

DB Commodity Harvest 3.5 TV - Excess Return DBCMHVEC (Index)

DB Commodity Booster - S&P GSCITM Light Energy Excess Return DBCMBLEU (Index)

S&P GSCITM Light Energy Excess Return SPGSLEP (Index)

S&P 500 SPTR (Index)

DBLCI-MRTM Excess Return DBLCMMCL (Index)

S&P GSCITM Excess Return SPGSCIP (Index)

page 24

|  |

Important Notes

The analysis set forth herein is based on information we believe to be reliable,

including internal models, certain assumptions (all of which are subject to

change without notice) and available market data, which may be internally

generated.

"Deutsche Bank" means Deutsche Bank AG and its affiliated companies, as the

context requires. Deutsche Bank Private Wealth Management refers to Deutsche

Bank's wealth management activities for high net worth clients around the world.

Investors should consider an investment linked to the indices described herein

only after careful consideration and consultation with their legal, tax,

accounting and other advisers as to the suitability of the investments in light

of their own particular financial, tax and other circumstances, and the

information set out in this document and the other documents we provide to you.

Deutsche Bank AG has filed a registration statement (including a prospectus)

with the Securities and Exchange Commission, or SEC, for offerings to which

these materials relate. Before you invest, you should read the prospectus in

that registration statement and the other documents relating to such offering

that Deutsche Bank AG has filed with the SEC for more complete information about

Deutsche Bank AG and such offering. You may obtain these documents without cost

by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, Deutsche

Bank AG, any agent or any dealer participating in such offering will arrange to

send you the prospectus, prospectus supplement and other documents relating to

the offering if you so request by calling toll-free 1-800-311-4409.

Your return on an investment linked to the indices described herein will be

dependent on the performance of the indices during the term of the instrument.

The composite is subject to change and there is no assurance that the

commodities which comprise an index will have positive performance, and past

performance of any of the commodities which comprise an index is not a

guarantee, nor necessarily indicative, of their future performance.

Deutsche Bank AG, including its subsidiaries and affiliates, does not provide

legal, tax or accounting advice. This communication was prepared solely in

connection with the promotion or marketing, to the extent permitted by

applicable law, of the matter addressed herein, and was not intended or written

to be used, and cannot be used or relied upon, by any taxpayer for purposes of

avoiding any U.S. federal tax penalties. The recipient of this communication

should seek advice from an independent tax advisor regarding any tax matters

addressed herein based on its particular circumstances.

page 25

|  |

S&P GSCI Disclaimer

These materials are not sponsored, endorsed, sold or promoted by Standard &

Poor's, a division of The McGraw-Hill Companies, Inc. ("S&P"). Standard & Poor's

does not make any representation or warranty, express or implied, to the owners

of any instrument linked to the indices described herein or any member of the

public regarding the advisability of investing in securities generally or in any

instrument linked to the indices described herein or the ability of S&P GSCI

Index to track general commodity market performance. S&P's only relationship to

Deutsche Bank AG is the licensing of certain trademarks and trade names of S&P

and of S&P GSCI Index, which indices are determined, composed and calculated by

S&P without regard to Deutsche Bank AG or any instrument linked to the indices

described herein. S&P has no obligation to take the needs of Deutsche Bank AG or

the owners of any instrument linked to the indices described herein into

consideration in determining, composing or calculating S&P GSCI Index. S&P is

not responsible for and has not participated in the determination of the timing

of, prices at, or quantities of any instrument linked to the indices described

herein to be issued or in the determination or calculation of the equation by

which the S&P GSCI Index are to be converted into cash. S&P has no obligation or

liability in connection with the administration, marketing or trading of any

instrument linked to the indices described herein.

S&P DOES NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF S&P GSCI INDEX OR

ANY DATA INCLUDED THEREIN AND S&P SHALL HAVE NO LIABILITY FOR ANY ERRORS,

OMISSIONS, OR INTERRUPTIONS THEREIN. S&P MAKES NO WARRANTY, EXPRESS OR IMPLIED,

AS TO RESULTS TO BE OBTAINED BY DEUTSCHE BANK AG, OWNERS OF ANY INSTRUMENT

LINKED TO THE INDICES DESCRIBED HEREIN OR ANY OTHER PERSON OR ENTITY FROM THE

USE OF S&P GSCI INDEX OR ANY DATA INCLUDED THEREIN. S&P MAKES NO EXPRESS OR

IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR

FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE S&P INDICES OR ANY

DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL

S&P HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL

DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH

DAMAGES.

S&P GSCI Index is a trademark of The McGraw-Hill Companies, Inc. and has been

licensed for use by Deutsche Bank AG.

page 26

|  |